finance chapter 14

习题答案PrinciplesofCorporateFinance第十版Chapter14

习题答案PrinciplesofCorporateFinance第⼗版Chapter14 CHAPTER 14An Overview of Corporate Financing Answers to Problem Sets1. a. Falseb. Truec. True2. a. 40,000/.50 = 80,000 sharesb. 78,000 sharesc. 2,000 shares are held as Treasury stockd. 20,000 sharese. See table belowf. See table below3. a. 80 votesb. 10 X 80 = 800 votes.4. a. subordinatedb. floating ratec. convertibled. warrante. common stock; preferred stock.5. a. Falseb. Truec. False6. a. Par value is $0.05 per share, which is computed as follows:$443 million/8,863 million sharesb. The shares were sold at an average price of:[$443 million + $70,283 million]/8,863 million shares = $7.98c. The company has repurchased:8,863 million – 6,746 million = 2,117 million sharesd. Average repurchase price:$57,391 million/2,117 million shares = $27.11 per share.e. The value of the net common equity is:$443 million + $70,283 million + $44,148 million – $57,391 million= $57,483 million7. a. The day after the founding of Inbox:Common shares ($0.10 par value) $ 50,000Additional paid-in capital 1,950,000Retained earnings 0Treasury shares 0Net common equity $ 2,000,000b. After 2 years of operation:Common shares ($0.10 par value) $ 50,000Additional paid-in capital 1,950,000Retained earnings 120,000Treasury shares 0Net common equity $ 2,120,000c. After 3 years of operation:Common shares ($0.10 par value) $ 150,000 Additional paid-in capital 6,850,000Retained earnings 370,000Treasury shares 0Net common equity $ 7,370,0008. a.Common shares ($1.00 par value) $1,008Additional paid-in capital 5,444Retained earnings 16,250Treasury shares (14,015)Net common equity $8,687b.Common shares ($1.00 par value) $1,008Additional paid-in capital 5,444Retained earnings 16,250Treasury shares (14,715)Net common equity $7,9879. One would expect that the voting shares have a higher price because theyhave an added benefit/responsibility that has value.10. a.Gross profits $ 760,000Interest 100,000EBT $ 660,000Tax (at 35%) 231,000Funds available to common shareholders $ 429,000b.Gross profits (EBT) $ 760,000Tax (at 35%) 266,000Net income $ 494,000Preferred dividend 80,000Funds available to common shareholders $ 414,00011. Internet exercise; answers will vary.12. a. Less valuableb. More valuablec. More valuabled. Less valuable13. Answers may differ. Some key events of the financial crisis through the end of2008 include:June 2007: Bear Stearns pledges $3.2 billion to aid one of its ailing hedge funds Sept. 2007: Northern Rock receives emergency funding from the Bank of England Oct. 2007: Citigroup begins a string of writedowns based on mortgage losses Dec. 2007: Fed establishes Term Auction Facility linesJan. 2008: Ratings agencies threaten to downgrade Ambac and MBIA (major bond issuers)Feb. 2008: Economic stimulus package signed into lawMar. 2008: JPMorgan purchases Bear Stearns with support from the FedMar. 2008: SEC proposes ban on naked short sellingJuly 2008: FDIC takes over IndyMac BankSept. 2008: Lehman forced into bankruptcyB of A purchases Merrill Lynch10 banks create $70 billion liquidity fundAIG debt downgradedRMC money market fund “breaks the buck”Treasury bailout plan voted down in the HouseOct. 2008: 9 large banks agree to capital injection from TreasuryRevised bailout plan passes in HouseConsumer confidence hits lowest point on recordThe NY Fed has an excellent timeline of events at:/doc/24f5ef393968011ca30091d5.html /research/global_economy/Crisis_Timeline.pdf14. Answers will differ. Some purported causes of the financial crisis include:Long periods of very low interest rates leading to easy credit conditionsHigh leverage ratiosThe bursting of the US housing market bubbleHigh rates of default on subprime mortgagesMassive losses on investments in mortgage backed securitiesOpaque derivative markets and amplified losses through credit default swaps High rates of unemployment and job losses 15.a.For majority voting, you must own or otherwise control the votes of a simple majority of the shares outstanding, i.e., one-half of the shares outstanding plus one. Here, with 200,000 shares outstanding, you must control the votes of 100,001 shares. b.With cumulative voting, the directors are elected in order of the total number of votes each receives. With 200,000 shares outstanding and five directors to be elected, there will be a total of 1,000,000 votes cast. To ensure you can elect at least one director, you must ensure that someone else can elect at most four directors. That is, you must have enough votes so that, even if the others split their votes evenly among five other candidates, the number of votes your candidate gets would be higher by one.Let x be the number of votes controlled by you, so that others control (1,000,000 - x) votes. To elect one director:Solving, we find x = 166,666.8 votes, or 33,333.4 shares. Because there are no fractional shares, we need 33,334 shares.15x000,000,1x +-=。

F7-Chapter 14 Financial assets and liabilities

Examples

Financial asset Trade receivable Options Shares Financial liabilities Trade payables Debenture loans payable Redeemable preference(non-equity) shares Forward contracts standing at a loss

9

Hale Waihona Puke Equity instruments

• An equity instrument is defined as 'any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities'.

Equity instruments

Illustration

A company issues 100,000 $1 shares when the market price is $2.60 per share. Issue costs of $3,000 are incurred.

The shares are shown at their net proceeds in accordance with IAS 32 Financial Instruments: Presentation, i.e. any issue costs reduce the value recorded for the shares as follows:

Cash

斯坦利·B·布洛克-财务管理基础(第14版)chap008

– Deregulation has created greater competition among other financial institutions

8-2

Trade Credit

• Approximately 40 percent of short-term financing is in the form of accounts payable o trade credit

– Accounts payable

• Is a spontaneous source of funds • Grows as the business expands • Contracts when business declines

– Required account balance computed on the basis of:

• Percentage of customer loans outstanding • Percentage of bank commitments towards future

loans to a given account

8-6

Bank Credit

• Provide self-liquidating loans

– Use of funds ensures a built-in or automatic repayment scheme

• Changes in the banking sector today:

– Centered around the concept of ‘full service banking’

财金英语教程参考答案

财金英语教程参考答案Chapter 1: Introduction to Finance1. What is finance?- Finance is the management of money and includesactivities such as investing, borrowing, lending, budgeting, saving, and forecasting.2. What are the three main functions of finance?- The three main functions of finance are planning, acquiring, and managing financial resources.3. What is the time value of money?- The time value of money is the concept that a sum of money is worth more now than the same sum in the future dueto its potential earning capacity.4. How does inflation affect the value of money?- Inflation erodes the purchasing power of money over time, meaning that the same amount of money will buy fewer goodsand services in the future.5. What is the difference between a bond and a stock?- A bond is a debt instrument where an investor lends money to an entity in exchange for interest payments, while a stock represents ownership in a company and offers thepotential for capital gains and dividends.Chapter 2: Financial Statements1. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, cash flow statement, and statement of changes in equity.2. What is the purpose of a balance sheet?- The balance sheet provides a snapshot of a company's financial position at a specific point in time, showing its assets, liabilities, and equity.3. How is net income calculated?- Net income is calculated by subtracting all expensesfrom the total revenue of a company during a specific period.4. What does the cash flow statement show?- The cash flow statement shows the inflow and outflow of cash within a business over a period of time, categorizedinto operating, investing, and financing activities.5. What is the statement of changes in equity?- The statement of changes in equity shows the changes in the equity accounts of a company over a period of time, including retained earnings, capital contributions, and other comprehensive income.Chapter 3: Financial Analysis1. What are the main types of financial analysis?- The main types of financial analysis are ratio analysis,horizontal analysis, vertical analysis, and trend analysis.2. What is the purpose of ratio analysis?- Ratio analysis is used to evaluate a company's financial health by comparing various financial ratios such asliquidity, profitability, and leverage ratios.3. What is horizontal analysis?- Horizontal analysis involves comparing financial statement items over multiple periods to identify trends and changes in performance.4. What is vertical analysis?- Vertical analysis, also known as common-size analysis,is a method of financial statement analysis where each itemis expressed as a percentage of a base figure, typicallytotal assets or total revenue.5. What is trend analysis?- Trend analysis involves examining the historical data of financial metrics over time to predict future trends and performance.Chapter 4: Risk Management1. What is risk management?- Risk management is the process of identifying, assessing, and prioritizing potential risks to an investment or project, and taking steps to mitigate or avoid these risks.2. What are the types of risks in finance?- The types of risks in finance include market risk,credit risk, liquidity risk, operational risk, and legal risk.3. What is diversification?- Diversification is a risk management strategy that involves spreading investments across various financial instruments, industries, or geographic regions to reduce overall risk.4. What is hedging?- Hedging is a risk management technique used to reducethe risk of price fluctuations in an asset by taking an offsetting position in a related security.5. What is the role of insurance in risk management?- Insurance is a risk management tool that providesfinancial protection against potential losses or damages by transferring the risk to an insurance company in exchange for a premium.Chapter 5: Investment Strategies1. What are the different types of investment strategies?- Types of investment strategies include passive investing, active investing, value investing, growth investing, and income investing.2. What is the difference between passive and active investing?- Passive investing involves a "set it and forget it" approach, typically using index funds, while active investingrequires regular buying and selling of individual securities based on market research and analysis.3. What is value investing?- Value investing is an investment strategy that involves buying stocks that are considered undervalued by the market, with the expectation that their true value will eventually be recognized.4. What is growth investing?- Growth investing focuses on companies that are expected to grow at an above-average rate compared to the market, often investing in companies with strong competitive advantages and high growth potential.5. What is income investing?- Income investing is an investment strategy aimed at generating a steady stream of income from investments, typically through dividends or interest payments.Chapter 6: International Finance1. What is international。

