DOW三乙醇胺, 99%(TRIETHANOLAMINE)

中世纪2全面战争城市名

一,全面战争都柏林Dublin 英伦三岛因弗内斯Inverness爱丁堡Edinburgh约克York诺丁汉Nottingham伦敦London卡那封Caernarvon弗莱昂Leon 欧洲潘普洛纳Pamplona里斯本Lisbon托莱多Toleda科尔多瓦Cordoba萨拉戈萨Zaragoza瓦伦西亚Valencia格兰纳达Granada卡昂Caen布鲁日Bruges安特卫普Antwerp雷恩Rennes昂热Angers巴黎Paris兰斯Rheims波尔多Bordeaux图卢兹Toulouse第戎Dijon马塞Marseille梅斯Metz奥尔胡斯Arhus汉堡Hamburg法兰克福Frankfurt马格德堡Magdeburg纽伦堡Nuremburg霍亨斯道芬Hohenstauffen 伯尔尼Bern米兰Milan热那亚Genoa阿雅克修Ajaccio卡利亚里Cagliari巴勒莫Palermo因斯布鲁克Innsbruck威尼斯Venice博洛尼亚Bologna佛罗伦萨Florence罗马Rome那不勒斯Naples斯德丁Stettin布拉格Prague维也纳Vienna萨格勒布Zagreb布莱斯劳Breslau克拉科夫Krakow布达佩斯Budapest拉古萨Ragusa都拉佐Durazzo科林斯Corinth索恩Thorn加利奇Halych布朗Bran索非亚Sofia萨瑟洛尼亚Thessalonica 赫尔辛基Helsinki里加Riga维尔纽斯Vilnius基辅Kiev雅西Iasi布加勒斯特Bucharest诺夫哥罗德Novgorod斯摩棱斯克Smolensk卡法Coffa君士坦丁堡Constantinople奥斯陆Oslo斯德哥尔摩Stockholm莫斯科Moscow梁赞Ryazan保加尔Bulgar萨克尔Sarkell伊拉克里翁Iraklion 欧亚交接三岛罗德Rhodes尼科西亚Nicosia马拉喀什Marrakesh 北非及西亚阿尔及尔Algiers突尼斯Tunis的黎波里Tripoli阿尔金Arguin延巴克图Timbuktu 尼西亚Nicaea士麦那Smyrna西泽利亚Caesarea 伊康Iconium阿达纳Adana特拉比松Trebizond 第比利斯Tbilisi埃里温Yerevan埃德萨Edessa摩苏尔Mosul安条克Antioch阿勒颇Aleppo巴格达Baghdad阿克里Acre大马士革Damascus 耶路撒冷Jerusalem 加沙Gaza亚历山大Alexandria 开罗Cario栋古拉Dongola吉达Jedda二,美洲风云古巴Cuba韦拉克鲁斯Vera_Cruz蒂科斯特拉Tixtla韦拉克鲁斯VeraCruz_r特诺奇蒂特兰Tenochtitlan_r 瓦斯特佩克Huaxtepec_r托兰Tula_r特瓦坎Tehuacan_r蒂科斯特拉Tixta_r托奇潘Tuxpan_r塔尼切卡奇Danipaguache_r 米克特兰Mitla_r特宽特佩克Tehuantepec_r 奇琴伊察Chichen_Itza_r乌斯马尔Uxmal_r坎佩克Canpech_r蒂卡尔Tikal_r特拉斯卡拉Tlaxcala_r阿帕钦甘Apatzignan_r萨卡普Zacapu_r萨卡特卡斯Zacatecas_r科洛坦Colotan_r阿帕奇Apache_r夸特莫克Cuahtemoc_r阿瓦卡特兰Ahuacatlan_r科奇米Cochimi_r库利亚坎Culiacan_r纳瓦霍Navojoa_Region科曼奇Comanche_r科阿韦拉Coahulia_r阿瓜帕拉姆Aguapalam_r奇瓦瓦Chihuahua_r皮蒂科Pitic_r卡多Caddo_r乔克托Choctaw_r密克苏基Miccosoukee_r卡卢萨Calusa_r特奇斯塔Tequesta_Region 亚马科洛Yamacraws_Region阿里巴姆Alibamu_Region奇克索Chickasaw_Region通瓦Tongva_Region奥科特兰Ocotlan_r特科曼Tecoman_r托洛坎Toluca_r切图马尔Chetumal_r希拉兰科Xicalango_r波顿昌Potochan_r乔鲁拉Cholula_r夸赛夸尔科斯Coatzalcoalcos_r 阿顿哈Althun_Ha_r雅克奇兰Yaxchilan_r托奇特兰Tuxtla_r特鲁希略Trujillo_r托托特佩克Tututepec_r特拉科奇卡潘Tegucigalpa_r基里瓜Quirigua_r希拉杰Quezaltenango_r哈瓦纳Havana三,英伦霸主伦敦London_Region汉普郡Hampshire_Region萨里-萨塞克斯Surry_and_Sussex_Regions 东盎格鲁East_Anglia诺丁汉Nottinghamshire牛津Oxford_Region肯特Kent_Region康沃尔Cornwall_Region多塞特Dorsetshire_Region韦斯特West_Country摩根维格Morgannwg_Principality什罗普Shropshire_Region柴Cheshire_Region林肯Lincolnshire兰开夏Lancashire坎伯兰Cumberland_Region诺森伯兰Northumberland伦斯特Leinster_Region米斯Meath_Region约克Yorkshire康诺特Connaught_Region阿尔斯特Ulster_Province芒斯特Munster_Region唐Down_Region托蒙德Thomond_Region泰孔内尔Tyrconnel_Region格温内斯Gwynedd_Principality波厄斯Powys_Principality德赫巴思Deheubarth_Principality珀斯Perth_Region拉纳克Lanark_Region斯特林Stirling_Region高地Highlands_Region洛锡安Lothian_Region阿伯丁Aberdeen_Region邓弗里斯Dumfries_Region曼岛Isle_of_Man奥克尼Orkney_Region凯斯内斯-萨瑟兰Caithness_and_Sutherland_Regions外赫布里底Outer_Hebrides 马尔Isle_of_Mull阿伦Isle_of_Arran艾莱Isle_of_Islay_Region西高地West_Highlands斯凯Isle_of_Skye_Region阿盖尔-比特Argyle_and_Bute 阿伦德尔Arundel阿森莱Athenry坎特伯雷Canterbury加的夫Cardiff卡莱尔Carlisle卡斯尔顿Castle_Town切斯特Chester卡纳封Caernarvon科克Cork德里Derry唐帕特里克Downpatrick都柏林Dublin邓斯代夫纳奇Dunstaffnage 爱丁堡Edinburgh格拉斯哥Glasgow格洛斯特Gloucester因弗洛克莱Inverlochly因弗内斯Inverness柯克沃尔Kirkwall兰开斯特Lancaster朗塞斯顿Launceston斯托诺韦Lewis利福德Lifford蒙哥马利Montgomery泰恩-纽卡斯尔Newcastle_Upon_Tyne 诺里奇Norwich彭布罗克Pembroke沙夫茨伯里Shaftsbury什鲁斯伯里Shrewsbury蒂珀雷里Tipperary特里姆Trim威克Wick温切斯特Winchester四,天国王朝阿拜多斯Abydos_Region阿克里Acre_Province阿达纳Adana_Province巴士拉Al_Basrah苏伊士Al_Suways阿兰亚Alanya_Region阿勒颇Aleppo_Province亚历山大利亚Alexandria_Province 阿利耶Alia_Region阿摩利阿姆Amorium_Region安卡拉Ankara_Region安条克Antioch_Province贝尼海尔拉营地Arab_Camp_2贝尼哈立德营地Arab_Camp_3贝尼苏雷姆营地Arab_Camp_6贝尼海尔拉部落Tribelands2贝尼哈立德部落Tribelands3贝尼苏雷姆部落Tribelands6阿苏夫Arsuf_Region阿什凯隆Ascalon_Region阿塔雷亚Attaleia_Region巴勒贝克Baalbek_Region巴格达Baghdad_Province班亚斯Banyas_Region巴士拉Basra_Region凯撒里亚Caesarea_Province开罗Cairo_Province君士坦丁堡Constantinople_Province 乔鲁姆Corum_Region大马士革Damascus_Province迪亚巴克Diyabakir_Region多利留姆Doryleum_Region杜姆亚特Dumyat_Region埃德萨Edessa_Province赫拉克利亚Heraclea_Region霍姆斯Homs_Region伊康Iconium_Province伊拉克吕翁Iraklion克里特Isle_of_Crete罗德Isle_of_Rhodes贝尼苏莱曼Jedda_Province耶路撒冷Jerusalem_Province卡拉克Kerak_Region克尔曼沙阿Kermanshah_Region基尔库克Kirkuk_Region克尔谢希尔Kirsehir_Region骑士堡Krak_de_Chavliers_Region库法Kufa_Region莱迪西亚Laodicea_Region利马索尔Limassol马拉蒂亚Malatya_Region摩苏尔Mosul_Province尼西亚Nicaea_Province尼科西亚Northern_Cyprus帕拉伊奥卡斯通Palaeokastron_Region 克瑞西亚Qarisiya_Region拉卡Raqqa_Region罗德Rhodes塞巴斯蒂亚Sebastea_Region锡诺普Sinope_Region锡瓦Siwa_Region士麦那Smyrna_Province利马索尔Southern_Cyprus苏伊士Suways_Region大不里士Tabriz_Region塔克利特Takrit_Region坦塔Tanta_Region第比利斯Tbilisi_Province塞奥多西奥波利斯Theodoiopolis_Region 特拉布宗Trebizond_Province的黎波里Tripoli_Province提尔Tyre_Region凡城Van_Region埃里温Yerevan_Province五,条顿悲哀奥尔胡斯Aarhus阿博Abo阿格德Agder_Region阿克什胡斯Akershus阿伦斯伯格Arensburg_Region巴拉诺维奇Baranavichy_Region 比亚韦斯托克Bialystok_Region 波希米亚Bohemia瑞典中部Central_Sweden切尔尼戈夫Chernigov_Region切尔诺贝利Chornobyl_Region克兰德Corland克拉科夫Cracow琴斯托霍瓦Czestochowa_Region 但泽Danzig丹麦Denmark_Region多克西泽Dokshitsy_Region多瑙堡Dunaburg芬兰Finland_Region格尔利茨Gorlitz_Region哥德堡Goteborg哥特兰Gotland哈尔姆斯塔德Halmstad_Region汉堡Hamburg汉诺威Hannover_Region海斯勒霍尔姆Hassleholm_Region 霍夫Hof_Region戈梅利Homyel_Region格罗德诺Hrodna_Region贾兹都Jazdow卡尔马Kalmar_Region考纳斯Kaunus_Region霍尔姆Kholm_Region基辅Kiev_Region克沃兹科Klodzko_Region柯尼希堡Konigsberg_Region科沙林Koszalin_Region利沃夫L_vov_Region利达Lida_Region立陶宛Lithuania琉博莫Liuboml_Region立窝尼亚Livonia马格德堡Magdeburg_Region马林堡Marienburg_Region马素比亚Masovia姆格林Mglin_Region明斯克Minsk_Region姆斯季斯拉夫尔Mstislavl_Region 纳尔瓦Narva_Region新斯德丁Neustettin_Region普斯科夫North_Pskov_Region 德意志Northern_Germany挪威Norway_Region诺夫哥罗德Novgorod_Region奥里斯塔Olysta_Region帕兰加Palanga_Region帕涅韦日斯Panevezys_Region 派尔努Parnu_Region波尔瑙Pernau平斯克Pinsk_Region普沃茨克Plock_Region波美拉尼亚Pomerania波茨坦Potsdam_Region波兹南Poznan布拉格Prague普热沃斯克Przeworsk_Region普斯科夫Pskov雷瓦尔Reval_Region里加Riga罗斯基勒Roskilde希奥利艾Siauliai_Region斯卡拉Skara_Region斯摩棱斯克Smolensk_Region 波兰Southern_Poland瑞典Southern_Sweden斯德丁Stettin施特拉尔松德Stralsund_Region 索恩Thorn_Region廷韦拉Tingvalla_Region托斯诺Tosno_Region图罗夫Turov_Region于尔岑Uelzen_Region乌普萨拉Uppsala大卢基Velikiye_Luki_Region维尔纽斯Vilnius维斯比Visby维捷布斯克Vitebsk_Region波兰West_Poland波美拉尼亚West_Pomerania温道Windau_Region西兰Zealand日托米尔Zhytomyr_Region泽布斯托夫Zubstov_Region[文档可能无法思考全面,请浏览后下载,另外祝您生活愉快,工作顺利,万事如意!]21 / 21。

