财务分析第四版课后习题译文 词汇表

财务管理常用术语(英汉对照)

Business cycle (of a firm) (1) 经营周期 从权益资本,筹集新债务,和 通过资产收购来增长业务的一系列事件,这 样,又开始一个新的周期。

Business risk (1,5,10,11) 经营风险 经济风险 和营业风险的累积影响,来源于公司不可能 知道目前投资和营业活动 /决策的确定结果。

347

公经理人员财务管理—创造价值的过程

下载

作为发行证券公司的代理人尽最大努力销售 证券的一种证券分销方式。 Beta (coefficient) (10) ß系数 基于一种私人股 票的回报率变化相对于股票市场指数回报率 变化的敏感性的风险测量工具。与系统风 险,市场风险,不可分散风险,和相对风险 同义。 Bid-ask spread (13) 买卖价差 买价与卖价之间 的差额。 Bid price (13) 买价 市场交易者愿意购买的价 格。 Bidder (12) 投标商 在收购中,想购买另一家 公司全部或部分股份的公司。 Bond (9) 债券 说明债权人与发行公司之间关系和 规定资金借入和偿还的条件和条款的一种负 债证券。 Bond market (9) 债券市场 发行和交易债券的 市场。 Bond rating (9) 债券等级评定 由代理机构 (例 如标准普尔和莫迪投资服务公司 )评定的等 级以提供一种债券信用风险的估计。 Bond value (9) 债券价值 债券预期现金流序列 以与现金流序列的风险相联系的贴现率折 现的现值。 Bond value of a convertible bond (9)可转换债 券的债券价值 如果可转换债券没有转换选择权 的价值。 Bonding costs (11) 债券发行成本 贷款人对管 理灵活性设置限制性条款导致的成本 (由股 东承担 )。 Book value of asset (2) 资产的账面价值 资产 在公司资产负债表中列示的价值。 Book value of equity (1,2) 所有者权益的账面价 值 Book value multiple (12) 账面价值乘数 股价 除以每股权益账面价值。与 price-to-book ratio同义。用于公司价值估计。 Bookrunner (9) 发起人 Bottom line (2) 净收益 Brokers (9) 经纪人 不拥有证券,代表第三方 进行证券交易的个人或机构。 Business assets (5) 营业资产 营运资本需求 加净固定资产。

财务报表分析(第4版)练习题参考答案

财务报表分析(第四版)练习题参考答案第1章基本财务报表★网络习题略★业务题1.(1)年末资产总额=年末负债总额+年末所有者权益总额=20,000+30,000=50,000(元)年初资产总额=年末资产总额-20×1年度资产增加额=50,000-10,000=40,000(元)年初所有者权益总额=年初资产总额-年初负债总额=40,000-25,000=15,000(元)20×1年度利润=年末所有者权益总额-年初所有者权益总额-20×1年度资本投入净额=30,000-15,000-4,000=11,000(元)或者:所有者权益变动额=资产变动额-负债变动额=10,000-(20,000-25,000)=15,000(元)20×1年度利润=所有者权益变动额-20×1年度资本投入金额=15,000-4,000=11,000(元)(2)尽管根据前后两期的资产负债表就可以计算出当期利润,但是,这只是履行会计的内部职能(会计核算)。

基于现代企业制度与金融市场框架,会计还需要履行其外部功能,对外披露有助于决策的信息。

财务报表(利润表)是会计履行其外部职能的重要载体。

况且,利润表不仅仅要披露当期利润的数额,更要充分展现当期利润的形成过程。

因此,企业还要编制利润表。

2.(1)某服务企业20×1年度的利润表和资产负债表(2)某服务企业20×1年12月31日的未分配利润为13,516元。

★案例分析2.由此可能导致中间指标如销售毛利、营业利润、营业外收支净额和利润总额等有用信息的缺失。

第2章财务报表分析基本框架★案例分析1.(1)亨利与银行之间可能存在的利益冲突:股东作为“分享”阶层与债权人作为“支薪”的利益冲突。

债权人只关注“还本付息”问题。

(2)亨利与其他股东之间可能存在的利益冲突:大股东与小股东的利益冲突。

(3)亨利企业的经理与亨利和其他股东之间可能存在的利益冲突:经理作为“支薪”阶层与股东作为“分享”阶层的利益冲突,由此可能产生“道德风险”与“逆向选择”问题。

财务报表分析课后习题答案

财务报表分析课后习题答案第一章财务报表分析概述一、名词解释财务报表分析筹资活动投资活动经营活动会计政策会计估计资产负债表日后事项二、单项选择1.财务报表分析的对象是企业的基本活动,不是指()。

A筹资活动B投资活动C经营活动D全部活动2.企业收益的主要来源是()。

A经营活动B 投资活动C筹资活动D 投资收益3.短期债权包括()。

A 融资租赁B银行长期贷款C 商业信用D长期债券4.下列项目中属于长期债权的是()。

A短期贷款B融资租赁C商业信用D短期债券5.在财务报表分中,投资人是指()。

A 社会公众B 金融机构C 优先股东D 普通股东6.流动资产和流动负债的比值被称为()。

A流动比率B 速动比率C营运比率D资产负债比率7.资产负债表的附表是()。

A利润分配表B分部报表C财务报表附注D应交增值税明细表。

8.利润表反映企业的()。

A财务状况B经营成果C财务状况变动D现金流动9.我国会计规范体系的最高层次是()。

A企业会计制度B企业会计准则C会计法D会计基础工作规范10.注册会计师对财务报表的()。

A公允性B真实性C正确性D完整性三、多项选择1.财务报表分析具有广泛的用途,一般包括()。

A.寻找投资对象和兼并对象B.预测企业未来的财务状况C.预测企业未来的经营成果D. 评价公司管理业绩和企业决策E.判断投资、筹资和经营活动的成效2.分析可以分为()等四种。

