Introducton To Conditional Random Fields

条件随机场-机器学习系列

概率模型

条件随机场(Conditional Random Fields,以下简称为 CRF)是一种概率模型。除 此之外,其它常用的概率模型有朴素贝叶斯分类模型(Naive Bayes)和隐马尔 科夫模型(Hidden Markov Model,HMM)。 下面先从简单的概率模型开始,逐步引入 CRF。

隐马尔可夫模型 HMM 是对 Naive Bayes 的扩展,预测的不是单个类变量,而是 类变量序列 y=(y1,y2,…,yn),或者称状态序列。即,HMM 就是根据输入观测 序列 x =(x1,x2,…,xn)预测状态序列 y=(y1,y2,…,yn)。 自然想到的是,可否通过多个 Naive Bayes 模型来实现?具体来说,就是分别针 对每个观测变量 xi 来预测对应的状态变量 yi,这可以通过 Naive Bayes 模型来实 现。将这些模型组合起来,就得到根据观测序列 x =(x1,x2,…,xn)预测状态序列 y=(y1,y2,…,yn)的模型,即构造如下的联合概率

条件随机场概率计算问题 ..................................................................................................... 13

线性链条件随机场的学习 ..................................................................................................... 15

文档中符号的说明(本文基本遵循该约定,个别地方可能会违背,这时需根据 上下文确定): l ℝ 表示实空间,ℝ# 表示 n 维实空间。 l 普通变量一般用斜体小写字母标识,例如 a,x。 l 向量一般用小写粗斜体字母标识,例如 a,x。未转置时向量是指列向量。 l 矩阵一般用大写粗斜字母标识,例如 A,X。 l 随机变量一般用大写粗斜字母标识,例如 X。 l 函数名以及专有名称一般用正体字符串标识,大小写字母均可,例如 exp。 非特定的函数通常用斜体字符串标识,例如普通函数的标识 f。 l 矩阵或向量右上角的 T 表示转置,例如 ������% 表示向量 x 的转置。 l 矩阵与矩阵、矩阵与向量、向量与向量相连,如果中间没有连接符号,表 示一般的乘法运算,例如 Ax 表示矩阵 A 与向量 x 的乘法。 关于随机变量、随机向量等,本文约定如下: l 随机变量一般用大写字母标识,例如 X;随机向量(随机变量序列)或随机 变量组一般用粗体大写字母标识,例如 X。 l 随机变量 X 的具体取值一般 x 表示,随机向量 X =(X1,X2,…,Xn)的具体取 值一般用 x =(x1,x2,…,xn)表示。随机向量 X 的联合概率一般用 p(x)或 p(x1,x2,…,xn)表示。 l 在随机向量 X =(X1,X2,…,Xn)取值为 x =(x1,x2,…,xn)的条件下,随机向量 Y =(Y1,Y2,…,Ym)取值为 y =(y1,y2,…,ym)的条件概率表示为 p(y|x)、 p(y1,y2,…,ym|x1,x2,…,xn)或 p(y1,y2,…,ym|x) l 为了简化,文中常常省略掉随机变量或随机向量的说明,直接使用 p(x)、 p(y)、p(y|x)、p(x1,x2,…,xn)、p(y1,y2,…,yn)等表示各种概率。

ConditionalProbabilityandConditionalExpectation

K N−K

P{X = k} =

k

n−k N

n

In other words, X can be defined as the number of successes when

a sample of n items is randomly chosen from population that

P {X1

=

k |X1

+

X2

=

m}

=

P{X1 = k, X1 + X2 = P{X1 + X2 = m}

m}

=

P{X1 = k, X2 = m − P{X1 + X2 = m}

k}

=

P{X1 = k}P{X2 = m − P{X1 + X2 = m}

k}

=

n1 k

pk qn1−k

n2 m−k

pm−k qn2−m+k

P {X

=

k |X

+Y

=

n}

=

P{X = k, X + Y = P{X + Y = n}

n}

=

P{X = k, Y = n − P{X + Y = n}

k}

=

P {X

= k}P{Y = n − P{X + Y = n}

k}

Example

If X and Y are independent Poisson RVs with respective means λ1 and λ2, what is the conditional expectation of X given that X + Y = n?

ross introduction to probability models

ross introduction to probability models

"Introduction to Probability Models"是由Sheldon M.Ross编写的概率论教材。

该教材着重介绍了概率论的基本理论、模型和应用。

以下是对这本书的简要介绍:

书名:《概率模型导论》(Introduction to Probability Models)

作者:Sheldon M.Ross

出版时间:1972年(第一版),之后有多个版本

内容概要:这本书是概率论领域的经典教材之一,旨在向学生介绍概率模型及其在不同领域的应用。

它包含了从基础概率概念到更高级的概率模型的内容,如马尔可夫链、排队论等。

主要内容:

1.基础概率概念:样本空间、事件、概率等。

2.随机变量和概率分布。

3.大数定律和中心极限定理。

4.随机过程和马尔可夫链。

5.排队论和可靠性理论。

6.模拟方法及其应用。

目标受众:适用于概率论入门课程的本科生和研究生,以及对概率模型在实际问题中应用感兴趣的专业人士。

请注意,由于书籍可能有不同版本,建议查阅你所使用的具体版本以获取更详细的信息。

研究NLP100篇必读的论文---已整理可直接下载

研究NLP100篇必读的论⽂---已整理可直接下载100篇必读的NLP论⽂⾃⼰汇总的论⽂集,已更新链接:提取码:x7tnThis is a list of 100 important natural language processing (NLP) papers that serious students and researchers working in the field should probably know about and read.这是100篇重要的⾃然语⾔处理(NLP)论⽂的列表,认真的学⽣和研究⼈员在这个领域应该知道和阅读。

This list is compiled by .本榜单由编制。

I welcome any feedback on this list. 我欢迎对这个列表的任何反馈。

This list is originally based on the answers for a Quora question I posted years ago: .这个列表最初是基于我多年前在Quora上发布的⼀个问题的答案:[所有NLP学⽣都应该阅读的最重要的研究论⽂是什么?]( -are-the-most-important-research-paper -which-all-NLP-students-should- definitread)。

I thank all the people who contributed to the original post. 我感谢所有为原创⽂章做出贡献的⼈。

This list is far from complete or objective, and is evolving, as important papers are being published year after year.由于重要的论⽂年复⼀年地发表,这份清单还远远不够完整和客观,⽽且还在不断发展。

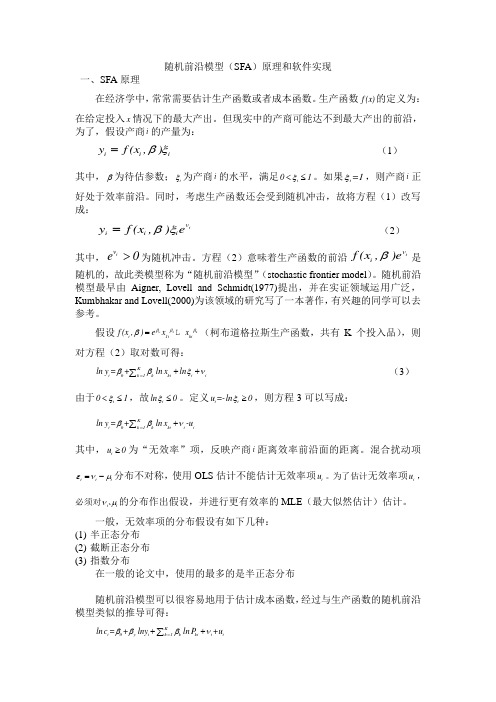

随机前沿模型SFA原理解读

随机前沿模型(SFA )原理和软件实现一、SFA 原理在经济学中,常常需要估计生产函数或者成本函数。

生产函数f (x)的定义为:在给定投入x 情况下的最大产出。

但现实中的产商可能达不到最大产出的前沿,为了,假设产商i 的产量为:i i i y f (x ,)βξ= (1) 其中,β为待估参数;i ξ为产商i 的水平,满足i 01ξ<≤。

如果i =1ξ,则产商i 正好处于效率前沿。

同时,考虑生产函数还会受到随机冲击,故将方程(1)改写成:i v i i i y f (x ,)e βξ= (2) 其中,i v e 0>为随机冲击。

方程(2)意味着生产函数的前沿i v i f (x ,)e β是随机的,故此类模型称为“随机前沿模型”(stochastic frontier model )。

随机前沿模型最早由Aigner, Lovell and Schmidt(1977)提出,并在实证领域运用广泛,Kumbhakar and Lovell(2000)为该领域的研究写了一本著作,有兴趣的同学可以去参考。

假设o k 1i 1i ki f (x ,)e x x ββββ=(柯布道格拉斯生产函数,共有K 个投入品),则对方程(2)取对数可得:K i 0k ki i i k 1ln y =+ln x ln ββξν=++∑ (3)由于i 01ξ<≤,故i ln 0ξ≤。

定义i i u =-ln 0ξ≥,则方程3可以写成:Ki 0k ki i i k 1ln y =+ln x -u ββν=+∑ 其中,i u 0≥为“无效率”项,反映产商i 距离效率前沿面的距离。

混合扰动项i i i ενμ=-分布不对称,使用OLS 估计不能估计无效率项i u 。

为了估计无效率项i u ,必须对i i νμ、的分布作出假设,并进行更有效率的MLE (最大似然估计)估计。

一般,无效率项的分布假设有如下几种:(1) 半正态分布(2) 截断正态分布(3) 指数分布在一般的论文中,使用的最多的是半正态分布随机前沿模型可以很容易地用于估计成本函数,经过与生产函数的随机前沿模型类似的推导可得:Ki 0y i k ki i i k 1ln c =+lny ln P +u βββν=++∑其中,i c 为产商i 的成本,i y 为产出,ki P 为要素K 的价格,i u 为无效率项,i ν为成本函数的随机冲击。

IntroductiontoEconometrics

9

我们需要关于低STR的学区是否具有较高测 试成绩的数值证据——问题是怎么做?

