Behavioural Finance Case Study

终于还是行为金融学拿了今年的诺贝尔为芒格喝彩

终于还是⾏为⾦融学拿了今年的诺贝尔为芒格喝彩2017年10⽉9⽇,2017诺贝尔奖最后⼀个奖项——经济学奖颁布,颁给了Richard H. Thaler,获奖原因是'for his contributions to behavioural economics',表彰他在⾏为经济学(更倾向于⾏为⾦融学)⽅⾯的贡献,是⽼爷⼦⼀个⼈拿奖,值得庆贺。

⽼实说,这个奖项终于揭晓的时候,还是有点窃喜的。

12-14年读⾦融MBA的时候,和教授讨论过经济学、⾦融学的未来发展、现状问题等,当时最直观的问题就是股市⾥明明就是有⼈赔有⼈赚的,有效市场假说条件这么苛刻、现实社会太难达到,⽼师就提到了⾏为⾦融学,对我这个当时的⾦融⼩⽩来讲,很是感兴趣,讨教了不少问题。

⽼师还特意说⾏为⾦融学有很多借鉴⽣物学的地⽅,⽣物系统⾥有⾷物链、⾦字塔、有群体也有个体、有⽣物多样性,⾦融系统有很多类似的地⽅,⽐想象的更复杂、有⽣态。

从此记住了这个词,关注这个领域,没想到⼏年后拿了诺贝尔奖。

⼀. 什么是⾏为⾦融学behavior finance⾏为⾦融学是⾏为经济学behavior economics的分⽀。

根据定义,⾏为⾦融学是研究⼼理、社会、认知、情绪等因素在个体和机构经济决策中的作⽤,以及对市场价格、投资回报、资源分配产⽣的后果。

所以⾏为⾦融学算是交叉学科,是⾦融学、⼼理学、⾏为学、社会学等学科相交叉的边缘学科,⼒图揭⽰⾦融市场的⾮理性⾏为和决策规律。

同样在2013年获得诺贝尔奖的有效市场假说(efficient market hypothesis,EMH)简单假设所有⾦融市场的⼈都是理性的,不理性的⼈会被赶出市场。

要真是这样,那⾲菜怎么会⼀茬⼀茬地被割呢。

简单常识,这个假设没有考虑到⼈的寿命,这⼀波⾮理性的⼈被赶出市场,还有下⼀批新的⾮理性⼈冲进来。

与之相对,⾏为⾦融学认为市场上除了理性参与者,还有有限理性参与者,有限理性参与者是会犯错误的;在绝⼤多数时候,市场中理性和有限理性的投资者都是起作⽤的,共同决定市场价格。

哈佛案例库英文

哈佛案例库英文1. Harvard Case Study Library -哈佛案例库2. Case study -案例研究3. University -大学4. Business -商业5. Management -管理6. Strategy -战略7. Marketing -市场营销8. Finance -财务9. Entrepreneurship -创业10. Leadership -领导力11. Decision-making -决策12. Analysis -分析13. Innovation -创新14. Problem-solving -解决问题15. Organizational behavior -组织行为16. Negotiation -谈判17. Corporate culture -企业文化18. Ethical dilemma -道德困境19. Teamwork -团队合作20. Globalization -全球化21. Human resources -人力资源22. Supply chain -供应链23. Industry -行业24. Case method -案例教学方法1. The Harvard Case Study Library is a valuable resource for students and researchers. -哈佛案例库对于学生和研究人员来说是一个宝贵的资源。

2. The case studies in the Harvard Case Study Library cover a wide range of topics. -哈佛案例库中的案例研究涵盖了广泛的话题。

3. Harvard University is renowned for its rigorous academic programs. -哈佛大学以其严谨的学术课程而闻名。

journal of behavioral and experimental finance发表日记

journal of behavioral and experimental finance发表日记全文共四篇示例,供读者参考第一篇示例:《Journal of Behavioral and Experimental Finance》是一本国际学术期刊,致力于探讨金融领域中行为金融和实验金融学的研究。

该期刊涵盖了许多重要的话题,如投资决策、资产定价、市场行为和金融市场的效率性等。

在这篇文章中,我将分享我在该期刊上发表文章的日记,并介绍一些关于行为金融和实验金融领域的最新研究成果。

第一天:提交稿件今天我决定将我团队最新的实验研究成果提交到《Journal of Behavioral and Experimental Finance》进行发表。

我们的研究主题是关于投资者情绪对股票市场波动的影响。

通过实验模拟投资者的情绪波动,我们发现投资者情绪的波动会导致股票市场的价格波动更加频繁和剧烈。

这一发现对于理解金融市场的运行机制有着重要的启示。

第十天:收到审稿意见今天我们收到了《Journal of Behavioral and Experimental Finance》的审稿意见,审稿人建议我们对研究框架和实验设计进行进一步的完善和调整。

他们认为我们的实验结果很有启发性,但是在研究方法和数据分析上还需要更加细致的处理。

我们决定根据审稿意见对论文进行修改,并重新提交给编辑部。

第三十天:被接受发表我们的研究论文今天正式在线发表在《Journal of Behavioral and Experimental Finance》的网站上。

这标志着我们的研究工作正式对外公开,可以为其他学者和研究者提供有益的参考和启示。

我希望通过这篇文章能够引起更多人对行为金融和实验金融学的关注,促进这一领域的研究和发展。

第二篇示例:第一篇文章是一篇关于“情绪在金融市场中的影响”的实证研究。

文章通过对投资者情绪和市场交易行为之间的关系进行了深入分析,并得出了一些有趣的结论。

cfa3级 case study

CFA3级案例研究一、概述CFA3级考试是 Chartered Financial Analyst(注册金融分析师)资格认证考试的最高级别。

该考试是金融行业著名的专业人士认证考试之一,被认为是全球金融行业最具专业性和权威性的认证考试之一。

CFA3级考试的案例研究部分是考试的一个重要组成部分,通过对真实世界的金融案例进行分析和解决问题,考察考生在实际工作中处理复杂金融问题的能力,是考试的重点难点之一。

