tax law

中华人民共和国外商投资企业和外国企业所得税法(英文版)

中华人民共和国外商投资企业和外国企业所得税法(英文版)INCOME TAX LAW OF THE PEOPLE'S REPUBLIC OF CHINA FOR ENTERPRISESWITH FOREIGN INVESTMENT AND FOREIGN ENTERPRISES(Adopted at the Fourth Session of the Seventh National People'sCongress on April 9, 1991, promulgated by Order No. 45 of the President ofthe People's Republic of China on April 9, 1991 and effective as of July1, 1991)Important Notice:In case of discrepancy, the original version in Chinese shall prevail.Whole DocumentINCOME TAX LAW OF THE PEOPLE'S REPUBLIC OF CHINA FOR ENTERPRISES WITHFOREIGN INVESTMENT AND FOREIGN ENTERPRISES (Adopted at the Fourth Session of the Seventh National People's Congress on April 9, 1991, promulgated by Order No. 45 of the President ofthe People's Republic of China on April 9, 1991 and effective as of July1, 1991)Article 1Income tax shall be paid in accordance with the provisions of this Law byenterprises with foreign investment within the territory of the People's Republic of China on their income derived from production, businessoperations and other sources. Income tax shall be paid in accordance withthe provisions of this Law by foreign enterprises on their income derivedfrom production, business operations and other sources within theterritory of the People's Republic of China.Article 2"Enterprises with foreign investment" referred to in this LawmeanChinese-foreign equity joint ventures, Chinese-foreign contractual jointventures and foreign-capital enterprises that are established in China. "Foreign enterprises" referred to in this Law mean foreign companies,enterprises and other economic organizations which have establishments orplaces in China and engage in production or business operations, andwhich, though without establishments or places in China, have income fromsources within China.Article 3Any enterprise with foreign investment which establishes its head officein China shall pay its income tax on its income derived from sourcesinside and outside China. Any foreign enterprise shall pay its income taxon its income derived from sources within China.Article 4The taxable income of an enterprise with foreign investment and anestablishment or a place set up in China to engage in production orbusiness operations by a foreign enterprise, shall be the amount remainingfrom its gross income in a tax year after the costs, expenses and losses have been deducted.Article 5The income tax on enterprises with foreign investment and the income taxwhich shall be paid by foreign enterprises on the income of theirestablishments or places set up in China to engage in production orbusiness operations shall be computed on the taxable income at the rate of thirty percent, and local income tax shall be computed on the taxableincome at the rate of three percent.Article 6The State shall, in accordance with the industrial policies, guidetheorientation of foreign investment and encourage the establishment ofenterprises with foreign investment which adopt advanced technology andequipment and export all or greater part of their products.Article 7The income tax on enterprises with foreign investment established inSpecial Economic Zones, foreign enterprises which have establishments orplaces in Special Economic Zones engaged in production or businessoperations, and on enterprises with foreign investment of a productionnature in Economic and Technological Development Zones, shall be levied atthe reduced rate of fifteen percent.The income tax on enterprises with foreign investment of a productionnature established in coastal economic open zones or in the old urbandistricts of cities where the Special Economic Zones or the Economic andTechnological Development Zones are located, shall be levied at thereduced rate of twenty-four percent.The income tax on enterprises with foreign investment in coastal economicopen zones, in the old urban districts of cities where the SpecialEconomic Zones or the Economic and Technological Development Zones arelocated or in other regions defined by the State Council, within the scope of energy, communications, harbour, wharf or other projects encouraged bythe State, may be levied at the reduced rate of fifteen percent. Thespecific measures shall be drawn up by the State Council.Article 8Any enterprise with foreign investment of a production nature scheduled tooperate for a period of not less than ten years shall, from theyearbeginning to make profit, be exempted from income tax in the first andsecond years and allowed a fifty percent reduction in the third to fifth years. However, the exemption from or reduction of income tax onenterprises with foreign investment engaged in the exploitation ofresources such as petroleum, natural gas, rare metals, and precious metals shall be regulated separately by the State Council. Enterprises withforeign investment which have actually operated for a period of less thanten years shall repay the amount of income tax exempted or reducedalready.The relevant regulations, promulgated by the State Council before theentry into force of this Law, which provide preferential treatment ofexemption from or reduction of income tax on enterprises engaged inenergy, communications, harbour, wharf and other major projects of aproduction nature for a period longer than that specified in the preceding paragraph, or which provide preferential treatment of exemption from orreduction of income tax on enterprises engaged in major projects of a non-production nature, shall remain applicable after this Law enters intoforce.Any enterprise with foreign investment which is engaged in agriculture,forestry or animal husbandry and any other enterprise with foreigninvestment which is established in remote underdeveloped areas may, uponapproval by the competent department for tax affairs under the StateCouncil of an application filed by the enterprise, be allowed a fifteen to thirty percent reduction of the amount of income tax payable for a periodof another ten years following the expiration of the period fortaxexemption or reduction as provided for in the preceding two paragraphs. After this Law enters into force, any modification to the provisions ofthe preceding three paragraphs of this Article on the exemption from orreduction of income tax on enterprises shall be submitted by the StateCouncil to the Standing Committee of the National People's Congress fordecision.Article 9The exemption from or reduction of local income tax on any enterprise withforeign investment which operates in an industry or undertakes a projectencouraged by the State shall, in accordance with the actual situation, be at the discretion of the people's government of the relevant province,autonomous region or municipality directly under the Central Government.Article 10Any foreign investor of an enterprise with foreign investment whichreinvests its share of profit obtained from the enterprise directly into that enterprise by increasing its registered capital, or uses the profit as capital investment to establish other enterprises with foreigninvestment to operate for a period of not less than five years shall, upon approval by the tax authorities of an application filed by the investor, be refunded forty percent of the income tax already paid on the reinvested amount. Where regulations of the State Council provide otherwise inrespect of preferential treatment, such provisions shall apply. If theinvestor withdraws its reinvestment before the expiration of a period offive years, it shall repay the refunded tax.Article 11Losses incurred in a tax year by any enterprise with foreign investmentand by an establishment or a place set up in China by a foreign enterprise to engage in production or business operations may be made upby theincome of the following tax year. Should the income of the following taxyear be insufficient to make up for the said losses, the balance may bemade up by its income of the further subsequent year, and so on, over aperiod not exceeding five years.Article 12Any enterprise with foreign investment shall be allowed, when filing aconsolidated income tax return, to deduct from the amount of tax payablethe foreign income tax already paid abroad in respect of the incomederived from sources outside China. The deductible amount shall, however,not exceed the amount of income tax otherwise payable under this Law inrespect of the income derived from sources outside China.Article 13The payment or receipt of charges or fees in business transactions betweenan enterprise with foreign investment or an establishment or a place setup in China by a foreign enterprise to engage in production or businessoperations, and its associated enterprises, shall be made in the samemanner as the payment or receipt of charges or fees in businesstransactions between independent enterprises. Where the payment or receiptof charges or fees is not made in the same manner as in businesstransactions between independent enterprises and results in a reduction of the taxable income, the tax authorities shall have the right to makereasonable adjustment.Article 14Where an enterprise with foreign investment or an establishment or a placeset up in China by a foreign enterprise to engage inproduction orbusiness operations is established, moves to a new site, merges withanother enterprise, breaks up, winds up or makes a change in any of themain entries of registration, it shall present the relevant documents to and go through tax registration or a change or cancellation inregistration with the local tax authorities after the relevant event is registered, or a change or cancellation in registration is made with the administrative agency for industry and commerce.Article 15Income tax on enterprises and local income tax shall be computed on anannual basis and paid in advance in quarterly instalments. Such paymentsshall be made within fifteen days from the end of each quarter and thefinal settlement shall be made within five months from the end of each taxyear. Any excess payment shall be refunded and any deficiency shall berepaid.Article 16Any enterprise with foreign investment and any establishment or place setup in China by a foreign enterprise to engage in production or businessoperations shall file its quarterly provisional income tax return inrespect of advance payments with the local tax authorities within theperiod for each advance payment of tax, and it shall file an annual income tax return together with the final accounting statements within fourmonths from the end of the tax year.Article 17Any enterprise with foreign investment and any establishment or place setup in China by a foreign enterprise to engage in production or businessoperations shall report its financial and accounting systems to the local tax authorities for reference. All accounting records must be complete and accurate, with legitimate vouchers as the basis for entries.If the financial and accounting bases adopted by an enterprise withforeign investment and an establishment or a place set up in China by aforeign enterprise to engage in production or business operationscontradict the relevant regulations on tax of the State Council, taxpayment shall be computed in accordance with the relevant regulations ontax of the State Council.Article 18When any enterprise with foreign investment goes into liquidation, and ifthe balance of its net assets or the balance of its remaining propertyafter deduction of the enterprise's undistributed profit, various funds and liquidation expenses exceeds the enterprise's paid-in capital, theexcess portion shall be liquidation income on which income tax shall bepaid in accordance with the provisions of this Law.Article 19Any foreign enterprise which has no establishment or place in China butderives profit, interest, rental, royalty and other income from sources in China, or though it has an establishment or a place in China, the saidincome is not effectively connected with such establishment or place,shall pay an income tax of twenty percent on such income. For the paymentof income tax in accordance with the provisions of the precedingparagraph, the income beneficiary shall be the taxpayer and the payershall be the withholding agent. The tax shall be withheld from the amountof each payment by the payer. The withholding agent shall, within fivedays, turn the amount of taxes withheld on each payment over to the StateTreasury and submit a withholding income tax return to thelocal taxauthorities.Income tax shall be exempted or reduced on the following income: (1) the profit derived by a foreign investor from an enterprise withforeign investment shall be exempted from income tax;(2) income from interest on loans made to the Chinese government orChinese State banks by international financial organizations shall beexempted from income tax;(3) income from interest on loans made at a preferential interest rate to Chinese State banks by foreign banks shall be exempted from income tax; and(4) income tax of the royalty received for the supply of technical know-how in scientific research, exploitation of energy resources, developmentof the communications industries, agricultural, forestry and animalhusbandry production, and the development of important technologies may,upon approval by the competent department for tax affairs under the StateCouncil, be levied at the reduced rate of ten percent. Where thetechnology supplied is advanced or the terms are preferential, exemptionfrom income tax may be allowed.Apart from the aforesaid provisions of this Article, if preferentialtreatment in respect of reduction of or exemption from income tax onprofit, interest, rental, royalty and other income is required, it shallbe regulated by the State Council.Article 20The tax authorities shall have the right to inspect the financial,accounting and tax affairs of enterprises with foreign investment andestablishments or places set up in China by foreign enterprises to engagein production or business operations, and have the right to inspecttaxwithholding of the withholding agent and its payment of the withheld taxinto the State Treasury. The entities and the withholding agents being so inspected must report the facts and provide relevant information. They maynot refuse to report or conceal any facts.When making an inspection, the tax officials shall produce their identity documents and be responsible for confidentiality.Article 21Income tax payable according to this Law shall be computed in terms ofRenminbi (RMB). Income in foreign currency shall be converted intoRenminbi according to the exchange rate quoted by the State exchangecontrol authorities for purposes of tax payment.Article 22If any taxpayer fails to pay tax within the prescribed time limit, or if the withholding agent fails to turn over the tax withheld within theprescribed time limit, the tax authorities shall, in addition to setting anew time limit for tax payment, impose a surcharge for overdue payment,equal to 0.2 percent of the overdue tax for each day in arrears, starting from the first day the payment becomes overdue.Article 23The tax authorities shall set a new time limit for registration orsubmission of documents and may impose a fine of five thousand yuan orless on any taxpayer or withholding agent which fails to go through taxregistration or make a change or cancellation in registration with the tax authorities within the prescribed time limit, or fails to submit incometax return, final accounting statements or withholding income tax returnto the tax authorities within the prescribed time limit, or fails toreport its financial and accounting systems to the tax authorities forreference. Where the tax authorities have set a new time limit forregistration or submission of documents, they shall impose a fine of tenthousand yuan or less on the taxpayer or withholding agent which againfails to meet the time limit for going through registration or making achange in registration with the tax authorities, or for submitting income tax return, final accounting statements or withholding income tax returnto the tax authorities. Where the circumstances are serious, the legalrepresentative and the person directly responsible shall be investigatedfor criminal responsibility by applying mutatis mutandis the provisions of Article 121 of the Criminal Law.Article 24Where the withholding agent fails to fulfil its obligation to withhold tax as provided in this Law, and does not withhold or withholds an amount lessthan that should have been withheld, the tax authorities shall set a time limit for the payment of the amount of tax that should have beenwithheld,and may impose a fine up to but not exceeding one hundred percent of theamount of tax that should have been withheld. Where the withholding agentfails to turn the tax withheld over to the State Treasury within theprescribed time limit, the tax authorities shall set a time limit for turning over the taxes and may impose a fine of five thousand yuan or lesson the withholding agent; if the withholding agent fails to meet the time limit again, the tax authorities shall pursue the taxes according to law and may impose a fine of ten thousand yuan or less on the withholdingagent. If the circumstances are serious, the legal representative and the person directly responsible shall be investigated for criminalresponsibility by applying mutatis mutandis the provisions of Article 121of the Criminal Law.Article 25Where any person evades tax by deception or concealment or fails totax within the time limit prescribed by this Law and, after the taxauthorities pursued the payment of tax, fails again to pay it within the prescribed time limit, the tax authorities shall, in addition torecovering the tax which should have been paid, impose a fine up to butnot exceeding five hundred percent of the amount of tax which should havebeen paid. Where the circumstances are serious, the legal representativeand the person directly responsible shall be investigated for criminalresponsibility in accordance with the provisions of Article 121 of theCriminal Law.Article 26Any enterprise with foreign investment, foreign enterprise or withholdingagent, in case of a dispute with the tax authorities on payment ofmust pay tax according to the relevant regulations first. Thereafter, the taxpayer or withholding agent may, within sixty days from the date ofreceipt of the tax payment certificate issued by the tax authorities,apply to the tax authorities at the next higher level for reconsideration. The higher tax authorities shall make a decision within sixty days afterreceipt of the application for reconsideration. If the taxpayer orwithholding agent is not satisfied with the decision, it may institutelegal proceedings in the people's court within fifteen days from the date of receipt of the notification on decision made after reconsideration.If the party concerned is not satisfied with the decision on punishment by the tax authorities, it may, within fifteen days from the date of receiptof the notification on punishment, apply for reconsideration to the taxauthorities at the next higher level than that which made the decision on punishment. Where the party is not satisfied with the decision made afterreconsideration, it may institute legal proceedings in the people's court within fifteen days from the date of receipt of the decision made afterreconsideration. The party concerned may, however, directly institutelegal proceedings in the people's court within fifteen days from the date of receipt of the notification on punishment. If the party concernedneither applies for reconsideration to the higher tax authorities, norinstitutes legal proceedings in the people's court within the time limit, nor complies with the decision on punishment, the tax authorities whichmade the decision on punishment may apply to the people's court forcompulsory execution.Article 27Where any enterprise with foreign investment which was established beforethe promulgation of this Law would, in accordance with the provisions ofthis Law, otherwise be subject to higher tax rates orenjoy lesspreferential treatment of tax exemption or reduction than before the entry into force of this Law, in respect to such enterprise, within its approved period of operation, the law and relevant regulations of the State Council in effect before the entry into force of this Law shall apply. If any such enterprise has no approved period of operation, the law and relevantregulations of the State Council in effect before the entry into force of this Law shall apply within the period prescribed by the State Council. Specific measures shall be drawn up by the State Council.Article 28Where the provisions of a tax agreement concluded between the governmentof the People's Republic of China and a foreign government are differentfrom the provisions of this Law, the provisions of the agreement shallprevail.Article 29Rules for implementation shall be formulated by the State Council inaccordance with this Law.Article 30This Law shall enter into force on July 1, 1991. The Income Tax Law of thePeople's Republic of China for Chinese-Foreign Equity Joint Ventures andthe Income Tax Law of the People's Republic of China for ForeignEnterprises shall be annulled as of the same date.。

