ACCA《F4公司法与商法》精选讲义第一章(1)

公司法讲义

公司法讲义第一章公司法概述l 共四节:l 第一节、公司的法律界定l 第二节、公司法的概念与性质l 第三节、公司法的历史沿革与发展趋势l 第四节、公司法的基本原则l 本章重点讲授:公司的法律界定、公司法的基本原则第一节公司的法律界定一、公司的概念1、“公司”词义英文中“公司”对应的词有两个,但其外延均比我国公司概念大:一个是company,通常指社团,不问其是否以营利为目的,或是否为法人;另一个是corporation,专指法人社团,也不以营利性为其特征,商业性的公司,应该称为Business corporation。

Company多为西欧国家所习惯使用,而corporation多为美国所习惯使用。

l 日本称公司为“会社”。

2、公司的一般定义l 大陆法系公司的概念,可以简单概括为:依法设立的营利性社团法人。

l 英美法系国家没有明确的公司的定义,但其内涵、特征与大陆法系相似。

3、我国公司的法定定义l 我国《公司法》第2条规定:“本法所称公司是指依照本法在中国境内设立的有限责任公司和股份有限公司。

”l 第3条规定:“公司是企业法人,有独立的法人财产,享有法人财产权。

公司以其全部资产对公司的债务承担责任。

”“有限责任公司的股东以其出资额为限对公司承担责任;股份有限公司的股东以其认购股份为限对公司承担责任。

”4、学理定义l 【公司】是指股东依照公司法的规定,以出资方式设立,股东以其出资额或所持股份为限对公司承担责任,公司以其全部资产对公司债务承担责任的企业法人。

(见赵旭东《公司法学》P2)l *参考概念:公司是指由两个或两个以上的股东出资组成的,从事营利性经济活动的企业法人。

(见范健《商法》P90)对于“法人”概念的理解包含两层含义:第一,依法定程序和法定条件设立的法律主体;第二,具有独立的法律人格,可以依法独立享有民事权利并承担民事义务。

二、公司的特征l 1.营利性——l 2.社团性——l 3.法人性——第一、关于营利性------------------------社会责任一、概念广义:是指公司不能仅仅以最大限度地为股东们营利或赚钱作为自己的唯一存在目的,而应当最大限度地增进股东利益之外的其他所有社会利益,这种社会利益包括雇员利益、消费者利益、债权人利益、中小竞争者利益、当地社区利益、环境利益、社会弱者利益以及整个社会公共利益等内容,既包括自然人的人权尤其是《经济、社会和文化权利国际公约》中规定的社会、经济、文化权利,也包括自然人之外的法人和非法人组织的权利和利益。

第1章 商法导论 《商法》PPT课件

4、商品经济的发展使民法的含义得以丰富与 扩充。 5、主张民商分立将会使民法与经济法之争得 以继续。 6、民商合一对市场商品经济关系进行统一的 法律调整,有利于维护市场的统一性。 7、主张民商分立制定单独的商法典的方案, 在法律实务、理论观念和法律文化传统上都 不具备相应的条件。

7

8、如果以企业为核心,制定一部调整企业内外 部关系的商法,又会形成主体立法而非行为立 法的弊端。

12

2、民商合一与商法学作为一个法学学科矛盾

吗? (提示):不矛盾,民商合一是就立法

模式而言的,与商法学是否可以成为一个法 学学科没有多大联系。

13

四、关于“民法的商法化”和“商法的民法 化”

不管民法和商法如何的相互吸收扩张 ,我们都不应该否认商法的特殊性和一定的 独立性。商法的某些具有典型特征的规则不 可能在民法中或者民法的财产法中普遍推行。

(二)主张民商分立的理由 1、从我国经济体制改革的进程来看,民商分立 是适应市场经济发展需要的立法模式。 2、民商分立模式有利于民法与商法的发展,从 而能早日建立起适应市场经济发展所需要的法 律体系。

8

3、从商法的性质、商事交易关系的特性、商 法的特征及民商分立法体例的历史和发展看, 应采民商分立立法体例。 4、有利于表现商事主体与民事主体、商事行 为与民事行为的区别。 5、是立法技术和方法完善的标志之一。

