会计英语第三章作业

会计基础第三章课后作业(含答案)

第 6页

6、 【正确答案】 错 【答案解析】 财务费用属于费用要素,损益类科目。 【该题针对“会计科目按反映的经济内容分类”知识点进行考核】 【答疑编号 10866046】 7、 【正确答案】 错 【答案解析】 合法性原则是指企业设置会计科目时应当符合国家统一的会计制度的规定,以保证会计信息的可比性。 【该题针对“会计科目的设置原则”知识点进行考核】 【答疑编号 10865900】 8、 【正确答案】 对 【答案解析】 【该题针对“账户与会计科目的联系和区别”知识点进行考核】 【答疑编号 10876811】 9、 【正确答案】 对 【答案解析】 【该题针对“账户的概念”知识点进行考核】 【答疑编号 10876782】 10、 【正确答案】 错 【答案解析】 总分类科目对明细分类科目具有统驭和控制作用,而明细分类科目是对其所属的总分类科目的补充和说明。 【该题针对“会计科目按提供信息的详细程度及其统驭关系不同分类”知识点进行考核】 【答疑编号 10865986】

3、 【正确答案】 C

第 3页

【答案解析】 制造费用属于成本类科目;长期待摊费用属于资产类科目;应交税费属于负债类科目。销售费用属于损益类科目中 反映费用的科目。 【该题针对“会计科目按反映的经济内容分类”知识点进行考核】 【答疑编号 10866037】

4、 【正确答案】 B 【答案解析】 会计科目按其提供信息的详细程度及其统驭关系,可以分为总分类科目和明细分类科目。其中总分类科目,又称总 账科目或一级科目。 【该题针对“会计科目按提供信息的详细程度及其统驭关系不同分类 ”知识点进行考核】 【答疑编号 10865938】

