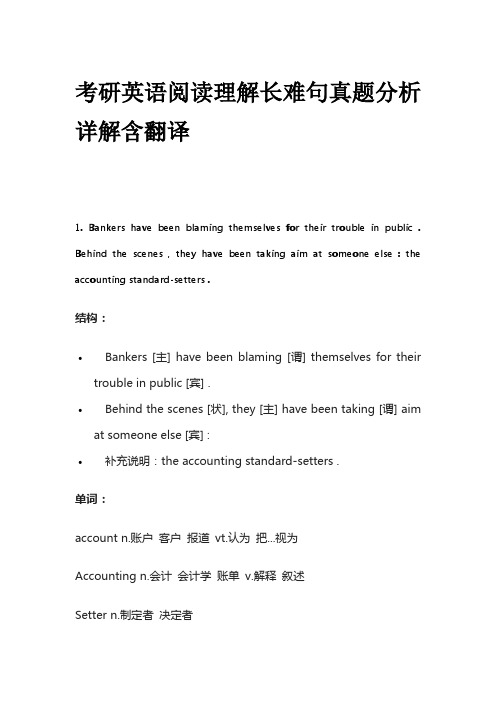

Banks and accounting standards

会计专业英语词汇

会计专业英语词汇obligation债项;责任;义obligation bond债务债券obligee受惠人occupational retirement scheme职业退休计划Occupational Retirement Schemes Division [Financial Services Bureau] 退休计划部〔财经事务局〕odd lot散股;碎股;零股odd lot broker散股经纪OECD country经济合作及发展组织国家;经济合作及发展组织的成员国OECD stock market经济合作及发展组织国家的证券市场off-balance-sheet exposure资产负债表外的风险off-balance-sheet financing帐外融资;资产负债表外的融资off-balance-sheet item资产负债表外的项目off-balance-sheet transaction帐外交易;资产负债表外的交易offer要约;建议;收购offer by tender招标发售offer document要约文件;建议文件offer for sale要约出售offer for subscription公开招股offer mechanism招股机制offer of shares for public subscription 公开招股offer period要约期offer price要约价;发盘价offer rate拆出息率offer to buy要约买入offer to lend要约贷出offer to sell要约卖出offeree受要约人offeree company受要约公司offeree shareholder受要约公司的股东offeror要约人offeror company要约公司;提出要约公司off-floor terminal离场交易终端机off-floor trading离场交易office of profit有收益的职位Office of the Commissioner for Securities and Commodities Trading 证券及商品交易监理专员办事处Office of the Commissioner of Banking银行业监理处Office of the Commissioner of Insurance保险业监理处Office of the Exchange Fund外汇基金管理局Office of the Telecommunications Authority Trading Fund电讯管理局营运基金Official Administrator遗产管理官official emolument官职薪酬official listing正式上市official rate法定汇率;官价Official Receiver破产管理署署长Official Receiver's Office破产管理署official trustee法定受托人off-market dealing场外买卖offset抵销;弥补;冲销offsetting position相抵持仓offshore bank离岸银行offshore borrowing海外借款offshore borrowing transaction 海外借款交易offshore business海外业务offshore currency deposit market 海外货币存款市场offshore fund离岸基金offshore interest海外利息offshore reinsurance income离岸再保险入息Offshore Supervisors Group离岸监理组织off-site review非实地审查off-site scrutiny非实地审核Ogaki Kyoritsu Bank, Ltd.大垣共立银行omission of income漏报入息omission of profit漏报利润on account basis记帐方式;赊帐方式on-balance-sheet item资产负债表内的项目on-cost间接成本;间接费用;附加行政费用one board lot of securities“一手”证券"one building" condition“一家分行”的规定one day rolling currency futures单日掉期外汇期货one day rolling currency futures contract 单日掉期外汇期货合约one price单一价格;不二价one-line vote整笔拨款one-off grant一次过拨款one-off item非经常项目one-off payment一次过拨款;单一笔款项one-off subsidy一次过补贴onerous tax繁苛税项;繁重税率on-floor order场内买卖盘on-lending转借on-site examination实地审查open a position“做仓”;开仓open account未清帐户;记帐交易;往来帐户open contract未平仓合约open economy开放经济open interest未平仓合约数量open market公开市场open market value公开市场价值;市值open offer [listing method]公开售股〔上市方式〕open order开仓订单open outcry公开叫价;公开喊价open position未平仓交易open price开仓价格open tender公开投标open-end fund开端基金open-ended investment corporation 股份不定的投资公司opening balance期初结余opening price开盘价格;开市价opening quotation开市价;开市行情opening rate开盘汇价operating account营业帐目;营业帐户;经营帐目operating agreement营运协议operating cost营运成本;运作成本;操作成本operating deficit营业亏损;经营赤字operating expenditure经营开支;营运开支;营业支出operating expenses营运开支;营业费用operating income营运收入;营业收入operating loan经营业务所需贷款operating profit营业利润operating revenue营运收入;营业收益operating services account营运服务帐目operating statement经营收支表;营业损益表operating surplus经营盈余;营业盈余operation经营;营运;投产operational fund经费operative aggregate现行总体数字operator经营者;营运者;营办商opportunity cost机会成本optimist“好友”optimum rate of expenditure最适当支出率option期权;认购权;选择权;选购权option contract期权合约option money期权费option on a futures contract期货合约期权;期货期权option on commodities商品期权option position期权持仓量option premium期权金;期权溢价optional stipulation选择性规定Options Clearing Corporation [Chicago]期权结算公司〔芝加哥〕Options Clearing House Pty Limited [Sydney] 期权结算所有限公司〔悉尼〕Options Clearing Rules《期权结算规则》options market期权市场options market maker期权“庄家”options pricing model期权定价模式options trading期权交易options trading member期权交易会员Options Trading Rules《期权交易规则》order订单;命令;买卖盘order cheque记名支票;抬头支票order for payment of money 付款指令票据order for purchase订购书order for redirection转寄令order for sale售卖令order of discharge破产解除令order of foreclosure absolute 绝对止赎令order of mail transfer信汇委托书order to pay admitted debt 偿付承认债项令order-based system以买卖盘为基础的制度ordinary annual contribution经常性每年捐款ordinary course of business通常业务运作ordinary creditor普通债权人ordinary share普通股ordinary share capital普通股股本organization expenses开办费Organization for Economic Co-operation and Development [OECD]经济合作及发展组织〔经合组织〕Organization of Petroleum Exporting Countries [OPEC]石油出口国组织Orient First Capital Limited建银财务(香港)有限公司original estimates原来预算original executor原遗嘱执行人original issue price原本发行价original margin原始保证金;基本按金original mortgagee原承按人original mortgagor原按揭人original receipt收据正本;收条正本original securities原有的证券ORIX Asia Limited欧力士(亚洲)有限公司ornament gold饰金Osaka Securities Exchange 大阪证券交易所Oslo Stock Exchange奥斯陆证券交易所O.T.B. Card Co. Ltd.海外信用卡有限公司ounce troy金衡安士outflow of capital资本外流;资金外流outflow of fund资金外流outflow of money资金外流outgoing partner退出的合伙人outgoings支出outgoings and expenses支出及开支outlay费用;开支;支出outlying business district市区外商业区out-of-hours trading在正式交易时间以外的交易out-of-pocket expenses实付费用;付现费用out-of-the-money option无价期权;价外期权outport collection外埠代收款项output产出;产值;产量outside dealing场外买卖;场外交易outstanding未偿还;尚未支付outstanding account未清帐项;未清帐目outstanding allocation应拨未拨的款项outstanding amount未偿还的数额outstanding balance未清帐款;未清余额outstanding bill未偿付票据;未兑现票据outstanding borrowing未清偿债项outstanding claim portfolio未决申索组合outstanding commitment尚未支付的承担额outstanding derivatives contract尚未平仓的衍生工具合约outstanding loan尚未清还的贷款outstanding negotiable certificate of deposit 未兑现的可转让存款证outstanding tax欠税outstanding uncapitalized interest尚未支付且未化作本金的利息outturn结算;结算数字outward documentary bill出口跟单汇票outward remittance汇出汇款over and above inflation减除通胀因素overall average internal rate of return平均总体内部回报率overall Consumer Price Index总体消费物价指数overall domestic export本地产品出口总额overall growth rate整体增长率;总增长率overall investment总投资额;总体投资overall liquidity ratio总体流动资金比率overall price relative全面相对价格overall surplus总盈余overall tally全面总计overbuying超买;买空over-commitment超额承担overdraft透支overdraft by banks abroad海外银行同业透支overdraft by banks in foreign countries 外国银行同业透支overdraft by local banks本港银行同业透支overdraft by outport banks外埠银行同业透支overdraft of an account户口透支overdraft on banks向银行同业透支overdraft on banks abroad向海外银行同业透支overdraft on banks in foreign countries向外国银行同业透支overdraft on local banks向本港银行同业透支overdraft on outport banks向外埠银行同业透支overdraft secured抵押透支overdue逾期overdue loan过期贷款over-employed economy过度活跃的经济overhang剩余承担;未完成的承担额;过剩额overhead间接费用;间接成本overhead cost间接成本overheated economy过热的经济overheated market过热的市场overnight Hong Kong interbank offered rate 香港银行同业隔夜拆息率overnight liquidity assistance隔夜流动资金贷款overnight margin隔夜保证金;隔夜按金overnight money隔夜拆借资金;隔夜钱overnight position隔夜头寸overnight rate隔夜利率overpaid amount多缴数额overpayment of contribution多缴供款overrun超支overrun cost超额费用Oversea-Chinese Banking Corporation Ltd.华侨银行有限公司overseas bank海外银行overseas banking corporation海外银行法团overseas branch海外分行Overseas Companies Section [Companies Registry] 海外公司注册组〔公司注册处〕overseas currency balance海外货币结余overseas financial institution 海外财务机构overseas interest海外利息overseas investment海外投资overseas market海外市场overseas representative office 海外代表办事处Overseas Trust Bank Ltd.海外信托银行有限公司Overseas Union Bank Ltd. 华联银行overselling超卖;卖空oversight of markets监察市场over-spending超额支出;超支overtax超额征税;征税过重over-the-counter derivative 场外交易衍生工具over-the-counter market场外交易市场over-the-counter trading场外交易;柜台交易over-the-counter transaction 场外交易;柜台交易overtrading过量交易owner-occupier allowance自住业主津贴ownership所有权;拥有权ownership in common分权共有权会计专业英语会计专业英语AccountingEnglishINTRODUCTION TO ACCOUNTING ENGLISH 5CHAPTER 1 INTRODUCTION TO ACCOUNTING 6§ 1.1 THE IMPORTANCE OF ACCOUNTING (会计的重要性)6§ 1.2.ACCOUNTING AS A PROFESSION (会计职业)7§ 1.3.ACCOUNTING KNOWLEDGE SYSTEM(会计学科体系)7§ 1.4.PROFESSIONAL ACCOUNTING BODIES(专业会计团体)8§ 1.5.ACCOUNTING POLICIES AND ACCOUNTING STANDARD 9(会计的法规体系和基本会计准则)9§ 1.6.FUNDAMENTAL ACCOUNTING CONCEPTS (基本会计理念) 101.6. 1. FOUR BASIC ACCOUNTING ASSUMPTIONS 101.6.2. IMPORTANT BASIC ACCOUNTING PRINCIPLES 11CHAPTER 2 THE ACCOUNTING ELEMENTS AND EQUA TION 132.1.THE ACCOUNTING ELEMENTS 132.1.1 ASSETS 132.1.2 LIABILITIES 负债142.1.3 OWNER’S EQUITY所有者权益142.1.4 REVENUE (INCOME) 收入152.1.5 EXPENSE (OUTCOME) 费用152.1.6 PROFIT/ LOSS 利润或亏损152.2. THE ACCOUNTING EQUA TION 162.2.1 THE ACCOUNTING EQUITA TION(会计恒等式)162.2.2 HOW THE BUSINESS TRANSACTIONS EFFECT ON THE ACCOUNTINGEQUITA TION (经济业务与会计恒等式的关系) 162.2.3 CONCLUSION 18EXERCISES 18CHAPTER 3 DOUBLE ENTRY ACCOUNTING & LEDGER ACCOUNTS 193.1. THE DOUBLE ENTRY ACCOUNTING (复式记账) 193.2. APPLICA TION OF DOUBLE-ENTRY ACCOUNTING PRINCIPLE (复式记账的应用) 21 3.3. THE LEDGER ACCOUNTS分类账户223.3.1 THE LEDGER ACCOUNTS 223.3.2 PRACTICE: RECORD THE TRANSACTIONS ON THE RELEV ANT LEDGER ACCOUNTS (实训: 登T型账) 233.4 TRIAL BALANCE (试算平衡) 2626TABLE 3.4 :TRIAL BALANCE (试算平衡表) 27CHAPTER 4 TRANSACTIONS & DOUBLE-ENTRY ACCOUNTING 314.1. INTRODUCTION OF BUSINESS OPERA TIONS: 314.2. ACCOUNTING FOR MERCHANDISING BUSINESSES 334.2.1 ACCOUNTING FOR SUPPLYING TRANSACTIONS(供应过程的会计核算) 33--- MERCHANDISES / INVENTORY(存货, 货物)334.2.2 ACCOUNTING FOR SALES TRANSACTIONS(销售过程的会计核算)374.3. MANUFACTURING BUSINESS 404.3.1 INTRODUCTION OF MANUFACTURING CYCLES 404.3.2 ACCOUNTING FOR MANUFACTURING PROCESSES (生产过程的会计核算) 414.4. REVISION CLASSES 43CHAPTER 5 BASIC FINANCIAL STA TEMENT 455.1. BALANCE SHEETS (资产负债表) 455.1.1 EXHIBITION5-1: BALANCE SHEET 465.1.2 PRACTICAL EXAMPLE OF BALANCE SHEET 48-- PRACTICAL EXAMPLE 1(实例 1 ): BALANCE SHEET OF ABC CO. LTD 48-- PRACTICAL EXAMPLE 2(实例 2 ): BALANCE SHEET OF TM CO. LTD 485.2. INCOME STA TEMENT (OR PROFIT AND LOSS STA TEMENT) (利润表) 515.2.1 EXHIBITION5-2: INCOME STA TEMENT 52-- PRACTICAL EXAMPLE 1(实例 1 ): INCOME STA TEMENT OF XYZ CO. LTD 53-- PRACTICAL EXAMPLE 2(实例 2 ): BALANCE SHEET OF TM CO. LTD 545.3. CASH FLOW STA TEMENTS (现金流量表) 565.3.1 CLASSIFICA TION OF CASH FLOWS 565.3.2 EXHIBITION5-3: CASH FLOW STA TEMENT 57-- PRACTICAL EXAMPLE 1(实例 1 ): STA TEMENT OF CASH FLOW XYZ CO. LTD 59 CHAPTER 6 ACCOUNTING CYCLES 616.1. STEPS IN ACCOUNTING CYCLE 616.2. RECORDING JOURNAL ENTRIES AND POSTING TO LEDGER ACCOUNTS (编制日记账和登记总账)626.2.1 WHA T SHOULD BE POSTED? 626.3. ADJUSTING ENTRIES (账户的调整)646.3. CLOSING ENTRIES (临时账户的结转) 67CHAPTER 7 SAMPLE DOCUMENTS 617.1. BILLS (票据) 697.1.1 汇票697.1.1支票707.2. INVOICES (单据) 727.2.1 合同727.2.2海运提单737.2.3装箱单767.3. OTHER RELEV ANT DOCUMENTS(其它凭证和文件) 78CHAPTER 8 APPENDIXES 91第一节:英语最常用口语118句91第二节:公司部门名称对照94第三节:常见职务中英对照95Introduction to Accounting English会计英语概论l Why do we learn it? (为什么要学《会计英语》?)(1)跨国公司(2)国际业务(3)国际投资l What are the Learning objectives? (《会计英语》的学习目标?)1.快速掌握财会专业通用英语词汇,以提高专业英语能力。

