swift trade(Orbixa)香港市场指南2011

香港金银业贸易场AA类平台哪个好

香港金银业贸易场AA类平台哪个好?

香港金银业贸易场(CGSE)是亚洲老牌的贵金属交易所,拥有超过110年的市场管理经验,它通过会员制度管理旗下的持牌电子交易平台。

平台在通过贸易场的资质认证后,就有资格经营正宗的国际现货贵金属电子产品。

目前贸易场规定交易的保证金为合约总值的2%以上,因此香港的现货黄金交易的杠杆比例可达1:50以上,现货黄金交易的杠杆比例可达1:40以上,而且全天有22个小时的连续行情。

目前香港金银业贸易场有171家行员,其中分为认可铸造商、认可电子交易商、认可流通量提供者三类。

因此能成为第一梯队的平台,首先必须是贸易场的认可的电子交易商,而且要持有AA级的牌照。

投资者开户前可以通过贸易场官网的“会籍事务”核实平台的资质和持牌情况,远离一些浑水摸鱼的平台。

与国内的小型交易所相比,CGSE在监管方面是相对可靠的,如果平台经营作风欠佳,屡遭投诉,那么就可能遭到降级处罚,甚至被吊销营业资格。

而贸易场也会定期在官网上公布一些套牌平台的名单,也会定期推出一些宣传教育短片,教导投资者远离投资骗局。

至于贸易场中的会员平台哪家好,投资者应该根据平台的资质级别(最好是AA级)、获奖情况和所采用的交易模式来综合判断。

例如香港金荣中国(http://www.jrjr.hk/?347)是香港资质级别最高现货贵金属平台,持有CGSE的AA牌照和电子交易牌照,所采用的A+NDD(验证无交易员)模式会将客户的订单第一时间发送至国际市场成交,优质的服务已经得到国内多个财经榜单的奖项肯定。

AETOS艾拓思外汇相关问题集

AETOS艾拓思:外汇相关问题集关于外汇交易盘查介绍在各个成功的外汇市场中,为外汇交易提供效劳的机构和场所其实各不相同,具体划分起来,又可分为没有固定交易场所的无形市场,以伦敦外汇市场和苏黎士外汇市场为代表,可称为欧式;有在商品交易所内进行外汇生意业务的,以美国的纽约商品交易所(COMEX)和芝加哥商品交易所(IMM)为代表,可称为美式;有的外汇市场在专门的外汇交易所里进行交易,以香港金银业贸易场和新加坡外汇交易所为代表,可称为亚式。

(1)欧式外汇交易这种外汇市场里的外汇交易没有一个固定的场所。

在伦敦外汇市场,整个市场是由各大金商、下属公司之间的彼此联系组成,通过金商与客户之间的、电传等进行交易;在苏黎士外汇市场,那么由三大银行为客户代为生意并负责结账清算。

伦敦和苏黎士市场上的买家和卖家都是较为保密的,交易量也都难于真实估量。

(2)美式外汇文易这种外汇市场事实上成立在典型的期货市场基础上,其交易类似于在该市场上进行交易的其它种商品。

外汇交易所作为一个非获利性机构,本身不参加交易,只是为交易提供场地、设备,同时制定有关法规,确保交易公平、公正地进行,对交易进行严格地监控。

(3)亚式外汇文易这种外汇交易一样有专门的外汇交易场所,同时进行外汇的现货和期货交易。

外汇做空也能赚钱?现货外汇与其它投资产品不同确实是因为现货外汇是双向交易,股票基金都是单向交易的,只能高抛低吸。

那么什么是做空?什么缘故做空也能赚钱?想更深层次了解。

简单的说:倘假设目前的汇价是1200美元,那么你预示外汇后期面临调整要跌,那个时候你在1200周围买一手外汇跌,当外汇跌至1150的时候也确实是你赚取了50个点的利润,现货外汇一手交易赚取一个点差价利润是100美金赚取了50个点,也确实是说你的利润在5000美元。

那么买跌什么缘故能赚钱呢?比如你是一个做大米生意的老板,你周围有很多的朋友跟你一样的,若是你预示着大米的价钱过几天可能会下跌,那个时候你找周围的朋友同行先借1吨大米,当你把借来的大米依照目前的市价卖掉卖了2000块钱,过几天大米价钱下跌你再依照市价1500元/吨买一吨大米还给开始的那个朋友,如此岂不是大米也还了,自己荷包钱也赚到了?现货外汇做空就和那个的意思差不多!而全世界的外汇交易市场就承担了那个借米老板的角色!外汇交易手续费问题严格来讲现货外汇交易一手交易手续费是的点差+50美金的佣金。

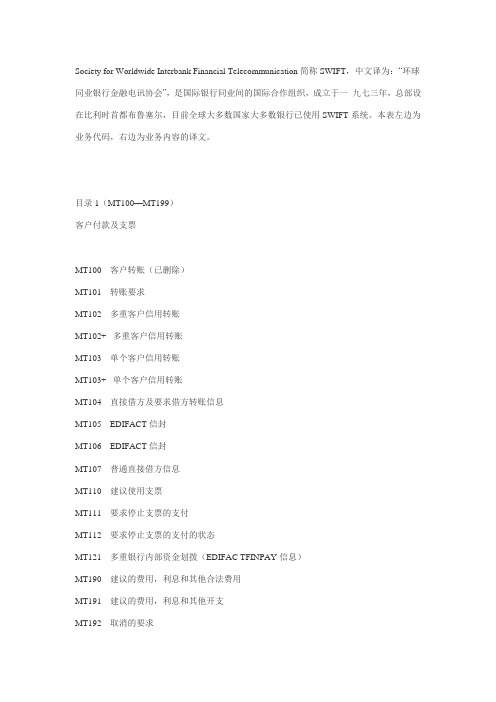

HK Financial Institutions SWIFT codes

B elow are the SWIFT codes for all banks in Hong Kong.These SWIFT codes are only the active participants who are connected to SWIFT network. The passive participant’s codes are excluded from the list.SWIFT code is a standard format of Bank Identifier Codes (BIC) and it is unique identification code fora particular bank.These codes are used when transferring money between banks, particularly for international wire transfers. Banks also used the codes for exchanging other messages between them.The SWIFT code consists of 8 or 11 characters. When 8-digits code is given, it refers to the primary office.•First 4 characters - bank code (only letters)•Next 2 characters - ISO 3166-1 alpha-2 country code (only letters)•Next 2 characters - location code (letters and digits) (passive participant will have "1" in the second character)•Last 3 characters - branch code, optional ('XXX' for primary office) (letters and digits)Currently, there are over 7,500 “live” SWIFT codes. The "live" codes are for the partners who are actively connected to the SWIFT network. On top of that, there are more than 10,000 additional codes, which are used for manual transactions. These additional codes are for the passive participants.No Bank or Institution Branch Name Swift Code 1 AB INTERNATIONAL FINANCE LTD ABFLHKHHXXX2 ABN AMRO BANK N.V. HONG KONGBRANCH(INTERNATIONAL PRIVATECLIENTS DEPARTMENT)ABNAHKAAIPC3 ABN AMRO BANK N.V. HONG KONGBRANCHABNAHKAAIDJ4 ABN AMRO BANK N.V. HONG KONGBRANCHABNAHKAATRY5 ABN AMRO BANK N.V. HONG KONGBRANCHABNAHKAAXXX6 AGRICULTURAL BANK OF CHINA LIMITEDHONG KONG BRANCHABOCHKHHXXX7 AIG ASSET MANAGEMENT (ASIA) LTD AGITHKHHXXX8 ALLAHABAD BANK ALLAHKHHXXX。

SWIFT MT业务代码大全

Society for Worldwide Interbank Financial Telecommunication 简称SWIFT,中文译为:“环球同业银行金融电讯协会”,是国际银行同业间的国际合作组织,成立于一九七三年,总部设在比利时首都布鲁塞尔,目前全球大多数国家大多数银行已使用SWIFT系统。