A 定性分析B定量分析C因果分析D系统分析E以上几种都包括3.财务报表分析的主体是()。

A 债权人B 投资人C 经理人员D 审计师E 职工和工会4.作为财务报表分析主体的政府机构,包括()。

A税务部门B国有企业的管理部门C证券管理机构D会计监管机构E社会保障部门5.财务报表分析的原则可以概括为()。

A目的明确原则B动态分析原则C系统分析原则D成本效益原则E实事求是原则6.在财务报表附注中应披露的会计政策有()。

A坏账的数额B收入确认的原则C 所得税的处理方法D存货的计价方法E固定资产的使用年限7.在财务报表附注中应披露的会计政策有()。

财务英语基础词汇表中英文对照

1 资产assets11~ 12 流动资产current assets111 现金及约当现金cash and cash equivalents1111 库存现金cash on hand1112 零用金/周转金petty cash/revolving funds1113 银行存款cash in banks1116 在途现金cash in transit1117 约当现金cash equivalents1118 其它现金及约当现金other cash and cash equivalents 112 短期投资short-term investment1121 短期投资-股票short-term investments - stock1122 短期投资-短期票券short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds1124 短期投资-受益凭证short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds1128 短期投资-其它short-term investments - other1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现discounted notes receivable1137 应收票据-关系人notes receivable - related parties 1138 其它应收票据other notes receivable1139 备抵呆帐-应收票据allowance for uncollectible accounts- notes receivable114 应收帐款accounts receivable1141 应收帐款accounts receivable1142 应收分期帐款installment accounts receivable1147 应收帐款-关系人accounts receivable - related parties 1149 备抵呆帐-应收帐款allowance for uncollectible accounts - accounts receivable118 其它应收款other receivables1181 应收出售远汇款forward exchange contract receivable 1182 应收远汇款-外币forward exchange contract receivable - foreign currencies1183 买卖远汇折价discount on forward ex-change contract 1184 应收收益earned revenue receivable1185 应收退税款income tax refund receivable1187 其它应收款- 关系人other receivables - related parties 1188 其它应收款- 其它other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollectible accounts - other receivables121~122 存货inventories1211 商品存货merchandise inventory1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失allowance for reduction of inventory to market1221 制成品finished goods1222 寄销制成品consigned finished goods1223 副产品by-products1224 在制品work in process1225 委外加工work in process - outsourced1226 原料raw materials1227 物料supplies1228 在途原物料materials and supplies in transit1229 备抵存货跌价损失allowance for reduction of inventory to market125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费prepaid insurance1254 用品盘存office supplies1255 预付所得税prepaid income tax1258 其它预付费用other prepaid expenses126 预付款项prepayments1261 预付货款prepayment for purchases1268 其它预付款项other prepayments128~129 其它流动资产other current assets1281 进项税额VAT paid ( or input tax)1282 留抵税额excess VAT paid (or overpaid VAT)1283 暂付款temporary payments1284 代付款payment on behalf of others1285 员工借支advances to employees1286 存出保证金refundable deposits1287 受限制存款certificate of deposit-restricted1291 递延所得税资产deferred income tax assets1292 递延兑换损失deferred foreign exchange losses1293 业主(股东)往来owners(stockholders) current account 1294 同业往来current account with others1298 其它流动资产-其它other current assets - other13 基金及长期投资funds and long-term investments131 基金funds1311 偿债基金redemption fund (or sinking fund)1312 改良及扩充基金fund for improvement and expansion 1313 意外损失准备基金contingency fund1314 退休基金pension fund1318 其它基金other funds132 长期投资long-term investments1321 长期股权投资long-term equity investments1322 长期债券投资long-term bond investments1323 长期不动产投资long-term real estate in-vestments 1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资other long-term investments1329 备抵长期投资跌价损失allowance for excess of cost over market value of long-term investments14~ 15 固定资产property , plant, and equipment141 土地land1411 土地land1418 土地-重估增值land - revaluation increments142 土地改良物land improvements1421 土地改良物land improvements1428 土地改良物-重估增值land improvements - revaluation increments1429 累积折旧-土地改良物accumulated depreciation - landimprovements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值buildings -revaluation increments1439 累积折旧-房屋及建物accumulated depreciation - buildings144~146 机(器)具及设备machinery and equipment1441 机(器)具machinery1448 机(器)具-重估增值machinery - revaluation increments 1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产leased assets1511 租赁资产leased assets1519 累积折旧-租赁资产accumulated depreciation - leased assets152 租赁权益改良leasehold improvements1521 租赁权益改良leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment1561 未完工程construction in progress1562 预付购置设备款prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, and equipment16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resources -revaluation increments1619 累积折耗-天然资源accumulated depletion - natural resources17 无形资产intangible assets171 商标权trademarks1711 商标权trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权franchise174 著作权copyright1741 著作权copyright175 计算机软件computer software1751 计算机软件computer software cost176 商誉goodwill1761 商誉goodwill177 开办费organization costs1771 开办费organization costs178 其它无形资产other intangibles1781 递延退休金成本deferred pension costs1782 租赁权益改良leasehold improvements1788 其它无形资产-其它other intangible assets - other18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond issuance costs 1812 长期预付租金long-term prepaid rent1813 长期预付保险费long-term prepaid insurance 1814 递延所得税资产deferred income tax assets 1815 预付退休金prepaid pension cost1818 其它递延资产other deferred assets182 闲置资产idle assets1821 闲置资产idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据long-term notes receivable1842 长期应收帐款long-term accounts receivable1843 催收帐款overdue receivables1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others1851 出租资产assets leased to others1858 出租资产-重估增值assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others186 存出保证金refundable deposit1861 存出保证金refundable deposits188 杂项资产miscellaneous assets1881 受限制存款certificate of deposit - restricted1888 杂项资产-其它miscellaneous assets - other2 负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(debt)2111 银行透支bank overdraft2112 银行借款bank loan2114 短期借款-业主short-term borrowings - owners2115 短期借款-员工short-term borrowings - employees 2117 短期借款-关系人short-term borrowings- related parties2118 短期借款-其它short-term borrowings - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价discount on short-term notes andbills payable213 应付票据notes payable2131 应付票据notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据other notes payable214 应付帐款accounts pay able2141 应付帐款accounts payable2147 应付帐款-关系人accounts payable - related parties 216 应付所得税income taxes payable2161 应付所得税income tax payable217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金accrued rent payable2173 应付利息accrued interest payable2174 应付营业税accrued VAT payable2175 应付税捐-其它accrued taxes payable- other2178 其它应付费用other accrued expenses payable218~219 其它应付款other payables2181 应付购入远汇款forward exchange contract payable 2182 应付远汇款-外币forward exchange contract payable - foreign currencies2183 买卖远汇溢价premium on forward exchange contract2184 应付土地房屋款payables on land and building purchased2185 应付设备款Payables on equipment2187 其它应付款-关系人other payables - related parties 2191 应付股利dividend payable2192 应付红利bonus payable2193 应付董监事酬劳compensation payable to directors and supervisors2198 其它应付款-其它other payables - other226 预收款项advance receipts2261 预收货款sales revenue received in advance2262 预收收入revenue received in advance2268 其它预收款other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债other current liabilities2281 销项税额VAT received(or output tax)2283 暂收款temporary receipts2284 代收款receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities 2291 递延所得税负债deferred income tax liabilities2292 递延兑换利益deferred foreign exchange gain2293 业主(股东)往来owners current account2294 同业往来current account with others2298 其它流动负债-其它other current liabilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds payable2311 应付公司债corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款long-term loans payable2321 长期银行借款long-term loans payable - bank2324 长期借款-业主long-term loans payable - owners 2325 长期借款-员工long-term loans payable - employees 2327 长期借款-关系人long-term loans payable - related parties2328 长期借款-其它long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes payable2332 长期应付帐款long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities 2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税estimated accrued land value incremental tax pay-able235 应计退休金负债accrued pension liabilities2351 应计退休金负债accrued pension liabilities238 其它长期负债other long-term liabilities2388 其它长期负债-其它other long-term liabilities - other28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入deferred revenue2814 递延所得税负债deferred income tax liabilities2818 其它递延负债other deferred liabilities286 存入保证金deposits received2861 存入保证金guarantee deposit received288 杂项负债miscellaneous liabilities2888 杂项负债-其它miscellaneous liabilities - other3 所有者权益(股东权益)owners equity31 资本capital311 资本(或股本)capital3111 普通股股本capital - common stock3112 特别股股本capital - preferred stock3113 预收股本capital collected in advance3114 待分配股票股利stock dividends to be distributed3115 资本capital32 资本公积additional paid-in capital321 股票溢价paid-in capital in excess of par3211 普通股股票溢价paid-in capital in excess of par- common stock3212 特别股股票溢价paid-in capital in excess of par- preferred stock323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积capital surplus from gain on disposal of assets3241 处分资产溢价公积capital surplus from gain on disposal of assets325 合并公积capital surplus from business combination 3251 合并公积capital surplus from business combination 326 受赠公积donated surplus3261 受赠公积donated surplus328 其它资本公积other additional paid-in capital3281 权益法长期股权投资资本公积additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积legal reserve3311 法定盈余公积legal reserve332 特别盈余公积special reserve3321 意外损失准备contingency reserve3322 改良扩充准备improvement and expansion reserve 3323 偿债准备special reserve for redemption of liabilities 3328 其它特别盈余公积other special reserve335 未分配盈余(或累积亏损) retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏accumulated profit or loss3352 前期损益调整prior period adjustments3353 本期损益net income or loss for current period34 权益调整equity adjustments341 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments3411 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments342 累积换算调整数cumulative translation adjustment 3421 累积换算调整数cumulative translation adjustments 343 未认列为退休金成本之净损失net loss not recognized as pension cost3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股treasury stock351 库藏股treasury stock3511 库藏股treasury stock36 少数股权minority interest361 少数股权minority interest3611 少数股权minority interest4 营业收入operating revenue41 销货收入sales revenue411 销货收入sales revenue4111 销货收入sales revenue4112 分期付款销货收入installment sales revenue417 销货退回sales return4171 销货退回sales return419 销货折让sales allowances4191 销货折让sales discounts and allowances46 劳务收入service revenue461 劳务收入service revenue4611 劳务收入service revenue47 业务收入agency revenue471 业务收入agency revenue4711 业务收入agency revenue48 其它营业收入other operating revenue488 其它营业收入-其它other operating revenue4888 其它营业收入-其它other operating revenue - other5营业成本operating costs51 销货成本cost of goods sold511 销货成本cost of goods sold5111 销货成本cost of goods sold5112 分期付款销货成本installment cost of goods sold 512 进货purchases5121 进货purchases5122 进货费用purchase expenses5123 进货退出purchase returns5124 进货折让charges on purchased merchandise 513 进料materials purchased5131 进料material purchased5132 进料费用charges on purchased material5133 进料退出material purchase returns5134 进料折让material purchase allowances514 直接人工direct labor5141 直接人工direct labor515~518 制造费用manufacturing overhead5151 间接人工indirect labor5152 租金支出rent expense, rent5153 文具用品office supplies (expense)5154 旅费travelling expense, travel5155 运费shipping expenses, freight5156 邮电费postage (expenses)5157 修缮费repair(s) and maintenance (expense ) 5158 包装费packing expenses5161 水电瓦斯费utilities (expense)5162 保险费insurance (expense)5163 加工费manufacturing overhead - outsourced 5166 税捐taxes5168 折旧depreciation expense5169 各项耗竭及摊提various amortization5172 伙食费meal (expenses)5173 职工福利employee benefits/welfare5176 训练费training (expense)5177 间接材料indirect materials5188 其它制造费用other manufacturing expenses56 劳务成本制ervice costs561 劳务成本service costs5611 劳务成本service costs57 业务成本gency costs571 业务成本agency costs5711 业务成本agency costs58 其它营业成本other operating costs588 其它营业成本-其它other operating costs-other 5888 其它营业成本-其它other operating costs - other6 营业费用operating expenses61 推销费用selling expenses615~618 推销费用selling expenses6151 薪资支出payroll expense6152 租金支出rent expense, rent6153 文具用品office supplies (expense)6154 旅费travelling expense, travel6155 运费shipping expenses, freight6156 邮电费postage (expenses)6157 修缮费repair(s) and maintenance (expense)6159 广告费advertisement expense, advertisement6161 水电瓦斯费utilities (expense)6162 保险费insurance (expense)6164 交际费entertainment (expense)6165 捐赠donation (expense)6166 税捐taxes6167 呆帐损失loss on uncollectible accounts6168 折旧depreciation expense6169 各项耗竭及摊提various amortization6172 伙食费meal (expenses)6173 职工福利employee benefits/welfare6175 佣金支出commission (expense)6176 训练费training (expense)6188 其它推销费用other selling expenses62 管理及总务费用general & administrative expenses625~628 管理及总务费用general & administrative expenses 6251 薪资支出payroll expense6252 租金支出rent expense, rent6253 文具用品office supplies6254 旅费travelling expense, travel6255 运费shipping expenses,freight6256 邮电费postage (expenses)6257 修缮费repair(s) and maintenance (expense)6259 广告费advertisement expense, advertisement6261 水电瓦斯费utilities (expense)6262 保险费insurance (expense)6264 交际费entertainment (expense)6265 捐赠donation (expense)6266 税捐taxes6267 呆帐损失loss on uncollectible accounts6268 折旧depreciation expense a6269 各项耗竭及摊提various amortization6271 外销损失loss on export sales6272 伙食费meal (expenses)6273 职工福利employee benefits/welfare6274 研究发展费用research and development expense 6275 佣金支出commission (expense)6276 训练费training (expense)6278 劳务费professional service fees6288 其它管理及总务费用other general and administrative expenses63 研究发展费用research and development expenses635~638 研究发展费用research and development expenses6351 薪资支出payroll expense6352 租金支出rent expense, rent6353 文具用品office supplies6354 旅费travelling expense, travel6355 运费shipping expenses, freight6356 邮电费postage (expenses)6357 修缮费repair(s) and maintenance (expense)6361 水电瓦斯费utilities (expense)6362 保险费insurance (expense)6364 交际费entertainment (expense)6366 税捐taxes6368 折旧depreciation expense6369 各项耗竭及摊提various amortization6372 伙食费meal (expenses)6373 职工福利employee benefits/welfare6376 训练费training (expense)6378 其它研究发展费用other research and development expenses7 营业外收入及费用non-operating revenue and expenses, other income(expense)71~74 营业外收入non-operating revenue711 利息收入interest revenue7111 利息收入interest revenue/income712 投资收益investment income7121 权益法认列之投资收益investment income recognized under equity method7122 股利收入dividends income7123 短期投资市价回升利益gain on market price recovery of short-term investment713 兑换利益foreign exchange gain7131 兑换利益foreign exchange gain714 处分投资收益gain on disposal of investments7141 处分投资收益gain on disposal of investments715 处分资产溢价收入gain on disposal of assets7151 处分资产溢价收入gain on disposal of assets748 其它营业外收入other non-operating revenue7481 捐赠收入donation income7482 租金收入rent revenue/income7483 佣金收入commission revenue/income7484 出售下脚及废料收入revenue from sale of scraps7485 存货盘盈gain on physical inventory7486 存货跌价回升利益gain from price recovery of inventory7487 坏帐转回利益gain on reversal of bad debts7488 其它营业外收入-其它other non-operating revenue- other items75~ 78 营业外费用non-operating expenses751 利息费用interest expense7511 利息费用interest expense752 投资损失investment loss7521 权益法认列之投资损失investment loss recog- nized under equity method7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investments to market753 兑换损失foreign exchange loss7531 兑换损失foreign exchange loss754 处分投资损失loss on disposal of investments7541 处分投资损失loss on disposal of investments755 处分资产损失loss on disposal of assets7551 处分资产损失loss on disposal of assets788 其它营业外费用other non-operating expenses7881 停工损失loss on work stoppages7882 灾害损失casualty loss7885 存货盘损loss on physical inventory7886 存货跌价及呆滞损失loss for market price decline andobsolete and slow-moving inventories7888 其它营业外费用-其它other non-operating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit)811 所得税费用(或利益) income tax expense (or benefit)8111 所得税费用(或利益)income tax expense ( or benefit) 9 非经常营业损益nonrecurring gain or loss91 停业部门损益gain(loss) from discontinued operations 911 停业部门损益-停业前营业损益income(loss) from operations of discontinued segments9111 停业部门损益-停业前营业损益income(loss) from operations of discontinued segment912 停业部门损益-处分损益gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益gain(loss) from disposal of discontinued segment92 非常损益extraordinary gain or loss921 非常损益extraordinary gain or loss9211 非常损益extraordinary gain or loss93 会计原则变动累积影响数cumulative effect of changes in accounting principles931 会计原则变动累积影响数cumulative effect of changes in accounting principles9311 会计原则变动累积影响数cumulative effect of changes in accounting principles94 少数股权净利minority interest income941 少数股权净利minority interest income9411 少数股权净利minority interest income。

财务分析英语词汇表

财务分析英语词汇表一、资产类词汇1、 Assets(资产):企业拥有或控制的具有经济价值的资源。

2、 Current assets(流动资产):能够在一年内或一个经营周期内变现或运用的资产,如 Cash(现金)、Accounts receivable(应收账款)、Inventory(存货)等。

3、 Fixed assets(固定资产):使用期限较长,价值较高,并在使用过程中保持原有实物形态的资产,例如 Plant and equipment(厂房和设备)、Land(土地)。

4、 Intangible assets(无形资产):没有实物形态,但能为企业带来经济利益的资产,如 Patents(专利)、Trademarks(商标)、Goodwill(商誉)。

二、负债类词汇1、 Liabilities(负债):企业过去的交易或事项形成的、预期会导致经济利益流出企业的现时义务。

2、 Current liabilities(流动负债):需要在一年或一个经营周期内偿还的债务,如 Accounts payable(应付账款)、Shortterm loans(短期借款)。

