ACCA-F1-19

会计学专业(ACCA班)本科人才培养方案(20090914)

会计学专业(ACCA实验班)本科人才培养方案一、专业名称、代码专业名称:会计学ACCA实验班专业代码:110203二、专业培养目标本专业培养德、智、体、美全面发展,适应社会经济发展和满足社会主义市场经济建设需要,基础扎实、知识面宽、业务能力强、综合素质高、富有创新意识和开拓精神,具备会计、审计及经济学、管理学以及法学等方面的知识和能力,具备良好的职业道德,能在国际会计公司、跨国企业、国内大中型会计师事务所、政府审计部门、企事业单位从事审计和相关业务及教学、科研工作的应用型、融通性、具有国际视野的高级审计人才。

三、专业特色与培养要求本专业特色是“ACCA体系”、“双语教学”和“多证书”。

本专业立足于我校国家级重点学科——会计学,依托我校经、法、管、文、史、哲、理、工等学科综合发展优势,充分利用ACCA的国际平台,将ACCA课程科学嵌入我校会计学专业本科全程培养方案,把学生培养成为以审计学专业为核心,具有较宽厚的经济学、法学和管理学相融通的学科背景的高级专门人才。

通过本专业教学计划所规定的学习与训练,学生基本达到以下培养要求:1.熟练掌握现代审计学的基本理论与方法,具备组织和管理大中型单位审计工作的基本技能;2.掌握从事现代审计工作所必须具备的会计、财务、管理、经济、法律等基本知识;3.熟悉与审计工作有关的会计、财务、经济、管理、财政、金融、税收等方面的法律法规;4.了解审计学科的最新研究成果和发展动态,熟悉国际会计、审计惯例;5.具有较强的语言与文字表达能力,以及获取信息和处理信息的能力;普通话达到国家规定的等级标准;6.具有较强的专业判断能力与决策能力,以及分析问题和解决问题的能力;7.具有创新意识和开拓精神,以及团队精神与合作意识;8.具有良好的职业道德、高尚的人格和社会责任感;9.具有较强的组织、管理能力和领导艺术;10.具有较强的计算机应用能力和较高的外语水平。

四、所属学科与主要课程所属学科:会计学主要课程:会计学原理、税法(Taxation,F6)、企业中的会计师(Accountant in Business,F1)、公司与商法(Corporate and Business Law,F4)、管理会计(Management Accounting,F2)、财务会计(Financial Accounting,F3)、财务报告(Financial Reporting,F7)、审计与鉴证(Auditing and Assurance,F8)、财务管理(Financial Management,F9)、业绩管理(Performance Management,F5)、职业会计师(Professional Accountant,P1)、公司报告(Corporate Report,P2 )、企业分析(Business Analysis,P3)、高级财务管理(Advanced Financial Management,P4)、高级业绩管理(Advanced Performance Management,P5)、会计电算化、会计与审计实验学等。

acca教材-ACCA F1 知识课程

ACCAspace 中国ACCA特许公认会计师教育平台

Copyright ©

12

The impact of technology on organisations

Homeworking and supervision

IT技术还使得部分工作得以在家里迚行,员工不用去上班。但这也带来了监管上的一 些问题。 -------------------------------------------------------------------------------------------------------------Outsourcing(外包)把一些非核心业务交给别人来做。

where the employee was employed.(公司全部关闭戒部分关闭导致的人员 冗余。) 2. The requirements of the business for employees to carry out work of a particular kind have ceased or diminished or are expected to.(流程改迚, 技术迚步导致的人员冗余。)

由内到外: 组织本身 经营环境(产业层面上的环境) 宏观环境(经济政治文化技术层 面的环境) 物理环境(整个以物质形态存在 的环境 )

ACCAspace 中国ACCA特许公认会计师教育平台

Copyright ©

3

The political and legal environment

9

Social and demographic trends

• Population and the labour market(人口数量,人口结构的变化,对劳劢力市场有 深刻长进的影响)

DIN EN 10305-5englisch 2010-05

Daimler AG;019 - HPC D652 - GR/PQS;

2

Unkontrollierte Kopie bei Ausdruck (GR/PQS: Rudolf Ehinger, 2010-09-23)

EUROPEAN STANDARD NORME EUROPÉENNE EUROPÄISCHE NORM

DIN EN 10305-5:2010-05 EN 10305-5:2010 (E)

Contents

Page

Foreword ..............................................................................................................................................................3 1 2 3 4 5 5.1 5.2 6 6.1 6.2 6.3 7 7.1 7.2 8 8.1 8.2 8.3 8.4 8.5 9 9.1 9.2 9.3 10 10.1 10.2 11 11.1 11.2 11.3 11.4 11.5 11.6 12 13

© 2010 CEN

All rights of exploitation in any form and by any means reserved worldwide for CEN national Members.

Ref. No. EN 10305-5:2010: E

Unkontrollierte Kopie bei Ausdruck (GR/PQS: Rudolf Ehinger, 2010-09-23)

Tubes de précision en acier - Conditions techniques de livraison - Partie 5 : Tubes soudés calibrés avec section carrée et rectangulaire Präzisionsstahlrohre - Technische Lieferbedingungen - Teil 5: Geschweißte maßumgeformte Rohre mit quadratischem und rechteckigem Querschnitt

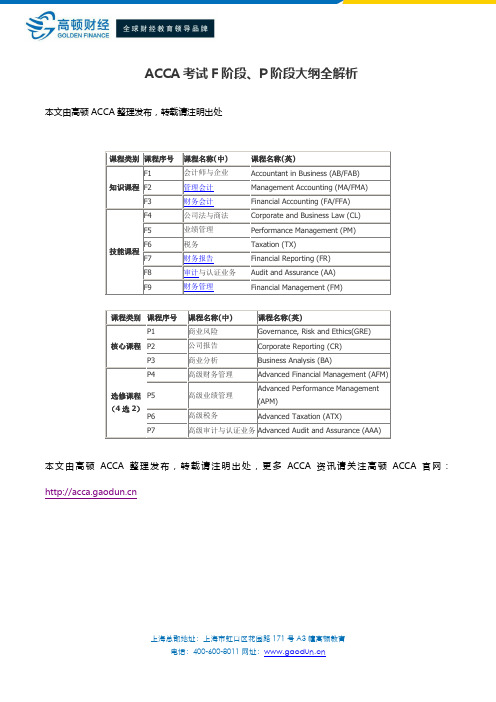

ACCA考试F阶段、P阶段大纲全解析

本文由高顿ACCA整理发布,转载请注明出处

课程类别

课程序号

课程名称(中)

课程名称(英)

知识课程

F1

会计师与企业

Accountant in Business (AB/FAB)

F2

管理会计

Management Accounting (MA/FMA)

F3

财务会计

Financial Accounting (FA/FFA)

本文由高顿ACCA整理发布,转载请注明出处,更多ACCA资讯请关注高顿ACCA官网:

选修课程

(4选2)

P4

高级财务管理

Advanced Financial Management (AFM)

P5

高级业绩管理

Advanced Performance Management (APM)

P6

高级税务

Advanced Taxation (ATX)

P7

高级审计与认证业务

Advanced Audit and Assurance (AAA)

技能课程

F4

公司法与商法

Corporate and Business Law (CL)

F5

业绩管理

Performance Management (PM)

F6

税务

Taxation (TX)

F7

财务报告

Financial Reporting (FR)

F8

审计与认证业务

Audit and Assurance (AA)

F9

财务管理

Financial Management (FM)

课程类别

课程序号

课程名称(中)

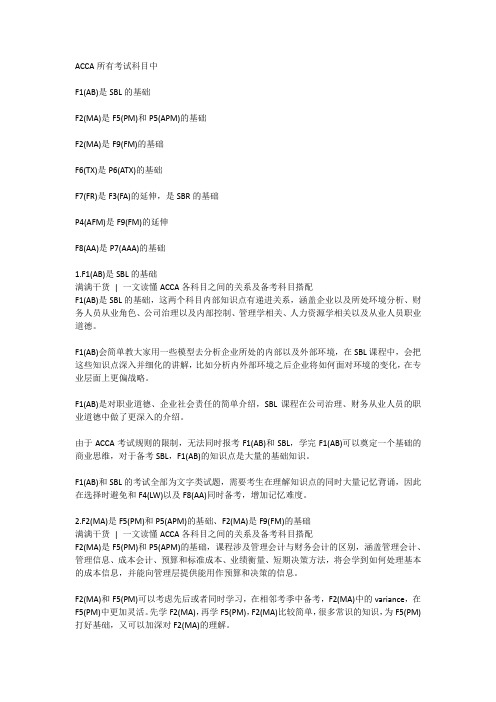

一文读懂ACCA各科目之间的关系及备考科目搭配

ACCA所有考试科目中F1(AB)是SBL的基础F2(MA)是F5(PM)和P5(APM)的基础F2(MA)是F9(FM)的基础F6(TX)是P6(ATX)的基础F7(FR)是F3(FA)的延伸,是SBR的基础P4(AFM)是F9(FM)的延伸F8(AA)是P7(AAA)的基础1.F1(AB)是SBL的基础满满干货| 一文读懂ACCA各科目之间的关系及备考科目搭配F1(AB)是SBL的基础,这两个科目内部知识点有递进关系,涵盖企业以及所处环境分析、财务人员从业角色、公司治理以及内部控制、管理学相关、人力资源学相关以及从业人员职业道德。

F1(AB)会简单教大家用一些模型去分析企业所处的内部以及外部环境,在SBL课程中,会把这些知识点深入并细化的讲解,比如分析内外部环境之后企业将如何面对环境的变化,在专业层面上更偏战略。

