日本失去的十年英文ppt

雾社事件,赛德克巴莱,英语PPT

Thank you

This incident has reflected a kind of national spirit .All of them had the aspect of the national energy which has encouraged them to fight against Japanese .

Part I : The Sun Flag Part II : The Rainbow Bridge

The most expensive produvtion in Taiwan. 12 Years 700 milus grovel is called civilization, and that I will take you to see the pride of savage. 如果文明让我们卑躬屈膝,那我就让你们看见野蛮 的骄傲。 A real man can sacrifice his body, but he must win his soul. 一个真正的人可以牺牲他的性命,但他必须赢得灵 魂。

Film andAA TRUE True Story AA FILM AND STORY

1 . a true story–Wushe incident 2 . a film - Seediq Bale true story –wushe incident

Wushe incident

The Wushe incident(雾社) began in October 1930 and was the last major uprising against colonial Japanese forces in Taiwan. In response to long-term oppression by Japanese authorities, the Seediq indigenous group in Wushe attacked the village, killing over 130 Japanese. In response, the Japanese led a relentless counter-attack, killing over 600 Seediq in retaliation.

流动性陷阱PPT课件

2021

25

流动性陷阱

2. “钱”多的第二个原因是居民总体 的消费意愿下降、储蓄上升,而这同中 国收入分配结构日趋不合理有着密切的 关系。从国际上通用的衡量收入分配结 构的指标、即基尼系数看,中国在1994 年就已经超过了分配结构不合理的警界 线,并且,还呈现日趋恶化的态势。

2021

26

流动性陷阱

2021

18

流动性陷阱

(二)流动性陷阱在 实体经济中的表现

2021

19

流动性陷阱

流动性陷阱在实体经济中的表现是国内需求开 始下滑。在中国GDP的支出构成中,投资和消费占 比一直在95%以上,其中,投资需求占比、即资本 形成率具有典型的顺周期特征,而消费占比自上个 世纪80年代以来一直处于下降态势。

行体系,逼使银行贷出更多本地贷往更有利可图的海

外新兴市场。斯蒂格利茨和其他人亦指出,银行亦会投

资外币,这有机会引发货币战争,尤其中国或许将有所

反应。

2021

33

流动性陷阱

3、其他观点 “ 流动性陷阱”的存在,意味着运用货币手段来解决经济 萧条问题可能是无效的。这一结论动摇了古典学派的理论 根基。因此,围绕流动性陷阱问题,西方经济学界争论很 大。凯恩斯学派代表人物之一,美国经济学家J.托宾在其 早期论文中,曾运用若干资料证明了流动性陷阱的存在, 并明确得出货币政策不如财政政策有效的结论。然而,另 两位美国经济学家M.布隆芬布雷纳和T.迈耶同样进行了实 证研究,却得出流动性陷阱并不存在的结论。货币主义代 表人物M.弗里德曼则持某种折衷态度。一方面,他否定有 流动性陷阱存在;另一方面,他又认为市场利率不可能无 限降低,因为人们需要以货币来替代其他金融资产的普遍 愿望会使利率的下降有一个最低的限度。

日本失去的十年

日本企业获得的国内,海外投资趋势 图

泡沫经济前后,日本各大银行对主要行业贷款额的 推移

资本市场获得投资在增加,生产领域获得投资却在减少

日本股票,土地价格变化

房地产价 格变化

在

地

产 价

年 股

格票

均 狂

, 土

跌地

,

房

1990

日本 1990 年贴现率变 化

股泡 票沫 与经 土济 跌地崩 的溃 价后 格日 狂本

(%)

世世 :1998 世 1999 年为财政年度数字,其余为自然年数字。 1998 和 1999 财年政府支出增长数字为公共消费开支增长速度数

字。

资料来源 : 日本经济企划厅 : 《国民经济计算》 (1998 、 2000 年 ) 。

返回

总览 GDP

返回

Part 3 经济萧条对 2000 年后的影 响

M2+CD(10亿日元)

M2+CD(10亿日元)

