chapter21

chapter21看内容

第二章 物理层和数据链路层从整个网络体系结构看,网络技术的发展在两个方向最多最复杂,一是体现在应用层的各种新的应用技术层出不穷,另外是在网络的低三层(通信子网的发展,为提高网络速度,承载各种应用),而中间层主要还是以TCP/UDP 为主,或对它提出的一些补充修改。

以下是近年来出现的一些新的网络技术的层次结构,图中没有传统的LAN 和x.25。

下面我们主要以IP 、ATM 和x.25为主介绍低3层结构与功能。

OSI Frame RelayMANSMDSEthernetATMSONETOSIMOBIL/Wireless(air)MOBIL/Wireless(network)用户宽带宽带信令(UNI)宽带信令(NNI)IntelligentNetwork(IN)2.1 物理层物理层完成相邻设备间的比特流传送。

主要任务是确定与传输媒体的接口的一些特性:机械特性 电气特性 功能特性 和规程特性。

它要定义传输介质、传输方式和传输规程。

传输介质:磁介质、双绞线、同轴电缆、光纤、无线传输(无线电波、微波、卫星、红外线、光波等);传输方式:模拟方式和数字方式;ATM 的物理媒体子层:ATM 的物理传输媒体可以是光纤,当在100米以内运转时5类双绞线也是可以的。

标准中没有定义具体的物理层,可以用其他的物理层标准传输,如SONET 。

ATM 传输的基本速率为155M ,可以到622M ,2488M 等。

接口 光 光 电 电布线形式 上下行各一条 上下行各一条 上下行各一条 上下行各一条传输媒体 单模光纤 多模光纤 微波同轴 CATV 同轴接口距离 2km 2km 100m 200m传输速率 155Mb/s 或多或622Mb/s 155Mb/s 或多或622Mb/s 155Mb/s 或多或622Mb/s 155Mb/s 或多或622Mb/s信道编码 NRZ NRZ CMI CMI非归零码(NRZ, Non Return to Zero ):1为高电平,0为低电平。

中级微观经济-Chapter21_Cost_Curves

固定,可变和总成本函数

c(y) 表示产出为y时所有固定和可变要素 投入总成本。 c(y) 为厂商的总成本函数 。

c(y) F cv (y).

$

F y

$ cv(y)

y

$ cv(y)

F y

$

c(y) F cv (y)

F

c(y) cv(y)

F y

平均固定,平均可变和平均总成本曲 线

MCs(y;x2)

ACs(y;x2) ACs(y;x2)

MCs(y;x2)

y

$/产出

MCs(y;x2) ACs(y;x2)

MCs(y;x2)

ACs(y;x2) ACs(y;x2)

AC(y) MCs(y;x2)

y

$/产出

MCs(y;x2) ACs(y;x2)

y

$/产出

MC(y) AVC(y) AVC(y) 0 y

MC(y)

AVC(y)

y

$/产出

MC(y) AVC(y) AVC(y) 0 y

MC(y)

AVC(y)

y

$/产出

MC(y) AVC(y) AVC(y) 0 y

短期MC 曲线与短期AVC曲线相交

厂商的中成本函数为:

c(y) F cv (y).

当 y > 0时, 厂商的平均总成本函数为:

AC(y) F cv (y) yy

AFC(y) AVC(y).

平均固定,平均可变和平均总成本曲 线

平均固定成本曲线是什么样子?

AFC(y) F y

AFC(y) 为双曲线,因此它的图像为:

边际成本函数

厂商的总成本函数为;

c(y) F cv (y)