本表左边为业务代码,右边为业务内容的译文。

目录1(MT100—MT199)客户付款及支票MT100 客户转账(已删除)MT101 转账要求MT102 多重客户信用转账MT102+ 多重客户信用转账MT103 单个客户信用转账MT103+ 单个客户信用转账MT104 直接借方及要求借方转账信息MT105 EDIFACT信封MT106 EDIFACT信封MT107 普通直接借方信息MT110 建议使用支票MT111 要求停止支票的支付MT112 要求停止支票的支付的状态MT121 多重银行内部资金划拨(EDIFAC TFINPAY信息)MT190 建议的费用,利息和其他合法费用MT191 建议的费用,利息和其他开支MT192 取消的要求MT195 询问MT196 答复MT198 所有权信息MT199 自由格式信息目录2(MT200—MT299)金融机构转账MT200 金融机构自有账户转账MT201 多重金融机构自有账户转账MT202 通用金融机构转账MT203 多重通用金融机构转账MT204 金融市场直接借方信息MT205 金融机构转账执行MT206 支票缩减信息MT210 接收通知MT256 支票支付款通知MT290 建议的费用,利息和其他合法费用MT291 建议的费用,利息和其他开支MT292 取消的要求MT293 服务信息MT295 询问MT296 答复MT298 所有权信息MT299 自由格式信息目录3(MT300—MT399)外汇金融市场,货币市场及其他MT300 外汇兑换确认MT303 外汇兑换/货币期权安排指标MT304 第三方交易建议及指标MT305 外汇期权确认MT306 外汇期权确认MT307 第三方外汇交易建议及指标MT308 第三方外汇交易毛利及净利指标MT320 固定贷款/存款确认MT321 解决第三方贷款/存款确认MT340 转寄利率协议确认MT341 转寄利率协议解决确认MT350 贷款/存款利率支付的建议MT360 单个货币利率支付的确认MT361 货币毛利率交换确认MT362 重置利率/支付建议MT364 单个货币利率衍生的终止/重新计算确认MT365 货币毛利率交换终止/重新计算的确认MT380 外汇兑换定单MT381 外汇兑换定单确认MT390 费用,利息和其他合理费用的确认MT391 要求的费用,利息和其他开支MT392 取消的要求MT395 询问MT396 答复MT398 所有权信息MT399 自由格式信息目录4(MT400—MT499)托收及现金运送单MT400 支付建议MT405 清算托收MT410 承诺MT412 接受确认MT416 未支付/未接受建议MT420 追踪MT422 建议的结果及票据要求MT430 票据的补充MT450 现金信用证的建议MT455 现金信用证调整建议MT456 票据拒收建议MT490 费用,利息和其他合理费用的建议MT491 要求的费用,利息和其他开支MT492 取消的要求MT495 询问MT496 答复MT498 所有权信息MT499 自由格式信息目录5(MT500—MT599)证券市场MT500 登记指标MT501 登记或者修改确认MT502 买入或者卖出指令MT503 抵押品申明MT504 抵押品建议MT505 抵押替换品MT506 抵押品及披露申明MT507 抵押品状态及处理建议MT508 内部关系建议MT509 交易状态信息MT510 登记状态及处理建议MT513 客户执行建议MT514 交易安置指示MT515 客户买卖确认MT516 证券贷款确认MT517 交易确认MT518 市场内部证券交易确认MT519 客户信息修改MT524 内部状态指标MT526 一般证券借贷信息MT527 三方抵押指标MT528 ETC客户方清算指标MT529 ETC市场内部清算指标MT535 持有状态MT536 交易状况MT537 悬而未决的交易说明MT538 内部建议说明MT540 自由接收MT541 支付后接收MT542 自由提交MT543 支付后提交MT544 自由接收确认MT545 支付后接收确认MT546 自由提交确认MT547 支付后提交确认MT548 清算状态及处理意见MT549 要求申明或建议MT558 三方抵押状态及处理意见MT559 支付代理人申明MT564 公司活动通知MT565 公司活动指示MT566 公司活动确认MT567 公司活动状态及处理意见MT568 公司活动描述MT569 三方抵押及披露申明MT574 (IRSLST)IRS 1441 NRA MT574 (W8BENO)IRS 1441 NRA MT575 综合业绩报告MT576 开发定单说明MT578 清算宣言MT579 证书号码MT581 抵押调整信息MT582 补偿申明或者建议MT584 ETC悬而未决交易的申明MT586 清算确认申明MT587 托管收据指示MT588 托管收据确认MT589 托管收据状态及处理建议MT590 费用,利息和其他合理费用的建议MT591 要求的费用,利息和其他开支MT592 取消的要求MT595 询问MT596 答复MT598 所有权信息MT599 自由格式信息目录7(MT700—MT799)跟单信用证及保函MT700 跟单信用证的发行MT701 跟单信用证的发行MT705 跟单信用证的预开通知MT707 跟单信用证的修改MT710 第三方银行跟单信用证的建议MT711 第三方银行跟单信用证的建议MT720 跟单信用证的转移MT721 跟单信用证的转移MT730 承诺MT732 清偿建议MT734 拒绝建议MT740 偿还授权MT742 偿还申明MT747 偿还授权书的修改MT750 差异建议MT752 支付,接受或者协商授权MT754 支付/接受/协商建议MT756 偿还或者支付建议MT760 保函MT767 修改保函MT768 保函信息的承诺MT769 减少或者释放保函的建议MT790 费用,利息和其他合理费用的建议MT791 要求的费用,利息和其他开支MT792 取消的要求MT795 询问MT796 答复MT798 所有权信息MT799 自由格式信息目录8(MT800—MT899)旅行支票MT800 旅行支票销售及清算建议(单个)MT801 旅行支票多重销售建议MT802 旅行支票清算建议MT810 旅行支票还款要求MT812 旅行支票还款授权MT813 旅行支票还款确认MT820 申请旅行支票MT821 旅行支票库存增加MT822 委托收款承诺MT823 旅行支票库存转账MT824 旅行支票库存减少或者取消通知MT890 费用,利息和其他合理费用的建议MT891 要求的费用,利息和其他开支MT892 取消的要求MT895 询问MT896 答复MT898 所有权信息MT899 自由格式信息目录9(MT900—MT999)现金管理和客户状态MT900 借方确认MT910 贷方确认MT920 要求信息MT935 利率更改建议MT940 客户申明信息MT941 余额对账单MT942 中期交易报告MT942 中期交易报告MT950 信息申明MT960 开始服务要求信息MT961 开始回复信息MT962 主要服务信息MT963 主要承诺信息MT964 错误信息MT965 主要服务信息错误MT966 终止服务信息MT967 终止承诺信息MT970 盈余申明MT971 盈余余额对账单MT972 盈余中期报告MT973 盈余要求信息MT985 股权状态MT986 报告状态MT990 费用,利息和其他合理费用的建议MT991 要求的费用,利息和其他开支MT992 取消的要求MT995 询问MT996 答复MT998 所有权信息MT999 自由格式信息。

境外机构投资者投资中国银行间债券市场备案表

申请材料示范文本债券投资人员情况说明本公司(单位)加强了对债券投资人员的管理和培训,建立了相应的管理和培训制度,具有专业的银行间债券市场投资人员,包括但不限于分管负责人、部门负责人和前、中、后台业务人员。

公司(单位)名称:(盖章)年月日一、分管负责人与部门负责人四、后台托管结算业务人员:境外机构投资者投资中国银行间债券市场备案表Registration Form for Overseas Institutional Investors in China’sInter-Bank Bond Market(法人类)(For Incorporated Entities)投资者名称:Name of Entity 结算代理备案□Settlement Agent“债券通”备案□盖章/签字(Official Seal/Signature):境外机构投资者投资中国银行间债券市场备案表Registration Form for Overseas Institutional Investors in China’sInter-Bank Bond Market(非法人类)(For Unincorporated Entities)投资者名称:Name of Entity结算代理备案□Settlement Agent“债券通”备案□填表说明Note:1.表格用中文和英文填写。

境外投资者若无中文名的,“投资者名称”可仅填写英文名。

Please fill out this form in both Chinese and English. If an overseas investor has no Chinese name, “Name of Entity” may be filled in English name only.2.申请机构简介或投资管理人简介包括监管法律、组织结构(含投资职能)等内容。

Brief Introduction or Brief Introduction of Investment Management Company:background on governing law, organizational structure (including investment function), etc.3.投资负责人信息须填写债券投资管理人及投资主要负责人的基本情况。

外汇买卖业务

外汇买卖业务外汇买卖业务⼀、汇率的表⽰⽅式1、直接报价法:1单位外币折合多少单位本国货币的标价法为直接标价法。

例:1美元=8.2769⼈民币(USD/RMB=8.2769)左边是外币,右边是本币2、间接报价法:1单位本国货币折合多少外币的标价法为间接报价法。

例: 1英镑=1.4215美元 (GBP/USD=1.4215)左边是本币,右边是外币⽬前外汇买卖报价只有澳⼤利亚元、欧元、英镑三个币种是采⽤间接报价法,其它币种均采⽤的是直接报价法。

⼆、汇率的涨跌例1:1欧元=0.780美元(欧元是被报价币,间接标价法)当1欧元=0.770美元则:欧元贬值,美元升值当1欧元=0.790美元则:欧元升值,美元贬值例2:1美元=7.940港币(美元为被报价币,直接标价法)当1美元=7.930港币则:美元贬值,港币升值当1美元=7.950港币则:美元升值,港币贬值三、交叉汇率两种⾮美元货币的⽐价,通过美元套算1.两种货币都必须是以美元作为被报价币,套算汇率为交叉相除;2.两种货币都是以美元作为报价币,套算汇率为交叉相乘;3.⼀种货币是以美元作为被报价币,另⼀种货币是以美元作为报价币,套算汇率为同边相乘;四、委托⽅式⽬前我⾏个⼈实盘外汇买卖共有以下⼏种委托⽅式:挂盘委托,⽌损委托,追加委托,⼆选⼀委托,撤单委托.(举例说明)五、汇率中“点”的含义:汇率报价都是由5个有效数字组成,⼩数点右边的最后⼀位,称为基本点,俗称“点”。

不同的点数代表不同的幅度。

例:⽬前美元/⽇元市场⾏情为:买⼊价/卖出价为110.50/110.70,当中的点差为20个点.点差实际就是客户在交易过程中所需要⽀付的成本,点差越低对客户越有利。

⽬前各分⾏可视情况⾃⾏制定当地点差。

各地区的点差查询可参考FAQ“外汇买卖交易参数”,但因市场波动,点差只能是相对固定,即时查询可参考“⼀⽹通外汇”⽹站中的报价计算得出。

六、主要外汇市场:1、全球最⼤的交易市场:伦敦2、亚洲最⼤的交易市场:东京3、北美最⼤的交易市场:纽约4、其它外汇中⼼还有:惠灵顿、悉尼、新加坡、⾹港、法兰克福、苏黎世、巴黎5、⽬前主要外汇市场的开闭市时间如下:(以下时间均为北京时间)七、基本⾯分析的常⽤经济数据1、国民⽣产总值;2、失业率;3、零售指数;4、个⼈消费⽀出;5、⼯业⽣产指数;6、全国采购经理协会指数;7、⼯⼚订单;8、消费物价指数;9、⽣产物价指数;10、商业库存;÷⼋、“外汇通2.0”⾏情分析软件该分析软件由杭州核⼼软件提供技术⽀持,其报价的来源直接联接我⾏与国际市场中外汇报价系统。

中国外汇交易中心产品指引(外汇市场)V1[1].1

![中国外汇交易中心产品指引(外汇市场)V1[1].1](https://img.taocdn.com/s3/m/54a68920482fb4daa58d4bfa.png)

有任何问题与建议,请联系: 市场一部 华小岳 021-68797572、63298988, huaxiaoyue@

版权所有©中国外汇交易中心 2011 未经授权 不得转载 Copyright © 2011China Foreign Exchange Trade System, All Rights Reserved

4

修订说明

2009 年 12 月 《中国外汇交易中心产品指引(外汇市场) 》V1.0 2011 年 4 月 《中国外汇交易中心产品指引(外汇市场) 》V1.1

V 1.1

一、修订背景 近一年多来,银行间外汇市场取得了一定发展,包括:人民币外汇做市商实行分层制 度,调整人民币外汇市场交易时间,增加外汇期权交易品种,增加人民币兑林吉特、人民 币兑卢布、美元对新加坡元三个货币对,外汇交易系统增加单独远期报价页面,调整外币 对市场流动性限额等。根据市场发展变化及市场建议,交易中心对指引 V1.0 版本进行相 应修订,并发布修订后的《中国外汇交易中心产品指引(外汇市场)》V1.1。

中国外汇交易中心

China Foreign Exchange Trade System

产品指引(外汇市场)