700000 600000 500000 400000 300000 200000 100000

0

1990 1991 1992 1993 1994 1995 1996 1997 1998

1999 2000

世世 20 世世 90 世世世世世世世世世世世世世世世世世

居民消费 住宅投资 设备投资 库存投资 政府支出 净出口

4.4 4.8 10.9 -27.0 3.2 -5.5

2.5 -8.5 6.3 56.8 2.8 123.2

2.1 -6.5 -5.6 -58.1 7.5 39.5

1.2 2.4 -10.2 -37.3 8.4 8.4

1.9 8.5 -5.3 -128.5 3.1 -12.5

日本福岛核辐射大学英语课堂PPT

Tokyo electric power company has abandoned re-works still be in danger of 1 to the idea of unit and stressed the Tokyo electric power company put processing f island first nuclear accident in the most preferred position.

What we all know is that exposed in the nuclear radiation is very dangerous. Excessive nuked will lead to many incurable diseases such as cancer and leukemia.Besides,the nuclear radiation can pollute the groudwater,which means that the animals drink the polluted water may die within a few years.In other words,it can cause a disaster in the long run.

It’s reported that the nuclear radiation has been found in our country now,both Beijing and Shanghai are detected nuclear material.However,the government has claimed that it is safe now in China,because the radiatiion does not reached the level of harm to human body.There is no need for us to be panic.

日本経済

停滞の具体的な 停滞の具体的な要因

資産価格の しい低下による、バランスシートの 資産価格の著しい低下による、バランスシートの悪化 価格 低下による 企業投資 歴史的な 投資の 企業投資の歴史的な停滞 少子化、高齢化による大衆の精神的活発性の しい低下 による大衆 低下。 少子化、高齢化による大衆の精神的活発性の著しい低下。 企業の債務返済による財政支出の乗数効果低下 返済による財政支出 企業の債務返済による財政支出の乗数効果低下 連立政権による政権交代での による政権交代での政変混乱 連立政権による政権交代での政変混乱 財務当局の失政(景気が回復基調に じた時点での消費税 時点での 財務当局の失政(景気が回復基調に転じた時点での消費税 率引き げや社会保険 給付引き 社会保険の 率引き上げや社会保険の給付引き締め) 日銀の金融緩和の不徹底や物価動向に逆行する金融政策の 日銀の金融緩和の不徹底や物価動向に逆行する金融政策の する金融政策 実施(速水優総裁 主導によるデフレ のゼロ金利解除等 総裁の によるデフレ下 金利解除等) 実施(速水優総裁の主導によるデフレ下のゼロ金利解除等) 大手金融機関 山一證券、三洋証券、北海道拓殖銀行、 金融機関( 大手金融機関(山一證券、三洋証券、北海道拓殖銀行、日 本長期信用銀行、日本債券信用銀行など など) 経営の 本長期信用銀行、日本債券信用銀行など)の経営の失敗 不良債権処理 先送り 処理の (不良債権処理の先送り)。 世界において相次いだ経済危機の余波( において相次いだ経済危機 世界において相次いだ経済危機の余波(1992年ポンド危 年ポンド危 危機、 機、1994年 - 1995年メキシコ危機、1997年アジア通貨危 年 年メキシコ危機 年アジア通貨危 機)

近期的日本经济

日本失去的十年英语

14 of 43

Thank you

End

5 of 43

The Japanese Slump

The Rise and Fall of the Nikkei

There are two reasons for the increase in a stock price:

•

A change in the fundamental value of the stock

9 of 43

The Japanese Slump

The Failure of Monetary and Fiscal Policy Monetary policy was used, but it was used too late, and when it was used, if faced the twin problems of the liquidity trap and deflation.

3 of 43

The Japanese Slump

Figure 2 Unemployment and Inflation in Japan since 1990 (percent) Low growth in output has led to an increase in unemployment. Inflation has turned into deflation.

7 of 43

The Japanese Slump

The Rise and Fall of the Nikkei

The fact that dividends remained flat while stock prices increased strongly suggests that a large bubble existed in the Nikkei. The rapid fall in stock prices had a major impact on spending—consumption was less affected, but investment collapsed.