新世界-美国财务会计准则fas-005

Statement of Financial AccountingStandards No. 5FAS5 Status PageFAS5 SummaryAccounting for ContingenciesMarch 1975Financial Accounting Standards Boardof the Financial Accounting Foundation401 MERRITT 7, P.O. BOX 5116, NORWALK, CONNECTICUT 06856-5116Copyright © 1975 by Financial Accounting Standards Board. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Standards Board.Statement of Financial Accounting Standards No. 5Accounting For ContingenciesMarch 1975CONTENTSParagraphNumbers Introduction................................................................................................................1– 7 Standards of Financial Accounting and Reporting:Accrual of Loss Contingencies (8)Disclosure of Loss Contingencies.......................................................................9– 13 General or Unspecified Business Risks.. (14)Appropriation of Retained Earnings (15)Examples of Application of this Statement (16)Gain Contingencies (17)Other Disclosures..............................................................................................18– 19 Effective Date and Transition.. (20)Appendix A: Examples of Application of this Statement......................................21– 45 Appendix B: Background Information...................................................................46– 54 Appendix C: Basis for Conclusions......................................................................55–104FAS 5: Accounting for ContingenciesINTRODUCTION1. For the purpose of this Statement, a contingency is defined as an existing condition, situation, or set of circumstances involving uncertainty as to possible gain (hereinafter a "gain contingency") or loss 1 (hereinafter a "loss contingency") to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur. Resolution of the uncertainty may confirm the acquisition of an asset or the reduction of a liability or the loss or impairment of an asset or the incurrence of a liability.2. Not all uncertainties inherent in the accounting process give rise to contingencies as that term is used in this Statement. Estimates are required in financial statements for many on-going and recurring activities of an enterprise. The mere fact that an estimate is involved does not of itself constitute the type of uncertainty referred to in the definition in paragraph 1. For example, the fact that estimates are used to allocate the known cost of a depreciable asset over the period of use by an enterprise does not make depreciation a contingency; the eventual expiration of the utility of the asset is not uncertain. Thus, depreciation of assets is not a contingency as defined in paragraph 1, nor are such matters as recurring repairs, maintenance, and overhauls, which interrelate with depreciation. Also, amounts owed for services received, such as advertising and utilities, are not contingencies even though the accrued amounts may have been estimated; there is nothing uncertain about the fact that those obligations have been incurred.3. When a loss contingency exists, the likelihood that the future event or events will confirm the loss or impairment of an asset or the incurrence of a liability can range from probable to remote. This Statement uses the terms probable, reasonably possible, and remote to identify three areas within that range, as follows:a. P robable. The future event or events are likely to occur.b. R easonably possible. The chance of the future event or events occurring is more than remote but less thanlikely.c. Remote. The chance of the future event or events occurring is slight.4. E xamples of loss contingencies include:a. C ollectibility of receivables.b. Obligations related to product warranties and product defects.Copyright © 1975, Financial Accounting Standards Board Not for redistributionc. R isk of loss or damage of enterprise property by fire, explosion, or other hazards.d. Threat of expropriation of assets.e. P ending or threatened litigation.f. A ctual or possible claims and assessments.g. Risk of loss from catastrophes assumed by property and casualty insurance companies includingreinsurance companies.h. Guarantees of indebtedness of others.i. O bligations of commercial banks under "standby letters of credit."2j. A greements to repurchase receivables (or to repurchase the related property) that have been sold.5. S ome enterprises now accrue estimated losses from some types of contingencies by a charge to income prior to the occurrence of the event or events that are expected to resolve the uncertainties while, under similar circumstances, other enterprises account for those losses only when the confirming event or events have occurred.6. T his Statement establishes standards of financial accounting and reporting for loss contingencies (see paragraphs 8-16) and carries forward without reconsideration the conclusions of Accounting Research Bulletin (ARB) No. 50, "Contingencies," with respect to gain contingencies (see paragraph 17) and other disclosures (see paragraphs 18-19). The basis for the Board's conclusions, as well as alternatives considered and reasons for their rejection, are discussed in Appendix C. Examples of application of this Statement are presented in Appendix A, and background information is presented in Appendix B.7. T his Statement supersedes both ARB No. 50 and Chapter 6, "Contingency Reserves," of ARB No. 43. The conditions for accrual of loss contingencies in paragraph 8 of this Statement do not amend any other present requirement in an Accounting Research Bulletin or Opinion of the Accounting Principles Board to accrue a particular type of loss or expense. Thus, for example, accounting for pension cost, deferred compensation contracts, and stock issued to employees are excluded from the scope of this Statement. Those matters are covered, respectively, in APB Opinion No. 8, "Accounting for the Cost of Pension Plans," APB Opinion No. 12, "Omnibus Opinion—1967," paragraphs 6-8, and APB Opinion No. 25, "Accounting for Stock Issued to Employees." Accounting for other employment-related costs, such as group insurance, vacation pay, workmen's compensation, and disability benefits, is also excluded from the scope of this Statement. Accounting practices for those types of costs and pension accounting practices tend to involve similar considerations. STANDARDS OF FINANCIAL ACCOUNTING AND REPORTINGAccrual of Loss Contingencies8. An estimated loss from a loss contingency (as defined in paragraph 1) shall be accrued by a charge to income 3 if both of the following conditions are met:Copyright © 1975, Financial Accounting Standards Board Not for redistributiona. I nformation available prior to issuance of the financial statements indicates that it is probable that an assethad been impaired or a liability had been incurred at the date of the financial statements.4 It is implicit in this condition that it must be probable that one or more future events will occur confirming the fact of the loss.b. T he amount of loss can be reasonably estimated.Disclosure of Loss Contingencies9. Disclosure of the nature of an accrual 5 made pursuant to the provisions of paragraph 8, and in some circumstances the amount accrued, may be necessary for the financial statements not to be misleading.10. If no accrual is made for a loss contingency because one or both of the conditions in paragraph 8 are not met, or if an exposure to loss exists in excess of the amount accrued pursuant to the provisions of paragraph 8, disclosure of the contingency shall be made when there is at least a reasonable possibility that a loss or an additional loss may have been incurred.6 The disclosure shall indicate the nature of the contingency and shall give an estimate of the possible loss or range of loss or state that such an estimate cannot be made. Disclosure is not required of a loss contingency involving an unasserted claim or assessment when there has been no manifestation by a potential claimant of an awareness of a possible claim or assessment unless it is considered probable that a claim will be asserted and there is a reasonable possibility that the outcome will be unfavorable.11. After the date of an enterprise's financial statements but before those financial statements are issued, information may become available indicating that an asset was impaired or a liability was incurred after the date of the financial statements or that there is at least a reasonable possibility that an asset was impaired or a liability was incurred after that date. The information may relate to a loss contingency that existed at the date of the financial statements, e.g., an asset that was not insured at the date of the financial statements. On the other hand, the information may relate to a loss contingency that did not exist at the date of the financial statements, e.g., threat of expropriation of assets after the date of the financial statements or the filing for bankruptcy by an enterprise whose debt was guaranteed after the date of the financial statements. In none of the cases cited in this paragraph was an asset impaired or a liability incurred