Chapter_21 怀尔德《会计学原理》19版答案

Chapter 21Exercise 21-1 (25 minutes)1. Allocation of Indirect Expenses to Four Operating DepartmentsPersonnel ..............................22 11 8,800 Manufacturing ......................104 52 41,600 Packaging ............................. 34 17 13,600 Totals ....................................200 100% $80,000Personnel ..............................5,000 5 3,050 Manufacturing ......................45,000 45 27,450 Packaging ............................. 23,000 23 14,030 Totals ....................................100,000 100% $61,000Personnel ..............................1,200 1 167 Manufacturing ......................42,000 35 5,845 Packaging ............................. 16,800 14 2,338 Totals ....................................$120,000 100% $16,700 2. Report of Indirect Expenses Assigned to Four Operating DepartmentsMaterials ...................$16,000 $16,470 $ 8,350 $ 40,820 Personnel ..................8,800 3,050 167 $ 12,017Manufacturing ..........41,600 27,450 5,845 $ 74,895 Packaging ................. 13,600 14,030 2,338 $ 29,968 Totals ........................$80,000 $61,000 $16,700 $157,700Exercise 21-2 (30 minutes)........................Depreciation ......................56,600 2,000 MH $28.30 per machine hour Line preparation ...............46,000250 setups $184.00 per setup1. Assignment of overhead costs to the two products using ABCMachinery depreciation ......... 500 hours $ 28.30 14,150 Line preparation ..................... 40 setups $184.00 7,360 Total overhead assigned ....... $23,340Machinery depreciation ......... 1,500 hours $ 28.3042,450 Line preparation ..................... 210 setups $184.00 38,640 Total overhead assigned ....... $84,660Direct labor .................................. 12,200 23,800 Overhead (using ABC) ................ 23,340 84,660 Total cost ..................................... $54,540 $151,660 Quantity produced ...................... 10,500 ft. 14,100 ft. Average cost per foot (ABC) ....... $5.19 $10.763. The average cost of rounded edge shelves declines and the average cost of squared edge shelves increases. Under the current allocation method, the rounded edge shelving was allocated 34% of all of the overhead cost ($12,200 direct labor/$36,000 total direct labor). However, it does not use 34% of all of the overhead resources. Specifically, it uses only 25% of machine hours (500 MH/2,000 MH), and 16% of the setups (40/250). Activity based costing allocated the individual overhead components in proportion to the resources used.Exercise 21-7 (15 minutes)(1) Items included in performance reportThe following items definitely should be included in the performance report for the auto service department manager because they are controlled or strongly influ enced by the manager’s decisions and activities:•Sales of parts•Sales of services•Cost of parts sold•Supplies•Wages (hourly)(2) Items excluded from performance reportThe following items definitely should be excluded from the performance report because the department manager cannot control or strongly influence them:•Building depreciation•Income taxes allocated to the department•Interest on long-term debt•Manager’s salary(3) Items that may or may not be included in performance reportThe following items cannot be definitely included or definitely excluded from the performance report because they may or may not be completely under the manager’s control or strong influence:•Payroll taxes Some portion of this expense relates to themanager’s salary and i s not controllable by themanager. The portion that relates to hourly wagesshould be treated as a controllable expense.•Utilities Whether this expense is controllable depends on thedesign of the auto dealership. If the auto servicedepartment is in a separate building or has separateutility meters, these expenses are subject to themanager’s control. Otherwise, the expense probablyis not controllable by the manager of the auto servicedepartment.Exercise 21-9 (20 minutes)(1)Electronics ...................$750,000 $3,750,000 20% Sporting Goods ...........800,000 5,000,000 16% Comment: Its Electronics division is the superior investment center on the basis of the investment center return on assets.Exercise 21-9 (continued)(2)Net income ...................$750,000 $800,000 Target net income$3,750,000 x 12% ...... 5,000,000 x 12% .......(450,000)(600,000)Residual income……. $300,000 $200,000Comment: Its Electronics division is the superior investment center on the basis of investment center residual income.(3) The Electronics division should accept the new opportunity, since it will generate residual income of 3% (15% - 12%) of the i nvestment’s invested assets.Exercise 21-10 (15 minutes)Electronics ...................$750,000 $10,000,000 7.50% Sporting Goods ...........800,000 8,000,000 10.0%Electronics ...................$10,000,000 $3,750,000 2.67 Sporting Goods ...........8,000,000 5,000,000 1.6 Comments: Its Sporting goods division generates the most net income per dollar of sales, as shown by its higher profit margin. The Electronics division however is more efficient at generating sales from invested assets, based on its higher investment turnover.Problem 21-1A (60 minutes)Part 1Average occupancy cost = $111,800 / 10,000 sq. ft. = $11.18 per sq. ft. Occupancy costs are assigned to the two departments as followsLanya’s Dept................. 1,000 $11.18 $11,180 Jimez’s Dept................. 1,700 $11.18 $19,006**A total of $30,186 ($11,180 + $19,006) in occupancy costs is charged to these departments. The company would follow a similar approach in allocating the remaining occupancy costs ($81,614, computed as $111,800 - $30,186) to its other departments (not shown in this problem).Part 2Market rates are used to allocate occupancy costs for depreciation, interest, and taxes. Heating, lighting, and maintenance costs are allocated to the departments on both floors at the average rate per square foot. These costs are separately assigned to each class as follows:Depreciation—Building .................$ 31,500 $31,500 Interest—Building mortgage .........47,000 47,000Taxes—Building and land .............14,000 14,000Gas (heating) expense ...................4,425 $ 4,425 Lighting expense ...........................5,250 5,250 Maintenance expense .................... 9,625 ______ 9,625 Total ................................................$111,800 $92,500 $19,300Value-based costs are allocated to departments in two stepsSecond floor ...................5,000 10 50,000Total market value .........$250,000Second floor ................... 50,000 20 18,500 3.70Totals ..............................$250,000 100% $92,500Usage-based costs allocation rate = $19,300 / 10,000 sq. ft.= $1.93 per sq. ft.We can then compute total allocation rates for the floors$16.73 Second floor ........................... 3.70 1.93 $ 5.63 These rates are applied to allocate occupancy costs to departmentsLanya’s Department......................... 1,000 $16.73 $16,730 Jimez’s Department......................... 1,700 5.63 $ 9,571Part 3A second-floor manager would prefer allocation based on market value. This is a reasonable and logical approach to allocation of occupancy costs. The current method assumes all square footage has equal value. This is not logical for this type of occupancy. It also means the second-floor space would be allocated a larger portion of costs under the current method, but less using an allocation based on market value.Part 1Professional salaries ..................$1,600,000 10,000 hours $160 per hour Patient services & supplies .......$ 27,000 600 patients $45 per patient Building cost ...............................$ 150,000 1,500 sq. ft. $100 per sq. ft. Total costs ...................................$1,777,000Part 2Allocation of cost to the surgical departments using ABCProfessional salaries ............. 2,500 hours $160 per hr. $400,000 Patient services & supplies ...... 400 patients $45 per patient 18,000 Building cost .......................... 600 sq. ft. $100 per sq. ft. 60,000 Total ...............................................................................................$478,000 Average cost per patient ...............................................................$ 1,195Professional salaries ............. 7,500 hours $160 per hr. $1,200,000 Patient services & supplies ...... 200 patients $45 per patient 9,000 Building cost .......................... 900 sq. ft. $100 per sq. ft 90,000 Total ................................................................................................$1,299,000 Average cost per patient ...............................................................$ 6,495[Note that the sum of the amounts allocated to General Surgery and Orthopedic Surgery ($478,000 + $1,299,000) equals the total amount of indirect costs ($1,777,000).] Part 3If all center costs were allocated on the number of patients, the average cost of general surgery would increase. Since general surgery sees 2/3 of all patients (400/600), it would get allocated 2/3 of all center costs. Orthopedic surgery is currently consuming more professional salaries and building space than general surgery, but has fewer patients.Problem 21-3A (70 minutes)Cost of goods sold ........................ 89,964 63,612 27,500 181,076 (2) Gross profit .................................... 93,636 38,988 22,500 155,124 Direct expensesSales salaries ............................... 21,000 7,100 8,500 36,600Advertising ................................... 2,100 700 1,100 3,900Store supplies used .................... 594 378 400 1,372 (3) Depreciation of equipment ......... 2,300 900 1,000 4,200Total direct expenses .................. 25,994 9,078 11,000 46,072 Allocated expensesRent expense ............................... 5,632 2,835 2,353 10,820 (4) Utilities expense .......................... 2,292 1,153 955 4,400 (4) Share of office dept. expenses ... 15,288 8,540 4,172 28,000 (5) Total allocated expenses ............ 23,212 12,528 7,480 43,220 Total expenses ............................... 49,206 21,606 18,480 89,292Net income ..................................... $ 44,430 $17,382 $ 4,020 $ 65,832 Supporting Computations—coded (1) through (5) in statement aboveGrowth rate (8% increase) ............... x 108% x 108%2010 sales ......................................... $183,600 $102,600 $ 50,000Growth rate (8% increase) ............... x 108% x 108% x 55%* 2010 cost of goods sold .................. $ 89,964 $ 63,612 $ 27,500 A LTERNATIVELY2009 cost of goods sold .................. $ 83,300 $ 58,9002009 sales ......................................... $170,000 $ 95,0002009 cost as % of sales ................... 49% 62%2010 sales ........................................ $183,600 $102,600 $ 50,000 2010 cost as % of sales .................. x 49% x 62% x 55%* 2010 cost of goods sold .................. $ 89,964 $ 63,612 $ 27,500 * T he 55% cost of goods sold percent is computed as 100% minus the predicted 45% gross profit margin.Growth rate (8% increase) ................x 108% x 108%2010 store supplies ..........................$ 594 $ 378 $ 400One-fifth from clock to paintings (1,408) $ 1,408 One-fourth from mirror topaintings ______ (945) 945 2010 allocation of $10,820 rent .........$ 5,632 $ 2,835 $ 2,353 Percent of total * ...............................2010 allocation of $4,400total utilities ....................................$ 2,292 $ 1,153 $ 955Percent of total sales * ......................54.6% 30.5% 14.9% 2010 allocation of $28,000total office departmentexpenses ($20,000 in 2009plus $8,000 increase) ......................$ 15,288 $ 8,540 $ 4,172 * Instructor note: If students round to something other than one-tenth of a percent, theirnumbers will slightly vary.Part 1a.Responsibility Accounting Performance ReportManager, Camper DepartmentFor the YearBudgeted Actual Over (Under)Amount Amount Budget Controllable CostsRaw materials .................................$195,900 $194,800 $ (1,100) Employee wages ............................104,200 107,200 3,000 Supplies used .................................34,000 32,900 (1,100) Depreciation—Equipment ............. 63,000 63,000 0 Totals ..............................................$397,100 $397,900 $ 800b.Responsibility Accounting Performance ReportManager, Trailer DepartmentFor the YearBudgeted Actual Over (Under)Amount Amount Budget Controllable CostsRaw materials .................................$276,200 $273,600 $ (2,600) Employee wages ............................205,200 208,000 2,800 Supplies used .................................92,200 91,300 (900) Depreciation—Equipment ............. 127,000 127,000 0 Totals ..............................................$700,600 $699,900 $ (700)c.Responsibility Accounting Performance ReportManager, Ohio PlantFor the YearBudgeted Actual Over (Under)Amount Amount Budget Controllable CostsDept. manager salaries ................. $ 97,000 $ 98,700 $ 1,700 Utilities ........................................... 8,800 9,200 400 Building rent .................................. 15,700 15,500 (200) Other office salaries ..................... 46,500 30,100 (16,400) Other office costs ......................... 22,000 21,000 (1,000) Camper department ...................... 397,100 397,900 800 Trailer department ........................ 700,600 699,900 (700) Total ............................................... $1,287,700 $1,272,300 $(15,400)Part 2The plant manager did a good job of controlling costs and meeting the budget. He came in under budget for the plant even though he paid the department managers more than budgeted and had to absorb the amounts over budget in their departments. This is because he spent less than the budget amount on building rent, other office salaries, and other office costs. The Trailer Department manager also came in under budget. The Camper Department manager came in over budget, and thus performed the worse of the three managers.Problem 21-1B (60 minutes)Part 1Average occupancy cost = $372,000 / 20,000 sq. ft. = $18.60 per sq. ft.Occu pancy costs are assigned to Miller’s department as followsMiller’s Dept.................. 2,000 $18.60 $37,200Part 2Market rates are used to allocate occupancy costs for the building rent. Lighting and cleaning costs are allocated to the departments on all three floors at the average rate per square foot. Costs assigned to each class are:Lighting expense ................... 20,000 $20,000 Cleaning expense .................. 32,000 _______ 32,000 Totals ...................................... $372,000 $320,000 $52,000Value-based costs are allocated in two steps(i) Compute market value of each floorSecond floor ...................7,500 24 180,000Basement floor ...............5,000 12 60,000Total market value .........$600,000Problem 21-1B (Continued)(ii) Allocate the $320,000 to each floor based on its percent of market valueSecond floor ...................180,000 30 96,000 12.80 Basement floor ............... 60,000 10 32,000 6.40$600,000 100% $320,000Usage-based costs allocation rate = $52,000 / 20,000 sq. ft.= $2.60 per sq. ft.Total allocation rates for the departments on all three floors areSecond floor .................12.80 2.60 15.40Basement floor ............. 6.40 2.60 9.00These rates are applied to alloc ate occupancy costs to Miller’s departmentMiller’s Department ................................2,000 $9.00 $18,000Part 3A basement manager would prefer the allocation based on market value. This is a reasonable and logical approach to allocation of occupancy costs. With a flat rate method, all square footage has equal value. This is not logical for this type of occupancy. Less cost would be allocated to the basement departments if the market value method were used.。