16

第六节 商法的基本原则

一、商法基本原则的含义

是商法的主旨和基本准则,是对于各类商事 关系具有普遍适用意义或司法指导意义,对于统 一的商法规则体系具有统率作用的某些基本法律 规则。

二、商法基本原则的功能

(一)指导功能

(二)约束功能

(三)补充和解释功能

三、我国商法的基本原则

2014年ACCA考试F4公司法与商法第一章总汇1

2014年ACCA考试F4公司法与商法第一章总汇1本文由高顿ACCA整理发布,转载请注明出处Session 1 The Nature, Source and Purpose of Management AccountingMain contents:1. Data and information2. The managerial processes of planning, decision making and control3. Responsibility accounting4. Management accounting and financing accounting5. Presentation of management information1.1 Data and Information· Data consists of raw materials, which include numbers, letters, symbols, facts, events and transactions, that have been recorded but not yet processed into a form suitable for use.· Information is data which has been processed in such a way that it is meaningful to the person to the person who receives it. (for decision making purpose) The attributes of good informati on can be identified by the “ACCURATE” as shown below:· Accurate: accurate enough for the purpose· Complete: all the necessary information· Cost- effective: benefit > costs· Understandable: clear and easy to understand· Relevant: relevant to purpose· Accessible: the best way to communicate with the related person· Timely: be available at the right time· Easy to use: by management1.2 The Managerial Process of Planning , Decision Making and ControlInformation for management is likely to be used for planning, control and decision making objectives:An objective is the aim or goal of an organization. A strategy is a possible course of action that might enable an organization or an individual to achieve its objective.Planning:· Planning involved the following two factors:Establishing the objectivesSelecting appropriate strategy to achieve those objectives· The link between structure and strategy ( understanding)1). Structure follows strategy: organizations develop strategies in order to cope with the changes in structure of an organization2) Strategy follows structure: the strategy of an organization is determined or influenced by the structure of the organization.· Planning can be either short-term (tactical planning) or long-term(strategic-planning)Planning hierarchyAt a strategic level, senior managers formulate long-term objectives and plans, and seek proper strategy to achieve these long-term goals.At a tactical level, senior managers make short-term plans for the efficient and effective use of an organization’s resources.e.g. annual plans or budgetsAt an operational level, managers take day-to-day decisions about what to do next and who to deal with problems arise.1.3 Responsibility accountingResponsibility accounting is a system of accounting that segregates revenue and costs into areas of personal responsibility in order to monitor and assess the performance of each part of an organization.The main responsibility centers are:Cost center – the performance of a cost center manager is judged on the extent to which cost targets have been achieved.Revenue center – Within an organization, this is a centre or activity that earns sales revenue. And whose manager is responsible for the revenue earned but not for the costs incurred.Profit center – A part of the business whose manager is responsible and accountable for both costs and revenue. The performance of a profit center manager is measured in terms of the profit made by the centre.Investment center – A profit center with additional responsibilities for investment and possibly also for financing, and whose performance is measured by its return on capital employed (ROCE).1.4 Summary of management accounting and financial accounting更多ACCA资讯请关注高顿ACCA官网:。

(新整理完整版)2017公司法(精编课件)

26

精品课件,下载后可直接使用excellent

4、公司与股东人格混同 (1)财产混同 (2)业务混同 (3)组织机构混同

27

精品课件,下载后可直接使用excellent

三、我国立法和实践 第二十条 公司股东应当遵守法律、行政法规和公

司章程,依法行使股东权利,不得滥用股东权利 损害公司或者其他股东的利益;不得滥用公司法 人独立地位和股东有限责任损害公司债权人的利 益。

案例

甲、乙、丙、丁、戊5人,准备成立“达有纺织有 限公司”,生产纺织品,销往国内外,其资本总 额为50万元,由甲、乙、丙、丁、戊分别认购2万、 8万、11万、13万、16万等,并成立筹备处,向A 租赁房屋一间,每月房租人民币1万元,作为办公 之用。嗣后,发起人甲因车祸死亡,致使该“达 有纺织有限公司”的筹备工作停顿。 [问题] 筹备处的开销费用1万元及欠A的房租1万元,应 由何人负担?为什么?

C、发起人的责任:要对公司设立行为承担任:

1、公司不成立时:

(1)对设立发生的债务、费用负连带责任。

(2)在募集设立中,对认缴人已收缴的股款负连 带的返还责任。

2、公司成立时:

(1)对未缴足股款及认购人逾期未缴股款负连带 的资本充实责任。

(2)因发起人过失造成公司损失的负连带损害赔 偿责任。

13

精品课件,下载后可直接使用excellent

2

二、特点 1、社团性 也即要求有二个以上的成员组成。 2、营利性 3、法人性 4、 依公司法的规定设立 三、公司法性质和特点 公司法是规范公司的组织与活动的法。

精品课件,下载后可直接使用exce组织法

② 公司法是行为法

3

③ 公司法属于私法、属于商法

(二) 公司法的特点 ① 强制规定多,使公司法具有公法性质。

2024版《公司法》精品PPT课件[1]

![2024版《公司法》精品PPT课件[1]](https://img.taocdn.com/s3/m/a02ea064e3bd960590c69ec3d5bbfd0a7856d55d.png)

2024/1/30

1

目录

• 公司法概述 • 公司的设立与组织机构 • 公司的资本与股份 • 公司的合并、分立与解散 • 公司的财务与会计制度 • 公司的法律责任与纠纷解决

2024/1/30

2

01

公司法概述

2024/1/30

3

公司法的定义与性质

公司法的定义

公司法是规定公司设立、组织、活动、解散以及其他对内对外关系的法律规范 的总称。

股份的转让

包括协议转让和集中竞价转让两种方式。协议转让需要双方达成协 议并办理过户手续,集中竞价转让则需要通过证券交易所进行。

股份转让的限制

如发起人、董事、监事、高级管理人员的股份转让限制,以及公司章 程可能对股份转让做出的其他限制。

2024/1/30

13

公司债券的发行与交易

2024/1/30

公司债券的发行 公司债券是公司依照法定程序发行的、约定在一定期限还 本付息的有价证券。公司债券的发行需要符合公司法、证 券法等法律法规的规定。

2024/1/30

22

06

公司的法律责任与纠 纷解决

2024/1/30

23

公司的法律责任概述

公司法律责任的种类

包括民事责任、行政责任和刑事责任。

行政责任

因违反行政法规而需承担的责任,如罚款、 吊销营业执照等。

2024/1/30

民事责任

主要涉及合同违约、侵权行为等,公司需承 担赔偿损失、恢复原状等责任。

2024/1/30

16

公司的解散与清算

2024/1/30

解散原因

包括公司章程规定的营业期限届满、股东会或股东大会决议解散、因 公司合并或分立需要解散等。

ACCAF4公司法与商法知识点讲解(4)