3、Longterm liabilities(长期负债):偿还期限在一年以上的债务,例如 Bonds payable(应付债券)、Longterm loans(长期借款)。

三、所有者权益类词汇1、 Owner's equity(所有者权益):企业资产扣除负债后由所有者享有的剩余权益。

2、 Share capital(股本):公司通过发行股票所筹集的资金。

3、 Retained earnings(留存收益):企业历年实现的净利润留存于企业的部分。

四、利润表相关词汇1、 Revenue(收入):企业在日常活动中形成的、会导致所有者权益增加的、与所有者投入资本无关的经济利益的总流入,如 Sales revenue(销售收入)、Service revenue(服务收入)。

财务分析(第四版)课后习题答案

附录一:基本训练参考答案第1章财务分析理论基本训练参考答案◊知识题●阅读理解1.1 简答题答案1)答:财务分析的总体范畴包括:(1)传统财务分析内容,如盈利能力分析、偿债能力或支付能力分析、营运能力分析(2)现代财务分析内容,如战略分析,会计分析,增长能力分析,预测分析,价值评估等。

2)答:会计分析与财务分析的关系:会计分析实质上是明确会计信息的内涵与质量。

会计分析不仅包含对各会计报表及相关会计科目内涵的分析,而且包括对会计原则与政策变动的分析;会计方法选择与变动的分析;会计质量及变动的分析;等等。

财务分析是分析的真正目的所在,它是在会计分析的基础上,应用专门的分析技术与方法,对企业的财务状况与成果进行分析。

通常包括对企业投资收益、盈利能力、短期支付能力、长期偿债能力、企业价值等进行分析与评价,从而得出对企业财务状况及成果的全面、准确评价。

会计分析是财务分析的基础,没有准确的会计分析,就不可能保证财务分析的准确性。

财务分析是会计分析的导向,财务分析的相关性要求会计分析的可靠性做保证。

3)答:财务活动与财务报表的关系是:(1)企业财务活动过程包括筹资活动、投资活动、经营活动和分配活动。

企业财务报表是由资产负债表、利润表和现金流量表组成的。

(2)企业的各项财务活动都直接或间接的通过财务报表来体现。

资产负债表是反映企业在某一特定日期财务状况的报表。

它是企业筹资活动和投资活动的具体体现。

利润表是反映企业在一定会计期间经营成果的报表。

它是企业经营活动和根本活动的具体体现。

现金流量表是反映企业在一定会计期间现金和现金等价物(以下简称现金)流入和流出的报表。

它以现金流量为基础,是企业财务活动总体状况的具体体现。

4)答:财务分析的形式包括:(1)财务分析根据分析主体的不同,可分为内部分析与外部分析;(2)财务分析根据分析的方法与目的可分为静态分析和动态分析;(3)财务分析根据分析的内容与范围的不同,可分为全面分析和专题分析;(4)财务分析从分析资料角度划分,可分为财务报表分析和内部报表分析。

中英文对照财务报表常用单词

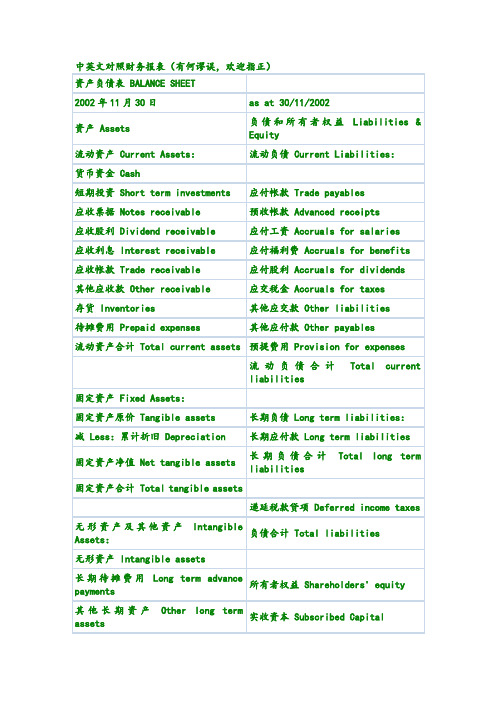

资产负债表 Balance Sheet项目 ITEM货币资金 Cash短期投资 Short term investments应收票据 Notes receivable应收股利 Dividend receivable应收利息 Interest receivable应收帐款 Accounts receivable其他应收款 Other receivables预付帐款 Accounts prepaid期货保证金 Future guarantee应收补贴款 Allowance receivable应收出口退税 Export drawback receivable存货 Inventories其中:原材料 Including:Raw materials产成品(库存商品) Finished goods待摊费用 Prepaid and deferred expenses待处理流动资产净损失 Unsettled G/L on current assets一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear其他流动资产 Other current assets流动资产合计 Total current assets长期投资: Long-term investment:其中:长期股权投资 Including long term equity investment长期债权投资 Long term securities investment*合并价差 Incorporating price difference长期投资合计 Total long-term investment固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated Dpreciation固定资产净值 Fixed assets-net value减:固定资产减值准备 Less:Impairment of fixed assets固定资产净额 Net value of fixed assets固定资产清理 Disposal of fixed assets工程物资 Project material在建工程 Construction in Progress待处理固定资产净损失 Unsettled G/L on fixed assets固定资产合计 Total tangible assets无形资产 Intangible assets其中:土地使用权 Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理 Including:Fixed assets repair固定资产改良支出 Improvement expenditure of fixed assets其他长期资产 Other long term assets其中:特准储备物资 Among it:Specially approved reserving materials 无形及其他资产合计 Total intangible assets and other assets递延税款借项 Deferred assets debits资产总计 Total Assets资产负债表(续表) Balance Sheet项目 ITEM短期借款 Short-term loans应付票款 Notes payable应付帐款 Accounts payab1e预收帐款 Advances from customers应付工资 Accrued payro1l应付福利费 Welfare payable应付利润(股利) Profits payab1e应交税金 Taxes payable其他应交款 Other payable to government其他应付款 Other creditors预提费用 Provision for expenses预计负债 Accrued liabilities一年内到期的长期负债 Long term liabilities due within one year其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期借款 Long-term loans payable应付债券 Bonds payable长期应付款 long-term accounts payable专项应付款 Special accounts payable其他长期负债 Other long-term liabilities其中:特准储备资金 Including:Special reserve fund长期负债合计 Total long term liabilities递延税款贷项 Deferred taxation credit负债合计 Total liabilities* 少数股东权益 Minority interests实收资本(股本) Subscribed Capital国家资本 National capital集体资本 Collective capital法人资本 Legal person"s capital其中:国有法人资本 Including:State-owned legal person"s capital集体法人资本 Collective legal person"s capital个人资本 Personal capital外商资本 Foreign businessmen"s capital资本公积 Capital surplus盈余公积 surplus reserve其中:法定盈余公积 Including:statutory surplus reserve公益金 public welfare fund补充流动资本 Supplermentary current capital* 未确认的投资损失(以“-”号填列) Unaffirmed investment loss未分配利润 Retained earnings外币报表折算差额 Converted difference in Foreign Currency Statements 所有者权益合计 Total shareholder"s equity负债及所有者权益总计 Total Liabilities & Equity利润表 INCOME STATEMENT项目 ITEMS产品销售收入Sales of products其中:出口产品销售收入 Including:Export sales减:销售折扣与折让 Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本 Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利 Gross profit on sales减:销售费用 Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome)汇兑损失(减汇兑收益) Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years 利润总额 Total profit减:所得税 Less:Income tax净利润 Net profit本文来自: 人大经济论坛会计与财务管理版,详细出处参考:/bbs/viewthread.php?tid=335564&page=1会计要素的计量属性 basis of measurement历史成本 historical cost重置成本 replacement cost可实现净值 net-realizable value现值 present value公允价值 fair value财务报告 financial statement资产负债表 Balance Sheet利润表 Income Statement现金流量表 Cash Flow Statement所有者权益变动表 Statement of Changes in Equity附注 notesDisclosure notesChap. 2货币资金 monetary assets现金 cash银行账户 bank account现金等价物 cash equivalentChap. 3金融资产 financial instruments以公允价值计量且变动计入当期损益的金融资产Measure at fair value through profit or loss交易性金融资产 held for trading指定为以公允价值计量且变动计入当期损益的金融资产Identified as at fair value through profit or loss 持有到期投资 Held-to –maturity investment贷款和应收账款 Loans and receivables可供出售金融资产 available-for-sale financial assets 减值 impairment减值损失 impairment lossChap. 4存货 inventory存货的种类:Classification of inventory原材料 raw materials inventory在产品 work-in-progress inventory半成品 component parts产成品 finished goods inventory商品 merchandise inventory周转材料 supplies inventory发出存货的计量 cost flow assumption先进先出法 first-in-first-out (FIFO)后进先出法 last-in-first-out (LIFO)移动加权平均法 moving-average unit cost全月一次加权平均法 weighted-average system个别计价法(具体辨认法) specific identification期末存货的计量 ending balance of inventory成本与可变现净值孰低 lower-of –cost-or-market valueNet-realizable value存货跌价准备 Allowance to reduce inventory to LCM资产减值损失—存货减值损失 loss of impairment on assets ---- loss of impairment on inventoryChap. 5长期股权投资 long-term investment –shareInvestment in subsidiary ***成本法 cost method权益法 equity method投资收益 investment income可转换 convertibleChap. 6固定资产 capital assets在建工程 wok-in-progress construction折旧 amortization平均年限法 straight-line-method工作量法 unit-of- production双倍余额递减法 declining-balance method年数总和法 sum-of-the-years-digits method后续支出 subsequent expenditure资本化 capitalized cost费用化 expensed cost处置 retirement and disposal持有待售的固定资产capital assets held for sale固定资产清理 disposal of capital assets固定资产减值准备 allowance of impairments on capital assetsChap. 7无形资产 intangible assets专利权 patents非专利技术 industrial design registration商标权 trademarks and trade name著作权 copyright特许权 franchise rights土地使用权 rights of using landChap. 8投资性房地产 investment property / profitable estateChap. 9非货币性资产交换 non-monetary assets exchange商业实质 commercial substanceChap. 10资产减值 assets impairment估计 evaluation资产组 assets group cash generate unit商誉 goodwillChap. 11负债 liabilities流动负债 current liabilities非流动负债 non-current liabilities初始计量 initial measurement辞退福利 fire fringe进口 import出口 export可转换公司债券 convertible bondChap. 12所有者权益 equity实收资本 issued capital资本公积 capital reserve股本溢价 share premium留存收益 retained earnings未分配利润 distributed profitChap. 13完工百分比法 percentage of completion method建造合同 construction contract直接法 direct method间接法 indirect method分部报告 segment report关联方 related party租赁 lease担保 guaranteeChap. 15或有事项 contingencies或有资产 contingent assets或有负债 contingent liabilities亏损合同 onerous contractChap.16重组 reorganization /resutructionChap. 18借款费用 borrowing costs borrowing expenditure 溢价 premium折价 discount资本化 capitalize costsChap. 20所得税 income tax计税基础 tax base永久性差别 permanent difference暂时性差别 temporary difference应纳税暂时性差异 taxable temporary differences 可抵扣暂时性差异 deductible temporary difference递延所得税资产 deferred tax assets递延所得税负债 deferred tax liabilitiesChap. 21外币折算 translation of foreign currency外币交易 foreign currency transactions外币财务报表折算 translation of foreign currency financial statement 即期汇率current exchange rate远期汇率 future exchange rate通货膨胀 inflationChap. 22出租人 lessor承租人 lessee经营租赁 operating lease融资租赁 finance lease / capital lease售后租回 sale and leasebackChap. 23会计政策、会计估计变更和差错更正Changes in accounting policies, changes in accounting estimates and corrections of errors会计估计Accounting estimatesChap. 24资产负债表日后事项Events after the balance sheet date调整事项 Adjusting event非调整事项 Unadjusting event利润分配 profit allocation以前年度损益调整 retained earnings--prior year adjustment Undistributed profit—prior year adjustmentChap. 25企业合并 corporate combination长期股权投资 long-term investment--shareInvestment in subsidiary ***Chap. 26合并财务报表 consolidated financial statementConsolidated Balance SheetConsolidated Income StatementConsolidated Cash Flow StatementConsolidated Statement of Changes in Equity。