China Income tax law

中华人民共和国企业所得税法2007更新日期:2008-4-8 18:37:00 出处:乐趣园作者:老西 .3610891转载请声明出处8正8方8翻8译8网.5229762中华人民共和国主席令第63号Order of the President of the People's Republic of China No. 63《中华人民共和国企业所得税法》已由中华人民共和国第十届全国人民代表大会第五次会议于2007年3月16日通过,现予公布,自2008年1月1日起施行。

中华人民共和国主席胡锦涛二○○七年三月十六日The Enterprise Income Tax Law of the People's Republic of China has been adopted at the 5th Session of the 10th National People's Congress of the People's Republic of China on March 16, 2007. It is hereby promulgated and shall go into effect as of January 1, 2008. President of the People's Republic of China Hu Jintao March 16, 2007中华人民共和国企业所得税法(2007年3月16日第十届全国人民代表大会第五次会议通过)Enterprise Income Tax Law of the People's Republic of China (Adopted at the 5th Session of the 10th National People's Congress of the People's Republic of China on March 16, 2007)目录Contents第一章总则Chapter I General Rules第二章应纳税所得额Chapter II Taxable Income Amount第三章应纳税额Chapter III Payable Tax Amount第四章税收优惠Chapter IV Preferential Tax Treatments第五章源泉扣缴Chapter V Withholding by Sources第六章特别纳税调整Chapter VI Special Adjustments to Tax Payments第七章征收管理Chapter VII Administration of Tax Levy第八章附则Chapter VIII Supplementary Rules第一章总则Chapter I General Rules第一条在中华人民共和国境内,企业和其他取得收入的组织(以下统称企业)为企业所得税的纳税人,依照本法的规定缴纳企业所得税。

