财务管理英文Chapter 3PPT课件

合集下载

Chapter 3 The Time Value of Money 货币的时间价值 财务管理(双语版) 教学课件

年金现值:PVAn(Present Value of an Ordinary Annuity)

n 1

11i n

PV nR A t 11it R i

R PVi,nI

PVIFAi,n 年金现值系数(the Present Value Interest Factor of an Annuity at i for n periods)

P0V P 0FnV 1inFnV PVi,nIF

7. PVIFi,n : (the Present Value Interest Factor at i for n

periods)

8.

复利现值系数,利率为i,期数为n

6. Annuities 年金

系列、等额的收付

Ordinary Annuity 普通年金 收付款发生于每期期末 Annuity Due 预(即)付年金 收付款发生于每期期初

Perpetuity 永续年金

无限期支付的普通年金

Ordinary Annuity(普通年金)

0

R

R

R

R

年金终值:FVAn(Future Value of an Annuity)

FV nR A t n11intR1iin1RFVi,nIFA

FVIFAi,n 年金终值系数(the Future Value Interest Factor of an Annuity at i for n periods)

1

每年计息一次时产生的利息=名义利率每年计息m次时产生的利息

FV n A R F DV i,n 1 I 1 FA

现值 (Present Value)

比普通年金少折现一期

PV n A R P D V i,nI 1 F i A

财务管理 英文版ppt

– Unlimited liability to the owner – Profits and losses are taxed as though they belong to the individual owner

1-14

Partnership

• Similar to sole proprietorship except there are two or more owners

– B2C model:

• Products are bought with credit cards • Credit card checks are performed • Selling firms get the cash flow faster

– B2B model can help companies

• At the turn of the century: Emerged as a field separate from economics • By 1930s: Financial practices revolved around such topics as:

– Preservation of capital – Maintenance of liquidity – Reorganization of financially troubled corporations – Bankruptcy process

• Lower the cost of managing inventory, accounts receivable, and cash

1-9

Financial Management

Financial management or business finance is concerned with managing an entity’s money Functions:

1-14

Partnership

• Similar to sole proprietorship except there are two or more owners

– B2C model:

• Products are bought with credit cards • Credit card checks are performed • Selling firms get the cash flow faster

– B2B model can help companies

• At the turn of the century: Emerged as a field separate from economics • By 1930s: Financial practices revolved around such topics as:

– Preservation of capital – Maintenance of liquidity – Reorganization of financially troubled corporations – Bankruptcy process

• Lower the cost of managing inventory, accounts receivable, and cash

1-9

Financial Management

Financial management or business finance is concerned with managing an entity’s money Functions:

财务管理ppt英文课件Chapter-3.ppt

100 106 112 118

Copyright 2001 Prentice-Hall, Inc.

12

Fundamentals of Financial Management, 11/e by Van Horne and Wachowicz.

Slides prepared by Wu Xiaolan

Example - Simple Interest

Interest earned at a rate of 6% for five years on a principal balance of $100.

Today

Future Years

1 2345

Interest Earned 6

Value

100 106

Future Values

Example - Simple Interest

Example - Simple Interest

Interest earned at a rate of 6% for five years on a principal balance of $100.

Today

Future Years

1 2345

Interest Earned 6 6 6

Value

5

Fundamentals of Financial Management, 11/e by Van Horne and Wachowicz.

Slides prepared by Wu Xiaolan

Interest Rate Terminology

Simple interest refers to interest earned only on the

财务管理英文课件 (3)

All rights reserved.

Cash AR Inventories Total CA Gross FA Less: Deprec. Net FA Total assets

Copyright © 2001 by Harcourt, Inc.

3-3

Liabilities and Equity 2001E 2000 Accounts payable 436,800 524,160 Notes payable 600,000 720,000 Accruals 408,000 489,600 Total CL 1,444,800 1,733,760 Long-term debt 500,000 1,000,000 Common stock 1,680,936 460,000 Retained earnings (128,584) (327,168) Total equity 1,552,352 132,832 Total L & E 3,497,152 2,866,592

n Expected to improve but still below the industry average. n Liquidity position is weak.

