《金融机构管理》作业

金融机构考试题及答案详解

金融机构考试题及答案详解一、单项选择题(每题1分,共10分)1. 以下哪项不是金融机构的类型?A. 商业银行B. 保险公司C. 证券交易所D. 房地产开发商答案:D2. 金融市场的基本功能不包括以下哪项?A. 资金融通B. 风险管理C. 信息提供D. 产品制造答案:D3. 以下哪个是中央银行的职能?A. 制定货币政策B. 经营商业银行业务C. 销售保险产品D. 提供投资咨询答案:A4. 以下哪项不是金融市场的特点?A. 高效性B. 流动性C. 稳定性D. 灵活性答案:C5. 金融机构在进行风险管理时,通常不采用以下哪种方法?A. 风险分散化B. 风险对冲C. 风险转移D. 风险接受答案:D6. 以下哪个不是金融监管的目的?A. 保护投资者利益B. 维护金融市场秩序C. 促进金融机构盈利D. 防范金融风险答案:C7. 以下哪种货币形式属于电子货币?A. 纸币B. 硬币C. 信用卡D. 支票答案:C8. 以下哪个是金融衍生品的特点?A. 低风险B. 高杠杆C. 无风险D. 低杠杆答案:B9. 以下哪个不是金融创新的驱动因素?A. 技术进步B. 市场需求C. 监管政策D. 金融产品过剩答案:D10. 以下哪个是金融中介机构的职能?A. 吸收存款B. 生产商品C. 提供咨询服务D. 销售房地产答案:A二、多项选择题(每题2分,共10分)11. 金融机构可以提供哪些服务?(ABCDE)A. 信贷服务B. 投资服务C. 保险服务D. 咨询服务E. 资产管理服务答案:ABCDE12. 以下哪些是金融监管机构的职责?(ABCD)A. 制定监管政策B. 监督金融机构的合规性C. 处理违规行为D. 维护金融市场稳定E. 为金融机构提供咨询服务答案:ABCD13. 金融市场的参与者包括哪些?(ABCE)A. 个人投资者B. 机构投资者C. 政府D. 房地产开发商E. 金融机构答案:ABCE14. 以下哪些是金融市场的分类?(ABD)A. 货币市场B. 资本市场C. 商品市场D. 外汇市场E. 房地产市场答案:ABD15. 以下哪些是金融风险的类型?(ABC)A. 信用风险B. 市场风险C. 操作风险D. 技术风险E. 法律风险答案:ABC三、判断题(每题1分,共5分)16. 所有金融机构都必须接受金融监管机构的监管。

金融机构风险管理练习习题

【经典资料,WORD文档,可编辑修改】【经典考试资料,答案附后,看后必过,WORD文档,可修改】金融机构风险管理练习题第七章金融中介机构的风险练习1.描述下列金融机构在交易中遇到的风险敞口,请选出下面的一种或几种。

a利率风险b信用风险c表外风险d技术风险e汇率风险f国家风险(1)银行通过出售一年期CD为价值$2000万的五年期固定汇率的商业贷款融资。

(2)保险公司把保险费投在长期政府债券组合中。

(3)一家德国银行出售2年期、固定利率债券为波兰公司提供的2年期、固定利率贷款融资。

(4)英国银行收购澳大利亚银行减少结算操作的麻烦。

(5)使用远期或有合约对利率风险敝口进行了完全的套期保值。

(6)债券经纪人公司用自己的股本在LDC债券市场上购买巴西债务。

(7)银行出售一组抵押贷款作为抵押证券。

练习2公司特有信用风险与系统信用风险的区别是什么金融机构如何减少公司特有信用风险第八章:利率风险:重定价模型练习1:下面哪一项资产或负债符合一年期利率或重定价的敏感性条件天期美国国库券年期美国国库券年期美国国库券bank repurchases $100000 of common stockbank issues $2000000 of CDs and uses the proceeds for loans to home-owners.bank receives $500000 in deposits and invests them in T-bills.bank issued $800000 in common stock and lends it to help finance a new shopping mall.bank issued $1000000 in nonqualifying perpetual preferred stock and purchases general obligation municipal bonds.pay back $4000000 of mortgages, and the bank used the proceeds to build new ATMs.练习3:What is the bank’s capital adequacy level (unde r Basel I and Basel II)Off-balance-sheet items:Risk weight 100%:1.$80m in 2-year loan commitments to a large BB+ rated . corporation.2.$10m direct credit substitute standby letters of credit issued to a BBB rated . corporation.3.$50m in commercial letters of credit issued to a BBB- rated . corporation.Risk weight 50%:fixed-floating interest rate swap for 4 year with notional dollar value of $100m and replacement cost of $3m.two year Euro$ contract for $40m with a replacement cost of -$1m练习4:Third bank has following balance sheet (in millions) with the risk weights in parentheses.Assets Liabilities and EquityCash(0%)$20 Deposits$175OECD interbank deposits(20%)25Subordinated debt years)3Mortgage loans(50%)70cumulative preferred stock5。

《金融风险管理》习题集

《金融风险管理》习题集第一章、中国金融业概论一、名词解释1、“大一统”的银行体系2、双重银行体系3、政策性银行4、信用合作社5、汇率并轨二、单项选择1、在中国银行业的分类中,下列选项属于“国有银行”的是()A.商业银行B.农村商业银行C.政策性银行D.信用合作社2、2001年中国成立了第一家政策性保险公司,它是()A.中国人民保险公司B.太平洋保险公司C.平安保险公司D.中国进出口信用保险公司3、下列选项中不属于我国按照债券品种分类的市场是()A.银行间债券市场B.债券柜台交易市场C.交易所债券市场D.凭证式债券市场4、下列监管职能中,自2003年4月起不属于人民银行监管范围的有()A.不良贷款及银行的资本充足率B.银行间拆借市场C.银行间债券市场D.执行存款准备金的管理5、根据中国对世贸组织的承诺下列城市中,属于第一批开放的城市是()A.成都B.大连C.南京D.北京6、《境外金融机构投资入股中金融机构管理办法》中规定,境外金融投资机构中资机构入股比例的上限是()A.15%B.20%C.25%D.30%7、下列选项中,不属于中国银行业三个有待解决的问题是()A.使应该中国银行的资本充足率达到《巴塞尔协议Ⅱ》的要求B.改革四大国有银行C.改革农村信用合作社D.充足小型银行和困难银行8、保监会对设立中外合资寿险公司中外资参股比例的规定是()A.不得超过25%B.不得超过30%C.不得超过50%D.不得超过51%9、1995年《中国商业银行法》中第一次明确规定所有商业银行的资本充足率不得低于()A.2%B.4%C.6%D.8%10、下列选项中,不属于《巴塞尔协尔Ⅱ》的三大核心内容的是()A.信息披露B.资本充足率要求C.金融监管D.市场约束三、简答题1、请简要回答中国金融业的发展过程。

2、请简要回答中国银监会的主要职能与目标。

3、请简要回答外资银行进入中国的五个阶段。

4、请简要回答中国监管当局目前关于资本充足率的规定。

第五章金融机构体系作业和答案

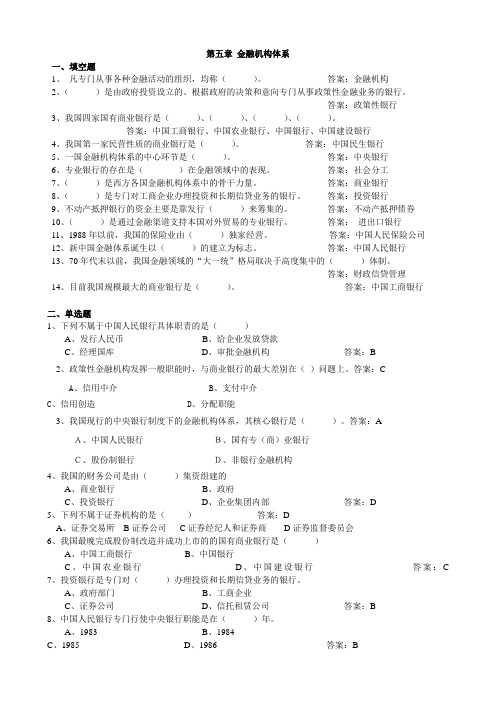

第五章金融机构体系一、填空题1、凡专门从事各种金融活动的组织,均称()。

答案:金融机构2、()是由政府投资设立的、根据政府的决策和意向专门从事政策性金融业务的银行。

答案:政策性银行3、我国四家国有商业银行是()、()、()、()。

答案:中国工商银行、中国农业银行、中国银行、中国建设银行4、我国第一家民营性质的商业银行是()。

答案:中国民生银行5、一国金融机构体系的中心环节是()。

答案:中央银行6、专业银行的存在是()在金融领域中的表现。

答案:社会分工7、()是西方各国金融机构体系中的骨干力量。

答案:商业银行8、()是专门对工商企业办理投资和长期信贷业务的银行。

答案:投资银行9、不动产抵押银行的资金主要是靠发行()来筹集的。

答案:不动产抵押债券10、()是通过金融渠道支持本国对外贸易的专业银行。

答案:进出口银行11、1988年以前,我国的保险业由()独家经营。

答案:中国人民保险公司12、新中国金融体系诞生以()的建立为标志。

答案:中国人民银行13、70年代末以前,我国金融领域的“大一统”格局取决于高度集中的()体制。

答案:财政信贷管理14、目前我国规模最大的商业银行是()。

答案:中国工商银行二、单选题1、下列不属于中国人民银行具体职责的是()A、发行人民币B、给企业发放贷款C、经理国库D、审批金融机构答案:B2、政策性金融机构发挥一般职能时,与商业银行的最大差别在()问题上。

