2015年ACCA报名材料有哪些

acca报考条件和要求

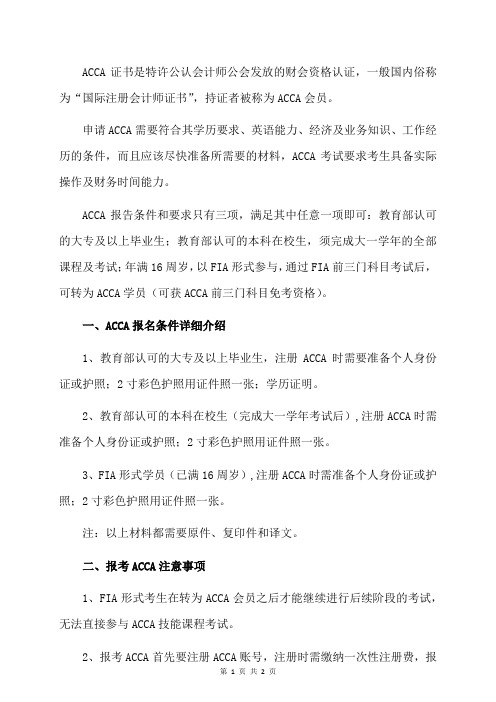

ACCA证书是特许公认会计师公会发放的财会资格认证,一般国内俗称为“国际注册会计师证书”,持证者被称为ACCA会员。

申请ACCA需要符合其学历要求、英语能力、经济及业务知识、工作经历的条件,而且应该尽快准备所需要的材料,ACCA考试要求考生具备实际操作及财务时间能力。

ACCA报告条件和要求只有三项,满足其中任意一项即可:教育部认可的大专及以上毕业生;教育部认可的本科在校生,须完成大一学年的全部课程及考试;年满16周岁,以FIA形式参与,通过FIA前三门科目考试后,可转为ACCA学员(可获ACCA前三门科目免考资格)。

一、ACCA报名条件详细介绍1、教育部认可的大专及以上毕业生,注册ACCA时需要准备个人身份证或护照;2寸彩色护照用证件照一张;学历证明。

2、教育部认可的本科在校生(完成大一学年考试后),注册ACCA时需准备个人身份证或护照;2寸彩色护照用证件照一张。

3、FIA形式学员(已满16周岁),注册ACCA时需准备个人身份证或护照;2寸彩色护照用证件照一张。

注:以上材料都需要原件、复印件和译文。

二、报考ACCA注意事项1、FIA形式考生在转为ACCA会员之后才能继续进行后续阶段的考试,无法直接参与ACCA技能课程考试。

2、报考ACCA首先要注册ACCA账号,注册时需缴纳一次性注册费,报名考试时需要缴纳考试报名费。

3、ACCA各科目有报名顺序要求,需按阶段报考,即:知识课程阶段(F1-F3)—技能课程阶段(F4—F9)—战略课程阶段(P阶段)。

4、ACCAK傲视形式分为随时机考和分季机考,随时机考(F1—F4)联系机考中心报名,分季机考(F5—F9和P阶段)在ACCA官网报名。

5、报名之后可能受某些原因影响,导致报名信息变化,届时考试需要以准考证上的报考信息为准去参加考试。

ACCA

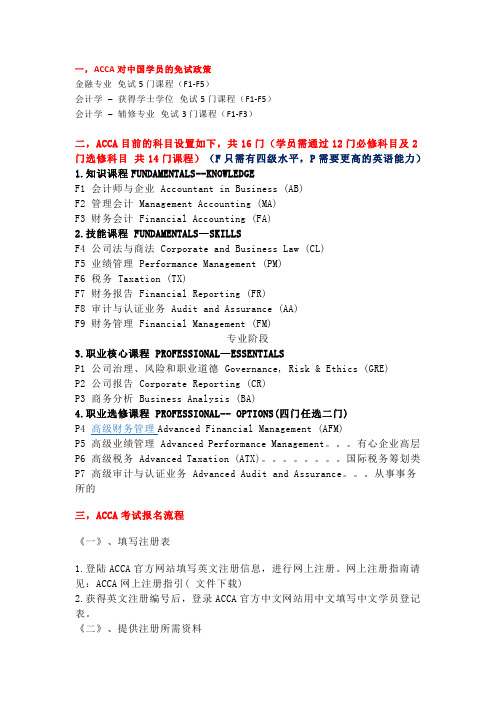

一,ACCA对中国学员的免试政策金融专业免试5门课程(F1-F5)会计学–获得学士学位免试5门课程(F1-F5)会计学–辅修专业免试3门课程(F1-F3)二,ACCA目前的科目设置如下,共16门(学员需通过12门必修科目及2门选修科目共14门课程)(F只需有四级水平,P需要更高的英语能力)1.知识课程FUNDAMENTALS--KNOWLEDGEF1 会计师与企业 Accountant in Business (AB)F2 管理会计 Management Accounting (MA)F3 财务会计 Financial Accounting (FA)2.技能课程 FUNDAMENTALS—SKILLSF4 公司法与商法 Corporate and Business Law (CL)F5 业绩管理 Performance Management (PM)F6 税务 Taxation (TX)F7 财务报告 Financial Reporting (FR)F8 审计与认证业务 Audit and Assurance (AA)F9 财务管理 Financial Management (FM)专业阶段3.职业核心课程 PROFESSIONAL—ESSENTIALSP1 公司治理、风险和职业道德 Governance, Risk & Ethics (GRE)P2 公司报告 Corporate Reporting (CR)P3 商务分析 Business Analysis (BA)4.职业选修课程 PROFESSIONAL-- OPTIONS(四门任选二门)P4 高级财务管理Advanced Financial Management (AFM)P5 高级业绩管理 Advanced Performance Management。

有心企业高层P6 高级税务 Advanced Taxation (ATX)。

ACCA Qualification网上注册指引-GXUFE

ACCA Qualification网上注册指引欢迎注册Certified Accounting T echnician (CAT) Qualification!请登陆/join/register/online, 点击Certified Accounting Technician Scheme,注册共有23个步骤。

每一步骤都有详细的解释和介绍,以下是注册过程中可能遇到的问题的中文注释,希望能够帮助您顺利完成网上注册。

Step 1 of 23: 欢迎来到CAT网上注册页面仔细阅读网上注册的注意事项后点击proceedStep 2 of 23:选择注册类型请选择Accounting Technician Register, Diploma in Financial Management, 确认无误后,点击proceed。

Step 3 of 23:选择注册前状态如果以前没有注册过PER、MSER或TR , 请点击No,否则点击Yes。

(同学直接点No)Step 4 of 23:注册前提如果以前曾经注册过ACCA Diploma , 请点击Yes,否点击No。

(同学直接点No)Step 5 of 23:选择注册CAT选择Certified Accounting Technician Register, 然后点击continue。

Step 6 of 23:Direct Entry如果您有财会相关的学位证书及相关的工作经验,可以申请直接获得CAT的资格证书,如果您符合条件的话,请勿选择网上注册,请与ACCA联系。

详情请点住页面中的Notes for Completing this Section查看。

同学点击noStep 7 of 23:相关认证和经历情况由于中国没有“Joint Scheme”,请点击no。

Step 8 of 23:个人信息填写选择您的Title, 在“Surname or Family name”一栏填写姓名的拼音,姓在前,空一格后填名字,例如:李小明“”填写格式:Li Xiaoming;在“Date of Birth”一栏填写/选择出生日期,“Gender”一栏选择性别,“Nationality”一栏选择China;“Email address”一栏填写个人邮箱,并根据个人要求选择Email Consent;□不希望收到电子邮件□希望收到一对一的回复性电子邮件□希望收到关于ACCA信息电子邮件□愿意将E-mail地址给予ACCA所认可的第三方,并获取更多信息“Ethnic Origin”,种族选择--Asian Chinese,填写完确认无误后,点击proceed。

考会计证需要哪些材料

考会计证需要哪些材料考取会计证是每个想在财务领域发展的人必须具备的资格。

但是,想要成功考取会计证,需要准备许多材料。

以下是考取会计证所需的材料,以及一些专业建议。

一、身份证明材料申请会计证需要提供有效的身份证明材料。

身份证、护照和其他可以证明身份的材料都可以被接受。

申请人需要确保这些证件的副本是有效的,所有信息都是清晰的。

二、学历证明材料申请会计证的人必须提供有效学历证明材料。

学位证书和毕业证书是目前最常用的证明材料。

国外学历证明材料可以使用国外学历认证机构的证明材料。

三、工作经历证明材料申请会计证需要提供工作经历证明材料。

这可能包括员工证明或工作证明。

在填写申请表时,还需要详细说明候选人所从事的工作领域和工作职责。

四、考试报名费在申请考取会计证之前,需要支付考试报名费。

考试报名费通常包括考试的费用和相关文件的处理费用。

在缴纳考试费用后,申请人可以获得考试指南和考试录取通知等相关文件。

五、其他材料此外,申请人还需要填写完整的申请表,填写该表需要提供以下信息:1、基本信息,如姓名,国籍,籍贯,联系信息;2、教育和工作经历,包括所读课程,毕业时间,职务和所在公司;3、资格证书,如ACCA,CPA等的证书;4、推荐信,提供两封推荐信。

