Fixed Assets

固定资产英文会计科目

固定资产英文会计科目在会计中,固定资产通常用英文词汇表示为"Fixed Assets"。

这是一个会计科目,用于记录公司拥有并在生产中使用的长期资产。

这些资产的特点是它们不是为销售而持有的,而是用于支持业务运营。

以下是固定资产科目的英文词汇和相关表达:●Fixed Assets: The company's balance sheet includes a section for Fixed Assets, such asbuildings, machinery, and vehicles.●Property, Plant, and Equipment (PP&E): The PP&E section of the financial statementsdetails the company's investment in property, plant, and equipment.●Capital Assets: Capital assets, also known as fixed assets, are significant long-terminvestments that contribute to a company's production and operational activities.●Tangible Assets: Tangible assets represent physical assets like land, buildings, andequipment, and are recorded under Fixed Assets on the balance sheet.●Non-Current Assets: Non-current assets include fixed assets with a useful life extendingbeyond one year.这些表达方式都指代了公司持有的长期、非流动性的资产,这些资产通常在多个会计期间内使用,并在财务报表中以固定资产科目进行记录。

固定资产管理制度

固定资产管理制度Managerial system of fixed assets第一章Section One为了加强公司固定资产的管理,明确部门及员工的职责,现结合公司实际,特制定本制度。

In order to regulate the management of fixed assets of WSHL and confirm duty and responsibility of departments and staffs, now think oer company’s actual status and especially constitute this following system.1、固定资产标准:The standard of fixed assets1.1固定资产是指公司生产经营中使用期在一年以上,单位价值在2000元以上,并在使用过程中保持原来物质形态的资产。

The fixed assets mean that the assets will be used beyond one year and their unit value is beyond two thousands and keep original physical form during the usingprocess.1.2除固定资产以外的物质资产,列入低值易耗品或物料的管理。

Except for fixed assets, other physical assets are managed as the low value and easily worn-out articles and materials.2、固定资产内容:The content of fixed assets2.1土地;房屋及建筑物;机器设备;电子设备;运输设备;工具、器具;管理用具等。

Land; Houses and buildings; machines; electronic equipments; conveyanceequipments; tools and instruments; implements of management, etc.3、固定资产实物管理部门:The managerial department of fixed assets3.1人事总务部为公司固定资产管理部门;The general affairs department is the managerial department of fixed assets.3.2人事总务部设置固定资产实物台帐及卡片;The general affairs department sets up the cards and detail accounting bookof fixed assets.3.3人事总务部设专人负责对固定资产进行分类编号、购建、验收、保管、调拨、出售、报废、定期盘点等有关事项;The general affairs department appoints someone to assort, code, purchase, construct, check before acceptance, safe-keep, allocation, sell, discard,stock-take periodically, etc.3.4人事总务部对每项固定资产的使用落实到人,并订立相关的使用、交接,丢失、损坏赔偿规定。

微软官方教材_财务_ Fixed Assets

Basic Setup of Fixed Assets

Simplify setup of Assets

Inquiries

Uses of Fixed Asset Groups

Reporting

Setting up Posting Profiles

19 of 8

Parameters

Parameters are the last step in setting up Fixed Assets.

15 of 8

Five Methods for Depreciation Calculation – Manual

• Manual depreciation is always calculated as the percentage of the Acquisition price – Scrap value • Most flexible … more setup! • Depreciate base on schedule specified by user • (Example of Manual schedule setup): • - Year 1 = 10 % (10,000*10%) • - Year 2 = 50 % (10,000*50%) • - Year 3 = 8 % (10,000*8%) • - Year 4 = 12 % (10,000*12%) • - Year 5 = 20 % (10,000*20%)

Test Your Skills – General Setup of Fixed Assets Test Your Skills – Basic Setup of Fixed Assets

Microsoft® Business Solutions –Axapta ® Fixed Assets Module

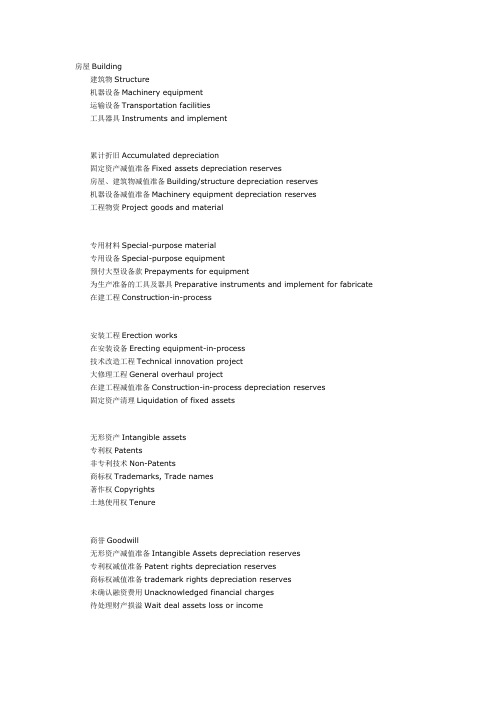

会计常用英语词汇——资产类Assets

房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate 在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or incom e 待处理固定资产损溢Wait deal fixed assets loss or income流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments-stock债券Short-term investments-corporate bonds基金Short-term investments-corporate funds其他Short-term investments-other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrap page低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process-outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis 存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investm ent长期股权投资Long-term investm ent on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investm ent on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investm ents depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备B creditor''s rights investment depreciation reserves 委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets。

