纳税人的权利和义务(英文版)

中华人民共和国营业税暂行条例中英对照

中华人民共和国营业税暂行条例中英对照中华人民共和国营业税暂行条例PROVISIONAL REGULATIONS OF THE PEOPLE'S REPUBLIC OF CHINA ONBUSINESSTAX第一条在中华人民共和国境内提供本条例规定的劳务(以下简称应税劳务)、转让无形资产或者销售不动产的单位和个人,为营业税的纳税义务人(以下简称纳税人),应当依照本条例缴纳营业税。

Article 1 All units and individuals engaged in the provision of services as prescribed in these Regulations (hereinafter referred to as 'taxable services'), the transfer of intangible assets or the sale of immovable properties within the territory of the People's Republic of China shall be taxpayers of Business Tax (hereinafter referred to be 'taxpayers'), and shall pay Business Tax in accordance with these Regulations.第二条营业税的税目、税率,依照本条例所附的《营业税税目税率表》执行。

Article 2 The taxable items and tax rates of Business Tax shall be determined in accordance with the <Business Tax Taxable Items and Tax Rates Table> attached to these Regulations.税目、税率的调整,由国务院决定。

法律英语11税法111 税法简介

2020/9/2

tax law

8

Two specific limitations

Direct taxes Capitation taxes

1. 直接税与人头税必须在各州间按人 口的比例合理分配;

2. 美国境内的所有关税和货物税必须 统一。

Custom duties

2020/9/2

tax law

广泛的 Exert a controlling impact upon the

nation’s economy 对全国经济产生支配性影响

2020/9/2

tax law

5

Federal Fiscal Powers

Among the most important of the powers granted to the federal government

2020/9/2

tax law

14

The Graves case effectively overruled the Pollock decision

The courts continually have held that a tax on income was an excise tax.

indirect taxes ultimately proved to be a stumbling block in the development of our present federal tax structure. ……,直接税与间接税之间的差异已 成为美国现行联邦税制发展的障碍。

2020/9/2

对经营和职业所得的征税不是直接税, 不必以人口为基础分配。

2020/9/2

tax law

22ቤተ መጻሕፍቲ ባይዱ

税务英语教学参考书Unit 9,11,12

Unit 9 Taxpayers’ Rights and Obligations(纳税人的权利和义务)Section I:Dialogue情境对话:税务代理接待客户咨询(商人为自己的公司寻找合适的税务代理)教学目的与要求:通过本情境的学习使学生了解作为税务代理从业人员如何向客户介绍相关涉税业务及为客户提供税务代理服务。

教学难点与重点:1.各种税务代理服务的英语表达方式tax advice 税务咨询tax planning 税务规划tax agents 税务代理tax review 税务审查tax and financial training 税务和金融培训tax agents’ board 税务代理委员会tax categories 税的种类set up accounts and keep books 设立账户和设置会计账簿establish financial management systems 建立财务管理制度tax registration 税务登记operation alteration and cancellation 税务变更和注销tax deduction and exemption 减免税tax calculations and clearing 税务计算和结算asset loss 资产损失2. 用英语向客户推介税务代理相关业务所需的交际能力Useful Expressions:What can I do for you?Do you want a tax agent?Would you like to tell me something more in details?Can I be sure that……Sure. We‘ll act as permanent agent for clients and provide with other services as requested.What do I need to prepare the information for it?教学方法与手段:角色扮演背诵对话课堂演示教学时数:50分钟教学评估:学生自评学生互评教师点评对话译文:(情境:怀特先生是一名美国商人,现在,他在为他的公司寻找合适的税务代理。

纳税人的权利和义务

纳税人的权利纳税人的权利是指纳税人在依法履行纳税义务时,由法律确认、保障与尊重的权利和利益,以及当纳税人的合法权益受到侵犯时,纳税人所应获得的救助与补偿权利。

我国现行税法规定,纳税人以及扣缴义务人(以下统称纳税人)的权利主要包括以下方面:一、税收知情权纳税人有权向税务机关了解国家税收法律、行政法规的规定以及与纳税程序有关的情况,享有被告知与自身纳税义务有关信息的权利。

纳税人的知情权主要包括:(1)税收政策知情权。

(2)涉税程序知情权。

(3)应纳税额核定知情权。

(4)救济方法知情权。

二、保密权纳税人有权要求税务机关对其商业秘密及个人隐私保密。

包括纳税人的储蓄存款、账号、个人财产状况、婚姻状况等个人隐私,符合现行法律规定的做法、经营管理方式、生产经营、金融、财务状况等商业秘密。

只要纳税人不愿公开的信息,同时又不是违法行为,税务机关就应该尊重纳税人的这项权利,履行为被检查人保守秘密的义务。

纳税人的税收违法行为不属于保密范围。

三、依法申请税收优惠权纳税人依法享有申请减税、免税、退税的权利,即纳税人有权根据税收法律规定及自己的实际情况向税务机关申请享受税收优惠的权利。

但必须依据法律、行政法规的规定,按照法定程序进行申请、审批。

行使享受税收优惠权的申请人,必须是纳税义务人,不能是代扣代缴义务人。

纳税人同时符合同一税种两个或两个以上优惠条件的,只能选择其中一个享受,不能重复享受。

四、陈述与申辩权纳税人对税务机关所作出的行政处罚决定,享有陈述权、申辩权。

陈述权是指纳税人对税务机关做出的决定所享有的陈述自己意见的权利,申辩权是纳税人认为税务机关对自己所为在定性或适用法律上不够准确,根据事实和法律进行反驳、辩解的权利。

如果纳税人有充分的证据证明自己的行为合法,税务机关就无权对其实行行政处罚,即使纳税人的陈述或申辩不充分合理,税务机关也应当解释其行政处罚行为的原因,并将纳税人的陈述内容和申辩理由记录在案,以便在行政复议或司法审查过程中能有所依据。

税收英语对话:纳税申报

税收英语对话:纳税申报税收英语对话:纳税申报纳税申报比我想象的重要的多!The tax return is far more than I thought.税务局:您好。

您看上去有些不快,有什么事需要帮助吗?Tax official: hello. You look unhappy. What can I do for you.纳税人:我公司因未申报而被罚款。

可我们并没有取得营业收入呀?Taxpayer: my company have been fined because we failed to file the tax return .but we have not got any business income at all .税务局:中国法律规定,即使没有营业收入、没有税可缴也要申报。

Tax official:well ,according to the Chinese law ,the taxpayer must file its Tax return within the prescribed time , no matter whether it has business turnover .纳税人:如果缴税和申报同时过期了怎么办?Taxpayer: if both the tax payable and tax return are overdue,what will happen ?税务局:要重新指定申报期限,并在罚款的同时,对逾期纳税按日加罚滞纳金。

Tax official: the tax authority will set new dead line for the return and impose a fine not exceeding 2000 Yuan on the taxpayer that fail to file the return .on the other hand ,levy a surcharge equal to 0.2% of the overdue tax for each day that the tax remain in arrears .纳税人:如果申报不实怎么办?Taxpayer: what about the punishment In the case of false tax return?税务局:如果是故意的,就要被定为偷税。

纳税人的权利与义务培训课件

按时、如实申报的义务

二、纳税人的义务

按时缴纳税款的义务 代扣、代收税款的义务 接受依法检查的义务 及时提供信息的义务

报告其他涉税信息的义务

(一)、依法进行税务登记的义务

法律依据: 《税收征管法》第十五条:企业,企业在外地设立的分 支机构和从事生产、经营的场所,个体工商户和从事生产、 经营的事业单位(以下统称从事生产、经营的纳税人)自领 取营业执照之日起三十日内,持有关证件,向税务机关申报 办理税务登记。

ቤተ መጻሕፍቲ ባይዱ

税务机关作出的罚款数额达到一定金额(公民罚款 2000 元以上、对法人或其他组织罚款 10000 元以上)的税务 行政处罚时,纳税人享有要求听证的权利。

(十三)、依法要求听证的权利

纳税人应在税务机关送达《税务行政处罚事项告知书》后 三日内,书面提出听证申请,如果逾期不提出的,视为放弃 听证权利。

(十一)、对未出示税务检查证和税务检查通知书的拒绝检查权

税务检查通知书是实施检查的税务机关开具给被查纳 税人的告知书,载明了检查时间、检查人员的姓名、证号、 检查所属期间、实施检查的税务机关名称及文书号等,并盖 有签发税务机关的公章。

