会计英语翻译chapter1

会计英语课本翻译

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语课本翻译

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

为满足上述需求,国际会计准则委员会(IASC)于1973年成立,并致力于国际公认的会计准则的制定。

chapter用法

chapter用法"Chapter" 是一个英语词汇,通常翻译成中文为"章节" 或"篇章"。

在不同的语境中,"chapter" 有不同的用法:1. 书籍和文学作品:在书籍和文学作品中,"chapter" 表示书或文学作品中的一个主要部分,通常用来划分书籍的内容。

每个"chapter" 可能包含一个特定的主题、情节或思想。

例如:• "Chapter 1: The Beginning"• "第一章:开始"2. 生活中的经历或事件:有时人们也用 "chapter" 来形容生活中的经历或事件,表示人生的不同阶段或经历的特定时期。

例如:• "This was a difficult chapter in my life."• "这是我生活中的一个艰难时期。

"3. 会议和讨论:在会议或讨论中,"chapter" 可能表示会议的不同议程或讨论的主要部分。

例如:• "Let's move on to the next chapter of our discussion."• "让我们继续进行我们讨论的下一个议程。

"总体而言,"chapter" 是一个多义词,其具体含义取决于上下文。

在文学和书籍中,它通常指代书籍的一个主要部分;在生活中,它可以用来描述人生的时期或经历;在会议和讨论中,它可能表示讨论的主要部分或议程。

1/ 1。

会计英语术语解释

会计英语术语解释第一章Account payable 应付账款Account receivable 应收账款Accounting 会计Accounting equation 会计等式Asset 资产Audit 审计Balance sheet 平衡表(资产负债表)Capital 资本Certified management accountant (CMA) 注册管理会计Certified public accountant (CPA) 注册会计师Corporation 公司Entity 主体Expense 费用Financial accounting 财务会计Financial Accounting Standards Board (FASB) 财务会计准则委员会Financial statements 财务报告Generally accepted accounting principles(GAAP)公认接受会计准则Income statement 收入表(利润损益表)Liability 负债Management accounting 管理会计Net earnings 净收益Net income 净收入Net loss 净损失Net profit 净利润Note payable 应付票据Note receivable 应收票据Owner's equity 所有者权益Owner withdrawals 实收资本Partnership 合伙制Proprietorship 个体制Revenue 收入Shareholder 股东Statement of cash flows 现金流量表Statement of earnings 净盈余报表Statement of financial position 财务状况报表Statement of operations 运营表Statement of owner's equity 所有者权益报表Stockholder 股东Transaction 交易第二章Account 账簿、账户Chart of accounts会计科目表把……记入贷方CreditDebit把……记入借方Journal日记账Ledger总账、分类账Normal balance 正常余额、平衡Posting登帐、过账Trial balance 试算平衡第三章Accrual accounting 权责发生制book value(of a plant asset) 账面价值plant asset 固定资产Accrued expense 应计费用cash-basis accounting 收付实现制prepaid expense 预付费用Accrued revenue 应计收入contra account 抵消账户revenue principle 收入确认准则Accumulated depreciation累计折旧deferred revenue 递延收入time-period concept会计期间Adjusted trial balance 调整试算平衡depreciation折旧unearned revenue递延收入Adjusting entry 调整分录matching principle 配比原则第四章Accounting cycle 会计循环fixed asset固定资产plant asset 固定资产Closing the accounts 结账income summary 损益汇总账户postclosing trial balance 试算平衡Closing entries 结账分录liquidity 流动性reversing entries 转回分录Current asset 流动资产long-term asset 长期资产temporary accounts 临时性账户Current liability 流动负债long-term liability 长期负债work sheet 工作表Current ratio 流动比率operating cycle 营业周期Debt ratio 资产负债率永久性账户permanent accounts第五章Cost of goods sold 销售成本sales 销货成本of Costmargin边际收入Grosspencentage毛利润率margin Gross毛利润Gross profit 毛利率profit pencentageGross运营收入Income from operations 存货inventory 存货周转inventory turnover发票,收据,单证Invoice多步式利润表Multi-step income statement 净销售Net purchases 净销售收入Net sales revenue 运营成本Operatingexpenses 运营收入income Operating其他费用expenseOther其他收入revenueOther定期盘存制system Periodic inventorysystem永续盘存制inventory Perpetualsales销售Sales discount销售折扣allowances销售返还补贴Sales returns and销售收入revenue Salessingle-step income statement单步式利润表第六章平均成本法Average-cost method谨慎性原则Conservatism 持续经营principle Consistency充分性披露(原则)Disclosure principle先进先出法Firsr-in first-out(FIFO) inventory costing method 加权平均法inventory costing methodWeighted average毛利润法method Gross profitlast-in first-out(FIFO) inventory costing method后进先出法Lower-of -cost-or-market(LCM)rule成本与市价孰低法Materiality concept重要性原则个别确认法indentifiction methodSpecific 个别成本法Specific -unit-cost method 第七章system会计信息系统information accounting processing 分批加工、成批处理batch journal disbursements cash现金支出日记账支票登记簿journal payment cashcash receipts journal 现金收入日记账check register 支票登记簿control account 统驭账户credit memorandum or credit memo 贷方备忘录data warehouse 数据仓库database 数据库debit memorandum or debit memo 借方备忘录、借记卡备忘录Enterprise Resource Planning 企业文化、企业资源规划general journal 普通日记账general ledger 总账hardware 硬件menu 菜单module 模板network 网络online processing 在线处理、联机处理purchases journal 购货日记账sales journal 销售日记账server 服务器software 软件special journal 特种日记账、专用日记账spreadsheet 试算表subsidiary ledger 明细分类账、辅助分类账第八章audit 审计、审核bank collection 银行托收bank reconciliation 银行往来对账单、银行存款余额调节表bank statement 银行对账单、银行结算清单check 支票computer virus 计算机病毒controller 财务主管deposit in transit 在途存款electronic funds transfer 电子资金调拨系统encryption 加密firewalls 防火墙imprest system 定额备用金制度internal control 内部控制nonsufficient funds(NSF)check 空头支票outstanding check 在途支票、未兑付支票petty cash 零用现金、零用金、小额现款Trojan horse 木马、特洛伊木马voucher 付款凭证、传票、凭单第九章Acid-test ratio酸性测试比率账龄分析法Aging-of-accounts method Allowance of Doubtful Accounts坏账准备Allowance for uncollectible accounts坏账准备Allowance method备抵法Bad-debt expense坏账损失Balance-sheet approach决算表平衡法Collection period收账日期Creditor债权人Day's sales in receivables应收账款周转天数Debtor债务人Default on a note不履行付款义务Direct write-off method直接注销法Discounting a note receivable应收票据折价Dishonor of a note 没有追索权Doubtful-account expense呆账费用Due date到期日Income-statement approach损益表方法Interest利息Interest period计息期Interest rate利率Maker of a note出票人Maturity date到期日Maturity value到期价值Note term票据条款Payee of a note持票人(收款票据)Percent-of-sales method销货百分比法Principal本金Principal amount本金金额Promissory note本票Quick ratio速动比率Receivables应收账款Time时间Uncollectible-account expense坏账损失第十章Accelerated depreciation method快速折旧法Amortization摊销Brand names商标名Capital expenditure资本支出Copyright版权Depletion expense折耗费Depreciable cost折旧成本Double-declining-balance(DDB)depreciation method双倍余额递减法Estimated residual value估计残值Estimated useful life估计使用年限非常维修Extraordinary repairFranchises特许权Goodwill商誉Intangibles无形资产Licenses授权Ordinary repair普通修理Patent专利Plant assets固定资产Salvage value残值Straight-line (SL)depreciation method直线法折旧Trademark商标Trade name商标名Units-of-production (UOP)depreciation method单位产量法第十一章accrued expense 应计费用、预提费用accrued liability 应计负债current portion of long-term debt 长期负债中一年内到期的部分current maturity 本期或一年内到期employee compensation 雇员薪酬FICA tax 联邦保险捐助税gross pay 工资的毛收入net pay 净支出payroll 工薪、工资short-term note payable 短期应付票据Social Security tax 社会保险税unemployment compensation tax 事业补偿税withheld income tax 预扣收入税第十三章additional paid-in capital 股本溢价authorization of stock 授权股票board of directors 董事book value 账面价值bylaws 规章、章程chairperson 主席charter 特许权、授权common stock 普通股contributed capital 已投股本cumulative preferred stock 累计优先股deficit 赤字、亏空dividends 股利double taxation 双重税收legal capital 法定资本limited liability 有限责任market value 市场价值发行在外股票outstanding stockpaid-in capital 实收资本par value 票面价值、面值preferred stock 优先股president 总裁、董事长rate of return on common stockholders'equity普通股收益率rate of return on total assets 资产回报率retained earnings 留存收益return on assets 资产回报return on equity 所有者权益回报shareholder 股东stated value设定价值、宣称价值、无票面值股票stock 股票stockholder 股东、股票持有者stockholders' equity 所有者权益第十四章Appropriation of retained earnings 分类盈余Comprehensive income 毛利润,综合收入Earnings per share (EPS)每股收益Extraordinary gains and losses 营业外收入/支出Extraordinary item 异常项目Prior-period adjustment 先期调整Segment of the business 经营部门Statement of stockholders' equity 所有者权益状况变动表Stock dividend 股票股利Stock split 股票分割(折分)Treasury stock 库藏股第十五章Bond discount 债券折价Bond premium 债券溢价Bonds payable 应付债券Callable bonds 可回购债券Capital lease 融资租赁Convertible bonds 可转换债券Debentures 信用债券(无担保债券)Discount(on a bond)折价Effective interest rate 有效利(息)率Lease 租赁Lessee 承租人Lessor 出租人Leverage 杠杆Market interest rate 投资者实际回报率Mortgage 抵押Operating lease 经营性租赁溢价PremiumPresent value 现值Serial bonds 系列债券Stated interest rate 票面利息率Term bonds 定期债券第十六章available-for-sale investments 可供出售投资(不以控制为目的)consolidated statements 合并会计报表controlling interest 主权益equity method 权益法foreign-currency exchange rate 汇率hedging 套期保值held-to-maturity investments 持有至到期投资long-term investment 长期投资majority interest 主权益marketable security 短期投资market-value method 市场法。