F1(AB)是对职业道德、企业社会责任的简单介绍,SBL课程在公司治理、财务从业人员的职业道德中做了更深入的介绍。

由于ACCA考试规则的限制,无法同时报考F1(AB)和SBL,学完F1(AB)可以奠定一个基础的商业思维,对于备考SBL,F1(AB)的知识点是大量的基础知识。

F1(AB)和SBL的考试全部为文字类试题,需要考生在理解知识点的同时大量记忆背诵,因此在选择时避免和F4(LW)以及F8(AA)同时备考,增加记忆难度。

2.F2(MA)是F5(PM)和P5(APM)的基础、F2(MA)是F9(FM)的基础满满干货| 一文读懂ACCA各科目之间的关系及备考科目搭配F2(MA)是F5(PM)和P5(APM)的基础,课程涉及管理会计与财务会计的区别,涵盖管理会计、管理信息、成本会计、预算和标准成本、业绩衡量、短期决策方法,将会学到如何处理基本的成本信息,并能向管理层提供能用作预算和决策的信息。

F2(MA)和F5(PM)可以考虑先后或者同时学习,在相邻考季中备考,F2(MA)中的variance,在F5(PM)中更加灵活。

ACCAF1专业班100道练习题

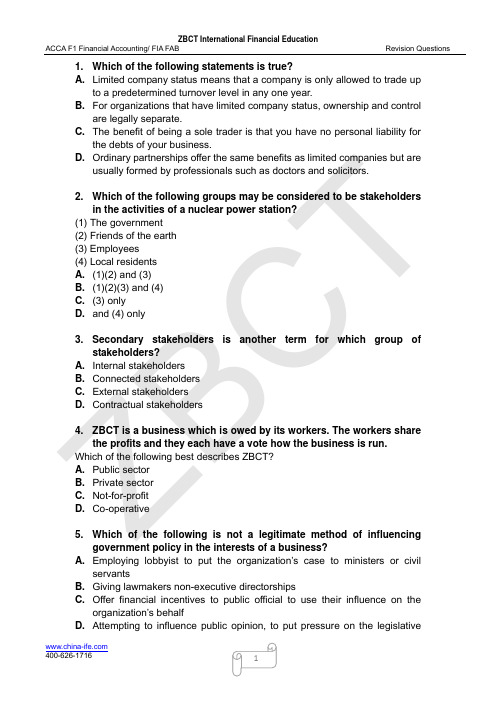

Z BC T 1. Which of the following statements is true?A. Limited company status means that a company is only allowed to trade upto a predetermined turnover level in any one year.B. For organizations that have limited company status, ownership and controlare legally separate.C. The benefit of being a sole trader is that you have no personal liability forthe debts of your business.D. Ordinary partnerships offer the same benefits as limited companies but areusually formed by professionals such as doctors and solicitors.2. Which of the following groups may be considered to be stakeholdersin the activities of a nuclear power station?(1) The government(2) Friends of the earth(3) Employees(4) Local residentsA. (1)(2) and (3)B. (1)(2)(3) and (4)C. (3) onlyD. and (4) only3. Secondary stakeholders is another term for which group ofstakeholders?A. Internal stakeholdersB. Connected stakeholdersC. External stakeholdersD. Contractual stakeholders4. ZBCT is a business which is owed by its workers. The workers sharethe profits and they each have a vote how the business is run.Which of the following best describes ZBCT?A. Public sectorB. Private sectorC. Not-for-profitD. Co-operative5. Which of the following is not a legitimate method of influencinggovernment policy in the interests of a business?A. Employing lobbyist to put the organization’s case to ministers or civilservantsB. Giving lawmakers non-executive directorshipsC. Offer financial incentives to public official to use their influence on theorganization’s behalfD. Attempting to influence public opinion, to put pressure on the legislativeZ BC T agenda6. is an analysis of statistics on birth and death rate,age structures of people and ethnic groups within a community.Which word correctly completes the sentence?A. ErgonomicsB. EconomicsC. PsychographicsD. Demographics7. The stationery and printing company Sunny Co, has recentlyupgraded its computers and printers so that more production hasbecome automated. Many middle managers will now be maderedundant. This is known as:A. DownsizingB. DelayeringC. OutsourcingD. Degrading8. For what function in an organization would demographic informationabout social class be most relevant?A. FinanceB. Human ResourcesC. MarketingD. Purchasing9. ZBCT Co is a large trading company.Alex is the administration manager and is also responsible for legal andcompliance functions. Amy is responsible for after sales service and haresponsibility for ensuring that customers who have purchased goods fromZBCT Co are fully satisfied. Sarenna deals with suppliers and negotiates onthe price and quality of inventory. He is also responsible for identifying themost appropriate suppliers of plant and machinery for the factory. Frank is theinformation technology manager and is responsible for all information systemswithin the company.According to Porter’s value chain, which of the managers is involved in aprimary activity as opposed to a support activity?A. AlexB. AmyC. SarennaD. Frank10. What is the latest stage at which a new recruit to a company shouldfirst be issued with a copy of the company’s health and safety policyZ BC T statement? A.On accepting the position with the company B.As early as possible after employment C.After the first few weeks of employment D.During the final selection interview11. Which of the following is not an element of fiscal policy?A. Government spendingB. Government borrowingC. TaxationD. Exchange rates12. Which of the following is associated with a negative Public SectorNet Cash Requirement?A. The government is running a budget deficitB. The government’s expenditure exceeds its incomeC. The government is running a budget surplusD. Public Sector Debt Repayment (PSDR) is high13. taxes are collected by the Revenue authority from anintermediary, which attempts to pass on the tax to consumers in theprice of goods.Which wore correctly completes this statement?A. RegressiveB. ProgressiveC. DirectD. Indirect14. The currency in country X is the Krone while country Y uses the Euro.Country Y has recently experienced an increase in its exchange ratewith Country X. which of the following effects is likely to result inCountry Y?A. A stimulus to exports in Country YB. An increase in the costs of imports from Country XC. Reducing demand for imports from County XD. A reducing in the rate of cost push inflation15. The following, with one exception, are “protectionist measures” ininternational trade. Which is the exception?A. Import quotasB. Harmonisation of technical standardsC. Customs proceduresD. TariffsZ B C T 16. Which of the following organizations might benefit from a period of high price inflation? A. An organization which has a large number of long term payables B. An exporter of goods to a country with relatively low inflation C. A supplier of goods in a market where consumers au=re highly price sensitive and substitute goods are available D. An organization which receives income at a fixed amount predetermined in a long-term contract 17. Which of the following is an example of cyclical unemployment? A. The entry of school leavers into the labour pool each year B. Lay-offs among agricultural labourers in winter C. Automation of ticketing services in tourism D. Recession in the building industry 18. A surplus on the balance of payments usually means a surplus or deficit on the account. Which word correctly complete this statement? A. Current B. Capital C. Financial D. Income statement 19. Northland, Southland, Eastland and Westland are four countries of Asia. The following economic statistics have been produced for the year of 2007. Country N S E WChange in GDP (%) -0.30 +2.51 -0.55 +2.12Balance of payments current account ($m) +5550.83 -350.47 -150.90 +220.39Change in consumer price (%) +27.50 +15.37 +2.25 +2.15Change in working population employed (%) -4.76 +3.78 +1.76 -8.76Which country experienced stagflation in the relevant period?A. NB. SC. ED. W20. In a free market economy, the price mechanism:A. Aids government controlB. Allocates resourcesC. Reduces unfair completionD. Measure national wealthZ BC T 21. A legal minimum price is set which is below the equllibrrlum price.What will be the impact of this?A. Excess of demand over supplyB. Excess of supply over demandC. An increase in priceD. Nothing22. Which of the following statements about an organization chart is nottrue?A. An organization chart provides a summary of the structure of a businessB. An organization chart can improve internal communications with abusinessC. An organization chart can improve employees’ understanding of their rolein a businessD. An organization chart can Indicate functional authority but not line authoritywithin a business23. Which of the following is a correct definition of “span of control’?A. The number of employees subordinate in the hierarchy to a give managerB. The number of level of levels in the hierarchy ‘below’ a given manager’sC. The length of time between a manager’s decision and the evaluation of itby his superiorD. The number of employees directly responsible to a manager24. Which of the following terms is not use by Mintzherg in hisdescription of organizational structure?A. Strategic apexB. Support baseC. TechnostructureD. Operating core25. Y plc is a growing organisation which has recently diversified into anumber of significant new product markets. It has also recentlyacquired another company in one of its overseas markets.What would be the most appropriate form of organisation for Y plc?A. Geographical departmentationB. DivisionalisationC. Functional departmentationD. Hybrid structure26. Which of the following principles of classical management ischallenged by matrix management?A. Structuring the organization on functional lines .B. Structuring the organization on geographical lines .Z BC T C. Unity of commandD. Decentralisation of decision-making27. Which of the following statements about the informal organization isnot true?A. The influence of the informal organization was highlighted by theHawthorne Studies, in the way group norms and dynamicsaffected productivityB. Informal organization can pose a threat to employee health andsafetyC. Informal organization can stimulate innovationD. Managers in positions of authority generally cannot be part ofinformal organization28. Which of the following statements is/are true?(ⅰ) An informal organization exists with every formal organization(ⅱ) The objectives of the informal organization are broadly the same asthose of the formal organization(ⅲ) A strong, close-knit informal organization is desirable within the formalorganizationA. Statement (ⅰ) onlyB. Statements (ⅰ) and (ⅲ) onlyC. Statements (ⅱ) and (ⅲ) onlyD. Statement (ⅲ) only29. BZ Ness Ltd is an organization with a strongly traditional outlook.It is structured and managed according to classical principles: specialization,the scalar chain of command, unity of command and direction. Personneltend to focus on their own distinct tasks, which are strictly defined anddirected. Communication is vertical, rather than lateral. Discipline is muchprized and enshrined in the rule book of the company.From the scenario, what sort of culture does BZ Ness Ltd have, usingHarrison’s classifications?A. Role cultureB. Task cultureC. Existential cultureD. Power culture30. Which of the following is not one of the terms used by Hofstede todescribe a key dimension of culture?A. Power-distanceB. Acquisitive/givingC. Individualism/collectivismD. Uncertainty avoidanceZ BC T31. Which is the ‘deepest’ set of underlying factors which determineculture, and the hardest to manage?A. ValuesB. BeliefsC. RitualsD. Assumptions32. Research has indicated that workers in country A displaycharacteristics such as toughness and the desire for material wealthand possessions, while workers in country B value personalrelationships, belonging and the quality of life.According to Hofstede’s theory, these distinctions relate to which of thefollowing cultural dimensions?A. Masculinity-feminityB. Power-distanceC. Individualism-collectivismD. Uncertainty avoidance33. Services have certain qualities which distinguish them from products.Because of their ﹍﹍﹍, physical elements such as vouchers, tickets,confirmations and merchandise are an important part of serviceprovision.Which of the following words most accurately completes the sentence?A. IntangibilityB. InseparabilityC. VariabilityD. Perishability34. Which of the following is/are objective of human resourcemanagement?1. To meet the organisation’s social and legal responsibilities relating tothe human resource.2. To manage an organisation’s relationship with its customers3. To develop human resources that will respond effectively to changeA. 1 and 2B. 1 and 3C. 1D. 1, 2 and 335. Jeff, Jane and Jaitinder work in different departments in the firm XYZCo.They are members of the permanent ‘staff committee’ which meets on amonthly basis to discuss staff issues as pensions and benefits. TheirZ BC T purpose is to listen to communication from staff within their departmentand raise issues on of their department at committee meetings. What isthe name given to his type of committee?A. Joint committeeB. Task forceC. Ad hoc committeeD. Standing committee36. Managers Jill and Paul are talking about how to resolve a businessproblem. Jill suggests that a committee should be formed to discussthe issues. Paul argues that committees are:(ⅰ) time-consuming and expensive(ⅱ) they invite a compromise instead of a clear-cut decisionWhich of these statements is true?A. Both (ⅰ) and (ⅱ)B. (ⅰ) onlyC. (ⅱ) onlyD. Neither statement is true37. Diane carries out routine processing of invoices in the purchasingdepartment of L Co.Joanne is Diane’s supervisor. Lesley is trying to decide how many staffwill be needed if some proposed new technology is implemented.Tracey is considering the new work that L Co. will be able to offer andthe new markets it could enter, once the new technology is wellestablished.Which member of L Co. carries out tactical activities?A. DianeB. JoanneC. LesleyD. Tracey38. Which of the following statements about corporate socialresponsibility is true?(ⅰ) CSR guarantees increased profit levels(ⅱ) CSR adds cost to organizational activities and reduces profit levels(ⅲ) Social responsibility may have commercial benefits(ⅳ)Social responsibility is a concern confined to business organisationsA. (ⅰ), (ⅱ), (ⅲ) and (ⅳ)B. (ⅰ) and (ⅲ)C. (ⅱ) and (ⅳ)D. (ⅲ) only39. Which of the following is a feature of poor corporate governance ?Z BC T A.Domination of the board by a single individual B.Critical questioning of senior managers by external auditors C.Supervision of staff in key roles D. Lack of focus on short-term profitability40. The tasks of which body include: monitoring the chief executiveofficer; formulating strategy; and ensuring that there is effectivecommunication of the strategic plan?A. The audit committeeB. The Public Oversight BoardC. The board of directorsD. The nomination committee41. Which of the following would be included in the principles ofCorporate Social Responsibility ?