税务机关将以前会计年度的账簿、记账凭证、报表和 其他有关资料调回税务机关进行检查时,需经县级以上税务 局(分局)局长批准;调回当年的账簿、记账凭证、报表和 其他有关资料进行检查,需经设区的市、自治州以上税务局 局长批准。

(十二)、税收法律救济权

纳税人对税务机关作出的决定,依法享有申请行政复 议、提起行政诉讼、请求国家赔偿等权利。

税收法律救济权分为申请行政复议权、提起行政诉讼 权和请求国家赔偿权。

(十二)、税收法律救济权

如果对征税行为不服,必须依照税务机关根据法律、法规 确定的税额、期限,先行缴纳或者解缴税款和滞纳金,或者 提供相应的担保,才可以在缴清税款和滞纳金以后或者所提 供的担保得到作出具体行政行为的税务机关确认之日起 60日 内提出行政复议申请。对行政复议决定不服的,可以向人民 法院提起行政诉讼。

税收英语词汇

税务专用英语词汇State Administration for Taxation 国家税务总局Local Taxation bureau 地方税务局Business Tax 营业税Individual Income Tax 个人所得税Income Tax for Enterprises企业所得税Income Tax for Enterprises with Foreign Investment and Foreign Enterprises外商投资企业和外国企业所得税tax returns filing 纳税申报taxes payable 应交税金the assessable period for tax payment 纳税期限the timing of tax liability arising 纳税义务发生时间consolidate reporting 合并申报the local competent tax authority 当地主管税务机关the outbound business activity 外出经营活动Tax Inspection Report 纳税检查报告tax avoidance 逃税tax evasion 避税tax base 税基refund after collection 先征后退withhold and remit tax 代扣代缴collect and remit tax 代收代缴income from authors remuneration 稿酬所得income from remuneration for personal service 劳务报酬所得income from lease of property 财产租赁所得income from transfer of property 财产转让所得contingent income 偶然所得resident 居民non-resident 非居民tax year 纳税年度temporary trips out of 临时离境flat rate 比例税率withholding income tax 预提税withholding at source 源泉扣缴State Treasury 国库tax preference 税收优惠the first profit-making year 第一个获利年度refund of the income tax paid on the reinvested amount 再投资退税export-oriented enterprise 出口型企业technologically advanced enterprise 先进技术企业Special Economic Zone 经济特区tax exemption 免税Tax Exemption Certificate 免税证明书tax heldover 延缓缴纳的税款tax holiday 免税期tax in default 拖欠税款tax investigation税务调查tax liability 纳税责任;税务负担tax payable应缴税款body corporate 法团;法人团体保护关税(Protective Tariff)保税制度(Bonded System)布鲁塞尔估价定义(Brussels Definition of Value BDV)差别关税(Differential Duties)差价关税(Variable Import Levies)产品对产品减税方式(Product by Product Reduction of Tariff)超保护贸易政策(Policy of Super-protection)成本(Cost)出厂价格(Cost Price)初级产品(Primary Commodity)初级产品的价格(The Price of Primang Products)出口补贴(Export Subsidies)出口退税(Export Rebates)从量税(Specific Duty)从价(Ad Valorem)从价关税(Ad Valorem Duties)反补贴税(Counter Vailing Duties)反倾销(Anti-Dumping)反倾销税(Anti-dumping Duties)关税(Customs Duty)关税和贸易总协定(The General Agreement On Tariffs And Trade)关税配额(Tariff Quota)自主关税(Autonomous Tariff)最惠国税率(The Most-favoured-nation Rate of Duty)优惠税率(Preferential Rate)标题:能介绍一下营业税的知识吗TOPIC: Would you please give the general introduction of the business tax?对话内容:纳税人:我公司马上就要营业了,能介绍一下营业税的知识吗?Taxpayer: my company will begin business soon, but I have little knowledge about the business tax. Can you introduce it?税务局:尽我所能吧!一般地说,提供应税业务、转让无形资产和出卖不动产都要交纳营业税。