会计专业基础英语

Unit 4 AccountingPART I Fundamentals to Accounting第一部分会计基本原理1.accounting [ə'kaʊntɪŋ]n. 会计2.double-entry system复式记账法2-1 Dr.(Debit) 借记2-2 Cr.(Credit) 贷记3.accounting basic assumption会计基本假设4.accounting entity会计主体5.going concern持续经营6.accounting periods会计分期7.monetary measurement货币计量8.accounting basis会计基础9.accrual [ə'krʊəl] basis权责发生制【讲解】accrual n. 自然增长,权责发生制原则,应计项目accrual concept 应计概念accrue [ə'kruː] v. 积累,自然增长或利益增加,产生10.accounting policies会计政策11.substance over form实质重于形式12.accounting elements会计要素13.recognition [rekəg'nɪʃ(ə)n] n. 确认13-1 initial recognition [rekəg'nɪʃ(ə)n] 初始确认【讲解】recognize ['rɛkəg'naɪz] v. 确认14.measurement ['meʒəm(ə)nt] n. 计量14-1 subsequent ['sʌbsɪkw(ə)nt] measurement 后续计量15.asset ['æset] n. 资产16.liability [laɪə'bɪlɪtɪ] n. 负债17.owners’ equity所有者权益18.shareholder’s equity股东权益19.expense [ɪk'spens; ek-] n. 费用20.profit ['prɒfɪt] n. 利润21.residual [rɪ'zɪdjʊəl] equity剩余权益22.residual claim剩余索取权23.capital ['kæpɪt(ə)l] n. 资本24.gains [ɡeinz] n. 利得25.loss [lɒs] n. 损失26.Retained earnings留存收益27.Share premium股本溢价28.historical cost历史成本【讲解】historical [hɪ'stɒrɪk(ə)l] adj. 历史的,历史上的historic [hɪ'stɒrɪk] adj. 有历史意义的,历史上著名的28-1 replacement [rɪ'pleɪsm(ə)nt] cost 重置成本29.Balance Sheet/Statement of Financial Position资产负债表29-1 Income Statement 利润表29-2 Cash Flow Statement 现金流量表29-3 Statement of changes in owners’equity (or shareholders’equity) 所有者权益(股东权益)变动表29-4 notes [nəʊts] n. 附注PART II Financial Assets*第二部分金融资产*30.financial assets金融资产e.g. A financial instrument is any contract that gives rise to a financial asset of one enterprise and a financial liability or equity instrument of another enterprise. 【讲解】give rise to 引起,导致31.cash on hand 库存现金32.bank deposits [dɪ'pɒzɪt] 银行存款33.A/R, account receivable应收账款34.notes receivable应收票据35.others receivable其他应收款项36.equity investment股权投资37.bond investment债券投资38.derivative financial instrument衍生金融工具39.active market活跃市场40.quotation [kwə(ʊ)'teɪʃ(ə)n]n. 报价41.financial assets at fair value through profit or loss以公允价值计量且其变动计入当期损益的金融资产41-1 those designated as at fair value through profit or loss 指定为以公允价值计量且其变动计入当期损益的金融资产41-2 financial assets held for trading 交易性金融资产42.financial liability金融负债43.transaction costs交易费用43-1 incremental external cost 新增的外部费用【讲解】incremental [ɪnkrə'məntl] adj. 增量的,增值的44.cash dividend declared but not distributed 已宣告但尚未发放的现金股利投资收益45.profit and loss arising from fair value changes公允价值变动损益46.Held-to-maturity investments持有至到期投资47.amortized cost摊余成本【讲解】amortized [ə'mɔ:taizd]adj. 分期偿还的,已摊销的48.effective interest rate实际利率49.loan [ləʊn] n. 贷款50.receivables [ri'si:vəblz] n. 应收账款51.available-for-sale financial assets可供出售金融资产52.impairment of financial assets金融资产减值52-1 impairment loss of financial assets 金融资产减值损失53.transfer of financial assets金融资产转移53-1 transfer of the financial asset in its entirety 金融资产整体转移53-2 transfer of a part of the financial asset 金融资产部分转移54.derecognition [diː'rekəg'nɪʃən] n. 终止确认,撤销承认54-1 derecognize [diː'rekəgnaɪz] v. 撤销承认e.g. An enterprise shall derecognize a financial liability (or part of it) only when the underlying present obligation (or part of it) is discharged/cancelled.【译】金融负债的现时义务全部或部分已经解除的,才能终止确认该金融负债或其一部分。

会计学专业英语第一章

D

Unit 4 Information Users

Words and Expressions

Unit 1 Accounting and Accounting Profession

• 1.accounting 会计(核算); 会计学 • 2.accountant 会计师;会计人 员

• 6.operational audits 经营审计 • pliance audits 合规审计 • 8.income tax returns 所得税申 报单 • 9.nonprofit organizations 非盈 利组织 • ptroller 会计主任

• 3.bookkeeping 簿记;簿记学

• 4.chartered accountants 特许会 计师 • 5.auditing 审计;审计学

• 11.professional ethics 职业道德

• 12.proprietorship 独资企业 • 13.partnership 合伙企业 • 14.double-entry accounting

of these accountants work on a salary basis.