答案:CA、信用中介B、支付中介C、信用创造D、分配职能3、我国现行的中央银行制度下的金融机构体系,其核心银行是()。

答案:AA、中国人民银行B、国有专(商)业银行C、股份制银行D、非银行金融机构4、我国的财务公司是由()集资组建的A、商业银行B、政府C、投资银行D、企业集团内部答案:D5、下列不属于证券机构的是()答案:DA、证券交易所B证券公司C证券经纪人和证券商D证券监督委员会6、我国最晚完成股份制改造并成功上市的的国有商业银行是()A、中国工商银行B、中国银行C、中国农业银行D、中国建设银行答案:C7、投资银行是专门对()办理投资和长期信贷业务的银行。

金融机构风险管理金融机构风险管理习题2

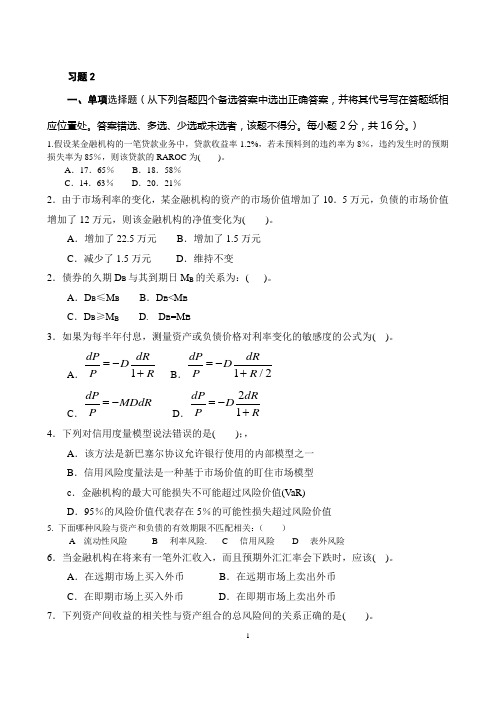

习题2一、单项选择题(从下列各题四个备选答案中选出正确答案,并将其代号写在答题纸相应位置处。

答案错选、多选、少选或未选者,该题不得分。

每小题2分,共16分。

)1.假设某金融机构的一笔贷款业务中,贷款收益率1.2%,若未预料到的违约率为8%,违约发生时的预期损失率为85%,则该贷款的RAROC 为( )。

A .17.65%B .18.58%C .14.63%D .20.21%2.由于市场利率的变化,某金融机构的资产的市场价值增加了10.5万元,负债的市场价值增加了12万元,则该金融机构的净值变化为( )。

A .增加了22.5万元B .增加了1.5万元C .减少了1.5万元D .维持不变2.债券的久期D B 与其到期日M B 的关系为:( )。

A .DB ≤M B B .D B <M BC .D B ≥M B D. D B =M B3.如果为每半年付息,测量资产或负债价格对利率变化的敏感度的公式为( )。

A .1dP dR D PR =-+ B .1/2dP dR D P R =-+ C .dP MDdR P =- D .21dP dR D PR =-+ 4.下列对信用度量模型说法错误的是( );,A .该方法是新巴塞尔协议允许银行使用的内部模型之一B .信用风险度量法是一种基于市场价值的盯住市场模型c .金融机构的最大可能损失不可能超过风险价值(VaR)D .95%的风险价值代表存在5%的可能性损失超过风险价值5. 下面哪种风险与资产和负债的有效期限不匹配相关:( )A 流动性风险B 利率风险.C 信用风险D 表外风险6.当金融机构在将来有一笔外汇收入,而且预期外汇汇率会下跌时,应该( )。

A .在远期市场上买入外币B .在远期市场上卖出外币C .在即期市场上买入外币D .在即期市场上卖出外币7.下列资产间收益的相关性与资产组合的总风险间的关系正确的是( )。

A.资产间收益若为完全正相关则资产组合的总风险越大B.资产间收益若为完全负相关则资产组合的总风险越大C.资产间收益若不相关则资产组合的总风险越大D.资产间收益若一些为负相关,而另一些为正相关则资产8.金融机构的表外业务是( )。

金融机构考试题及答案

金融机构考试题及答案一、选择题(每题1分,共10分)1. 以下哪个不是金融机构的类型?A. 商业银行B. 保险公司C. 证券交易所D. 房地产开发商答案:D2. 金融监管机构的主要职能是什么?A. 提供金融服务B. 监管金融市场C. 进行金融投资D. 管理金融风险答案:B3. 以下哪个不是金融产品?A. 股票B. 债券C. 期货D. 房地产答案:D4. 金融衍生品的主要功能是什么?A. 投资B. 投机C. 风险管理D. 赚取利润答案:C5. 以下哪个是金融市场的参与者?A. 政府B. 个人投资者C. 企业D. 所有以上选项答案:D6. 什么是信用评级机构的主要任务?A. 评估企业的财务状况B. 提供投资建议C. 管理金融市场D. 发行金融产品答案:A7. 以下哪个是金融创新的类型?A. 金融产品创新B. 金融技术创新C. 金融服务创新D. 所有以上选项答案:D8. 什么是金融杠杆?A. 金融工具的放大效应B. 金融风险的减少C. 金融资产的减少D. 金融收益的减少答案:A9. 什么是货币政策?A. 政府对经济的直接干预B. 中央银行调控货币供应量的政策C. 企业对经济的间接影响D. 个人对经济的直接干预答案:B10. 什么是利率?A. 货币的购买力B. 货币的时间价值C. 货币的存储成本D. 货币的交换价值答案:B二、判断题(每题1分,共5分)1. 银行是唯一可以提供贷款的金融机构。

(错误)2. 金融监管可以完全消除金融市场的风险。

(错误)3. 金融衍生品可以用来对冲风险。

(正确)4. 信用评级机构的评级结果对投资者没有影响。

(错误)5. 中央银行是货币政策的制定者和执行者。

(正确)三、简答题(每题5分,共15分)1. 请简述金融市场的功能。

金融市场具有资金配置、价格发现、风险分散和信息传递等功能。

2. 请解释什么是金融监管?金融监管是指政府或其授权的机构对金融市场和金融机构进行监督和管理,以维护金融市场的稳定和公平。

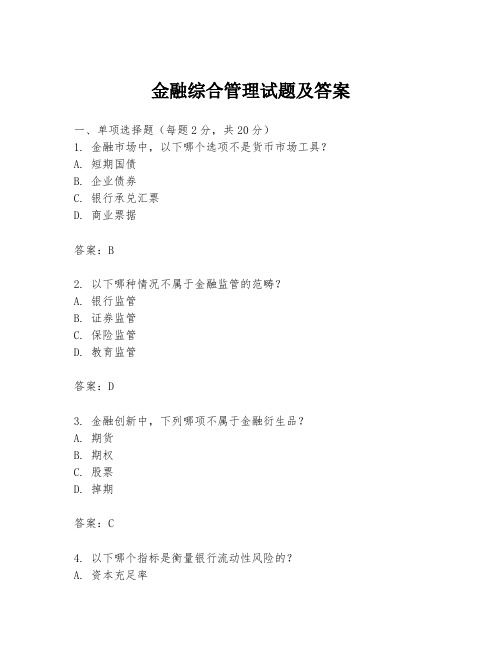

金融综合管理试题及答案

金融综合管理试题及答案一、单项选择题(每题2分,共20分)1. 金融市场中,以下哪个选项不是货币市场工具?A. 短期国债B. 企业债券C. 银行承兑汇票D. 商业票据答案:B2. 以下哪种情况不属于金融监管的范畴?A. 银行监管B. 证券监管C. 保险监管D. 教育监管答案:D3. 金融创新中,下列哪项不属于金融衍生品?A. 期货B. 期权C. 股票D. 掉期答案:C4. 以下哪个指标是衡量银行流动性风险的?A. 资本充足率B. 杠杆率C. 贷款损失准备金D. 流动性覆盖率答案:D5. 以下哪个选项不是金融风险管理的步骤?A. 风险识别B. 风险评估C. 风险规避D. 风险转移答案:C6. 金融科技(FinTech)主要不包括以下哪项技术?A. 大数据B. 云计算C. 人工智能D. 传统银行业务答案:D7. 以下哪种金融产品不属于资产管理业务?A. 基金B. 股票C. 债券D. 保险答案:B8. 以下哪个因素不是影响汇率变动的主要因素?A. 利率水平B. 政治稳定性C. 贸易顺差D. 人口数量答案:D9. 以下哪个选项不是金融稳定委员会(FSB)的成员?A. 国际货币基金组织(IMF)B. 世界银行C. 国际清算银行(BIS)D. 联合国答案:D10. 以下哪个金融工具不是用于对冲利率风险的?A. 利率互换B. 利率期货C. 货币期权D. 股票期权答案:D二、多项选择题(每题3分,共30分)1. 以下哪些属于金融监管的基本原则?A. 监管独立性B. 监管透明度C. 监管灵活性D. 监管统一性答案:A、B、D2. 金融创新对金融市场的影响包括以下哪些方面?A. 增加了金融产品的种类B. 提高了金融市场的效率C. 增加了金融市场的风险D. 减少了金融市场的参与者答案:A、B、C3. 金融科技(FinTech)对传统金融行业的影响主要体现在以下哪些方面?A. 支付方式的变革B. 信贷审批流程的优化C. 投资顾问服务的个性化D. 金融产品的同质化答案:A、B、C4. 以下哪些措施可以提高银行的流动性?A. 增加现金储备B. 减少长期贷款C. 增加短期存款D. 增加长期债券投资答案:A、B、C5. 以下哪些属于金融风险管理的工具?A. 风险分散B. 风险转移C. 风险对冲D. 风险补偿答案:A、B、C6. 以下哪些因素会影响货币市场的需求?A. 利率水平B. 通货膨胀率C. 政府财政政策D. 消费者信心答案:A、B、C7. 以下哪些属于资产管理业务的范畴?A. 基金管理B. 股票投资C. 债券投资D. 保险产品答案:A、C、D8. 以下哪些因素会影响汇率的稳定性?A. 国际收支状况B. 国内经济状况C. 国际政治局势D. 贸易政策答案:A、B、C9. 金融稳定委员会(FSB)的主要任务包括以下哪些方面?A. 监管全球系统重要性金融机构B. 制定国际金融监管标准C. 促进各国金融监管机构的合作D. 推动全球金融市场的自由化答案:A、B、C10. 以下哪些措施可以降低金融风险?A. 加强风险管理B. 提高资本充足率C. 增加流动性储备D. 减少金融创新答案:A、B、C三、判断题(每题2分,共20分)1. 金融监管的目的是确保金融市场的稳定和公平。