fixed asset 的介绍

fixed asset 的介绍

固定资产(Fixed Assets)是指企业在其预期使用寿命超过一

年的时期内,拥有、使用、从事生产经营活动的所有物品,包括物质资产和无形资产。

物质资产包括土地、建筑物、机械设备、运输工具、电脑设备、家具和装饰物等,它们用于支持企业的生产和运营活动。

这些资产通常不能迅速变现,但它们能够长期为企业创造价值。

无形资产主要指企业的知识产权、专利权、商誉、技术秘密、专有的商业模型等。

与物质资产不同,无形资产在形式上没有实体存在,但能够创造一定的经济效益,并且也需要长期使用。

固定资产一般都以成本计量,包括购买价格、运输费用、安装费用等,减去预计的残值后,按照一定的折旧规则进行摊销。

摊销期限根据资产的预计使用寿命来确定。

固定资产的管理对于企业的运营和决策有重要的影响。

合理的固定资产管理可以帮助企业降低成本、提高效率、增加生产能力,并保护资产的价值。

固定资产还可以作为企业财务报表的重要组成部分,反映企业的投资情况和经营状况。

总之,固定资产是企业长期用于生产和经营活动的物质和无形资产。

它们对公司的稳定运营和价值创造起到重要的作用。

普华永道--财务管理最佳实践之固定资产管理

Controls

➢ Asset verification ➢ Asset valuation ➢ Acquisition and

disposal authorities

Measures

➢ Number of assets maintained

➢ Cost of department

➢ Elapsed time to record asset

➢ Report on identified or missing assets

➢ Hold non capitalised physical assists for verification

➢ Leased asset features compliant with accounting standards

Fixed Assets - Level 0 Context Diagram

10 percentile

Fixed Assets processing time

1 day

14 days

40 days

10 percentile

Median

90 percentile

Fixed Assets cost per Business Unit FTE (in £s) £31

£7

10 percentile Median

not verify network assets: the fact that the network works is verification enough)

➢ Verify non capitalised assets

System Features

➢ On line asset register holding key data and current cost allocation

固定资产下一步工作思路和计划

固定资产下一步工作思路和计划1.首先,我们需要对当前的固定资产清单进行全面的审查和更新。

First, we need to conduct a comprehensive review and update of the current fixed asset inventory.2.确保所有的固定资产都有准确的标识并且登记在册。

Ensure that all fixed assets are accurately identifiedand recorded.3.对每一项固定资产进行评估,包括其当前状态、价值和使用情况。

Evaluate each fixed asset, including its current condition, value, and utilization.4.确认所有固定资产的折旧和摊销情况,以便进行合理的财务核算。

Confirm the depreciation and amortization of all fixed assets to facilitate proper financial accounting.5.检查固定资产的维护和保养情况,确保其能够正常运行并且延长使用寿命。

Inspect the maintenance and upkeep of fixed assets to ensure they are operational and have an extended lifespan.6.排查固定资产可能存在的损耗、盗窃或者报废情况,并采取相应的补救措施。

Identify any potential loss, theft, or obsolescence of fixed assets and take appropriate remedial actions.7.更新固定资产的保险和保值情况,确保其得到充分的保障和价值补偿。

Update the insurance and appreciation of fixed assets to ensure they are adequately protected and valued.8.制定固定资产的长期发展规划,包括增加或替换旧资产,以适应业务的发展需要。

资产类科目英文名称

资产类科目英文名称 This manuscript was revised on November 28, 2020资产类科目英文名称现金:Cash and cash equivalents银行存款:Bank deposit应收账款:Account receivable应收票据:Notes receivable应收股利:Dividend receivable应收利息:Interestreceivable其他应收款:Other receivables原材料:Raw materials在途物资:Materials in transport库存商品:inventory存货跌价准备:provision forthe declinein value ofinventories坏账准备:Bad debt provision待摊费用:Prepaid expense交易性金融资产:Trading financial assets持有至到期投资:held-to-maturity investment可供出售金融资产:Available-for-sale financial assets短期投资:Short-term investment长期股权投资:Long-term equity investment固定资产:Fixed assets累计折旧:Accumulated depreciation在建工程:Construction-in-process固定资产减值准备:provision for the decline in value of fixed assets 无形资产:Intangible assets累计摊销:Accumulated amortization商誉:Goodwill递延所得税资产:deferred tax assets (DTA )固定资产的相关单词常见的固定资产building 建筑物plant 厂房machinery 机械equipment 设备vehicles 车辆fixture 固定设施Acquisition cost 购置成本acquire v. 获得,取得purchase price 买价transportation cost 运费installation cost 安装费用tax 税金等historical cost:原始成本fair value 公允价值market value 市场价值depreciation n. 折旧,损耗(有些资产)amortization 摊销(无形资产)accumulated depreciation 累积折旧depreciation expense 折旧费用depreciation base 折旧基数book value /carrying value 账目价值(=historical cost – accumulated depreciation)estimated residual value/ estimated salvage value 预计净残值estimated useful life 预计使用年限(No.of years)/(No.of production units)useful life 使用寿命,使用年限固定资产提折旧的方法a.straight-line method 直线折旧法,平均年限法b.units of production method 工作量法Accelerated depreciation 加速折旧法:c.double-declining balance method 双倍余额递减法d.sum-of-the-years' digits method 年数总和法journal entry 与折旧有关的会计分录Dr.depreciation expense 折旧费用Cr.accumulated depreciation 累计折旧。