会计学原理Financial-Accounting-by-Robert-Libby第八版-第三章-答案

会计学原理Financial-Accounting-by-Rob ert-Libby第八版-第三章-答案Chapter 3Operating Decisions andthe Accounting SystemANSWERS TO QUESTIONS1. A typical business operating cycle for a manufacturer would be as follows:inventory is purchased, cash is paid to suppliers, the product is manufactured and sold on credit, and the cash is collected from the customer.2. The time period assumption means that the financial condition andperformance of a business can be reported periodically, usually every month, quarter, or year, even though the life of the business is much longer.3. Net Income = Revenues + Gains - Expenses - Losses.Each element is defined as follows:Revenues -- increases in assets or settlements of liabilities from ongoing operations.Gains -- increases in assets or settlements of liabilities from peripheral transactions.Expenses -- decreases in assets or increases in liabilities from ongoingoperations.Losses -- decreases in assets or increases in liabilities from peripheraltransactions.4. Both revenues and gains are inflows of net assets. However, revenuesoccur in the normal course of operations, whereas gains occur from transactions peripheral to the central activities of the company. An example is selling land at a price above cost (at a gain) for companies not in the business of selling land.Both expenses and losses are outflows of net assets. However, expenses occur in the normal course of operations, whereas losses occur from transactions peripheral to the central activities of the company. An example is a loss suffered from fire damage.5. Accrual accounting requires recording revenues when earned andrecording expenses when incurred, regardless of the timing of cash receipts or payments. Cash basis accounting is recording revenues when cash is received and expenses when cash is paid.Financial Accounting, 8/e 3-2 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Financial Accounting, 8/e3-3© 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.6. The four criteria that must be met for revenue to be recognized under theaccrual basis of accounting are (1) delivery has occurred or services have been rendered, (2) there is persuasive evidence of an arrangement for customer payment, (3) the price is fixed or determinable, and (4) collection is reasonably assured.7. The expense matching principle requires that expenses be recorded whenincurred in earning revenue. For example, the cost of inventory sold during a period is recorded in the same period as the sale, not when the goods are produced and held for sale.8. Net income equals revenues minus expenses. Thus revenues increase netincome and expenses decrease net income. Because net income increases stockholders’ equity, revenues increase stockholders’ equity and expenses decrease it.9. Reve nues increase stockholders’ equity and expenses decreasestockholders’ equity. To increase stockholders’ equity, an account must be credited; to decrease stockholders’ equity, an account must be debited. Thus revenues are recorded as credits and expenses as debits. 10.11.12.13. Total net profit margin ratio is calculated as Net Income Net Sales (orOperating Revenues). The net profit margin ratio measures how much of every sales dollar is profit. An increasing ratio suggests that the company is managing its sales and expenses effectively.ANSWERS TO MULTIPLE CHOICE1. c2. a3. b4. b5. c6. c7. d8. b9. a10. bFinancial Accounting, 8/e 3-4 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Authors' Recommended Solution Time(Time in minutes)* Due to the nature of this project, it is very difficult to estimate the amount of time students will need to complete the assignment. As with any open-ended project, it is possible for students to devote a large amount of time to these assignments. While students often benefit from the extra effort, we find that some become frustrated by the perceived difficulty of the task. You can reduce student frustration and anxiety by making your expectations clear. For example, when our goal is to sharpen research skills, we devote class time discussing research strategies. When we want the students to focus on a real accounting issue, we offer suggestions about possible companies or industries.Financial Accounting, 8/e 3-5 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Financial Accounting, 8/e 3-6© 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.MINI-EXERCISESM3–1.TERMG (1) LossesC (2) Expense matching principle F (3) RevenuesE (4) Time period assumption B(5) Operating cycleM3–2.Cash Basis Income StatementAccrual Basis Income StatementRevenues: Cash sales Customer deposits$8,000 5,000 Revenues: Sales to customers$18,000 Expenses:Inventory purchases Wages paid 1,000 900 Expenses: Cost of sales Wages expense Utilities expense 9,000 900 300Net Income$11,100Net Income $7,800Revenue Account Affected Amount of Revenue Earned in JulyM3–4.Expense Account Affected Amount of Expense Incurred in JulyFinancial Accounting, 8/e 3-7 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.a. Cash (+A) ............................................................................ 15,000Games Revenue (+R, +SE) .......................................... 15,000 b. Cash (+A) ............................................................................ 3,000Accounts Receivable (+A) ................................................ 5,000 Sales Revenue (+R, +SE) ............................................. 8,000 c. Cash (+A) ............................................................................ 4,000Accounts Receivable (-A) ........................................... 4,000 d. Cash (+A) ............................................................................ 2,500Unearned Revenue (+L) ............................................... 2,500 M3–6.e. Cost of Goods Sold (+E, -SE)........................................... 6,800Inventory (-A) ............................................................... 6,800 f. Accounts Payable (–L) (800)Cash (-A) (800)g. Wages Expense (+E, -SE) ................................................. 3,500Cash (-A) ...................................................................... 3,500 h. Insurance Expense (+E, -SE) . (500)Prepaid Expenses (+A) ...................................................... 1,00 Cash (-A) ...................................................................... 1,500 i. Repairs Expense (+E, -SE) .. (700)Cash (-A) (700)j. Utilities Expense (+E, -SE) (900)Accounts Payable (+L) (900)Financial Accounting, 8/e 3-8 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Transaction (c) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.M3–8.Transaction (h) results in an increase in an asset (prepaid expenses) and a decrease in an asset (cash). Therefore, the net effect on assets is 500.Financial Accounting, 8/e 3-9 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Craig’s Bowling, Inc.Income StatementFor the Month of July 2014Revenues:Games revenue $15,000Sales revenue 8,000Total revenues 23,000Expenses:Cost of goods sold 6,800Utilities expense 900Wages expense 3,500Insurance expense 500Repairs expense 700Total expenses 12,400Net income $ 10,600M3–10.Financial Accounting, 8/e 3-10 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.M3–11.These results suggest that Jen’s Jewelry Company earned approximately $0.31 for every dollar of revenue in 2015, and over time, the ratio has improved. Jen’s has become more effective at managing sales and expenses.As additional analysis:Between 2013 to 2014 and 2014 to 2015, sales have increased at a lower percentage than net income. This suggests that the company has been more effective at controlling expenses than generating revenues.EXERCISESE3–1.TERMK (1) ExpensesE (2) GainsG (3) Revenue realization principleI (4) Cash basis accountingM (5) Unearned revenueC (6) Operating cycleD (7) Accrual basis accountingF (8) Prepaid expensesJ (9) Revenues - Expenses = Net IncomeL (10) Ending Retained Earnings =Beginning Retained Earnings + Net Income - Dividends DeclaredE3–2.Req. 1Cash Basis Income StatementAccrual Basis Income StatementRevenues:Cash sales Customer deposits $500,00070,000Revenues:Sales tocustomers$750,000Expenses:Inventory purchases Wages paidUtilities paid90,000180,30017,200Expenses:Cost of salesWages expenseUtilities expense485,000184,00019,130Net Income $282,500 Net Income $61,870Req. 2Accrual basis financial statements provide more useful information to external users. Financial statements created under cash basis accounting normally postpone (e.g., $250,000 credit sales) or accelerate (e.g., $70,000 customer deposits) recognition of revenues and expenses long before or after goods andservices are produced and delivered (until cash is received or paid). They also do not necessarily reflect all assets or liabilities of a company on a particular date.Activity Revenue AccountAmount of RevenueActivity Expense AccountAmount of ExpenseE3–5.Transaction (k) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.* A loss affects net income negatively, as do expenses.E3–6.Transaction (f) results in an increase in an asset (property, plant, and equipment) and a decrease in an asset (cash). Therefore, there is no net effect on assets.E3–7.(in thousands)a. Plant and equipment (+A) (636)Cash ( A) (636)Debits equal credits. Assets increase and decrease by the same amount.b. Cash (+A) (181)Short-term notes payable (+L) (181)Debits equal credits. Assets and liabilities increase by the same amount.c. Cash (+A) ..........................................................................Accounts receivable (+A) ................................................ 10,765 28,558Service revenue (+R, +SE) ........................................ 39,323 Debits equal credits. Revenue increases retained earnings (part of stockholders' equity). Stockholders' equity and assets increase by the same amount.E3–7. (continued)d. Accounts payable (-L) ..................................................... 32,074Cash (-A) ................................................................... 32,074 Debits equal credits. Assets and liabilities decrease by the same amount.e. Inventory (+A) ................................................................... 32,305Accounts payable (+L) .............................................. 32,305 Debits equal credits. Assets and liabilities increase by the same amount.f. Wages expense (+E, -SE) ............................................... 3,500Cash (-A) ................................................................... 3,500 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.g. Cash (+A) .......................................................................... 39,043Accounts receivable (-A) ....................................... 39,043 Debits equal credits. Assets increase and decrease by the same amount.h. Fuel expense (+E, -SE) (750)Cash (-A) (750)Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.i. Retained earnings (-SE) (597)Cash (-A) (597)Debits equal credits. Assets and stock holders’ equity decrease by thesame amount.j. Utilities expense (+E, -SE) (68)Cash (-A) ................................................................... Accounts payable (+L) .............................................. 55 13Debits equal credits. Expenses decrease retained earnings (part of stockholders' equity). Together, stockholders' equity and liabilities decrease by the same amount as assets.E3–8.Req. 1a.Cash (+A) ................................................................... 2,300,000Short-term note payable (+L) ........................ 2,300,000 Debits equal credits. Assets and liabilities increase by the same amount.b.Equipment (+A) ......................................................... 98,000Cash (-A) ........................................................ 98,000 Debits equal credits. Assets increase and decrease by the same amount.c.Merchandise inventory (+A) .................................... 35,000Accounts payable (+L) .................................. 35,000 Debits equal credits. Assets and liabilities increase by the same amount.d.Repairs (or maintenance) expense (+E, -SE) ......... 62,000Cash (-A) ........................................................ 62,000 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.e.Cash (+A) ................................................................... 390,000Unearned pass revenue (+L) ......................... 390,000 Debits equal credits. Since the season passes are sold before Vail Resorts provides service, revenue is deferred until it is earned. Assets andliabilities increase by the same amount.f.Two transactions occur:(1) Accounts receivable (+A) (800)Ski shop sales revenue (+R, +SE) (800)Debits equal credits. Revenue increases retained earnings (a part ofstockholders' equity). Stockholders' equity and assets increase by thesame amount.(2) Cost of goods sold (+E, -SE) (500)Merchandise inventory (-A) (500)Debits equal credits. Expenses decrease retained earnings (a part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.E3–8. (continued)g.Cash (+A) ................................................................... 320,000Lift revenue (+R, +SE) .................................... 320,000 Debits equal credits. Revenue increases retained earnings (a part ofstockholders' equity). Stockholders' equity and assets increase by thesame amount.h.Cash (+A) ................................................................... 3,500Unearned rent revenue (+L) .......................... 3,500 Debits equal credits. Since the rent is received before the townhouse isused, revenue is deferred until it is earned. Assets and liabilities increase by the same amount.i. Accounts payable (-L) ............................................. 17,500Cash (-A) ........................................................ 17,500 Debits equal credits. Assets and liabilities decrease by the same amount. j.Cash (+A) . (400)Accounts receivable (-A) (400)Debits equal credits. Assets increase and decrease by the same amount. k.Wages expense (+E, -SE) ........................................ 245,000Cash (-A) ........................................................ 245,000 Debits equal credits. Expenses decrease retained earnings (a part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.Req. 22/1 Rent expense (+E, -SE) (275)Cash (-A) (275)2/2 Fuel expense (+E, -SE) (490)Accounts payable (+L) (490)2/4 Cash (+A) (820)Unearned revenue (+L) (820)2/7 Cash (+A) (910)Transport revenue (+R, +SE) (910)2/10 Advertising expense (+E, -SE) (175)Cash (-A) (175)2/14 Wages payable (-L) ......................................................... 2,300Cash (-A) ......................................................... 2,3002/18 Cash (+A) ..........................................................................Accounts receivable (+A) ................................................ 1,600 2,200Transport revenue (+R, +SE) ......................... 3,800 2/25 Parts supplies (+A) .......................................................... 2,550Accounts payable (+L) ................................... 2,550 2/27 Retained earnings (-SE) .. (200)Dividends payable (+L) (200)Req. 1 and 2Accounts Unearned Fee NoteAdditional Paid-inRebuilding Fees RentItem (f) is not a transaction; there has been no exchange.E3–10. (continued)Req. 3Net income using the accrual basis of accounting:Revenues $19,850 ($19,000 + $850)– Expenses 16,900 ($16,500 + $400)Net Income $ 2,950Assets = Liabilities + Stockholders’ Equity$12,090 $ 7,700 $ 1,70024,800 4,440 7,8202,460 48,500 9,36010,420 2,950 netincome7,40025,300$82,470 $60,640 $21,830Req. 4Net income using the cash basis of accounting:Cash receipts $27,650 (transactions a through d)–Cash disbursements 19,760 (transactions g, i, and k)Net Income $ 7,890Cash basis net income ($7,890) is higher than accrual basis net income ($2,950) because of the differences in the timing of recording revenues versus receipts and expenses versus disbursements between the two methods. The $7,800 higher amount in cash receipts over revenues includes cash received prior to being earned (from (b), $600) and cash received after being earned (in (d), $7,200). The $2,860 higher amount in cash disbursements over expenses includes cash paid after being incurred in the prior period (in (g), $2,300), plus cash paid for supplies to be used and expensed in the future (in (k), $960), less an expense incurred in January to be paid in February (in (e), $400).STACEY’S PIANO REBUILDING COMPANYIncome Statement (unadjusted)For the Month Ended January 31, 2014 Operating Revenues:Rebuilding fees revenue $ 19,000 Total operating revenues 19,000 Operating Expenses:Wages expense 16,500 Utilities expense 400 Total operating expenses 16,900 Operating Income 2,100 Other Item:Rent revenue 850 Net Income $ 2,950Req. 1 and 2Common Additional RetainedFood Sales Revenue Catering Sales RevenueE3–14.Req. 1TRAVELING GOURMET, INC.Income Statement (unadjusted)For the Month Ended March 31, 2014 Revenues:Food sales revenueCatering sales revenueTotal revenues Expenses:Supplies expenseUtilities expenseWages expenseFuel expenseTotal costs and expenses $ 11,9004,20016,10010,8304206,28036317,893Net Loss $ (1,793) Req. 2Transaction O, I, or F Activity (or No Effect) on Statement ofDirection and AmountReq. 3The company generated a small loss of 1,793 during its first month of operations, before making any adjusting entries. The adjusting entries for use of the building and equipment and interest expense on the borrowing will increase the loss. Cash flows from operating activities were also negative at $2,973 (= + 11,900 + 2,600 –10,830 –363 –6,280) . So far the company does not appear to be successful, but it is only in its first month of operating a retail store. If sales can be increased without inflating fixed costs (particularly salaries expense), the company may soon turn a profit. It is not unusual for small businesses to report a loss or have negative cash flows from operations as they start up operations.E3–15.Req. 1Transaction Brief Explanationa Issued 10,000 shares of common stock to shareholders for $82,000cash.b Purchased store fixtures for $15,400 cash.c Purchased $24,800 of inventory, paying $6,200 cash and thebalance on account.d Sold $14,000 of goods or services to customers, receiving $9,820cash and the balance on account. The cost of the goods sold was$7,000.e Used $1,480 of utilities during the month, not yet paid.f Paid $1,300 in wages to employees.g Paid $2,480 in cash for rent, $620 related to the current month and$1,860 related to future months.h Received $3,960 cash from customers, $1,450 related to currentsales and $2,510 related to goods or services to be provided in thefuture.Req. 2Kate’s Kite CompanyIncome StatementFor the Month Ended April 30, 2014Sales Revenue Expenses:Cost of salesWages expenseRent expenseUtilities expenseTotal expenses $ 15,4507,0001,3006201,48010,400Net Income $ 5,050Kate’s Kite CompanyBalance SheetAt April 30, 2014Assets Liabilities and Shareholders’ Equity Current Assets: Current Liabilities:Cash $70,400 Accounts payable $20,080 Accounts receivable 4,180 Unearned revenue 2,510 Inventory 17,800 Total current liabilities 22,590 Prepaid expenses 1,860 Shareholders’ Equity:Total current assets 94,240 Common stock 10,000 Store fixtures 15,400 Additional paid-in capital 72,000Retained earnings 5,050Total shareholders’equity87,050Total Assets $109,640 Total Liabilities &Shareholders’ Equity$109,640E3–16.Req. 1Assets = Liabilities + Stockholders’ Equity $ 3,200 $ 2,400 $ 800 8,000 5,600 4,0006,400 1,600 3,200 $17,600 $9,600 $ 8,000Req. 2Accounts Long-TermAccounts Unearned Long-TermAdditionalConsulting Fee InvestmentRent ExpenseE3–16. (continued)Req. 3Revenues $58,400 ($58,000 from sales + $400 on investments)– Expenses 56,400 ($36,000 + $12,000 + $800 + $7,600)Net Income $ 2,000Assets = Liabilities + Stockholders’ Equity$ 1,120 $ 1,600 $ 80012,400 7,200 4,0006,400 1,600 2,7202,000 net income $19,920 $10,400 $ 9,520 Req. 4Net Profit Margin = Net Income = $2,000 = 0.0345Ratio Sales (Operating) Revenues $58,000* or 3.45% * The $400 of investment income is not an operating revenue and is not included in the computation.The increasing trend in the net profit margin ratio (from 2.5% in 2013 to 2.9% in 2014 and then to 3.45% in 2015) suggests that the company is managing its sales and expenses more effectively over time.E3–17.Req. 1Accounts receivable increases with customer sales on account and decreases with cash payments received from customers.Prepaid expenses increase with cash payments of expenses related to future periods and decrease as these expenses are incurred over time.Unearned subscriptions increase with cash payments received from customers for goods or services to be provided in the future and decreases when those goods or services are provided.Req. 2Trade Accounts ReceivablePrepaidExpensesUnearnedSubscriptionsComputations:Beginning + “+”-“-”= EndingTrade accounts receivable 717 + 5,240 -??==6935,264Prepaid expenses 95 + 203 -??==107191Unearned subscriptions 224 + 2,690 -??==2312,683E3–18.ITEM LOCATION1. Description of a company’sprimary business(es). Letter to shareholders;Management’s Discussion and Analysis; Summary of significant accounting policies note2. Income taxes paid. Notes; Statement of cash flows3. Accounts receivable. Balance sheet4. Cash flow from operatingactivities.Statement of cash flows5. Description of a company’srevenue recognition policy. Summary of significant accounting policies note6. The inventory sold during theyear.Income statement (Cost of Goods Sold)7. The data needed to compute thenet profit margin ratio.Income statementPROBLEMSP3-1.Transactions Debit Credita. Example: Purchased equipment for use in the business;5 1, 8paid one-third cash and signed a note payable for thebalance.b. Paid cash for salaries and wages earned by employees thisperiod.15 1 c. Paid cash on accounts payable for expensesincurred last period.7 1d. Purchased supplies to be used later; paid cash. 3 1e. Performed services this period on credit. 2 14f. Collected cash on accounts receivable for servicesperformed last period. 1 2g. Issued stock to new investors. 1 11, 12h. Paid operating expenses incurred this period.15 1i. Incurred operating expenses this period to be paidnext period.15 7 j. Purchased a patent (an intangible asset); paid cash. 6 1 k. Collected cash for services performed this period. 1 14 l. Used some of the supplies on hand for operations.15 3 m. Paid three-fourths of the income tax expense for the year;the balance will be paid next year.16 1, 10 n. Made a payment on the equipment note in (a); the paymentwas part principal and part interest expense.8, 17 1 o. On the last day of the current period, paid cash for aninsurance policy covering the next two years. 4 1a. Cash (+A) ........................................................................... 40,000Common stock (+SE) (20)Additional paid-in capital (+SE) ................................ 39,980 b. Cash (+A) ........................................................................... 60,000Note payable (long-term) (+L) ..................................... 60,000 c. Rent expense (+E, -SE) .................................................... 1,500Prepaid rent (+A) ............................................................... 1,500 Cash (-A) ...................................................................... 3,000 d. Prepaid insurance (+A) ..................................................... 2,400Cash (-A) ..................................................................... 2,400 e. Furniture and fixtures (or Equipment) (+A) ..................... 15,000Accounts payable (+L) ............................................... 12,000Cash (-A) ..................................................................... 3,000 f. Inventory (+A) .................................................................... 2,800Cash (-A) ..................................................................... 2,800 g. Advertising expense (+E, -SE) .. (350)Cash (-A) (350)h. Cash (+A) (850)Accounts receivable (+A) (850)Sales revenue (+R, +SE) ............................................ 1,700 Cost of goods sold (+E, -SE) . (900)Inventory (-A) (900)i. Accounts payable (-L) ...................................................... 12,000Cash (-A) ..................................................................... 12,000 j. Cash (+A) (210)Accounts receivable (-A) (210)。