魔兽世界3.22单机版GM命令

.leve lup 70 为目标(或自己)增加70级.quest comp lete.a ddite mset增加套装.b ank 打开仓库.ma xskil l 将已会技能学至300/300 (单手剑熟练度..等).modif y mon ey 9999999给自己加金钱,后面空一格加数字,数字是以铜为单位的,.addit em 增加物品后面加相应的物品代码。

.npc add添加NPC刷怪.KILL杀死所选中的NPC(声望点数要受影响).DEL删除所选中物件(声望点数不受影响).gps 显示角色或生物的坐标(x,y,z) 地图标号和地区.re vive复活,先选中自己(可以用公会聊天模式输入 /o).mo difyhonor增加荣誉,数字自己调.s tart传回到你的出生点卡号自救.lear n 674学习双手武器.nameg o 召唤玩家到自己的当前位置.add item990001 随身宝石.a ddite m 21876 包包.le arn 32345召唤凤凰!顶级飞行坐骑.m odify morp h 变形例如:.modif y mor ph 21135 .demo rph 取消变形.hove r 腾空(变形为伊利丹后很帅).hover off取消腾空.exp lorec heat1 地图作弊,打开全部地图魔兽.lear n 7600 提高致命一击 56.lea rn 7599 提高致命一击 42.lear n 9405 提高致命一击 70.lea rn 17713 提高致命一击100.learn 16906 +攻击.le arn 35785+980攻击强度.lear n 35786 1296攻击强度.l earn35868 1164攻击强度.lea rn 39421 +500防御等级=神器戒指.learn 34772 ++400法伤.lea rn 24243 +840法伤.lear n 35830 +642法伤.learn 35832 +683法伤.l earn35842+700法伤.le arn 35854 +698法伤这些是增加40以上属性的...le arn 14935-40 增加敏捷.le arn 14941-46 增加智力.le arn 14947-52 增加精神.le arn 14953-58 增加耐力.le arn 14959-64 增加力量.le arn 14976增加火焰抗性.lea rn 14970 增加秘法抗性.lear n 14982 增加冰霜抗性.learn 14989 增加自然抗性.l earn14995增加暗影抗性.lear n 34182 神圣免疫 .l earn34184秘法免疫.le arn 7940 冰霜免疫.learn 7941自然免疫 .l earn7942火焰免疫.lear n 7743 暗影免疫.l earn39811伤害免疫:火焰、冰霜、暗影、自然、秘法.l earn39804伤害免疫:魔法.lea rn 34310 物理免疫.lear n 34311 伤害免疫:物理人物属性修改格式为:.m odify hp 888888 1000000 (修改血为8888/10000)当前值和最大值,修改前先选中自己,其他修改类推。

Dow公司和美国能源部共同致力于生物质气化项目

技术 的新加坡科学技术研究厅进行合作 , 共同对沸石催 化剂 进行研究 , 进一步提高催化 剂的性 能 , 同时开发 催化剂 的再

生 方 法 和使 用 该 催 化 剂 的工 艺 技 术 。 日本 三 井 化 学 公 司 将 建 二 氧 化 碳 制 甲醇 示 范 装 置

Ⅳ . P erd c d AIO3 S p o d Coห้องสมุดไป่ตู้p r J Caa ,1 91,1 2 r—e u e 2 一 u p se p e . tl 9 3

( )2 3 1 :2~ 4

1 Av o r p u o , l a n d s 2 g uo o ls G o n i e T, M ar i ta s l H. I f e c o h n u n e f te l P e a ai n M eh d o h e f r n e o O r p t t o n t e P ro ma c f Cu r o Ce t y t O2 Ca a ss l

Oxds p l aa, 19 1 2 1~ ) 2 3~ 2 ie.A p tl C A,9 7,6 ( 2 : 1 2 2

1 Ch i K 1 o L,Va n c n ie M A.CO i a o v rP n t l ss Ox d t n o e d a d Cu Ca ay t i

Caa y i y F u r e Ox d s t ssb l o i i e :A t d f CO i a o v rCu l t Su y o Ox d t n o e / i

C O .C e n ,19 6 2 : 8 e 2 hm E gJ 9 6, 4( ) 2 3~24 9

MSDS_Dowanol EPH 苯氧乙醇_EN

1.CHEMICAL PRODUCT&COMPANY IDENTIFICATION24-HOUR EMERGENCY PHONE NUMBER:989-636-4400Product:DOWANOL*EPH GLYCOL ETHER,LOW PHENOL GRADEProduct Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329The Dow Chemical Company,Midland,MI48674Customer Information Center:800-258-2436POSITION/INFORMATION ON INGREDIENTSEthylene glycol phenyl ether CAS#000122-99-699% Diethylene glycol phenyl ether CAS#000104-68-71% 3.HAZARDS IDENTIFICATIONEMERGENCY OVERVIEW************************************************************************ *Colorless liquid.Pleasant odor.Causes eye irritation.Toxic* *fumes are released in fire situations.* ** ************************************************************************POTENTIAL HEALTH EFFECTS(See Section11for toxicological data.)EYE:May cause moderate eye irritation.May cause moderate corneal injury.SKIN:Prolonged or repeated exposure not likely to cause significant skin irritation.May cause more severe response ifconfined to skin.A single prolonged exposure is not likely toresult in the material being absorbed through skin in harmfulamounts.Repeated skin exposure may result in absorption ofharmful amounts.Excessive exposure may cause hemolysis,thereby impairing the blood's ability to transport oxygen.INGESTION:Single dose oral toxicity is considered to be low.Small amounts swallowed incidental to normal handling operationsare not likely to cause injury;swallowing amounts larger thanthat may cause injury.INHALATION:At room temperature,exposures to vapors are minimal due to physical properties;higher temperatures maygenerate vapor levels sufficient to cause irritation and othereffects.(Continued on Page2)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------3.HAZARDS IDENTIFICATION(CONTINUED)SYSTEMIC&OTHER EFFECTS:Observations in animals include liver, kidney,thyroid,and blood effects.CANCER INFORMATION:No relevant information found.TERATOLOGY(BIRTH DEFECTS):Birth defects are unlikely.Even exposures having an adverse effect on the mother should have noeffect on the fetus.REPRODUCTIVE EFFECTS:In animal studies,repeated exposures did not have any effect on reproductive organs.4.FIRST AIDEYES:Irrigate with flowing water immediately and continuously for15minutes.Consult medical personnel.SKIN:Wash off in flowing water or shower.INGESTION:If swallowed,seek medical attention.Do not induce vomiting unless directed to do so by medical personnel.INHALATION:Remove to fresh air if effects occur.Consult a physician.NOTE TO PHYSICIAN:No specific antidote.Supportive care.Treatment based on judgment of the physician in response toreactions of the patient.5.FIRE FIGHTING MEASURESFLAMMABLE PROPERTIESFLASH POINT:127C(260F)METHOD USED:PMCCAUTOIGNITION TEMPERATURE:Not determined.FLAMMABILITY LIMITSLFL:Not determinedUFL:Not determinedHAZARDOUS COMBUSTION PRODUCTS:During a fire,smoke may contain the original material in addition to unidentified toxic and/orirritating compounds.OTHER FLAMMABILITY INFORMATION:Dense smoke is produced when (Continued on Page3)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------5.FIRE FIGHTING MEASURES(CONTINUED)product burns.Violent steam generation or eruption mayoccur upon application of direct water stream to hot liquids.Flammable concentration of vapor can accumulate at room tempera-tures above260.0F.Spills of these organic liquids on hotfibrous insulations may lead to lowering of the autoignitiontemperatures possibly resulting in spontaneous combustion.EXTINGUISHING MEDIA:Water fog or fine spray.Carbon dioxide.Dry chemical.Foam.Alcohol resistant foams(ATC type)arepreferred if available.General purpose synthetic foams(in-cluding AFFF)or protein foams may function,but much lesseffectively.Water fog,applied gently may be used as a blan-ket for fire extinguishment.Do not use direct water stream.Will spread fire.MEDIA TO BE AVOIDED:Do not use direct water stream.FIRE FIGHTING INSTRUCTIONS:Keep people away.Isolate fire area and deny unnecessary entry.Burning liquids may be moved byflushing with water to protect personnel and minimize propertydamage.Water fog applied gently may be used as a blanket forfire extinguishment.Do not use direct water stream.Mayspread fire.PROTECTIVE EQUIPMENT FOR FIRE FIGHTERS:Wear positive-pressure self-contained breathing apparatus(SCBA)and protective firefighting clothing(includes fire fighting helmet,coat,pants,boots,and gloves).If protective equipment is not availableor not used,fight fire from a protected location or safe dis-tance.6.ACCIDENTAL RELEASE MEASURES(See Section15for RegulatoryInformation)PROTECT PEOPLE:Isolate area.PROTECT THE EVIRONMENT:Contain liquid to prevent contamination of soil,surface water or ground water.CLEANUP:Clean up with absorbent material.Collect material in suitable and properly labeled open containers.(Continued on Page4)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------7.HANDLING AND STORAGEHANDLING:Do not eat,drink or smoke in working area.STORAGE:Keep containers tightly closed when not in use.Store in carbon steel,stainless steel,Teflon.8.EXPOSURE CONTROLS/PERSONAL PROTECTIONENGINEERING CONTROLS:Good general ventilation should be sufficient for most conditions.Local exhaust ventilation maybe necessary for some operations.PERSONAL PROTECTIVE EQUIPMENTEYE/FACE PROTECTION:Use chemical goggles.SKIN PROTECTION:Use protective clothing impervious to this material.Selection of specific items such as faceshield,gloves,boots,apron,or full body suit will depend onoperation.Remove contaminated clothing immediately,washskin area with soap and water,and launder clothing beforereuse.Notes:The following should be effective protective clothingmaterials:Neoprene and butyl rubber.RESPIRATORY PROTECTION:Atmospheric levels should be maintained below the exposure guideline.For most conditions,norespiratory protection should be needed;however,if handlingat elevated temperatures without sufficient ventilation,usean approved air-purifying respirator.EXPOSURE GUIDELINE(S):Ethylene glycol phenyl ether:Dow IHG is 25ppm,Skin.A"skin"notation following the exposure guideline refers to thepotential for dermal absorption of the material.25ppm(skin)for Dowanol EPH.It is intended to alert the reader thatinhalation may not be the only route of exposure and that measures to minimize dermal exposures should be considered.9.PHYSICAL AND CHEMICAL PROPERTIESAPPEARANCE:Colorless.ODOR:Pleasant smelling liquid.VAPOR PRESSURE:.007mmHg@25CVAPOR DENSITY: 4.8(Continued on Page5)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------9.PHYSICAL AND CHEMICAL PROPERTIES(CONTINUED)BOILING POINT:245.6C(473F)SOLUBILITY IN WATER: 2.3g/100gSPECIFIC GRAVITY: 1.104@20/4CFREEZING POINT:51F,11C.VOLATILE ORGANIC COMPOUNDS(VOC)CONTENT:1104g/L or9.20lb/gal as per Rule443.1of California SCAQMD10.STABILITY AND REACTIVITYCHEMICAL STABILITY:Stable under recommended storage conditions.See storage section.CONDITIONS TO AVOID:Product can decompose at elevatedtemperatures.INCOMPATIBILITY WITH OTHER MATERIALS:Avoid contact with oxidizing materials.HAZARDOUS DECOMPOSITION PRODUCTS:Hazardous decomposition products depend upon temperature,air supply and the presenceof other materials.HAZARDOUS POLYMERIZATION:Will not occur.11.TOXICOLOGICAL INFORMATION(See Section3for Potential HealthEffects.For detailed toxicological data,write or call theaddress or non-emergency number shown in Section1)SKIN:The LD50for skin absorption in rabbits is>2000mg/kg.INGESTION:The oral LD50for rats is in the range of1400-4000mg/kg.MUTAGENICITY:In vitro mutagenicity studies were negative.Animal mutagenicity studies were negative.12.ECOLOGICAL INFORMATION(For detailed Ecological data,write or callthe address or non-emergency number shown in Section1) ENVIRONMENTAL FATEMOVEMENT&PARTITIONING:Bioconcentration potential is low(BCF less than100or Log Kowless than3).Log octanol/water partition coefficient(log Pow)is 1.16.Log soil organic carbon partition coefficient(log (Continued on Page6)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------12.ECOLOGICAL INFORMATION(For detailed Ecological data,write or callKoc)is estimated to be 1.2-2.0.Potential for mobility in soilis high(Koc between50and150).Henry's Law Constant(H)isestimated to be 2.0E-07atm-m3/mol.DEGRADATION&PERSISTENCE:Biodegradation under aerobic static laboratory conditions ishigh(BOD20of BOD28/ThOD greater than40%)5-Day biochemical oxygen demand(BOD5)is0.48p/p.10-Day biochemical oxygen demand(BOD10)is 1.54p/p.20-Day biochemical oxygen demand(BOD20)is 1.74p/p.Theoretical oxygen demand(ThOD)is calculated to be 2.18p/p.Biodegradation rate may increase in soil and/or water withacclimation.ECOTOXICITY:Material is practically non-toxic to aquatic organisms on anacute basis(LC50greater than100mg/L in most sensitivespecies).Acute LC50for fathead minnow(Pimephales promelas)is347mg/L.Acute LC50for water flea(Daphnia magna)is460mg/L.13.DISPOSAL CONSIDERATIONS(See Section15for Regulatory Information)DISPOSAL:DO NOT DUMP INTO ANY SEWERS,ON THE GROUND OR INTO ANY BODY OF WATER.All disposal methods must be in compliance withall Federal,State/Provincial and local laws and regulations.Regulations may vary in different locations.Waste character-izations and compliance with applicable laws are the responsi-bility solely of the waste generator.THE DOW CHEMICAL COMPANYHAS NO CONTROL OVER THE MANAGEMENT PRACTICES OR MANUFACTURINGPROCESSES OF PARTIES HANDLING OR USING THIS MATERIAL.THEINFORMATION PRESENTED HERE PERTAINS ONLY TO THE PRODUCT ASSHIPPED IN ITS INTENDED CONDITION AS DESCRIBED IN MSDS SECTION2(Composition/Information On Ingredients).FOR UNUSED&UNCONTAMINATED PRODUCT,the preferred options in-clude sending to a licensed,permitted:recycler,reclaimer,incinerator or other thermal destruction device.As a service to its customers,Dow can provide names ofinformation resources to help identify waste managementcompanies and other facilities which recycle,reprocess ormanage chemicals or plastics,and that manage used drums.Telephone Dow's Customers Information Center at(Continued on Page7)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------13.DISPOSAL CONSIDERATIONS(See Section15for Regulatory Information)800-258-2436or989-832-1556for further details.14.TRANSPORT INFORMATIONCANADIAN TDG INFORMATION:For TDG regulatory information,if required,consult transportation regulations,product shipping papers,or your Dow representative.DEPARTMENT OF TRANSPORTATION(D.O.T.):This product is not regulated by D.O.T.when shipped domestically by land.15.REGULATORY INFORMATION(Not meant to be all-inclusive--selectedregulations represented)NOTICE:The information herein is presented in good faith andbelieved to be accurate as of the effective date shown above.However, no warranty,express or implied is given.Regulatory requirementsare subject to change and may differ from one location to another;it is the buyer's responsibility to ensure that its activities comply with federal,state or provincial,and local laws.The followingspecific information is made for the purpose of complying withnumerous federal,state or provincial,and local laws and regulations. See other sections for health and safety information.U.S.REGULATIONS=================SARA313INFORMATION:This product contains the following substances subject to the reporting requirements of Section313of Title III ofthe Superfund Amendments and Reauthorization Act of1986and40CFRPart372:CHEMICAL NAME CAS NUMBER CONCENTRATION------------------------------------------------------------------------GLYCOL ETHERS100%SARA HAZARD CATEGORY:This product has been reviewed according to the EPA"Hazard Categories"promulgated under Sections311and312of the Superfund Amendment and Reauthorization Act of1986(SARA Title III)and is considered,under applicable definitions,to meet the following categories:(Continued on Page8)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------REGULATORY INFORMATION:(CONTINUED)An immediate health hazardA delayed health hazardTOXIC SUBSTANCES CONTROL ACT(TSCA):All ingredients are on the TSCA inventory or are not required to belisted on the TSCA inventory.-----The CAS number for TSCA is000122-99-6.STATE RIGHT-TO-KNOW:This product is not known to contain anysubstances subject to the disclosure requirements ofNew JerseyPennsylvaniaOSHA HAZARD COMMUNICATION STANDARD:This product is a"Hazardous Chemical"as defined by the OSHA Hazard Communication Standard,29CFR1910.1200.CANADIAN REGULATIONS=====================WHMIS INFORMATION:The Canadian Workplace Hazardous MaterialsInformation System(WHMIS)Classification for this product is:D2B-eye or skin irritantRefer elsewhere in the MSDS for specific warnings andsafe handling information.Refer to the employer'sworkplace education program.-----CPR STATEMENT:This product has been classified in accordance with the hazard criteria of the Canadian Controlled Products Regulations(CPR) and the MSDS contains all the information required by the CPR.-----(Continued on Page9)Product Code:00610Effective Date:03/23/99Date Printed:08/27/02MSD:002329 ------------------------------------------------------------------------REGULATORY INFORMATION:(CONTINUED)HAZARDOUS PRODUCTS ACT INFORMATION:This product contains the following ingredients which are Controlled Products and/or on the Ingredient Disclosure List(Canadian HPA section13and14):COMPONENTS:CAS#AMOUNT(%w/w) Ethylene glycol phenyl ether CAS#000122-99-699% Diethylene glycol phenyl ether CAS#000104-68-71%.16.OTHER INFORMATIONNATIONAL FIRE PROTECTION ASSOCIATION(NFPA)RATINGS:Health1Flammability1Reactivity0MSDS STATUS:Revised Section13,Disposal.*or(R)Indicates a Trademark of The Dow Chemical CompanyThe Information Herein Is Given In Good Faith,But No Warranty,Express Or Implied,Is Made.Consult The Dow Chemical Company For Further Information.。

