Results of Taxonomic Evaluation of RDF(S) and DAML+OIL Ontologies using RDF(S

中文标题

中文标题: 中国2007年出口退税政策变动对出口影响的实证分析英文标题:The Effect of the Export Tax Rebate PolicyChange on Chinaʹs Exports: An EmpiricalAnalysis研究领域:国际经济学作者姓名:白重恩 王鑫 钟笑寒①工作单位:清华大学经济管理学院经济系通讯地址:北京市清华大学紫荆公寓13#208B(王鑫)邮政编码:100084①作者署名以姓氏拼音为序。

中国2007年出口退税政策变动对出口影响的实证分析内容提要2007年7月1日我国大规模下调了出口退税率,本文运用双差法(difference in difference),对出口退税率的降低引起的中国出口变动进行了实证分析,结果表明:出口退税率下调对出口增长率而非出口水平有显著的负影响;分类来讲,退税率降低对“易引起贸易摩擦的商品”出口增长率负影响显著,对“高耗能、高污染、资源型”产品的出口增长率负影响不显著。

因而部分(而非全部)达到了预想的政策效果。

AbstractOn July 1st, 2007, China reduced the export tax rebate rate of almost 37% of all products. Based on the export data from January 2005 to June 2008, using the theory of “Difference in Difference”, we did empirical test to the export and growth rate of export. The result shows that reducing the export tax rebate rate distinctly reduced growth rate of export, but didn’t distinctly have minus effect on export. Compared with reducing the growth rate of “easy to cause trade friction” good, this policy didn’t control the rapid growth of “high-energy-consumption, high-pollution, resource-based” products’ export.关键词出口额出口退税政策双差法一 导言2007年6月8日,我国财政部和国家税务总局同国家发改委、商务部、海关总署发布了《财政部国家税务总局关于调低部分商品出口退税率的通知》,规定自2007年7月1日起,调整部分商品的出口退税政策。

CFA 级财务报表读书笔记

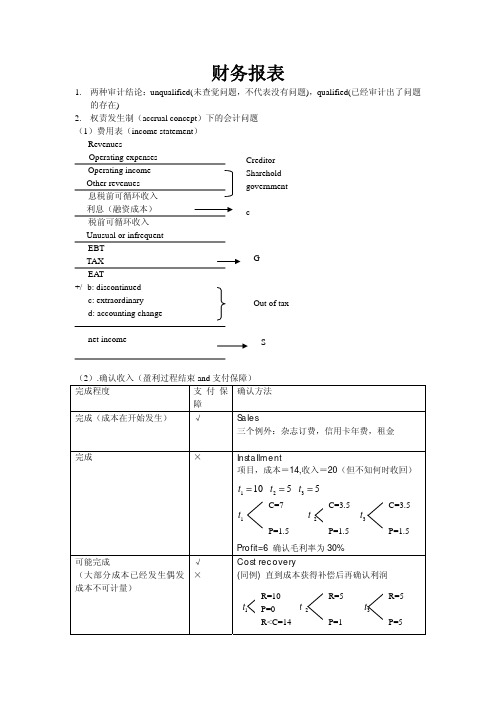

财务报表1.两种审计结论:unqualified(未查觉问题,不代表没有问题),qualified(已经审计出了问题的存在)2.权责发生制(accrual concept)下的会计问题(1)费用表(income statement)(2).确认收入(盈利过程结束and支付保障)权责发生制可用于利润操纵(按坏消息的税前后列示,平滑收入,全部确认损失抬高未来走势,改变会计方法)3. 现金流量分析(1)CFO (sales ,cost of sales, expense, AR, Inv, tax 利息支付,红利收入,GAAP 预付,递延税)CFI(买PP&E,联合投资,购买business, sales of assets,证券投资),CFF (付红利,长短期负债,stock sales/repurchase ) (2)直接法(+来源--支出) CFO(考虑折旧和摊销):cash collection =sales-AR ↑ cash input=-COGS+ lnv↓+ AP↑ cash expense=-wages-WP↓ Cash interest=-interest + IP↓, cash tax =-tax expense +TP↑+DT↑, CFI: cash assets sales=asset↓ +gain,if PP&E 大于0,use -,if PPE 小于0,use+, CFF: credit cash =new 借-归还(没有利息)Shareholder cash =发新股-日期-股利支付+DP↑(3)间接法Net income+ Non cash 花费(折旧、折耗、摊销)处理资产的损失- non cash gain (处理长期资产所得)(3)完工百分比 完工法 CF 同同 NI大(确认利润)小I.V. 收入波动小 大 A 大 小 E 大 小 D/E小大 (4)几个项目分析a.(business segment, sale asset. environmental. impairment. integration expense )b.(net of tax)c. both unusual and infrequent(loss from expropriation asset. disasters. early retirement of debt)d. principal/estimate- AR ↑,Inv↑,(-CA↑) + AR ↓,Inv↓,(+CA↓)+ CL ↑(AP↑,IP↑,TP↑,DT↑,WP↑) - CL ↓ CFO(4)两个因素A:Acquisition B: foreign subsidiaries(5) FCF=CFO-资本净支出=CFO-(净资本支出-税后收益)4. 报表分析(1)内部流动性 CR=CA/CL,QR=(C+S+AR)/CL,CR=(C+S)/Cl, AP turn=COGS/现金周期=365/ART +365/lnvT-360/APT ,lnv turn=COGS/LNV AR turn=Sales/LNV (2)运营效率 Total assets turnover=revenue/Average total asset,Fixed asset Turnover = revenue/fixed total asset.GPM(纯利率)=GP/S.. OPM=EBIT/S,NPM=EAT/S.ROTC=(EAT+I)/ROE=NI/RCE=(NI-优先股股利)/(3)风险分析s m 1)/()1(,/()EBIT EBIT S P V QFC DOL Q Q S VC FC P V Q FD --==抄?D ----*FCP V-EPS D =DFL%EBIT D →%%EPS S VCDTL EPS S VC FC I D -==D --- = EPS/EPS/ EBIT/EBIT= EPS=DFL DTL= EPS/ Q=(S-VC)/(S-VC-FC-I),D/E=(LD+DT)/E,D/A=(LD+SD)/A,CF/LD=CFO/(BV of LD +PV of OL)(4)成长动力g=ROE ×(1-dividends ratio)=ROE×(1-D/EAT) (5)杜邦体系ROE=NI/E=(NI/S)×(S/A)×(A/E)=NL→(EBIT-I)(1-t)=ROE=((EBIT/S)×(S/A)-I/A) ×A/E×(1-T)5. EPS 分析(简单资本结构-CS ,PS ,不含权债券;复杂资本结构-含有摊薄证券,可转换成债券)(1)Basic EPS=NL-Pre.D)/加权平均普通股股数。

计量经济学斯托克沃森第三版答案

计量经济学斯托克沃森第三版答案1、盈余公积是企业从()中提取的公积金。

[单选题] *A.税后净利润(正确答案)B.营业利润C.利润总额D.税前利润2、企业在转销已经确认无法支付的应付账款时,应贷记的会计科目是()。

[单选题] *A.其他业务收入B.营业外收入(正确答案)C.盈余公积D.资本公积3、企业因解除与职工的劳动关系给予职工补偿而发生的职工薪酬,应借记的会计科目是()。

[单选题] *A.管理费用(正确答案)B.计入存货成本或劳务成本C.营业外支出D.计入销售费用4、由投资者投资转入的无形资产,应按合同或协议约定的价值,借记“无形资产”科目,按其在注册资本所占的份额,贷记“实收资本”科目,按其差额记入()科目。

[单选题] *A.“资本公积—资本溢价”(正确答案)B.“营业外收入”C.“资本公积—其它资本公积”D.“营业外支出”5、下列各项,不影响企业营业利润的项目是()。

[单选题] *A.主营业务收入B.其他收益C.资产处置损益D.营业外收入(正确答案)6、2018年12月31日,甲公司某项固定资产计提减值准备前的账面价值为1 000万元,公允价值为980万元,预计处置费用为80万元,预计未来现金流量的现值为1 050万元。

2018年12月31日,甲公司应对该项固定资产计提的减值准备为()万元。

[单选题] *A.0(正确答案)B.20C.50D.1007、.(年浙江省高职考)下列各项中,属于会计对经济活动进行事中核算的主要形式的是()[单选题] *A预测B决策C计划D控制(正确答案)8、专利权有法定有效期限,一般发明专利的有效期限为()。