1. 比较低 STR 的学区和高 STR 学区的平均测试成绩(“估 计”)

2. 检验原假设:2 种学区的平均测试成绩相同对备择假设:

它们不同 (“假设检验”)

3. 估计高 STR 学区和低 STR 学区之间差异的区间 (“置 信区间”)

1 nlarge

Ysmall Ylarge = nsmall

Yi

i1

– nlarge

Yi

i1

= 657.4 – 650.0

= 7.4

该差异在现实意义下大吗?

• 学区间的标准差 = 19.1 • 测试成绩分布的 60P和 75PP百分位数之差为 667.6 – 659.4 =

8.2 • 这个差异是否大到足以让家长或者学校委员会讨论学校

3

数据类型

• 截面数据 • 时间序列数据 • 面板数据

4

本课程的学习内容:

• 利用观测数据估计因果效应的方法 • 用于解决其它目的一些工具,如利用时间序列进行预测 • 集中于应用 ——理论仅仅只是用于理解采用这些方法的

原因 • 在练习中得到一些回归分析的实际操作经验

5

实证问题: 班级规模和教育产出 • 政策涉及的问题: 每班减少 1 人对测试成绩(或者其它后 果的度量)的效应有多大?每班减少 8 人呢? • 我们必须利用数据找出答案(在没有数据的情况下有其 它任何方法回答这个问题吗?)

2

如何利用数据度量因果效应

• 理想的状况是进行一项试验 • 为了估计班级规模对标准化测试成绩影响应该做怎样 的试验?