个人所得税实施条例英文版

中华人民共和国个人所得税法实施条例(英文版)类别: 部门: 未知地区: 全国颁布时间: 1994年1月28日阅读次数: 366REGULATIONS FOR THE IMPLEMENTATION OF THE INDIVIDUAL INCOME TAXLAW OF THE PEOPLE'S REPUBLIC OF CHINA(State Council: 28 January 1994)Whole Doc.Article 1These Regulations are formulated in accordance with the IndividualIncome Tax law of the People's Republic of China (the "Tax Law").Article 2For the Purposes of the first paragraph of Article 1 of the Tax Law,the term "individuals who have domicile in China" shall mean individualswho by reason of their permanent registered address, family or economicinterests, habitually reside in the People's Republic of China.Article 3For the purposes of the first paragraph of Article 1 of the Tax Law,the term "have resided for one year or move in China" shall mean to haveresided within the People's Republic of China for 365 days in a Tax Year.No deductions shall be made from that number of days for Temporary Tripsout of the People's Republic of China.For the purposes of preceding paragraph, the term "Temporary Tripsout of the People's Republic of China" shall mean absence from thePeople's Republic of China for not more than 30 days during a single trip,or not more than a cumulative total of 90 days over a number of trips,within the same Tax Year.Article 4For the purposes of the first and second paragraphs of Article 1 ofthe Tax Law, the term "income derived from sources within China" shallmean income the source of which is inside the People's Republic of China,and the term "from sources outside China" shall mean income the source ofwhich is outside the People's Republic of China.Article 5The following income, whether the place of payment is inside thePeople's Republic of China or not, shall be income derived from sourcesinside the People's Republic of China.(1) income from personal services provided inside the People'sRepublic of China because of the tenure of an office, employment, theperformance of a contract, etc.;(2) income from the lease of property to a lessee for use inside thePeople's Republic of China;(3) income from the assignment of property such as buildings, land use rights, etc. inside the People's Republic of China or the assignment inside the People's Republic of China of any other property;(4) Income from the licensing for use inside the People's Republic of China of any kind of licensing rights;(5) income from interest, dividends and extra dividends derived from companies, enterprises and other economic organizations or individuals inside the People's Republic of China.Article 6For income derived from sources outside the People's Republic of China of individuals not domiciled in the People's Republic of China, but resident for more than one year and less than five years, subject to the approval of the tax authorities-in-charge, individual income tax may be paid on only that part which was paid by companies, enterprises or other economic organizations or individuals which are inside the People's Republic of China. Individuals who reside for more than five years shall, commencing from the sixth year, pay individual income tax on the whole amount of income derived from sources outside the People's Republic of China.Article 7For individuals who are not domiciled in the People's Republic of China, but who reside inside the People's Republic of China consecutively or accumulatively for not more than 90 days in any one Tax Year, their income derived from sources inside the People's Republic of China which is paid by an employer outside the People's Republic of China, and which is not borne by the employer's establishment or business place within the People's Republic of China, shall be exempt from individual income tax.Article 8The scope of the categories of income mentioned in Article 2 of the Tax Law shall be as set forth below;(1) The term "income from wages and salaries" shall mean wages, salaries, bonuses, year-end extras, profit shares, subsidies, allowances and other income related to the tenure of an office or employment that is derived by individuals by virtue of the tenure of an office or employment.(2) The term "income from production or business operation derived by individual industrial and commercial households" shall mean the following:(a) income derived by individual industrial and commercial households from engagement in industry, handicrafts, construction, transportation, commerce, the food and beverage industry, the service industry, the repair industry and production and business in other industries;(b) income derived by individuals from engagement, with approval from the relevant government authorities and after having obtained licenses, inthe provision of educational. medical, advisory and other services activities for consideration;(c) other income derived by individuals from engagement in individual industrial and commercial production and business;(d) all taxable income related to production and business of the above individual industrial and commercial households and individuals.(3) The term "income from contracted or leased operation of enterprises or institutions" shall mean income derived by individuals from contracted or leased operations, or from assigning such contracts or leases, including income of a wage or salary nature derived by individuals on a monthly basis or from time to time.(4) The term "income from remuneration for personal services" shall mean income derived by individuals from engagement in design, decoration, installation, drafting, laboratory testing, other testing, medical treatment, legal accounting, advisory, lecturing, news, broadcasting, translation, proofreading, painting and calligraphic, carving, moving picture and television, sound recording, video recording, show, performance, advertising, exhibition and technical services, introduction services, brokerage services, agency services and other personal services.(5) The term "income from author's remuneration" shall mean income derived by individuals by virtue of the publication of their works in books, newspapers and periodicals.(6) The term "income from royalties" shall mean income derived by individuals from provision of the right to use patent rights, trademark rights, copyrights, non-patented technology and other licensing rights, Income from provision of the fight to use copyrights shall not include income from author's remuneration.(7) The term "income from interest, dividends and extra dividends" shall mean income from interest, dividends and extra dividends that is derived by individuals by virtue of their possession of creditor's rightsand share rights.(8) The term "income from lease of property" shall mean income derived by individuals from the lease of buildings, land use rights, machinery, equipment, means of transportation and other property.(9) The term "income from transfer of properly" shall mean income derived by individuals from the assignment of negotiable securities, share rights, structures, land use rights, machinery, equipment, means of transportation and other property.(10) The term "contingent income" shall mean income derived by individuals from winning awards, prizes and lotteries and other income of an occasional nature.Income derived by individuals for which the taxable category is difficult to determine shall be decided upon by the taxauthorities-in-charge.Article 9Measures for the levy and collection if individual income tax on income from the transfer of shares shall be separately formulated by the Ministry of Finance and implemented upon approval by the State Council. Article 10Taxable income derived by individuals shall include cash, physical objects and negotiable securities. If the income is in the form of physical objects, the amount of taxable income shall be determined according to the price specified on the voucher obtained. If there is no receipt for the physical objects or if the price specified on the voucheris obviously on the low side, the tax authorities-in-charge shall determine the amount of taxable income by reference to the local market price, If the income is in the form of negotiable securities, the amountof taxable income shall be determined by the tax authorities-in-charge according to the face value and the market price.Article 11For the purposes of item (4) of Article 3 of the Tax Law, the phrase"a specific payment of income from remuneration for personal service is excessively high" shall mean a payment received as remuneration for personal service with an amount of taxable income exceeding RMB 20000.That part of taxable income as mentioned in the preceding paragraph which exceeds RMB 20000 but does not exceed RMB 50000 shall, after the amount of tax payable is calculated in accordance with the Tax Law. be subject to an additional levy at the rate of 50 percent of the amount oftax payable. That part which exceeds RMB 50000 shall be subject to an additional levy at the rate of 100 percent of tax payable.Article 12For the purposes of item (2) of Article 4 of the Tax Law, the term "interest on national debt obligations" shall mean interest income derivedby individuals by virtue of holding bonds issued by the Ministry of Finance of the People's Republic of China, and the term "interest on financial debentures issued by the state" shall mean interest income derived by individuals by viture of holding financial bonds issued with State Council approval.Article 13For the purposes of item (3) of Article 4 of the Tax Law, the term "subsidies and allowances paid in accordance with uniform regulations of the state" shall mean special government subsidies issued in accordance with State Council regulations and allowances and subsidies that are exempt from individual income tax by State Council regulations.Article 14For the purposes of item (4) of Article 4 of the Tax Law, the term"welfare benefits" shall mean cost-of-living subsidies paid to individuals according to relevant state regulations out of the welfare benefits orlabor union funds allocated by enterprises, institutions, government agencies and social organizations, and the term "relief payments" shall mean hardship subsidies paid to individuals by civil affairs authoritiesof the state.Article 15For the purposes of item (8) of Article 4 of the Tax Law, the "income derived by the diplomatic agents, consular officers and other personnel who are exempt from tax under the provisions of the relevant Laws of China" shall mean income that is tax-exempt under the Regulations of the People's Republic of China Concerning Diplomatic Privileges and Immunities and the Regulations of the People's Republic of China concerning Consular Privileges and Immunities.Article 16The ranges and periods of the reductions in individual income tax referred to in Article 5 of the Tax Law shall be stipulated by the People's Governments of the provinces, autonomous regions and municipalities directly under the central government.Article 17For the purposes of item (2) of the first paragraph of Article 6 ofthe Tax Law, the terms "costs" and "expenses" shall mean all direct expenditures, indirect expenses allocated as costs, as well as marketing expenses, administrative expenses and financial expenses incurred by taxpayers while engaging in production and business, and the term "losses" shall mean all non-operating expenditures incurred by taxpayers in the course of production and business.If a taxpayer engaging in production or business fails to provide complete and accurate tax information and is unable to correctly calculate the amount of taxable income, his amount of taxable income shall be determined by the tax authorities-in-charge.Article 18For the purposes of item (3) of the first paragraph of Article 6 ofthe Tax Law, the term "the gross income in a tax year" shall mean the share of the operating profit or the income of a wage or salary nature derived by the taxpayer according to the contract for the contracted or leased operation and the term "deduction of necessary expenses" shall mean a monthly deduction of RMB 800.Article 19For the purposes of item (5) of the first paragraph of Article 6 ofthe Tax Law, the term "the original value of the property" shall mean:(1) in the case of negotiable securities, the price for which theywere purchased and related expenses paid according to regulations at thetime of purchase;(2) in the case of buildings, the construction expenses or purchase price, and other related expenses;(3) in the case of land use rights, amount paid to acquire the landuse rights, land development expenses and other related expenses;(4) in the case of machinery, equipment, vehicles and vessels, the purchase, freight, installation expenses and other related expenses;(5) in the case of other property, the original value shall be determined by reference of the above methods.If a taxpayer fails to provide complete and accurate vouchers concerning the original value of the property and is unable to correctly calculate the original value of the property, the original value of the property shall be determined by the tax authorities-in-charge.Article 20For the purposes of item (5) of the first paragraph of Article 6 ofthe Tax Law, the term "reasonable expenses" shall mean relevant expenses paid in accordance with regulations at the time of sale.Article 21For the purposes of items (4) and (6) of the first paragraph of Article 6 of the Tax Law, the term "each payment" shall mean:(1) in the case of income from remuneration for personal services, the amount, if the income is derived in a lump sum, of that lump sum; and, if the income is of a continuing nature and pertains to the same project, the income derived during one month;(2) in the case of income from author's remuneration, the income derived on each instance of publication;(3) in the case of income from royalties, the income derived from each instance of licensing a licensing right;(4) in the ease of income from the lease of property, the income derived during one month;(5) in the case of income from interest, dividends and extra dividends, the income derived each time interest, dividends or extra dividends are paid;(6) in the case of contingent income, each payment of such income obtained.Article 22Tax on income from the assignment of property shall be calculated and paid on the proceeds of a single assignment of property less the original value of the property and reasonable expenses.Article 23If the same item of income is derived by two or more individuals, tax thereon shall be calculated and paid separately on the income derived by each individual after the deduction of expenses respectively in accordancewith the Tax Law.Article 24For the purposes of the second paragraph of Article 6 of the Tax Law,the term "individual income donated to educational and other public welfare undertakings" refers to the donation by individuals of their income to educational and other public welfare undertakings, and to areas suffering from serious natural disasters or poverty, through social organizations or government agencies in the People's Republic of China.That part of the amount of donations which does not exceed 30 percentof the amount of taxable income declared by the taxpayer may be deducted from his amount of taxable income.Article 25For the purposes of the third paragraph of Article 6 of the Tax Law,the term "income from wages and salaries from sources outside China" shall mean income from wages and salaries derived from the tenure of an officeor employment outside the People's Republic of China.Article 26For the purposes of the third paragraph of Article 6 of the Tax Law,the term: "additional deductions for expenses" shall mean a monthly deduction for expenses in the amount specified in Article 28 hereof in addition to the deduction for expenses of RMB 800.Article 27For the purposes of the third paragraph of Article 6 of the Tax Law,the term "the scope of applicability of such additional deductions for expenses" shall mean:(1) foreign nationals working in foreign investment enterprises and foreign enterprises in the People's Republic of China;(2) foreign experts hired to work in enterprises, institutions,social organizations and government agencies in the People's Republic of China;(3) individuals who are domiciled in the People's Republic of Chinaand derive income from wages and salaries by virtue of their tenure of an office or employment outside the People's Republic of China; and(4) other personal as determined by the Ministry of Finance.Article 28The standard for the additional deductions for expenses mentioned inthe third paragraph of Article 6 of the Tax Law shall be RMB 3200.Article 29Overseas Chinese and Hong Kong, Macao and Taiwan compatriots shall be treated by reference to Article 26, 27 and 28 hereof.Article 30Individuals who are domiciled in the People's Republic of China, orwho are not domiciled but have resided in the People's Republic of Chinafor at least one year shall calculate the amounts of tax payable for income derived from sources within and outside the People's Republic of China separately.Article 31For the purposes of Article 7 of the Tax Law, the term "income tax paid to foreign authorities" shall mean the amount of income tax payable, and actually paid, on income derived by a taxpayer from sources outside the People's Republic of China, according to the laws of the country or region from which that income was derived.Article 32For the purposes of Article 7 of the Tax Law, the term "the amount of tax otherwise payable under this Law" shall mean the amount of tax payable on income derived by a taxpayer from sources outside the People's Republic of China, computed separately for each different country or region and for each different income category, in accordance with the standards for the deduction of expenses and the applicable tax rates stipulated in the Tax Law. The sum of the amounts of tax payable in the different income categories within the same country or region shall be the limit for deductions for that country or region.If the actual amount of individual income tax paid by a taxpayer in a country or region outside the People's Republic of China is less than the limit for deductions for that country or region computed in accordance with the provisions of the preceding paragraph, the balance shall be paidin the People's Republic of China. If the amount exceeds the limit for deductions for that country or areas, the excess portion may not be deducted from the amount of tax payable for that Tax Year; however, such excess portion may be deducted from any unused portion of the limit for deductions for that country or region during subsequent Tax Years, for a maximum period of five years.Article 33When taxpayers apply for approval to deduct the amounts of individual income tax paid outside the People's Republic of China in accordance with Article 7 of the Tax Law, they shall provide the original tax payment receipts issued by the tax authorities outside the People's Republic of China.Article 34When withholding agents make taxable payments to individuals, they shall withhold tax in accordance with the Tax Law, pay the tax over to the treasury in a timely manner, and keep special records for future inspection.For the purposes of the preceding paragraph, the term "payments" shall include payments in cash, payments by remittance, payments byaccount transfer, and payments in the form of negotiable securities, physical objects and other forms.Article 35Taxpayers who personally file tax returns shall file the returns withand pay tax to the tax authorities-in-charge of the place where their income is derived. Taxpayers who derive income from sources outside the People's Republic of China, or who derive income in two or more places inside the People's Republic of China, may select one place in which to file tax returns and pay tax. Taxpayers who wish to change the location in which they file tax returns and pay tax shall obtain the approval of the original tax authorities-in-charge.Article 36When taxpayers who personally file tax returns file their returns,tax payments that have been withheld inside the People's Republic of China may be deducted from the amount of tax payable, in accordance with relevant regulations.Article 37Taxpayers who concurrently derive income under two or more of the categories listed in Article 2 of the Tax Law shall compute and pay tax separately for each category. Taxpayers who derive income under items (1), (2) or (3) of Article 2 of the Tax Law in two or more places insidethe People's Republic of China shall combine the income under the same category for the computation and payment of tax.Article 38For the purposes of the second paragraph of Article 9 of the Tax Law, the term "specified industries" shall mean the excavation industry, ocean-shipping industry, deepsea fishing industry and other industries as determined by the Ministry of Finance.Article 39For the purposes of the second paragraph of Article 9 of the Tax Law, the term "tax computed on an annual basis and paid in advance in monthly installments" shall mean the monthly prepayment of the tax payable on the income from wages and salaries of staff and workers in the specified industries listed in Article 38 hereof, and the computation of the actualtax payment due, within 30 days from the last day of the year, by averaging over 12 months the total wages and salary income for the whole year, at which time excess payments shall be refunded and deficiencies shall be made good.Article 40For the purposes of the fourth paragraph of Article 9 of the Tax Law, the phrase "the tax shall be paid into the state treasury within 30 days after the end of each tax year" shall mean that taxpayers who derive their income from contracted or leased operation of enterprises in a lump sumpayment at the end of the year, shall pay the tax payable thereon into theState treasury within 30 days of the date on which the income is derived. Article 41In accordance with Article 10 of the Tax Law, foreign currency income shall be converted into Renminbi for the computation of the amount of taxable income at the exchange rate published by the People's Bank of China on the last day of the month preceding that in which the tax payment receipt is issued. At the time of the annual settlement after the end ofthe year in accordance with the Tax Law, the amounts of foreign currency income on which tax has been prepaid on a monthly basis or each time the income was derived shall not be converted again. As for the portion of income the tax on which is to be made up, the amount of taxable income shall be computed by converting such portion of income into Renminbi according to the exchange rate published by the People's Bank of China onthe last day of the preceding Tax Year.Article 42When tax authorities pay commissions to withholding agents in accordance with Article 11 of the Tax Law, they shall issue to the withholding agents monthly refund certificate, on the strength of whichthe withholding agent shall carry out treasury refund procedures with designated banks.Article 43The models for individual income tax returns, individual income tax withholding returns and individual income tax payment receipts shall be formulated by the State Administration of Taxation in a unified manner. Article 44For the purposes of the Tax Law and these Regulations, the term "Tax Year" shall mean the period commencing on January 1 and ending on December 31 on the Gregorian calendar.Article 45Commencing with the 1994 Tax Year, individual income tax shall be computed, levied and collected in accordance with the Tax Law and these Regulations.Article 46These Regulations shall be interpreted by the Ministry of Finance andthe State Administration of Taxation.Article 47These Regulations shall be implemented as from the date of promulgation. The Provisional Regulations of the State Council of the People's Republic of China Concerning the Reduction of Individual Income Tax on the Income From Wages and Salaries Derived by Foreign Personnel Working in China promulgated by the State Council on August 8, 1987 shall be repealed at the same time.。