Product Guide (FX Market) V 1.1

2011 年 4 月

前

言

本指引仅作银行间外汇市场会员从事外汇交易参考指引性用途, 旨在介绍中国外汇交易 中心(除特定规范引用处外,指引中简称 “交易中心”)外汇产品,以及明确交易双方在无 特别约定情况下外汇交易的术语释义、 一般准则和基本规程, 以帮助理解银行间外汇市场产 品,降低交易成本和提高市场效率。在不违反相关法律、法规、规章、交易规则及交易中心 颁布的其它相关文件的前提下,交易双方一致达成的特别约定具有优先性。 交易中心不保证本指引所载文字、图形、公式、说明、陈述及任何其它项目的准确性及 完整性。指引中所列英文仅供参考,以中文为准。交易中心对因使用或信赖本指引中任何所 载内容造成的任何损失,包括特定的、直接的、间接的、意外的、可意识到的各种收入或盈 利损失不承担任何责任。 本指引著作权归属交易中心, 银行间外汇市场会员可在交易协议或其他交易文件中予以 部分或全部引用,其他单位或个人基于非赢利性目的可予以摘录、引用,但必须注明出处。 未经交易中心授权,任何单位和个人不得复制、翻译或分发本指引的纸质、电子或其他形式 版本。 本指引主要由 6 部分内容和附录组成,第 1 部分为外汇交易的通用定义;第 2、3、4、 5、6 部分为银行间外汇市场产品,包括与各产品相关的定义、产品基本要素和示例;附录 包括表格与规则。 交易中心将在不作特定通知的情况下,根据市场发展变化、市场建议、外汇交易系统升 级等情况不定期更新或修订本指引并及时公布最新版本,并对最新版本的修订情况进行说 明。

汇入汇款(至香港)客户参考资料表

如何汇款至您的银行账户:

请指示汇款银行使用 SWIFT MT103 的汇款指示并递交以下*汇款资料予香港汇丰(HSBCHKHHHKH)。 如汇款银行未能直接递交汇款指示予香港汇丰,请指示汇款银行与汇丰其他#海外办事处/代理行安排使用

SWIFT MT103 的汇款指示并递交以下*汇款资料予香港汇丰(HSBCHKHHHKH)。

丹麦克朗(DKK) Nordea Bank Danmark A/S, Copenhagen SWIFT: NDEADKKK 丹麦克朗账户号码:5000405861

新加坡元(SGD) The Hongkong and Shanghai Banking Corporation Limited Singapore SWIFT: HSBCSGSG 新加坡元账户号码:141-311787-001

欧罗(EUR) HSBC France, Paris SWIFT: CCFRFRPP IBAN: FR7630056000100010000405731

瑞士法郎(CHF) UBS AG, Zurich SWIFT: U7050000M

REM144R10SC-m (251018) FI

汇入汇款(至香港)客户参考资料表

一般查询

电话 : (852) 2233 3000 (汇丰个人理财客户适用)/(852) 2748 8288 (商业客户适用) 传真 : (852) 2288 2400 (汇丰个人理财客户适用)/(852) 2288 2332 (商业客户适用) 地址 : 汇丰总行 香港皇后大道中 1 号 SWIFT : HSBCHKHHHKH

- 受款人名称

Tag 59(请参考备注 2)

备注 1:

若您将汇款存入至综合理财账户内的港币或其他外币的储蓄账户,请提供最尾三个数字为 833、838 或 888 的账户号码,您可通过网上理财或流动理财应用程序、联系客户服务热线或本行任何分行查询账户 详情。另一方面,若受款账户指定为综合理财账户港币往来账户(账户号码最尾的三个数字为 001), 有关汇款将按当时汇率兑换为港币及存入您的往来账户。