at the date of the financial statements, and the condition for accrual in paragraph 8(a) is, therefore, not met. Disclosure of those kinds of losses or loss contingencies may be necessary, however, to keep the financial statements from being misleading. If disclosure is deemed necessary, the financial statements shall indicate the nature of the loss or loss contingency and give an estimate of the amount or range of loss or possible loss or state that such an estimate cannot be made. Occasionally, in the case of a loss arising after the date of the financial statements where the amount of asset impairment or liability incurrence can be reasonably estimated, disclosure may best be made by supplementing the historical financial statements with pro forma financial data giving effect to the loss as if it had occurred at the date of the financial statements. It may be desirable to present pro forma statements, usually a balance sheet only, in columnar form on the face of the historical financial statements.12. Certain loss contingencies are presently being disclosed in financial statements even though the possibility of loss may be remote. The common characteristic of those contingencies is a guarantee, normally with a right to proceed against an outside party in the event that the guarantor is called upon to satisfy the Copyright © 1975, Financial Accounting Standards Board Not for redistributionguarantee. Examples include (a) guarantees of indebtedness of others, (b) obligations of commercial banks under "standby letters of credit," and (c) guarantees to repurchase receivables (or, in some cases, to repurchase the related property) that have been sold or otherwise assigned. The Board concludes that disclosure of those loss contingencies, and others that in substance have the same characteristic, shall be continued. The disclosure shall include the nature and amount of the guarantee. Consideration should be given to disclosing, if estimable, the value of any recovery that could be expected to result, such as from the guarantor's right to proceed against an outside party.13. This Statement applies to regulated enterprises in accordance with provisions of the Addendum to APB Opinion No. 2, "Accounting for the 'Investment Credit.'" If, in conformity with the Addendum, a regulated enterprise accrues for financial accounting and reporting purposes an estimated loss without regard to the conditions in paragraph 8, the following information shall be disclosed in its financial statements:a) The accounting policy including the nature of the accrual and the basis for estimation.b) The amount of any related "liability" or "asset valuation" account included in each balance sheet presented. General or Unspecified Business Risks14. Some enterprises have in the past accrued so-called "reserves for general contingencies." General or unspecified business risks do not meet the conditions for accrual in paragraph 8, and no accrual for loss shall be made. No disclosure about them is required by this Statement.Appropriation of Retained Earnings15. Some enterprises have classified a portion of retained earnings as "appropriated" for loss contingencies. In some cases, the appropriation has been shown outside the stockholders' equity section of the balance sheet. Appropriation of retained earnings is not prohibited by this Statement provided that it is shown within the stockholders' equity section of the balance sheet and is clearly identified as an appropriation of retained earnings. Costs or losses shall not be charged to an appropriation of retained earnings, and no part of the appropriation shall be transferred to income.Examples of Application of This Statement16. Examples of application of the conditions for accrual of loss contingencies in paragraph 8 and the disclosure requirements in paragraphs 9-11 are presented in Appendix A.Gain Contingencies17. The Board has not reconsidered ARB No. 50 with respect to gain contingencies. Accordingly, the following provisions of paragraphs 3 and 5 of that Bulletin shall continue in effect:a. Contingencies that might result in gains usually are not reflected in the accounts since to do so might be to Copyright © 1975, Financial Accounting Standards Board Not for redistributionrecognize revenue prior to its realization.b. Adequate disclosure shall be made of contingencies that might result in gains, but care shall be exercised toavoid misleading implications as to the likelihood of realization.Other Disclosures18. Paragraph 6 of ARB No. 50 required disclosure of a number of situations including "unused letters of credit, long-term leases, assets pledged as security for loans, pension plans, the existence of cumulative preferred stock dividends in arrears, and commitments such as those for plant acquisition or an obligation to reduce debts, maintain working capital, or restrict dividends." Subsequent Opinions issued by the Accounting Principles Board established more explicit disclosure requirements for a number of those items, i.e., leases (see APB Opinions No. 5 and 31), pension plans (see APB Opinion No. 8), and preferred stock dividend arrearages (see APB Opinion No. 10, paragraph 11(b)).19. Situations of the type described in the preceding paragraph shall continue to be disclosed in financial statements, and this Statement does not alter the present disclosure requirements with respect to those items. Effective Date and Transition20. This Statement shall be effective for fiscal years beginning on or after July 1, 1975, although earlier application is encouraged. A change in accounting principle resulting from compliance with paragraph 8 or 14 of this Statement shall be reported in accordance with APB Opinion No. 20, "Accounting Changes." Accordingly, except in the special circumstances referred to in paragraphs 29-30 of APB Opinion No. 20, the cumulative effect of the change on retained earnings at the beginning of the year in which the change is made shall be included in net income of the year of the change, and the disclosures specified in APB Opinion No. 20 shall be made. Reclassification of an appropriation of retained earnings to comply with paragraph 15 of this Statement shall be made in any financial statements for periods before the effective date of this Statement, or financial summaries or other data derived therefrom, that are presented after the effective date of this Statement.The provisions of this Statement need notbe applied to immaterial items.This Statement was adopted by the unanimous vote of the seven members of the Financial Accounting Standards Board:Marshall S. Armstrong, ChairmanOscar S. GelleinDonald J. KirkArthur L. LitkeRobert E. MaysWalter SchuetzeRobert T. SprouseCopyright © 1975, Financial Accounting Standards Board Not for redistributionAppendix A: EXAMPLES OF APPLICATION OF THIS STATEMENT21. This Appendix contains examples of application of the conditions for accrual of loss contingencies in paragraph 8 and of the disclosure requirements in paragraphs 9-11. Some examples have been included in response to questions raised in letters of comment on the Exposure Draft. It should be recognized that no set of examples can encompass all possible contingencies or circumstances. Accordingly, accrual and disclosure of loss contingencies should be based on an evaluation of the facts in each particular case.Collectibility of Receivables22. The assets of an enterprise may include receivables that arose from credit sales, loans, or other transactions. The conditions under which receivables exist usually involve some degree of uncertainty about their collectibility, in which case a contingency exists as defined in paragraph 1. Losses from uncollectible receivables shall be accrued when both conditions in paragraph 8 are met. Those conditions may be considered in relation to individual receivables or in relation to groups of similar types of receivables. If the conditions are met, accrual shall be made even though the particular receivables that are uncollectible may not be identifiable.23. If, based on available information, it is probable that the enterprise will be unable to collect all amounts due and, therefore, that at the date of its financial statements the net realizable value of the receivables through collection in the ordinary course of business is less than the total amount receivable, the condition in paragraph 8(a) is met because it is probable that an asset has been impaired. Whether the amount of loss can be reasonably estimated (the condition in paragraph 8(b)) will normally depend on, among other things, the experience of the enterprise, information about the ability of individual debtors to pay, and appraisal of the receivables in light of the current economic environment. In the case of an enterprise that has no experience of its own, reference to the experience of other enterprises in the same business may be appropriate. Inability to make a reasonable estimate of the amount of loss from uncollectible receivables (i.e., failure to satisfy the condition in paragraph 8(b)) precludes accrual and may, if there is significant uncertainty as to collection, suggest that the installment method, the cost recovery method, or some other method of revenue recognition be used (see paragraph 12 of APB Opinion No. 10, "Omnibus Opinion—1966"); in addition, the disclosures called for by paragraph 10 of this Statement should be made.Obligations Related to Product Warranties and Product Defects24. A warranty is an obligation incurred in connection with the sale of goods or services that may require further performance by the seller after the sale has taken