ACCA F4《公司法与商法》知识点讲解(4)1 Human Rights ACT 19981.1 The Human Rights Act imposes a duty in "public authorities" to comply with the European Convention on Human Rights, and allows us to take action in the UK courts for violations of Convention rights.1.2 Prior to the Act conventions rights could only be enforced in the European Court of Human Rights in Strasbourg which could be time consuming, expensive and daunting.1.3 Now that the convention is part of UK law (HRA98) those rights can now be enforced in UK courts.2 The rights (articles)2.1 The main rights are:2.1.1 the right to life (A.2)2.1.2 prohibition of torture (A.3)2.1.3 no slavery or forced labour (A.4)2.1.4 right to liberty and security (A.5)2.1.5 right to a fair trial (A.6)2.1.6 no punishment without law (A.7) (generally therefore criminal offences should not be retrospective)2.1.7 right to respect for privacy, family life (A.8)2.1.8 freedom of thought, conscience and religion (A.9)2.1.9 freedom of expression, assembly and association (A.10/A.11)right to marry (A.12)no discrimination in rights (A.14)right to free elections.(Note that the Articles are set out in full in your Study Text).3 Impact on interpretation of statutes3.1 As a 'public authority' the courts are required to construe legislation so that – as far as possible – it is compatible with the rights contained within the convention and apply existing common law in a manner that is compatible with convention rights. S2 of the Act requires future courts to take account of previous decisions of the ECHR.If reconciliation with an Act of Parliament is not possible the existing legislation prevails although that may trigger a fast track procedure in the Act requiring Parliament to change existing laws. In such circumstances the court issues a declaration of incompatibility, it is then for the legislature to remedy the situation through new legislation. If the fast track procedure is used this gives ministers the power to alter incompatible parts of any primary legislation by way of statutory instrument.If a court cannot reconcile 'delegated' legislation with the convention it can decide that the legislation does not apply.It may no longer be appropriate for the courts to follow some precedents on the interpretation of statutes which pre date the Act. These may now be reviewed in light of the Act.4 Impact on new legislation4.1 Before the Second Reading of the Bill the Minister responsible must make a statement either that the legislation is compatible with Convention rights, or such a statement cannot be made but the government still wants to proceed. Not all of the Articles can be derogated from. Articles 2,3,4,7 and 14 are absolute rights and cannot be interfered with. In exercising the right of derogation however the member state must be both convinced of the need for derogation and that the response is proportionate to any perceived problem.5 Impact on public authorities5.1 Public authorities are Courts and tribunals and any other person whose functions are of a public nature eg Registrar of Companies and government departments such as the DTI.5.2 It is unlawful for public authorities to act in a way which is incompatible with a convention right. A person who considers he has beena victim of an unlawful act by that authority may bring proceedings within12 months of the act occurring.5.3 The court has power to do as it thinks fit.6 European Court of Human Rights (ECHR)6.1 The final source of appeal (after the House of Lords) on human rights issues is the European Court of Human Rights. There is no appeal from the European Court of Human Rights to the European Court of Justice. Decisions of the ECHR must be taken into account when deciding interpretation.NB. Note that new cases on the HRA98 are being decided all the time. The examiner plans to write an article to consider these cases. Keep checking your student accountant for developments.7 Examinability of HRA 98This is an area that the examiner has expressed to be important so be aware of developments that may be referred to in the press.Make sure that you have an appreciation of how HRA 98 may impact on other syllabus areas. For example:。

2015ACCA《F4公司法与商法》辅导讲义(2)

2015ACCA《F4公司法与商法》辅导讲义(2)本文由高顿ACCA整理发布,转载请注明出处1 Sources of law(a) Common law(b) Equity(c) Statute (legislation) including delegated legislation(d) European Union Law2 Common law and equity2.1 This is a system of law based upon decided cases. Legal rules (initially created by judges when hearing cases) are followed by judges in subsequent like cases.It developed after the Norman Conquest.2.2 Initially only common law rules were derived from cases. The aim of common law was certainty. However various problems within the common law system resulted in the development of another kind of case law called equity. Equity sought to address some of the problems contained in the common law system. Its aim is fairness.2.3 Amongst the common law problems were inadequate remedies, a failure to recognise trusts and a reluctance to allow new causes of action to develop.2.4 At first common law and equity operated as two distinct systems of law with their own independent court and judges. Given that equity is based on fairness however it was eventually decided that in the event of conflict between the two systems equity should prevail.2.5 The two systems have now been merged together. In practice therefore, if you seek a remedy in the courts today, the court will look first to the common law. If the common law can deal with your problem adequately there will be no recourse to equity. If the common law is unable to deal adequately with the problem the court will look to equity.2.6 Equity is therefore referred to as to a supplement to the common law.2.7 The operation of equity is entirely discretionary whereas common law applies automatically.2.8 Maxims:'He who comes to equity must come with clean hands.''Equity does not suffer a wrong to be without a remedy.'更多ACCA资讯请关注高顿ACCA官网:。

ACCAF4公司法与商法知识点讲解(4)