Copyright © 2001 by Harcourt, Inc. All rights reserved.

3 - 11

All rights reserved.

250,000 $1.014 $0.220 $12.17 $40,000

3-6

Why are ratios useful? n Standardize numbers; facilitate comparisons n Used to highlight weaknesses and strengths

Cash AR Inventories Total CA Gross FA Less: Deprec. Net FA Total assets

Copyright © 2001 by Harcourt, Inc.

3-3

Liabilities and Equity 2001E 2000 Accounts payable 436,800 524,160 Notes payable 600,000 720,000 Accruals 408,000 489,600 Total CL 1,444,800 1,733,760 Long-term debt 500,000 1,000,000 Common stock 1,680,936 460,000 Retained earnings (128,584) (327,168) Total equity 1,552,352 132,832 Total L & E 3,497,152 2,866,592

n Expected to improve but still below the industry average. n Liquidity position is weak.

Copyright © 2001 by Harcourt, Inc. All rights reserved.

3 - 11

All rights reserved.

250,000 $1.014 $0.220 $12.17 $40,000

3-6

Why are ratios useful? n Standardize numbers; facilitate comparisons n Used to highlight weaknesses and strengths

英文版中级财务会计第3章PPT

Periodic Inventory System

Beginning inventory + Purchases (net)-Ending Inventory = cost of goods sold

example

Periodic System

Apr. 1 Apr. 10 Apr. 20

100 units 80 units 70 units 250 units

Balance Sheet ($ in millions) 2009 2008 Current assets: Inventories Finished goods $ 660 $ 775 Work in process 38 43 Materials and supplies 330 402 Total $1,028 $1,220

Alternative inventory systems

A company using a perpetual system maintains a continuous record of the physical quantities in its inventory.

Comparison of system

Classification of inventory in different types of company

Merchandising company Merchandise inventory

Manufacturing company Raw materials inventory Work in process Finished goods inventory

2011 Inventory Accounts payable

财务管理英文课件3

1

2. Holding period return

If an investor has hold an assets for n periods with annual rate of return r, his holding period return is :

Holding period return 1 r 1

Geometric average return 4 (1.10) (.95) (1.20) (1.15) 1 .095844 9.58%

3

Holding Period Return: Example

Note that the geometric average is not the same thing as the ariБайду номын сангаасhmetic average:

7

Rates of Return 1926-2002

60 40

20

0

-20

Common Stocks Long T-Bonds T-Bills

-40 -60 26 30 35 40 45 50 55

60

65

70

75

80

85

90

95 2000

Source: © Stocks, Bonds, Bills, and Inflation 2000 Yearbook™, Ibbotson Associates, Inc., Chicago (annually updates work by Roger G. Ibbotson and Rex A. Sinquefield). All rights reserved.

$5,520

2. Holding period return

If an investor has hold an assets for n periods with annual rate of return r, his holding period return is :

Holding period return 1 r 1

Geometric average return 4 (1.10) (.95) (1.20) (1.15) 1 .095844 9.58%

3

Holding Period Return: Example

Note that the geometric average is not the same thing as the ariБайду номын сангаасhmetic average:

7

Rates of Return 1926-2002

60 40

20

0

-20

Common Stocks Long T-Bonds T-Bills

-40 -60 26 30 35 40 45 50 55

60

65

70

75

80

85

90

95 2000

Source: © Stocks, Bonds, Bills, and Inflation 2000 Yearbook™, Ibbotson Associates, Inc., Chicago (annually updates work by Roger G. Ibbotson and Rex A. Sinquefield). All rights reserved.

$5,520

财务管理英语chapter3

2) The non-operating section (非营运部分) of the income statement includes all financing costs, such as interest expense.

3) Usually a separate section reports the amount of taxes levied on income.

则(GAPP)).