Unit 1 Accounting and Accounting Profession

Private accounting

Private

accountants, also called executive or administrative accountants,

Accountingபைடு நூலகம்is

often known as one of the most useful tools of business because all

会计英语(第二版)第一章中英文互译

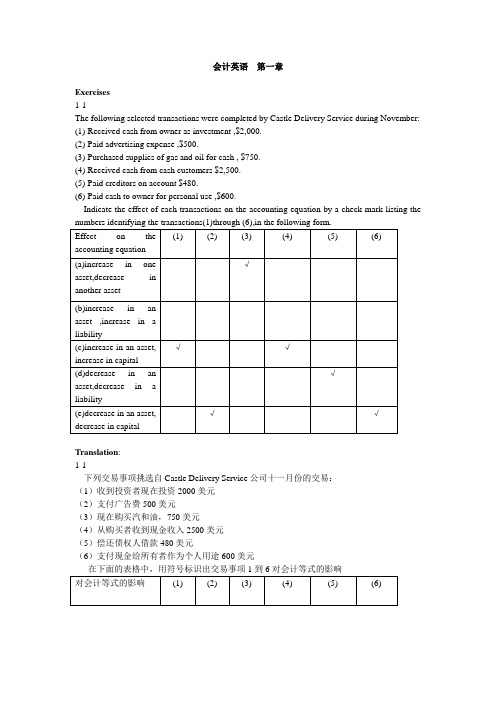

会计英语第一章Exercises1-1The following selected transactions were completed by Castle Delivery Service during November:(1)Received cash from owner as investment ,$2,000.(2)Paid advertising expense ,$500.(3)Purchased supplies of gas and oil for cash , $750.(4)Received cash from cash customers $2,500.(5)Paid creditors on account $480.(6)Paid cash to owner for personal use ,$600.Indicate the effect of each transactions on the accounting equation by a check mark listing theTranslation:1-1下列交易事项挑选自Castle Delivery Service公司十一月份的交易:(1)收到投资者现在投资2000美元(2)支付广告费500美元(3)现在购买汽和油,750美元(4)从购买者收到现金收入2500美元(5)偿还债权人借款480美元(6)支付现金给所有者作为个人用途600美元1-2Foreman Corporation, engaged in a service business , completed the following selected transactions during the period:1)Added additional investment, receiving cash2)Purchased supplies on account3)Returned defective supplies purchased on account and not yet paid for4)Received cash as a refund from the erroneous overpayment of an expense5)Charged customers for services sold on account6)Paid salary expense7)Paid a creditor on account8)Received cash on account from charge customer9)Paid cash for the owner’s personal use10)Determined the amount of supplies used during the monthTranslation :Foreman是一家从事服务行业的公司,以下是该公司在一段时间内的交易事项。

会计英语 翻译chapter1

Chapter one Introduction to Accounting 1.1 Bookkeeping and AccountingAccounting is an information system that identifies,measures,records and communicates relevant,reliable,consistent,and comparable information about an organization’s economic activity. Its objective is to help people make better decisions.An understanding of the principles of bookkeeping and accounting is essential for anyone who is interested in a successful career in business. The purpose of bookkeeping and accounting is to provide information concerning the financial affairs of a business. Owners, managers, creditors, and governmental agencies need this information.An individual who earns living by recording the financial activities of business is known as a bookkeeper, while the process of classifying and summarizing business transactions and interpreting their effects is accomplished by an accountant. Accountant is the individual who understands the accounting principles, theoretical and practical application, and can manage, analyze, and interpret the accounting records. The bookkeeper is concerned with techniques involving the recording of transactions, and the accountant’s objective is the use of data for interpretation.第一章['tʃæptə]会计导论[.intrə'dʌkʃən]1.1 簿记与会计会计是一个信息系统,[ai'dentəfai]辨别、['meʒəz]测量、记录和交流相关的['reləvənt]、可靠的[ri'laiəbl]、持续的[kən'sistənt]和可比的['kɔmpərəbl]一个组织经济活动的信息。

会计英语怎么说

会计英语怎么说会计是以货币为主要计量单位,以凭证为主要依据,借助于专门的技术方法,对一定单位的资金运动进行全面、综合、连续、系统的核算与监督,向有关方面提供会计信息、参与经营管理、旨在提高经济效益的一种经济管理活动。

那么,你知道会计的英语怎么说吗?会计的英文释义:accountingaccountanttreasureraccounting and satisicsbursaraccount会计的英文例句:那个会计向营业部的职员介绍了自己的工作情况。

The accountant described his work to the sales staff.雇会计划得来。

It would pay (you) to use an accountant.他已由仓库调到会计室任职。

He has transferredfrom the warehouse to the accounts office.会计拐走了俱乐部的资金。

The treasurer has run off with the club's funds.会计科已完全计算机化了。

The accounts section has been completely computerized.我们的经理精通会计制度。

Our manager is conversant with account system.通过分析虚假会计报告的成因,提出了治理会计报告中虚假会计信息的对策。

The ctmse of the mendacious financial report is analyzed in this paper.会计信息资源是通过会计核算建造的人造资源;It is manmade resources by the wag of accounting.会计学就是一部会计伦理学。

Accounting science is accounting ethics.会计及时卡住了这笔不必要的开支。

会计的英文翻译是什么及例句

会计的英文翻译是什么及例句会计的英文翻译是什么及例句会计是众多职业中的一种,那么会计的英文翻译是什么你了解吗?那么现在来学习关于会计的英语知识及一些相关例句吧,希望能够帮到大家!会计的英文翻译会计[kuài jì]accounting:会计;会计学;记账。

accountant:会计人员,会计师。

accountancy:会计学;会计工作,会计职业。

bookkeeper:(商人的)记账人,(政府机关等的)簿记员,会计。

bursar:(大学等的)财务主管;奖学金获得者。

会计的网络解释1、Accountant:[问题] 有税务代开的做路劳务发票(Invoice)入账的`.盼高人指点 [以下内容仅供参考] 如果金...[问题] 我们是小公司 1.职工李四用自己的现金(cash)为公司垫付给b公司账款5000,b公司发票(Invoice)没到2.收到b公司开来发票(Invoice)5000 , 3.偿还李四现金(cash)5000 会计(accountant)分录怎么做谢谢。

