Cost and Management Accounting Topic1&2

成本与管理会计亨格瑞第13版英文版CA

The development of management accounting emerged in the 1920s, when the focus shifted from mere cost measurement to cost analysis and control, emphasizing the role of accounting in decision-making and management control.

It involves the identification, measurement, and allocation of costs, as well as the preparation of cost reports and other management information to assist management in making decisions about product pricing, production, and resource allocation.

Direct and indirect costs

Activity Identification

The first step in the activity-based costing method involves identifying the various activities that take place within the organization.

Cost allocation and collection

Cost Allocation

Allocating costs to specific departments, projects, or products is essential for accurate financial reporting and decision-making.

F5复习之决策技术及专业的成本和管理会计技术

F5复习之决策技术及专业的成本和管理会计技术本文由高顿ACCA整理发布,转载请注明出处一. Specialist cost and management accounting techniques(专业的成本和管理会计技术)到了F5的学习中,学员们刚一上来就会接触到很多管理会计技术,其实就是平时所说的不同的核算方法,它们分别是Activities based costing, Target costing, Life-cycle costing, Throughput accounting和Environmental accounting。

虽然方法比较多,但是学员们也没有必要紧张,因为每一种方法都会有自己独特的一面,让您有一个记住它的理由,并且应用熟悉了以后,就会发现每种方法都是有它自身存在的价值,因为可以帮助企业在不同阶段,对应不同的商品解决相应的问题,好让企业的shareholders做出更有利的决策。

二. Decision-making techniques(决策技术)上面提到了可以帮助shareholders做出更有利的决策,那么在决策中会有一些什么样的数据和方法作为参考呢?网校为学校归纳成为了以下这个标题:Relevant cost analysis, Cost volume profit analysis, Limiting factors, Pricing decisions, Make-or-buy and other short-term decisions和Dealing with risk and uncertainty in decision-making。

其中希望学员们引起注意的是Limiting factors这个标题,因为在学习中就会发现,其中会有数形结合的问题出现,帮助学员们解决相应的问题。

不仅仅只在数学中会用数形结合,在业绩管理中这种方法同样适用,而且也会带来更直观的解释和答案。

Lesson1 Management Accounting Fundamentals 英文管理会计课件 Management Accounting

Contents of the MA

1. Management accounting Fundamentals ( Review Chapter 1, 2 and 13)

2. Cost behavior and Variable Costing ( Chapter 9 and 10) 3. Cost-Volume-Profit Analysis (Chapter 3) 4. Decision Making (Chapter 11 and 12) 5. Capital Budgeting (Chapter 21) 6. Inventory Management ( Chapter 20) 7. Quality and Time ( Chapter 19) 8. Balanced Scorecard ( Chapter 19) 9. Transfer Pricing ( Chapter 22) 10. Performance Management and Compensation ( Chapter 23)

9

Topic 1:The role of management accounting

• 1 What is Management accounting? • 2 Management VS. Financial accounting • 3 The History and Current Focus of

Management Accounting

2011

• This course combines traditional Managerial Accounting with modern Managerial Accounting. This course introduces systematically the basics theory of Managerial Accounting, planning and control, and managerial decision-making.