会计英语第三章复习

T-account

T-account: a simplest form of an account, used to help illustrate the effect of transaction.

Account name

Debit

(left side)

Credit

(right side)

Rules of debits &credits

Record transactions in the journal

Recording Phase

General ledger (Control account)

Step 1 Analyzing business documents

Step 2 Journalizing transactions

Key words, phrases and special terms

Journalize 登记日记账[‘dʒɜːn(ə)laɪz] Journal 日记账,序时账 Journal entry 日记账分录 Cash journal 现金日记账 Post 过账 Ledger accounts 分类账'ledʒə总帐,分户总帐; Account 账户

Double-Entry Accounting

“ Double-entry accounting is based on a simple concept: each party in a business transaction will receive something and give something in return. In terms, what is received is a debit and what bookkeeping is given is a credit. The T account is a representation of a scale or balance.”

会计英语张其秀第四版课后第三章答案

会计英语张其秀第四版课后第三章答案1、20.Jerry is hard-working. It’s not ______ that he can pass the exam easily. [单选题] *A.surpriseB.surprising (正确答案)C.surprisedD.surprises2、69.Online shopping is easy, but ________ in the supermarket usually ________ a lot of time. [单选题] *A.shop; takesB.shopping; takeC.shop; takeD.shopping; takes(正确答案)3、There _____ wrong with my radio. [单选题] *A. are somethingB. are anythingC. is anythingD. is something(正确答案)4、Do not _______ me to help you unless you work harder. [单选题] *A. expect(正确答案)B. hopeC. dependD. think5、Everyone knows that the sun _______ in the east. [单选题] *A. fallsB. rises(正确答案)C. staysD. lives6、—I can’t always get good grades. What should I do?—The more ______ you are under, the worse grades you may get. So take it easy!()[单选题] *A. wasteB. interestC. stress(正确答案)D. fairness7、Alice is a ______ girl. She always smiles and says hello to others.()[单选题] *A. shyB. strictC. healthyD. friendly(正确答案)8、I don’t like snakes, so I ______ read anything about snakes.()[单选题] *A. alwaysB. usuallyC. oftenD. never(正确答案)9、I always make my daughter ______ her own room.()[单选题] *A. to cleanB. cleaningC. cleansD. clean(正确答案)10、Yesterday I _______ a book.It was very interesting. [单选题] *A. lookedB. read(正确答案)C. watchedD. saw11、8.—Will she have a picnic next week?—________. And she is ready. [单选题] * A.Yes, she doesB.No, she doesn'tC.Yes, she will(正确答案)D.No, she won't12、--All of you have passed the test!--_______ pleasant news you have told us! [单选题] *A. HowB. How aC. What(正确答案)D. What a13、The bookstore is far away. You’d better _______ the subway. [单选题] *A. sitB. take(正确答案)C. missD. get14、The story has _______ a lot of students in our class. [单选题] *A. attracted(正确答案)B. attackedC. appearedD. argued15、—Who came to your office today, Ms. Brown?—Sally came in. She hurt ______ in P. E. class. ()[单选题] *A. sheB. herC. hersD. herself(正确答案)16、Tony can _______ the guitar.Now he _______ the guitar. [单选题] *A. play; plays(正确答案)B. playing; playingC. plays; is playingD. play; is playing17、30.It is known that ipad is _________ for the old to use. [单选题] *A.enough easyB.easy enough (正确答案)C.enough easilyD.easily enough18、Mary is interested ______ hiking. [单选题] *A. onB. byC. in(正确答案)D. at19、It’s windy outside. _______ your jacket, Bob. [单选题] *A. Try onB. Put on(正确答案)C. Take offD. Wear20、At half past three she went back to the school to pick him up. [单选题] *A. 等他B. 送他(正确答案)C. 抱他D. 接他21、There is not much news in today's paper,_____? [单选题] *A. is itB. isn't itC.isn't thereD. is there(正确答案)22、Nearly everything they study at school has some practical use in their life, but is that the only reason _____ they go to school? [单选题] *A. why(正确答案)B. whichC. becauseD. what23、Bill Gates is often thought to be the richest man in the world. _____, his personal life seems not luxury. [单选题] *A. MoreoverB. ThereforeC. However(正确答案)D. Besides24、Many people believe that _________one has, _______ one is, but actually it is not true. [单选题] *A. the more money ; the happier(正确答案)B. the more money ; the more happyC. the less money ; the happierD. the less money ; the more happy25、A survey of the opinions of students()that they admit several hours of sitting in front of the computer harmful to health. [单选题] *A. show;areB. shows ;is(正确答案)C.show;isD.shows ;are26、Don’t ______. He is OK. [单选题] *A. worriedB. worry(正确答案)C. worried aboutD. worry about27、—The weather in Shanghai is cool now, ______ it? —No, not exactly. ()[单选题] *A. doesn’tB. isC. isn’t(正确答案)D. does28、Last year Polly _______ an English club and has improved her English a lot. [单选题] *A. leftB. sawC. joined(正确答案)D. heard29、E-mail is _______ than express mail, so I usually email my friends. [单选题] *A. fastB. faster(正确答案)C. the fastestD. more faster30、Sorry, I can't accept your invitation. [单选题] *A. 礼物B. 观点C. 邀请(正确答案)D. 好意。

会计英语——用英语了解会计的定义和运用

第一章 会计的基本框架

3

第二章 会计信息系统

3

第三章 财务报表

3

第四章 流动资产

3

第五章 长期资产

3

第六章 负债与或有事项

3

第七章 所有者权益

3

第八章 会计的其它领域—成本会计,管理会计和审计3

习题、实践操作习题演练

3

总复习 习题讲解

3

合计

30

1

Chapter 1

I. New words: 1. Account n. statement of money paid or owed for goods or services --The accounts show a profit of $9000. Open/close an account、account payable, account receivable, On account (1) pay part of the money (2)on credit --I will give you$30 on account. --buy things on account.

bank account -- Credit $8 to a customer / an account. Credit n. (1)permission to delay payment for goods and

services --No ~ is given at this shop. Payment must be in

prediction. --There is a lack of ~ between his promises

and his actions. ~ college, ~ column, ~course, ~school Corresponding a. more or less the same ~ fingerprints, the ~ period last year

《会计学》—作业题(第二次)第三章习题 (2)