• 但大部分的实际状况是我们只有观测(非试验)数据 • 教育的收益 • 香烟价格 • 货币政策

伍德里奇计量经济学导论第四版

15CHAPTER 3TEACHING NOTESFor undergraduates, I do not work through most of the derivations in this chapter, at least not in detail. Rather, I focus on interpreting the assumptions, which mostly concern the population. Other than random sampling, the only assumption that involves more than populationconsiderations is the assumption about no perfect collinearity, where the possibility of perfect collinearity in the sample (even if it does not occur in the population should be touched on. The more important issue is perfect collinearity in the population, but this is fairly easy to dispense with via examples. These come from my experiences with the kinds of model specification issues that beginners have trouble with.The comparison of simple and multiple regression estimates – based on the particular sample at hand, as opposed to their statistical properties – usually makes a strong impression. Sometimes I do not bother with the “partialling out” interpretation of multiple regression.As far as statistical properties, notice how I treat the problem of including an irrelevant variable: no separate derivation is needed, as the result follows form Theorem 3.1.I do like to derive the omitted variable bias in the simple case. This is not much more difficult than showing unbiasedness of OLS in the simple regression case under the first four Gauss-Markov assumptions. It is important to get the students thinking aboutthis problem early on, and before too many additional (unnecessary assumptions have been introduced.I have intentionally kept the discussion of multicollinearity to a minimum. This partly indicates my bias, but it also reflects reality. It is, of course, very important for students to understand the potential consequences of having highly correlated independent variables. But this is often beyond our control, except that we can ask less of our multiple regression analysis. If two or more explanatory variables are highly correlated in the sample, we should not expect to precisely estimate their ceteris paribus effects in the population.I find extensive treatments of multicollinearity, where one “tests” or somehow “solves” the multicollinearity problem, to be misleading, at best. Even the organization of some texts gives the impression that imperfect multicollinearity is somehow a violation of the Gauss-Markovassumptions: they include multicollinearity in a chapter or part of the book devoted to “violation of the basic assumptions,” or something like that. I have noticed that master’s students who have had some undergraduate econometrics are often confused on the multicollinearity issue. It is very important that students not confuse multicollinearity among the included explanatory variables in a regression model with the bias caused by omitting an important variable.I do not prove the Gauss-Markov theorem. Instead, I emphasize its implications. Sometimes, and certainly for advanced beginners, I put a special case of Problem 3.12 on a midterm exam, where I make a particular choice for the function g (x . Rather than have the students directly 课后答案网ww w.kh d aw .c om16compare the variances, they should appeal to the Gauss-Markov theorem for the superiority of OLS over any other linear, unbiased estimator.SOLUTIONS TO PROBLEMS3.1 (i Yes. Because of budget constraints, it makes sense that, the more siblings there are in a family, the less education any one child in the family has. To find the increase in the number of siblings that reduces predicted education by one year, we solve 1 = .094(Δsibs , so Δsibs = 1/.094 ≈ 10.6.(ii Holding sibs and feduc fixed, one more year of mother’s education implies .131 years more of predicted education. So if a mother has four more years of education, her son is predicted to have about a half a year (.524 more years of education. (iii Since the number of siblings is the same, but meduc and feduc are both different, the coefficientson meduc and feduc both need to be accounted for. The predicted difference in education between B and A is .131(4 + .210(4 = 1.364.3.2 (i hsperc is defined so that the smaller it is, the lower the student’s standing in high school. Everything else equal, the worse the student’s standing in high school, the lower is his/her expected college GPA. (ii Just plug these values into the equation:n colgpa= 1.392 − .0135(20 + .00148(1050 = 2.676.(iii The difference between A and B is simply 140 times the coefficient on sat , because hsperc is the same for both students. So A is predicted to have ascore .00148(140 ≈ .207 higher.(iv With hsperc fixed, n colgpaΔ = .00148Δsat . Now, we want to find Δsat such that n colgpaΔ = .5, so .5 = .00148(Δsat or Δsat = .5/(.00148 ≈ 338. Perhaps not surprisingly, a large ceteris paribus difference in SAT score – almost two and one-half standard deviations – is needed to obtain a predicted difference in college GPA or a half a point.3.3 (i A larger rank for a law school means that the school has less prestige; this lowers starting salaries. For example, a rank of 100 means there are 99 schools thought to be better.课后答案网ww w.kh d aw .c om17(ii 1β > 0, 2β > 0. Both LSAT and GPA are measures of the quality of the entering class. No matter where better students attend law school, we expect them to earn more, on average. 3β, 4β > 0. The numbe r of volumes in the law library and the tuition cost are both measures of the school quality. (Cost is less obvious than library volumes, but should reflect quality of the faculty, physical plant, and so on. (iii This is just the coefficient on GPA , multiplied by 100: 24.8%. (iv This is an elasticity: a one percent increase in library volumes implies a .095% increase in predicted median starting salary, other things equal. (v It is definitely better to attend a law school with a lower rank. If law school A has a ranking 20 less than law school B, the predicted difference in starting salary is 100(.0033(20 = 6.6% higher for law school A.3.4 (i If adults trade off sleep for work, more work implies less sleep (other things equal, so 1β < 0. (ii The signs of 2β and 3β are not obvious, at least to me. One could argue that more educated people like to get more out of life, and so, other things equal,they sleep less (2β < 0. The relationship between sleeping and age is more complicated than this model suggests, and economists are not in the best position to judge such things.(iii Since totwrk is in minutes, we must convert five hours into minutes: Δtotwrk = 5(60 = 300. Then sleep is predicted to fall by .148(300 = 44.4 minutes. For a week, 45 minutes less sleep is not an overwhelming change. (iv More education implies less predicted time sleeping, but the effect is quite small. If we assume the difference between college and high school is four years, the college graduate sleeps about 45 minutes less per week, other things equal. (v Not surprisingly, the three explanatory variables explain only about 11.3% of the variation in sleep . One important factor in the error term is general health. Another is marital status, and whether the person has children. Health (however we measure that, marital status, and number and ages of children would generally be correlated with totwrk . (For example, less healthy people would tend to work less.3.5 Conditioning on the outcomes of the explanatory variables, we have 1E(θ =E(1ˆβ + 2ˆβ = E(1ˆβ+ E(2ˆβ = β1 + β2 = 1θ.3.6 (i No. By definition, study + sleep + work + leisure = 168. Therefore, if we change study , we must change at least one of the other categories so that the sum is still 168. 课后答案网ww w.kh d aw .c om18(ii From part (i, we can write, say, study as a perfect linear function of the otherindependent variables: study = 168 − sleep − work − leisure . This holds for every observation, so MLR.3 violated. (iii Simply drop one of the independent variables, say leisure :GPA = 0β + 1βstudy + 2βsleep + 3βwork + u .Now, for example, 1β is interpreted as the change in GPA when study increases by one hour, where sleep , work , and u are all held fixed. If we are holding sleep and work fixed but increasing study by one hour, then we must be reducing leisure by one hour. The other slope parameters have a similar interpretation.3.7 We can use Table 3.2. By definition, 2β > 0, and by assumption, Corr(x 1,x 2 < 0.Therefore, there is a negative bias in 1β: E(1β < 1β. This means that, on average across different random samples, the simple regression estimator underestimates the effect of thetraining program. It is even possible that E(1β is negative even though 1β > 0.3.8 Only (ii, omitting an important variable, can cause bias, and this is true only when the omitted variable is correlated with the included explanatory variables. The homoskedasticity assumption, MLR.5, played no role in showing that the OLS estimators are unbiased.(Homoskedasticity was used to o btain the usual variance formulas for the ˆjβ. Further, the degree of collinearity between the explanatory variables in the sample, even if it is reflected in a correlation as high as .95, does not affect the Gauss-Markov assumptions. Only if there is a perfect linear relationship among two or more explanatory variables is MLR.3 violated.3.9 (i Because 1x is highly correlated with 2x and 3x , and these latter variables have largepartial effects on y , the simple and multiple regression coefficients on 1x can differ by largeamounts. We have not done this case explicitly, but given equation (3.46 and the discussion with a single omitted variable, the intuition is pretty straightforward.(ii Here we would expect 1β and 1ˆβ to be similar (subject, of course, to what we mean by “almost uncorrelated”. The amount of correlation between 2x and 3x does not directly effect the multiple regression estimate on 1x if 1x is essentially uncorrelated with 2x and 3x .(iii In this case we are (unnecessarily introducing multicollinearity into the regression: 2x and 3x have small partial effects on y and yet 2x and 3x are highly correlated with 1x . Adding2x and 3x like increases the standard error of the coefficient on 1x substantially, so se(1ˆβis likely to be much larger than se(1β . 课后答案网ww w.kh d aw .c om19(iv In this case, adding 2x and 3x will decrease the residual variance without causingmuch collinearity (because 1x is almost uncorrelated with 2x and 3x , so we should see se(1ˆβ smaller than se(1β. The amount of correlation between 2x and 3x does not directly affect se(1ˆβ.3.10 From equation (3.22 we have111211ˆ,ˆni ii ni i r yr β===∑∑where the 1ˆi rare defined in the problem. As usual, we must plug in the true model for y i : 1011223311211ˆ(.ˆni i i i ii ni i r x x x u r βββββ==++++=∑∑The numerator of this expression simplifies because 11ˆni i r=∑ = 0, 121ˆni i i r x =∑ = 0, and 111ˆni i i r x =∑ = 211ˆni i r =∑. These all follow from the fact that the 1ˆi rare the residuals from the regression of 1i x on 2i x : the 1ˆi rhave zero sample average and are uncorrelated in sample with 2i x . So the numerator of 1βcan be expressed as2113131111ˆˆˆ.n n ni i i i i i i i rr x r u ββ===++∑∑∑Putting these back over the denominator gives 13111113221111ˆˆ.ˆˆnni i ii i nni i i i r x rur r βββ=====++∑∑∑∑课后答案网ww w.kh d aw .c om20Conditional on all sample values on x 1, x 2, and x 3, only the last term is random due to its dependence on u i . But E(u i = 0, and so131113211ˆE(=+,ˆni i i ni i r xr βββ==∑∑which is what we wanted to show. Notice that the term multiplying 3β is the regressioncoefficient from the simple regression of x i 3 on 1ˆi r.3.11 (i 1β < 0 because more pollution can be expected to lower housing values; note that 1β isthe elasticity of price with respect to nox . 2β is probably positive because rooms roughlymeasures the size of a house. (However, it does not allow us to distinguish homes where each room is large from homes where each room is small. (ii If we assume that rooms increases with quality of the home, then log(nox and rooms are negatively correlated when poorer neighborhoods have more pollution, something that is often true. We can use Ta ble 3.2 to determine the direction of the bias. If 2β > 0 andCorr(x 1,x 2 < 0, the simple regression estimator 1βhas a downward bias. But because 1β < 0, this means that the simple regression, on average, overstates the importance of pollution. [E(1β is more negative than 1β.] (iii This is what we expect from the typical sample based on our analysis in part (ii. The simple regression estimate, −1.043, is more negative (larger in magnitude than the multiple regression estimate, −.718. As those estimates are only for one sample, we can never know which is closer to 1β. But if this is a “typical” sample, 1β is closer to −.718.3.12 (i For notational simplicity, define s zx = 1(;ni i i z z x =−∑ this is not quite the samplecovariance between z and x because we do not divide by n – 1, but we are only using it tosimplify notation. Then we can write 1β as11(.niii zxz z ys β=−=∑This is clearly a linear function of the y i : take the weights to be w i = (z i −z /s zx . To show unbiasedness, as usual we plug y i = 0β + 1βx i + u i into this equation, and simplify: 课后答案网w w w .k h d aw .c o m21 11 1 011 111(( (((n ii i i zxnni zx i ii i zxniii zxz z x u s z z s z z u s zz u s ββββββ====−++=−++−=−=+∑∑∑∑where we use the fact that 1(ni i z z =−∑ = 0 always. Now s zx is a function of the z i and x i and theexpected value of each u i is zero conditional on all z i and x i in the sample. Therefore, conditional on these values,1111(E(E(niii zxz z u s βββ=−=+=∑because E(u i = 0 for all i . (ii From the fourth equation in part (i we have (again conditional on the z i and x i in the sample,2111222212Var ((Var(Var((n ni i i i i i zx zxnii zxz z u z z u s s z z s βσ===⎡⎤−−⎢⎥⎣⎦==−=∑∑∑because of the homoskedasticit y assumption [Var(u i = σ2 for all i ]. Given the definition of s zx , this is what we wanted to show.