二、案例分析1. 案例背景本次案例研究的主题是关于某家上市公司的财务报表分析及估值分析。

这家公司是一家跨国企业,主要经营范围涉及多个行业,是全球知名的多元化企业。

在过去的几年中,该公司的业绩呈现出了一定的波动,市场对其未来的发展前景存在一定的分歧。

2. 案例问题本次案例研究主要围绕以下几个问题展开分析:(1)通过分析该公司的财务报表,对其财务状况做出评估,并指出存在的风险和挑战;(2)采用合适的方法对该公司进行估值分析,并提出自己的估值结论;(3)分析该公司所处行业的市场环境和竞争格局,评估其未来的发展潜力;(4)就公司的财务和经营情况,提出自己的投资建议。

3. 解决方法针对上述问题,考生需要运用所学的财务分析、公司估值、风险管理、投资组合管理等知识,结合行业动态和相关领域的最新研究成果,对该公司的财务状况和未来发展进行全面、深入的分析,并给出自己的见解和建议。

三、分析方法1. 财务报表分析需要对该公司的财务报表进行深入分析,包括利润表、资产负债表、现金流量表等,从中提取相关的财务指标,如利润率、资产负债率、经营现金流等,以此来评估该公司的财务状况。

2. 公司估值分析考生需要采用适当的估值模型对该公司进行估值,可以选择盈余折现模型(DCF)、市盈率法、市净率法等多种方法进行估值,综合考虑估值结果的优劣势,得出自己的估值结论。

3. 行业分析第三,需要对该公司所处行业的市场环境进行深入分析,包括行业生命周期阶段、市场增长率、供应链及竞争格局等,以便更好地了解该公司的发展潜力。

行政管理专业英语词汇

行政管理专业英语一、人力资源管理:(Human Resource Management ,HRM)人力资源经理:( human resource manager)高级管理人员:(executive) / i`gzekjutiv职业:(profession)道德标准:(ethics)操作工:(operative employees)专家:(specialist)人力资源认证协会:(the Human Resource Certification Institute,HRCI) 二、外部环境:(external environment)内部环境:(internal environment)政策:(policy)企业文化:(corporate culture)目标:(mission)股东:(shareholders)非正式组织:(informal organization)跨国公司:(multinational corporation,MNC)管理多样性:(managing diversity)三、工作:(job)职位:(posting)工作分析:(job analysis)工作说明:(job description)工作规范:(job specification)工作分析计划表:(job analysis schedule,JAS)职位分析问卷调查法:(Management Position DescriptionQuestionnaire,MPDQ)行政秘书:(executive secretary)地区服务经理助理:(assistant district service manager)四、人力资源计划:(Human Resource Planning,HRP)战略规划:(strategic planning)长期趋势:(long term trend)要求预测:(requirement forecast)供给预测:(availability forecast)管理人力储备:(management inventory)裁减:(downsizing)人力资源信息系统:(Human Resource Information System,HRIS)五、招聘:(recruitment)员工申请表:(employee requisition)招聘方法:(recruitment methods)内部提升:(Promotion From Within ,PFW)工作公告:(job posting)广告:(advertising)职业介绍所:(employment agency)特殊事件:(special events)实习:(internship)六、选择:(selection)选择率:(selection rate)简历:(resume)标准化:(standardization)有效性:(validity)客观性:(objectivity)规范:(norm)录用分数线:(cutoff score)准确度:(aiming)业务知识测试:(job knowledge tests)求职面试:(employment interview)非结构化面试:(unstructured interview)结构化面试:(structured interview)小组面试:(group interview)职业兴趣测试:(vocational interest tests)会议型面试:(board interview)七、组织变化与人力资源开发人力资源开发:(Human Resource Development,HRD)培训:(training)开发:(development)定位:(orientation)训练:(coaching)辅导:(mentoring)经营管理策略:(business games)案例研究:(case study)会议方法:(conference method)角色扮演:(role playing)工作轮换:(job rotating)在职培训:(on-the-job training ,OJT)媒介:(media)八、企业文化与组织发展企业文化:(corporate culture)组织发展:(organization development,OD)调查反馈:(survey feedback)质量圈:(quality circles)目标管理:(management by objective,MBO)全面质量管理:(Total Quality Management,TQM)团队建设:(team building)九、职业计划与发展职业:(career)职业计划:(career planning)职业道路:(career path)职业发展:(career development)自我评价:(self-assessment)职业动机:(career anchors)十、绩效评价绩效评价:(Performance Appraisal,PA)小组评价:(group appraisal)业绩评定表:(rating scales method)关键事件法:(critical incident method)排列法:(ranking method)平行比较法:(paired comparison)硬性分布法:(forced distribution method)晕圈错误:(halo error)宽松:(leniency)严格:(strictness)3600反馈:(360-degree feedback)叙述法:(essay method) 集中趋势:(central tendency)十一、报酬与福利报酬:(compensation) 直接经济报酬:(direct financial compensation) 间接经济报酬:(indirect financial compensation)非经济报酬:(no financial compensation)公平:(equity)外部公平:(external equity)内部公平:(internal equity)员工公平:(employee equity)小组公平:(team equity)工资水平领先者:(pay leaders)现行工资率:(going rate)工资水平居后者:(pay followers)劳动力市场:(labor market)工作评价:(job evaluation) 排列法:(ranking method) 分类法:(classification method) 因素比较法:(factor comparison method)评分法:(point method) 海氏指示图表个人能力分析法:(Hay GuideChart-profile Method)工作定价:(job pricing) 工资等级:(pay grade) 工资曲线:(wage curve) 工资幅度:(pay range)十二、福利和其它报酬问题福利(间接经济补偿)员工股权计划:(employee stock ownership plan,ESOP) 值班津贴:(shift differential)奖金:(incentive compensation) 分红制:(profit sharing)十三、安全与健康的工作环境安全:(safety) 健康:(health) 频率:(frequency rate) 紧张:(stress) 角色冲突:(role conflict) 催眠法:(hypnosis) 酗酒:(alcoholism) 十四、员工和劳动关系工会:(union) 地方工会:(local union) 行业工会:(craft union) 产业工会:(industrial union) 全国工会:(national union) 谈判组:(bargainingunion) 劳资谈判:(collective bargaining) 仲裁:(arbitration)罢工:(strike) 内部员工关系:(internal employee relations) 纪律:(discipline) 纪律处分:(disciplinary action)申诉:(grievance) 降职:(demotion) 调动:(transfer) 晋升:(promotion)1、操作工:(operative employees)-我认为operation staff更符合实际和贴切2、既然提到企业文化,我想加上愿景应该更好-愿景:(vision)3、目标:(mission) -mission翻译成使命更好,目标可以是goal,没有mission 这种使命感给人感觉更强烈;4、职位:(posting)-显然应该是position5、工作说明:(job description)-译成职位描述或许更加,HR专业术语中我们称其为JD6、行政秘书:(executive secretary)-应该是执行秘书,“执行秘书”比一般的“行政秘书”更高一级,基本等同主管级员工;7、地区服务经理助理:(assistant district service manager)-这个词组对一般企业来说基本没有意义,应该只是某个特定公司设置的特定职位。