道(Dow)化学危险指数分析

道(Dow)化学危险指数分析道(Dow)化学危险指数分析3.4道(Dow)化学危险指数分析本报告采⽤道(Dow)化学第七版的数据,对该企业储存4t酒精桶装罐的⽕灾爆炸危险性进⾏评价。

3.4.1 物质系数的确定物质系数MF是表述由燃烧或化学反应引起的⽕灾、爆炸过程中潜在能量释放的尺度,由美国防⽕协会(NFPA)确定的物质可燃性NF和化学活泼性NR求得。

本项⽬贮存单元中的主要物料为酒精,查表可确定其可燃性等级NF=3.0,物质系数MF=16。

3.4.2单元⼯艺危险系数F3及⽕灾爆炸指数单元⼯艺危险系数F3的值是由⼀般⼯艺危险系数F1与特殊⼯艺危险系数F2相乘得出。

⽕灾爆炸指数见表3-2。

(1)⼀般⼯艺危险性⼀般⼯艺危险系数是确定事故损害⼤⼩的主要因素,包括:放热化学反应、吸热反应、物质的处理和输送,封闭结构单元或室内单元、通道、排放和泄漏控制等6项内容。

基本危险系数:给定值1.00。

a、放热反应本单元中没有放热反应,故危险系数为0。

b、吸热反应本单元中没有吸热反应,故危险系数为0。

c、物料的处理和输送酒精桶装罐存放于库房内,根据酒精NF=3.0,故取系数0.85。

d、封闭结构单元或室内单元危险系数范围为0.25~0.90,在封闭区域内,在闪点以上处理易燃液体时,系数取0.3,故取系数0.3。

e、通道在两个⽅向上设有通道,系数取0.20。

f、排放和泄漏控制单元周围为⼀可排放泄漏液的平坦地,⼀旦失⽕,会引起⽕灾,故取系数0.5。

单元⼀般⼯艺危险系数F1=1.00+0.85+0.3+0.20+0.50=2.85。

(2)特殊⼯艺危险性特殊⼯艺过程危险性是导致事故发⽣概率的主要因素,道⽒7版共提出了毒性物质、负压操作、爆炸极限范围内及其附近的操作、粉尘爆炸、压⼒释放、低温、易燃物质的数量、腐蚀、轴封和接头处的泄漏、明⽕设备的使⽤、热油交换系统、转动设备等12项内容。

基本危险系数:给定值1.00。

a、毒性物质毒性物质的危险系数为0.2NH,混合物中取最⼤的NH值。

DOW公司开发出新型聚合物阻燃剂

高相对 分子质 量溴化 聚合 物阻燃 剂 ( F 。预计 这 P R) 种 P R将成 为全 球 在 挤 塑 聚苯 乙烯 ( P ) 可 发 F XS 和 性 聚苯 乙烯 ( P ) E S 泡沫 绝缘应 用 中的下一 代 工业标

准 阻燃 剂 。这 种新 型 P R 的开 发是 D T公 司为 了 F G

种 10 MF 的 L m cn P模 塑周 期 比一种 7 I 1 I u ieeP 0MF

的P P缩短 1% , 0 同时 还获 得 了较 高 的刚性 和抗 冲 击强 度 , 容许减 厚 4 ~ % 。 并 % 8 Tcn 公 司推 出 G RX12超 细 粉特 高相 对 分 ioa U 9 子质 量 P 。它 可 以被烧 结用 于生产 多孔 部件 , 于 E 用 具有 较高流 速 、 压 降及高 强度液 体和气 体过 滤 。 较低

m r E— H接枝 技术 。 o P MA

3种 Cait ri P) 密 封树脂 , 它们 被设 计 用 于 可 提供 极 好 的 味觉 和 嗅 觉性 能并 具有 轻量化 性能 。

5种用 于硬质 包装 的新 型高 流动 P P共 聚物 , 它

5 6

信 息与动 态 P A薄膜 , V 这是 液 晶显 示器 的一种基 础元 件 。

粘 合剂 和 纤 维 上 浆 剂 领 域 , 时 还 应 用 于 光 学 级 同

D W 公 司开 发 出新 型 聚合 物 阻 燃剂 O

D W 环 球技 术 ( G ) 司开 发成 功一 种 新 型 O D T公 烷 的阻燃剂 的结果 。D T公 司 已宣 布 了与 C e t— G h m u

S rn公 司宣布 了用于 冰箱 内衬 的其 下一 代 耐 to y 环境 应 力 开 裂 ( S R) 抗 冲 聚 苯 乙 烯 ( IS EC 高 HP )

Dow化学公司签订加拿大油砂原料合同

种小尺寸的管道能提高传热效率和提高反应 速度, 因而可在较 低的投资成本下获得高生

产率。此外 , 该新 型反 应器还可 以利用具有 定制性能的高活性催化剂 。 这种 G L装 置 利 用 Ve cs 司 开 发 T ly 公 o 的微通 道 反 应 器 技 术 , T C进 行 工 程 设 由 E

H P O 提供 原料 。B 能源 公 司成 立于 20 A 02 年 , 造并 运 行 这 一 加 拿 大 西 部 第 一 套 独 立 建

运行 的沥 青 质量 提升 装 置 。

或外购 的煤 , 以及至少 5 %的生物质 为气化 原料。生产的合成气 和 C O将转化成直 链石蜡烃 , 然后通 过加氢裂解成不含硫 的柴

Sb G alN L加拿大公 司合作 , e 开发用 于废气 质量提升 的处 理装 置 , 回收烃类 原料。D w o

公 司 和 SbeNG 加 拿 大 公 司 将 与 Abra al L let

的质量提 升装 置及炼油 厂合作 开发废气 项

维普资讯

前正 在 F r S s ac e n A bra ot ak thwa , let 建造 。

D w 公 司 称 , 些 油 砂 为 D w 公 司 的 o 这 o Abra 营 提 供 大 量 的 未 被 利 用 的 原 料 来 let运

Fsh r rpc 术 的 商 业化 i e —T o sh技 c

该装 置还 有 73 0bld以上 的丙 烷 ~丙烯 ,0 b/

使用铁 基催 化 剂 , 一 台 淤 浆 反 应 器 中 转 化 在

合成气 。该公 司表示 , 该技术 的一个 优点是 使用 I : 比范 围为 0 7 1 3 1 4 C 2O . : 到 : 的合成 气。如果 H 过量太多 , 2 多余的 H 可 以就地 2