[单选题] *A.5年B.10年C.15年D.20年(正确答案)9、.(年预测)下列属于货币资金转换为生产资金的经济活动的是()[单选题] *A购买原材料B生产领用原材料C支付工资费用(正确答案)D销售产品10、.(年浙江省第一次联考)下列各项中,不属于会计核算的前提条件的是()[单选题] *A持续经营B货币计量C权责发生制(正确答案)D会计主体11、下列各项税金中不影响企业损益的是()。

美国拉弗最高税率估计及减税政策评价

关键词 : 宏观税 负; 经济增长 ; 弗最高税 率 拉

中 图分 类 号 :S0 4 2 7 2 F 1 .2 ( 1 )

问题 的提 出

文献标识码 : A

文章 编 号 :62— 09 2 0 )3— 0 6 4 17 6 4 (0 8 0 0 4 —0

二 、 观 税 负 理 论 研 究 现 状 宏

税率 O A为拉弗 最高税 率 。但 是 当税率 继续 升 高时 , 税

收量不升反降。所 以 A G区域 也 就 被称 之 为 “ 区 ” B 禁 。 在以拉弗为首的供给学派看来 , 要维持税 收行为 的有效 , 政府只能在 O G区域征税。即税 率不能高 于 O 。至于 A A 造成这种现象的原因 , 拉弗认为 , 高税 率会减少人们 正常 的经济活动 , 而降低 国民收入 。在低税率 上 , 从 人们 逃避 纳税的少 , 这时用 闲暇替换 劳动 或者用 消费替 换投 资和 储蓄是不合算的 , 找税 收的漏 洞或者将 生产 活动转 移 寻

一

、

方经济学流派 。其主要代表人物有拉弗 、 尔德 、 古 沃尼斯 基和费尔德斯坦 、 文斯等 。供 应学 派的理论 是 围绕如 埃 何使资本主义经济摆脱滞胀 的困境这一问题产 生和发展 的。在税收方 面主要 的理 论有 如下 几点 : 1 税 率是 经 () 济活动 的最有效刺激 。( ) 2 反对 高税率 特别 是累进 税制

维普资讯

20 0 8年 报

J u a o N nigU i r t o i n ea dE o o c o r l f a j n es y f n c n cn mi n n v i F a s

到 地 下 也 是 不 值 得 的 , 使 所 申 报 的 税 基 即征 税 的基 础 这

r语言风险差异rd的计算公式

r语言风险差异rd的计算公式全文共四篇示例,供读者参考第一篇示例:在金融领域,风险是一个非常重要的概念。

对于投资者来说,了解投资组合中不同资产之间的风险差异是至关重要的。

在R语言中,有很多函数和包可以帮助我们计算风险差异,其中最为常用的就是rd 函数。

rd函数用于计算不同资产之间的风险差异,即风险差异。

它是通过比较两个或多个资产的收益率来衡量不同资产之间的风险。

通常来说,风险差异越大,资产之间的相关性越小,风险越高。

在R语言中,我们可以使用rd函数来计算资产之间的风险差异。

其基本公式如下:rd = sqrt(w1^2 * sd1^2 + w2^2 * sd2^2 + 2 * w1 * w2 * cov(sd1, sd2))w1和w2分别为两个资产的权重,sd1和sd2分别为两个资产的标准差,cov(sd1, sd2)为两个资产的协方差。

通过这个公式,我们可以计算得到两个资产之间的风险差异。

在实际应用中,我们可以通过遍历不同的权重组合来寻找最小的风险差异,从而找到最优的投资组合。

除了rd函数外,R语言还提供了其他很多用于风险度量和投资组合优化的函数和包,比如quantmod、PerformanceAnalytics、PortfolioAnalytics等。

这些函数和包可以帮助投资者更好地管理风险、优化投资组合,并实现更好的投资回报。

第二篇示例:R语言是一种广泛应用于数据分析和统计建模的编程语言,它具有强大的功能和丰富的数据操作工具。

在金融市场中,风险差异(rd)是一个重要的指标,用来衡量不同资产或投资组合之间的风险差异程度。

在R语言中,计算风险差异的公式可以通过计算两个资产或投资组合之间的标准差来实现。

标准差是一种衡量随机变量离散程度的统计指标,它可以反映资产或投资组合在未来可能发生的波动性,从而帮助投资者评估投资风险。

假设我们有两个资产或投资组合A和B,它们的日收益率分别为r_A和r_B。

我们可以通过R语言中的var函数来计算它们的方差,然后取方差的开平方就可以得到标准差,即风险。

美国R&D税收抵免制度

美国企业“研究与实验”税收抵免制度【摘要】美国联邦政府是最早实施R&D税收优惠的国家,文章试图对美国R&E抵免制度发展历程、R&E活动及QREs界定、税收激励的主要内容、R&E支出的会计处理及R&E抵免制度的评估等进行解析,以便为我国R&D税收激励政策的完善提供可借鉴的经验。

【关键词】美国;R&E抵免制度;R&E活动;QREs(合格的研究费用支出);ASC(替代简化抵免法)自1954年起,美国联邦税法就有关于研发支出从当期所得税中扣除的相关规定,但实施研发税收优惠是从1981年开始的。

从1981年到2011年的30年间,美国企业“研究与实验税收抵免制度”(Research and Eexperiment Tax Credit,简称R&E抵免制度)一直都是临时性制度,但每次到期前美国政府都通过了有关法案对该项制度给予延长,共进行了14次修订,并在不断修订的过程中越来越完善、简化、易于被理解和应用。

一、税收意义上的研发活动及研发支出(一)合格的R&E活动①从税收角度,“合格的研究活动”必须同时满足美国《国内税收法典》(Internal Revenue Code,简称I.R.C.)41条(d)中所列示的“四方面测试”。

1.174条测试。

I.R.C.174条规定,当R&E活动的研究支出满足下面两个条件时,就可以获得税收抵免:一是与纳税人的交易或经营相关;二是属于“实验或实验室意义上的”研发项目成本及随后与之相关的开发和改良成本(包括取得专利的成本)。

但以下活动不能享受R&E抵免:(1)产品商业化后进行的研究活动;(2)为了达到特定客户的要求对现存产品或工艺流程进行的研究;(3)对现存产品或工艺流程进行的复制;(4)调查或研究,包括消费者调查、效率调查和管理研究;(5)对企业内部使用的计算机软件的研究;(6)在美国领土、波多黎各自由邦,以及任一美国领地之外开展的研发活动;(7)在社会科学、艺术或人文学方面的研究;(8)其它个体或政府实体主持的研究;(9)ISO认证。

福斯特税收实验报告

一、引言税收是国家实现宏观调控、调节收入分配、促进经济发展的重要手段。

税收政策的制定与实施直接关系到国家财政收入和纳税人权益。

为了研究税收政策对经济发展的影响,本文以福斯特税收实验为研究对象,通过分析实验结果,探讨税收政策对经济增长、收入分配和税收负担的影响。

二、实验背景与设计1. 实验背景福斯特税收实验是由美国经济学家阿瑟·奥肯于20世纪60年代提出的一种模拟实验。

实验旨在研究税收政策对经济的影响,为政府制定合理的税收政策提供理论依据。

2. 实验设计实验采用模拟经济环境,设定一定的初始条件,通过调整税收政策,观察对经济增长、收入分配和税收负担的影响。

实验分为以下几个阶段:(1)设定初始条件:设定一定的经济规模、人口数量、技术水平、资源禀赋等初始条件。

(2)制定税收政策:设定不同的税率、税收优惠政策等税收政策。

(3)模拟实验:在模拟的经济环境中,根据设定的税收政策,观察经济增长、收入分配和税收负担的变化。

(4)分析实验结果:对实验结果进行统计分析,探讨税收政策对经济的影响。

三、实验结果与分析1. 经济增长实验结果显示,在适当的税收政策下,经济增长呈现出以下特点:(1)税收优惠政策能够刺激经济增长。

实验表明,当税率降低或税收优惠政策实施时,经济增长速度明显加快。

(2)税收政策对经济增长的影响具有滞后性。

税收政策的调整对经济增长的影响并非立即显现,而是经过一段时间后才能体现。

2. 收入分配实验结果显示,税收政策对收入分配的影响主要体现在以下几个方面:(1)税收政策能够调节收入分配。

通过调整税率、税收优惠政策等,税收政策能够使收入分配更加公平。

(2)税收政策对收入分配的影响具有动态性。

随着税收政策的调整,收入分配状况也会发生变化。

3. 税收负担实验结果显示,税收政策对税收负担的影响主要体现在以下几个方面:(1)税收政策能够减轻纳税人负担。

通过降低税率、税收优惠政策等,税收政策能够减轻纳税人负担。

美国CPA考试知识点:联邦个人所得税体系

美国CPA考试知识点:联邦个人所得税体系美国CPA考试知识点:联邦个人所得税体系众所周知,在REG的考试中,联邦税法的内容占到了60%以上的分值,而个人所得税更是重中之重。