Cost and Managerial Accounting(成本管理会计)智慧树知到课后章节答案

Cost and Managerial Accounting(成本管理会计)智慧树知到课后章节答案2023年下兰州理工大学兰州理工大学第一章测试1.Which of the following management responsibilities often involvesevaluating the results of operations against the budget? ()答案:Controlling2.Managerial accounting differs from financial accounting in that managerialaccounting ()答案:emphasizes data relevance over data objectivity3.Which of the following corporate positions is responsible for generalfinancial accounting, managerial accounting, and tax reporting? ()答案:Controller4.Of the following skills, which are needed by today's management accountants?()答案:All choices are correct5.Which of the following professional standards requires managementaccountants to continually develop their knowledge and skills? ()答案:Competence6.Critical thinking can be improved by asking yourself a series of questionsabout any issue or problem you encounter. These questions, for example,include: What is the objective? What data will I need? What assumptions am I making? Is my conclusion logical? .()答案:对7.Which of the following requires the company's CEO and CFO to assumeresponsibility for the company's financial statements and disclosures? ()答案:Sarbanes-Oxley Act of 2002 (SOX)8.Which of the following is false? ()答案:The triple bottom line focuses on three items: net income, net assets,and return on investment .9.All of the following are business trends affecting management accounting ()答案:All choices are correct10.Which TWO of the following statements about management accountinginformation are true?()答案:They are used to aid planning;They may include non-financial information第二章测试1.Which of the following costs are treated as product costs by a merchandisingcompany, such as Walmart? ()答案:nullRalph's Sporting Goods is a merchandising company, given the following information, the Cost of Goods Sold is 417,000 ( )答案:对3.Which of the following types of companies would have work in processinventory? ()答案:Manufacturing4.Which of the following is not an activity in the value chain? ( )答案:Administration5. A cost that can be traced to a cost object is known as a ( )答案:direct cost .6.Conversion costs consist of ( )答案:direct labor and manufacturing overhead7.Which of the following is part of manufacturing overhead? ( )答案:null8.The average cost per unit can be used for predicting total costs at manydifferent output levels ()答案:错9.Sunk costs are generally relevant to decisions ()答案:错10.Which of the following types of companies will always have the Cost of GoodsSold account on their income statements? ()答案:Merchandising and manufacturing companies第三章测试1.For which of the following would job costing not be appropriate? ()对于以下哪一项,不适合采用分批法进行成本核算?答案:Manufacturer of mass-produced beverages 大规模生产饮料的制造商2.Assuming the amount of manufacturing overhead over-allocation or under-allocation is material, which account is adjusted at the end of the period? ()答案:Work in Process Inventory;Finished goods Inventory;Cost of Goods Sold3.Whenever direct material, direct labor, and manufacturing overhead arerecorded on a job cost record, an associated journal entry is made to debitwhich of the following accounts? ()答案:Work in Process Inventory4.When a job is completed, the total cost of manufacturing the job should bemoved to which of the following general ledger accounts? ()答案:Finished Goods Inventory5.When using job costing at a service firm, professional labor cost would beconsidered an indirect cost of serving the client. ()答案:错6. A company calculates the prices of jobs by adding overheads to the primecost and adding 30% to total costs as a profit margin. Job number Y256 was sold for $1,690 and incurred overheads of $694. What was the prime cost of the job? ()答案:$6067.Which of the following is/are characteristics of job costing? ()答案:null8.The following information relates to job 2468, which is being carried out by AB Company to meet a customer's order. What is the selling price to thecustomer for job 2468? ()答案:$19,5009. A firm makes special assemblies to customers' orders and uses job costing.The data for a period are:What overhead should be added to job number CC20 for the period? ( )答案:$72,76110. A firm makes special assemblies to customers' orders and uses job costing.The data for a period are:Job number BB15 was completed and delivered during the period. What was the approximate value of closing work-in-progress at the end of the period? ( )答案:$217,323第四章测试1.Activity-Based Costing System focuses on activities as the fundamental costobjects. The costs of those activities become building blocks for compiling the indirect costs of products, services, and customers. ()答案:对2.Non-Value-Added Activities neither enhance the customer's image of theproduct or service nor provide a competitive advantage; also known as waste activities()答案:对3.Cost distortion is more likely to occur when ()答案:departments incur different types of overhead and the products or jobs use the departments to a different extent4.Activities incurred regardless of how many units, batches, or products areproduced are called: ( )答案:facility-level activities5.The Walliston Group (WG) provides tax advice to multinational firms. WGcharges clients for (a) direct professional time (at an hourly rate) and (b)support services (at 30% of the direct professional costs billed). The three professionals in WG and their rates per professional hour are as follows:WG has just prepared the May 2020 bills for two clients. The hours ofprofessional time spent on each client are as follows:What amounts did WG bill to San Antonio Dominion for May 2020 ( )答案:$28,1326.Automotive Products (AP) designs and produces automotive parts. In 2014,actual variable manufacturing overhead is $308,600. There are three main departments that consume overhead resources: design, production, andengineering. Interviews with the department personnel and examination of time records yield the following detailed information:If AP uses the simple costing system that uses machine-hours as theallocation base to allocate variable manufacturing overhead to its threecustomers, the manufacturing overhead allocated to United Motor is: ( )答案:$9,2587.Automotive Products (AP) designs and produces automotive parts. In 2014,actual variable manufacturing overhead is $308,600. There are three main departments that consume overhead resources: design, production, andengineering. Interviews with the department personnel and examination of time records yield the following detailed information:If AP allocates variable manufacturing overhead to each customer in 2014 using department-based manufacturing overhead rates, the manufacturing overhead allocated to United Motor is: ( )答案:$23,8008.The potential benefits of ABC/ ABM are generally higher for companies that( )答案:Products that a company is well-suited to make and sell show small profits;All or most indirect costs are identified as output unit–level costs,batch-level costs, product-sustaining costs, or facility-sustaining costs.;Significant amounts of indirect costs are allocated using only one or two cost pools9.Product-sustaining costs (service-sustaining costs) are the costs of activitiesundertaken to support individual products or services regardless of thenumber of units or batches in which the units are produced. ( )答案:对10. A cost hierarchy categorizes various activity cost pools on the basis of thedifferent types of cost drivers, cost-allocation bases, or different degrees ofdifficulty in determining cause-and-effect (or benefits-received)relationships. ( )答案:对第五章测试1.Which one of the following statements is incorrect? ( )答案:In process costing, but not job costing, the cost of normal loss will beincorporated into normal product costs2.Equivalent units express ()答案:the amount of work done during a period in terms of fully completedunits of output.3.Process B had no opening inventory. 13,500 units of raw material weretransferred in at $4.50 per unit. Additional material at $1.25 per unit wasadded in process. Labour and overheads were $6.25 per completed unit and $2.50 per unit incomplete. If 11,750 completed units were transferred out, what was the closing inventory in Process B? ( )答案:$14,437.504.Dairymaid makes organic yogurt. The only ingredients, milk and bacteriacultures, are added at the very beginning of the fermentation process. Atmonth end, Dairymaid has 100,000 cups of yogurt that are only 25% of the way through the fermentation process. The equivalent units of directmaterials in ending work in process are ( )答案:100,000 cups5.Which of the following is false concerning process costing? ( )答案:It accumulates production costs by activities.6.Conversion costs consist of ( )答案:direct labor + manufacturing overhead7.The journal entry needed to record direct labor used but unpaid in theFinishing Department during the month would be Debit Finished GoodsInventory; Credit Wages Payable ( )答案:错8.The distinction between job costing and process costing can be summarized as ( )答案:对9.The weighted-average method computes unit costs by dividing total costs inthe Work in Process account by total equivalent units completed to date and assigns this average cost to units completed and to units in ending work-in-process inventory. ()答案:对10.Operating income can differ materially between the weighted-averagemethod and the first-in, first-out method when (1) direct material orconversion cost per equivalent unit varies significantly from period to period and (2) physical-inventory levels of work in process are large in relation to the total number of units transferred out of the process. ( )答案:对第六章测试1.Variable costs are conventionally deemed to ( )答案:be constant per unit of output2.The following is a graph of cost against level of activity. To which one of the following costs does the graph correspond? ()答案:null3. A production worker is paid a salary of $650 per month, plus an extra 5 centsfor each unit produced during the month. This labour cost is best describedas ( )答案:A semi-variable cost4.B Co has recorded the following data in the two most recent periods. What isthe best estimate of the company's fixed costs per period? ( )答案:$5,1005.According to the following EXHIBIT, the fixed cost is ( )答案:14538.056.Under absorption costing and variable costing, the calculation of productcosts can be summarized as ( )答案:对7.Why is variable costing often used for internal management purposes? ( )答案:Variable costing does not give managers incentives to build upunnecessary inventory.;Variable costing helps managers with decision making because itallows them to easily see the cost of making one more unit of product ;Variable costing and the contribution margin income statement help managers easily predict the cost of operating at different volumeswithin the relevant rangemitted Fixed Costs are fixed costs that are locked in because of previousmanagement decisions; management has little or no control over these costs in the short run. ( )答案:对9.Which of the following is false? ( )答案:The operating income of manufacturers will always be the same,regardless of whether variable or absorption costing is used10.Which of the following is false? ( )答案:Data points falling in a linear pattern suggest a weak relationshipbetween cost and volume .