Behavior-Finance-复旦行为经济学

实证

• 孪生股权(twin shares)

1907年皇家荷兰(在美国和纽芬兰交易)

和壳牌运输(在英国交易)按60:40的基率 同意合并他们的股权,但仍保留为分离的实 体。如果价格等于基本价值,皇家荷兰的股 权价值应总是壳牌股权价值的1.5倍。 Froot and Dabora(1999)发现两者的股权价值 之比严重偏离1.5,而且,皇家荷兰按平价有 时35%被低估,有时15%被高估。

20 世纪70 年代法马(Fama) 对有效市场假说 ( EMH) 进行了正式表述,布莱克、斯科尔斯和莫

顿(Black-Scholes-Merton) 建立了期权定价模 型(OPM) ,至此,现代金融学已经成为一门逻辑

严密的具有统一分析框架的学科。

第四页,编辑于星期四:十六点 二十八分。

行为金融学理论简介

第三页,编辑于星期四:十六点 二十八分。

1952 年马克威茨(Markowitz) 发表了著名的论文 “portfolio selection”,建立了现代资产组合理 论,标志着现代金融学的诞生。

20 世纪60 年代夏普和林特纳(Sharp,Lintner) 建立并扩展了资本资产定价模型(CAPM)。

• ①投资者是有限理性的,投资者是会犯错误的。

• ② 在绝大多数时候,市场中理性和非理性的投 资者都是起作用的(而非标准金融理论中的非理 性投资者最终将被赶出市场,理性投资者最终决 定价格)。非理性对价格的影响是实质性的和长 期的。文献称之为“套利限制 (limits of arbitrage).

• 利用前景理论解释了不少金融市场中的异常现象:如股价 溢价之迷(equity premium puzzle)

英国留学国际金融专业

英国留学国际金融专业英国留学金融专业详解分类及介绍国外关于金融专业的设置,是两方面都有。

一、以微观为主,也就是研究与公司个体有关的投资、融资等行为。

另一方面就是和国内类似的宏观金融的研究。

专业细分英国大学的金融专业按细分不同通常设置在商学院、经济学院或数学学院。

在参考专业排名时需要考虑会计与金融、经济、商学三个方向。

金融专业细分可分为:金融学、公司金融、金融与投资、国际金融、银行与金融、金融与管理、会计与金融、风险管理、房地产金融与投资、金融与经济、金融工程。

金融学:对金融各个细分领域的综合介绍。

下面以曼彻斯特大学为例来看下金融学专业的课程设置:第一学期必修课:Introductory Research Methods for Accounting and Finance; 会计与金融学方法导论Essentials of Finance;金融学精要Derivative Securities衍生证券选修一门:Portfolio Investment证券投资International Macroeconomics and Global Capital Markets国际宏观经济学与全球资本市场Foundations of Finance Theory金融学基础第二学期Financial Econometrics金融计量经济学Advanced Empirical Finance高级实证金融学Corporate Finance; 公司金融选修一门International Finance国际金融Financial Statement Analysis财务报表分析Real Options in Corporate Finance公司金融中的实物期权Mergers and Acquisitions: Economic and Financial Aspects关于企业并购的经济金融思考Dissertation毕业论文公司金融:解决以公司财务、公司融资、公司治理为核心的公司治理结构方面的问题,综合运用各种形式的金融工具与方法,进行风险管理和财富创造。

行为金融学(下)

• 又被称为“赢者输者效应”

4、动量效应与反转效应的解释 代表性启发法可用于解释“动量效应与 反转效应”,投资者依赖于过去的经验法 则进行判断,并将这种判断外推至将来。

七、过度反应和反应不足

1、反应不足 • 反应不足是指证券价格对影响公司价值的 基本面消息没有做出充分的、及时的反应。

2、过度反应 • 过度反应是指人们过于重视新的信息而忽 略老的信息,即使老的信息对于价格的影 响更大。

Lee,Shleifor和Thaler于1991年提出了 著名的LST模型,认为基金折价率变化反映 的是个人投资者情绪的变化。他们认为持 有封闭式基金的个人投资者中有许多噪声 交易者 。 基金价值波动风险和噪声交易者情绪波 动风险

在这一过程中,基金发行人发挥了“诱 导效应”