2、accountancy:2006年3月,ICAEW的会刊《会计》(Accountancy)公布了一份由独立机构所作的问卷调查、该问卷以反对合并的ICAEW 会员为对象,了解他们反对的理由、问卷显示,64%是担心合并会稀释C.A.在市场上的含金量,这事关会员的身份与地位.3、treasurer:办公室由会长(President)、副会长(Vice President)、秘书、会计(Treasurer)及其他所需人员组成、会长是业主协会的法人代表、会长和副会长必须是理事会理事,会长人选必须具有1年以上理事工作经验、会长的任期为1年,只可以连任1届.会计的双语例句1、据世界著名会计师事务所德勤评估,巨人网络员工平均收入水平位于行业高端。

The average salary of Giant's employees tops others'in the same industry, according to Deloitte, one of the world's leading accounting firms.2、公司内部组织机构健全,内部管理规范有序,公司主要管理制度有:公司管理手册、人事管理手册、行政后勤管理手册,工程招标代理管理手册,财务会计管理手册,公司员工业绩考评管理手册等。

李海红编著《实用会计英语第一章》中英文对照

CONTENTS 目录Chapter 1 General View of Accounting (1)第一章会计学概况Chapter 2 Forms of Business Organization (9)企业组织形式Chapter 3 Accounting Equation and Illustration (17)会计等式和举例说明Chapter 4 Accounts (24)账户(科目、账款、账目)Chapter 5 Double-Entry System (32)复式记账制(制度、体系、系统)Chapter 6 Journalizing (39)记日记账Chapter 7 Posting and Trial Balance (46)过账和试算平衡表Chapter 8 Adjustments (55)调账Chapter 9 Financial Statements (63)财务报表Chapter 10 Closing Entries (69)结账分录Chapter 11 Sales and Purchases (81)销货和购货Chapter 12 Cash and Marketable Securities (87)现金和有价证券Chapter 13 Accounts Receivable (92)应收账款Chapter 14 Notes Receivable (97)应收票据Chapter 15 Inventories (103)存货盘点to take inventories at the end of accounting period在会计期末盘点存货Chapter 16 Plant Assets (109)厂房设备资产Chapter 17 Bonds Payable (117)应付债券Chapter 18 Capital Stocks (122)股本Reference Answer (127)参考答案General View of AccountingCHAPTER 1Chapter 1General View of Accounting会计学概况As one of the oldest professions,作为历史最古老的职业之一,accounting is as old as the civilization of human.会计和人类文明一样历史悠久。

会计英语(中英对照)

Unit OneAccounting Profession第一单元会计职业INTRODUCTION OF ACCOUNTING. Accounting is a process of recorded, classifying, summarizing, and interpreting of those business activities that can be in expressed in monetary terms. A person who specializes in this field is known as an accountant.会计简介会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程。

专门从事这方面工作的人员叫做会计师。

Accounting frequently offers the qualified person an opportunity to move ahead quickly in today’s business world. Indeed, many of the heads of large corporations throughout the world have advanced to their position from the accounting department. Accounting is a basic and vital element in every modern business. It records the past growth or decline of the business. Careful analysis of these results and trends may suggest the ways in which the business may grow in future. Expan-sion or reorganization should not be planned without proper analysis of the accounting informa-tion; and new products and the campaign to advertise and sell them should not be launched with-out the help of accounting expertise.会计这一职业在当今经济社会中给有能力的人提供了升迁的机会。

会计英语 unit 1 Accounting

1.5 Professional ethics in accounting

1.1 Accounting: an information system

Accounting is an information system necessitated by the great complexity of modern business. In developing information about the activities of a business, every accounting system performs the following basic functions: ⑴ Interpret and record the effects of business transactions. ⑵ Classify the effects of similar transactions in a manner that permits determination of the various totals and subtotals useful to management and used in accounting reports. ⑶ Summarize and communicate the information contained in the system to decision-makers.

Unit One

会计,会计学 会计师,会计从业人员 簿记 企业 商业,企业 制定决策 交易,经济业务 投资者 债权人 资产

Vocabulary

liability owner’s equity / capital revenue expense income double-entry system American Institute of Certified Public Accountants (AICPA) Chinese Institute of Certified Public Accountants (CICPA)

会计英语1-14章术语翻译(仅供参考-不足之处望批评指正。)