第七章测试1. A company makes a single product and incurs fixed costs of $30,000 permonth. Variable cost per unit is $5 and each unit sells for $15. Monthly salesdemand is 7,000 units. The breakeven point in terms of monthly sales units is:()答案:3,000 units2. A company manufactures a single product for which cost and selling pricedata are as follows.The margin of safety, expressed as a percentage of budgeted monthly sales,is : ( )答案:20%3. A single product company has a contribution to sales ratio of 40%. Fixedcosts amount to $90,000 per annum. The number of units required to breakeven is:( )答案:impossible to calculate without further information4. A company's breakeven point is 6,000 units per annum. The selling price is$90 per unit and the variable cost is $40 per unit. What are the company's annual fixed costs? ( )答案:$300,0005.The operating leverage factor indicates the percentage change in operatingincome that will occur from a 1% change in volume . It tells managers how sensitive the company's operating income is to changes in volume . ()答案:对6.Sensitivity Analysis is a "what-if" technique that asks what results will be ifactual prices or costs change or if an under lying assumption changes. ( )答案:对7.Which of the following is false regarding choosing between two coststructures( )答案:The indifference point is the point where total revenues equal totalexpenses8.Which of the following is true regarding a company that offers more than oneproduct? ( )答案:The breakeven point is dependent on sales mix assumptions.9. A company with a low operating leverage ( )答案:has relatively more variable costs than fixed costs10.Contribution margin is revenues minus all variable costs whereas grossmargin is revenues minus cost of goods sold. Contribution margin measures the risk of a loss, whereas gross margin measures the competitiveness of aproduct.()答案:对第八章测试1.Baron Co. incurs the following costs to make 25,000 switches:Switches can be purchased for $8 per switch,and all variable costs and$10,000 of fixed costs can be eliminated, however, $50,000 of fixed costsremain. Baron Co. should ( )答案:make switches2.The following data relate to the Super.The capital invested in manufacturing and distributing 9,530 units of theSuper per annum is estimated to be $36,200. If the required annual rate of return on capital invested in each product is 14%, the selling price per unit of the Super is, to the nearest $0.01: ( )答案:$144.313.Ess Company manufactures four products but next month there is likely to bea shortage of labour. The following information is available.What order should the products be made in, in order to maximize profits? ( )答案:R,Q,S,T4.The characteristics of Price-Takers can be summarized as ( )答案:Pricing approach emphasizes target costing;Heavy competition;Product lacks uniqueness;Not a brand name5.The characteristics of Price- Setters can be summarized as ( )答案:Pricing approach emphasizes cost-plus pricing;Product is more unique;Product is branded;Less competition6.Relevant information has two characteristics: (1) It pertains to the future.(2)It differs between alternatives. ()答案:对7.Considerations for Discontinuing Products, Departments, or Stores include ( )答案:null8.In making "sell as is" decisions, companies should consider all of thefollowing EXCEPT for: ( )答案:Costs incurred up to the "sell as is" decision point .9.The formula for arriving at target cost is which of the following?( )答案:Revenue minus desired profit10.Keys to making short-term decisions include which of the following? ( )答案:Both of the above第九章测试1.Flexible budgeting is the calculation of the quantity and cost of inputs thatshould have been consumed given the achieved level of production. ( )答案:对2.The advantages of the use of budgets in a management control systeminclude ( )答案:Promote communication and coordination within the organization.;Provide performance criteria.;Force management planning.3.In the budgeting and planning process for a firm, which one of the followingshould be completed first ( )答案:Strategic plan.4.Which one of the following best describes the role of top management in thebudgeting process? Top management ()答案:Needs to be involved, including using the budget process tocommunicate goals.5.Budgetary slack describes the situation in which a manager intentionallyover-budgets expenses or under-budgets revenue. ( )答案:对6.Which of the following budgets must be prepared first, as it serves as a basisfor most other budgets?()答案:Sales budget7.In preparing a corporate master budget, which one of the following is mostlikely to be prepared last? ()答案:Cash budget8.Barnes Corporation expected to sell 150,000 board games during the monthof November, and the company's master budget contained the following datarelated to the sale and production of these games:Actual sales during November were 180,000 games. Using a flexible budget, the company expects the operating income for the month of November to be ( )答案:$420,0009.The operating budgets culminate in the budgeted ( )答案:null10.DeBerg Company has developed sales projections for the calendar year.Normal cash collection experience has been that 50% of sales are collected during the month of sale and 45% in the month following sale. The remaining 5% of sales is never collected. DeBerg's budgeted cash collections for thethird calendar quarter are ( )答案:$414,000第十章测试1.Unfavorable variances should always be interpreted as "bad news" for thecompany. ( )答案:错2.Which of the following are advantages of decentralization? ( )答案:null3.In terms of responsibility centers, a large corporate division would beconsidered a(n) ( )答案:investment center .4."Number of new products developed" would be a key performance indicator(KPI) for which of the four balanced scorecard perspectives? ( )答案:Internal business5."Hours of employee training" would be a key performance indicator (KPI) forwhich of the four balanced scorecard perspectives? ( )答案:Learning and growth6.The basic purpose of a responsibility accounting system is ( )答案:Motivation.7.Listed below is selected financial information for the Western Division of theHansel Company for lastyear.If Hansel treats the Western Division as an investment center forperformance measurement purposes, whatis the before-tax return on investment (ROI) for last year? ()答案:16.67%8.The imputed interest rate used in the residual income approach toperformance evaluation can best be described as the ()答案:null9.Managerial performance can be measured in many different ways, includingreturn on investment (ROl) and residual income. A good reason for usingresidual income instead of ROl is that goal congruence is more likely to be promoted by using residual income. ( )答案:对10. A limitation of transfer prices based on actual cost is that they ()答案:Can lead to sub-optimal decisions for the company as a whole.第十一章测试1.Which of the following is true? ()答案:A standard cost is the budgeted cost for one unit2.Which of the following is not an advantage of using standard costs? ( )答案:Standards can cause unintended behavioral consequences3.Which of the following is not true about standard costing systems? ( )答案:At the end of the period, the variances are closed to the Sales Revenue account4.For the fixed overhead volume variance, if production volume is greater thanoriginally anticipated, the variance will be unfavorable . ()答案:错5.Fixed overhead budget variance is the difference between actual fixedoverhead and budgeted fixed overhead . ()答案:对6.Dolphin Ceramics produces large planters to be used in urban landscapingprojects. A special earth clay is used to make the planters. The standardquantity of clay used for each planter is 24 pounds. Dolphin uses a standard cost of $2.00 per pound of clay. Dolphin produced 3,125 planters in May. In that month, 78,125 pounds of clay were purchased and used at the total cost of $150,000. The direct material quantity variance is ( )答案:$6250 unfavorable variance7.Vemoirs, Inc,produces several different styles and sizes of picture frames.The following activity describes its overhead costs during March, the variable overhead rate variances for the month of March is ( )答案:$1,625 unfavorable variance8.Direct Labor Rate Variance tells managers how much of the total laborvariance is due to paying a higher or lower hourly wage rate than anticipated.( ).答案:对9. A company budgets to make and sell 4,000 units of its product, actual volumeare 4,200 units. The product has a standard direct labor cost of $43. Whenanalyzing its direct labor flexible- budget variance for the period, thecompany determined that its direct labor efficiency variance was anunfavorable variance of $8,600. Which one of the following is closest to the actual cost for direct labor if the total direct labor flexible- budget variance was an unfavorable variance of $4,400? ( )一家公司预算生产和销售 4,000 件产品。