Systematic risk and international portfolio choice

THE JOURNAL OF FINANCE•VOL.LIX,NO.6•DECEMBER2004Systemic Risk and International Portfolio Choice SANJIV RANJAN DAS and RAMAN UPPAL∗ABSTRACTReturns on international equities are characterized by jumps;moreover,these jumpstend to occur at the same time across countries leading to systemic risk.We capturethese stylized facts using a multivariate system of jump-diffusion processes where thearrival of jumps is simultaneous across assets.We then determine an investor’s opti-mal portfolio for this model of returns.Systemic risk has two effects:One,it reducesthe gains from diversification and two,it penalizes investors for holding levered posi-tions.We find that the loss resulting from diminished diversification is small,whilethat from holding very highly levered positions is large.R ETURNS ON INTERNATIONAL EQUITIES are characterized by jumps;1moreover,these jumps tend to occur at the same time across countries,implying that conditional correlations between international equity returns tend to be higher in periods of high market volatility or following large downside moves.2Our objective in ∗Sanjiv Ranjan Das and Raman Uppal are with Santa Clara University,and CEPR and London Business School,respectively.We are grateful to Stephen Lynagh for excellent research assistance. We thank an anonymous referee,Andrew Ang,Pierluigi Balduzzi,Suleyman Basak,Greg Bauer, Geert Bekaert,Harjoat Bhamra,Michael Brandt,John Campbell,George Chacko,Jo˜ao Cocco, Glen Donaldson,Darrell Duffie,Bernard Dumas,Ken Froot,Francisco Gomes,Eric Jacquier,Tim Johnson,Andrew Karolyi,Andrew Lo,Michelle Lee,Jan Mahrt-Smith,Scott Mayfield,Narayan Naik,Vasant Naik,Roberto Rigobon,Geert Rouwenhorst,Piet Sercu,Milind Shrikhande,Rob Stambaugh,Raghu Sundaram,Luis Viceira,Jiang Wang,Tan Wang,Greg Willard,Wei Xiong,and Hongjun Yan for their suggestions.We also gratefully acknowledge comments from seminar par-ticipants at Bank of England,Boston College,Erasmus University,HEC Paris,London Business School,Maryland University,MIT,Swiss National Bank,University of Essex,University of Exeter, University of Maryland,University of Rochester,the1999Global Derivatives Conference,VIIth International Conference on Stochastic Programming,International Finance Conference at Geor-gia Institute of Technology,Conference of International Association of Financial Engineers,NBER Finance Lunch Seminar Series,the1999meetings of the European Finance Association,the2001 meetings of the Western Finance Association,the2002meetings of INQUIRE,the2003meetings of the American Finance Association,and the2003CIRANO Conference on Portfolio Choice.1Evidence on jumps in international equity returns is provided by Jorion(1988),Akgiray and Booth(1988),Bates(1996),and Bekaert et al.(1998).2For example,on July19,2002,the Dow fell by4.6%,the Dax by5.0%,the Cac by5.4%,the FTSE by4.6%,and the Nikkei by2.8%.Similarly,world equity markets fell in lockstep on October27, 1997,when the drop from the12-month peak was9.2%in Britain,35.4%in Hong Kong,21.3% in Japan,2.1%in Australia,10.7%in Mexico,27.9%in Brazil,and9.1%in the United States. Other events with large correlated price drops include the Debt crisis of1982,the Mexican crisis in December1994,and the Russian crisis in August1998;see Rigobon(2003)for a complete list of dates with large market moves.For evidence on changing conditional correlations see,for instance, Speidell and Sappenfield(1992),Odier and Solnik(1993),Erb,Harvey,and Viskanta(1994),Longin and Solnik(1995),Karolyi and Stulz(1996),Chakrabarti and Roll(2000),and Ang and Chen(2002).28092810The Journal of Financethis paper is to evaluate the effect on portfolio choice of systemic risk,defined as the risk from infrequent events that are highly correlated across a large number of assets.Our contribution is to provide a mathematical model of security returns that captures the stylized facts about international equity returns described above. We do this by modeling security returns as jump-diffusion processes where jumps across assets are systemic(occur simultaneously),though the size of each jump is allowed to differ across assets.Next,we derive the optimal portfo-lio weights for this model of returns.Then,we calibrate the portfolio model to the U.S.equity index and to five international equity indexes.For robustness, we consider two sets of international indexes:the first for developed countries and the second for emerging countries.Systemic risk has two effects:It reduces the gains from diversification and also penalizes investors for holding levered positions.We find that the loss resulting from diminished diversification is small,while that from holding highly levered positions is large.For instance, the certainty equivalent cost of ignoring systemic risk for a conservative agent with relative risk aversion of3who is investing$1,000for1year is on the or-der of$0.10for the developed-country indexes and$3for the emerging-country indexes.However,for more aggressive investors who hold heavily levered port-folios,the cost of ignoring systemic risk is substantial:For example,an investor with a risk aversion of1who ignores systemic risk has a positive probability of losing all her wealth.Our work can be distinguished from the literature on portfolio choice with idiosyncratic jumps in returns,for example,Aase(1984),Jeanblanc-Picque and Pontier(1990),and Shirakawa(1990).In more recent work,Liu,Longstaff,and Pan(2003)study a model of portfolio choice with event risk.In contrast to these theoretical models,our motivation is to evaluate the effect of systemic jumps on portfolio selection by empirically estimating the parameters of the returns in our model,and implementing the model based on these estimates. In contrast to the static model in Chunhachinda et al.(1997),where polynomial goal programming is used to examine the effect of skewness on portfolio choice by assuming a utility function defined over the moments of the distribution of returns,our model is dynamic,with preferences given by a standard constant relative risk-averse utility function,and in our model the effect of skewness (and higher moments)arises because of jumps in the returns process rather than being introduced explicitly through the utility function.3Our work is also related to Ang and Bekaert(2002),who embed an inter-national portfolio choice problem in a dynamic model with a regime-switching data-generating process.Two regimes are considered that correspond to a 3For early work on how skewness influences portfolio choice,see Samuelson(1970),Tsiang (1972),and Kane(1982).Kraus and Litzenberger(1976)show the implications for equilibrium prices of a preference for positive skewness,while Kraus and Litzenberger(1983)derive the suf-ficient conditions on return distributions to get a three-moment(mean,variance,and skewness) capital asset pricing model.Harvey and Siddique(2000)provide an empirical test of the effect of skewness on asset prices.Systemic Risk and International Portfolio Choice2811 normal regime with low correlations and a downturn regime with higher cor-relations.In their setup,regimes can be persistent,and their paper includes an analysis of portfolio choice when the short interest rate and earnings yields predict returns.The framework in Ang and Bekaert,however,does not accom-modate intermediate consumption,admits only a numerical solution even in the absence of intermediate consumption,and is difficult to estimate when there are more than two regimes or three risky assets.In contrast to Ang and Bekaert,we develop a theoretical framework along the lines of Merton(1971);because our model nests the well-understood Merton model as a special case,it allows one to interpret cleanly the effect of systemic jumps.Also,we provide analytic expressions for the optimal portfolio weights. Moreover,our model can incorporate intermediate consumption(the solution to the portfolio problem stays the same),and can be estimated and implemented for any number of assets.While in the paper we consider only a simple IID en-vironment where the unconditional correlations between returns are constant over time,we argue that this is sufficient to show that the effect of systemic jumps will not be large even in the presence of regime shifts.4Our framework can also allow for predictability in returns and for other state variables,just as they are incorporated in Merton,but because this is tangential to our main objective,we do not include these features in the model we present.The rest of the paper is organized as follows.In Section I,we develop a model of asset returns that captures systemic risk.In Section II,we derive the opti-mal portfolio weights when asset returns have a systemic-jump component.In Section III,we describe our data,give the moments for the returns in the pres-ence of systemic risk,and estimate the parameters of the returns processes. We then calibrate the portfolio model to the estimated parameters in order to compare the portfolio weights of an investor who accounts for systemic risk and an investor who ignores systemic risk.We conclude in Section IV.Proofs for propositions are presented in the Appendix.I.Asset Returns with Systemic RiskIn this section,we develop a model of asset prices that allows for systemic jumps and compare it to a pure-diffusion model without jumps.The two features of the data that we wish our returns-model to capture are(1)large changes in asset prices,and(2)a high degree of correlation across these changes.To allow for large changes in returns,we introduce a jump component in prices;to model these jumps as being systemic,we assume that this jump is common across all assets,though the distribution of the jump size is allowed to vary across assets. We start by describing the standard continuous-time process that is typically assumed for asset returns:dS n=ˆαn dt+ˆσn dz n,n=1,...,N,(1)S n4Das and Uppal(2003)show how to extend the model to allow for persistence in jumps.2812The Journal of FinancewithE tdS nS n=ˆαn dt(2)E tdS nS n×dS mS m=ˆσnm dt=ˆσnˆσmˆρnm dt,(3)where S n is the price of asset n,N is the total number of risky assets being considered for the portfolio,and the correlation between the shocks dz n and dz m is denoted byˆρnm dt=E(dz n×dz m).We will denote the N×N matrix of the covariance terms arising from the diffusion components by Σ,with its typ-ical element beingˆσnm≡ˆσnˆσmˆρnm.We adopt the convention of denoting vectors and matrices with boldface characters in order to distinguish them from scalar quantities;parameters of the pure-diffusion returns process,and other quan-tities related to the pure-diffusion model,are denoted with aˆ(carat)over the variable.To allow for the possibility of infrequent but large changes in asset returns,5 we extend the specification in equation(1)by introducing a jump component to the process for returns,as in Merton(1976).In order to capture the systemic nature of these jumps,we impose two restrictions on the jump-diffusion pro-cesses:one,the jump is assumed to arrive at the same time across all risky assets;two,conditional on a jump,the jump size is assumed to be perfectly correlated across assets;that is,the value of all the assets jumps in the same direction.Below,we formally describe a returns process for the risky assets that has these properties.Introducing a jump component to the process of returns in(1),we have dS nS n=αn dt+σn dz n+(˜J n−1)dQ(λ),n=1,...,N,(4)where Q is a Poisson process with intensityλ,and(˜J n−1)is the random jump amplitude that determines the percentage change in the asset price if the Poisson event occurs.Given our desire to model the large changes in prices as occurring at the same time across the risky assets,we have assumed that the ar-rival of jumps is coincident across all risky assets;that is,dQ n(λn)=dQ m(λm)= dQ(λ),∀n={1,...,N},m={1,...,N}.6We also assume that the diffusion shock,the Poisson jump,and the random variable˜J n are independent and that J n≡ln(˜J n)has a normal distribution with meanµn and varianceν2n,implying that the distribution of the jump size is asset-specific(below we will assume5In contrast to systemic risk,systematic risk refers to correlation between assets and a common factor,but does not require that the size of this correlation be large or that the correlated changes be infrequent.6The returns process described above is IID;in particular,and in contrast to Ang and Bekaert (2002),there is no persistence in jumps.Das and Uppal(2003)show how one could extend this model to allow for persistence in systemic jumps by making the arrival rate of jumps,λ,stochastic.Systemic Risk and International Portfolio Choice 2813that,conditional on a jump,the jump sizes for different assets are perfectly correlated).Thus,for the process in (4),the total expected return in equation (5)has two components:One part comes from the diffusion process,αn and the other,denoted αJ n ,comes from the jump process:E t dS n S n=αn dt +αJ n dt .(5)We also assume that the jump size is perfectly correlated across assets;as we shall see in Section III,this turns out to be a conservative assumption,and has the further advantage of reducing the number of parameters to be estimated.The total covariance between dS n and dS m ,given in the equation below ,E t dS n S n × dS m S m=σnm dt +σJ nm dt ,(6)arises from two sources:The covariance between the diffusion components of the returns,σnm ≡σn σm ρnm ,and the covariance between the jump compo-nents,σJ nm .The N ×N matrix containing the covariation arising from the jump terms is denoted by J ,while the N ×N matrix of the covariance terms aris-ing from the diffusion components is denoted by ,with its typical elementbeing σnm ≡σn σm ρnm .Explicit expressions for αJ n in (5)and σJ nm in (6),in termsof the parameters of the underlying returns processes,{λ,µn ,νn },are given in equations (26)and (27).In our experiment,we wish to compare the portfolio of an investor who models security returns using the pure-diffusion process in (1)with that of an investor who accounts for systemic risk by using the jump-diffusion process in (4)but matches the first two moments of returns.Thus,we need to choose the parame-ters of the jump-diffusion processes in such a way that the first two moments for this process given in equations (5)and (6)match exactly the first two moments of the pure-diffusion returns process in equations (2)and (3).7Even though it is straightforward to do this,we highlight it in a proposition because this result is important for understanding our analysis.P ROPOSITION 1:In order for the first and second moments from the jump-diffusion process to match the corresponding moments from the pure-diffusion process,we set,for n ,m ={1,...,N },αn =ˆαn −αJ n ,(7)σnm =ˆσnm −σJ nm .