课后答案网ww w.kh d aw .c om22(iii We know that Var(1ˆβ = σ2/21[(].ni i x x =−∑ Now we can rearrange the inequality in the hint, drop x from the sample covariance, and cancel n -1everywhere, to get 221[(]/ni zx i z z s =−∑ ≥211/[(].ni i x x =−∑ When we multiply through by σ2 we get Var(1β ≥ Var(1ˆβ, which is what we wanted to show.3.13 (i The shares, by definition, add to one. If we do not omit one of the shares then the equation would suffer from perfect multicollinearity. The parameters would not have a ceteris paribus interpretation, as it is impossible to change one share while holding all of the other shares fixed. (ii Because each share is a proportion (and can be at most one, when all other shares are zero, it makes little sense to increase share p by one unit. If share p increases by .01 – which is equivalent to a one percentage point increase in the share of property taxes in total revenue – holding share I , share S , and the other factorsfixed, then growth increases by 1β(.01. With the other shares fixed, the excluded share, share F , must fall by .01 when share p increases by .01.SOLUTIONS TO COMPUTER EXERCISESC3.1 (i Prob ably 2β > 0, as more income typically means better nutrition for the mother and better prenatal care. (ii On the one hand, an increase in income generally increases the consumption of a good, and cigs and faminc could be positively correlated. On the other, family incomes are also higher for families with more education, and more education and cigarette smoking tend to benegatively correlated. The sample correlation between cigs and faminc is about −.173, indicating a negative correlation.(iii The regressions without and with faminc aren 119.77.514bwghtcigs =−21,388,.023n R ==and n 116.97.463.093bwghtcigs faminc =−+21,388,.030.n R ==课后答案网ww w.kh d aw .c om23The effect of cigarette smoking is slightly smaller when faminc is added to the regression, but the difference is not great. This is due to the fact that cigs and faminc are not very correlated, and the coefficient on faminc is practically small. (The variable faminc is measured in thousands, so $10,000 more in 1988 income increases predicted birth weight by only .93 ounces.C3.2 (i The estimated equation isn 19.32.12815.20price sqrft bdrms =−++288,.632n R ==(ii Holding square footage constant, n price Δ = 15.20 ,bdrms Δ and so n price increases by 15.20, which means $15,200.(iii Now n price Δ = .128sqrft Δ + 15.20bdrms Δ = .128(140 + 15.20 = 33.12, or $33,120. Because the size of the house is increasing, this is a much larger effect than in (ii. (iv About 63.2%. (v The predicted price is –19.32 + .128(2,438 + 15.20(4 = 353.544, or $353,544. (vi From part (v, the estimated value of the home based only on square footage and number of bedrooms is $353,544. The actual selling price was $300,000, which suggests the buyer underpaid by some margin. But, of course, there are many other features of a house (some that we cannot even measure that affect price, and we have not controlled for these.C3.3 (i The constant elasticity equation isn log( 4.62.162log(.107log(salary sales mktval =++ 2177,.299.n R ==(ii We cannot include profits in logarithmic form because profits are negative for nine of the companies in the sample. When we add it in levels form we getn log( 4.69.161log(.098log(.000036salary sales mktval profits =+++2177,.299.n R ==The coefficient on profits is very small. Here, profits are measured in millions, so if profits increase by $1 billion, which means profits Δ = 1,000 – a huge change – predicted salaryincreases by about only 3.6%. However, remember that we are holding sales and market value fixed.课后答案网ww w.kh d aw .c om24Together, these variables (and we could drop profits without losing anything explain almost 30% of the sample variation in log(salary . This is certainly not “most” of the variation.(iii Adding ceoten to the equation givesn log( 4.56.162log(.102log(.000029.012salary sales mktval profits ceoten =++++2177,.318.n R ==This means that one more year as CEO increases predicted salary by about 1.2%. (iv The sample correlation between log(mktval and profits is about .78, which is fairly high. As we know, this causes no bias in the OLS estimators, although it can cause their variances to be large. Given the fairly substantial correlation between market value andfirm profits, it is not too surprising that the latter adds nothing to explaining CEO salaries. Also, profits is a short term measure of how the firm is doing while mktval is based on past, current, and expected future profitability.C3.4 (i The minimum, maximum, and average values for these three variables are given in the table below:Variable Average Minimum Maximum atndrte priGPA ACT 81.71 2.59 22.516.25 .86131003.93 32(ii The estimated equation isn 75.7017.26 1.72atndrtepriGPA ACT =+− n = 680, R 2 = .291.The intercept means that, for a student whose prior GPA is zero and ACT score is zero, the predicted attendance rate is 75.7%. But this is clearly not an interesting segment of thepopulation. (In fact, there are no students in the college population with priGPA = 0 and ACT = 0, or with values even close to zero. (iii The coefficient on priGPA means that, if a student’s prior GPA is one point higher (say, from 2.0 to 3.0, the attendance rate is about 17.3 percentage points higher. This holds ACT fixed. The negative coefficient on ACT is, perhaps initially a bit surprising. Five more points on the ACT is predicted to lower attendance by 8.6 percentage points at a given level of priGPA . As priGPAmeasures performance in college (and, at least partially, could reflect, past attendance rates, while ACT is a measure of potential in college, it appears that students that had more promise (which could mean more innate ability think they can get by with missing lectures. 课后答案网ww w.kh d aw .c om(iv We have atndrte = 75.70 + 17.267(3.65 –1.72(20 ≈ 104.3. Of course, a student cannot have higher than a 100% attendance rate. Getting predictions like this is always possible when using regression methods for dependent variables with natural upper or lower bounds. In practice, we would predict a 100% attendance rate for this student. (In fact, this student had an actual attendance rate of 87.5%. (v The difference in predicted attendance rates for A and B is 17.26(3.1 − 2.1 − (21 − 26 = 25.86. C3.5 The regression of educ on exper and tenure yields n = 526, R2 = .101. ˆ Now, when we regres s log(wage on r1 we obtain ˆ log( wage = 1.62 + .092 r1 n = 526, R2 = .207. (ii The slope coefficientfrom log(wage on educ is β1 = .05984. ˆ ˆ (iv We have β1 + δ 1 β 2 = .03912 +3.53383(.00586 ≈ .05983, which is very close to .05984; the small difference is due to rounding error. C3.7 (i The results of the regression are math10 = −20.36 + 6.23log(expend − .305 lnchprg 课 (iii The slope coefficients from log(wage on educ and IQ are ˆ = .03912 and β = .00586, respectively. ˆ β1 2 后答案 C3.6 (i The slope coefficient from the regression IQ on educ is (rounded to five decimal places δ1 = 3.53383. n = 408, R2 = .180. 25 This edition is intended for use outside of the U.S. only, with content that may be different from the U.S. Edition. This may not be resold, copied, or distributed without the prior consent of the publisher. 网ˆ As expected, the coefficient on r1 in the second regression is identical to the coefficient on educ in equation (3.19. Notice that the R-squared from the above regression is below that in (3.19. ˆ In effect, the regression of log(wage on r1 explains log(wage using only the part of educ that is uncorrelated with exper and tenure; separate effects of exper and tenure are not included. ww w. kh da w. co m ˆ educ = 13.57 − .074 exper + .048 ten ure + r1 .The signs of the estimated slopes imply that more spending increases the pass rate (holding lnchprg fixed and a higher poverty rate (proxied well by lnchprg decreases the pass rate (holding spending fixed. These are what we expect. (ii As usual, the estimated intercept is the predicted value of the dependent variable when all regressors are set to zero. Setting lnchprg = 0 makes sense, as there are schools with low poverty rates. Setting log(expend = 0 does not make sense, because it is the same as setting expend = 1, and spending is measured in dollars per student. Presumably this is well outside any sensible range. Not surprisingly, the prediction of a −20 pass rate is nonsensical. (iii The simple regression results are failing to account for the poverty rate leads to an overestimate of the effect of spending. C3.8 (i The average of prpblck is .113 with standarddeviation .182; the average of income is 47,053.78 with standard deviation 13,179.29. It is evident that prpblck is a proportion and that income is measured in dollars. (ii The results from the OLS regression are psoda = .956 + .115 prpblck + .0000016 income 后 If, say, prpblck increases by .10 (ten percentage points, the price of soda is estimated toincrease by .0115 dollars, or about 1.2 cents. While this does not seem large, there are communities with no black population and others that are almost all black, in which case the difference in psoda is estimated to be almost 11.5 cents. (iii The simple regression estimate on prpblck is .065, so the simple regression estimate is actually lower. This is because prpblck and income are negatively correlated (-.43 and income has a positive coefficient in the multiple regression. (iv To get a constant elasticity, income should be in logarithmic form. I estimate the constant elasticity model: 26 This edition is intended for use outside of the U.S. only, with content that may be different from the U.S. Edition. This may not be resold, copied, or distributed without the prior consent of the publisher. 课答案 n = 401, R2 = .064. 网ww ˆ (v We can use equation (3.23. Because Corr(x1,x2 < 0, which means δ1 < 0 , and β 2 < 0 , ˆ the simple regression estimate, β , is larger than the multiple regression estimate, β . Intuitively, 1 w. kh (iv The sample correl ation between lexpend and lnchprg is about −.19 , which means that, on average, high schools with poorer students spent less per student. This makes sense, especially in 1993 in Michigan, where school funding was essentially determined by local property tax collections. da w. n = 408, R2 = .030 and the estimated spending effect is larger than it was in part (i –almost double. co 1 m math10 = −69.34 + 11.16 log(expendlog( psoda = −.794 + .122 prpblck + .077 log(income n = 401, R2 = .068. If prpblck increases by .20, log(psoda is estimated to increase by .20(.122 = .0244, or about 2.44 percent. ˆ (v β prpblck falls to about .073 when prppov is added to the regression. (vi The correlation is about −.84 , which makes sense because poverty rates are determined by income (but not directly in terms of median income. (vii There is no argument that they are highly correlated, but we are using them simply as controls to determine if the is price discrimination against blacks. In order to isolate the pure discrimination effect, we need to control for as many measures of income as we can; including both variables makes sense. C3.9 (i The estimated equation is (iv The estimated equation is gift = −7.33 + 1.20 mailsyear − .261 giftlast + 16.20 propresp + .527 avggift Aft er controlling for the average past gift level, the effect of mailings becomes even smaller: 1.20 guilders, or less thanhalf the effect estimated by simple regression. (v After controlling for the average of past gifts – which we can view as measuring the “typical” generosity of the person and is positively related to the current gift level – we find that the current gift amount is negatively related to the most recent gift. A negative relationship makes some sense, as people might follow a large donation with a smaller one. 27 This edition is intended for use outside of the U.S. only, with content that may be different from the U.S. Edition. This may not be resold, copied, or distributed without the prior consent of the publisher. 课 n = 4,268, R 2 = .2005 后 (iii Because propresp is a proportion, it makes little sense to increase it by one. Such an increase can happen only if propresp goes from zero to one. Instead, consider a .10 increase in propresp, which means a 10 percentage point increase. Then, gift i s estimated to be 15.36(.1 ≈ 1.54 guilders higher. 答案 (ii Holding giftlast and propresp fixed, one more mailing per year is estimated to increase gifts by 2.17 guilders. The simple regression estimate is 2.65, so the multiple regression estimate is somewhat smaller. Remember, the simple regression estimate holds no other factors fixed. 网 ww The R-squared is now about .083, compared with about .014 for the simple regression case. Therefore, the variables giftlast and propresp help to explain significantly more variation in gifts in the sample (although still just over eight percent. w. n = 4,268, R 2= .0834 kh gift = −4.55 + 2.17 mailsyear + .0059 giftlast + 15.36 propresp da w. co m。