Student self study copy CMA1 -Costs in the CMA System

•

Read the section headed “The functions of CMA” on pages 2 -3 and answer the following questions. Please work quietly and alone.

• True or False?

– The managers in an organisation must maximize the profits made or the services it supplies. – Among other thing managers have to plan future operations, analyze and evaluate results and act to remedy mistakes. – The management accountant (MA) is a member of the team who provides team members with information to help them in their task – The expertise of the MA will not improve performance – The advice given by the MA will not improve the quality of decisions made by the management team. – The MA uses data for interpretation or other management purposes

•

•

•

•

Planning – The business plan (corporate strategy) sets ____ ____ objectives, a budget decides in detail how these will be achieved in the shorter term, say a ____. – Without ________ cost estimates a budget cannot be prepared with __________. Controlling – Cost statements compare the budget with actual performance and can reveal departments which are ___________. Managers will feel more in control of their department. Estimating – If costs are analysed the information will enable a company to decide with confidence on a _________ that will cover cost and make a profit. Decision Making – The MA must explain the ____ ______ of the alternative decisions managers may choose from, such as whether to make a component “in-house” or buy it in from another company.

成本与管理会计英文课件 (1)

1.

© 2009 Pearson Prentice Hall. All rights reserved.

The Value Chain Illustrated

and that are key to the success of a company include:

Cost and efficiency

Quality

Time Innovation

© 2009 Pearson Prentice Hall. All rights reserved.

A Five-Step Decision Making Process in Planning & Control

1. 2. 3. 4. 5.

Identify the problem and uncertainties Obtain information Make predictions about the future Make decisions by choosing between alternatives Implement the decision, evaluate performance, and learn

© 2009 Pearson Prentice Hall. All rights reserved.

Strategy & Management Accounting

Management accounting helps answer important

管理会计英文版

5000

2500

Manufactures

1000 Fuels and mining products

500

Agricultural products

250

100

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Source: World Trade Organization, International Trade Statistic 2010

• Identify job descriptions as either line or staff positions.

• Explain the concepts of lean production: Six Sigma, e-commerce, enterprise systems, and enterprise risk management. • Explain the importance of ethical standards in an advanced economy.

1-11

1.1 Information needs of managers and other users

1. Background

• Globalization –> More competition – >Timely, up to date, and relevant information needed

• For final exam • 15 MCQs 30 points • 5-6 Calculation questions 70 points

1-3

Main Contents of MA1

MANAGEMENT ACCOUNTING教学大纲

《管理睬计学》MANAGEMENTACCOUNTING教学大纲第一部分:教学要求一、授课对象《管理睬计》的讲授对象为会计系会计学专业的本科学生。

二、先修课程《管理睬计》课程是会计学专业的专业主干课程之一,其先修课程主要有《基础会计学》、《中级会计学》、《成本会计》、《财务管理》及《微观经济学》等。

三、学分学时支配《管理睬计》课程的学分为3学分,共18周课,54学时。

课时支配表如下:其次部分:教学内容《管理睬计》是会计学专业必修课。

它是一门新兴的综合性边缘学科。

它是为强化企业经营管理,提高企业经济效益服务的。

侧重于企业的预料、决策、规划和限制。

为企业培育高级财会人员。

学习这门课程目的在于驾驭管理睬计的基本理论、基本方法和基本技能。

要求驾驭预料、决策和限制理论和方法,并能娴熟运用这些理论和方法,预料前景、规划将来和参与决策,充分发挥会计的管理职能,以帮助企业改善经营管理,提高经济效益。

要求学生了解管理睬计的内容、管理睬计的职能和管理睬计的特点,驾驭预料、决策、限制及业绩评价的基本理论,并能以此指导企业的实践活动。

管理睬计要求学生不满足计账、算账,而且要求学生能娴熟驾驭预料、决策及限制方法,为企业预料前景和规划将来服务。

第一章管理睬计概论一、教学目的和基本要求本章内容是关于本课程的总括说明,通过本章学习,帮助学生了解管理睬计的产生与发展,弄清管理睬计与财务会计的区分与联系,相识其职能及内容。