风险管理与金融机构第五版作业题答案15章

风险管理与金融机构第五版作业题答案15章一、解释名词1、金融监管:金融监管是金融监督和金融管理的复合词。

金融监管有狭义和广义之分。

狭义的金融监管是指金融主管当局依据国家法律法规的授权对金融业(包括金融机构以及它们在金融市场上的业务活动)实施监督、约束、管制.使它们依法稳健运行的行为总称。

广义的金融监管除主管当局的旦莹管之外,还包括金融机构的内部控制与稽核、行业自律性组织的监督以及社会中介组织的监督等。

2、金融监管体制:金融监管体制,指的是金融监管的制度安排,它包括金融监管当局对金融机构和金融市场施加影响的机制以及监管体系的组织结构。

山于各国历史文化传统、法律、政治体制、经济发展水平等方面的差异,金融监管机构的设置颇不相同。

根据监管主体的多少,各国的金融监管体制大致可以划分为单监管体制和多头监管体制。

3、单一金融监管体制:它是金融监管体制的一种类型,即由一家金融监管机关对金融业实施高度集中监管的体制。

单一体制的监管机关通常是各国的中央银行,也有另设独立监管机关的。

监管职责是归中央银行还是归单设的独立机构,并非确定不移。

4、多头金融监管体制:它是金融监管体制的一种类型,是根据从事金融业务的不同机构主体及其业务范围的不同.由不同的监管机构分别实施监管的体制。

根据监管权限在中央和地方的不同划分,又可将其区分为分权多头式和集权多头式两种。

5、分权多头金融监管体制:它是多头式金融监管体制的一种形式,实行这种监管体制的国家一般为联邦制国家。

其主要特征表现为:不仪不同的金融机构或金融业务由不同的监管机关来实施监管,而且联邦和州(或省)都有权对相应的金融机构实施监管。

6、集权多头金融监管体制:它是多头式金融监管体制的一种形式,实行这种监管体制的国家,对不同金融机构或金融业务的监管,由不5同的监管机关来实施,但监管权限集中于中央政府。