香港会计准则11号

Joint ArrangementsEffective for annual periodsbeginning on or after 1 January 2013COPYRIGHT© Copyright 2011 Hong Kong Institute of Certified Public AccountantsThis Hong Kong Financial Reporting Standard contains IFRS Foundation copyright material. Reproduction within Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and inquiries concerning reproduction and rights for commercial purposes within Hong Kong should be addressed to the Director, Finance and Operation, Hong Kong Institute of Certified Public Accountants, 37/F., Wu Chung House, 213 Queen's Road East, Wanchai, Hong Kong.All rights in this material outside of Hong Kong are reserved by IFRS Foundation. Reproduction of Hong Kong Financial Reporting Standards outside of Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce for commercial purposes outside Hong Kong should be addressed to the IFRS Foundation at .Further details of the copyright notice form IFRS Foundation is available at .hk/ebook/copyright-notice.pdfC ONTENTSparagraphs INTRODUCTION IN1–IN11 HONG KONG FINANCIAL REPORTING STANDARD 11JOINT ARRANGEMENTSOBJECTIVE 1–2 SCOPE 3 JOINT ARRANGEMENTS 4–19 Joint control 7–13 Types of joint arrangement 14–19 FINANCIAL STATEMENTS OF PARTIES TO A JOINT ARRANGEMENT 20–25 Joint operation 20–23 Joint venture 24–25 SEPARATE FINANCIAL STATEMENTS 26–27 APPENDICESA Defined termsB Application guidanceC Effective date, transition and withdrawal of other HKFRSsD Amendments to other HKFRSsE Comparison with International Financial Reporting StandardsBASIS FOR CONCLUSIONS (see separate booklet)APPENDIXAmendments to the Basis for Conclusions on other HKFRSsILLUSTRATIVE EXAMPLES (see separate booklet)IntroductionOverviewIN1 Hong Kong Financial Reporting Standard 11 Joint Arrangements establishes principles for financial reporting by parties to a joint arrangement.IN2 The HKFRS supersedes HKAS 31 Interests in Joint Ventures and HK(SIC)-Int 13 Jointly Controlled Entities—Non-Monetary Contributions by Venturers and is effective for annual periods beginning on or after 1 January 2013. Earlier application is permitted.Reasons for issuing the HKFRSIN3 The HKFRS is concerned principally with addressing two aspects of HKAS 31: first, that the structure of the arrangement was the only determinant of the accounting and, second, that an entity had a choice of accounting treatment for interests in jointly controlled entities.IN4 HKFRS 11 improves on HKAS 31 by establishing principles that are applicable to the accounting for all joint arrangements.Main features of the HKFRSIN5 The HKFRS requires a party to a joint arrangement to determine the type of joint arrangement in which it is involved by assessing its rights and obligations arising from the arrangement.General requirementsIN6 The HKFRS is to be applied by all entities that are a party to a joint arrangement. A joint arrangement is an arrangement of which two or more parties have joint control.The HKFRS defines joint control as the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities (ie activities that significantly affect the returns of the arrangement) require the unanimous consent of the parties sharing control.IN7 The HKFRS classifies joint arrangements into two types—joint operations and joint ventures. A joint operation is a joint arrangement whereby the parties that have joint control of the arrangement (ie joint operators) have rights to the assets, and obligations for the liabilities, relating to the arrangement. A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement (ie joint venturers) have rights to the net assets of the arrangement.IN8 An entity determines the type of joint arrangement in which it is involved by considering its rights and obligations. An entity assesses its rights and obligations by considering the structure and legal form of the arrangement, the contractual terms agreed to by the parties to the arrangement and, when relevant, other facts and circumstances.IN9 The HKFRS requires a joint operator to recognise and measure the assets and liabilities (and recognise the related revenues and expenses) in relation to its interest in the arrangement in accordance with relevant HKFRSs applicable to the particular assets, liabilities, revenues and expenses.IN10 The HKFRS requires a joint venturer to recognise an investment and to account for that investment using the equity method in accordance with HKAS 28 Investments in Associates and Joint Ventures, unless the entity is exempted from applying the equity method as specified in that standard.IN11 The disclosure requirements for parties with joint control of a joint arrangement are specified in HKFRS 12 Disclosure of Interests in Other Entities.Hong Kong Financial Reporting Standard 11Joint ArrangementsObjective1 The objective of this HKFRS is to establish principles for financial reporting byentities that have an interest in arrangements that are controlled jointly (ie joint arrangements).Meeting the objective2 To meet the objective in paragraph 1, this HKFRS defines joint control and requiresan entity that is a party to a joint arrangement to determine the type of joint arrangement in which it is involved by assessing its rights and obligations and to account for those rights and obligations in accordance with that type of joint arrangement.Scope3 This HKFRS shall be applied by all entities that are a party to a jointarrangement.Joint arrangements4 A joint arrangement is an arrangement of which two or more parties have jointcontrol.5 A joint arrangement has the following characteristics:(a) The parties are bound by a contractual arrangement (see paragraphs B2–B4).(b) The contractual arrangement gives two or more of those parties jointcontrol of the arrangement (see paragraphs 7–13).6 A joint arrangement is either a joint operation or a joint venture.Joint control7 Joint control is the contractually agreed sharing of control of an arrangement,which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control.8 An entity that is a party to an arrangement shall assess whether the contractualarrangement gives all the parties, or a group of the parties, control of the arrangement collectively. All the parties, or a group of the parties, control the arrangement collectively when they must act together to direct the activities that significantly affect the returns of the arrangement (ie the relevant activities).9 Once it has been determined that all the parties, or a group of the parties, control thearrangement collectively, joint control exists only when decisions about the relevant activities require the unanimous consent of the parties that control the arrangement collectively.10 In a joint arrangement, no single party controls the arrangement on its own. A partywith joint control of an arrangement can prevent any of the other parties, or a group of the parties, from controlling the arrangement.11 An arrangement can be a joint arrangement even though not all of its parties havejoint control of the arrangement. This HKFRS distinguishes between parties that have joint control of a joint arrangement (joint operators or joint venturers) and parties that participate in, but do not have joint control of, a joint arrangement.12 An entity will need to apply judgement when assessing whether all the parties, or agroup of the parties, have joint control of an arrangement. An entity shall make this assessment by considering all facts and circumstances (see paragraphs B5–B11).13 If facts and circumstances change, an entity shall reassess whether it still has jointcontrol of the arrangement.Types of joint arrangement14 An entity shall determine the type of joint arrangement in which it is involved.The classification of a joint arrangement as a joint operation or a joint venture depends upon the rights and obligations of the parties to the arrangement.15 A joint operation is a joint arrangement whereby the parties that have jointcontrol of the arrangement have rights to the assets, and obligations for the liabilities, relating to the arrangement. Those parties are called joint operators.16 A joint venture is a joint arrangement whereby the parties that have jointcontrol of the arrangement have rights to the net assets of the arrangement.Those parties are called joint venturers.17 An entity applies judgement when assessing whether a joint arrangement is a jointoperation or a joint venture. An entity shall determine the type of joint arrangement in which it is involved by considering its rights and obligations arising from the arrangement. An entity assesses its rights and obligations by considering the structure and legal form of the arrangement, the terms agreed by the parties in the contractual arrangement and, when relevant, other facts and circumstances (see paragraphs B12–B33).18 Sometimes the parties are bound by a framework agreement that sets up the generalcontractual terms for undertaking one or more activities. The framework agreement might set out that the parties establish different joint arrangements to deal with specific activities that form part of the agreement. Even though those joint arrangements are related to the same framework agreement, their type might be different if the parties’ rights and obligations differ when undertaking the different activities dealt with in the framework agreement. Consequently, joint operations and joint ventures can coexist when the parties undertake different activities that form part of the same framework agreement.19 If facts and circumstances change, an entity shall reassess whether the type of jointarrangement in which it is involved has changed.Financial statements of parties to a joint arrangement Joint operations20 A joint operator shall recognise in relation to its interest in a joint operation:(a) its assets, including its share of any assets held jointly;(b) its liabilities, including its share of any liabilities incurred jointly;(c) its revenue from the sale of its share of the output arising from the jointoperation;(d) its share of the revenue from the sale of the output by the joint operation;and(e) its expenses, including its share of any expenses incurred jointly.21 A joint operator shall account for the assets, liabilities, revenues and expensesrelating to its interest in a joint operation in accordance with the HKFRSs applicable to the particular assets, liabilities, revenues and expenses.22 The accounting for transactions such as the sale, contribution or purchase of assetsbetween an entity and a joint operation in which it is a joint operator is specified in paragraphs B34–B37.23 A party that participates in, but does not have joint control of, a joint operation shall alsoaccount for its interest in the arrangement in accordance with paragraphs 20–22 if that party has rights to the assets, and obligations for the liabilities, relating to the joint operation. If a party that participates in, but does not have joint control of, a joint operation does not have rights to the assets, and obligations for the liabilities, relating to that joint operation, it shall account for its interest in the joint operation in accordance with the HKFRSs applicable to that interest.Joint ventures24 A joint venturer shall recognise its interest in a joint venture as an investmentand shall account for that investment using the equity method in accordance with HKAS 28 Investments in Associates and Joint Ventures unless the entity is exempted from applying the equity method as specified in that standard.25 A party that participates in, but does not have joint control of, a joint venture shallaccount for its interest in the arrangement in accordance with HKFRS 9 Financial Instruments, unless it has significant influence over the joint venture, in which case it shall account for it in accordance with HKAS 28 (as amended in 2011).Separate financial statements26 In its separate financial statements, a joint operator or joint venturer shallaccount for its interest in:(a) a joint operation in accordance with paragraphs 20–22;(b) a joint venture in accordance with paragraph 10 of HKAS 27 SeparateFinancial Statements.27 In its separate financial statements, a party that participates in, but does nothave joint control of, a joint arrangement shall account for its interest in:(a) a joint operation in accordance with paragraph 23;(b) a joint venture in accordance with HKFRS 9, unless the entity hassignificant influence over the joint venture, in which case it shall applyparagraph 10 of HKAS 27 (as amended in 2011).Appendix ADefined termsThis appendix is an integral part of the HKFRS.joint arrangement An arrangement of which two or more parties have jointcontrol.joint control The contractually agreed sharing of control of an arrangement,which exists only when decisions about the relevant activitiesrequire the unanimous consent of the parties sharing control. joint operation A joint arrangement whereby the parties that have jointcontrol of the arrangement have rights to the assets, andobligations for the liabilities, relating to the arrangement.joint operator A party to a joint operation that has joint control of that jointoperation.joint venture A joint arrangement whereby the parties that have jointcontrol of the arrangement have rights to the net assets of thearrangement.joint venturer A party to a joint venture that has joint control of that jointventure.party to a joint arrangement An entity that participates in a joint arrangement, regardless of whether that entity has joint control of the arrangement.separate vehicle A separately identifiable financial structure, including separatelegal entities or entities recognised by statute, regardless ofwhether those entities have a legal personality.The following terms are defined in HKAS 27 (as amended in 2011), HKAS 28 (as amended in 2011) or HKFRS 10 Consolidated Financial Statements and are used in this HKFRS with the meanings specified in those HKFRSs:•control of an investee•equity method•power•protective rights•relevant activities•separate financial statements•significant influence.Appendix BApplication guidanceThis appendix is an integral part of the HKFRS. It describes the application of paragraphs 1–27 and has the same authority as the other parts of the HKFRS.B1 The examples in this appendix portray hypothetical situations. Although some aspects of the examples may be present in actual fact patterns, all relevant facts and circumstances of a particular fact pattern would need to be evaluated when applying HKFRS 11.Joint arrangementsContractual arrangement (paragraph 5)B2 Contractual arrangements can be evidenced in several ways. An enforceable contractual arrangement is often, but not always, in writing, usually in the form of a contract or documented discussions between the parties. Statutory mechanisms can also create enforceable arrangements, either on their own or in conjunction with contracts between the parties.B3 When joint arrangements are structured through a separate vehicle (see paragraphs B19–B33), the contractual arrangement, or some aspects of the contractual arrangement, will in some cases be incorporated in the articles, charter or by-laws of the separate vehicle.B4 The contractual arrangement sets out the terms upon which the parties participate in the activity that is the subject of the arrangement. The contractual arrangement generally deals with such matters as:(a) the purpose, activity and duration of the joint arrangement.(b) how the members of the board of directors, or equivalent governing body, of thejoint arrangement, are appointed.(c) the decision-making process: the matters requiring decisions from the parties,the voting rights of the parties and the required level of support for thosematters. The decision-making process reflected in the contractualarrangement establishes joint control of the arrangement (see paragraphs B5–B11).(d) the capital or other contributions required of the parties.(e) how the parties share assets, liabilities, revenues, expenses or profit or lossrelating to the joint arrangement.Joint control (paragraphs 7–13)B5 In assessing whether an entity has joint control of an arrangement, an entity shall assess first whether all the parties, or a group of the parties, control the arrangement.HKFRS 10 defines control and shall be used to determine whether all the parties, or a group of the parties, are exposed, or have rights, to variable returns from their involvement with the arrangement and have the ability to affect those returns through their power over the arrangement. When all the parties, or a group of the parties, considered collectively, are able to direct the activities that significantly affect the returns of the arrangement (ie the relevant activities), the parties control the arrangement collectively.B6 After concluding that all the parties, or a group of the parties, control the arrangement collectively, an entity shall assess whether it has joint control of the arrangement.Joint control exists only when decisions about the relevant activities require the unanimous consent of the parties that collectively control the arrangement.Assessing whether the arrangement is jointly controlled by all of its parties or by a group of the parties, or controlled by one of its parties alone, can require judgement. B7 Sometimes the decision-making process that is agreed upon by the parties in their contractual arrangement implicitly leads to joint control. For example, assume two parties establish an arrangement in which each has 50 per cent of the voting rights and the contractual arrangement between them specifies that at least 51 per cent of the voting rights are required to make decisions about the relevant activities. In this case, the parties have implicitly agreed that they have joint control of the arrangement because decisions about the relevant activities cannot be made without both parties agreeing.B8 In other circumstances, the contractual arrangement requires a minimum proportion of the voting rights to make decisions about the relevant activities. When that minimum required proportion of the voting rights can be achieved by more than one combination of the parties agreeing together, that arrangement is not a joint arrangement unless the contractual arrangement specifies which parties (or combination of parties) are required to agree unanimously to decisions about the relevant activities of the arrangement.B9 The requirement for unanimous consent means that any party with joint control of the arrangement can prevent any of the other parties, or a group of the parties, from making unilateral decisions (about the relevant activities) without its consent. If therequirement for unanimous consent relates only to decisions that givea partyprotective rights and not to decisions about the relevant activities of an arrangement, that party is not a party with joint control of the arrangement.B10 A contractual arrangement might include clauses on the resolution of disputes, such as arbitration. These provisions may allow for decisions to be made in the absence of unanimous consent among the parties that have joint control. The existence of such provisions does not prevent the arrangement from being jointly controlled and, consequently, from being a joint arrangement.Assessing joint controlB11 When an arrangement is outside the scope of HKFRS 11, an entity accounts for its interest in the arrangement in accordance with relevant HKFRSs, such as HKFRS 10, HKAS 28 (as amended in 2011) or HKFRS 9.Types of joint arrangement (paragraphs 14–19)B12 Joint arrangements are established for a variety of purposes (eg as a way for parties to share costs and risks, or as a way to provide the parties with access to new technology or new markets), and can be established using different structures and legal forms.B13 Some arrangements do not require the activity that is the subject of the arrangement to be undertaken in a separate vehicle. However, other arrangements involve the establishment of a separate vehicle.B14 The classification of joint arrangements required by this HKFRS depends upon the parties’ rights and obligations arising from the arrangement in the normal course of business. This HKFRS classifies joint arrangements as either joint operations or joint ventures. When an entity has rights to the assets, and obligations for the liabilities, relating to the arrangement, the arrangement is a joint operation. When an entity has rights to the net assets of the arrangement, the arrangement is a joint venture.Paragraphs B16–B33 set out the assessment an entity carries out to determine whether it has an interest in a joint operation or an interest in a joint venture.Classification of a joint arrangementB15 As stated in paragraph B14, the classification of joint arrangements requires the parties to assess their rights and obligations arising from the arrangement. When making that assessment, an entity shall consider the following:(a) the structure of the joint arrangement (see paragraphs B16–B21).(b) when the joint arrangement is structured through a separate vehicle:(i) the legal form of the separate vehicle (see paragraphs B22–B24);(ii) the terms of the contractual arrangement (see paragraphs B25–B28); and(iii) when relevant, other facts and circumstances (see paragraphs B29–B33).Structure of the joint arrangementJoint arrangements not structured through a separate vehicleB16 A joint arrangement that is not structured through a separate vehicle is a joint operation. In such cases, the contractual arrangement establishes the parties’ rights to the assets, and obligations for the liabilities, relating to the arrangement, and the parties’ rights to the corresponding revenues and oblig ations for the corresponding expenses.B17 The contractual arrangement often describes the nature of the activities that are the subject of the arrangement and how the parties intend to undertake those activities together. For example, the parties to a joint arrangement could agree to manufacturea product together, with each party being responsible for a specific task and eachusing its own assets and incurring its own liabilities. The contractual arrangement could also specify how the revenues and expenses that are common to the parties are to be shared among them. In such a case, each joint operator recognises in its financial statements the assets and liabilities used for the specific task, and recognises its share of the revenues and expenses in accordance with the contractual arrangement.B18 In other cases, the parties to a joint arrangement might agree, for example, to share and operate an asset together. In such a case, the contractual arrangement establishes the parties’ rights to the ass et that is operated jointly, and how output or revenue from the asset and operating costs are shared among the parties. Each joint operator accounts for its share of the joint asset and its agreed share of any liabilities, and recognises its share of the output, revenues and expenses in accordance with the contractual arrangement.Joint arrangements structured through a separate vehicleB19 A joint arrangement in which the assets and liabilities relating to the arrangement are held in a separate vehicle can be either a joint venture or a joint operation.B20 Whether a party is a joint operator or a joint venturer depends on the party’s rights to the assets, and obligations for the liabilities, relating to the arrangement that are held in the separate vehicle.B21 As stated in paragraph B15, when the parties have structured a joint arrangement in a separate vehicle, the parties need to assess whether the legal form of the separate vehicle, the terms of the contractual arrangement and, when relevant, any other facts and circumstances give them:(a) rights to the assets, and obligations for the liabilities, relating to the arrangement(ie the arrangement is a joint operation); or(b) rights to the net assets of the arrangement (ie the arrangement is a jointventure).Classification of a joint arrangement: assessment of the parties’rights and obligations arising from the arrangementThe legal form of the separate vehicleB22 The legal form of the separate vehicle is relevant when assessing the type of joint arrangement. The legal form assists in the initial assessment of the parties’ rights to the assets and obligations for the liabilities held in the separate vehicle, such as whether the parties have interests in the assets held in the separate vehicle and whether they are liable for the liabilities held in the separate vehicle.B23 For example, the parties might conduct the joint arrangement through a separate vehicle, whose legal form causes the separate vehicle to be considered in its own right (ie the assets and liabilities held in the separate vehicle are the assets and liabilities of the separate vehicle and not the assets and liabilities of the parties). In such a case, the assessment of the rights and obligations conferred upon the parties by the legal form of the separate vehicle indicates that the arrangement is a joint venture. However, the terms agreed by the parties in their contractual arrangement (see paragraphs B25–B28) and, when relevant, other facts and circumstances (see paragraphs B29–B33) can override the assessment of the rights and obligations conferred upon the parties by the legal form of the separate vehicle.B24 The assessment of the rights and obligations conferred upon the parties by the legal form of the separate vehicle is sufficient to conclude that the arrangement is a joint operation only if the parties conduct the joint arrangement in a separate vehicle whose legal form does not confer separation between the parties and the separate vehicle (ie the assets and liabilities held in the separate vehicle are the parties’ assets and liabilities).Assessing the terms of the contractual arrangementB25 In many cases, the rights and obligations agreed to by the parties in their contractual arrangements are consistent, or do not conflict, with the rights and obligations conferred on the parties by the legal form of the separate vehicle in which the arrangement has been structured.B26 In other cases, the parties use the contractual arrangement to reverse or modify the rights and obligations conferred by the legal form of the separate vehicle in which the arrangement has been structured.B27 The following table compares common terms in contractual arrangements of parties to a joint operation and common terms in contractual arrangements of parties to a joint venture. The examples of the contractual terms provided in the following table are not exhaustive.B28 When the contractual arrangement specifies that the parties have rights to the assets, and obligations for the liabilities, relating to the arrangement, they are parties to a joint operation and do not need to consider other facts and circumstances (paragraphs B29–B33) for the purposes of classifying the joint arrangement.Assessing other facts and circumstancesB29 When the terms of the contractual arrangement do not specify that the parties have rights to the assets, and obligations for the liabilities, relating to the arrangement, the parties shall consider other facts and circumstances to assess whether the arrangement is a joint operation or a joint venture.B30 A joint arrangement might be structured in a separate vehicle whose legal form confers separation between the parties and the separate vehicle. The contractual terms agreed among the parties might not specify the parties’ rights to the assets and obligations for the liabilities, yet consideration of other facts and circumstances can lead to such an arrangement being classified as a joint operation. This will be the case when other facts and circumstances give the parties rights to the assets, and obligations for the liabilities, relating to the arrangement.B31 When the activities of an arrangement are primarily designed for the provision of output to the parties, this indicates that the parties have rights to substantially all the economic benefits of the assets of the arrangement. The parties to such arrangements often ensure their access to the outputs provided by the arrangement by preventing the arrangement from selling output to third parties.B32 The effect of an arrangement with such a design and purpose is that the liabilities incurred by the arrangement are, in substance, satisfied by the cash flows received from the parties through their purchases of the output. When the parties are substantially the only source of cash flows contributing to the continuity of the operations of the arrangement, this indicates that the parties have an obligation for the liabilities relating to the arrangement.。