F4-chapter 14

ACCAInstructor: GabrielleChapter 14loan capital•Define companies ' borrowing powers .•Explain the meaning of loan capital and debenture .•Distinguish loan capital from share capital ,and explain the different rights held by shareholders and debenture holders .•Explain the concept of a company charge and distinguish between fixed and floating charges .Chapter 14 loan capital Chapter GuideLoan capitalDebentures ChargesFixed v Floating Registration ReceiversDefine Debentures v SharesChapter 14 loan capital OverviewChapter 14 loan capital1.Define companies' borrowing powers •The power to borrow money is usually expressly stated inthe company’s constitution, where this is not the case it can usually be implied from the trading activities of the company.•2.1 Debentures are a form of loan capital a company can use to raise finance. In strict legal term they are known as‘a written acknowledgement of indebtedness’.•Debentures may be issued in a number of ways: •(a) Single debentures–issued to a single provider, this document sets out the terms of the loan•(b) Debentures issued in series–the loan is raised from several providers, each ranking equally (paripassu)•(c) Debenture stock–finance is raised from thepublic, each owning a proportion of the debt via acertificate, in much the same way as owning shares.The details of the overall loan are set out in aFeature SharesDebentures Status Member Creditor VotingMay vote May not vote Returns Dividends Interest Issued No discount Discounted/par Redemption Restrictions No restrictions Security None Fixed/Floating Liquidation Rank lastRank firstChapter 14 loan capital3. Distinguish loan capital from share capital,andexplain the different rights held by shareholders and debentu holdersLoan CapitalLoan Capital DebenturesDebentures Charges Charges FixedFixed FloatingFloating Chapter 14 loan capital4. Explain the concept of a company charge and distinguish between fixed and floating charges•As noted above a key distinction of debentures is the ability to secure the investment via charges . Security means , that in the event of a company being wound up , the creditor with a secured debt will receive a priority as regards payment over unsecured creditors and shareholders . There are two types of charges available to debenture holders .Chapter 14 loan capital4. Explain the concept of a company charge and distinguish between fixed and floating charges4.1 Fixed charges have the following properties : a )They attach to specific assets upon creation (subject to registration )b )The charged asset may not be disposed of by the companyc )Default on the loan by the company enables the charge holder to sell the asset and recover monies owedd )Upon liquidation fixed charge holders rank firstChapter 14 loan capital4. Explain the concept of a company charge and distinguish between fixed and floating chargesdistinguish between fixed and floating charges4.2 Floating charges have the following properties:a)They do not attach to specific assets upon creation, merely‘hovering’over classes of assetsb)Upon a‘crystallising event’the charge attaches itself to the remaining assets within the charged class c)The company is free to deal in charged assets up to the point of crystallisationd)Upon liquidation the floating charge holders’rank behind fixed charge holders, the liquidator, and otherdistinguish between fixed and floating charges•4.3Any amounts of monies owed to any charge holders not settled by the sale of charged assets become unsecured. Without court approval the Fixed charge holders may appoint a Receiver to take control of the charged asset. Floating charge holders may appoint an administrative receiver in the event of a crystallising event, but whose powers are limited by the Enterprise Act 2003.•5.1 Charges must be registered with the Registrar within 21 days of their creation ; else they become void , rendering the debt unsecured . Assuming this deadline is met , the charges become effective from date of creation – not registration . Charges that are delivered late will only beregistered to the extent that they do not prejudice the rights of other charge holders .Chapter 14 loan capital5. Describe the need and procedure for registering company charges .company charges.•5.2 The strict priority of charges is that fixed charges always rank above floating charges. For example a fixed charge created and registered on a factory in May, would rank before a floating charge created and registered over‘all of the companies assets’in January of the same year.company charges.•5.3 Should a floating charge holder wish to prevent themselves being overtaken by a subsequent fixed charge over the same asset then they can create a Negative Pledge Clause (NPC). As long as the creditor has provided some form of additional consideration, and all subsequent charge holders are informed of the presence of the NPC, it cannot be overtaken by subsequent fixed charges granted over the asset(s).The following charged debentures were issued by a company against overlapping asset(s):1st Mar–fixed charge debenture to A, registered on 14th Mar12th Mar–floating charge debenture to B, registered on 16th Mar24th Mar–floating charge with Negative Pledge Clause to C, registered on 31st Mar28th Mar–fixed charge to X, registered on 31st Mar•RequiredWhat is the order in which these debentures will be repaid assuming the company goes into liquidation?•A floating charge is created on 1 March 200X , and crystallises on 1 October 200X . A fixed charge over the same property is created on 1 September 200X . Assuming both are registered within the prescribed time limits which ranks first ?•A The fixed charge•B The floating charge•C On crystallisation of the floating charge to a fixed charge , both rank pari passu•D The floating charge becomes a fixed charge on Chapter 14 loan capitalLecture example 2Section Topic Summary1Debentures A debenture is a written acknowledgement ofdebt issued by a company in order to raise finance.Debentures may be issued singly, in series, or asdebenture stock. Debentures differ from sharesin the classification of the investors, returns,they can be issued at a discount, can besecured, and they rank higher on liquidation.Section Topic Summary2Charges Charges may be fixed or floating. Fixed charges are a lotmore secure as they attach to assets that cannot bedisposed off, and rank higher on liquidation. Floatingcharges only attach to assets upon a crystallising event.Fixed charges always rank above floating charges, unlessan NPC is created. This is subject to the charge beingsubmitted to the Registrar within 21 days of creation.Late registration will be allowed, but not to the detriment ofcorrectly registered charges.Slide 61You should now be able to attempt the following key questions from the Golden Global Learning Media Practice and Revision Kit.You should now be able to attempt the following key questions from the Golden Global Learning Media Practice and Revision Kit.Chapter 14 loan capitalQuestion practice – end of Chapter。