固定资产管理文献翻译

Fixed assets refer to enterprises use period more than 1 year of houses, buildings, machines, machinery, transport, and other related to the production and operation of equipment, instruments, tools, etc. Fixed assets is the enterprise of the means of labor, but also the production and operation of company's main assets. From the Angle of the accounting division, with fixed assets, fixed assets is generally divided into production non-production use of fixed assets, rent out, without the use of fixed assets, fixed assets don't need a fixed assets, fixed assets, financing lease receive donated fixed assets, etc. Fixed assets in the process of production can be use to make for a long time, its value will gradually with the enterprise production and business operation activities transferred to the product into this, and constitute a part of product value. Fixed assets of the enterprises a lot of money, so the management of fixed assets, has become the important part of enterprise management, the enterprise assets value has important significance. The yao, fixed asset management have what specific practical significance for the enterprise? When the former is the basic status quo of enterprise fixed assets management in China? And enterprise will face and the means through which the existing fixed assets management is optimized with perfect, realize the fixed assets management level improve? The following main needle to the three questions to carry on the simple analysis and discussion. A, fixed assets management of practical significance For enterprise, fixed asset management is an important part of its financial management work, the overall quality of the fixed assets management, directly affects the enterprise can have assets of current situation, but also reflect that the whole level of its internalmanagement and water level. Fixed assets management is not one branch or part of the personnel's responsibility, but the enterprise internal all employees should be involved in a job. Strengthen corporate fixed asset management can make the enterprise internal property of the existing problems is more clear, avoid enterprise assets loss due to mismanagement. At the same time, the enterprise through the effective management of the fixed assets, can improve the using efficiency of fixed assets, and improve the efficiency of input and output of the enterprise. In addition, in order to strengthen the management of enterprise fixed assets can also effectively to revitalize the assets of the enterprise, make it play a proper role and value, can guarantee the stability of enterprise assets flow and healthful, all business development for the enterprise behavior to lay a solid economic foundation. Second, the current situation of enterprise fixed assets management Fixed assets as an important part of enterprise total assets should not be ignored, in the enterprise the proportion of total assets is relatively large, the fixed assets management not resulting in the loss of corporate assets, as this will no doubt for the management and development of the enterprise a very adverse impact. In recent years, with the development and the deepening of the market economy in our country, the overall quality of the cost management has become an important factor decided the enterprise market competitiveness, because while strengthen the cost management become the focus of the enterprise internal management. And as part of the corporate cost can not be ignored among, concerning the management of fixed assets to more and more enterprises attach importance to. With the development of science and technology and the progress ofknowledge, some fixed assets management advanced technology and means are constantly emerging, the technology and method of enterprise fixed assets management efficiency great promotion effect. They can effectively change the way of fixed assets data processing, improve the efficiency of the fixed assets physical count and inventory, solve the actual problem of enterprise fixed assets management, make the enterprise of fixed assets management more scientific and more simple and more effective. However, fixed asset management as a complex process, the management content more systemic work, with almost every sector of business, every employee has more or less relationship between. That is to say, the enterprise fixed assets management is not a department or a certain person's responsibility, but need to enterprise internal all personnel to participate in a company-wide job. Although in recent years a lot of enterprises to the internal management of fixed assets have a certain value, also began to take corresponding measures to adjust its internal fixed assets management and improvement, but the majority of enterprises in our country based on business model, management ideas, technology level, and about the limitations of fixed assets, combined with our country enterprise in the fixed assets management itself is a late start, so many enterprises in the fixed assets management still exist many defects and deficiencies. And conclusion, this kind of enterprise in the shortage of fixed assets management, mainly reflected in three aspects. 1, backward management thoughts, management consciousness In the current operation and management, the leaders of some enterprises still use the traditional thought of management. They only stay on the surface, the fixed assets management in the fixed assets management work a negativeattitude, system execution rules fan. Only to the fixed assets purchased, sold, and scrap on management accounting statements, and don't pay attention to the fixed assets of daily use, repair and maintenance system of execution Conditions, also do not understand the meaning and value of investment in fixed assets management way, one-sided responsibility of the fixed assets management in the financial sector and technical maintenance department, and depending on the fixed assets management in other departments of characteristics and functions, lead to the function of the fixed asset management has been greatly weakened. 2, personnel quality is not high, management means lag behind With the rapid development of science and technology, technology cycle is shorten, on the one hand, some new type of fixed assets, their higher efficiency, less energy consumption, more excellent performance, which leads to the original intangible depreciation of fixed assets. On the other hand some of the more advanced technology and scientific management methods also will produce And development, for enterprise may bring management system and the transformation of the concept, the change is both an opportunity and risk for the business. But at present our country enterprise universal existence of the fixed assets management means backward, such as not widespread, and the advanced information technology, personnel quality is not neat, the business level is not high, not a positive work attitude and so on, has increased the difficulty of enterprise fixed assets management, caused the enterprise fixed assets management is not standard, not science. 