以上就是考取会计证所需准备的所有材料。

请注意,申请人提交的材料必须真实有效、且满足考试要求。

下面,我们列举五个实际案例,帮助各位更了解申请考取会计证所需准备的材料。

案例一小张是一名在校大学生,他正在学习会计专业,并希望将来能够成为一名注册会计师。

考虑到他的大学课程刚结束,他需要一些额外的材料来申请考试。

小张需要准备:1、身份证复印件(正反面);2、学位证书和毕业证书(复印件);3、大学成绩单,以证明他的学术成绩;4、工作经验证明;5、考试报名费。

案例二小王在一家会计事务所工作已经三年了,他想申请注册会计师资格考试。

他的公司愿意出资助他考试,但需要他准备全套考试申请材料。

小王需要准备:1、身份证复印件(正反面);2、毕业证书;3、工作经验证明;4、由雇主出具的工作推荐信;5、考试报名费。

找工作需要做好哪些准备资料

找工作需要做好哪些准备资料想要提高找工作的成功机率,那就要提前做好充分的准备。

找工作前有很多准备的工作,不单单是一份简历那么简单的。

下面就是店铺给大家整理的找工作前的准备资料,希望对你有用!找工作需要准备什么1、找工作需要准备什么材料准备标准中英文简历及对应求职信。

准备各类证件的原件和复印件、扫描版。

身份证学生证户口本(部分招聘本地生源的公务员报名时可能会用到)。

英语四级或英语六级等级证书(必要,很多情况下不能用其他任何英语证书代替)。

托福、GRE、计算机等其他证书。

学校正式开具的、盖学校章的成绩单。

研究生建议把本科的成绩单也加上,送材料的时候,如果单位没有具体要求,则本科、硕士成绩单都要送,这样可以给用人单位留下非常好的印象。

一寸和两寸证件照都要准备,建议这些照片要随身携带,面试、笔试等场合随时会要求使用,而且要多准备。

一寸证件照的电子版图片,随时会被要求放进网上提交的报名表格中(即网申),必备。

关于网申的注意事项参见本文第五章《网申》部分。

5寸或6寸的个人生活照一张,洗出来,还有生活照的电子版也要准备,很多单位要求你必须把一张个人生活照随其他材料一起寄过去或者Email过去。

2、找工作要写好自我评价对于没有相关工作经验的求职者来说,要想获得用人单位的青睐,自我评价必须重视起来。

自我评价着重写个人爱好、气质与性格以及对自己在学校里学到的东西进行总结,向用人单位显示出自己的潜力。

记住,原则是让用人单位对你留下好印象,相信你有相应的学习能力。

3、找工作要有优化教育培训经历要是没有足够多与欲申请的工作相干的经验,你应当更着重强调最近的教育与培训,尤其是与正在申请的工作最直截相关的课程或实践活动。

刚毕业的学生应该重视自己在学校里的毕业实践和毕业设计,这些活动也同样要求高度自律的特点、完成不同任务的能力以及其它方面的个人素质,它赋予你的是可以广泛应用的工作技巧。

准备找工作时最有用的十类证书NO.1:英语证书大学英语四、六级证书(CET-4,CET-6):极其重要;专业八级:只有英语专业才有资格考,但很多职位要求,如翻译或者外籍主管的助理;大学英语四、六级口语证书:证书不重要,能力重要,面试的表达重要;英语中高级口译:含金量很高;托福(TOFEL):只有少数企业会问到是否考过托福,但同时会担心你工作不久后,可能会出国溜掉;雅思(IELTS):少数英联邦国家企业会注意到你考过雅思,但绝不是必要条件;剑桥商务英语(BEC):证书说明了你的英语能力,还有你在大学里很好学,懒惰的同学不会去学,或者学了考不过的;这是企业关注的。

法语二级《口译实务》录音材料(样题)

全国翻译专业资格(水平)考试法语二级《口译实务》录音材料(样题)◆Transcription de l’enregistrementPartie ITraduisez du français en chinois les deux allocutions suivantes.Il faut commencer l’interprétationàchaque signal sonore donnéet l’arrêter avant le signal suivant.Vous pouvez prendre des notes enécoutant l’enregistrement.Mais,attention,vous ne l’entendez qu’une fois.1.法国总统希拉克2002年9月在全球可持续发展首脑会议上的讲话Monsieur le Président,Mesdames,Messieurs,Notre maison brûle et nous regardons nature,mutilée,surexploitée, ne parvient plusàse reconstituer et nous refusons de l’admettre.L’humanitésouffre. Elle souffre de mal-développement,au nord comme au sud,et nous sommes indiffé terre et l’humanitésont en péril et nous en sommes tous responsables. //Il est temps,je crois,d’ouvrir les yeux.Sur tous les continents,les signaux d’alerte s’allument.L’Europe est frappée par des catastrophes naturelles et des crises sanitaires.L’économie américaine,souvent boulimique en ressources naturelles, paraît atteinte d’une crise de confiance dans ses modes de régulation.// L’Amérique latine estànouveau secouée par la crise financière et donc sociale. En Asie,la multiplication des pollutions,dont témoigne le nuage brun,s’étend et menace d’empoisonnement un continent tout entier.L’Afrique est accablée par les conflits,le SIDA,la désertification,la famine.Certains pays insulaires sont menacés de disparition par le réchauffement climatique.//Nous ne pourrons pas dire que nous ne savions pas!Prenons garde que le XXI e siècle ne devienne pas,pour les générations futures,celui d’un crime de l’humanitécontre la vie.//Notre responsabilitécollective est engagée.Responsabilitépremière des pays développés.Première par l’histoire,première par la puissance,première par le niveau de leurs consommations.Si l’humanitéentière se comportait comme les pays du Nord, il faudrait deux planètes supplémentaires pour faire faceànos besoins.// Responsabilitédes pays en développement aussi.Nier les contraintesàlong terme au nom de l’urgence n’a pas de sens.Ces pays doivent admettre qu’il n’est d’autre solution pour eux que d’inventer un mode de croissance moins polluant.// 2.国际劳工组织负责非洲事务的副总干事朗贝尔·格博萨2002年3月在关于跨国贩卖儿童问题咨询会议上的讲话C’est un immense encouragement de constater aujourd’hui la mobilisation de tous les pays ici représentés,pour mettre fin,ensemble et au plus tôt,au trafic transfrontalier des enfants en Afrique de l’Ouest et du Centre.//Si l’Organisation internationale du Travail lutte de façon vigoureuseàla fois contre le travail forcéet contre le travail des enfants―et ceci depuis sa création en 1919―,elle a voulu en1999se doter d’instruments spécifiques pour lutter contre les pires formes de travail des enfants―au rang desquelles se trouve le trafic des enfants―afin d’en assurer de façon claire et rapide l’interdiction et l’éliminationàl’échelle mondiale.//Tous les pays membres de l’OIT ont adhéréàcette démarche,adoptantàl’unanimitéla nouvelle convention,ratifiée depuis lors par115pays dans le monde, dont une trentaine en Afrique,qui seront bientôt rejoints par d’autres oùle processus de ratification est déjàengagé.//En Afrique de l’Ouest et du Centre,nous connaissons malheureusement ces fléaux qui prennent la forme du trafic des enfants,de l’engagement des enfants dans les conflits armés,de l’exploitation des enfants dans des formes et conditions de travail inacceptables,mettant en péril leur vie,leur santéphysique et psychologique, et qui les privent de toute chance d’être demain des adultes capables de participer au développement de leur pays.//Car l’enjeu n’est pas seulement aujourd’hui et maintenant de faire cesser une exploitation injuste et criminelle,il est aussi de donner une chanceàl’avenir,de permettreàtous les enfants d’être demain des citoyensàpart entière,productifs, pleinement intégrés et moteurs du développement de leur pays.C’est seulement ainsique nous mettrons finàla pauvretéet engagerons,pour tous et avec tous,un développement durable.//Si la pauvretéconstitue l’une des causes du trafic des enfants,elle ne saurait en aucune façon le justifier.Bien plus,la lutte contre la pauvretécommence par l’élimination de ces formes honteuses d’exploitation.//Partie IITraduisez du chinois en français les deux allocutions suivantes.Il faut commencer l’interprétationàchaque signal sonore donnéet l’arrêter avant le signal suivant.Vous pouvez prendre des notes enécoutant l’enregistrement.Mais,attention,vous ne l’entendez qu’une fois.1.Allocution du Premier ministre Wen Jiabaoàla cérémonie d’ouverture de ladeuxième Conférence ministérielle du Forum sur la coopération sino-africaine, décembre2003.女士们,先生们:我很高兴来到亚的斯亚贝巴,与出席中非合作论坛第二届部长级会议的各位朋友共商中非合作大计。