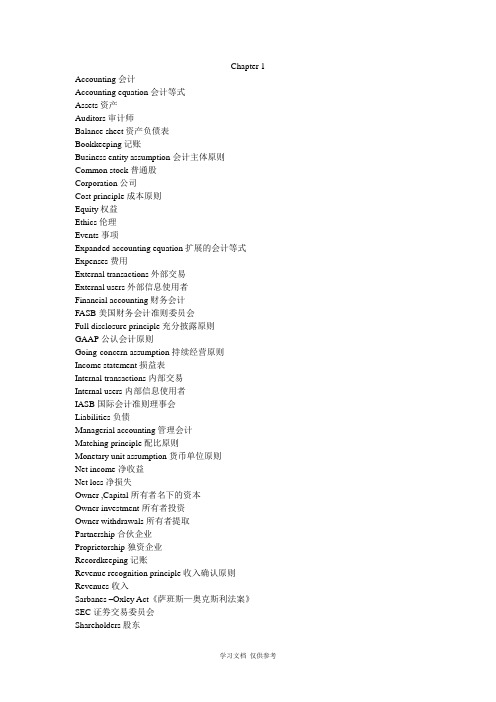

Chapter 1 Accounting会计Accounting equation会计等式Assets资产Auditors审计师Balance sheet资产负债表Bookkeeping记账Business entity assumption会计主体原则Common stock普通股Corporation公司Cost principle成本原则Equity权益Ethics伦理Events事项Expanded accounting equation扩展的会计等式Expenses费用External transactions外部交易External users外部信息使用者Financial accounting财务会计FASB美国财务会计准则委员会Full disclosure principle充分披露原则GAAP公认会计原则Going-concern assumption持续经营原则Income statement损益表Internal transactions内部交易Internal users内部信息使用者IASB国际会计准则理事会Liabilities负债Managerial accounting管理会计Matching principle配比原则Monetary unit assumption货币单位原则Net income净收益Net loss净损失Owner ,Capital所有者名下的资本Owner investment所有者投资Owner withdrawals所有者提取Partnership合伙企业Proprietorship独资企业Recordkeeping记账Revenue recognition principle收入确认原则Revenues收入Sarbanes –Oxley Act《萨班斯—奥克斯利法案》SEC证劵交易委员会Shareholders股东Shares股份Sole proprietorship个人独资企业Statement of cash flows现金流量表Statement of owner’s equity所有者权益表Stock股票Stockholders股东Time period assumption会计分期原则Withdrawals提取Chapter 2 Account账户Account balance账户余额Balance column account三栏式账户Chart of accounts会计科目表Compound journal entry复合日记账分录Credit贷方Creditors债权人Debit借方Debtors债务人Double-entry accounting复式记账法General journal普通日记账General ledger总分类账Journal日记账Journalizing 登记日记账Ledger分类账Posting过账(PR) column过账索引栏Source documents原始凭证T-account T型账户Trial balance试算平衡表Unearned revenue预收收入Chapter 3 Accounting period会计期间Accrual basis accounting权责发生制会计Accrued expenses应计费用Accrued revenues应计收入Adjusted trial balance调整后试算平衡表Adjusting entry调整分录Annual financial statements年度财务报表Book value账面价值Cash basis accounting收付实现制会计Contra account备抵账户Depreciation折旧Fiscal year会计年度Interim financial statements中期财务报表Matching principle配比原则Natural business year自然营业年度Plant assets固定资产Prepaid expenses预付费用Straight-line depreciation method直线折旧法Time period assumption会计分期原则Unadjusted trial balance调整前的试算平衡表Unearned revenues 预收收入Chapter 4 Accounting cycle会计循环Classified balance sheet分类资产负债表Closing entries结账分录Closing process结账过程Current assets流动资产Current liabilities流动负债Income summary损益汇总账户Intangible assets无形资产Long-term investments长期投资Long-term liabilities长期负债Operating cycle营业周期Permanent accounts永久性账户Post-closing trial balance结账后试算平衡表Pro forma financial statements预测财务报表Temporary accounts临时性账户Unclassified balance sheet未分类资产负债表Working papers工作底稿Work sheet工作底表Chapter 5 Cash discount现金折扣Cost of goods sold商品销售成本Credit memorandum贷记通知单Credit period 信用期Credit terms信用条件Debit memorandum借记通知单Discount period折扣期EOM月末FOB交货点General and administrative expenses一般及行政管理费用Gross margin毛利Gross profit毛利Inventory存货List price价目表价格Merchandise 商品Merchandise inventory库存商品Merchandiser商业企业Multiple-step income statement多步式损益表Periodic inventory system定期盘存制Perpetual inventory system永续盘存制Purchase discount购货折扣Retailer零售商Sales discount销售折扣Selling expenses销售费用Shrinkage损耗Single-step income statement单步式损益表Supplementary records辅助记录Trade discount商业折扣Wholesaler批发商Chapter 6 Average cost平均成本Conservatism constraint稳健性原则Consignee 收货人Consignor发货人Consistency concept一致性原则FIFO先进先出法Interim statements中期报告LIFO后进先出法LCM成本与市价孰低法Net realizable value可变现净值Specific identification个别认定法Weighted average加权平均法Chapter 7 Accounts payable ledger应付账款分类账Accounts receivable ledger应收账款分类账Cash disbursements journal现金支出日记账Cash receipts journal现金收入日记账Check register支票登记薄Columnar journal多栏式日记账Compatibility principle适应性原则Controlling account统驭账户Control principle控制原则Cost-benefit principle成本—收益原则Flexibility principle灵活性原则General journal普通日记账Internal controls内部控制Purchases journal购货日记账Relevance principle相关性原则Sales journal销售日记账Schedule of accounts payable应付账款明细表Schedule of accounts receivable应收账款明细表Special journal特种日记账Subsidiary ledger明细分类账Chapter 8 Bank reconciliation银行存款余额调节表Bank statement银行对账单Canceled checks注销支票Cash 现金Cash equivalents现金等价物Cash over and short现金溢缺Check支票Deposit ticket存款单Deposits in transit在途存款EFT电子资金转账Internal control system内部控制制度Liquid assets流动资产Liquidity偿债能力Outstanding checks未兑现支票Petty cash备用金Principles of internal control内部控制原则Sarbanes-Oxley Act《萨班斯—奥克斯利法案》Signature card印鉴卡Voucher 凭单Voucher system凭单制Chapter 9 Accounts receivable应收账款Aging of accounts receivable应收账款账龄分析Allowance for Doubtful Accounts呆帐准备金Allowance method备抵法Bad debts坏账Direct write-off method直接核销法Interest 利息Maker of the note出票人Matching principle配比原则Materiality constraint重要性约束Maturity date of a note票据到期日Payee of the note票据收款人Principal of a note票据的本金Promissory note票据Realizable value可变现价值Chapter 10 Accelerated depreciation method加速折旧法Amortization摊销Asset book value资产账面价值Betterments改进工程投资Capital expenditures资本支出Change in an accounting estimate会计估计变更Copyright版权Cost成本Declining-balance method余额递减法Depletion折耗Depreciation折旧Extraordinary repairs非常修理Franchises特许权Goodwill商誉Impairment减损Inadequacy生产能力不足Indefinite life不确定使用年限Intangible assets无形资产Land improvements土地改进物Lease租约Leasehold租赁权Leasehold improvements租赁资产改进Lessee承租人Lessor 出租人Licenses特许权Limited life有限使用年限MACRS修正后的加速成本回收制度Natural resources自然资源Obsolescence陈旧,过时Ordinary repairs日常维修Patent专利权Plant asset age固定资产寿命Plant assets固定资产Plant asset useful life固定资产使用年限Revenue expenditures收益性支出Salvage value残值Straight-line depreciation直线折旧法Trademark or trade (brand) name商标或品牌Units-of-production depreciation工作量法Useful life使用年限Chapter 11 Contingent liability或有负债Current liabilities流动负债Current portion of long-term debt一年内到期的长期负债Employee benefits职工福利Estimated liability估计负债〔FICA〕Taxes联邦社会保险税FUTA联邦失业税Gross pay薪资总额Known liabilities已知负债Long-term liabilities长期负债Merit rating考绩Net pay薪资净额Payroll deductions薪资扣款Short-term note payable短期应付票据SUTA州失业救济税Warranty保修Chapter 12Bond 债券Bond certificate债券证书Bond indenture债券契约Carrying (book) value of bonds债券账面价值Discount on bonds payable应付债券折旧Installment note分期付款期票Market rate市场利率Mortgage抵押权Pension plan养老金计划Premium on bonds债券溢价Par value of a bond债券面值Straight-line bond amortization债券利息直线摊销法Chapter 13(AFS) securities可供出售证劵Comprehensive income综合收益Consolidated financial statements合并财务报表Equity method权益法Equity securities with controlling influence具有控制权的权益类证劵Equity securities with significant influence具有重大影响力的权益类证劵(HTM) securities持有至到期证劵Long-term investments长期投资Parent母公司Short-term investments短期投资Subsidiary子公司Trading securities交易性证劵Unrealized gain (loss)未实现收益〔损失〕Chapter 14Appropriated retained earnings拨定留存收益Authorized stock核定股本Call price赎回价格Callable preferred stock可赎回优先股Capital stock股本Changes in accounting estimates会计估计变更Common stock普通股Convertible preferred stock可转换优先股Corporation股份制公司Cumulative preferred stock累积优先股Date of declaration股利宣告日Date of payment股利发放日Date of record股权登记日Discount on stock股票折旧Dividend in arrears积欠股利Financial leverage财务杠杆Large stock dividend大额股票股利Liquidating cash dividend清算性现金股利Market value per share每股市价Minimum legal capital最低法定资本Noncumulative preferred stock非累积优先股Nonparticipating preferred stock非参与式股票No-par value stock无面值股票Organization expenses组建费Paid-in capital实收资本Paid-in capital in excess of par value资本溢价Participating preferred stock参与式股票Par value面值Par value stock有面值股票Preemptive right优先认股权Preferred stock优先股Premium on stock股票溢价Prior period adjustments前期损益调整Proxy授权委托书Restricted retained earnings限定用途留存收益Retained earnings 留存收益Retained earnings deficit留存收益赤字Reverse stock split并股Small stock dividend小额股票股利Stated value stock设定价值股票Statement of stockholders’ equity股东权益表Stock dividend股票股利Stock options股票期权Stock split股票分割Stockholders’ equity股东权益Treasury stock库藏股。