(ⅰ) Human right(ⅱ) Employee(ⅲ) Professional ethics(ⅳ) Support for local suppliersA. (ⅱ) and (ⅲ) onlyB. (ⅰ) onlyC. (ⅱ) ,(ⅲ) and (ⅳ) onlyD. (ⅰ), (ⅱ) and (ⅳ) only42. Which of the following is subject to the least direct regulation ?A. Employment protectionB. Corporate social responsibilityC. Professional ethicsD. Corporate governance43. Which of the following are advantages of having non-executivedirectors on the company board ?1 They can provide a wider perspective than executive directors2 They provide reassurance to shareholders3 They may have external experience and knowledge which executivedirectors do not possess4 They have more time to devote to the roleA. 1 and 3B. 1,2 and 3C. 1,3and 4D. 2 and 444. What is implied be an ‘accommodation’ strategy, in the context ofcorporate social responsibility ?Z BC T A. The business is prepared to take full responsibility for itsactions and plans in advance to minimize its adverse impactson stakeholders and the environmentB. The business recognizes that it has a problem, and attemptsto minimise or avoid additional obligations arising from it.C. The business sites its facilities in areas which will benefitfrom economic activity, while minimsing environmental impactsat the sites.D. The business takes responsibility for its actions in responseto pressure form interest groups or the risk of governmentinterference if it does not.45. Three of the following are outputs of a payroll system,and one is aninput to the system. Which is the input ?A. Credit transferB. Time sheetsC. Payroll analysisD. Pay slips46. Which of the following does company law require a statement offinance position to give ?A. A true and fair view of the profit or loss o the company for thefinancial yearB. An unqualified (or ‘clean’) report on the statement of affairsof the company as at the end of the financial yearC. A true and fair view of the statement of affairs of thecompany as at the end of the financial yearD. A qualified report, setting out matters on which independentauditors disagree with management47. A……………………………is a program which deals with one particularpart of a computerized business accounting system.Which of the following terms correctly completes this definition ?A. SuiteB. ModuleC. SpreadsheetD. Database48. A spreadsheet software application may perform all of the followingbusiness tasks except one. Which one of the following is theexception ?A. The presentation of numerical data in the form of graphsand chartsB. The application of logical tests to dataZ BC T C. The application of ‘What if ?’ scenariosD. Automatic correction of all data entered by the operator intothe spreadsheet49. The preparation and filing of accounts by limited companies eachyear is required by which of the following ?A. Codes of corporate governanceB. National legislationC. International Accounting StandardsD. Local Accounting Standards50. ……………………………..System pool data from internal and externalsources and make information available to senior managers, forstrategic, unstructured decision-marking.A. ExpertB. Decision SupportC. Executive SupportD. Management Support51. All the following statements except one describe the relationshipbetween data and information. Which one is the exception?A. Information is data which has been processed in such a wayas to be meaningful to the person who receives it.B. The relationship between data and information is one of itsinputs and outputsC. Information from one process can be used as data in a secondprocessD. Data is always in numerical form whereas information isalways in text form.52. Which of the following is not an aim of internal controls?A. To enable the organization to respond appropriately tobusiness, operational and financial risksB. To eliminate the possibility of impacts from poor judgment andhuman errorC. To help ensure the quality of internal and external reportingD. To help ensure compliance with applicable laws andregulations53. Which of the following statements about internal audit is true?A. Internal audit is an independent appraisal activityB. Internal audit is separate from the organization’s internalcontrol systemC. Internal audit is carried out solely for the benefit of theZ BC T organization’s stakeholdersD. The internal audit function reports to the finance director54. In the context of audit, what are ‘substantive tests’ designed toaccomplish?A. To establish whether internal controls are being applied asprescribedB. To identify errors and omissions in financial recordsC. To establish the causes of errors or omissions in financialrecordsD. To establish an audit trail55. All of the following, with one exception, are internal factors whichmight increase the risk profile of a business. Which is the exception ?A. Increased competitionB. Corporate restructuringC. Upgraded management information systemD. New personnel56. Which of the following would most clearly present a personnal risk offraud ?A. Segregation of dutiesB. High staff moraleC. Staff not taking their full holiday entitlementsD. Consultative management style57. Which of the following internal controls might be least effective inpreventing fraud, if staff are in collusion with customers ?A. Physical securityB. Requiring signatures to confirm receipt of goods or servicesC. Sequential numbering of transaction documentsD. Authorisation policies58. Leaders may be distinguished from managers by the fact that do notdepend on……………………………..power in the organization.A. Person powerB. Expert powerC. Position powerD. Physical power59. Which of the following writers is not a member of the school ofmanagement thought to which the others belong ?A. FW TaylorB. Elton MayoZ BC T C. Abraham MaslowD. Frederick Herzberg60. Monica is a manager in the finance department of P Co and she hasseveral staff working for her. She has become quite friendly withmost of her staff and like her and appreciate that she does everythingshe can to attend to their needs. Which type of managerial style doesMonica have ?A. ImpoverishedB. Task ManagementC. Country clubD. Dampened pendulum61. According to Fielder, which of the following are true ofpsychologically distant managers ?1. They judge their staff on the basis of performance2. They are primarily Task-oriented3.They prefer formal consultation methods rather than seeking staff opinions4.They are closer to their staffA. 1 and 2B. 2 and 3C. 1,2 and 3D. 1,2,3and 462. What is delegated by a superior to a subordinate ?A. AuthorityB. PowerC. ResponsibilityD. Accountability63. Which of the following is not a technique of scientific management orTaylorism ?A. Micro-design of iobsB. Work study techniques to establish efficient methodsC. Multi-skilled teamworkingD. Financial incentives64. According to research, which of the following statements is true of aconsultative style of management, compared to other styles ?A. It is most popular among subordinatesB. It is most popular among leadersC. It encourages the highest productivityD. It provokes most hostility in groupsZ BC T 65. Which of the following would be classed as a ‘selection’ rather than a‘recruitment’ activity ?A. Job descriptionB. Designing application formsC. Screening application formsD. Advertising vacancies66. What is the current trend in human resource management ?A. Centralise recruitment and selection within HRB. Devolve recruitment and selection to line managersC. Devolve recruitment and selection to the boardD. None of the above67. A financial consultancy firm has a job vacancy for a junior officeassistant at one of its offices. Which of the following would be themost suitable external medium for the job advertisement ?A. Accountancy journalB. National newpapersC. Local newpapersD. The company web site68. Sound business argument can be made for having an equalopportunities policy. Which of the following reasons apply?1 To show common decency and fairness in lines with business ethics2 To widen the recruitment pool3 To attract and retain the best people for the job4 To improve the organization’s images as a good employerA. 1, 2 and 3B. 2 and 3C. 1 and 3D. 1, 2, 3 and 469. Which of the following statements are true?1 Taking active steps to encourage people from disadvantage groups to applyfor jobs and training is classed as positive discrimination.2 Diversity in the workplace means implementing an equal opportunities policy.A. They are both trueB. 1 is true and 2 is falseC. 1 is false and 2 is trueD. They are both false70. Members of the religious minority in a workplace are frequentlysubjected to jokes about their dress and dietary customs, and a bit ofname-calling, by non-religious workmates. They find this offensiveZ BC T and hurtful – even though their colleagues say it is ‘just a bit of fun’.What type of discrimination (if any) would this represent?A. VictimizationB. Indirect discriminationC. HarassmentD. No discrimination is involved71. Which of the following is a potential business benefit of a corporatediversity policy ?A. Compliance with equal opportunities legislationB. Respect for individualsC. Better understanding of target market segmentsD. Efficiency in managing human resources72. Which of the following is most clearly a sign of an ineffective group?A. There is disagreement and criticism within the groupB. There is competition with other groupsC. Members passively accept work decisionsD. Individuals achieve their own targets73. A team leader is having difficulties with conflict in the team, due to‘clashes’ or incompatibilities in the personalities of its members. Theleader draws up a list of options for managing the problem.Which option, from the following list, would be the least practicable?A. Education the members about personality differencesB. Encourage the members to modify their behaviorsC. Encourage the members to modify their personalitiesD. Remove one of the members from the team74. At the Soil-Darretty Bros factory, a project team has been puttogether by management.The team is engaged in debating how they are going to approach the task, andwho is going to do what. Some of their first ideas have not worked out but theyare starting to put forward some really innovative ideas: they get quite excitedin brainstorming sessions, and are uninhibited in putting forward their viewsand suggestions. Factions are emerging, not only around two dominatingindividuals who always seem to disagree.At what stage of Tuckman’s group development model is this team?A. FormingB. StormingC. NormingD. Performing75. In Belbin’s model of team roles, which of the following is mostZ BC T important for a well-functioning team?A. A mix and balance of team rolesB. Nine members, so that all roles are filledC. A focus on functional/task roles, not process rolesD. As few members as possible76. Which of the following theories suggests that people behaveaccording to other people’s expectations of how they should behavein that situation?A. Group think theoryB. Team identity theoryC. Role theoryD. Hero theory77. Phil T Luker & Son offers its employees a reward package whichincludes salary and company car, its factory is safe and clean andrather smart. The work is technically challenging and employees areencouraged to produce innovating solutions to problems.Which of the rewards offered by the firm is a form of intrinsic reward?A. The salaryB. The carC. The factory environmentD. The work78. Which of the following is not a category in Maslow’s hierarchy ofneeds theory?A. Physiological needsB. Freedom of inquiry and expression needsC. Need for affiliationD. Safety needs79. Willy Dewitt-Omott works in Sales. There is always a salescompetition at the year end and the winner is likely to be made teamleader. Willy’s quite certain that he will be able to win and that he willhave more responsibility, which he would like, but he would alsohave to work much longer hours, and he is quite reluctant to do thisfor family reasons.If an expectancy equation were used to assess Willy’s motivation to work hardat the end of the year, based on the information given, which of the followingresults would you expect to see?A. Valence would be high, expectancy high, motivation highB. Valence would be high, expectancy low, motivation lowC. Valence would be around 0, expectancy high, motivation lowD. Valence would around 0, expectancy high, motivation highZ BC T80. The management of Guenguiss Cans Co runs a ‘tight ship’, withclocking-on timekeeping systems, close supervision and rules foreverything. ‘Well’, says the general manger, ‘if you allow people tohave any freedom at work, they will take advantage and their workrate will deteriorate’.Which of Douglas McGregor’s ‘theories’ does this management teamsubscribe to?A. Theory XB. Theory YC. Theory WD. Theory Z81. The following, with one exception, are claimed as advantages for jobenrichment as a form of job redesign. Which is the exception?A. It increases job satisfactionB. It enhances quality of outputC. It replaces monetary rewardsD. It reduces supervisory costs82. Trainee Sare is unhappy in her current training programme, becauseit is too ‘hands on’: she is required to attempt techniques before shehas had a chance to study the underlying principles first. She spendsthe evenings trying to read ahead in the course text-book.Which of Honey and Mumford’s learning styles is probably Sare’s preferredstyle?A. ReflectorB. PragmatistC. TheoristD. Activist83. Whcih of the following statement about training is most likely to bethe foundation of an effective training policy?A. Training is the responsibility of the HR departmentB. Training is all cost and no quantifiable benefitC. The important thing is to do lots of trainingD. Training can be an effective solution to some performance problems84. All the following ,with one exception, are clear benefits of trainingand development for an organization. Which is the exception?A. Increased organizational flexibilityB. Less need for detailed supervisionC. Enhanced employability of staff membersD. Improve succession planning。