第三章工业企业主要生产经营过程核算和成本计算本章习题一、单项选择题1.企业实际收到投资者投入的资金属于企业所有者权益中的()。

A.固定资产B.银行存款C.实收资本D.利润分配2.工业企业因采购材料而发生的装卸搬运费,支付时应计入()。

A.“周转材料”账户B.“在途物资”账户C.“管理费用”账户D.“营业外支出”账户3.为了反映企业库存材料的增减变化及其结存情况,应设置()账户。

A.在途物资B.原材料C.存货D.库存材料4.企业销售产品实现了收入,应()。

A.借记“主营业务收入”账户B.贷记“主营业务收入”账户C.贷记“本年利润”账户D.贷记“营业外收入”账户5.企业结转已销售产品的制造成本时,应借记()。

A.借记“主营业务收入”账户B.借记“本年利润”账户C.借记“主营业务成本”账户D.借记“库存商品”账户6.下列项目中属于营业外收入的有()。

A.销售产品的收入B.销售材料的收入C.固定资产清理净收益D.出租固定资产的收入7.下列人员的工资中,通过“管理费用”科目核算的是()。

A.生产车间工人工资B.车间管理人员工资C.企业管理人员工资D.销售部门职工工资8.“实收资本”账户一般按()设置明细账户。

A.企业B.投资人C.捐赠者D.受资企业9.下面属于其他业务收入的是()。

A.利息收入B.投资收益C.清理固定资产净收益D.出售材料收入10.张华出差时借款900元,回来后报销差旅费800元,退回现金100元,会计分录应为()。

A.借:管理费用800库存现金100贷:其他应收款一张华900B.借:管理费用900贷:其他应收款一张华800库存现金100C.借:其他应收款一张华900贷:管理费用800库存现金100D.借:库存现金100其他应收款一张华800贷::管理费用900二、多项选择题1.工业企业的主要经营过程包括()。

A.筹资过程B.供应过程C.生产过程D.销售过程2.下列费用中应计入外购材料采购成本的有()。

会计第三章附答案

第三章会计科目与账户课后练习一、单项选择题(下列每小题备选答案中,只有一个符合题意的正确答案。

请将选定答案的编号,用英文大写字母填入括号内)1.会计科目是指对( B )的具体内容进行分类核算的项目。

A.经济业务B.会计要素c.会计账户D.会计信息2.会计科目按其所( D )不同,分为总分类科目和明细分类科目。

A.反映的会计对象B.反映的经济业务C.归属的会计要素D.提供信息的详细程度及其统驭关系3.( A) 设置会计科目的原则。

A.重要性原则B.合法性原则C.相关性原则D.实用性原则4.( D 原则.是指所设置的会计科目应符合单位自身特点.满足单位实际需要。

A.合法性B.相关性C.谨慎性D.实用性5.会计科目是( A )的名称。

A.账户B.会计凭证C.会计报表D.会计要素6.对会计要素具体内容进行总括分类、提供总括信息的会计科目称为( A )。

A.总分类科目B.明细分类科目C.二级科目D.备查科目7.二级科目是介于( A)之间的科目。

A.总分类科目和明细分类科目B.总账与明细账C.总分类科目D.明细分类科目8.会计科目按其所( C 不同,分为资产类、负债类、所有者权益类、成本类、损益类五大类。

A.反映的会计对象B.反映的经济业务C.归属的会计要素D.提供信息的详细程度及其统驭关系9.“预付账款”科目按其所归属的会计要素不同,属于( A ) 类科目。

A.资产B.负债C.所有者权益D.成本10.“预收账款”科目按其所归属的会计要素不同,属于( B )类科目。

A.资产B.负债C.所有者权益D.成本11.“资本公积”科目按其所归属的会计要素不同,属于( C )类科目。

A.资产B.负债C.所有者权益D.损益12.“主营业务收入”科目按其所归属的会计要素不同,属于( D )类科目。

A.资产B.所有者权益c.成本D.损益13.“管理费用”科目接其所归属的会计要素不同,属于( D )类科目。

A.资产B.所有者权益 C.成本D.损益14.“制造费用”科目按其所归属的会计要素不同,属于( D )类科目。

《会计学》—作业题(第二次)第三章习题

《会计学》—作业题(第二次)第三章习题第三章工业企业主要生产经营过程核算和成本计算本章习题一、单项选择题1.企业实际收到投资者投入的资金属于企业所有者权益中的()。

A.固定资产B.银行存款C.实收资本D.利润分配2.工业企业因采购材料而发生的装卸搬运费,支付时应计入()。

A.“周转材料”账户B.“在途物资”账户C.“管理费用”账户D.“营业外支出”账户3.为了反映企业库存材料的增减变化及其结存情况,应设置()账户。

A.在途物资B.原材料C.存货D.库存材料4.企业销售产品实现了收入,应()。

A.借记“主营业务收入”账户B.贷记“主营业务收入”账户C.贷记“本年利润”账户D.贷记“营业外收入”账户5.企业结转已销售产品的制造成本时,应借记()。

A.借记“主营业务收入”账户B.借记“本年利润”账户C.借记“主营业务成本”账户D.借记“库存商品”账户6.下列项目中属于营业外收入的有()。

A.销售产品的收入B.销售材料的收入C.固定资产清理净收益D.出租固定资产的收入7.下列人员的工资中,通过“管理费用”科目核算的是()。

A.生产车间工人工资B.车间管理人员工资C.企业管理人员工资D.销售部门职工工资8.“实收资本”账户一般按()设置明细账户。

A.企业B.投资人C.捐赠者D.受资企业9.下面属于其他业务收入的是()。

A.利息收入B.投资收益C.清理固定资产净收益D.出售材料收入10.张华出差时借款900元,回来后报销差旅费800元,退回现金100元,会计分录应为()。

A.借:管理费用800库存现金100贷:其他应收款一张华900B.借:管理费用900贷:其他应收款一张华800库存现金100C.借:其他应收款一张华900贷:管理费用800库存现金100D.借:库存现金100其他应收款一张华800贷::管理费用900二、多项选择题1.工业企业的主要经营过程包括()。

A.筹资过程B.供应过程C.生产过程D.销售过程2.下列费用中应计入外购材料采购成本的有()。

会计英语.课件.

立信会计出版社

第 三 章

Unit 3 Accounting cycle Ⅱ 第三章 会计循环 Ⅱ

• 1. Books of prime entry 原始账簿 • 1.1 Sales day book 销售日记账 • 1.2 Purchases day book 采购日记账

立信会计出版社

• 1.3 Cash book and petty • 现金日记账及零用现金簿 • 1.3.1 Cash book • 1.3.2 Petty cash book

立信会计出版社

• 4. GAAP 一般公认会计原则 • 5.IASs and IFRSs • 国际会计准则及国际财务报告准则

立信会计出版社

• 6. •

Assumptions and characteristics of financial statement. 财务报告的假设及特征

立信会计出版社

高职高专十二五规划重点教材

会计英语 ACCOUNTING ENGLISH 宁小博 主编

立信会计出版社

第 一 章

Unit 1 Introduction to accounting 第一章 会计导论

• 1. Definition • 会计的概念

of accounting

• 6.1 Underlying assumptions • Accrual basis权责发生制 • Going concern 6.2 • • • • •

Qualitative Characteristics of financial statement 财务报告的质量特征 Understandability可理解性 Relevance 相关性 Reliability 可靠性 Comparability 可比性

会计英语第四版第三章课后题答案

会计英语第四版第三章课后题答案1、—How do you find()birthday party of the Blairs? —I should say it was __________ complete failure.[单选题] *A.a; aB. the ; a(正确答案)C.a; /D.the; /2、Before you quit your job, ()how your family will feel about your decision. [单选题] *A. consider(正确答案)B. consideringC. to considerD. considered3、Mary is interested ______ hiking. [单选题] *A. onB. byC. in(正确答案)D. at4、79.On a ________ day you can see the city from here. [单选题] * A.warmB.busyC.shortD.clear(正确答案)5、Mary _____ be in Paris. I saw her just now on campus. [单选题] *A. mustn'tB. can't(正确答案)C. need notD. may not6、He spoke too fast, and we cannot follow him. [单选题] *A. 追赶B. 听懂(正确答案)C. 抓住D. 模仿7、He was born in Canada, but he has made China his _______. [单选题] *A. familyB. addressC. houseD. home(正确答案)8、Yesterday I _______ a book.It was very interesting. [单选题] *A. lookedB. read(正确答案)C. watchedD. saw9、You could hardly imagine _______ amazing the Great Wall was. [单选题] *A. how(正确答案)B. whatC. whyD. where10、( ) The salesgirls in Xiushui Market have set a good example______us in learning English. [单选题] *A. to(正确答案)B. forC. withD. on11、7.—________ is the Shanghai Wild Animal Park?—It’s 15km east of the Bund. [单选题] *A.WhoB.WhatC.WhenD.Where (正确答案)12、一Mary wants to invite you to see the movie today. 一I would rather she(B)me tomorrow. [单选题] *A.tellsB. told (正确答案)C. would tellD. had told13、( ) What she is worried __ is ____ her daughter is always addicted to chatting online./; that [单选题] *A /; thatB of thatC about that(正确答案)D about what14、40.—________ apples do we need to make fruit salad?—Let me think…We need three apples. [单选题] *A.How longB.How oftenC.How muchD.How many(正确答案)15、--Jenny, what’s your favorite _______?--I like potatoes best. [单选题] *A. fruitB. vegetable(正确答案)C. drinkD. meat16、He gathered his courage and went on writing music. [单选题] *A. 从事B. 靠······谋生C. 继续(正确答案)D. 致力于17、Which animal do you like _______, a cat, a dog or a bird? [单选题] *A. very muchB. best(正确答案)C. betterD. well18、At last the plane landed at the Beijing Airport safely. [单选题] *A. 平稳地B. 安全地(正确答案)C. 紧急地D. 缓缓地19、74.No person ()carry a mobile phone into the examination room during the national college Entrance Examinations.[单选题] *A.shall(正确答案)B.mustC.canD.need20、I like this house with a beautiful garden in front, but I don't have enough money to buy _____. [单选题] *A. it(正确答案)B. oneC. thisD. that21、It is an online platform _____ people can buy and sell many kinds of things. [单选题] * A.whenB. where(正确答案)C.thatD.which22、This girl is my best friend, Wang Hui. ______ English name is Jane.()[单选题] *A. HeB. HisC. SheD. Her(正确答案)23、He was?very tired,so he stopped?_____ a rest. [单选题] *A. to have(正确答案)B. havingC. haveD. had24、One effective()of learning a foreign language is to study the language in its cultural context. [单选题] *A. approach(正确答案)B. wayC. mannerD. road25、Every means _____ but it's not so effective. [单选题] *A. have been triedB. has been tried(正确答案)C. have triedD. has tried26、45.—Let's make a cake ________ our mother ________ Mother's Day.—Good idea. [单选题] *A.with; forB.for; on(正确答案)C.to; onD.for; in27、We had a party last month, and it was a lot of fun, so let's have _____ one this month. [单选题] *A.otherB.the otherC.moreD.another(正确答案)28、I hadn't realized she was my former teacher _____ she spoke [单选题] *A. asB. sinceC. until(正确答案)D. while29、Can I _______ your order now? [单选题] *A. makeB. likeC. giveD. take(正确答案)30、I am worried about my brother. I am not sure _____ he has arrived at the school or not. [单选题] *A. whether(正确答案)B. whatC. whenD. how。

会计英语.