法律英语词汇大全【下】

法律英语词汇大全【下】法律英语词汇大全【下】法律英语词汇大全【上】Ssabotage 蓄意破坏,怠工蓄意破坏,怠工sacrilege 渎圣,冒渎渎圣,冒渎sadism 虐待狂虐待狂safety inspection (auto) (汽车)安全检查 (汽车)安全检查safety regulation 安全规则安全规则sale of a child 贩卖儿童贩卖儿童sanction 制裁制裁sane 神志正常神志正常scapegoat 替罪羊替罪羊scene of crime 作案现场作案现场search and seizure 搜查与充公搜查与充公search warrant 搜查令搜查令secret agent 特务,特工特务,特工Secret Service 特勤部特勤部security fraud 证券欺诈证券欺诈sedition 煽动叛乱煽动叛乱self determination 自决自决self incrimination 自证其罪,自我牵连自证其罪,自我牵连self-defense 自卫自卫sensitive 敏感的敏感的sentence 判刑判刑separation agreement 分居协议分居协议sequester a jury 隔离陪审团隔离陪审团serve a subpoena 送达传票送达传票serve papers on a party 送交文件给某方送交文件给某方set bail 定保释金额定保释金额sever case 将案件分离将案件分离sexual abuse 性虐待性虐待sexual assault 性侵犯性侵犯shackles 手铐,脚镣手铐,脚镣sheriff (县)警长 (县)警长shoplifting 入店行窃入店行窃shotgun 散弹枪,猎枪散弹枪,猎枪sidewalk 人行道人行道sight translation 视译视译simultaneous interpretation 同声传译同声传译skid row 贫民区街道,没落地段贫民区街道,没落地段slander 诽谤诽谤slavery 奴隶制奴隶制slip and fall 滑倒滑倒slugs 假硬币,子弹假硬币;子弹smuggling 走私走私snowmobile 雪车雪车sodomy 鸡奸,兽奸鸡奸,兽奸solicitation 教唆,拉客教唆,拉客solicitor 法务官法务官special agent 特务,特工特务,特工specification 规格规格speedy trial 快速审理快速审理squatter 擅自居住,擅自占地擅自居住,擅自占地stalking 潜行追踪潜行追踪standard weights 砝码砝码standards 标准标准status quo 现状现状statute 法规法规statute of limitation 时效法规时效法规statutory law 成文法,制定法成文法,制定法statutory rape 制定法上的强奸制定法上的强奸stay a warrant 中止刑事手令中止刑事手令stay of execution 延缓执行死刑延缓执行死刑sting operation (为捉拿疑犯所设置的)突击圈套 (为捉拿疑犯所设置的)突击圈套stipulation 规定,协议规定,协议strangulation 勒死,掐死,绞死勒死,掐死,绞死strike from the record 从记录中删除从纪录中删除subject to prosecution 可被公诉可被公诉suborn perjury 唆使提供伪证唆使提供伪证submit evidence 提出证据提出证据subpoena 传票传票substance abuse 滥用药物滥用药物substance abuse prevention 防止滥用药物的措施防止滥用药物的措施substantive count 实质罪项实质罪项substantive law 实体法,主法实体法,主法sue 起诉,打官司起诉,打官司suit 诉讼诉讼summary judgment 即决审判即决审判suppress evidence 压制证据压制证据supreme court 最高法院最高法院surcharge 附加费附加费surrogate parenthood 代父母身份代父母身份surveillance 监视监视susceptible 易受影响的易受影响的suspect 犯罪嫌疑人,疑犯犯罪嫌疑人suspended license 暂时吊销执照暂时吊销执照suspended sentence 缓刑缓刑swear to tell the truth 发誓说实话发誓说实话sworn testimony 宣誓作证宣誓作证syndicate 犯罪集团犯罪集团Ttacit approval 默许默许take issue 提出异议,反对提出异议take the stand 到证人席作证,出庭作证到证人席作证,出庭作证tampering with a witness 干扰证人干扰证人tampering with evidence 损坏证据损坏证据tampering with jury 干预陪审团干预陪审团tariff 关税关税tax advantage 有利税率有利税率tax deduction 减税减税tax evasion 逃税逃税tax exempt 免税免税tax fraud 税务行骗税务行骗tax in kind 实物税,以实物缴纳的税实物税,以实物缴纳的税tax law 税法税法tax rate 税率税率tax return 税表,报税单税表,报税单tax shelter 合法避税手段合法避税手段telecommunications fraud 电信行骗电信行骗telephone fraud 电话行骗电话行骗temporary restraining order 暂时禁令暂时禁令temporary insanity 暂时性精神错乱暂时性精神错乱tenor (gist) 要旨,大意要旨,大意tentative 暂定的暂定的terrorism 恐怖主义恐怖主义terrorist 恐怖分子恐怖分子testify under oath/affirmation 宣誓作证宣誓作证testimony 证词证词the people 人民,公诉人人民,公诉人threatening elected officials 威胁公选官员威胁公选官员time off for good behavior 因表现良好而减刑因表现良好而减刑time served 已服刑期已服刑期tobacco product warning 烟草产品警告烟草产品警告tort 民事侵权行为民事侵权行为towing regulation 拖车规定拖车规定trade names 商品/商号/商业名称商品/商号/商业名称trademark 商标商标traffic citation 交通罚单交通罚单traffic court 交通法庭交通法庭trafficking in 非法贩卖非法贩卖transcript 记录抄本纪录抄本transliteration 音译音译trespassing 擅自进入擅自进入trial 审讯审讯trial on merit 实体审判实体审判trier of fact 事实的审判者事实的审判者truancy 旷课,逃学,旷工旷课,逃学,矿工truant officer 调查旷课/旷工的官员调查旷课/矿工的官员true bill 大陪审团签署的起诉书大陪审团签署的起诉书true copy 准确的副本准确的副本trumped up charge 诬告,无中生有诬告,无中生有truthful statement 真实声明真实声明twist (the facts) 歪曲事实歪曲事实Uulterior motive 别有用心,另有动机别有用心,另有动机un alienable right 不容剥夺的权利不容剥夺的权利unanimous verdict 全体一致的判决全体一致的判决unconstitutional 违宪的违宪under advisement, take 会考虑周全会考虑周全under oath 宣过誓宣过誓under penalty of 处以……的惩罚处以….的惩罚undermine 暗中破坏暗中破坏underwrite 承保,负责保险,负责支付承保,负责保险,负责支付unfair competitive practice 不公平竞争不公平竞争uniform 一律,一致,统一;制服一律,一致,统一;制服uniform crime reporting 统一的罪案报告方式统一的罪案报告方式unit (police) (警察)小组,警车 (警察)小组,警车unlawful handling of 非法处理非法处理unlawful retention 非法拘留非法拘留unlawful sexual intercourse 非法性交非法性交unloaded weapon 没装弹药的枪械没装弹药的枪械unpremeditated crime 非预谋罪行非预谋罪行uphold verdict 维持原判维持原判urine test 尿液测试尿液测试use of force 使用武力\暴力使用武力/暴力usurpation 篡夺,非法使用篡夺,非法使用usury 高利贷高利贷utter 行使伪造物行使伪造物utility theft 盗窃公用设备\设施盗窃公用设备/设施U-turn 汽车调头\回转汽车调头/回转Vvacate 搬出;撤销搬出;撤销vagrancy 流浪流浪validation 批准,证实,使生效批准,证实,使生效vandalism 肆意破坏财产肆意破坏财产vehicular homicide 车祸致死车祸致死vendetta 世仇,家族仇杀世仇venereal disease 性病性病venue 审判地点审判地点verbal agreement 口头协议口头协议verbatim 咬文嚼字咬文嚼字verdict 判决,裁决判决,裁决vested rights 既定权利,应有权利既定权利,应有权利veto 否决否决vice 恶性恶性vice squad 警察缉捕队,刑警队警察缉捕队victim 受害者受害者victim"s right 受害者的权利受害者的权利vigilance 警惕,防范警惕,防范vigilante 民间警戒行动者,民间治安维持者民间警戒行劫者,民间治安维持者villain 恶棍恶棍vindication 证实无罪,证实清白证实无罪,证实清白vindictive punishment 报复性惩罚报复性惩罚vintage vehicle 古董车古董车violent crime 暴力罪行暴力罪行visitation 探亲,探视;临检探亲,探视;临检vulgarity 粗鄙粗鄙vulnerability 弱点,易受伤害弱点,易受伤害vulture 贪婪而残酷的人贪婪而残酷的人Wwaive rights 放弃权利放弃权利waive time 放弃时限权利放弃时限权利waiver of rights 弃权书弃权书wanton (willful or reckless) 任性,肆意,肆无忌惮任性,肆意,肆无忌惮wanton negligence 任意过失任意过失war crimes 战争罪行战争罪行ward of the court 受法院监护的任受法院监护的任warden 监狱长监狱长warning lights 警告灯警告灯warning sign 警告标志警告标志warrant 法令,逮捕证,搜查证法令,逮捕证,搜查证warranty 保单,担保保单,担保water rights 用水权用水权weapon 武器武器whereabouts 下落下落white supremacy 白人种族至上主义白人种族至上主义wildlife 野生动植物野生动植物will 遗嘱遗嘱wire tap 窃听电话窃听电话withdraw 撤回,撤销撤回,撤销with prejudice 有偏见有偏见without prejudice 无偏见无偏见witness of the defense 辨方证人辩方证人witness of the prosecution 控方证人控方证人work furlough 暂准狱外工作暂准监外工作work release 白天监外工作白天监外工作writ 书面命令,传票书面命令,传票wrongful act 不法行为,不当行为不法行为,不当行为Xxenophile 崇洋迷外崇洋迷外xenophobe 仇外仇外X-rated film 色情电影色情电影Yyes/no question 是非问题是非问题yield 让步,屈服让步,屈服youth authority 少年罪犯管理机构少年罪犯管理机构Zzealot 狂热,过分热心狂热,过分热心zoning 城市区划城市区划。

Unit 4 税法 Taxation Law

Unit 4 税法Taxation LawUnit 4 税法 Taxation Law1.企业所得税 Corporate Income Tax(1)符合条件的技术转让所得 Income from qualified transfer of technology企业所得税法称符合条件的技术转让所得免征、减征企业所得税,是指一个纳税年度内,居民企业转让技术所有权所得不超过500万元的部分,免征企业所得税;超过500万元的部分,减半征收企业所得税。

The income from qualified transfer of technology eligible for tax exemption or tax reduction refers to the part of income from qualified transfer of technology that is no more than 5 million yuan is eligible for tax exemption and the part that exceed 5 million yuan is subject to income tax with a reduction of 50%.(2)高新技术企业优惠 High and new technology Enterprises国家需要重点扶持的高新技术企业减按15%的税率征收企业所得税。

High and new technology enterprises that require key state support are subject to the applicable enterprise income tax rate of 15%.(3)研究开发费 Research and development expenses研究开发费是指企业为开发新技术、新产品、新工艺发生的研究开发费用,未形成无形资产计入当期损益的,在按照规定据实扣除的基础上,按照研究开发费用的50%加计扣除;形成无形资产的,按照无形资产成本的150% 摊销。

常用税收词汇中英文对照

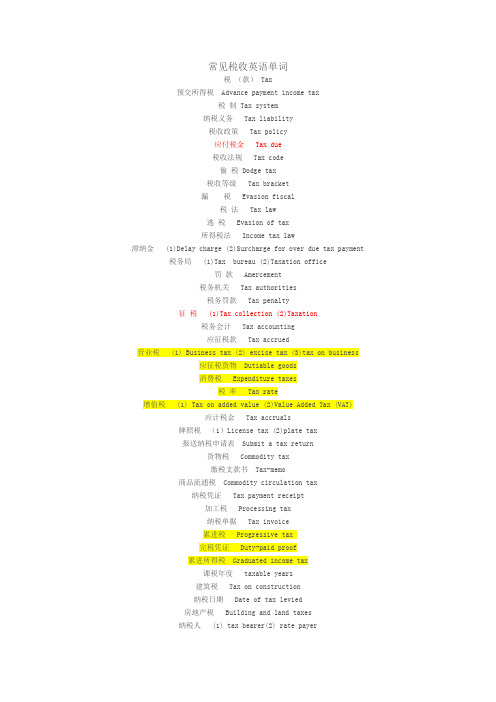

常见税收英语单词税(款) Tax预交所得税Advance payment income tax税制 Tax system纳税义务 Tax liability税收政策 Tax policy应付税金 Tax due税收法规 Tax code偷税 Dodge tax税收等级 Tax bracket漏税 Evasion fiscal税法 Tax law逃税 Evasion of tax所得税法 Income tax law滞纳金 (1)Delay charge (2)Surcharge for over due tax payment 税务局 (1)Tax bureau (2)Taxation office罚款 Amercement税务机关 Tax authorities税务罚款 Tax penalty征税 (1)Tax collection (2)Taxation税务会计 Tax accounting应征税款 Tax accrued营业税 (1) Business tax (2) excise tax (3)tax on business应征税货物Dutiable goods消费税 Expenditure taxes税率 Tax rate增值税 (1) Tax on added value (2)Value Added Tax (VAT)应计税金 Tax accruals牌照税(1)License tax (2)plate tax报送纳税申请表Submit a tax return货物税 Commodity tax缴税支款书Tax-memo商品流通税Commodity circulation tax纳税凭证 Tax payment receipt加工税 Processing tax纳税单据 Tax invoice累进税 Progressive tax完税凭证 Duty-paid proof累进所得税Graduated income tax课税年度 taxable years建筑税 Tax on construction纳税日期 Date of tax levied房地产税 Building and land taxes纳税人 (1) tax bearer(2) rate payer城市建设税City planning tax多缴税款 Tax overpaid所得税 Income tax退税 (1)drawback from duties paid(2)refund of关税(海关)Customs申请退还税金Application for drawback附加税 Additional tax应退税款 Refundable tax资源税 Resource tax退税通知书Notice of refund采掘税 Severance tax减税 (1) tax reduction (2)tax cut养路税 Highway maintenance tax免税品 Non-dutiable goods销售税 Tax on sales减免税 Tax reliefs消费税 Tax on consumption免税 (1)tax free (2)duty free资产税 Tax on captital免收税款 Waive duty财产税 Property tax税收减让 (1) tax concession(2)tax abatement固定资产税Fix assets tax免税货物 Duty free goods奢侈税 Tax on superfluity进口免税 Exemption from duty个所得税Personal incom人e tax免税期 Tax holiday应缴所得税Income tax payable印花税票 Adhesive revenue stamp应纳税工资额taxable salary贴用印花 Affix revenue stamps暂定税金 Tentative tax保税货物 Goods in bonds税务员(1)tax staff (2)tax gather[/hide]。