accaf1skateholder 的·定义

ACCAF1stakeholder具有重要影响力和利益相关性的裙体,其行为和决策能够直接影响到组织的经营和发展。

正确理解和有效管理stakeholder对于组织的长期发展至关重要。

1. 什么是ACCAF1stakeholder?ACCAF1stakeholder是指对组织有重要利益相关性和影响力的各种裙体,包括但不限于股东、员工、客户、供应商、政府机构、媒体、社会公众等。

这些裙体与组织之间存在着相互依存的关系,其行为和决策能够直接影响到组织的经营和发展。

2. stakeholder的特点ACCAF1stakeholder的特点主要包括以下几个方面:(1)利益相关性:stakeholder与组织之间存在着利益的相互关系,其行为和决策会对组织的利益产生直接或间接的影响。

(2)影响力:stakeholder拥有对组织的经营和发展产生重要影响的能力,其行为和决策对组织的决策和战略制定产生重要影响。

(3)多样性:ACCAF1stakeholder具有多样性和复杂性,包括股东、员工、客户、供应商、政府机构、媒体、社会公众等各种裙体。

3. stakeholder的重要性ACCAF1stakeholder对于组织的经营和发展具有重要影响,其重要性主要体现在以下几个方面:(1)战略决策:stakeholder的行为和决策对组织的战略决策和发展方向产生直接影响,正确理解和有效管理stakeholder对于组织进行战略决策具有重要意义。

(2)风险管理:stakeholder的行为和决策可能会对组织带来各种风险,包括经济风险、法律风险、声誉风险等,正确理解和有效管理stakeholder对于降低组织的风险具有重要意义。

(3)社会责任:stakeholder的利益相关性和影响力与组织的社会责任密切相关,正确理解和有效管理stakeholder对于组织履行社会责任具有重要意义。

4. 如何正确理解和有效管理stakeholder有效理解和管理stakeholder对于组织的长期发展至关重要,主要包括以下几个方面:(1)识别和分析:识别和分析对组织具有重要利益相关性和影响力的各种stakeholder,包括股东、员工、客户、供应商、政府机构、媒体、社会公众等。

ACCA16门科目简介

ACCA F阶段与P阶段共16门科目简介第一部分为基础阶段,主要分为知识课程和技能课程两个部分。

知识课程主要涉及财务会计和管理会计方面的核心知识,也为接下去进行技能阶段的详细学习打下坚实的地基。

知识课程的三个科目同时也是FIA方式注册学员所学习的FAB、FMA、FFA三个科目。

技能课程共有六门课程,广泛的涵盖了一名注册会计师所涉及的知识领域及必须掌握的技能。

知识课程FUNDAMENTALS——KNOWLEDGEF1 会计师与企业Accountant in Business (AB)F2 管理会计Management Accounting (MA)F3 财务会计Financial Accounting (FA)技能课程FUNDAMENTALS——SKILLSF4 公司法与商法Corporate and Business Law (CL)F5 业绩管理Performance Management (PM)F6 税务Taxation (TX)F7 财务报告Financial Reporting (FR)F8 审计与认证业务Audit and Assurance (AA)F9 财务管理Financial Management (FM)第二部分为专业阶段,主要分为核心课程和选修(选二)课程。

该阶段的课程相当于硕士阶段的课程难度,是对第一部分课程的引申和发展。

该阶段课程引入了作为未来的高级会计师所必须的更高级的职业技能和知识技能。

选修课程为从事高级管理咨询或顾问职业的学员,设计了解决更高级和更复杂的问题的技能。

核心课程PROFESSIONAL——ESSENTIALSP1 专业会计师Professional Accountant (PA)P2 公司报告Corporate Reporting (CR)P3 商务分析Business Analysis (BA)选修课程PROFESSIONAL——OPTIONS(四门任选二门)P4 高级财务管理Advanced Financial Management (AFM)P5 高级业绩管理Advanced Performance Management (APM)P6 高级税务Advanced Taxation (ATX)P7 高级审计与认证业务Advanced Audit and Assurance (AAA)Written by first intuition China(第一直觉教育ACCA)。