至于多头的监管主体,有的是以财政部和中央银行为主,有的则另设机构。

我国当前的金融监管体制,属丁集权多头式。

Chap008金融机构管理课后题答案

Chapter EightInterest Rate Risk IChapter OutlineIntroductionThe Central Bank and Interest Rate RiskThe Repricing ModelRate-Sensitive AssetsRate-Sensitive LiabilitiesEqual Changes in Rates on RSAs and RSLsUnequal Changes in Rates on RSAs and RSLsWeaknesses of the Repricing ModelMarket Value EffectsOveraggregationThe Problem of RunoffsCash Flows from Off-Balance Sheet ActivitiesThe Maturity ModelThe Maturity Model with a Portfolio of Assets and Liabilities Weakness of the Maturity ModelSummaryAppendix 8A: Term Structure of Interest RatesUnbiased Expectations TheoryLiquidity Premium Theory Market Segmentation TheorySolutions for End-of-Chapter Questions and Problems: Chapter Eight1. What was the impact on interest rates of the borrowed reserves targetingregime used by the Federal Reserve from 1982 to 1993The volatility of interest rates was significantly lower than under the nonborrowed reserves target regime used in the three years immediately prior to 1982. Figure 8-1 indicates that both the level and volatility of interest rates declined even further after 1993 when the Fed decided that it would target primarily the fed funds rate as a guide for monetary policy.2. How has the increased level of financial market integration affectedinterest ratesIncreased financial market integration, or globalization, increases the speed with which interest rate changes and volatility are transmitted among countries. The result of this quickening of global economic adjustment is to increase the difficulty and uncertainty faced by the Federal Reserve as it attempts to manage economic activity within the U.S. Further, because FIs have become increasingly more global in their activities, any change in interest rate levels or volatility caused by Federal Reserve actions more quickly creates additional interest rate risk issues for these companies.3. What is the repricing gap In using this model to evaluate interest raterisk, what is meant by rate sensitivity On what financial performance variable does the repricing model focus Explain.The repricing gap is a measure of the difference between the dollar value of assets that will reprice and the dollar value of liabilities that will reprice within a specific time period, where reprice means the potential to receive a new interest rate. Rate sensitivity represents the time interval where repricing can occur. The model focuses on the potential changes in the net interest income variable. In effect, if interest rates change, interest income and interest expense will change as the various assets and liabilities are repriced, that is, receive new interest rates.4. What is a maturity bucket in the repricing model Why is the length oftime selected for repricing assets and liabilities important when using the repricing modelThe maturity bucket is the time window over which the dollar amounts of assets and liabilities are measured. The length of the repricing period determines which of the securities in a portfolio are rate-sensitive. The longer the repricing period, the more securities either mature or need to be repriced, and, therefore, the more the interest rate exposure. An excessively short repricing period omits consideration of the interest rate risk exposure of assets and liabilities are that repriced in the period immediately following the end of the repricing period. That is, it understates the rate sensitivity of the balance sheet. An excessively long repricing period includes many securities that are repriced at different times within the repricing period, thereby overstating the rate sensitivity of the balance sheet.5. Calculate the repricing gap and the impact on net interest income of a 1percent increase in interest rates for each of the following positions:Rate-sensitive assets = $200 million. Rate-sensitive liabilities =$100 million.Repricing gap = RSA - RSL = $200 - $100 million = +$100 million.NII = ($100 million)(.01) = +$ million, or $1,000,000.Rate-sensitive assets = $100 million. Rate-sensitive liabilities =$150 million.Repricing gap = RSA - RSL = $100 - $150 million = -$50 million.NII = (-$50 million)(.01) = -$ million, or -$500,000.Rate-sensitive assets = $150 million. Rate-sensitive liabilities =$140 million.Repricing gap = RSA - RSL = $150 - $140 million = +$10 million.NII = ($10 million)(.01) = +$ million, or $100,000.a. Calculate the impact on net interest income on each of the abovesituations assuming a 1 percent decrease in interest rates.NII = ($100 million) = -$ million, or -$1,000,000.NII = (-$50 million) = +$ million, or $500,000.NII = ($10 million) = -$ million, or -$100,000.b. What conclusion can you draw about the repricing model from theseresultsThe FIs in parts (1) and (3) are exposed to interest rate declines(positive repricing gap) while the FI in part (2) is exposed to interest rate increases. The FI in part (3) has the lowest interest rate riskexposure since the absolute value of the repricing gap is the lowest,while the opposite is true for part (1).6. What are the reasons for not including demand deposits as rate-sensitiveliabilities in the repricing analysis for a commercial bank What is the subtle, but potentially strong, reason for including demand deposits inthe total of rate-sensitive liabilities Can the same argument be madefor passbook savings accountsThe regulatory rate available on demand deposit accounts is zero. Although many banks are able to offer NOW accounts on which interest can be paid, this interest rate seldom is changed and thus the accounts are not really sensitive. However, demand deposit accounts do pay implicit interest in the form of not charging fully for checking and other services. Further, when market interest rates rise, customers draw down their DDAs, which may cause the bank to use higher cost sources of funds. The same or similar arguments can be made for passbook savings accounts.7. What is the gap ratio What is the value of this ratio to interest raterisk managers and regulatorsThe gap ratio is the ratio of the cumulative gap position to the total assets of the bank. The cumulative gap position is the sum of the individual gaps over several time buckets. The value of this ratio is that it tells the direction of the interest rate exposure and the scale of that exposure relative to the size of the bank.8. Which of the following assets or liabilities fit the one-year rate or repricing sensitivity test91-day . Treasury bills Yes1-year . Treasury notes Yes20-year . Treasury bonds No20-year floating-rate corporate bonds with annual repricing Yes30-year floating-rate mortgages with repricing every two years No30-year floating-rate mortgages with repricing every six months YesOvernight fed funds Yes9-month fixed rate CDs Yes1-year fixed-rate CDs Yes5-year floating-rate CDs with annual repricing YesCommon stock No9. Consider the following balance sheet for WatchoverU Savings, Inc. (in millions):Assets Liabilities and EquityFloating-rate mortgages Demand deposits(currently 10% annually) $50 (currently 6% annually) $7030-year fixed-rate loans Time deposits(currently 7% annually) $50 (currently 6% annually $20Equity $10 Total Assets $100 Total Liabilities & Equity$100a. What is WatchoverU’s expected net interest income at year-endCurrent expected interest income:$5m + $3.5m = $8.5m.Expected interest expense: $4.2m + $1.2m = $5.4m.Expected net interest income: $8.5m - $5.4m = $3.1m.b. What will be the net interest income at year-end if interest ratesrise by 2 percentAfter the 200 basis point interest rate increase, net interest incomedeclines to:50 + 50 - 70 - 20(.06) = $9.5m - $6.8m = $2.7m, a decline of $0.4m.c. Using the cumulative repricing gap model, what is the expected netinterest income for a 2 percent increase in interest rates Wachovia’s' repricing or funding gap is $50m - $70m = -$20m. The change in net interest income using the funding gap model is (-$20m) = -$.4m.d.What will be the net interest income at year-end if interest ratesincrease 200 basis points on assets, but only 100 basis points onliabilities Is it reasonable for changes in interest rates to affectbalance sheet in an uneven manner WhyAfter the unbalanced rate increase, net interest income will be 50 +50 - 70 - 20(.06) = $9.5m - $6.1m = $3.4m, an increase of $0.3m. It isnot uncommon for interest rates to adjust in an uneven manner over two sides of the balance sheet because interest rates often do not adjust solely because of market pressures. In many cases the changes areaffected by decisions of management. Thus you can see the difference between this answer and the answer for part a.10. What are some of the weakness of the repricing model How have largebanks solved the problem of choosing the optimal time period forrepricing What is runoff cash flow, and how does this amount affect the repricing model’s analysisThe repricing model has four general weaknesses:(1) It ignores market value effects.(2) It does not take into account the fact that the dollar value of ratesensitive assets and liabilities within a bucket are not similar. Thus, if assets, on average, are repriced earlier in the bucket thanliabilities, and if interest rates fall, FIs are subject to reinvestment risks.(3) It ignores the problem of runoffs, that is, that some assets are prepaidand some liabilities are withdrawn before the maturity date.(4) It ignores income generated from off-balance-sheet activities.Large banks are able to reprice securities every day using their own internal models so reinvestment and repricing risks can be estimated for each day ofthe year.Runoff cash flow reflects the assets that are repaid before maturity and the liabilities that are withdrawn unsuspectedly. To the extent that either of these amounts is significantly greater than expected, the estimated interest rate sensitivity of the bank will be in error.11. Use the following information about a hypothetical government securitydealer named . Jorgan. Market yields are in parenthesis, and amounts are in millions.Assets Liabilities and EquityCash $10 Overnight Repos $1701 month T-bills %) 75 Subordinated debt3 month T-bills %) 75 7-year fixed rate % 1502 year T-notes %) 508 year T-notes %) 1005 year munis (floating rate)% reset every 6 months) 25 Equity 15 Total Assets $335 Total Liabilities & Equity$335a. What is the funding or repricing gap if the planning period is 30 days91 days 2 years Recall that cash is a noninterest-earning asset.Funding or repricing gap using a 30-day planning period = 75 - 170 = -$95 million.Funding gap using a 91-day planning period = (75 + 75) - 170 = -$20 million.Funding gap using a two-year planning period = (75 + 75 + 50 + 25) - 170 = +$55 million.b. What is the impact over the next 30 days on net interest income if allinterest rates rise 50 basis points Decrease 75 basis pointsNet interest income will decline by $475,000. NII = FG(R) = -95(.005) = $0.475m.Net interest income will increase by $712,500. NII = FG(R)= -95(.0075) = $0.7125m.c.The following one-year runoffs are expected: $10 million for two-yearT-notes, and $20 million for eight-year T-notes. What is the one-year repricing gapFunding or repricing gap over the 1-year planning period = (75 + 75 + 10 + 20 + 25) - 170 = +$35 million.d. If runoffs are considered, what is the effect on net interest incomeat year-end if interest rates rise 50 basis points Decrease 75 basispointsNet interest income will increase by $175,000. NII = FG(R) = 35 = $0.175m.Net interest income will decrease by $262,500, NII = FG(R) = 35 = -$0.2625m.12. What is the difference between book value accounting and market valueaccounting How do interest rate changes affect the value of bank assets and liabilities under the two methods What is marking to marketBook value accounting reports assets and liabilities at the original issue values. Current market values may be different from book values because they reflect current market conditions, such as interest rates or prices. This is especially a problem if an asset or liability has to be liquidated immediately. If the asset or liability is held until maturity, then the reporting of book values does not pose a problem.For an FI, a major factor affecting asset and liability values is interestrate changes. If interest rates increase, the value of both loans (assets) and deposits and debt (liabilities) fall. If assets and liabilities are held until maturity, it does not affect the book valuation of the FI. However, ifdeposits or loans have to be refinanced, then market value accounting presents a better picture of the condition of the FI.The process by which changes in the economic value of assets and liabilities are accounted is called marking to market. The changes can be beneficial as well as detrimental to the total economic health of the FI.13. Why is it important to use market values as opposed to book values whenevaluating the net worth of an FI What are some of the advantages ofusing book values as opposed to market valuesBook values represent historical costs of securities purchased, loans made, and liabilities sold. They do not reflect current values as determined by market values. Effective financial decision-making requires up-to-date information that incorporates current expectations about future events. Market values provide the best estimate of the present condition of an FI and serve as an effective signal to managers for future strategies.Book values are clearly measured and not subject to valuation errors, unlike market