《孟德尔随机化研究指南》中英文版

《孟德尔随机化研究指南》中英文版全文共3篇示例,供读者参考篇1Randomized research is a vital component of scientific studies, allowing researchers to investigate causal relationships between variables and make accurate inferences about the effects of interventions. One of the most renowned guides for conducting randomized research is the "Mendel Randomization Research Guide," which provides detailed instructions and best practices for designing and implementing randomized controlled trials.The Mendel Randomization Research Guide offers comprehensive guidance on all aspects of randomized research, from study design and sample selection to data analysis and interpretation of results. It emphasizes the importance of randomization in reducing bias and confounding effects, thus ensuring the validity and reliability of study findings. With clear and practical recommendations, researchers can feel confident in the quality and rigor of their randomized research studies.The guide highlights the key principles of randomization, such as the use of random assignment to treatment groups, blinding of participants and researchers, and intent-to-treat analysis. It also discusses strategies for achieving balance in sample characteristics and minimizing the risk of selection bias. By following these principles and guidelines, researchers can maximize the internal validity of their studies and draw accurate conclusions about the causal effects of interventions.In addition to the technical aspects of randomized research, the Mendel Randomization Research Guide also addresses ethical considerations and practical challenges that researchers may face. It emphasizes the importance of obtaining informed consent from participants, protecting their privacy and confidentiality, and ensuring the safety and well-being of study subjects. The guide also discusses strategies for overcoming common obstacles in randomized research, such as recruitment and retention issues, data collection problems, and statistical challenges.Overall, the Mendel Randomization Research Guide is a valuable resource for researchers looking to improve the quality and validity of their randomized research studies. By following its recommendations and best practices, researchers can conductstudies that produce reliable and actionable findings, advancing scientific knowledge and contributing to evidence-based decision making in various fields.篇2Mendel Randomization Study GuideIntroductionMendel Randomization Study Guide is a comprehensive and informative resource for researchers and students interested in the field of Mendel randomization. This guide provides anin-depth overview of the principles and methods of Mendel randomization, as well as practical advice on how to design and conduct Mendel randomization studies.The guide is divided into several sections, each covering a different aspect of Mendel randomization. The first section provides a brief introduction to the history and background of Mendel randomization, tracing its origins to the work of Gregor Mendel, the father of modern genetics. It also discusses the theoretical foundations of Mendel randomization and its potential applications in causal inference.The second section of the guide focuses on the methods and techniques used in Mendel randomization studies. This includesa detailed explanation of how Mendel randomization works, as well as guidelines on how to select instrumental variables and control for potential confounders. It also discusses the strengths and limitations of Mendel randomization, and provides practical tips on how to deal with common challenges in Mendel randomization studies.The third section of the guide is dedicated to practical considerations in Mendel randomization studies. This includes advice on how to design a Mendel randomization study, collect and analyze data, and interpret the results. It also provides recommendations on how to report Mendel randomization studies and publish research findings in scientific journals.In addition, the guide includes a glossary of key terms and concepts related to Mendel randomization, as well as a list of recommended readings for further study. It also includes case studies and examples of Mendel randomization studies in practice, to illustrate the principles and techniques discussed in the guide.ConclusionIn conclusion, the Mendel Randomization Study Guide is a valuable resource for researchers and students interested in Mendel randomization. It provides a comprehensive overview ofthe principles and methods of Mendel randomization, as well as practical advice on how to design and conduct Mendel randomization studies. Whether you are new to Mendel randomization or looking to deepen your understanding of the field, this guide is an essential reference for anyone interested in causal inference and genetic epidemiology.篇3"Guide to Mendelian Randomization Studies" English VersionIntroductionMendelian randomization (MR) is a method that uses genetic variants to investigate the causal relationship between an exposure and an outcome. It is a powerful tool that can help researchers to better understand the underlying mechanisms of complex traits and diseases. The "Guide to Mendelian Randomization Studies" provides a comprehensive overview of MR studies and offers practical guidance on how to design and carry out these studies effectively.Chapter 1: Introduction to Mendelian RandomizationThis chapter provides an overview of the principles of Mendelian randomization, including the assumptions andlimitations of the method. It explains how genetic variants can be used as instrumental variables to estimate the causal effect of an exposure on an outcome, and outlines the key steps involved in conducting an MR study.Chapter 2: Choosing Genetic InstrumentsIn this chapter, the guide discusses the criteria for selecting appropriate genetic instruments for Mendelian randomization. It covers issues such as the relevance of the genetic variant to the exposure of interest, the strength of the instrument, and the potential for pleiotropy. The chapter also provides practical tips on how to search for suitable genetic variants in public databases.Chapter 3: Data Sources and ValidationThis chapter highlights the importance of using high-quality data sources for Mendelian randomization studies. It discusses the different types of data that can be used, such asgenome-wide association studies and biobanks, and offers advice on how to validate genetic instruments and ensure the reliability of the data.Chapter 4: Statistical MethodsIn this chapter, the guide explains the various statistical methods that can be used to analyze Mendelian randomization data. It covers techniques such as inverse variance weighting, MR-Egger regression, and bi-directional Mendelian randomization, and provides guidance on how to choose the most appropriate method for a given study.Chapter 5: Interpretation and ReportingThe final chapter of the guide focuses on the interpretation and reporting of Mendelian randomization results. It discusses how to assess the strength of causal inference, consider potential biases, and communicate findings effectively in research papers and presentations.ConclusionThe "Guide to Mendelian Randomization Studies" is a valuable resource for researchers who are interested in using genetic data to investigate causal relationships in epidemiological studies. By following the guidance provided in the guide, researchers can enhance the rigor and validity of their Mendelian randomization studies and contribute to a better understanding of the determinants of complex traits and diseases.。

《条件随机场》课件

01

•·

02

基于共轭梯度的优化算法首先使用牛顿法确定一个大致的 参数搜索方向,然后在该方向上进行梯度下降搜索,以找 到最优的参数值。这种方法结合了全局和局部搜索的优势 ,既具有较快的收敛速度,又能避免局部最优解的问题。

03

共轭梯度法需要计算目标函数的二阶导数(海森矩阵), 因此计算量相对较大。同时,该方法对初始值的选择也有 一定的敏感性。在实际应用中,需要根据具体情况选择合 适的优化算法。

高效存储

研究如何利用高效存储技术(如分布式文件系统、NoSQL数据库 等)存储和处理大规模数据。

06

结论与展望

条件随机场的重要性和贡献

01

克服了传统机器学习方法对特征工程的依赖,能够 自动学习特征表示。

02

适用于各种自然语言处理和计算机视觉任务,具有 广泛的应用前景。

03

为深度学习领域带来了新的思路和方法,推动了相 关领域的发展。

概念

它是一种有向图模型,通过定义一组条件独立假设,将观测 序列的概率模型分解为一系列局部条件概率的乘积,从而简 化模型计算。

条件随机场的应用场景

序列标注

在自然语言处理、语音识别、生物信 息学等领域,CRF常用于序列标注任 务,如词性标注、命名实体识别等。

结构化预测

在图像识别、机器翻译、信息抽取等 领域,CRF可用于结构化预测任务, 如图像分割、句法分析、关系抽取等 。

04

条件随机场的实现与应用

自然语言处理领域的应用

词性标注

条件随机场可以用于自然语言处理中 的词性标注任务,通过标注每个单词 的词性,有助于提高自然语言处理的 准确性和效率。

句法分析

条件随机场也可以用于句法分析,即 对句子中的词语进行语法结构分析, 确定词语之间的依存关系,有助于理 解句子的含义和生成自然语言文本。

随机微分方程的英文

随机微分方程的英文Random Differential EquationsIntroduction:Definition:Importance of Random Differential Equations:Solving Random Differential Equations:Solving random differential equations is a challenging task due to the uncertainty associated with the variables or parameters. Traditional methods for solving deterministic differential equations may not be applicable directly due to the randomness involved. However, various techniques have been developed to tackle these equations efficiently:1. Numerical Methods: Numerical methods, such as Monte Carlo simulations or stochastic differential equations, can be employed to solve random differential equations. These methods use random sampling techniques to approximate the solution of the equation. Monte Carlo simulations generate a large number of random samples and evaluate the equation for each sample, providing an approximation of the solution. Stochastic differential equations, on the other hand, incorporate the randomness directly into the differential equation itself.3. Stochastic Calculus: Stochastic calculus is a branch of mathematics that deals with calculus-based operations involving random processes. It provides a rigorous mathematical framework for solving random differential equations. Stochastic calculus introduces the concept of stochastic integrals, which allows for the integration of stochastic processes. This enables the application of traditional calculus techniques to stochastic equations, leading to the development of powerful methods for solving random differential equations.Applications:Random differential equations find applications in various scientific and engineering fields. Some notable examples include:3. Control Systems: Random differential equations are employed in control theory to model and design control systems that are robust to uncertainties. By considering the randomness in the system parameters, engineers can develop controllers that are more resilient to variations in the environment or disturbances.Conclusion:。

ConditionalLogitModel解读

实际操作之模型回归

• Stata中使用条件logit模型的回归命令语句如 下所示: • clogit y x1 x2 …[if] [in] [weight] , group(varname) [options] • 其中,clogit表示对y、x进行条件logit模型回 归,if和in表示回归的条件和范围,weight表 示观测值的权重值,group设定个体识别变 量

条件logit模型(conditional logit model,CL)是 常用的离散选择模型,IIA假设能令CL的参 数易于估计和被广泛使用,但在很多离散选 择问题上,如患者择医购药、毕业生择业、 居民就餐和出行等,其备择项可能是相关的, 即IIA假设不成立。若此时坚持使用CL予以 分析,其参数估计必将产生严重的不一致性。 为此,McFadden构建了嵌套logit模型(nested logit model,NL),该模型是CL的推广,不要求 各备择项服从IIA假设。(该模型假定个人 的选择能够按照一种特定的顺序进行)