ACCA F4《公司法与商法》知识点讲解(4)1 Human Rights ACT 1998The Human Rights Act imposes a duty in "public authorities" to comply with the European Convention on Human Rights, and allows us to take action in the UK courts for violations of Convention rights.Prior to the Act conventions rights could only be enforced in the European Court of Human Rights in Strasbourg which could be time consuming, expensive and daunting.Now that the convention is part of UK law (HRA98) those rights can now be enforced in UK courts.2 The rights (articles)The main rights are:the right to lifeprohibition of tortureno slavery or forced labourright to liberty and securityright to a fair trialno punishment without law (generally therefore criminal offences should not be retrospective)right to respect for privacy, family lifefreedom of thought, conscience and religionfreedom of expression, assembly and associationright to marryno discrimination in rightsright to free elections.(Note that the Articles are set out in full in your Study Text).3 Impact on interpretation of statutesAs a 'public authority' the courts are required to construe legislation so that – as far as possible – it is compatible with the rights contained within the convention and apply existing common law in a manner that is compatible with convention rights. S2 of the Act requires future courts to take account of previous decisions of the ECHR.If reconciliation with an Act of Parliament is not possible the existing legislation prevails although that may trigger a fast track procedure in the Act requiring Parliament to change existing laws. In such circumstances the court issues a declaration of incompatibility, it is then for the legislature to remedy the situation through new legislation. If the fast track procedure is used this gives ministers the power to alter incompatible parts of any primary legislation by way of statutory instrument.If a court cannot reconcile 'delegated' legislation with the convention it can decide that the legislation does not apply.It may no longer be appropriate for the courts to follow some precedents on the interpretation of statutes which pre date the Act. These may now be reviewed in light of the Act.4 Impact on new legislationBefore the Second Reading of the Bill the Minister responsible must make a statement either that the legislation is compatible with Convention rights, or such a statement cannot be made but the government still wants to proceed. Not all of the Articles can be derogated from. Articles 2,3,4,7 and 14 are absolute rights and cannot be interfered with. In exercising the right of derogation however the member state must be both convinced of the need for derogation and that the response is proportionate to any perceived problem.5 Impact on public authoritiesPublic authorities are Courts and tribunals and any other person whose functions are of a public nature eg Registrar of Companies and government departments such as the DTI.It is unlawful for public authorities to act in a way which is incompatible with a convention right. A person who considers he has beena victim of an unlawful act by that authority may bring proceedings within12 months of the act occurring.The court has power to do as it thinks fit.6 European Court of Human Rights (ECHR)The final source of appeal (after the House of Lords) on human rights issues is the European Court of Human Rights. There is no appeal from the European Court of Human Rights to the European Court of Justice. Decisions of the ECHR must be taken into account when deciding interpretation.NB. Note that new cases on the HRA98 are being decided all the time. The examiner plans to write an article to consider these cases. Keep checking your student accountant for developments.7 Examinability of HRA 98This is an area that the examiner has expressed to be important so be aware of developments that may be referred to in the press.Make sure that you have an appreciation of how HRA 98 may impact on other syllabus areas. For example:。

2024版《公司法培训讲义》ppt课件

05

04

选择管理者权

通过股东会选举或更换董事、监事, 决定有关董事、监事的报酬事项。

股东义务履行

出资义务

遵守公司章程

按期足额缴纳公司章程中规定的各自所认缴 的出资额。

公司章程是公司内部的“宪法”,股东必须 一体遵行。

不得滥用股东权利

不得抽逃出资

不得滥用股东权利损害公司或者其他股东的 利益,不得滥用公司法人独立地位和股东有 限责任损害公司债权人的利益。

吸收合并

一个公司吸收其他公司为吸收合并,被吸收的公司解散。

新设合并

两个以上公司合并设立一个新的公司为新设合并,合并各方解 散。

企业重组方式选择

派生分立

公司将一部分资产分出去另设一个或 若干个新的公司,原公司存续。

新设分立

公司将全部资产分别划归二个或二个以 上的新公司,原公司解散。

企业重组方式选择

公司治理将更加透明和规范

未来公司治理将更加注重透明度和规范性,强化信息披露制度,完善内部控制体系,提 高公司治理水平。

资本市场将更加成熟和多元化

随着资本市场的不断发展和完善,未来公司将拥有更多元化的融资渠道和投资方式,同 时资本市场监管将更加严格和规范。

THANKS

感谢观看

公司章程制定与修改

公司章程内容

包括公司名称、住所、经 营范围、注册资本、股东 权利和义务、组织机构设 置及职权等方面的规定。

公司章程制定程序

由发起人制定,经股东会 或股东大会审议通过,并 报公司登记机关备案。

公司章程修改程序

由董事会提出修改建议, 经股东会或股东大会审议 通过,并报公司登记机关 备案。

针和投资计划等重大事项。

董事会

公司的决策机构,由股东会选举 产生,负责公司的日常经营管理 和决策。

ACCA F4《公司法与商法》知识点讲解(4)