ACCA考试注册报名的在校生证明信英文翻译范本

ACCA考试注册报名需要提供相应的英文资料,在校生证明信就是其中一项,在校生证明信翻译范本如下:在校生证明信(Letter of Verification)Letter of VerificationThis is to certify that ________ (NAME OF STUDENT) is a student of Grade_________ (CLASS), Department of _________ (DSICIPLINE OF STUDY),specialty of _________ (PROGRAMME).He/she is (studying toward bachelor/master degree) at our university.He/she enrolled in ________ (YEAR) and has already successfully completedthe courses of the first ________ (YEARS COMPLETED) full years of the total_______ year(s) degree.Office of Academic Affairs_________________________University(Seal)____________(Date)身份证(ID Card)IDENTITY CARD THE PEOPLE'S REPUBLIC OF CHINAFrontName:___________Sex:___________Nationality:___________Date of Birth:___________Residential Address:___________ID No.:___________BackIssued by: ___________Valid: from ________to_______CET-6大学英语考试六级证书(Certificate of College English Test)Certificate of College English TestThis is to certify that ___________, a student of Grade ______ at Department of __________, ___________ University/Institute, passed the examination of College English Test Band-6 (CET-6) in January/June XXXX. Upon examination, he/she has fulfilled the band 6 requirements College English Syllabus Band Six with excellent/qualified score and is hereby awarded the Certificate of CET-6.Department of Higher EducationState Education Commission (国家教委)或Ministry of Education (教育部)Date of Issuance:___________Certificate No.:___________CET-6大学英语考试六级成绩单翻译(Transcript Report of College English Test Band) Transcript Report of College English Test Band-6Name:University:Institute/Department:Exam Attendance Docket No.:ID Card No.:Exam Time:Department of Higher EducationMinistry of EducationEntrust to Issue by: National College English Testing Committee(Seal) Website: TEM专业英语考试证书(Test for English Majors)Test for English MajorsThis is to certify that___________, a student of_ _from_______, participated in the TEM___________ exam (Test for English Majors) organized by the English Group of the National Higher Education Foreign Language Major Teaching Supervisory Committee of the State Education Ministry and passed the exam. Hereby he/she is awarded theTEM-__Certificate.Issuing Date: ___________Certificate No.:___________English GroupNational Higher Education Foreign Language MajorTeaching Supervisory Committee (seal) 本科毕业证书(Graduation Certificate)Graduation CertificateCertificate No. _____________This is to certify that ___________, born on __________, native of__________, has been majoring in the specialty of ________________ at our university/institute from September ________ to July _________. Upon completion of all the courses specified by the four-year undergraduate teaching programme with qualified score, he/she is hereby qualified for graduation.___________(signature)President___________University (seal)XX July XXXX 学士学位证书(Certificate of Bachelor's Degree)Certificate of Bachelor's DegreeCertificate No.:___________ This is to certify that___________ , male / female, native of __________, born on __________, has been majoring in the specialty of ___________at our university/ institute from September_____ to July _______. Upon completion of all the courses specified by the four-year undergraduate teaching programme with qualified score, he/she is qualified for graduation. In conformity with the articles of the Regulations Regarding Academic Degrees of the People's Republic of China, he/she has been conferred to the degree of Bachelor of ___________.___________(signature)ChairmanCommittee of Degree Accreditation___________University (seal)XX July XXXX 硕士研究生毕业证书(Graduation Certificate for Postgraduate Students)Graduation Certificate for Postgraduate StudentsCertificate No. _____________This is to certify that ___________, born on __________, native of__________, has been majoring in the specialty of ________________ at our university/institute from September ________ to July _________. Having completed all the courses specified by the three-year postgraduate teaching programme with qualified score and passed the graduation thesis, he/she is hereby qualified for graduation.___________(signature)President___________University (seal)XX July XXXX 硕士学位证书(Certificate of Master's Degree)Certificate of Master's DegreeCertificate No.:__________ This is to certify that , male / female, native of __________, born on __________, has been majoring in the specialty of__________ at our university/ institute from September __________ to July __________. Upon completion of all the courses specified by the three-year postgraduate teaching programme with qualified score and passed the thesis defense. In conformity with the articles of the Regulations Regarding Academic Degrees of the People’s Republic of China, he/she has been conferred to the degree of Maser of ___________.( signature )ChairmanCommittee of Degree AccreditationUniversity (seal)XX July XXXX 中注协全科合格证(CICPA Certificate of Completion)Chinese Institute of Certified Public AccountantsCertificate of CompletionThis is to certify that __________ has completed the full scheme of examinations of the Chinese Institute of Certified Public Accountants (CICPA) and is hereby awarded the Certificate of Completion.Issuing Authority: Examination Council of CPAsMinistry of Finance (seal) Issuing Date: ____________________No.: ___________________ID No.:____________________Valid until:____________________Remarks1. This is to certify that the holder of this certificate has been awarded the CICPA qualification. In accordance with the Law of CPAs of the People's Republic of China and the relevant regulations, the certificate holder is eligible to apply for practicing.2. The certificate does not entitle its holder to do public practice.3. Please keep this certificate carefully. No duplicate copy will be issued if lost. 中注协会员证(CICPA membership certificate)Chinese Institute of Certified Public AccountantsMembership CertificateName: _______________________Sex: _______________________Date of Birth: _______________________Membership Category: Practicing membership or Non-practicing membership Certificate No: _______________________Issuing Body: Beijing Institute of Certified Public Accountants (按实际情况填写) Issuing Date: _______________________中注协考试成绩通知单(CICPA Examination results notification)National Examination for Certified Public AccountantsNotification of Examination ResultsDear_______,Hereby we confirm that your exam results in the year of _______ National Examination of Certified Public Accountants are as follows:Accounting __________Auditing __________Financial and Cost Management ________Economic Law __________Taxation Law __________Notification number: __________Exam docket number: __________Exam entry number: __________Issued by: General Office ExaminationCouncil of CPAs Ministry of FinanceSeal by: _________ Institute of CPAsDate: ___________________。

acca资格证书获取条件

acca资格证书获取条件ACCA(Association of Chartered Certified Accountants)是国际上最具影响力的专业会计师协会之一。