本章分别论述管理睬计的概念,管理睬计的形成和发展,管理睬计职能作用,会计与财务会计的区分与联系,管理睬计与财务会计的区分与联系。

二、讲授内容(一)什么是管理睬计关于管理睬计的定义,在理论界有着不同的看法,其中美国管理睬计委员会给管理睬计所下定义尤为引人注目。

(二)管理睬计的基本内容1 .管理睬计初级阶段2 .管理睬计发展阶段(三)管理睬计职能作用1 .参与企业预料2 .参与经营决策3 .规划经营目标4 .限制经济活动5 .评价经营业绩(四)管理睬计与财务会计的区分与联系1 .管理睬计与财务会计的区分2 .管理睬计与财务会计的联系复习思索题:1 .管理睬计的基本内容是什么?2 .管理睬计形成与发展过程阅历了哪几个阶段?各阶段的主要特点是什么?3 .管理睬计的作用有哪些?4 .试论管理睬计与财务会计的区分及联系?其次章成本习性分析一、教学目的和基本要求本章内容是管理睬计的基本概念说明,通过本章学习,相识成本的各种分类,驾驭成本习性分析的有关内容。

Task1 Accounting for Management

Task 1Accounting for ManagementWhat is Management Accounting? Role of Management Accountant. Anthony’s Hierarchy.Management VS Financial Accounting. Management VS Cost Accounting.1. What is Management Accounting Management Accounting is concerned with the provision and the use of accounting information.This information is used by managers of the business to assist them when making decisions to achieve the organisation’s overall objective.2. Role of Management AccountantThe role of Management Accountant depend on the role of Management.The role of management:•Planning•Control•Decision making2. Role of Management AccountantPlanning involves :a.Establishing objectivesb.Selecting appropriate strategies to achieve those objectivesControl involves :paring the actual performance with planning performance.b.Reviewing the corporate plan.Management is decision-taking.Decision making always involves a choice between alternatives.ExampleWhich of the following is not part of the planning stage?A.Deciding on the optimal way in which an objective might beachievedB.Identifying ways which might contribute to the achievement ofspecified objectivesC.Obtaining data about actual resultsD.Identifying goals or objectivesAnswer: C3. Anthony’s HierarchyAnthony divides management activities into strategic planning, management control and operational control.•Strategic planning:'the process of deciding on objectives of the organisation, on changes inthese objectives, on the resources used to attain these objectives, and on the policies that are to govern the acquisition, use and disposition of theseresources'.•Tactical (or management) control:'the process by which managers assure that resources are obtained and used effectively and efficiently in the accomplishment of the organisation'sobjectives'.•Operational control:'the process of assuring that specific tasks are carried out effectively and efficiently'.3. Anthony’s HierarchyExampleDiane carries out routine processing of invoices in the purchasing department of L Co. Joanne is Diane’s supervisor. Lesley is trying to decide how many staff will be needed if some proposed new technology is implemented. Tracey is considering the new work that L Co will be able to offer and the new markets it could enter, once the new technology is well established.Which member of L Co carries out tactical activities?A DianeB JoanneC LesleyD TraceyAnswer : C4. Management vs Financial Accounting Financial accounting systems ensure that the assets and liabilities of a business are properly accounted for, and provide information about profits and so on to shareholders and to other interested parties(external users).4. Management vs Financial Accounting Similarity:a branch of Accounting; use the same source dataDifference:information user.4. Management vs Financial AccountingFinancial Management User External and Internal InternalLegal requirement ✔✗Precision True and Fair As accurate as possible forusers needs Rules GAAP No rules bus some establishedtechniques Reporting Past data Past and present data to makedecisions about future Scope Whole organisation Segment/Divisions or whateveris needed by business Frequency Annual As requiredFormat Governed by Companies Act No set formatExampleWhich of the following statements about management accounts is/are true?I.There is a legal requirement to prepare management accounts. II.The format of management accounts is largely determined by law. III.They serve as a future planning tool and are not used as a historical record.A (i) and (ii)B (ii) and (iii)C (iii) onlyD None of the statements are correct.Answer: D5. Management vs Cost AccountingCost accounting is part of management accounting. Cost accounting provides a bank of data for the managementaccountant to use.Cost accounting is the ‘gathering of cost information and its attachment to cost objects, the establishment of budgets,standard costs and actual costs of operations, processes,activities or products; and the analysis of variances,profitability or the social use of funds.’5. Management vs Cost Accounting Cost accounting information is, in general, unsuitable for decision making.Decision-making information should be relevant and incorporate uncertainty.You’re a Champion! Thanks for staying with us. You have finished this task.。

成本管理会计课件(英文版)