place. Because of the uncertainty surrounding claims that may be made under warranties, warranty obligations fall within the definition of a contingency in paragraph 1. Losses from warranty obligations shall be accrued when the conditions in paragraph 8 are met. Those conditions may be considered in relation to individual sales made with warranties or in relation to groups of similar types of sales made with warranties. If the conditions are met, accrual shall be made even though the particular parties that will make claims under warranties may not be identifiable.Copyright © 1975, Financial Accounting Standards Board Not for redistribution25. If, based on available information, it is probable that customers will make claims under warranties relating to goods or services that have been sold, the condition in paragraph 8(a) is met at the date of an enterprise's financial statements because it is probable that a liability has been incurred. Satisfaction of the condition in paragraph 8(b) will normally depend on the experience of an enterprise or other information. In the case of an enterprise that has no experience of its own, reference to the experience of other enterprises in the same business may be appropriate. Inability to make a reasonable estimate of the amount of a warranty obligation at the time of sale because of significant uncertainty about possible claims (i.e., failure to satisfy the condition in paragraph 8(b)) precludes accrual and, if the range of possible loss is wide, may raise a question about whether a sale should be recorded prior to expiration of the warranty period or until sufficient experience has been gained to permit a reasonable estimate of the obligation; in addition, the disclosures called for by paragraph 10 of this Statement should be made.26. Obligations other than warranties may arise with respect to products or services that have been sold, for example, claims resulting from injury or damage caused by product defects. If it is probable that claims will arise with respect to products or services that have been sold, accrual for losses may be appropriate. The condition in paragraph 8(a) would be met, for instance, with respect to a drug product or toys that have been sold if a health or safety hazard related to those products is discovered and as a result it is considered probable that liabilities have been incurred. The condition in paragraph 8(b) would be met if experience or other information enables the enterprise to make a reasonable estimate of the loss with respect to the drug product or the toys.Risk of Loss or Damage of Enterprise Property27. At the date of an enterprise's financial statements, it may not be insured against risk of future loss or damage to its property by fire, explosion, or other hazards. The absence of insurance against losses from risks of those types constitutes an existing condition involving uncertainty about the amount and timing of any losses that may occur, in which case a contingency exists as defined in paragraph 1. Uninsured risks may arise in a number of ways, including (a) noninsurance of certain risks or co-insurance or deductible clauses in an insurance contract or (b) insurance through a subsidiary or investee 7 to the extent not reinsured with an independent insurer. Some risks, for all practical purposes, may be noninsurable, and the self-assumption of those risks is mandatory.28. The absence of insurance does not mean that an asset has been impaired or a liability has been incurred at the date of an enterprise's financial statements. Fires, explosions, and other similar events that may cause loss or damage of an enterprise's property are random in their occurrence.8 With respect to events of that type, the condition for accrual in paragraph 8(a) is not satisfied prior to the occurrence of the event because until that time there is no diminution in the value of the property. There is no relationship of those events to the activities of the enterprise prior to their occurrence, and no asset is impaired prior to their occurrence. Further, unlike an insurance company, which has a contractual obligation under policies in force to reimburse insureds for losses, an enterprise can have no such obligation to itself and, hence, no liability.Copyright © 1975, Financial Accounting Standards Board Not for redistributionRisk of Loss from Future Injury to Others, Damage to the Property of Others, and Business Interruption 29. An enterprise may choose not to purchase insurance against risk of loss that may result from injury to others, damage to the property of others, or interruption of its business operations.9 Exposure to risks of those types constitutes an existing condition involving uncertainty about the amount and timing of any losses that may occur, in which case a contingency exists as defined in paragraph 1.30. Mere exposure to risks of those types, however, does not mean that an asset has been impaired or a liability has been incurred. The condition for accrual in paragraph 8(a) is not met with respect to loss that may result from injury to others, damage to the property of others, or business interruption that may occur after the date of an enterprise's financial statements. Losses of those types do not relate to the current or a prior period but rather to the future period in which they occur. Thus, for example, an enterprise with a fleet of vehicles should not accrue for injury to others or damage to the property of others that may be caused by those vehicles in the future even if the amount of those losses may be reasonably estimable. On the other hand, the conditions in paragraph 8 would be met with respect to uninsured losses resulting from injury to others or damage to the property of others that took place prior to the date of the financial statements, even though the enterprise may not become aware of those matters until after that date, if the experience of the enterprise or other information enables it to make a reasonable estimate of the loss that was incurred prior to the date of its financial statements. Write-Down of Operating Assets31. In some cases, the carrying amount of an operating asset not intended for disposal may exceed the amount expected to be recoverable through future use of that asset even though there has been no physical loss or damage of the asset or threat of such loss or damage. For example, changed economic conditions may have made recovery of the carrying amount of a productive facility doubtful. The question of whether, in those cases, it is appropriate to write down the carrying amount of the asset to an amount expected to be recoverable through future operations is not covered by this Statement.Threat of Expropriation32. The threat of expropriation of assets is a contingency within the definition of paragraph 1 because of the uncertainty about its outcome and effect. If information indicates that expropriation is imminent and compensation will be less than the carrying amount of the assets, the condition for accrual in paragraph 8(a) is met. Imminence may be indicated, for example, by public or private declarations of intent by a government to expropriate assets of the enterprise or actual expropriation of assets of other enterprises. Paragraph 8(b) requires that accrual be made only if the amount of loss can be reasonably estimated. If the conditions for accrual are not met, the disclosures specified in paragraph 10 would be made when there is at least a reasonable possibility that an asset has been impaired.Litigation, Claims, and AssessmentsCopyright © 1975, Financial Accounting Standards Board Not for redistribution33. The following factors, among others, must be considered in determining whether accrual and/or disclosure is required with respect to pending or threatened litigation and actual or possible claims and assessments:a. The period in which the underlying cause (i.e., the cause for action) of the pending or threatened litigationor of the actual or possible claim or assessment occurred.b. The degree of probability of an unfavorable outcome.c. The ability to make a reasonable estimate of the amount of loss.34. As a condition for accrual of a loss contingency, paragraph 8(a) requires that information available prior to the issuance of financial statements indicate that it is probable that an asset had been impaired or a liability had been incurred at the date of the financial statements. Accordingly, accrual would clearly be inappropriate for litigation, claims, or assessments whose underlying cause is an event or condition occurring after the date of financial statements but before those financial statements are issued, for example, a suit for damages alleged to have been suffered as a result of an accident that occurred after the date of the financial statements. Disclosure may be required, however, by paragraph 11.35. On the other hand, accrual may be appropriate for litigation, claims, or assessments whose underlying cause is an event occurring on or before the date of an enterprise's financial statements even if the enterprise does not become aware of the existence or possibility of the lawsuit, claim, or assessment until after the date of the financial statements. If those financial statements have not been issued, accrual of a loss related to the litigation, claim, or assessment would be required if the probability of loss is such that the condition in paragraph 8(a) is met and the amount of loss can be reasonably estimated.36. If the underlying cause of the litigation, claim, or assessment is an event occurring before the date of an enterprise's financial statements, the