获得ACCA资格证书,可以为个人职业发展开创更广阔的天地,同时也能让个人在全球范围内得到更好的职业机会。

所以越来越多的学生和职场人士开始关注ACCA特别是ACCA资格证书的获取条件。

ACCA资格证书的获取条件如下:1. 获得学历:ACCA协会要求考生至少具有大学本科学历。

如果考生的母语不是英语,还需要获得相应的英语语言证明。

2. 报名注册:考生需要在ACCA官网上注册自己的相关信息,包括个人信息、学历情况、工作经历和联系方式等。

3. 完成14门考试:ACCA资格证书需要考生通过14门考试来获得。

其中,前3门考试为基础考试,主要测试考生对财务会计、财务管理和业务管理的理解。

接下来的9门考试是专业的,主要涉及企业财务管理、审计、税务和商业法等领域。

最后的2门考试为基于职场的实地考试,旨在测评考生在职业实践中的能力。

4. 实践要求:ACCA还要求考生在相关领域有三年以上的工作经验。

ACCA资格证书的获取,需要考生具备一定的专业知识和技能,因此,相关考试内容和难度比较高,考生需要通过系统的学习和实践来积累经验和技能。

同时,ACCA资格证书的合法性和信誉,也要求考生具备严格的诚信和道德素养,以符合国际财务标准和道德行为准则。

总的来说,ACCA资格证书的获取条件较为苛刻,对考生的学历、知识和职业实践经验都有较高的要求。

但是,通过获得ACCA资格证书,学生和职场人士能够获得更加广阔的职业发展机会,拥有更高的职业声望和收入水平。

因此,对于有志于从事财务及管理类职业的人士,获得ACCA资格证书是一个值得投入精力和时间的选择。

ACCA F6 2015 June specimen 答案

P a p e r F 6 ( U K )SUPPLEMENTARY INSTRUCTIONS1.Calculations and workings need only be made to the nearest £.2.All apportionments should be made to the nearest month.3.All workings should be shown in Section B.TAX RATES AND ALLOWANCESThe following tax rates and allowances are to be used in answering the questions.Income taxNormal Dividendrates ratesBasic rate£1 – £31,86520%10%Higher rate£31,866 to £150,00040%32·5% Additional rate£150,001 and over45%37·5%A starting rate of 10% applies to savings income where it falls within the first £2,880 of taxable income.Personal allowancePersonal allowanceBorn on or after 6 April 1948£10,000Born between 6 April 1938 and 5 April 1948£10,500Born before 6 April 1938 £10,660Income limitPersonal allowance£100,000Personal allowance (born before 6 April 1948)£27,000Residence statusDays in UK Previously resident Not previously residentLess than 16Automatically not resident Automatically not resident16 to 45Resident if 4 UK ties (or more)Automatically not resident46 to 90Resident if 3 UK ties (or more)Resident if 4 UK ties91 to 120Resident if 2 UK ties (or more)Resident if 3 UK ties (or more)121 to 182Resident if 1 UK tie (or more)Resident if 2 UK ties (or more)183 or more Automatically resident Automatically residentChild benefit income tax chargeWhere income is between £50,000 and £60,000, the charge is 1% of the amount of child benefit received for every £100 of income over £50,000.Car benefit percentageThe relevant base level of COemissions is 95 grams per kilometre.2The percentage rates applying to petrol cars with COemissions up to this level are:275 grams per kilometre or less5%76 grams to 94 grams per kilometre11%95 grams per kilometre12%2Car fuel benefitThe base figure for calculating the car fuel benefit is £21,700.New individual savings accounts (NISAs)The overall investment limit is £15,000.Pension scheme limitAnnual allowance –2014–15£40,000–2011–12 to 2013–14£50,000 The maximum contribution that can qualify for tax relief without any earnings is £3,600.Authorised mileage allowances: carsUp to 10,000 miles45p Over 10,000 miles25pCapital allowances: rates of allowancePlant and machineryMain pool18% Special rate pool8% Motor carsNew cars with CO2emissions up to 95 grams per kilometre100%CO2emissions between 96 and 130 grams per kilometre18%CO2emissions over 130 grams per kilometre8%Annual investment allowanceRate of allowance100% Expenditure limit£500,000Cap on income tax reliefsUnless otherwise restricted, reliefs are capped at the higher of £50,000 or 25% of income.Corporation taxFinancial year201220132014Small profits rate20%20%20%Main rate24%23%21%Lower limit£300,000£300,000£300,000Upper limit£1,500,000£1,500,000£1,500,000Standard fraction1/1003/4001/400Marginal reliefStandard fraction x (U –A) x N/A3[P.T.O.Value added tax (VAT)Standard rate20% Registration limit£81,000 Deregistration limit£79,000Inheritance tax: tax rates£1 –£325,000Nil Excess–Death rate40%–Lifetime rate20%Inheritance tax: taper reliefYears before death Percentagereduction Over 3 but less than 4 years20% Over 4 but less than 5 years40% Over 5 but less than 6 years60% Over 6 but less than 7 years80%Capital gains taxRates of tax–Lower rate18%–Higher rate28% Annual exempt amount£11,000 Entrepreneurs’ relief–Lifetime limit£10,000,000–Rate of tax 10%National insurance contributions(Not contracted out rates)%Class 1Employee£1 – £7,956 per year Nil£7,957 – £41,865 per year12·0£41,866 and above per year12·0Class 1Employer£1 – £7,956 per year Nil£7,957 and above per year13·8Employment allowance£2,000Class 1A13·8Class 2£2·75 per weekSmall earnings exemption limit£5,885Class 4£1 – £7,956 per year Nil£7,957 – £41,865 per year9·0£41,866 and above per year2·0Rates of interest (assumed)Official rate of interest 3·25%Rate of interest on underpaid tax 3%Rate of interest on overpaid tax0·5%4Section A – ALL 15 questions are compulsory and MUST be attemptedPlease use the space provided on the inside cover of the Candidate Answer Booklet to indicate your chosen answer to each multiple-choice question.Each question is worth 2 marks.1During the tax year 2014–15, William was paid a gross annual salary of £82,700. He also received taxable benefits valued at £5,400.What amount of class 1 national insurance contributions (NIC) will have been suffered by William for the tax year 2014–15?A£4,994B£8,969C£4,886D£4,0692You are a trainee Chartered Certified Accountant and your firm has a client who has refused to disclose a chargeable gain to HM Revenue and Customs (HMRC).From an ethical viewpoint, which of the following actions could be expected of your firm?(1)Reporting under the money laundering regulations(2)Advising the client to make disclosure(3)Ceasing to act for the client(4)Informing HMRC of the non-disclosure(5)Warning the client that your firm will be reporting the non-disclosure(6)Notifying HMRC that your firm has ceased to act for the clientA2, 3 and 5B1, 2, 3 and 6C2, 3 and 4D1, 4, 5 and 63Martin was born on 28 June 1965. He is self-employed, and for the year ended 5 April 2015 his trading profit was £109,400. During the tax year 2014–15, Martin made a gift aid donation of £800 (gross) to a national charity.What amount of personal allowance will Martin be entitled to for the tax year 2014–15?A£10,000B£5,700C£5,300D Nil5[P.T.O.4For the year ended 31 March 2015, Halo Ltd made a trading loss of £180,000.Halo Ltd has owned 100% of the ordinary share capital of Shallow Ltd since it began trading on 1 July 2014. For the year ended 30 June 2015, Shallow Ltd will make a trading profit of £224,000.Neither company has any other taxable profits or allowable losses.What is the maximum amount of group relief which Shallow Ltd can claim from Halo Ltd in respect of the trading loss of £180,000 for the year ended 31 March 2015?A£180,000B£168,000C£45,000D£135,0005For the year ended 31 March 2014, Sizeable Ltd had a corporation tax liability of £384,000, and for the year ended31 March 2015 had a liability of £456,000.Sizeable Ltd is a large company, and is therefore required to make instalment payments in respect of its corporation tax liability.The company’s profits have accrued evenly throughout each year.What is the amount of each instalment payable by Sizeable Ltd in respect of its corporation tax liability for the year ended 31 March 2015?A£228,000B£114,000C£96,000D£192,0006For the year ended 31 December 2014, Lateness Ltd had a corporation tax liability of £60,000, which it did not pay until 31 March 2016. Lateness Ltd is not a large company.How much interest will Lateness Ltd be charged by HM Revenue and Customs (HMRC) in respect of the late payment of its corporation tax liability for the year ended 31 December 2014?A£900B£2,250C£300D£4507On 26 November 2014 Alice sold an antique table for £8,700. The antique table had been purchased on 16 May 2011 for £3,800.What is Alice’s chargeable gain in respect of the disposal of the antique table?A£4,500B£1,620C£4,900D Nil68On 14 November 2014, Jane made a cash gift to a trust of £800,000 (after deducting all available exemptions).Jane paid the inheritance tax arising from this gift. Jane has not made any other lifetime gifts.What amount of lifetime inheritance tax would have been payable in respect of Jane’s gift to the trust?A£95,000B£190,000C£118,750D£200,0009During the tax year 2014–15, Mildred made the following cash gifts to her grandchildren:(1)£400 to Alfred(2)£140 to Minnie(3) A further £280 to Minnie(4)£175 to WinifredWhich of the gifts will be exempt from inheritance tax under the small gifts exemption?A1, 2, 3 and 4B2, 3 and 4 onlyC 2 and 4 onlyD 4 only10For the quarter ended 31 March 2015, Zim had standard rated sales of £59,700 and standard rated expenses of £27,300. Both figures are inclusive of value added tax (VAT).Zim uses the flat rate scheme to calculate the amount of VAT payable, with the relevant scheme percentage for her trade being 12%.How much VAT will Zim have to pay to HM Revenue and Customs (HMRC) for the quarter ended 31 March 2015?A£6,396B£3,888C£6,480D£7,16411Which of the following assets will ALWAYS be exempt from capital gains tax?(1) A motor car suitable for private use(2) A chattel(3) A UK Government security (gilt)(4) A houseA 1 and 3B 2 and 3C 2 and 4D 1 and 47[P.T.O.12Winston has already invested £8,000 into a cash new individual savings account (NISA) during the tax year 2014–15. He now wants to invest into a stocks and shares NISA.What is the maximum possible amount which Winston can invest into a stocks and shares NISA for the tax year 2014–15?A£15,000B£7,000C NilD£7,50013Ming is self-employed. How long must she retain the business and non-business records used in preparing her self-assessment tax return for the tax year 2014–15?Business records Non-business recordsA31 January 201731 January 2017B31 January 201731 January 2021C31 January 202131 January 2021D31 January 202131 January 201714Moon Ltd has had the following results:Period Profit/(loss)£Year ended 31 December 2014 (105,000)Four-month period ended 31 December 201343,000Year ended 31 August 2013 96,000The company does not have any other income.How much of Moon Ltd’s trading loss for the year ended 31 December 2014 can be relieved against its total profits of £96,000 for the year ended 31 August 2013?A£64,000B£96,000C£70,000D£62,00015Nigel has not previously been resident in the UK, being in the UK for less than 20 days each tax year. For the tax year 2014–15, he has three ties with the UK.What is the maximum number of days which Nigel could spend in the UK during the tax year 2014–15 without being treated as resident in the UK for that year?A90 daysB182 daysC45 daysD120 days8Section B – ALL SIX questions are compulsory and MUST be attempted1(a)On 10 June 2014, Delroy made a gift of 25,000 £1 ordinary shares in Dub Ltd, an unquoted trading company, to his son, Grant. The market value of the shares on that date was £240,000. Delroy had subscribed for the 25,000 shares in Dub Ltd at par on 1 July 2004. Delroy and Grant have elected to hold over the gain as a gift of a business asset.Grant sold the 25,000 shares in Dub Ltd on 18 September 2014 for £240,000.Dub Ltd has a share capital of 100,000 £1 ordinary shares. Delroy was the sales director of the company from its incorporation on 1 July 2004 until 10 June 2014. Grant has never been an employee or a director of Dub Ltd.For the tax year 2014–15 Delroy and Grant are both higher rate taxpayers. Neither of them has made any other disposals of assets during the year.Required:(i)Calculate Grant’s capital gains tax liability for the tax year 2014–15.(3 marks)(ii)Explain why it would have been beneficial for capital gains tax purposes if Delroy had instead sold the 25,000 shares in Dub Ltd himself for £240,000 on 10 June 2014, and then gifted the cash proceedsto Grant.(2 marks)(b)On 12 February 2015, Marlon sold a house for £497,000, which he had owned individually. The house hadbeen purchased on 22 October 1999 for £146,000. Marlon incurred legal fees of £2,900 in connection with the purchase of the house, and legal fees of £3,700 in connection with the disposal.Throughout the period of ownership the house was occupied by Marlon and his wife, Alvita, as their main residence. One-third of the house was always used exclusively for business purposes by the couple.Entrepreneurs’ relief is not available in respect of this disposal.For the tax year 2014–15 Marlon is a higher rate taxpayer, but Alvita did not have any taxable income. Neither of them has made any other disposals of assets during the year.Required:(i)Calculate Marlon’s chargeable gain for the tax year 2014–15.(3 marks)(ii)Calculate the amount of capital gains tax which could have been saved if Marlon had transferred 50% ownership of the house to Alvita prior to its disposal.(2 marks)(10 marks)9[P.T.O.2You should assume that today’s date is 15 March 2015.Opal Elder, aged 71, owns the following assets:(1)T wo properties respectively valued at £374,000 and £442,000. The first property has an outstanding repaymentmortgage of £160,000, and the second property has an outstanding endowment mortgage of £92,000.(2)Vintage motor cars valued at £172,000.