而当封闭式转为开放式或者清盘时,噪 声交易者和理性交易者都知道将按照资产 净值来进行

下图是历史上的折价率情况。

2003年底,封闭式基金的平均折价率为22%,

2004年6月30日达到27.07%,2005年4月29 日达到37.01%。

• • • • • • • • • • • • • • • •

代码 名称 交易价 净值代码 基金净值 升贴水值 折价率(2007年6月18日) 510880 红利ETF 3.622 495303N 3.539 -0.083 510180 180ETF 9.102 491105N 2.724 -6.378 510180 180ETF 9.102 491105N 3.119 -5.983 510050 上证50ETF 3.080 495001N 2.976 -0.104 500058 基金银丰 2.450 500058N 2.701 0.251 500056 基金科瑞 2.637 500056N 3.153 0.515 500039 基金同德 2.675 500039N 2.715 0.040 500038 基金通乾 2.297 500038N 2.646 0.349 500029 基金科讯 3.374 500029N 3.306 -0.068 500025 基金汉鼎 2.261 500025N 2.381 0.120 500018 基金兴和 2.274 500018N 2.718 0.444 500015 基金汉兴 1.719 500015N 2.076 0.357 500011 基金金鑫 2.651 500011N 2.424 -0.227 500009 基金安顺 2.510 500009N 2.916 0.406 500008 基金兴华 2.510 500008N 2.894 0.384 2.35% 4.17% 1.82% 3.49% -9.29% -16.35% -1.47% -13.18% 2.06% -5.04% -16.35% -17.20% 9.35% -13.93% -13.28%

价值投资的理论与实践(英文)

The soundness of a common stock investment, in a single issue or a group of issues, may well depend on the ability of the investor or the analyst-advisor to justify the purchase by a process of formal valuation. In plainer language, a common-stock purchase may not be regarded as a proper constituent of a true investment program unless some rational calculation will show that it is worth at least as much as the price paid for it."

Picture credit: Dimensional Fund Advisors

Efficient markets hypothesis

• Weak form: all past market prices and data are fully reflected in securities prices. (Technical analysis is of no use.)

Value investing in theory and in practice

Travis Morien Compass Financial Planners Pty Ltd

In the beginning…

What is value investing?

Case Studies in finance - Case 2

Asset Utilization Ratios

Inventory Turnover Ratio = Cost of Goods Sold / Inventory Days sales in Inventory = 365 / Inventory Turnover Receivables Turnover = Sales / Receivables Days’ Sales in Receivables =365 / Receivables Turnover

CASE STUDIES

Lets get started with case 2 in your book

CASE 2: BIGGER ISN’T ALWAYS BETTER

Objective: financial ratio analysis

Case 2

When doing financial analysis …

Financial analysis …

Each are using the financial analysis for different particular objectives:

Short-term creditors place emphasis on immediate liquidity of the business because they seek an early payback of their investment Long-term investors in bonds are primarily concerned with the long-term asset position and earning power of the company The equity investor is primarily interested in long-term earning power of the company, its ability to grow, and pay dividends and increase in value.

Behavioral Economics and Decision-Making

Behavioral Economics and Decision-Making Behavioral economics is a subfield of economics that studies how people make decisions, particularly in situations where their choices are influenced by psychological and social factors. This field of study has gained increasing attention in recent years, as it has become clear that traditional economic models do not always accurately predict human behavior. In this essay, I will explore the key concepts of behavioral economics and decision-making, and discuss their relevance in today's society.One of the key concepts in behavioral economics is the idea of bounded rationality. This refers to the fact that people are not always able to make fully rational decisions, due to limitations in their cognitive abilities and information processing. For example, people may have limited attention spans, and may not be able to fully consider all the relevant information when making a decision. Additionally, people may be influenced by biases and heuristics, which can lead them to make decisions that are not fully rational.Another important concept in behavioral economics is the idea of loss aversion. This refers to the fact that people tend to place a higher value on avoiding losses than on achieving gains. For example, people may be more willing to take risks in order to avoid losing money than they would be to make the same amount of money in a safe investment. This can have important implications for decision-making, as people may be more likely to make decisions that avoid losses, even if those decisions are not in their best interests in the long run.A related concept in behavioral economics is the idea of framing effects. This refers to the fact that people's perceptions of a decision can be influenced by the way it is presented to them. For example, people may be more likely to choose a product if it is presented as having a discount, even if the actual price is the same as a similar product that is not advertised as being on sale. This can have important implications for marketing and advertising, as companies may be able to influence consumers' choices by framing their products in a certain way.Another important concept in behavioral economics is social norms. This refers to the unwritten rules and expectations that govern behavior in a particular society or group. For example, people may be more likely to recycle if they believe that it is a social norm in their community. This can have important implications for policy-making, as policymakers may be able to encourage certain behaviors by promoting social norms that support those behaviors.Finally, behavioral economics also considers the role of emotions in decision-making. This is an important area of study, as emotions can have a powerful influence on our choices. For example, people may be more likely to make impulsive purchases when they are feeling stressed or anxious. Additionally, people may be more likely to make charitable donations when they are feeling empathetic towards the people or causes they are supporting.In conclusion, behavioral economics is a fascinating field of study that has important implications for our understanding of decision-making. By studying the ways in which people make choices, we can gain insights into why people behave the way they do, and how we can encourage more positive behaviors. As our society becomes more complex and interconnected, the insights of behavioral economics will become increasingly important in shaping policy and improving our lives.。

行为金融学理论(Behavioralfinancetheory)