日本失去的十年

日本失去的十年上世纪60-70年代,日本经济经历了黄金发展时期,经济高速增长,出口大幅提升,积累了大量的贸易顺差,其中主要是对美国的顺差。

80年代之后,日本与美国的双边贸易摩擦不断加剧,贸易战逐渐升级到汇率战,美国认为是日元低估造成日本对美的巨额贸易顺差。

在美国的压力下,1985年,五国集团(G5)签订了著名的“广场协议”,日元被迫大幅度升值。

其后,由于日本宏观政策的失误,日本遭遇了严重的资产泡沫,并于90年代初破灭,此后日本进入长达十年的经济萧条。

图一:日本经济增速的超级L型一、80年代日本的政治经济格局日本成为全球第二大经济体之后,日本经济的封闭性、管制性受到了当时国际社会的极大批判。

日本在70年代开始了经济结构调整、金融自由化和国际化改革,但是进程缓慢。

80年代之后,日本出于自身需要和国际压力的考虑,经济改革、金融自由化和国际化进程加快,日本政治经济面临三个重大的战略调整。

一是政治国际化。

日本政府一直希望通过积极参与国际经济政策协调行动,扩大国际影响、提升国际地位,实现其从“经济大国”走向“政治大国”的理想。

1983年,曾根康弘提出了日本的“大国思维战”战略,并把对美关系作为这一战略的基石。

二是金融、经济自由化、国际化。

20世纪80年代之后,日本放弃了战后一直延续的封闭和管制,逐步放宽了利率限制,修订了外汇与外贸管理法,开放了日本金融市场,并积极拓展日本银行海外业务。

1985年,日本政府发表了《关于金融自由化、日元国际化的现状与展望》公告,推进了日本利率市场化、金融业务开放、资本流动自由化和日元国际化等进程。

三是经济结构调整。

从20世纪80年代初期,国际社会要求日本开放国内市场、改变出口导向型经济增长模式的呼声日高,日本的经济增长模式由“外需主导型”向“内需主导型”转变的压力渐升。

日本政府也认为,出口导向型的经济增长模式已经不可持续,日本必须扩大内需,以缓和与国际社会的关系。

简言之,80年代中期,日本面临着三个重大的战略转变:一是由“管制经济”向“开放经济”的转变;二是由“经济大国”向“政治大国”的转变;三是由“外需主导型经济”向“内需主导型经济”的转变。

日本失去的十年

-0.1

2001年3月,公定贴现率从0.35%下调至0.25%。 银行同业间无担保隔夜拆借利率从0.25%降至 0.15%。

将货币政策操作目标由原来的隔夜拆借利率改为货 币供应量,即确定央行的活期存款余额作为操作目 标。具体是通过公开市场操作,增加金融机构在央 行的活期存款余额,以此来增加货币供应量,向市 场提供流动性资金。 将日本银行的活期存款余额由4万亿元日元增加至5 万亿日元,增幅约为25%。 继续实施宽松的货币政策,直到消费物价持续、稳 定保持0%以上的增长。 为了保证货币供应量的增加,在必要时可以增加从 二级市场回购长期国债的规模,以达到央行目标。

1989年年底对日本不动产价值的官方估计是20000

兆日元。虽然日本的国土面积仅是美国的二十五分 之一,日本不动产的价值却四倍于美国。在1990年 初,按当时的土地价格,用东京可以买下整个美国,用 日本皇宫一带的土地可以买下整个加拿大。

1989年5月 1989年底 1989年5月1990年8月 效果

• 公定贴现率从2.5%提高至3.25%

• 自1980年来首次提息

• 三重野康 • 3.75% 4.25%

• 连续5次提高公定贴现率 • 最终至6% • 股市重挫 • 货币供应量增速骤减

1991年7月1日, 公定贴现率6%下调到5.5%。不久 之后,日本银行又把公定贴现率进一步下调到5%和 4.5%。 1992年底,3.25%。 1993年2月,2.5%。