(8)One interpretation of the above compensation of the parameters is that the in-vestor using the jump-diffusion returns process takes the total expected 7An important difference between our work and that of Liu et al.(2003)is that while we control for the magnitude of the first two moments when comparing the portfolio strategy that accounts for jumps with the one that ignores jumps,they do not.2814The Journal of Financereturn on the asset,ˆαn,and the covariance,ˆσnm,and subtracts from themαJ n and σJ nm,respectively,with the understanding that this will be added back through the jump term,(˜J n−1)dQ(λ).In this way,she reduces the expected return and covariance coming from the diffusion terms in order to offset exactly the contribution of the jump.Even though the unconditional expected return and covariance under the compensated jump-diffusion process will match those from the pure-diffusion process,the two processes will not lead to identical portfolios.This is because the jump also introduces skewness and kurtosis into the returns process(see equations(24)and(25)).8In the next section,we analyze the difference between the portfolio of an investor who allows for systemic jumps in returns and an investor who ignores this effect.II.Portfolio Selection in the Presence of Systemic RiskIn this section,we formulate and solve the portfolio selection problem when returns are given by the jump-diffusion process in(4).Given that financial markets are incomplete in the presence of jumps of random size,we determine the optimal portfolio weights using stochastic dynamic programming rather than the martingale pricing approach.Our modeling choices are driven by the desire to develop the simplest possible framework in which one can examine the portfolio selection problem in the presence of systemic risk.Hence,we work with a model that has a constant investment opportunity set;an extension of this model to the case where the investment opportunity set is changing over time,via shifts in the likelihood of systemic jumps,is considered in Das and Uppal(2003).Also,we model the portfolio problem in continuous time because of the analytical convenience this affords.Finally,we describe the model in the context of international portfolio selection,but the model applies to any set of securities with appropriate returns processes.A.Optimal Portfolio WeightsWe consider a U.S.investor who wishes to maximize the expected utility from terminal wealth,9W T,with utility being given by U(W T)=W1−γT,whereγ>0,1−γγ=1,so that constant relative risk aversion is equal toγ.10The investor can allocate funds across n={0,1,...,N}assets:a riskless asset denominated in U.S.dollars(n=0),a risky U.S.equity index(n=1),and risky foreign equity indexes,n={2,...,N}.8Jumps are not the only way of introducing skewness and kurtosis into the process for returns—stochastic volatility would also generate such effects.Of course,jumps have the additional effect that they constrain portfolio weights in order to prevent wealth from becoming negative.9We do not consider intermediate consumption because it has no effect on the optimal weights in our model.10For the case whereγ=1,the utility function is given by U(W T)=ln W T.Systemic Risk and International Portfolio Choice2815 The price process for the riskless asset,S0,isdS0=r S0dt,(9) where r is the instantaneous riskless rate of interest,which is assumed to be constant over time.The stochastic process for the price of each equity index(in dollar terms)11with a common jump term is as given in equation(4),which is restated below:dS nS n=αn dt+σn dz n+(˜J n−1)dQ(λ),n=1,...,N,(10)withαn andσnm defined in equations(7)and(8).Denoting the proportion of wealth invested in asset n by w n,n={1,...,N}, the investor’s problem at t can be written asV(W t,t)≡max{w n}EW1−γT1−γ,(11)subject to the dynamics of wealthd W tW t=[w R+r]dt+w (σ·dZ t)+w J t dQ(λ),W0=1,(12)where w is the N×1vector of risky-asset portfolio weights,R≡{α1−r,...,αN−r} is the excess-returns vector,σis the vector of volatilities,dZ is the vector of diffusion shocks,with the dot productσ·dZ t denoting element-by-element multiplication ofσn and dZ n,and J t≡[˜J1−1,˜J2−1,...,˜J N−1] is the vector of random jump amplitudes for the N assets at time t.The covariance matrix of the diffusion component of the joint stochastic process is given byΣ. Using the standard approach to stochastic dynamic programming and the appropriate form of Ito’s lemma for jump-diffusion processes,one can obtain the following Hamilton–Jacobi–Bellman equation0=max{w}∂V(W t,t)+∂V(W t,t)W t[w R+r]+12∂2V(W t,t)2W2t w Σw+λE[V(W t+W t w J t,t)−V(W t,t)],(13)where the terms on the first line are the standard terms when the processes for returns are continuous,and the term on the second line accounts for jumps in returns.11The dollar return on a foreign equity index includes the return on currency and the return on the international equity index in local-currency terms.For international equity returns,one could model separately the equity return in local-currency terms and the return on currency.We do not do this because it complicates the notation without adding any insights.2816The Journal of FinanceWe guess(and verify)that the solution to the value function is of the following form:V(W t,t)=A(t)W1−γt1−γ.(14)Expressing the jump term using this guess for the value function(details are in the proof for the proposition below),and simplifying the resulting differential equation,we get an equation that is independent of wealth:0=max{w}1A(t)dA(t)dt+(1−γ)[w R+r]−(1−γ)γ2w Σw+λE(1+w J t)1−γ−1.(15)Differentiating the above with respect to w,one gets the following result.P ROPOSITION2:The optimal portfolio weights in the presence of systemic risk are given by the solution to the following system of N nonlinear equations:0=R−γΣw+λEJ t(1+w J t)−γ,∀t.(16)Note that(16)gives only an implicit equation for the unconditional portfolio weights,w.Thus,to determine the magnitude of the optimal portfolio weights, one needs to solve this equation numerically,which we do in Section III.In contrast to the above solution,an investor who ignores the possibility of systemic jumps and assumes the standard model in which price processes are multivariate diffusions without jumps will choose the portfolio weights given by the familiar Merton(1971)expression below.C OROLLARY1:The weights chosen by an investor who assumes that returns are described by the pure-diffusion process in equation(1)areˆw=1Σ−1ˆR.(17)The difference between the portfolio of the investor who accounts for systemic jumps,w,and that of an investor who ignores this feature of the data and chooses portfolioˆw can be understood by comparing equation(16)and(17): The two equations are the same when there are no jumps(λ=0).Thus,the difference between w andˆw arises from the higher moments ignored in(17).12 12This also shows how our model is related to that of Chunhachinda et al.(1997),who use polynomial goal programming in a single-period model to examine the effect of skewness on portfolio choice by assuming a utility function defined over the moments of the distribution of returns.In contrast,we work with the standard power utility function that is commonly used to examine optimal portfolio selection and instead modify the returns process to allow for the possibility of skewness and higher moments.Systemic Risk and International Portfolio Choice2817B.Certainty Equivalent Cost of Ignoring Systemic RiskAbove,we have compared the optimal portfolio weights for an investor who accounts for systemic jumps in returns and the investor who ignores this feature of the data.In this section,we compare the certainty equivalent cost of following the suboptimal portfolio strategy.The objective of this exercise is to express in dollar terms the cost of ignoring systemic risk.In order to quantify the cost of ignoring systemic jumps,we compute the addi-tional wealth needed to raise the expected utility of terminal wealth under the suboptimal portfolio strategy to that under the optimal strategy.In this com-parison,we denote by CEQ the additional wealth that makes lifetime expected utility underˆw,the portfolio policy that ignores systemic risk,equal to that under the optimal policy,ing the notation V(W t,t;w i),where w i={w,ˆw} indicates the particular portfolio weights used to compute the value function,the compensating wealth,CEQ,is computed as follows:V((1+CEQ)W t,t;ˆw)=V(W t,t;w).(18) Then,from equations(14)and(18),we haveA(t;ˆw)11−γ((1+CEQ)W t)1−γ=A(t;w)11−γW1−γt,(19)which implies thatCEQ=A(t;w)A(t;ˆw)1/(1−γ)−1,(20)where,from the proof for Proposition2,A(t;w i)≡e((1−γ)[w i R+r]−12γ(1−γ)w iΣw i+λE[(1+w i J t)1−γ−1])(T−t),(21) with w i={w,ˆw}.III.Calibrating the Effect of Systemic RiskIn this section,we evaluate the effect of systemic risk on portfolio choice by calibrating the jump-diffusion model to returns on the U.S.equity index,and to five international equity indexes.This section is divided into three subsections. In the first,we describe the data and explain how we use the method of moments to estimate the parameters of the returns processes.In the second,we evalu-ate the effect of systemic risk on portfolio policies using the estimated values for the parameters of the returns process.In the third subsection,we evaluate the sensitivity of our results to the choices we have made in undertaking the calibration exercise.2818The Journal of FinanceA.Description of the Data and Estimation of the ModelThe data for the developed countries consist of the month-end U.S.dollar values of the equity indexes for the period January 1982to February 1997for the United States (U.S.),United Kingdom (U.K.),Switzerland (SW),Germany (GE),France (FR),and Japan (JP).The data for emerging economies are for the period January 1980to December 1998,and consist of the beginning-of-month value of the equity index for the United States (USA),Argentina (ARG),Hong Kong (HKG),Mexico (MEX),Singapore (SNG),and Thailand (THA).To distinguish the two sets of data,we abbreviate the countries in the developed-economy data set with two characters and denote countries in the emerging-economy data set with three characters.Table I reports the descriptive statistics for the continuously compounded monthly return on index j in U.S.dollars,r jt ,which is defined as the ratio of the log of the index value at time t and its lagged value:r j t =ln S j t j ,t −1 ,where S jt is the U.S.dollar value of the index at time t .Examining first the moments for developed economies,we observe from Panel A of Table I that the excess kurtosisTable IDescriptive Statistics for Equity Returns—UnivariatePanel A of this table gives the first four moments of the monthly returns in U.S.dollar terms for the developed-country indexes and Panel B gives the same information for the U.S.and five emerging markets.The data for the developed countries are for the period January 1982to February 1997,and include 182observations of month-end values of the equity indexes for the United States (U.S.),United Kingdom (U.K.),Japan (JP),Germany (GE),Switzerland (SW),and France (FR).The data for emerging economies consist of 227observations of the beginning-of-month value of the equity indexes for the USA,Argentina (ARG),Hong Kong (HKG),Mexico (MEX),Singapore (SNG),and Thailand (THA)for the period January 1980to December 1998.Panel A:Developed CountriesU.S.U.K.JP GE SW FR Avg.Mean0.01020.00840.00800.01200.01020.01130.0100Standard deviation0.04200.05670.06970.05760.05150.06110.0564Skewness−1.1648−0.4623−0.0508−0.2308−0.6382−0.4325−0.4966Significance level0.00000.01150.78150.20740.00040.0181Excess kurtosis7.2236 1.92120.8754 2.9546 5.5405 1.5780 3.3489Significance level 0.00000.00000.01800.00000.00000.0000Panel B:Emerging CountriesUSAARG HKG MEX SNG THA Avg.Mean0.01040.00400.00760.00340.00650.000040.0053Standard deviation0.04140.21530.10260.14370.07720.10370.1140Skewness−1.13530.1187−1.4163−2.0224−0.7684−0.6077−0.9719Significance level0.00000.46810.00000.00000.00000.0002Excess kurtosis6.1823 6.2377 6.93889.1851 4.8603 3.7800 6.1974Significance level 0.00000.00000.00000.00000.00000.0000of returns is substantially greater than that for normal distributions(in the table,we report kurtosis in excess of3,which is the kurtosis for the normal distribution).The excess kurtosis in the data ranges from0.87for France to7.22 for the U.S.For the data on emerging economies,as one would expect,the excess kurtosis is much greater,ranging from3.77for Thailand to9.18for Mexico.All 12kurtosis estimates are significant.There are two possible reasons for the kurtosis:(1)When the multivariate return series is not stationary,the mixture of distributions results in kurtosis;and(2),if the returns are characterized by large shocks,then the outliers inject kurtosis.The second feature of the data is that the skewness of returns for all the developed-market indexes is negative,and for the emerging-country indexes it is more strongly negative,except for Argentina,where it is insignificantly different from zero.The negative skewness is a well-known feature of equity index time series over this time period(1982–1997).Within this period,there were several large negative shocks to the markets contributing to the negative skewness:for instance,the market crash of October1987,the outbreak of the Gulf War in August1990,the Mexican crisis in December1994,and the Russian crisis in August1998.13Table II reports the covariances and correlations between the returns on the international equity indexes.The correlations for the developed countries range from a low of0.33between the United States and Japan,to a high of 0.68between Germany and Switzerland.The average correlation between the equity markets for developed countries is0.51.For the emerging countries,the correlations range from the very low0.05between Hong Kong and Argentina to0.55between Singapore and the United States.The average correlation for the emerging countries is0.31,which,as one would expect,is much lower than that for the developed countries.For the benchmark case of the pure-diffusion process in equation(1),the parameters to be estimated are{ˆα, Σ},with the moment conditions available being the ones in equations(2)and(3).From these moment conditions we see that{ˆα, Σ}can be estimated directly from the means and the covariances of the data series.To derive the unconditional moments of the jump-diffusion returns processes in(4),we identify the characteristic function by exploiting its relation to the Kolmogorov backward equation.14Differentiating the characteristic function then gives the moments of the returns process.The expressions for the moments of the continuously compounded returns are the following:for n,m={1,...,N},mean=tαn−12σ2n+λµn,(22)covariance=t[σnm+λ(µnµm+νnνm)],(23) 13The negative skewness arises also because volatility tends to be higher when returns are negative.14Details of this derivation are given in Das and Uppal(2003).。