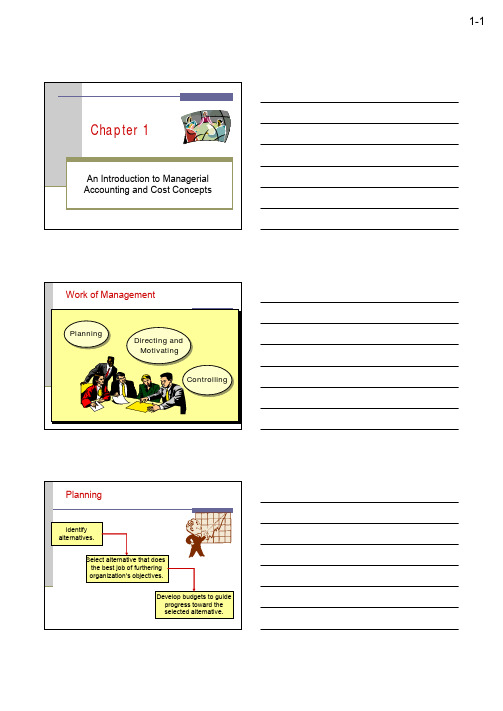

Chapter 1An Introduction to Managerial Accounting and Cost Concepts Work of ManagementPlanning Planning ControllingControlling Directing and MotivatingDirecting and Motivating PlanningIdentifyalternatives.Identify alternatives.Select alternative that does the best job of furthering organization’s objectives.Select alternative that does the best job of furthering organization’s objectives.Develop budgets to guide progress toward the selected alternative.Develop budgets to guide progress toward the selected alternative.Directing and MotivatingDirecting and motivating involves managing day-to-day activities to keep the organization running smoothly.n Employee work assignments.n Routine problem solving.n Conflict resolution.n Effective communications.ControllingThe control function ensuresthat plans are being followed.The control function ensures that plans are being followed. Feedback in the form of performance reports that compare actual results with the budget are an essential part of the control function.Feedback in the form of performance reports that compare actual results with the budget are an essential part of the control function.Planning and Control CycleDecision Making Formulating long-and short-termplans (Planning)Formulating long-and short-term plans (Planning)Measuringperformance(Controlling)Measuringperformance (Controlling)Implementing plans (Directingand Motivating)Implementing plans (Directing and Motivating)Comparing actual to planned performance(Controlling)Comparing actual to planned performance (Controlling)BeginComparison of Financial and Managerial AccountingFinancial Accounting Managerial Accounting1. Users External persons who Managers who plan formake financial decisions and control an organization2. Time focus Historical perspective Future emphasis3. Verifiability Emphasis on Emphasis on relevance versus relevance verifiability for planning and control4. Precision versus Emphasis on Emphasis on timeliness precision timeliness5. Subject Primary focus is on Focuses on segmentsthe whole organization of an organization6. GAAP Must follow GAAP Need not follow GAAPand prescribed formats or any prescribed format7. Requirement Mandatory for Notexternal reports MandatoryLearning Objective 1Identify and give examples ofeach of the three basicmanufacturing cost categories.The Product DirectMaterials Direct Materials Direct Labor Direct Labor Manufacturing OverheadManufacturing Overhead Manufacturing CostsDirect MaterialsRaw materials that become an integral part of the product and that can be conveniently traced directly to it.Example: A radio installed in an automobile Example: A radio installed in an automobile Direct LaborThose labor costs that can be easily traced to individual units of product.Example:Wages paid to automobile assembly workers Example:Wages paid to automobile assembly workers Manufacturing OverheadManufacturing costs cannot be traced directly to specific units produced.Examples:Indirect materials and indirect labor Examples:Indirect materials and indirect labor Wages paid to employees who are not directlyinvolved in productionwork.Examples:Maintenanceworkers, janitors andsecurity guards.Materials used to support the production process. Examples:Lubricants andcleaning supplies used in the automobile assembly plant.Classifications of Nonmanufacturing CostsSelling Costs Costs necessary to get the order and deliverthe product.AdministrativeCostsAll executive, organizational, and clerical costs.Learning Objective 2Distinguish betweenproduct costs and periodcosts and give examplesof each.Product Costs Versus Period CostsInventoryCost of Goods SoldBalance SheetIncomeStatement SaleProduct costs include direct materials, directlabor, andmanufacturingoverhead.Period costs are not included in product costs. They are expensed on the income statement.ExpenseIncomeStatementQuick Check üWhich of the following costs would beconsidered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.Which of the following costs would beconsidered a period rather than a product cost in a manufacturing company?A. Manufacturing equipment depreciation.B. Property taxes on corporate headquarters.C. Direct materials costs.D. Electrical costs to light the production facility.E. Sales commissions.Quick Check üPrime Cost and Conversion Cost Direct Material Direct Material Direct Labor Direct Labor Manufacturing OverheadManufacturing Overhead Prime Cost ConversionCost Manufacturing costs are oftenclassified as follows:Comparing Merchandising and Manufacturing ActivitiesMerchandisers . . .n Buy finished goods.n Sell finished goods.Manufacturers . . .n Buy raw materials.n Produce and sell finished goods.MegaLoMartBalance SheetMerchandiser Current Assets v Cash v Receivables v Prepaid Expenses v Merchandise Inventory Manufacturer Current Assets v Cashv Receivables v Prepaid Expenses v Inventories:1.Raw Materials2.Work in Process3.Finished GoodsMerchandiser Current Assets v Cash v Receivablesv Prepaid Expenses v Merchandise Inventory Manufacturer Current Assets v Cashv Receivables v Prepaid Expenses v Inventories:1.Raw Materials2.Work in Process3.Finished GoodsBalance SheetPartially complete products –some material, labor, oroverhead has been added. Completed productsawaiting sale. Materials waiting to be processed.Learning Objective 3Prepare an incomestatement includingcalculation of the cost ofgoods sold.The Income StatementCost of goods sold for manufacturers differs only slightly from cost of goodssold for merchandisers.Manufacturing Company Cost of goods sold: Beg. finished goods inv.14,200$ + Cost of goods manufactured 234,150 Goods available for sale 248,350$ - Endingfinished goods inventory (12,100)= Cost of goodssold 236,250$ Merchandising Company Cost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goodssold 236,250$ Inventory Flows Beginning balance Beginning balance Additions to inventory Additions to inventory +=Ending balance Endingbalance Withdrawals frominventory Withdrawalsfrom inventory +Quick Check üIf your inventory balance at the beginning of the month was $1,000, you bought $100 during the month, and sold $300 during the month, what would be the balance at the end of the month?A. $1,000.B. $ 800.C. $1,200.D. $ 200.If your inventory balance at the beginning of the month was $1,000, you bought $100 during the month, and sold $300 during the month, what would be the balance at the end of the month?A. $1,000.B. $ 800.C. $1,200.D. $ 200.Quick Check ü$1,000 + $100 = $1,100$1,100 -$300 = $800Learning Objective 4Prepare a schedule of cost of goods manufactured.Schedule of Cost of Goods Manufactured Calculates the cost of rawmaterial, direct labor andmanufacturing overheadused in production.Calculates the manufacturingcosts associated with goodsthat were finished during the period.ManufacturingWorkRaw Materials Costs In ProcessBeginning rawmaterials inventory +Raw materialspurchased =Raw materials available for usein production–Ending raw materialsinventory=Raw materials usedin productionAs items are removed from raw materials inventory and placed into the production process, they are called directmaterials.As items are removed from raw materials inventory and placed into the productionprocess, they are called direct materials.Schedule of Cost of Goods ManufacturedManufacturingWorkRaw Materials Costs In ProcessBeginning raw Direct materials materials inventory +Direct labor+Raw materials +Mfg. overhead purchased =Total manufacturing =Raw materials costs available for use in production –Ending raw materialsinventory=Raw materials used in production Conversion costs are costs incurred toconvert the direct material into a finishedproduct.Conversion costs are costs incurred to convert the direct material into a finished product.As items are removed from rawmaterials inventory and placed into the production process, they are called direct materials. As items are removed from raw materials inventory and placed into the production process, they are called direct materials. Schedule of Cost of Goods ManufacturedManufacturing WorkRaw Materials Costs In Process Beginning raw Direct materials Beginning work in materials inventory +Direct labor process inventory +Raw materials +Mfg. overhead +Total manufacturing purchased =Total manufacturing costs =Raw materials costs =Total work in available for use process for the in production period –Ending raw materials–Ending work in inventory process inventory=Raw materials used =Cost of goodsin production manufactured.All manufacturing costs incurred during the period are added to the beginning balance of work in process.All manufacturing costs incurred during the period are added to the beginning balance of work in process. Schedule of Cost of Goods Manufactured Manufacturing WorkRaw Materials Costs In Process Beginning raw Direct materials Beginning work in materials inventory +Direct labor process inventory +Raw materials +Mfg. overhead +Total manufacturing purchased =Total manufacturing costs =Raw materials costs =Total work in available for use process for the in production period –Ending raw materials –Ending work in inventory process inventory =Raw materials used =Cost of goods in production manufactured.Costs associated with the goods that are completed during the period are transferred to finished goods inventory.Costs associated with the goods that are completed during the period are transferred to finished goods inventory.Schedule of Cost of Goods ManufacturedWorkIn Process Finished GoodsBeginning work in Beginning finishedprocess inventory goods inventory+Manufacturing costs +Cost of goodsfor the period manufactured=Total work in process =Cost of goodsfor the period available for sale–Ending work in -Ending finishedprocess inventory goods inventory=Cost of goods Cost of goodsmanufactured sold Cost of Goods SoldManufacturing Cost FlowsSelling and Administrative Period Costs Finished Goods Cost ofGoodsSoldSelling and Administrative Manufacturing Overhead Work inProcessDirect Labor Balance Sheet Costs Inventories IncomeStatement Expenses Material Purchases Raw Materials Quick Check üBeginning raw materials inventory was $32,000. During the month, $276,000 of raw material was purchased. A count at the end of the month revealed that $28,000 of raw material was still present. What is the cost of direct material used?A.