挤出效应 1999年2月,将银行同业间无担保隔夜拆借利 率诱导目标值设定为0.15%,同年3月,继续下 调至0.04%(零利率)。

GDP增长率%

6.8

5.3 5.5 4.4 2.9 0.5 0.4 0.6 3 0.5 3 2.1 1.1 -0.8 2.4 2 2

日本“失去的十年”

• 有一则故事足以让人体会到日本人的 疯狂,一栋报价4亿多美元的美国大楼 谈好要卖给日本人,只等付钱交割时, 日本人忽然拿出了新的合同书,上面 写的价格却变成了6.1亿美元,这让美 国人莫名其妙。日方人员解释说: “老板昨天在吉尼斯世界纪录里看到, 历史上单栋大楼出售的最高价是6亿美 元。我们愿意无偿追加2亿美元,就是 想要打破这个纪录。”

日本“失去的十年”

泡沫的形成

•“广场协议”

•阴谋?

广场协议

• 1985年9月22日,美国、日本、联邦 德国、法国以及英国的财政部长和中 央银行行长(简称G5)在纽约广场饭 店举行会议,达成五国政府联合干预 外汇市场,诱导美元对主要货币的汇 率有秩序地贬值,因协议在广场饭店 签署,故该协议又被称为“广场协 议”。

泡沫破灭

• 所有泡沫总有破灭的时候。1991年后, 随着国际资本获利后撤离,很大程度 上由外来资本推动的日本房地产泡沫 迅速破灭。

• 当时,国土面积相当于美国加利福尼 亚州的日本,其地价市值总额竟相当 于整个美国地价总额的4倍。仅东京都 的地价就相当于美国全国的总地价。

• 1、 资产价格缩水 • 股票价格从1990年起,开始下跌,到1992 年8月,已从38915的峰值跌至15000以下, 跌幅超过62%。98年跌破13000,1999在 130万亿日元的财政金融刺激下,才有所回 升,但也未能达到前期峰值的一半。 • 2、房地产价格下降,长期衰退的主要原因 • 从1992年开始,到2004年,经历了连续14 年的下降,这是明治维新以来的空前纪录。

•

1987年,日本三菱土地公司以14亿美元, 购买了纽约曼哈顿闹市洛克菲勒中心的14栋办 公大楼,成为拥有洛克菲勒中心80%股份的控 股公司。当时,洛克菲勒中心被视为美国的象 征,美国媒体将这一收购行为称为日本人“买 走了美国人的灵魂”。 1991年,东京亿万富翁横井英树又以4000 万美元,将被视为纽约心脏的帝国大985年,日本取代美国成为世界 上最大的债权国,日本制造的产 品充斥全球。日本资本疯狂扩张 的脚步,令美国人惊呼“日本将 和平占领美国!”

日本地震英文演讲ppt

The influence of the earthquake

• The impact of the earthquake in Japan is undoubtedly huge . Until March 19,4377 people were killed and 9083 missing . Life and property safety of people is in the face of danger. Nuclear radiation is threatening people's health .People are in panics. They lost their houses and families like the victims in Wenchuan, Chile, and Yushu. Meanwhile, the Japanese economy suffers a huge trauma . Many factories closed because of the destruction of the equipment and houses . The supply of electricity also stops in some places. After the earthquake, many animals died ,especially the Marine life.

• Television pictures showed that vehicles, houses and farmlands were rolled up, white hull is like a razor sharp landward crosscut. The place is disastrous(损失惨重 ( 的) .

The 1990s in Japan - A Lost Decade

October 2001, revised and expanded August 2003

*We thank Tim Kehoe, Nobu Kiyotaki, Ellen McGrattan and Lee Ohanian for helpful comments, and Sami Alpanda, Pedro Amaral, Igor Livshits, and Tatsuyoshi Okimoto for excellent research assistance and the Cabinet Office of the Japanese government, the United States National Science Foundation, and the College of Liberal Arts of the University of Minnesota for financial support. The views expressed herein are those of the authors.