ACCA F4《公司法与商法》知识点讲解(4)1 Human Rights ACT 19981.1 The Human Rights Act imposes a duty in "public authorities" to comply with the European Convention on Human Rights, and allows us to take action in the UK courts for violations of Convention rights.1.2 Prior to the Act conventions rights could only be enforced in the European Court of Human Rights in Strasbourg which could be time consuming, expensive and daunting.1.3 Now that the convention is part of UK law (HRA98) those rights can now be enforced in UK courts.2 The rights (articles)2.1 The main rights are:2.1.1 the right to life (A.2)2.1.2 prohibition of torture (A.3)2.1.3 no slavery or forced labour (A.4)2.1.4 right to liberty and security (A.5)2.1.5 right to a fair trial (A.6)2.1.6 no punishment without law (A.7) (generally therefore criminal offences should not be retrospective)2.1.7 right to respect for privacy, family life (A.8)2.1.8 freedom of thought, conscience and religion (A.9)2.1.9 freedom of expression, assembly and association (A.10/A.11)2.1.10 right to marry (A.12)2.1.11 no discrimination in rights (A.14)2.1.14 right to free elections.(Note that the Articles are set out in full in your Study Text).3 Impact on interpretation of statutes3.1 As a 'public authority' the courts are required to construe legislation so that – as far as possible – it is compatible with the rights contained within the convention and apply existing common law in a manner that is compatible with convention rights. S2 of the Act requires future courts to take account of previous decisions of the ECHR.If reconciliation with an Act of Parliament is not possible the existing legislation prevails although that may trigger a fast track procedure in the Act requiring Parliament to change existing laws. In such circumstances the court issues a declaration of incompatibility, it is then for the legislature to remedy the situation through new legislation. If the fast track procedure is used this gives ministers the power to alter incompatible parts of any primary legislation by way of statutory instrument.If a court cannot reconcile 'delegated' legislation with the convention it can decide that the legislation does not apply.It may no longer be appropriate for the courts to follow some precedents on the interpretation of statutes which pre date the Act. These may now be reviewed in light of the Act.4 Impact on new legislation4.1 Before the Second Reading of the Bill the Minister responsible must make a statement either that the legislation is compatible with Convention rights, or such a statement cannot be made but the government still wants to proceed. Not all of the Articles can be derogated from. Articles 2,3,4,7 and 14 are absolute rights and cannot be interfered with. In exercising the right of derogation however the member state must be both convinced of the need for derogation and that the response is proportionate to any perceived problem.5 Impact on public authorities5.1 Public authorities are Courts and tribunals and any other person whose functions are of a public nature eg Registrar of Companies and government departments such as the DTI.5.2 It is unlawful for public authorities to act in a way which is incompatible with a convention right. A person who considers he has beena victim of an unlawful act by that authority may bring proceedings within12 months of the act occurring.5.3 The court has power to do as it thinks fit.6 European Court of Human Rights (ECHR)6.1 The final source of appeal (after the House of Lords) on human rights issues is the European Court of Human Rights. There is no appeal from the European Court of Human Rights to the European Court of Justice. Decisions of the ECHR must be taken into account when deciding interpretation.NB. Note that new cases on the HRA98 are being decided all the time. The examiner plans to write an article to consider these cases. Keep checking your student accountant for developments.7 Examinability of HRA 98This is an area that the examiner has expressed to be important so be aware of developments that may be referred to in the press.Make sure that you have an appreciation of how HRA 98 may impact on other syllabus areas. For example:。

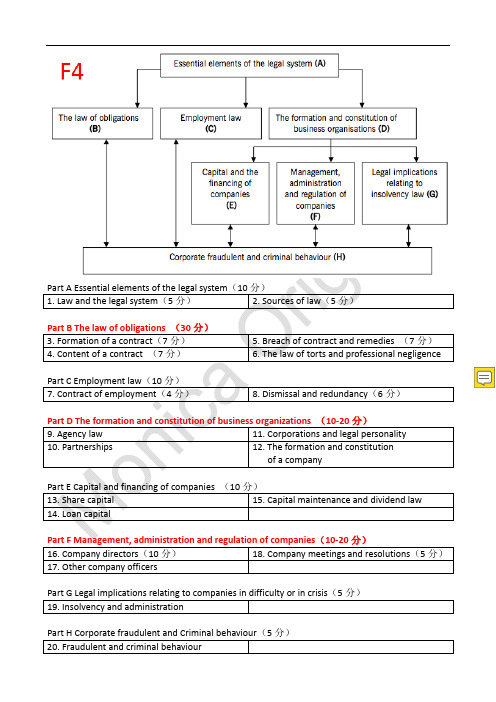

ACCAF4公司法和商法考试大纲

ACCAF4公司法和商法考试大纲 ACCA All rights reserved.1Corporate and BusinessLaw (ENG)(F4)September 2014 toAugust 2015(PAPER EXAM SESSIONS IN DEC 2014 AND JUN2015. START DATE FOR CBE NOVEMBER 192014.)This syllabus and study guide is designed to helpwith planning study and to provide detailedinformation on what could be assessed inany examination session.THE STRUCTURE OF THE SYLLABUS ANDSTUDY GUIDERelational diagram of paper with other papersThis diagram shows direct and indirect linksbetween this paper and other papers preceding orfollowing it. Some papers are directly underpinned by other papers such as Advanced Performance Management by Performance Management. These links are shown as solid line arrows. Other papers only have indirect relationships with each other such as links existing between the accounting and auditing papers. The links between these are shown as dotted line arrows. This diagram indicates where you are expected to have underpinning knowledge and where it would be useful to review previous learning before undertaking study.Overall aim of the syllabusThis explains briefly the overall objective of the paper and indicates in the broadest sense the capabilities to be developed within the paper.Main capabilitiesThis paper’s aim is broken down into several main capabilities which divide the syllabus and study guide into discrete sections.Relational diagram of the main capabilitiesThis diagram illustrates the flows and links between the main capabilities (sections)of the syllabus and should be used as an aid to planning teaching and learning in a structured way.Syllabus rationaleThis is a narrative explaining how the syllabus is structured and how the main capabilities are linked. The rationale also explains in further detail what the examination intends to assess and why.Detailed syllabusThis shows the breakdown of the main capabilities (sections)of the syllabus into subject areas. This is the blueprint for the detailed study guide.Approach to examining the syllabusThis section briefly explains the structure of the examination and how it is assessed.Study GuideThis is the main document that students, learningand content providers should use as the basis of their studies, instruction and materials. Examinations will be based on the detail of the study guide which comprehensively identifies what could be assessed in any examination session.The study guide is a precise reflection and breakdown of the syllabus. It is divided into sections based on the main capabilities identified in the syllabus. These sections are divided into subject areas which relate to the sub-capabilities includedin the detailed syllabus. Subject areas are broken down into sub-headings which describe the detailed outcomes that could be assessed in examinations. These outcomes are described using verbs indicating what exams may require students to demonstrate, and the broad intellectual level at which these may need to be demonstrated(*see intellectual levels below)。