模型的使用领域

• 这些模型可以解释价格变化、通过改进而 获得的可能性或者人口构成的变动是如何 影响使用不同交通方式所占比例的。

模型的使用领域

• 这些模型在其他领域也具有应用意义,比如 说对居住方式和居住地以及教育的选择等。 McFadden还将他自己的模型应用到对许多 社会问题的分析上,比如民用电力、电话服 务和为老年人所提供的住所等。

模型定义

• 根据条件概率可以定义条件logitபைடு நூலகம்型

实际操作

• 数据来自某统计资料关于研究初生婴儿体重的影响因素的统 计数据。命名数据文件为“lowbirth” • 数据中的变量有parid(个体识别变量),low(婴儿低体重, 若体重低则取值1,否则0),age(母亲的年龄),lowt(母亲 最近一个月的体重),smoke(母亲怀孕期间是否吸烟,若吸 烟为1,否则为0),ptd(母亲以前有早产经历,若有则1,反 之为0),ht(母亲高血压,若是则取值1,否则为0),ui(母亲是 否子宫敏感,若是则取值1,否取值0),race1(母亲是白种 人,若是则取值1,反之0),race2(母亲是黑种人,若是取 值1,反之0),race3(母亲是其他色种人,若是取值1,反 之取值0)。 • 模型中被解释变量是low,以上的解释变量均是婴儿妈妈的因素, 那么这些因素就是与选择特征变量,所以应该建立条件logit模 型进行回归。

条件随机场相关的方法

条件随机场相关的方法全文共四篇示例,供读者参考第一篇示例:条件随机场(Conditional Random Fields, CRF)是一种统计建模方法,常用于序列标注、自然语言处理和计算机视觉等领域。

CRF的主要优势是可以利用上下文信息进行建模,以及可以处理由于标签之间的依赖关系导致的标签歧义问题。

本文将介绍一些与条件随机场相关的方法,包括CRF的基本概念、CRF的训练和推断算法、以及CRF 在自然语言处理和计算机视觉中的应用。

一、CRF的基本概念CRF是一种概率图模型,用于对序列数据进行建模。

在CRF中,我们需要定义一个特征函数集合,每个特征函数表示输入序列和输出标签之间的依赖关系。

给定一个输入序列X和对应的输出标签序列Y,我们可以定义CRF的概率分布为:P(Y|X) = 1/Z(X) * exp(∑wi*fi(Y,X))其中Z(X)是规范化因子,使得条件概率分布P(Y|X)的所有可能取值的总和等于1;wi是特征函数fi的权重。

二、CRF的训练和推断算法CRF的训练过程通常使用最大似然估计或最大熵准则,通过利用训练数据集的标注信息来学习特征函数的权重。

CRF的推断过程通常使用近似推断算法,如维特比算法或前向-后向算法,来寻找给定输入序列X的最优输出标签序列Y。

三、CRF在自然语言处理中的应用在自然语言处理领域,CRF常用于词性标注、命名实体识别、句法分析等任务。

通过利用上下文信息和标签之间的依赖关系,CRF可以在这些任务中取得更好的性能。

四、CRF在计算机视觉中的应用条件随机场是一种强大的概率建模方法,可以用于序列标注、自然语言处理、计算机视觉等各种领域。

通过使用CRF,我们可以充分利用上下文信息和标签之间的依赖关系,从而提高模型的性能和泛化能力。

希望本文介绍的与条件随机场相关的方法能够对读者有所帮助。

第二篇示例:条件随机场(Conditional Random Field, CRF)是一种用于序列标注问题的概率模型,它在自然语言处理、计算机视觉、生物信息学等领域都有广泛的应用。

Conditionalindependence

Conditional independenceThese are two examples illustrating conditional independence. Each cell represents a possible outcome. The events R, B and Y are represented by the areas shaded red, blue and yellow respectively. And the probabilities of these events are shaded areas with respect to the total area. In both examples R and B are conditionally independent given Y because: \Pr(R \cap B \mid Y) = \Pr(R \mid Y)\Pr(B \mid Y)\,To see that this is the case,one needs to realise that Pr(R ∩ B | Y) is the probability of an overlap of R and B in the Y area. Since, in the picture on the left, there are two squares where R and B overlap within the Y area, and the Y area has twelve squares, Pr(R ∩ B | Y) = \tfrac{2}{12} =\tfrac{1}{6}. Similarly, Pr(R | Y) = \tfrac{4}{12} = \tfrac{1}{3} and Pr(B | Y) =\tfrac{6}{12} = \tfrac{1}{2}.but not conditionally independent given not Ybecause:\Pr(R \cap B \mid \text{not } Y) \not= \Pr(R \mid \mbox{not } Y)\Pr(B \mid\text{not } Y).\,In probability theory, two events R andB are conditionally independentgiven a third event Y precisely if theoccurrence or non-occurrence of R andthe occurrence or non-occurrence of Bare independent events in theirconditional probability distributiongiven Y . In other words, R and B areconditionally independent if and onlyif, given knowledge of whether Yoccurs, knowledge of whether R occursprovides no information on thelikelihood of B occurring, andknowledge of whether B occursprovides no information on thelikehood of R occurring.In the standard notation of probabilitytheory, R and B are conditionallyindependent given Yif and only ifor equivalently,Two random variables X and Y are conditionally independent given a third random variable Z if and only if they are independent in their conditional probability distribution given Z . That is, X and Y are conditionally independent given Z if and only if, given any value of Z , the probability distribution of X is the same for all values of Y and the probability distribution of Y is the same for all values of X .Two events R and B are conditionally independentgiven a σ-algebra Σ ifwhere denotes the conditional expectation of the indicator function of the event , , given the sigma algebra. That is,Two random variables X and Y are conditionally independent given a σ-algebra Σ if the above equation holds for all R in σ(X ) and B in σ(Y ).Two random variables X and Y are conditionally independent given a random variable W if they are independent given σ(W ): the σ-algebra generated by W. This is commonly written:This is read "X is independent of Y, given W"; the conditioning applies to the whole statement: "(X is independentof Y) given W".If W assumes a countable set of values, this is equivalent to the conditional independence of X and Y for the events of the form [W = w]. Conditional independence of more than two events, or of more than two random variables, is defined analogously.The following two examples show that X⊥Y neither implies nor is implied by X⊥Y | W. First, suppose W is 0 with probability 0.5 and 1 otherwise. When W = 0 take X and Y to be independent, each having the value 0 with probability 0.99, the value 1 otherwise. When W = 1, X and Y are again independent, but this time they take the value 1 with probability 0.99. Then X⊥Y | W. But X and Y are dependent, because Pr(X = 0) < Pr(X = 0|Y = 0). This is because Pr(X = 0) = 0.5, but if Y = 0 then it's very likely that W = 0 and thus that X = 0 as well, so Pr(X = 0|Y = 0) > 0.5. For the second example, suppose X⊥Y, each taking the values 0 and 1 with probability 0.5. Let W be the product X×Y. Then when W = 0, Pr(X = 0) = 2/3, but Pr(X = 0|Y = 0) = 1/2, so X ⊥ Y | W is false. This also an example of Explaining Away. See Kevin Murphy's tutorial [2] where X and Y take the values "brainy" and "sporty".Uses in Bayesian statisticsLet p be the proportion of voters who will vote "yes" in an upcoming referendum. In taking an opinion poll, one chooses n voters randomly from the population. For i = 1, ..., n, let Xi= 1 or 0 according as the i th chosen voter will or will not vote "yes".In a frequentist approach to statistical inference one would not attribute any probability distribution to p (unless the probabilities could be somehow interpreted as relative frequencies of occurrence of some event or as proportions ofsome population) and one would say that X1, ..., Xnare independent random variables.By contrast, in a Bayesian approach to statistical inference, one would assign a probability distribution to p regardless of the non-existence of any such "frequency" interpretation, and one would construe the probabilities as degrees of belief that p is in any interval to which a probability is assigned. In that model, the random variablesX 1, ..., Xnare not independent, but they are conditionally independent given the value of p. In particular, if a largenumber of the X s are observed to be equal to 1, that would imply a high conditional probability, given that observation, that p is near 1, and thus a high conditional probability, given that observation, that the next X to be observed will be equal to 1.Rules of conditional independenceA set of rules governing statements of conditional independence have been derived from the basic definition.[3][4] Note: since these implications hold for any probability space, they will still hold if considers a sub-universe by conditioning everything on another variable, say K. For example, would also mean that.Note: below, the comma can be read as , and thus can be visualized as a Venn Diagram.SymmetryDecompositionProof:•(meaning of )•(ignore variable by integrating it out)•repeat proof to show independence of X and B .Weak unionContractionContraction-weak-union-decomposition Putting the above three together, we have:IntersectionIf the probabilities of X, A, B are all positive, then the following also holds:References [1]To see that this is the case, one needs to realise that Pr(R ∩ B | Y ) is the probability of an overlap of R and B in the Y area. Since, in the pictureon the left, there are two squares where R and B overlap within the Y area, and the Y area has twelve squares, Pr(R ∩ B | Y ) == .Similarly, Pr(R | Y ) = = and Pr(B | Y ) = = .[2]http://people.cs.ubc.ca/~murphyk/Bayes/bnintro.html[3]Dawid, A. P. (1979). "Conditional Independence in Statistical Theory". Journal of the Royal Statistical Society Series B 41 (1): 1–31.MR0535541. JSTOR 2984718.[4]J Pearl, Causality: Models, Reasoning, and Inference, 2000, Cambridge University PressArticle Sources and Contributors4Article Sources and ContributorsConditional independence Source: /w/index.php?oldid=418113252 Contributors: 3mta3, Alansohn, AzaToth, Brighterorange, Btyner, Cesarth, Charles Matthews,Circeus, Citrus Lover, DGJM, Ddxc, Dominus, Duoduoduo, Epachamo, Fresheneesz, Gareth Owen, Giftlite, Jeff G., Mackseem, Melcombe, Michael Hardy, Ms2ger, Mtcv, Nasz, Neilc,Ninjagecko, Ogai, Oleg Alexandrov, Pr.elvis, Qwfp, Redrocket, Rkashuba, Splat2010, Tsirel, 31 anonymous editsImage Sources, Licenses and ContributorsImage:Conditional independence.svg Source: /w/index.php?title=File:Conditional_independence.svg License: Creative Commons Attribution-Sharealike 3.0,2.5,2.0,1.0 Contributors: Original uploader was AzaToth at en.wikipedia Later version(s) were uploaded by Ddxc at en.wikipedia.LicenseCreative Commons Attribution-Share Alike 3.0 Unported/licenses/by-sa/3.0/。