会计概念中英文

1-1 accounting:会计1-1 financial statement:会计报表,财务报表1-1 Balance Sheet:资产负债表1-2 entity:会计实体1-4 financial position:财务状况1-6 asset:资产1-6 liabilities:负债1-6 equity:权益1-7 cash:现金1-9 fund:资金;基金,专款1-10 obligation:义务,责任;偿还债务的责任1-10 creditor:债权人1-10 credit:信用,信贷1-10 supplier:供应商1-10 amount:数量,金额1-10 accounts payable:应付账款1-10 payable:应付的1-11 clai:M债权,要求权1-11 current:流动的,短期的1-13 common stock:普通股1-13 paid-in capital:实收资本1-14 profit:利润1-14 earnings:营业利润,盈利,收益1-14 dividend:股利1-14 retained earnings:留存收益1-15 due:欠款的,应付的1-15 residual clai:M剩余要求权B1-16 dual-aspect concept:复式簿记原则1-20 balance:(使资产负债表两边)平衡(即资产=负债+所有者权益)1-20 accountant:会计师,会计专家,审计员1-22 accounting concept:会计原则1-24 bank account:银行往来账户1-26 net assets:净资产B1-27 money-measurement concept:货币核算原则1-28 supplies:物料用品B1-34 entity concept:会计实体原则1-34 account:账户1-34 withdraw:提款,提取(资金)1-34 withdrawal:提款1-35 sole owner:独资经营者,个体户N1-38 corporation:法人,公司N1-38 partnership:合伙企业N1-38 proprietorship:独资企业1-39 deposit:存款B1-40 going-concern concept:持续经营原则1-41 concern:公司(对工商企业的一般称呼)N1-43 monetary asset:货币资产N1-43 fair value:公平价值N1-43 nonmonetary asset:非货币资产N1-43 cost:成本B1-44 asset-measurement concept:资产核算原则1-44 market value:市场价值,市价1-45 marketable securities:有价证券,适销证券1-45 stock exchange:证券交易所1-49 depreciation:折旧1-50 inventory:存货1-56 bond:债券1-62 cash register:现金出纳机1-62 petty cash:零用现金N1-64 lease:租赁N1-64 capital lease:资本租赁1-65 contract:合同,契约1-67 trademark:商标N1-69 noncurrent:非流动的1-70 current asset:流动资产1-74 current liabilities:流动负债1-74 become / fall due:到期1-75 repay:偿付B1-77 current ratio:流动比率1-77 meet one's obligations:偿债1-80 share:份额,股份,股票1-80 shareholder:股东1-80 stockholder:股东1-80 ownership:所有权1-81 additional paid-in capital:资本溢价,实收资本溢价,追加缴入资本1-82 transaction:交易1-83 profitable:赚钱的,有利可图的,盈利的1-86 operating activity:经营活动1-P20 goodwill:商誉PT1Q19 insurance policy:保单PT1Q19 prepaid expense:预付费用PT1Q20 plant and property:固定资产PT1Q22 accounts receivable:应收账款2-2 securities:有价证券2-2 stock:股票,股份;存货,库存2-2 Treasury:财政部(英美常用,其他国家多用Ministry of Finance)2-2 treasury bonds:长期国债(由英、美政府发行的长期债券)N2-3 investment in safe:保值投资,安全投资= safe investmenTN2-3 money market fund:货币市场基金N2-3 cash equivalent:现金等价物2-5 goods:货物2-5 raw material:原材料2-5 partially finished product:半成品2-5 resale:转卖,转售2-8 intangible asset:无形资产2-10 tangible asset:有形资产2-11 property, plant and equipment:财产、厂房与设备,固定资产2-12 accumulated depreciation:累计折旧2-15 patent:专利权2-15 brand:商标,品牌,牌子2-15 logo:(企业、公司等的)专用标识、标记、商标(如用于广告中的)2-20 bank loan:银行借款2-20 promissory note:本票,期票N2-20 accrued liabilities:应计负债2-21 tax liability:应纳税款2-22 long-term debt:长期债务N2-24 income tax:个人所得税;(美)也指公司所得税N2-24 deferred income tax:递延所得税2-37 note:票据;现钞,钞票2-37 note payable:应付票据2-37 note receivable:应收票据2-43 double-entry:复式记账,复式簿记2-51 sell at a profit:含利销售2-53 vendor:卖方2-55 on credit:信用交易,赊账2-57 mortgage:抵押贷款,按揭贷款2-57 balance:余额2-59 offer:递价,出价;出售,发盘2-62 interest:利息;权益B2-64 income:收入,收益,利润2-68 financial information:财务信息2-68 income statement:损益表= profit and loss accoun T2-72 revenue:收入2-73 expense:费用2-81 surplus:盈余,利润N2-81 sales revenue:销售收入N2-81 interest revenue:利息收入N2-81 salary expense:工资费用N2-81 rent expense:租金费用2-P44 amortization:摊销,分期偿还3-4 Beg. Bal.:期初余额= Beginning balanceB3-26 debit:n. 借方;v. 借记B3-26 credit:n. 贷方;v. 贷记N3-36 entry:会计分录3-38 net income:净收益N3-38 gross income:总收益,毛收益N3-38 operating income:营业收益B3-43 ledger:总账,总分类账B3-43 journal:日记账3-49 posting:过账B3-51 closing:结账,结转3-62 temporary account:临时性账户3-62 permanent account:永久性账户3-63 maintenance expense:维修费用3-P64 check:支票3-P64 chart of accounts:会计科目表,账户一览表,科目汇总表3-P64 bookkeeper:簿记员,记账员3-P66 inflow:流入3-P66 outflow:流出B4-3 fiscal year:财务年度,财政年度,财年4-4 interim statement:中期报表,期中报表B4-6 accrual accounting:权责发生制会计,应计制会计4-14 cash accounting:现金会计B4-18 conservatism concept:稳健性原则,保守性原则N4-18 materiality concept:重要性原则N4-18 realization concept:收入实现原则4-38 salesperson:推销员4-44 advances from customers:预收客户款N4-47 deferred revenue:递延收入N4-47 precollected revenue:预收收入N4-47 unearned revenue:未获收入4-53 rental revenue:租金收入N4-57 installment sales:分期收款销售4-59 bad debt:坏账4-65 allowance for doubtful accounts:坏账准备= allowance for bad debtsN4-65 contra-asset account:资产备抵账户,资产对销账户4-66 bad debt expense:坏账费用4-69 write off:撤销(债务);冲销,注销4-70 sales:销售额,销售量4-74 days' sales uncollected:日销货未收款率,应收账款回收天数= average collection periodPT4Q11 allowance for bad debts:坏账准备= allowance for doubtful accountsB5-3 expenditure:支出,开支B5-15 unexpired cost:未耗成本B5-15 expired cost:已耗成本B5-19 matching concept:配比原则5-27 prepaid insurance:预付保险费5-31 prepaid rent:预付租金5-34 depreciation expense:折旧费用5-35 disbursement:付款5-37 accrued salaries:应计未付工资N5-38 withhold:扣款,扣缴N5-38 social security tax:社会保险税,社会福利税B5-40 fringe benefits:附加福利5-40 pension:养老金,退休金,补助金5-40 pension benefit:退休津贴,退休费5-40 accrued pension:应计养老金5-41 pension expense:养老金费用5-43 other post-employment benefits:其他就业后福利(abbr. OPEB)5-45 accrued rent:应付租金,应计租金B5-50 loss:损失,亏损5-58 deed:契约,证书5-59 down payment:定金,首期付款5-61 commission:佣金N5-68 profit and loss statement:损益表= income statement = profit and loss account N5-68 earnings statement:损益表= income statement = profit and loss account5-70 cost of sales:销售成本5-71 gross margin:毛利,边际贡献,贡献毛益5-72 operating expense:营业费用5-72 income before tax:税前收益5-74 provision for income tax:备付所得税,所得税准备5-75 net