• • •

4. GAAP 一般公认会计原则 5.IASs and IFRSs 国际会计准则及国际财务报告准则

• •

6. Assumptions and characteristics of financial statement. 财务报告的假设及特征

• • •

6.1 Underlying assumptions 基本假设 Accrual basis权责发生制 Going concern 持续经营

• • • • • •

6.2 Qualitative Characteristics of financial statement 财务报告的质量特征 Understandability可理解性 Relevance 相关性 Reliability 可靠性 Comparability 可比性

第 二 章

2.5 Posting from the day books to ledger 日记账结转至总账(分类账) After recording day books, the next step in the accounting process is to post transactions to the accounts in the general ledger and personal ledger.

Unit 2 Accounting cycle Ⅰ 第二章 会计循环Ⅰ

• • •

1. Documenting business transactions 记录企业业务交易 1.1 External documentation 外部凭证

• • • •

1.2 Internal documentation 内部凭证 1.2.1 invoices 发票 1.2.2 Credit Note 抵扣发票 1.2.3 Petty cash voucher 零用资金报 销单

会计英语

会计英语一、听力Three key (1) financial statements represent the essentials in obtaining these information. They are the (2) balance sheet, the (3) income statement and the (4) cash flow statement . Financial statements are usually prepared by the companies on the (5) accounts . And they may be (6) reviewed or (7) audited and (8) certified for the (9) accuracy by outside the client firms. All (10) public traded companies are required to (11) publish financial statements. Most other businesses supply them as well. Financial statements are truly the language of business. In this program, we will follow two (12) managers as they assess the (13) financial help of two restaurants that they candidate for the (14) potential purchase or (15) acquisition . The story we will see is an imaginary one. The lessons are very real. You will learn how to use financial data to read the tales of these two restaurants. Most important, the lessons learnt can be applied to other businesses as well.The types of course work that we would look for when we are hiring someone straight out of undergraduate would be 1.__accounting_and 2.___finance_, because it provides a terminology. It allows us to communicate things quickly in a terminology we understand. People who have the detail-oriented approach to understand the 3._financial__statements__ from an 4. _accounting_perspective_. And also understand you know, the difference between the accounting statement, which is a 5._snapshot(快门)_ of what is going on now, and the financial type of 6. _forecast__ that allow us to then 7._project________ and think about how those financial statements are going to change going forward based on the things that the company is doing. That is the combination we are looking for, is being able to 8.___ understand the data___. But then being able to be flexible enough to look forward and think about how that data is going to change as the company 9.evolves. So it is very much a combination of accounting and finance. And again, to stress the written communication and the oral communication is just vital because people have to understand your analysis before they are going to be willing to 10._invest___on it.二、单选题1. Which of the following service involves providing an independent report on the appropriateness of financial statements? (A)A. AuditB. TaxC. ConsultingD. Budgeting2. Which of the following is a liability account?(C)A. Prepaid InsuranceB. Intangible AssetsC. Salaries PayableD. Accumulated Depreciation3、W hich of the following is a contra asset account?(C)A、InventoryB、GoodwillC、Accumulated DepreciationD、Retained Earnings4、Which of the following belongs to the current assets?(D)a.Long-term investmentb. Plant and equipmentc. Intangible assetsd. Inventory5、W hich of the following belongs to the long-term liabilities?(C)A、Retained earningsB、Capital stockC、Dividend payableD、Bonds payable6、Financial statement does not include ( D)A、lance sheetB、come statementC、sh flow statementD、king sheet7、profit-making business operating as a separate legal entity and in which ownershipis divided into shares of stock is known as a:(D)A. proprietorship.B. service business.C. partnership.D. corporation.8、2. If revenue was $45,000, expenses were $37,500, and the owner’s withdrawalswere $10,000, the amount of net income or net loss would be:(B)A. $45,000 net income.B. $7,500 net income.C. $37,500 net loss.D. $2,500 net loss.9、Which of the following items represents a deferral?(A)A. Prepaid insuranceB. Wages payableC. Fees earnedD. Accumulated depreciation10、If the estimated amount of depreciation on equipment for a period is $2,000, theadjusting entry to record depreciation would be:(C)A. debit Depreciation Expense, $2,000; credit Equipment,$2,000.B. debit Equipment, $2,000; credit Depreciation Expense,$2,000.C. debit Depreciation Expense, $2,000; credit Accumulated Depreciation,$2,000.D. debit Accumulated Depreciation, $2,000; credit Depr eciation Expense,$2,000.11、Which of the following accounts would not be closed to the income summaryaccount at the end of a period?(D)A. Depreciation ExpenseB. Wages ExpenseC. Rent ExpenseD. Accumulated Depreciation12、Which of the following is an example of an intangible asset?(D)A. PatentsB. GoodwillC. CopyrightsD. All of the above三、计算题(关于会计投资、筹资活动的现金流量)(2) Compute the net cash used (provided) by financing activities.Net cash provided by investing activities =81000-37000-53000=91000Net cash used by financing activities =47000-40000-85000-1000000= -78000四、填空题1、填字母(交易与相应的分类对上号)2、填数字(成本流转假设)——计算P553、排序题A. To record receipt of unearned revenue.B. To record this period’s earning of prior unearned revenue.C. To record payment of an accrued expense.D. To record receipt of an accrued revenue.E. To record an accrued expense.F. To record an accrued revenue.G. To record this period’s use of a prepaid expense.五、论述题(一)、chapter10(课本上96~97页)1、The factors that are directly relevant to an analysis of business performance:(1)、the size of the business(2)、the business risk(3)、the economic environment(4)、Industry trends ,effects of changes in technology2、The information that the public company provided includes:(1)、Chairman’s statement(2)、Director s’ report(3)、the balance sheet(4)、Statements of income and changes in equity(5)、Statement of cash flows(6)、Notes to the statements(7)、Auditors’ report(8)、External sources(二)、交易效果题(即资产、负债、所有者权益的增减问题)例:Describe the effects of each of the following business transactions on assets, liabilities and owners’equity.(1). Bought equipment on credit.(2). Paid salaries to employees.(3). Sold services for cash.答案:(1). Increase both asset and liability.(2). Decrease both asset and liability.(3). Increase both asset and owners’equity.知识点:第一章:1、Two objectives of financial statements(P5)会计目标2、Underlying Assumptions (P6)第三章:1、Financial statement consists (P19)财务报表的组成2、资产、负债、所有者的构成(P19~P20)——table 3-33、the format of balance sheet: the account form and the report (区别)例:In the report form,(报告式) the assets are listed on the left side of the page and liabilities and owner’s equity on the right side .(其中report form 应该是account form)*4、income Statement (P22-23)5、Three Categories of Cash Flows (区别)(P26)1、Investing activities2、Financing activities3、Operating activities第四章1、Accounting Equation: asset=liabilities+equity(P33)2、复式记账法(double-Entry Bookkeeping)的含义(P33)Debits must equal credits3、会计循环(Accounting Cycle)——排序题(P35)理解:过账、结账分录、试算平衡表、结账后试算平衡表的含义4、Accruals and deferrals adjustments 应计和递延项目的含义及能简单的区分它们5、close temporary accounts (P45)了解下期末的结算。

《会计学》—作业题(第二次)第三章习题 (2)

第三章工业企业主要生产经营过程核算和成本计算本章习题一、单项选择题1.企业实际收到投资者投入的资金属于企业所有者权益中的()。

A.固定资产B.银行存款C.实收资本D.利润分配2.工业企业因采购材料而发生的装卸搬运费,支付时应计入()。

A.“周转材料”账户B.“在途物资”账户C.“管理费用”账户D.“营业外支出”账户3.为了反映企业库存材料的增减变化及其结存情况,应设置()账户。

A.在途物资B.原材料C.存货D.库存材料4.企业销售产品实现了收入,应()。

A.借记“主营业务收入”账户B.贷记“主营业务收入”账户C.贷记“本年利润”账户D.贷记“营业外收入”账户5.企业结转已销售产品的制造成本时,应借记()。

A.借记“主营业务收入”账户B.借记“本年利润”账户C.借记“主营业务成本”账户D.借记“库存商品”账户6.下列项目中属于营业外收入的有()。

A.销售产品的收入B.销售材料的收入C.固定资产清理净收益D.出租固定资产的收入7.下列人员的工资中,通过“管理费用”科目核算的是()。

A.生产车间工人工资B.车间管理人员工资C.企业管理人员工资D.销售部门职工工资8.“实收资本”账户一般按()设置明细账户。

A.企业B.投资人C.捐赠者D.受资企业9.下面属于其他业务收入的是()。

A.利息收入B.投资收益C.清理固定资产净收益D.出售材料收入10.张华出差时借款900元,回来后报销差旅费800元,退回现金100元,会计分录应为()。

A.借:管理费用800库存现金100贷:其他应收款一张华900B.借:管理费用900贷:其他应收款一张华800库存现金100C.借:其他应收款一张华900贷:管理费用800库存现金100D.借:库存现金100其他应收款一张华800贷::管理费用900二、多项选择题1.工业企业的主要经营过程包括()。