人大社《税法》课程教学大纲

《税法》(第3版,王红云主编)课程教学大纲一、课程基本信息课程代码:课程名称:税法课程英文名称:TaxationLaws学时/学分:54学时/3学分开课系(部):会计系、财务管理系和工商管理系等先修课程:经济法面向对象:会计、财务管理、工商管理等专业二、课程性质与目标课程性质:本课程是会计、财务管理、工商管理等专业的一门专业限定选修课,是会计、财务管理、工商管理等专业的主干课程之一,是学生参加会计从业资格证考试、助理会计师、会计师、注册会计师、注册税务师考试必考的一门课。

课程目标:通过本课程的学习,应使学生掌握税法的基本知识、流转税法与所得税法,对我国的现行税收体系有一个比较概括的了解,特别是掌握税收的征收办法及计算方法,增强学生的税法素质,为学生今后从事税务工作、会计实务工作以及企业管理工作打下坚实的基础。

三、理论教学基本内容及学时分配第一章税法概述(2学时)【教学目的】本章是该课程的理论基础,掌握好本章内容是学好以后各章的关键。

本章主要介绍税法的基础知识和我国建国以来的税制发展,其主要内容包括税法的概念、税收法律关系,税法的制定与实施,税法体系和税收管理体制等内容。

通过本章的教学,要求学生了解我国税制的发展演变历史和税收法律关系的基本内容;熟悉我国税制改革的基本内容和我国现行的税收管理体制;掌握税法、税收法律关系等概念内涵,掌握税法要素、税制体系和税收管理体制的内容;积累一定的税制和税法知识,为学习以后各章打好基础。

【教学重点】税法的概念;税法的构成要素;税收法律关系的特征;现行税法体系;税收管理体制;我国税制改革的主要内容。

【教学难点】全额累进税率和超额累进税率的比较;税法的制定。

第一节税法的概念第二节我国税法原则第三节我国税收立法机关和税法体系第四节我国税收制度的改革和发展第五节我国税收管理体制【教学基本内容】1.税收的概念和税收的职能2.税收的产生与发展3.我国现行税制体系4.税法分类5.税制构成要素第二章税收征收管理(2学时)【教学目的】本章主要介绍纳税人或扣缴义务人的权利和义务,税务登记、纳税申报和税款征管。