法律英语词汇大全【下】

法律英语词汇大全【下】法律英语词汇大全【下】法律英语词汇大全【上】Ssabotage蓄意破坏,怠工蓄意破坏,怠工sacrilege 渎圣,冒渎渎圣,冒渎sadi 狂狂safety inspection(auto) (汽车)安全检查(汽车)安全检查safety regulation安全规则安全规则sale of a child 贩卖儿童贩卖儿童sanction制裁制裁sane神志正常神志正常scapegoat 替罪羊替罪羊scene of crime 作案现场作案现场searchand seizure 搜查与充公搜查与充公search warrant 搜查令搜查令secret agent ,特工,特工Secret Service 特勤部特勤部securityfraud 证券欺诈证券欺诈sedition 煽动叛乱煽动叛乱self determination自决自决self incrimination 自证其罪,自我牵连自证其罪,自我牵连self-defense 自卫自卫sensitive敏感的敏感的sentence判刑判刑separation agreement 协议协议seuester a jury隔离陪审团隔离陪审团serve asubena送达传票送达传票serve papers onaparty送交文件给某方送交文件给某方set bail定保释金额定保释金额sever case将案件分离将案件分离ualabuse性性ual assault性侵犯性侵犯shackles 手铐,脚镣手铐,脚镣sheriff (县)警长(县)警长shoplifting入店行窃入店行窃shotgun 散弹,猎散弹,猎sidewalk 人行道人行道sight translation 视译视译s**ltaneousinterpretation同声传译同声传译skid row贫民区街道,没落地段贫民区街道,没落地段slander诽谤诽谤slery制制slip andfall滑倒滑倒slugs假硬币, 假硬币;ugglingsnowbile 雪车雪车sodomy 鸡,兽鸡,兽solicitation 教唆,拉客教唆,拉客solicitor法务法务special agent,特工,特工specification 规格规格speedy trial 快速审理快速审理suatter擅自居住,擅自占地擅自居住,擅自占地stalking潜行追踪潜行追踪standard weights 砝码砝码standards 标准标准status uo现状现状statute 法规法规statute of limitation时效法规时效法规statutory law 成文法,制定法成文法,制定法statutory rape制定法上的强制定法上的强stay a warrant中止刑事手令中止刑事手令stayof execution延缓执行死刑延缓执行死刑stingoperation(为捉拿疑犯所设置的)突击圈套(为捉拿疑犯所设置的)突击圈套st**lation 规定,协议规定,协议strangulation 勒死,掐死,绞死勒死,掐死,绞死strike from the record从记录中删除从纪录中删除subject to prosecution 可被公诉可被公诉suborn perjury唆使提供伪证唆使提供伪证submit evidence 提出证据提出证据subena 传票传票substance abuse 滥用药物滥用药物substance abuse prevention 防止滥用药物的措施防止滥用药物的措施 substantivecount 实质罪项实质罪项substantive law实体法,主法实体法,主法sue 起诉,打司起诉,打司suit 诉讼诉讼summary judgment 即决审判即决审判suppress evidence压制证据压制证据supreme court最高XX 最高XXsurrge 附加费附加费surrogate parenthood 代父母身份代父母身份surveillance监视监视susceptible 易受影响的易受影响的suspect犯罪嫌疑人,疑犯犯罪嫌疑人suspended license 暂时吊销执照暂时吊销执照suspended sentence 缓刑缓刑swear to tell the truth发誓说实话发誓说实话sworn testiny宣誓作证宣誓作证syndicate犯罪集团犯罪集团Ttacit approval默许默许take issue提出异议,反对提出异议take the stand到证人席作证,出庭作证到证人席作证,出庭作证 tampering with a witness 干扰证人干扰证人tampering withevidence 损坏证据损坏证据tampering with jury 干预陪审团干预陪审团tariff关税关税tax advantage 有利税率有利税率tax deduction 减税减税tax evasion逃税逃税tax exempt 免税免税tax fraud税务行骗税务行骗tax in kind实物税,以实物缴纳的税实物税,以实物缴纳的税tax law税法税法tax rate税率税率tax return税表,报税单税表,报税单tax shelter 合法避税手段合法避税手段telemucationsfraud 行骗行骗telephone fraud 电话行骗电话行骗temraryrestraing order暂时暂时temraryinsaty 暂时性精神错乱暂时性精神错乱tenor (gist) 要旨,大意要旨,大意tentative暂定的暂定的terrori恐怖主义恐怖主义terroristtestify under oath/affirmation宣誓作证宣誓作证testiny证词证词the people人民,公诉人人民,公诉人threatengelected officials 威胁公选员威胁公选员timeoff for good behior因表现良好而减刑因表现良好而减刑 time served已服刑期已服刑期tobacco product warng 烟草产品烟草产品tort 民事侵权行为民事侵权行为towing regulation拖车规定拖车规定trade names商品/商号/商业名称商品/商号/商业名称trademark商标商标traffic citation 罚单罚单traffic court法庭法庭trafficking in 非法贩卖非法贩卖transcript 记录抄本纪录抄本transliteration音译音译trespassing 擅自进入擅自进入trial 审讯审讯trial on merit 实体审判实体审判trier of fact 事实的审判者事实的审判者truancy 旷课,逃学,旷工旷课,逃学,矿工truant officer调查旷课/旷工的员调查旷课/矿工的员truebill 大陪审团签署的起诉书大陪审团签署的起诉书true copy 准确的副本准确的副本trumped up rge 诬告,无中生有诬告,无中生有truthful statement 真实声明真实声明twist (the facts) 曲事实曲事实Uulterior tive别有用心,另有动机别有用心,另有动机unalienable right不容剥夺的权利不容剥夺的权利unaus verdict 全体一致的判决全体一致的判决unconst**tional违宪的违宪under advisement, take 会考虑周全会考虑周全under oath 宣过誓宣过誓under penalty of处以的处以。