财务词汇中英对照

财务词汇中英对照(总8页) -本页仅作为预览文档封面,使用时请删除本页-财务词汇以及其他金融词汇INCOME STATEMENT损益表balance sheet 资产负债表Revenue 收入Disbursement 支出Gross revenues 总收入/毛收入Net revenues 销售收入/净收入Non-operating income 营业外收入Sales 销售额Turnover 营业额Operating expenses 销售(营业)成本Operating income(loss)营业利润/(亏损)Operating profit 营业利润Operating margin 营业利润率/营业毛利EBIT margin EBIT率(营业利润率)Gross profit 毛利润Gross margin 毛利率Other income and gain 其他收入及利得Other (expense) / income 其他收入/(费用)Ordinary income 普通所得、普通收益、通常收入Operating expenses 营业费用Profit from operating activities 营业利润/经营活动之利润Research and development costs (R&D)研发费用Selling Cost 销售成本cost of sales 销售成本production cost 生产成本product cost 产品成本Net operating revenue 销售(营业)收入净额Selling and distribution costs 营销费用/行销费用selling、general and administrative expenses 销售及一般管理费用administrative accounting 行政管理会计administrative budget 行政管理预算administrative expense行政管理费用departmental budget 部门预算flexible budget 弹性预算development cost 开发成本salary bonus、 Employee benefits、Employee labor union dues、Employee education expenses工资薪金职工福利费、职工工会经费、职工教育经费Employee compensation 职工薪酬Entertainment expenses 业务招待费Advertising expenditure 广告支出Auditing, consulting and litigation expenses 审计、咨询、诉讼费Travelling expenses 差旅费Conference expenses 会议费Including entertainment expenses交际应酬费Salary and welfare fund expense 工资、福利费Rental expense 租金支出Royalty fee 特许权使用费Interest expense 利息支出manufacturing overhead 制造费用overhead 制造费用overhead cost 制造费用burden 制造费用overhead absorption rate 制造费用分配率fixed overhead 固定制造费用Fixed Assets 固定资产fixed asset turnover 固定资产周转率fixed cost 固定成本Depreciation of fixed assets 固定资产折旧Depreciation expense 折旧费depreciation 折旧Depreciation and amortization 折旧及摊销distribution cost 摊销成本Intangible assets 无形资产Other intangible assets 其他无形资产Goodwill 商誉Tangible assets 有形资产Available-for-sale investments 可供出售投资Property, plant and equipment 物业、厂房及设备或财产、厂房及设备或固定资产Investment properties 投资物业Plant Assets 厂房资产Lease prepayments 预付租金accounts payable 应付账款accounts receivable 应收账款Trade accounts receivable 应收账款Trade and bills receivables 应收账款及应收票据Accounts and bills payable 应付账款及应付票据bill payable 应付票据 bill receivable 应收票据accounts receivable aging schedule 应收账款账龄分析表accounts receivable assigned 已转让应收账款accounts receivable collection period应收账款收款期accounts receivable financing 应收账款筹资,应收账款融资accounts receivable management 应收账款管理accounts receivable turnover 应收账款周转率,应收账款周转次数Inventories 存货/库存Prepayments and other receivables 预付款及其他应收款Accrued expenses and other payables 预提费用及其他应付款prepayments 预付款项Prepayments, deposits and other receivables 预付账款、按金及其它应收款budgetary control 预算控制budgeted capacity 预算生产能力Total current assets 流动资产合计Tax rate 税率Income taxes 所得税Sales tax 销售税金及附加Income before taxes 税前利润Profit before tax 税前利润Taxable Income 应纳税所得额Income tax payable 应缴所得税额Company income tax payable 应纳企业所得税额Local income tax payable 应纳地方所得税额Loss before income taxes 税前损失taxes 税项Current Income tax 当期所得税Deferred Income tax 递延所得税Deferred tax liabilities 递延税deferred taxation 递延税款added value tax 增值税additional tax 附加税VAT on sales 销项税额VAT on purchase 进项税额VAT Refund for exported goods 出口退税Amount transferred out from VAT on purchase 进项税额转出数Transfer out overpaid VAT 转出多交增值税VAT Paid 已交税金Tax reduced and exempted减免税款Transfer out unpaid VAT 转出未交增值税Amount not deducted at end of period (represented by a "-" sign)期末未抵扣数(用"-"号反映)VAT unpaid 未交增值税Finance costs 财务费用/财务成本Financial result 财务费用Finance income 财务收益Interest income 利息收入Interest income net 利息收入净额Additional paid-in capital 资本公积Statutory reserves 法定公积/法定准备金Retained earnings 未分配利润capital gain 资本收益capital surplus 资本盈余 capital turnover 资本周转率contingent liabilities 或有负债Net income 净利润Net loss 净损失Net Margin 净利率OI(Operating Income) 经营收益OA(Operating Assets)经营性资产flow of funds statement 资金流量表Net cash flow 现金流量净额net realizable value 可变现净值Fair Value 公允价值net assets 净资产net book value 净帐面价值net liquid funds 净可变现资金Net Profit Margin on Sales/Net profit margin 销售净利率net presentvalue(NPV) 净现值 net profit 净利润 net realizable value 可变现净值 net worth 资产净值EBITDA 息、税、折旧、摊销前利润(EBITDA)EBITDA margin EBITDA率 EBITA 息、税、摊销前利润EBIT 息税前利润/营业利润Operating Results 经营业绩Financial Highlights 财务摘要aggregate balance sheet 合并资产负债表Hong Kong listed investments, at fair value 于香港上市的投资,以公允价值列示Investment deposits 投资存款Designated loan 委托贷款Financial assets 金融资产Pledged deposits 银行保证金/抵押存款accounts receivable discounted 已贴现应收账款Prepayments for acquisition of properties 收购物业预付款项fair value 公允价值现金流量表STATEMENTS OF CASH FLOWS / Cash flow statementsCash flow from operating activities 经营活动产生的现金流Net cash provided by / (used in) operating activities 经营活动产生的现金流量净额Net income /loss 净利润或损失Adjustments to reconcile net loss to net cash provided by/(used in) operating activities: 净利润之现金调整项:Addition of bad debt expense 坏账增加数/(冲回数)Provision for obsolete inventories 存货准备Share-based compensation 股票薪酬Exchange loss 汇兑损失Loss of disposal of property, plant and equipment 处置固定资产损失Changes in operating assets and liabilities: 经营资产及负债的变化Net cash provided by / (used in) operating activities 经营活动产生/(使用)的现金Free cash flow 自由现金流Cash flow from investing activities 投资活动产生的现金流Net cash used in investing activities 投资活动产生的现金流量净额Purchases of property, plant and equipment 购买固定资产Payment of lease prepayment 支付预付租金Purchases of intangible assets 购买无形资产Proceeds from disposal of property, plant and equipment 处置固定资产所得Government grants received 政府补助Equity in the income of investees 采权益法认列之投资收益Cash flow from financing activities 筹资活动产生的现金流Net cash provided by financing activities 筹资活动产生的现金流量净额Proceeds from borrowings 借款所得Repayment of borrowings 还款Decrease / (increase) in pledged deposits 银行保证金(增加)/ 减少Proceeds from issuance of capital stock 股本发行所得Net cash provided by financing activities 筹资活动产生的现金Effect of exchange rate changes on cash and cash equivalents 现金及现金等价物的汇率变更的影响Net decrease in cash and cash equivalents 现金及现金等价物的净减少Cash and cash equivalents at thebeginning of period 期初现金及现金等价物Cash and cash equivalents at the end of period 期末现金及现金等价物 Investments in acquisitions 并购投资Total assets 资产合计Exchange of non-monetary assets 非货币性资产Liabilities 负债 Current liabilities 流动负债Short-term bank loans 短期银行借款Current maturities of long-term bank loans 一年内到期的长期银行借款Total current liabilities 流动负债合计Deferred income 递延收入Financial Net Debt 净金融负债Total liabilities 负债合计Commitments and contingencies 资本承诺及或有负债Assets 资产Current assets 流动资产current liabilities 流动负债current ration 流动比率Non-current assets 非流动资产Interests in subsidiaries 附属公司权益Cash and cash equivalents 现金及现金等价物Investment income 投资收益price ratio 市盈率Aggregate income statement 合并损益表Profit before disposal of investments 出售投资前利润Equity loss of affiliates 子公司权益损失Government grant income 政府补助Profit for the period 本期利润Comprehensive income 综合收益、全面收益bond certificate 债券debenture 债券stock certificate 股票Donated shares 捐赠股票Accumulated other comprehensive income 累积其他综合所得Treasury shares 库存股票Total shareholders’ equity股东权益合计Equity 股东权益、所有者权益、净资产Shareholders Equity股东权益Total liabilities and shareholders equity 负债和股东权益合计Capital and reserves attributable to the Company’s equity holders本公司权益持有人应占资本及储备Issued capital 已发行股本Share capital 股本Reserves 储备Cash reserves 现金储备Interim Dividend 中期股息Proposed dividend 拟派股息Proposed special dividend 拟派末期股息Proposed special dividend 拟派特别股息Proposed final special dividend 拟派末期特别股息Convertible bonds 可换股债券debit capacity 举债能力debt ratio 债务比率 debtor 债务人Income from royalties 特许权使用费收益Net income in investment transfer 投资转让净收益Rental net income 租赁净收益Exchange net income 汇兑净收益Income from continuing operations 持续经营收益或连续经营部门营业收益Income from discontinued operations 非持续经营收益或停业部门经营收益extraordinary gain and loss 特别损益、非常损益Gain on trading securities 交易证券收益Net Profit attributable to Equity Holders of the Company 归属于本公司股东所有者的净利润Net income attributed to shareholders 归属于母公司股东的净利润或股东应占溢利Profit attributable to shareholders 归属于股东所有者(持有者)的利润或股东应占溢利Minority interests 少数股东权益/少数股东损益Change in fair value of exchangeable securities 可交换证券公允值变动Other comprehensive income — Foreign currency translation adjustment 其他综合利润—外汇折算差异Comprehensive (loss) / income 综合利润(亏损)Gain on disposal of assets 处分资产溢价收入Loss on disposal of assets 处分资产损失Asset impairments 资产减值Gain on sale of assets 出售资产利得Dividends 股息/股利/分红Deferred dividends 延派股利Net loss per share: 每股亏损Earnings per share(EPS)每股收益Earnings per share attributable to ordinary equity holders of the parent 归属于母公司股东持有者的每股收益-Basic -基本-Diluted -稀释/摊薄(每股收益一般用稀释,净资产用摊薄)Diluted EPS 稀释每股收益Basic EPS 基本每股收益Weighted average number of ordinary shares: 加权平均股数:-Basic -基本-Diluted -稀释/摊薄Derivative financial instruments 衍生金融工具Borrowings 借貸 Historical Cost 历史成本Capital expenditures 资本支出revenues expenditure 收益支出equity in affiliates 附属公司权益Equity Earning 股权收益、股本盈利Equity Compensation 权益报酬Weighted average number of shares outstanding 加权平均流通股treasury shares 库存股票Number of shares outstanding at the end of the period 期末流通股数目Equity per share, attributable to equity holders of the Parent 归属于母公司所有者的每股净资产Dividends per share 每股股息、每股分红Cash flow from operations (CFFO)经营活动产生的现金流量Weighted average number of common and common equivalent shares outstanding:加权平均普通流通股及等同普通流通股Equity Compensation 权益报酬Weighted Average Diluted Shares 稀释每股收益加权平均值Gain on disposition of discontinued operations 非持续经营业务处置利得(收益)Loss on disposition of discontinued operations 非持续经营业务处置损失participation in profit 分红profit participation capital 资本红利、资本分红profit sharing 分红Employee Profit Sharing 员工分红(红利)Dividends to shareholders 股东分红(红利)Average basic common shares outstanding 普通股基本平均数Average diluted common shares outstanding 普通股稀释平均数Securities litigation expenses, net 证券诉讼净支出ROA(Return on assets)资产回报率/资产收益率ROE(Return on Equity) 股东回报率/股本收益率(回报率)净资产收益率Equity ratio 产权比率ROCE(Return on Capital Employed)资本报酬率(回报率)或运营资本回报率或权益资本收益率或股权收益率RNOA(Return on Net Operating Assets)净经营资产收益率(回报率)ROI(Return on Investment)投资回报率OL(Operating Liabilities)经营性负债NBC(Net Borrow Cost) 净借债费用NOA(Net Operating Assets) 净经营性资产NFE(Net Financial Earnings) 净金融收益net financial liabilities 净金融负债FLEV(Financial leverage) 财务杠杆OLLEV(Operating Liabilities leverage) 经营负债杠杆CSE(Common Stock Equity) 普通股权益Spread/ price difference 差价RE(Residual Earning) 剩余收益discount rate 贴现率discounted cash flow 现金流量贴现。