(3)Investments in new individual savings accounts (NISAs) valued at £47,000, savings certificates from NS&I(National Savings and Investments) valued at £36,000, and government stocks (gilts) valued at £69,000.Opal owes £22,400 in respect of a personal loan from a bank, and she has also verbally promised to pay legal fees of £4,600 incurred by her nephew.Under the terms of her will, Opal has left all of her estate to her children. Opal’s husband is still alive.On 14 August 2005, Opal had made a gift of £100,000 to her daughter, and on 7 November 2014, she made a gift of £220,000 to her son. Both these figures are after deducting all available exemptions.The nil rate band for the tax year 2005–06 is £275,000.Required:(a)(i)Calculate Opal Elder’s chargeable estate for inheritance tax purposes were she to die on20 March 2015.(5 marks)(ii)Calculate the amount of inheritance tax which would be payable in respect of Opal Elder’s chargeable estate, and state who will be responsible for paying the tax. (3 marks)(b)Advise Opal Elder as to why the inheritance tax payable in respect of her estate would alter if she were tolive for another seven years until 20 March 2022, and by how much.Note: You should assume that both the value of Opal Elder’s estate and the nil rate band will remain unchanged.(2 marks)(10 marks)103Glacier Ltd runs a business providing financial services. The following information is available in respect of the company’s value added tax (VAT) for the quarter ended 31 March 2015:(1)Invoices were issued for sales of £44,600 to VAT registered customers. Of this figure, £35,200 was in respectof exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is exclusive of VAT.(2)In addition to the above, on 1 March 2015 Glacier issued a VAT invoice for £8,000 plus VAT of £1,600 to aVAT registered customer. This was in respect of a contract for financial services which will be completed on15 April 2015. The customer paid for the contract in two instalments of £4,800 on 31 March 2015 and30 April 2015.(3)Invoices were issued for sales of £289,100 to non-VAT registered customers. Of this figure, £242,300 was inrespect of exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is inclusive of VAT.(4)The managing director of Glacier Ltd is provided with free fuel for private mileage driven in her company motorcar. During the quarter ended 31 March 2015, this fuel cost Glacier Ltd £260. The relevant quarterly scale charge is £408. Both these figures are inclusive of VAT.For the quarters ended 30 September 2013 and 30 June 2014, Glacier Ltd was one month late in submitting its VAT returns and in paying the related VAT liabilities. All of the company’s other VAT returns have been submitted on time.Required:(a)Calculate the amount of output VAT payable by Glacier Ltd for the quarter ended 31 March 2015.(4 marks)(b)Advise Glacier Ltd of the default surcharge implications if it is one month late in submitting its VAT returnfor the quarter ended 31 March 2015 and in paying the related VAT liability.(3 marks)(c)State the circumstances in which Glacier Ltd is and is not required to issue a VAT invoice, and the periodduring which such an invoice should be issued.(3 marks)(10 marks)4Sophie Shape has been a self-employed sculptor since 1996, preparing her accounts to 5 April. Sophie’s tax liabilities for the tax years 2013–14 and 2014–15 are as follows:2013–142014–15££Income tax liability5,2406,100Class 2 national insurance contributions143143Class 4 national insurance contributions1,2401,480Capital gains tax liability04,880No income tax has been deducted at source.Required:(a)Prepare a schedule showing the payments on account and balancing payment which Sophie Shape will havemade, or will have to make, during the period from 1 April 2015 to 31 March 2016.Note: Your answer should clearly identify the relevant due date of each payment.(4 marks)(b)State the implications if Sophie Shape had made a claim to reduce her payments on account for the tax year2014–15 to nil without any justification for doing so.(2 marks)(c)Advise Sophie Shape of the latest date by which she can file a paper self-assessment tax return for the taxyear 2014–15.(1 mark)(d)State the period during which HM Revenue and Customs (HMRC) will have to notify Sophie Shape if theyintend to carry out a compliance check in respect of her self-assessment tax return for the tax year 2014–15, and the possible reasons why such a check would be made.Note: You should assume that Sophie will file her tax return by the filing date.(3 marks)(10 marks)5On 6 April 2014, Simon Bass, who was born on 14 June 1991, commenced employment with Echo Ltd as a music critic. On 1 January 2015, he commenced in partnership with Art Beat running a small music venue, preparing accounts to 30 April. The following information is available for the tax year 2014–15:Employment(1)During the tax year 2014–15, Simon was paid a gross annual salary of £23,700.(2)During May 2014, Echo Ltd paid £11,600 towards Simon’s removal expenses when he permanently moved totake up his new employment with the company, as he did not live within a reasonable commuting distance. The £11,600 covered both his removal expenses and the legal costs of acquiring a new main residence.(3)Throughout the tax year 2014–15, Echo Ltd provided Simon with living accommodation. The company hadpurchased the property in 2004 for £89,000, and it was valued at £143,000 on 6 April 2014. The annual value of the property is £4,600. The property was furnished by Echo Ltd during March 2014 at a cost of £9,400.Partnership(1)The partnership’s tax adjusted trading profit for the four-month period ended 30 April 2015 is £29,700. Thisfigure is before taking account of capital allowances.(2)The only item of plant and machinery owned by the partnership is a motor car which cost £18,750 on1 February 2015. The motor car has a CO2emission rate of 155 grams per kilometre. It is used by Art, and40% of the mileage is for private journeys.(3)Profits are shared 40% to Simon and 60% to Art. This is after paying an annual salary of £6,000 to Art. Property income(1)Simon owns a freehold house which is let out furnished. The property was let throughout the tax year 2014–15at a monthly rent of £660.(2)During the tax year 2014–15, Simon paid council tax of £1,320 in respect of the property, and also spent£2,560 on purchasing new furniture.(3)Simon claims the wear and tear allowance.Required:(a)Calculate Simon Bass’s taxable income for the tax year 2014–15.(13 marks)(b)State TWO advantages for the partnership of choosing 30 April as its accounting date rather than 5 April.(2 marks)(15 marks)6You are a trainee accountant and your manager has asked you to correct a corporation tax computation which has been prepared by the managing director of Naive Ltd, a company which manufactures children’s board games. The corporation tax computation is for the year ended 31 March 2015 and contains a significant number of errors: Naive Ltd – Corporation tax computation for the year ended 31 March 2015£T rading profit (working 1)494,200 Loan interest received (working 2)32,100–––––––––526,300 Dividends received (working 3)28,700–––––––––555,000–––––––––Corporation tax (555,000 at 21%)116,550–––––––––Working 1 – Trading profit£Profit before taxation395,830 Depreciation15,740 Donations to political parties400 Qualifying charitable donations900 Accountancy2,300 Legal fees in connection with the issue of loan notes (the loan was used to financethe company’s trading activities) 5,700 Entertaining suppliers3,600 Entertaining employees1,700 Gifts to customers (pens costing £40 each and displaying Naive Ltd’s name)920 Gifts to customers (food hampers costing £45 each and displaying Naive Ltd’s name)1,650 Capital allowances (working 4)65,460–––––––––T rading profit494,200–––––––––Working 2 – Loan interest received£Loan interest receivable32,800 Accrued at 1 April 201410,600 Accrued at 31 March 2015(11,300)–––––––––Loan interest received32,100–––––––––The loan was made for non-trading purposes.Working 3 – Dividends received£From unconnected UK companies20,700 From a 100% UK subsidiary company8,000–––––––––Dividends received28,700–––––––––These figures were the actual cash amounts received.Working 4 – Capital allowancesMain Motor Special Allowancespool car rate pool££££Written down value (WDV) brought forward12,40013,600AdditionsMachinery 42,300Motor car [1] 13,800Motor car [2] 14,000––––––––68,500Annual investment allowance (AIA)(68,500)68,500 Disposal proceeds(9,300)––––––––4,300Balancing allowance(4,300)(4,300)––––––––Writing down allowance (WDA) – 18%(2,520) x 50%1,260––––––––––––––––WDV carried forward 011,480––––––––––––––––––––––––T otal allowances65,460––––––––(1)Motor car [1] has a CO2emission rate of 110 grams per kilometre.(2)Motor car [2] has a CO2emission rate of 155 grams per kilometre. This motor car is used by the sales managerand 50% of the mileage is for private journeys.(3)All of the items included in the special rate pool at 1 April 2014 were sold for £9,300 during the year ended31 March 2015. The original cost of these items was £16,200.Other informationFrom your files, you note that Naive Ltd has one associated company (the 100% UK subsidiary company mentioned in working 3).Required:Prepare a corrected version of Naive Ltd’s corporation tax computation for the year ended 31 March 2015. Note: You should indicate by the use of zero any items in the computation of the trading profit for which no adjustment is required.(15 marks)End of Question PaperFundamentals Level – Skills Module, Paper F6 (UK)Specimen Exam Answers Taxation (United Kingdom)and Marking Scheme Section A1C(33,909 (41,865 –7,956) at 12%) + (40,835 (82,700 –41,865) at 2%) = £4,8862B3B£Personal allowance10,000Restriction (109,400 – 800 – 100,000 = 8,600/2)(4,300)––––––Restricted personal allowance5,700––––––4DLower of:£135,000 (180,000 x 9/12)£168,000 (224,000 x 9/12)5B456,000/4 = £114,0006A60,000 x 3% x 6/12 = £900 (period 1 October 2015 to 31 March 2016)7A2,700 (8,700 –6,000) x 5/3 = £4,500This is less than £4,900 (8,700 – 3,800)8C475,000 (800,000 – 325,000) x 20/80 = £118,7509D10D59,700 x 12% = £7,16411A12B15,000 – 8,000 = £7,00013CMarks 14D105,000 – 43,000 = £62,00015 A–––2 marks each30–––Section B Marks 1(a)Delroy and Grant(i)Grant – Capital gains tax liability 2014–15£Ordinary shares in Dub LtdDisposal proceeds240,000½Cost (25,000)1––––––––215,000 Annual exempt amount(11,000)½––––––––204,000––––––––Capital gains tax: 204,000 at 28%57,1201–––––––––––3–––Tutorial notes:(1)Because the whole of Delroy’s chargeable gain has been held over, Grant effectively took over theoriginal cost of £25,000.(2)The disposal does not qualify for entrepreneurs’ relief as Grant was neither an officer nor anemployee of Dub Ltd.(ii)(1)The disposal would have qualified for entrepreneurs’ relief as Delroy was the sales director of Dub Ltd, and his shareholding of 25% (25,000/100,000 x 100) was more than the minimum requiredholding of 5%.1(2)The capital gains tax liability would therefore have been calculated at the rate of 10%.½(3) There are no capital gains tax implications regarding a gift of cash. ½–––2–––(b)Marlon and Alvita(i)Marlon – Chargeable gain 2014–15££HouseDisposal proceeds497,000½Cost 146,000½Incidental costs (2,900 + 3,700)6,6001––––––––(152,600)––––––––344,400Principal private residence exemption (229,600)1–––––––––––114,8003–––––––––––(1)One-third of Marlon’s house was always used exclusively for business purposes, so the principalprivate residence exemption is restricted to £229,600 (344,400 x 2/3).(ii)(1)The capital gains tax saving if 50% ownership of the house had been transferred to Alvita prior to its disposal would have been £6,266, calculated as follows:£Annual exempt amount11,000 at 28%3,0801Lower rate tax saving31,865 at 10% (28% –18%)3,1861–––––––––6,2662–––––––––10–––Tutorial note:Transferring 50% ownership of the house to Alvita prior to its disposal would haveenabled her annual exempt amount and lower rate tax band of 18% for 2014–15 to be utilised.Marks 2(a)(i)Opal Elder – Chargeable estate££Property (374,000 + 442,000)816,000½Repayment mortgage160,000½Endowment mortgage01––––––––(160,000)––––––––656,000 Motor cars172,000½Investments (47,000 + 36,000 + 69,000)152,0001––––––––980,000 Bank loan22,400½Legal fees01––––––––(22,400)–––––––––––Chargeable estate 957,6005–––––––––––Tutorial notes:(1)There is no deduction in respect of the endowment mortgage as this will be repaid upon death bythe life assurance element of the mortgage.(2)The promise to pay the nephew’s legal fees is not deductible as it is not legally enforceable.(ii)Opal Elder – Inheritance tax on death estate£Chargeable estate957,600––––––––IHT liability 105,000 (working) at nil%0W 852,600 at 40% 341,040½––––––––341,040––––––––(1)The personal representatives of Opal’s estate will be responsible for paying the inheritance tax.1Working – Available nil rate band£Nil rate band325,000½Potentially exempt transfers – 14 August 20050½–7 November 2014(220,000)½––––––––––––105,0003––––––––––––Tutorial note:The potentially exempt transfer on 14 August 2005 is exempt from inheritance tax as itwas made more than seven years before 20 March 2015.(b)(1)If Opal were to live for another seven years, then the potentially exempt transfer on 7 November 2014would become exempt.1(2)The inheritance tax payable in respect of her estate would therefore decrease by £88,000 (220,000 at40%).1–––2–––10–––。