China Corporate Income Tax Law

China Corporate Income Tax Law1 Chinese Law1.1China Corporate Income Tax Law" People's Republic of China Corporate Income Tax Law " is a law which is used to make the Chinese domestic enterprises and other organizations to obtain income to pay corporate income tax law. The current law was revised and promulgated on the fifth meeting of General Assembly of the Tenth National People's Congress on March 16, 2007 by the People's Republic of China. It went into effect on January 1, 2008. At present, the corporate income tax in our country occupies more than 75% of the income tax revenue of our country.Basically, the development of the corporate income tax in China experienced three stages. The first stage is in the early 1980s, the second stage is from the middle 1980s to late 1980s, the last stage is from 1990s to nowadays. In the first stage, China set up the system and the law of the income tax, including the personal income tax, domestic corporate tax, and the Sino-foreign joint venture income tax. In the second stage, China set up the state-owned enterprises income tax system in our country, set up a private enterprise income tax system, and perfected the system of collective enterprise income tax. in the last stage, China uphold the principle of the unity government in our country, the fair tax burden, simplifying the tax system, and promoting competition. Meanwhile, china has completed the unification of the foreign capital enterprise income tax law, the unity of the domestic enterprise income tax law, and the unity ofthe individual income tax law, the longevity of the tax law to the new enterprise income tax in 2008, realized the unification of the domestic and foreign enterprise income tax law.1.2Basic information about China corporate income tax.Our country corporate income tax object can be divided into two categories, one kind is resident, impose their worldwide income. Another kind is a non-resident enterprise, and impose its income in China. According to the newly revised corporation income tax law in 2008, we use the flat rate. Our country corporate income tax rate is 25%, conform to the conditions of small miniature enterprise, the corporate income tax rate is 20%. For a non-resident enterprise, if it has no agencies or set up institutions in China, and obtains the source has nothing to do with institutions of income. Its income from China’ part is applied to the tax rate of 20%, but be levied at a reduced 10%. Conform to the conditions of the state council and approved by the new and high technology industries, they have the corporate income tax rate is 15%. In addition, the characteristics of the corporate income tax in China mainly include: (1) the taxable income tax basis;(2) the process of calculating the taxable income amount is complicated;(3) the amount can be a burden, the more income, the more tax, while the less income, the less tax. (4) pay the tax yearly, but can prepay monthly or quarterly.2 American Law2.1 American Corporate Income TaxCorporate income tax is imposed at the federal level[1]. on all entities treated as corporations (see Entity classification below), and by 47 states and the District of Columbia. Certain localities also impose corporate income tax. Corporate income tax is imposed on all domestic corporations and on foreign corporations having income or activities within thejurisdiction. For federal purposes, an entity treated as a corporation and organized under the laws of any state is a domestic corporation. [2]For state purposes, entities organized in that state are treated as domestic, and entities organized outside that state are treated as foreign. [3] 2.2Basic information about American corporate income tax.Here is the chart [4] of the federal American corporate income tax.According to the chart, we know, the tax rate of the American corporate income tax is from 15% to 35 % and using the extra progressive tax rate.3Comparison of the law between America and China3.1 Different Develop of the Corporate Income Tax in HistoryCompared to income tax in China and the United States of the development process, it is not hard to find, America setting up and developing the system of income tax is earlier than the China’s system, and it is nearly half a century in advance. America's corporate income taxemerged and developed in the 1920 s, and in the 80 s became the main tax revenue. In America, the country's corporate income tax is implemented the unified tax inside and outside in the 1990s. In addition, the United States claims that the principle of separation of powers—federalism, is the reason that the income tax system in the United States reflects the combination of democratic principles and the principle of separation of powers. This makes the United States once the corporate income tax reform, can very good and widely recognized, applied at the same time. the income tax revenue also began to make up most of the national fiscal revenue. In today, the corporate income tax system in America is going to be the most perfect system in world, and can be very good to the development as time goes by. Compared with America, the earliest Chinese income tax system is used for the needs of the control class to rule the country, so China's income tax legislation lacks democratic decision-making process, as well as the adaptability and scientific. Although, after the reform and opening-up policy, our country income tax system as learnt a lot from abroad, and has become increasingly perfect. But, in contrast to the United States, China's nearly seventy years behind the America in the income tax law’s establishing, revising and developing. Although, the first time establishing the income tax in two countries in the history had a difference with only fifty years. However, after that our country has been falling behind for 20 years, therefore, our country income tax system still has a lot of space to develop.3.2 Different Tax RateThe corporate income tax rate in China is below 25% and the maximum is 25%, with the flat rate. However, America uses the extra progressive tax rate, and the rate is from 15% to 35%. Meanwhile, America has two or three level of corporate income tax. So combining the local andstate level corporate income tax, we can find the average corporate income tax in America is quite high, and sometimes, it may be higher than China. The United States has the third highest general top marginal corporate income tax rate in the world at 39.1 percent, exceeded only by Chad and the United Arab Emirates. [5]Actually, the different tax rate is because of the economic growth and the country structure. For China is a developing country, we using the flat rate and lower rate to improve our economic and the precise our income tax system. meanwhile, we all know china a is a power- centralized country, so we only using one tax rate across the whole country. On the contrary, America is a federalism country, and according to their federal constitution, federal has no power on the state taxation, as a result, America has a relatively high tax rate, for the company in the different states have to pay different rate of the sates level tax and the federal level at the same time. In addition, America is developed country, and most developed countries using the progressive rate instead of flat rate. To be honest, progressive rate is more complicated than the flat rate but much more fair and equity.3.3 Different Tax Revenue proportionIn china, corporate tax is a heavy part of Chinese tax revenue. As I mentioned before, the corporate income tax in our country occupies more than 75% of the income tax revenue of our country. However, at the federal level, it is different. The biggest single tax is federal individual income tax, the second is the social insurance tax, and the third is the corporate income tax. America only levy the “S” corporation for the corporate income tax, and this corporation only occupies 25% of the total amount of companies. So clearly, that is the reason why the American corporate income tax does not have the same proportion as China has.3.4 Different Tax Problem in These Two CountriesIn China, the mainly problem of the corporate income tax is the incentive policies, there are not too much polices and government using the policy to control the market, as a result there is not a relatively freedom market as the America. However, America has a quite free market, and has an important problem, “race to bottom”. The state level corporate income tax may compete extremely. State government usually like to use tax package to attract big company. For example, the state of Illinois using the Tax package—a combination of the property tax credits, personal tax credits and corporate tax credits, to land the headquarter of the Boeing company in Chicago. And some states even like to eliminate the corporate income tax, and leads some important results, for instance, the deficit on budget. According to a report, the state of Virginia had a 2.6 billions deficit in the fiscal year 2015, and the deficit will expand in the future 3 years.4The Policy from the Chinese Corporate Income TaxThe CIT regime adopts the “predominantly industry-oriented, limited geography-based” tax incentive policy. Key emphasis is placed on “industry-oriented” incentives aiming at directing investments into those industry sectors and projects encouraged and supported by the State. The tax incentive policies mainly include the tax reduction, deductible tax rate, and so on [6].Tax reduction and exemption in the following program, as the chart shows. [7]China still have the policy of tax rate reduction.IC production enterprises with a total investment exceeding RMB8 billion, or which produce integrated circuits with a line-width of less than 0.25um are applicable to the reduced CIT rate of 15%.Key software enterprises and IC design enterprises are eligible for a reduced CIT rate of 10%. An enterprise has to fulfill a set of prescribed criteria and be subject to an assessment in order to qualify as a key software enterprise or key IC design enterprise.From 1 January 2009 to 31 December 2018, qualified technology- advanced service enterprises in 21 cities (such as Beijing, Shanghai, Tianjian, Guangzhou, Shenzhen, etc.) are applicable to a reduced CIT rate of 15%.All these policies are the law of complementariness. In China, we can find the policies are mainly focusing on the small business and high tech business, which shows the country is encouraging the company and industries to develop high tech, and change the company from traditional industry to high tech, long-lasting industry. All the policies are ideal, and rational but not benefit the large group people, so it may have some equity problem in the income tax system.5ConclusionAccording to the comparison and the background, policy of the corporate income tax in these two countries, we find both countries have their own rational income tax law andsystem, while both systems have some problems. Meanwhile, I think China can learn from the America to promote the freedom market competition and create a relatively equity and fair tax systems.Reference and BibliographyREFERENCE[1] Subtitle A of Title 26 of the United States Code, in particular 26 U.S.C. § 11, § 881, and § 882. For a thorough overview of federal income taxation of corporations, see Internal Revenue Service Publication 542, Corporations. See also Willis Hoffman chapters 17-20, Pratt & Kulsrud chapters 19–21, Fox chapter 30 (each fully cited under Further reading). For purely corporate tax matters, the Bittker & Eustice treatise cited fully under Treatises is authoritative and has been cited by the Supreme Court.[2] 26 U.S.C. § 7701(a)(4). Note that a sham entity may be ignored. See Pratt & Kulsrud 2005 p. 19-4.[3] See, e.g., New York State Publication 20, Tax Guide for Business, page 8.[4] Form 1120 Instructions for 2015 page 17[5] Puzzanghera, Jim (15 December 2015). "Corporate Income Tax Rates around the World, 2014". . Retrieved 28 December 2012.[6] [7] PricewaterhouseCoopers Consultants. (2015). The People’s Republic of China Tax Facts and Figures. Hongkong: PWC.Bibliography[1] Willis, Eugene; Hoffman, William H. Jr., et al: South-Western Federal Taxation, published annually. 2013 edition (cited above as Willis|Hoffman) ISBN 978-1-133-18955-8.[2] Pratt, James W.; Kulsrud, William N., et al: Federal Taxation, updated periodically. 2013 edition ISBN 978-1-133-49623-6 (cited above as Pratt & Kulsrud).[3] Fox, Stephen C., Income Tax in the USA, published annually. 2013 edition ISBN 978-0-985-18231-1。

律师的多种称呼(英文)

中国外向型经济和法律服务的发展使越来越多的中国律师事务所和律师有机会接触涉外案件,与海外同行合作,处理英文法律文件。

中国律师套印lawyer的名片也多了起来。

因此有人认为,用以表示“律师”的英文单词,非lawyer莫属。

翻开国内的英汉法律字典,为自己没有这样而暗自庆幸的同时感到有些眼花缭乱:与“律师”相对应的单词有很多。

像advocate,attorney, attorney at law; attorney-at-law, bar, barrister, counsel, counselor, counselor-at-law,,esquire, gentleman of the robe, gentleman of the long robe, lawyer, solicitor等。

到底用哪一个?怎么用?这些表示律师含义的词汇如何出现在书面和口头上呢?是指学习法律、依法获准执业、为当事人提供法律意见,并有资格出庭参加案件;又指法国、英格兰等地律师、法律顾问。