可以说,掌握个税知识是通过REG考试的充分必要条件。

回顾公式框架:Gross Income 总收入(Adjustment) 调整项(符合相关规定的费用,可以从总收入中抵减)Adjusted Gross Income 调整后总收入(AGI)(Standard Deduction) 标准扣除Or (二者间取金额较高的一方进行扣除)(Itemized Deduction) 逐项扣除(Exemption) 免税额度Taxable Income 应税收入首先一起来看一下Gross Income的计算。

Gross Income主要包括:劳务与工薪所得、股息所得、财产租赁所得、营业所得、资本利得、退休年金所得等。

大家可以根据Form 1040个人所得税表的Income栏进行学习(Form 1040 Line7-22)下面简单的`介绍一下Becker教材中提到的Gross Income的主要项目:1. Compensation for services(包括工资薪酬,奖金小费,债务减免,廉价购买,guaranteed payment,应税的福利收入)都是应税的,除了以下的三类情况)- Tax exempt interest incomeState and local government bonds/obligationsBonds of a U.S. possessionSeries EE (U.S. savings bond)3. Dividend Income(使用附表Schedule B,通常情况,股利收益都是应税的,但是有较低的税率0%,15%,20%)- Taxable Dividend(Cash= amount received; Property = FMV) - Tax-Free Distributions(Return of Capital,Stock Split,Stock Dividend,Life Insurance Dividend)4. State and Local Tax Refunds(根据去年使用的是Itemized Deduction或者Standard Deduction,来确定州/地方的退税是否应税。

cfa2024年二级原版书课后题

CFA 2024年二级原版书课后题一、公司金融和财务报告分析1.1 企业金融报告的意义企业金融报告是企业向外界公开披露的财务信息,包括企业的资产负债状况、经营成果、现金流量以及股东权益等信息。

通过对企业金融报告的分析,可以帮助投资者了解企业的财务状况,评估企业的经营风险和盈利能力,为投资决策提供重要的参考依据。

1.2 企业金融报告分析的方法企业金融报告分析主要采用财务比率分析、财务趋势分析、现金流量分析、股票市场指标分析等方法。

其中,财务比率分析是最常用的方法之一,通过计算企业的财务比率,包括盈利能力、偿债能力、运营能力、收益能力等指标,来评估企业的财务状况。

1.3 财务报表分析的注意事项在进行财务报表分析时,需要注意一些问题,包括财务信息的准确性和真实性、企业的会计政策和会计估计的合理性、行业和竞争对手的情况、宏观经济环境等因素对企业财务状况的影响。

二、固定收益投资2.1 固定收益投资的特点固定收益投资是指投资者通过购物债券、债务工具等金融资产获得固定的利息收入。

与股票投资相比,固定收益投资具有收益稳定、风险较低的特点,适合风险偏好较低的投资者。

2.2 债券投资的评价指标在进行固定收益投资时,债券的评价指标是十分重要的。

包括债券的到期收益率、债券的久期和凸性、信用评级等指标,可以帮助投资者评估债券的风险和回报。

2.3 固定收益投资组合的管理固定收益投资组合的管理包括资产配置、收益再投资、久期匹配等内容,通过对固定收益投资组合的管理,可以实现风险的分散和收益的最大化。

三、权益投资3.1 权益投资的特点权益投资是指投资者通过购物股票等金融资产获得股息收入和资本收益。

权益投资具有较高的收益潜力,但也伴随着较高的风险。

3.2 股票投资的评价指标在进行权益投资时,股票的评价指标包括市盈率、市净率、股息率、股票的盈利增长率等指标,可以帮助投资者评估股票的估值和风险。

3.3 权益投资组合的管理权益投资组合的管理包括资产配置、股票选择、风险控制等内容,通过对权益投资组合的管理,可以实现风险的分散和收益的最大化。

费尔森-奥尔森估价模型实证检验

pt=bt+α1Xta+α2vt

(7)

公式(7)中,α1=ω/(1+γ-ω) α2=(1+r)/[(1+γ-ω)(1+r-γ)]

这 一 估 值 函 数 ,即 不 需 要 预 测 未 来 股 利 ,也 不 需 要

关于终值的假设,而是通 过 以 上 修 正 回 归 模 型 来 估 计

执业会员,硕士研究生。

36

徐 红 军 :费 尔 森 - 奥 尔 森 估 价 模 型 的 实 证 检 验

Pt=n∑∞=1Et[bt+n-(11++xrt)+nn-bt+n]

(3)

经代数计算可将(3)式写成:

pt=bt+n∑∞=1Et[xt+(1n-+rrb)tn+n-1]-E(1t[+btr+)∞∞]

应计制会计在估值方面 优 于 现 金 制 会 计,则 费 尔 森 -

奥尔森模型的有用性应更多建立在会计数据的特性上。尔 森 - 奥 尔 森 模 型

的实证意义依赖于其第 三 假 设,即 剩 余 收 益 的 信 息 动

态性。这一假设赋予了费尔森-奥尔森模型严格的约

型 的 一 种 重 新 表 述 ,由 以 上 推 演 过 程 可 以 清 楚 地 看 到 ,

它并不依赖于会计数据 的 特 性,而 是 依 赖 于 净 剩 余 会

计 关 系 。Frankel、Lee(1998)证 明 尽 管 股 利 折 现 模 型 的

剩余收益表达形式表面上具有依赖于会计数据的特

点 ,但 从 实 证 角 度 却 没 有 任 何 意 义 。 因 为 ,如 果 要 说 明

一模型 提 出 了 相 对 于 其 他 模 型 更 加 全 面 的 估 值 方 法 。[5-6]但 这 些 实 证 研 究 忽 视 了 剩 余 收 益 的 信 息 动 态 性 特征,将该模型变成了用 剩 余 收 益 代 替 的 股 利 折 现 模 型的衍生模型,导致这一模型失去了其内核。 笔者认为,剩余收益 模 型 所 依 赖 的 理 论 基 础 仍 然

美国RD税收鼓励政策

美国R&D税收鼓励政策由于经济的市场化程度很高,美国政府对内资和外资一视同仁,卡特政府曾于1977年制定了被称为“中性条款”的政策①——美国政府既不鼓励也不阻碍外国投资,从法律上明确了美国对外资和内资相同的政策。

因此,本文介绍的R&D税收鼓励政策一样适用于在美国的外国跨国公司。

固然,美国还有一个关于外资审批制度的规定——埃克森·弗罗里奥条款②,使美国政府能够国家安全为理由对外资进行限制。

随着经济全球化的发展,R&D活动也越来越呈现全球化的趋势。

跨国公司由于自身可持续发展的内在要求,再加上雄厚的资金实力,成为R&D活动的最重要投资来源之一。

世界各国政府为了吸引更多的R&D投资,促进本国科技水平和创新能力的提高,都推出相应的优惠政策,而R&D税收激励政策就是其中重要的政策之一。

一、美国R&D税收激励政策的立法历史③1981年,里根政府通过《经济振兴税收法案》④,规定:以过去3年企业R&D 有效投入的平均值为R&D投入基准值,企业在纳税年度R&D活动的有效投入超出R&D投入基准值的部份,税收可减免25%。

该法案中有关R&D税收鼓励的内容一共进行了12次修订,但每次都是临时立法,最长的有效期为5年,最短的只有6个月。

1986年通过的《税收改革法案》⑤,把税收减免的幅度降为20%,同时延长了R&D税收鼓励政策的有效期,至1988年12月。

1988年通过的《技术与多种收入法案》⑥,改变了R&D投入基准值的计算方式,把以过去3年平均值的浮动基准值改成1984-1988年的平均值的固定基准值,同时将法案的有效期延长1年。