公司的主要权利与义务 合同英语

公司的主要权利与义务合同英语全文共3篇示例,供读者参考篇1Company's Major Rights and Obligations in ContractsWhen two parties enter into a contract, they are bound by certain rights and obligations laid out in the agreement. Companies, as legal entities, have their own set of rights and obligations that stem from the contracts they enter into with other parties. These rights and obligations are essential for maintaining smooth business operations and ensuring the parties involved fulfill their duties as expected.Rights of the Company:1. Right to Terminate: Companies have the right to terminatea contract if the other party fails to meet its obligations or breaches the terms of the agreement. This right is essential for protecting the company's interests and ensuring that it is not bound by an agreement that is not being honored by the other party.2. Right to Performance: Companies have the right to expect the other party to perform its obligations as outlined in thecontract. This includes delivering goods or services on time, meeting quality standards, and adhering to the agreed-upon terms.3. Right to Payment: Companies have the right to receive payment for the goods or services they provide as per the terms of the contract. This right ensures that the company is compensated for its work and can continue to operate efficiently.4. Right to Legal Action: Companies have the right to take legal action against the other party if they fail to fulfill their obligations under the contract. This could involve seeking damages, enforcing specific performance, or pursuing other legal remedies available under the law.Obligations of the Company:1. Obligation to Perform: Companies have an obligation to perform their obligations as outlined in the contract. This includes delivering goods or services as promised, meeting quality standards, and fulfilling any other requirements specified in the agreement.2. Obligation to Pay: Companies have an obligation to pay the other party for the goods or services provided as per the terms of the contract. This ensures that the company is fulfillingits financial responsibilities and maintaining a good business relationship with the other party.3. Obligation to Comply with Laws: Companies have an obligation to comply with all relevant laws and regulations when entering into contracts. This includes adhering to contract law, consumer protection laws, labor laws, and any other legal requirements that may apply.4. Obligation to Act in Good Faith: Companies have an obligation to act in good faith when entering into contracts. This means conducting business honestly, fairly, and reasonably, and not engaging in any deceptive or fraudulent practices that could harm the other party.In conclusion, understanding the rights and obligations of companies in contracts is essential for ensuring that business agreements are upheld and that all parties are treated fairly. By knowing these rights and obligations, companies can protect their interests, maintain successful business relationships, and navigate the complex landscape of contract law with confidence.篇2Rights and Obligations of Companies in ContractsIn any business transaction, contracts play a crucial role in defining the rights and obligations of the parties involved. Companies, as legal entities, have their own set of rights and obligations when entering into contracts. Understanding these rights and obligations is essential for businesses to protect their interests and ensure compliance with legal requirements. In this article, we will explore the main rights and obligations of companies in contracts.Rights of Companies in Contracts:1. Right to Contract: Companies have the legal right to enter into contracts with other parties for various purposes, such as buying or selling goods and services, entering into partnerships, or hiring employees. This right allows companies to conduct their business activities in a legally binding and enforceable manner.2. Right to enforce contract terms: Companies have the right to enforce the terms and conditions of the contract against the other party. This includes the right to seek remedies for any breach of contract, such as damages, specific performance, or termination of the contract.3. Right to confidentiality: Companies have the right to confidentiality in contracts, especially in sensitive businesstransactions. This includes the protection of trade secrets, proprietary information, and other confidential data shared between the parties. Companies can include confidentiality clauses in contracts to safeguard their interests.4. Right to indemnification: Companies have the right to seek indemnification from the other party for any losses or damages incurred due to a breach of contract or negligence. Indemnification clauses can be included in contracts to allocate risks and liabilities between the parties.5. Right to terminate the contract: Companies have the right to terminate the contract in certain circumstances, such as a material breach by the other party, insolvency, or force majeure events. Termination clauses can be included in contracts to define the conditions and procedures for terminating the contract.6. Right to interpretation: Companies have the right to interpret the terms and provisions of the contract in their favor, as long as the interpretation is reasonable and in accordance with the contract language. In case of disputes or ambiguity, companies can seek legal guidance to clarify the intent of the parties.Obligations of Companies in Contracts:1. Obligation to perform: Companies have the obligation to fulfill their contractual obligations and perform the agreed-upon services or deliver the goods in a timely and satisfactory manner. Failure to perform can lead to breach of contract and legal consequences.2. Obligation to act in good faith: Companies have the obligation to act in good faith in all their dealings with the other party. This includes honesty, fairness, and integrity in the negotiation, performance, and enforcement of the contract. Acting in bad faith can result in a breach of contract and legal liability.3. Obligation to comply with laws: Companies have the obligation to comply with all applicable laws, regulations, and industry standards in their contractual activities. This includes labor laws, consumer protection laws, antitrust laws, and other legal requirements. Non-compliance can lead to legal sanctions and reputational damage.4. Obligation to maintain confidentiality: Companies have the obligation to maintain the confidentiality of the other party's sensitive information and not disclose it to third parties without proper authorization. Confidentiality clauses in contracts canspecify the duties of confidentiality and the consequences of breach.5. Obligation to pay: Companies have the obligation to pay the agreed-upon price or compensation for the goods or services rendered by the other party. Failure to pay can constitute a breach of contract and entitle the other party to seek remedies for non-payment.6. Obligation to mitigate damages: Companies have the obligation to mitigate damages in case of a breach of contract by the other party. This includes taking reasonable steps to minimize the losses and expenses resulting from the breach. Failure to mitigate damages can limit the remedies available to the injured party.In conclusion, companies have both rights and obligations in contracts that define their legal responsibilities and entitlements in business transactions. Understanding these rights and obligations is essential for companies to protect their interests, maintain compliance with legal requirements, and build successful business relationships. By upholding their rights and fulfilling their obligations, companies can ensure the enforceability and effectiveness of the contracts they enter into.篇3Company's Main Rights and Obligations in ContractsIn business, contracts play a crucial role in defining the rights and obligations of parties involved. It is important for a company to understand its main rights and obligations when entering into contracts to ensure a smooth and successful business relationship. This article will discuss the main rights and obligations of a company in contracts, as well as some key considerations to keep in mind.1. Rights of the Company:a. Right to Enforce the Contract: One of the fundamental rights of a company in a contract is the right to enforce the terms and conditions agreed upon by both parties. If the other party fails to fulfill its obligations, the company has the right to take legal action to seek redress.b. Right to Terminate: In the event that the other party breaches the contract or fails to meet its obligations, the company has the right to terminate the contract. However, this right should be exercised in accordance with the terms and conditions specified in the contract to avoid any legal repercussions.c. Right to Receive Payment: A company has the right to receive payment for goods or services provided as per the terms agreed upon in the contract. If the other party fails to make payment on time, the company can take legal action to recover the amount owed.d. Right to Confidentiality: Companies often enter into contracts that involve the exchange of sensitive information. In such cases, the company has the right to confidentiality to protect its trade secrets and intellectual property.2. Obligations of the Company:a. Obligation to Perform: One of the main obligations of a company in a contract is the duty to perform the agreed-upon obligations in a timely and satisfactory manner. Failure to do so can result in breach of contract and legal consequences.b. Obligation to Comply with Laws: Companies are obligated to comply with all applicable laws and regulations when entering into contracts. This includes ensuring that the terms of the contract do not violate any legal requirements.c. Obligation to Provide Information: Companies are obliged to provide accurate and complete information to the other party to enable them to fulfill their obligations under the contract.Failure to provide necessary information can result in a breach of contract.d. Obligation to Maintain Records: Companies are required to maintain proper records of all contracts entered into, including correspondence, agreements, and payment details. This is essential for compliance purposes and to resolve any disputes that may arise.Key Considerations:a. Clear and Specific Terms: It is crucial for companies to ensure that the terms and conditions of the contract are clear, specific, and unambiguous. This can help avoid misunderstandings and disputes in the future.b. Legal Review: It is advisable for companies to have contracts reviewed by legal professionals to ensure that the terms are legally sound and protect the company's interests.c. Communication: Effective communication with the other party is essential to ensure that both parties understand their rights and obligations under the contract. Regular updates and discussions can help prevent misunderstandings and conflicts.In conclusion, understanding the main rights and obligations of a company in contracts is essential for successful businessdealings. By upholding these rights and fulfilling their obligations, companies can maintain good relationships with their partners and ensure the smooth execution of contracts. It is important for companies to seek legal advice when necessary to protect their interests and comply with all legal requirements.。

中国银行 机构税收居民身份声明 英文

中国银行机构税收居民身份声明英文China Bank Institutional Tax Resident Identity DeclarationI. BackgroundIn accordance with the tax laws and regulations of the People's Republic of China, all financial institutions operating in China are required to identify and report the tax residence status of their account holders. This is to ensure that the appropriate tax treatment is applied to income earned by individuals and entities in China.II. PurposeThe purpose of this Institutional Tax Resident Identity Declaration is to collect relevant information from China Bank's clients in order to determine their tax resident status in China. This information will be used to comply with tax reporting requirements and to ensure that appropriate tax withholding is applied to income earned by China Bank's clients.III. Definitions1. Tax Resident: A tax resident of China is an individual or entity that is subject to tax in China on their worldwide income.2. Non-Tax Resident: A non-tax resident of China is an individual or entity that is subject to tax in China only on income earned within China.IV. DeclarationI, [Name of Account Holder], hereby declare that the information provided in this Institutional Tax Resident Identity Declaration is true and accurate. I understand that China Bank may use this information to determine my tax residence status in China and to comply with tax reporting requirements.V. Information RequiredPlease provide the following information as accurately as possible:1. Name of Account Holder:2. Account Number:3. Tax Residence Status (Tax Resident/Non-Tax Resident):4. Country(ies) of Tax Residence:5. Tax Identification Number (TIN):6. Address:7. Contact Number:8. Email Address:VI. SubmissionPlease submit this Institutional Tax Resident Identity Declaration to China Bank's tax department by [Due Date]. Failure to submit this form by the due date may result in withholding of tax on income earned by the account holder.VII. ConfidentialityChina Bank will treat all information provided in this declaration as confidential and will only use it for the purpose of complying with tax reporting requirements. The bank will not disclose this information to any third party without the account holder's consent.VIII. Contact InformationIf you have any questions or require assistance in completing this form, please contact China Bank's tax department at [Contact Number] or [Email Address].By signing below, I acknowledge that I have read and understood the contents of this Institutional Tax Resident Identity Declaration.[Signature of Account Holder][Date]Please note that failure to provide accurate and complete information may result in tax penalties or other consequences as per the tax laws of China. Thank you for your cooperation.。