acca报名流程超详细版

acca报名流程超详细版ACCA(特许公认会计师公会)报名流程可以分为以下几个详细步骤:1. 了解ACCA资格要求:-在报名之前,确保你符合ACCA的入学要求。

ACCA通常要求学生拥有相当于英国高中毕业的学历,例如两个'A'级水平及其等价的学历。

2. 创建MyACCA账户:-访问ACCA官方网站。

-点击“Register now”或“Apply now”按钮开始创建账户。

-填写个人资料,包括姓名、地址、电子邮件等。

-设置安全问题和密码。

-提交注册信息并等待确认邮件。

3. 提交申请材料:-登录MyACCA账户。

-完成在线申请表,包括教育背景和工作经验等信息。

-上传必要的文件,如学历证明、身份证明和英语水平证明(如果适用)。

-选择你打算参加的ACCA考试科目。

4. 支付费用:-根据选择的考试科目和注册类型,支付相应的注册费、年费和考试费。

-费用可以通过信用卡、借记卡或其他在线支付方式支付。

5. 等待审核:-提交申请后,ACCA会对你的资料进行审核。

-如果需要额外的资料或有任何问题,ACCA会通过电子邮件与你联系。

6. 获得确认:-一旦你的申请被批准,你会收到一封确认邮件,其中包含你的ACCA注册号和接下来的步骤。

7. 考试准备:-你可以开始准备ACCA考试,可以选择自学或加入ACCA认可的教育机构。

-你还可以通过MyACCA账户访问学习资源和练习材料。

8. 考试报名:-登录MyACCA账户,选择考试周期和科目,进行考试报名。

-确认考试日期和考试中心。

-再次支付所选考试科目的费用。

9. 参加考试:-在确认的考试日期和地点参加考试。

-考试通过后,继续完成剩余的科目。

10. 持续专业发展:-成为ACCA会员后,需遵守ACCA的持续专业发展(CPD)要求,确保专业知识和技能的持续更新。

请注意,上述流程可能会有所变动,具体步骤应以ACCA官方网站提供的最新信息为准。

另外,由于报名流程可能涉及个人信息的处理,请确保在安全的网络环境下操作,并保护好个人隐私。

ACCA

新手导航:ACCA报考指南及常见相关问题汇总2009年6月ACCA各科考试通过率教材真题下载:[ACCA]—2009年6月考题及答案超级汇总版[ACCA]ACCA历年全球统考考题汇总[ACCA]—历年试题下载汇总(P1—P7,F1—F9)[ACCA]—新旧大纲历年试题下载汇总(P1—P7,F1—F9)ACCA教材下载—F1_chapter1-3(word版)ACCA教材下载—F5_word版[ACCA]—2009年F4模拟试题课件及讲义:[ACCA]—2009年12月份各科讲义下载汇总F4—公司法和商法—讲义下载09年12月f4讲义09.6 F9讲义及练习[ACCA考试]《F1 会计师与企业Accountant in Business (AB)》讲座课件下载[ACCA考试]《F2 管理会计Management Accounting(MA)》讲座课件下载[ACCA考试]《F3 财务会计Financial Accounting (FA)》讲座课件下载[ACCA考试]《F7 财务报告Financial Reporting (FR)》讲座课件下载[ACCA考试]《F8 审计与认证服务Audit and Assurance Services(AAS)》讲座课件下载备考辅导:F5复习资料F9复习资料整理分享2009年11月考官文章汇总资料2009年10月考官文章汇总资料2009年12月ACCA考试tips大全!ACCA字典会计科目中英对照经验分享:[经验分享]ACCA看书有诀窍[经验分享]中国ACCA第一人:吴卫军[经验分享]我的ACCA考试经验、教训以及建议[经验分享]F7,F9 的攻略(ACCA考试总结)[经验分享]ACCA考试高手的经验[经验分享]ACCA考试技巧与学习方法[经验分享]ACCA工作经验-work Experience[经验分享]—ACCA考试试题的特点及做题技巧分析[经验分享]—ACCA考试技巧与学习方法![经验分享]—ACCA三遍循环法[经验分享]—ACCA考试实战攻略(1)[经验分享]—ACCA考试实战攻略(2)[ACCA考试]《F3 财务会计 Financial Accounting (FA)》讲座课件下载ACCA F6 真题[ACCA]ACCA各Paper考官一览表[ACCA考试]《F1 会计师与企业 Accountant in Business (AB)》讲座课件下载[ACCA考试]2007年12月开始执行的新大纲的模拟试题[ACCA]ACCA历年全球统考考题汇总[ACCA]教材相关问题汇总[转贴]我是这样考过ACCA的(word版)[转贴]ACCA考试经验及P1.2-P2.2攻略(完整下载版)[转帖]ACCA看书有诀窍[转帖]中国ACCA第一人:吴卫军[转帖]我的ACCA考试经验、教训以及建议[ACCA考试]《F8 审计与认证服务 Audit and Assurance Services(AAS)》讲座课件下载[ACCA考试]《F2 管理会计 Management Accounting(MA)》讲座课件下载[ACCA考试]《F7 财务报告 Financial Reporting (FR)》讲座课件下载[ACCA]ACCA 考试报考指南ACCA 考试介绍特许公认会计师公会(The Association of Chartered Certified Accountants,简称ACCA) 成立于1904年,是目前全球最大的国际会计师组织。