Week

UK and US Survey Week 4 Chapter 14 Events before the end of WWIIUK history from 1199❝1199 -John became the King of England. John angered the King of France and the French decided to fight for land in Normandy that the English aristocracy owned. This made the aristocracy mad at King John and they started fighting against him.❝Such kinds of rebellions were not unusual. Every king had faced rebellions. What was unusual about this rebellion was that John had no replacement, no son to take over. So the aristocracy decided that his form of ruling had to change and the Magna Carta was written.❝In 1215 the Magna Carta was signed by King John. It became the first document forced onto a King of England by a group of his subjects (aristocracy) to limit his powers by law and protect their privileges.❝Three clauses remain part of the law of England and it is considered part of the constitution today. It is described as "the greatest constitutional document of all times –the foundation of the freedom of the individual against the authority of the despot”.The Magna Carta was also important in the colonization of America. England's legal system was used as an example for many of the colonies as they were developing their own legal systems.The 100-Years’ War 1337 -1453❝The Hundred Y ears' War was fought between the Kingdom of England and the Kingdom of France for control of the French throne.❝As the owner of land in France, the English king owed tribute to the king of France. In 1337, Edward III of England refused to pay homage to Philip VI of France. So the French king took back Edward's lands in Aquitaine, France.Edward responded by declaring that he, not Philip, was the rightful king of France because his mother was from French royalty. However, at that time the right to be king could not come from female heritage, it had to come from the male heritage.Edward of England kneeling toPhilip IV of FranceWar of the Roses –1455 (2 years later)❝The War of the Roses were a series of wars fought between two rivals, the houses of Lancaster and Y ork, whose symbols were the red and the white rose, for the throne of England. They were fought in several separate wars between 1455 and 1485.❝They resulted from the social and financial troubles following the Hundred Y ears' War. The final victory went to a Lancastrian, Henry T udor. The House of T udor ruled England and Wales for 117 years.House of Y ork –white rose House of Lancaster –red roseThe Industrial Revolution 1760 -1820❝The Industrial Revolution started a change to new manufacturing processes. This change included going from hand production methods to machines, improved efficiency of water power, the increasing use of steam power and development of machine tools.❝The transition also included the change from wood to coal. The Industrial revolution began in Britain and within a few decades spread to Western Europe and the United States.❝The Industrial Revolution began a time of economic growth in capitalist economies.❝Economic historians agree that the Industrial Revolution is the most important event in the history of humanity since the domestication of animals and plants.Major technological developments❝T extiles –Cotton spinning machines powered by steam or water increased the output of a worker by about 1000 times.❝The power loom increased the output of a worker by over 40 times.❝The cotton gin increased the ability to remove seeds from cotton by 50 times.❝Steam power –The efficiency of steam engines increased so that they used between one-fifth and one-tenth as much fuel.Iron making –The substitution of coke for charcoal greatly lowered the fuel cost to make iron. Using coke also allowed larger furnaces which resulted in economies of scale.US War of Independence 1775-1783❝The thirteen colonies in North America joined together to break from the British Empire and combined to become the United States of America.❝Claiming the rule of Great Britain was illegal, Congress declared independence as a new nation in July 1776. Thomas Jefferson wrote and the states unanimously signed the Declaration of Independence.❝Americans rejected the aristocracy of England and chose instead the development of republicanism.❝The result of the revolution was the creation of a democratically-elected government responsible to the will of the people.❝However, it took until 1783 for the British to claim defeat and give the country to the Americans.War of 1812 -1815❝The United States declared war in 1812 for several reasons, including trade restrictions brought about by Britain's war with France that forced American sailors into the English Navy.❝The British also supported American Indians against American expansion, providing them with guns so they could fight against the expansion into their territory.❝This was the last war between England and the United States and settled the independence of the US.❝During this war the “Star Spangled Banner was written.American Civil War 1861 -1865❝The American Civil War was fought between the “Union” or the "North" and several Southern slave states that had declared their secession and formed the Confederate State of America (or the "South").❝Slavery was only one of many issuesfor the war, and after four years of bloody combat (mostly in the South), the Confederacy was defeated, andslavery was abolished.Not all Southerners saw themselves as fighting to keep slavery, but most of the officers in the Confederate army had close family ties to slavery. T o many Northerners the war was primarily to preserve the Union, not to abolish slavery.World War I 1914 -1918❝WWI started with two opposing groups. The Allies were made up of the UK, France and Russia. The Central Powers included Germany, Austria-Hungary and Italy.❝As the war continued more countries joined, including the US, Japan, China, India.❝On 28 July, 1914 Austria-Hungary fired the first shots of the war as preparation for the invasion of Serbia, which was supported by Russia. While the Russians got troops together, the Germans invaded Belgium and Luxembourg on their way to France. This gave Britain a reason to declare war against Germany.❝Soon the conflict spread around the world.Map of the participants of World War I; the Allied Powers in green, and the Central Powers in orange. The neutral countries are in grey.The Great Depression 1929 -1933❝The Great Depression was a severe worldwide economic depression . The start of the Great Depression varied across countries, but in most countries it started in 1930 and lasted until the late 1930s or middle 1940s.It was the longest, most widespread, and deepest depression of the 20th century.❝The depression originated in the U.S., after the fall in stock prices that began around September 4, 1929, and became worldwide news with the stock market crash of October 29, 1929 (known as Black T uesday).❝The Great Depression had devastating effects in countries all over the world.❝Change in economic indicators 1929–32US Great Britain France Germany ❝Industrial production –46% –23% –24% –41%❝Wholesale prices –32% –33% –34% –29%❝Foreign trade –70% –60% –54% –61%❝Unemployment +607% +129% +214% +232%❝T o bring the US out of the Depression, President Franklin Roosevelt began the “New Deal” program.❝His program included reforms in banking, farm programs to help farmers, and public works programs, the PWA, Public Works Administration.❝Under the public works programs new hospitals, schools, roads, bridges and dams were built. Unemployed persons were hired as workers on these programs.World War II 1939 -1945❝WWII involved the majority of the countries in the world, including all of the great powers. These formed two opposing military alliances: the Allies and the Axis.❝WWII resulted in between 50 million and 75 million deaths. These deaths make it the deadliest conflict in human history.Japan was already at war with China in 1937,but the world war is generally said to have begun on September 1, 1939 with the invasion of Poland by Germany.Japan also chose to attack the US, bombing the military air base at Pearl Harbor, Hawaii in 1941. This brought the US into the war.❝July, 1945 the Potsdam conference was held and Germany surrendered. The Japanese ignored the terms of the agreement until the US dropped atomic bombs on Nagasaki and Hiroshima. They surrendered in August, 1945.❝In an effort to maintain peace,the Allies formed the United Nations, which officially came into existence on October 24,1945.Homework for Next Week❝Chapter 15 discusses the UK and the US from the end of WWII to present days.❝Group A –read pages 208 –215 (7 pages)❝Group B –read pages 215 –219 (4 pages)❝Be prepared to share with your classmates.Vocabulary for Next Week1)Capitalism—an economic system in which investment in andownership of the means of production, distribution, andexchange of wealth is made and maintained chiefly by private individuals or corporations, especially as contrasted tocooperatively or state-owned means of wealth2)Deficit finance—expenditures in excess of public revenues,made possible typically by borrowing3)Integration—an act or instance of combining into an integralwhole4)Hegemony—leadership or predominant influence exercisedby one nation over others, as in a confederation5)Imperialism—the policy of extending the rule or authorityof an empire or nation over foreign countries, or ofacquiring and holding colonies and dependencies6)Arms race—competition between countries to achievesuperiority in quantity and quality of military arms (weapons) 7)Sovereignty—supreme and independent power or authorityin government as possessed or claimed by a state orcommunity8)Infrastructure—the fundamental facilities and systemsserving a country, city, or area, as transportation andcommunication systems, power plants, and schools9)Welfare—financial or other assistance to an individual orfamily from a city, state, or national government10)Nationalization—the act of being brought under theownership or control of a nation, as industries and land 11)Privatization—the act of transferring from public orgovernment control or ownership to private enterprise or ownership12)Mitigate—lessen in force or intensity, as wrath, grief,harshness, or pain; moderate。

what is project finance

16

2.1 Why Project Finance?

Project Owners’ Perspective

Size and cost of projects Risk minimization Preservation of borrowing capacity and credit rating May be the only way that enough funds can be raised

International Project Finance

Chapter 1 What is Project Finance

2

Focus of this chapter

1.

2.

3. 4.

5.

The differences between conventional company finance and Project Finance. The advantages and disadvantages of Project Finance. The features of Project Finance. The participants in Project Finance and the part they play. The key risks in Project Finance.

1.3 What is Project Finance?

Project Finance involves a corporate sponsor investing in and owning a single purpose, industrial asset through a legally independent entity financed with non-recourse debt. Project financing refers to a financing in which lenders to a project look primarily to the cash flow and assets of that project as the source of payment of their loans. See paragraph 2 and 3 on page 3.

Chapter_14 Investment Spending多恩布什宏观经济学(教学课件)PPT

Flow of investment is quite small compared to the stock of capital.

• Capital wears out over time must include depreciation, d • The complete formula for the rental cost of capital is:

The complete formula for trhe rcer nt ald co stio f cae pi tald is

of capital

• Diminishing marginal product of capital means that each successive unit of capital yields less than the previous unit Figure 14-2

• An increase in the rental cost of capital can only be justified by an increase in the marginal product of capital, and a lower level of K

14-4

The Desired Capital Stock

• Firms use capital, along with labor and other resources, to produce output The goal of a given firm is to maximize profits