哈利波特与凤凰社21章英文原文

哈利波特与凤凰社21章英文原文英文标题:Harry Potter and the Order of the Phoenix - Chapter 21 English Original TextChapter 21 - The Unknowable RoomIt was hard to concentrate on anything that weekend, even though Harry had promised himself that he would finish his History of Magic essay and the presentation for Defense Against the Dark Arts. Fred, George, and Ginny were all sitting around him at the Gryffindor table at mealtimes, planning. Harry contented himself with making vague noises, and as soon as was polite, he escaped to the Room of Requirement.He had soon become as well acquainted with the Room's many tricks as the other denizens of the Hog's Head. He had been chased by the Hufflepuff cup and the fake locket and been burned by the cursed handle. The room had even sprouted a beech tree in one of its corners the previous night. There had been no sign of Draco Malfoy, or any of the Carrows, but it would have been nice if the two people he most wanted to avoid had not known exactly where and when he was planning to come.However, as he paced up and down the Charms corridor for the fifth time, the map still firmly in his hand, he came across something he had not spotted before. The map showed him, labeled as he had hoped, his current position labeled as "The Unknowable Room."He went into the room directly opposite, which looked empty to him. It was surely nobody's office as it was completely bare, but he just could notshake off the feeling that he was being watched. The wooden door creaked slightly as he pushed it open and he walked inside.The room was nearly as shabby as the one in which he was now sleeping, though quite a bit smaller. The reason for the extra space in the other room became clear as he looked around. There were no fewer than six portraits of the same girl around the room, all with the same initials written beneath, which he recognized instantly as Luna Lovegood.He moved closer to the picture, gazing at her as beautiful as ever. Luna had decorated her belongings with them. They looked in great condition, untouched by time or circumstance. And then, behind her picture, something caught his eye. It was a small, bright, and sharp gleam.Harry stepped toward it and saw that it was a tiny silver key. He picked it up and was surprised at how naturally it fit into his hand. He was even more surprised when he inserted it into the keyhole to the left of Luna's picture and, with a satisfying click, the door opened.The door led into a narrow, dimly lit passageway. The rustling noise from behind was louder, but he thought perhaps he was imagining it. He walked forward, the light from the Gryffindor common room fading until he could see only a little way ahead. He could not hear anything over the pounding of his heart. He stopped, his palms sweaty from both anticipation and nerves.What lay ahead, he did not know, but he had to find out. With every ounce of courage he possessed, he continued walking through the Unknowable Room.As he moved further into the passageway, the noise grew closer and clearer. It was not just the rustling sound anymore. There were murmurs, harsh whispers that sounded like the rustling of leaves on a blustery autumn day. There were footsteps, heavy, dragging, as if someone was being forced to walk against their will.And then, with a sudden realization, Harry gasped. He knew where he was. He had stumbled upon the meeting place, deep within the castle, where the Dark Lord himself held secret gatherings with his Death Eaters. The Unknowable Room was no longer a mystery to him; it was a dangerous nexus, a portal to the heart of Voldemort's power.Harry's mind raced as he wondered what to do next. Should he retreat, report what he had found to the Headmaster? Or should he press on, gather more information, and risk the wrath of the Dark Lord? The weight of the key in his hand seemed to pull him forward, urging him to uncover the secrets hidden within the Unknowable Room.In the end, Harry made his decision. He would continue on, navigating the treacherous halls of the Unknowable Room, and expose the hidden truth to the wizarding world. For the sake of his friends, for the sake of Hogwarts, and for the sake of all that was good, Harry would face whatever dangers lay ahead.And so, with his heart pounding, Harry took a deep breath and stepped into the darkness, ready to confront the unknown and confront the darkness that threatened to consume them all.。

Chapter 21 Chekhov 契诃夫

Chapter 21 Chekhov 契诃夫Anton Chekhov (1860-1904)·Russian writer, who brought both the short story and the drama to new prominence卓越in Russia and eventually in the Western world.·One of 3 greatest short story writers·"Medicine is my lawful wife", he once said, "and literature is my mistress情妇."His life & works:Born in the small seaport of Taganrog, Ukraine乌克兰on January 17th in the year 1860.He was the grandson of a serf农奴who had bought his freedom.Father, owner of a grocer杂货店.He lived an unhappy life in his childhood●Chekhov spent his early years under the shadow of his father's religious fanaticism 狂热while working long hours in his store.●Chekhov…s mother was an excellent storyteller讲故事的人who entertained the childrenwith tales of her travels all over Russia before she had married.●"Our talents we got from our father, but our soul from our mother."His education:●Chekhov attended a school for Greek boys in his hometown.●Later, his father went bankrupt. In order to avoid the debtor's prison, the family fled toMoscow, Chekhov's mother physically and emotionally broken.The family moved to Moscow.Chekhov, only 16 at the time, decided to remain in his hometown and supported himself by tutoring as he continued his schooling for 3 more years.He tried various kinds of jobs●Tutor.家庭教师●He began to write humorous short stories.In 1879 he entered the University of Moscow to study medicine.●It was from this time that Chekhov began to publish comic short stories and used themoney to support himself and his family.●His early stories ironically satirized讽刺the servile奴隶的character of the people●The Death of a Government Clerk《一个文官的死》(1883)Ivan, sneeze喷嚏; spatter溅on the bald秃头head of a general,the high political pressure政治压力of Tzarist Russia.● A Chameleon《变色龙》(1884)Otchumyelov, A police officer‟s double sides: flattery奉承and terribleHe developed his ability to say a great deal in a few words.At the same time, he began to explore serious themes that figure in his later work, such as human isolation隔离and the difficulty of communication.In 1884 Chekhov became a doctor. Around this year, he found himself coughing blood (tuberculosis).肺结核Meanwhile, he continued to write.Chekhov was awarded the Pushkin Prize in 1888. "for the best literary production distinguished by high artistic worth"His travel in 1890●Chekhov made an arduous努力的9650-km journey across Siberia by train, river steamer,and horse-drawn carriage to conduct a sociological and medical survey in a Russian penal colony流放地on Sakhalin Island库页岛, off the eastern coast of Russia.A Journey To Sakhalin库页岛is an amazing document.●“Hell Island!”●This book had some influence in moderating the harsh严厉的prison rule on the island. Around the year 1890, Chekhov moved toward publishing longer, more serious and more technically accomplished stories.●Ward No. 6(1892)《第六病室》mental patientsDoctor Andrey Y efimitch 拉京The door keeper Nikita 尼基达The story deals with the persecution to the common peopleand the consequences of indifference to human suffering.● A Man in a Case (1898)《套中人》Byelikov “I hope it won't lead to anything!”The story satirized讽刺the old tradition and autocratic专制的government.He also wrote plays戏剧:In his dramatic works Chekhov sought to convey the texture本质of everyday life, moving away from traditional ideas of plot情节and conventions惯例of dramatic speech.The major theme in Anton Chekhov's plays:●the psychologically bitterness苦难、怨恨of the Russian intellectuals知识分子●The Seagull《海鸥》(1896)Three a rtists‟ unfortunate fate.●Uncle V anya《万尼亚舅舅》(1899)The embodiment体现of the Russian intellectuals’unfortunate fate●Three Sisters《三姐妹》(1901)Three kind-hearted intellectual sisters and their helplesswaitingThe three sisters never realized their dream to go to Moscow (a major symbolic element).The Cherry Orchard《樱桃园》(1904)is his last drama works●The play concerns an aristocratic Russian woman and her family as they return to thefamily's estate (which includes a large and well-known cherry orchard) just before it is auctioned拍卖to pay the debt.the passing away of the old, aristocratic RussiaLopakhin,the former serf, who becoming an upstart暴发户, rich and powerful but rude and violent.Lopakhin had all the trees cut down, …This symbolizes the society changed by capitalism资本主义with its violence.Lopakhin, a neighbor of Madame Ranevsky, the former serf●The story presents themes of cultural futility无用、徒劳—both the futility ofthe aristocracy贵族 to maintain its status and the futility of the bourgeoisie资产阶级to find meaning in its newfound materialism唯物主义.Chekhov and Olga, 1901, on honeymoon 结婚His style (1):●Taking a cool冷静的, objective stance立场toward his characters, Chekhov conveystheir inner lives内心生活and feelings indirectly, by suggestion rather than statement陈述.His style (2):His plots are usually simple, and the endings of both his stories and his plays tend toward openness开放rather than finality定局.His style (3) - his realism:Chekhov‟s works create the effect of profound experience taking place beneath the surface in theordinary lives of unexceptional people.A warm-hearted writer●“We shall find the peace. We shall hear the angels. We shall see the sky sparkled闪耀with diamonds.”contents● 1. Russian background in late 19th century● 2. His early short stories● 3. his works after 1890s.● 4. His representative: Ward No. 6《第六病室》The Man in a Case《套中人》1. BackgroundA. society polarized偏振的.●Reform of Muzhik. (Emancipation reform ) The peasants who had lost their land andrushed into cities became industrial workers.●Contradiction between working class and bourgeoisie.B. The Russian PopulistsThe Russian Populists : to resist the prevail流行of capitalism with the traditional Russian patriarchal clan system 宗法制so as to establish the Russian socialism.In 1880s The social contradiction turned severe and the Russian government of Tzarist俄国帝制的autocracy 专制strengthened political pressure on the people.C. high political pressure●The Russian Populists assassinated暗杀Tzar Alexander II in 1881. This terrorist恐怖主义者action caused the overwhelming压倒性的revenge报复of Russian government over the Russian people.●In turn, Russian people became more and more intolerant of the government.2. his early storiesHis early stories ironically satirized the servile character of the people.●The Death of a Government Clerk《一个文官的死》● A Chameleon《变色龙》ONE fine evening, a no less fine government clerk called Ivan Dmitritch T chervyakov was sitting in the second row of the stalls, gazing through an opera glass at the Cloches de Corneville. "I have spattered him," thought T chervyakov, "he is not the head of my department, but still it is awkward. I must apologize."In mid-1880s his stories reveals a sympathy toward the miserable people.●Sorrow《哀伤》THE turner, Grigory Petrov, who had been known for years past as a splendid craftsman工匠, and at the same time as the most senseless愚蠢的peasant in the Galtchinskoy district区域, was taking his old woman to the hospital.His old woman died●At last, to make an end of uncertainty, without looking round he felt his old woman's coldhand. The lifted hand fell like a log.●"She is dead, then! What a business!"●And the turner cried. He was not so much sorry as annoyedHe nearly went insane疯狂的●V anka《万卡》V ANKA ZHUKOV, a boy of nine, who had been for three months apprenticed to Alyahin the shoemaker, was sitting up on Christmas Eve. Waiting till his master and mistress and their workmen had gone to the midnight service, he took out of his master's cupboard a bottle of ink and a pen with a rusty nib, and, spreading out a crumpled sheet of paper in front of him, began writing.His grandpa:●He was a thin but extraordinarily nimble and lively little old man of sixty-five, with aneverlastingly laughing face and drunken eyes. By day he slept in the servants' kitchen, or made jokes with the cooks; at night, wrapped in an ample sheepskin, he walked round the grounds and tapped with his little mallet木槌.3. His works after 1889After 1889 Chekhov turned into serious criticism on dark reality in his short stories.Ward No. 6《第六病室》The Man in a Case《套中人》(1888)4. His representativeWard No. 6《第六病室》:It deals with the consequences of indifference漠不关心to human suffering.·Andrey Y efimitch拉京,Doctor of Ward No. 6, a humanist, who believes in non-violence●In response to the last question Andrey Y efimitch turned rather red and said: "Y es, he ismentally deranged, but he is an interesting young man."●They asked him no other questions.Nikita tortures折磨Andrey Y efimitch:Nikita opened the door quickly, and roughly with both his hands and his knee shoved Andrey Y efimitch back, then swung his arm and punched him in the face with his fist.Andrey Y efimitch dies死:Next day Andrey Y efimitch was buried. Mihail Averyanitch and Daryushka were the only people at the funeral葬礼.·Nikita尼基达,The porter守门人, Nikita, an old soldier wearing rusty生锈的good-conduct stripes, is always lying on the litter with a pipe烟斗between his teeth. He has a grim冷酷的, surly板面孔的, battered磨损的-looking face, overhanging eyebrows which give him the expression of a sheep-dog of the steppes, and a red nose;he is short and looks thin and scraggy瘦弱的, but he is of imposing deportment行为举止and his fists are vigorous. He belongs to the class of simple-hearted, practical实际的, and dull-witted people, prompt in carrying out orders, who like discipline better than anything in the world, and so are convinced that it is their duty to beat people.His cruelty:He showers blows on the face, on the chest, on the back, on whatever comes first, and is convinced that there would be no order in the place if he did not.·Ivan Dmitritch Gromov格罗莫夫,a man of thirty-three, who is a gentleman by birth, and has been a court usher接待员and provincial secretary, suffers from the mania狂热of persecution.迫害an official called Gromov,Some twelve or fifteen years ago an official called Gromov, a highly respectable and prosperous person, was living in his own house in the principal street of the town. he was well educated and well read; according to the townspeople's notions, he knew everything, and was in their eyes something like a walking encyclopedia活百科全书He became persecution mania受迫害妄想症●In the morning Ivan Dmitritch got up from his bed in a state of horror惊骇, with coldperspiration汗水on his forehead, completely convinced that he might be arrested any minute.Ward No. 6 is a symbol of the Tzarist Russia●And its only function is to persecute迫害the common people in Russia.●Nikita symbolizes tools of the government.The Man in a Case《套中人》(1888):Byelikov tried to hide his thoughts●And Byelikov tried to hide his thoughts also in a case. The only things that were clear tohis mind were government circulars通告and newspaper articles in which something was forbidden.●Byelikov always says,"It is all right, of course; it is all very nice, but I hope it won't leadto anything!“●"Byelikov had a little bedroom like a box; his bed had curtains. When he went to bed hecovered his head over; it was hot and stuffy; the wind battered on the closed doors; there was a droning noise in the stove and a sound of sighs from the kitchen -- ominous sighs. . . . And he felt frightened under the bed-clothes.●He was afraid that something might happen, that Afanasy might murder him, that thievesmight break in, and so he had troubled dreams all night, and in the morning, when we went together to the high-school, he was depressed and pale, and it was evident that the high-school full of people excited dread and aversion恐惧和厌恶in his whole being, and that to walk beside me was irksome to a man of his solitary temperament.●"Y ou see and hear that they lie," said Ivan Ivanovitch, turning over on the other side,"and they call you a fool for putting up with their lying. Y ou endure insult and humiliation, and dare not openly say that you are on the side of the honest and the free, and you lie and smile yourself; and all that for the sake of a crust of bread, for the sake of a warm corner, for the sake of a wretched little worthless rank in the service. No, one can't go on living like this."不能这样生活Anthropus!恋爱的人。