ACCAF1StudyText,PDF原版BPP教材

Accountant in Business Paper F1 Course Notes ACF1CN07 l i BPP provides revision courses question days mock days and specific material to assist you in this important phase of your studies. F1 Accountant in Business Study Programme for Standard Taught Course Page Introduction to the paper and the course...............................................................................................................iii 1 Business organisation and structure...........................................................................................................1.1 2 Information technology and systems...........................................................................................................2.1 3 Influences on organisational culture............................................................................................................3.1 4 Ethical considerations........................................................................................................................ ..........4.1 5 Corporate governance and social responsibility..........................................................................................5.1 6 Home study chapter – The macro economic environment..........................................................................6.1 End of Day 1 – refer to Course Companion for Home Study 7 The business environment..........................................................................................................................7.1 8 Home study chapter – The role of accounting.............................................................................................8.1 9 Control security and audit............................................................................................................................9.1 10 Identifying and preventing fraud................................................................................................................10.1 11 Leadership and managing people.............................................................................................................11.1 12 Individuals groups teams.........................................................................................................................12.1 End of Day 2 – refer to Course Companion for Home Study Course exam 1 13 Motivating individuals and groups.............................................................................................................13.1 14 Personal effectiveness and communication..............................................................................................14.1 15 Recruitment and selection.........................................................................................................................15.1 16 Diversity and equal opportunities..............................................................................................................16.1 17 Training and development. (1)7.1 18 Performance appraisal (1)8.1 End of Day 3 – refer to Course Companion for Home Study Course exam 2 19 Answers to Lecture Examples...................................................................................................................19.1 20 Appendix: Pilot Paper questions................................................................................................................20.1 ??Revision of syllabus ?? Testing of knowledge ?? Question practice ?? Exam technique practice INTRODUCTION ii Introduction to Paper F1 Accountant in Business Overall aim of the syllabus To introduce knowledge and understanding of the business and its environment and the influence this has on how organisations are structured on the role of the accounting and other key business functions in contributing to the efficient effective and ethical management and development of an organisation and its people and systems. The syllabus The broad syllabus headings are: A Business organisation structure governance and management B Key environmental influences and constraints on business and accounting C History and role of accounting in business D Specific functions of accounting and internal financial control E Leading and managing individuals and teams F Recruiting and developing effective employees Main capabilities On successful completion of this paper candidates should be able to: ?? Explain how the organisation is structured governed and managed ?? Identify and describe the key environmental influences and constraints ?? Describe the history purpose and position of accounting ?? Identify and explain the functions of accounting systems ?? Recognise the principles of leadership and authority ?? Recruit and develop effective employees Links with other papers This diagram shows where direct solid line arrows and indirect dashed line arrows links exist between this paper and other papers that may follow it. The Accountant in Business is the first paper that students should study as it acts as an introduction to business structure and purpose and to accountancy as a core business function. BA P3 MA F2 and FA F3PA P1 AB F1 INTRODUCTION iii Assessment methods and format of the exam Examiner: Bob Souster The examination is a two hour paper-based or computer-based examination. Questions will assess all parts of the syllabus and will test knowledge and some comprehension of application of this knowledge. The examination will consist of 40 two mark and 10 one mark multiple choice questions. The pass mark is 50 ie. 45 out of 90. INTRODUCTION iv Course Aims Achieving ACCAs Study Guide Outcomes Business organisations structure governance and management A1 The business organisation and its structure Chapter 1A2 The formal and informal business organisation Chapter 3 A3 Organisational culture in business Chapter 3 A4 Stakeholders of business organisations Chapter 3 A5 Information technology and information systems in business Chapter 2 A6 Committees in the business organisation Chapter 1 A7 Business ethics and ethical behaviour Chapter 4 A8 Governance and social responsibility Chapter 5 Key environmental influences and constraints on business and accounting B1 Political and legal factors Chapter 7 B2 Macro-economic factors Chapter 6 B3 Social and demographic factors Chapter 7 B4 Technological factors Chapter 7 B5 Competitive factors Chapter 7 History and role of accounting in business C1 The history and functions of accounting in business Chapter 8 C2 Law and regulations governing accounting Chapter 8 C3 Financial systems procedures and IT applications Chapter 8 C4 The relationship between accounting and other business functions Chapter 1 Specific functions of accounting and internal financial control D1 Accounting and financial functions within business Chapter 1 D2 Internal and external auditing and their functions Chapter 9 D3 Internal financial control and security within business organisations Chapter 9 D4 Fraud and fraudulent behaviour and their prevention in business Chapter 10 INTRODUCTION v Leading and managing individuals and teams E1 Leadership management and supervision Chapter 11 E2 Individual and group behaviour in business organisations Chapter 12 E3 Team formationdevelopment and management Chapter 12 E4 Motivating individuals and groups Chapter 13 Recruiting and developing effective employees F1 Recruitment and selection managing diversity and equal opportunities Chapter 15 16 F2 Techniques for improving personal effectiveness at work and their benefits Chapter 14 F3 Features of effective communication Chapter 14 F4 Training development and learning in the maintenance and improvement of business performance Chapter 17 F5 Review and appraisal of individual performance Chapter 18 INTRODUCTION vi Classroom tuition and Home study Your studies for BPP consist of two elements classroom tuition and home study. Classroom tuition In class we aim to cover the key areas of the syllabus. To ensure examination success you will need to spend private study time reinforcing your classroom course with question practice and reviewing areas of the Course Notes and Study Text. Home study To support you with your private study BPP provides you with a Course Companion which helps you to work at home and aims to ensure your private study time is effectively used. The Course Companion includes a Home Study section which breaks down your home study by days one to be covered at the end of each day of the course. You will find clear guidance as to the time to spend on various activities and their importance. You are also provided with sample questions and either two course exams which should be submitted for marking as they become due or an I-pass CD which is full of questions. These may include questions on topics covered in class and home study. BPP Learn Online Come and visit the BPP Learn Online free at/acca/learnonline for exam tips FAQs and syllabus health check. ACCA Forum We have thriving ACCA bulletin boards at /accaforum. Register and discuss your studies with tutors and students. Helpline If you have any queries during your private study simply contact your class tutor on the telephone number or e-mail address that they will supply. Alternatively call 44 020 8740 2222 or your local training centre if outside the London area and ask for a tutor for this paper to speak to you or to call you back within 24 hours. Feedback The success of BPP’s courses has been built on what you the students tell us. At the end of the course for each subject you will be given a feedback form to complete and return. If you have any issues or ideas before you are given the form to complete please raise them with the course tutor or relevant head of centre. If this is not possible please email . INTRODUCTION vii Key to icons Question practice from the Study Text This is a question we recommend you attempt for home study. Real world examples These can be found in the Course Companion. Section reference in the Study Text Further reading is needed on this area to consolidate your knowledge. INTRODUCTION viii 1.1 Syllabus Guide Detailed Outcomes Having studied this chapter you will be able to: ?? Ascertain the appropriate organisational structure for different types and sizes of business. ?? Understand the concepts of span of control and scalar chains. ?? Appreciate the differing levels of strategy in an organisation. Exam Context This chapter lays the foundation for an understanding of what organisations are what they do and how they do it. Section 2 Organisational structure represents a higher level of knowledge. You must be able to apply knowledge to exam questions. Qualification Context An understanding of business structures is important with regard to higher level accounting papers as well as P3 Business Analysis. Business Context Appreciating why organisations are structured in different ways will help with an understanding of how they should be managed. Business organisation and structure 1: BUSINESS ORGANISATION AND STRUCTURE 1.2Overview Departments and functions Why does the organisation exist Structural forms Business hierarchy 1: BUSINESS ORGANISATION AND STRUCTURE 1.3 1 Organisations 1.1 Definition – An organisation is a social arrangement which pursues collective goals which controls its own performance and which has a boundary separating it from its environment. Boundaries can be physical or social. 1.2 Key categories: ?? Commercial ?? Not for profit ?? Public sector ?? Charities ?? Trade unions ?? Local authorities ?? Mutual associates Class exercise Required Identify a real-world example of the above categories of organisation. 1.3 Organisations owned or run by the government local or national or government agencies are described as being in the public sector. All other organisations are classified as the private sector. Limited liability 1.4 Limited companies denoted by X Ltd or X plc are set up so as to have a separate legal entity from their owners shareholders. Liability of these owners is thus limited to the amount invested. Private v public 1.5 Private companies are usually owned by a small number of people family members and these shares are not easily transferable. Shares of public companies will be traded on the Stock Exchange. Pg 52-561: BUSINESS ORGANISATION AND STRUCTURE 1.4 2 Organisational structure 2.1 Henry Mintzberg believes that all organisations can be analysed into five components according to how they relate to the work of the organisation and how they prefer to co-ordinate. a Strategic apex Drives the direction of the business through control over decision-making. b Technostructure Drives efficiency through rules and procedures. c Operating core Performs the routine activities of the organisation in a proficient and standardised manner. d Middle line Performs the management functions of control over resources processes and business areas. e Support staff Provide expertise and service to the organisation. Strategic Apex Support Staff Technostructure Middle Line Operating Core 1: BUSINESS ORGANISATION AND STRUCTURE 1.5 Exam standard question Required Match the following staff/rules to Mintzbergs technostructure: a Manager of a retail outlet supervising 40 staff. b A salesman responsible for twenty corporate accounts. c The owner of a start-up internet company employing two staff. d The HR department which provides support to business managers. e The IT department seeking to standardise internal systems. 3 Structural forms for organisations Scalar chain and span of control 3.1 As organisations grow in size and scope different organisational structures may be suitable. 3.2 The Scalar chain and Span of control determine the basic shape. The scalar chain relates to levels in the organisation and the span of control the number of employees managed. 3.3 Tall organisations have a: a Long scalar chain via layers of management b Hierarchy c Narrow span of control. 3.4 Flat organisations have a: a Short scalar chain less layers b Wide span of control. 1: BUSINESS ORGANISATION AND STRUCTURE 1.6 3.5 MD Divisional directors Department managers Section managers MD Supervisors Department managers Charge hands Supervisors Workers Workers Tall Flat Pilot paper Required Identify factors which may contribute to the length of the chain and the span of control. Organisational structures 3.6 Entrepreneurial A fluid structure with little or no formality. Suitable for small start-up companies the activities and decisions are dominated by a key central figure the owner/entrepreneur. 3.7 Functional This structure is created via separate departments or functions. Employees are grouped by specialism and departmental targets will be set. Formal communication systems will be set up to ensure information is shared. 1: BUSINESS ORGANISATION AND STRUCTURE 1.7 3.8 Matrix A matrix organisation crosses a functional with a product/customer/projectstructure. This structure was created to bring flexibility to organisations geared towards project work or customer-specific jobs. Staff may be employed within a hierarchy or within specific functions but will be slotted into different teams or tasks where their skill is most needed. The matrix structure is built upon the principles of flexibility and dual authority. Required Identify two advantages and two disadvantages of each structure. Advantages Disadvantages Entrepreneurial Functional Matrix 3.9 Organisations are rarely composed of only one type of structure especially if the organisation has been in existence for some time and as a consequence a hybrid structure may be established. Hybrid structures involve a mixture of functional divisionalisation and at least one other form of divisionalisation. Area Manager A Area Manager B Area Manager C.。