probability of an outcome unfavorable to the enterprise must be assessed to determine whether the condition in paragraph 8(a) is met. Among the factors that should be considered are the nature of the litigation, claim, or assessment, the progress of the case (including progress after the date of the financial statements but before those statements are issued), the opinions or views of legal counsel and other advisers, the experience of the enterprise in similar cases, the experience of other enterprises, and any decision of the enterprise's management as to how the enterprise intends to respond to the lawsuit, claim, or assessment (for example, a decision to contest the case vigorously or a decision to seek an out-of-court settlement). The fact that legal counsel is unable to express an opinion that the outcome will be favorable to the enterprise should not necessarily be interpreted to mean that the condition for accrual of a loss in paragraph 8(a) is met.37. The filing of a suit or formal assertion of a claim or assessment does not automatically indicate that accrual of a loss may be appropriate. The degree of probability of an unfavorable outcome must be assessed. The condition for accrual in paragraph 8(a) would be met if an unfavorable outcome is determined to be probable. If an unfavorable outcome is determined to be reasonably possible but not probable, or if the amount of loss cannot be reasonably estimated, accrual would be inappropriate, but disclosure would be required by paragraph 10 of this Statement.Copyright © 1975, Financial Accounting Standards Board Not for redistribution。

会计英语 常用词

Account 帐户Accounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室Income statement 损益表Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会Statement of cash flow 现金流量表Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系Assets 资产Business entity 企业个体Capital stock 股本Corporation 公司Cost principle 成本原则Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设Inflation 通货膨涨Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量Operating activities 经营活动Owners equity 所有者权益Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设Stockholders 股东Stockholders equity 股东权益Window dressing 门面粉饰Tier1capital一类资本Tier2capital二类资本Totalcreditlimit整体信用限额Totalcurrentassets流动资产总额Trade-off协定Tradecompanies贸易企业Tradecreditors应付账款Tradecredit商业信用Tradecycletimes商业循环周期Tradecycle商业循环Tradedebtors贸易债权人Tradedebt应收账款TradeIndemnity贸易赔偿Tradereferences贸易参考Tradingoutlook交易概况Tradingprofit营业利润Traditionalcashflow传统现金流量TripleA三AUCP跟单信用证统一惯例Uncovereddividend未保障的股利UniformCustoms&Practice跟单信用证统一惯例Unpaidinvoices未付款发票Unsecuredcreditors未担保的债权人Usefulnessofliquidityratios流动性比率的作用Usesofcash现金的使用Usingbankriskinformation使用银行风险信息Usingfinancialassessments使用财务评估Usingratios财务比率的运用Usingretention-of-titleclauses使用所有权保留条款V aluechain价值链V alueofZscoresZ值模型的价值V ariablecosts变动成本V ariableinterest可变利息V arietyoffinancialratios财务比率的种类V ettingprocedures审查程序V olatitlerevenuedynamic收益波动V olumeofsales销售量Warningsignsofcreditrisk信用风险的警示Workingassets营运资产Workingcapitalchanges营运资本变化额Workingcapitalmanagement营运资本管理workingcapitalratios营运资本比率workingcapital营运资本Write-downs资产减值Write-offs勾销ZscoreassessmentsZ值评估zscoremodelsz值模型Zscoresz值ZscoringZ值评分系统2Mmethod2M法3Mmethod3M法Ratioanalysis比率分析Ratioanalystweaknesses~L率分析的缺陷Realinsolvency真实破产Realizationconcept实现原则Realsalesgrowth实际销售收入增长率Receivables应收账款Recession衰退Reducingdebtors冲减应收账款Reducingprofits冲减利润Reducingprovisions冲减准备金Reducingreportedprofits冲减账面利润Reducingstocks减少存货RegistrarofCompanies企业监管局Regulatoryrisk监管风险Releasingprovisions冲回准备金Relocationexpenses费用再分配Reminderletters催缴单Repaymentondemandclause即期偿还条款Replacementofprincipal偿还本金Reportofchairman总裁/董事长报告Reserveaccounting准备金核算Residualcashflows剩余现金流量Restrictingbaddebts限制坏账Restrictionsonsecuredborrowing担保借款限制Retention-of-titleclauses所有权保留条款Revenues总收入Risk-reward风险回报Risk-weightedassets风险加权资产Riskanalysisreports风险分析报告Riskandbanks风险与银行Riskandcompanies风险与企业RiskandReturn风险与回报Riskcapital风险资本ROCE资本收益率Romaplaclauses“一手交钱一手交货”条款Sales销售额Secondaryratios分解比率Securedassets担保资产Securedcreditors有担保债权人Securedloans担保贷款Securemethodsofpayment付款的担保方式SecuritiesandExchangeCommission(美国)证券交易委员会Securitygeneralprinc iples担保的一般原则Securityguarantees抵押担保Securityofpayment付款担保Segmentation细分Settingandpolicingcreditlimits信用限额的设定与政策制定Settlementdiscount(提前)结算折扣Settlementterms结算条款Shareprice股价Short-termborrowing短期借款Short-termcreditors短期负债Short-termism短期化SIC常务诠释委员会Short-termliabilities短期债务Significanceofworkingcapital营运资金的重要性Singlecreditcustomer单一信用客户Singleratioanalysis单一比率分析Sizeofcreditrisk信用风险的大小Slowstockturnover较低的存货周转率Sourcesofassessments评估信息来源Sourcesofcreditinformation信用信息来源Sourcesofrisk风险来源Sovereignrating主权评级Specialistagencies专业机构Specificdebtissue特别债券发行Speculativegrades投机性评级Speculative投机性Splitrating分割评级Spotrate现价(即期比率)Spreadsheets电子数据表Staffredundancies员工遣散费Standard&Poor's标准普尔StandardandPoor标准普尔Standardsecurityclauses标准担保条款Standbycredits备用信用证StandingInterpretationsCommittee证券交易委员会Standingstartingcreditlimits持续更新信用限额Statisticalanalys is统计分析Statisticaltechniques统计技巧Statusreports(企业)状况报告Stocks股票Stockvaluations存货核算Straightlinedepreciationmethod直线折旧法Strategicpositioning战略定位Suplusassets盈余资产Suplusrating盈余评级Supplierpower供应商的力量Supplychain供应链Supportrating支持评级Swapagreement换合约Swaps互换SWOTanalysisSWOT分析Symptomsoffailurequestionnaires企业破产征兆调查表Takeovers收购Taxpayments税务支付Technicalinsolvency技术破产Technologyandchange技术进步Termloan定期贷款Termofborrowing借款期限Thirdpartyguarantees第三方担保Measurementandjudgment计量与判断Measuringrisk风险计量Medium-termloan中期贷款Microcomputermodelling计算机建模Minimumcurrentratiorequirement最低流动比率要求Minimumleverageratio最低举债比率Minimumnet-worthrequirement最低净值要求Minimumnetworth最低净值Minimumriskassetratio最低风险资产比率Monitoringactivity监管活动Monitoringcredit信用监控Monitoringcustomercreditlimits监管客户信贷限额Monitoringrisks监管风险Monitoringtotalcreditlimits监管全部信贷限额Monthlyreports月报Moody'sdebtrating穆迪债券评级Mortgage抵押mpr…ovingbalancesheet改善资产负债表Multiplediscriminateanalysis多元分析Nationaldebt国家债务NCI无信贷间隔天数Near-cashassets近似于现金的资产Negativecashflow负现金流量Negativenetcashflow负净现金流量Negativeoperationalcashflows负的经营性现金流量Negativepledge限制抵押Netbookvalue净账面价值Netcashflow净现金流量Networthtest净值测试Newentrants新的市场进人者Nocreditinterval无信贷间隔天数Non-cashitems非现金项目Non-corebusiness非核心业务Non-operationalitems非经营性项目Obtainingpayment获得支付One-manrule一人原则Openaccountterms无担保条款Operatingleases经营租赁Operatingprofit营业利润Operationalcashflow营性现金流量Operationalflexibility~营弹性Optimalcredit最佳信贷Ordercycle订货环节Ordinarydividendpayments普通股股利支付Organizationofcreditactivities信贷活动的组织Over-trading过度交易Overduepayments逾期支付Overviewofaccounts财务报表概览Parentcompany母公司PA T税后利润Paymentinadvance提前付款Paymentobligations付款义务Paymentrecords付款记录Paymentscore还款评分PBIT息税前利润PBT息后税前利润Percentagechange百分比变动Performancebonds履约保证Personalguarantees个人担保Planningsystems计划系统Pledge典押Points-scoringsystem评分系统Policysetting政策制定Politicalrisk政治风险Potentialbaddebt潜在坏账Potentialcreditrisk潜在信用风险Potentialvalue潜在价值Predictingcorporatefailures企业破产预测Preferencedividends优先股股息Preferredstockholders优先股股东Preliminaryassessment预备评估Premiums溢价Primaryratios基础比率Priorchargecapital优先偿付资本Prioritycashflows优先性现金流量Priorityforcreditors债权人的清偿顺序Prioritypayments优先支付Productlifecycle产品生命周期Productmarketanalysis产品市场分析Productrange产品范围Products产品Professionalfees专业费用Profitabilitymanagement盈利能力管理Profitabilityratios盈利能力比率Profitability盈利能力Profitandlossaccount损益账户Profitmargin利润率Profit利润Promissorynotes本票Propertyvalues所有权价值Providersofcredit授信者Provisionaccounting准备金会计处理Prudenceconcept谨慎原则Publicinformation公共信息Publicrelations公共关系Purposeofcreditratings信用评级的目的Purposeofratios计算比率的目的Qualitativecovenants定性条款Quantitativecovenants定量条款Querycontrol质疑控制Quickratio速动比率Ratingexercise评级实践Ratingprocessforacompany企业评级程序Implieddebtrating隐含债务评级Importanceofcreditcontrol信贷控制的重要性Improvedproducts改进的产品In-housecreditratings内部信用评级Incomebonds收入债券Incomestatement损益表Increasingprofits提高利润Increasingreportedprofits提高账面利润Indemnityclause赔偿条款Indicatorsofcreditdeterioration信用恶化征兆Indirectloss间接损失Individualcredittransactions个人信用交易Individualrating个体评级Industrialreports行业报告Industrialunrest行业动荡Industrylimit行业限额Industryriskanalysis行业风险分析Industryrisk行业风险Inflow现金流入Informationinfinancialstatements财务报表中的信息Inhouseassessment内部评估Inhousecreditanalysis内部信用分析Inhousecreditassessments内部信用评估Inhousecreditratings内部信用评级Initialpayment初始支付Insolvencies破产Institutionalinvestors机构投资者Insureddebt投保债务Intangiblefixedasset无形固定资产Inter-companycomparisons企业间比较Inter-companyloans企业间借款Interestcost利息成本Interestcoverratio利息保障倍数Interestcovertest利息保障倍数测试Interestholiday免息期Interestpayments利息支付Interestrates利率Interest利息Interimstatements中报(中期报表)Internalassessmentmethods内部评估方法Internalfinancingratio内部融资率InternalRevenueService美国国税局InternationalAccountingStandards(IAS)国际会计准则InternationalAccountingStandardsCommittee国际会计准则委员会InternationalChamberofCommerce国际商会Internationalcreditratings国际信用评级InternationalFactoringAssociation国际代理商协会Internationalsettlements国际结算Inventory存货Inverseofcurrentratio反转流动比率Investmentanalysts投资分析人员Investmentpolicy投资政策Investmentrisk投资风险Investmentspending投资支出Invoicediscounting发票贴现Issueddebtcapital发行债务资本Issueofbonds债券的发行Junkbondstatus垃圾债券状况Just-in-timesystem(JIT)适时系统Keycashflowratios主要现金流量指标Laborunrest劳动力市场动荡Large.Scaleborrower大额借贷者Legalguarantee法律担保Legalinsolvency法律破产Lendingagreements贷款合约Lendingcovenants贷款保证契约Lendingdecisions贷款决策Lendingproposals贷款申请Lendingproposition贷款申请Lendingtransactions贷款交易Lettersofcredit信用证Leverage财务杠杆率LIBOR伦敦同业拆借利率Lien留置Liquidassets速动资产Liquidationexpenses清算费Liquidation清算Liquidityandworkingcapital流动性与营运资金Liquidityratios流动比率Liquidityrun流动性危机Liquidityshortage流动性短缺Liquidity流动性Loancovenants贷款合约Loanguarantees贷款担保Loanprincipalrepayments贷款本金偿还Loanprincipal贷款本金Loanreview贷款审查LondonInter-bankOfferedRate伦敦同业拆借利率Long-termfunding长期融资Long-termrisk长期风险Long…termdebt长期负债Management管理层Marginallending边际贷款Marginaltradecredit边际交易信