3, fixed assets management method is flawed Because the enterprise fixed assets has large number, variety, and high value, etc., must carry on the scientificmanagement of enterprises. But make the fixed assets with time is long, use sites scattered, using the characteristics of the method is not unified, make management difficult. First of all in terms of financial management, some enterprise informatization of water Level is not high, accounting treatment mainly depends on manual bookkeeping, for various complex accounting vouchers and accounting treatment provisions, enterprises have to invest a lot of manpower material resources to manage. Secondly, scrutiny of fixed assets and statistical work takes up a lot of time, the phenomenon of accounts disagreeing with physical inventory will often appear, easy to cause the loss of assets and the reset, causing unnecessary waste of resources. Finally, the fixed assets of the lack of effective supervision, on the one hand can make the fixed assets not effectively maintain and protect, shorten its service life, reduce the use effect, increase the unit cost of production, and even lead to accidents, on the other hand, accounting treatment is not timely, not specification, easy to produce power and responsibility is unclear, corruption of unhealthy phenomenon. Thus, the current our country enterprise in the fixed assets management does not reach to the mature development level, management consciousness and management means, or the construction of the management team, are also has some deficiency. Enterprises existing in the fixed assets management of these shortcomings, for strengthening the enterprise internal management work, to improve the economic benefits of the enterprises and improve the enterprise market competitiveness has more negative meaning. So in order to strengthen the management of enterprise fixed assets is enterprise and the improvement of a problem in the operation and development.Third, to strengthen the management of fixed assets To solve the current our country enterprise in all kinds of problems of the fixed assets management, make the fixed assets from the assets purchase, use, statistics and inventory of the whole process more simple and scientific, the enterprise shall be its existing cost management into the optimization and adjustment, and fully dig up the potential of its fixed assets management. 1, raising awareness, establish scientific management system Enterprises should set up the consciousness of scientific management, from top to bottom attaches great importance to the fixed assets management work. Leaders want to combine the actual situation of enterprises, establish a unified standard, perfect the management system, set up necessary full-time jobs in fixed assets, equipped with full-time personnel, a clear responsibility for the department or staff. Graded the fixed assets management tasks to each department and personnel, clear the construction, use, increase or decrease in fixed assets changes, maintenance, disposal and calculated value and real responsibility of daily management work and operation method. To carry out the effective rewards and punishment system, to stimulate the body towards a unified management goal, to optimize the rational allocation of resources, improve the effect of fixed assets management. 2, using advanced scientific management methods Using scientific method of fixed assets management, can make the whole process of fixed assets life cycle management. First of all, in front of the fixed assets to build, to project into the earnings evaluated and calculated. Second, to strengthen the management of fixed assets accounting. Enterprise should promote the informationization construction, also can use the advanced management method,management of fixed assets management in the whole, such as the recent promotion of bar code technology, through the relevant data for each new purchase assets are timely input to the fixed assets management information system, classified management, to speed up the information transmission, the supervision, and can provide convenient for use. In use process, one selector enterprise accounting processing method of the real value of fixed assets depreciation make sure timely metering and billing, can make the fixed assets management department in a timely and accurate understanding of the changes in the fixed assets, found management oversight, developing value-added potential, improve the effect of using fixed assets. 3, organize the training, improve the quality of the enterprise to improve the efficiency of the fixed assets management, must first to ensure that the fixed assets management level of business and professional moral quality. And thanks to the development of ideas and technology upgrading, enterprise must through constantly learning, to more new own management knowledge, constantly improve the management level, so that they can obtain good management effect, gain a competitive advantage. The management of fixed assets management is a complex work, various departmentsand to assume different roles and responsibilities in the management, therefore enterprises have targeted training, firstof all to convey the goal of fixed assets management and the general principle, determine the starting point and the footholdof fixed assets management, to achieve unified ideological understanding for everyone. Then according to the responsibilities of different from. To clarify its fixed asset management function, the operation of the fixed assets, dprotection, maintenance and other work to establish uniform standards and norms, to ensure that the fixed assets security integrity, to ensure that the fixed assets in good condition, strengthen audit and supervision, dish deficient inventory surplus of fixed assets. Value-added impairment should be based on actual situation to make a scientific and reasonable treatment. In order to make the safe operation of the fixed assets, obtain economic benefits. Four, conclusion enterprise fixed assets as an important part of its internal assets, in the corporate management have an important role in the development process. In order to strengthen the management of enterprise fixed assets can clear internal property right problem, avoid the loss of corporate assets, improve the utilization rate of corporate assets and input output, at the same time also can revitalize the enterprise funds, to make it in the enterprise management and development of all kinds of economic business and play the real meaning and value of the cut. With the development of the market economy, although the majority of enterprises in our country in recent years has begun to pay attention to the internal management of fixed assets, but our country enterprise in the management of fixed assets management system, management mode and team construction are also put in some shortcomings and deficiencies, needs to be improved. After all, only in in the exploration of the existing fixed assets of continuous optimization and improvement, to be able to promote the stable development of the enterprise.。