罗斯公司理财题库全集

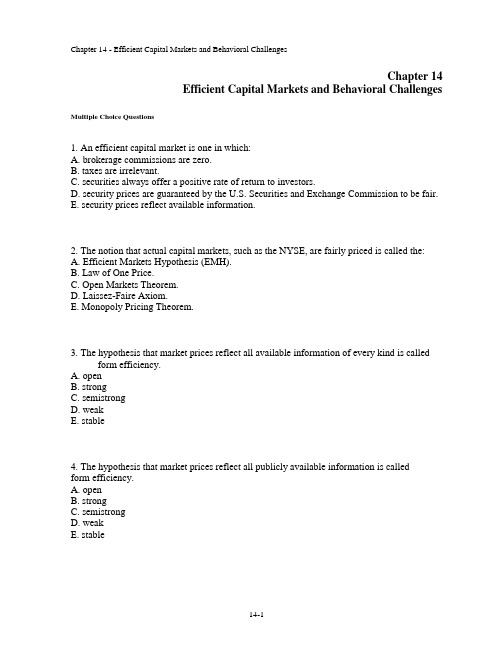

Chapter 14Efficient Capital Markets and Behavioral Challenges Multiple Choice Questions1. An efficient capital market is one in which:A. brokerage commissions are zero.B. taxes are irrelevant.C. securities always offer a positive rate of return to investors.D. security prices are guaranteed by the U.S. Securities and Exchange Commission to be fair.E. security prices reflect available information.2. The notion that actual capital markets, such as the NYSE, are fairly priced is called the:A. Efficient Markets Hypothesis (EMH).B. Law of One Price.C. Open Markets Theorem.D. Laissez-Faire Axiom.E. Monopoly Pricing Theorem.3. The hypothesis that market prices reflect all available information of every kind is called_____ form efficiency.A. openB. strongC. semistrongD. weakE. stable4. The hypothesis that market prices reflect all publicly available information is called _____ form efficiency.A. openB. strongC. semistrongD. weakE. stable5. The hypothesis that market prices reflect all historical information is called _____ form efficiency.A. openB. strongC. semistrongD. weakE. stable6. In an efficient market, the price of a security will:A. always rise immediately upon the release of new information with no further price adjustments related to that information.B. react to new information over a two-day period after which time no further price adjustments related to that information will occur.C. rise sharply when new information is first released and then decline to a new stable level by the following day.D. react immediately to new information with no further price adjustments related to that information.E. be slow to react for the first few hours after new information is released allowing time for that information to be reviewed and analyzed.7. If the financial markets are efficient, then investors should expect their investments in those markets to:A. earn extraordinary returns on a routine basis.B. generally have positive net present values.C. generally have zero net present values.D. produce arbitrage opportunities on a routine basis.E. produce negative returns on a routine basis.8. Which one of the following statements is correct concerning market efficiency?A. Real asset markets are more efficient than financial markets.B. If a market is efficient, arbitrage opportunities should be common.C. In an efficient market, some market participants will have an advantage over others.D. A firm will generally receive a fair price when it sells shares of stock.E. New information will gradually be reflected in a stock's price to avoid any sudden change in the price of the stock.9. According to the efficient market hypothesis, financial markets fluctuate daily because they:A. are inefficient.B. slowly react to new information.C. are continually reacting to new information.D. offer tremendous arbitrage opportunities.E. only reflect historical information.10. Insider trading does not offer any advantages if the financial markets are:A. weak form efficient.B. semiweak form efficient.C. semistrong form efficient.D. strong form efficient.E. inefficient.11. According to theory, studying historical prices in order to identify mispriced stocks will not work in markets that are _____ efficient.I. weak formII. semistrong formIII. strong formA. I onlyB. II onlyC. I and II onlyD. II and III onlyE. I, II, and III12. Which of the following tend to reinforce the argument that the financial markets are efficient?I. Information spreads rapidly in today's world.II. There is tremendous competition in the financial markets.III. Market prices continually fluctuate.IV. Market prices react suddenly to unexpected news announcements.A. I and III onlyB. II and IV onlyC. I, II, and III onlyD. II, III, and IV onlyE. I, II, III, and IV13. If you excel in analyzing the future outlook of firms, you would prefer that the financial markets be ____ form efficient so that you can have an advantage in the marketplace.A. weakB. semiweakC. semistrongD. strongE. perfect14. Your best friend works in the finance office of the Delta Corporation. You are aware that this friend trades Delta stock based on information he overhears in the office. You know that this information is not known to the general public. Your friend continually brags to you about the profits he earns trading Delta stock. Based on this information, you would tend to argue that the financial markets are at best _____ form efficient.A. weakB. semiweakC. semistrongD. strongE. perfect15. The U.S. Securities and Exchange Commission periodically charges individuals for insider trading and claims those individuals have made unfair profits. Based on this fact, you would tend to argue that the financial markets are at best _____ form efficient.A. weakB. semiweakC. semistrongD. strongE. perfect16. Individuals that continually monitor the financial markets seeking mispriced securities:A. tend to make substantial profits on a daily basis.B. tend to make the markets more efficient.C. are never able to find a security that is temporarily mispriced.D. are always quite successful using only well-known public information as their basis of evaluation.E. are always quite successful using only historical price information as their basis of evaluation.17. Efficient capital markets are financial markets:A. in which current market prices reflect available information.B. in which current market prices reflect the present value of securities.C. in which there is no excess profit from using available information.D. All of the above.E. None of the above.18. If the efficient market hypothesis holds, investors should expect:A. to earn only a normal return.B. to receive a fair price for their securities.C. to always be able to pick stocks that will outperform the market averages.D. Both A and B.E. Both B and C.19. Financial managers can create value through financing decisions that:A. reduce costs or increase subsidies.B. increase the product prices.C. create a new security.D. Both A and B.E. Both A and C.20. In an efficient market when a firm makes an announcement of a new product or product enhancement with superior technology providing positive NPV, the price of the stock will:A. rise gradually over the next few days.B. decline gradually over the next few days.C. rise on the same day to the new price.D. stay at the same price, with no net effect.E. drop on the same day to the new price.21. An investor discovers that for a certain group of stocks, large positive price changes are always followed by large negative price changes. This finding is a violation of the:A. moderate form of the efficient market hypothesis.B. semistrong form of the efficient market hypothesis.C. strong form of the efficient market hypothesis.D. weak form of the efficient market hypothesis.E. None of the above.22. Which of the following would be indicative of inefficient markets?A. Overreaction and reversionB. Delayed responseC. Immediate and accurate responseD. Both A and B.E. Both A and C.23. When the stock price follows a random walk, the price today is said to be equal to the prior period price plus the expected return for the period with any remaining difference to the actual return due to:A. a predictable amount based on the past prices.B. a component based on new information unrelated to past prices.C. the security's risk.D. the risk free rate.E. None of the above.24. Which form of the efficient market hypothesis implies that security prices reflect only information contained in past prices?A. Weak formB. Semistrong formC. Strong formD. Hard formE. Past form25. If the weak form of efficient markets holds, then:A. technical analysis is useless.B. stock prices reflect all information contained in past prices.C. stock prices follow a random walk.D. All of the above.E. None of the above.26. Under the concept of an efficient market, a random walk in stock prices means that:A. there is no driving force behind price changes.B. technical analysts can predict future price movements to earn excess returns.C. the unexplained portion of price change in one period is unrelated to the unexplained portion of price change in any other period.D. the unexplained portion of price change in one period that can not be explained by expected return can only be explained by the unexplained portion of price change in a prior period.E. None of the above.27. A semistrong form efficient market is distinct from a weak form efficient market by:A. incorporating only random movements in the price.B. incorporating all publicly available information in the price.C. incorporating inside information in the price.D. All of the above.E. None of the above.28. If a market is strong form efficient, it also implies that:A. semistrong form efficiency holds.B. weak form efficiency holds.C. one cannot earn abnormal returns with inside information.D. Both A and C.E. A, B and C.29. An investor discovers that predictions about weather patterns published years in advance and found in the Farmer's Almanac are amazingly accurate. In fact, these predictions enable the investor to predict the health of the farm economy and therefore certain security prices. This finding is a violation of the:A. moderate form of the efficient market hypothesis.B. semistrong form of the efficient market hypothesis.C. strong form of the efficient market hypothesis.D. weak form of the efficient market hypothesis.E. None of the above.30. A lawyer works for a firm that advises corporate firms planning to sue other corporations for antitrust damages. He finds that he can "beat the market" by short-selling the stock of the firm that will be sued. This finding is a violation of the:A. moderate form of the efficient market hypothesis.B. semistrong form of the efficient market hypothesis.C. strong form of the efficient market hypothesis.D. weak form of the efficient market hypothesis.E. None of the above.31. An investor discovers that stock prices change drastically as a result of certain events. This finding is a violation of the:A. moderate form of the efficient market hypothesis.B. semistrong form of the efficient market hypothesis.C. strong form of the efficient market hypothesis.D. weak form of the efficient market hypothesis.E. None of the above.32. The semistrong form of the efficient market hypothesis states that:A. all information is reflected in the price of securities.B. security prices reflect all publicly available information.C. future prices are predictable.D. Both A and C.E. None of the above.33. The market price of a stock moves or fluctuates daily. This fluctuation is:A. inconsistent with the semistrong efficient market hypothesis because prices should be stable.B. inconsistent with the weak form efficient market hypothesis because all past information should be priced in.C. consistent with the semistrong form of the efficient market hypothesis because as new information arrives daily prices will adjust to it.D. consistent with the strong form because prices are controlled by insiders.E. None of the above.34. An investor who picks a portfolio by throwing darts at the financial pages:A. believes that efficient markets will protect the portfolio from harm as all information is priced.B. believes that riskier portfolios earn the same as less risky portfolios.C. does so because stock prices do not matter; only cash flow generated matters.D. Both A and C.E. Both B and C.35. Suppose that firms with unexpectedly high earnings earn abnormally high returns for several months after the announcement. This would be evidence of:A. efficient markets in the weak form.B. inefficient markets in the weak form.C. efficient markets in the semistrong form.D. inefficient markets in the semistrong form.E. inefficient markets in the strong form.36. Which of the following is not true about serial correlation?A. It measures the correlation between the current return on a security and the current return on another security.B. It involves only one security.C. Positive serial correlation indicates a tendency for continuation.D. Negative serial correlation indicates a tendency toward reversal.E. Significant positive or negative serial correlation coefficients are indicative of market inefficiency in the weak form.37. Which of the following is true?A. A random walk for stock price changes is inconsistent with observed patterns in price changes.B. If the stock market follows a random walk, price changes should be highly correlated.C. If the stock market is weak form efficient, then stock prices follow a random walk.D. All of the above.E. Both B and C.38. Event studies attempt to measure:A. the influence of information released to the market on returns in days surrounding its announcement.B. if the market is at least semistrong form efficient.C. whether there is a significant reaction to public announcements.D. All of the above.E. None of the above.39. The abnormal return in an event study is described as:A. the return earned on the day of announcement for the stock.B. the excess return earned on the day of announcement for the stock.C. the total return earned for the investment holding period.D. All of the above.E. None of the above.40. Evidence on stock prices finds that the sudden death of a chief executive officer causes stock prices to fall and the sudden death of an active founding chief executive officer causes stock price to rise. This contrary evidence happens because:A. markets