公路工程标准施工招标文件-2018年版

中华人民共和国交通运输部公路工程标准施工招标文件(2018 年版)交通运输部公告2017 年第51 号自2018 年3 月1 日起施行交通运输部关于发布公路工程标准施工招标文件及公路工程标准施工招标资格预审文件2018 年版的公告(交通运输部公告2017 年第51 号)为加强公路工程施工招标管理,规范招标文件及资格预审文件编制工作,依照《中华人民共和国招标投标法》《中华人民共和国招标投标法实施条例》等法律法规,按照《公路工程建设项目招标投标管理办法》(交通运输部令 2015 年第 24 号),在国家发展改革委牵头编制的《标准施工招标文件》及《标准施工招标资格预审文件》(以下简称《标准文件》)基础上,结合公路工程施工招标特点和管理需要,交通运输部组织制定了《公路工程标准施工招标文件》(2018 年版)及《公路工程标准施工招标资格预审文件》(2018 年版)(以下简称《公路工程标准文件》),现予发布。

《公路工程标准文件》(2018 年版)自 2018 年 3 月 1 日起施行,原《公路工程标准文件》(交公路发〔2009〕221 号)同时废止,之前根据《公路工程标准文件》(2009 年版)完成招标工作的项目仍按原合同执行。

自施行之日起,依法必须进行招标的公路工程应当使用《公路工程标准文件》(2018 年版),其他公路项目可参照执行。

在具体项目招标过程中,招标人可根据项目实际情况,编制项目专用文件,与《公路工程标准文件》(2018 年版)共同使用,但不得违反国家有关规定。

《公路工程标准文件》(2018 年版)中“申请人须知”“资格审查办法”“投标人须知”“评标办法”和“通用合同条款”等部分,与《标准文件》内容相同的只保留条目号,具体内容见《标准文件》。

《公路工程标准文件》电子文本可在交通运输部网站()“下载中心”下载。

请各省级交通运输主管部门加强对《公路工程标准文件》(2018 年版)贯彻落实情况的监督检查,注意收集有关意见和建议,及时反馈。

acca副高级职称 申请高级

acca副高级职称申请高级

摘要:

一、引言

二、ACCA 副高级职称的申请条件

三、申请高级职称的流程

四、申请过程中需要准备的材料

五、注意事项

六、总结

正文:

一、引言

ACCA,即Association of Chartered Certified Accountants,特许公认会计师公会,是国际上具有影响力的财会职业会员组织。

在我国,ACCA 会员可以申请副高级职称。

本文将详细介绍申请ACCA 副高级职称的相关条件和流程。

二、ACCA 副高级职称的申请条件

1.持有ACCA 会员证书;

2.具有本科及以上学历;

3.持有相关行业的工作经验证明;

4.通过副高级职称评审。

三、申请高级职称的流程

1.准备申请材料:学历证书、ACCA 会员证书、工作经验证明等;

2.在线填写申请表格,并上传相关材料;

3.提交申请,等待审核;

4.审核通过后,参加副高级职称评审;

5.通过评审,获得副高级职称证书。

四、申请过程中需要准备的材料

1.个人基本信息:身份证、护照等;

2.学历证明:学位证书、毕业证书等;

3.ACCA 会员证书;

4.工作经验证明:单位出具的工作经历证明或劳动合同等;

5.个人简历:详细列出个人工作经历、项目经验等。

五、注意事项

1.申请材料需真实、完整、有效;

2.申请过程中,确保个人信息的准确性;

3.按照规定的流程和时间节点完成申请;

4.评审通过后,及时领取职称证书。

六、总结

申请ACCA 副高级职称是一个严谨的过程,需要满足一定的条件,按照规定的流程准备材料。

考会计证在哪里报名啊

考会计证在哪里报名啊

如果你想考取会计证,可以通过以下几种方式进行报名。

1. 中国注册会计师协会(ACCA)

中国注册会计师协会是中国财政部批准的全国性会计师组织,负责注册会计师的资格认证和管理工作。

你可以访问ACCA的

官方网站,了解报名要求和流程。

在网站上你可以找到最新的报名信息和考试日期。

你需要填写报名表格,缴纳报名费,并提交相关的证明材料。

2. 国家会计职称考试

国家会计职称考试是中国财政部主管的会计专业职称考试,灵活性较强,适用于不同层次和专业背景的人员。

你可以在中国财政部的官方网站上了解更多的信息。

根据你的专业背景和职称要求,选择合适的职称级别,并填写相应的报名表格。

3. 大学、高级职业学校和培训机构

一些大学、高级职业学校和培训机构也提供会计证的培训和考试报名服务。

你可以前往相关的学校或机构,咨询报名要求和流程。

通常你需要填写报名表格,并提供相关的材料,如身份证复印件和学历证明。

总而言之,无论你选择哪种方式报名,你都需要仔细阅

读相关的报名信息和要求,并按照要求准备好提供的证明材料。

报名成功后,注意及时关注考试的时间和地点,合理安排学习时间,以便顺利通过会计证考试。

【最新】 ACCA 第三阶段备考攻略汇总(AFM、AAA、ATX、APM篇)(5)

【最新】ACCA 第三阶段备考攻略汇总(AFM、AAA、ATX、APM篇)(5)今天,我们一起来看看Top Winners在AFM、AAA、ATX和APM这四门科目上的考试锦囊。

高级财务管理(Advanced Financial Management)获奖学员:袁晨希、陈强瑜(上海对外经贸大学)、成哲颖(西安交通大学)AFM的时间规划和学习安排袁晨希:根据可支配的时间及学习提纲提前做好学习和复习计划,建议至少留一个月用于复习和做题。

陈强瑜:2个半月理解知识点,掌握大题计算逻辑;半个月完成BPP练习册,并将已整理知识点反复记忆;半个月按照考场要求完成真题模卷,提升时间管理能力。

成哲颖:先做例题,然后做真题,了解考官的出题思路和考试类型;把所有的文字部分都整理出来,方便考前复习;考前一个月左右进入最后复习状态,错题动手操练,并深入理解、记忆和背诵文字部分。

AFM的要点和难点袁晨希:Investment Appraisal中NPV的计算需要正确理解题意并完整收集信息;并购重组的题目较为综合和灵活;Forex Risk 和 InterestRate Risk 的考点及出题方式较为固定,其中汇率的题目对于汇率的使用较易混淆,建议总结一套记忆技巧。

陈强瑜:我认为重要的知识点是风险管理(金融衍生品的计算),企业并购与重组(估值计算),投资评估(APV),股息规划等;APV计算较难,虽然计算框架较易搭建,但是数据很多且繁琐。

成哲颖:Interest Risk和Currency Risk是每次必考考点;Financial Reconstruction & Reorganization是难点,同学们可以多复习。

AFM的复习渠道和材料袁晨希:我个人还报名了一些网课和线下课程,经过老师的点拨,我更能理解知识点和答题思路。

陈强瑜:官网上的历年真题,考前可以模拟练练手感。

考前串讲也能够有效地查漏补缺。

张锦越:真题是最有参考意义的。

内地与香港注册会计师部分考试科目互免问题介绍材料之四

内地与香港注册会计师部分考试科目互免问题介绍材料之四内地与香港部分考试科目相互豁免常见问题回答1.问:内地与香港部分考试科目相互豁免是由何而来的?答:2004年8月27日,为了促进内地与香港注册会计师行业的共同发展,中华人民共和国财政部会计司和香港特别行政区财经事务及库务局在与两地注册会计师协会共同研究的基础上,签署了《内地与香港注册会计师部分考试科目相互豁免协议》,协议规定:参加内地注册会计师全国统一考试并全科合格的人员,在报名应考香港会计师公会的专业资格课程时,可以豁免“财务管理”和“审计和资讯管理”两个单元科目;参加香港会计师公会的专业资格课程考试并全科合格的人员,在报名应考内地注册会计师全国统一考试时,可以豁免“财务成本管理”和“审计”两个考试科目。

2. 问:两地部分考试科目相互豁免从什么时候开始生效?将持续多长时间?答:两地部分考试科目相互豁免从2004年8月27日起正式生效,并于2005年5月19日后开始实施。

即从2005年度注册会计师考试开始中国注册会计师协会和香注册会计师公会可以接受部分考试科目豁免申请。

目前,考试豁免期限没有限制。

3. 问:我参加了内地注册会计师全国统一考试,并取得了审计和财务成本管理两科单科合格成绩,那么我可以申请获得香港专业资格课程相应考试科目豁免吗?答:不可以。

按照《内地与香港注册会计师部分考试科目相互豁免协议》的规定,只有参加内地注册会计师全国统一考试并且全部合格的人员(领有全科合格证人员),才可以申请香港专业资格课程部分考试科目豁免。

