《会计专业英语》教材PPT (5)

合集下载

会计专业英语 (5)

Accounting English

Lesson five— accounting cycle

On 1 June 20X8, Jock Heiss commenced trading as an ice cream salesman, using a van which he drove around the streets of his town. (a) He rented the van at a cost of $1,000 for three month. Running expenses for the van averaged $300 per month. (b) He hired a par time helper at a cost of $100 per month. (c) He borrowed $2,000from his bank, and the interest cost of the loan was $25 per month. (d) His main business was to sell ice cream to customers in the street, but he also did some special catering for business customers, supplying ice creams for office parties. Sales to these customers were usually on credit. (e) for the three months to 31 August 20X8, his total sales were as follows: (i) cash sales $8,900 (ii) credit sales $1,100

会计专业英语PPT

Management accounting (next page)

Management accounting:

use both historical data in assisting management daily operations and in planning future operations.

concepts one more time. • Combine both freely but English is more

important.

二 Improve English by ….

– Read textbook in class and after class – Remember new words – Answer questions in exercise is important – Overlook some parts while emphasizing some

• Financial accounting: provides external reports o outsiders, financial information.

2 Reporting management information to internal users

Internal users are senior management-level personnel.

• What do you think?

二 Functions

1 Reporting financial information to outside interested users

• Outside users are:investors,banks and other creditors,government agencies,general publics

Management accounting:

use both historical data in assisting management daily operations and in planning future operations.

concepts one more time. • Combine both freely but English is more

important.

二 Improve English by ….

– Read textbook in class and after class – Remember new words – Answer questions in exercise is important – Overlook some parts while emphasizing some

• Financial accounting: provides external reports o outsiders, financial information.

2 Reporting management information to internal users

Internal users are senior management-level personnel.

• What do you think?

二 Functions

1 Reporting financial information to outside interested users

• Outside users are:investors,banks and other creditors,government agencies,general publics

《会计学专业英语》幻灯片

• Question:

– How to define external users of accounting information?

– Who are external users of accounting information?

– Could the accountant provide accounting information to meet the needs of diverse users?

《会计学专业英语》幻灯 片

本课件PPT仅供大家学习使用 学习完请自行删除,谢谢! 本课件PPT仅供大家学习使用 学习完请自行删除,谢谢!

• Why do you take the course of Accounting English?

• What are the learning objectives of Accounting English?

Accounting: Information for Decision Making

• The primary objective of accounting

– to provide information that is useful for making decisions.

Users of Accounting Information

Internal users of accounting information

• Question:

– Which decisions are to be made by internal users except for management?

External users of accounting information

– How to define external users of accounting information?

– Who are external users of accounting information?

– Could the accountant provide accounting information to meet the needs of diverse users?

《会计学专业英语》幻灯 片

本课件PPT仅供大家学习使用 学习完请自行删除,谢谢! 本课件PPT仅供大家学习使用 学习完请自行删除,谢谢!

• Why do you take the course of Accounting English?

• What are the learning objectives of Accounting English?

Accounting: Information for Decision Making

• The primary objective of accounting

– to provide information that is useful for making decisions.

Users of Accounting Information

Internal users of accounting information

• Question:

– Which decisions are to be made by internal users except for management?

External users of accounting information

《会计专业英语辅导》PPT课件

❖ 2.Most companies have fewer assets accounts than liability account.大多数公 司资产账目比负债账目少。 错

二、判断题〔10分〕

❖ 3.If the number of debit entries in an account is greater than the number of credit entries, the account will have a debit balance.如果借方帐目的数量比贷方工 程的数量大,该帐户将有借方余额。 错

三、简答题〔10分〕

❖ (3) The first-in, first-out method which is often referred to as FIFO, is based upon the assumption thais the first merchandise sold. Each sale is made out of the older goods in stock; the ending inventory therefore consists of the most recently acquired goods.

一、选择题〔40分〕

❖ 3.During a period of rising prices, the inventory method that yields the highest net income and the lowest inventory value, respectively, will be ____D_________.

❖ A. Tangible 有形的 ❖ B. Long-lived ❖ C. Unchanged outlook ❖ D. For resale

二、判断题〔10分〕

❖ 3.If the number of debit entries in an account is greater than the number of credit entries, the account will have a debit balance.如果借方帐目的数量比贷方工 程的数量大,该帐户将有借方余额。 错

三、简答题〔10分〕

❖ (3) The first-in, first-out method which is often referred to as FIFO, is based upon the assumption thais the first merchandise sold. Each sale is made out of the older goods in stock; the ending inventory therefore consists of the most recently acquired goods.