$276,000B.$272,000C.$280,000D.$ 2,000Beginning raw materials inventory was $32,000. During the month, $276,000 of raw material was purchased. A count at the end of the month revealed that $28,000 of raw material was still present. What is the cost of direct material used?A.$276,000B.$272,000C.$280,000D.$ 2,000Quick Check üBeg. raw materials 32,000$ +Raw materialspurchased 276,000=Raw materials availablefor use in production 308,000$ –Ending raw materialsinventory 28,000=Raw materials usedin production 280,000$Quick Check üDirect materials used in production totaled $280,000. Direct labor was $375,000 and factory overhead was $180,000. What were total manufacturing costs incurred for the month?A.$555,000B.$835,000C.$655,000D.Cannot be determined.Direct materials used in production totaled $280,000. Direct labor was $375,000 and factory overhead was $180,000. What were total manufacturing costs incurred for the month?A.$555,000B.$835,000C.$655,000D.Cannot be determined.Quick Check üDirect Materials 280,000$ +Direct Labor 375,000 +Mfg. Overhead 180,000=Mfg. Costs Incurredfor the Month 835,000$ Quick Check üBeginning work in process was $125,000. Manufacturing costs incurred for the month were $835,000. There were $200,000 of partially finished goods remaining in work in process inventory at the end of the month. What was the cost of goods manufactured during the month?A.$1,160,000B.$ 910,000C.$ 760,000D.Cannot be determined.Beginning work in process was $125,000. Manufacturing costs incurred for the month were $835,000. There were $200,000 of partially finished goods remaining in work in process inventory at the end of the month. What was the cost of goods manufactured during the month?A.$1,160,000B.$ 910,000C.$ 760,000D.Cannot be determined.Quick Check üBeginning work inprocess inventory 125,000$ +Mfg. costs incurredfor the period 835,000=Total work in processduring the period 960,000$ –Ending work inprocess inventory 200,000=Cost of goodsmanufactured 760,000$ Quick Check üBeginning finished goods inventory was $130,000. The cost of goods manufactured for the month was $760,000. The ending finished goods inventory was $150,000. What was the cost of goods sold for the month?A. $ 20,000.B. $740,000.C. $780,000.D. $760,000.Beginning finished goods inventory was$130,000. The cost of goods manufactured for the month was $760,000. The ending finished goods inventory was $150,000. What was the cost of goods sold for the month?A. $ 20,000.B. $740,000.C. $780,000.D. $760,000.Quick Check ü$130,000 + $760,000 = $890,000$890,000 -$150,000 = $740,000Learning Objective 5Define and giveexamples of variablecosts and fixed costs.Cost Classifications for Predicting Cost BehaviorHow a cost will react to changes in the level of business activity.v Total variable costschange when activitychanges.v Total fixed costs remainunchanged when activitychanges.How a cost will react to changes in the level of business activity.v Totalvariable costs change when activity changes.v Total fixed costs remain unchanged when activity changes.Total Variable Cost Your total long distance telephone bill is based on how many minutes you talk.Minutes Talked Tot a lL o n g D is t a n ceT elephon eBillVariable Cost Per UnitMinutes TalkedP e rM i n u te TelephoneC h argeThe cost per long distance minute talked is constant. For example, 10 cents per minute.Total Fixed CostYour monthly basic telephone bill probably does not change when youmake more local calls.Number of Local CallsM o n t h ly B a s icTelephoneB ill Fixed Cost Per Unit Number of Local Calls M o n t h l y B a s i c T e l e p h on eBillpe rLocalCa l lThe average fixed cost per local call decreases as more local calls are made.Cost Classifications for Predicting Cost BehaviorBehavior of Cost (within the relevant range)Cost In Total Per UnitVariable Total variable cost changes Variable cost per unit remains as activity level changes.the same over wide rangesof activity.Fixed Total fixed cost remains Average fixed cost per unit goes the same even when the down as activity level goes up.activity level changes.Quick Check üWhich of the following costs would be variable with respect to the number of cones sold at aBaskins & Robbins shop? (There may bemore than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.D. The cost of napkins for customers.Quick Check üWhich of the following costs would be variable with respect to the number of cones sold at aBaskins & Robbins shop? (There may bemore than one correct answer.)A. The cost of lighting the store.B. The wages of the store manager.C. The cost of ice cream.D. The cost of napkins for customers.Learning Objective 6Define and giveexamples of direct andindirect costs. Assigning Costs to Cost ObjectsDirect costsn Costs that can beeasily and convenientlytraced to a unit ofproduct or other costobject.n Examples: Directmaterial and direct labor Indirect costsn Costs that cannot be easily and convenientlytraced to a unit ofproduct or other costobject.n Example: Manufacturing overheadLearning Objective 7Define and give examples ofcost classifications used inmaking decisions: differentialcosts, opportunity costs, andsunk costs.Cost Classifications for Decision MakingEvery decision involves a choicebetween at least two alternatives. Only those costs andbenefits that differbetween alternativesare relevant to thedecision. All othercosts and benefits canand should be ignored.Differential Costs and RevenuesCosts and revenues that differamong alternatives. Example:You have a job paying $1,500 per month in your hometown. You have a job offer in a neighboring city that pays $2,000 per month. The commuting cost to the city is $300 per month.Differential revenue is: $2,000 –$1,500 = $500Differential cost is:$300Net Differential Benefit is:$200Opportunity CostsThe potential benefit that is given up when one alternative is selectedover another.Example:If you werenot attending college,you could be earning$15,000 per year.Your opportunity costof attending college forone year is $15,000.Sunk CostsSunk costs cannot be changed by any decision. They are not differential costs and should be ignored when making decisions. Example:You bought an automobile that cost $10,000 two years ago. The $10,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $10,000 cost. Quick Check üSuppose you are trying to decide whether todrive or take the train to Portland to attend a concert. You have ample cash to do either, butyou don’t want to waste money needlessly. Isthe cost of the train ticket relevant in thisdecision? In other words, should the cost of thetrain ticket affect the decision of whether youdrive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is notrelevant.Quick Check üSuppose you are trying to decide whether todrive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the cost of the train ticket relevant in this decision? In other words, should the cost of the train ticket affect the decision of whether you drive or take the train to Portland?A. Yes, the cost of the train ticket is relevant.B. No, the cost of the train ticket is notrelevant.Quick Check üSuppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.Quick Check üSuppose you are trying to decide whether to drive or take the train to Portland to attend a concert. You have ample cash to do either, but you don’t want to waste money needlessly. Is the annual cost of licensing your car relevant in this decision?A. Yes, the licensing cost is relevant.B. No, the licensing cost is not relevant.Quick Check üSuppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.Suppose that your car could be sold now for $5,000. Is this a sunk cost?A. Yes, it is a sunk cost.B. No, it is not a sunk cost.Quick Check üSummary of the Types of Cost ClassificationsFinancial Reporting PredictingCost BehaviorAssigning Costs to Cost Objects Decision MakingEnd of Chapter 1。