财务分析第四版课后习题参考答案

比性问题。 8)错误。比率分析法一般不能综合反映比率与计算它的会计报表 之间的联系,因为比率通常只反映两个指标之间的关系。 9)正确。因为一方面企业偿债能力通常与盈利能力有一定的关 系;另一方面从长期的观点看,债务也需要靠盈利来偿还。 ◊ 技能题 ● 计算分析题答案 2.1 垂直分析与比率分析 解:1)编制资产负债表垂直分析表如下: 资 产 负债及所有者权益 项 目 % 项 目 % 流动资产 34.95 流动负债 16.94 其中:速动资产 11.89 长期负债 13.85 固定资产净值 41.02 负债小计 30.79 无形资产 24.03 所有者权益 69.21 合计 100.00 合计 100.00 2)计算资产负债表比率 201970 流动比率=──────×100%=206% 97925 68700 速动比率=───────×100%=70% 97925 237000 固定长期适合率=───────×100%=49.38% 80000+400000 177925 资产负债率=───────×100%=30.79% 577925 3)评价 第一,企业资产结构中有形资产结构为76%,无形资产结构为24%; 流动资产结构占35%,非流动资产结构占65%。这种结构的合理程度要结 合企业特点、行业水平来评价。

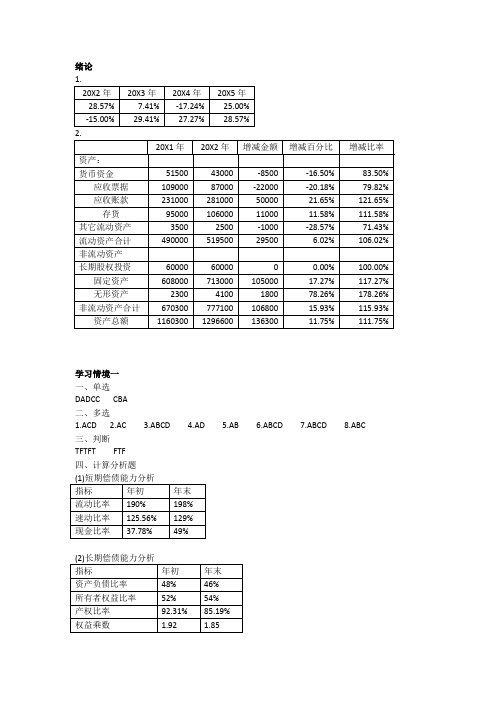

资产负债表水平分析表资产年末数年初数变动量变动率流动资产应收账款40713144927295存货30252178847389流动资产合计868467911893279固定资产固定资产原值15667137891878136固定资产净值801366631350203无形及递延资产6267124450234038资产总计22964146988266562流动负债应付帐款527736141663460流动负债合计585041401710413长期负债长期借款7779238253972266负债合计1618486857499863所有者权益实收资本6000500010000200所有者权益合计67806013767128负债加所有者权益22964146988266562从资产负债表的水平分析表中可看出1999年企业总资产比1998年增加了8266万元增长率为562

财务分析第四版课后习题答案 参考文献

Rimerman, Thomas W. ,“The Changing Significance of Financial Statements,” Journal of Accountancy (April 1990), pp.79-183.Rogero, L.H., “Characteristics of High Quality Accounting Standards,” Accounting Horizons (June 1998), pp.177-183.Shafer, W.E.R.E. Morris, and A.A. Ketchand,“The Effects of Formal Sanctions on Auditor Independen-ce,” Auditing: A Journal of Practice & Theory (Su- pplement 1999), pp.85-101.Solomons, D. ,“The FASB’s Conceptual Framework: An Evaluation,” Journal of Accountancy (June 1986), pp.114-124. Stamp, Edward. “why Can Accounting Not Become aScience Like Physics?” Abacus(Spring 1981), pp.13-27.Sutton, Michael H., “Financial Reporting in U.S. CaptialMarkets: International Dimensions,” Accounting Hor-izons (June 1997), pp.96-102.Wyatt, Arthur,“Accounting Standards: Conceptual or P-olitical?” Accounting Horizons (September1990), pp.83- 88.Collett, Peter H., Jayne M. Godfrey, and Sue L. Hrasky,“International Harmonization:Cautions from the Australian Experience,” Accounting Horizons (June 2001),pp.171-182.Collins, Stephen,“The Move to Globalization,” Journal of Accountancy (March 1989), pp.82-85.Cook, J. Michael, and Michael H. Sutton, “Summary Annual Reporting: A Cure For Information Overload,” Financial Executive (January/February 1995), pp.12-25.Davidson, Ronald A., Alexander M.G. Gelardi, and Fa- ngyve Li, “Analysis of the Conceptual Framework of China’s New Accounting System,” Journal of Ac- countancy (March 1996), pp.58-74.Dye, Ronald A., and Shyam Sunder. “Why Not Allow FAST and IASB Standards to Compete in the U.S.?” Accounting Horizons (September 2001), pp.257-271.Epstein, Marc J., and Moses L. Pava, “Profile of an A- nnual Report,” Financial Executive (January/Febru- ary 1994), pp.41-43.Erickson, Merle, Brian W.Mayhew, and William L. Felix, Jr, “Why Do Audits Fail? Evidence from Lin- coln Savings and Loan,” Journal of Accounting Research (Spring 2000), pp.165-194.Firth, Michael, “Auditor-Provided Consultancy Servi- ces and Their Associations with Audit Fees and Au-dit Opinions,” Journal of Business Finance & Accou- nting (June/July 2002), pp.661-694.Hartgraves, Al L., and George J. Benston, “The Evolv-ing Accounting Standards for Special Purpose Entit- ies and Consolidations,” Accounting Horizons (September 2002), pp.245-258.Ingberman, M., and G.H. Sorter, “The Role of Financial Statements in an Efficient Market,” Journal of Acc-ounting, Auditing, & Finance (Fall 1978), pp.58-62.Lee, Charles, and Dale Morse, “Summary Annual Repor-ts,” Accounting Horizons (March 1990), pp.39-50.Lowe, Herman J., “Ethics in Our 100-Year History,” Journal of Accountancy (May 1987), pp.78-87.McEnroe, John E., and Stanley C. Martens, “Auditors’ and Investors’ Perceptions of the Expectation Gap,” Accounting Horizons (December 2001), pp.345-358.Milan, Edgar, “Ethical Compliance at Tenneco Inc.,” Management Accounting (August 1995), p.59.Millman, Gregory J., “New Scandals, Old Lessons: Financial Ethics after Enron,” Financial Executive (July/August 2002), pp.16-19.Nair, R.D., and Larry E.Rittenberg, “Summary Annual Reports: Background and Implications for Financial Reporting and Auditing,” Accounting Horizons (March 1990), pp.25-38.Perera, M.H., “Towards a Framework to Analyzing the Impact of Culture on Accounting,” International Journal of Accounting (1989), pp.42-56.Rich, Anne J., “Understanding Global Standards,”Management, Accounting (April 1995), pp.51-54.Sainty, Barbara J., Gary K. Taylor, and David D. Williams, “Investor Dissatisfaction Toward Auditors,”Journal of Accounting, Auditing, & Finance (Spring 2002), pp.111-136.Schroeder, Nicholas W., and Charles H. Gibson, “Are Summary Annual Reports Successful?” Accounting Horizons (June 1992), pp.28-37.Schroeder, Nicholas W., and Charles H. Gibson, “Improving Annual Reports by Improving the Readability of Footnotes,” The W oman CP A (April 1998),pp.13-16.Shafer, William E., D. Jordan Lowe, and Timothy J. Fogarty, “The Effects of Corporate Ownership on Public Accountants’ Professionalism and Ethics,” Accounting Horizons (June 2002), pp.109-124.W allace, R.S. Olusegun, “Survival Strategies of a Global Organization: The Case of the International Accounting Standards Committee,” Accounting Horizons(June 1990), pp.1-22.Wallace, Wanda A., and John Walsh, “Apples-to-Apples Profits Abroad,” Financial Executives (May/June 1995), pp.28-31. W ells, Joseph T., “So That’s Why It’s Called A Pyramid Scheme,” Journal of Accountancy (October 2000),pp.91-95.Wells, Joseph T., “Timing Is of the Essence,” Journal of Accountancy (May 2001), p.78; pp.81-82; pp.85-87.Wyatt, Arthur R., and Joseph F. Y ospe, “Wake-UP Call to U.S. Business: International Accounting Standards Are on the Way,” Journal of Accountancy (July 1993),pp.80-85.Zimbelman, M.F., “The Effects of SAS NO. 82 on Auditor’s Attention to Fraud Risk Factors and Audit Planning Decision,” Journal of Accounting Research (Supplement 1997), pp.75-97.Numbers That Exclude Goodwill Amortization?”Accounting Horizons (September 2001),pp.243-255.Samuelson, Richard A., “Accounting for Liabilities to Perform Services,” Accounting Horizons (September1993), pp.32-45. Sanders, George, Paul Munter, and Tommy Moures, “Software —The Unrecorded Asset,” Management Accounting (August 1994), pp.57-61.Schuetze, Walter P., “What Is an Asset?” Accounting Horizons (September 1993), pp.66-70.Earnings,” Journal of Accounting Research (Spring 2000), pp.71-102.MacDonald, Elizabeth, Accounting in the Danger Zone,”Forbes(September 2, 2002), p.138. Moses, D., “Income Smoothing and Incentives: Empirical Tests Using Accounting Changes,” The Accounting Review (April 1987), pp.358-377.Worthy, F.S., “Manipulating Profits: How It’s Done,” Fortune (June 15, 1984), pp.50-54.Ou, Jane A., and Stephen H. Penman,Financial Statement Analysis and the Prediction of Stock Returns,”Journal of Accounting and Economics (November 1989),pp.295-329.Zarowin, P., “What Determines Earnings-Price Ratios Revisited,”Journal of Accounting, Auditing, & Finance (Summer 1990),pp. 439-454.Beasley, M.S., “An Empirical Analysis of the Relation Between the Board of Director Composition and Finance Statement Fraud,” The Accounting Review (October 1996),pp. 443-465.Bell, T.B., and J.V. Carcello,“A Decision Aid for Assessing the Likelihood of Fraudulent Financial Reporting,” Auditing : A Journal of practice & Theory (Spring 1999), pp.169-184.Beneish, Messod P., “The Detection of Earnings Manipulation,” Financial Analysts Journal (September-October 1999), pp.24-36.Burgess, Deanna Qender, “Graphical Sleight of Hand,” Journal of Accountancy (February 2002), pp.45-48, p.51.Casey, C.J., Jr., “V ariation in Accounting Information Load: The Effect on Loan Officers’ Prediction of Bankruptcy,” Accounting Review (January 1980), pp.36-49.Casey, C.J., and N.J. Bartczak, “Using Operating Cash Flow Data to Predict Financial Distress: Some Extensions,” Journal of Accounting Research (Spring 1985), pp.384-401.Chandra, Uday, Bradley D. Childs, and Bturvg T. Ro, “The Association Between LIFO Reserve and Equity Risk: An Empirical Assessment,” Journal of Accounting, Auditing, & Finance (Summer 2002), pp.185-208.Dambolena, I.G., and S.J. Khorvry, “Ratio Stability and Corporate Failure,” Journal of Finance (September 1980), pp.1017-1026Dechow, P.A., R.G. Sloan, and A.P. Sweeney, “Causes and Consequences of Earnings Manipulation: An Analysis of Firms Subject to Enforcement Actions by the SEC,” Contemporary Accounting Research (Spring 1996), pp.1-36.1999), pp.757-778. Dutta, Sunil, and Frank Gigler, “The Effect of Earnings Forecasts on Earnings Management,” Journal of Accounting Research (June 2002), pp.631-656.Gombola, M.J., and J.E. Ketz , “Financial Ratio Patterns in Retail and Manufacturing Organizations,” Financial Management (Summer 1983), pp.45-56.Grent, C. Terry, Chaunrey M. Depree, Jr., and Gerry H. Grant, “Earnings Management and the Abuse of Materiality,” Journal of Accountancy (September 2000),pp. 41-44.Howell, Robert A., “Fixing Financial Reporting: Financi- al Statement Overhaul,” Financial Executive (March/ April 2002), pp.40-42.Jaggi, B., “Which Is Better, D & B or Zeta in Forecasting Credit Risk?” Journal of Business Forecasting (Summer 1984), pp.13-16, p.22.Johnson, W.B., and D.S. Dhaliwal, “LIFO Abandonment,” Journal of Accounting Research (Autumn 1988), pp.236-272.Kasznik, Ron and Maureen F.McNichols, “Does Meeting Earnings Expectations Matter? Evidence from Analyst Forecast Revisions and Share Prices,” Journal of Accouting Research (June 2002), pp.727-760.Kirschenheiter, Michael, and Nahum D. Melumad, “Can ‘Big Bath’ and Earnings Smoothing Co-exist as Equil- ibrium Financial Reporting Strategies?” Journal of Accounting Research (June 2002), pp.761-796.Largay, James A., “Lessons from Enron,” Accounting Horizons (June 2002), pp.153-156.Lennox, C.S., “The Accuracy and Incremental Information Content of Audit Reports in Predicting Bankruptcy,” Journal of Business Finance & Accounting (June/ JulyLincoln, M., “An Empirical Study of the Usefulness of Accounting Ratios to Describe Levels of Insolvency Risk,” Journal of Banking and Finance (June 1984), pp.321-340.Lynch, David, and Steven Galen, “Got the Picture? CPAs Can Use Some Simple Principles to Create Effective Charts and Graphs for Financial Reports and Presentations,” Journal of Accountancy (May 2002), pp.183-187.Makeever, D.A., “Predicting Business Failures,” The Journal of Commercial Bank Lending (January 1984), pp.14-18.McDonald, B., and M.H. Morris, “The Statistical Validity of the Ratio Method in Financial Analysis: An Empirical Examination,” Journal of Business Finance & Accounting (Spring 1984), pp.89-97.Mendenhall, Richard R., “How Naive Is the Market’s Use of Firm-Specific Earnings Information?” Journal of Accounting Research (June 2002), pp.841-864.Miller, Paul B., “Quality Financial Reporting,” Journal of Accountancy (April 2002), pp.70-74.Parsons, O., “Using Financial Statement Data to Indentify Factors Associated with Fraudulent Financial Reporting,” Journal of Applied Business Research (Summer 1995), pp.38-46.Patell, J.M., and M.A. Wolfson, “The Intraday Speed of Adjustment of Stock Prices to Earnings and Dividend Announcements,” Journal of Financial Economics (June 1984), pp.223-252.Patrone, F.L., and D. duBois, “Financial Ratios Analysis in the Small Business,” Journal of Small Business Williamson, R.W., “Evidence on the SelectiveManagement (January 1981), pp.35-40.Peterson, M., “Putting Extra Fizz into Profits; Critics Say Coca-Cola Dumps Debt on Spin Off,” New York Times (August 4, 1998), D1.Rama, D.V., K. Raghunandan, and M.A, Gerger, “The Association Between Audit Reports and Bankruptcies: Further Evidence,” Advances in Accounting 15 (1997), pp.1-15Rege, V.P., “Accounting Ratios to Locate Take-Over Targets,” Journal of Business Finance & Accounting (Autumn 1984), pp.301-311.Richardson, F.M., G.D. Kane, and P. Lobingier, “The Impact of Recession on the Prediction of Corporate Failure,” Journal of Business Finance & Accounting (January/March 1998), p.167, p.186.Shelton, Sandra Waller, O. Ray Whittington, and David Landsittel, “Auditing Firms’ Fraud Risk Assessment Practices,” Accounting Horizons (March 2001), pp.19-33.Steinbart, Paul John, “The Auditor’s Responsibility for the Accuracy of Graphs in Annual Reports: Some Evidence of the Need for Additional Guidance,” Accounting Horizons (September 1989), pp.60-70.Stober, T.L., “The Incremental Information Content of Financial Statement Disclosures: The Case of LIFO Liquidations,” Journal of Accounting Research (Supp- lement 1986), pp.138-160.Summers, S.L., and J.T. Sweeney, “Fraudulently Misstated Financial Statements and Insider Trading: An Empirical Analysis,” The Accounting Review (January 1998), pp.131-146.Tse, S., “LIFO Liquidations,” Journal of Accounting Research (Spring 1990), pp.229-238.Reporting of Financial Ratios,” The Accounting Review (April 1984), pp.296-299.Chase, Bruce, New Reporting Standards For Not-For- Profits,”Management Accounting (October 1995), pp.34-37.Chase, Bruce, W., and Laura B. Triggs, “How to Implement GASB Statement No.34,” Journal of Accountancy (November 2001), pp.71-79.Downs, G.W., and D.M. Rocke, “Municipal Budget Forecasting with Multivariate ARMA Models,” Journal of Forecasting (October-December 1983), pp.377-387.Gordon, Teresa P., Janet S. Greenlee, and Denise Nitter- house, “Tax-Exempt Organization Financial Data: Availability and Limitations,” Accounting Horizons (June 1999), pp.113-128.Hay, E., and James F. Antonio, “What Users Want In Government Financial Reports,” Journal of Accoun-tancy (August 1990), pp.91-98.Ives, Martin, “Accountability and Governmental Fina-1987), pp.130-134.Kinsman, Michael D., and Bruce Samuelson, “Personal Financial Statements: V aluation Challenges and Solutions,” Journal of Accountancy (September 1987),pp.138-148.Klasny, Edward M., and James M. Williams, “Governm-ent Reporting Faces an Overhaul,” Journal of Accoun- tancy (January 2000), pp.49-51.Meeting, David T., Randall W. Luecke, and Edward J. Giniat, “Understanding and Implementing FASB124,” Journal of Accountancy (March 1996), pp.62-66.Shoulder, Craig D., and Robert J. Freeman, “Which GAAP Should NOPs Apply?” Journal of Accountancy (November 1995), pp.77-78,p.80,p.82,p.84.Statement of Position of the Accounting Standards Division 82-1, “Accounting and Financial Reporting for Personal Financial Statements” (New York: American Institute of Certified Public Accountants, 1982).。