商法学1讲——商法总论之1(商法概述)

商法学讲座第1讲《商法总论》之商法概述赵万一西南政法大学民商法学院教授商法是调整市场经济关系中商人及其营利性活动的法律规范的总称。

商法发生作用的领域是市场经济关系商人营利性活动(商行为)商法的调整内容是商,主要包括两方面内容:商法的内容和分类广义的商法狭义的商法国际商法国内商法商事公法商事私法商法商法产生于市场经济并服务于市场经济商法的主要作用在于促进市场经济的发展商法的发达程度和市场经济的发展水平呈正向关系(一)商法是以市场经济作为直接为作用对象①商法最鲜明地体现了社会经济发展的时代要求②体系的开放性和制度的开放性保证了商法对社会关系的容纳性主体:从简单到复杂个人独资、合伙、公司——行为:从单一到复合买卖、代理、保管、运输——营业让与、并购、证券交易、电子商务(二)商法是最具先进性、开放性和包容性的法律体系(三)商法是具有较强国际性的法律制度设计法国商法典◼1803年公布,1807年议会通过,1808年施行◼立法标准:客观主义,以商行为为其立法基础◼内容:商法总则、海商、破产、商事法院◼意义:首次打破了中世纪商人法只适用于商人阶层的特权,使商法具有普适性。

民商分立体制◼1897年公布,1900年生效。

◼立法标准:主观主义,以商人作为立法基础。

◼主要内容:德国商法典商人商行为公司及隐名合伙海商◼瑞士:1872年颁布《债务法》,其内容包括:总则、合同分则、公司、有价证券及商号、商业合伙、商业登记、商业帐簿。

民商合一1907年制定《民法典》1911年将《债务法》纳入民法典之中成为第五篇:人法、亲属法、继承法、特权法、债务法。

◼意大利:1942年《民法典》◼荷兰:1992年《民法典》我国对商事立法的基本态度◼将民事商事的一些共同原则和内容纳入到民法典之中。

◼承认商法的相对独立性坚持民商合一立法的特殊性:将一些特殊的商事制度制定单行商事法规司法的特殊性:在审判中承认商事审判的独立性谢谢观看赵万一西南政法大学民商法学院教授。

2024版《公司法》ppt课件[1]

![2024版《公司法》ppt课件[1]](https://img.taocdn.com/s3/m/06b75ecc82d049649b6648d7c1c708a1284a0aa1.png)