1989年、1990年、1991年先后3次通过法案,将有效期分别延长1年、1年、6个月;1992年7月开始,法案失效;1993年再次通过法案,追溯有效期从1992年7月开始,至1995年7月结束。

耶鲁大学学费对运作收入贡献率的实证分析

注

学费收入包括用于奖

助学金的资金

收稿日期

�� 0 - 0教育部国 Fra bibliotek教育发 展研究中心 高等教育研 究室主

作 者简介 罗建平 北京航空航天大学高 等教育研究所博士研 究生 马陆亭 � � 任 研究员 北京航空航天大学博士生导师 � � � � ( 北京 / 0 0 )

� 确实存 在着 十分 紧密 的内 在依 存关 系

表 年耶鲁大学学费与运作总收入之间的 � � � � � � � 相关分析

� � � � � � � � � � T C OR R P � � � � � � � � � 2 V a ab : � � � � � � � � � � � � � S S a � � � � V a ab � � N � � � � � � M � � � a� � S D S M Ma 16 14 . 89 000 5. 4 3 6 30 238.24 00 0 7. 1 500 0 25. 6 0 000 16 2. 52750 0. 71 84 9 4 0. 4 4 000 1. 4 4 00 0 3. 6 4 0 00 � � � � � � � � � � � � � � � � � � � � Pa C a C , N = 16 � � � � � � � � � � P b > H 0: R =0 � � � � 1. 000 00 0. 91 84 6 < . 0 001 0. 9 184 6 1. 000 00 < . 0 001

� � � � � � 处理 用 表 示 运作 收 入 的 增 长 率 表示 � � � � � � � � � � 二 模 型的 运用 � � � 学费的 增长 率 根据 1994 2009 年 的历 史数据 以 学 本研究以 S P SS 统计分析软件 为分析工具 费收 入 增 长率 为 自 变量 和 运 作 总收 入 增 长率 为 因 变 以耶鲁 大学 1994 统 计数 据为 基础 揭 量进行 简单 线性 回归 分析 结 果如表 3 所 示 � 2009 年间的 � 示运 作 总 收 入 与 学 费 收 入 之 间 的 内 在 的 依 存 关 系 在 学 费 增 长率 对 运 作收 入 增 长率 的 简 单 线 性 回 构建 相 关的 数 学 模� 型 探 讨 学费 收 入 对 运作 总 收 入 � 归模型 中 自变 量和 常数 项的 回归 系数 统计 值都 超 的贡献 率 过了 临 界值 检验 结 果 呈显 著 性 表 明 学 费增 长 率 对 � � � 一� 学费 收入 增长 � 率对运 作收 入 增长 率的 简单 运作 收 入增 长 率的 影 响是 显 著的 回归 方 程 的 F 统 线性回 � 归分 析 � 计值为 6 . 984 也 通过 了显 著性 检验 但回 归模 型的 复 由于 学 费 增长 率 和 运作 收 入 增长 率 指标的变化 相关 系数 为 0. � � 13787 其方 差 解释 能 力仅 为 13. 79% 趋势具 有一 定的 波动 性 很可 能会 产生 异方 差 问题 � D W 统 计 值仅 为 0. 714 4 与 D W 标 准 值 2 还 有较 大 的 � 从而导 致伪 回归 现象 致 使研究 结 论无 效 为了 消 除 差距 这说 明回归 模型 残差 项存 在较 为严 重的 序列 自 � 异方 差 笔 者 对学 费 和 运作 收 入 取对 数 并进 行 差 分 相关问 题

RD税收激励政策效应的实证研究spssstata(1)

R&D税收激励政策效应的实证研究内容摘要:R&D的税收激励政策是在经济一体化的竞争环境下,企业营造自主创新环境并成为技术创新主体的有效对策。

本文选取医药、生物制品和信息技术业两大高新技术产业作为研究对象,研究税收优惠政策对我国高技术产业R&D活动的激励效应。

本文发现:2006年的税收激励政策显著促进了企业的研发投资强度,而2008年的税收激励政策没有起到明显的效果。

同时,本文补充了20个高新技术企业2009-2011年的数据分析,进一步对2008年的R&D税收激励政策进行研究。

这一结论显示了我国采取的R&D费用税前加计扣除的税收优惠政策的有效性。

关键词:研究与开发税收激励政策高新技术企业R&D Empirical Study on the Effect of T ax Incentives Abstract: In the global competitive environment of Economic integration, R&D costs to pre-tax deduction is an effective policy to make an innovation-oriented environment and let Chinese enterprises become the subject of technological innovation. In this paper, we take pharmaceutical, biotechnology and information technology industry in the two major high-tech industries for example to study the effect that preferential taxation policy has put on the R&D costs of high-tech industry. The results showed that: in 2006 the tax incentives promoted enterprise R&D investment intensity significantly, while in 2008 the tax incentives did not play a significant effect. At the same time, this paper has also added new data of 20 high-tech industries from 2009 to 2011, doing further study of the 2008’s R&D preferential taxation policy. This study has concluded that China’s R&D costs to pre-tax deduction plus effectiveness of tax incentives.Key Words: research and development; preferential taxation policy; high-tech industry一、引言(一)研究背景及本文框架在全球经济一体化的竞争环境下,我国企业面临着国外跨国公司的严峻挑战。

RD溢出对中国制造业全要素生产率的影响基于产业间、国际贸易和FDI三种溢出渠道的实证检验

将国际贸易和FDI作为解释变量,运用面板数据模型进行回归分析。最后, 我们对模型进行协整检验,以判断这些变量之间是否存在长期均衡关系。

在实证分析阶段,我们发现国际贸易和FDI对中国全要素生产率的影响存在 明显的地区差异。具体来说,对于东部地区而言,国际贸易和FDI对全要素生产 率的促进作用较为显著;而对于中西部地区来说,这两个因素可能会对全要素生 产率产生负面影响。

为了缓解国际贸易对生产率增长的负面影响,我们可以采取以下措施。首先, 加强贸易自由化,推动多边贸易体系的完善,降低贸易壁垒,从而促进国际贸易 的发展。其次,推动技术创新和技术转移,提升自身技术水平的加强国际技术合 作,

实现技术共享。此外,政府可以通过政策扶持,鼓励企业加大研发投入,提 高企业的技术创新能力。

在目前的文献中,关于人力资本、空间溢出与省际全要素生产率增长的研究 已经取得了不少进展。然而,大多数研究集中在国家或区域层面,针对我国省际 层面的研究相对较少。此外,在研究方法上,传统的研究往往采用单一的空间权 重测度方法,

难以全面反映空间溢出的效应。因此,本次演示旨在通过实证检验,探讨不 同空间权重测度方法对省际全要素生产率增长的影响,为相关政策制定提供科学 依据。

然而,国际贸易对生产率增长的影响并非全然积极。在现实中,国际贸易往 往受到各种贸易壁垒的制约,这些壁垒包括关税、非关税壁垒等,对生产率的提 升产生了负面影响。此外,国际贸易还可能导致技术转移的不均衡。一些发达国 家可能通过技术

封锁和知识产权保护等手段,维持自身技术在全球的领先地位,阻碍了技术 的传播和生产率的全面提升。

对于不同方法的差异和原因,我们认为:空间自回归模型和空间误差模型均 基于传统的线性回归模型,难以充分考虑非线性关系和复杂机制的影响。相比之 下,空间权重矩阵可以更加灵活地处理各种空间关系,但可能受到数据质量和准 确性的影响。

全球价值链与最优关税政策

有鉴于此,本文在 Bl

ancha

r

de

ta

l(

2016)模型的基础上,融入企业运用中间投入品生产并征收中

间品关税的行为。之后ຫໍສະໝຸດ 本文 运 用 2000—2014 年 世 界 投 入 产 出 表 (

wo

r

l

di

npu

t

ou

t

tt

对进口最终品所征关税。机制分析发现,中间品关税主要通过产品价格影响最终品关税的制定;国

内增加值对最终品关税的影响会随着国内增加值的增加而加 强,国 外 增 加 值 对 最 终 品 关 税 的 影 响

会随着国外增加值的增加而有所削弱。

关键词:全球价值链

最终品关税

中间品关税

增加值

一、引言

全球价值链(

l

oba

— 75 —

2020 年第 12 期

定”是对西方代议制民主简化的一种描述,实际中的政策会受到选票、舆论和游说集团捐献的共同影

响。针对于此,

Gr

o

s

sman & He

l

1994)构建了同时考虑游说集 团 捐 献 和 消 费 者 福 利 的 保 护 待

pman(

售模型。模型中政府和游说集团存在策略性互动:有组织的游说集团通过政治献金游说政府寻求政

察模型的解释力。第三,本文也是对 近 期 运 用 投 入 产 出 方 法 研 究 贸 易 增 加 值 相 关 文 献 的 补 充,研 究

方法和计算结果为后续的研究提供了参考。

二、文献综述

与本文相关的文献主要可分两类:一是关于传统情形下一国最优关税的设定,二是有关 GVC 核

异质消费者条件下的最大收入关税和最佳福利关税

异质消费者条件下的最大收入关税和最佳福利关税

翟伟峰;左跃荣

【期刊名称】《石家庄学院学报》

【年(卷),期】2011(013)002

【摘要】在异质消费者条件下,无论企业只进行价格竞争还是先进行位置竞争后进行价格竞争,其结果都是最佳福利关税大于最大收入关税,这与Johnson(1951)的结论截然相反.