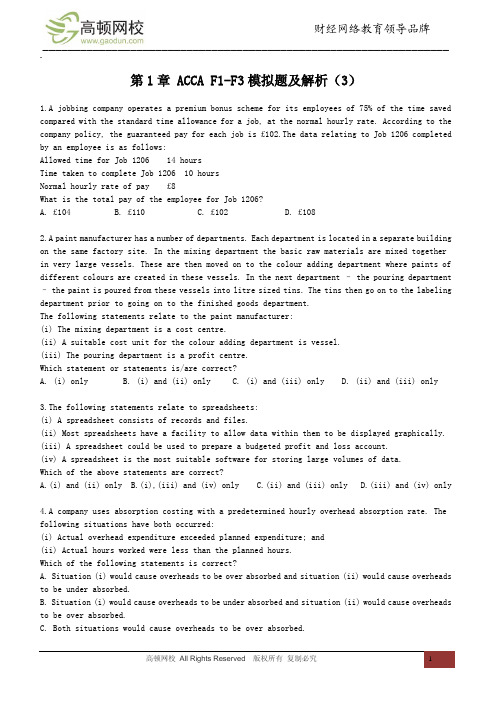

ACCA F1-F3模拟题及解析(3)

第1章 ACCA F1-F3模拟题及解析(3)1.A jobbing company operates a premium bonus scheme for its employees of 75% of the time saved compared with the standard time allowance for a job, at the normal hourly rate. According to the company policy, the guaranteed pay for each job is £102.The data relating to Job 1206 completed by an employee is as follows:Allowed time for Job 1206 14 hoursTime taken to complete Job 1206 10 hoursNormal hourly rate of pay £8What is the total pay of the employee for Job 1206?A. £104B. £110C. £102D. £1082.A paint manufacturer has a number of departments. Each department is located in a separate building on the same factory site. In the mixing department the basic raw materials are mixed togetherin very large vessels. These are then moved on to the colour adding department where paints of different colours are created in these vessels. In the next department – the pouring department – the paint is poured from these vessels into litre sized tins. The tins then go on to the labeling department prior to going on to the finished goods department.The following statements relate to the paint manufacturer:(i) The mixing department is a cost centre.(ii) A suitable cost unit for the colour adding department is vessel.(iii) The pouring department is a profit centre.Which statement or statements is/are correct?A. (i) onlyB. (i) and (ii) onlyC. (i) and (iii) onlyD. (ii) and (iii) only3.The following statements relate to spreadsheets:(i) A spreadsheet consists of records and files.(ii) Most spreadsheets have a facility to allow data within them to be displayed graphically. (iii) A spreadsheet could be used to prepare a budgeted profit and loss account.(iv) A spreadsheet is the most suitable software for storing large volumes of data.Which of the above statements are correct?A.(i) and (ii) onlyB.(i),(iii) and (iv) onlyC.(ii) and (iii) onlyD.(iii) and (iv) only4.A company uses absorption costing with a predetermined hourly overhead absorption rate. The following situations have both occurred:(i) Actual overhead expenditure exceeded planned expenditure; and(ii) Actual hours worked were less than the planned hours.Which of the following statements is correct?A. Situation (i) would cause overheads to be over absorbed and situation (ii) would cause overheads to be under absorbed.B. Situation (i) would cause overheads to be under absorbed and situation (ii) would cause overheads to be over absorbed.C. Both situations would cause overheads to be over absorbed.D. Both situations would cause overheads to be under absorbed.5.A company operates a job costing system. Job 812 requires £60 of direct materials, £40 of direct labour and £20 of direct expenses. Direct labour is paid £8 per hour. Production overheads are absorbed at a rate of £16 per direct labour hour and non-production overheads are absorbed at a rate of 60% of prime cost.What is the total cost of Job 812?A. £240B. £260C. £272D. £3206.At the end of manufacturing in Process I, product K can be sold for £10 per litre. Alternatively product K could be further processed into product KK in Process II at an additional cost of £1 per litre input into this process. Process II is an existing process in which a loss of 10% of the input volume occurs. At the end of the further processing, product KK could be sold for £12 per litre.Which of the following statements is correct in respect of 9,000 litres of product K?A. Further processing into product KK would increase profits by £9,000.B. Further processing into product KK would increase profits by £8,100.C. Further processing into product KK would decrease profits by £900.D. Further processing into product KK would decrease profits by £1,800.The following information relates to questions 17 and 18:The standard direct material cost for a product is £50 per unit (12·5 kg at £4 per kg). Last month the actual amount paid for 45,600 kg of material purchased and used was £173,280 and the direct material usage variance was £15,200 adverse.7.What was the direct material price variance last month?A. £8,800 AdverseB. £8,800 FavourableC. £9,120 AdverseD. £9,120 Favourable8. What was the actual production last month?A. 3,344 unitsB. 3,520 unitsC. 3,952 unitsD. 4,160 units9. Equipment owned by a company has a net book value of £1,800 and has been idle for some months. It could now be used on a six months contract which is being considered. If not used on this contract, the equipment would be sold now for a net amount of £2,000. After use on the contract, the equipment would have no saleable value and would be dismantled. The cost of dismantling and disposing of it would be £200.What is the total relevant cost of the equipment to the contract?A. £1,200B. £1,800C. £2,000D. £2,20010. A contract is under consideration which requires 800 labour hours to complete. There are 450 hours of spare labour capacity for which the workers are still being paid the normal rate of pay. The remaining hours required for the contract can be found either by overtime working paid at 50% above the normal rate of pay or by diverting labour from the manufacture of product OT. If the contract is undertaken and labour is diverted, then sales of product OT will be lost. Product OT takes seven labour hours per unit to manufacture and makes a contribution of £14 per unit.The normal rate of pay for labour is £8 per hour.What is the total relevant labour cost to the contract?A. £3,500B. £4,200C. £4,500D. £4,90011. A company determines its order quantity for a raw material by using the Economic Order Quantity (EOQ) model.What would be the effects on the EOQ and the total annual holding cost of a decrease in the cost of ordering a batch of raw material?EOQ Total annual holding costA. Higher LowerB. Higher HigherC. Lower HigherD. Lower Lower12. A company manufactures two products, X and Y, in a factory divided into two production cost centres, Primary and Finishing. The following budgeted data are available:Cost centre Primary FinishingAllocated and apportioned fixedoverhead costs £96,000 £82,500Direct labour minutes per unit:– product X 36 25– product Y 48 35Budgeted production is 6,000 units of product X and 7,500 units of product Y.Fixed overhead costs are to be absorbed on a direct labour hour basis.What is the budgeted fixed overhead cost per unit for product Y?A. £11B. £12C. £14D. £1513. A company has three shops (R, S and T) to which the following budgeted information relates:Shop R Shop S Shop T Total£000 £000 £000 £000Sales 400 500 600 1,500–––– –––– –––– ––––Contribution 100 60 120 280Less: Fixed costs (60) (70) (70) (200)–––– –––– –––– ––––Profit/(Loss) 40 (10) 50 80–––– –––– –––– ––––60% of the total fixed costs are general company overheads. These are apportioned to the shops on the basis of sales value. The other fixed costs are specific to each shop and are avoidable if the shop closes down.If shop S is closed down and the sales of the other two shops remained unchanged, what would be the revised budgeted profit for the company?A. £50,000B. £60,000C. £70,000D. £90,00014.An organization manufactures a single product which has a variable cost of £36 per unit. The organization’s total weekly fixed costs are £81,000 and it has a contribution to sales ratio of 40%. This week it plans to manufacture and sell 5,000 units.What is the organization’s margin of safety this week (in units)?A. 1,625B. 2,750C. 3,375D. 3,50015. An organization has the following total costs at two activity levels:Activity level (units) 15,000 24,000Total costs £380,000 £470,000Variable cost per unit is constant in this activity range but there is a step up of£18,000 in the total fixed costs when the activity exceeds 20,000 units.What are the total costs at an activity level of 18,000 units?A. £404,000B. £410,000C. £422,000D. £428,00016. The following statements refer to different types of planning within a manufacturing organization:(i) Operational planning includes the scheduling of work to be done in the short term.(ii) Tactical planning includes consideration of ways in which the productivity of the factory workforce could be improved.(iii) Strategic planning includes the setting of the organization’s long term objectives. Which of the statements are correct?A. (i) and (ii) onlyB. (i) and (iii) onlyC. (ii) and (iii) onlyD. (i), (ii) and (iii)17.The following statements relate to spreadsheets:(i) A spreadsheet is the most suitable software for the storage of large amounts of data. (ii) A spreadsheet consists of rows, columns and cells.(iii) A forecast profit and loss account could be prepared using a spreadsheet.Which of the statements are correct?A. (i) and (ii) onlyB. (i) and (iii) onlyC. (ii) and (iii) onlyD.