张道真实用英语语法课件Chapter 21

General introduction

b. Indirect object It is usually after the ditransive verbs. The one is direct object, and the other is the indirect object, which indicates the action is done for whom or to whom. e.g. My wife sends you her greeting. I will play you some light music. c. Complex object object + complement e.g. She saw a girl waving to her. They elected him vice-president.

B. Preparatory “it”

a. To indicate the infinitive e.g. She found it difficult to convince him. I’d think it well worthwhile to go. b. To indicate that clause e.g. I took it for granted (that) you would be coming. You can put it that it was arranged before. * Sometimes indicate the gerund or clause introduced by conjunctive pronoun or adverb e.g. He hasn’t made it clear when he is coming back. I think it very unwise going on like this.

Pharmacology Chapter 21颜光美药理学 钙通道阻滞药-文档资料

一、细胞内钙的调节与钙离子病理生理意义 (一) 细胞内钙的调节

Na+ Ca2+

1 Ca2+

ROC 2

Ca2+

inside

MITO Na+

7 ATP CM Ca2+

9 8

Ca2+

Ca2+

VDC 3

Ca2+ LC

4

SR ATP 5 Ca2+

6

Ca2+

Na+ 1 Ca2+

(二)钙离子的病理生理意义

钙离子 在生物信息传递和内环境稳定中起重要作用。 钙超载 (calcium overload) 在细胞损伤和细胞病理生理发生过程中具有重要意义。

二、钙通道的类型及分子结构

1. 电压依赖性钙通道(VDC)

L型钙通道(long-lasting calcium channel) 最具药理学意义

+++

Suppression of Automaticity

(SA node)

+++

Suppression of conduction (AV node)

+++

Diltiazem

+

++

+++

++

Nifedipine

+++

+

+

Nicardipin

+++

+

e

+

The relative effects are from no effect () to most prominent (+++).

Chapter 21 - Risk Management 现代财务管理英文版课件

Non-Hedging Strategies

Acquisition of additional information: Test marketing, consumer surveys, and market research can reduce the risk of making poor decisions

At a specified price At a specified time

The party agreeing to buy the asset holds a “long” position

The party agreeing to sell the asset holds a “short” position

Fearful that the price of wheat will decline by November, Earthgrains constructs a short hedge by taking a short position in November wheat futures

14

4

Risk Management Benefits

Management of risk at the firm level reduces the probability of financial distress and the loss of value from forced liquidation

10

More on Futures Contracts

Futures contracts require:

Daily settlement between buyers and sellers (marking to market)

Chapter 21 p区金属

College of Chemistry & Materials Science

Al2O3 γ-Al2O3 -Al2O3 活性氧化铝

硬度不大 可作催化剂载体 可溶于酸、碱 《无机化学》-p区金属

Sichuan Normal University

College of Chemistry & Materials Science

College of Chemistry & Materials Science

从铝矾土矿(Al2O3)冶炼金属铝的步骤:

College of Chemistry & Materials Science

Sichuan Normal University

碱溶铝矾土矿 过滤 通CO2于滤 液析出Al(OH)3 灼烧 纯氧化铝 Al2O3 石墨阳极 铁槽 (阴极) 熔融金属铝

熔点低,易挥发, 共价键 分子晶体 易溶于有机溶剂 《无机化学》-p区金属

Sichuan Normal University

结构

College of Chemistry & Materials Science

Al原子是缺

电子原子,因此 AlCl3是典型的

3p

3s

Al原子基态

Lewis酸。

3s

3p

Sichuan Normal University

College of Chemistry & Materials Science

21-1 p区金属概述

1.p区金属在价层电子结构上与s区金属的区别 p区金属包括:Al、Ga、In、Tl、Ge、Sn、

Pb、Sb、Bi和Po共10种金属。

(1) p区金属元素的价电子构型为ns2np1~4 ,与s 区金属相比,有了np电子,即价电子数增多。

货币金融学(第十二版)英文版题库及答案chapter 21

Economics of Money, Banking, and Financial Markets, 12e (Mishkin)Chapter 21 The Monetary Policy and Aggregate Demand Curves21.1 The Federal Reserve and Monetary Policy1) Because prices are slow to move in the short-run, when the Federal Reserve lowers the federal funds rateA) nominal interest rates rise.B) real interest rates fall.C) inflation falls.D) real interest rates rise.Answer: BQues Status: Previous EditionAACSB: Analytical Thinking2) Because prices are sticky in the short-run, when the Federal Reserve raises the federal funds rateA) nominal interest rates fall.B) real interest rates rise.C) inflation falls.D) real interest rates fall.Answer: BQues Status: Previous EditionAACSB: Analytical Thinking21.2 The Monetary Policy Curve1) The monetary policy (MP) curve indicates the relationship betweenA) the Federal Funds Rate and the real interest rate.B) the Federal Funds Rate and the inflation rate.C) the inflation rate and the expected inflation rate.D) the real interest rate the central bank sets and the inflation rate.Answer: DQues Status: Previous EditionAACSB: Reflective Thinking2) The upward slope of the MP curve indicates thatA) the central bank lowers real interest rates when inflation rises.B) the central bank raises real interest rates when inflation falls.C) the central bank raises nominal interest rates when inflation rises.D) the central bank raises real interest rates when inflation rises.Answer: DQues Status: Previous EditionAACSB: Reflective Thinking3) The Taylor Principle states that central banks raise nominal rates by ________ than any rise in expected inflation so that real interest rates ________ when there is a rise in inflation.A) less; riseB) more; fallC) less; fallD) more; riseAnswer: DQues Status: Previous EditionAACSB: Reflective Thinking4) An autonomous tightening of monetary policyA) causes an upward movement along the monetary policy curve.B) causes a downward movement along the monetary policy curve.C) shifts the monetary policy curve upward.D) shifts the monetary policy curve downward.Answer: CQues Status: Previous EditionAACSB: Analytical Thinking5) An autonomous easing of monetary policyA) causes an upward movement along the monetary policy curve.B) causes a downward movement along the monetary policy curve.C) shifts the monetary policy curve upward.D) shifts the monetary policy curve downward.Answer: DQues Status: Previous EditionAACSB: Analytical Thinking6) Based on the Taylor Principle, a central bank's endogenous response of raising interest rates when inflation risesA) causes an upward movement along the monetary policy curve.B) causes a downward movement along the monetary policy curve.C) shifts the monetary policy curve upward.D) shifts the monetary policy curve downward.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking7) Based on the Taylor Principle, a central bank's endogenous response of decreasing interest rates when inflation fallsA) causes an upward movement along the monetary policy curve.B) causes a downward movement along the monetary policy curve.C) shifts the monetary policy curve upward.D) shifts the monetary policy curve downward.Answer: BQues Status: Previous EditionAACSB: Analytical Thinking8) Inflationary pressures caused the FOMC to increase the federal funds rate by ¼ of a percentage point in June 2004, and by exactly the same amount at every subsequent FOMC meeting through June of 2006. Theses actionsA) caused an upward movement along the monetary policy curve.B) caused a downward movement along the monetary policy curve.C) shifted the monetary policy curve upward.D) shifted the monetary policy curve downward.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking9) The Fed's policy actions of reacting to higher inflation by raising the real interest rate during 2004-2006 wereA) upward movements along the monetary policy curve.B) downward movement along the monetary policy curve.C) upward shifts of the monetary policy curve.D) downward shifts of the monetary policy curve.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking10) When the financial crisis started in August 2007, inflation was rising and the Fed began an aggressive easing lowering of the federal funds rate, which indicated thatA) the Fed pursued an autonomous monetary policy tightening.B) the Fed pursued an autonomous monetary policy easing.C) the Fed had an automatic negative response to inflation based on the Taylor rule.D) the Fed had an automatic positive response to inflation based on the Taylor rule. Answer: BQues Status: Previous EditionAACSB: Analytical Thinking11) When the financial crisis started in August 2007, inflation was rising and the Fed began an aggressive easing lowering of the federal funds rate, which indicated thatA) there was an upward movement along the monetary policy curve.B) there was a downward movement along the monetary policy curve.C) the monetary policy curve shifted upward.D) the monetary policy curve shifted downward.Answer: DQues Status: Previous EditionAACSB: Analytical Thinking21.3 The Aggregate Demand Curve1) In deriving the aggregate demand curve a ________ inflation rate leads the central bank to________ real interest rates, thereby ________ the level of equilibrium aggregate output.A) higher; raise; loweringB) lower; raise; loweringC) higher; lower; loweringD) higher; lower; raisingAnswer: AQues Status: Previous EditionAACSB: Reflective Thinking2) The aggregate demand curve is downward sloping because a higher inflation rate leads the central bank to raise ________ interest rates, thereby ________ the level of equilibrium aggregate output., everything else held constant.A) real; loweringB) real; raisingC) nominal; loweringD) nominal; raisingAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking3) The aggregate demand curve is downward sloping because a higher inflation rate leads the central bank to ________ real interest rates, thereby ________ the level of equilibrium aggregate output., everything else held constant.A) raise; loweringB) raise; raisingC) reduce; loweringD) reduce; raisingAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking4) Everything else held constant, an increase in government spending will causeA) aggregate demand to increase.B) aggregate demand to decrease.C) the quantity of aggregate demand to increase.D) the quantity of aggregate demand to decrease.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking5) Everything else held constant, an autonomous easing of monetary policy will causeA) the quantity of aggregate demand to increase.B) the quantity of aggregate demand to decrease.C) aggregate demand to decrease.D) aggregate demand to increase.Answer: DQues Status: Previous EditionAACSB: Analytical Thinking6) Everything else held constant, an autonomous tightening of monetary policy will causeA) the quantity of aggregate demand to increase.B) the quantity of aggregate demand to decrease.C) aggregate demand to increase.D) aggregate demand to decrease.Answer: DQues Status: Previous EditionAACSB: Analytical Thinking7) Everything else held constant, an autonomous easing of monetary policy will causeA) aggregate demand to increase.B) aggregate demand to decrease.C) the quantity of aggregate demand to increase.D) the quantity of aggregate demand to decrease.Answer: AQues Status: Previous EditionAACSB: Analytical Thinking8) Everything else held constant, an increase in autonomous consumer spending will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking9) Everything else held constant, a decrease in autonomous consumer spending will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: DQues Status: Previous EditionAACSB: Analytical Thinking10) Everything else held constant, an increase in autonomous planned investment spending will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking11) Everything else held constant, a decrease in autonomous planned investment spending will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: DQues Status: Previous EditionAACSB: Analytical Thinking12) Everything else held constant, a decrease in net taxes will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking13) Everything else held constant, an increase in net taxes will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: DQues Status: Previous EditionAACSB: Analytical Thinking14) Everything else held constant, an appreciation of the domestic currency will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: DQues Status: Previous EditionAACSB: Analytical Thinking15) Everything else held constant, a depreciation of the domestic currency will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: AQues Status: Previous EditionAACSB: Analytical Thinking16) Everything else held constant, a decrease in government spending will cause the IS curve to shift to the ________ and aggregate demand will ________.A) right; increaseB) right; decreaseC) left; increaseD) left; decreaseAnswer: DQues Status: Previous EditionAACSB: Analytical Thinking。

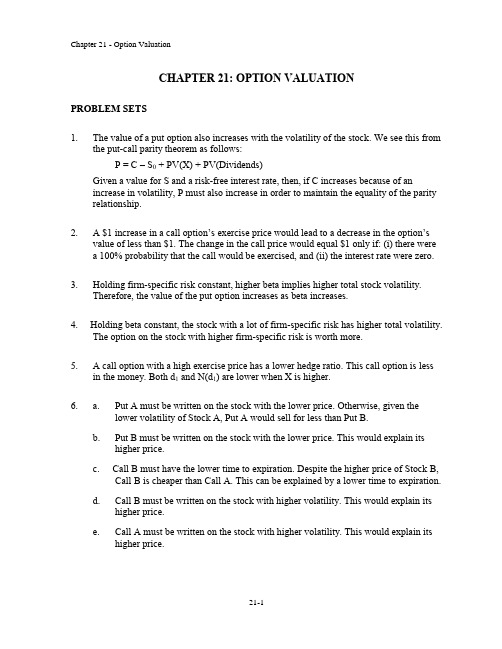

期权期货与其他衍生产品第九版课后习题与答案Chapter (21)

A binomial tree cannot be used in the way described in this chapter. This is an example of what is known as a history-dependent option. The payoff depends on the path followed by the stock price as well as its final value. The option cannot be valued by starting at the end of the tree and working backward since the payoff at the final branches is not known unambiguously. Chapter 27 describes an extension of the binomial tree approach that can be used to handle options where the payoff depends on the average value of the stock price. Problem 21.6. “For a dividend-paying stock, the tree for the stock price does not recombine; but the tree for the stock price less the present value of future dividends does recombine.” Explain this statement. Suppose a dividend equal to D is paid during a certain time interval. If S is the stock price at the beginning of the time interval, it will be either Su D or Sd D at the end of the time interval. At the end of the next time interval, it will be one of (Su D)u , (Su D)d , (Sd D)u and (Sd D)d . Since (Su D)d does not equal (Sd D)u the tree does not recombine. If S is equal to the stock price less the present value of future dividends, this problem is avoided. Problem 21.7. Show that the probabilities in a Cox, Ross, and Rubinstein binomial tree are negative when the condition in footnote 8 holds. With the usual notation

人民大2023张道真英语语法(第三版)(精华版)课件Chapter 21

1.5 其他的的倒装句

(1)某些表示祝愿的句子: Long live the solidarity of the people of the world! (2)含直接引语的插入语: ①在直接引语后的插入语中,主语可以放到谓语后面,特别是当它比较 长时: "Try again." said Ann's friends encouragingly. ②如果主语不长,直接引语放在谓语前后都可以: "I've just heard the news," said Tom. "I've just heard the news," Tom said. ③如果谓语后面有宾语,主语也不能放到后面: "That man is a famous film star, " Bill told me in a whisper.