Introduction to Finite Fields and Their Applications

BULLETIN(New Series)OF THEAMERICAN MATHEMATICAL SOCIETYVolume36,Number1,January1999,Pages99–101S0273-0979(99)00768-5Finitefields,by Rudolf Lidl and Harald Niederreiter,Second edition,Cambridge University Press,1997,xiv+755pp.,$95.00,ISBN0-521-39231-4Finitefields arefields that have only afinite number of elements.The simplest examples are the rings of integers modulo a prime number p.The origins and history offinitefields can be traced back to the17th and18th centuries,but there, thesefields played only a minor role in the mathematics of the day.In more recent times,however,finitefields have assumed a much more fundamental role and in fact are of rapidly increasing importance because of practical applications in a wide variety of areas including information science.More generally,finitefields play vital roles in computer science,coding theory,cryptography,algebraic geometry,number theory and group theory as well as in a variety of areas of discrete mathematics.It unfortunately does not seem to be widely known in the mathematical commu-nity how importantfinitefields really are.They provide a truly beautiful meeting ground for good theoretical problems as well as very practical applications.Because of this interaction between theory and application,finitefields offer a fertile area where mathematicians,engineers and computer scientists can all work,each to the benefit of the others.The initial edition of this book was published by Addison-Wesley in1983and was thefirst book devoted solely tofinitefields;however,that edition was never reviewed in the Bulletin of the American Mathematical Society.Considering the immense impact of the original volume,which has often been called the Bible on finitefields,it is indeed important that a full review be written at this time.One point of clarification is that this current volume was listed by the new pub-lisher,Cambridge University Press,as a second edition unbeknown to the authors. This is misleading,as the current volume is just a reprint of the original version with some minor corrections.Since the publication of the original volume in1983,there has been an explosion offinitefield publications in both theoretical and applied aspects.Mathematical Reviews lists as appearing since1983more than700papers with the words“finite fields”in their titles,and since that time there have also been more than20books as well as5conference proceedings on the subject(see also D.Wan’s review in the A.M.S.Bulletin30(1994),284-290,of severalfinitefield related books).In addition,there is now an international conference on the theory and application of finitefields which has been held every two years since1991.In1995Academic Press began publication of a new research journal Finite Fields and Their Applications. These observations should help convince the reader thatfinitefields are indeed very important mathematical structures and that interest in them is growing rapidly.The authors have done a masterful job infirst digesting an enormous amount of material and then organizing it in an efficient way to make for a clear and readable treatise onfinitefields.There were very few errors or typos in the original edition and I suspect almost none in this second corrected edition.1991Mathematics Subject Classification.Primary11Txx;Secondary05Bxx,11B37,94A55, 94Bxx.c 1999American Mathematical Society99100BOOK REVIEWSWe very briefly summarize each of the chapter contents: 1.“Algebraic Foun-dations”is a review of some basic algebraic material with an emphasis on rings andfields;2.“Structure of Finite Fields”discusses bases,primitive elements,trace and norm functions,cyclotomic polynomials and Wedderburn’s theorem;3.“Poly-nomials over Finite Fields”considers the concept of order(or exponent)of poly-nomials,irreducible and primitive polynomials,linearized polynomials as well as various properties of binomials and trinomials;4.“Factorization of Polynomials”considers algorithms(Berlekamp’s for example)for the factorization of polynomi-als in a single indeterminate over smallfields,algorithms for factorization over largefields(where large means that the number of elements in thefield is sub-stantially larger than the degree of the polynomial to be factored)and methods of rootfinding;5.“Exponential Sums”provides a careful and detailed treatment of various kinds of exponential sums including Gauss,Jacobi and Kloosterman sums and gives proofs of Weil’s theorems for polynomial arguments;6.“Equations over Finite Fields”deals with the number of solutions to various types of equations overfinitefields,including quadratic and diagonal equations,and also discusses the elementary method of Stepanov;7.“Permutation Polynomials”provides criteria for and classes of permutation polynomials in one and several variables and dis-cusses groups of permutation polynomials;8.“Linear Recurring Sequences”givesa thorough discussion of the theory of linear recurring sequences overfinitefields;9.“Applications of Finite Fields”provides an introduction to coding theory and combinatorics including projective and affine planes and geometries,mutually or-thogonal latin squares,Hadamard matrices,block designs,difference sets and linear modular systems;10.“Tables”provides tables of logarithms and exponentials for hand calculations in smallfinitefields and lists of irreducible polynomials of small degrees over small primefields and a primitive polynomial of each degree n over thefield of p elements where p n<109with p<50.The Bibliography consists of160pages and approximately2,500references.This is a very complete bibliography through1983(the date of publication of thefirst edition)and as such it is one of the most valuable parts of the book.There is also an author index,a list of symbols,and a subject index.Other very valuable parts of the book are the detailed Notes given at the end of each chapter.In these notes the authors describe historical perspectives as well as provide a quick review of the literature related to that chapter’s material.In particular,they give brief statements of the main results of most of the references referred to in that chapter.In an effort to enhance the attractiveness of their monograph as a textbook, the authors have included numerous worked-out examples.Additionally,each of thefirst nine chapters contains a set of exercises that either illustrate the theory or provide extensions and alternative proofs of some of the results within that chapter. These exercises are well chosen and as such they could provide excellent homework problems.(For a more textbook-oriented version of this book,I refer to the related book by the authors entitled Introduction tofinitefields and their applications, Revised edition,Cambridge University Press,1994.)One could argue that various additional topics should have been included in the original volume.In his Mathematical Review86c:11106of the original volume, S.D.Cohen mentions several such omissions including functionfield theory,non-Desarguesian geometry,and cryptography.Another missing topic which is veryBOOK REVIEWS101 important for computational work is that offinitefield algorithms and their com-plexities.Of course,entire volumes could be written about each of these topics; thus the inclusion of all or even any of these topics would have made the current volume unmanageably large.This monograph has already become the standard reference onfinitefields;in-deed,it is referenced in nearly every paper related tofinitefields.The book is extremely valuable for the nonspecialist or the practitioner wanting to learn and work in the general area offinitefields and their applications.Moreover,because of its very extensive bibliography,it is also an excellent starting point for a literature search by someone well-versed infinitefield theory.Every college,university,and institute library needs a copy,and since,in my experience,the library copy is likely to be signed out when the book is needed,individuals should consider buying a personal copy.I predict it will be used many times.Gary L.MullenThe Pennsylvania State UniversityE-mail address:mullen@。

条件随机场模型及其应用

P(Y )

1 c(Yc ) Z c

其中,Z 是规范化因子,由下式给出:

Z c(Yc )

Y c

规范化因子保证 P(Y)构成了一个概率分布。函数 c(Yc ) 称为势函数。这里 要求势函数 c(Yc ) 是严格正的,通常定义为指数函数:

c(Yc ) exp{E(Yc )}

条件随机场模型介绍及其应用

1. 条件随机场模型介绍

条件随机域(场) (Conditional Random Fields) ,简称 CRF 或 CRFs,是一 种判别式的概率图模型。条件随机场是在给定随机变量 X 条件下,随机变量 Y 的马尔科夫随机场。原则上,条件随机场的图模型布局是可以任意给定的,但比 较常用的是定义在线性链上的特殊的条件随机场,称为线性链条件随机场。因为 其不论在训练、推论或是解码上,都存在效率较高的算法可供演算。 条件随机场最早由 John D. Lafferty 等[1]在 2001 年提出,结合了最大熵模型 和隐马尔可夫模型的特点,是一种概率无向图模型。它常用于序列标注等问题, 比如可以用于分词(Segmentation) 、词性标注(Part of Speech)和命名实体识别 (Named Entity Recognition)任务。一般序列分类问题常常采用隐马尔可夫模型 (HMM)[2],但隐马尔可夫模型中存在两个假设:输出独立性假设和马尔可夫 性假设。 其中, 输出独立性假设要求序列数据严格相互独立才能保证推导的正确 性, 而事实上大多数序列数据不能被表示成一系列独立事件。而条件随机场则使 用一种概率图模型, 具有表达长距离依赖性和交叠性特征的能力,能够较好地解 决标注(分类)偏置等问题的优点,而且所有特征可以进行全局归一化,能够求 得全局的最优解。