Windows--常用端口号及其意义

Window s--常用端口号及其意义常用端口在计算机的6万多个端口,通常把端口号为1024以内的称之为常用端口,这些常用端口所对应的服务通常情况下是固定的,所以了解这些常用端口在一定程序上是非常必要的,下表2列出了计算机的常用端口所对应的服务(注:在这列表中各项"="前面的数字为端口号,"="后面的为相应端口服务。

)。

T CP 1=TCP P ort S ervic e Mul tiple xer TCP 2=Deat hTC P 5=R emote JobEntry,yoyoTCP 7=Ec hoT CP 11=SkunTCP 12=B omberTCP 16=S kun TCP 17=Sku nTC P 18=消息传输协议,sku nTC P 19=SkunTCP20=FT P Dat a,Ama nda TCP 21=文件传输,Bac k Con struc tion,Blade Runn er,Do lyTr ojan,Fore,FTP t rojan,Invi sible FTP,Larva, Web Ex,Wi nCras hTC P 22=远程登录协议TC P 23=远程登录(Telne t),Ti ny Te lnetServe r (=TTS)TCP25=电子邮件(SM TP),A jan,A ntige n,Ema il Pa sswor d Sen der,H appy99,Ku ang2,ProMa il tr ojan,Shtri litz,Steal th,Ta piras,Term inato r,Win PC,Wi nSpy,Haebu Coce daT CP 27=Assa sin TCP 28=Ama nda TCP 29=MSG ICPTCP30=Ag ent 40421TCP31=Ag ent 31,Hac kersParad ise,M aster s Par adise,Agen t 40421T CP 37=Time,ADMwormTCP39=Su bSARITCP 41=D eepTh roat,Forep lay TCP 42=Hos t Nam e Ser ver TCP 43=WHO IST CP 44=Arct icT CP 48=DRATTCP 49=主机登录协议TCP 50=D RAT TCP 51=IMP Logi cal A ddres s Mai ntena nce,F uck L amers Back doorTCP52=Mu Ska52,SkunTCP 53=D NS,Bo nk (D OS Ex ploit)TC P 54=MuSka52T CP 58=DMSe tup TCP 59=DMS etupTCP63=wh ois++TCP 64=C ommun icati ons I ntegr atorTCP65=TA CACS-Datab ase S ervic eTC P 66=Oracl e SQL*NET,AL-Ba rekiTCP67=Bo otstr ap Pr otoco l Ser ver TCP 68=Boo tstra p Pro tocol Clie ntT CP 69=W32.Evala.Worm,Back GateKit,N imda,Pasan a,Sto rm,St orm w orm,T heef,Worm.Cycle.a T CP 70=Goph er服务,ADM w orm TCP 79=用户查询(Fin ger),Fireh otcke r,ADM wormTCP 80=超文本服务器(Http),Exe cutor,Ring ZeroTCP81=Ch ubo,W orm.B beagl e.q TCP 82=Net sky-ZTCP 88=K erber os kr b5服务TCP99=Hi ddenPortTCP102=消息传输代理TCP 108=SNA网关访问服务器TCP 109=思科2 TCP 110=电子邮件(思科3),Pr oMailTCP 113=Kazim as, A uther Idne tTC P 115=简单文件传输协议TCP118=S QL Se rvice s, In fecto r 1.4.2T CP 119=新闻组传输协议(Newsg roup(Nntp)), Ha ppy 99TC P 121=Jamm erKil ler,Bo ja mmerk illahTCP 123=网络时间协议(NTP),Net Cont rolle rTC P 129=Pass wordGener atorProto col TCP 133=In fecto r 1.xTCP 135=微软DCE RPCend-p ointmappe r服务TCP 137=微软Netbi os Na me服务(网上邻居传输文件使用) TC P 138=微软Ne tbios Name服务(网上邻居传输文件使用)TCP139=微软Netb ios N ame服务(用于文件及打印机共享) T CP 142=Net TaxiTCP143=I MAP TCP 146=FC Infe ctor,Infec tor TCP 150=Ne tBIOS Sess ion S ervic eTC P 156=SQL服务器T CP 161=Snm pTC P 162=Snmp-TrapTCP 170=A-Tro jan TCP 177=XDispl ay管理控制协议TCP 179=Bo rder网关协议(B GP) TCP 190=网关访问控制协议(GAC P)T CP 194=IrcTCP 197=目录定位服务(DLS)TC P 256=Nirv ana TCP 315=Th e Inv asorTCP371=C learC ase版本管理软件TCP389=L ightw eight Dire ctory Acce ss Pr otoco l (LD AP) TCP 396=No vellNetwa re ov er IPTCP 420=Breac hTC P 421=TCPWrapp ers TCP 443=安全服务T CP 444=Sim ple N etwor k Pag ing P rotoc ol(SN PP) TCP 445=Mi croso ft-DSTCP 455=Fatal Conn ectio nsT CP 456=Hac kersparad ise,F useSp ark TCP 458=苹果公司Qui ckTim eTC P 513=Grlo gin TCP 514=RP C Bac kdoorTCP 531=Rasmi n,Net666 TCP 544=ke rbero s ksh ell TCP 546=DH CP Cl ientTCP547=D HCP S erverTCP 548=Macin tosh文件服务TCP 555=In i-Kil ler,P haseZero,Steal th Sp yTC P 569=MSNTCP605=S ecret Servi ceT CP 606=Nok nok8TCP661=N oknok8TC P 666=Atta ck FT P,Sat anz B ackdo or,Ba ck Co nstru ction,Dark Conn ectio n Ins ide 1.2 T CP 667=Nok nok7.2TC P 668=Nokn ok6 TCP 669=DP troj anT CP 692=Gay OLT CP 707=Wel chiaTCP777=A IM Sp yTC P 808=Remo teCon trol,WinHo leT CP 815=Eve ryone Darl ing TCP 901=Ba ckdoo r.Dev ilT CP 911=Dar k Sha dow TCP 993=IM APT CP 999=Dee pThro atT CP 1000=De r Spa eherTCP1001=Silen cer,W ebEx,Der S paehe rTC P 1003=Bac kDoorTCP 1010=DolyTCP 1011=DolyTCP 1012=DolyTCP 1015=DolyTCP 1016=DolyTCP 1020=Vamp ire TCP 1023=W orm.S asser.eT CP 1024=Ne tSpy.698(Y AI) TCP 1059=n imreg//T CP 1025=Ne tSpy.698,U nused Wind ows S ervic es Bl ock //TCP 1026=Unus ed Wi ndows Serv icesBlock//T CP 1027=Un usedWindo ws Se rvice s Blo ck//TCP1028=Unuse d Win dowsServi ces B lock//TC P 1029=Unu sed W indow s Ser vices Bloc k//TCP 1030=U nused Wind ows S ervic es Bl ock //TCP 1033=Nets py//TCP1035=Multi dropp er//TCP1042=Bla //TCP 1045=Rasm in//TCP1047=GateC rashe r//TCP 1050=M iniCo mmandTCP 1069=Back door.Theef Serve r.202TCP 1070=Voic e,Psy ber S tream Serv er,St reami ng Au dio T rojan TCP 1080=Wing ate,W orm.B ugBea r.B,W orm.N ovarg.B//TCP1090=Xtrem e, VD OLive//T CP 1095=Ra t//TCP 1097=R at//TCP1098=Rat //TCP 1099=RatTCP1110=nfsd-keepa liveTCP1111=Backd oor.A IMVis ion TCP 1155=N etwor k Fil e Acc ess //TCP 1170=Psyb er St reamServe r,Str eamin g Aud io tr ojan,Voice //T CP 1200=No BackO//T CP 1201=No BackO//T CP 1207=So ftwar//T CP 1212=Ni rvana,Visu l Kil ler //TCP 1234=Ulto rs//TCP1243=BackD oor-G, Sub Seven, Sub Seven Apoc alyps e//TCP 1245=V ooDoo Doll//T CP 1269=Ma veric ks Ma trix//TC P 1313=Nir vana//TC P 1349=Bio Net TCP 1433=M icros oft S QL服务//TC P 1441=Rem ote S torm//TC P 1492=FTP99CMP(Back Oriff ice.F TP) TCP 1503=N etMee tingT.120//T CP 1509=Ps yberStrea mingServe r//TCP 1600=S hivka-Burk a//TCP 1703=E xloit er 1.1TC P 1720=Net Meeti ng H.233 c all S etupTCP1731=NetMe eting音频调用控制//TCP 1966=Fake FTP2000//TC P 1976=Cus tom p ort //TCP 1981=Shoc kraveTCP 1990=stun-p1 c iscoSTUNPrior ity 1 portTCP 1990=stun-p1 c iscoSTUNPrior ity 1 portTCP 1991=stun-p2 c iscoSTUNPrior ity 2 portTCP 1992=stun-p3 c iscoSTUNPrior ity 3 port,ipse ndmsg IPse ndmsg TCP 1993=snmp-tcp-portcisco SNMP TCPportTCP1994=stun-portcisco seri al tu nnelportTCP1995=perf-portcisco perf portTCP 1996=tr-r srb-p ort c iscoRemot e SRB portTCP 1997=gdp-portcisco Gate way D iscov ery P rotoc olT CP 1998=x25-svc-port cisc o X.25 ser vice(XOT)//T CP 1999=Ba ckDoo r, Tr ansSc out //TCP 2000=DerSpaeh er,IN saneNetwo rkT CP 2002=W32.Bea gle.A X @mm//T CP 2001=Tr ansmi ssonscout//T CP 2002=Tr ansmi ssonscout//T CP 2003=Tr ansmi ssonscout//T CP 2004=Tr ansmi ssonscout//T CP 2005=TT ransm isson scou tTC P 2011=cyp ressTCP2015=raid-cs//TCP2023=Rippe r,Pas s Rip per,H ack C ity R ipper ProTCP2049=NFS //TCP 2115=Bugs//T CP 2121=Ni rvana//T CP 2140=De ep Th roat, TheInvas or//TCP2155=Nirva na//TCP2208=RuX //TCP 2255=Illu sionMaile r//TCP 2283=H VL Ra t5//TCP2300=PC Ex plore r//TCP 2311=S tudio54T CP 2556=Wo rm.Bb eagle.q//TCP2565=Strik er//TCP2583=WinCr ash //TCP 2600=Digi tal R ootBe er//TCP2716=Praye r Tro jan TCP 2745=W orm.B Beagl e.k //TCP 2773=Back door,SubSe ven //TCP 2774=SubS even2.1&2.2//TCP 2801=P hinea s Phu cker//TC P 2989=Rat//T CP 3024=Wi nCras h tro jan TCP 3128=Ring Zero,Worm.Novar g.B //TCP 3129=Mast ers P aradi se//TCP3150=DeepThroa t, Th e Inv asorTCP3198=Worm.Novar g//TCP 3210=S chool Bus TCP 3332=W orm.C ycle.aTC P 3333=Pro siakTCP3389=超级终端//TC P 3456=Ter ror //TCP 3459=Ecli pse 2000 //TCP 3700=Port al of Doom//T CP 3791=Ec lypse//T CP 3801=Ec lypseTCP 3996=Port al of DoomTCP 4000=腾讯QQ客户端TCP 4060=P ortal of D oom TCP 4092=W inCra shT CP 4242=VH MTC P 4267=Sub Seven2.1&2.2T CP 4321=Bo BoT CP 4444=Pr osiak,Swif t rem ote TCP 4500=W32.HL LW.Tu fas TCP 4567=F ile N ail TCP 4590=I CQTro jan TCP 4899=R emote Admi nistr ator服务器T CP 4950=IC QTroj anT CP 5000=Wi ndows XP服务器,Blaz er 5,Bubbe l,Bac k Doo r Set up,So ckets de T roieTCP5001=BackDoorSetup, Soc ketsde Tr oie TCP 