管理会计第一章(英文版)

targets included in

system should be set at such a level that m an ag e r s and th e people who work for them are motivated to achieve them.

02

Describe and explain the essential requirements of a management accounting system

Chapter catalogue

Management Accounting Information

Collection and Measurement of Information 内容说明内容说明内容说明 Information for Strategic, Operational and Management 内容说明内容说明内容说明 Control

1.4 The Effect of Management Style and Structure

Style

Autocratic vs democratic 内容说明

Structure

内容说明 内容说明

02

An autocratic style, by contrast, means that decision 内容说明 making is exercised at a higher level and therefore the necessary information to enable the function to be carried out will similarly be provided at this level also.

Unit 6 Financial Management and Cost Management

第二部分--Unit 6 Financial Management and Cost Management Topic 1 筹资渠道 Financing SourcesTopic 2 营运资本管理 Working Capital ManagementTopic 3 股利政策 Dividend PolicyTopic 4 资本成本 The cost of capitalTopic 5 企业价值评估 Business valuationsTopic 6 本量利分析 CVP AnalysisTopic 7 绩效评价 Performance MeasurementTopic 1 筹资渠道 Financing Sources1.短期筹资 Short-term finance2.长期筹资 Long-term finance1.短期筹资 Short-term finance短期负债筹资所筹集资金的使用时间较短,一般不超过1年。

短期负债筹资具有如下特点:Funds can be raised by short-term liabilities in short time. Usually short-term liabilities are due within one year. Characteristics of short-term liabilities include the following:(1)筹资速度快,容易取得;Readily available;(2)筹资富有弹性;Flexible;(3)筹资成本较低;Financing cost is low;(4)筹资风险高。

Financing risk is high.企业可使用的短期融资渠道包括短期借款和商业信用。

A range of short-term sources of finance is available to businesses including short-term loans and trade credit.2.长期筹资 Long-term finance长期融资通常用于重要投资,与短期融资相比,成本较高且缺乏灵活性。

Ch02 Managerial Accounting and Cost Concepts

costs. • Cost of regulatory

compliance.

McGraw-Hill/Irwin

Does not include selling or general and administrative

$$$ $$$

Cost of Goods Sold

$$$

McGraw-Hill/Irwin

Copyright © 2006, The McGraw-Hill Companies, Inc.

Flow of Costs Associated With Production

example

Manufacturing cost incurred during this period: $605000

McGraw-Hill/Irwin

Chapter 2 Managerial Accounting and Cost Concepts

Copyright © 2006, The McGraw-Hill Companies, Inc.

Types of Cost Classifications

There are many types of cost in operation of a business In managerial accounting, cost is defined and classified in different ways for different management purposes

Costs necessary to secure the order and deliver the product.

Cost management∶accounting and control 第十一章解答手册