are inefficient and unsure of the real value of the events.B. death is inevitable and market prices are random.C. things simply happen.D. the value of the founding executive was a negative to the firm.E. None of the above.41. Studies of the performance of professionally managed mutual funds find that these funds:A. do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semistrong form of the efficient market hypothesis.B. do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semistrong form of the efficient market hypothesis.C. outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semistrong form of the efficient market hypothesis.D. outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semistrong form of the efficient market hypothesis.E. Both C and D.42. Which of the following statements is true?A. In efficient markets, a stock's price should change with the arrival of new information.B. Average stock returns are higher in January than other months.C. Studies by Fama and French and others find that returns of high book to market stocks are much higher than low book to market value stocks to be consistent with the efficient market hypothesis.D. All of the above.E. None of the above.43. Which of the following is true?A. Most empirical evidence is consistent with strong form efficiency.B. Most empirical evidence is inconsistent with weak form efficiency.C. Strong form market efficiency is not supported by the empirical evidence.D. Both A and C.E. Both B and C.44. In examining the issue of whether the choice of accounting methods affects stock prices, studies have found that:A. accounting depreciation methods can significantly affect stock prices.B. switching depreciation methods can significantly affect stock prices.C. accounting changes that increase accounting earnings also increases stock prices.D. accounting changes can affect stock prices if the company were either to withhold information or provide incorrect information.E. All of the above.45. Market efficiency says:A. prices may not reflect underlying value.B. a good financial manager can time stock sales.C. managers may profitablly speculate in foreign currency.D. managers cannot boost stock prices through creative accounting.E. None of the above.46. The abnormal returns for initial public offerings over longer time periods seem to call market efficiency into question because:A. the average returns at announcement are large and positive while the long-term results are much lower than the returns for seasoned equity offerings.B. the average returns at announcement are small and negative while the long-term results are much lower than the returns for seasoned equity offerings.C. the average returns at announcement are zero while the long-term results are much higher than the returns for seasoned equity offerings.D. the average returns at announcement are large and positive while the long-term results are much higher than the returns for seasoned equity offerings.E. the average returns at announcement are insignificant while the long-term results are much lower than the returns for seasoned equity offerings.47. An example of financially irrational behavior is:A. gambling in Las Vegas.B. when a firm announces an increase in earnings and the stock price enjoys three days of large abnormal returns.C. when a firm announces an increase in earnings and the stock price enjoys an immediate surge in value which is captured in one day.D. Both A and B.E. Both A and C.48. Ritter's study of Initial Public Offerings (IPOs) showed that the post offering stock performance was:A. less than the control group by about 2% in the five years following the IPO.B. incorrectly priced at issuance because over the next five years the abnormal returns were greater than zero on average.C. immaterial to the pricing of the IPO because future market performance is unknown at issuance.D. equal across IPOs, irrespective of risk or which year they were issued.E. All of the above.49. If the securities market is efficient, an investor need only throw darts at the stock pages to pick securities and be just as well off.A. This is true because there are no differences in risk and return.B. This is true because in an efficient stock market prices do not fluctuate.C. This is false because professional portfolio managers prefer to generate commissions by active trading.D. This is false because investors may not hold a desirable risk-return combination in their portfolio.E. This is false because the markets are controlled by the institutional investors.50. Financial managers must be cognizant of market efficiency because:A. manipulating earnings by accounting changes does not fool the market.B. timing security sales is futile because without private information the current price reflects all known information.C. there is limited price pressure from any large sale of stock depressing prices only momentarily before recovering to prior levels.D. All of the above.E. None of the above.51. Event studies have been used to examine:A. IPOs, SEOs, and other equity issuances.B. changes in earnings.C. mergers and acquisitions.D. most financial events.E. All of the above.52. If the market is weak form efficient:A. semistrong form efficiency holds.B. strong form efficiency must hold.C. semistrong form efficiency may hold.D. markets are not weak form efficient.E. None of the above.53. In order to create value from capital budgeting decisions, the firm is likely to:A. locate an unsatisfied demand for a particular product or service.B. create a barrier to make it more difficult for other firms to compete.C. produce products or services at a lower cost than the competition.D. A and C.E. A, B, and C.54. Valuable financing opportunities can be created by:A. fooling investors.B. reducing costs or increasing subsidies.C. the creation of a new security.D. A and B.E. A, B, and C.55. The following time period(s) is/are consistent with the bubble theory:A. the stock market crash of 1929.B. the stock market crash of 1972.C. the stock market crash of 1987.D. A and C.E. A, B, and C.56. In the five years after the offering, ___ underperform matched control groups.A. initial public offeringsB. seasoned equity offeringsC. bond offeringsD. A and BE. A, B, and C57. In the three years prior to a forced departure of management, stock prices, adjusted for market performance, on average will:A. decline about 20%.B. decline about 40%.C. decline about 60%.D. remain stable.E. increase about 20%.Essay Questions58. Define the three forms of market efficiency.59. Explain why it is that in an efficient market, investments have an expected NPV of zero.60. Do you think the lessons from capital market history will hold for each year in the future? That is, as an example, if you buy small stocks will your investment always outperformU.S. Treasury bonds?61. Suppose your cousin invests in the stock market and doubles her money in a single year while the market, on average, earned a return of only about 15%. Is your cousin's performance a violation of market efficiency?62. Why should a financial decision maker such as a corporate treasurer or CFO be concerned with market efficiency?Chapter 14 Efficient Capital Markets and Behavioral Challenges Answer KeyMultiple Choice Questions1. An efficient capital market is one in which:A. brokerage commissions are zero.B. taxes are irrelevant.C. securities always offer a positive rate of return to investors.D. security prices are guaranteed by the U.S. Securities and Exchange Commission to be fair.E. security prices reflect available information.Difficulty level: EasyTopic: EFFICIENT CAPITAL MARKETType: DEFINITIONS2. The notion that actual capital markets, such as the NYSE, are fairly priced is called the:A. Efficient Markets Hypothesis (EMH).B. Law of One Price.C. Open Markets Theorem.D. Laissez-Faire Axiom.E. Monopoly Pricing Theorem.Difficulty level: EasyTopic: EFFICIENT MARKETS HYPOTHESISType: DEFINITIONS3. The hypothesis that market prices reflect all available information of every kind is called _____ form efficiency.A. openB. strongC. semistrongD. weakE. stableDifficulty level: EasyTopic: STRONG FORM EFFICIENCYType: DEFINITIONS4. The hypothesis that market prices reflect all publicly available information is called _____ form efficiency.A. openB. strongC. semistrongD. weakE. stableDifficulty level: EasyTopic: SEMI STRONG FORM EFFICIENCYType: DEFINITIONS5. The hypothesis that market prices reflect all historical information is called _____ form efficiency.A. openB. strongC. semistrongD. weakE. stableDifficulty level: EasyTopic: WEAK FORM EFFICIENCYType: DEFINITIONS6. In an efficient market, the price of a security will:A. always rise immediately upon the release of new information with no further price adjustments related to that information.B. react to new information over a two-day period after which time no further price adjustments related to that information will occur.C. rise sharply when new information is first released and then decline to a new stable level by the following day.D. react immediately to new information with no further price adjustments related to that information.E. be slow to react for the first few hours after new information is released allowing time for that information to be reviewed and analyzed.Difficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS7. If the financial markets are efficient, then investors should expect their investments in those markets to:A. earn extraordinary returns on a routine basis.B. generally have positive net present values.C. generally have zero net present values.D. produce arbitrage opportunities on a routine basis.E. produce negative returns on a routine basis.Difficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS8. Which one of the following statements is correct concerning market efficiency?A. Real asset markets are more efficient than financial markets.B. If a market is efficient, arbitrage opportunities should be common.C. In an efficient market, some market participants will have an advantage over others.D. A firm will generally receive a fair price when it sells shares of stock.E. New information will gradually be reflected in a stock's price to avoid any sudden change in the price of the stock.Difficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS9. According to the efficient market hypothesis, financial markets fluctuate daily because they:A. are inefficient.B. slowly react to new information.C. are continually reacting to new information.D. offer tremendous arbitrage opportunities.E. only reflect historical information.Difficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS10. Insider trading does not offer any advantages if the financial markets are:A. weak form efficient.B. semiweak form efficient.C. semistrong form efficient.D. strong form efficient.E. inefficient.Difficulty level: EasyTopic: MARKET EFFICIENCYType: CONCEPTS11. According to theory, studying historical prices in order to identify mispriced stocks will not work in markets that are _____ efficient.I. weak formII. semistrong formIII. strong formA. I onlyB. II onlyC. I and II onlyD. II and III onlyE. I, II, and IIIDifficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS12. Which of the following tend to reinforce the argument that the financial markets are efficient?I. Information spreads rapidly in today's world.II. There is tremendous competition in the financial markets.III. Market prices continually fluctuate.IV. Market prices react suddenly to unexpected news announcements.A. I and III onlyB. II and IV onlyC. I, II, and III onlyD. II, III, and IV onlyE. I, II, III, and IVDifficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS13. If you excel in analyzing the future outlook of firms, you would prefer that the financial markets be ____ form efficient so that you can have an advantage in the marketplace.A. weakB. semiweakC. semistrongD. strongE. perfectDifficulty level: EasyTopic: MARKET EFFICIENCYType: CONCEPTS14. Your best friend works in the finance office of the Delta Corporation. You are aware that this friend trades Delta stock based on information he overhears in the office. You know that this information is not known to the general public. Your friend continually brags to you about the profits he earns trading Delta stock. Based on this information, you would tend to argue that the financial markets are at best _____ form efficient.A. weakB. semiweakC. semistrongD. strongE. perfectDifficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS15. The U.S. Securities and Exchange Commission periodically charges individuals for insider trading and claims those individuals have made unfair profits. Based on this fact, you would tend to argue that the financial markets are at best _____ form efficient.A. weakB. semiweakC. semistrongD. strongE. perfectDifficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS16. Individuals that continually monitor the financial markets seeking mispriced securities:A. tend to make substantial profits on a daily basis.B. tend to make the markets more efficient.C. are never able to find a security that is temporarily mispriced.D. are always quite successful using only well-known public information as their basis of evaluation.E. are always quite successful using only historical price information as their basis of evaluation.Difficulty level: MediumTopic: MARKET EFFICIENCYType: CONCEPTS。