5002=c d00r,ShaftTCP 5011=Oneof th e Las t Tro jans(OOTL T)T CP 5025=WM Remo te Ke yLogg erT CP 5031=Fi rehot cker,Metro polit an,Ne tMetr oTC P 5032=Met ropol itanTCP5190=ICQ Q ueryTCP5321=Fireh otcke rTC P 5333=Bac kageTroja n Box 3T CP 5343=WC rat TCP 5400=B ladeRunne r, Ba ckCon struc tion1.2T CP 5401=Bl ade R unner,Back Cons truct ion TCP 5402=B ladeRunne r,Bac k Con struc tionTCP5471=WinCr ash TCP 5512=I llusi on Ma ilerTCP5521=Illus ion M ailerTCP 5550=Xtcp,INsa ne Ne tworkTCP 5554=Worm.Sass erT CP 5555=Se rveMeTCP 5556=BO F acilTCP5557=BO Fa cil TCP 5569=R obo-H ack TCP 5598=B ackDo or 2.03T CP 5631=PC AnyWh ere d ata TCP 5632=P CAnyW hereTCP5637=PC Cr asherTCP 5638=PC C rashe rTC P 5698=Bac kDoorTCP 5714=Winc rash3TCP 5741=WinC rash3TCP 5742=WinC rashTCP5760=Portm ap Re moteRootLinux Expl oit TCP 5880=Y3K RA TTC P 5881=Y3K RATTCP5882=Y3K R ATT CP 5888=Y3K RATTCP 5889=Y3KRAT TCP 5900=W inVnc,Wise VGA广播端口TCP 6000=B ackdo or.ABTCP 6006=Nokn ok8 TCP 6129=D amewa re Nt Util ities服务器TCP 6272=S ecret Servi ceT CP 6267=广外女生T CP 6400=Ba ckdoo r.AB,The T hingTCP6500=Devil 1.03TCP 6661=Tema nTC P 6666=TCP shell.cT CP 6667=NT Remo te Co ntrol,Wise播放器接收端口TCP 6668=W ise V ideo广播端口TCP 6669=V ampyr eTC P 6670=Dee pThro at,iP honeTCP6671=DeepThroa t 3.0TCP 6711=SubS evenTCP6712=SubSe ven1.xTC P 6713=Sub SevenTCP 6723=Mstr eam TCP 6767=N T Rem ote C ontro lTC P 6771=Dee pThro atT CP 6776=Ba ckDoo r-G,S ubSev en,2000 Cr acksTCP6777=Worm.BBeag leT CP 6789=Do ly Tr ojanTCP6838=Mstre amT CP 6883=De ltaSo urceTCP6912=ShitHeepTCP6939=Indoc trina tionTCP6969=GateC rashe r, Pr iorit y, IR C 3 TCP 6970=R ealAu dio,G ateCr asherTCP 7000=Remo te Gr ab,Ne tMoni tor,S ubSev en1.xTCP 7001=Frea k88 TCP 7201=N etMon itorTCP7215=BackD oor-G, Sub SevenTCP 7001=Frea k88,F reak2kTC P 7300=Net Monit orT CP 7301=Ne tMoni tor TCP 7306=N etMon itor,NetSp y 1.0TCP 7307=NetM onito r, Pr ocSpyTCP 7308=NetM onito r, XSpy TCP 7323=S ygate服务器端TCP7424=HostContr olT CP 7597=Qa zTC P 7609=Sni d X2TCP7626=冰河T CP 7777=Th e Thi ngT CP 7789=Ba ck Do or Se tup,ICQKi llerTCP7983=Mstre amT CP 8000=腾讯OICQ服务器端,X DMA TCP 8010=W ingat e,Log fileTCP8080=WWW 代理,Rin g Zer o,Chu bo,Wo rm.No varg.B TC P 8520=W32.Soca y.Wor mTC P 8787=Bac kOfri ce 2000T CP 8897=Ha ck Of fice,Armag eddonTCP 8989=Reco nTC P 9000=Net minis trato rTC P 9325=Mst reamTCP9400=InCom mand1.0 TCP 9401=I nComm and 1.0T CP 9402=In Comma nd 1.0TC P 9872=Por tal o f Doo mTC P 9873=Por tal o f Doo mTC P 9874=Por tal o f Doo mTC P 9875=Por tal o f Doo mTC P 9876=Cyb er At tacke rTC P 9878=Tra nsSco utT CP 9989=In i-Kil ler TCP 9898=W orm.W in32.Dabbe r.a TCP 9999=P rayer Troj anT CP 10067=P ortal of D oom TCP 10080=Worm.Novar g.B TCP 10084=Syphi llisTCP10085=Syph illisTC P 10101=Br ainSp yTC P 10167=Po rtalOf Do omT CP 10168=W orm.S upnot.78858.c,W orm.L ovGat e.T TCP 10520=AcidShive rsT CP 10607=C oma t rojanTCP 10666=Amb ush TCP 11000=Senna SpyTCP11050=Host Cont rol TCP 11051=HostContr olT CP 11223=P rogen ic,Ha ck '99KeyL oggerTCP 11831=TRO J_LAT INUS.SVR TCP 12076=Gjame r, MS H.104bTC P 12223=Ha ck'99 KeyL oggerTCP 12345=Gab anBus, Net Bus 1.6/1.7, Pi e Bil l Gat es, X-billTCP 12346=Gab anBus, Net Bus 1.6/1.7, X-billTCP12349=BioN etT CP 12361=W hack-a-mol eTC P 12362=Wh ack-a-moleTCP 12363=Wha ck-a-moleTCP[emai l=12378=W32/Gib e@MM]12378=W32/Gibe@MM[/e mail] TCP 12456=Net Bus TCP 12623=DUN C ontro lTC P 12624=Bu ttmanTCP 12631=Wha ckJob, Wha ckJob.NB1.7TC P 12701=Ec lipse2000TCP12754=Mstr eam TCP 13000=Senna SpyTCP13010=Hack er Br azilTCP13013=Psyc hwardTCP 13223=Tri bal V oice的聊天程序P owWowTCP 13700=Kua ng2 T he Vi rus TCP 14456=Soler oTC P 14500=PC Inva der TCP 14501=PC In vaderTCP 14502=PCInvad erT CP 14503=P C Inv aderTCP15000=NetD aemon 1.0TCP15092=Host Cont rol TCP 15104=Mstre amT CP 16484=M osuck erT CP 16660=S tache ldrah t (DD oS) TCP 16772=ICQ R eveng eTC P 16959=Pr iorit yTC P 16969=Pr iorit yTC P 17027=提供广告服务的Condu cent"adbot"共享软件TCP 17300=Kuang2 The Viru sTC P 17490=Cr azyNe tTC P 17500=Cr azyNe tTC P 17569=In fecto r 1.4.x +1.6.xTCP 17777=Nep hronTCP18753=Shaf t (DD oS) TCP 19191=蓝色火焰TCP19864=ICQReven geT CP 20000=M illen niumII (G rilFr iend)TCP 20001=Mil lenni um II (Gri lFrie nd) TCP 20002=Acidk oRT CP 20034=N etBus 2 Pr oTC P 20168=Lo vgateTCP 20203=Log ged,C hupac abraTCP20331=BlaTCP20432=Shaf t (DD oS) TCP 20808=Worm.LovGa te.v.QQT CP 21544=S chwin dler1.82,GirlF riendTCP 21554=Sch windl er 1.82,Gi rlFri end,E xloit er 1.0.1.2 TCP 22222=Pro siak,RuX U pload er 2.0TC P 22784=Ba ckdoo r.Int ruzzoTCP 23432=Asy lum 0.1.3TCP23456=Evil FTP, Ugly FTP, Whac kJobTCP23476=Dona ld Di ckT CP 23477=D onald DickTCP 23777=INe t SpyTCP 26274=Del taT CP 26681=S py Vo ice TCP 27374=Sub S even2.0+, Back door.BasteTCP 27444=Tri bal F loodNetwo rk,Tr inooTCP27665=Trib al Fl ood N etwor k,Tri noo TCP 29431=HackAttac kTC P 29432=Ha ck At tackTCP29104=Host Cont rol TCP 29559=TROJ_LATIN US.SV RTC P 29891=Th e Une xplai ned TCP 30001=Terr0r32 TCP 30003=Death,Lame rs De ath TCP 30029=AOL t rojanTCP 30100=Net Spher e 1.27a,Ne tSphe re 1.31T CP 30101=N etSph ere 1.31,N etSph ere 1.27aTCP30102=NetS phere 1.27a,Net Spher e 1.31TC P 30103=Ne tSphe re 1.31T CP 30303=S ocket s deTroieTCP 30947=Int ruseTCP30999=Kuan g2T CP 21335=T ribal Floo d Net work,Trino oTC P 31336=Bo Whac kTC P 31337=Ba ron N ight,BO cl ient,BO2,B o Fac il,Ba ckFir e,Bac k Ori fice,DeepB O,Fre ak2k,NetSp yTC P 31338=Ne tSpy,BackOrifi ce,De epBOTCP31339=NetS py DKTCP 31554=Sch windl erT CP 31666=B OWhac kTC P 31778=Ha ck At tackTCP31785=Hack Atta ckT CP 31787=H ack A ttackTCP 31789=Hac k Att ack TCP 31791=HackAttac kTC P 31792=Ha ck At tackTCP32100=Pean utBri ttleTCP32418=Acid Batt ery TCP 33333=Prosi ak,Bl akhar az 1.0TC P 33577=So n OfPsych wardTCP33777=SonOf Ps ychwa rdT CP 33911=S pirit 2001aTC P 34324=Bi gGluc k,TN,TinyTelne t Ser ver TCP 34555=Trin00 (Wi ndows) (DD oS) TCP 35555=Trin00 (Wi ndows) (DD oS) TCP 36794=Worm.Bugbe ar-ATCP37651=YATTCP40412=TheSpy TCP 40421=Agent 40421,Mas tersParad ise.96TC P 40422=Ma sters Para diseTCP40423=Mast ers P aradi se.97TCP 40425=Mas tersParad ise TCP 40426=Maste rs Pa radis e 3.xTCP 41666=Rem ote B oot TCP 43210=Schoo lbus1.6/2.0T CP 44444=D eltaSourc eTC P 44445=Ha ppypi gTC P 47252=Pr osiakTCP 47262=Del taT CP 47878=B irdSp y2T CP 49301=O nline Keyl oggerTCP 50505=Soc ketsde Tr oie TCP 50766=Fore, Schw indle rTC P 51966=Ca feIniTCP 53001=Rem ote W indow s Shu tdownTCP 53217=Aci d Bat tery2000TCP54283=Back Door-G, S ub7 TCP 54320=BackOrifi ce 2000,Sh eep TCP 54321=Schoo l Bus .69-1.11,Sheep, BO2K TC P 57341=Ne tRaid erT CP 58008=B ackDo or.Tr onT CP 58009=B ackDo or.Tr onT CP 58339=B uttFu nnelTCP59211=Back Door.DuckT oyT CP 60000=D eep T hroatTCP 60068=Xzi p 6000068TCP60411=Conn ectio nTC P 60606=TR OJ_BC KDOR.G2.ATCP61466=Tele comma ndo TCP 61603=Bunke r-kil lTC P 63485=Bu nker-killTCP65000=Devi l, DD oST CP 65432=T h3tr41t0r, TheTrait orT CP 65530=T ROJ_W INMIT E.10TCP65535=RC,A doreWorm/LinuxTCP 69123=Shi tHeepTCP 88798=Arm agedd on,Ha ck Of fice。

DOW分析法在原油罐区安全评估中的应用浅谈

2 1评 价方 法简 介 .