2

1. INTRODUCTION The performance of the Japanese economy in the 1990s was less than stellar. The average annual growth rate of per capita GDP was 0.5 percent in the 1991-2000 period. The comparable figure for the United States was 2.6 percent. Japan in the last decade, after steady catch-up for 35 years, not only stopped catching up but lost ground relative to the industrial leader. The question is why. A number of hypotheses have emerged: inadequate fiscal policy, the liquidity trap, depressed investment due to over-investment during the “bubble” period of the late 1980s and early 1990s, and problems with financial intermediation. These hypotheses, while possibly relevant for business cycles, do not seem capable of accounting for the chronic slump seen ever since the early 1990s. This paper offers a new account of the “lost decade” based on the neoclassical growth model. Two developments are important for the Japanese economy in the 1990s. First and most important is the fall in the growth rate of total factor productivity (TFP). This had the consequence of reducing the slope of the steady-state growth path and increasing the steady-state capital-output ratio. If this were the only development, invesห้องสมุดไป่ตู้ment share and labor supply would decrease to their new lower steady-state values during the transition. But, the drop in the rate of productivity growth alone cannot account for the near-zero output growth in the 1990s. The second development is the reduction of the workweek length (average hours worked per week) from 44 hours to 40 hours between 1988 and 1993, brought about by the 1988 revision of the Labor Standards Law. In the most standard growth model, where aggregate hours (average hours worked times employment) enter the utility function of the stand-in consumer, a decline in workweek length does not affect the steady-state growth path because the decline is offset by an increase in employment. However, in our specification of the growth model, the workweek length and employment enter the utility function separately, so that a shortening of the workweek shifts the level of the steady-state growth path down. If the only change were a reduction in

90年代日本债务危机

日本金融业出现如此多问题的主要原因在于以下几 个方面:

1.日本的金融体系缺乏透明度和应变能力。

大和银行事件说明,日本的银行虽然拥有庞大的 资金量,但是却不很熟悉国际上先进的金融交易, 而且也暴露了银行内部管理混乱、信息度透明度低、 违法的秘密交易盛行等重ቤተ መጻሕፍቲ ባይዱ弊端。

2.严重的不良资产是导致众多金融机构破产 的重要因素。

日本政府采取的对策

1.提高金融体系的透明度,加强监管的力度。 2. 借鉴和采用美国的做法,改组东京共同银行,以 解决金融机构破产问题。 3.运用金融手段刺激经济的增长。

总之,解决日本金融危机的办法就是使错综复 杂的金融体系提高透明度,建立稳定的金融体系, 加强金融监管的力度。

对中国金融改革的启示

中国的金融体制改革需要借鉴国外的经验。 战后日本的金融制度、金融自由化、以及目前 所面临的金融危机,对于正在进行金融改革的 中国来说,有着许多令人深思的启示。 ① “取其精华,去其糟粕” ② “对外透明,积极应变”

第八小组

90年代日本债务危机

——国际资本流劢与债务危机

二战之后 日本迅速从战败中复兴重建 借助大量高质量人才资源 具备优势的汇率 国内一系列产业复兴政策和先进的完备的经济管理模式 创造出有一个世界经济奇迹 世界银行排名前十位全部是日本银行 在最顶峰时曾达到吞并美国之势然 1995年 日本的金融界却相继发生数起恶性事件 给已经面临危机的日本银行业带来极大的冲击和震动 特别是1995年“大和银行”事件

不良资产”是前些年日本“泡沫经济”时的产物。 “泡沫经济”崩溃后,金融机构贷出的大量款项, 有的因融资企业破产,或因经营不善,大部分无法 收回,形成了所谓的“不良资产”,消耗银行自有 资产。

日本金融危机的影响

泡沫经济以来的日本经济PPT课件

→地价上升也使得土地所有者的帐面 财产增加,刺激了消费欲望,从而导 致了国内消费需求增长,进一步刺激 了经济发展

泡沫破裂

• 1990年3月,日本大藏省发布《关于控制土 地相关融资的规定》,对土地金融进行总 量控制

•破裂。

• 起因: ①《广场协议》的签订。 ②1970年代后期开始,日本的银行烦恼于向优良制造业 企业的融资案件,于是开始倾向于向不动产、零售业、 个人住宅等融资。 ③1980年代以来,全球性的通货紧缩形成了股票市场的 上升通道。