Annual Report (年报):

年报中包括2种信息

公司总经理的公开信(letter to stockholders) 4种基本的财务报表(financial statements)

1-7

Balance sheet Income statement Statement of cash flows Statement of retained earnings

to determine incentives and rewards to allocate capital investment in firm’s segment or divisions

1-5

Anyway ,financial statements are probably the most important source of information,because various stakeholders can assess a firm’s financial health. Whereas,it is not easy to assess a firm’s real financial status

1-10

Debt versus Equity •Creditors generally receive the first claim on the firm’s cash flow. •Shareholder’s equity is the residual difference between assets and liabilities.

3) Usually a separate section reports the amount of taxes levied on income.

则(GAPP)).

Annual Report (年报):

年报中包括2种信息

公司总经理的公开信(letter to stockholders) 4种基本的财务报表(financial statements)

1-7

Balance sheet Income statement Statement of cash flows Statement of retained earnings

to determine incentives and rewards to allocate capital investment in firm’s segment or divisions

1-5

Anyway ,financial statements are probably the most important source of information,because various stakeholders can assess a firm’s financial health. Whereas,it is not easy to assess a firm’s real financial status

1-10

Debt versus Equity •Creditors generally receive the first claim on the firm’s cash flow. •Shareholder’s equity is the residual difference between assets and liabilities.

International FinancialManagement 3国际财务管理课件课件

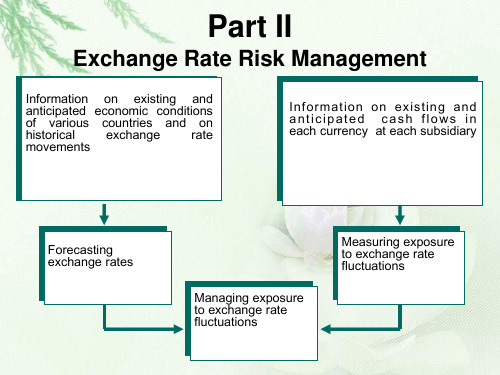

Part II

Exchange Rate Risk Management

Information on existing and anticipated economic conditions of various countries and on historical exchange rate movements

this regression model:

14

Fundamental Forecasting

et = a0 + a1INTt + a2INFt-1 + µt

where et = percentage change in the peso’s exchange rate over period t

10

Fundamental Forecasting

* The second step is to generate the values of regression coefficients (b0, b1, and b2) by using the historical data of BP, INF and INC. To illustrate, assume the following values:

9

Fundamental Forecasting

* The first step is to determine how these variables have affected the percentage change in the pound’s value based on historical data.

13

Fundamental Forecasting

• Use of sensitivity analysis for fundamental

Exchange Rate Risk Management

Information on existing and anticipated economic conditions of various countries and on historical exchange rate movements

this regression model:

14

Fundamental Forecasting

et = a0 + a1INTt + a2INFt-1 + µt

where et = percentage change in the peso’s exchange rate over period t

10

Fundamental Forecasting

* The second step is to generate the values of regression coefficients (b0, b1, and b2) by using the historical data of BP, INF and INC. To illustrate, assume the following values:

9

Fundamental Forecasting

* The first step is to determine how these variables have affected the percentage change in the pound’s value based on historical data.

13

Fundamental Forecasting

• Use of sensitivity analysis for fundamental

财务管理 第三章 课件

843 / (843 + 2,556) = 24.80%

B/S I/S

3-13

Computing Coverage Ratios

• Times Interest Earned = EBIT / Interest

1,138 / 7 = 162.57 times

• Cash Coverage = (EBIT + Depreciation) / Interest

Operating Activity – includes net income and changes in most current accounts Investment Activity – includes changes in fixed assets Financing Activity – includes changes in notes payable, long-term debt, and equity accounts, as well as dividends

• Notes payable and long-term debt

3-6

Statement of Cash Flows

• Statement that summarizes the sources and uses of cash • Changes divided into three major categories