loss:净损失N5-86 statement of cash flows:现金流量表5-87 gross margin percentage:毛利率5-89 net income percentage:净收益率6-1 manufacturing company:制造业公司6-1 cost of goods sold:销货成本6-2 specific identification method:个别辨认法,分批认定法6-5 shipment:运送,运送货物6-5 perpetual inventory:永续盘存B6-9 deduction method:扣减法N6-10 point of sale:销售点6-13 goods available for sale:可销售货物6-16 physical inventory:实地盘存,实物盘存N6-17 loss on inventory:存货损失6-18 shrinkage:缩水,损耗B6-22 inventory valuation:存货估价B6-27 first-in first-out method:先进先出法FIFO6-27 financial accounting:财务会计B6-32 last-in first-out method:后进先出法LIFOB6-35 average-cost method:平均成本法6-39 taxable income:应税所得,应纳税所得额,应税收益6-43 write down:减记6-46 merchandising company:商业公司6-47 finished goods:成品,制成品,产成品= finished product 6-48 invoice:发票6-48 conversion cost:加工成本6-49 finished product:成品,制成品,产成品= finished goods 6-49 overhead:间接费用,管理费用6-50 direct material:直接材料6-50 direct labor:直接人工N6-51 other production cost:其他生产成本6-53 cost accounting:成本会计B6-54 product cost:产品成本B6-54 period cost:期间成本B6-59 overhead rate:间接费用分配率6-59 indirect cost:间接成本N6-63 activity-based costing:作业成本法N6-63 cost driver:成本动因B6-64 inventory turnover:存货周转,存货周转率7-3 fixed assets:固定资产B7-5 acquisition:获得(或购买)行为,购置,收购7-6 broker:经纪人7-7 freight:运费7-9 lessor:出租人7-9 lessee:承租人7-16 service life:使用年限,耐用年限,使用寿命7-20 obsolescence:陈旧过时7-25 residual value:残值,剩余价值7-28 depreciable cost:应计折旧成本N7-29 units-of-production depreciation:产量折旧法,生产单位折旧法N7-29 straight-line depreciation:直线折旧法N7-29 accelerated depreciation:加速折旧法7-33 depreciation rate:折旧率7-46 book value:账面价值7-56 gain ( or loss ) on disposition of plant:固定资产处理收益(或损失)B7-62 depletion:递耗,折耗7-62 wasting asset:递耗资产B8-1 working capital:营运资本,营运资金,周转资金8-5 permanent capital:永久资本B8-7 debt capital:债务资本,借入资本8-9 face amount:票面金额,面额8-12 principal:本金8-16 portfolio:投资组合8-16 derivative:衍生工具,衍生产品8-21 shareholders' equity:股东权益8-22 common shareholder:普通股股东8-22 preferred shareholder:优先股股东8-22 preferred stock:优先股N8-22 limited partnership:有限责任合伙企业N8-22 trust:信托,托拉斯N8-22 S corporation:S公司8-23 par value:票面价值,面值8-26 no-par-value stock:无面值股票8-26 director:董事8-26 stated value:设定价值8-28 treasury stock:库存股份,库存股票8-28 outstanding stock:未清偿股票8-35 liquidate:清算,清盘8-43 net worth:净值,资本净值8-47 stock dividend:股票股利8-48 stock split:股份拆细,分股8-60 leverage:杠杆,杠杆作用,杠杆效应B8-62 debt ratio:债务比率,负债比率B8-65 consolidated financial statement:合并会计报表,合并财务报表8-65 parent:母公司8-65 subsidiary:子公司8-69 intrafamily transaction:家族内交易8-75 minority interest:少数股东权益9-3 accrual basis:权责发生制,应计制N9-3 liquidity:流动性,变现能力,清偿能力N9-3 solvency:偿债能力N9-7 cash flow from operating activities:营业活动现金流量N9-7 cash flow from investing activities:投资活动现金流量N9-7 cash flow from financing activities:筹资活动现金流量B9-8 cash basis:收付实现制,现金收付制N9-15 double counting:重复计算9-17 administrative expense:管理费用9-19 credit sale:赊销,递延付款销售9-22 End. Bal.:期末余额= Ending balance9-40 cash flow statement:现金流量表= statement of cash flows9-43 net:净得,净赚(某利润等)9-50 breakdown:分解,分类剖析9-53 mortgage bond:抵押债券,按揭债券N9-53 redemption:偿还,赎回N9-56 Generally Accepted Accounting Principles:公认会计准则= GAAP N9-56 disposition:财产分配[遗产税]N9-63 free cash flow:自由现金流量N9-63 replacement:重置N9-63 cushion:余量9-P183 proceeds:收入,进款9-P184 financial crisis:财务危机10-6 auditing:审计,核数10-6 certified public accountant:注册会计师,执业会计师= CPA10-6 auditor:审计师,核数师N10-10 clean opinion:无保留意见[指审计报告]N10-10 unqualified opinion:无保留意见[指审计报告]N10-10 exception:审计异议,例外N10-10 qualified opinion:有保留意见[指审计报告]N10-10 qualification:附条件声明N10-10 suspend trading:停牌10-11 return on equity:权益报酬率,净资产收益率= ROE10-15 benchmark:基准,标杆10-26 profit margin percentage:毛利率;利润率,净利率10-43 quick ratio:速动比率,酸性测试比率= acid test ratio = liquidity ratio 10-43 acid test ratio:速动比率,酸性测试比率= quick ratio = liquidity ratio 10-45 capitalization:资本化10-50 earnings per share:每股收益= EPS10-53 price-earnings ratio:市盈率= P/E ratio = PER10-56 return on permanent capital:永久资本回报率,永久资本收益率10-56 return on investment:投资回报率,投资收益率= ROI10-57 pretax income:税前收益,税前利润10-58 EBIT:息税前利润,息税前收益= earnings before interest and tax 10-59 EBIT margin:EBIT利润率10-62 capital turnover ratio:资本周转率10-63 capital intensive:资本密集型10-69 fixtures:固定装置,装置,装修10-72 insolvency:无偿债能力,无力偿付10-80 real earnings:实际收益10-84 foreign operation:国外业务,境外业务10-85 red flag:红色报警信号10-86 accounting practice:会计实务,会计惯例B10-88 accountability:经营责任,问责性;负责B10-88 corporate governance:公司治理,公司管治,公司管制10-88 board of directors:董事会,董事局10-89 public company:公众公司,公开公司10-89 Securities and Exchange Commission:[美]证券交易委员会= SEC 10-90 publicly-traded company:股份公开交易的公司10-93 public accounting firm:会计师事务所B11-1 nonprofit organization:非营利组织11-7 accumulated surplus:累计盈余,累积盈余,滚存盈余11-8 statement of financial position:财务状况表11-8 statement of activities:业务活动情况表,业务报表,活动报表N11-14 balanced scorecard:平衡计分卡11-16 permanently restricted net asset:永久受限制净资产11-16 temporarily restricted net asset:暂时受限制净资产11-16 unrestricted net asset:不受限制净资产11-35 endowment:捐款,资助11-43 fee:报酬;付给专业人员(如会计师、医生、律师等)的工作酬金B11-46 transfer:转移B12-1 Government Accounting Standards Board:政府会计准则委员会= GASB12-12 Financial Accounting Standards Board:财务会计准则委员会= FASB12-13 Federal Accounting Standards Advisory Board:联邦会计准则咨询委员会= FASAB 12-16 budget:预算12-16 Office of Management and Budget:预算管理委员会= OMB12-18 stewardship:保管责任12-34 interperiod:跨期的。

会计英语第一章

-------------- What is Accounting?