行为金融学理论(Behavioral finance theory)The modern financial theory classic that people's decisions are based on rational expectations (Rational Expectation), risk avoidance (Risk Aversion), the utility maximization and constantly update their knowledge and decision making assumptions, but a lot of psychological research shows that people's actual investment decision is not so. Secondly, the modern financial theory and the efficient market hypothesis is established on the basis of effective competition in the market, and a large number of studies show that non rational investors often can obtain higher returns than investors. Behavioral finance is based on this kind of market vision, and develops a new financial study using the psychological study of people's actual decision-making process.Behavioral finance studies the mispricing of investment in the investment market due to its own investment behavior, and the resulting behavioral anomaly is the place where Alfa (beyond the market rate of return) is generated. Experts on behavioral finance more, managers have more chances to find Alfa, but also the financial behavior so the seed and buried self destruction, Alfa in the market is less, the market will become more effective, and behavioral anomalies in the market less, then study the financial financial will have no need to there. Second, the more managers who want to beat the market, the harder they work, the more effective the market will become and the less likely it will be to beat the market.The emergence of 4.3.1. behavioral financeAs early as 1950s, people began to study behavioral economics,but earlier studies were rather scattered. It was not until 1970s that Kahneman (Daniel Kahneman) and Tversky (Amos Tversky) conducted extensive and systematic research on this field. Behavioral economics emphasizes that people's behavior is not only driven by interest, but also influenced by many psychological factors. The prospect theory combines psychological research and economic research effectively, reveals the decision-making mechanism under uncertainty, and opens up a completely new research field.4.3.2. is a leading representative of behavioral financeKahneman, the founder of Behavioral Finance (Daniel Kahneman) in 1934 was born in Israel in 1954, graduated from the Hebrew University, and in 1961 obtained a doctorate in psychology at the University of California, after the turn at the Hebrew University faculty. Another creator Tversky (Amos Tversky) was born on 1937 in Israel, has been at the University of Michigan studied philosophy and psychology at the Hebrew University, after graduation, here met his best partner Kahneman, which opened their lifelong friendship and excellence in academic research, and in 1979 jointly issued the basic theory of "behavioral finance prospect theory" (Prospect Theory). Later, he went to the University of California at Berkeley in the United States, and he went to Standford in the United states.Kahneman because of the prospect theory of behavioral finance contribution in 2002 received the Nobel Prize in economics, but it is a pity but Tversky in 6 years ago (1996 years) died, only 59 years old, can not wait for the arrival of honor.4.3.3. behavioral finance, major perspectivesBehavioral finance mainly puts forward two theories:A. BSV (Barberis, Shlefer, and, Vishny, 1998),B. DHS (Daniel, Hirsheifer, and, Subramanyam, 1998).First, the BSV theory holds that returns are stochastic, but the general investor erroneously believes that there are two paradigms for income change:Paradigm A: investors think that earnings change is mean reversion, and stock volatility is only a temporary phenomenon, and does not need to adjust its behavior according to changes in income. This behavior will cause investors to respond to the expected lack of earnings, and when the actual earnings do not match the expectations, they will be adjusted, so that changes in the stock price reaction to changes in earnings lags behind.Paradigm B: investors think that changes in earnings tend to be trend, and share prices have the same direction and continuous effects on earnings. Such investors tend to tend to expand the trend by mistake and overreact to changes in earnings.Second, DHS theory divides investors into two categories: one is the information one, the other is the non information. Without information, its investment behavior will not be affected by the judgment bias, and the information can be easily affected by the judgment bias.The DHS model divides the judgment bias of the information into two categories: one is overconfidence, and the other is biased self attribution (self-contribution). Overconfidence leads investors to exaggerate the accuracy of their stock valuation; biased self attribution leads investors to underestimate the impact of public information on stock value. That is to say, when the investor pursues this model, it will lead to the deviation between the personal information and the public information,This divergence leads to short-term continuity and long-term support for share prices.4.3.4. main behavioral finance modelUnder the framework of the two kinds of BSV and DHS, put forward the prospect theory of Behavioral Finance (Prospect Theory), behavioral portfolio theory (Behavioral Portfolio Theory) and the behavior asset pricing model (Behavioral BAPM Asset Pricing Model) on behavioral finance model.A. prospect theoryTheory (Prospect) combines psychological research and economic research effectively, reveals the decision-making mechanism under uncertainty, and opens up a whole new research field. In this sense, Kahneman's award may change the direction of future economics.In general, the prospect theory has the following three basicprinciple: (a) the majority of people in the face of the time are risk averse; (b) the majority of people in the face of loss when the risk preference; (c) are more sensitive to losses than get.Law of prospect theory: people are often cautious and unwilling to take risks when they are faced with them, while everyone is an adventurer in the face of losses. In the face of the time to avoid risks, and in the face of preference for the risk of loss, and the loss and the gain is relative to the reference point for the change, people use things in the evaluation point of view, can change people's attitude toward risk.The law of prospect theory two: People's sensitivity to loss and gain is different, and the pain of loss is far greater than that of happiness. In the 1992 study, Tversky and Kahneman found that people usually needed two times the loss of earnings to make up for the pain caused by the loss.B. behavioral portfolio theoryThe combination theory of BPT (Behavioral Portfolio Theory) behavior of assets, in 1985 by Shefrin and Statman put forward the theory that Pyramid investors have layered structure of the portfolio, each layer corresponds to the specific investment objectives and risk investors. Some of the money is invested at the bottom of the safest, and some funds are invested in more risky higher ups, with correlations between layers.Relatively speaking, the traditional portfolio theory to portfolio as a whole, and it is assumed that only the covariancebetween different securities account in building the portfolio, and are risk averse investors, and this behavior in real life is not entirely consistent.C. behavioral asset pricing modelBehavioral Model BAPM (Behavioral Asset Pricing asset pricing) investors are divided into information traders and noise traders. Information traders are rational investors who support the CAPM model of modern financial theory, avoid cognitive errors, and have variance preferences. Noise traders are apt to make conscious errors and have no strict variance preferences.When the information traders occupy the main body of the market, the market is efficient; when the noise traders occupy the market main body, the market is inefficient. In BAPM, the returns on securities are determined by the "Behavioral Beta", where the market portfolio is more representative. For example, noise traders tend to overestimate the price of growth stocks, and the proportion of growth stocks in the corresponding market is higher, because the behavioral portfolio is proportional to the market mix and the proportion of mature stocks should be raised.Statman further pointed out that the decision to supply and demand is people's utilitarian considerations (product costs, alternatives, prices, etc.) and value expression considerations (personal tastes, special preferences, etc.). CAPM includes only utilitarian considerations, while BAPM includes both. Due to the characteristics of BAPM value, andthe utilitarian characteristics, therefore, it is effective to accept a market from can't beat the market, on the other hand, from the meaning of rationalism of refuse market efficiency, the future development of finance has a profound revelation.In short, the behavioral finance through questioning on modern financial core hypothesis "theory of rational people", put forward the prospect theory, utility function of investors is concave function, and face the loss of utility function is a convex function. In financial transactions, investors psychological factors will make the actual decision-making process of optimal decision process is described from the classical finance theory, and system of rational deviation, and not because of the statistical average and eliminate.The investment strategies based on behavioral finance include average capital strategy, time diversification strategy, contrarian investment strategy and inertial investment strategy.4.3.5. behavioral finance explains the main behavioral anomalies in the marketA. overreactionPeople are too sensitive to asset prices, information conferences make people overreact, resulting in excessive or falling securities prices.B. disposition effectDue to the cognitive bias of investors,For the performance of the investment profit and loss of certainty ". The" loss aversion of the heart ", reflected in the behavior for selling profitable stocks to sell, easy to be a losing stock phenomenon, resulting in the relatively long time firmly.C. noise tradingShort - term investors and noise traders in the market have their own information. In his collection of information, by which investors more specific information, the more likely he is to profit, and such information may be associated with the basic value of information, also may be unrelated with the basic value of noise, which is called the information aggregation positive spillover effect. This effect may make the traders who obtain new information can not get the corresponding return, which is not conducive to the collection of information and the allocation of resources.D. herd effectInvestors are affected and imitated by other investors under the influence of uncertain information. That is, "all investors run in the same direction, and no one struggles with the overwhelming majority of people."."There are two main herding effects in the stock market:The first is the information based herd effectComplete information is a premise hypothesis of neo classical finance theory, but in fact, even in the modern society where information is highly disseminated, information is inadequate. In the case of insufficient information, investors do not make decisions entirely on the basis of their own information decisions, but on the basis of other people's investment behavior. The herding performance is "follow suit" or "the village" phenomenon.The second is the reputation based and reward based herd effectThis effect is most common in the fund manager, because employers do not understand the fund managers, fund managers do not understand their own investment capacity, in order to avoid investment mistakes and reputation risks and their remuneration, fund managers have motivation to mimic other fund managers' investment behavior. If many fund managers take the same action, the herd effect will emerge.。