• 主要表现:日本国内兴起了投机热潮, 尤其在股票交易市场和土地交易市场 更为明显

泡沫经济以来的日本经济

什么是泡沫经济

• 泡沫经济:是指资产价值超越实体经济, 极易丧失持续发展能力的宏观经济状态。

→经常由大量投机活动支撑。由于缺乏实 体经济的支撑,因此其资产犹如泡沫一般 容易破裂。

日本泡沫经济

• 时间:1986年12月到1991年2月 (4年零3个月) 仅次于1960年代后期的经济高速发展

• 其次,人民币虽然没有像日元那样大幅度升值, 但在历史上也第一次面临巨大的升值压力;

• 最后,我国虽然还是发展中国家,可是低利率政 策却比当时的日本持续了更长的时间,利率也更 低。

教训!

• 第一,汇率的调整并不能阻止经济的泡沫 化

• 第二,在CPI(消费物价指数)尤其稳定的时 期,我们更应该当心资产的泡沫化

• 第三,我们应处理好眼前的经济繁荣与经 济的长期持续健康发展之间的关系

Thank you.

感谢观看

《广场协议》

• 背景: ①美国财政赤字剧增,对外贸易逆差大幅增 长。美国希望通过美元贬值来增加产品的出 口竞争力,以改善美国国际收支不平衡状态。 ②为了打击美国当时最大的债权国——日本。

中美之间的经济战.ppt

我只是美国财团中的一个,其它财团呢?嘿嘿, 而且我的假设还只是到1988年,如果是到1995年, 日元升值到1:79,你我能想象美国在这场经济战争 的胜利中,到底从日本刮走了多少财富?

美国赚够了,日元现在又重新回到了1:140的位置 上,美元的坚挺依然和30年前一样!美元暂时性 的贬值,并没有损害到美元的国际地位。这场美 日的经济战争,以美国完胜而告终!!

美国人玩上瘾了。1998年,同样的手法在东南亚四小龙四 小虎身上又来了一次,这就是亚洲金融风暴!唯一不同的, 这次不需要广场协议了。因为亚洲这些小虎小龙的外汇储 备们直接阻击就可以大获全胜!但是,还是没有战胜财大 气粗、军事强盛、奉行霸权主义的美国,结局大家也看到 了,东南亚货币在先升后跌中,经济发展的成果被美国抢 掠一空!!

可是,美国也没有闲着,而且,作为经济进攻的 第一步他们已经早早的迈出了,向美国“凯雷财 团”这样的世界性投机财团收购中国的“徐州重 工”这样的事情已经发生了很多了,在这里我就 不一一例举了。他们的目的很明确,控制中国的 核心技术,进行世界性的技术垄断,迫使??量。 同时乘汇率没有变化之前以美元套取人民币,迫 使中国央行大量发行人民币以应付大量的货币兑 换需求,为拖垮中国经济打下伏笔。这还是明的 进入,暗地里的就更无法统计了。

举个例子:中国有13亿人口,平均每人的财富拥 有量为1万元每人,中国总共有13万亿元财富,而 现实生活中,每个人不可能把自己的全部财富都

带在身上,这里就平均一下,平均每个人身上携 带1000元现金(携带量为10%,其实这个量已经是 很大了),其余的存在银行,也就是说,在正常 情况下的流动现金量(术语为:现金流量)为1千 亿元,乘以一定的突变系数,(这里为了便于计 算,就理想的取值100%),也就是说在正常的经 济活动下,中国只要发行2千亿人民币就可以满足 本国的经济活动了。