一、选择题〔40分〕

❖ 3.During a period of rising prices, the inventory method that yields the highest net income and the lowest inventory value, respectively, will be ____D_________.

❖ A. Tangible 有形的 ❖ B. Long-lived ❖ C. Unchanged outlook ❖ D. For resale

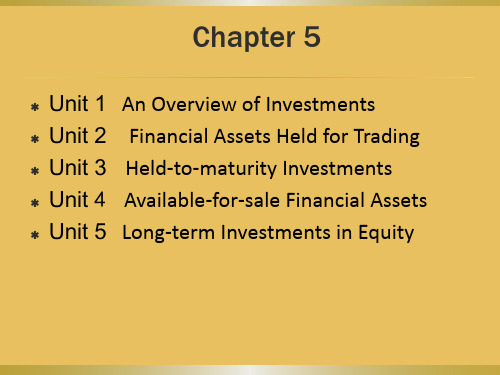

大学课程《会计英语》PPT课件:Chapter 5 Unit 1

Significant influence exists when an investor can influence, but cannot control, the operating and financing policies of the investee.

When the investor holds at least 20%, but not more than 50%, of the voting stock of another company, it is presumed that it has significant influence over the investee company.

Strategic Considerations

Another reason firms invest in the securities of other firms, especially in voting shares, is to develop a beneficial inter-company relationship that will increase the profitability of the investing company, both directly and indirectly. Strategic decisions may be made to invest in suppliers, customers, and even competitors.

Chapter 5

Unit 1 An Overview of Investments Unit 2 Financial Assets Held for Trading Unit 3 Held-to-maturity Investments Unit 4 Available-for-sale Financial Assets Unit 5 Long-term Investments in Equity

When the investor holds at least 20%, but not more than 50%, of the voting stock of another company, it is presumed that it has significant influence over the investee company.

Strategic Considerations

Another reason firms invest in the securities of other firms, especially in voting shares, is to develop a beneficial inter-company relationship that will increase the profitability of the investing company, both directly and indirectly. Strategic decisions may be made to invest in suppliers, customers, and even competitors.

Chapter 5

Unit 1 An Overview of Investments Unit 2 Financial Assets Held for Trading Unit 3 Held-to-maturity Investments Unit 4 Available-for-sale Financial Assets Unit 5 Long-term Investments in Equity

《会计专业英语》教材PPT (6)

Base: (1) Every category of accounts has its nature. Assets, expenses are of debit nature. Liabilities, owner’s equity, revenue are of credit nature. (2) Increases to accounts are recorded on the same side as the nature of the account. And decreases are recorded on the opposite side to the nature of the account.

S t e p s t o f o l l o w t o record transactions with double entry bookkeeping system

Step 1: Determine which two or more accounts will be affected by the transaction; Step 2: For each of the accounts you identify in Step 1, you must determine whether it is an asset, liability, expense or income and so determine their natures; Step 3: For each of the accounts you identify in Step 1, you must judge whether the account increases or decreases and determine whether to debit them or credit them.

会计英语财务会计(ppt版)

executives 高级(gāojí)管理人员

professional judgment

职业判断力

第六页,共八十四页。

ethical standard 道德(dàodé)准那么

integrity 整合性

AICPA

美国(měi ɡuó)注册会计师 协会

第七页,共八十四页。

Chapter 2

第四十六页,共八十四页。

weight average

加权平均

(píngjūn)

第四十七页,共八十四页。

Chapter 7

第四十八页,共八十四页。

accumulated depletion

累计折耗(shéhào)

accumulated depreciation

累计折旧

acquisition cost 取得(qǔdé)本钱

第二十九页,共八十四页。

bad debt recovery 已确认(quèrèn)坏账的收

回

bed debt expense 坏账费用

bank charges 银行(yínháng)手续费

bank credit memorandum

银行贷项通知

第三十页,共八十四页。

bank debit memorandum

closing the accounts

结账

(jié zhànɡ)

closing entry 结账分录

credit balance 贷方余额

第十八页,共八十四页。

debit balance 借方余额

depreciation expense 折旧费用

double-entry accounting

第二十七页,共八十四页。

会计英语教程课件

会计英语教程

9

• dissolve 解散 • cash 现金,现款 • balance 余额,结余;差额;平衡 • amount 金额;合计;共计 • credit 信用;信誉;贷方,贷项 • material 原料,材料,物资 • captial 资本,首都