增值税暂行条例中英文对照

中华人民共和国增值税暂行条例The Provisional Regulations of the People‘s Republic of China on Value-Added Tax第一条在中华人民共和国境内销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人,为增值税的纳税义务人(以下简称纳税人),应当依照本条例缴纳增值税。

Article 1 All units and individuals engaged in the sales of goods, provision of processing,repairs and replac ement services, and the importation of goods within the territory of the People“s Republic of China are taxpayers of Value-Added Tax (heteinafter referred to as "taxpayers“),and shall pay VAT in acco rdance with these Regulations.第二条增值税税率:Article 2 VAT rates:(一)纳税人销售或者进口货物,除本条第(二)项、第(三)项规定外,税率为17%。

(1)For taxpayers selling or importing goods,other than those stipulated in items (2)and (3)of this Article,the tax rate shall be 17%.(二)纳税人销售或者进口下列货物,税率为13%:(2)For taxpayers selling or importing the following goods,the tax rate shall be 13%:1.粮食、食用植物油;i。

纳税人的权利和义务(英文版)

(在厦门地税网站找到的,供参考)Rights and Obligations of TaxpayersThe Rights of TaxpayersAccording to 《 THE LAW OF THE PEOPLE’S REPUBLIC OF CHINA CONCERNING THE ADMINISTRATION OF TAX COLLECTION 》, the taxpayers have the following rights:1. The right to know tax laws and tax payment proceduresTaxpayers and withholding agents have the right to know tax laws, administrative regulations and tax payment procedures.2. The right to apply for tax reduction, exemption and refund according to tax lawsIn the case of a taxpayer having paid tax in excess of the due taxable amount, the tax authority shall immediately refund the excess amount to the taxpayer. Where a taxpayer discovers the situation within three years from the payment date, it may claim a tax refund and the bank deposit interest of the corresponding period from the tax authority. Upon examination and verification of the case, the tax authority shall immediately refund the excess amount of tax.A taxpayer may submit a written application for tax reduction or exemption to the tax authority in accordance with the law or the administrative regulations. Applications for tax reduction or exemption shall be examined and approved by the authority designated for examination and approval of tax reduction or exemption as prescribed in the law or the administrative regulations. The decisions on tax reduction or exemption made by the people’s governments at various local levels, the competent departments of the people’s governments at various levels, entities or individuals without authorization in violation of the law or the administrative regulations shall be null and void.3. The right to require the tax authority to maintain confidentiality for their informationTaxpayers and withholding agents have the right to require the taxauthority to maintain confidentiality for their information. And the tax authority must maintain confidentiality for taxpayers’ information according to laws.4. The right to make statement and defend oneselfTaxpayers and withholding agents have the right to make statement and defend themselves for the decisions made by the tax authority.5. The right to apply for administrative reconsideration and administrative legal proceedingsTaxpayers and withholding agents have the right to apply for reconsideration and propose administrative legal proceedings for the decisions made by the tax authority according to laws.6. The right of application for compensation from government according to lawsTaxpayers and withholding agents have the right to apply for compensation from government for the decisions made by the tax authority the according to laws.7. The right to accuse and prosecute the tax authority and tax officials of violating law and disciplineTaxpayers and withholding agents have the right to accuse and prosecute the tax authority and tax officials of violating law and discipline.8. The right to apply for tax deferralWhen taxpayers or withholding agents are unable to apply for due tax declaration, make tax payment or submit tax withholding form the prescribed time limit, they may, upon examination and approval of the tax authority, apply for tax deferral for a period of not more than 3 months.9. The right to apply for postponing the tax paymentWhen a taxpayer is unable to pay tax within the prescribed time limit due to special difficulties, it may, upon approval of a State Tax Administration at the provincial, municipal directly under the State Council or autonomous region level, apply to postpone the tax payment fora period of not more than 3 months.10. The right to choose declaration methodsTaxpayers or withholding agents may directly go to the tax authority to make tax payment or submit tax withholding forms. They may also file, submit tax declaration by mail, data telex or other means according to the regulations.11. The right to demand the tax officials to avoid involvementThe tax officials in charge of tax collection and illegal case investigation shall avoid involvement provided that they have personal interests with the taxpayers, the withholding agents or the related case.12. The right to refuse being investigated if no investigating card or notice is presentedWhen carrying out tax investigation dispatched by the tax authority, the tax officials must show their Tax Investigation Card and Notice for Tax Investigation, and be obliged to keep confidentiality for the taxpayers; Taxpayers or the withholding agents and other parties concerned have the right to refuse the investigation if no such card or notice is presented.13. The right to getting a commission fee for tax payments withheld or collectedThe tax authority shall pay a commission fee to withholding agents for withholding or collecting tax in accordance with the relevant provisions.14. When commodities, goods or other property are impounded or sealed up, the taxpayers have the right to demand receipt or list of the items.When impounding commodities, goods or other property, the tax authority must issue a receipt for the items impounded. When sealing up commodities, goods or other property, the tax authority must present a list of these items.15. The right to get tax payment receiptWhen the tax authority collects tax payment, tax payment receipts mustbe issued to the taxpayers. When withholding or collecting tax payment, withholding agents shall issue tax withheld or collected receipts upon the taxpayer’s request.16. The right to entrust tax agents to handle taxation mattersTaxpayers and withholding agents can entrust tax agents to handle matters related to taxation.The Obligations of TaxpayersAccording to THE LAW OF THE PEOPLE’S REPUBLIC OF CHINA CONCERNING THE ADMINISTRATION OF TAX COLLECTION,the taxpayers have the following obligations:1. The obligation of paying the tax, withholding and remitting or collecting and remitting tax according to the provisions of laws and regulations.Taxpayers and withholding agents must pay their tax, withhold and remit or collect and remit tax according to the provisions of laws and regulations.2. The obligation of providing the information concerning the tax paymentTaxpayers and withholding agents shall provide the tax authority with true information concerning their tax payment, tax withholding and remittance or tax collection and remittance with the relevant provisions.Taxpayers engaged in production or business operations shall report all accounts number to the tax authority.3. The obligation of completing tax registration formalities within 30 days after receiving the business license.Enterprises, branches in other jurisdictions and sites engaged in production or business operations established by enterprises, individual households engaged in industry and commerce as well as institutions engaged in production or business operations (hereinafter refer to taxpayers engaged in production or business operations) shall, within 30 days after receiving the business license, handle tax registration formalities with the tax authority by presenting relevant documents.4. The obligation of reporting alteration or cancellation of tax registration with the tax authority, within 30 days after completing the business registration or prior to the submission of applications for cancellation of business registration, where changes occur in the contents of tax registration.Where changes occur in the contents of tax registration of taxpayers engaged in production or business operations, the taxpayers concerned shall, within 30 days after completing the formalities for such changes in the business registration with the Administration for Industry and Commerce or prior to the submission of applications for cancellation of business registration to the Administration for Industry and Commerce, report to complete the formalities for the change or cancellation of tax registration with the tax authority by presenting the relevant documents.5. The obligation of presenting tax registration certificates when opening account, and reporting to the tax authority.Taxpayers shall present tax registration certificates when opening basic bank account and other account in banks and other financial institutions, and report all accounts number to the tax authority.6. The obligation of using the tax registration certificates in accordance with the provisions.Taxpayers shall use their tax registration certificates in accordance with the provisions of the tax authority under the State Council. Such certificates shall not be lent, tampered with, damaged, traded or forged.7. The obligation of submitting the financial and accounting system or methods, accounting software to the tax authority.The financial and accounting systems or methods, accounting software and its user’s direction and other relevant materials of taxpayers engaged in production and operations shall be submitted to the tax authority for keep records. Should the financial and accounting systems or methods of taxpayers or withholding agents be in conflict with the relevant tax rules formulated by the State Council or the competent public finance and taxation departments under the State Council, the amount of tax payment, tax withholding and remittance and tax collecting and remittance shall be calculated according to the relevant provisions of the State Council or the competent public finance and taxation authority under the StateCouncil.8. The obligation of issuing, using, requesting or well-managing invoice according to regulations.When purchasing or selling goods, providing or receiving business services and performing other business activities, each unit or individual has the obligation to issue, use or request invoice according to regulations.9. The obligation of establishing, keeping accounting books, accounting documents, tax payment certificates and other related materials according to regulations.Taxpayers engaged in production and operations and withholding agents shall, according to the preservation period as specified by the competent public finance and taxation authority under the State Council, keep accounting books, accounting documents, tax payment certificates and other related materials. Accounting book, documents, record, tax payment certificate and other relevant materials are not allowed to be forged, altered or destroyed.10. The obligation of declaring tax due timely and actually according to regulations.Taxpayer shall, according to the declaration period and the declaration content specified in the provisions of laws and administrative regulations or by the tax authority in line with the provisions in laws and administrative regulations, submit their tax declaration form, financial and accounting statements and other tax payment materials requested by the tax authority based upon actual needs. Withholding agents shall, according to the declaration period and the declaration content specified in the provisions of laws and administrative regulations or by the tax authority in line with the provisions in laws and administrative regulations, submit the tax withholding and remitting form, collecting and remitting form, and other tax payment materials requested by the tax authority based upon actual needs.11. The obligation of taking in tax inspections, providing true situation and offering related information.All taxpayers and withholding agents must take in tax inspections conducted by the tax authority, provide true situation, offer related information. Refusal or hiding information is not allowed.12. The obligation of paying or transferring the tax due and late fee or providing corresponding guarantee in the first place when any dispute arises.Should any dispute arise between taxpayers, withholding agents or tax payment guarantors and the tax authority with regard to tax payment, the tax due and arrearage shall be paid or transferred or the guarantee shall be offered according to the provisions in laws and administrative regulations in the first place; and then may apply for reconsideration according to laws. If they do not accept the reconsideration decision, they may institute litigation before a people’s court.13. The obligation of reporting to the tax authority when merging or separation in company structure occurs.Taxpayers shall report to the tax authority when merging or separation in company structure occurs and settle tax payment in accordance with the law.14. The obligation of continuing the tax obligation that have not been fulfilled at the time of merging.Taxpayers shall continue to fulfill the tax obligation that has not been fulfilled at the time of merging.15. The obligation of bearing the joint tax liability unsettled at the time of separation.Taxpayers after the separation shall bear the joint tax liability unsettled at the time of separation.16. The obligation of reporting to the tax authority for taxpayers with large tax arrears before disposing immovable property or large amount of capital.Taxpayers with big tax arrears shall report to the tax authority before disposing their immovable property or large amount of capital.。