1040 Lessons from a lost decade-original language-English

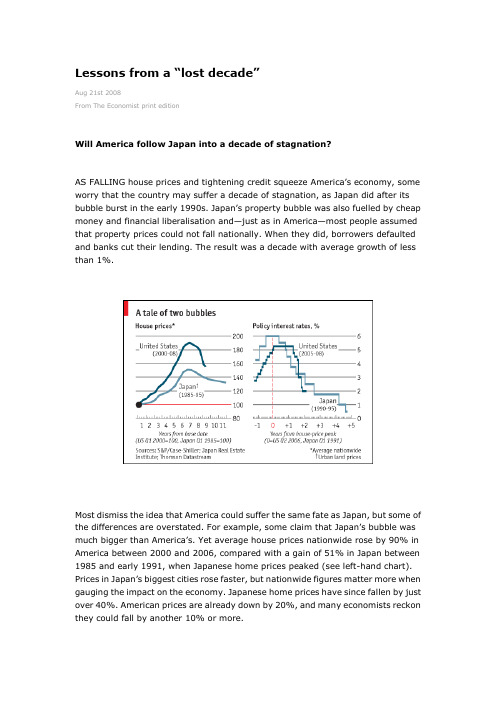

Lessons from a “lost decade”Aug 21st 2008From The Economist print editionWill America follow Japan into a decade of stagnation?AS FALLING house prices and tightening credit squeeze America’s economy, some worry that the country may suffer a decade of stagnation, as Japan did after its bubble burst in the early 1990s. Japan’s property bubble was also fuelled by cheap money and financial liberalisation and—just as in America—most people assumed that property prices could not fall nationally. When they did, borrowers defaulted and banks cut their lending. The result was a decade with average growth of less than 1%.Most dismiss the idea that America could suffer the same fate as Japan, but some of the differences are overstated. For example, some claim that Japan’s bubble was much bigger than America’s. Yet average house prices nationwide rose by 90% in America between 2000 and 2006, compared with a gain of 51% in Japan between 1985 and early 1991, when Japanese home prices peaked (see left-hand chart). Prices in Japan’s biggest cities rose faster, but nationwide figures matter more when gauging the impact on the economy. Japanese home prices have since fallen by just over 40%. American prices are already down by 20%, and many economists reckon they could fall by another 10% or more.What about commercial property? Again, average prices rose by less in Japan (80%) than in America (90%) over those same per iods. Thus Japan’s property boom was, if anything, smaller than America’s. Japan also had a stockmarket bubble, which burst a year earlier than that in property. This hurt banks, because they counted part of their equity holdings in other firms as capital. But its impact on households was modest, because only 30% of the population held shares, compared with over half of Americans.Nor were Japanese policymakers any slower than American ones to cut interest rates and loosen fiscal policy after the bubble burst, contrary to popular misconceptions. The Bank of Japan (BoJ) began to lower interest rates in July 1991, soon after property prices began to decline. The discount rate was cut from 6% to 1.75% by the end of 1993. Two years after American house prices started to slide, the Fed funds rate has fallen from 5.25% to 2% (see right-hand chart). A study by America’s Federal Reserve concluded that Japanese interest rates fell more sharply in the early 1990s than required by the “Taylor rule”, which establishes t he appropriate rate using the amount of spare capacity and inflation.Japan also gave its economy a big fiscal boost. The cyclically adjusted budget deficit (which excludes the automatic impact of slower growth on tax revenues) increased by an annual average of 1.8% of GDP in 1992 and 1993—similar to America’s budget boost this year. Japan’s monetary and fiscal stimulus did help to lift the economy. After a recession in 1993-94, GDP was growing at an annual rate of around 2.5% by 1995. But deflation also emerged that year, pushing up real interest rates and increasing the real burden of debt. It was from here on that Japan made its biggest policy mistakes. In 1997 the government raised its consumption tax to try to slim its budget deficit. And with interest rates close to zero, the BoJ insisted that there was nothing more it could do. Only much later did it start to print lots of money.America’s inflation rate of above 5% is an advantage. Not only are real interest rates negative, but inflation is also helping to bring the housing market back to fair value with a smaller fall in prices than otherwise. But in another way America is more exposed than Japan was. When its bubble burst in 1991, Japan’s households saved 15% of their income. By 2001 saving had fallen to 5%, which helped to prop up consumer spending. America’s saving rate of close to zero leaves no such cushion.The perils of procrastinationJohn Makin, at the American Enterprise Institute, a think-tank, argues that monetary and fiscal relief were ne cessary but not sufficient to revive Japan’s economy. The missing ingredient was a clean-up of the banking system, on which Japanese firms were more dependent than their American counterparts. Japanese banks hid their bad loans beneath opaque corporate structures, and curtailed newlending to profitable businesses. A vicious circle developed, whereby banks’ bad loans depressed growth which then created more bad loans.In another new report Richard Jerram, at Macquarie Securities, concludes that America “will not come close to repeating the experience of Japan”, because its regulatory system, financial markets and political structure will not let it procrastinate for so long. America has a more transparent regulatory structure which presses banks into recognising losses and repairing theirbalance-sheets—even if regulators were slow to recognise that the banks were shifting risky securitised assets off their balance-sheets in the first place. But Japan’s regulators for a long while were in cahoots with banks over hiding their bad loans.Over the past year, American banks have been quicker than those in Japan in the 1990s to disclose and write off losses and raise new capital. In Japan it took a long while before the political will was there to use taxpayers’ m oney to plug the banking system. A big test for America’s Treasury will be how quickly it recognises the need to nationalise Fannie Mae and Freddie Mac, the teetering mortgage giants.One advantage over Japan, says Mr Jerram, is that America is spreading the costs of its housing bust across other countries. Foreigners hold a large slice of American mortgage-backed securities. Sovereign-wealth funds have provided new capital for American banks. And America’s booming exports have helped to support its economy, thanks to the cheap dollar. In contrast, the yen’s sharp appreciation after Japan’s bubble burst hurt exports at the same time as domestic demand was being squeezed.By learning from Japan’s mistakes, America can avoid a dismal decade. However, it would be arrogant for those in Washington, DC, to assume that Japan’s troubles simply reflected its macroeconomic incompetence. Experience in other countries shows that serious asset-price busts often lead to economic downturns lasting several years. Only a wild optimist would believe that the worst is over in America.。