是法国律师统称。

诉讼代理人,常用于书面用语。

attorney一地区普通法高等法庭的公共官员(public officer)。

一词经常与attorney一词互用,用法同attorney-at-law。

指法庭外接受委托的律师,也称为lawyer in fact。

bar association表达。

新加坡等国和香港地区,又称大律师、辩护律类似称呼还有barrister, counsel和barrister-at-law。

solicitor。

指出庭律师工作室。

英国的出庭律师不准合伙开业,所以他们通常数chamber),提供法律服务。

通常一个工作室有15个出庭律师。

日本人对律师的称呼,也称为“辩护士”。

专门为个人、公司和政府公务部门提供法律服务的人,称为法律顾问。

6、第14修正案和联邦法庭规则中均有the right to counsel的规定,即刑事被counsel也有律师之意。

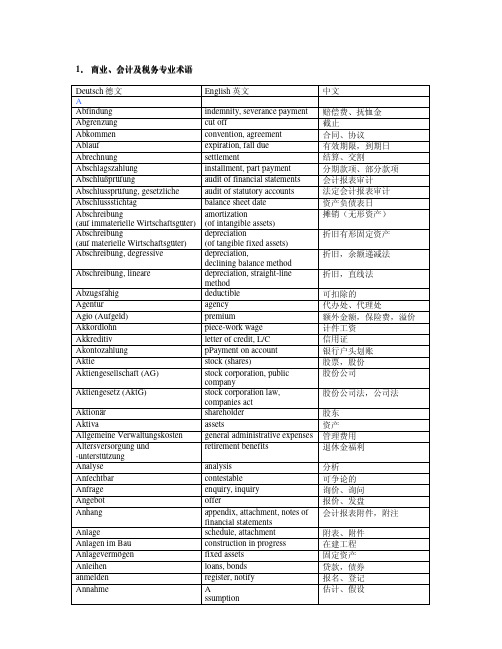

英文d tax law

1.商业商业、、会计及税务专业术语Deutsch德文English英文中文AAbfindung indemnity, severance payment 赔偿费、抚恤金Abgrenzung cut off 截止Abkommen convention, agreement 合同、协议Ablauf expiration, fall due 有效期限,到期日Abrechnung settlement 结算、交割Abschlagszahlung installment, part payment 分期款项、部分款项Abschlußprüfung audit of financial statements 会计报表审计Abschlussprüfung, gesetzliche audit of statutory accounts 法定会计报表审计Abschlussstichtag balance sheet date 资产负债表日Abschreibung(auf immaterielle Wirtschaftsgüter) amortization(of intangible assets)摊销(无形资产)Abschreibung(auf materielle Wirtschaftsgüter) depreciation(of tangible fixed assets)折旧有形固定资产Abschreibung, degressive depreciation,declining balance method折旧,余额递减法Abschreibung, lineare depreciation, straight-linemethod折旧,直线法Abzugsfähig deductible 可扣除的Agentur agency 代办处、代理处Agio (Aufgeld) premium 额外金额,保险费,溢价Akkordlohn piece-work wage 计件工资Akkreditiv letter of credit, L/C 信用证Akontozahlung pPayment on account 银行户头划账Aktie stock (shares) 股票,股份Aktiengesellschaft (AG) stock corporation, publiccompany股份公司Aktiengesetz (AktG) stock corporation law,companies act股份公司法,公司法Aktionär shareholder 股东Aktiva assets 资产Allgemeine Verwaltungskosten general administrative expenses 管理费用Altersversorgung und-unterstützungretirement benefits 退休金福利Analyse analysis 分析Anfechtbar contestable 可争论的Anfrage enquiry, inquiry 询价、询问Angebot offer 报价、发盘Anhang appendix, attachment, notes offinancial statements会计报表附件,附注Anlage schedule, attachment 附表、附件Anlagen im Bau construction in progress 在建工程Anlagevermögen fixed assets 固定资产Anleihen loans, bonds 贷款,债券anmelden register, notify 报名、登记Annahme Assumption估计、假设annulieren cancel 取消,注销Anrecht claim, title 权益,所有权Anschaffungskosten acquisition cost 取得成本Anspruch claim 要求索赔,追偿shares in affiliated companies 关联企业股份Anteile an verbundenenUnternehmenAnteile, eigene treasury stock (own shares) 库存股票Antrag (singular) Anträge (pl) application 申请Anwalt lawyer, attorney 律师Anzahl number, quantity 树木、数量Anzalungen, erhaltene deposits received 已收押金Anzahlungen, geleistete deposits paid 已付押金Aufnahme (Vorräte) physical count (inventories) 实地盘点,实物盘存Aufsichtsrat supervisory board 监事会Auftrag (sl) Aufträge (pl) order, assignment 订单;委托任务Aufwand, Aufwendungen expenses 费用Aufwendungen, außerordentliche extraordinary expenses 非经常费用Ausbildung training 培训Außenprüfung, steuerliche tax audit 税务审计impairment of long-lived assets 长期资产减值Außerplanmäßige Abschreibungenauf langfristigeVermögensgegenständeAusfuhr export 出口Ausgaben expenditure 支出Ausland abroad, foreign country 外国Ausländer foreigner 外国人Ausleihungen loans receivable 应收贷款loans to affiliated companies 向关联企业贷出款项Ausleihungen an verbundeneUnternehmenAuslieferung delivery 出货Ausschüttung distribution 分派,分销BBankgebühren bank charges 银行手续费Bankkonto bank account 银行账户Bankzinsen bank interest 银行利息Bargeld cash 现金Bau, Bauten building 建筑物、楼宇Beherrschungsvertrag control agreement,管理合同、监督协议dependency agreementBehörde authorities (local), civil service 官方机构、行政机关Beirat advisory council, advisory企业顾问委员会、理事会boardBeitrag (sl) Beiträge (pl) contribution 贡献、出资Beleg voucher 凭证Bemessungsgrundlage assessment basis 评估基础Beratung advice, debate 咨询、协商Berichte reports 报告Berufstätigkeit occupation, job 职业、工作Beschluß resolution 决定、决议Besitz possession, occupancy 占有、所有Bestandaufnahme Physical count (inventory) 实地盘点、实物盘存Bestansveränderungen inventory increase/decrease 库存增加/减少Bestätigungsvermerk audit opinion, auditors´ report 审计意见、审计报告Bestätigungsvermerk, eingeschränkte qualified audit opinion,qualified auditor´s report保留意见的审计意见、保留意见的审计报告Bestellung order, reservation 订货、预定Besteuerung taxation 课税、税金Beteiligung participation, investment 参股、投资Betrag amount, sum 数目、数额、款项Betreff subject 事由Betrieb plant, business, factory 工厂、企业Betriebs- und Geschäftsausstattung office furniture and equipment 办公家具及设备Betriebsabrechnungsbogen (BAB) cost distribution sheet 成本核算单Betriebsergebnis operating profit/loss 营业损益betriebsfremde Aufwendungen (Erträge) non-operating expenses(income)营业外费用(收入)Betriebsprüfung, steuerliche tax audit 税务审计Bevollmächtigung authorization, power of attorney 委托,法律授权书Betrug fraud, swindle 欺骗、欺诈Beweis proof 证明、证据Beweisaufnahme evidence 凭证、证据Bewertung valuation 评估Bewirtungskosten entertainment expenses 业务招待费,交际费Bezug refrence 涉及、援引Bilanz balance sheet 资产负债表Bilanzgewinn retained earnings 未分配利润Bilanzierungsprinzipien accounting principles 会计原则Bilanzstichtag balance sheet date 资产负债表日Bilanzsumme balance sheet total, total assets 总资产Bilanzverlust accumulated deficit 累计亏损Bilanzvermerk footnote to the balance sheet 资产负债表注释Bonität solvency, validity 支付能力、资信Börse stock exchange 证券交易所Bruttoergebnis vom Umsatz gross profit/loss 毛损益Buchführung accounting, bookkeeping 会计簿记Buchführung, doppelte double entry bookkeeping 复式簿记Buchhaltung accounting department 会计部Buchung entry 记账Buchwert book value 账面价值Budget budget 预算Bürgschaft guarantee 担保、保证Bürobedarf office supplies 办公用品Büroeinrichtung office furniture and equipment 办公家具及设备Buße, Bußgeld monetary fine, penalty 罚金、罚款CCash flow cash flow 现金流量DDachgesellschaft holding company 控股公司Darlehen loan 贷款Daten data, information 数据,信息Datenbank data bank 数据库Datenverarbeitung (DV) data processing (DP) 数据处理Datum date 日期Debitorische Kreditoren suppliers with debit balances 账面上有借方余额的供货商Defizit deficit 赤字、亏损Delkredere security, guarantee 抵押,担保Devisen foreign exchange, foreign外汇、外币currencyDevisentermingeschäft forward foreign exchange远期外汇交易transactionDevisenterminkurs forward contract rate 远期合约汇款Dienstleistung service 服务Differenzgeschäft dealing in futures 期货交易Dividende dividend 股息、股利Dokument document, paper 文件、公文Doppelbesteuerungsabkommen double taxation agreement 避免双重征税协定Durchschnitts-Verfahren weighted average 加权平均EEffektivverzinsung yield 实际收益Eigenkapital equity, shareholders´ equity 股权,股东权益Eigentum ownership 所有权Eigentumsvorbehalt retention of title 所有权的保留Einkommensteuer (ESt) income tax 所得税Einkommensteuererklärung income tax return 所得税申报Einkommensteuergesetz (EStG) income tax law 说的税法Einkommensteuerrückerstattung income tax refund 所得税退还Einlage capital contribution 投入资本Einlage, eingezahlte contributed capital 实缴资本Einlagen ausstehende outstanding capital未缴入股额、未注入股本contributionsEintrag entry (in register) 登记、记录Einverständnis approval, consent 认可、同意Ergebnis, außerordentliches extraordinary result 非正常纯损益Ergebnis der gewöhnlichenresult from ordinary operations 正常营业损益GeschäftstätigkeitErgebnisabführungsvertrag profit and loss transfer损益移交协议agreementEröffnungsbilanz opening balance sheet 期初资产负债表Erklärung statement, explanation 说明,解释Erlös proceeds (net) 净收入Erlösschmälerungen sales deductions 销售损失Ersatz replacement, substitute 替代、取代Ersatzteile spare parts 备件Erstattung refund 退还,返还Ertrag income, proceeds 受益、收入Erträge, außerordentliche extraordinary income 非正常收益Erträge, betriebliche operating income 营业收入Erzeugnisse goods, products 产品Erzeugnisse, fertige finished goods 产成品Erzeugnisse, unfertige work in progress 半成品Eventualverbindlichkeiten contingencies and commitments 或有事项及承担Exportgeschäft export trade 出口业务FFabrik factory, plant 工厂、工场Factoring (-geschäft) factoring 代收帐款Fair Value fair value 公允价值Fälligkeitsdatum due date 到期日Fehlbetrag deficit, shortfall 亏损、不足Festgeld time deposit 定期存款festverzinslich fixed interest-bearing 定息的FIFO-Verfahren First-in first-out 先进先出Filiale (Zweigniederlassung) branch, branch office 分公司、分店Finanzamt tax bureau 税务局Finanzanlagen financial assets 金融资产Fianzergebnis financial result 财务损益Finanzierung financing 筹资、融资Finanzierungs-Leasing finance lease 融资租赁Finanzlage financial position 财务状况firmeninhaber proprietor 公司所有人Firmenwert goodwill 商誉Flüssige Mittel liquid funds 流动资金trade accounts receivable 应收账款Forderungen aus Lieferungen undLeistungenForderung, zweifelhafte bad debt 坏账Forderungen receivables 应收款项Forschung und Entwicklung research and development 研究与开发Fracht freight, cargo 载运货物Frachtbrief bill of landing, consignment货物运单、运单、载货票据noteFrachtkosten freight charges 运费Freibetrag taxallowance 免税限额Freigrenze tax exemption limit, tax