values. Moreover, if the FI intends to hold the security until maturity, then the security's current liquidation value will not be relevant. That is, the paper gains and losses resulting from market value changes will never be realized if the FI holds the security until maturity. Thus, the changes in market value will not impact the FI's profitability unless the security is sold prior to maturity.14. Consider a $1,000 bond with a fixed-rate 10 percent annual coupon (Cpn %)and a maturity (N) of 10 years. The bond currently is trading to amarket yield to maturity (YTM) of 10 percent. Complete the followingtable.From Par, $ From Par, %N Cpn % YTM Price Change in Price Change in Price8 10% 9% $1, $ %9 10% 9% $1, $ %10 10% 9% $1, $ %10 10% 10% $1,10 10% 11% $ -$ %11 10% 11% $ -$ %12 10% 11% $ -$ %Use this information to verify the principles of interest rate-pricerelationships for fixed-rate financial assets.Rule One: Interest rates and prices of fixed-rate financial assets move inversely. See the change in price from $1,000 to $ for the change in interest rates from 10 percent to 11 percent, or from $1,000 to $1, when rates change from 10 percent to 9 percent.Rule Two: The longer is the maturity of a fixed-income financial asset, the greater is the change in price for a given change in interest rates.A change in rates from 10 percent to 11 percent has caused the 10-yearbond to decrease in value $, but the 11-year bond will decrease in value $, and the 12-year bond will decrease $.Rule Three: The change in value of longer-term fixed-rate financialassets increases at a decreasing rate. For the increase in rates from 10 percent to 11 percent, the difference in the change in price between the 10-year and 11-year assets is $, while the difference in the change in price between the 11-year and 12-year assets is $.Rule Four: Although not mentioned in the text, for a given percentage () change in interest rates, the increase in price for a decrease in ratesis greater than the decrease in value for an increase in rates. Thus for rates decreasing from 10 percent to 9 percent, the 10-year bond increases $. But for rates increasing from 10 percent to 11 percent, the 10-year bond decreases $.15. Consider a 12-year, 12 percent annual coupon bond with a required returnof 10 percent. The bond has a face value of $1,000.a. What is the price of the bondPV = $120*PVIFAi=10%,n=12 + $1,000*PVIFi=10%,n=12= $1,b. If interest rates rise to 11 percent, what is the price of the bondPV = $120*PVIFAi=11%,n=12 + $1,000*PVIFi=11%,n=12= $1,c. What has been the percentage change in priceP = ($1, - $1,/$1, = or – percent.d. Repeat parts (a), (b), and (c) for a 16-year bond.PV = $120*PVIFAi=10%,n=16 + $1,000*PVIFi=10%,n=16= $1,PV = $120*PVIFAi=11%,n=16 + $1,000*PVIFi=11%,n=16= $1,P = ($1, - $1,/$1, = or – percent.e. What do the respective changes in bond prices indicateFor the same change in interest rates, longer-term fixed-rate assets have a greater change in price.16. Consider a five-year, 15 percent annual coupon bond with a face value of$1,000. The bond is trading at a market yield to maturity of 12 percent.a. What is the price of the bondPV = $150*PVIFAi=12%,n=5 + $1,000*PVIFi=12%,n=5= $1,b. If the market yield to maturity increases 1 percent, what will be thebond’s new pricePV = $150*PVIFAi=13%,n=5 + $1,000*PVIFi=13%,n=5= $1,c. Using your answers to parts (a) and (b), what is the percentage changein the bond’s price as a result of the 1 percent increase in interest ratesP = ($1, - $1,/$1, = or – percent.d. Repeat parts (b) and (c) assuming a 1 percent decrease in interestrates.PV = $150*PVIFAi=11%,n=5 + $1,000*PVIFi=11%,n=5= $1,P = ($1, - $1,/$1, = or percente. What do the differences in your answers indicate about the rate-pricerelationships of fixed-rate assetsFor a given percentage change in interest rates, the absolute value of the increase in price caused by a decrease in rates is greater than the absolute value of the decrease in price caused by an increase in rates.17. What is maturity gap How can the maturity model be used to immunize anFI’s portfolio What is the critical requirement to allow maturitymatching to have some success in immunizing the balance sheet of an FIMaturity gap is the difference between the average maturity of assets and liabilities. If the maturity gap is zero, it is possible to immunize the portfolio, so that changes in interest rates will result in equal but offsetting changes in the value of assets and liabilities and net interest income. Thus, if interest rates increase (decrease), the fall (rise) in the value of the assets will be offset by a perfect fall (rise) in the value of the liabilities. The critical assumption is that the timing of the cash flows on the assets and liabilities must be the same.18. Nearby Bank has the following balance sheet (in millions):Assets Liabilities and EquityCash $60 Demand deposits $1405-year treasury notes $60 1-year Certificates of Deposit $160 30-year mortgages $200 Equity $20Total Assets $320 Total Liabilities and Equity$320What is the maturity gap for Nearby Bank Is Nearby Bank more exposed to an increase or decrease in interest rates Explain whyM A = [0*60 + 5*60 + 200*30]/320 = years, and ML= [0*140 + 1*160]/300 = .Therefore the maturity gap = MGAP = – = years. Nearby bank is exposed toan increase in interest rates. If rates rise, the value of assets will decrease much more than the value of liabilities.19. County Bank has the following market value balance sheet (in millions,annual rates):Assets Liabilities and EquityCash $20 Demand deposits $10015-year commercial loan @ 10% 5-year CDs @ 6% interest,interest, balloon payment $160 balloon payment $21030-year Mortgages @ 8% interest, 20-year debentures @ 7% interest$120monthly amortizing $300 Equity $50Total Assets $480 Total Liabilities & Equity $480a. What is the maturity gap for County BankMA= [0*20 + 15*160 + 30*300]/480 = years.ML= [0*100 + 5*210 + 20*120]/430 = years.MGAP = – = years.b. What will be the maturity gap if the interest rates on all assets andliabilities increase by 1 percentIf interest rates increase one percent, the value and average maturity of the assets will be:Cash = $20Commercial loans = $16*PVIFAn=15, i=11% + $160*PVIFn=15,i=11%= $Mortgages = $,294*PVIFAn=360,i=9%= $MA= [0*20 + *15 + *30]/(20 + + = yearsThe value and average maturity of the liabilities will be: Demand deposits = $100CDs = $*PVIFAn=5,i=7% + $210*PVIFn=5,i=7%= $Debentures = $*PVIFAn=20,i=8% + $120*PVIFn=20,i=8%= $ML= [0*100 + 5* + 20*]/(100 + + = yearsThe maturity gap = MGAP = – = years. The maturity gap increased because the average maturity of the liabilities decreased more than the average maturity of the assets. This result occurred primarily because of the differences in the cash flow streams for the mortgages and the debentures.c. What will happen to the market value of the equityThe market value of the assets has decreased from $480 to $, or $. The market value of the liabilities has decreased from $430 to $, or $. Therefore the market value of the equity will decrease by $ - $ = $, or percent.d. If interest rates increased by 2 percent, would the bank be solvent The value of the assets would decrease to $, and the value of the liabilities would decrease to $. Therefore the value of the equity would be $. Although the bank remains solvent, nearly 65 percent of the equity has eroded because of the increase in interest rates.20. Given that bank balance sheets typically are accounted in book valueterms, why should the regulators or anyone else be concerned about howinterest rates affect the market values of assets and liabilitiesThe solvency of the balance sheet is an important variable to creditors of the bank. If the capital position of the bank decreases to near zero, creditors may not be willing to provide funding for the bank, and the bank may need assistance from the regulators, or may even fail. Thus any change in the market value of assets or liabilities that is caused by changes in the level of interest rate changes is of concern to regulators.21. If a bank manager is certain that interest rates were going to increasewithin the next six months, how should the bank manager adjust thebank’s maturity gap to take advantage of this antici pated increase What if the manager believed rates would fall Would your suggestedadjustments be difficult or easy to achieveWhen rates rise, the value of the longer-lived assets will fall by more the shorter-lived liabilities. If the maturity gap (or duration gap) is positive, the bank manager will want to shorten the maturity gap. If the repricing gap is negative, the manager will want to move it towards zero or positive. If rates are expected to decrease, the manager should reverse these strategies. Changing the maturity, duration, or funding gaps on the balance sheet often involves changing the mix of assets and liabilities. Attempts to make these changes may involve changes in financial strategy for the bank which may notbe easy to accomplish. Later in the text, methods of achieving the same results using derivatives will be explored.22. Consumer Bank has $20 million in cash and a $180 million loan portfolio.The assets are funded with demand deposits of $18 million, a $162 million CD and $20 million in equity. The loan portfolio has a maturity of 2years, earns interest at the annual rate of 7 percent, and is amortized monthly. The bank pays 7 percent annual interest on the CD, but theinterest will not be paid until the CD matures at the end of 2 years.a. What is the maturity gap for Consumer Bank= [0*$20 + 2*$180]/$200 = yearsMA= [0*$18 + 2*$162]/$180 = yearsMLMGAP = – = 0 years.b. Is Consumer Bank immunized or protected against changes in interestrates Why or why notIt is tempting to conclude that the bank is immunized because thematurity gap is zero. However, the cash flow stream for the loan and the cash flow stream for the CD are different because the loan amortizesmonthly and the CD pays annual interest on the CD. Thus any change in interest rates will affect the earning power of the loan more than the interest cost of the CD.c. Does Consumer Bank face interest rate risk That is, if marketinterest rates increase or decrease 1 percent, what happens to thevalue of the equityThe bank does face interest rate risk. If market rates increase 1percent, the value of the cash and demand deposits does not change.However, the value of the loan will decrease to $, and the value of the CD will fall to $. Thus the value of the equity will be ($ + $20 - $18 - $ = $. In this case the increase in interest rates causes the marketvalue of equity to increase because of the reinvestment opportunities on the loan payments.If market rates decrease 1 percent, the value of the loan increases to $, and the value of the CD increases to $. Thus the value of the equitydecreases to $.d. How can a decrease in interest rates create interest rate riskThe amortized loan payments would be reinvested at lower rates. Thuseven though interest rates have decreased, the different cash flowpatterns of the loan and the CD have caused interest rate risk.23. FI International holds seven-year Acme International bonds and two-yearBeta Corporation bonds. The Acme bonds are yielding 12 percent and the Beta bonds are yielding 14 percent under current market conditions.a. What is the weighted-average maturity of FI’s bond portfolio if 40percent is in Acme bonds and 60 percent is in Beta bondsAverage maturity = x 7 years + x 2 years = 4 yearsb. What proportion of Acme and Beta bonds should be held to have aweighted-average yield of percentLet X* + (1 - X)* = . Solving for X, we get 25 percent. In order to get an average yield of percent, we need to hold 25 percent of Acme and 75 percent of Beta.c. What will be the weighted-average maturity of the bond portfolio ifthe weighted-average yield is realizedThe average maturity of the portfolio will decrease to x 7 + x 2 = years.24. An insurance company has invested in the following fixed-incomesecurities: (a) $10,000,000 of 5-year Treasury notes paying 5 percentinterest and selling at par value, (b) $5,800,000 of 10-year bonds paying7 percent interest with a par value of $6,000,000, and (c) $6,200,000 of20-year subordinated debentures paying 9 percent interest with a parvalue of $6,000,000.a. What is the weighted-average maturity of this portfolio of assets= [5*$10 + 10*$ + 20*$]/$22 = 232/22 = yearsMAb. If interest rates change so that the yields on all of the securitiesdecrease 1 percent, how does the weighted-average maturity of theportfolio changeTo determine the weighted-average maturity of the portfolio for a rate decrease of 1 percent, the new value of each security must be determined. This calculation will require knowing the YTM of each security before the rate change.T-notes are selling at par, so the YTM = 5 percent. Therefore, the new value will bePV = $500,000*PVIFAn=5,i=4% + $10,000,000*PVIFn=5,i=4%= $10,445,182.10-year bonds: Par = $6,000,000, PV = $5,800,000, Cpn = 7 percent YTM= %. The new PV = $420,000*PVIFAn=10,i=% + $6,000,000*PVIFn=10,i=%= $6,222,290.Debentures: Par = $6,000,000, PV = $6,200,000, Cpn = 9 percentpercent. The new PV = $540,000*PVIFAn=20,i=% + $6,000,000*PVIFn=20,i==$6,820,418.The total value of the assets after the change in rates will be$23,487,890, and the weighted-average maturity will be [5*10,445,182 +10*6,222,290 + 20*6,820,418]/23,487,890 = 250,857,170/23,487,890 = years.c. Explain the changes in the maturity values if the yields increase by 1 percent.。