2024/1/30

股东平等原则

股东在享有权利和承担义务上 应当平等,不得因出资额、持

股比例等因素而有所歧视。

资本多数决原则

公司的重大决策应当按照股东 的出资比例或持股比例进行表 决,体现资本多数决的原则。

公司社会责任原则

股东可以用货币出资,也可 以用实物、知识产权、土地 使用权等可以用货币估价并 可以依法转让的非货币财产 作价出资。

公司章程是公司的宪章性文 件,对公司、股东、董事、 监事、高级管理人员具有约 束力。

公司名称是公司的标志,应 当符合国家有关规定。公司 组织机构包括股东会、董事 会、监事会和经理等。

公司住所是公司主要办事机 构所在地,经公司登记机关 登记的公司的住所只能有一 个。

公司的解散与清算

2024/1/30

解散的概念和原因

介绍公司解散的定义及可能导致解散的原因,如公司章程规定的 解散事由发生、股东会决议解散等。

清算的程序和种类

详细阐述公司清算的步骤和种类,包括普通清算、特别清算和破产 清算等。

清算的法律效果

分析公司清算后产生的法律效果,如债权债务的清偿、剩余财产的 分配等。

22

06

公司的财务与会计制度

2024/1/30

23

公司的财务会计制度

会计制度

公司必须依法建立规范的财务会计制度,确保财 务信息的真实、准确和完整。

会计要素

包括资产、负债、所有者权益、收入、费用和利 润等,是财务会计的基础。

会计核算

公司应按照会计准则进行会计核算,包括确认、 计量、记录和报告等环节。

《公司法》ppt课件

accaf4公司法和商法考试

ACCAF4公司法和商法考试大纲 ACCA All rights reserved.1Corporate and BusinessLaw (ENG)(F4)September 2014 toAugust 2015(PAPER EXAM SESSIONS IN DEC 2014 AND JUN2015. START DATE FOR CBE NOVEMBER 192014.)This syllabus and study guide is designed to helpwith planning study and to provide detailedinformation on what could be assessed inany examination session.THE STRUCTURE OF THE SYLLABUS ANDSTUDY GUIDERelational diagram of paper with other papersThis diagram shows direct and indirect linksbetween this paper and other papers preceding orfollowing it. Some papers are directly underpinned by other papers such as Advanced Performance Management by Performance Management. These links are shown as solid line arrows. Other papers only have indirect relationships with each other such as links existing between the accounting and auditing papers. The links between these are shown as dotted line arrows. This diagram indicates where you are expected to have underpinning knowledge and where it would be useful to review previous learning before undertaking study.Overall aim of the syllabusThis explains briefly the overall objective of the paper and indicates in the broadest sense the capabilities to be developed within the paper.Main capabilitiesThis paper’s aim is broken down into several main capabilities which divide the syllabus and study guide into discrete sections.Relational diagram of the main capabilitiesThis diagram illustrates the flows and links between the main capabilities (sections)of the syllabus and should be used as an aid to planning teaching and learning in a structured way.Syllabus rationaleThis is a narrative explaining how the syllabus is structured and how the main capabilities are linked. The rationale also explains in further detail what the examination intends to assess and why.Detailed syllabusThis shows the breakdown of the main capabilities (sections)of the syllabus into subject areas. This is the blueprint for the detailed study guide.Approach to examining the syllabusThis section briefly explains the structure of the examination and how it is assessed.Study GuideThis is the main document that students, learningand content providers should use as the basis of their studies, instruction and materials. Examinations will be based on the detail of the study guide which comprehensively identifies what could be assessed in any examination session.The study guide is a precise reflection and breakdown of the syllabus. It is divided into sections based on the main capabilities identified in the syllabus. These sections are divided into subject areas which relate to the sub-capabilities includedin the detailed syllabus. Subject areas are broken down into sub-headings which describe the detailed outcomes that could be assessed in examinations. These outcomes are described using verbs indicating what exams may require students to demonstrate, and the broad intellectual level at which these may need to be demonstrated(*see intellectual levels below)。

公司法第一章

有利于形成规模经济、分散投资风险、降 有利于形成规模经济、分散投资风险、 低投资成本、刺激投资者积极性。 低投资成本、刺激投资者积极性。

关于有限责任

美国1855年 月颁布的《有限责任法》要求“有限” 美国1855年8月颁布的《有限责任法》要求“有限”字 样须在公司名称中反映出来。 有限”一词作为一面红旗, 样须在公司名称中反映出来。“有限”一词作为一面红旗, 警告与此类危险性甚大的新发明打交道的公众当心自己面 临的风险。一旦高风险的经营活动成功, 临的风险。一旦高风险的经营活动成功,股东即可获得高 额股利,而公司债权人却无此获利; 额股利,而公司债权人却无此获利;一旦高风险的经营活 动失败,股东个人也不必在其出资之外掏钱偿债, 动失败,股东个人也不必在其出资之外掏钱偿债,充其量 收不回其已缴纳的股款而已,若公司因此而陷于支付不能, 收不回其已缴纳的股款而已,若公司因此而陷于支付不能, 则高风险经营活动的高额成本最终只能由公司的债权人承 担。 ――刘俊海《股份有限公司股东权的保护》 ――刘俊海 股份有限公司股东权的保护》 刘俊海《

案例分析

正大有限责任公司是光明百货商店和万利有限责任公 司的债权人。 司的债权人。 光明百货商店由甲、 丙三人合伙组成, 光明百货商店由甲、乙、丙三人合伙组成,每人出资 30万元 共有资本90万元。1997年12月初 万元, 90万元 月初, 30万元,共有资本90万元。1997年12月初,正大公司 曾向光明百货商店发运一批针织服装,价款总计30 30万 曾向光明百货商店发运一批针织服装,价款总计30万 元人民币。付款期限届满时, 元人民币。付款期限届满时,光明百货商店没有按约 付款,经正大公司多方调查, 付款,经正大公司多方调查,才知道该店由于经营不 已经拖欠了多笔大额债务。 善,已经拖欠了多笔大额债务。而合伙人甲因商店负 债累累,不告而别。 丙也不得不宣告企业解散。 债累累,不告而别。乙、丙也不得不宣告企业解散。 在清算过程中发现,百货商店已经严重资不抵债, 在清算过程中发现,百货商店已经严重资不抵债,其 尚有资产60万元,所欠债务已经达到150万元, 60万元 150万元 尚有资产60万元,所欠债务已经达到150万元,其中 包括欠正大公司的30万元货款。 30万元货款 包括欠正大公司的30万元货款。乙、丙声称他们将以 企业的全部剩余财产清偿债务, 企业的全部剩余财产清偿债务,超过部分的债务不再 清偿。正大公司因此与之发生纠纷。 清偿。正大公司因此与之发生纠纷。

[ACCA]F4公司法与商法入门

![[ACCA]F4公司法与商法入门](https://img.taocdn.com/s3/m/04fec22458fafab068dc022f.png)

[ACCA]F4公司法与商法入门F4要点解读会为大家带来合同法(Contract Law)的相关知识。

一个合同的形成,需要4个不可或缺的要素——要约(Offer)、对价(Consideration)、建立法律关系的意愿(Intention to enter into legal relations)和接受(Acceptance)。