香港金银业贸易场AA类会员名单

香港金银业贸易场AA 类84号行员 香港金银业贸易场AA 类会员名单香港金银业贸易场是我国正规的黄金交易场所,也是投资者们外汇交易的重要场所。

香港金银业贸易场实行会员管理制度,目前共有171家会员平台,组织规模正在不断扩大。

我们经常能看到,有些贸易场的会员显示的是AA 类会员,那么贸易场的会员是怎么区分的呢?香港金银业贸易场会员分类目前为止,香港金银业贸易场共有171家会员,香港金银业贸易场的营业牌照共有AA 、A1、A2、B 、C 、D 和S 这7个类别,AA 类会员是贸易场最高级别的会员,其中包括AA 类会员62家,A1类会员22家,A2类会员1家,B 类会员22家,C 类会员2家,D 类会员51家,S 类会员11家。

香港金银业贸易场AA 类会员名单 1、金荣中国金融业有限公司金荣中国金融业有限公司,2010年经香港政|府批准成立,并受到香港金银业贸易场的监管。

是香港金银业贸易场最高级别AA 类行员,主要经营伦敦金、伦敦银、人民币公斤条等贵金属业务。

金荣中国自成立以来,一直以维护客户权益为己任。

为了降低客户的投资成本和门槛,方便客户更好的进行投资交易活动,公司为客户提供免费开户,并不间断的推出优惠赠送活动。

极大的增加了投资者的投资获利空间。

行员编号:084号 2、国盛金业有限公司国盛金业有限公司,简称(GS GOLD )总部位于中国香港,专注于全球投资者提供贵金属投资服务,国盛金业持有香港金银业贸易场AA 类牌照。

可合法经营伦、伦敦银等贵金属业务,所有交易均受到金银业贸易场的认可和监管,并受香港法律之管制。

行员编号:015号 3、天誉金号有限公司天誉国际为一间植根香港面向全球的金融机构,业务遍及亚太区及中国各大城市。

其中天誉金号更是香港金银业贸易会员,而且同时是香港金银业贸易场的认可电子交易商。

香港金银业贸易场AA 类84号行员 行员编号:025号 4、金道贵金属有限公司金道贵金属有限公司为金道投资控股有限公司(金道集团)之成员,于2009年在香港注册成立,持有香港金银业贸易场AA 类别市场交易有效营业牌照,可经营99金、港元公斤条、伦敦金/银及人民币公斤条业务。

《国际金融概论》习题集答案

《国际金融概论》习题集答案《国际金融概论》习题集thepraxisofinternationalfinance金融系国际金融教研室目录第一章外汇与汇率 (2)第二章汇率制度与外汇管制.............................................................9第三章外汇交易与外汇风险.........................................................12第四章第五章第六章第七章第八章第九章第十章国际结算............................................................................ 15国际资本流动....................................................................18国际金融市场....................................................................22国际收支............................................................................ 27国际储备............................................................................ 33国际货币制度....................................................................37国际金融机构.. (40)1第一章外汇与汇率一、选择题1、动态外汇是指(a)。