casestudy范文

casestudy范文英文回答:Case Study: Evaluating the Effectiveness of a New Marketing Campaign.Executive Summary.A leading consumer goods manufacturer launched a new marketing campaign to promote its flagship product. The campaign employed a multi-channel approach, including television, print, and digital advertising, as well as social media and influencer marketing. The primary objective of the campaign was to increase brand awareness and drive sales.Methodology.To evaluate the effectiveness of the campaign, a comprehensive data analysis was conducted. Key performanceindicators (KPIs) were identified and tracked, including brand awareness, website traffic, and sales conversion rates. Data was collected from various sources, including Google Analytics, social media platforms, and internal sales records.Results.The campaign was highly successful in achieving its objectives. Brand awareness increased by 20%, website traffic surged by 35%, and sales conversion rates improved by 15%. The campaign also generated significant buzz on social media, with over 1 million impressions and 50,000 shares.Analysis.The positive results of the campaign can be attributed to a combination of factors. The multi-channel approach ensured that the message reached a wide audience. The creative execution was impactful and memorable, resonating with consumers. The use of influencers and social mediamarketing amplified the reach and credibility of the campaign.Recommendations.Based on the findings of the evaluation, several recommendations were made to further enhance the effectiveness of future campaigns. These include:Optimizing creative assets for different channels and platforms.Increasing the frequency and consistency of messaging across channels.Exploring additional channels, such as paid search and email marketing.Continuously monitoring and analyzing campaign performance to identify areas for improvement.Conclusion.The new marketing campaign was a resounding success. It effectively increased brand awareness, drove website traffic, and boosted sales conversion rates. The multi-channel approach, impactful creative execution, and strategic use of social media and influencers were key factors contributing to the positive results.中文回答:案例分析,评估新营销活动的效果性。