Finance(国际金融)关键术语名词解释

Finance(国际金融)关键术语名词解释Chapter 1《American EconomicReview》《美国经济评论》《Journal of Finance》《金融学报》《The Wealth of Nations》《国富论》acquisition 收购adjust risk 调整风险aggressive target 激进(性)的目标asset 资产asset allocation 资产配置bidder 出价者,竞标者Black-Scholes optionspricing formulaB-S期权定价公式business finance 企业财务(金融)capital budgeting 资本预算capital expenditure 资本支出capital structure 资本结构cash flow 现金流chief executive officer(CEO)首席执行官chief financial officer(CFO)首席财务官(财务总监)claims 权益(证)、索取权利classical economics 古典经济学common stock 普通股competitive stock market 竞争性的股票市场conflict of interest 利益冲突consumption and savingdecisions消费和储蓄决策consumption preference 消费偏好controller 审计员convertible securities 可转换证券corporation (有限责任)公司corporation finance 公司财务(金融)debt outstanding 未清偿贷款(债务)derivative securities 衍生证券diversify risk 分散风险dividend and financialpolicies红利(股利)和财务政策economic value 经济价值entertainment industry 娱乐行业(产业)entity 实体equity权益(与Liability(负债对应)evaluation of cost 成本估算(评价)exclusive goal 唯一目标executive compensationprogram管理者补偿(薪酬)计划extended family 大家庭finance 金融, 财政, 金融学finance system 金融系统financial advisory firm 金融咨询公司financial capital 金融资本financial contracting 订立金融合约(合同)Financial Executive Institute 财务执行官组织financing 筹措资金(融资)financing decision 融资决策general partner 一般合伙人going concern 关注效应infrastructure 基础设施、架构initial outlay 初始投入integrated financial program 完整的财务计划investment decision 投资决策ITT corporation 国际电报电话公司learning curve 学习曲线liability 负债、债务、责任limited liability 有限责任limited partner 有限责任合伙人long-lived asset 长期资产long-range incentivesystem长期激励系统market discipline 市场规则market interest rate 市场利率market risk premium 市场风险价格market value of shares 股票市场价值(简称市值)marketing 营销maximize the wealth (使)财富最大化merger 兼并,合并mortgage loan 抵押贷款multinational conglomerate 跨国企业集团mutual fund 共同基金net worth 净资产operating margin 营业利润option 期权original core business 原始的核心业务partnership 合伙企业pension liabilities 养老金负债personal investing 个人投资physical capital 实物资本pool联营;集中使用的(资金,物)portfolio 投资组合portfolio of asset 资产组合preferred stock 优先股president 总裁primary commitment 首要(基本)任务private corporation 私人(非公众)公司professional managers 职业经理人profit 利润profit-maximizationcriterion利润最大化标准proposition 命题public corporation 公众公司quantitative model 定量模型regulatory body 监管机构resource allocationdecision资源配置决策retail outlet 零售摊点return 回报,收益risk-averse 风险厌恶(规避)security price 证券价格share price appreciation 股价上涨(增值)shareholder-wealth-maximization股东财富最大化sole proprietorship 个体(业主制)企业spin-off 配股spread out over time 跨时间分布stake 资助,资金stock option 股票期权strategic planning 战略规划supplier 供货商takeover 接管the exchange of assetsand risks资产和风险的交换the set of markets andother institutions市场及其它机构的集合trade off 权衡uncertain benefit 不确定性收益unlimited (limited)liability无(有)限责任vice-president forfinancial财务副总裁voting right (股东)投票权welfare 福利well-functioning capitalmarket高效的资本市场working capitalmanagement营运资本管理Chapter 2accounting procedure 会计程序adverse selection 逆向选择American Express 美国运通信用卡arithmetic mean 算术平均数asymmetry 不对称average risk premium 平均风险升水(溢价)Bank for InternationalSettlement(BIS)国际清算银行banking panic 银行危机bartern. 易货贸易;v. 讨价还价board of directors 董事会by-product 副产品call option 买入期权(看涨期权)capital gain(loss)资本收益(损失)Capital market资本市场(即长期资金市场)cash dividend 现金股利(红利)central bank 中央银行charge price 要价clearing and settlingpayment清算和结算支付closed-end 封闭式的collateral 担保品collateralization 以…担保commercial loan 商业贷款commercial loan rate 商业贷款利率credit card 信用卡default 违约、托债、弃权default risk 违约风险deficit unit 赤字部门defined-benefit pensionplan规定收益型养恤金制defined-contributionpension plan规定缴费型养恤金制depository savingsinstitution存款储蓄机构(系统)derivative 衍生(证券)Deutsche Bank 德意志银行dissemination 推广、传播dividend reinvestment 红利(股利)再投资dollar-denominated asset 以美元计价的资产double-entry-bookkeeping 复式记账法equity 权益equity-kickers 权益条件expected rates of return 期望(预期)收益率Federal Reserve System 联邦储备系统Finance AccountingStandardsBoard财务会计标准委员会financial instrument 金融工具financial intermediary 金融中介financial market parameters 金融市场参数financial variable 金融(财务)变量fixed-income-instruments 固定收益证券flow of fund 资金流flow of fund 资金流foreign exchange 外汇formation extraction 信息提取forward contract 远期合约functional perspective (从)功能(的角度或观点)future 期货German marks 德国马克go public 上市incentive problem 激励问题index fund 指数(化)基金index-linked bonds(与物价)指数联系的债券information service 信息咨讯(服务)insurance company 保险公司interest rate 利息率(简称利率)interest rate arbitrage 利率套利interest rate equalization 利率平价intermediary 中介International BankforReconstruction andDevelopment国际复兴开发银行International Monetary Fund(IMF)国际货币基金组织International Swap DealersAssociation国际掉期交易商协会intertemporal 跨期的(多阶段的)IOUI owe you的简称,喻指“借条”issuing stock 发行股票Japanese yen 日元life annuity 人寿年金limited liability 有限责任liquidity 流动性maturity (票据)到期日;期限money market货币市场(即短期资金市场)moral-hazard 道德风险mortgage 抵押mortgage rate 抵押利率mutual fund 共同基金New York Stock Exchange 纽约股票交易所nominal interest rate 名义利率offset 弥补、抵消open-end 开放式的option 期权Osaka Options and FuturesExchange大阪期货期权交易所over-the-counter-market(OTC)场外(交易)市场parties to contract 合约的参与者pool or aggregate 联营;集中使用的(资金或物品);premium 升水、溢价price appreciation 增值principal-agent problem 委托-代理问题pro rata 按比例的put option 卖出期权(看跌期权)qusai- 准、半rate of exchange 汇率rates of return 收益(回报)率rating agency 评级机构real interest rate 实际利率real rate of return 实际收益率redeem 赎回、偿还residual claim 剩余索取(求偿)权risk aversion 风险厌恶(规避)risk premium 风险升水(溢价)security dealer 证券交易商shed specific risk 规避(分散)特定(或私有)风险standard deviation 标准差standardized option contract (经)标准化的期权合约surplus unit 盈余部门trade-off 权衡trust company 信托公司U.S Treasury Bills 美国国库券underwrite 认购、包销unit of account 计值单位universal bank全能银行(指兼做中央银行和商业银行业务的银行)volatility 波动性well-information 信息充分的yen rate of return(以)日元(记值)的收益率yield curve 收益(率)曲线yield spread 收益价差Chapter 3accounting earnings 会计收入accounting rule 会计规则accrual 应计的accrual accounting 应计制(权责发生制)accumulated depreciation 累计折旧amortize 摊销、分期偿还apocryphal 伪经的、假冒的asset turnover(ATO)资产周转率(销售收入/总资产)audit 查账、审计balance sheet 资产负债表benchmark (比较)基准bond-rating 债券评级book value 账面价值capital structure 资本结构capital-incentive utility 资本密集型的公用事业(公司)cash and equivalents 现金及其等价物cash budget 现金预算cash cycle time 现金循环周期cash inflow 现金流入cash outflow 现金流出common stock outstanding 流通在外的普通股contingent liability 或有负债(如:可能发生的诉讼赔偿等)current asset 流动资产current liability 流动负债current ratio 流动比率depreciation 折旧、贬值disclose 披露dividend payout rate 股利支付率earnings before interest and tax (EBIT)息税前利润(=毛利- GS&A)earnings per share 每股盈余(收益)earnings retention rate (收益)留存比率expiration date 到期日external financing 外部融资(比如,发行股票和债券)financial distress 财务危机(困境)financial leverage 财务杠杆(率)financial ratio 财务比率financial statement 财务报表general, selling, andadministrative expenses(GS&A)管理及销售费用goodwill 商誉gross margin 毛利(润)(=销售收入-产品销售成本)income statement 损益表income tax 所得税intangible asset 无形资产inventory 库存、存货inventory turnover 存货周转率liquidity 流动性long-term debt 长期负债market to book 市值价值/账面价值marking to market 盯住市场net income(or net profit)净利润(即税后利润=EBIT-利息-所得税)net working capital 净营运资本(=流动资产-流动负债)net worth 净资产(即权益,=资产-负债)off-balance-sheet 表外项目operation income 营运收益(营业利润)opportunity cost 机会成本owner’s equity所有者权益paid-in capital 实收资本payable 应付账款percent-of-sales method 销售(收入)百分比法planning horizon 计划(时间)跨度price to earnings 市盈率(价格/盈余)profitability 盈利能力、盈利性property 土地、地产、所有权quick ratio 速动比率receivable 应收账款receivables turnover 应收账款周转率retained earnings 留存收益ROA(return on asset)资产收益率(EBIT/资产)ROE(return on equity)净资产收益率(即权益报酬率,=税后利润/净资产)ROS(return on sales)销售利润率(EBIT/销售收入)short-term debt 短期负债specify performance target 设定业绩目标statements of cash flow 现金流量表sustainable growth rate 持续增长率taxable income 应税收益(即税前利润=EBIT-利息)times interest earned 利息保障倍数Tobin’s Q托宾Q值(=资产市值/重置成本)total shareholder returns 总的股东收益(率)Chapter 4after-tax interest rate 税后利率amortization 分期偿还、摊销annual percentage rate(APR)年度百分比(利率)annuity 年金before-tax interest rate 税前利率compound interest 复利compounding 复和(与discounting 相反的概念)discount rate 折现率、贴现率discounted cash flow(DCF)折现现金流discounting 折现、折扣effective annual rate(EFF)有效年利率exchange rate 汇率future value 终值future value factor 终值系数(即由现值计算终值的换算因子)growth annuity 增长年金immediate annuity 即付年金implied interest rate 隐含利率installment 分期付款internal rate of return(IRR)内部报酬率market capitalizationrate市场资本化利率(简称市场利率)net present value净现值opportunity cost ofcapital资本的机会成本ordinary annuity 普通年金(即后付年金)original principal (初始)本金outstanding balance 未平头寸payback period 回收期perpetual annuity(orperpetuity)永续年金present value 现值present value factor (终值)现值系数(终值系数的倒数)reinvest 再投资simple interest 单利tax-exempt 免税的time value of money (TVM)货币(或资金)的时间价值yield to maturity 到期收益率Chapter 5bequest 遗赠、遗赠物break-even 得失相当的,盈亏平衡的deductible 可扣除(或抵扣)的explicit cost 显性成本feasible plan 可行(的)计划human capital 人力资本implicit cost 隐性成本incremental 增量的、增值的intertemporal budget跨期预算约束optimization model 优化模型permanent income 永久性收入provision 条文、条款tax deferred 税收(可)延缓的tax exempt 免税的trial-and-error 试错Chapter 6after-tax cash flow 税后现金流all-equity-financed