中英文财务报表词语对照表

中英文财务报表词语对照表一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时刻点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流淌资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期托付贷款Entrusted loan receivable due within one y ear减:一年内到期托付贷款减值预备Less: Impairment for Entruste d loan receivable due within one year减:短期投资跌价预备Less: Impairment for current investment短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账预备Less: Bad debt provision for Account rec eivable应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账预备Less: Bad debt provision for Other rec eivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价预备Less: Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due withi n one year一年内到期的应收融资租赁款Finance lease receivables due with in one year其他流淌资产Other current assets流淌资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment托付贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值预备Less: Impairment for long-term equit y investment减:长期债权投资减值预备Less: Impairment for long-term debt investment减:托付贷款减值预备Less: Provision for entrusted loan receiva ble长期投资净额Net bal of long-term investment其中:合并价差Include: Goodwill (Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less: Accumulated Depreciation固定资产净值Net bal减:固定资产减值预备Less: Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值预备Less: Impairment for construction in prog ress在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets & Intangible assets无形资产Intangible assets减:无形资产减值预备Less: Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease –Unguaranteed residua l values融资租赁——应收融资租赁款Finance lease –Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets & intangible assets递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability & Equity流淌负债Current liability短期借款Short-term loans应对票据Notes payable应对账款Accounts payable已结算尚未完工款预收账款Advance from customers应对工资Payroll payable应对福利费Welfare payable应对股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应对款Other payable预提费用Accrued Expense估量负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流淌负债Other current liability流淌负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应对债券Bonds payable长期应对款Long-term payable专项应对款Grants & Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益) Owners’Equity实收资本(或股本) Paid in capital减;已归还投资Less: Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资缺失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include: Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表Income statement and profit appropriation一、主营业务收入Revenue减:主营业务成本Less: Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列) Gross Profit ( - means lo ss)加:其他业务收入Add: Other operating income减:其他业务支出Less: Other operating expense减:营业费用Selling & Distribution expense治理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列) Profit from operation ( - means los s)加:投资收益(亏损以“—”填列) Add: Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less: Non-operating expense四、利润总额(亏损总额以“—”填列) Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资缺失Add: Unrealised investment losses五、净利润(净亏损以“—”填列) Net profit ( - means loss)加:年初未分配利润Add: Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution( - means loss)减:提取法定盈余公积Less: Appropriation of statutory surplus r eserves提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and w elfare fund提取储备基金Appropriation of reserve fund提取企业进展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners distribution减:应对优先股股利Less: Appropriation of preference shares di vidend提取任意盈余公积Appropriation of discretionary surplus reserve应对一般股股利Appropriation of ordinary shares dividend转作资本(或股本)的一般股股利Transfer from ordinary shares di vidend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1. 出售、处置部门或被投资单位收益Gains on disposal of opera ting divisions or investments2. 自然灾难发生缺失Losses from natural disaster3. 会计政策变更增加(或减少)利润总额Increase (decrease) in pr ofit due to changes in accounting policies4. 会计估量变更增加(或减少)利润总额Increase (decrease) in pr ofit due to changes in accounting estimates5. 债务重组缺失Losses from debt restructuring。

财务分析第四版课后习题译文 词汇表

词汇表本词汇表的多数术语在教材中已经作了解释。

教材中没有解释的某些词汇也包括在本词汇表中,因为年报中经常出现这些词汇。

AAccelerated Cost Recovery System (ACRS)(加速成本回收制):1981年基于税收目的而引入的折旧方法,后来作了修正。

请参见修正的加速成本回收制。

accelerated depreciation(加速折旧):一种前期折旧额大于后期折旧额的折旧方法。

account(账户):用于归类和概括交易的记录工具。

account form of balance sheet(账户式资产负债表):左边是资产,右边是负债和所有者权益的资产负债表。

accounting(会计):通过计量主体的经济活动,向那些作商业和经济决策的人提供有用信息的系统过程。

accounting changes(会计变更):用于描述与前期不同的会计原则、会计估计和报告主体的使用。

accounting controls(会计控制):与维护资产及财务报表可靠性有关的过程。

accounting cycle(会计循环):用于分析、记录、归类和汇总交易的一系列步骤。

accounting equation(会计方程式):资产=负债+所有者权益。

accounting errors(会计差错):由计算差错、会计原则的不恰当运用及重大事件的忽略所导致的错误。

accounting period(会计期间):与会计报告相关的时间。

accounting policies(会计政策):用于报告公司财务成果的会计原则及惯例。

Accounting Principles Board (APB)(会计原则委员会):一个由美国注册会计师成立的委员会,这些注册会计师在1959—1973年期间,发布制定会计准则的意见书。