同理,只参加并通过香港专业资格课程审计和资讯管理、财务管理两科目考试也不能相应豁免内地注册会计师的考试。

必须取得香港专业资格课程考试并且全部合格的人员才可以申请内地注册会计师部分考试科目豁免。

4. 问:我是香港会计师公会会员,我可以申请内地注册会计师考试科目豁免吗?答:要视情况而定。

香港会计师公会会员分为三种,分别为:通过与ACCA联合考试计划的会员,通过与其他海外会计师组织签订资格互认协议的会员和通过专业资格课程考试认证的会员。

CIA--八种国际认可证书之一

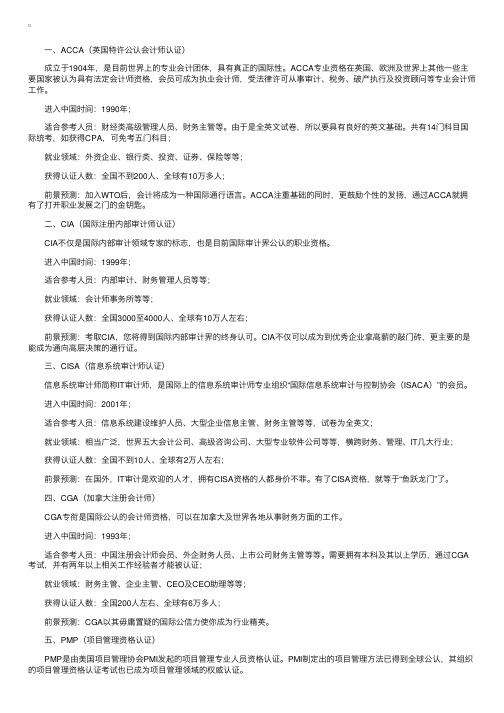

⼀、ACCA(英国特许公认会计师认证) 成⽴于1904年,是⽬前世界上的专业会计团体,具有真正的国际性。

ACCA专业资格在英国、欧洲及世界上其他⼀些主要国家被认为具有法定会计师资格,会员可成为执业会计师,受法律许可从事审计、税务、破产执⾏及投资顾问等专业会计师⼯作。

进⼊中国时间:1990年; 适合参考⼈员:财经类⾼级管理⼈员、财务主管等。

由于是全英⽂试卷,所以要具有良好的英⽂基础。

共有14门科⽬国际统考,如获得CPA,可免考五门科⽬; 就业领域:外资企业、银⾏类、投资、证券、保险等等; 获得认证⼈数:全国不到200⼈、全球有10万多⼈; 前景预测:加⼊WTO后,会计将成为⼀种国际通⾏语⾔。

ACCA注重基础的同时,更⿎励个性的发扬,通过ACCA就拥有了打开职业发展之门的⾦钥匙。

⼆、CIA(国际注册内部审计师认证) CIA不仅是国际内部审计领域专家的标志,也是⽬前国际审计界公认的职业资格。

进⼊中国时间:1999年; 适合参考⼈员:内部审计、财务管理⼈员等等; 就业领域:会计师事务所等等; 获得认证⼈数:全国3000⾄4000⼈、全球有10万⼈左右; 前景预测:考取CIA,您将得到国际内部审计界的终⾝认可。

CIA不仅可以成为到优秀企业拿⾼薪的敲门砖,更主要的是能成为通向⾼层决策的通⾏证。

三、CISA(信息系统审计师认证) 信息系统审计师简称IT审计师,是国际上的信息系统审计师专业组织“国际信息系统审计与控制协会(ISACA)”的会员。

进⼊中国时间:2001年; 适合参考⼈员:信息系统建设维护⼈员、⼤型企业信息主管、财务主管等等,试卷为全英⽂; 就业领域:相当⼴泛,世界五⼤会计公司、⾼级咨询公司、⼤型专业软件公司等等,横跨财务、管理、IT⼏⼤⾏业; 获得认证⼈数:全国不到10⼈、全球有2万⼈左右; 前景预测:在国外,IT审计是欢迎的⼈才,拥有CISA资格的⼈都⾝价不菲。

有了CISA资格,就等于“鱼跃龙门”了。

acca sbl 12月 pre seen 材料解读 -回复

acca sbl 12月pre seen 材料解读-回复关于ACCA SBL 12月Pre-seen材料的解读ACCA(特许公认会计师协会)SBL(战略商务领导)考试是ACCA职业资格中的重要科目之一。

在12月的备考中,学员们将开始研究和分析Pre-seen材料,以便更好地应对考试。

在本文中,我们将一步一步地解读这些材料,并提供一些建议,以帮助学员们在考试中取得成功。

第一步:阅读材料并建立框架首先,学员们应该仔细阅读Pre-seen材料,并理解其中所提供的信息。

这包括公司的背景、组织结构、战略目标、财务状况等。

学员们可以将这些信息整理成一个框架,以便更好地组织和理解材料。

例如,可以将公司的组织结构制作成一个组织图,标示出不同的部门和职能,并将战略目标和财务状况与各部门相关联。

第二步:分析问题并制定解决方案在理解了Pre-seen材料的基础上,学员们应该开始分析材料中提出的问题,并制定相应的解决方案。

这些问题可能涉及到公司的战略问题、业务流程改进、财务管理等方面。

为了更好地回答这些问题,学员们可以根据材料中提供的信息,运用SWOT分析、PESTEL分析等工具和框架,深入分析公司的内部和外部环境,并找出解决问题的途径和方法。

第三步:与实际经验和理论知识结合在进行材料分析和解决方案制定的过程中,学员们应该运用自己的实际经验和理论知识,来进一步丰富和支持自己的分析和建议。

比如,学员们可以结合自己在实际工作中的经验,提供实际操作性的解决方案;同时,也可以结合自己学习ACCA课程中的知识,为自己的分析提供专业性的支持。

第四步:考虑利益相关方和可持续发展在解决问题和制定解决方案的过程中,学员们应该考虑到不同利益相关方的需求和期望,以及公司的可持续发展。

这包括股东、员工、客户、社会和环境等方面。

学员们可以通过分析材料,了解公司目前面临的挑战和机遇,制定可持续发展的战略,并考虑各利益相关方的需求,以实现公司的长期发展目标。

ACCA注册报名材料:大学英语考试六级证书(翻译样本)

ACCA注册报名材料:大学英语考试六级证书(翻译样本)CET-6大学英语考试六级证书IDENTITY CARD THE PEOPLE'S REPUBLIC OF CHINAName:_______________Sex:_______________Date of Birth:_______________Nationality:_______________Chinese Address:_______________Issuing Date:_______________Validity:ID Number:_______________Certificate of College English TestThis is to certify that __________,a student of Grade __________ at Department of __________,__________ University/Institute,passed the examination of College English Test Band-6(CET-6)in January/June XXXX.Upon examination,he/she has fulfilled the band 6 requirements College English Syllabus Band Six with excellent/qualified score and is hereby awarded the Certificate of CET-6.Department of Higher EducationState Education Commission(国家教委)或Ministry of Education(教育部)Date of Issuance:_______________Certificate No.:_______________Test for English MajorsThis is to certify that__________,a student of __________ from __________,participated in the TEM __________ exam(Test for English Majors)organized by the English Group of the National Higher Education Foreign Language Major Teaching Supervisory Committee of the State Education Ministry and passed the exam.Hereby he/she is awarded the TEM-__________Certificate.Issuing Date:_______________Certificate No.:_______________English GroupNational Higher Education Foreign Language MajorTeaching Supervisory Committee(seal) Transcript Report of College English Test Band-6Name:_______________University:_______________Institute/Department:_______________Exam Attendance Docket No.:_______________ID Card No.:_______________Exam Time:_______________Total Score:_______________Transcript No.:_______________Department of Higher EducationMinistry of EducationEntrust to Issue by:National College English Testing Committee(Seal)此文为浦江.财经原创,如需转载请注明出处!。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2015年ACCA报名材料有哪些?

本文由高顿ACCA整理发布,转载请注明出处

根据高顿网校ACCA:

在校学生所需准备的ACCA注册报名材料

中英文在校证明(原件必须为彩色扫描件)

中英文成绩单(均需为加盖所在学校或学校教务部门公章的彩色扫描件)

中英文个人身份证件或护照(原件必须为彩色扫描件、英文件必须为加盖所在学校或学校教务部门公章的彩色扫描件)

2寸彩色护照用证件照一张

用于支付注册费用的国际双币信用卡或国际汇票(推荐使用Visa)

非在校学生所需准备的ACCA注册报名资料(符合学历要求)

中英文个人身份证件或护照(原件必须为彩色扫描件、英文件必须为加盖翻译公司翻译专用章的彩色扫描件)

中英文学历证明(原件必须为彩色扫描件、英文件必须为加盖翻译公司翻译专用章的彩色扫描件*MPAcc专业,需提供中英文成绩单*国外学历均需提供成绩单)

2寸彩色护照用证件照一张

用于支付注册费用的国际双币信用卡或国际汇票(推荐使用Visa)

非在校学生所需准备的ACCA注册报名资料(不符合学历要求- FIA形式)

中英文个人身份证件或护照(原件必须为彩色扫描件、英文件必须为加盖翻译公司翻译专用章或者学校教务部门公章的彩色扫描件)

2寸彩色护照用证件照一张

用于支付注册费用的国际双币信用卡或国际汇票(推荐使用Visa)

更多ACCA资讯请关注高顿ACCA官网:。