贷Marketing市场营销Marketsurveys市场调查Markets市场Matchingconcept配比原则Materialadverse-changeclause重大不利变动条款Maximumleveragelevel最高财务杠杆率限制Electronicdatainterchange(EDI)电子数据交换Environmentalfactors环境因素Equitycapital权益资本Equityfinance权益融资Equitystake股权Eucountries欧盟国家Eudirectives欧盟法规Eulaw欧盟法律Eurobonds欧洲债券Europeanparliament欧洲议会EuropeanUnion欧盟Evergreenloan常年贷款Exceptionalitem例外项目Excessivecapitalcommitments过多的资本承付款项Exchange-controlregulations外汇管制条例Exchangecontrols外汇管制Exhaustmethod排空法Existingcompetitors现有竞争对手Existingdebt未清偿债务Exportcreditagencies出口信贷代理机构Exportcreditinsurance出口信贷保险Exportfactoring出口代理Exportsales出口额ExportsCreditGuaranteeDepartment出口信贷担保局Extendingcredit信贷展期Externalagency外部机构Externalassessmentmethods外部评估方式Externalassessments外部评估Externalinformationsources外部信息来源Extraordinaryitems非经常性项目Extras附加条件Facilityaccount便利账户Factoringdebts代理收账Factoringdiscounting代理折扣Factoring代理FactorsChainInternational国际代理连锁Failurepredictionscores财务恶化预测分值FASB(美国)财务会计准则委员会Faultycreditanalysis破产信用分析Fees费用Finance,workingcapital为营运资金融资Finance,newbusinessventures为新兴业务融资Finance,repayexistingdebt为偿还现有债务融资Financialassessment财务评估Financialcashflows融资性现金流量Financialcollapse财务危机Financialflexibility财务弹性Financialforecast财务预测Financialinstability财务的不稳定性Financialratinganalysis财务评级分析Financialratios财务比率Financialriskratios财务风险比率Financialrisk财务风险FitchIBCAratings惠誉评级FitchIBCA惠誉评级Fixedassets固定资产Fixedchargecover固定费用保障倍数Fixedcharge固定费用Fixedcosts固定成本Floatingassets浮动资产Floatingcharge浮动抵押Floorplanning底价协议Focus聚焦Forcedsalerisk强制出售风险Foreignexchangemarkets外汇市场Forfaiting福费廷Formalcreditrating正式信用评级Forwardrateagreements远期利率协议FRAs远期利率协议Fundmanagers基金经理Fxtransaction外汇交易GAAP公认会计准则Gearing财务杠杆率Geographicalspreadofmarkets市场的地理扩展Globaltarget全球目标Goingconcernconcept持续经营原则Goodlending优质贷款Goodtimes良好时期Governmentagencies政府机构Governmentinterference政府干预Grossincome总收入Guaranteedloans担保贷款Guaranteeofpayment支付担保Guarantees担保High-riskloan高风险贷款High-valueloan高价值贷款Highcreditquality高信贷质量Highcreditrisks高信贷风险Highdefaultrisk高违约风险Highinterestrates高利率Highlyspeculative高度投机Highriskregions高风险区域Historicalaccounting历史会计处理Historicalcost历史成本IASC国际会计准则委员会IAS国际会计准则IBTT息税前利润ICE优质贷款原则Idealliquidityratios理想的流动性比率Iimprovingreportedassetvalues改善资产账面价值Creditdeterioration信用恶化Creditexposure信用敞口Creditgrantingprocess授信程序Creditinformationagency信用信息机构Creditinformation信用信息Creditinsuranceadvantages信贷保险的优势Creditinsurancebrokers信贷保险经纪人Creditinsurancelimitations信贷保险的局限Creditinsurance信贷保险Creditlimitsforcurrencyblocs货币集团国家信贷限额Creditlimitsforindividualcountries国家信贷限额Creditlimits信贷限额Creditmanagement信贷管理Creditmanagers信贷经理Creditmonitoring信贷监控Creditnotes欠款单据Creditordays应付账款天数Creditperiod信用期Creditplanning信用计划Creditpolicyissues信用政策发布Creditpolicy信用政策Creditproposals信用申请Creditprotection信贷保护Creditquality信贷质量Creditratingagencies信用评级机构Creditratingprocess信用评级程序Creditratingsystem信用评级系统Creditrating信用评级Creditreferenceagencies信用评级机构Creditreference信用咨询Creditriskassessment信用风险评估Creditriskexposure信用风险敞口Creditriskinsurance信用风险保险Creditrisk.Individualcustomers个体信用风险Creditrisk:bankcredit信用风险:银行信用Creditrisk:tradecredit信用风险:商业信用Creditrisk信用风险Creditscoringmodel信用评分模型Creditscoringsystem信用评分系统Creditscoring信用风险评分Creditsqueeze信贷压缩Credittakenratio受信比率Creditterms信贷条款Creditutilizationreports信贷利用报告Creditvetting信用审查Creditwatch信用观察Creditworthiness信誉Cross-defaultclause交叉违约条款Currencyrisk货币风险Currentassets流动资产Currentdebts流动负债Currentratiorequirement流动比率要求Currentratios流动比率Customercare客户关注Customercreditratings客户信用评级Customerliaison客户联络Customerrisks客户风险Cut-offscores及格线Cycleofcreditmonitoring信用监督循环Cyclicalbusiness周期性行业Dailyoperatingexpenses经营费用Day…ssalesoutstanding收回应收账款的平均天数Debentures债券Debtcapital债务资本Debtcollectionagency债务托收机构Debtissuer债券发行人Debtor'sassets债权人的资产Debtordays应收账款天数Debtprotectionlevels债券保护级别Debtratio负债比率Debtsecurities债券Debtserviceratio还债率Default违约Deferredpayments延期付款Definitionofleverage财务杠杆率定义Depositingmoney储蓄资金Depositlimits储蓄限额Depreciationpolicies折旧政策Depreciation折旧Developmentbudget研发预算Differentiation差别化Directloss直接损失Directorssalaries董事薪酬Discretionarycashflows自决性现金流量Discretionaryoutflows自决性现金流出Distributioncosts分销成本Dividendcover股息保障倍数Dividendpayoutratio股息支付率Dividends股利Documentarycredit跟单信用证DSO应收账款的平均回收期Durationofcreditrisk信用风险期Easternbloccountries东方集团国家EBITDA扣除利息、税收、折旧和摊销之前的收益ECGD出口信贷担保局Economicconditions经济环境Economiccycles经济周期Economicdepression经济萧条Economicgrowth经济增长Economicrisk经济风险Capitalizinginterestcosts利息成本资本化Capitalstrength资本实力Capitalstructure资本结构Cascadeeffect瀑布效应Cash-in-advance预付现金Cashassets现金资产Cashcollectiontargets现金托收目标Cashcycleratios现金循环周期比率Cashcycletimes现金循环周期时间Cashcycle现金循环周期Cashdeposit现金储蓄Cashflowadjustments现金流调整Cashflowanalysis现金流量分析Cashflowcrisis现金流危机Cashflowcycle现金流量周期Cashflowforecasts现金流量预测Cashflowlending现金流贷出Cashflowprofile现金流概况Cashflowprojections现金流预测Cashflowstatements现金流量表Cashflows现金流量Cashposition现金头寸CashpositiveJE现金流量Cashrichcompanies现金充足的企业Cashsurplus现金盈余Cashtank现金水槽Categorizedcashflow现金流量分类CEO首席执行官CE优质贷款原则Chairman董事长,总裁Chapter11rules第十一章条款Chargedassets抵押资产Charge抵押Chiefexecutiveofficer首席执行官Collateralsecurity抵押证券Collectingpayments收取付款Collectionactivitv收款活动Collectioncycle收款环节Collectionprocedures收款程序Collectivecreditrisks集合信用风险Comfortableliquiditypositi9n适当的流动性水平Commercialmortgage商业抵押Commercialpaper商业票据Commission佣金Commitmentfees承诺费Commonstockholders普通股股东Commonstock普通股Companyanditsindustry企业与所处行业Companyassets企业资产Companyliabilities企业负债Companyloans企业借款Competitiveadvantage竞争优势Competitiveforces竞争力Competitiveproducts竞争产品Complaintprocedures申诉程序Computerizedcreditinformation计算机化信用信息Computerizeddiaries计算机化日志Confirmedletterofcredit承兑信用证Confirmedlettersofcredit保兑信用证Confirmingbank确认银行Conservatismconcept谨慎原则Consistencyconcept一贯性原则Consolidatedaccounts合并报表Consolidatedbalancesheets合并资产负债表Contingentliabilities或有负债Continuingsecurityclause连续抵押条款Contractualpayments合同规定支出Controllimits控制限度Controllingcreditrisk控制信用风险Controllingcredit控制信贷Controlofcreditactivities信用活动控制Corporatecreditanalysis企业信用分析Corporatecreditcontroller企业信用控制人员Corporatecreditriskanalysis企业信用风险分析Corporatecustomer企业客户Corporatefailurepredictionmodels企业破产预测模型Corporatelending企业贷款Costleadership成本领先型Costofsales销售成本Costs成本Countrylimit国家限额Countryrisk国家风险Courtjudgments法院判决Covenants保证契约Covenant贷款保证契约Creativeaccounting寻机性会计Creditanalysisofcustomers客户信用分析Creditanalysisofsuppliers供应商的信用分析Creditanalysisonbanks银行信用分析Creditanalysis信用分析Creditanalysts信用分析Creditassessment信用评估Creditbureaureports信用咨询公司报告Creditbureaux信用机构Creditcontrolactivities信贷控制活动Creditcontrollers信贷控制人员Creditcontrolperformancereports信贷控制绩效报告Creditcontrol信贷控制Creditcycle信用循环Creditdecisions信贷决策Accountingconvention会计惯例Accountingforacquisitions购并的会计处理Accountingfordebtors应收账款核算Accountingfordepreciation折旧核算Accountingforforeigncurrencies外汇核算Accountingforgoodwill商誉核算Accountingforstocks存货核算Accountingpolicies会计政策Accountingstandards会计准则Accrualsconcept权责发生原则Achievingcreditcontrol实现信用控制Acidtestratio酸性测试比率Actualcashflow实际现金流量Adjustingcompanyprofits企业利润调整Advancepaymentguarantee提前偿还保金Adversetrading不利交易Advertisingbudget广告预算Advisingbank通告银行Ageanalysis账龄分析Ageddebtorsanalysis逾期账款分析Ageddebtors…exceptionreport逾期应收款的特殊报告Ageddebtors…exceptionreport逾期账款特别报告Ageddebtors…report逾期应收款报告Ageddebtors…report逾期账款报告All—moniesclause全额支付条款Amortization摊销Analyticalquestionnaire调查表分析Analyticalskills分析技巧Analyzingfinancialrisk财务风险分析Analyzingfinancialstatements财务报表分析Analyzingliquidity流动性分析Analyzingprofitability盈利能力分析Analyzingworkingcapital营运资本分析Annualexpenditure年度支出Anticipatingfutureincome预估未来收入Areasoffinancialratios财务比率分析的对象Articlesofincorporation合并条款AscoresA值Asiancrisis亚洲(金融)危机Assessingcompanies企业评估Assessingcountryrisk国家风险评估Assessingcreditrisks信用风险评估Assessingstrategicpower战略地位评估Assessmentofbanks银行的评估Assetconversionlending资产转换贷款Assetprotectionlending资产担保贷款Assetsale资产出售Assets资产Assetturnover资产周转率AssociationofBritishFactorsandDiscounters英国代理人与贴现商协会Auditor'sreport审计报告A val物权担保Baddebtlevel坏账等级Baddebtrisk坏账风险Baddebtsperformance坏账发生情况Baddebt坏账Badloans坏账Balancesheetstructure资产负债表结构Balancesheet资产负债表Bankcredit银行信贷Bankfailures银行破产Bankloans.A vailability银行贷款的可获得性Bankruptcycode破产法Bankruptcypetition破产申请书Bankruptcy破产Bankstatusreports银行状况报告BasleAgreement《巴塞尔协议》Basleagreement塞尔协议Behavorialscoring行为评分Billofexchange汇票Billoflading提单BISagreement国际清算银行协定BIS国际清算银行Bluechip蓝筹股Bonds债券Bookreceivables账面应收账款Borrowingmoney借人资金Borrowingproposition借款申请Breakthroughproducts创新产品Budgets预算Buildingcompanyprofiles勾画企业轮廓Bureaux(信用咨询)公司Businessdevelopmentloan商业开发贷款Businessfailure破产Businessplan经营计划Businessrisk经营风险Buyercredits买方信贷Buyerpower购买方力量Buyerrisks买方风险CAMPARI优质贷款原则Canonsoflending贷款原则Capex资本支出Capitaladequacyrules资本充足性原则Capitaladequacy资本充足性Capitalcommitments资本承付款项Capitalexpenditure资本支出Capitalfunding资本融资Capitalinvestment资本投资Capitalizationofinterest利息资本化Capitalizingdevelopmentcosts研发费用资本化Capitalizingdevelopmentexpenditures研发费用资本化。

国际业务常用英语词汇