【总页数】4页(P16-19)

【作者】翟伟峰;左跃荣

【作者单位】南开大学,经济研究所,天津,300071;石家庄市桥东区文化体育局,河北,石家庄,050011

【正文语种】中文

【中图分类】F745.0

【相关文献】

1.异质产品条件下最佳关税对本土企业的影响 [J], 刘艳梅;段欣辰

2.Stackelberg竞争条件下的最佳福利关税与最大收入关税 [J], 谢申祥;李长英

3.价格领导竞争下的最大收入关税与最佳福利关税 [J], 谢申祥;商龙燕

4.关税对企业贸易边际的异质性影响——基于关税水平和关税政策不确定性的视角[J], 赵晓涛;邱斌;陈晓平

5.关税递减的福利效应及其实证分析——CEPA货物贸易零关税的一种验证 [J], 郑桂环;汪寿阳

因版权原因,仅展示原文概要,查看原文内容请购买。

负所得税问题

负所得税问题负所得税效果 (Negative income tax)弗里德曼对没有独立生活才干的儿童的直接救援与援助方案,不过是整个福利冰山的高峰而已。

存在着令人眼花照乱的、从福利的角度被证明是正确的、详尽的政府方案——虽然普通说来它们的结果经常是不幸的:如公共住房方案,城市重建方案,老人与失业保险方案,任务培训方案,以及在错误地命名的〝贫穷之战〞的名义下所停止的那许许多多各式各样的方案,农产品价钱支持方案,等等,无量无尽。

负所得税在确保一切的人的最低年支出效果上,存在着一种与我们目前的方案百宝囊相比要好得多的方法。

这种方法就是要应用我们借以收缴大局部税收的那种机制,即团体所得税。

一度,公民们被要求以实物支付的方式来为国度作出贡献——如用于公共项目的食物或木材的强迫征集,或休息力的强迫征用。

这一原那么在许多落后地域依然存在。

货币税对实物税的替代,既促进了自在,又促进了效率。

在我们的福利方案中,我们又回到了早先的时代:以实物方式来施予恩赐〔或许试图这样做〕,并且调查接受者的详细的物质条件。

这里,取得提高的途径异样是用货币支付来取代实物支付,用单一的、数字的支出状况调查来取代我们如今所运用的、含义模糊的生活状况调查。

我将这种协助穷人的方法称之为〝负所得税〞,目的是要强调它与现行的所得税之间,在概念上与方法上的分歧性。

这种方法的实质是想经过补贴穷人的支出来扩展所得税,补贴的数额就是穷人不曾运用的所得税减免份额。

依照目前的法律,一个四口之家有资历享用不低于 3O00美元〔假设这个家庭运用的是规范扣除额的话,那么刚好是3000美元〕的税收减免。

假设这样一个家庭的总支出是3000美元的话,那么他们一分钱的税也没有交。

假设这个家庭的税前总支出是4000美元的话〔而且运用规范扣除额〕,那么,它有1000美元的、正的应征税支出。

在目前适用于这一等级的、14% 的税率之下,它一年应交税140美元。

留下了 3860美元的税后支出〔见表〕。

英国高等教育财政问责:成本透明核算

英国高等教育财政问责:成本透明核算摘要:财政透明度是现代公共管理的必然要求,财政信息公开是财政透明度的本质规定和重要内容。

成本透明核算使英国高校的财务透明度大大提高,成为英国高等教育财政问责的重要路径。

成本透明核算体系具备如下四个特征:其一,以作业成本法为基础,使高校成本核算对象更加明确;其二,通过选取合理的成本动因,使间接成本的分配更加科学;其三,通过成本调整计算,能够更全面地反映各类活动的成本;其四,间接成本率的计算为项目资助方补偿高校的间接成本提供了合理依据,最终推进高校的可持续发展。

关键词:英国;高等教育;财政问责;成本透明核算中图分类号:G649.561文献标识码:A文章编号:1672-0059 (2013) 06-0071-05自20世纪80年代起,在新公共管理思潮影响下,英国政府逐渐削减高等教育经费,与此同时,对财政拨款的使用效率和效益方面的要求也越来越高。

1985年,《贾勒特报告》提出:“大学在资源规划和使用中,应尽可能提高效率和效益” ;1988年,英国教育和科学部通过了《教育改革法案》,该法案将财务预算的概念引入到高校校长管理学校财务的过程中,这与《贾勒特报告》倡导的高等教育机构加强自身的财务责任精神相一致,并都在高等教育领域得到贯彻:1994 年,英格兰高等教育基金委员会要求:“高等教育机构按照每年的实际情况递交研究经费分配报告”。

为了确保流向高等院校的财政拨款能够得到合理运用,保证大学财政健康,防范大学出现无可挽回的财政亏损与财政赤字,英国各级政府经过长期探索和实践,采取三个主要措施对高等教育进行财政问责:一是与高校签署财政备忘录;二是对高校进行风险评估和风险管理;三是要求高校实施成本透明核算。

本文将主要对英国高等教育的成本透明核算体系进行研究。

财政透明度是现代公共管理的必然要求,也是保障政府履行财政受托责任的必由之路。

财政信息公开是财政透明度的本质规定和重要内容。

英国政府1998年在《财政稳定守则》中将财政透明度作为财政政策的五个原则之一。

费希尔指数

费希尔指数

费希尔指数(Theil index)是衡量财富或收入分配不平等程度的一个指数。

它由荷兰经济学家范·费希尔于1967年提出,是一种常见的财富或收入分配不平等度量方法,广泛应用于经济学、社会学、政治学等领域。

T=X1ln(X1/Y1)+X2ln(X2/Y2)+……+Xnln(Xn/Yn)