会计科目英语基本词汇

会计科目英语基本词汇1. Current Assets:流动资产2. Fixed Assets:固定资产3. Intangible Assets:无形资产4. Accounts Receivable:应收账款5. Inventory:存货6. Cash and Cash Equivalents:现金及现金等价物7. Prepaid Expenses:预付费用1. Current Liabilities:流动负债2. Long-term Liabilities:长期负债3. Accounts Payable:应付账款4. Short-term Loans Payable:短期借款5. Bonds Payable:应付债券6. Accrued Expenses Payable:应计费用7. Deferred Revenue:递延收益三、所有者权益类1. Shareholder's Equity:股东权益2. Common Stock:普通股3. Preferred Stock:优先股4. Capital Surplus:资本公积5. Retained Earnings:留存收益6. Accumulated Other Comprehensive Income:其他综合收益累计额1. Cost of Goods Sold:销售成本2. Depreciation Expense:折旧费用3. Amortization Expense:摊销费用4. Direct Labor Cost:直接人工成本5. Indirect Labor Cost:间接人工成本6. Production Overhead:生产间接费用1. Sales Revenue:销售收入2. Service Revenue:服务收入3. Interest Income:利息收入4. Dividend Income:股利收入5. Rental Income:租金收入6. Gain on Sale of Assets:资产出售收益1. Operating Expenses:营业费用2. Administrative Expenses:管理费用3. Selling Expenses:销售费用4. Financial Expenses:财务费用5. Research and Development Expenses:研发费用6. Income Tax Expense:所得税费用以上是关于会计科目的英语基本词汇,希望能对您的学习和工作有所帮助。

固定资产入账通知范文

固定资产入账通知范文英文回答:Fixed Asset Posting Notification.Dear Team,。

I am writing to inform you about the posting of fixed assets in our company. This notification is important as it affects the accounting records and financial statements of the company.Firstly, let me explain what fixed assets are. Fixed assets are long-term tangible assets that are used in the production or supply of goods and services, for rental to others, or for administrative purposes. Examples of fixed assets include buildings, machinery, vehicles, furniture, and equipment.When fixed assets are acquired by the company, theyneed to be recorded in the accounting system. This processis called posting. Posting involves assigning a value tothe asset and recording it as an asset in the balance sheet. It is important to accurately record fixed assets to ensure that the company's financial statements reflect the true value of the assets.To illustrate this process, let's say the company recently purchased a new delivery van for $30,000. The van would be recorded as a fixed asset in the accounting system. The value of $30,000 would be assigned to the van, and it would appear as an asset on the balance sheet.Another example could be the purchase of a new computer for the office. Let's say the computer costs $2,000. The computer would be recorded as a fixed asset, and its valueof $2,000 would be added to the balance sheet.It is important to note that fixed assets are not immediately expensed. Instead, they are depreciated over their useful life. Depreciation is the process ofallocating the cost of an asset over its useful life. Thisallows for the recognition of the asset's expense over time, rather than all at once.For example, if the delivery van has a useful life of 5 years, it would be depreciated at a rate of $6,000 per year ($30,000 divided by 5 years). The depreciation expensewould be recorded in the income statement, reducing the company's net income.In conclusion, fixed asset posting is an important process in accounting. It involves recording theacquisition of fixed assets and assigning a value to them. This ensures that the company's financial statements accurately reflect the value of the assets. It is important to accurately record fixed assets to comply with accounting standards and provide a true and fair view of the company's financial position.中文回答:固定资产入账通知。

盘点固定资产 英语

盘点固定资产英语

在企业的财务管理中,固定资产是一个重要的概念,是指企业购置的长期使用价值较高且预期使用时间超过一年的资产。

以下是关于固定资产相关的英文词汇和表达:

1. Fixed assets:固定资产

2. Depreciation:折旧

3. Book value:账面价值

4. Accumulated depreciation:累计折旧

5. Depreciation expense:折旧费用

6. Capital expenditure:资本支出

7. Salvage value:残值

8. Useful life:使用寿命

9. Depreciation method:折旧方法

10. Straight line method:直线法

11. Declining balance method:递减余额法

12. Sum of years digits method:年数总和法

13. Revaluation of fixed assets:固定资产重估

14. Disposal of fixed assets:固定资产处置

15. Sale of fixed assets:固定资产出售

16. Write-off of fixed assets:固定资产报废

以上是关于固定资产的英文词汇和表达,对于企业的财务管理人员来说,熟练掌握这些词汇和表达是非常重要的。

“固定资产投资”英语怎么翻译

“固定资产投资”英语怎么翻译

固定资产投资fixed-asset investment /investment in fixed assets

中国1-9⽉份固定资产投资完成91529亿元,同⽐增长25.7%。

国务院上周召开会议表⽰将抑制固定资产投资增长过快,意味着可能采取进⼀步的紧缩措施。

相关报道:

China's fixed assets investment rose to 9,152.9 billion yuan (US$1,220.4 billion) in the first nine months, up 25.7 percent from the same period last year, and the increase was 1.6 percentage points lower than the growth rate in the same period last year the National Bureau of Statistics (NBS) announced.

国家统计局数据显⽰,今年前三季度全社会固定资产投资完成91529亿元,同⽐增长25.7%,增速⽐上年同期回落1.6个百分点。

固定资产投资为fixed-asset investment/ investment in fixed assets。

与之相关的经济词汇有:

存款准备⾦率benchmark lending rate

资⾦流动capital flowing

宏观经济调控macro-economic control .。

固定资产的计算公式

固定资产的计算公式固定资产(FixedAssets)是一种指由企业购买的、长期用于企业生产、经营活动的固定的且不易折现的有形资产。

固定资产的购买成本是一个企业经营成本的重要组成部分,企业需要对其进行精确的计算,以保证企业的财务状况的合理性。

企业计算固定资产的方法有很多,其中最常用的是原值法,也叫现值法。

这种方法具有省时、省力、便捷的优点,可以有效地帮助企业计算出固定资产的确切成本。

根据此方法,企业计算固定资产的公式如下:原值法可以用来计算固定资产的总价值:固定资产价值 =始价格 -役金 -旧金其中,原始价格(Original Price)是指企业最初支付的购买固定资产的价格。

除役金(Salvage Value)是指在固定资产失去使用价值后可以回收的价值;折旧金(Depreciation Expense)是指按固定资产的有用寿命折算出来的价值。

固定资产的折旧金可以用受益法、平均年限法、双倍余额递减法等方法来计算,根据购买时间长短、使用情况和分账流程等因素来选择使用衰减法的类型。

下面简单介绍几种常用的折旧法:(1)受益法(Benefit Method):根据固定资产的预计使用时间计算出均匀折旧金。

(2)平均年限法(Straight-Line Method):根据固定资产的预计使用年限计算出均匀折旧金。

(3)双倍余额递减法(Double-Declining Balance Method):把固定资产的年初原值乘以一个百分率,得出折旧金额,然后把折旧金额从原值中扣除,如此反复,直到固定资产变成残值为止。

上述公式可以用来计算企业购买固定资产时所产生的总价值。

精确估算出企业购买固定资产的总价值,可以帮助企业合理统筹企业未来的财务状况。

固定资产的精确计算不仅在企业的财务计算中重要,在更广泛的经济统计监测中也显得尤其重要。

比如,根据固定资产投资来衡量某个国家或地区经济发展水平和财富实力,根据投资增长率来评估国家或地区的投资环境和投资政策等。

ISO9001固定资产管理规定(中英文)

ISO9001固定资产管理规定The fixed assets Management Procedure1. 目的:确定本公司固定资产定义及分类,确保公司所有固定资产之申购、运用、处理得到有效控制。

2. 范围:本程序适用于本公司固定资产的控制。

3. 定义:固定资产:单位采购价值在人民币两千元以上,使用期限超过一年的为生产商品、提供劳务、出租或经营管理而持有的机器、机械、运输工具以及其它设备、工具、器具等物品;我公司对单位价值低于2000元的空调、电视、电脑显示器及打印机也作为固定资产。

ESR:工程服务申请单4. 职责权限:4.1 使用部门:参与固定资产的验收、维护、保养、保管、报废、停用的评估和固定资产的申请。

4.2 QA:负责对办公电脑及与生产有关的固定资产的申购、验收、停用、报废、调拨的评估。

4.3 HR&A:负责厂房设施及其他非生产性固定资产的申购、验收、停用、报废、调拨的评估。

4.4 PUR:负责固定资产的采购和请款,采购定单上要清楚标示固定资产采购以区分其他采购订单,付款申请需附固定资产验收单。

4.5 FIN:根据QA或HR&A提供的固定资产验收单编列固定资产编号,列账管理,編制固定资产清单。

统筹部门需提供使用部门保管人签名的保管人清单正本,向财务部申請固定资产发放标签並配合标签的粘贴。

FIN负责检查和监督标签的粘贴和保管人的签名确认;采购申请付款时负责审核付款条件和附件,对公司固定资产进行财务管理,定期组织固定资产盘点。

5. 程序:5.1 固定资产的配置5.1.1 固定资产的购买申请需使用部门最高负责人批准。

5.1.2 公司可自行设计制作的固定资产,由QA或HR&A部安排自制。

5.1.3外购的固定资产,经PUR选择供应商并进行报价,经使用部门和FIN最高负责人批准后方可采购。

5.2 安装5.2.1生产性固定资产到达公司后,由QA按说明书及相关规定进行安装、调试。

固定资产英语词汇

固定资产英语词汇

我们先来看⼀下固定资产英语怎么说?