行为金融学英文文献读后感

行为金融学英文文献读后感Behavioral Finance: A Reflection on the LiteratureThe field of behavioral finance has gained significant traction in the past few decades, challenging the traditional assumptions of rational decision-making in the realm of finance. By incorporating insights from psychology and cognitive science, behavioral finance seeks to understand the complex and often irrational behaviors that influence financial decision-making. As an avid reader of the literature in this domain, I have been captivated by the insights and implications that this field has to offer.One of the core tenets of behavioral finance is the acknowledgment that individuals do not always act in a purely rational manner when it comes to financial decisions. The concept of bounded rationality, as proposed by Herbert Simon, suggests that our cognitive abilities are limited, and we often rely on heuristics, or mental shortcuts, to make decisions. These heuristics can lead to systematic biases and errors in judgment, such as the availability bias, where we tend to give more weight to information that is easily accessible, or the anchoring bias, where we heavily rely on initial information when making decisions.The work of Daniel Kahneman and Amos Tversky, pioneers in the field of behavioral economics, has been instrumental in understanding these biases and their impact on financial decision-making. Their prospect theory, for instance, challenges the traditional expected utility theory by demonstrating that individuals tend to be more averse to losses than they are attracted to gains of the same magnitude. This loss aversion can lead to suboptimal investment decisions, such as the reluctance to sell losing stocks in order to avoid realizing a loss.Another important aspect of behavioral finance is the role of emotions in financial decision-making. Emotions such as fear, greed, and overconfidence can significantly influence how individuals perceive and respond to market conditions. The herd mentality, where investors blindly follow the actions of others, is a prime example of how emotions can lead to irrational investment decisions. The fear of missing out (FOMO) can drive investors to jump on bandwagons, often at the expense of sound investment strategies.The implications of behavioral finance extend beyond the individual investor level. Researchers have also explored the impact of behavioral biases on financial markets as a whole. The concept of market inefficiency, where asset prices do not fully reflect all available information, is closely linked to the behavioral biases of market participants. The phenomenon of asset bubbles and crashes,for instance, can be better understood through the lens of behavioral finance, as investors may succumb to the herd mentality or overreact to new information.Moreover, the insights from behavioral finance have important implications for the field of finance education and practitioner training. By understanding the cognitive biases and emotional factors that influence financial decision-making, educators and practitioners can develop strategies to mitigate these biases and improve investment outcomes. This includes promoting financial literacy, developing debiasing techniques, and incorporating behavioral finance principles into investment decision-making processes.Despite the significant progress made in the field of behavioral finance, there are still many avenues for further research and exploration. One area of interest is the cross-cultural and demographic differences in financial decision-making behaviors. As the global financial landscape becomes increasingly interconnected, understanding how cultural and individual factors shape financial decision-making will be crucial for developing more inclusive and effective financial policies and practices.Additionally, the rapid technological advancements in the financial industry, such as the rise of algorithmic trading and the increasinguse of artificial intelligence, present new challenges and opportunities for behavioral finance researchers. Exploring the interplay between human decision-making and technological innovations in finance will be a crucial area of study in the years to come.In conclusion, the field of behavioral finance has provided a valuable lens through which we can better understand the complex and often irrational nature of financial decision-making. By incorporating insights from psychology and cognitive science, behavioral finance has challenged the traditional assumptions of rational decision-making and has offered important implications for individual investors, financial markets, and the broader financial industry. As the field continues to evolve, I remain excited to see the new insights and practical applications that will emerge, ultimately contributing to a more comprehensive understanding of human behavior in the realm of finance.。

Lecture 10a -Behavioural Finance 2016_17 v.25

• Recognises that people are different, and not all the same:

– Biology affects how people trade in financial markets.

3

The style of this section

Lots of references to papers and studies:

• Emotions

– People feel happy or sad (technical terms: experience reward or regret), and this affects how they trade.

• Psychological Biases

– People frequently behave in a predictable manner that traditional finance would label as “irrational.”

Lecture 10a: Behavioural Finance

Outline:

• • What is it? The Failure of Rational Expectations models of human behaviour

•

•

The first successes of Behavioural Finance

5

• • •

The Rational Expectations models of human behaviour

• The neoclassical school of Finance makes some unrealistic assumptions about humans behaviour, which often don’t work in practice.

journal of behavioral finance好吗

journal of behavioral finance好吗Journal of Behavioral FinanceThe field of finance has always been a subject of great interest and importance, as it directly affects the economy on a global scale. In recent years, there has been a growing recognition of the role that human behavior plays in financial decision-making. This has led to the emergence of a specialized area of study known as behavioral finance. In this article, we will explore the Journal of Behavioral Finance and its significance in contributing to our understanding of financial markets and investor behavior.1. Introduction to Journal of Behavioral FinanceThe Journal of Behavioral Finance is a scholarly publication that focuses on research related to the intersection of psychology and finance. It provides a platform for academics, researchers, and practitioners to share their insights and findings on various aspects of behavioral finance. The journal covers a wide range of topics, including investor psychology, market anomalies, decision-making biases, and the influence of emotions on financial choices.2. Research ContributionsOne of the primary objectives of the Journal of Behavioral Finance is to contribute to the existing body of knowledge in the field. Through rigorous academic research, the journal aims to shed light on the complexities of financial decision-making and its underlying psychological factors. By publishing original studies and empirical research, the journal helps to bridge the gap between theory and practice in the field of finance.3. Market Anomalies and Investor BehaviorMarket anomalies refer to patterns or trends that contradict traditional financial theories and principles. The Journal of Behavioral Finance explores these anomalies and seeks to understand the underlying behavioral factors that contribute to them. For example, the journal may publish research on the disposition effect, which examines why investors tend to hold on to losing stocks and sell winning stocks prematurely. By uncovering these anomalies, the journal provides valuable insights into investor behavior and market inefficiencies.4. Decision-Making BiasesHuman beings are subject to various cognitive biases that can impact their decision-making processes. The Journal of Behavioral Finance delves into these biases and their implications for financial choices. It may publish studies on the impact of overconfidence, loss aversion, or the availability heuristic on investment decisions. These insights are crucial for both individuals and institutions in making more informed financial decisions.5. The Role of Emotions in FinanceEmotions play a significant role in shaping financial behavior. Greed, fear, and regret can influence investment decisions and market outcomes. The Journal of Behavioral Finance explores the emotional aspects of finance and analyzes how emotions can impact risk-taking behavior, asset pricing, and market volatility. By studying the emotional dynamics of financial markets, the journal aims to enhance our understanding of market trends and investor sentiment.6. Practical ImplicationsThe research published in the Journal of Behavioral Finance has practical implications for professionals in the finance industry. Asset managers, financial advisors, and policymakers can draw insights from the journal's findings to better understand investor behavior and develop effective investment strategies. By incorporating behavioral finance principles into their practices, industry professionals can potentially enhance investment performance and mitigate risks.7. Future DirectionsAs the field of behavioral finance continues to evolve, the Journal of Behavioral Finance plays a crucial role in facilitating further research and exploration. It provides a platform for scholars and researchers to exchange ideas and collaborate on new studies. The journal also encourages interdisciplinary approaches, combining insights from psychology, economics, and finance. This interdisciplinary perspective is essential for advancing our understanding of financial decision-making and shaping future trends in the field.ConclusionIn conclusion, the Journal of Behavioral Finance is an important publication that contributes to our understanding of the psychological factors that influence financial decision-making. Through its research contributions on market anomalies, decision-making biases, and the role of emotions in finance, the journal provides valuable insights for both academics and practitioners. By staying at the forefront of behavioral finance research, theJournal of Behavioral Finance enables us to make more informed and responsible financial choices.。