Compute all accounts as a percent of total assets

• Common-Size Income Statements

Compute all line items as a percent of sales

B/S I/S

3-13

Computing Coverage Ratios

• Times Interest Earned = EBIT / Interest

1,138 / 7 = 162.57 times

• Cash Coverage = (EBIT + Depreciation) / Interest

Operating Activity – includes net income and changes in most current accounts Investment Activity – includes changes in fixed assets Financing Activity – includes changes in notes payable, long-term debt, and equity accounts, as well as dividends

• Notes payable and long-term debt

3-6

Statement of Cash Flows

• Statement that summarizes the sources and uses of cash • Changes divided into three major categories

Compute all accounts as a percent of total assets

• Common-Size Income Statements

Compute all line items as a percent of sales

财务管理课件chanpter3

附:梦幻酒店和希尔顿酒店1991年的资产负债表及损益表。

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

n 梦幻酒店:资产负债率=96.85% 应收帐款周转率= 30.75 存货周转率=2.21 总资产周转率=0.58 流动 比率=0.76 利息所得倍数=0.57 毛利率=86%

计算速动比率时将存货从流动资产中剔除,主要原因是:(1)流动资产中 存货的变现速度最慢;(2)由于某种原因,部分存货可能已过时,损失 还未作报废处理;(3)部份存货已抵押给债权人;(4)存货估价上存 在成本与合理市价相差悬殊的问题。

通常情况下,速动比率为1被认为是较正常的。影响速动比率可信度的主要 因素是应收帐款的变现能力,因为帐面上的应收帐款不一定都能变成现 金。分析时,要考虑行业和企业的具体情况。

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

(一)偿债能力评价

1、流动比率 流动比率是流动资产除以流动负债的比值。其计算公式为:

它表明飞天公司每1元负债有1.71元流动资产作保障。

在财务管理中,流动比率是评价、反映企业短期偿债能力的 一个重要指标。它是个正指标,一般情况下,流动资产越 多,短期负债越少,则偿债能力越强,债权人的权益越有 保障。

(3))相关比率

两个相关指标之比,揭示酒店某一方面财务状况的财务比率。如 流动比率,通过流动资产与流动负债之比,反映酒店的短期还 款能力。

3)趋势分析法

趋势分析法指通过比较酒店连续数期财务报表有关项目的金额, 以揭示其财务状况变动趋势的一种分析方法。它从动态的角度 反映企业的财务状况及经营成果,较深刻地揭示了各财务指标 的消长变化及发展趋势,有利于对酒店未来作出合乎逻辑的预 测。

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

n 梦幻酒店:资产负债率=96.85% 应收帐款周转率= 30.75 存货周转率=2.21 总资产周转率=0.58 流动 比率=0.76 利息所得倍数=0.57 毛利率=86%

计算速动比率时将存货从流动资产中剔除,主要原因是:(1)流动资产中 存货的变现速度最慢;(2)由于某种原因,部分存货可能已过时,损失 还未作报废处理;(3)部份存货已抵押给债权人;(4)存货估价上存 在成本与合理市价相差悬殊的问题。

通常情况下,速动比率为1被认为是较正常的。影响速动比率可信度的主要 因素是应收帐款的变现能力,因为帐面上的应收帐款不一定都能变成现 金。分析时,要考虑行业和企业的具体情况。

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

PPT文档演模板

财务管理课件chanpter3

(一)偿债能力评价

1、流动比率 流动比率是流动资产除以流动负债的比值。其计算公式为:

它表明飞天公司每1元负债有1.71元流动资产作保障。

在财务管理中,流动比率是评价、反映企业短期偿债能力的 一个重要指标。它是个正指标,一般情况下,流动资产越 多,短期负债越少,则偿债能力越强,债权人的权益越有 保障。

(3))相关比率

两个相关指标之比,揭示酒店某一方面财务状况的财务比率。如 流动比率,通过流动资产与流动负债之比,反映酒店的短期还 款能力。

3)趋势分析法

趋势分析法指通过比较酒店连续数期财务报表有关项目的金额, 以揭示其财务状况变动趋势的一种分析方法。它从动态的角度 反映企业的财务状况及经营成果,较深刻地揭示了各财务指标 的消长变化及发展趋势,有利于对酒店未来作出合乎逻辑的预 测。

财务管理英文Cha3课件

➢ Assets covenants ➢ Dividend covenants ➢ Financing covenants ➢ Bonding covenants ➢ Financial ratio covenants ➢ Sinking fund covenants.