固定资产的英语翻译是:Plant assets or Fixed assets

下⾯我们来学习⼀下跟固定资产相关的英语词汇

原值 Original value

预计使⽤年限 Expected useful life

预计残值 Estimated residual value

折旧费⽤ Depreciation expense

累计折旧 Accumulated depreciation

帐⾯价值 Carrying value

应提折旧成本 Depreciation cost

净值 Net value

在建⼯程 Construction-in-process

磨损 Wear and tear

过时 Obsolescence

直线法 Straight-line method (SL)

⼯作量法 Units-of-production method (UOP)

加速折旧法 Accelerated depreciation method

双倍余额递减法 Double-declining balance method (DDB) 年数总和法 Sum-of-the-years-digits method (SYD)

以旧换新 Trade in

经营租赁 Operating lease

融资租赁 Capital lease

廉价购买权 Bargain purchase option (BPO)

资产负债表外筹资 Off-balance-sheet financing

最低租赁付款额 Minimum lease payments。

企业会计准则第4号——固定资产

Accounting Standard for Business Enterprises No.4 – Fixed Assets企业会计准则第4号——固定资产Chapter I General Provisions第一章总则Article 1 In order to regulate the recognition and measurement of the fixed assets, and disclosure of the relevant information, these Standards are formulated in the light of the Accounting Standards for Enterprises – Basic Standards.第一条为了规范固定资产的确认、计量和相关信息的披露,根据《企业会计准则——基本准则》,制定本准则。

Article 2 Other relevant accounting standards shall apply to the items as follows:(1) The Accounting Standards No. 3 –Investment Real Estates, shall apply tobthe buildings as investment real estates; and(2)The Accounting Standards No. 5 – Biological Assets, shall apply to the productive biological assets.第二条下列各项适用其他相关会计准则:(一)作为投资性房地产的建筑物,适用《企业会计准则第3号——投资性房地产》。

(二)生产性生物资产,适用《企业会计准则第5号——生物资产》。

Chapter II Recognition第二章确认Article 3 The term "fixed assets" refers to the tangible assets that simultaneously possess the features as follows:(1)They are held for the sake of producing commodities, rendering labor service, renting or business management; and(2)Their useful life is in excess of one fiscal year.The term "useful life" refers to the period of time over which a fixed asset is expected to use, or the quantity of products expected to produce or services expected to render through the fixed asset.第三条固定资产,是指同时具有下列特征的有形资产:(一)为生产商品、提供劳务、出租或经营管理而持有的;(二)使用寿命超过一个会计年度。

8.固定资产

Auto-number bar codes 自动编号

bar codes number sequence 若此处没有选中,则采用parameter中的设置

Type 类型 Tangible Intangible Financial Land and buildings Goodwill Other

Value mode

Service life remaining 按剩余折旧周期折旧 Service life

Depreciation profiles 折旧方法

Reducing balance 余额递减法

Prcentgae 折旧比率 Depreciation year 折旧年限 period frequency 折旧频率

Fixed assets journal

Transaction type

Acquisition 取得 Acquisition adjustment 取得调整 Depreciation 折旧 Depreciation adjustment 折旧调整 Revaluation 重新评估 Write up adjustment 升值调整 Write down adjustment 减值调整 Disposal – sale 处理-销售(详细科目) Disposal – scrap 处理-报废(详细科目) Provision for reserve Transfer from reserve Extraordinary depreciation 特别折旧

fixed assets

Structure

Main fixed asset

Value model

Status

Not yet acquired 未取得 Open 正常 Suspended 暂停 Close 关闭 Sold 已销售 Scrapped 已报废

会计学(第21版)课件:Fixed Assets and Intangible Assets

Buildings

✓ Sales taxes ✓ Repairs (purchase of

existing building) ✓ Reconditioning

(purchase of an existing building) ✓ Modifying for use ✓ Permits from governmental agencies

Cost – estimated residual value Estimated life

= Annual depreciation

Straight-Line Method

$24,000 – $2,000 5 years

= $4,400 annual depreciation

Straight-Line Rate

as part of normal operations.

Classifying Costs

Is the purchased item long-lived?

Yes

No

Is the asset used in

a productive

purpose?

Yes

No

Expense

Fixed Assets Investment

depletion. 8. Describe the accounting for intangible assets,

such as patents, copyrights, and goodwill. 9. Describe how depreciation expense is

reported in an income statement, and prepare a balance sheet that includes fixed assets and intangible assets. 10. Compute and interpret the ratio of fixed assets to long-term debt.