其中,Y=[y1,y2,……,yn]是比例值向量的平均值。

费希尔指数的值越大,表明收入或财富分配越不平等;指数越小,则反映出分配越平等。

费希尔指数是一种相对指标,不受经济体总量变化的影响,主要用于衡量不同群体之间的分配差异。

它的优点是比较直观、易于计算,并且能够同时考虑不同人口群体之间的收入、财富分配。

在实际应用中,费希尔指数可以用于分析不同年龄、性别、地区、职业、民族、教育程度等人口群体之间的收入或财富分配差异。

比如,可以用费希尔指数来分析某个国家或地区中城乡收入分配的不平等程度,或者比较不同国家之间的收入或财富分配的差异。

然而,费希尔指数也存在一些局限性。

首先,它没有考虑人口数量等其他因素对收入或财富分配的影响。

其次,它的计算方法比较复杂,需要对大量数据进行分类、排序和归一化处理,容易出现误差。

最后,由于收入或财富的分配具有多维度、复杂性和动态性,费希尔指数也不能完全反映它们的本质特征和演化规律。

因此,应用费希尔指数需要结合其他指标和方法来综合分析,以更全面、深入和准确地了解收入或财富分配的状况和趋势,为制定合理的经济、社会和政策决策提供科学的依据。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Results of Taxonomic Evaluation of RDF(S) and DAML+OIL Ontologies using RDF(S) and DAML+OIL Validation Tools and Ontology Platforms Import ServicesAsunción Gómez-Pérez, M. Carmen Suárez-FigueroaLaboratorio de Inteligencia Artificial Facultad de Informática Universidad Politécnica de Madrid Campus de Montegancedo sn. Boadilla del Monte, 28660. Madrid, Spain asun@fi.upm.es mcsuarez@delicias.dia.fi.upm.esAbstract. Before using RDF(S) and DAML+OIL ontologies in Semantic Web applications, its content should be evaluated from a knowledge representation point of view. In recent years, some RDF(S) and DAML+OIL ‘checkers’, ‘validators’, and ‘parsers’ have been created and several ontology platforms are able to import RDF(S) and DAML+OIL ontologies. Two are the experiments presented in this paper. The first one reveals that the majority of RDF(S) and DAML+OIL parsers (Validating RDF Parser, RDF Validation Service, DAML Validator, and DAML+OIL Ontology Checker) do not detect taxonomic mistakes in ontologies implemented in such languages. So, if such ontologies are imported by ontology platforms, are they able to detect such problems? The second experiment presented in this paper reveals that the majority of the ontology platforms (OilEd, OntoEdit, Protégé-2000, and WebODE) only detect a few of mistakes in concept taxonomies before importing them.1 Introduction In recent years, considerable progress has been made in developing the conceptual bases for building technology that allows reusing and sharing ontologies for the Semantic Web. As any other resource used in software applications, ontology content should be evaluated before (re)using it in other ontologies or applications. In that sense, we could say that it is unwise to publish an ontology or to implement software that relies on ontologies written by others (even by yourself) without first evaluating its content, that is, its concept definitions, its taxonomy and its formal axioms. Ontology evaluation is an important activity to be carried out during the whole ontology life-cycle. Up to now, few domain-independent methodological approaches [6, 11, 15, 17] include an evaluation activity. The first works on ontology content evaluation started in 1994 [9, 10], and in the last three years the interest of the Ontological Engineering community in this issue has grown. The main efforts were made by Gómez-Pérez [7, 8] and by Guarino andcolleagues with the OntoClean method [12]. ODEClean [5] is a tool integrated into the WebODE environment that gives support to the OntoClean method. With the increasing number of ontologies implemented in the ontology markup languages RDF(S) [3, 13] and DAML+OIL [18], many specialized ontology validation tools for these languages have been built: Validating RDF Parser1, RDF Validation Service2, DAML Validator3, DAML+OIL Ontology Checker4, etc. These tools are mainly focused on evaluating ontologies from a syntactic point of view, that is, checking whether the ontologies are compliant with the languages specification. However, they are not focused on detecting mistakes from a knowledge representation point of view, that is, if the ontologies have inconsistencies and redundancies. We have performed experiments with 24 ontologies (7 on RDF(S) and 17 on DAML+OIL), which are well built from a syntactic point of view, according to the languages specifications, but have inconsistencies and redundancies. We have parsed them with the previous four tools and we have discovered that on the majority of the experiments, they do not detect the taxonomic mistakes identified in [7]. The key point is that RDF(S) and DAML+OIL ontologies are imported by ontology platforms. In fact, OilEd [2], OntoEdit [16], Protégé-2000 [14], and WebODE [4, 1] are able to import ontologies implemented in both languages, but there are not previous works analysing whether such platforms are able to detect wrong RDF(S) and DAML+OIL ontologies. In order to carry out this analysis, we have used the same 24 ontologies (7 on RDF(S) and 17 on DAML+OIL) and we have imported them within the previous ontology platforms. We have found out that on the majority of the experiments, these ontology platforms do not detect mistakes in concept taxonomies represented in RDF(S) and DAML+OIL. This paper is organized as follows, section two presents briefly the method for evaluating taxonomic knowledge in ontologies. Section three presents a description of some ontology ‘checkers’, ‘validators’, and ‘parsers’. Section four includes our first comparative study, including examples of the RDF(S) and DAML+OIL ontologies used on the testbed. Section five presents an overview of some ontology platforms. Section six presents the results of importing RDF(S) and DAML+OIL ontologies with taxonomic mistakes in the ontology platforms. Finally, we conclude with further work on evaluation. 2 Method for Evaluating Taxonomic Knowledge in Ontologies Figure 1 presents a set of possible mistakes that can be made by ontologists when modeling taxonomic knowledge in an ontology under a frame-based approach [7]. In this paper we only focus on inconsistency mistakes (circularity and partition) and redundancy mistakes (grammatical), and we postpone the analysis of the others for further works. Below we explain briefly the studied mistakes.1 2http://139.91.183.30:9090/RDF/VRP/ /RDF/Validator/ 3 /validator/ 4 /oil/CheckerFigure 1. Types of mistakes that might be made when developing taxonomies with framesInconsistency: Circularity Errors occur when a class is defined as a specialization or generalization of itself. Depending on the number of relations involved, circularity errors can be classified as circularity errors at distance zero (a class with itself), circularity errors at distance 1, and circularity errors at distance n. Inconsistency: Partition errors. Concept classifications can be defined in a disjoint (disjoint decompositions), a complete (exhaustive decompositions), and a disjoint and complete manner (partitions). The following types of partition errors are identified: Common classes in disjoint decompositions and partitions. These occur when there is a disjoint decomposition or a partition class-p1,…, class-pn defined in a class class-A, and one or more classes class-B1,..., class-Bk are subclasses of more than one class-pi. Common instances in disjoint decompositions and partitions. These errors happen when one or several instances belong to more than one class of a disjoint decomposition or partition. External classes in exhaustive decompositions and partitions. They occur when having defined an exhaustive decomposition or a partition of the base class (class-A) into the set of classes class-p1,..., class-pn, and there are one or more classes that are subclasses of the class-A, instead of being subclasses of a class the set of classes class-p1,..., class-pn. External instances in exhaustive decompositions and partitions. These errors occur when we have defined an exhaustive decomposition or a partition of the base class (class-A) into the set of classes class-p1,..., class-pn, and there are oneor more instances of the class-A that do not belong to any class class-pi of the exhaustive decomposition or partition. Redundancy: Grammatical Errors. Redundancies of ‘subclass-of’ relations occur between classes they have more than one ‘subclass-of’ relation. We can distinguish direct and indirect repetition. Redundancies of ‘instance-of’ relations. As in the above case, we can distinguish between direct and indirect repetition. 