高三英语培优外刊阅读 地震话题

高三英语培优外刊阅读班级:____________学号:____________姓名:____________外刊精选|日本3·11大地震十周年:消失的村庄和坚守的老人【背景介绍】十年前的3月11日,日本发生9级大地震,引发强烈海啸,也造成了福岛第一核电站发生泄漏。

伤亡之外,地震区域的幸存者也基本离开了故乡。

但是,有这样一群人,地震过后却选择留下来,他们坚定地守在故土,试图在废墟上重建家乡。

是怎样的信念支撑着他们?他们究竟是怎样的一群人?A Village ErasedBy Russell GoldmanFor centuries, this village rode the currents of time: war and plague, the sowing and reaping of rice, the planting and felling of trees.Then the wave hit. Time stopped. And the village became history.When a catastrophic earthquake and tsunami struck coastal Japan on March 11, 2011, more than 200 residents of the village, Kesen, in Iwate Prefecture, were killed. All but two of 550 homes were destroyed.After the waters receded, nearly everyone who survived fled. They left behind their destroyed possessions, the tombs of their ancestors and the land their forefathers had farmed for generations.But 15 residents refused to abandon Kesen and vowed to rebuild."Our ancestors lived in this village 1,000 years ago," said Naoshi Sato, 87, a lumberjack and farmer whose son was killed in the tsunami. "There were disasters then, too. Each time the people stayed. They rebuilt and stayed. Rebuilt and stayed. I feel an obligation to continue what my ancestors started. I don't want to lose my hometown."Those who chose to stay in Kesen were old in 2011. Now in their 70s, 80s and 90s, they are older still. Slowly, over the past decade, a grim reality has settled over this place: There is no going back. Kesen will never be restored. This emptiness will last forever.A decade feels like an eternity for those who lost a child in mere seconds, but it's a brief moment in Japan's history. It's an even shorter blip in the billion-year history of the tectonic plates, whose grinding shifts triggered the earthquake and tsunami.It's that long view of history that gives the holdouts hope that Kesen will again rise from the wreckage."I'd like to see how this place will look 30 years from now," Sato said. "But by then, I'll have to see it from heaven. And I don't think that will be possible."【词汇过关】请写出下面文单词在文章中的中文意思。