跟单结算及国际保函信用证Documentary credit跟单信用证Back to back credit背对背信用证Transferable credit可转让信用证Un-transferable credit不可转让信用证Red clause credit红条款信用证Revolving credit循环信用证Standby letter of credit备用信用证Negotiation credit议付信用证Acceptance credit承兑信用证Payment credit付款信用证Irrevocable credit不可撤销信用证Payment credit付款信用证Deferred payment credit延期付款信用证Confirmed credit保兑信用证Usance credit payable at sight假远期信用证Commercial contract商务合同Importer进口商Exporter出口商ApplicantxxBeneficiary受益人Opening bank/issuing bank开证行Advising bank通知行Reimbursing bank偿付行Presenting bank交单行Confirming bank保兑行Negotiating bank议付行Accepting bank承兑行Drawee bank付款行Freely negotiable自由议付Restricted negotiable限制议付Cumulative可累计Non-cumulative不可累计Deferred payment延期付款Discounting贴现Acceptance承兑Negotiation议付Discrepancies不符点Presentation date交单日期Period for presentation of documents交单期限托收Collection托收Collecting bank代收行Remitting bank托收行Principal委托人Drawee付款人Clean collection光票托收Documentary collection跟单托收Outward collection出口托收Collection instruction托收指示Collection order托收指令Inward collection进口代收Financial documents金融单据Commercial documents商业单据Documents against acceptance (D/A)承兑交单Documents against payment (D/P)付款交单Documents against payment at sight (D/P at sight)即期付款交单Documents against payment of usance bill远期付款交单Commercial invoice 商业发票Customs invoicexx发票Consular领事发票Pro forma invoice形式发票Insurance policy保险单Transport documents运输单据Bill of exchange/draft汇票Usance bill远期汇票Packing list装箱单Weight list重量单Quantity certificate数量单Certificate of origin原产地证明Certificate of quality品质证明书Bill of lading提单Blank back bill of lading/short form bill of lading背面空白/ 简式提单Charter party bill of lading租船提单Combined transport bill of lading多式联运提单Container bill of lading集装箱提单Airway bill空运单Postal receipt邮包收据Cargo receipt货物收据其它Banking charges银行费用Presentation of documents提示单据Reimbursement/claim instructions索汇路线Payment付款Advice of payment付款通知Acceptance承兑Carrier承运人Consignee收货人Shipping mark唛头Shipment date装运日Discrepancy不符点Freight charge运费Freight payable at destination运费预付至Correspondent bank代理行Partial shipment分批装运Transshipment转运Port of loading装货港Port of discharge卸货港Price terms价格条款Release documents against payment付款赎单Release documents against acceptance承兑赎单EXW(ex works)工厂交货价FCA( free carrier)货交承运人价FAS(free alongside ship)装运港船边交货价FOB(free on board)装运港船上交货价CFR(cost and freight)成本加运费价CIF(cost, insurance and freight)成本、保险费加运费价CPT(carriage paid to)运费付至……价CIP(carriage and insurance paid to)运费、保险费付至……价DAF(delivered at frontier)边境交货价DES( delivered ex ship)目的港船上交货价DEQ(delivered ex quay)目的港码头交货价DDU(delivered duty unpaid)未完税交货价DDP(delivered duty paid)完税交货价Tender guarantee/bid bond guarantee投标保函Performance guarantee履约保函Advance payment guarantee预付款保函Warranty guarantee质量保函Retention money guarantee留滞金保函Payment guarantee付款保函Financial standby letter of credit融资备用信用证Counter guarantee反担保函Principal被担保人Guarantor担保人Written statement书面声明Multiple drawing多次索赔Claims under a bank guarantee保函的索赔Place of jurisdiction司法管辖地Commission on bond保函佣金外汇资金Remittance; funds transfer汇款Outward remittance汇出汇款Inward remittance汇入汇款TELEX电传CABLE,TELEGRAM电报Draft票汇Mail transfer信汇Remitter汇款xxPayee or Beneficiary收款人Remitting bank汇出行Receiving/Paying bank汇入/解付行Intermediary bank中间行Drawee bank汇票付款行Issue of draft汇票的签发Reimbursement of drafts汇票的索偿Clearing清算Trade date交易日Reference date参考日Value date起息日Maturity date/Expiry date到期日Basis point基点Buyer’s market买方市场Purchase and sale of foreign exchange结售汇Foreign exchange surrender结汇Spot即期Forward远期Current account经常项目Current account convertibility经常项目可兑换Managed floating exchange rate 有管理的浮动汇率Pegged exchange rate钉住汇率Real effective exchange rate实际有效汇率Position头寸Term structure期限结构Capital account资本项目Interest-bearing asset生息资产Foreign direct investment外国直接投资CHIPS (Clearing House Inter-bank Payment System)同业支付清算系统Closing price收盘价Extension展期Fixed exchange rate固定汇率Floating exchange rate浮动汇率Premium升水Discount贴水Financial derivative instruments金融衍生工具Futures期货Option期权Option trading期权的交易Swap掉期In the Money溢价期权At the Money平价期权Out of the Money折价期权Put option看跌期权Call option看涨期权Long (buyer)买方Short (seller)卖方Position买卖角色Long call买入看涨期权Short call卖出看涨期权Long put买入看跌期权Short put卖出看跌期权Out-Of-Money不执行(期权)Interest rate lap利率上限Interest rate floor利率下限Relative value相对价值Pay swap支付互换Option contract期权合约American style option美式期权European style option欧式期权The strike price/the exercise price执行价格Hedge对冲Dual currency deposit双币存款USD/CNY linked deposit美元/人民币挂钩产品Interest rate derivatives利率衍生产品Interest rate option利率期权Structured interest rate products结构性利率产品To hedge currency exposures对冲货币敞口Speculate投机Yield enhancement products增值产品Interest basis计息方式Principal amount本金Principal guaranteed本金担保Principal guaranteed deposit本金担保存款Spot reference即期参考汇率Short-term view products短期产品Hedge against套期保值Exchange-rate regime汇率机制Deposit account定期存款账户Cheque account支票账户Clearing bank清算银行Foreign currency (exchange) reserve外汇储备Devaluation货币贬值Revaluation货币升值International balance of payment国际收支Cross rate/Arbitrage rate套汇汇率Foreign exchange fluctuation外汇波动信贷基本词汇(包括会计)Accounting convention会计惯例Accounting for acquisitions购并的会计处理Accounting for debtors应收账款核算Accounting for depreciation折旧核算Accounting for foreign currencies外汇核算Accounting for goodwill商誉核算Accounting for stocks存货核算Accounting policies会计政策Accounting standards会计准则Accruals concept权责发生原则Achieving credit control实现信用控制Acid test ratio酸性测试比率Actual cash flow实际现金流量Advance payment guarantee提前偿还保金Adverse trading不利交易Advertising budget广告预算Advising bank通告银行Age analysis账龄分析Aged debtors analysis逾期账款分析Aged debtors’report逾期应收款报告Aged debtors’exception report逾期应收款的特殊报告All—monies clause全额支付条款Amortization摊销Analytical questionnaire调查表分析Analytical skills分析技巧Analyzing financial risk财务风险分析Analyzing financial statements财务报表分析Analyzing liquidity流动性分析Analyzing profitability盈利能力分析Analyzing working capital营运资本分析Articles of incorporation合并条款Asian cris亚洲(金融)危机Assessing country risk国家风险评估Assessing credit risks信用风险评估Assessing strategic power战略地位评估Assessment of banks银行的评估Asset conversion lending资产转换贷款Asset protection lending资产担保贷款Asset sale 资产出售Asset turnover资产周转率Assets资产Association of British Factors and Discounters英国代理人与贴现商协会Auditor's report审计报告Aval物权担保Bad debt坏账Bad debt level坏账等级Bad debt risk坏账风险Bad debts performance坏账发生情况Bad loans坏账Balance sheet资产负债表Balance sheet structure资产负债表结构Bank credit银行信贷Bank failures银行破产Bank loans.availability银行贷款的可获得性Bank status reports银行状况报告Bankruptcy破产Bankruptcy code破产法Bankruptcy petion破产申请书Basle agreement塞尔协议Basle Agreement《巴塞尔协议》Behavioral scoring行为评分Bill of exchange汇票Bill of lading提单BIS (Bank for International Settlements)国际清算银行BIS agreement国际清算银行协定Blue chip蓝筹股Borrowing money借人资金Borrowing proposition借款申请Breakthrough products创新产品Budgets预算Business development loan商业开发贷款Business failure破产Business plan经营计划Business risk经营风险Buyer credits买方信贷Buyer power购买方力量Buyer risks买方风险CAMPARI优质贷款原则Canons of lending贷款原则Capital adequacy资本充足性Capital adequacy rules资本充足性原则Capital expenditure (Capex)资本支出Capital funding资本融资Capital investment资本投资Capital strength资本实力Capital structure资本结构Capitalization of interest利息资本化Capitalizing R&D costs/expenditures研发费用资本化Capitalizing interest costs利息成本资本化Cascade effect瀑布效应Cash assets现金资产Cash collection targets现金托收目标Cash cycle现金循环周期Cash cycle ratios现金循环周期比率Cash cycle times现金循环周期时间Cash deposit现金储蓄Cash flows现金流量Cash flow adjustments现金流调整Cash flow analysis现金流量分析Cash flow cris现金流危机Cash flow cycle现金流量周期Cash flow forecasts/projections现金流量预测Cash flow statements现金流量表Cash position现金头寸Cash positive JE现金流量Cash tank现金水槽Cash-in-advance预付现金Categorized cash flow现金流量分类CE优质贷款原则CEO首席执行官Chairman董事长,总裁Chapter 11 rules第十一章条款Charge抵押Charged assets抵押资产Chief executive officer首席执行官Collateral security抵押证券Collecting payments收取付款Collection activity收款活动Collection cycle收款环节Collection procedures收款程序Collective credit risks集合信用风险Comfortable liquidity position适当的流动性水平Commercial mortgage商业抵押Commercial paper商业票据Commission佣金Commitment fees承诺费Common stock普通股Common stockholders普通股股东Company and its industry企业与所处行业Company assets企业资产Company liabilities企业负债Company loans企业借款Competive advantage竞争优势Competive forces竞争力Competive products竞争产品Complaint procedures申诉程序Computerized credit information计算机化信用信息Computerized diaries计算机化日志Confirming bank确认银行Conservatism concept谨慎原则Consistency concept一贯性原则Consolidated accounts合并报表Consolidated balance sheets合并资产负债表Contingent liabilities或有负债Continuing security clause连续抵押条款Contractual payments合同规定支出Control limits控制限度Control of credit activities信用活动控制Controlling credit控制信贷Controlling credit risk控制信用风险Corporate banking公司业务Corporate credit analysis企业信用分析Corporate credit controller企业信用控制人员Corporate credit risk analysis企业信用风险分析Corporate customer企业客户Corporate failure prediction models企业破产预测模型Corporate lending企业贷款Cost leadership成本领先型Cost of sales销售成本Costs成本Country limit国家限额Country risk国家风险Court judgments法院判决Covenant贷款保证xxCovenants保证xxCreative accounting寻机性会计Credit analysis信用分析Credit analysis of customers客户信用分析Credit analysis of suppliers供应商的信用分析Credit analysis on banks银行信用分析Credit assessment信用评估Credit bureau信用机构Credit control信贷控制Credit control activities信贷控制活动Credit controllers信贷控制人员Credit cover信用风险担保Credit cycle信用循环Credit decisions信贷决策Credit deterioration信用恶化Credit exposure信用敞口Credit granting process授信程序Credit information信用信息Credit information agency信用信息机构Credit insurance信贷保险Credit insurance advantages信贷保险的优势Credit insurance brokers信贷保险经纪人Credit insurance limitations信贷保险的局限Credit limits信贷限额Credit limits for currency blocs货币集团国家信贷限额Credit limits for individual countries国家信贷限额Credit line授信额度Credit management信贷管理Credit managers信贷经理Credit monitoring信贷监控Credit notes欠款单据Credit period信用期Credit policy信用政策Credit policy issues信用政策发布Credit proposals信用申请Credit protection信贷保护Credit quality信贷质量Credit rating信用评级Credit reference agencies信用评级机构Credit risk信用风险Credit risk assessment信用风险评估Credit risk exposure信用风险敞口Credit risk insurance信用风险保险Credit risk:trade credit信用风险:商业信用Credit scoring信用风险评分Credit scoring model信用评分模型Credit scoring system信用评分系统Credit squeeze信贷压缩Credit taken ratio受信比率Credit terms信贷条款Credit utilization reports信贷利用报告Credit vetting信用审查Credit watch信用观察Credit worthiness信誉Creditor days应付账款天数Cross-default clause交叉违约条款Currency risk货币风险Current assets流动资产Current debts流动负债Current ratio requirement流动比率要求Current ratios流动比率Customer care客户关注Customer credit ratings客户信用评级Customer liaison客户联络Customer risks客户风险Cut-off scores及格线Cycle of credit monitoring信用监督循环Cyclical business周期性行业Daily operating expenses经营费用Day’s sales outstanding收回应收账款的平均天数Debentures债券Debt capital债务资本Debt collection agency债务托收机构Debt issuer债券发行人Debt protection levels债券保护级别Debt ratio负债比率Debt securities债券Debt service ratio还债率Debtor days应收账款天数Debtor's assets债权人的资产Default违约Deposit limits储蓄限额Depositing money储蓄资金Depreciation折旧Depreciation policies折旧政策Development budget研发预算Differentiation差别化Direct loss直接损失Directors salaries董事薪酬Discretionary cash