金融基础知识作业(含答案)1-4

金融基础知识 第1次平时作业一、名词解释1.金融:从广义上说,政府、个人、组织等市场主体通过募集、配置和使用资金而产生的所有资本流动都可称之为金融。

2.金融体系:金融体系是一个经济体中资金流动的基本框架,它是资金流动的工具〔金融资产〕、市场参与者〔中介机构〕和交易方式〔市场〕等各金融要素构成的综合体。

3.金融资产管理公司:是经国务院决定设立的收购国有独资商业银行不良贷款,管理和处置因收购国有独资商业银行不良贷款形成的资产的国有独资非银行金融机构。

4.金融制度:是各种金融制度构成要素的有机综合体,是有关金融交易、组织安排、监督管理与其创新的一系列在社会上通行的或被社会采纳的习惯.道德.法律.法规等构成的规则集合。

5.间接融资:是指拥有暂时闲置货币资金的单位通过存款的形式,或者购买银行、信托、保险等金融机构发行的有价证券,将其暂时闲置基金的资金先行提供给这些金融中介机构,然后再由这些金融机构以贷款.贴现等形式,或通过购买需要资金的单位发行的有价证券,把资金提供给这些单位使用,从而实现资金融通的过程。

6.直接融资:是没有金融机构作为中介的融通资金的方式。

需要融入资金的单位与融出资金单位双方通过直接协议后进行货币资金的转移。

7.信用货币:就是以信用作为保证,通过信用程序发行和创造的货币,包括流通中货币和银行存款。

8.货币制度:是国家法律规定的货币流通的规则、结构和组织机构体系的总称。

换言之,货币制度是国家对货币的有关要素、货币流通的组织与管理等加以规定所形成的制度。

9.格雷欣法则:就是“劣币驱逐良币〞的现象,即金银两种金属中市场价值高于官方确定比价的不断被人们收藏时,金银两者中的“贵〞金属最终会退出流通,使复本位制无法实现。

10.超主权货币:就是一种与主权国家脱钩、并能保持币值长期稳定的,用以解决金融危机暴露出的现行国际货币体系的一系列问题的国际储备货币。

二、单项选择题1.货币资金的融通,一般指货币流通与〔〕有关的一切活动。

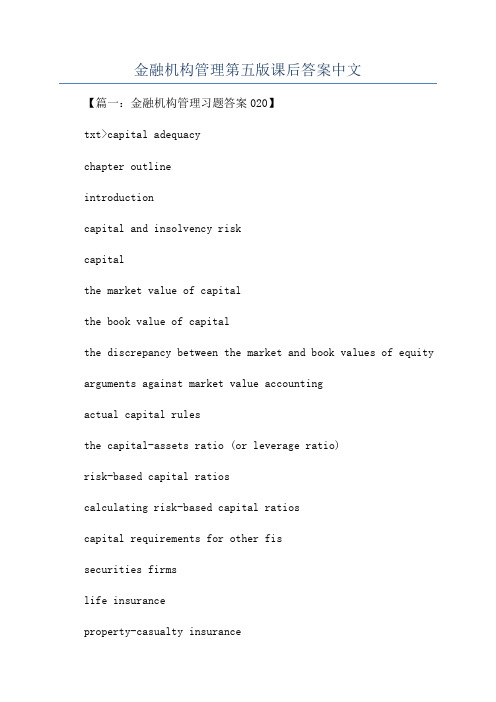

金融机构管理第五版课后答案中文

金融机构管理第五版课后答案中文【篇一:金融机构管理习题答案020】txt>capital adequacychapter outlineintroductioncapital and insolvency riskcapitalthe market value of capitalthe book value of capitalthe discrepancy between the market and book values of equity arguments against market value accountingactual capital rulesthe capital-assets ratio (or leverage ratio)risk-based capital ratioscalculating risk-based capital ratioscapital requirements for other fissecurities firmslife insuranceproperty-casualty insurancesummaryappendix 20a: internal ratings based approach to measuring credit risk-adjusted assetssolutions for end-of-chapter questions and problems: chapter twenty1. identify and briefly discuss the importance of the five functions of an fi’s capitalcapital serves as a primary cushion against operating losses and unexpected losses in the value of assets (such as thefailure of a loan). fis need to hold enough capital to provide confidence to uninsured creditors that they can withstand reasonable shocks to the value of their assets. in addition, the fdic, which guarantees deposits, is concerned that sufficient capital is held so that their funds are protected, because they are responsible for paying insured depositors in the event of a failure. this protection of the fdic funds includes the protection of the fi owners against increases in insurance premiums.finally, capital also serves as a source of financing to purchase and invest in assets.financial institutionregulators are concerned with the levels of capital held by an fi because of its special role in society. a failure of an fican have severe repercussions to the local or national economy unlike non-financial institutions. such externalities impose a burden on regulators to ensure that these failures do not impose major negative externalities on the economy. higher capital levels will reduce the probability of such failures.3. what are the differences between the economic definition of capital and the book valuedefinition of capitalthe book value definition of capital is the value of assets minus liabilities as found on the balance sheet.this amount often is referred to as accounting net worth.the economicdefinition of capital is the difference between the market value of assets and the market value of liabilities.a. how does economic value accounting recognize the adverse effects of credit andinterest rate riskthe loss in value caused by credit risk and interest rate risk is borne first by the equityholders, and then by the liability holders.in market value accounting, the adjustments to equity value are made simultaneously as the losses due to these risk elements occur.thus economic insolvency may be revealed before accounting value insolvency occurs.b. how does book value accounting recognize the adverse effects of credit and interestrate riskthey were placed on the books or incurred by the firm, losses are not recognized until the assets are sold orregulatory requirements force the firm to make balance sheet accounting adjustments.in the case of credit risk, these adjustments usually occur after all attempts tocollect or restructure the loans have occurred. in the case of interest rate risk, the change in interest rates will not affect the recognized accounting value of the assets or the liabilities.4. a financial intermediary has the following balance sheet (in millions) with all assets and liabilities in market values:6 percent semiannual 4-year5 percent 2-year subordinated debttreasury notes (par value $12) $10(par value $25)$207 percent annual 3-yearaa-rated bonds (par=$15) $159 percent annual 5-yearbbb rated bonds (par=$15)equity capitaltotal assetstotal liabilitiesequitya. under fasb statement no. 115, what would be the effect on equity capital (net worth)if interest rates increase by 30 basis points the t-notes are held for trading purposes, the rest are all classified as held to maturity.only assets that are classified for trading purposes or available-for-sale are to be reported atmarket values. those classified as held-to-maturity are reported at book values.thechange in value of the t-notes for a 30 basis points change in interest rates is:$10 = pvan=8,k= ($0.36) + pvn=8,k= ($12)k = 5.6465 x 2 = 11.293%if k =11.293% + 0.30% =11.593/2 = 5.7965%, the value of the notes will decline to:pvan=8,k=5.7965($0.36) + pvn=3,k=5.7965($12) = $9.8992. and the change in value is $9.8992 -。

江财金融机构管理系统地作业及问题详解

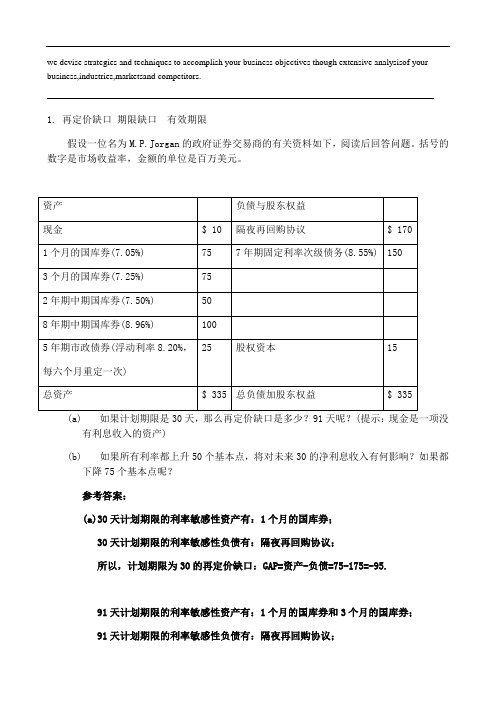

we devise strategies and techniques to accomplish your business objectives though extensive analysisof your business,industries,marketsand competitors.1. 再定价缺口期限缺口有效期限假设一位名为M.P.Jorgan的政府证券交易商的有关资料如下,阅读后回答问题。

括号的数字是市场收益率,金额的单位是百万美元。

(a)如果计划期限是30天,那么再定价缺口是多少?91天呢?(提示:现金是一项没有利息收入的资产)(b)如果所有利率都上升50个基本点,将对未来30的净利息收入有何影响?如果都下降75个基本点呢?参考答案:(a)30天计划期限的利率敏感性资产有:1个月的国库券;30天计划期限的利率敏感性负债有:隔夜再回购协议;所以,计划期限为30的再定价缺口:GAP=资产-负债=75-175=-95.91天计划期限的利率敏感性资产有:1个月的国库券和3个月的国库券;91天计划期限的利率敏感性负债有:隔夜再回购协议;所以,计划期限为91的再定价缺口:GAP=资产-负债=75+75-175=-20.(b)如果所有利率都上升50个基本点,那么未来30的净利息收入变化为:∆=∆=-=-,净利息收入减少0.475*95*0.00500.475NII GAP R如果所有利率都下降75个基本点,那么未来30的净利息收入变化为:*95*(0.0075)0.7125∆=∆=--=,净利息收入增加0.7125NII GAP R以下是County银行按市场价值记账的资产负债表(单位:百万美元,所有利率都是年利率)(a)County 银行的期限缺口是多少?(b)如果所有资产和负债的利率都上升1%,那么期限缺口又是多少? 参考答案:1ni ij ij j M W M ==∑,1ijij nijj P W P==∑,i =资产组合、负债组合(a )资产组合的平均期限112233A A A A A A A M W M W M W M =++, 其中1230,15,30A A A M M M ===,12320160300,,480480480A A A W W W ===。

金融风险管理作业3完整答案.