firm 全权益融资公司annualized capital cost 年金化资本成本appropriation 拨款、占用break-even point 盈亏平衡点capital budgeting 资本预算cost of capital 资本成本coupon bond 息票债券cumulative present value 累计现值full-fledged 完备的、正式的horizontal axis 横轴(或横坐标)labor-intensive 劳动密集型的liquidate 清算、清偿market-related risk 市场相关(或者承认予以补偿)的风险,即系统风险(systematic risk)prototype 模型、原型residual value 残值risk premium 风险溢价risk-adjusted discountrate(经)风险调整的折现率sensitivity analysis 敏感性分析vertical axis 纵轴(或纵坐标)zero-inflation 零通涨(率)Chapter 7Arbitrage 套利arbitrageurs 套利(交易)者beverage 饮料bona fide 真正的bond 债券default risk 违约风险default-free 无违约(风险)的earnings per share 每股盈余efficient marketshypothesis(EMH)有效市场假说fetch 售得…fixed-income securities 固定收益证券foreign exchangemarket外汇市场fundamental value 基础价值information set 信息集interest-rate arbitrage 利率套利intrinsic value 内在价值laundry 洗衣店Law of One Price 一价定律price/earnings multiple 市盈率(倍数)real estate 房地产、不动产sibling 兄弟、同胞、氏族成员tautologically 同意反复地transaction costs 交易成本triangular arbitrage 三角套利vending 售货well-informed 信息充分的Chapter 8abscissa 横坐标ask price 卖价、要价(报价)bid price 买价、出价(询价)callable bond 可赎回债券convertible bond 可转换债券coupon bond 带息债券、息票债券current yield 即期收益(率)discount bond 折价债券face value/ par value 面值maturity 到期日ordinate 纵坐标par bond 平价债券premium bond 溢价债券pure discount bond 纯折现债券quote 牌价redeem 赎回、偿还risk-free interest rate 无风险利率yield curve 收益(率)曲线yield to maturity 到期收益(率)zero-coupon bond 零息(票)债券Chapter 9New York StockExchange纽约股票交易所cash dividend 现金股利(或红利、分红)closing price 收盘价Constant-Growth-RateDDM不变增长率股利折现模型current/existingstockholders现有股东、老股东discounted-dividendmodel(DDM)股利折现模型dividend policy 股利政策dividend yield 分利收益率ex-dividend price 除息(即股息)价格expected rate of return 期望收益率(或报酬率)infinite 无穷(或无限)的internal equity financing 内部权益融资Investment opportunity 投资机会market capitalization rate 市场资本化利率odd lots 零星(交易量)per se 亲自、亲身perpetual 永久的price/earnings ratio 市盈率Reinvested earnings 再投资收益required rate of return 必要报酬率(或收益率)risk-adjusted discountrate(经)风险调整折现率round lots 整批(交易量)share repurchase 股票回购skeptical 怀疑的stock dividend 股票股利stock splits 股票分割Chapter 10actuary 精算师caterer 酒席承办人colossal 巨大的、异常的confidence intervals 置信区间consortium 社团、合伙continuous probability distribution 连续概率分布diversification 分散化(投资)diversifying 分散化、多样化dunce 笨蛋、书呆子ex ante 事先的ex post 事后的expected rate of return 期望收益率(报酬率)flexibility 灵活性、柔性forward contract 远期合约hedger (套期)保值者、对冲者hedging 保值、对冲、对两方下注以防止(赌博、冒险等)的损失insuring 投保、给…保险jurisdiction 司法、权力、权限layoff 解雇、失业materialize 实现mean 均值normal distribution 正态分布overview 概述perverse 故意作对的、任性的portfolio 投资组合precautionary saving 预防性储蓄probability distribution 概率分布quadruple adj. 四倍的;v. 使…(增加)四倍recrimination 反责refund 退还risk assessment 风险评估risk aversion 风险规避risk avoidance 风险避免risk exposure 风险暴露risk identification 风险识别risk management 风险管理risk retention 风险保留risk transfer 风险转移sinful 有罪的、过错的、不道德的speculator 投机者square root 平方根stakeholder 利益相关者standard deviation 标准差swap 互换volatility 波动率Chapter 11American-type option 美式期权call option 买入期权(简称“买权”)cap (利率)上限condominium 公寓私有的共有方式co-payment 共同支付counterparty 交易对手credit guarantee 信用担保credit risk 信用风险deductible/deduction 免赔额delivery 交割delivery date 交割日derivative 衍生工具diversifiable risk 可分散的风险diversification principle 分散化(或多元化)原则European-type option 欧式期权exclusion 除外责任expiration date 到期日expire 到期face value 面值fictitious 虚构的firm-specific risk (公司)私有(或特有)风险forward contract 远期合约forward price 远期价格future contract 期货合约guarantee 保证、保证人、担保、担保品loan guarantee 债务保单long position 多头market risk 市场风险non-diversifiable risk 不可分散的风险premium 保险费、附加费、溢价proceed n. 盈利put option 卖出期权(简称“卖权”)rolling over 滚动(式)的short position 空头shortfall 不足之数、赤字spot price 即期价格standardized (经)标准化的strike price/ exerciseprice执行价格、行权价swap contract 互换合约、调期合约Chapter 12decision horizon 决策(修正)期限efficient portfolio 有效组合efficient portfolio frontier 有效组合前沿expected return 期望收益率mean-variance model 均值-方差模型minimum-varianceportfolio最小方差组合mutual fund 共同基金optimal combination ofrisky assets风险资产最优组合planning horizon 计划期、规划期point of tangency 切点portfolio selection (投资)组合选择risk premium 风险溢价risk tolerance 风险容忍(度)riskless asset 无风险资产risky-asset portfolio 风险资产组合set of……的集合tangency portfolio 切线组合target expected return 目标期望收益率trade-off 权衡、平衡trading horizon 交易(间隔)期限Chapter 13active investmentstrategies积极投资策略active portfolio selectionstrategy积极的组合选择策略Arbitrage Pricing Theory (APT)套利(定价)理论beat the market 打败市场benchmark 基准benchmark portfolio 基准组合Capital Asset PricingModel(CAPM)资本资产定价模型capital market line(CML)资本市场线consensus 一致、一致同意cost of capital 资本成本covariance 协方差equilibrium asset price 均衡(的)资产价格equilibrium expectedreturn均衡(的)期望收益率equilibrium price 均衡价格equilibrium risk premium 均衡风险溢价indexing 指数化irreducible 不能减少的、难复位的marginal contribution 边际贡献market portfolio 市场组合market-related risk 市场相关的(或承认的)风险multifactor IntertemporalCapital Asset PricingModel(ICAPM)多因子、跨期资本资产定价模型mutual fund 共同基金non-market risk 非市场风险passive investing 消极投资passive portfolio selectionstrategy消极的组合选择策略pension fund 养老基金regression coefficient 回归系数reward-to-risk ratio 风险补偿比率security market line(SML)证券市场线short-sale 卖空systematic risk 系统风险unsystematic risk 非系统风险Chapter 14arbitrageur 套利者bountiful 慷慨的、充足的casino 卡西诺赌场、小别墅closing out(one’s/a)position平仓continuouscompounding连续复利cost of carry 持有成本daily marking to market 逐日盯市(即每日无负债清算制度)delivery 交割delivery date 交割日delivery price 交割价格expectationshypothesis期望假说financial future 金融期货(即标的物为金融产品的期货合约)foreign-exchangeparity relation汇率平价关系forward contract 远期合约forward price 远期价格forward-spotprice-parity relation 远期-即期价格间的平价关系future contract 期货合约future price 期货价格future spot price 将来的现货价格hedger 套期保值者intrinsic value 内在价值margin 保证金open interest 未平仓合约数、头寸开放权益数position 头寸posting of margin (对)保证金(进行)过帐quasi-arbitrage 准套利(机会)replicate 复制speculator 投机者spoilage 损坏spot price 即期价格、现货价格spread 价差、差额the wall street journal 《华尔街日报》Chapter 15American-typeoption美式期权arrear 应付欠款、储备物at the money option 两平期权Black-Scholes model 布莱克-斯科尔斯期权定价模型boom 繁荣的bullish 乐观的call (option)买入期权(简称买权)、看涨期权capital-gain 资本(性)收益cash settlement 现金结算Chicago BoardOptions Exchange(CBOE)芝加哥期权交易所commission 佣金Contingent Claims 或有权益(简称或有权、或然权)credit guarantee 信用保证(或承诺)de facto 实际的、实际上decision tree 决策树delinquency 失职、违法行为dividend yield 股利收益率dividend-adjusted option formula 股利调整期权(定价)公式embedded option 嵌入式期权European put option 欧式卖权European-type欧式期权evasion 逃避、躲避Exchange-traded option 场内(即在交易所交易的)期权exercise price/strikeprice执行价格/敲定价格expirationdate/maturity date到期日explicit 外生的flexibility 灵活性、柔性FutureOptions/Option onFutures期货期权growth option 增长期权guarantor 保证人hedge ratio 对冲比率、套期比率implicit 内生的implied volatility 隐含波动率in the money option 虚值期权incremental 增量的、增加的index option 指数期权intrinsicvalue/tangible value内在价值、执行价值junk bond 垃圾债券litigation 诉讼、争论mainline 主流的、传统的natural logarithm 自然对数normal distribution 正态分布Option 期权out of the moneyoptionOver-the-counteroption场外(交易的)期权payoff diagrams 支付图plaintiff 起诉人provision 条文、条款put (option)卖出期权(简称卖权)、看跌期权put-call parityrelation买(权)与卖(权)间的平价关系real option 实物期权recession 衰退self-financinginvestment strategy自融资投资策略sequel 续篇、后果shortfall 不足之数、赤字stochastic 随机的 swap 互换 time value 时间价值 truncate截断two-state (binomial )option pricing model 两状态(二项式)期权定价模型 underlying asset 标的资产、基础资产Chapter 16account payable 应付账款accrued wage应计工资adjusted present value (APV )(经)调整的现值 after-tax incremental cash flow 税后增量现金流agency cost 代理成本allegiance 忠诚、忠贞all-equtiy financing 全权益融资 bankruptcy cost破产成本bankruptcy proceeding 破产程序、破产诉讼 Capital Structure 资本结构capital structure irrelevance proposition 资本结构无关性定理circumvent 绕过、智胜collateral 担保品common stock 普通股corporate income tax公司所得税cost of financial distress 财务危机(危难)成本 debt financing 债务融资 entity实体、本质、存在equity financing 权益融资external financing外部融资(筹资) fiduciary受信托的 financial distress财务危机(危难) financing instrument 金融工具 franchise 特许权 free cash flow自由现金流 frictionless 无摩擦的gourmet供美食家的享用的、美食家imminent 临近的、迫在眉睫的 interest tax shield (债务)利息税盾 internal financing 内部融资(筹资) issuing new stock 发行新股leveraged investment 杠杆投资(即投资额中有部分债务融资)long-term lease 长期租赁M & M proposition MM 定理market debt-to-equity ratio(用)市场(价值表示的)债务-权益比率market-value/economic balance sheet (用)市场价值(表示的)资产负债表 Modigliani & Miller (M 莫迪里阿尼和米勒& M )optimal capital structure 最优资本结构 pension liability 养老金(形式的)债务 perk额外补贴 personal income tax 个人所得税 preferred stock优先股学习必备欢迎下载prestige 威信、声望pro rata 按比例的realized capital gains 已实现资本收益redeploy 重新部署(布置、调派)repurchase stock 回购股票residual claim 剩余索取权(求偿权)retained earning 留存收益scrutiny 细致检查secured debt 安全债务stock option 股票期权subsidy 津贴、财政援助、特别津贴voting right 投票权warrant 认股权证、认股权weighted average costof capital(WACC)加权资本成本Chapter 17acquisition 收购bargain v. 讲价、讨价还价;n. 便宜货、交易、协定breakup 分散、中止、崩溃consolidation 合并、联合、巩固consummate 完成、使…完美contest 竞争、争夺corroborate 加强证实、巩固、支持discretion 决定权、谨慎、判断力divest 使…脱去information set 信息集loss carry-forward 亏损递延malevolence 恶意、坏影响merger 兼并opaqueness 不透明real option 实物期权spin-off 派生出、让产易股、抽资脱离synergy 协同增效takeover 接管。