A.筹资过程B.供应过程C.生产过程D.销售过程2.下列费用中应计入外购材料采购成本的有()。

会计学原理financialaccountingbyrobertlibby第八版第三章答案

Chapter 3Operating Decisions and the Accounting SystemANSWERS TO QUESTIONS1. A typical business operating cycle for a manufacturer would be asfollows: inventory is purchased, cash is paid to suppliers, the productis manufactured and sold on credit, and the cash is collected from thecustomer.2. The time period assumption means that the financial condition andperformance of a business can be reported periodically, usually everymonth, quarter, or year, even though the life of the business is muchlonger.3. Net Income = Revenues + Gains - Expenses - Losses.Each element is defined as follows:Revenues -- increases in assets or settlements of liabilities fromongoing operations.Gains -- increases in assets or settlements of liabilities fromperipheral transactions.Expenses -- decreases in assets or increases in liabilities from ongoing operations.Losses -- decreases in assets or increases in liabilities fromperipheral transactions.4.Both revenues and gains are inflows of net assets. However, revenuesoccur in the normal course of operations, whereas gains occur from transactions peripheral to the central activities of the company. An example is selling land at a price above cost (at a gain) for companies not in the business of selling land.Both expenses and losses are outflows of net assets. However, expenses occur in the normal course of operations, whereas losses occur from transactions peripheral to the central activities of the company. An example is a loss suffered from fire damage.5. Accrual accounting requires recording revenues when earned and recordingexpenses when incurred, regardless of the timing of cash receipts or payments. Cash basis accounting is recording revenues when cash is received and expenses when cash is paid.6. The four criteria that must be met for revenue to be recognized underthe accrual basis of accounting are (1) delivery has occurred or services have been rendered, (2) there is persuasive evidence of an arrangement for customer payment, (3) the price is fixed or determinable, and (4) collection is reasonably assured.7. The expense matching principle requires that expenses be recorded whenincurred in earning revenue. For example, the cost of inventory sold during a period is recorded in the same period as the sale, not when the goods are produced and held for sale.8. Net income equals revenues minus expenses. Thus revenues increase netincome and expenses decrease net income. Because net income increases stockholders’ equity, revenues increase stockholders’ equity and expenses decrease it.9. Revenues increase stockholders’ equity and expenses decreasestockholders’ equity. To increase stockholders’ equity, an account must be credited; to decrease stockholders’ equity, an account must be debited. Thus revenues are recorded as credits and expenses as debits.10.11.12.13.Total net profit margin ratio is calculated as Net Income Net Sales(or Operating Revenues). The net profit margin ratio measures how much of every sales dollar is profit. An increasing ratio suggests that the company is managing its sales and expenses effectively.ANSWERS TO MULTIPLE CHOICE1. c2. a3. b4. b5. c6. c7. d8. b9. a10. bAuthors' Recommended Solution Time(Time in minutes)* Due to the nature of this project, it is very difficult to estimate the amount of time students will need to complete the assignment. As with any open-ended project, it is possible for students to devote a large amount of time to these assignments. While students often benefit from the extra effort, we find that some become frustrated by the perceived difficulty of the task. You can reduce student frustration and anxiety by making your expectations clear. For example, when our goal is to sharpen research skills, we devote class time discussing research strategies. When we want the students to focus on a real accounting issue, we offer suggestions about possible companies or industries.MINI-EXERCISESM3–1.TERMG(1)LossesC(2)Expense matchingprincipleF(3)RevenuesE(4)Time period assumptionB(5)Operating cycleM3–2.Cash Basis Income StatementAccrual Basis Income StatementRevenues:Cash salesCustomer deposits $8,0005,000Revenues:Sales tocustomers$18,000Expenses:Inventory purchases Wages paid 1,000900Expenses:Cost of salesWages expenseUtilitiesexpense9,000900 300Net Income $11,100Net Income$7,800M3–3.Revenue Account Affected Amount of Revenue Earned in JulyM3–4.Expense Account Affected Amount of Expense Incurred in JulyM3–5.a.Cash (+A)...........................................15,000Games Revenue (+R, +SE)..........................15,000b.Cash (+A)...........................................3,000Accounts Receivable (+A)............................5,000 Sales Revenue (+R, +SE)..........................8,000c.Cash (+A)...........................................4,000Accounts Receivable (A)........................4,000d.Cash (+A)...........................................2,500Unearned Revenue (+L)............................2,500 M3–6.e.Cost of Goods Sold (+E, SE).......................6,800Inventory (A)..................................6,800f.Accounts Payable (–L) (800)Cash (A) (800)g.Wages Expense (+E, SE)............................3,500Cash (A).......................................3,500h.Insurance Expense (+E, SE) (500)Prepaid Expenses (+A)...............................1,00 Cash (A).......................................1,500i.Repairs Expense (+E, SE) (700)Cash (A) (700)j.Utilities Expense (+E, SE) (900)Accounts Payable (+L) (900)M3–7.Balance Sheet Income StatementTransaction (c) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.M3–8.Balance Sheet Income Statement+1,000i.–700NE–700NE+700–700 j.NE+900–900NE+900–900Transaction (h) results in an increase in an asset (prepaid expenses) and a decrease in an asset (cash). Therefore, the net effect on assets is 500.M3–9.Craig’s Bowling, Inc.Income StatementFor the Month of July 2014Revenues:Games revenue$15,000Sales revenue8,000Total revenues23,000 Expenses:Cost of goods sold6,800Utilities expense900Wages expense3,500Insurance expense500Repairs expense700Total expenses 12,400 Net income$ 10,600M3–10.M3–11.These results suggest that Jen’s Jewelry Company earned approximately $ for every dollar of revenue in 2015, and over time, the ratio has improved. Jen’s has become more effective at managing sales and expenses.As additional analysis:Between 2013 to 2014 and 2014 to 2015, sales have increased at a lower percentage than net income. This suggests that the company has been more effective at controlling expenses than generating revenues.EXERCISESE3–1.TERMK (1) ExpensesE (2) GainsG (3) Revenue realization principleI (4) Cash basis accountingM (5) Unearned revenueC (6) Operating cycleD (7) Accrual basis accountingF (8) Prepaid expensesJ (9) Revenues Expenses = Net IncomeL(10) Ending Retained Earnings =Beginning Retained Earnings + Net Income DividendsDeclaredE3–2.Req. 1Cash Basis Income StatementAccrual Basis Income StatementRevenues:Cash salesCustomer deposits$500,000 70,000Revenues:Sales tocustomers$750,00Expenses:Inventory purchases Wages paidUtilities paid90,000180,30017,200Expenses:Cost of salesWages expenseUtilitiesexpense485,000184,00019,130Net Income$282,500 Net Income$61,870Req. 2Accrual basis financial statements provide more useful information to external users. Financial statements created under cash basis accounting normally postpone ., $250,000 credit sales) or accelerate ., $70,000 customer deposits) recognition of revenues and expenses long before or after goods and services are produced and delivered (until cash is received or paid). They also do not necessarily reflect all assets or liabilities of a company on a particular date.E3–3.ActivitRevenue AccountAmount of RevenueyE3–4.Activity Expense Account Affected Amount of ExpenseE3–5.Balance Sheet Income StatementTransaction (k) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.* A loss affects net income negatively, as do expenses.E3–6.Balance Sheet Income StatementTransaction (f) results in an increase in an asset (property, plant, and equipment) and a decrease in an asset (cash). Therefore, there is no net effect on assets.E3–7.(in thousands)a.Plant and equipment (+A) (636)Cash (A) (636)Debits equal credits. Assets increase and decrease by the same amount.b.Cash (+A) (181)Short-term notes payable (+L) (181)Debits equal credits. Assets and liabilities increase by the sameamount.c.Cash (+A) ..........................................Accounts receivable (+A) ........................... 10,765 28,558Service revenue (+R, +SE) ...................... 39,323 Debits equal credits. Revenue increases retained earnings (part of stockholders' equity). Stockholders' equity and assets increase by the same amount.E3–7. (continued)d.Accounts payable (L) ............................. 32,074Cash (A) ..................................... 32,074 Debits equal credits. Assets and liabilities decrease by the sameamount.e.Inventory (+A) ..................................... 32,305Accounts payable (+L) .......................... 32,305 Debits equal credits. Assets and liabilities increase by the sameamount.f.Wages expense (+E, SE) ........................... 3,500Cash (A) ..................................... 3,500 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by the same amount.g.Cash (+A) .......................................... 39,043Accounts receivable (A) ..................... 39,043 Debits equal credits. Assets increase and decrease by the same amount.h.Fuel expense (+E, SE) (750)Cash (A) (750)Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by the same amount.i.Retained earnings (SE) (597)Cash (A) (597)Debits equal credits. Assets and stock holders’ equity decrease by the same amount.j.Utilities expense (+E, SE) (68)Cash (A) ..................................... Accounts payable (+L) .......................... 55 13Debits equal credits. Expenses decrease retained earnings (part of stockholders' equity). Together, stockholders' equity and liabilities decrease by the same amount as assets.E3–8.Req. 1a.Cash (+A)...................................... 2,300,000Short-term note payable (+L)............. 2,300,000 Debits equal credits. Assets and liabilities increase by the sameamount.b.Equipment (+A)................................. 98,000Cash (A)............................... 98,000 Debits equal credits. Assets increase and decrease by the same amount.c.Merchandise inventory (+A)..................... 35,000Accounts payable (+L).................... 35,000 Debits equal credits. Assets and liabilities increase by the sameamount.d.Repairs (or maintenance) expense (+E, SE).... 62,000Cash (A)............................... 62,000 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by the same amount.e.Cash (+A)...................................... 390,000Unearned pass revenue (+L)............... 390,000 Debits equal credits. Since the season passes are sold before VailResorts provides service, revenue is deferred until it is earned.Assets and liabilities increase by the same amount.f. Two transactions occur:(1) Accounts receivable (+A) (800)Ski shop sales revenue (+R, +SE) (800)Debits equal credits. Revenue increases retained earnings (a part of stockholders' equity). Stockholders' equity and assets increase by the same amount.(2) Cost of goods sold (+E, SE) (500)Merchandise inventory (A) (500)Debits equal credits. Expenses decrease retained earnings (a part of stockholders' equity). Stockholders' equity and assets decrease by the same amount.E3–8. (continued)g.Cash (+A)...................................... 320,000Lift revenue (+R, +SE)................... 320,000 Debits equal credits. Revenue increases retained earnings (a part ofstockholders' equity). Stockholders' equity and assets increase by thesame amount.h.Cash (+A)...................................... 3,500Unearned rent revenue (+L)............... 3,500 Debits equal credits. Since the rent is received before the townhouseis used, revenue is deferred until it is earned. Assets and liabilitiesincrease by the same amount.i. Accounts payable (L)......................... 17,500Cash (A)............................... 17,500 Debits equal credits. Assets and liabilities decrease by the sameamount.j.Cash (+A) (400)Accounts receivable (A) (400)Debits equal credits. Assets increase and decrease by the same amount.k.Wages expense (+E, SE)....................... 245,000Cash (A)............................... 245,000 Debits equal credits. Expenses decrease retained earnings (a part ofstockholders' equity). Stockholders' equity and assets decrease by the same amount.Req. 2Accounts ReceivableE3–9.2/1Rent expense (+E, SE) (275)Cash (A) (275)2/2Fuel expense (+E, SE) (490)Accounts payable (+L) (490)2/4Cash (+A) (820)Unearned revenue (+L) (820)2/7Cash (+A) (910)Transport revenue (+R, +SE) (910)2/10Advertising expense (+E, SE) (175)Cash (A) (175)2/14Wages payable (L) ................................ 2,300 Cash (A) ............................... 2,3002/18Cash (+A) ..........................................Accounts receivable (+A) ........................... 1,600 2,200Transport revenue (+R, +SE) .............. 3,8002/25Parts supplies (+A) ................................ 2,550 Accounts payable (+L) .................... 2,5502/27Retained earnings (SE) (200)Dividends payable (+L) (200)E3–10.Req. 1 and 2CashAccounts ReceivableSuppliesEquipmentLandBuildingAccounts PayableUnearned Fee Revenue Note PayableCommon StockAdditional Paid-inCapitalRetained EarningsRebuilding FeesRevenueRent RevenueWages Expense Utilities ExpenseItem (f) is not a transaction; there has been no exchange.E3–10. (continued)Req. 3Net income using the accrual basis of accounting:Revenues$19,850($19,000 + $850)– Expenses 16,900($16,500 + $400)Net Income$ 2,950(accrual basis)Assets=Liabilities+Stockholders’Equity $12,090$ 7,700 $ 1,70024,800 4,440 7,8202,460 48,500 9,36010,420 2,950 netincome7,40025,300$82,470$60,640$21,830Req. 4Net income using the cash basis of accounting:Cash receipts$27,650(transactions a through d)– Cash disbursements 19,760(transactions g, i, and k)Net Income$ 7,890(cash basis)Cash basis net income ($7,890) is higher than accrual basis net income ($2,950) because of the differences in the timing of recording revenues versus receipts and expenses versus disbursements between the two methods. The $7,800 higher amount in cash receipts over revenues includes cash received prior to being earned (from (b), $600) and cash received after being earned (in (d), $7,200). The $2,860 higher amount in cash disbursements over expenses includes cashpaid after being incurred in the prior period (in (g), $2,300), plus cash paid for supplies to be used and expensed in the future (in (k), $960), less an expense incurred in January to be paid in February (in (e), $400).STACEY’S PIANO REBUILDING COMPANYIncome Statement (unadjusted)For the Month Ended January 31, 2014 Operating Revenues:Rebuilding fees revenue$ 19,000 Total operating revenues19,000 Operating Expenses:Wages expense16,500 Utilities expense400 Total operating expenses16,900 Operating Income2,100 Other Item:Rent revenue850 Net Income$ 2,950Req. 1 and 2Cash Accounts Receivable SuppliesEquipment Building Accounts PayableNote PayableMortgage PayableCommon StockAdditional Paid-in Capital Retained EarningsFood Sales RevenueCatering SalesRevenueSupplies ExpenseUtilities Expense Wages ExpenseFuel ExpenseE3–14.Req. 1TRAVELING GOURMET, INC.Income Statement (unadjusted)For the Month Ended March 31, 2014 Revenues:Food sales revenueCatering sales revenueTotal revenues Expenses:Supplies expenseUtilities expenseWages expenseFuel expenseTotal costs and expenses$ 11,900 4,20016,100 10,8304206,280363 17,893Net Loss$ (1,793) Req. 2TransactionO, I, or F Activity(or No Effect) onStatement of CashFlows Direction and Amountof EffectReq. 3The company generated a small loss of 1,793 during its first month of operations, before making any adjusting entries. The adjusting entries for use of the building and equipment and interest expense on the borrowing will increase the loss. Cash flows from operating activities were also negative at $2,973 (= + 11,900 + 2,600 – 10,830 – 363 – 6,280) . So far the company does not appear to be successful, but it is only in its first month of operating a retail store. If sales can be increased without inflating fixed costs (particularly salaries expense), the company may soon turn a profit. It is not unusual for small businesses to report a loss or have negative cash flows from operations as they start up operations.E3–15.Req. 1Transaction Brief Explanationa Issued 10,000 shares of common stock to shareholders for$82,000 cash.b Purchased store fixtures for $15,400 cash.c Purchased $24,800 of inventory, paying $6,200 cash and thebalance on account.d Sold $14,000 of goods or services to customers, receiving$9,820 cash and the balance on account. The cost of the goodssold was $7,000.e Used $1,480 of utilities during the month, not yet paid.f Paid $1,300 in wages to employees.g Paid $2,480 in cash for rent, $620 related to the current monthand $1,860 related to future months.h Received $3,960 cash from customers, $1,450 related to currentsales and $2,510 related to goods or services to be provided inthe future.Req. 2Kate’s Kite CompanyIncome StatementFor the Month Ended April 30, 2014Sales RevenueExpenses:Cost of salesWages expenseRent expenseUtilities expenseTotal expenses$ 15,450 7,0001,300620 1,480 10,400Net Income$ 5,050E3–15. (continued)Kate’s Kite CompanyBalance SheetAt April 30, 2014Assets Liabilities and Shareholders’EquityCurrent Assets:Current Liabilities:Cash$70,400Accounts payable$20,080 Accounts receivable4,180Unearned revenue2,510 Inventory17,800 Total currentliabilities22,590Prepaid expenses1,860Shareholders’ Equity:Total current assets94,240Common stock10,000 Store fixtures15,400Additional paid-in capital72,000Retained earnings5,050Total shareholders’equity87,050Total Assets$109,640Total Liabilities &Shareholders’ Equity$109,64E3–16. Req. 1。