道化 学公司火灾爆炸指数法( 简称 DO 指数法) W 是美 国道 化 学公 司于 16 在 化 工 过 程 及 生产 装 置 的 火 灾爆 炸危 险 9 4年 度评价 法及其相应措 施 中提 出的, 它利用工艺过程 中的物质、 设 备 等 数 据 逐 步 推 算 , 出其 火 灾 爆炸 的 潜 在危 险 。 估 中使 求 评

T b3 Co e s t n f ea d e p o i nrs d x c lu a in a . mp n ai r n x l so i i e ac l t o i k n o

() 2 3V 的计算根据 该油库的具体条件和 DO 指数法的有 W 关规定 ,得出基本系数为 1 ( 毒性物质 危险系数为 05 ,罐 .) 0, .0 装可燃性液体 的危 险系数为 05 , . 储存 中的液体及气体 的危险 0 系数为 02 ,腐蚀与磨损危 险系数为 0 0 . 0 . ,泄漏( 4 接头 和填 料) 的危 险系 数为 O6 ,使 用 明火设 备 的危险 系数 为 0 0 .0 . ,则 2

Applc to fD o C h m i a r sa p o i eI i a i n o w e c l Fie nd Ex l sv nde nay i e ho xA l ssM t d i i De tS f t n O l po a ey Eva u to l a in

212 单 元 危 险 度 的初 期 评 价 ._ 火灾、爆炸危险指数(&E ) 下式计算 : F I 按

F& EI M F =F3 X

式 中:F一工艺单元危 险系数 , 3 l 2 3 F=F ×F ;MF 物质系 一 数 ;F一一般工艺危 险系数 ;F一特殊工艺危险系数 。 2 求 出火灾 、爆炸危险指数后 , 按表确定 其火灾、爆炸危 险

DOW CORNING

Dow Corning Corporation

12

SR2410树脂耐溶剂性

溶剂

擦拭试验(回数)注2) 室温×7日 200℃×30分

甲苯 苯乙烯 1,1,1-三氯乙烷 乙二醇乙醚醋酸 酯

40-50 20-30 40-50 40-50

170-180 200以上 200以上

120-130

注1)基材:软钢板 注2)擦拭试验:用浸透溶剂的纱布,荷重700g在SR2410树脂涂膜上擦拭, 以露出基材时往返移动的次数表示

Dow Corning Corporation

15

SR2510的一般特性

项目 外观 粘度 比重 不挥发份 溶剂

单位

特性

—

无色微浊液体

mm2/s

1.8

—

0.81

%

20

异丙醇

20-30%

异链烷烃(isoparaffin) 40-50%

Dow Corning Corporation

16

SR2510固化后的特性

Magic ink drawing test

Dow Corning Corporation

Wipe off test

25

塗佈在PC上的性能

Propeolloidal silica

水接觸角

96°

°

73°

87°

耐磨 (Tabor Test)(%) 耐磨 (Steel Wool Test)(%) 铅筆硬度 (SUS) 铅筆硬度(PET) 靜磨擦系數 密著 耐酸性 耐鹼性 耐溶劑性 油污擦拭性

Dow Corning Corporation

8

SR 2410 的固化條件

Cure Temp. (C degree)

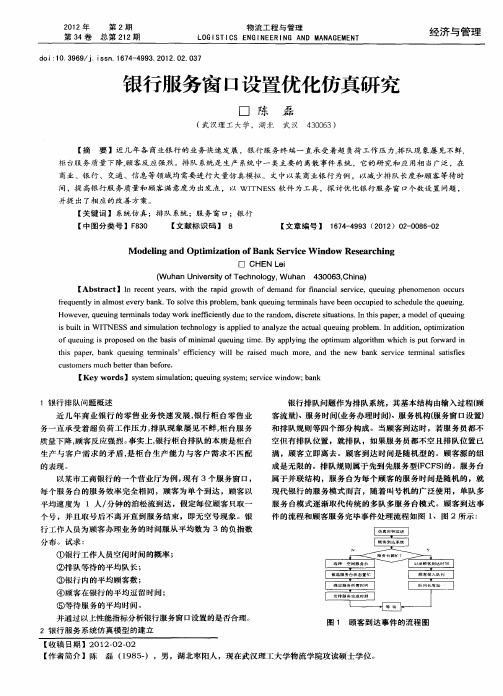

银行服务窗口设置优化仿真研究

( u a n es yo e h oo y W u a 4 0 6 ,hn ) W h nU i ri f c n lg , h n 3 0 3C ia v t T

[ Absr c ]I e e ty as t erpd go h o e n o n n ilsr ie q e ig p e o n n O C R ta t n rcn er,wi t a i rwt fd ma d frf a ca evc , u un h n me o CU S hh i

行工作人员为顾客办理业务的时间服从 平均数为 3的负指数

分 布 。试 求 : ① 银 行 工 作 人 员 空 闲 时 间 的概 率 ;

②排队等待的平均队长 ;

③ 银 行 内 的平 均 顾 客 数 ;

④顾客在银行的平均逗留时问 ;

⑤等待服务的平均时间 。 并通 过 以上 性能 指 标 分析 银 行 服 务窗 口设置 的是 否合 理 。

银行服务窗 口设置优化仿真研 究

口 陈 磊

( 汉理 5 大 学 , 湖北 武 - 武汉 406 3 03)

【 摘

要 】近 几 年 各 商 业 银 行 的业 务 快 速发 展 ,银 行 服 务 终 端 一 直 承 受 着 超 负荷 工作 压 力 , 队现 象屡 见 不 鲜 , 排

柜 台服 务 质 量 下 降 , 客 反 应 强 烈 。排 队 系统 是 生 产 系统 中 一类 主 要 的 离散 事 件 系统 ,它 的研 究 和 应 用 相 当广 泛 ,在 顾 商 业 、银 行 、 交通 、信 息 等 领 域 均 需 要 进 行 大量 仿 真模 拟 。 文 中 以某 商 业 银 行 为 例 ,以 减 少排 队 长 度 和 顾 客 等 待 时

美国Dow化学公司与SiamCement集团公司合资在泰国建特殊弹性体生产装置

Байду номын сангаас

( 司苒 ) 张

BS A F公司推 出 首例抗茵 A A塑料 S

E rPts. ws 1 tb r 0 8 u . a tNe ,3 Oco e 0 2

据称 , 种水 平 的 透 明度 目前 可 以 与 能 这 够提供玻璃状 透 明度 的 P C和其 他 工程 聚合

医用治疗椅或办公室计算机键盘。 B S A F公 司称 : 与 典 型 的 A A性 能 如 “ S

耐风化 性 、 温老 化稳定 性 、 高 良好 的耐化学性

沙特 阿拉伯基础产业公司

新 建聚 丙 烯 生 产 装 置

石油化 学新报 ( ,0 8 ( 2 0 : 日)2 0 ;4 7 )4

国内外石 油化 工快 报

・7 2

今后 还 要进行 P VA树脂 的多牌号 的生产 。

可 乐丽公司在 德 国的子 公 司可 乐丽 欧 洲

公 司计划 2 1 之前 增 设 P A 树脂 生 产装 0 1年 V

置, 以扩增 P A树脂 的生产能力。然后 , V 为了

两公 司 在 2 0 0 5年 成 立 了 合 资 公 司

与P C相 比较低 的加工 温 度 将转 化 成能 耗 的

降低 。另外 , 高 的熔 体 流 动还 意 味 着 极好 较 的“ 剪切稀 化性 能 ”这 将 导 致 输 出功 率 的 改 ,

进。

( 淑战 ) 赵

包括, 烘手器、 皂盒 、 肥 整体公共盥洗室 的卫

生设 备 。可能受 益 的其 它 方面包括 : 医用 床 、

药设 备用 途 。

示 , 以得到 白色样 品 。 可 这 种抗菌 材 料含 有 银 化 合 物 , 它结 合 把 到该塑 料 中 , 赋予其 表 面杀菌作 用 。 将 BS A F公 司认 为 , 种 材 料 的 应 用 范 围 这

用DOW对双氧水生产装置的危险评价

坚

O ( )+ 83k/ l 2 g 9 . Jmo

,Ho( )+ 2 1 ,Ho( )+ 2: g

生产工艺使用 了芳烃 、 氢气等易燃物质 , 存在压缩 空气等助燃物 , 这些都是发生火灾、 爆炸的充分必 要条件。现分别对各个工序进行危险因素识别。

2 1 配制 工序 .

塑

和 白土床 来分解 、 吸收 , 去双 氧水 和水分 。 除 26 成 品灌装 工序 . 成 品灌装 工 序 的 主 要 设 备 为 2个 双 氧水 储

时 , 会 引起爆 炸 。 因此 , 本工 序 必须利 用 碱塔 就 在

氧化 工序 主要设 备为 氧化 塔 。氧化 工 序采用 空气 液相 氧化 的工 艺 , 然 该 工 艺 具 有 氧 化 剂 简 虽 便易 得 、 产 成本 低 等 优 点 , 安 全 性 较 差 , 生 但 主要

表现 在氧 化反 应 的条件 上 。 因氢化 液被 空气 氧化 是气 一液 相反 应 , 相 向液相 扩 散速 度慢 , 由于 气 又 空气 中氧含 量 的 限制 , 影 响反 应速 度 , 高温度 会 提

不 当 、 料等 , 险就 会发 生 。 跑 危

2 3 氧 4 Y序 . E- - -

的重 金属 离子 必 须 去 掉 , 因为 重 金 属 离子 能促 使

双氧水 的分解 。

2 5 后 处理 工序 .

后处理工序主要设备为碱塔。从萃取塔顶排

出 的萃 余 液含 有少 量 的双 氧水 ( . / ) O 1gL 和水 , 如 果 直接 返 回氢 化 系统使 用 , 将导致 氢 化塔 中的氢 、 氧混合 , 成爆 炸性 混合 物 , 形 氧含 量达 到爆 炸 范 围

进行 了分析与识别 , 利用 D W 对生产工艺各单元进 行了危险评价 , O 并给出了对 策措施 。 关键词

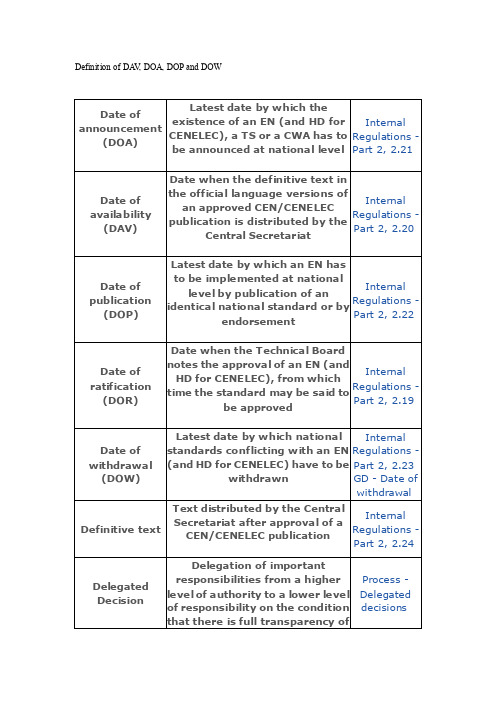

DefinitionofDAV,DOA,DOPandDOW

Latest date by which the

Date of announcement

(DOA)

existence of an EN (and HD for Internal CENELEC), a TS or a CWA has to Regulations -

Deliverable

The ess, usually used as a

generic term for a type of

published document, e.g.

European Standard, a Technical Internal

CEN/CENELEC publication Regulations Part 2, 2.24

Delegated Decision

Delegation of important responsibilities from a higher le ve l of a uthority to a lower le ve l of responsibility on the condition that there is full transparency of

Internal

publication is distributed by the Regulations -

Central Secretariat

Part 2, 2.20

Date of publication

(DOP)

Latest date by which an EN has

to be implemented at national

notes the approval of an EN (and

Standard Poor s Research Insight Compustat 使用手冊