(i), (ii) and (iii)18. Data relating to one particular stores item are as follows:Average daily issues 70 unitsMaximum daily issues 90 unitsMinimum daily issues 50 unitsLead time for the replenishment of stock 11 to 17 daysReorder quantity 2,000 unitsReorder level 1,800 unitsWhat is the maximum stock level (in units) for this stores item?A. 2,950B. 3,100C. 3,250D. 3,80019.A company determines its order quantity for a component using the Economic Order Quantity (EOQ) model.What would be the effects on the EOQ and the total annual ordering cost of a decrease in the annual cost of holding one unit of the component in stock?EOQ Total annual ordering costA Lower No effectB Higher No effectC Lower HigherD Higher Lower20. A company operates a job costing system. Job number 607 requires £300 of direct materials, £400 of direct labour and £100 of direct expenses. Direct labour is paid at a rate of £8 per hour. Production overheads are absorbed at a rate of £40 per direct labour hour and non-production overheads are absorbed at a rate of 150% of prime cost.What is the total cost of job number 607?A. £3,750B. £3,850C. £4,000D. £4,20021. A company uses absorption costing with a predetermined hourly fixed overhead absorption rate. The following situations arose last month:(i) Actual overhead expenditure was less than the planned expenditure.(ii) Actual hours worked exceeded planned hours.Which statement is correct?A. Situation (i) would cause overheads to be under absorbed and situation (ii) would cause overheads to be over absorbed.B. Situation (i) would cause overheads to be over absorbed and situation (ii) would cause overheads to be under absorbed.C. Both situations would cause overheads to be over absorbed.D. Both situations would cause overheads to be under absorbed.22.A company manufactures two products K1 and K2 in a factory consisting of two cost centres, Y and Z. The following budgeted data are available:Cost centreY ZAllocated and apportioned fixedoverhead costs £576,000 £288,000Direct labour hours per unit:Product K1 5 2Product K2 3 4Budgeted output is 12,000 units of each product. Fixed overhead costs are absorbed on a direct labour hour basis.What is the budgeted fixed overhead cost per unit for product K2?A. £34B. £36C. £38D. £4223.A factory consists of two production cost centres (P and Q) and two service cost centres (T and V). The total overheads allocated and apportioned to each cost centre are as follows:P Q T VTotal overheads £180,000 £120,000 £128,000 £140,000The work done by the service cost centres can be represented as follows:P Q T VPercentage of service cost centre T to: 70% 30% – –Percentage of service cost centre V to: 40% 30% 30% –The service cost centre costs are apportioned to production cost centres using a method that fully recognises any work done by one service cost centre for another.What are the total overheads for production cost centre P after the reapportionment of all servicecost centre costs?A. £325,600B. £349,600C. £355,000D. £379,000The following information relates to questions 34 and 35:A company operates a process costing system using the first-in-first-out (FIFO) system of valuation. No losses occur in the process. The following data relate to last month:UnitsOpening work-in-progress 200 with a total value of £1,530Input to the process 1,000Completed production 1,040Last month the cost per equivalent unit of production was £20 and the degree of completion of the work-in-progress was 40% throughout the month.24.What was the value (at cost) of last month’s closing work-in-progress?A. £1,224B. £1,280C. £1,836D. £1,92025.What was the cost of the 1,040 units completed last month?A. £19,200B. £19,930C. £20,730D. £20,80026.The following statements relate to the calculation of the regression line y = a + bx using the information on the formulae sheet at the end of this examination paper:(i) _xy is calculated by multiplying _x by _y.(ii) _y2 is not the same as (_y)2 .(iii) n represents the number of pairs of data items used.Which statements are correct?A. (i) and (ii) onlyB. (i) and (iii) onlyC. (ii) and (iii) onlyD. (i), (ii) and (iii)27.Which of the following correlation coefficients indicates the weakest relationship between two variables?A. +0·9B. – 0·6C. – 0·8D. – 1·028. The following statements relate to responsibility centres:(i) The manager of a revenue centre is responsible for sales and costs in a segment of an organisation. (ii) Return on capital employed is a suitable measure of performance in a profit centre.(iii) Cost centres are found in manufacturing and service organisations.Which of the statements, if any, is correct?A. (i) onlyB. (ii) onlyC. (iii) onlyD. None of them.29.A company operates a standard absorption costing system in which the standard fixed production overhead rate is £9 per hour.The following data relate to last month:Budgeted hours 8,000Standard hours for actual production 8,200Actual hours worked 8,400What was the fixed production overhead capacity variance for last month?A. £1,800 AdverseB. £1,800 FavourableC. £3,600 AdverseD. £3,600 Favourable30.A company operates a standard marginal costing system. Last month the company sold 200 unitsmore than it planned to sell. The following data relate to last month:Standard Actual£ £Selling price per unit 40 38Variable cost per unit 30 29What was the favourable sales volume contribution variance last month?A.£1,600B. £1,800C. £2,000D. £2,2001.【答案】A【解析】(10 x £8) + [(14 – 10) x 0·75 x £8] = £1042.【答案】B3.【答案】C4.【答案】D5.【答案】C【解析】(60 + 40 + 20) + [(40 ÷ 8) x 16] + (0·60 x 120) = £2726.【答案】D£【解析】Sales value after further processing = (9,000 x 0·9) x £12 = 97,200Sales value without further processing = (9,000 x £10) 90,000––––––Increase in sales revenue 7,200Less: Further processing cost = (9,000 x £1) (9,000)––––––Decrease in profit by further processing (£1,800)7.【答案】D【解析】[(45,600 x 4) – 173,280] = £9,120 Favourable8.【答案】A£【解析】Actual usage at standard cost (45,600 x 4) 182,400Less: Adverse usage variance (15,200)–––––––Standard cost for actual production 167,200–––––––Actual production (units) = (167,200 ÷ 50) = 3,3449.【答案】 D【解析】Opportunity cost now + disposal cost at end of contract (2,000 + 200) = £2,20010.【答案】A【解析】(800 – 450) x [8 + (14 ÷ 7)] = £3,50011.【答案】D12.【答案】D【解析】Total direct labour hours:Primary (6,000 x 36 ÷ 60) + (7,500 x 48 ÷ 60) 9,600Finishing (6,000 x 25 ÷ 60) + (7,500 x 35 ÷ 60) 6,875Absorption rates:Primary (96,000 ÷ 9,600) £10 per hourFinishing (82,500 ÷ 6,875) £12 per hourFixed cost per unit (Y): (48 ÷ 60) x 10 + (35 ÷ 60) x 12 = £1513.【答案】 A£【解析】Total fixed costs for shop S 70,000Less: Apportioned general costs (200 x 0.60) ÷ (500 ÷ 1,500) (40,000)–––––––Specific fixed costs for shop S 30,000–––––––If shop S closed down net contribution lost (60,000 – 30,000) 30,000Revised budgeted profit for company (80,000 – 30,000) £50,00014. 【答案】A【解析】Contribution per unit (CPU) = (36 ÷ 0·60) ⋅ 0·40 = £24Break-even point = (81,000 ÷ 24) = 3,375 unitsMargin of safety = (5,000 – 3,375) = 1,625 units15. 【答案】A【解析】Using the high low method:Variable cost per unit = [(470,000 – 18,000) – 380,000] ÷ [24,000 – 15,000] = £8 Total fixed costs (below 20,000 units) = 380,000 – (15,000 ⋅ 8) = £260,000Total costs for 18,000 units = 260,000 + (18,000 ⋅ 8) = £404,00016. 【答案】D17. 【答案】C18. 【答案】C【解析】Reorder level – (Minimum usage in shortest lead time) + Reorder quantity =1,800 – (50 ⋅ 11) + 2,000 = 3,250 units = Maximum stock level19. 【答案】D20. 【答案】C £【解析】Prime cost (300 + 400 + 100) = 800+ Production overheads (400 ÷ 8) ⋅ 40 = 2,000+ Non-production overheads (1·5 ⋅ 800) = 1,200–––––Total cost 4,00021. 【答案】C22. 【答案】A【解析】Absorption rate (Y) = 576,000 ÷ [(5 + 3) ⋅ 12,000] = £6 per hourAbsorption rate (Z) = 288,000 ÷ [(2 + 4) ⋅ 12,000] = £4 per hourFixed overhead cost per unit (K2) = [(3 ⋅ £6) + (4 ⋅ £4)] = £3423.【答案】 C【解析】Total overheads (T) = 128,000 + (0·30 ⋅ 140,000) = £170,000Total overheads (P) = 180,000 + (0·70 ⋅ 170,000) + (0·40 ⋅ 140,000) = £355,00024.【答案】B【解析】Closing work in progress (WIP) = (200 + 1,000 – 1,040) = 160 units WIP valuation = (160 ⋅ 0·40 ⋅ 20) = £1,28025.【答案】 C£【解析】Opening WIP value 1,530+ Completion of opening WIP (200 ⋅ 0·60 ⋅ 20) 2,400+ Units started and finished in the month [(1,040 – 200) ⋅ 20] 16,800–––––––Total value of 1,040 completed units 20,73026.【答案】C27.【答案】B28.【答案】C29.【答案】D【解析】Fixed production overhead capacity variance:(Budgeted hours – Actual hours worked) ⋅ Standard fixed overhead rate =(8,000 – 8,400) ⋅ 9 = £3,600 Favourable30.【答案】C【解析】200 units ⋅ standard contribution per unit = [200 ⋅ (40 – 30)] = £2,000 (F)参与ACCA考试的考生可按照复习计划有效进行,另外高顿网校官网ACCA考试辅导高清课程已经开通,还可索取ACCA考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升复习备考效果。