第四期的要点解读,将为大家简单讲解第一个要素“邀约”。

一、何谓要约?要约听起来很高大上,实则于我们的日常生活中随处可见。

一个学生最期待可能就是来自某大型企业或知名学府的Offer,指的就是要约了。

要约即“当事人向对方发出的希望与对方订立合同的请求、要求”,像是一种邀请。

大多数情况下,如果对方无条件地接受邀约的内容,合同就成立了。

二、不是所有的“邀请”都是“要约”实际生活中,有很多看起来像要约的邀请,需要我们认清。

1、Supply of information只有接受要约的内容,合同才能成立。

但有一些表达,仅仅是对“合同中可能存在的条款”的描述、预测。

这一类表达仅仅是为合同成立的过程提供额外信息,并无法律上的拘束力。

听起来很抽象吧?以下这个例子会帮助大家弄明白该概念。

【Example】买家A问建材商B:“你可否卖我一些木料呢?请告诉我最低价”。

B回答:“300元/㎡”。

收到此回复后,A以此为offer,表示接受,并直接向B表示要以此价格购买B的木料,。

很长时间以后未得到进一步答复的A将B告上法庭。

【Explanation】这里的“300元/㎡”就是”Supply of information”。

这只是一个可能发生的价格,可能需要达到某些条件才能实现,如一次性大批量购买、签订长期购买的合同等等,而非B真正的邀约,自然不会形成合同,也不会有法律拘束力。

2、A statement of intention仅仅是对成立合同表达意愿,而并未提出offer的实际内容,并不是有效的offer。

ACCA F4知识要点汇总(精简版)

1. Law and the legal system(5 分)

2. Sources of law(5 分)

Part B The law of obligations (30 分) 3. Formation of a contract(7 分) 4. Content of a contract (7 分)

European Court of Human Rights (ECtHR) 欧洲人权法院

The Privy Council 枢密院

d) In the Factortamecase(欧洲移民法和商船法): 欧洲法 EU law>欧盟成员国国内法律。 所以,最高法院的有效性受到 EU law 判决的约束。

Magistrates 治安官法院、Crown court

offences

偷盗、吸毒、对他人实施暴力 皇冠法院都可以审理

上述两种皆可能

刑事诉讼操作:

Magistrates 治安官法院

a) Summary offences without a jury 轻微罪行(没有陪审团) b) Commit defendants charged with an indictable offence to the Crown

平衡可能性,谁的证据更占优 排除合理怀疑,疑罪从无

Decision 判决结果

Remedies 法律救济 Distinct courts of instance court 初审法 院

Judge 法官:Liable/Not liable 有 责任/无责任 Damages(损害赔偿金) Magistrates 治安官法院、County court 郡法院

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

ACCA《F4公司法与商法》精选讲义第一章(1)

本文由高顿ACCA整理发布,转载请注明出处

Session 1 The Nature, Source and Purpose of Management Accounting

Main contents:

1. Data and information

2. The managerial processes of planning, decision making and control

3. Responsibility accounting

4. Management accounting and financing accounting

5. Presentation of management information

1.1 Data and Information

· Data consists of raw materials, which include numbers, letters, symbols, facts, events and transactions, that have been recorded but not yet processed into a form suitable for use.

· Information is data which has been processed in such a way that it is meaningful to the person to the person who receives it. (for decision making purpose)

The attributes of good information can be identified by the “ACCURATE” as shown below:

· Accurate: accurate enough for the purpose

· Complete: all the necessary information

· Cost- effective: benefit > costs

· Understandable: clear and easy to understand

· Relevant: relevant to purpose

· Accessible: the best way to communicate with the related person

· Timely: be available at the right time

· Easy to use: by management

1.2 The Managerial Process of Planning , Decision Making and Control

Information for management is likely to be used for planning, control and decision making objectives:

An objective is the aim or goal of an organization. A strategy is a possible course of action that might enable an organization or an individual to achieve its objective.

Planning:

· Planning involved the following two factors:

Establishing the objectives

Selecting appropriate strategy to achieve those objectives

· The link between structure and strategy (understanding)

1)。

Structure follows strategy: organizations develop strategies in order to cope with the changes in structure of an organization

2)Strategy follows structure: the strategy of an organization is determined or influenced by the structure of the organization.

· Planning can be either short-term (tactical planning)or long-term

(strategic-planning)

Planning hierarchy

At a strategic level, senior managers formulate long-term objectives and plans, and seek proper strategy to achieve these long-term goals.

At a tactical level, senior managers make short-term plans for the efficient and effective use of an organization’s resources.

e.g. annual plans or budgets

At an operational level, managers take day-to-day decisions about what to do next and who to deal with problems arise.

1.3 Responsibility accounting

Responsibility accounting is a system of accounting that segregates revenue and costs into areas of personal responsibility in order to monitor and assess the performance of each part of an organization.

The main responsibility centers are:

Cost center – the performance of a cost center manager is judged on the extent to which cost targets have been achieved.

Revenue center – Within an organization, this is a centre or activity that earns sales revenue. And whose manager is responsible for the revenue earned but not for the costs incurred.

Profit center – A part of the business whose manager is responsible and accountable for both costs and revenue. The performance of a profit center manager is measured in terms of the profit made by the centre.

Investment center – A profit center with additional responsibilities for investment and possibly also for financing, and whose performance is measured by its return on capital employed (ROCE)。

1.4 Summary of management accounting and financial accounting

更多ACCA资讯请关注高顿ACCA官网:。