会计英语教程

10

基本语法

• 非限制性定语从句 • 状语从句 • 宾语从句 • 从句的引导词

会计英语教程

24

基本句型

• It is suggested that • It is ordered that • It is required that

会计英语教程

25

translation

会计英语教程

26

Lesson 11 Inventories

• New words • Inventory 存货 • Costing 成本计算,成本计价 • Cost flow 成本流动 • Inflation 通货膨胀 • Footote 脚注 • Replenish 补充,补足

in order that

会计英语教程

6

翻译课文

会计英语教程

7

Lesson 3 The Accounting System

• 教学步骤: • 复习单词 • 学习新单词、课文 • 翻译

会计英语教程

8

New words,PhraseAnd Special Terms

• affect 影响,感动 • accounting system 会计系统;会计制度 • equity 权益,产权 • debt 债务;借款,欠款 • creditor 债权人,债主 • payable 应付的 • claim 要求权;索赔权

会计英语第5版教学课件lesson5

▪ Interest—the cost of borrowing— accrues with the passage of time.

▪ When companies enter into long-term financing agreements, they may become committed to paying large amounts of interest for many years to come. At any balance sheet date, however, only a small portion of this total interest obligation represents a “liability”.

Notes Payable 10 000 Cash 10 000

▪ Some long-term debts, such as mortgage loans, are payable in a series of monthly or quarterly installments.

▪ In these cases, the principal amount due within one year (or the operating cycle) is regarded as a current liability, and the remainder of the obligation is classified as a long-term liability.

the discount is $10 000 × 7% × 1 period (year) = $700.

the principal is $10 000-$700. `

At the time of issuing the note on May 1st, 2018, the journal entry is Cash 9 300 Discount on Notes Payable 700

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Contents:

Accounts Format of accounts Chart of accounts

Double entry bookkeeping

3.1.1 Introduction to accounts

Business transactions are recorded through accounts. Accounting item is a specific item of six accounting elements

Based on the two equations, other rules are: (1) Every category of accounts has its nature. Assets, expenses are of debit nature. Liabilities, owner’s equity, revenue are of credit nature. (2) Increases to accounts are recorded on the same side as the nature of the account. And decreases are recorded on the opposite side to the nature of the account.

3.1 Accounts源自3.1.2 Format of accounts

example Accounts receivable account is an asset item. Increase in this account is debited, and decrease is credited. At the beginning of January, there’re ¥2,000 balance remained, and following are the changes occur in this account during this month. 10 Jan., increase ¥10,000(Sales on credit).

S t e p s t o f o l l o w t o record transactions with double entry bookkeeping system

Step 1: Determine which two or more accounts will be affected by the transaction; Step 2: For each of the accounts you identify in Step 1, you must determine whether it is an asset, liability, expense or income and so determine their natures; Step 3: For each of the accounts you identify in Step 1, you must judge whether the account increases or decreases and determine whether to debit them or credit them.

3.2 Double Entry Bookkeeping

3.2.2 Rules for double entry bookkeeping

Two equations to be based on: Total Debits = Total Credits

Assets = Liabilities + Owner's Equity

3.2.1 Introduction to double entry bookkeeping

Content: Each business transaction affects at least two accounts. when there’s one account debited, and there will be another accounts equally credited.

12 Jan., increase ¥15,000(Sales on credit).

15 Jan., decrease ¥20,000(customer pay off). 20 Jan., increase ¥5,000(Sales on credit).

At the end of this month, we have a debit balance of ¥5000. The balance will be carried to the next accounting period.

Part 2 Double Entry System

Task 3 Double Entry System

Mini Case:

Mr. Bush set up a business called Bush’s Consultancy Services on 1 January. During the first month, transactions occurred as the following: (1) Investment cash in the business, $50,000; (2) Bought office furniture for cash, $8,000; (3) Bought office supplies on account, $2,000; (4) Received cash from clients for services, $5,000; (5) Paid staff salary with cash, $8,000; (6) Earned professional fees on account, $10,000; (7) Paid cash on account for office supplies, $2,000; (8) Withdraw cash for personal use, $5,000. If you are the accountant of the business, how to start with accounting, how to record these transactions?