企业会计准则第4号——固定资产

企业会计准则第4号——固定资产Accounting Standard for Business Enterprises No.4 – Fixed Assets企业会计准则第4号——固定资产Chapter I General Provisions第⼀章总则Article 1 In order to regulate the recognition and measurement of the fixed assets, and disclosure of the relevant information, these Standards are formulated in the light of the Accounting Standards for Enterprises – Basic Standards.第⼀条为了规范固定资产的确认、计量和相关信息的披露,根据《企业会计准则——基本准则》,制定本准则。

Article 2 Other relevant accounting standards shall apply to the items as follows:(1) The Accounting Standards No. 3 –Investment Real Estates, shall apply tobthe buildings as investment real estates; and(2)The Accounting Standards No. 5 – Biological Assets, shall apply to the productive biological assets.第⼆条下列各项适⽤其他相关会计准则:(⼀)作为投资性房地产的建筑物,适⽤《企业会计准则第3号——投资性房地产》。

(⼆)⽣产性⽣物资产,适⽤《企业会计准则第5号——⽣物资产》。

Chapter II Recognition第⼆章确认Article 3 The term "fixed assets" refers to the tangible assets that simultaneously possess the features as follows:(1)They are held for the sake of producing commodities, rendering labor service, renting or business management; and(2)Their useful life is in excess of one fiscal year.The term "useful life" refers to the period of time over which a fixed asset is expected to use, or the quantity of products expected to produce or services expected to render through the fixed asset.第三条固定资产,是指同时具有下列特征的有形资产:(⼀)为⽣产商品、提供劳务、出租或经营管理⽽持有的;(⼆)使⽤寿命超过⼀个会计年度。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Monitor

asset maintenance charges Report on acquisitions Depreciation rates and disposals on a in management monthly basis Apply insurance accounts in line with valuation to key statutory rates Monitor tax issues assets related to acquisitions or Links asset CIP Ensure asset depreciation to responsibility at BU Ensure BU responsibility production and level product for assets in their use and for disposal losses costs/development Identify asset usage

Acquisition

Cost

linked to purchase order and accounts payable ledger linked to sales ledger

Depreciation

Variable

charged automatically to cost centres in GL

PwC175

3

Fixed Assets - Best Practice Features

Maintain fixed asset register

Control acquisitions and disposals

Manage periodic asset depreciation

Verify and value asset base

Manage periodic asset depreciation

Verify and value asset base

System Features

On

line asset register holding key data and current cost allocation code validation with GL

Asset verification Asset valuation Acquisition and disposal authorities

Number of assets maintained Cost of department Elapsed time to record asset

Asset Register Rules incorporated into Master File, which control issues of new numbers within structured coding scheme

Staff trained in Fixed Asset Accounting processes and have clear roles and responsibilities. They should

Depreciate

at point of asset use depreciation rules to asset classes

Revalue

Apply

key assets on a regular basis based on book value and high risk asset verification on regular periodic or rolling basis where asset cannot be verified via technical assumptions (most telco’s do not verify network assets: the fact that the network works is verification enough)

Process Features

Determine

asset categories for internal and statutory purposes

Set

up appropriate control of asset acquisition and disposals across company

Asset accounting policies clearly documented Appropriate coding by asset category established Authority levels clearly defined Procedures surrounding Fixed Asset process are documented and communicated to staff Budgets in place for capital expenditure All existing assets identified and classified Staff trained in FA process and have clear roles and responsibilities Statutory and tax requirements understood FA calendar in place and communicated to staff

Control focused Challenge asset requisition proposals

Processes

Information Systems

Maintain asset register Acquisitions and disposals Depreciation charge Verifying asset base Maintaining of valuation basis

PwC175

5

Fixed Assets - Critical Success Factors

These are a summary of the key business requirements, which must be met to achieve the objectives.

Assets

Hold

non capitalised physical assists for verification

coding of assets for verification

can be grouped for

depreciation rules

Bar

Leased

asset features compliant with accounting standards

Forecast

asset valuation mechanisms eg historic, current replacement asset reports by physical location and cost centre on identified or missing assets

Effective

asset depreciation for budget purposes

Report

Variable

Revaluation

tax management integrated with the fixed assets system

depreciation rules for classes of assets

have a good understanding of network and engineering areas

Supervisory staff understand statutory and tax requirements

Internal Control Requirements

Standing data set up on the system reflecting asset accounting policies

Ability to model depreciation scenario

PwC175

6

Fixed Assets - Notes on Maintain Standing Data

Asset ledgers integrated with GL and AP Depreciation and project control by cost centre Automated depreciation calculation

Controls

Measures

Best Practice Features

Asset accounting polices clearly documented; Master Data set up on the system to reflect these policies Appropriate coding by asset category established Procedures surrounding the Fixed Asset process are documented and communicated to staff including requirements for issuing new codes

Comprehensive

Verify

non capitalised assets

PwC175

4

Fixed Assets - Best Practice Features

Maintain fixed asset register