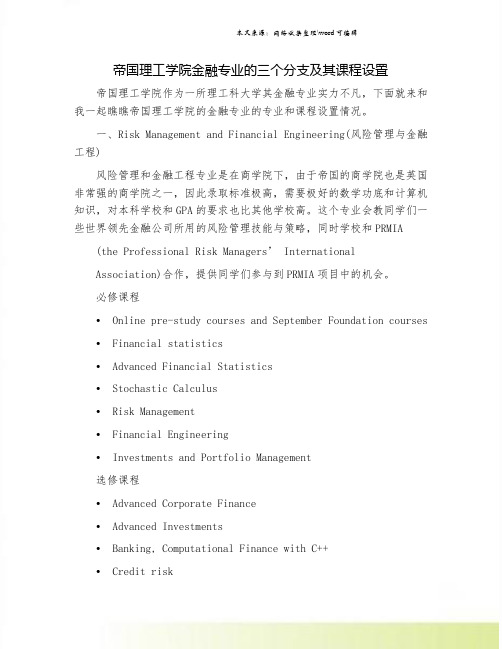

帝国理工学院金融专业的三个分支及其课程设置

帝国理工学院金融专业的三个分支及其课程设置帝国理工学院作为一所理工科大学其金融专业实力不凡,下面就来和我一起瞧瞧帝国理工学院的金融专业的专业和课程设置情况。

一、Risk Management and Financial Engineering(风险管理与金融工程)风险管理和金融工程专业是在商学院下,由于帝国的商学院也是英国非常强的商学院之一,因此录取标准极高,需要极好的数学功底和计算机知识,对本科学校和GPA的要求也比其他学校高。

这个专业会教同学们一些世界领先金融公司所用的风险管理技能与策略,同时学校和PRMIA (the Professional Risk Managers’ InternationalAssociation)合作,提供同学们参与到PRMIA项目中的机会。

必修课程• Online pre-study courses and September Foundation courses • Financial statistics• Advanced Financial Statistics• Stochastic Calculus• Risk Management• Financial Engineering• Investments and Portfolio Management选修课程• Advanced Corporate Finance• Advanced Investments• Banking, Computational Finance with C++• Credit risk• Enterprise Risk Management• Fixed-Income securities• General Insurance• Hedge Funds• International Finance• Life Insurance• Numerical Finance• Private Equity and Entrepreneurial Finance• Venture Capital Finance and Innovation• Structured Credit and Equity Products• Behavioural Investment Management• Advanced Options Theory二、Finance(金融)IC 的金融专业相比其他学校算是课业压力比较重的,各个金融课题都被清楚地设置成了一个独立的课程,除了会有相关公司的融资,各种资产投资外,IC还设有金融计量经济学、银行业等其他大学没有的课程。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Two-fold analysis

Examine the extent to which the disposition effect is present in the equity trades of mutual funds. Investigate how the disposition effect influences mutual funds’ investment style and performance.

Behavioural Finance Case Study

The Prevalence of the Disposition Effect in Mutual Funds’ Trades

ZHANG XIAONING

ZHANG WEICHAO

XU YANG

Outline

The research question Methodology used Main results

Methodology

• Detection of Disposition-Driven Behaviour

• Calculate the disposition spread • Create Metric of disposition ratio for Cross-Fund Comparisons

Q1. Why a substantial fraction of mutual funds exhibits the disposition effect? Q2. How do investors react when they are under pressure to act on their investments? Q3. Whether the teams have on disposition-prone behavior?

Implications

The research question

With skillful and experienced experts and superior technologies, U.S. equity mutual funds, on average, prefer realization of capital losses to capital gains.

Main results 2

Influences of the disposition effect on funds’ style and performance

Style • Lower market betas • Higher loadings on the book-to-market equity common risk factor is consistent with a value-oriented investment style • Lower (negative) loadings on the momentum factor is consistent with a short-term contrarian investment style Performance • No evidence that the disposition effect will have a negative impact on fund performance • The power of test may be limited by the quarterly frequency of trading extrapolated from quarterly holdings – study of more frequent data may indicate otherwise

Heterogeneity among sample results (22-55%)

• Persistent in the behaviour • Tend to add to losses More likely to be affected by the disposition effect when under pressure Funds managed by teams are more susceptible to disposition effect

Methodology

Data Sources and Sample Construction

• Portfolio holdings data for U.S. equity mutual funds from January 1980 to December 2009 came from Thomson/CDA

Methodology

Table 3. Proportion of Realized Gains and Losses by Type of Fund

Table 4. Logit Regression on Sell versus Hold Decision

Methodology

Table 5. Characteristics of Decile Portfolios Formed on DISP RATIO

Main results 1

Prevalence of disposition effect in US equity mutual funds’ trading

No aggregate tendency to realise gains ggesting that mutual funds serve as potential mitigators of distortions caused by retail investors

Implications of the study

For investment managers

For investors

Recognition of the disposition effect Self-assessment questions:

Real style vs. claimed style of a mutual fund

To what extent am I influenced? Is such influence justified?

E.g. claimed to be growth fund, but can be tilted towards value

E.g. value strategy, contrarian strategy Performance analysis

Methodology

Table 1. Proportion of Realized Gains and Losses Table 2. Proportion of Realized Gains and Losses by Subperiod

Figure 1. Large versus Small Families by Subperiods

Risk management procedures Performance record

Techniques to isolate trading decisions from the disposition effect

• Examination of the relation between disposition-driven behavior and portfolio style and performance

• Rank funds into deciles based on their disposition ratio in quarter t-1 at the beginning of each quarter t • Funds in each decile are placed into portfolios and held for 3 months, with the same ranking procedure and portfolio updating repeated every quarter. • After creating time series of monthly returns of the decile portfolios, evaluate their style characteristics and performance with the Fama and French (1993) and Carhart (1997) models