Accounting Research Bulletins (ARBs)(会计研究公报):由美国注册会计师协会会计程序委员会发布的公告。

中英文常用财务词汇对照表

中英文常用财务词汇对照表

以下是一些中英文常用财务词汇对照表:

中文英文中文英文

收入 revenue 资产 asset

支出 expenditure 负债 liability

成本 cost 所有者权益 owner's equity

利润 profit 现金流量 cash flow

净利润 net profit 流动比率 current ratio

毛利润 gross profit 速动比率 quick ratio

毛利率 gross profit margin 资产负债率 gearing ratio

净利润率 net profit margin 存货周转率 inventory turnover ratio 总资产收益率 return on total assets 应收账款周转率 receivables turnover ratio

市盈率 P/E ratio 资本回报率 return on capital employed

市净率 P/B ratio 销售利润率 profit margin on sales

市现率 P/CF ratio 经营现金流增长率 growth rate of operating cash flow

市销率 P/S ratio 存货周转天数 days of inventory on hand

ROE(净资产收益率) ROE(return on equity) 应收账款周转天数 days of receivables outstanding。

财务报表及分析词汇的中英文汇总

财务报表及分析词汇的中英文汇总企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year减:一年内到期委托贷款减值准备Less:Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less:Impairment for current investment短期投资净额Net bal of current investment三、利润及利润分配表Income statement and profit appropriation一、主营业务收入Revenue减:主营业务成本Less:Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以"-"填列)Gross Profit(-means loss)加:其他业务收入Add:Other operating income减:其他业务支出Less:Other operating expense减:营业费用Selling&Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以"-"填列)Profit from operation(-means loss) 加:投资收益(亏损以"-"填列)Add:Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less:Non-operating expense四、利润总额(亏损总额以"-"填列)Profit before Tax减:所得税Less:Income tax少数股东损益Minority interest加:未确认投资损失Add:Unrealised investment losses五、净利润(净亏损以"-"填列)Net profit(-means loss)加:年初未分配利润Add:Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution(-means loss)减:提取法定盈余公积Less:Appropriation of statutory surplus reserves提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners'distribution减:应付优先股股利Less:Appropriation of preference share's dividend提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase(decrease)in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase(decrease)in profit due to changes in accounting estimates5.债务重组损失Losses from debt restructuring应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less:Bad debt provision for Account receivable应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less:Bad debt provision for Other receivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less:Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year一年内到期的应收融资租赁款Finance lease receivables due within one year其他流动资产Other current assets流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less:Impairment for long-term equity investment减:长期债权投资减值准备Less:Impairment for long-term debt investment减:委托贷款减值准备Less:Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include:Goodwill(Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less:Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less:Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less:Impairment for construction in progress在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets&Intang ible assets无形资产Intangible assets减:无形资产减值准备Less:Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁--未担保余值Finance lease– Unguaranteed residual values融资租赁--应收融资租赁款Finance lease– Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets&intangible assets 递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability&Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants&Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners'Equity实收资本(或股本)Paid in capital减;已归还投资Less:Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include:Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include:Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability&Equity。

财务报表分析第4版高教版习题答案

绪论学习情境一一、单选DADCC CBA二、多选1.ACD2.AC3.ABCD4.AD5.AB6.ABCD7.ABCD8.ABC三、判断TFTFT FTF四、计算分析题学习情境二一、单选CBDCA BCB二、多选1.BD2.ABCD3.ABC4.BC5.BD6.AB7.BCD8.ABD三、判断TFTTF FFF学习情境三一、单选ADBBC ACD二、多选1.CD2.AC3.AB4.ABD5.BCD6.AC7.AB8.ABCD三、判断TFTFF FFF四、(1)现金比率=310/10000=31%(2)现金充分性比率=310/(300+700+280+160)=21.53%(3)净利润现金比率=886/[2800*(1-25%)]=42.19%学习情境四一、单选DCABA ADB二、多选1.ABCD2.CD3.ABCD4.ABC5.BD6.BC7.8.BCD三、判断FFTTT TTT学习情境五一、单选CCDAC DABDB BDBCC DCCCB二、多选1.ABCD2.ABCD3.ABCD4.ACD5.BCD6.ABC7.CD 8.ABCD 9.ABC 10.ABCD 11.ABC 12.AD三、判断FFFFF FFTFT TTFFT FFFT四、业务处理1.(1)交易后的流动资产=820000+160000-80000-18000=882000元交易后的流动负债=820000/1.6+80000+28000=620500元交易后的营运资本=882000-620500=261500元(2)882000/620500=1.422.(1)(14+42)/180=31%(2)1/(1-31%)=1.45(3)198/[(180+140)/2]=1.24(4)14*2.5-14*1.2=18.2万元(5)[(15+18.2)/2]*5=83万元(6)净利润=(198-83-9-10)*(1-25%)=72万元,销售净利率=72/198=36.36%净资产收益率=36.36%*1.24*1.45=65.38%3.(1)20××年年初的负债总额=500÷25%=2000(万元)20××年年初的资产总额=800÷20%=4000(万元)20××年年初的股东权益总额=4000-2000=2000(万元)20××年年初的权益乘数=4000÷2000=220××年年初的流动比率=800÷500=1.620××年年初的速动比率=(250+200)÷500=0.9(2)20××年末的股东权益总额=2000×120%=2400(万元)20××年末的资产总额=1200÷24%=5000(万元)20××年末的负债总额=5000-2400=2600(万元)20××年末的产权比率=2600÷2400=1.0820××年末的流动负债=2600×35%=910(万元)20××年末的流动比率=1200÷910=1.3220××年末的速动比率=(350+400)/910=0.82(3)20××年末的股东权益总额=2000×120%=2400(万元)20××年末的资产总额=1200÷24%=5000(万元)20××年末的负债总额=5000-2400=2600(万元)20××年末的产权比率=2600÷2400=1.0820××年末的流动负债=2600×35%=910(万元)20××年末的流动比率=1200÷910=1.3220××年末的速动比率=(350+400)/910=0.82(4)20××年平均负债=(2000+2600)÷2=2300(万元)利息费用=2300×8%=184(万元)税前利润=营业收入-营业成本-三项期间费用合计=5000-4000-400=600 (万元)息税前利润=税前利润+利息费用=600+184=784(万元)净利润=600×(1-25%)=450(万元)总资产报酬率=784/[(4000+5000)÷2]×100%=17.42%净资产收益率=450/[(2000+2400)÷2]×100%=20.45%经营现金净流量=0.6×910=546(万元)盈余现金保障倍数=546÷450=1.21已获利息倍数=784÷184=4.26。

财务报表(翻译词汇)

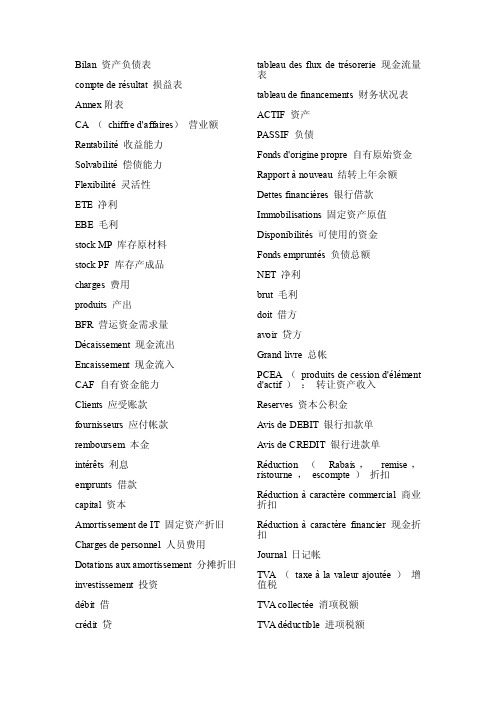

Bilan 资产负债表compte de résultat 损益表Annex附表CA (chiffre d'affaires)营业额Rentabilité收益能力Solvabilité偿债能力Flexibilité灵活性ETE 净利EBE 毛利stock MP 库存原材料stock PF 库存产成品charges 费用produits 产出BFR 营运资金需求量Décaissement 现金流出Encaissement 现金流入CAF 自有资金能力Clients 应受账款fournisseurs 应付帐款remboursem 本金intérêts 利息emprunts 借款capital 资本Amortissement de IT 固定资产折旧Charges de personnel 人员费用Dotations aux amortissement 分摊折旧investissement 投资débit 借crédit 贷tableau des flux de trésorerie 现金流量表tableau de financements 财务状况表ACTIF 资产PASSIF 负债Fonds d'origine propre 自有原始资金Rapport à nouveau 结转上年余额Dettes financières 银行借款Immobilisations 固定资产原值Disponibilités 可使用的资金Fonds empruntés 负债总额NET 净利brut 毛利doit 借方avoir 贷方Grand livre 总帐PCEA (produits de cession d'élément d'actif ):转让资产收入Reserves 资本公积金Avis de DEBIT 银行扣款单Avis de CREDIT 银行进款单Réduction (Rabais,remise,ristourne ,escompte )折扣Réduction àcaractère commercial 商业折扣Réduction àcaractère financier 现金折扣Journal 日记帐TVA (taxe àla valeur ajoutée )增值税TVA collectée 消项税额TVA déductible 进项税额TVA à payer 应交税金capitaux propres,所有者权益ACTIFS :资产ACTIF CIRCULANT :流动资产ACTIF IMMOBILISE :不动产AGENCEMENTS, AMENAGEMENTS :装配、装饰费用,维修设备APPROVISIONNEMENTS :原材料BESOIN EN FONDS DE ROULEMENT :流动资金BILAN COMPTABLE :财务资产负债表BILAN FINANCIER :管理分析资产负债表CAPACITE D’AUTOFINANCEMENT :自主融资能力CAPACITE D’ENDETTEMENT :负债能力CAPACITE DE REMBOURSEMENT :偿债能力CAPITAL SOUSCRIT -APPELE NON VERSE :认缴未支付的资本CAPITAUX PROPRES :所有者权益CHARGES CO NSTATEES D’AVANCE :待摊费用CHARGES A REPARTIR SUR PLUSIEURS EXERCICES:长期待摊费用CHIFFRE D’AFFAIRES :营业额COMPTES DE REGULARISATION :调整账户CONCOURS BANCAIRES COURANTS :负银行存款(相当于短期借款)CREDIT -BAIL :租赁DEPOTS ET CAUTIONNEMENTS VERSES :担保金DETTES PROVISIONNEES OU CHARGES A PAYER :预提费用ECART DE REEVALUATION :重估价差ECART DE CONVERSION :外币兑换差EFFETS A L’ECAISSEMENT :票据兑现(encaissement)EFFETS A L’ESCOMPTE :票价贴现EFFETS A RECEVOIR :应收票据EFFETS A PAYER :应付票据EFFETS ESCOMPTES NON ECHUS :未到期的贴现票据EMPRUNTS ET DETTES AUPRES DES ETABLISSEMENTS DE CREDIT :向金融机构的借款EMPRUNT OBLIGATOIRE CONVERTIBLE :可转换债券ESCOMPTE :贴现ESCOMPTE DE REGLEMENT :贴现清偿EXCEDENT BRUT D’EXPLOITATION (E.B.E.) :经营利润EXCEDENT DE TRESORERIE D’EXPLOITATION (E.T.E..) :营运现金盈余FONDS COMMERCIAL :商誉FONDS DE ROULEMENT :营运资本FRAIS D’ETABLISSEMENT :开办费FRAIS DE RECHERCHE ET DE DEVELOPPEMENT :研发费用IMMOBILISATIONS (non financières) :不动产IMMOBILISATIONS CORPORELLES :固定资产IMMOBILISATIONS FINANCIERES ::金融资产IMMOBILISATIONS INCORPORELLES :无形资产MARGE COMMERCIALE :商业利润MARGE BR UTE D’AUTOFINANCEMENT :税前自主融资余额MATIERES CONSOMMABLES (et fournitures) :易耗品PARTICIPATION :长期投资PARTICIPATION DES SALARIES :职工持有的股份PASSIFS :负债PLAN D’AMORTISSEMENT :折旧表PRIMES D’EMISSION, DE FUSION ET D’APPORT:合并溢价PRODUCTION IMMOBILISEE :不动产生产变动PRODUCTION STOCKEE :自产存货变动PRODUCTION VENDUE :服务收入PRODUITS CONSTATES D’AVANCE :待摊收入PRODUITS A RECEVOIR :预提收入PROVISIONS POUR DEPRECIATION :资产减值PROVISIONS POUR RISQUES ET CHARGES :预计负债PROVISIONS REGLEMENTEES :(中国无此账户)按税法应计提费用RABAIS, REMISES, RISTOURNES :销售折扣、销售退回RENTABILITE FINANCIERE :投资盈利RENTABILITE ECONOMIQUE :经济盈利REPORT A NOUVEAU BENEFICIAIRE :未分配利润(盈利)REPORT A NOUVEAU DEFICITAIRE :未分配利润(亏损)RESERVES :资本公积RESULTAT D’EXPLOITATION :营业利润RESULTAT EXCEPTIONNEL :营业外收支RESULTAT FINANCIER :投资收益SITUATION NETTE :净资产SOLDES INTERMEDIAIRES DE GESTION :利润分析SOLVABILITE :偿付能力STOCKS :存货SUBVENTIONS D’EXPLOITATION :补助金(一般与购买固定资产有关)TABLEAU DE FINANCEMENT :融资表TEMPS D’ECOULEMENT:TITRES DE PARTICIPATION :长期股权投资TRESORERIE NETTE :净现金VALEUR AJOUTEE :增值额VALEURS MOBILIERES DE PLACEMENT :短期投资VARIATION DES STOCKS :存货变动BFRE 营运活动流动资金需求ETE 营运活动产生的现金盈余Flux de tresorerie 现金流(现金流量表)CAF 自融资能力。