1.5 其他的的倒装句

(3)出于修辞考虑的表语提前: ①为了给表语以更突出的位置: Very grateful we are for your help. ②为了使这个句子和前面句子联系更紧密: He was born poor and poor he remained all his life. (4)原形动词提前: 助动词或情态动词后的原形动词,有时也可能提到句子前部: We'll win through and win through we shall.

3.2 定语放在所修饰词后面的情况

放在所修饰词后面的主要有下面几种定语: (1)定语从句: People whose rents have been raised can appeal. (2)介词短语: It was a bolt from the blue. (3)分词短语及不定式短语: Here are the seats reserved for you.

针织学(双语)课件Chapter21

7.

8.

In order to ‘interweave’/交织 an inlaid yarn vertically with a knitted yarn, it is necessary to cause it to evade for three courses and to miss-lap for one course during the repeat.

7

Fig 21.2 Fall-plate raised out of action

Fig 21.3 Fall-plate lowered into action

21.4 fall-plate patterning 压纱板花型

It is necessary to knit the ground structure overlaps on the guide bars behind the fall-plate because these are unaffected by its descent.

Fig 21.1 The action of inlay in warp knitting

2

21.2 general rules governing laying-in in warp knitting 形成经编衬纬的基本原则

1.

An inlaid yarn will pass across one less wale than a knitted yarn than has the same extent pf underlap. To eliminate the overlap movement (when using a two-link-percourse chain/二行程链条) it is necessary to put two links of the same height at the point where this should take place. The inlaid yarn will be tied in at every wale it crosses (if the overlapping guide bar is in front of it). If the knitting bar underlaps in opposition to the inlay, it will add an extra thread for tying it into the structure. When the laying-in and knitting bars lap in unison, there will be one less thread available for tying in the inlay so that the inlay will be tied-in by one less thread than the number of needles the inlay underlaps.