3 Ontology ‘Checkers’, ‘Validators’ and ‘Parsers’ At the moment, there exist various ontology ‘checkers’, ‘validators’, and ‘parsers’ which are intended to carry out some kind of validation and/or checking of ontologies on diverse web-based languages. In this paper, we focus on the most frequently used parsers that validate and/or check ontologies on RDF(S) and DAML+OIL: Validating RDF Parser and RDF Validation Service for RDF(S), and DAML Validator and DAML+OIL Ontology Checker for DAML+OIL. Other parsers not included in this paper are: Rapier RDF Parser5, Thea RDF Parser6, Chimaera7, ConsVISor8, etc. The Validating RDF Parser. The ICS-FORTH RDFSuite9 is a suite of tools for RDF metadata management. This RDFSuite consists of tools for parsing, validating, storing and querying RDF descriptions, namely the Validating RDF Parser (VRP), the RDF Schema Specific DataBase (RSSDB) and the RDF Query Language (RQL). The ICSFORTH Validating RDF Parser (VRP v2.5)10 analyzes, validates and processes RDF schemas and resource descriptions. This parser offers the following functions: • Syntactic Validation for checking if the RDF/XML syntax of the input namespace conforms to the updated RDF/XML syntax proposed by W3C. • Semantic Validation for verifying the selected constraints derived from RDF Schema Specification (RDFS). VRP allows to choose several semantic validation constraints: class hierarchy loops, property hierarchy loops, domain and range of subproperties, source and target resources of properties, and types of resources. RDF Validation Service. The W3C RDF Validation Service11 is based on HP-Labs Another RDF Parser (ARP12), which currenlty uses the version 2-alpha-1. This online service supports the Last Call Working Draft specifications issued by the RDF Core Working Group, including datatypes. This online service offers the following functions: • Syntactic Validation for checking if the input namespace conforms to the updated RDF/XML Syntax Specification proposed by W3C.5 6/raptor/ http://www.semanticweb.gr/ 7 /software/chimaera/ 8 /index.html 9 Partially supported by EU projects C-Web (IST-1999-13479), MesMuses (IST-2001- 26074), and QUESTION-HOW (IST-2000-28767) 10 http://139.91.183.30:9090/RDF/VRP/index.html 11 /RDF/Validator/ 12 ARP was created and is maintained by Jeremy Carroll at HP-Labs in Bristol• Semantic Validation. The service does not do any RDF Schema Specification validation. DAML Validator. The DAML Validator13 is available via either a WWW interface or download. The Validator uses the ARP parser from the Jena (1.6.1) toolkit to create an RDF triple model from the input code being validated. The DAML Validator checks DAML+OIL markup for problems beyond simple syntax errors. The Validator reads in a DAML file and examines it for a variety of potential errors. The output is a list of indications (errors, warnings, or information), a pointer to the errors in the file, and some guidance on the nature of the problems. It offers the following functions: • Syntactic Validation for checking for namespace problems (outdated URIs, file extensions in URIs) during model creation. The validator tests RDF resources for existence: any subject, or object resource that is referenced must have a defined type. • Semantic Validation for verifying the global domain and range constraints of the predicate. The subject and object of a statement should be instances of the predicate’s domain and range classes. Each node (RDF Resource and it’s accompanying statements) is validated based on the following types: Class, Property, Restriction, ObjectRestriction, DatatypeRestriction, or an Instance of one or more classes. DAML+OIL Ontology Checker. The DAML+OIL Checker14 was developed by University of Manchester (UK). The DAML+OIL Checker is a servlet that uses the OilEd codebase to check the syntax of DAML+OIL ontologies and returns a report on the classes and properties in the model. This checker is a web interface to check DAML+OIL ontologies and content using Jena. It offers the following functions: • Syntactic Validation for checking missing definitions. The checker is fairly strict about the format of the input: in particular “rdf:ID attributes” must be conforming XML names, and unqualified attributes should not be used. • Semantic Validation for verifying class hierarchy loops. 4 Comparative Study of RDF(S) and DAML+OIL ‘Checkers’, ‘Validators’ and ‘Parsers’ As we said before, the first goal of this paper is to analyse whether RDF(S) and DAML+OIL parsers presented in section 3 detect the concept taxonomy mistakes presented in section 2. In order to achieve this goal, we have built a testbed of 24 ontologies (7 in RDF(S) and 17 in DAML+OIL), each of which implements one of the errors presented in section 2. And we have parsed them with the previous parsers. In the case of RDF(S) we have only 7 ontologies because partitions cannot be defined in this language. These ontologies and the results of their evaluation can be found at http://minsky.dia.fi.upm.es/odeval/index.html.13 14/validator/ /oil/CheckerIn figure 2 we show the RDF(S) code and graphical notation of two of these ontologies: the one that implements the circularity error at distance 2, and the one that implements the mistake of indirect redundancy of ‘instance-of’ relation. Figure 3 shows the DAML+OIL code and graphical notation of three of these ontologies: the one that implements the circularity error at distance 1, the one that implements the mistake of common class in disjoint decomposition, and the last one that implements the mistake of external instance in partition.a) Loop at distance 2b) Indirect redundancy of ‘instance-of’ relationFigure 2. Examples of RDF(S) ontologiesAfter parsing the ontologies on the testbed with the parsers, we found that all these parsers recognised the code as well formed code, but the majority had problems detecting most of the knowledge representation mistakes that these ontologies contained. The results of analysing and comparing these parsers are shown in table 1. The symbols used in this table are the following: : The parser does not accept files written in this language : The parser detects the mistake in this language : The parser does not detect the mistake in this language --: The mistake cannot be represented in this languagea) Loop at distance 1b) Common class in disjoint decompositionc) External instance in partitionFigure 3. Examples of DAML+OIL ontologiesAs we can see in table 1, we have checked whether RDF(S) tools (VRP and RDF Validation Service) were able to evaluate DAML+OIL files, and whether DAML+OIL tools (DAML Validator and DAML+OIL Ontology Checker) were able to evaluate RDF(S) files. In the case of RDF(S) tools, the experiments showed that RDF Validation Service can read DAML+OIL ontologies, although it does not detect the mistakes, but VRP cannot read them. In the case of DAML+OIL tools, the experiments showed that both of them are able to recognize RDF(S) files. Althoughthe DAML+OIL Ontology Checker is not a RDF(S) validation tool, it was able to detect circularity errors in that language. Before going in detail with circularity errors, we have an important comment to make. The RDF(S) and DAML+OIL specifications allow cycles in concept taxonomies. However, we consider that this is a mistake from the knowledge representation point of view, that is, we would not recommend designing ontologies with cycles in their concept taxonomies. So here we want to stress the distinction between checking an ontology from a syntactic point of view (checking whether the ontology is compliant with the language specification) and checking an ontology from a knowledge representation point of view (checking whether the ontology does not have the mistakes presented in section 2). Circularity errors are the only ones detected by some of the parsers studied in this experiment. VRP is able to detect circularity errors at any distance in RDF(S) ontologies, indicating that there is a semantic error (“loop detected”). The DAML+OIL Ontology Checker detects circularity errors at any distance in RDF(S) and DAML+OIL ontologies, throwing a warning about it (“cycles in class hierarchy”). Regarding partition errors, they have only been studied for DAML+OIL, since they cannot be represented in RDF(S). None of the DAML+OIL validators, neither the RDF Validation Service, have detected partition errors with the 10 ontologies from the testbed. The same occurs with the grammatical redundancy errors, which are not detected by any of the RDF(S) and DAML+OIL parsers studied. 5 Ontology Platforms In this paper we focus on the most representative ontology platforms that can be used for importing ontologies: OilEd, OntoEdit, Protégé-2000, and WebODE. In this section, we provide a broad overview of these ontology platforms. OilEd15 [2] was initially developed as an ontology editor for OIL ontologies, in the context of the European IST OntoKnowledge project. However, OilEd has evolved and now is an editor of DAML+OIL and OWL ontologies. OilEd can import ontologies implemented in RDF(S), OIL, DAML+OIL, and the SHIQ XML format. Besides exporting ontologies to DAML+OIL, OilEd ontologies can be exported to the RDF(S) and OWL ontology languages and to the XML formats SHIQ and DIG. OntoEdit16 [16] has been developed by AIFB in Karlsruhe University. It is an extensible and flexible environment, based on a plugin architecture, which provides functionality to browse and edit ontologies. It includes plugins for reasoning using Ontobroker, plugins for exporting and importing ontologies in different formats (FLogic, OXML, RDF(S), DAML+OIL), etc. Two versions of OntoEdit are available: OntoEdit Free and OntoEdit Professional.15 16 http://www.ontoprise.de/com/start_downlo.htmICS-FORTH Validating RDF ParserRDF(S) DAML+OILRDF Validation ServiceRDF(S) DAML+OILDAML ValidatorRDF(S) DAML+OILDAML+OIL Ontology CheckerRDF(S) DAML+OILInconsistency: Circularity ErrorsAt distance zero At distance one At distance n Direct Common classes in disjoint decompositions Indirect Common classes in partitions Direct Common instances in disjoint decompositions Indirect Common instances in partitions External classes in exhaustive decompositions External classes in partitions External instances in exhaustive decompositions External instances in partitions Redundancies of ‘subclass-of’ relations Redundancies of ‘instance-of’ relations Direct Indirect Direct IndirectInconsistency: Partition Errors-------------------------------------------Redundancy: Grammatical ErrrosTable 1. Results of the analysis of the RDF(S) and DAML+OIL parsersProtégé-200017 [14] has been developed by the Stanford Medical Informatics (SMI) at Stanford University, and is the latest version of the Protégé line of tools. It is an open source, standalone application with an extensible architecture. The core of this environment is the ontology editor, and it holds a library of plugins that add more functionality to the environment (ontology language importation and exportation, OKBC access, constraints creation and execution, etc.). Protégé-2000 ontologies can be exported and imported with some of the backends provided in the standard release or as plugins: RDF(S), DAML+OIL, OWL, XML, XML Schema, and XMI. WebODE18 [4, 1] has been developed by the Ontology Engineering Group at Universidad Politécnica de Madrid (UPM). It is an ontology-engineering suite created with an extensible architecture. WebODE is not used as a standalone application, but as a Web application. There are several services for ontology language import and export (XML, RDF(S), DAML+OIL, OIL, OWL, CARIN, FLogic, Jess, Prolog), axiom edition with WAB (WebODE Axiom Builder), ontology documentation, ontology evaluation, and ontology merge. 