Not all of these types of covenants are included in every bond.

Copyright 2001 Prentice-Hall, Inc.

9

Bonding covenants

Describe the mechanism for enforcement of the covenants.

For example, the mechanism includes an independent audit of the company’s financial statements and appointment of a trustee to represent the bondholders and monitor the firm’s compliance with bond covenants.

Chapter Objectives

Explain the characteristics of debt. Identify the different types of debentures. Outline the provisions of a Bond Covenants. Discuss the different features of both preferred

Copyright 2001 Prentice-Hall, Inc.

13

Not all of these types of covenants are included in every bond.

Copyright 2001 Prentice-Hall, Inc.

9

Bonding covenants

Describe the mechanism for enforcement of the covenants.

For example, the mechanism includes an independent audit of the company’s financial statements and appointment of a trustee to represent the bondholders and monitor the firm’s compliance with bond covenants.

Chapter Objectives

Explain the characteristics of debt. Identify the different types of debentures. Outline the provisions of a Bond Covenants. Discuss the different features of both preferred

Copyright 2001 Prentice-Hall, Inc.

13

财务管理英文版(PPT 60页)

13-2

13-3

Proposed Project Data

Julie Miller is evaluating a new project for her firm, Basket Wonders (BW).

She has determined that the after-tax cash flows for the project will be

$40,000 = $10,000(.909) + $12,000(.826) + $15,000(.751) + $10,000(.683) + $ 7,000(.621)

$40,000 = $9,090 + $9,912 + $11,265 + $6,830 + $4,347

= $41,444 [Rate is too low!!]

$1,444 $4,603

X

$1,444

.05 = $4,603

13-15

IRR Solution (Interpolate)

X .05

.10 $41,444 IRR $40,000 .15 $36,841

$1,444 $4,603

X

$1,444

.05 = $4,603

13-16

IRR Solution (Interpolate)

13-13

IRR Solution (Try 15%)

$40,000 = $10,000(PVIF15%,1) + $12,000(PVIF15%,2) + $15,000(PVIF15%,3) + $10,000(PVIF15%,4) + $ 7,000(PVIF15%,5)

13-3

Proposed Project Data

Julie Miller is evaluating a new project for her firm, Basket Wonders (BW).

She has determined that the after-tax cash flows for the project will be

$40,000 = $10,000(.909) + $12,000(.826) + $15,000(.751) + $10,000(.683) + $ 7,000(.621)

$40,000 = $9,090 + $9,912 + $11,265 + $6,830 + $4,347

= $41,444 [Rate is too low!!]

$1,444 $4,603

X

$1,444

.05 = $4,603

13-15

IRR Solution (Interpolate)

X .05

.10 $41,444 IRR $40,000 .15 $36,841

$1,444 $4,603

X

$1,444

.05 = $4,603

13-16

IRR Solution (Interpolate)

13-13

IRR Solution (Try 15%)

$40,000 = $10,000(PVIF15%,1) + $12,000(PVIF15%,2) + $15,000(PVIF15%,3) + $10,000(PVIF15%,4) + $ 7,000(PVIF15%,5)

相关主题

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

amount for both one period and multiple periods. Calculate the present value and future value of multiple

cash flows. Calculate the present value and future value of annuities. Compare nominal interest rates (NIR) and effective

Copyright 2001 Prentice-Hall, Inc.

Compound interest复利 refers to interest earned on

both the initial capital investment and on the interest reinvested from prior period.

“World’s eighth wonder” – the power of compounding.

If you're in your 30s, you've probably started a family ... You're scraping enough together to buy your first home and make the mortgage payments.

Now in your 40s, you may be facing demands on your earnings ... You need a larger home ... The kids are taking dance and piano lessons ... they need braces ... You may have some financial responsibility for rentice-Hall, Inc.