投资学Chap021

CHAPTER 21: OPTION VALUATIONPROBLEM SETS1. The value of a put option also increases with the volatility of the stock. We see this from theput-call parity theorem as follows:P = C – S0 + PV(X) + PV(Dividends)Given a value for S and a risk-free interest rate, then, if C increases because of an increase in volatility, P must also increase in order to maintain the equality of the parity relationship.2. A $1 increase in a call option’s exercise price would lead to a decrease in the option’s value ofless than $1. The change in the call price would equal $1 only if: (i) there were a 100%probability that the call would be exercised, and (ii) the interest rate were zero.3. Holding firm-specific risk constant, higher beta implies higher total stock volatility. Therefore,the value of the put option increases as beta increases.4. Holding beta constant, the stock with a lot of firm-specific risk has higher total volatility. Theoption on the stock with higher firm-specific risk is worth more.5. A call option with a high exercise price has a lower hedge ratio. This call option is less in themoney. Both d1 and N(d1) are lower when X is higher.6. a. Put A must be written on the stock with the lower price. Otherwise, given the lowervolatility of Stock A, Put A would sell for less than Put B.b. Put B must be written on the stock with the lower price. This would explain its higherprice.c. Call B must have the lower time to expiration. Despite the higher price of Stock B, CallB is cheaper than Call A. This can be explained by a lower time to expiration.d. Call B must be written on the stock with higher volatility. This would explain its higherprice.e. Call A must be written on the stock with higher volatility. This would explain its higherprice.7.Exercise Price Hedge Ratio 120 0/30 = 0.000 110 10/30 = 0.333 100 20/30 = 0.667 90 30/30 = 1.000As the option becomes more in the money, the hedge ratio increases to a maximum of 1.0.8.S d 1 N(d 1) 45 -0.0268 0.4893 50 0.5000 0.6915 550.97660.83569.a. uS 0 = 130 ⇒ P u = 0 dS 0 = 80 ⇒ P d = 30 The hedge ratio is:5380130300dS uS P P H 00d u -=--=--=b.Riskless Portfolio S = 80 S = 130 Buy 3 shares 240 390 Buy 5 puts 150 0 Total390390Present value = $390/1.10 = $354.545c.The portfolio cost is: 3S + 5P = 300 + 5P The value of the portfolio is: $354.545 Therefore: P = $54.545/5 = $10.9110. The hedge ratio for the call is:5280130020dS uS C C H 00d u =--=--=Riskless Portfolio S = 80 S = 130 Buy 2 shares 160 260 Write 5 calls 0 -100 Total160160Present value = $160/1.10 = $145.455 The portfolio cost is: 2S – 5C = $200 – 5C The value of the portfolio is: $145.455 Therefore: C = $54.545/5 = $10.91 Does P = C + PV(X) – S?10.91 = 10.91 + 110/1.10 – 100 = 10.9111. d 1 = 0.3182 ⇒ N(d 1) = 0.6248d 2 = –0.0354 ⇒ N(d 2) = 0.4859 Xe - r T = 47.56 C = $8.1312. P = $5.69This value is derived from our Black-Scholes spreadsheet, but note that we could have derived the value from put-call parity:P = C + PV(X) – S 0 = $8.13 + $47.56 - $50 = $5.6913. a. C falls to $5.5541b. C falls to $4.7911c. C falls to $6.0778d. C rises to $11.5066e. C rises to $8.718714. According to the Black-Scholes model, the call option should be priced at:[$55 ⨯ N(d1)] – [50 ⨯ N(d 2)] = ($55 ⨯ 0.6) – ($50 ⨯ 0.5) = $8Since the option actually sells for more than $8, implied volatility is greater than 0.30.15. A straddle is a call and a put. The Black-Scholes value would be:C + P = S0 N(d1) - Xe–rT N(d 2) + Xe–rT [1 - N(d 2)] - S0 [1 - N(d1)]= S0 [2N(d1) - 1] + Xe–rT [1 - 2N(d 2)]On the Excel spreadsheet (Spreadsheet 21.1), the valuation formula would be:B5*(2*E4 - 1) + B6*EXP(-B4*B3)*(1 - 2*E5)16. The rate of return of a call option on a long-term Treasury bond should be more sensitive tochanges in interest rates than is the rate of return of the underlying bond. The option elasticityexceeds 1.0. In other words, the option is effectively a levered investment and the rate of return on the option is more sensitive to interest rate swings.17. Implied volatility has increased. If not, the call price would have fallen as a result of thedecrease in stock price.18. Implied volatility has increased. If not, the put price would have fallen as a result of thedecreased time to expiration.19. The hedge ratio approaches one. As S increases, the probability of exercise approaches 1.0.N(d1) approaches 1.0.20. The hedge ratio approaches –1.0. As S decreases, the probability of exercise approaches 1.[N(d1) –1] approaches –1 as N(d1) approaches 0.21. A straddle is a call and a put. The hedge ratio of the straddle is the sum of the hedge ratios ofthe individual options: 0.4 + (–0.6) = –0.222. a. The spreadsheet appears as follows:The standard deviation is: 0.3213b. The spreadsheet below shows the standard deviation has increased to: 0.3568Implied volatility has increased because the value of an option increases with greatervolatility.c. Implied volatility increases to 0.4087 when expiration decreases to four months. Theshorter expiration decreases the value of the option; therefore, in order for the optionprice to remain unchanged at $8, implied volatility must increase.d. Implied volatility decreases to 0.2406 when exercise price decreases to $100. Thedecrease in exercise price increases the value of the call, so that, in order to the optionprice to remain at $8, implied volatility decreases.e. The decrease in stock price decreases the value of the call. In order for the option priceto remain at $8, implied volatility increases.23. a. The delta of the collar is calculated as follows:Position DeltaBuy stock 1.0Buy put, X = $45 N(d1) – 1 = –0.40Write call, X = $55 –N(d1) = –0.35Total 0.25If the stock price increases by $1, then the value of the collar increases by $0.25. Thestock will be worth $1 more, the loss on the purchased put will be $0.40, and the callwritten represents a liability that increases by $0.35.b.If S becomes very large, then the delta of the collar approaches zero. Both N(d1) termsapproach 1. Intuitively, for very large stock prices, the value of the portfolio is simply the(present value of the) exercise price of the call, and is unaffected by small changes in thestock price.As S approaches zero, the delta also approaches zero: both N(d1) terms approach 0.For very small stock prices, the value of the portfolio is simply the (present value of the)exercise price of the put, and is unaffected by small changes in the stock price.24. Put X DeltaA 10 -0.1B 20 -0.5C 30 -0.925. a. Choice A: Calls have higher elasticity than shares. For equal dollar investments, a call’scapital gain potential is greater than that of the underlying stock.b. Choice B: Calls have hedge ratios less than 1.0, so the shares have higher profit potential.For an equal number of shares controlled, the dollar exposure of the shares is greaterthan that of the calls, and the profit potential is therefore greater.26. a. uS 0 = 110 ⇒ P u = 0 dS 0 = 90 ⇒ P d = 10 The hedge ratio is:2190110100dS uS P P H 00d u -=--=--=A portfolio comprised of one share and two puts provides a guaranteed payoff of $110, with present value: $110/1.05 = $104.76 Therefore:S + 2P = $104.76$100 + 2P = $104.76 ⇒ P = $2.38b. Cost of protective put portfolio = $100 + $2.38 = $102.38c.Our goal is a portfolio with the same exposure to the stock as the hypothetical protective put portfolio. Since the put’s hedge ratio is –0.5, the portfolio consists of (1 – 0.5) = 0.5 shares of stock, which costs $50, and the remaining funds ($52.38) invested in T-bills, earning 5% interest. Portfolio S = 90 S = 110 Buy 0.5 shares 45 55 Invest in T-bills 55 55 Total100110This payoff is identical to that of the protective put portfolio. Thus, the stock plus bills strategy replicates both the cost and payoff of the protective put.27. The put values in the second period are:P uu = 0P ud = P du = 110 − 104.50 = 5.50 P dd = 110 − 90.25 = 19.75To compute P u , first compute the hedge ratio:3150.10412150.50udSuuSP P H 0ud uu -=--=--=Form a riskless portfolio by buying one share of stock and buying three puts. The cost of the portfolio is: S + 3P u = $110 + 3P u The payoff for the riskless portfolio equals $121: Riskless Portfolio S = 104.50 S = 121 Buy 1 share 104.50 121.00 Buy 3 puts 16.50 0.00 Total121.00121.00Therefore, find the value of the put by solving:$110 + 3P u = $121/1.05 ⇒ P u = $1.746 To compute P d , compute the hedge ratio:0.125.9050.10475.1950.5ddSduSP P H 0dd du -=--=--=Form a riskless portfolio by buying one share and buying one put. The cost of the portfolio is: S + P d = $95 + P d The payoff for the riskless portfolio equals $110: Riskless Portfolio S = 90.25 S = 104.50 Buy 1 share 90.25 104.50 Buy 1 put 19.75 5.50 Total110.00110.00Therefore, find the value of the put by solving:$95 + P d = $110/1.05 ⇒ P d = $9.762 To compute P, compute the hedge ratio:5344.095110762.9746.1dS uS P P H 00d u -=--=--=Form a riskless portfolio by buying 0.5344 of a share and buying one put. The cost of the portfolio is: 0.5344S + P = $53.44 + PThe payoff for the riskless portfolio equals $60.53:Riskless Portfolio S = 95 S = 110Buy 0.5344 share 50.768 58.784Buy 1 put 9.762 1.746Total 60.530 60.530Therefore, find the value of the put by solving:$53.44 + P = $60.53/1.05 ⇒ P = $4.208Finally, we verify this result using put-call parity. Recall from Example 21.1 that:C = $4.434Put-call parity requires that:P = C + PV(X) – S$4.208 = $4.434 + ($110/1.052) - $100Except for minor rounding error, put-call parity is satisfied.28. If r = 0, then one should never exercise a put early. There is no “time value cost” to waiting toexercise, but there is a “volatility benefit” from waiting. To show this more rigorously, consider the following portfolio: lend $X and short one share of stock. The cost to establish the portfolio is (X – S 0). The payoff at time T (with zero interest earnings on the loan) is (X – S T). Incontrast, a put option has a payoff at time T of (X – S T) if that value is positive, and zerootherwise. The put’s payoff is at least as large as the portfolio’s, and therefore, the put must cost at least as much as the portfolio to purchase. Hence, P ≥ (X – S 0), and the put can be sold for more than the proceeds from immediate exercise. We conclude that it doesn’t pay to exercise early.29. a. Xe-rTb. Xc. 0d. 0e. It is optimal to exercise immediately a put on a stock whose price has fallen to zero. Thevalue of the American put equals the exercise price. Any delay in exercise lowers valueby the time value of money.30. Step 1: Calculate the option values at expiration. The two possible stock prices and thecorresponding call values are:uS 0 = 120 ⇒ C u = 20 dS 0 = 80 ⇒ C d = 0 Step 2: Calculate the hedge ratio.2180120020dS uS C C H 00d u =--=--=Therefore, form a riskless portfolio by buying one share of stock and writing two calls. The cost of the portfolio is: S – 2C = 100 – 2CStep 3: Show that the payoff for the riskless portfolio equals $80: Riskless Portfolio S = 80 S = 120 Buy 1 share 80 120 Write 2 calls 0 -40 Total8080Therefore, find the value of the call by solving:$100 – 2C = $80/1.10 ⇒ C = $13.636Notice that we did not use the probabilities of a stock price increase or decrease. These are not needed to value the call option.31.The two possible stock prices and the corresponding call values are:uS 0 = 130 ⇒ C u = 30 dS 0 = 70 ⇒ C d = 0 The hedge ratio is:2170130030dS uS C C H 00d u =--=--=Form a riskless portfolio by buying one share of stock and writing two calls. The cost of the portfolio is: S – 2C = 100 – 2CThe payoff for the riskless portfolio equals $70: Riskless Portfolio S = 70 S = 130 Buy 1 share 70 130 Write 2 calls 0 -60 Total7070Therefore, find the value of the call by solving:$100 – 2C = $70/1.10 ⇒ C = $18.182Here, the value of the call is greater than the value in the lower-volatility scenario.32. The two possible stock prices and the corresponding put values are:uS 0 = 120 ⇒ P u = 0dS 0 = 80 ⇒ P d = 20 The hedge ratio is:2180120200dS uS P P H 00d u -=--=--=Form a riskless portfolio by buying one share of stock and buying two puts. The cost of the portfolio is: S + 2P = 100 + 2PThe payoff for the riskless portfolio equals $120: Riskless Portfolio S = 80 S = 120 Buy 1 share 80 120 Buy 2 puts 40 0 Total120120Therefore, find the value of the put by solving:$100 + 2P = $120/1.10 ⇒ P = $4.545 According to put-call parity: P + S = C + PV(X) Our estimates of option value satisfy this relationship:$4.545 + $100 = $13.636 + $100/1.10 = $104.54533. If we assume that the only possible exercise date is just prior to the ex-dividend date, then therelevant parameters for the Black-Scholes formula are:S 0 = 60r = 0.5% per month X = 55 σ = 7%T = 2 monthsIn this case: C = $6.04If instead, one commits to foregoing early exercise, then we reduce the stock price by the present value of the dividends. Therefore, we use the following parameters:S 0 = 60 – 2e − (0.005 ⨯ 2) = 58.02 r = 0.5% per month X = 55 σ = 