MOOC会计学原理第三章作业

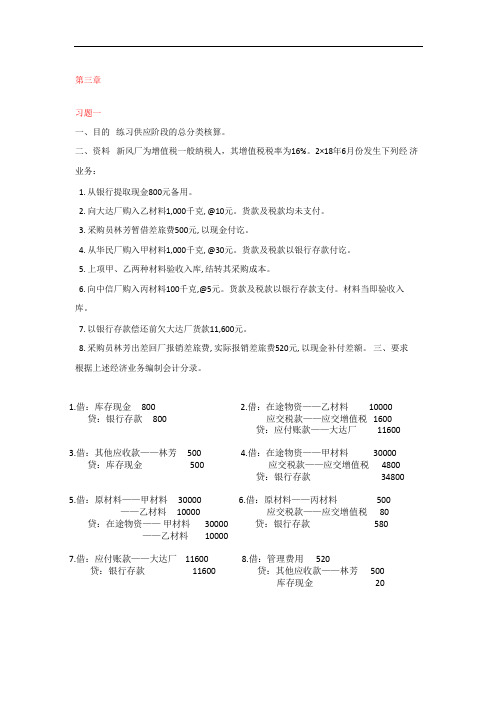

第三章习题一一、目的练习供应阶段的总分类核算。

二、资料新风厂为增值税一般纳税人,其增值税税率为16%。

2×18 年6月份发生下列经济业务:1. 从银行提取现金800 元备用。

2. 向大达厂购入乙材料1,000 千克, @10 元。

货款及税款均未支付。

3. 采购员林芳暂借差旅费500 元, 以现金付讫。

4. 从华民厂购入甲材料1,000 千克, @30 元。

货款及税款以银行存款付讫。

5. 上项甲、乙两种材料验收入库, 结转其采购成本。

6. 向中信厂购入丙材料100 千克, @5 元。

货款及税款以银行存款支付。

材料当即验收入库。

7. 以银行存款偿还前欠大达厂货款11,600 元。

8. 采购员林芳出差回厂报销差旅费, 实际报销差旅费520 元, 以现金补付差额。

三、要求根据上述经济业务编制会计分录。

1.借:库存现金 8002.借:在途物资——乙材料 10000贷:银行存款 800 应交税款——应交增值税 1600贷:应付账款——大达厂 11600 3.借:其他应收款——林芳 500 4.借:在途物资——甲材料 30000贷:库存现金 500 应交税款——应交增值税 4800贷:银行存款 34800 5.借:原材料——甲材料 30000 6.借:原材料——丙材料 500——乙材料 10000 应交税款——应交增值税 80 贷:在途物资——甲材料 30000 贷:银行存款 580——乙材料 100007.借:应付账款——大达厂 11600 8.借:管理费用 520贷:银行存款 11600 贷:其他应收款——林芳 500库存现金 20第三章习题二一、目的练习材料采购成本的计算二、资料1. 前锋厂2×09 年10 月从外地新兴厂购入下列材料:2.1. 以材料重量为标准, 分配材料采购的采购费用。

材料的采购费用分配表2. 编制材料采购成本计算表。

材料采购成本计算表第三章习题三一、目的练习生产阶段的总分类核算。

会计英语第3章

3.1.1 Components of Balance Sheet

The balance sheet mainly includes three segments: assets, liabilities, and owner’s equity.