6 Comparative Study of Ontology Platforms Import Services As we said before, the second main goal of this paper is to analyse whether ontology platforms presented in section 5, are able to detect taxonomic mistakes in RDF(S) and DAML+OIL ontologies before importing them. In order to carry out this experiment, we have reused the same 24 ontologies (7 in RDF(S) and 17 in DAML+OIL with inconsistency and redundancy mistakes) used in the previous experiment. In the case of RDF(S) we have only 7 ontologies because partitions cannot be defined in this language. We have imported these ontologies using the import facilities of the ontology platforms presented in section 5. Table 2 presents the results of the experiment using the following symbols: : The ontology platform does not allow representing this type of mistake : The ontology platform detects the mistake during ontology import : The ontology platform does not detect the mistake during ontology import -- : The mistake cannot be represented in this language The main conclusions of the RDF(S) and DAML+OIL ontology import are: Circularity errors at any distance are the only ones detected by most of ontology platforms analyzed in this experiment. However, OntoEdit Free does not detect circularity errors at distance zero, but it ignores them. Regarding partition errors, we have only studied DAML+OIL ontologies because this type of knowledge cannot be represented in RDF(S). Most of ontology platforms used in this study do not detect partition errors in DAML+OIL ontologies. Furthermore, some partition errors (common instance in partitions, external instance17 18/plugins.html http://webode.dia.fi.upm.es/in exhaustive decompositions, etc.) cannot be represented in the ontology platforms studied. Only WebODE detects some partition errors using the ODEval19 service. Grammatical redundancy errors are not detected by most of ontology platforms used in this work. However some ontology platforms ignore direct redundancies of ‘subclass-of’ or ‘instance-of’ relations. As the previous case, only WebODE detects indirect redundancies of ‘subclass-of’ relations in RDF(S) and DAML+OIL ontologies using the ODEval service. 7 Conclusions and Further Work In this paper we have shown that, in general, current RDF(S) and DAML+OIL ‘checkers’, ‘validators’, and ‘parsers’ are not able to detect mistakes from a knowledge representation point of view, but they mainly focus on the syntactic validation of the RDF(S) and DAML+OIL ontologies that they parser. We have also shown that only a few taxonomic mistakes in RDF(S) and DAML+OIL ontologies are detected by ontology platforms which are able to import ontologies in such languages. Taking into account that only a few parsers are able to detect loops in RDF(S) and DAML+OIL taxonomies, we considered that it is necessary to create more advanced evaluators than those already existing for evaluating RDF(S) and DAML+OIL from a knowledge representation point of view. We also consider that it is necessary to create more advanced ontology import services in ontology platforms. We think that much work must be made to integrate ontology evaluation functions in ontology development tools, and to create an integrated ontology evaluation tool suite that will permit analyzing ontologies in different languages and KR formalisms.Acknowledgements This work has been supported by the Esperonto project (IST-2001-34373), by the Spanish project ‘Plataforma Tecnológica para la web semántica: Ontologías, análisis de lenguaje natural y comercio electrónico’ (TIC-2001-2745), and by a research grant from UPM (“Beca asociada a proyectos modalidad B”). We thanks for his comments and revisions to Óscar Corcho.19http://minsky.dia.fi.upm.es/odevalOilEdRDF(S) DAML+OILOntoEdit FreeRDF(S) DAML+OILProtégé-2000RDF(S) DAML+OILWebODERDF(S) DAML+OILInconsistency: Circularity ErrorsAt distance zero At distance one At distance n Common classes in disjoint decompositions Direct IndirectInconsistency: Partition ErrorsCommon classes in partitions Direct Common instances in disjoint decompositions Indirect Common instances in partitions External classes in exhaustive decompositions External classes in partitions External instances in exhaustive decompositions External instances in partitions Direct Redundancies of subclass-of relations Indirect Direct Redundancies of instance-of relations Indirect--------------------------------------------Redundancy: Grammatical ErrorsTable 2. Results of the RDF(S) and DAML+OIL ontology importReferences1. 2. Arpírez JC, Corcho O, Fernández-López M, Gómez-Pérez A (2003) WebODE in a nutshell. AI Magazine To be published in 2003 Bechhofer S, Horrocks I, Goble C, Stevens R (2001) OilEd: a reason-able ontology editor for the Semantic Web. In: Baader F, Brewka G, Eiter T (eds) Joint German/Austrian conference on Artificial Intelligence (KI’01). Vienna, Austria. (Lecture Notes in Artificial Intelligence LNAI 2174) Springer-Verlag, Berlin, Germany, pp 396–408 Brickley D, Guha RV (2003) RDF Vocabulary Description Language 1.0: RDF Schema. W3C Working Draft. /TR/PR-rdf-schema Corcho O, Fernández-López M, Gómez-Pérez A, Vicente O (2002) WebODE: an Integrated Workbench for Ontology Representation, Reasoning and Exchange. In: GómezPérez A, Benjamins VR (eds) 13th International Conference on Knowledge Engineering and Knowledge Management (EKAW’02). Sigüenza, Spain. (Lecture Notes in Artificial Intelligence LNAI 2473) Springer-Verlag, Berlin, Germany, pp 138–153 Fernández-López M, Gómez-Pérez A (2002) The Integration of OntoClean in WebODE. In: Angele J, Sure Y (eds) EKAW02 Workshop on Evaluation of Ontology-based Tools (EON2002), Sigüenza, Spain, pp 38-52. Fernández-López M, Gómez-Pérez A, Pazos-Sierra A, Pazos-Sierra J (1999) Building a Chemical Ontology Using METHONTOLOGY and the Ontology Design Environment. IEEE Intelligent Systems & their applications 4(1) (1999) 37-46. Gómez-Pérez A (2001) Evaluating ontologies: Cases of Study. IEEE Intelligent Systems and their Applications. Special Issue on Verification and Validation of ontologies. Marzo 2001, Vol 16, Nº 3. Pag. 391 – 409. Gómez-Pérez A (1996) A Framework to Verify Knowledge Sharing Technology. Expert Systems with Application. Vol. 11, N. 4. PP: 519-529. Gómez-Pérez A (1994) Some ideas and Examples to Evaluate Ontologies. Technical Report KSL-94-65. Knowledge System Laboratory. Stanford University. Also in Proceedings of the 11th Conference on Artificial Intelligence for Applications. CAIA94. Gómez-Pérez A (1994) From Knowledge Based Systems to Knowledge Sharing Technology: Evaluation and Assessment. Technical Report. KSL-94-73. Knowledge Systems Laboratory. Stanford University. December. Grüninger M, Fox MS (1995) Methodology for the design and evaluation of ontologies. In Workshop on Basic Ontological Issues in Knowledge Sharing (Montreal, 1995). Guarino N, Welty C (2000) A Formal Ontology of Properties In R. Dieng and O. Corby (eds.), Knowledge Engineering and Knowledge Management: Methods, Models and Tools. 12th International Conference, EKAW2000, LNAI 1937. Springer Verlag: 97-112. 2000. Lassila O, Swick R (1999) Resource Description Framework (RDF) Model and Syntax Specification. W3C Recommendation. /TR/REC-rdf-syntax/ Noy NF, Fergerson RW, Musen MA (2000) The knowledge model of Protege-2000: Combining interoperability and flexibility. In: Dieng R, Corby O (eds) 12th International Conference in Knowledge Engineering and Knowledge Management (EKAW’00). JuanLes-Pins, France. (Lecture Notes in Artificial Intelligence LNAI 1937) Springer-Verlag, Berlin, Germany, pp 17–32 Staab S, Schnurr HP, Studer R, Sure Y (2001) Knowledge Processes and Ontologies, IEEE Intelligent Systems, 16(1). 2001. Sure Y, Erdmann M, Angele J, Staab S, Studer R, Wenke D (2002) OntoEdit: Collaborative Ontology Engineering for the Semantic Web. In: Horrocks I, Hendler JA (eds) First International Semantic Web Conference (ISWC’02). Sardinia, Italy. (Lecture Notes in Computer Science LNCS 2342) Springer-Verlag, Berlin, Germany, pp 221–2353. 4.5. 6. 7. 8. 9. 10. 11. 12.13. 14.15. 16.。