a、国际汇率风险b、外国货币c、外币现钞d、外币资产2、按《中华人民共和国外汇管理条理》的表述,外汇以外币则表示的可以看作(c)的缴付手段和资产。

中期标准交易手续费

序号交易所品种佣金(单边)序号交易所品种佣金(单边)1玉米Corn (C )US$15.0038布兰特期油 Brent Crude (BC )US$20.002黄豆 Soybean (S)US$15.0039布兰特气油 Gas Oil (GAS )US$20.003小麦 Wheat (W )US$15.0040铜 Copper (HG )US$20.004燕麦 Oats (O )US$15.0041金 Gold (GC )US$20.005黄豆油 Soybean Oil (BO )US$15.0042白银 Silver (SI )US$20.006豆粉 Soybean Meal (SM )US$15.0043钯金 Palladium (PA )US$20.007糙米 Rough Rice (RR )US$15.0044铂金 Platinum (PL )US$20.008小型玉米 Mini Corn (YC )US$15.0045纽约期油 Crude Oil (CL )US$20.009小型黄豆 Mini Soybean (YK )US$15.0046小型原油 Mini Crude (QM )US$15.0010小型小麦 Mini Wheat (YW )US$15.0047天然气 Natural Gas (NG )US$20.0011道琼斯指数 Dow Jones Index $10(DJ )US$15.0048小型天然气 Mini Natural Gas (QG )US$15.0012小型道琼斯指数Mini Dow Jones Index $5(YM )US$15.0049取暖油 Heating Oil (HO )US$20.0013美国5年票据 5 year US Treasury Notes(FV )US$15.0050汽油 RBOB Gasoline (RB )US$20.0014美国10年票据 10 year US Treasury Notes(TY )US$15.0051倫敦铜 Copper (CA )1/160015美国30年国债 30 year US Treasury Bonds(US)US$15.0052倫敦铝 Aluminum (AH )1/160016澳元 Australian Dollar (AD )US$20.0053倫敦镍 Nickel (NI )1/160017加元 Canadian Dollar (CD )US$20.0054倫敦铝合金 Aluminum Alloy (AA )1/160018欧元 Euro Currencies (EC )US$20.0055倫敦锡 Tin (SN )1/160019英镑 British Pound (BP )US$20.0056倫敦铅 Lead (PB )1/160020日圆 Japanese Yen (JY )US$20.0057倫敦锌 Zinc (ZS )1/160021瑞士法郎 Swiss Franc (SF )US$20.0058倫敦基本金属期权1/160022人民币 Chinese Renminbi (RMB )US$20.0059橡胶 Rubber (JPRU )JPY 2,00023纳斯达克100指数 Nasdaq 100(ND )US$20.0060黄金 Gold (JPIG )JPY 2,00024小型纳斯达克指数 Mini Nasdaq 100(NQ )US$15.0061白金 Platinum (JPIP )JPY 2,00025标准普尔500指数 S&P 500(SP )US$20.0062日经平均指数225 Nikkei 225(NK )JPY 1,50026小型标准普尔500 Mini S&P 500(ES )US$15.0063摩根台湾指数 MSCI Taiwan (TW )US$18.0027黄金 Gold (ZG )US$15.0064新华富时中国A50 Xinhua A50(CN )US$8.0028小型黄金 Mini Gold (YG )US$15.0065EUREX (歐洲期貨交易德国法兰克福DAX 30指数(DAX )EUR 15.0029白银 Silver (ZI )US$15.0066BMD(马来西亚期交所)棕榈油 Crude Palm Oil ( FCPO )MYR 5030小型白银 Mini Silver (YI )US$15.0067恒生指数期货 Hang Seng Index ( HSI )HKD 80.0031伦敦富时100指数(FTSE100)GBP 15.0068小型恒生指数期货 Mini Hang Seng Index( MHI )HKD 60.0032巴黎CAC40指数(CAC )EUR 15.0069H 股指数期货 H-Share Index ( HHI )HKD 80.0033棉花 Cotton (CT )US$20.0070小型H股指数期货 Mini H-Share Index(MCH )HKD 60.0034可可 Cocoa (CC )US$20.0071人民幣期貨合約 US/RMB Futures (CUS )RMB 80.0035咖啡 Coffee (KC )US$20.0036原糖No.11 Sugar No.11(SB )US$15.0037美元指数 US Dollar Index (DX )US$20.00*恒生指数期货: 交易所费用 HK$10.00 证监会征费 HK$0.80 共HK$10.80**小型恒生指数期货: 交易所费用 HK$3.50 证监会征费 HK$0.16 共HK$3.66***H 股指数期货: 交易所费用 HK$3.50 证监会征费 HK$0.80 共HK$4.30此表会不断更新,如有查询请联系本公司.地址:香港上环干诺道西3号亿利商业大厦23楼B 室Tel:2573 9868Address:B,23/F,Yardley Commercial Building,No.3,Connaught Road West,Sheung Wan,HKFax:2573 9123HKEX(香港交易所)标准 交易品种佣金表TOCOM (东京商品交易所)CME (芝加哥商业交易所)CBOT (芝加哥商业及交易所)NYSE-Liffe (纽约泛欧交易所)中 國 國 際 期 貨 (香 港) 有 限 公 司China International Futures (Hong Kong) Company LimitedICE-NYBOT (纽约期货交易所)ICE- IPE (洲际交易所)CME (芝加哥商业交易所)LME (伦敦金属交易所)SGX (新加坡国际交易所)。