According to the liquidity of accounts, items in balance sheet are subcategorized and listed separately.

Owner’s Equity=total assets - liabilities. represented on the balance sheet with two

accounts.

◦ (1) Contributed Capital ◦ (2) Retained Earning

3.1.2 Form of Balance Sheet

Assets are resources that have been acquired through transactions, owned or controlled by a business, and have future economic value.

Assets are usually subdivided into current assets and non-current assets.

2. Liabilities

Liabilities are obligations of one business. They are a source of assets and also a claim against assets. Liabilities are presented on the balance sheet by cash equivalent or discounted present value.

会计英语(分录部分)

第二章交易分析和记录1.所有者投资借:现金贷:所有者名下的资本2.用现金采购物料借:物料贷:现金3.用现金购置设备借:设备贷:现金4.赊购物料借:物料贷:应付账款5.提供服务赚取现金借:现金贷:咨询费收入6.用现金支付费用借:租金费用贷:现金7.以赊销方式提供服务和出租设备借:应收账款贷:咨询费收入租金收入8.应收账款变现借:现金贷:应收账款9.分期支付应付账款借:应收账款贷:现金10.所有者提取现金借:所有者提取的资产贷:现金11.预收服务费借:现金Chapter 2Receive investment by OwnerCashOwner, CapitalPurchase Equipment for CashSuppliesCashPurchase Equipment for Cash EquipmentCashPurchase Supplies on CreditSuppliesAccounts PayableProvide Services for CashCashConsulting RevenuePayment of Expense in CashRent ExpenseCashProvide Consulting and Rental Services on Credit Accounts ReceivableConsulting RevenueRental RevenueReceipt of Cash on AccountCashAccounts ReceivablePartial Payment of Accounts Payable Accounts PayableCashWithdrawal of Cash by OwnerOwner, WithdrawalsCashReceipt of Cash for Future ServicesCash贷:预收咨询费收入12.预付保险费借:预收保险费贷:现金第三章调整账户和编制财务报表(一)预付(递延)费用1.调整分录(预付保险费)借:保险费用贷:预付保险费2.调整分录(物料)借:物料费用贷:物料3.调整分录(折旧)借:折旧费用贷:累计折旧——设备(二)预收(递延)收入4.调整分录(预收收入)借:预收咨询费收入贷:咨询费收入(三)应计费用5.调整分录(应付工资费用)借:工资费用贷:应付工资(四)应计收入6.调整分录(应急服务费收入)借:应收账款贷:咨询费收入第四章完成会计循环1.将收入账户的贷方余额结转至利润汇总账户借:咨询费收入租金收入(所有收入账户)贷:利润汇总(结平收入账户)Unearned Consulting RevenuePay Cash for Future Insurance Coverage Prepaid InsuranceCashChapter 3A. Prepaid (Deferred) Expensesa. Adjustment (Prepaid Insurance) Insurance ExpensePrepaid Insuranceb. Adjustment (Supplies)Supplies ExpenseSuppliesc. Adjustment (Depreciation) Depreciation ExpenseAccumulated Depreciation – EquipmentB. Unearned (Deferred) Revenuesd. Adjustment (Unearned Revenues) Unearned Consulting RevenueConsulting RevenueC. Accrued Expensee. Adjustment (Accrued Salaried Expense) Salaries ExpenseSalaries PayableD. Accrued Revenuef. Adjustment (Accrued Services Revenue) Accounts ReceivableConsulting RevenueChapter 4Step 1: Close Credit Balances in Revenue Accounts to Income SummaryConsulting RevenueRental Revenue(Revenue Accounts)Income SummaryTo close revenue accounts.2.将费用账户的借方余额结转至利润汇总账户借:利润汇总贷:折旧费用——设备工资费用保险费用租金费用物料费公共事业费用(所有费用账户)(结平费用账户)3.将利润汇总账户的余额结转至所有者权益账户借:利润汇总贷:所有者名下的资本(结平利润汇总账户)4.将所有者提取账户的余额结转至所有者权益账户借:所有者名下的资本贷:所有者提取的资产(结平所有者提取账户)第五章商业活动的会计核算永续盘存制(一)商品买卖交易(购货)1.购买待售商品借:库存商品贷:现金或应付账款2.支付进货的运费成本(装运地交货)借:库存商品贷:现金3.在折扣期内付款借:应付账款贷:库存商品现金4.记录进货退回或折让借:现金或应付账款贷:库存商品Step 2: Close Debit Balances in Expense Accounts to Income SummaryIncome SummaryDepreciation Expense – Equipment Salaries ExpenseInsurance ExpenseRent ExpenseSupplies ExpenseUtilities Expense(Expense Accounts)To close expense accounts.Step 3: Close Income Summary to Owner’s CapitalIncome SummaryOwner, CapitalTo close Income Summary account.Step 4: Close Withdrawals Account to Owner’s CapitalOwner, CapitalOwner, withdrawalsTo close the withdrawals account.Chapter 5Perpetual Inventory SystemA. Merchandising Transactions (Purchases)a. Purchasing merchandise for resale. Merchandise InventoryCash or Accounts Payableb. Paying freight costs on purchases. (FOB shipping point)Merchandise InventoryCashc. Paying within discount period. Accounts PayableMerchandise InventoryCashd. Recording purchase returns or allowances. Cash or Account Payable Merchandise Inventory(二)商品买卖交易(销货)1.销售商品借:现金或应收账款贷:销售收入借:商品销售成本贷:库存商品2.在折扣期内收到货款借:现金销售折扣贷:应收账款3.接受销售退回或给予销货折让借:销货退回与折让贷:现金或应收账款借:库存商品贷:商品销售成本4.支付销货的运输成本(目的地交货)借:运输费用贷:现金(三)商品交易事项(调整)1.调整存货损耗(当账面余额大于实物盘点额时)借:商品销售成本贷:库存商品(四)商品交易事项(结账)1.结转各临时性账户的贷方余额借:销售收入贷:利润汇总2.结转各临时性账户的借方余额借:利润汇总贷:销售退回与折让销售折扣商品销售成本运输费用其他费用※定期盘存制参见书本147页。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Matching Questions140. Match the following terms the appropriate definition.1. Depreciation expense The accounting system that recognizes revenues when earned and expenses when incurred.2. Time period principleThe accounting system where revenues are recognized when cash is received and expenses arerecorded when cash is paid.3. Profit margin Items paid for in advance of receiving theirbenefits.4. Matchingprinciple Net income divided by net sales.5. Accrued revenuesThe expense created by allocating the cost of plant and equipment to the periods in which theyare used.6. Accrual basis accountingAllocates equal amounts of an asset's cost (less any salvage value) to depreciation expense during itsuseful life.7. Cash basis accounting A principle that assumes that an organization's activities can be divided into specific time periodssuch as months, quarters, or years.8. Prepaid expensesThe principle that requires expenses to be reported in the same period as the revenues that were earned as a result of the expenses.9. Straight-line depreciationRevenues earned in a period that are both unrecorded and not yet received in cash or otherassets.141. Match the following terms with the appropriate definition.1. Adjusted trial balance A balance sheet that lists assets on the left sideand liabilities and equity on the right.2. Adjusting entry A journal entry used at the end of an accounting period to bring an asset or liability account balance to its proper amount and update the related expenseor revenue account.3. Account form balance sheet A listing of accounts and balances preparedbefore adjustments are recorded.4. Accounting periodThe consecutive 12 months (or 52 weeks) selected as the organization's annual accountingperiod.5. Contra account A balance sheet that lists items vertically in theorder: assets, liabilities and equity.6. Unadjusted trial balance The length of time covered by financialstatements.7. Interim financial reports An account linked with another account and having an opposite normal balance.8. Fiscal year Financial reports covering less than one year, usually one, three, or six-month periods.9. Report form balance sheet A listing of accounts and balances prepared after adjustments are recorded and posted to the ledger.10. Natural business year A 12-month period that ends when a company'ssales activities are at their lowest point.Problems1. On December 14 Bench Company received $3,700 cash for consulting services that will be performed in January. Bench records all such prepayments in a liability account. Prepare a general journal entry to record the $3,700 cash receipt.2. On December 31, Connelly Company had performed $5,000 of management services for clients that had not yet been billed. Prepare Connelly's adjusting entry to record these fees earned.3. A company has 20 employees who each earn $500 per week for a 5-day week that begins on Monday. December 31 of Year 1 is a Monday, and all 20 employees worked that day.a) Prepare the required adjusting journal entry to record accrued salaries on December 31, 2009.b) Prepare the journal entry to record the payment of salaries on January 4, 2010.4. Pfister Co. leases an office to a tenant at the rate of $5,000 per month. The tenant contacted Pfister and arranged to pay the rent for December 2009 on January 8, 2010. Pfister agrees to this arrangement.a.) Prepare the journal entry that Pfister must make at December 31, 2009 to record the accrued rent revenue.b.) Prepare the journal entry to record the receipt of the rent on January 8, 2010.5. Prior to recording adjusting entries on December 31, a company's Store Supplies account had an $880 debit balance. A physical count of the supplies showed $325 of unused supplies available as of December 31. Prepare the required adjusting entry.6. Prepare general journal entries on December 31 to record the following unrelated year-end adjustments.a. Estimated depreciation on office equipment for the year, $4,000.b. The Prepaid Insurance account has a $3,680 debit balance before adjustment. An examination of insurance policies shows $950 of insurance expired.c. The Prepaid Insurance account has a $2,400 debit balance before adjustment. An examination of insurance policies shows $600 of unexpired insurance.d. The company has three office employees who each earn $100 per day for afive-day workweek that ends on Friday. The employees were paid on Friday, December 26, and have worked full days on Monday, Tuesday, and Wednesday, December 29, 30, and 31.e. On November 1, the company received 6 months' rent in advance from a tenant whose rent is $700 per month. The $4,200 was credited to the Unearned Rent account.f. The company collects rent monthly from its tenants. One tenant whose rent is $750 per month has not paid his rent for December.如有侵权请联系告知删除,感谢你们的配合!。