free免税额amountFristverlängerung extension (e.g. for filing) 延期、宽限Fusion merger 合并GGarant guarantor 担保人、担保方Garantie guarantee 担保、保证Gebühr agency free/commission fee 手续费,代办款,佣金Gegenangebot counter offer 还价Gegenposten off-set entry (bookkeeping) 抵销分录Gegenwartswert present value 现值Gehalt salary 薪金、工资Gehaltsabrechnung payroll 工资单Gelände land (plot) 土地、地块Geld money 钱Geldschein paper money 纸币Gemeinkosten overheads 制造费用Geringwertige Wirtschaftsgäter low value fixed assets 底值固定资产Gesamtkostenverfahren total costformat(for profit and loss account)损益表的全部成本计算法Geschäftsbericht annual report 年报Geschäftsführer general manager 总经理Geschäftsführung management board 管理层Geschäftsjahr financial year 会计年度Geschäftsvorfall business transaction 业务Geschäftswert goodwill 商誉Gesellschaft company, association 公司Gesellschafter(einer Kapitalgesellschaft)shareholder 股东、出资人Gesellschafter(einer Personengesellschaft)partner 合伙人Gesellschafterversammlung (einer Kapitalgesellschaft) stockholders´/shareholders´meeting股东大会Gesellschafterversammlung (einer Personengesellschaft shareholders´ meeting(partners´ meeting)合伙人大会Gesellschaftsvertrag articles of association 公司章程Gesellschaftsvertrag(einer Personengesellschaft)partnership agreement 合伙契约gesetzlich legal, statutory 法定的、法律上德、合法的gesetzwidrig unlawful, illegal 非法的、违法的Gewährleistung warranty 担保Gewinn profit 利润、收益Gewinn- und Verlustrechnung (GuV) profit an loss account,statement of income损益表Gewinnausschüttung distribution of earnings,dividend分红、利润分配、分配股利Gewinnrücklage revenue reserve 留存利润Gewinnvortrag retained earnings 未分配利润Gezeichnetes Kapital subscribed capital 任缴股本Girokonto current account 结算账户、转账户头Gläubiger creditor 债权人、债主GmbH=Gesellschaft mit beschränkter Haftung limited liability company(private)私人有限责任公司GmbH – Gesetz (GmbHG) limited liability company law 有限责任公司法Gratifikation bonus 奖金、红利Grundsätze ordnungsmäßiger Buchführung (GoB) generally accepted accountingprinciples公认会计准则Grundlagen des Abschlusses basis of preparation 编制基础Grundstück land, real estate 土地,不动产grundstücksgleiche Rechte similar land rights 准土地权益gültig valid, current 有效的、现行的Guthaben credit balance 贷方余额HHaben credit 贷方Habenbuchung credit entry 贷方分录Haftpflicht third party liability, public第三方责任,公众责任insurenceHaftpflichtversicherung third party liability insurance 公众(第三方)责任保险Haftungsverhältnisse contingent liabilities 或有债务Handelsbilanz commercial balance sheet 商业资产负债表Handelsgesetzbuch (HGB) commercial code 商业法典Handelsregister trade register 工商登记Handelswaren merchandise, goods for resale 商品,转售货品Hauptbuch general ledger 总分类账Hauptversammlung der Aktionäre stockholders´ meeting 股东大会Hebesatz multiplier 税率Herstellungskosten manufacturing costs,制造成本,生产成本cost of productionHoldinggesellschaft holding company 控股公司Honorar fee 报酬,收费Hypothek mortgage 抵押、抵押权IImmatrielleintangible assets 无形资产VermögensgegenständeImmobilien real estate 房地产、不动产Import import 进口Inanspruchnahme claim 要求,索赔,追偿Inflation inflation 通货膨胀Ingangsetzungskosten pre-operating and start-up costs 开办费Inland, inländisch inland, domestic 国内的Insolvenz insolvency 无力偿还债务,破产Instandhaltungskosten maintenance costs 维修费Inventar plant and equipment 厂房设备Inventur stocktake 盘点、盘存Investitionszuschuß investment grant 投资补贴JJahresabschluß annual financial statements 年度会计报表Jahresende year end 年末Jahres fehlbetrag net loss for the year 年度净亏损Jahresüberschuß net income for the year 年度净收入KKalenderjahr calendar year 公历年Kapitalerhöhung capital increase 增资Kapitalertrag capital gain 资本利得Kapitalertragsteuer auf Dividenden withholding tax on dividends 股利代扣代缴税Kapitalflußrechnung cash flow statement 现金流量表Kapitalgesellschaft corporation 公司Kapitalrücklage capital reserve 资本公积Kapitalverkehrsteuer capital transfer tax 资本转让税Kassenbestand cash balance 现金余额Kaufvertrag contract of perchase 购买合同Kommanditgesellschaft (KG) limited partnership 有限合伙业务Kommissionsgeschäft agency business 托售、代缴业务Konjunktur economic cycle 经济周期Konsignationsware consignment stocks 委托代销货物、寄售货物Konten accounts 会计科目Kontoauszug statement of bank account 银行对账单Kontokorrentkredit overdraft credit, open credit 帐户透支款项Kontrakt contract 契约、合同Konzern gruoup (of companies) 集团公司Konzernabschluß consolidated financial合并会计报表statementsKonzession franchise 特许权、转卖权Körperschaftsteuer (KSt) corporation tax 公司税、法人税Körperschaftsteuergesetz (KStG) corporation tax law 公司税法、法人税法Kostenrechnung cost accounting 成本核算Kreditinstitute commercial banks 商业银行Kreditlinie basic credit line 贷款限额、基本信用额度Kreditorische Debitoren customers with credit balances 账面上有贷方余额的客户Kunde customer 客户、用户Kurs exchange rate, stock price 汇率;股票牌价Kursgewinn exchange gain 汇兑收益Kursrisiko exchange risk 汇率风险Kurssicherung hedge 套汇,对冲Kursverlust exchange loss 汇兑损失LLagebericht management report 管理报告Lager warehouse 仓库、库房Lagerumschlagshäufigkeit inventory turnover ratio 库存周转率Landeswährung local currency 本地货币Latente Steuern deferred taxes 递延税项Laufzeit term 期限、有限期Leasing-Vertrag lease contract 租赁合同Lieferrant supplier 供货人、供应商Lieferung delivery 出货LIFO-Verfahren Last-in first-out 后进先出Liquidation liquidation 清算Liquidität liquidity 偿债能力、流动资金Lizenz licence 许可证、许用权Lizenzgebühr royalty 专利权使用费Lohne wage 工资Lohnsteuer wage tax 工资税MMarktanteil market share 市场份额Marktwert net realizable value, marketvalue可变现净值,市场价值Maschinen machinery 机器Miete rent 租金Mietertrag rental income 租赁收入Mietkauf hire perchase, instalmentperchase租购,分期付款购买Muttergesellschaft parent company 母公司NNachfrage demand 需求、询价Nebenkosten ancillary expenses, additionalcharges杂项费用、附加费用Nennwert face value, per value 面额价值、票面价值Nettoumlaufvermögen working capital 营运资本、周转资本Nettoverkaufserlöse net sales proceeds 销售净收入Nettowert net worth 净值neutraler aufwand (Ertrag) non-operating expenses(income)营业外支出(收入)Niederlassung branch 分公司、分行、分支机构Niederstwertprinzip lower of cost or marketprinciple成本与市价孰低原则Nutzungsdauer useful life 使用寿命,使用期限OOffenlegung(des Jahresabschlusses) publication(of the financial statement)会计报表的公布Operating-Leasing operating lease 经营租赁PPassiva lliabilities and shareholders´equity负债和股东权益Patent patent 专利Patentrecht patent law, patent right 专利法;专利权Pauschalpreis lump-sum, all-inclusive price 总价、统包价格Pauschalwertberichtigung general allowance 一般准备金Pension pension 退休金、养老金Pensionsrückstellung accrual for pensions 退休准备金periodenfremd relating to other periods 与其它期间相关的Personalaufwand personnel expenses 劳务费用Pfand pledge, security 押金、担保金、抵押品Preisnachlaß rebate, allowance 削价、肩胛、折扣Prokurist company officer with statutoryauthority代理人,全权代表Provision commission 佣金Prüfung audit 审计Prüfungsbericht audit report 审计报告QQuittung receipt 收据RRatenkauf Instalment purchase 分期付款购买Rechnungsabgrenzungsposten(RAP)Deferred items 递延项目Rechnungsabgrenzungsposten (RAP), aktive Prepaid expenses and deferredcharges预付费用和递延费用Rechnungsabgrenzungsposten(RAP), passiveDeferred income 递延收益Rechnungslegung accounting, reporting 财务报告制度Rechnungswesen accounting system 会计系统Reisekosten traveling expenses 差旅费Rentabilität profitability 盈利能力,盈利率Restwert residual value 残值Richtlinien regulations, guidelines 规定、准则、指引Roh-, Hilfs-, und Betriebsstoffe raw materials and supplies 原材料和辅助料Rohertrag gross profit 毛利Rollgeld carriage, freight charge 运费Rückerstattung refund 退坏,返还Rückkaufswert (Versicherung) surrender value (insurance) 退保价值(保险)Rücklage reserve 留存、准备、公积金Rücklage, gesetzliche legal reserve 法定留存、准备、公积金Rücklage,satzungsmäßige statutory reserveRückstellung accrual, provision 准备金、备抵Rückzahlung repayment 归还(借款)、偿还SSachanlagen tangible assets, property plantand equipment有形资产,厂房及设备Saldenbestätigung confirmation of balance 余额确认书Saldenbilanz trial balance (T/B) 试算平衡表Saldo balance 余额Saldo, debitorischer debit balance 借方余额Saldo, kreditorischer credit balance 贷方余额Saldo zu Ihren Gunsten balance in your favour 你方应收余额Saldo zu Ihren Lasten balance in our favour 我方应收余额Sanierung restructuring 重整、改建、改组Satzung statutes, articles 章程Säumniszahlung late payment fine 逾期罚金、滞纳罚金Schaden damage 损害、损坏Schätzung estimate 孤寂、估算Scheck check, cheque 支票Schulden debts, borrowings 债务,借款Schuldner cebtor 债务人Schuldverschreibung bond, debenture 公司债券、信用债券Sitz (einer Firma) domicile, registered office (公司)注册地、所在地Skonto discount 付现折扣Software software 软件Solawechsel promissory note 期票、本票Soll debit 借方Sollbuchung debit entry 借方分录(记帐)Sonderabschreibung special depreciation 特别折旧Sonderausgaben special expenses (deductible inassessing income tax) (在确定所得税时可扣除的)特别费用Sonderprüfung special audit 特别审计Sozialabgaben social insureance contributions 社会保险费Sozialversicherung social security 社会保险Sozialversicherungsbeiträge