条件随机场

Numerical Analysis and Scientific Computing

Comments

Postprint version. Copyright ACM, 2001. This is the author's version of the work. It is posted here by permission of ACM for your personal use. Not for redistribution. The definitive version was published in Proceedings of the 18th International Conference on Machine Learning 2001 (ICML 2001), pages 282-289. Publisher URL: /citation.cfm?id=655813

University of Pennsylvania

ScholarlyCommons

Departmental Papers (CIS) Department of Computer & Information Science

6-28-2001

Conditional Random Fields: Probabilistic Models for Segmenting and Labeling Sequence Data

Postprint version. Copyright ACM, 2001. This is the author's version of the work. It is posted here by permission of ACM for your personal use. Not for redistribution. The definitive version was published in Proceedings of the 18th International Conference on Machine Learning 2001 (ICML 2001), pages 282-289. Publisher URL: /citation.cfm?id=655813 This paper is posted at ScholarlyCommons. /cis_papers/159 For more information, please contact repository@.

条件随机场教学文案

条件随机场概述

条件随机场模型是Lafferty于2001年,在最大熵模型和隐马尔科夫 模型的基础上,提出的一种判别式概率无向图学习模型,是一种用 于标注和切分有序数据的条件概率模型。

CRF最早是针对序列数据分析提出的,现已成功应用于自然语言处理 (Natural Language Processing,NLP) 、生物信息学、机器视觉及网 络智能等领域。

产生式模型: P (x, y): P(1, 0) = 1/2, P(1, 1) = 0, P(2, 0) = 1/4, P(2, 1) = 1/4.

判别式模型: P (y | x): P(0|1) = 1, P(1|1) = 0, P(0|2) = 1/2, P(1|2) = 1/2

两种模型比较:

P(yj)代表还没有训练数据前,yj拥有的初始概率。P(yj)常被称为 yj的先验概率(prior probability) ,它反映了我们所拥有的关于yj 是正确分类机会的背景知识,它应该是独立于样本的。

如果没有这一先验知识,那么可以简单地将每一候选类别赋予相 同的先验概率。不过通常我们可以用样例中属于yj的样例数|yj|比 上总样例数|D|来近似,即

是联合概率,指当已知类别为yj的条件下 ,看到样本x出现的概率。

若设

则

条件独立性: 在给定随机变量C时,a,b条件独立。 假定:在给定目标值 yj 时,x的属性值之间相互条件独立。

是后验概率,即给定数据样本x时yj成立的概率,而这正 是我们所感兴趣的。

P(yj|x )被称为Y的后验概率(posterior probability),因为它反 映了在看到数据样本x后yj成立的置信度。

A First Course in Probability

A First Course in ProbabilityIntroductionProbability theory is a branch of mathematics that deals with the study of randomness and uncertainty. It provides a framework for understanding and quantifying uncertainties in various fields, ranging from finance and economics to engineering and science. A First Course in Probability aims to introduce the fundamental concepts and techniques of probability theory and provide a solid foundation for further study in the subject.Basic Probability TheorySample Space and EventsIn probability theory, we start by defining a sample space, denoted by Ω, which is the set of all possible outcomes of an experiment. An event, denoted by A, is a subset of the sample space. The probability of an event is a real number between 0 and 1, representing the likelihood of that event occurring.The Calculus of ProbabilityThe basic operations of probability include union, intersection, and complement. Given two events A and B, the union of A and B, denoted by A ∪ B, consists of a ll outcomes that belong to either A or B. The intersection of A and B, denoted by A ∩ B, consists of all outcomes that belong to bothA and B. The complement of an event A, denoted by A’, consists of all outcomes that do not belong to A.The probability of the union of two events is given by the sum of their individual probabilities minus the probability of their intersection:P(A ∪ B) = P(A) + P(B) - P(A ∩ B)Conditional ProbabilityConditional probability measures the likelihood of an event A occurring given that another event B has already occurred. It is denoted by P(A|B) and is defined as:P(A|B) = P(A ∩ B) / P(B), where P(B) > 0IndependenceTwo events A and B are said to be independent if the occurrence of one event does not affect the probability of the other event. Mathematically, two events are independent if and only if:P(A ∩ B) = P(A) * P(B)Random VariablesA random variable is a function that assigns a real number to each outcome in the sample space. It provides a way to quantify the uncertainty associated with an experiment. Random variables can be discrete or continuous, depending onwhether they take on a countable or uncountable number of values, respectively.Probability DistributionsDiscrete Probability DistributionsIn the case of discrete random variables, the probability distribution can be defined by a probability mass function (PMF), which gives the probability of each possible value of the random variable. The PMF satisfies two properties: it must be non-negative for all values of the random variable, and the sum of the probabilities must equal 1.Examples of discrete probability distributions include the Bernoulli distribution, the binomial distribution, and the Poisson distribution.Continuous Probability DistributionsFor continuous random variables, the probability distribution is defined by a probability density function (PDF), which specifies the relative likelihood of the random variable taking on different values. The PDF must be non-negative, and the total area under the curve must equal 1.Examples of continuous probability distributions include the normal distribution, the exponential distribution, and the uniform distribution.Expectation and VarianceExpectationThe expectation of a random variable, denoted by E(X), is a measure of its average value. For discrete random variables, the expectation is calculated by summing the product of each possible value and its corresponding probability. For continuous random variables, the expectation is calculated by integrating the product of each value and its corresponding density over the entire range of values.VarianceThe variance of a random variable, denoted by Var(X), measures the spread or dispersion of its probability distribution. It quantifies how far the values of the random variable deviate from its expectation. The variance is calculated by taking the expectation of the squared difference between each value and the expectation.Central Limit TheoremThe central limit theorem states that the sum or average of a large number of independent and identically distributed random variables will be approximately normally distributed, regardless of the shape of the original distribution. This theorem has wide-ranging applications in statistics and allows us to make inferences about population parameters based on sample data.ConclusionA First Course in Probability provides a solid foundation in the fundamental concepts and techniques of probability theory. It covers basic probability theory, probability distributions, expectation and variance, and the central limit theorem. This course serves as a starting point for further study in the field of probability and its applications.。

条件随机场(Conditionalrandomfield,CRF)

条件随机场(Conditionalrandomfield,CRF)本⽂简单整理了以下内容:(⼀)马尔可夫随机场(Markov random field,⽆向图模型)简单回顾(⼆)条件随机场(Conditional random field,CRF)这篇写的⾮常浅,基于 [1] 和 [5] 梳理。

感觉 [1] 的讲解很适合完全不知道什么是CRF的⼈来⼊门。

如果有需要深⼊理解CRF的需求的话,还是应该仔细读⼀下⼏个英⽂的tutorial,⽐如 [4] 。

(⼀)马尔可夫随机场简单回顾概率图模型(Probabilistic graphical model,PGM)是由图表⽰的概率分布。

概率⽆向图模型(Probabilistic undirected graphical model)⼜称马尔可夫随机场(Markov random field),表⽰⼀个联合概率分布,其标准定义为:设有联合概率分布 P(V) 由⽆向图 G=(V, E) 表⽰,图 G 中的节点表⽰随机变量,边表⽰随机变量间的依赖关系。

如果联合概率分布 P(V) 满⾜成对、局部或全局马尔可夫性,就称此联合概率分布为概率⽆向图模型或马尔可夫随机场。

设有⼀组随机变量 Y ,其联合分布为 P(Y) 由⽆向图 G=(V, E) 表⽰。

图 G 的⼀个节点v\in V表⽰⼀个随机变量Y_v,⼀条边e\in E就表⽰两个随机变量间的依赖关系。

1. 成对马尔可夫性(pairwise Markov property)设⽆向图 G 中的任意两个没有边连接的节点 u 、v ,其他所有节点为 O ,成对马尔可夫性指:给定Y_O的条件下,Y_u和Y_v条件独⽴P(Y_u,Y_v|Y_O)=P(Y_u|Y_O)P(Y_v|Y_O)2. 局部马尔可夫性(local)设⽆向图 G 的任⼀节点 v ,W 是与 v 有边相连的所有节点,O 是 v 、W 外的其他所有节点,局部马尔可夫性指:给定Y_W的条件下,Y_v和Y_O条件独⽴P(Y_v,Y_O|Y_W)=P(Y_v|Y_W)P(Y_O|Y_W)当P(Y_O|Y_W)>0时,等价于P(Y_v|Y_W)=P(Y_v|Y_W,Y_O)如果把等式两边的条件⾥的Y_W遮住,P(Y_v)=P(Y_v|Y_O)这个式⼦表⽰Y_v和Y_O独⽴,进⽽可以理解这个等式为给定条件Y_W下的独⽴。