金融风险管理作业3一、单项选择题1. 为了解决一笔贷款从贷前调查到贷后检查完全由一个信贷员负责而导致的决策失误或以权谋私问题,我国银行都开始实行了(D 制度,以降低信贷风险。

A. 五级分类B. 理事会C. 公司治理D. 审贷分离2. 保险公司的财务风险集中体现在(C。

A. 现金流动性不足B. 会计核算失误C. 资产和负债的不匹配D. 资产价格下跌3. 引起证券承销失败的原因包括操作风险(D 和信用风险。

A. 法律风险B. 流动性风险C. 系统风险D. 市场风险4. (B基金具有法人资格A. 契约型B. 公司型C. 封闭式D. 开放式5. 融资租赁一般包括租赁和(D 两个合同。

A. 出租B. 谈判C. 转租D. 购货二、多项选择题1. 商业银行面临的外部风险主要包括(ABD 。

A. 信用风险B. 市场风险C. 财务风险D. 法律风险2. 广义的保险公司风险管理涵盖的环节除了产品设计、展业,还包括等环节外(ACD 等环节。

A. 理赔B. 保险投资C. 核保D. 核赔3. 证券承销的类型包括(ACD 。

A. 全额包销B. 定额代销C. 余额包销D. 代销4. 基金的销售包括以下哪几种方式(ABCD 。

A. 计划销售法B. 直接销售法C. 承销法D. 通过商业银行或保险公司促销法5. 农村信用社的资金大部分来自农民的(AC 是最便捷的服务产品A. 小额农贷B. 证券投资C. 储蓄存款D. 养老保险、判断题(判断正误,并对错误的说明理由1. 商业银行的风险主要是信贷资产风险所以应加强对信贷资产质量的管理,可以忽视存款等负债业务的风险管理。

( ×错误理由:2. 为加强保险公司财务风险管理,在利率水平不稳定时保险公司可采用债券贡献策略。

( ×错误理由:3. 证券公司的经济业务将社会的金融剩余从盈余部门转移到短缺部门。

( ×错误理由:4. 契约型基金是依照信托法建立的而公司型基金是依据公司法设立的。

风险管理与金融机构(原书第二版)第一~五章作业题答案

风险管理与金融机构(原书第二版)第一~五章作业题答案 课本后面有练习题的答案,故在此不赘述,只罗列作业题答案,此答案根据网络资源和个人见解得出,若有错漏,请见谅~~1.16 解:由资本市场线可得:p m fm f p r r r r δδ-+= ,()()f m mf p p r r r r -⨯-=δδ,如题中所述%15%,7,12.0===m f m r r δ,则当%10=p r ,标准差%9=p δ;当%20=p r ,标准差%39=p δ1.17(1)设在99%置信度下股权资本为正的当前资本金持有率为A ,银行在下一年的盈利占资产的比例为X ,由于盈利服从正态分布,因此银行在99%的置信度下股权资本为正的当前资本金持有率的概率为)(A X P ->,由此可得%99)%2%8.0()%2%8.0(1)(1)(=+=---=-<-=->A N A N A X P A X P 查表得33.2%2%8.0=+A ,解得A=3.86%,即在99%置信度下股权资本为正的当前资本金持有率为3.86%。

(2)设在99.9%置信度下股权资本为正的当前资本金持有率为B ,银行在下一年的盈利占资产的比例为Y ,由于盈利服从正态分布,因此银行在99.9%的置信度下股权资本为正的当前资本金持有率的概率为)(B Y P ->,由此可得%9.99)%2%8.0()%2%8.0(1)(1)(=+=---=-<-=->B N B N B Y P B Y P 查表得10.3%2%8.0=+B ,解得B=5.4%,即在99.9%置信度下股权资本为正的当前资本金持有率为5.4%。

1.18 该经理产生的阿尔法为08.0)05.03.0(2.005.01.0-=--⨯---=α,即-8%,因此该经理的观点不正确,自身表现不好。

2.15收入服从正太分布,假定符合要求的最低资本金要求为X ,则有)99.0(Φ=-σμx ,既有01.326.0=-X ,解得X=6.62,因此在5%的资本充足率水平下,还要再增加1.62万美元的股权资本,才能保证在99.9%的把握下,银行的资本金不会被完全消除。

南开大学20秋《金融机构和金融市场》在线作业-2(参考答案)

1.通过投资者之间的公开竞价来产生发行价格的交易机制属于()。

A.固定价格机制B.浮动价格机制C.拍卖机制D.累计投标询价机制答案:C2.在现代经济中,银行信用仍然是最重要的融资形式。

以下对银行信用描述不正确的是()。

A.银行信用是在商业信用的基础上产生B.银行信用不可以由商业信用转化而来C.银行信用是以货币形式提供的信用D.银行在银行信用活动中充当信用中介的角色答案:B3.下列哪一项不能体现中央银行是“银行的银行”()。

A.发行货币B.最后贷款人C.组织全国范围内的资金清算D.集中存款准备金答案:A4.股东大会作出修改公司章程、增加或减少注册资本的决议,以及公司合并、分立、解散或者变更公司形式的决议,必须经出席会议的股东所持表决权的()以上通过。

A.2/3B.1/2C.3/4D.1/3答案:A5.下列哪个时期的创新是以逃避管制为主要特征的()。

A.20世纪60年代B.20世纪70年代C.20世纪80年代D.20世纪90年代答案:A6.货币市场有许多子市场,下列()不属于货币市场。

A.票据与贴现市场B.长期债券市场C.银行同业拆借市场D.回购市场答案:B7.金融互换交易的主要用途是改变交易者()的风险结构,从而规避相应的风险。

A.投资B.筹资C.生产经营D.资产或负债答案:D8.提出“利息剩余价值学说”的经济学家是()。

A.亚当·斯密B.庞巴维克C.马克思D.凯恩斯答案:A9.方先生将一笔10万元的资金投资在一个年收益率6%的工程项目中,试估算,大约经过()年这笔资金的本利和可以达到20万元。

A.10年B.11年C.12年D.13年答案:B10.下列哪种保险产品不属于人寿保险()。

A.定期寿险B.年金保险C.投资连结保险D.农业保险答案:D11.下列关于同业拆借的说法,错误的是()。

A.同业拆借是银行及其他金融机构之间进行短期的资金借贷B.借入资金称为拆入,贷出资金称为拆出C.同业拆借业务主要通过全国银行间债券市场进行D.同业拆借的利率随资金供求的变化而变化,常作为货币市场的基准利率答案:C12.上市公司申请发行新股,要求最近3年以现金或股票方式累计分配的利润不少于最近3年实现的平均()。

金融学金融机构习题与答案

金融学金融机构习题与答案一、选择题1、以下不属于金融机构的是()A 商业银行B 证券公司C 财务公司D 工商企业答案:D解析:工商企业主要从事生产经营活动,不是专门从事金融业务的机构。

商业银行、证券公司和财务公司都是以金融业务为核心的机构。

2、金融机构的核心功能是()A 风险管理B 资金融通C 信息提供D 支付结算答案:B解析:资金融通是金融机构最基本、最核心的功能,通过将资金从盈余方转移到短缺方,实现资源的优化配置。

3、以下属于存款类金融机构的是()A 投资银行B 保险公司C 储蓄银行D 信托公司答案:C解析:储蓄银行主要通过吸收公众存款来获取资金,属于存款类金融机构。

投资银行主要从事证券承销等业务,保险公司主要经营保险业务,信托公司主要从事信托业务,它们都不是以吸收存款为主要资金来源。

4、金融机构在金融市场上充当()A 资金需求者B 资金供给者C 中介机构D 以上都是答案:D解析:金融机构在金融市场上既可以是资金需求者,通过发行金融工具筹集资金;也可以是资金供给者,将资金投资于各种金融资产;同时还充当着资金融通的中介机构,促进资金的流动和配置。

5、以下关于中央银行的表述,错误的是()A 是发行的银行B 是银行的银行C 以盈利为目的D 是政府的银行答案:C解析:中央银行不以盈利为目的,而是代表国家制定和执行货币政策,维护金融稳定,为政府提供金融服务。