hkfrs-int11 Group and Treasury Share Transactions

HK(IFRIC)-Int11Issued January 2007Effective for annual periodsbeginning on or after 1 March 2007HKFRS 2–Group and Treasury Share TransactionsCOPYRIGHT© Copyright 2008 Hong Kong Institute of Certified Public AccountantsThis Hong Kong Financial Reporting Standard contains International Accounting Standards Committee Foundation copyright material. Reproduction within Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and inquiries concerning reproduction and rights for commercial purposes within Hong Kong should be addressed to the Director, Operation and Finance, Hong Kong Institute of Certified Public Accountants, 37/F., Wu Chung House, 213 Queen's Road East, Wanchai, Hong Kong.All rights in this material outside of Hong Kong are reserved by International Accounting Standards Committee Foundation. Reproduction of Hong Kong Financial Reporting Standards outside of Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce for commercial purposes outside Hong Kong should be addressed to the International Accounting Standards Committee Foundation at .CONTENTSparagraphs HONG KONG (IFRIC) INTERPRETATION 11HKFRS 2–GROUP AND TREASURY SHARE TRANSACTIONSREFERENCESISSUES 1–6 CONCLUSIONS 7–11 EFFECTIVE DATE 12 TRANSITION 13 ILLUSTRATIVE EXAMPLEBASIS FOR CONCLUSIONSHong Kong (IFRIC) Interpretation 11 HKFRS 2–Group and Treasury Share Transactions (HK(IFRIC)-Int 11) is set out in paragraphs 1-13. HK(IFRIC)-Int 11is accompanied by an Illustrative Example and a Basis for Conclusions. The scope and authority of Interpretations are set out in the Preface to Hong Kong Financial Reporting Standards.Hong Kong (IFRIC) Interpretation 11HKFRS 2–Group and Treasury Share TransactionsReferences• HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors• HKAS 32 Financial Instruments: Presentation• HKFRS 2 Share-based PaymentIssues1 This Interpretation addresses two issues. The first is whether the followingtransactions should be accounted for as equity-settled or as cash-settled under the requirements of HKFRS 2:(a) an entity grants to its employees rights to equity instruments of the entity (egshare options), and either chooses or is required to buy equity instruments (ietreasury shares) from another party, to satisfy its obligations to its employees;and(b) an entity’s employees are granted rights to equity instruments of the entity (egshare options), either by the entity itself or by its shareholders, and theshareholders of the entity provide the equity instruments needed.2 The second issue concerns share-based payment arrangements that involve two ormore entities within the same group. For example, employees of a subsidiary are granted rights to equity instruments of its parent as consideration for the services provided to the subsidiary. HKFRS 2 paragraph 3 states that:For the purposes of this HKFRS, transfers of an entity’s equity instruments byits shareholders to parties that have supplied goods or services to the entity(including employees) are share-based payment transactions, unless thetransfer is clearly for a purpose other than payment for goods or servicessupplied to the entity. This also applies to transfers of equity instruments ofthe entity’s parent, or equity instruments of another entity in the same groupas the entity, to parties that have supplied goods or services to the entity.[Emphasis added]However, HKFRS 2 does not give guidance on how to account for such transactions in the individual or separate financial statements of each group entity.3 Therefore, the second issue addresses the following share-based paymentarrangements:(a) a parent grants rights to its equity instruments direct to the employees of itssubsidiary: the parent (not the subsidiary) has the obligation to provide theemployees of the subsidiary with the equity instruments needed; and(b) a subsidiary grants rights to equity instruments of its parent to its employees:the subsidiary has the obligation to provide its employees with the equityinstruments needed.4 This Interpretation addresses how the share-based payment arrangements set out inparagraph 3 should be accounted for in the financial statements of the subsidiary that receives services from the employees.5 There may be an arrangement between a parent and its subsidiary requiring thesubsidiary to pay the parent for the provision of the equity instruments to the employees. This Interpretation does not address how to account for such an intragroup payment arrangement.6 Although this Interpretation focuses on transactions with employees, it also applies tosimilar share-based payment transactions with suppliers of goods or services other than employees.ConclusionsShare-based payment arrangements involving an entity’s own equity instruments (paragraph 1)7 Share-based payment transactions in which an entity receives services asconsideration for its own equity instruments shall be accounted for as equity-settled.This applies regardless of whether the entity chooses or is required to buy those equity instruments from another party to satisfy its obligations to its employees under the share-based payment arrangement. It also applies regardless of whether:(a) the employee’s rights to the entity’s equity instruments were granted by theentity itself or by its shareholder(s); or(b) the share-based payment arrangement was settled by the entity itself or by itsshareholder(s).Share-based payment arrangements involving equity instruments of the parentA parent grants rights to its equity instruments to the employees of itssubsidiary (paragraph 3(a))8 Provided that the share-based arrangement is accounted for as equity-settled in theconsolidated financial statements of the parent, the subsidiary shall measure the services received from its employees in accordance with the requirements applicable to equity-settled share-based payment transactions, with a corresponding increase recognised in equity as a contribution from the parent.9 A parent may grant rights to its equity instruments to the employees of its subsidiaries,conditional upon the completion of continuing service with the group for a specified period. An employee of one subsidiary may transfer employment to another subsidiary during the specified vesting period without the employee’s rights to equity instruments of the parent under the original share-based payment arrangement being affected. Each subsidiary shall measure the services received from the employee by reference to the fair value of the equity instruments at the date those rights to equity instruments were originally granted by the parent as defined in HKFRS 2 Appendix A, and the proportion of the vesting period served by the employee with each subsidiary.10 Such an employee, after transferring between group entities, may fail to satisfy avesting condition other than a market condition as defined in HKFRS 2 Appendix A, eg the employee leaves the group before completing the service period. In this case, each subsidiary shall adjust the amount previously recognised in respect of the services received from the employee in accordance with the principles in HKFRS 2 paragraph 19. Hence, if the rights to the equity instruments granted by the parent do not vest because of an employee’s failure to meet a vesting condition other than a market condition, no amount is recognised on a cumulative basis for the services received from that employee in the financial statements of any subsidiary.A subsidiary grants rights to equity instruments of its parent to its employees(paragraph 3(b))11 The subsidiary shall account for the transaction with its employees as cash-settled.This requirement applies irrespective of how the subsidiary obtains the equity instruments to satisfy its obligations to its employees.Effective date12 An entity shall apply this Interpretation for annual periods beginning on or after 1March 2007. Earlier application is permitted. If an entity applies this Interpretation for a period beginning before 1 March 2007, it shall disclose that fact.Transition13 An entity shall apply this Interpretation retrospectively in accordance with HKAS 8,subject to the transitional provisions of HKFRS 2.Illustrative ExampleThis example accompanies, but is not part of, HK(IFRIC)-Int 11.IE1 A parent grants 200 share options to each of 100 employees of its subsidiary, conditional upon the completion of two years’ service with the subsidiary. The fair value of the share options on grant date is CU30 each. At grant date, the subsidiary estimates that 80 per cent of the employees will complete the two-year service period.This estimate does not change during the vesting period. At the end of the vesting period, 81 employees complete the required two years of service. The parent does not require the subsidiary to pay for the shares needed to settle the grant of share options.IE2 The share-based payment transaction in the consolidated financial statements of the parent is accounted for as equity-settled in accordance with HKFRS 2.IE3 As required by HK(IFRIC)-Int 11 paragraph 8, over the two-year vesting period, the subsidiary measures the services received from the employees in accordance with the requirements applicable to equity-settled share-based payment transactions. Thus, the subsidiary measures the services received from the employees on the basis of the fair value of the share options at grant date. An increase in equity is recognised as a contribution from the parent in the financial statements of the subsidiary.IE4 The journal entries recorded by the subsidiary for each of the two years are as follows: Year 1Dr Remuneration expense CU240,000× 100 × 30 × 0.8/2)(200Cr Equity (Contribution from the parent) CU240,000Year 2Dr Remuneration expense CU246,000(200× 100 × 30 × 0.81 – 240,000)Cr Equity (Contribution from the parent) CU246,000Basis for Conclusions onHK(IFRIC)-Int 11This Basis for Conclusions accompanies, but is not part of, HK(IFRIC)-Int 11.HK(IFRIC)-Int 11 is based on IFRIC Interpretation 11 IFRS 2–Group and Treasury Share Transactions. In approving HK(IFRIC)-Int 11, Council of the Hong Kong Institute of Certified Public Accountants considered and agreed with the IFRIC’s Basis for Conclusions on IFRIC Interpretation 11. Accordingly, there are no significant differences between HK(IFRIC)-Int 11 and IFRIC Interpretation 11. The IFRIC’s Basis for Conclusions is reproduced below. The paragraph numbers of IFRIC Interpretation 11 referred to below generally correspond with those in HK(IFRIC)-Int 11.IntroductionBC1 This Basis for Conclusions summarises the IFRIC’s considerations in reaching its consensus. Individual IFRIC members gave greater weight to some factors than to others.BC2 The IFRIC released draft Interpretation D17 IFRS 2–Group and Treasury Share Transactions for public comment in May 2005. It received 40 letters in response. Consensus (paragraphs 7-11)Share-based payment arrangements involving an entity’s own equity instruments (paragraph 7)BC3 D17 proposed that, regardless of whether the entity chooses or is required to buy the equity instruments needed from another party to settle the share-based payment arrangement, the share-based payment transactions should be accounted for as equity-settled. The IFRIC’s rationale was that the consideration for the services received is equity instruments of the entity (rather than a liability to transfer cash or other assets). For the same reason, the IFRIC proposed in D17 that, regardless of whether the employees’ rights to the entity’s equity instruments were granted by the entity itself or by its shareholders, or whether the obligations under the share-based payment arrangement were settled by the entity itself or its shareholders, the share-based payment transactions should be accounted for as equity-settled.BC4 Of the 40 respondents to D17, only a small number disagreed with D17’s proposal to treat the transactions as equity-settled.BC5 For the reason stated in paragraph BC3, the IFRIC reaffirmed its view that the share-based payment transactions specified in IFRIC 11 paragraph 1(a) and (b) should be accounted for as equity-settled.BC6 Some respondents asked the IFRIC to clarify whether an entity should recognise a financial liability when the entity enters into a contractual arrangement to acquire its own equity instruments. The IFRIC noted that the relevant requirements in IAS 32 Financial Instruments: Presentation are clear. Therefore, the IFRIC decided not to explain those requirements in the Interpretation.Share-based payment arrangements involving equity instruments of the parent (paragraphs 8-11)BC7 D17 addressed the following share-based payment arrangements in which two or more entities in the same group are involved:(a) a parent grants rights to its equity instruments direct to its subsidiary’semployees; and(b) an entity grants rights to equity instruments of its parent to its employees.A parent grants rights to its equity instruments to the employeesof its subsidiary (paragraph 8)BC8 The IFRIC noted that paragraph 3 of IFRS 2 Share-based Payment requires an entity to recognise as share-based payment arrangements transfers of equity instruments ofthe entity’s parent to parties that have supplied goods or services to the entity.However, the IFRIC observed that, for the purposes of the preparation of the financialstatements of the subsidiary, the transaction described in paragraph BC7(a) does not meet the definition of either an equity-settled share-based payment transaction or a cash-settled share-based payment transaction. In this situation, the equity instruments granted are not the equity instruments of the subsidiary and the subsidiary has no obligation to transfer cash or other assets to the employees.BC9 Because the subsidiary does not have an obligation to deliver cash or other assets to the employees, the IFRIC proposed in D17 that it was not appropriate to account for the transaction as cash-settled in the financial statements of the subsidiary. Instead, the IFRIC suggested that the equity-settled basis was more consistent with the principles in IFRS 2.BC10 Of the 40 respondents to D17, only a small number disagreed that the transaction should be accounted for as equity-settled in the financial statements of the subsidiary. BC11 The IFRIC noted that the parent has an involvement in the arrangement by committing itself to provide the employees of the subsidiary with its equity instruments. To meet the requirement in IFRS 2 paragraph 3, the IFRIC believed that it was appropriate in this particular situation for the subsidiary in its own financial statements to apply the same measurement basis as the parent uses in its consolidated financial statements.Accordingly, the IFRIC concluded that, provided that the transaction is accounted for as equity-settled in the consolidated financial statements of the parent, the services received from the employees should be measured using the equity-settled basis in thefinancial statements of the subsidiary. Correspondingly, to reflect the parent’s grantingof rights to its equity instruments to the employees of the subsidiary, the IFRIC decided that the subsidiary should recognise in its equity a contribution from the parent equal to the amount at which the services from the employees are measured. BC12 The IFRIC discussed whether the Interpretation should address how to account for an intragroup payment arrangement requiring the subsidiary to pay the parent for the provision of the equity instruments to the employees. The IFRIC decided not to address that issue because it did not wish to widen the scope of the Interpretation to an issue that relates to the accounting for intragroup payment arrangements generally.A subsidiary grants rights to equity instruments of its parent to itsemployees (paragraph 11)BC13 Although the subsidiary in the transaction described in paragraph BC7(b) has an obligation to its employees, the obligation is not determined on the basis of the price of its own equity instruments. Thus, the transaction does not meet the definition of a cash-settled share-based payment transaction in the financial statements of the subsidiary. In addition, because the equity instruments provided to the employees arenot equity instruments of the subsidiary, the transaction does not meet the definition ofan equity-settled share-based payment transaction either in the financial statements of the subsidiary.BC14 D17 proposed that the subsidiary should account for the transaction with its employees as cash-settled in its own financial statements. The rationale was that the cash-settled basis was more consistent with the principles in IFRS 2 because the subsidiary has an obligation to provide its employees with the equity instruments of the parent, which are treated as assets of the subsidiary when the subsidiary acquires them.BC15 Many respondents to D17 disagreed with the proposed treatment. They disagreed that the accounting treatments for the two types of arrangement described in paragraph BC7 should depend on which entity grants to the employees rights to equity instruments of the parent. In their view, regardless of whether the parent or the subsidiary grants those rights to the employees, in most cases the parent is the one that supplies the equity instruments to settle the obligation. They believed that it was not appropriate to require the subsidiary to apply different accounting treatments to transactions with the same substance. They had concerns that different accounting treatments would give entities opportunities to structure their intragroup transactions in order to achieve desired accounting results.BC16 The IFRIC noted that arrangements described in paragraph BC7(a) and (b) might be the same in the consolidated financial statements of the parent, and also from the perspective of the employees who receive the equity instruments. However, from the perspective of the subsidiary, the IFRIC observed that the two arrangements are different. The IFRIC noted that under arrangement (a) the parent, rather than the subsidiary, has the obligation to provide its employees with the equity instruments, whereas under arrangement (b) it is the subsidiary that has that obligation.BC17 In addition, the IFRIC clarified that how the subsidiary acquires the equity instruments needed to meet its obligation to its employees is a separate transaction from its transaction with its employees.BC18 For the above reasons, the IFRIC reaffirmed its view that the transaction with the employees described in paragraph BC7(b) should be accounted for as cash-settled in the financial statements of the subsidiary.Transfers of employees between group entities(paragraphs 9 and 10)BC19 The IFRIC noted that some share-based payment arrangements involve a parent granting rights to the employees of more than one subsidiary with a vesting condition that requires the employees to work for the group for a particular period. Sometimes, an employee of one subsidiary transfers employment to another subsidiary during the vesting period, without the employee’s rights under the original share-based payment arrangements being affected. The IFRIC reasoned in D17 that the change of employment from one group entity to another does not represent a new grant of equity instruments, because the equity instruments were granted by the parent (not the individual subsidiary). Therefore, the IFRIC proposed in D17 that the subsidiary to which the employee transfers employment should measure the fair value of the services received from the employee by reference to the fair value of the equity instruments at the date those equity instruments were originally granted to the employee by the parent.BC20 The respondents to D17 generally supported this proposed treatment. Some respondents also asked the IFRIC to clarify the following two points:(a) whether the transfer of employees between group entities would beconsidered as a failure to satisfy a vesting condition in the financialstatements of the subsidiary from which the employees transferredemployment (ie whether that subsidiary should reverse the charge previouslyrecognised in respect of the services received from such employees); andHKFRS 2–GROUP AND TREASURY SHARE TRANSACTIONS(b) after the transfer of employment, if an employee leaves the group during thevesting period, whether each subsidiary should reverse the charge previouslyrecognised in respect of the services from that employee during the vestingperiod.BC21 The terms of the original share-based payment arrangement require the employees to work for the group, rather than for a particular group entity. Thus, the IFRIC in its redeliberations reaffirmed its view that the change of employment should not result ina new grant of equity instruments in the financial statements of the subsidiary to whichthe employees transferred employment. For the same reason, the IFRIC concluded that the transfer itself should not be treated as an employee’s failure to satisfy a vesting condition. Thus, the transfer should not trigger any reversal of the charge previously recognised in respect of the services received from the employee in the financial statements of the subsidiary from which the employee transfers employment. BC22 The IFRIC noted that IFRS 2 paragraph 19 requires the cumulative amount recognised for goods or services as consideration for the equity instruments granted to be based on the number of equity instruments that eventually vest. Accordingly, ona cumulative basis, no amount is recognised for goods or services if the equityinstruments do not vest because of failure to satisfy a vesting condition other than a market condition as defined in IFRS 2 Appendix A. Applying the principles in IFRS 2 paragraph 19, the IFRIC concluded that when the employee fails to satisfy a vesting condition other than a market condition, the services from that employee recognised in the financial statements of each subsidiary during the vesting period should be reversed.© Copyright 10 HK(IFRIC)-Int 11。

本币交易系统功能介绍(其他功能点介绍)(1)