(2021年整理)财务报表词汇-中英对照

(完整)财务报表词汇-中英对照编辑整理:尊敬的读者朋友们:这里是精品文档编辑中心,本文档内容是由我和我的同事精心编辑整理后发布的,发布之前我们对文中内容进行仔细校对,但是难免会有疏漏的地方,但是任然希望((完整)财务报表词汇-中英对照)的内容能够给您的工作和学习带来便利。

同时也真诚的希望收到您的建议和反馈,这将是我们进步的源泉,前进的动力。

本文可编辑可修改,如果觉得对您有帮助请收藏以便随时查阅,最后祝您生活愉快业绩进步,以下为(完整)财务报表词汇-中英对照的全部内容。

1财务报表示例一、财务报表I. Financial Statements1、合并资产负债表1。

Consolidated Balance Sheet编制单位:Name of enterprise:2016 年03 月31 日March 31, 2016单位:元Unit: Yuan2、合并利润表2. Consolidated Income Statement单位:元Unit: YuanIn case of enterprise merger under the same control, the merged party had a net profit: 0.00 Yuan before being merged and 0。

00 Yuan in prior period.3、合并现金流量表3. Consolidated Cash Flow Statement单位:元10Unit: Yuan14会计科目中英文对照(北京市审计局发布)15161920。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

词汇表本词汇表的多数术语在教材中已经作了解释。

教材中没有解释的某些词汇也包括在本词汇表中,因为年报中经常出现这些词汇。

AAccelerated Cost Recovery System (ACRS)(加速成本回收制):1981年基于税收目的而引入的折旧方法,后来作了修正。

请参见修正的加速成本回收制。

accelerated depreciation(加速折旧):一种前期折旧额大于后期折旧额的折旧方法。

account(账户):用于归类和概括交易的记录工具。

account form of balance sheet(账户式资产负债表):左边是资产,右边是负债和所有者权益的资产负债表。

accounting(会计):通过计量主体的经济活动,向那些作商业和经济决策的人提供有用信息的系统过程。

accounting changes(会计变更):用于描述与前期不同的会计原则、会计估计和报告主体的使用。

accounting controls(会计控制):与维护资产及财务报表可靠性有关的过程。

accounting cycle(会计循环):用于分析、记录、归类和汇总交易的一系列步骤。

accounting equation(会计方程式):资产=负债+所有者权益。

accounting errors(会计差错):由计算差错、会计原则的不恰当运用及重大事件的忽略所导致的错误。

accounting period(会计期间):与会计报告相关的时间。

accounting policies(会计政策):用于报告公司财务成果的会计原则及惯例。

Accounting Principles Board (APB)(会计原则委员会):一个由美国注册会计师成立的委员会,这些注册会计师在1959—1973年期间,发布制定会计准则的意见书。

Accounting Research Bulletins (ARBs)(会计研究公报):由美国注册会计师协会会计程序委员会发布的公告。

该协会在1939—1959年期间制定会计准则。

accounting system(会计制度):用于搜集和披露会计数据的过程和方法。

accounts payable(应付账款):因正常商业来往而负担的以存货、商品或服务等形式偿还的债务。

accounts receivable (trade receivables)(应收账款):因销售商品或提供服务而可以从客户那里获得现金收入的账户。

accrual basis(权责发生制):会计的权责发生制规定,收入在实现时确认(实现原则),而费用在发生时确认(配比原则)。

accrued expenses(应计费用):已经发生但并不在账户中确认的费用。

accrued liability(应计负债):支付现金前已确认的费用所产生的负债。

accrued pension cost(应计养老金成本):作为费用记录的养老金数额与偿债基金的差额。

accrued revenues(应计收入):已提供的服务或货物已发运但尚未入账的收入。

accumulated benefit obligation (ABO)(累计福利负债):以当时员工服务和补偿费用为基础的退休福利现值。

accumulated depreciation(累计折旧):折旧指在建筑物和机器的有效期限内分期摊销其成本。

每期发生的折旧费用累计在一个账户,便是累计折旧。

accumulated postretirement benefit obligation (APBO) (累计退休后福利负债):以当时员工服务为基础的退休后福利现值。

acquisition(收购):一个企业获得另一个企业控制权的企业合并。

acquisition cost(购置成本):包括所有用于获得资产并使之正常运作所必需的费用。

acquisitions(收购):被收购的企业。

actuarial assumptions(精算假设):以历史数据为基础,关于日后事项的假设,例如职工流转率、服务期限和寿命等,这些可用于估计例如养老金津贴的日后费用。

additional paid-in capital(资本公积):高于股票面值或设定价值、来自股东的投资或其他途径的投资资本,例如财产捐赠或库藏股的销售。

adjusting entries(调整分录):在每个会计期末用于更新账户的分录。

administrative controls(管理控制):与有效经营活动和管理政策一贯性相关的程序。

administrative expenses(管理费用):在公司日常经营过程中,管理部门产生的费用。

adverse opinion(反对意见):一旦财务报表含有与公认会计原则相违背的事项,不能证明其报表合格时,审计人员所发表的审计意见。

它反映了财务报表不能在遵循公认会计原则的基础上公允地反映公司财务状况、经营成果和现金流量。

aging of accounts receivables(应收账款账龄分析):一种用于检查坏账的方法,它确定坏账费用的估计数。

应收账款根据账龄分成不同的类别,然后估计坏账费用。

aging schedule(账龄分析表):一种根据未偿还时间的长短编制的,对各个不同应收账款进行分类的表格。

allowance for funds used during construction (AFUDC) (在建期间使用资金准备):在建期间使用资金准备是一个由州公用事业委员会签署的公用会计惯例。

它代表了在建工程融资的估计债务和权益费用。

在建期间使用资金准备并不是一种现金来源,但在受限制的利率条例下,在建期间使用资金准备的收益率和回收率允许用于计算公用事业的收费率。

一些公用事业部门把在建期间融资的估计债务和权益费用在单独账户内报告。

allowance for uncollectible accounts(坏账准备):应收账款备抵账户,用于估计坏账数额。

allowance method(备抵法):一种以当期赊销收入净额或应收账款期末数为基础估计坏账的方法。

American Accounting Association (AAA)(美国会计学会):由会计学者和会计从业人员所组成的会计组织。

American Institute of Certified Public Accountants (AICPA)(美国注册会计师协会):一个由注册会计师组成的专业组织。

amortization(摊销):无形资产在其有效期限内分期分摊其成本。

annual report(年度报告):每年由公司管理层编制的包括财务报表和其他重要信息的一种正式呈报。

annuity(年金):在特定的时间间隔内的一系列等额付款(收款)活动。

antidilution of earnings(收益的反稀释):假设可转换证券发生转换、行使股票期权,它们都可以导致每股收益上升或每股损失下降。

antidilutive securities(反稀释证券):一些因其自身的转换或行权会导致每股收益上升或每股损失下降的证券。

appropriated retained earnings(已分拨的留存收益):一部分限制用途的留存收益,它说明公司的一部分资产除了用于支付股利之外,还可用于其他目的。

arms-length transaction(正常交易):独立主体以各自利益为出发点进行的交易。

assets(资产):由过去交易或事项形成,并由特定主体拥有或控制的未来经济收益。

assignment of receivables(应收款项转让):以应收款项作为抵押物的借款。

attestation(验证):注册会计师执行的服务所形成的书面信息,它得出关于对另一投资主体负责的书面论断的可靠性结论。

audit committee(审计委员会):一个从属于董事会的委员会,它主要由与组织无管理关系的外部董事所组成。

audit report(审计报告):用于传达审计结果的载体。

auditing(审计):一个根据要求有目的地获取并评价证据,并且把审计结果传达给利益相关者的系统过程。

auditor(审计人员):执行审计的人。

authorized stock(核定股份):公司不需修改它的章程就可以发行的股票的最大数目。

available-for-sale securities(可销售证券):既不属于持有到期证券,又不属于交易证券的股票或债券。

average cost method (inventory)(平均成本法):平均成本法是把存货成本加总计算平均值的方法。

Bbalance sheet (statement of financial position)(资产负债表:(财务状况表)):财务报表反映了会计主体某个特定时点的财务状况。

资产负债表列示了资产(企业资源)、负债(企业债务)、股东权益(企业所有者的利益)。

balance sheet (classified)(分类式资产负债表):该形式的资产负债表把资产与负债分为流动与非流动两类。

balance sheet (financial position form)(财务状况式资产负债表):该形式的资产负债表就是用流动资产减去流动负债,得出营运资本。

在这个基础上再加上剩余的资产、减去剩余的负债,就得出剩余的股东权益。

balance sheet (unclassified)(非分类式资产负债表):该形式的资产负债表不把资产与负债分成流动与非流动两类。

bargain purchase option(承租人优惠购置权):该条款在租赁开始时,授予承租人有权(但不是义务)在执行日以远低于租赁资产的预期公允价值的价格购买它,这为权利的执行提供了保证。

bargain renewal option(承租人优惠续租权):该条款在租赁开始时,授予承租人有权(但不是债务)在执行日以远低于预期公允租金的价格去续租,这为权利的执行提供保证。

basic earnings per share(原始的每股收益):每股流通在外的普通股在报告期间能够获得的收益额。

当企业拥有稀释性证券时,它并不确认其对流通股的潜在稀释影响。

board of directors(董事会):由股东选举出来,代表他们管理公司的人。

bond(债券):债券通常是一种长期的证券,它代表企业对外借款,常常是以面值1 000美元的形式发行。

bond discount(债券折价):当债券以低于面值的价格出售时,面值与售价的差额就是债券折价。

bond issue price(债券发行价格):利息费用的年金现值加上本金的现值。

bond premium(债券溢价):当债券以高于面值的价格出售时,面值与售价的差额就是债券溢价。

bond sinking fund(债券偿债基金):在债券有效期内由分离出来的资产成立的基金,它在债券到期日支付给债券持有人。