二、判断题1、金融机构的经营风险比一般企业小。

()答案:错误解析:金融机构经营的是货币资金,面临着信用风险、市场风险、操作风险等多种风险,其经营风险并不比一般企业小。

2、所有金融机构都受到严格的金融监管。

()答案:正确解析:金融机构的业务活动对经济和金融体系的稳定具有重要影响,因此大多数金融机构都受到严格的监管,以防范金融风险和保护投资者利益。

3、商业银行是唯一能够创造存款货币的金融机构。

()答案:错误解析:在现代金融体系中,除了商业银行,中央银行通过货币发行也能创造货币,一些具有类似银行功能的非银行金融机构在一定条件下也可能创造货币。

金融机构管理第八章答案中文版

第8章利率风险I 课后习题答案(1-10)自己边做题边翻译的,仅供参考….1.利率波动程度比1979-1982年采用非借入准备金制度时显著降低。

2. 金融市场一体化加速了利率的变化,以及各个国家利率波动之间的传递;与过去相比,利率水平更难控制,不确定性也更大;另外,由于金融机构越来越全球化,任何利率水平的波动都会更迅速地引起公司额外的利率风险问题。

3. 再定价缺口指在一定时期内,需要再定价的资产价值和负债价值之间的差额,再定价即意味着面临一个新的利率。

利率敏感性意味着金融机构的管理者在改变每项资产或负债所公布的利率之前需等待的时间。

再定价模型关注净利息收入变量的潜在变化。

事实上,当利率变化时,资产和负债将被重新定价,利息收入和利息支出都将发生改变,这就是所谓的“面临一个新的利率”。

4. 期限等级是指衡量资产和负债的时间期,投资组合中的证券是否有利率敏感性取决于其再定价期限时间的长短。

再定价期限越长,到期或需要重新定价的证券就越多,利率风险就越大。

5. a.(1)再定价缺口= RSA - RSL = $200 - $100 million = +$100 million.净利息收入= ($100 million)(.01) = +$1.0 million, 或$1,000,000.(2)再定价缺口= RSA - RSL = $100 - $150 million = -$50 million.净利息收入= (-$50 million)(.01) = -$0.5 million, 或-$500,000.(3)再定价缺口= RSA - RSL = $150 - $140 million = +$10 million.净利息收入= ($10 million)(.01) = +$0.1 million, 或$100,000.b. (1)和(3)的情况下的金融机构在利率下降时面临风险(正的再定价缺口),(2)情况下的金融机构在利率上升时面临风险(负的再定价缺口)。

金融机构风险管理A03 作业7、8、9章答案

金融机构风险管理A03 作业7、8、9章答案第七章风险种类1.金融机构进行资产转换的过程是怎样的,为什么这个过程往往会导致利率险,什么是利率风险,金融机构进行资产转换的过程由购买初级资产和发行作为资金来源的二级资产构成。

金融机构购买的主要证券具有期限长和流动性的特点,这些特点也是金融机构发行的二级资产所不具备的。

例如,银行通过短期存款筹集资金来购买中长期债券以及发放中长期贷款。

利率风险的出现是因为市场利率的变化使长期资产的价格和再投资收入与短期负债的价格和利息支出不匹配。

利率风险是由金融资产期限水平变化影响中期现金流的利率而产生的风险。

2.什么是再融资风险,为什么再融资风险是利率风险的一部分,如果一家金融机构用短期负债为长期资产融资,那么利率上升对收益有什么影响,利率下降呢, 再融资风险是指相对负债持有期限较短的资产时,金融机构面临借入较长期资金在投资的利率不确定性。

当金融机构持有较负债期限长的资产,它就面临着再融资风险。

例如,假定一家银行通过借入2年期资金而放出10年期贷款,两年后这家银行就可能面临着需要以更高的利率借入新的存款或者再融资。

因此,利率上升将使得银行的净利息收入减少。

相反,如果利率下跌的话,这家银行将因为借款利息的降低、贷款利息不变而获得利润。

因此,净利息收入将增加。

2。

再融资的风险是什么,如何再融资的风险的利率风险的一部分吗,如果济基金长期固定利率与短期负债,这将是一个关于加息的影响,资产收益, 其中的下降率再融资的风险是一个正被用来资助一个长期固定利率资产资金的新来源的成本的不确定性。

这种风险发生时,与FI是持有期限超过其资产负债的期限更大例如,如果一家银行有一个为期十年的固定利率贷款2年定期存款投资,银行面临的借款在两年内新增存款率较高,或再融资的风险。

因此,利率上升将减少净利息收入。

3.是再投资风险,为什么再投资风险是利率风险的一部分,如果一家金融机构用长期负债为短期资产融资,那么利率上升对收益有什么影响,利率下降呢, 再投资风险是到期资产调动带来的收益率的不确定性。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

《金融机构管理》作业

一选择题

1.在我国的金融机构中,下列哪一项是政策性银行?()

A.交通银行

B.中国银行

C.中国农业发展银行

D.中国农业银行

2.商业银行最主要的资金来源是()

A.存款B.同业拆借C.回购协议D.向中央银行借款3.商业银行的资产业务包括()

A.存款业务B.放款业务C.结算业务D.信托业务

4.股份制银行的最高权利机构是()

A.董事会B.监事会C.股东大会

5.下列管理理论中,()是最注重赢利性的。

A.预期收入理论B.商业贷款理论C.负债管理理论D.资产转换理论6.流动性最强的资产是()

A.固定资产B.无形资产C.现金资产D.递延资产

7.我国实行的金融体系是()

A.复合银行体系

B.单一银行体系

C.没有中央银行的金融体系

8.下列特征中不属于金融机构业务的基本特征的是()

A.无形性

B.非歧视性

C.差异性

D.专业性

9.下列业务中属于银行的资产业务的是()

A.定期存款

B.期货交易

C.购买国库券

D.发行长期债券

10.下列构成银行核心资本的是()

A.普通准备金

B.公开储备

C.未公开储备

D.次级长期债券

11.投资银行财务管理的目标是使()

A.公司利润最大化

B.股东财富最大化

C.每股收益最大化

12.投资基金最早产生于哪个国家?()

A.英国

B.美国

C.法国

D.德国

13.下列各项中,构成投资银行的次级资本的是()

A.留存收益

B.意外损失准备金

C.普通股

D.附属债券

14.下列属于非系统风险的是()

A.市场风险

B.政治风险

C.利率风险

D.购买力风险

15.依据我国于1997年颁布的《证券投资基金管理暂行办法》规定,设立基金管理公司的最低实收资本为:()

A.1000万元 B800万元 C300万元 D100万元

16.保险公司筹集的资本金中,单个的个儿资本金不得超过()

A.10%

B.5%

C.30%

D.20%

17.我国第一家专业的租赁公司成立于()

A.1979.7

B.1979.10

C.1981.4

D.1982.4

18.现代银行业存款保险制度的开创者是()

A.美国

B.英国

C.法国

D.德国

19.我国第一家信托公司——通商信托公司于()在上海成立。

A.1927.10

B.1921.10

C.1927.3

D.1921.8

20.投资银行实行登记注册制的典型国家是()

A.英国

B.日本

C.美国

D.德国

21.在商业银行刚刚组建时,银行募集资本金的主要方式是:()

A.普通股

B.优先股

C.资本票据

D.可转换债券

22.下列功能不属于银行资本功能的是()

A.营业功能

B.安全功能

C.保护功能

D.管理功能

23.下列各项中,属于商业银行中间业务的是()

A.投资

B.同业拆借

C.咨询业务

D.外汇业务

24.金融机构体系中,历史最悠久,数量最大,同时也是对社会经济生活影响最大的是()

A.保险公司

B.投资基金

C.商业银行

D.中央银行

二名词解释

1.风险管理

2.同业拆借

3.附属资本

4.银行控股公司制

5.体系风险

6.投资风险

7.金融期货

8.开发式基金

9.金融租赁

10.保险公司的收益

11.信托存款

12.回租租赁

三简答题

1.简述风险的定义.特征和效应。

2.简述资产负债综合管理理论的主要内容。

3.简答投资银行的主要业务及经济功能。

4.简答基金证券与股票.债券的主要区别。

5.简述商业银行通过发行长期债券平整补充资本的优点。

6.简述投资银行财务管理的原则和目标

7.简述投资基金的特点

8.简述投资基金收益的主要来源

9.确立商业银行的组织形式的原则是什么?

10.简述监管当局对投资银行的风险管理与控制的内容

11.简述公司型基金与契约式基金的不同之处

12.简述投资基金的利润分配方式

13.简述投资银行的风险管理原则

14.商业银行利用回购协议融资的优点有哪些?

15.金融租赁的特征是什么?

16.简述政策性金融机构与商业性金融机构的关系

四辨析题

1.凡在中华人民共和国境内经营存款.外汇.居民储蓄.信托投资等业务的一切金融机构由中国人民银行管理。

2.银行控股公司制和连锁银行制没什么不同。

3.贸易融资是商业银行的中间业务。

4.欧洲美元仅指在欧洲市场上流通的美元。

5.商业银行最主要的资金来源是存款

6.在商业银行新组建时,优先证券是银行筹集资本金的主要方式。

7.美国是世界上公认的中央银行具有最有效率的监督管理的国家之一。

8.在西方国家,直接信托投资是信托机构投资的重点。

9.财务管理的职能是信托的基本职能。

10.金融体系的主体是中央银行。

11.在西方国家,只有美国的商业银行曾经采用过单一银行的组织形式。

12.流通市场是投资银行最主要也是最重要的功能领域。

五论述题

1.论述我国城镇社会保障制度存在的问题。

2.论述我国信托机构存在的问题。

3.结合实际,论述我国金融租赁发展的障碍。

4.试论述如何营造良好的环境促进我国金融租赁业的发展。