6

Interest Rate Terminology

Simple interest refers to interest earned only on the

original capital investment amount.

annual interest rates (EAR). Determine the amortization schedule.

Copyright 2001 Prentice-Hall, Inc.

2

When you're in your 20s, you're young ... Who thinks about retiring at this age? ... You're just beginning to make some money ... Perhaps there are college loans to be paid.

0

1

2

3

4

PV

FV

Future value (FV) is the amount an investment is worth after one or more periods.

Present value (PV) is the current value of future cash flows of an investment.

Chapter 3

Time Value of

Time Value of Money

“A dollar today is worth than a dollar tomorrow.”

Copyright 2001 Prentice-Hall, Inc.

1

Chapter Objectives

Distinguish between simple and compound interest. Calculate the present value and future value of a single

By your 50s, you have children in college ... You may be experiencing late-in-career job changes or setbacks.

Suddenly you're 60, and for all the best reasons in the world you didn't save along the way ... For so long it seemed so far away ... Retirement is now upon you, and you aren't ready financially.

The rate of interest for discounting or compounding is called ‘i’ or “r”.

All time value questions involve包括 four values: PV, FV, i and n. Given three of them, it is always possible to calculate the fourth.

Copyright 2001 Prentice-Hall, Inc.

5

Time Value Terminology

The number of time periods between the present value and the future value is represented by ‘n’ or “t”.

Copyright 2001 Prentice-Hall, Inc.

3

Cash-Flow Time Line

Cash flow-in (现金流入)

0

1

2

3

4

5 Time periods

Cash flow-out (现金流出)

Copyright 2001 Prentice-Hall, Inc.

4

Time Value Terminology

cash flows. Calculate the present value and future value of annuities. Compare nominal interest rates (NIR) and effective

Copyright 2001 Prentice-Hall, Inc.

Compound interest复利 refers to interest earned on

both the initial capital investment and on the interest reinvested from prior period.

“World’s eighth wonder” – the power of compounding.

If you're in your 30s, you've probably started a family ... You're scraping enough together to buy your first home and make the mortgage payments.

Now in your 40s, you may be facing demands on your earnings ... You need a larger home ... The kids are taking dance and piano lessons ... they need braces ... You may have some financial responsibility for rentice-Hall, Inc.

6

Interest Rate Terminology

Simple interest refers to interest earned only on the

original capital investment amount.

annual interest rates (EAR). Determine the amortization schedule.

Copyright 2001 Prentice-Hall, Inc.

2

When you're in your 20s, you're young ... Who thinks about retiring at this age? ... You're just beginning to make some money ... Perhaps there are college loans to be paid.

0

1

2

3

4

PV

FV

Future value (FV) is the amount an investment is worth after one or more periods.

Present value (PV) is the current value of future cash flows of an investment.

Chapter 3

Time Value of

Time Value of Money

“A dollar today is worth than a dollar tomorrow.”

Copyright 2001 Prentice-Hall, Inc.

1

Chapter Objectives

Distinguish between simple and compound interest. Calculate the present value and future value of a single

By your 50s, you have children in college ... You may be experiencing late-in-career job changes or setbacks.

Suddenly you're 60, and for all the best reasons in the world you didn't save along the way ... For so long it seemed so far away ... Retirement is now upon you, and you aren't ready financially.

The rate of interest for discounting or compounding is called ‘i’ or “r”.

All time value questions involve包括 four values: PV, FV, i and n. Given three of them, it is always possible to calculate the fourth.

Copyright 2001 Prentice-Hall, Inc.

5

Time Value Terminology

The number of time periods between the present value and the future value is represented by ‘n’ or “t”.

Copyright 2001 Prentice-Hall, Inc.

3

Cash-Flow Time Line

Cash flow-in (现金流入)

0

1

2

3

4

5 Time periods

Cash flow-out (现金流出)

Copyright 2001 Prentice-Hall, Inc.

4

Time Value Terminology