17

可快速撤销的报价包括:对话报价、单边点击成交报价、做市报价(双边报价)、限价报

意向报价不可一键撤销

3.交易流程

3.3.3 辅助功能:批量报价 ★

适用于所有报价方式 批量报价一次最多发送100笔 导出、导入Excel文件

18

导出excel文件

导入excel文件

3.前台辅助功能

3.3.4 辅助功能:布局管理 ★★

显示存款机构利 率债法发起报价,请检查是否 处于中后台子系统

2.中后台其他功能

2.1.2 中后台其他功能:信息查询 ★

信息查询菜单下可查询以下信息:

• 本方报价 • 本方成交 • 市场行情 • 本方头寸 • 关联机构 • 限额 • 风控比例 • 交易交易工具信息 • 做市券种信息 • 公告 • 交易手续费 • 缴费通知单 • …… 根据机构权限和交易员 权限显示

• 比前收盘净价高以红色字体显示 • 比前收盘净价低以绿色字体显示 • 比当日上一笔成交净价高以红色向上箭头表示 • 比当日上一笔成交净价低以绿色向下箭头表示

31

3.前台辅助功能

提纲 1. 概述及市场服务 2. 中后台其他功能介绍 3. 前台辅助功能介绍 4. 其他市场交易流程 5. 创新交易

32

• 证书助手(3.0驱动)(推荐),证书管理器(2.28驱动) • 都提供密码修改和证书信息查询功能

证书更新:

• 证书有效期为5年 • 证书到期日前90天和后90天可进行证书更新 3.前台辅助功能

3.2 用户管理:交易员资格证书管理 ★

前台子系统-资格证书管理 1、查看本人已激活用户的用户权限 2、进行关联机构用户的激活(基金等非法人投资产品) 3、解除本人的激活信息

3.前台辅助功能

跨境清算公司港币支付业务操作指引

跨境清算公司港币支付业务操作指引第一条为进一步规范信托公司私人股权投资信托业务的经营行为,保障私人股权投资信托各方当事人的合法权益,根据《信托公司管理办法》、《信托公司集合资金信托计划管理办法》等监管规章,制定本指引。

第二条本指引所称私人股权投资信托,是指信托公司将信托计划项下资金投资于未上市企业股权、上市公司限售流通股或中国银监会批准可以投资的其他股权的信托业务。

信托公司以信托资金投资于境外已上市企业股权的,应当经中国银监会及有关监管部门核准;私人股权投资信托投资于金融机构和拟将上市公司股权的,应当严格遵守有关金融监管部门的规定。

(一)具有完善的公司治理结构;(二)具备健全的内部掌控制度和风险管理制度;(三)为股权投资信托业务配备与业务相适应的信托经理及相关工作人员,负责股权投资信托的人员达到5人以上,其中至少名具备2年以上股权投资或相关业务经验;(四)固有资产状况和流动性较好,合乎监管建议;(五)中国银监会规定的其他条件。

第四条信托公司应制订私人股权投资信托业务流程和风险管理制度,经公司董事会批准后继续执行。

第五条私人股权投资信托风险管理制度包括但不限于以下内容:(一)目标企业的投资立项;(二)目标企业的实地尽职调查;(三)投资决策流程及限额管理;(四)目标企业的投资实施;(五)目标企业的管理;(六)目标企业股权的退出机制。

(一)严格遵守有关法律法规的规定,且信托目的严禁侵害社会公共利益;(三)信托期限与股权退出安排相匹配,持股期限相对稳定,并在信托文件中明确股权退出安排;(四)以固有资金参予私人股权投资信托计划的,应严格遵守信托公司净资本管理的有关规定,且在信托除斥期间不受让受益权,也严禁轻易或间接以该受益权为标的展开融资。

第八条信托公司开展私人股权投资信托业务时,应对该信托计划投资理念及策略、项目选取标准、行业价值、备选企业和风险因素分析方法等制作报告书,并经公司信托委员会通过。

第九条信托公司运用私人股权投资信托计划项下资金展开股权投资时,应付拟将投资对象的发展前景、公司环境治理、股权结构、管理团队、资产情况、经营情况、财务状况、法律风险等积极开展合规调查。

最大回撤 香港术语

最大回撤香港术语下载温馨提示:该文档是我店铺精心编制而成,希望大家下载以后,能够帮助大家解决实际的问题。

文档下载后可定制随意修改,请根据实际需要进行相应的调整和使用,谢谢!并且,本店铺为大家提供各种各样类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,如想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by the editor. I hope that after you download them, they can help yousolve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you!In addition, our shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts,other materials and so on, want to know different data formats and writing methods, please pay attention!投资者在进行股票交易时,总是希望获得尽可能高的收益,然而市场的波动不可避免,投资也存在风险。

香港外汇市场

原載《HKCER Letters》一九九八年五月第五十期香港外匯市場張賢旺香港外匯市場的規模在全球高踞前列。

國際結算銀行在一九九六年的調查發現,香港已超越瑞士,在全球外匯市場中排名第五。

一九九五四月,每日平均交易超過九百億美元。

香港被視為國際上一個主要的國際金融中心(簡稱“IFC”),部分拜外匯市場地位之賜。

不論香港還是內地官員,均深切明白金融部門在香港經濟中的重要性。

《基本法》即明文維護香港的國際金融中心地位。

香港的外匯市場在全球舉足輕重,與其他金融環節的關係又如此密切,若能維持健康的發展,將有利於加強以至提升香港的國際金融中心角色。

另一方面,香港的國際金融中心地位為外匯市場提供了健康的經營環境,有利其發展。

為了了解香港這方面的現狀、探討其前景,於一九九五年和九六年間,作者在港對銀行同業市場從業員進行問卷調查,發覺從業員對香港的外匯市場頗有一些相當有趣並有見地的看法。

下文簡述這次調查的結果。

從業員大都相信,外匯市場成功以賴的主要特點,香港都不缺(見英文表一)。

逾半被訪者認為,“政治穩定”、“資金和外匯不受管制”、“自由友善的經商環境”、“優良的基礎建設”、“訓練有素的金融專才”及“國際金融中心地位”是香港外匯市場得以成功的要素。

另一方面,略低於半數的被訪者認為,“與內地的貿易和金融關係”是香港外匯業務一個最重要的領域。

調查發現,在所有因素中,香港最不利的是經營成本。

這顯示房地產和勞工成本高漲,對經濟活動已產生不良的影響。

至於今後五年內,香港能否繼續享有上述的有利因素,以著名的外匯中心屹立於世,被訪者則稍有保留。

“資金和外匯不受管制”和“自由友善的商業環境”這兩個因素在回應率中跌幅最大。

香港回歸後,能否保持國際金融中心的各種有利因素,視乎中央政府的政策和行動。

至今為止,這方面的發展相當令人鼓舞。

香港享有高度的自治,中央政府也再度就香港的國際金融中心地位作出保證。

另一方面,較多被訪者預期,“與內地的貿易和金融關係”將會在今後五年內對香港的外匯業務作出更大的貢獻。

外汇基础知识培训课件hkns

各国现行利率表

外汇交易

• 外汇交易是针对不同国家的货币汇率日常波动,进行赚取 差价的一种金融交易行为。

• 举例来说:根据你对市场上欧元与美元的汇率的观察,你 认为当前欧元对美元的汇率是被低估了,你估计欧元会在 未来时间走强。于是,你提前买入一定数量的欧元。如果 市场的走向与你的判断吻合,欧元对美元升值了,这时你 就卖出欧元换回美元,达到了获利。相反,如果欧元对美 元继续贬值,那么你就亏损了。

汇率的标价方法:

◇ 直接标价法---以本国货币为基准货币的表示方法。即 一个单位的本国货币可以兑换若干单位的美元。该货币数 字增大,表示本国货币上升,反之。如EUR,GBP,AUD

◇ 间接标价法---以美元为基准货币的表示方法。即一 个单位的美元可以兑换若干单位的本国货币。该货币数值 增大时,表示本国货币下跌,反之。JPT,CHF,CAD

欧洲时段(法兰克福、伦敦) 14:30---00:30

美洲时段(纽约、美国) 20:20---04:00

主要外汇市场交易时间段

Hale Waihona Puke • 纽西兰 • 悉尼 • 东京 • 法兰克福 • 伦敦 • 纽约

06:00—11:00 07:00—12:00 08:00—14:00 14:00—23:00/15:00—24:00 15:30—23:30/16:30—00:30 20:20—03:30/21:20—04:00

外汇市场的特点

• 1、有市无场

• 2、循环作业 • 3、真正公平、公开、公正 • 4、零和游戏

主要外汇市场

• 1、伦敦外汇交易市场 • 2、纽约外汇交易市场 • 3、法兰克福外汇交易市场 • 4、东京外汇交易市场 • 5、新加坡外汇交易市场 • 6、瑞士苏黎士外汇交易市场

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

香港 2011 市场指南

索引 主要交易所 .................................................................................................................................................... 5 名称 ............................................................................................................................................................ 5 交易所商标 ................................................................................................................................................ 5 扩展名 ........................................................................................................................................................ 5 国家货币 .................................................................................................................................................... 5 网站 ............................................................................................................................................................ 5 历史 ............................................................................................................................................................ 5 交易资产类型 ............................................................................................................................................ 6 中国通过香港证交所交易的公司 ............................................................................................................ 7 ATS 运营在香港 ............................................................................................................................................. 7 概貌 ............................................................................................................................................................ 7 瑞银 CROSSFINDER ........................................................................................................................................ 7 地方监管当局 ................................................................................................................................................ 8 证券及期货事务监察委员会 (SFC) ........................................................................................................... 8 在香港交易 .................................................................................................................................................. 10 交易时间 .................................................................................................................................................. 10 单子薄类型 .............................................................................................................................................. 11 卖空 .......................................................................................................................................................... 11 竞价机制 .................................................................................................................................................. 11 单子股数 .................................................................................................................................................. 13 价格增量 .................................................................................................................................................. 13 价格变动限制 .......................................................................................................................................... 14 错误的交易 .............................................................................................................................................. 14 市场不当处理 .......................................................................................................................................... 15 Pablo Torre 香港 市场指南 页数 2 之 22

香港 2011 市场指南

单子类型 .................................................................................................................................................. 16 系统限制 .................................................................................................................................................. 16 交易费用 .................................................................................................................................................. 16 市场指数 ...............................................................................................................................