国际税收常用英语词汇

国际税收常用英语词汇$ abuse of tax treaties 滥用税收协定$ active income 主动收入$ advance pricing agreement (APA) 预约定价协议$ area jurisdiction 地域管辖权$ arm's length principle 独立交易原则$ associated enterprise 关联企业$ base company rule 基地公司规定$ best method rule 最佳方法规定$ bilateral 双边$ blocked income 滞留收入$ bounded area 保税区$ branch 分公司/分支机构$ branch rule 分支机构规定$ burden of proof 举证责任$ cancellation of debt (COD) 取消债务$ carried back 向前结转$ carried forward 结转(向后期)$ charitable foundation 慈善基金$ charitable trust 公益/慈善信托$ "check-the-box" rule “打勾选择”规定$ citizen jurisdiction 公民管辖权$ comparable profit method (CPM) 可比利润法$ comparable uncontrolled price method (CUP) 可比非受控价格法$ comparative profit method (CPM)可比利润法$ conduit company 中介/导管公司$ consolidate 合并$ contribution analysis 贡献分析$ controlled foreign company (CFC) 受控外国子公司$ controlling company 控股公司$ cost plus method (CP) 成本加利润法$ current rule 现行规则$ current tax 本期税额$ deduction 扣除$ deemed dividend 认定的红利$ deferral 递延$ device 工具$ domicile 住所标准$ dual residence 双重居民$ earnings stripping 收益剥离$ excess credit position 超额抵扣情况$ excess interest expense 超额利息支出$ exemption 免除$ force of attraction 吸引力规定$ foreign direct investment (FDI) 国际直接投资$ foreign indirect investment 国际间接投资$ formula apportionment 公式分配法$ freeport 自由港$ group 跨国企业集团$ holding company 持股公司$ income所得$ interest expense利息支出$ Internal Revenue Code (IRC)(美国)联邦税法典$ Internal Revenue Service (IRS) (美国)联邦税务局$ internal taxes 国内税$ jurisdiction 管辖权$ legal tax savings 合法节税$ limited liability company (LLC) 有限责任公司$ mobile 流动性(指可在世界各地作公司业务)$ multilateral 多边$ off-shore center 离岸中心$ parent company 母公司$ partnership 合伙人制$ passive income 被动收入$ phantom income 虚幻收入$ physical presence 实际存在(居住)$ pooling of interest 股权联营法$ portfolio exemption 组合投资免税$ profit split 利润分割$ profit split method (PSM)利润分割法$ purchasing method 盘购法$ recognition 确认(会计)$ resale price method (RPM) 再销售价格法$ residence 居所标准$ residence of individuals 自然人居民$ residence of legal entities 法人居民身份的判定标准$ resident jurisdiction 居民管辖权$ residual analysis 余额分析$ royalty 使用费$ source 来源$ subsidiary/affiliate company 子公司/附属公司$ substance over form 实质重于形式$ super royalty rule 超级使用费规定$ tax audit 税务审计$ tax avoidance 避税$ tax credit 税收抵扣$ tax evasion 偷/逃税$ tax haven 避税港——$ tax holiday 减税期$ tax jurisdiction 税收管辖权$ tax planning 税收筹划$ tax return 纳税申报$ tax sparing 税收抵扣限制$ the abstinence approach 禁止法$ the bona fide approach 真实法$ the channel approach 渠道法$ the exclusion approach 排除法$ the look-through approach 受益所有人法$ the number of days of presence 停留时间标准$ the subject-to-tax approach 纳税义务法$ thin capitalization 资本弱化$ threshold 下限$ trade or business 业务或经营$ transactional net margin method (TNMM)交易净利润率法$ transactional profit methods 交易利润法$ transfer pricing 转让定价$ treaty (双边税务)协议$ treaty override 协议优先$ treaty shopping 协议寻找$ withholding tax 预提税。

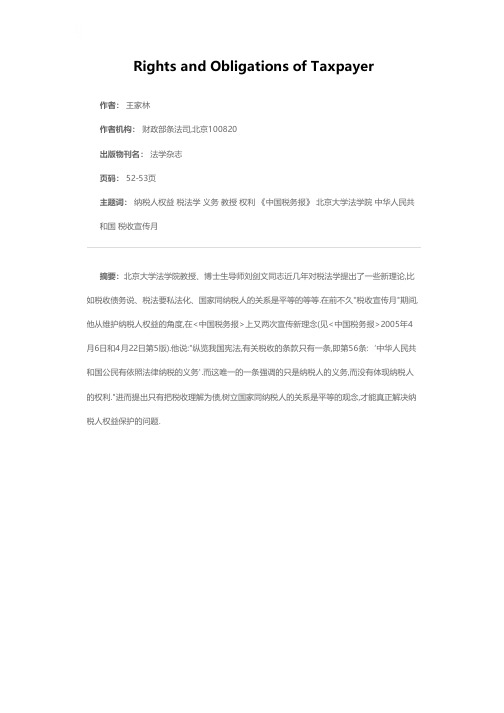

也从纳税人的权利和义务谈起——就一些税法新理论求教刘剑文教授

Rights and Obligations of Taxpayer 作者: 王家林

作者机构: 财政部条法司,北京100820

出版物刊名: 法学杂志

页码: 52-53页

主题词: 纳税人权益 税法学 义务 教授 权利 《中国税务报》 北京大学法学院 中华人民共和国 税收宣传月

摘要:北京大学法学院教授、博士生导师刘剑文同志近几年对税法学提出了一些新理论,比如税收债务说、税法要私法化、国家同纳税人的关系是平等的等等.在前不久"税收宣传月"期间,他从维护纳税人权益的角度,在<中国税务报>上又两次宣传新理念(见<中国税务报>2005年4月6日和4月22日第5版).他说:"纵览我国宪法,有关税收的条款只有一条,即第56条:‘中华人民共和国公民有依照法律纳税的义务'.而这唯一的一条强调的只是纳税人的义务,而没有体现纳税人的权利."进而提出只有把税收理解为债,树立国家同纳税人的关系是平等的观念,才能真正解决纳税人权益保护的问题.。