7%T = 3 months In this case, C = $5.05The pseudo-American option value is the higher of these two values: $6.0434. True. The call option has an elasticity greater than 1.0. Therefore, the call’s percentage rate ofreturn is greater than that of the underlying stock. Hence the GM call responds more thanproportionately when the GM stock price changes in response to broad market movements.Therefore, the beta of the GM call is greater than the beta of GM stock.35. True. The elasticity of a call option is higher the more out of the money is the option. (Eventhough the delta of the call is lower, the value of the call is also lower. The proportionalresponse of the call price to the stock price increases. You can confirm this with numerical examples.) Therefore, the rate of return of the call with the higher exercise price respondsmore sensitively to changes in the market index, and therefore it has the higher beta.36. As the stock price increases, conversion becomes increasingly more assured. The hedge ratioapproaches 1.0. The price of the convertible bond will move one-for-one with changes in the price of the underlying stock.37. Salomon believes that the market assessment of volatility is too high. Therefore, Salomonshould sell options because the analysis suggests the options are overpriced with respect to true volatility. The delta of the call is 0.6, while that of the put is 0.6 – 1 = –0.4. Therefore, Salomon should sell puts and calls in the ratio of 0.6 to 0.4. For example, if Salomon sells 2 calls and 3 puts, the position will be delta neutral:Delta = (2 ⨯ 0.6) + [3 ⨯ (–0.4)] = 038. If the stock market index increases 1%, the 1 million shares of stock on which the options arewritten would be expected to increase by:0.75% ⨯ $5 ⨯ 1 million = $37,500The options would increase by:delta ⨯ $37,500 = 0.8 ⨯ $37,500 = $30,000In order to hedge your market exposure, you must sell $3,000,000 of the market indexportfolio so that a 1% change in the index would result in a $30,000 change in the value of the portfolio.39. S = 100; current value of portfolioX = 100; floor promised to clients (0% return)σ = 0.25; volatilityr = 0.05; risk-free rateT = 4 years; horizon of programa. Using the Black-Scholes formula, we find that:d1 = 0.65, N(d1) = 0.7422, d 2 = 0.15, N(d 2) = 0.5596Put value = $10.27Therefore, total funds to be managed equals $110.27 million: $100 million portfolio valueplus the $10.27 million fee for the insurance program.The put delta is: N(d1) – 1 = 0.7422 – 1 = –0.2578Therefore, sell off 25.78% of the equity portfolio, placing the remaining funds in T-bills. Theamount of the portfolio in equity is therefore $74.22 million, while the amount in T-bills is:$110.27 million – $74.22 million = $36.05 millionb.At the new portfolio value, the put delta becomes: –0.2779This means that you must reduce the delta of the portfolio by:0.2779 – 0.2578 = 0.0201You should sell an additional 2.01% of the equity position and use the proceeds to buyT-bills. Since the stock price is now at only 97% of its original value, you need to sell: $97 million ⨯ 0.0201 = $1.950 million of stock40. Using the true volatility (32%) and time to expiration T = 0.25 years, the hedge ratio for Exxonis N(d1) = 0.5567. Because you believe the calls are under-priced (selling at an impliedvolatility that is too low), you will buy calls and short 0.5567 shares for each call you buy.41. The calls are cheap (implied σ = 0.30) and the puts are expensive (impliedσ = 0.34). Therefore, buy calls and sell puts. Using the “true” volatility ofσ = 0.32, the call delta is 0.5567 and the put delta is: 0.5567 – 1.0 = –0.4433Therefore, for each call purchased, buy: 0.5567/0.4433 = 1.256 puts42. a.To calculate the hedge ratio, suppose that the market index increases by 1%. Then the stock portfolio would be expected to increase by:1% ⨯ 1.5 = 1.5% or 0.015 ⨯ $1,250,000 = $18,750Given the option delta of 0.8, the option portfolio would increase by:$18,750 ⨯ 0.8 = $15,000Salomon’s liability from writing these options would increase by the same amount. The market index portfolio would increase in value by 1%. Therefore, SalomonBrothers should purchase $1,500,000 of the market index portfolio in order to hedge its position so that a 1% change in the index would result in a $15,000 change in the value of the portfolio.b.The delta of a put option is:0.8 – 1 = –0.2Therefore, for every 1% the market increases, the index will rise by 10 points and the value of the put option contract will change by:delta ⨯ 10 ⨯ contract multiplier = –0.2 ⨯ 10 ⨯ 100 = –$200 Therefore, Salomon should write: $12,000/$200 = 60 put contractsCFA PROBLEMS1. Statement a: The hedge ratio (determining the number of futures contracts to sell) ought to beadjusted by the beta of the equity portfolio, which is 1.20. The correct hedge ratio would be:400,22.1000,2β2,000β500100$million 100$=⨯=⨯=⨯⨯Statement b: The portfolio will be hedged, and should therefore earn the risk-free rate, not zero, as the consultant claims. Given a futures price of 100 and an equity price of 100, the rate of return over the 3-month period is: (100 - 99)/99 = 1.01% = approximately 4.1% annualized 2.a.The value of the call option is expected to decrease if the volatility of the underlying stock price decreases. The less volatile the underlying stock price, the less the chance of extreme price movements and the lower the probability that the option expires in the money. This makes the participation feature on the upside less valuable.The value of the call option is expected to increase if the time to expiration of the option increases. The longer the time to expiration, the greater the chance that the option will expire in the money resulting in an increase in the time premium component of the option’s value.b. i. When European options are out of the money, investors are essentially saying that theyare willing to pay a premium for the right, but not the obligation, to buy or sell theunderlying asset. The out-of-the-money option has no intrinsic value, but, since optionsrequire little capital (just the premium paid) to obtain a relatively large potential payoff,investors are willing to pay that premium even if the option may expire worthless. TheBlack-Scholes model does not reflect investors’ demand for any premium above thetime value of the option. Hence, if investors are willing to pay a premium for an out-of-the-money option above its time value, the Black-Scholes model does not value thatexcess premium.ii. With American options, investors have the right, but not the obligation, to exercise theoption prior to expiration, even if they exercise for non-economic reasons. This increasedflexibility associated with American options has some value but is not considered in theBlack-Scholes model because the model only values options to their expiration date(European options).3. a. American options should cost more (have a higher premium). American options give theinvestor greater flexibility than European options since the investor can choose whetherto exercise early. When the stock pays a dividend, the option to exercise a call early canbe valuable. But regardless of the dividend, a European option (put or call) never sellsfor more than an otherwise-identical American option.b. C = S0 + P - PV(X) = $43 + $4 - $45/1.055 = $4.346Note: we assume that Abaco does not pay any dividends.c. i) An increase in short-term interest rate ⇒ PV(exercise price) is lower, and call valueincreases.ii) An increase in stock price volatility ⇒ the call value increases.iii) A decrease in time to option expiration ⇒ the call value decreases.4. a. The two possible values of the index in the first period are:uS0 = 1.20 × 50 = 60dS0 = 0.80 × 50 = 40The possible values of the index in the second period are:uuS0 = (1.20)2 × 50 = 72udS0 = 1.20 × 0.80 × 50 = 48duS0 = 0.80 × 1.20 × 50 = 48ddS0 = (0.80)2 × 50 = 32C uu = 72 − 60 = 12 C ud = C du = C dd = 0 Since C ud = C du = 0, then C d = 0.To compute C u , first compute the hedge ratio:214872012udSuuSC C H 0ud uu =--=--=Form a riskless portfolio by buying one share of stock and writing two calls. The cost of the portfolio is: S – 2C u = $60 – 2C u The payoff for the riskless portfolio equals $48: Riskless Portfolio S = 48 S = 72 Buy 1 share 48 72 Write 2 calls 0 -24 Total4848Therefore, find the value of the call by solving:$60 – 2C u = $48/1.06 ⇒ C u = $7.358 To compute C, compute the hedge ratio:3679.040600358.7dS uS C C H 00d u =--=--=Form a riskless portfolio by buying 0.3679 of a share and writing one call. The cost of the portfolio is: 0.3679S – C = $18.395 – C The payoff for the riskless portfolio equals $14.716: Riskless Portfolio S = 40 S = 60 Buy 0.3679 share 14.716 22.074 Write 1 call 0.000 −7.358 Total14.71614.716Therefore, find the value of the call by solving:$18.395 – C = $14.716/1.06 ⇒ C = $4.512P uu = 0P ud = P du = 60 − 48 = 12 P dd = 60 − 32 = 28To compute P u , first compute the hedge ratio:214872120udSuuSP P H 0ud uu -=--=--=Form a riskless portfolio by buying one share of stock and buying two puts. The cost of the portfolio is: S + 2P u = $60 + 2P u The payoff for the riskless portfolio equals $72: Riskless Portfolio S = 48 S = 72 Buy 1 share 48 72 Buy 2 puts 24 0 Total7272Therefore, find the value of the put by solving:$60 + 2P u = $72/1.06 ⇒ P u = $3.962 To compute P d , compute the hedge ratio:0.132482812ddSduSP P H 0dd du -=--=--=Form a riskless portfolio by buying one share and buying one put. The cost of the portfolio is: S + P d = $40 + P d The payoff for the riskless portfolio equals $60: Riskless Portfolio S = 32 S = 48 Buy 1 share 32 48 Buy 1 put 28 12 Total6060Therefore, find the value of the put by solving:$40 + P d = $60/1.06 ⇒ P d = $16.604 To compute P, compute the hedge ratio:6321.04060604.16962.3dS uS P P H 00d u -=--=--=Form a riskless portfolio by buying 0.6321 of a share and buying one put.The cost of the portfolio is: 0.6321S + P = $31.605 + PThe payoff for the riskless portfolio equals $41.888:Riskless Portfolio S = 40 S = 60Buy 0.6321 share 25.284 37.926Buy 1 put 16.604 3.962Total 41.888 41.888Therefore, find the value of the put by solving:$31.605 + P = $41.888/1.06 ⇒ P = $7.912d. According to put-call-parity:C = S0 + P - PV(X) = $50 + $7.912 - $60/(1.062 ) = $4.512This is the value of the call calculated in part (b) above.5. a. (i) Index increases to 1402. The combined portfolio will suffer a loss. The written callsexpire in the money; the protective put purchased expires worthless. Let’s analyze theoutcome on a per-share basis. The payout for each call option is $52, for a total cashoutflow of $104. The stock is worth $1,402. The portfolio will thus be worth: $1,402 -$104 = $1,298The net cost of the portfolio when the option positions are established is:$1,336 + $16.10 (put) - [2 ⨯ $8.60] (calls written) = $1,334.90(ii) Index remains at 1336. Both options expire out of the money. The portfolio will thus beworth $1,336 (per share), compared to an initial cost 30 days earlier of $1,334.90. Theportfolio experiences a very small gain of $1.10.(iii) Index declines to 1270. The calls expire worthless. The portfolio will be worth $1,330,the exercise price of the protective put. This represents a very small loss of $4.90 comparedto the initial cost 30 days earlier of $1,334.90b. (i) Index increases to 1402. The delta of the call approaches 1.0 as the stock goes deep intothe money, while expiration of the call approaches and exercise becomes essentially certain.The put delta approaches zero.(ii) Index remains at 1336. Both options expire out of the money. Delta of eachapproaches zero as expiration approaches and it becomes certain that the options willnot be exercised.(iii) Index declines to 1270. The call is out of the money as expiration approaches. Deltaapproaches zero. Conversely, the delta of the put approaches -1.0 as exercise becomescertain.c. The call sells at an implied volatility (11.00%) that is less than recent historical volatility(12.00%); the put sells at an implied volatility (14.00%) that is greater than historicalvolatility. The call seems relatively cheap; the put seems expensive.。

《biology》Chapter 21

21.4 How Do Plants Affect Other Organisms?

© 2014 Pearson Education, Inc.

21.1 What Are the Key Features of Plants?

– The organism was bathed in a nutrient-rich solution – It was supported by buoyancy (浮力) and not likely to dry out – Life in water facilitates reproduction

Plants exhibit three characteristic traits:

1. Photosynthesis 2. Multicellular embryos 3. Alternation of generations

Each of these traits occurs in some other kinds of organisms, but only plants combine all three

© 2014 Pearson Education, Inc.

Food-storage

starch

Cell wall

Cellulose, hemicellulose, pectin (果 胶) cellulose, agar(琼脂 , carrageenan (角叉 菜胶)

chl a, chl b, carotenoids

© 2014 Pearson Education, Inc.

21.2 How Have Plants Evolved?

CHAPTER 21 OPTICAL PROPERTIES