flows自决性现金流量Discretionary outflows自决性现金流出Distribution costs分销成本Dividend cover股息保障倍数Dividend payout ratio股息支付率Dividends股利Documentary credit跟单信用证DSO应收账款的平均回收期Duration of credit risk信用风险期Eastern bloc countries东方集团国家EBITDA扣除利息、税收、折旧和摊销之前的收益Exports Credit Guarantee Department (ECGD)出口信贷担保局Economic conditions经济环境Economic cycles经济周期Economic depression经济萧条Economic growth经济增长Economic risk经济风险Electronic data interchange(EDI)电子数据交换Environmental factors环境因素Equity capital权益资本Equity finance权益融资Equity stake股权EU countries欧盟国家EU directives欧盟法规EU law欧盟法律Eurobondsxx债券European parliament欧洲议会European Union欧盟Evergreen loan常年贷款Exchange controls外汇管制Exchange-control regulations外汇管制条例Exhaust method排空法Existing debt未清偿债务Export buyer’s credit出口买方信贷Export collection loan出口托收贷款Export credit agencies出口信贷代理机构Export credit insurance出口信贷保险Export factoring出口代理Export sales出口额Export seller’s credit出口买方信贷Export negotiation出口议付Extending credit信贷展期External agency外部机构External assessment methods外部评估方式External assessments外部评估External information sources外部信息来源Extraordinary items非经常性项目Extras附加条件Facility account便利账户Factoring代理Factoring debts代理收账Factoring discounting代理折扣Factors Chain International国际代理连锁Failure prediction scores财务恶化预测分值FASB (xx)财务会计准则委员会Faulty credit analysis破产信用分析Fees费用Finance, new business ventures为新兴业务融资Finance, repay existing debt为偿还现有债务融资Finance, working capital为营运资金融资Financial assessment财务评估Financial cash flows融资性现金流量Financial collapse财务危机Financial flexibility财务弹性Financial forecast财务预测Financial instability财务的不稳定性Financial risk财务风险Financial risk ratios财务风险比率Fitch IBCA惠誉评级Fitch IBCA ratings惠誉评级Fixed assets固定资产Fixed charge固定费用Fixed charge cover固定费用保障倍数Fixed costs固定成本Floating assets浮动资产Floating charge浮动抵押Floor planning底价协议Focus聚焦Forced sale risk强制出售风险Foreign exchange markets外汇市场Forfaiting福费廷Formal credit rating正式信用评级Forward bill discount远期信用证项下汇票贴现Forward rate agreements远期利率协议FRAs远期利率协议Fund managers基金经理FX transaction外汇交易GAAP公认会计准则Gearing财务杠杆率Geographical spread of markets市场的地理扩展Global target全球目标Going concern concept持续经营原则Good lending优质贷款Good times良好时期Government agencies政府机构Guarantee of payment支付担保Guaranteed loans担保贷款Guarantees担保High credit quality高信贷质量High credit risk高信贷风险High default risk高违约风险High interest rates高利率High-risk loan高风险贷款High-value loan高价值贷款Historical accounting历史会计处理Historical cost历史成本IAS国际会计准则IASC国际会计准则委员会IBTT息税前利润ICE优质贷款原则Ideal liquidity ratios理想的流动性比率Implied debt rating隐含债务评级Importance of credit control信贷控制的重要性Improved products改进的产品Improving reported asset values改善资产账面价值In house assessment内部评估In house credit analysis内部信用分析In house credit assessments内部信用评估In house credit ratings内部信用评级Increasing profits提高利润Increasing reported profits提高账面利润Indemnity clause赔偿条款Indicators of credit deterioration信用恶化征兆Indirect loss间接损失Individual credit transactions个人信用交易Individual rating个体评级Industrial reports行业报告Industrial unrest行业动荡Industry limit行业限额Industry risk行业风险Industry risk analysis行业风险分析Inflow现金流入Information in financial statements财务报表中的信息Initial payment初始支付Insolvencies破产Institutional investors机构投资者Insured debt投保债务Intangible fixed asset无形固定资产Interest利息Interest cost利息成本Interest cover ratio利息保障倍数Interest cover test利息保障倍数测试Interest holiday免息期Interest payments利息支付Interest rates利率Interim statements中报(中期报表)Internal assessment methods内部评估方法Internal financing ratio内部融资率Internal Revenue Service美国国税局International Accounting Standards Committee国际会计准则委员会International Accounting Standards(IAS)国际会计准则International Chamber of Commerce国际商会International credit ratings国际信用评级International Factoring国际保理International Factoring Association国际代理商协会International settlements 国际结算Inventory存货Inverse of current ratio反转流动比率Investment analysts投资分析人员Investment policy投资政策Investment risk投资风险Investment spending投资支出Invoice discounting发票贴现Issue of bonds债券的发行Issued debt capital发行债务资本Junk bond status垃圾债券状况Just-in-time system(JIT)适时系统Key cash flow ratios主要现金流量指标Labor unrest劳动力市场动荡Large scale borrower大额借贷者Legal guarantee法律担保Legal insolvency法律破产Lending agreements贷款合约Lending covenants贷款保证契约Lending decisions贷款决策Lending transactions贷款交易Letters of credit信用证Leverage财务杠杆率London Inter-bank Offered Rate (LIBOR)伦敦同业拆借利率Lien留置Liquid assets速动资产Liquidation清算Liquidation expenses清算费Liquidity流动性Liquidity and working capital流动性与营运资金Liquidity ratios流动比率Liquidity run流动性危机Liquidity shortage流动性短缺Loan covenants贷款合约Loan guarantees贷款担保Loan principal贷款本金Loan principal repayments贷款本金偿还Loan review贷款审查Long-term debt长期负债Long-term funding长期融资Long-term risk长期风险Management管理层Marginal lending边际贷款Marginal trade credit边际交易信贷Market surveys市场调查Marketing市场营销Markets市场Matching concept配比原则Material adverse-change clause重大不利变动条款Maximum leverage level最高财务杠杆率限制Measurement and judgment计量与判断Measuring risk风险计量Medium-term loan中期贷款Minimum current ratio requirement最低流动比率要求Minimum leverage ratio最低举债比率Monitoring credit信用监控Monitoring customer credit limits监管客户信贷限额Monitoring risks监管风险Monitoring total credit limits监管全部信贷限额Monthly reports月报Moody's debt rating穆迪债券评级Mortgage抵押Mpr’oving balance sheet改善资产负债表Multiple discriminate analysis多元分析National debt国家债务NCI无信贷间隔天数Near-cash assets近似于现金的资产Negative cash flow负现金流量Net book value净账面价值Net cash flow净现金流量Net worth test净值测试New entrants新的市场进人者No credit interval无信贷间隔天数Non-cash items非现金项目Non-core business非核心业务Non-operational items非经营性项目Obtaing payment获得支付One-man rule一人原则Open account terms无担保条款Operating leases经营租赁Operating profit营业利润Operational cash flow营运性现金流量Operational flexibility经营弹性Optimal credit最佳信贷Order cycle订货环节Ordinary dividend payments普通股股利支付Organization of credit activities 信贷活动的组织Overdue payments逾期支付PAT税后利润Payment in advance提前付款Payment obligations付款义务Payment records付款记录Payment score还款评分PBIT息税前利润PBT息后税前利润Percentage change百分比变动Performance bonds履约保证Personal guarantees个人担保Planning systems计划系统Pledge典押Points-scoring system评分系统Policy setting政策制定Political risk政治风险Potential bad debt潜在坏账Potential credit risk潜在信用风险Potential value潜在价值Predicting corporate failures企业破产预测Preference dividends优先股股息Preferred stockholders优先股股东Preliminary assessment预备评估Premiums溢价Primary ratios基础比率Prior charge capital优先偿付资本Priority cash flows优先性现金流量Priority for creditors债权人的清偿顺序Priority payments优先支付Product life cycle产品生命周期Product market analysis产品市场分析Product range产品范围Products产品Professional fees专业费用Profit利润Profit and loss account损益账户Profit margin利润率Profitability盈利能力Promissory notes本票Property values所有权价值Providers of credit授信者Provision accounting准备金会计处理Prudence concept谨慎原则Public information公共信息Public relations公共关系Purpose of credit ratings信用评级的目的Purpose of ratios计算比率的目的Qualitative covenants定性条款Quantitative covenants定量条款Query control质疑控制Quick ratio速动比率Rating exercise评级实践Ratio analysis weaknesses比率分析的缺陷Real insolvency真实破产Real sales growth实际销售收入增长率Realization concept实现原则Receivables应收账款Recession衰退Reducing debtors冲减应收账款Reducing profits冲减利润Reducing provisions冲减准备金Reducing reported profits冲减账面利润Reducing stocks减少存货Registrar of Companies企业监管局Regulatory risk监管风险Releasing provisions冲回准备金Relocation expenses费用再分配Reminder letters催缴单Repayment on demand clause即期偿还条款Replacement of principal偿还本金Report of chairman总裁/董事长报告Reserve accounting准备金核算Residual cash flows剩余现金流量Restricting bad debts限制坏账Revenues总收入Risk analysis reports风险分析报告Risk and banks风险与银行Risk and Return风险与回报Risk capital风险资本Risk-reward风险回报Risk-weighted assets风险加权资产ROCE资本收益率Romapla clauses “一手交钱一手交货”条款Sales销售额Secondary ratios分解比率Secure methods of payment付款的担保方式Secured assets担保资产Secured creditors有担保债权人Secured loans担保贷款SecuritiesandExchangeCommission(SEC)(美国)证券交易委员会Security guarantees抵押担保Security of payment付款担保Security general principles担保的一般原则Segmentation细分Setting and policing credit limits信用限额的设定与政策制定Settlement discount (提前)结算折扣Settlement terms结算条款Share price股价Short-term borrowing短期借款Short-term creditors短期负债Short-term liabilities短期债务Short-termism短期化SIC常务诠释委员会Significance of working capital营运资金的重要性Single credit customer单一信用客户Single ratio analysis单一比率分析Size of credit risk信用风险的大小Slow stock turnover较低的存货周转率Sources of assessments评估信息来源Sovereign rating主权评级Specialist agencies专业机构Specific debt issue特别债券发行Speculative投机性Speculative grades投机性评级Split rating分割评级Spot rate现价(即期比率)Spreadsheets电子数据表Staff redundancies员工遣散费Standard security clauses标准担保条款Standard & Poor's标准普尔Standing Interpretations Committee证券交易委员会Standing starting credit limits持续更新信用限额Statistical analysis统计分析Statistical techniques统计技巧Status reports (企业)状况报告Stock valuations存货核算Stocks股票Straight line depreciation method直线折旧法Strategic positioning战略定位Surplus assets盈余资产Surplus rating盈余评级Supplier power供应商的力量Supply chain供应链Support rating支持评级Swap agreement换合约Swaps互换SWOT analysis SWOT分析Symptoms of failure questionnaires企业破产征兆调查表Takeovers收购Tax payments税务支付Technical insolvency技术破产Technology and change技术进步Term loan定期贷款Term of borrowing借款期限Third party guarantees第三方担保Tier 1 capital一类资本Trade credit商业信用Trade creditors应付账款Trade cycle商业循环Trade cycle times商业循环周期Trade debt应收账款Trade debtors贸易债权人Trade financing贸易融资Trade Indemnity贸易赔偿Trade references贸易参考Trade-off协定Trading outlook交易概况Trading profit营业利润Traditional cash flow传统现金流量Triple A三AUCP跟单信用证统一惯例Uncovered dividend未保障的股利Uniform Customs & Practice跟单信用证统一惯例Unpaid invoices未付款发票Unsecured creditors未担保的债权人Usefulness of liquidity ratios流动性比率的作用Uses of cash现金的使用Using bank risk information使用银行风险信息Using financial assessments使用财务评估Using ratios财务比率的运用Using retention-of-title clauses使用所有权保留条款Value chain价值链Value of Z scores Z值模型的价值Variable costs变动成本Variable interest可变利息Variety of financial ratios财务比率的种类Vetting procedures审查程序Volatile revenue dynamic收益波动Volume of sales销售量Warning signs of credit risk信用风险的警示Working assets营运资产working capital营运资本Working capital changes营运资本变化额working capital ratios营运资本比率Worldwide credit统一授信Write-downs资产减值Write-offs勾销Z score assessments Z值评估z score models z值模型Z scores z值Z scoring Z值评分系统。

国际会计准则