公司理财英文版第十四章

– Using SML: RE = 6% + 1.5(9%) = 19.5% – Using DGM: RE = [2(1.06) / 15.65] + .06 = 19.55%

14-14

Cost of Debt

• The cost of debt is the required return on our company’s debt • We usually focus on the cost of long-term debt or bonds • The required return is best estimated by computing the yield-to-maturity on the existing debt • We may also use estimates of current rates based on the bond rating we expect when we issue new debt • The cost of debt is NOT the coupon rate

– RE = 6.1 + .58(8.6) = 11.1%

• Since we came up with similar numbers using both the dividend growth model and the SML approach, we should feel good about our estimate

14-5

Cost of Equity

• The cost of equity is the return required by equity investors given the risk of the cash flows from the firm

金融学(博迪)英文版课后习题答案

金融学(博迪)英文版课后习题答案CONTENTSChapter 1: Financial Economics 1-1Chapter 2: Financial Markets and Institutions 2-1Chapter 3: Managing Financial Health and Performance 3-1Chapter 4: Allocating Resources Over Time 4-1Chapter 5: Household Saving and Investment Decisions 5-1Chapter 6: The Analysis of Investment Projects 6-1Chapter 7: Principles of Market Valuation 7-1Chapter 8: Valuation of Known Cash Flows: Bonds 8-1Chapter 9: Valuation of Common Stocks 9-1Chapter 10: Principles of Risk Management 10-1Chapter 11: Hedging, Insuring, and Diversifying 11-1Chapter 12 Portfolio Opportunities and Choice 12-1Chapter 13: Capital Market Equilibrium 13-1Chapter 14: Forward and Futures Markets 14-1Chapter 15: Markets for Options and Contingent Claims 15-1Chapter 16: Financial Structure of the Firm 16-1Chapter 17: Real Options 17-1CHAPTER 1 – Financial EconomicsEnd-of-Chapter ProblemsDefining Finance1. What are your main goals in life? How does finance play a part in achieving those goals? What are themajor tradeoffs you face?SAMPLE ANSWER:Finish schoolGet good paying job which I likeGetmarried and have childrenOwn my own homeProvide for familyPay for children’s educationRetireHow Finance Plays a Role:SAMPLE ANSWER:Finance helps me pay for undergraduate and graduate education and helps me decide whether spending themoney on graduate education will be a good investment decision or not.Higher education should enhance my earning power and ability to obtain a job I like.Once I am married and have children I will have additional financial responsibilities (dependents) and Iwill have to learn how to allocate resources among individuals in the householdand learn how to set aside enoughmoney to pay for emergencies, education, vacations etc. Finance also helps me understand how to manage risks suchas for disability, life and health.?Finance helps me determine whether the home I want to buy is a good value or not. The study of financealso helps me determine the cheapest source of financing for the purchase of that home.Finance helps me determine how much money I will have to save in order to pay for my children’seducation as well as my own retirement.Major Tradeoffs:SAMPLE ANSWERSpend money now by going to college (and possibly graduate school) but presumably make more moneyonce I graduate due to my higher education.Consume now and have less money saved for future expenditures such as for a house and/or car or savemore money now but consume less than some of my friends。

公司理财(罗斯)第14章(英文)

Replacement Value

The current cost of replacing the assets of the firm.

At the time a firm purchases an asset, market value, book value, and replacement value are equal.

Market Value is the price of the stock multiplied by the number of shares outstanding.

Also known as Market Capitalization

Book Value

The sum of par value, capital surplus, and accumulated retained earnings is the common equity of the firm, usually referred to as the book value of the firm.

Some stocks have no par value.

McGraw-Hill/Irwin Corporate Finance, 7/e

2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

14-4

Authorized vs. Issued Common Stock

McGraw-Hill/Irwin Corporate Finance, 7/e 2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

14-10

Cumulative vs. Straight Voting: Example

国际经济学的国际金融部分的选择题练习