social security contributions 社会保险费Spanne margin 毛利、利润Sparkasse savings bank 储蓄银行spende donation, gift 捐助、捐款Spesen expenses 开支、费用Stammaktie common stock 普通股票Stammeinlage paid-in capital stock, capitalinvested实收资本Stammkapital capital stock 创始资本、股份资本Steuer tax 税款Steueraufwand tax expense 税务费用Steuerausländer non-resident taxpayer 境外纳税人steuerbegünstigt tax privileged 税收优惠Steuerberater tax adviser 税务顾问Steuerbescheid tax assessment notice 征税单、征税通知书Steuerbilanz tax balance sheet 税务资产负债表Steuererklärung tax return 纳税申报表steuerfrei tax free 免税Steuerkasse tax collection office 税务征收处Steuerklasse wage tax classification 工资税率等级Steuerpflicht liability for taxation 纳税义务Steuerrückstellungen accrued taxes 预提税款Steuersatz tax rate 税率Steuerschätzung tax estimation 税款估计Steuervorauszahlung tax prepayment 预付税款Stichtag end of priod (date) 期末strafe fine, punishment 罚款,惩罚Stückpreis uUnit price 单价Subvention subsidy 补贴、津贴TTantieme management bonus 管理人员红利Tätigkeit, selbständige occupation, self-employed 自雇职业technische Anlagen technical equipment 技术设备Teilkonzern sub-group (of companies) 集团分公司Teilwert going concern value 持续经营价值Termin due date 到期日、期限Termingeschäfte forward contracts 远期合约Tochtergesellschaft subsidiary 子公司、分公司Treuhänder trustee 受托人ÜÜberliegegeld demurrage 滞期费、逾期停泊费Überstunden overtime 加班工时Überweisung bank transfer 银行转账Überziehungskredit overdraft 透支UUmbuchung reclassification, adjusting调账、科目转记journal entryUmlaufvermögen current assets 流动资产Umsatz sales 销售额Umsatzerlöse net sales, turnover 销售净额,营业额Umsatzkostenverfahren cost of sales format损益表的销售成本格式(for profit and loss account)Umsatzrealisierung revenue recognition 收入确认Umsatzsteuer value-added tax 增值税Umzugskosten moving expenses 搬迁费Unfallversicherung accident insurance 意外事故保险Unternehmen company, enterprise,企业、公司undertakingUntervermietung sublease 转租unterwegs befindliche Ware goods in transit 在途货物VVerbindlichkeiten liabilities 债务、负债Verbindlichkeiten aus Lieferungentrade accounts payable 应付账款und Leistungenbank loans, overdrafts 银行贷款,透支Verbindlichkeiten gegenüberKreditinstitutenVerbrauch consumption 消费verbundene Unternehmen affiliated companies 关联公司(企业)Vereinbarung agreement 协议Verpflichtungen commitments 承担Vergütung compensation 报酬Verhandlung negotiation 谈判,协商Verlagsrecht copyright 版权Verlust loss 亏损Verlustvortrag loss carry forward,结转累计亏损accumulated deficitVermietung tenancy 租赁Vermögen assets 资产Vermögensteuer net worth tax 资本净值税Verrechnungspreis transfer price 转移价格Verschmelzung merger, consolidation 合并Versicherung insurance 保险Vertrag contract, agreement 合同、协议Vertriebsgesellschaft distribution company 分销公司、经销商Vertriebskosten selling expenses 销售费用Verzugszinsen default interest 滞延付款利息Vorräte inventories 库存Vorratsbewertung inventory valuation 存货估价Vorschuß advance 预支、预付Vorstand baord of directors (股份公司)董事会Vorstandsmitglied board member 董事会成员Vorstandsvergütung directors´ fee 董事报酬Vorstandsvorsitzender chairman of the board 董事长Vorsteuer input tax (VAT) 进项增值税Vorzugsaktien preferred shares (stocks) 优先股WWährung currency 币种,货币waren goods, merchancise 商品Waren, bezogene purchased goods 购入商品Warenbestand trading stock 商品库存Wareneinsatz cost of sales 销售成本Wartungskosten maintenance expense 维修费Wechsel note, bill of exchange 汇票Wechsel, eigener promissory note 期票、本票Wechselforderungen notes receivable 应收票据Wechselkurs exchange rate 汇率Wechselverbindlichkeiten notes payable 应付票据Werbekosten advertising expenses 广告费Werbungskosten (im Steuerrecht) income-related expenses,professional expenses(German tax law)(德国税法上)与收入、职业相关的费用Wertberichtigung reserve, allowance, write-down 减记,削减(资产价值)Wertberichtigung auf zweifelhafte Froderungen allowance for doubtfulaccounts, bad debt allowance呆账/坏账备抵Wertminderung diminution 贬值Wertpapiere securities 有价证券Wertpapiere, notierte listed securities 上市证券Wettbewerb (Konkurrenz) competition 竞争Wiederbeschaffungswert current replacement value 重置价值、替换值Wirtschaftsgut asset 资产Wirtschaftsprüfer public accountant, auditor 注册会计师、审计师Wirtschaftsprüfung audit 审计Wirtschaftsjahr financial year 会计年度Wohnsitz residence 住所、居住地Zzahlbar payable 应付款项Zahlen figures, numbers 数字Zahlung payment 付款、支付Zeugnis job reference 职务证明Zielkauf purchase on credit 赊购Zinsen interest 利息Zinseszinsen compound interest 复利、利滚利Zinssatz interest rate 利率Zoll customs duty 关税Zollager bonded warehouse 保税仓库Zollamt customs duty office 海关管理局addition (to fixed assets) (固定资产)增加Zugang(zum Sachanlagevermögen)Zusatzkosten further costs 额外成本、追加成本Zuschreibung write-up, appreciation 增值、升值Zuschuß subsidy 补贴、补助Zuteilung allocation 配给、分配Zwischenabschluß interim financial statements 中期会计报表2.德国商业法典资产负债表与损益表Bilanz Balance Sheet 资产负资产负债表债表AKTIVA ASSETS 资产Ausstehende Einlagen, Davon eingefordert Unpaid capital, thereof calledup未缴付资本(其中一催缴部分)Aufwendungen für die Ingangsetzung (Erwerterung) des Geschäftsbetriebes Expenses incurred inconnection with the start-up,expansion of the business开办及业务扩张费A Anlagevermögen A Fixed Assets A 固定资产I. ImmaterielleVermögensgegenständeI. Intangible Assets I. 无形资产1 Konzessionen, gewerblicheSchutzrechte und ähnlicheRechte und Werte sowieLizenzen an solchen 1 Licences, trade marks andpatents, etc., as well aslicences to such right andassets1 特许权、商标权、专利和对类似的权益和资产的特许权2 Geschäft soder Firmenwert 2 Goodwill 2 商誉3 Geleistet Anzahlungen 3 Advances paid onintangible assets3 无形资产的预付款II. Sachanlagen II. Tangible Assets II. 有形资产1 Grundstücke,grundstücksgleiche Rechteund Bauten einschließlichder Bauten auf fremdenGrundstücken 1 Land, rights similar toland, and buildings,including buildings onproperty owned by others1 土地、类似土地权益和建筑物,包括在他人地产上的建筑物2 Technische Anlagen undMaschinen 2 Technical equipment andmachinery2 技术设备与机器3 Andere Anlagen, Betriebs-und Geschäftsausstattung 3 Other equipment, officefurniture and equipment3 其他设备、办公家具及设备4 Geleistet Anzahlungen undAnlagen im Bau 4 Advances paid on fixedassets, and assets underconstruction4 固定资产及在建工程的预付款III Finanzanlagen III: Financial Assets III. 金融资产1 Anteile an verbundenenUnternehmen 1 Shares in affiliatedcompanies1 关联企业股份2 Ausleihungen an verundeneUnternehmen 2 Loans to affiliatedcompanies2 相关联企业贷出款项3 Beteiligungen 3 Participations 3 参股25%或以上4 Ausleihungen anUnternehmen, mit denenein – Beteiligungsverhältnisbesteh 4 Loans to eintities inwhich participations areheld4 向有参股25%或以上企业贷出款项5 Wertpapiere desAnlagevermögens5 Long-term investments 5 长期投资6 Sonstige Ausleihungen 6 Other loans 6 其他贷款B. Umlaufvermögen B. Current Assets B. 流动资产I. Vorräte I. Inventories I. 库存1 Roh-, Hilfs- undBetriebsstoffe 1 Raw materials andsupplies1 原材料和辅料及生产2 Unfertige Erzeugnisse;unfertige Leistungen 2 Work in progress;incompleted projects2 半成品、未完工程3 Fertige Erzeugnisse undWaren 3 Finished goods andmerchandise3 产成品及商品4 Geleistete Anzahlungen 4 Payments on account 4 预付账款II. Forderungen und sonstige Vermögensgegenstände * II. Receivables and othercurrent assets *II. 应收款机其他流动资产*1 Forderungen ausLieferungen undLeistungen1 Trade receivables 1 应收账款2 Forderungen gegenverbundene Unternehmen 2 Amounts due from groupcompanies2 应收集团其他企业款项3 Forderungen gegenUnternehmen, mit denenein Beteiligungsverhältnisbesteht 3 Receivables from entitiesin which participationsare held3 有参股25%或以上企业的应收款4 SonstigeVermögensgegenstände4 Other current assets 4 其他流动资产III Wertpapiere III. Securities III. 有价证券1 Anteile an verbundenenUnternehmen 1 Shares in affiliatedcompanies1 占关联企业的股份2 Eigene Anteile 2 Treasury stock 2 库存股票3 Sonstige Wertpatiere 3 Other securities 3 其他有价证券IV Kassenbestand,Bundesbank guthaben,Guthaben beiKreditinstituten IV. Cash, Deposits withFederal Bank Depositswith commercial banksand chequesIV 现金、联邦银行,存款、商业银行存款和支票C. Rechnungsabgrenzungs-postenC. Prepaid Expenses C. 预付费用Nicht durch Eigenkapital gedeckter Fehlbetrag Excess of liabilities overassets负债超过资产的部分* Jeweils mit Angabe der Beträge mit einerRestlaufzeit von mehr alseinem Jahr * For each caption withdisclosure of amounts dueafter more than one year* 剩余偿还期限超过一年者须注明PASSIVA LIABILITIES AND EQUITY 负债及所有者权益A: Eigenkapital A. Shareholders´ Equity A. 股东权益I. Gezeichnetes Kapital I. Share Capital I. 股本II. Kapitalrücklage II. Capital Reserves II. 资本公积III Gewinnrücklagen III. Revenue Reserves III. 收益储备1 Gesetzliche Rücklage 1 Legal reserve 1 法定公积金2 Rücklage für eigene Anteile 2 Reserve for treasury stock 2 库存股份公积金3 Satzungsmäßige Rücklagen 3 Statutory reserves 3 法定公积金4 Andere Gewinnrücklagen 4 Other revenue reserves 4 其他收益公积金。

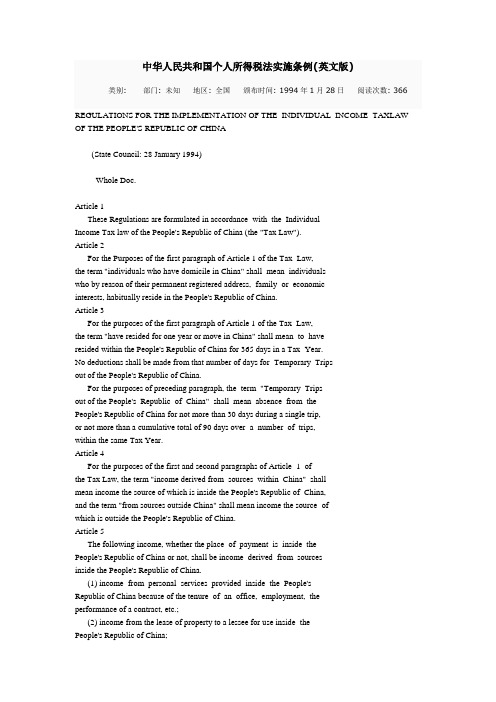

个人所得税实施条例英文版