1.1

What is Accounting

1.2

1.3 1.4

The Role of Accounting

Accounting and Bookkeeping The Accounting Process

1.5

Accounting Today

Accounting is the basic for decision making. Its purpose is to provide useful information to a variety of users so they can make informed decisions.

会计是决策的基础。它的目的是向大量的 用户提供有用的信息,从而让他们做出正 确的决策。

The Difference Between Accounting and Bookkeeping Bookkeeping Bookkeeping is the clerical side of accounting——the recording of routine transactions and day-to-day record keeping. Today such tasks are performed primarily by computers and skilled clerical personnel, not by accountant.

Basic Function of an Accounting 1.1.2 An information system System:

(1) Interpret and record the effects of

会计英语第1章

Chapter 1 Overview of Accounting

1.1 Accounting and Accounting Profession

Accounting is an information system designed to identify, record, and reflect economic activities and events about an enterprise with monetary unit as its main criterion.

◦ Different external users need different kinds of information.

1.1.4 Accounting Profession

The accounting profession can be divided into three broad categories: public accounting, private accounting, and accounting for government and nonprofit organizations.

The primary objective of accounting is to provide useful information to decision makers.

1.1.1 Ethics

Ethic is an ideological standard by which one’s conducts are judged as right or wrong, honest or dishonest, and fair or not fair.

As the basic premise of accounting, it’s of great significance to identify the business entity.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Chapter one Introduction to Accounting 1.1 Bookkeeping and AccountingAccounting is an information system that identifies,measures,records and communicates relevant,reliable,consistent,and comparable information about an organization’s economic activity. Its objective is to help people make better decisions.An understanding of the principles of bookkeeping and accounting is essential for anyone who is interested in a successful career in business. The purpose of bookkeeping and accounting is to provide information concerning the financial affairs of a business. Owners, managers, creditors, and governmental agencies need this information.An individual who earns living by recording the financial activities of business is known as a bookkeeper, while the process of classifying and summarizing business transactions and interpreting their effects is accomplished by an accountant. Accountant is the individual who understands the accounting principles, theoretical and practical application, and can manage, analyze, and interpret the accounting records. The bookkeeper is concerned with techniques involving the recording of transactions, and the accountant’s objective is the use of data for interpretation.第一章['tʃæptə]会计导论[.intrə'dʌkʃən]1.1 簿记与会计会计是一个信息系统,[ai'dentəfai]辨别、['meʒəz]测量、记录和交流相关的['reləvənt]、可靠的[ri'laiəbl]、持续的[kən'sistənt]和可比的['kɔmpərəbl]一个组织经济活动的信息。

它的目标是帮助人们做出更好的决定。

对在商业事业取得成功感兴趣的人,对账簿和会计的原理['prinsəpl]的理解是必要的[i'senʃəl]。

账簿和会计的目的['pə:pəs]是提供消息关于[kən'sə:niŋ]一个企业的财务事务。

业主,经理,债权人['kreditə],和政府的代理['eidʒənsi]需要这些消息。

一个个体[.indi'vidjuəl]通过记录企业的财务信息赚取生计(earn living)是簿记员;分类['klæsifai]与汇总企业交易[træn'zækʃənz]和解释[in'tə:pritiŋ]它们影响[i'fekt]的过程是被会计完成[ə'kɔmpliʃt]的。

会计师是知道会计准则、理论[θiə'retikəl,]与实际['præktikəl]应用[.æpli'keiʃən],能够管理、分析和解释会计记录的人。

簿记员涉及(is concerned with)一些技术[tek'ni:k]包括记录交易,会计师的目的是使用数据作解释[in.tə:pri'teiʃən]。

1.2 The Field of Professional AccountingThere are three fields of professional accounting.Public accounting is an area of accounting where accountants perform their services for the general public rather than for a single organization. The basic services provided by a public accountant are auditing and preparing tax reports, assisting in various tax problems, and making recommendations for business decisions.Most of the people in the public accounting are licensed as certified public accountants(CPAs).Almost all countries in the world have laws for the CPAs. In USA, the certification examinations are prepared and administrated by the American Institute of Certified Public Accountant (AICPA).The equivalent of a CPA in UK is called a chartered accountant. Chinese Institute of Certified Public Accountants (CICPA) is responsible for administrating Chinese CPAs.Private accounting is an area of accounting where accountants perform their services for a single organization. The private accountant maintains the accounting records and provides management with financial data needed for business decisions.Accountants provide services to all types of business entities. It is important, therefore, that you are familiar with the characteristics of the different forms of business organization. The three forms of business ownership are clearly presented in the text and are summarized as follows. 1.2 专业会计领域专业会计包含三个方面。

公共会计是会计的一个领域,会计师提供他们的服务给公众(general public)而不是一个单一的组织。

公共会计师提供的基础服务是审计['ɔ:ditiŋ]和准备税务报告,辅助各种税务问题,为商务决策提供建议[.rekəmen'deiʃən]。

从事公共会计的大多数人都是得到领有执照的['laisənst]注册会计师['sə:ti.faid]。

世界上几乎所有的国家都有关于CPA的法规。

在美国,认证考试(certification examinations)是由美国会计师协会['institju:t]准备与实施[əd'ministreit]的。

CPA相当于[i'kwivələnt]英国的特许['tʃɑ:təd]会计师.中国注册会计师协会对中国注册会计师负责。

私用['praivit]会计是会计的一个领域,会计师提供他们的服务给单一的企业。

私用会计维护[mein'tein]会计信息,为管理部门提供企业决策所需要的财务数据。

会计师提供服务于所有类型的商务实体。

它是重要的,因为,你必须熟悉(be familiar with)商务组织不同形态的特点。

企业所有权(business ownership)的三种形式在文章中被清楚地阐述,概述['sʌməraiz]如下。

A single or sole proprietorship is a business that is owned by one individual but is not established as a separate entity under the law.A partnership differs from a single proprietorship only in that it has more than one owner. The owner or owners of proprietorships and partnerships are personally liable for the debts of the business.A corporation is established under the law as a separate entity,hence, its owners (shareholders) are not liable for the debts of the corporation.The chief accounting officer in a medium-sized or large business is usually called the controller, who manages the work of the accounting staff. The work of accountant in a private business mainly includes the design of accounting system, cost accounting, internal control and auditing.Government and nonprofit accounting is an area of accounting where accountant perform their service for local, state,and federal governmental agencies, as well as for nonprofit organizations. The government accountant performs all the functions of private or public accountant. Nonprofit organizations include universities, hospitals, churches, symphony orchestras, charitable organization and so on. Nonprofit accounting follows a pattern of accounting that is similar to governmental accounting.个人独资企业[prə'praiətə.ʃip]是在法律下个人独有的[.indi'vidjuəl]而不是被作为单独实体(separate entity)被确立[is'tæbliʃt]的企业。