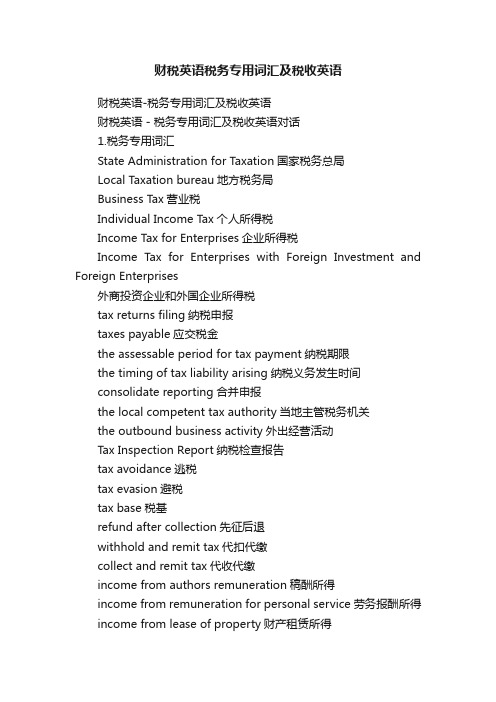

财税英语税务专用词汇及税收英语

财税英语税务专用词汇及税收英语财税英语-税务专用词汇及税收英语财税英语-税务专用词汇及税收英语对话1.税务专用词汇State Administration for Taxation国家税务总局Local Taxation bureau地方税务局Business Tax营业税Individual Income Tax个人所得税Income Tax for Enterprises企业所得税Income Tax for Enterprises with Foreign Investment and Foreign Enterprises外商投资企业和外国企业所得税tax returns filing纳税申报taxes payable应交税金the assessable period for tax payment纳税期限the timing of tax liability arising纳税义务发生时间consolidate reporting合并申报the local competent tax authority当地主管税务机关the outbound business activity外出经营活动Tax Inspection Report纳税检查报告tax avoidance逃税tax evasion避税tax base税基refund after collection先征后退withhold and remit tax代扣代缴collect and remit tax代收代缴income from authors remuneration稿酬所得income from remuneration for personal service劳务报酬所得income from lease of property财产租赁所得income from transfer of property财产转让所得contingent income偶然所得resident居民non-resident非居民tax year纳税年度temporary trips out of临时离境flat rate比例税率withholding income tax预提税withholding at source源泉扣缴State Treasury国库tax preference税收优惠the first profit-making year第一个获利年度refund of the income tax paid on the reinvested amount 再投资退税export-oriented enterprise出口型企业technologically advanced enterprise先进技术企业Special Economic Zone经济特区2.税收英语对话――营业税标题:能介绍一下营业税的知识吗TOPIC:Would you please give the general introduction of the business tax?对话内容:纳税人:我公司马上就要营业了,能介绍一下营业税的知识吗?Taxpayer:my company will begin business soon,but I have little knowledgeabout the business tax.Can you introduce it?税务局:尽我所能吧!一般地说,提供应税业务、转让无形资产和出卖不动产都要交纳营业税。

个人所得税法英文版

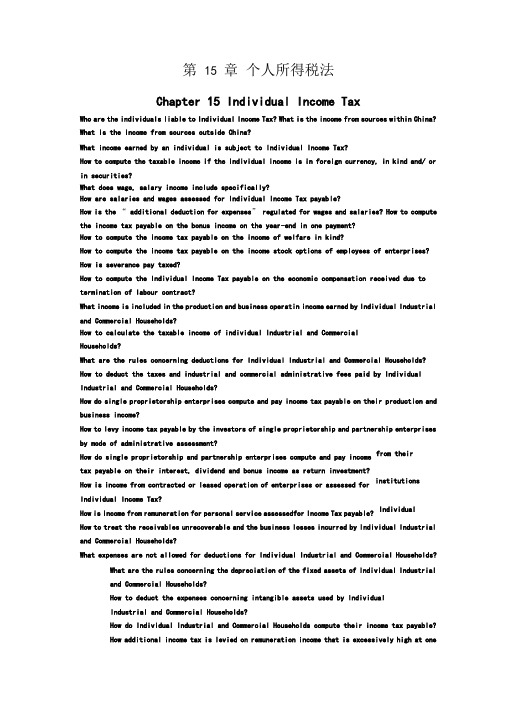

from their institutions Individual 第 15 章 个人所得税法Chapter 15 Individual Income TaxWho are the individuals liable to Individual Income Tax? What is the income from sources within China? What is the income from sources outside China?What income earned by an individual is subject to Individual Income Tax?How to compute the taxable income if the individual income is in foreign currency, in kind and/ or in securities?What does wage, salary income include specifically?How are salaries and wages assessed for Individual Income Tax payable?How is the “ additional deduction for expenses ” regulated for wages and salaries? How to compute the income tax payable on the bonus income on the year-end in one payment?How to compute the income tax payable on the income of welfare in kind?How to compute the income tax payable on the income stock options of employees of enterprises? How is severance pay taxed?How to compute the Individual Income Tax payable on the economic compensation received due to termination of labour contract?What income is included in the production and business operatin income earned by Individual Industrial and Commercial Households?How to calculate the taxable income of individual Industrial and CommercialHouseholds?What are the rules concerning deductions for Individual Industrial and Commercial Households? How to deduct the taxes and industrial and commercial administrative fees paid by Individual Industrial and Commercial Households?How do single proprietorship enterprises compute and pay income tax payable on their production and business income?How to levy income tax payable by the investors of single proprietorship and partnership enterprises by mode of administrative assessment?How do single proprietorship and partnership enterprises compute and pay income tax payable on their interest, dividend and bonus income as return investment? How is income from contracted or leased operation of enterprises or assessed for Individual Income Tax?How is income from remuneration for personal service assessedfor Income Tax payable? How to treat the receivables unrecoverable and the business losses incurred by Individual Industrial and Commercial Households?What expenses are not allowed for deductions for Individual Industrial and Commercial Households?What are the rules concerning the depreciation of the fixed assets of Individual Industrial and Commercial Households?How to deduct the expenses concerning intangible assets used by IndividualIndustrial and Commercial Households?How do Individual Industrial and Commercial Households compute their income tax payable? How additional income tax is levied on remuneration income that is excessively high at onepayment?How is author ' s remuneration income assessed for Individual Income Tax payable?How is income from royalties assessed for Individual Income Tax payable?How is income from lease of property assessed for Individual Income Tax payable?How is income from transfer of property assessed for Individual Income Tax payable?How to compute the income tax payable on income earned from auctions of paintings and calligraphy or antiques?What do the interest, dividend, bonus, contingent income and/ or other income include specifically?How are interests, dividends, bonuses, contingent income and/ or other income assessed for Individual Income Tax payable?How to compute the income tax payable on income derived by two individuals or more together? How is donation income assessed for Individual Income Tax payable?How to compute the income tax payable in case that the employers bear theIndividual Income Tax for the taxpayers?How is income derived from sources outside China assessed for Individual IncomeTax payable?What are the main exemptions for Individual Income Tax?What kind of bond interest income and earmarked saving deposit interest income are exempt from Individual Income Tax as ruled by the State?What are the main reductions for Individual Income Tax?What are the rules concerning the mode, time and places for Individual Income Tax payment? How to report and pay income tax on wages and salaries income?How to report and pay income tax the production and business operation income of Individual Industrial and Commercial Households?How to report and pay income tax on the income derived by enterprises and institutions from contracting businesses and/ or leasing businesses?How do the investors of the single proprietorship and partnership enterprises report and pay their income tax on production and business income?How to report and pay income tax on income earned by taxpayers from sources outside China?税率 个丄八所得税法趙颔累进税率*九级、五级 比例税率;20^0(有加咸与減征)应纳税所得额规走Y J 纳税申报及缴纳代扣代缴L 两个判走标准厂纳税义筈兀1-居民纳税人与非居民纳税人划分应税所得项目’ 11个税目税收优惠境外所得已纳税额扣除’分国又分项计算扣除限额,差颔补税自行申扌艮 纳税义务人 判定标准 征税对象范围1.居民纳税人 (负无限纳税 义务) (1) 在中国境内有住所的个人(2) 在中国境内无住所,而在中国境内居住满一年的个 人。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。