武汉纺织大学会计学院

武汉纺织大学会计学院武汉纺织大学会计学院会计学院是我校历史最悠久的教学单位之一,自1982年招生以来,为国家培养了大批财经专业人才,为湖北地区的经济发展起到了促进作用.经过几十年的发展、积淀,形成了会计学科特有的文化氛围——诚信、求真、创新.会计学院现有教职工68人,其中专任教师有52人,教师比例76.4%,其中:教授5人,副教授27人,讲师19人;9人具有博士学位,31人具有硕士学位;;从年龄结构来看,40岁以上的占39%,39以下的占61%.教师所学专业均为会计、财务管理、审计、企业管理等相关专业,具有较为合理的学缘结构;具有中国注册会计师、中国注册税务师、中国注册资产评估师资格的双师型教师12人.教学与科研相结合的教师占教师总数的100%.会计学院现有财务管理、工程造价和会计学(含注册会计师)3个本科专业,在校生3000多人.____年新开设的acca实验班受到了广大考生的热烈欢迎,报考十分踊跃.学院现具备工商管理学科硕士学位授予资格.学院现设会计学系、财务管理系、cpa中心、工程造价研究中心、财务会计实验中心、企业并购研究所、会计信息质量研究所和大学生实践创新基地.“创品牌专业,争重点学科”是会计学院全体师生不断努力的方向.我院是较早开设注册会计师专业的高等财经院校之一,教学质量得到了广泛认同,____年我院在学校的支持下开设了“卓越cpa”班,引起了校内外的广泛关注.____年我院《财务会计》被评为湖北省本科品牌专业;《财务管理》和《会计信息系统》先后被评为省级本科精品课程.在____年举行的“第三届全国会计知识大赛”、____年举行的“首届会计科目大赛”、____年度举办的第六届“用友杯”全国大学生会计信息化技能大赛总决赛中本院代表队表现优异,为学校争得了荣誉.本院雄厚的师资力量和优秀的专业教学团队,为培养优秀的学生提供了可靠的保障.此外,多年来形成的良好院风学风,为我院学生的成长、成才提供了良好的软环境.我院积极开展助学工作,在学院帮助下,一大批学生获得了国家级、省级奖学金、国家助学金、国家助学贷款,减免特别困难学生的学费.奖、贷、助、补、减等多种助学方式的实施,为贫困生顺利完成学业提供了全方位的支持.会计学(注册会计师方向)注册会计师方向是研究审计、验资、资产评估、会计咨询等理论与方法的一门学科.本专业旨在培养学生全面掌握会计、审计及管理、经济、法律等方面的知识,灵活运用现代财务和会计科学管理技能,具备从事财务会计、审计工作所需的基本职业道德素质.突出强调专业理论与基本技能的实际应用.要求学生熟悉与cpa工作有关的会计、审计、财务、经济、管理、财政、金融、税收等方面的法律法规;了解国内外会计、审计的最新研究成果和发展动态,熟悉国际会计、审计惯例;具有良好的职业道德和社会责任感.计算机操作和应用能力达到国家二级以上的测试水平,能熟练运用各种会计电算化软件.主要就业领域会计师事务所、各类管理咨询公司、证券公司、银行、政府部门、企事业单位、教学及科研机构.本科四年,授予管理学学士学位.会计学专业(acca方向)acca是特许会计师公会(theassociationofcharteredcertifiedaccountants)的简称,成立于19____年,总部设在英国伦敦,是世界上最大的国际性专业会计师组织,目前在170多个国家和地区拥有40多万名学员和会员,全球设有350多个考点.acca 以培养国际性的高级会计、财务管理专家著称,其高质量的课程设计、高标准的考试要求、高水平的考试安排,赢得联合国和大量国际性组织的高度评价,更为众多的跨国公司和专业机构所推崇.大部分会员在政府机构、大型跨国企业、著名会计师事务所、咨询公司以及证券金融企业担当重要职务.acca中国区成立____年,目前拥有会员2800余人,学员____0多名,在北京、上海和广州等世界上30多个城市均设有办事处.acca通过在中国____年的发展,拥有完整的职业支持体系、就业支持体系、会员和学员服务体系,可为其成员进行终身服务.中国区acca会员,在职业生涯中取得令人瞩目的成就.会计学专业(acca方向)是融合现代化会计专业知识体系和职业教育内容,与国际接轨的创新型专业.学制四年.专业核心课程是acca考试的十四门课程,内容涵盖会计、财务、管理学、经济学、税务、审计等各方面,全部采用英文原版教材,中英文(双语)授课,所有同学必须参加acca全球同步考试.其余公共基础课、专业基础课按照学校会计专业本科教育的规定设置.会计学专业(acca方向)旨在培养具有acca执业资格,培养国际性、精英型、能够直接进入大型跨国公司与机构施展才华的高级会计与管理人才.acca与英国牛津布鲁克斯大学达成合作协议,凡通过acca课程前9门(f1-f9)考试的学生,并向该校提交一篇论文就有机会获得该大学的应用会计理学士学位.实现不出国门的留学.武汉纺织大学会计学专业(acca)方向学生可以获得:1、武汉纺织大学会计本科毕业证书和管理学学士学位(修完规定学分);2、acca执业资格证书(通过acca14门课程并有一定实践经历);3、获得英国牛津布鲁克斯大学应用会计理学学士学位机会;4、高标准的国际财务专业水平;5、娴熟的专业财务英语听说读写技能;三、acca合作办学模式武汉纺织大学会计专业(acca方向)采用与acca合作办学模式.该办班模式是本科教育与国际职业教育接轨、国内学历教育与国际学历教育结合的一种很好的模式,已得到国内其他大学的长期实践.四、会计学专业(acca方向)就业前景目前acca班毕业同学就业率为100%;有1/3进入全球四大会计师事务所(安永、毕马威、普华永道、德勤);acca专业同学首次入职的基础工资大多在4000-6000人民币之间.财务管理本专业系统学习经济、管理、计算机等学科的基本知识,通过高级财务管理学习,拓展学生的财务管理专业知识面,培养学生理财融资的能力;通过计算机相关课程的学习,突出财务信息化的运用能力,注重实践能力的培养.在掌握会计电算化的基础上,充分发挥管理者的能力,实现企业筹资,投资,分配活动的科学化,系统化,从而为企业带来良好的理财效益.主要就业领域在跨国公司、集团公司、银行、证券公司等企业单位以及事业单位和政府部门. 学制及学位本科四年,授予管理学学士学位.工程造价工程造价专业是学习如何在保证工程质量的前提下,对建设项目从立项决策到竣工投产的全过程进行造价确定、优化、控制、管理等工作,以求资源的最有效的利用,确保建设项目效益和参与各方的合法权益.本专业着重培养知识、能力、品格协调发展,通晓现代管理理论与方法,具备经济学、管理学和工程技术的基本知识,熟悉有关产业的经济政策和法规,掌握现代工程造价的基本理论和技能的高素质应用型复合人才.工程造价专业是依托学校工程背景与经济管理学科平台新设的一个专业.目前,能胜任工程造价专业课教学教师13人,其中教授3人,副教授6人,讲师4人.其中取得博士学位的教师5名,取得硕士学位的7人,具有注册造价师、注册会计师等专业资格的6人.已建成一支学历层次高、教学经验丰富,教学效果优异、老中青相结合的工程造价专业师资队伍.一批中青年教师在投资经济管理领域崭露头角,曾多次参加全国性工程造价学术研讨会.工程造价专业教师近年来共主持包括国家自然科学基金在内的有影响的纵横向项目15项,出版专著10余部,发表学术论文200余篇,其中部分专著、论文发表后,受到同行、专家的好评.就业前景学生毕业后能够在工程(造价)咨询公司、建筑施工企业(乙方)、建筑装潢装饰工程公司、工程建设监理公司、房地产开发企业、设计院、会计审计事务所、政府部门企事业单位基建部门(甲方)等企事业单位,从事工程造价招标代理、建设项目投融资和投资控制、工程造价确定与控制、投标报价决策、合同管理、工程预(结)决算、工程成本分析、工程咨询、工程监理等工作,也可在高等学校或科研机构从事相关专业的教学或科研工作.学制及学位本科四年,授予管理学学士学位.正文已结束,您可以按alt+4进行评论。

ACCA(F1-F3)学习方法总结

ACCA(F1-F3)学习方法总结ACCA共有16门课程,其中基础阶段主要分为知识课程和技能课程两个部分。

知识课程主要涉及财务会计和管理会计方面的核心知识,也为接下去进行技能阶段的详细学习搭建了一个平台。

F1-F3由于是ACCA全部课程体系内容中最为基础的三门课程,又作为财务会计体系中的入门课程,知识难度并不高,同时通过考试的压力也并不大。

F1:Accountant inBusiness(AB)F1这门课的内容很杂,主要涉及到以下三门主要学科:组织行为学,人力资源管理,会计和审计。

F1要求学生学习时一定要通看课本和老师讲义,而且应该做大量阅读,注意广度,以理解为主,不要对某方面知识死钻牛角尖。

F1的学习绝对不可猜题,复习时也绝对不可有遗漏或空白。

学习方法:1.完整学习网课内容,理解和记忆主要知识点,勤做笔记,完成练习,加深对知识点的认识和印象。

章节结束及时总结,清晰每章内容和关键知识点,完成讲义的自我梳理和配套的练习,熟悉每章的知识结构。

实战练习,熟悉考点,把握基本的答题规律2.对基础知识进行梳理,对知识点有整体把握。

根据冲刺串讲课程,复习精要知识点,复述相关概念。

整理第一阶段的错题,查漏补缺,加强薄弱环节。

3.罗列复习纲要,对知识点进行复述式记忆,发现薄弱知识点,进行答疑和重新梳理。

对所有错题所考查的知识点再次梳理,对不熟悉和遗漏的知识点多次记忆。

对样卷和ACCA官网模拟题进行仿真训练,严格控制考试时间,并自我认真审阅。

F2:Management Accounting(MA)F2主要向学员介绍成本会计和管理会计的体系,以及管理会计如何发挥支持企业计划、决策、控制的作用。

主要包括:管理会计起源、成本的分类、成本核算的方法、预算控制、差异分析、绩效评估相关知识点。

学习方法:1.报了网课或者面授的话,那么聆听老师的讲解是非常重要的。

对于老师发下来的讲义一定要认真研读,讲义往往是老师对于这门课的精炼总结,涵盖了所有的考点,仔细研究讲义可以专注于对高频考点的学习、提高学习效率,同时也能节省自己的时间和精力。

ACCA 历年真题f5_2012_jun_q