cfa-quicksheet-2009

2009年 CFA 一级 Mock试题

1. Which of the following is a key characteristic of the Global Investment Performance Standards (GIPS)? The GIPS standards:A. rely on the integrity of input data.B. consist of required provisions for firms to follow to achieve best practice.C. must be applied with the goal of achieving excellence in performance presentation.Answer: A Global Investment Performance Standards (GIPS) 2009 Modular Level I, Volume 1, pp. 129-130 Study Session 1-4-a Describe the key characteristics of the GIPS standards and the fundamentals of compliance. A key characteristic of the Standards is that the Standards rely on the integrity of input data. The accuracy of input data is critical to the accuracy of the performance presentation2. According to the Standards of Practice Handbook, a member who is an investment manager is least likely to breach his duty to clients by:A. disclosing confidential client information to the CFA Institute Professional Conduct Program.B. using client brokerage to purchase goods or services that are used in the investment decision-making process.C. consistently supporting management’s recommendations by voting with management on proxies related to non-routine governance issues.Answer: B “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, pp. 48-51 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity.3. Carla Scott, CFA, is a portfolio manager for a company that manages investment accounts for wealthy individuals. Scott has no beneficial interest in any of the fee-paying accounts she manages, including her uncle’s account. When shares in initial public offerings (IPOs) become available, Scott first allocates shares to all her other clients for whom the investment is appropriate;only if shares are still available does she pu rchase shares in her uncle’s account, if the issue is appropriate for him. Scott provides each of her clients with full disclosure of her allocation procedures and has received each client’s verbal consent to her allocation procedures. According to the Standards of Practice Handbook, does Scott’s method of allocating oversubscribed IPOs violate any CFA Institute Standards of Professional Conduct?A. No.B. Yes, because she has breached her duty to her uncle.C. Yes, because she has not precleared and rep orted her Uncle’s transactions.Answer: B “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, pp. 50-55, 94-95, 98 (Example 3) Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity. Scott’s method of allocating oversubscribed IPOs discriminates against her uncle, who is a fee-paying client; she violates the Standard related to Fair Dealing. Family accounts that are fee-paying client accounts should be treated like any other firm account. They should neither receive special treatment nor be disadvantaged because of an existing family relationship.4. Kim Li, CFA, is a portfolio manager for an investment advisory firm. Li delegates some of her supervisory duties to Janet Marshall, CFA, after educating Marshall on methods to prevent and detect violations of the firm’s compliance procedures. Despite these efforts, Li discovers that an employee reporting to Marshall may have violated the procedures. According to the Standards of Practice Handbook, Li’s least likely initial course of action must be to:A. suspend the employee.B. increase supervision of Marshall.C. initiate an investigation to determine the extent of the wrongdoing.Answer: A “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, p. 78 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues ofprofessional integrity. A supervisor may delegate supervisory responsibilities, but such delegation does not relieve them of their supervisory responsibility. Once a violation is discovered, a supervisor should: respond promptly; conduct a thorough investigation of the activities to determine the scope of the wrongdoing; and increase supervision or place appropriate limitations on the wrongdoer pending the outcome of the investigation.5. The Standards of Practice Handbook is least likely to require a member to disclose which of the following to clients and prospective clients?A. Underwriting relationships.B. Service on a publicly-traded company’s board of dire ctors.C. Obligation to abide by CFA Institute Code of Ethics and Standards of Professional Conduct.Answer: C “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Vol. 1, pp. 89-92 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity.6. A CFA charterholder is the Fund Manager for a non-profit organization. During a presentation regarding the restructuring of their investment portfolio’s asset allocation, the Head of the Finance Committee questions the manager. As part of his response, the manager states, “I am a CFA charterholder, I know what I’m talking about, you should do what I say”. According to the Standards of Practice Handbook, has the charterholder violated any of the CFA Institute Standards of Professional Conduct?A. No.B. Yes, Responsibilities as a CFA Institute Member.C. Yes, Communication with Clients and Prospective Clients.Answer: B “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, pp. 103-105 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity. Standard VII-B Reference to CFA Institute, the CFA Designation, and the CFA Program under Responsibilities as a CFA Institute Member or CFA Candidate holds that individuals may reference their CFA designation, CFA Institute membership or candidacy in the CFA Program but must not exaggerate the meaning or implications of membership in the Institute, holding the CFA designation, or candidacy in the CFA Program. By inferring that since he is a CFA Charterholder his recommendations are correct exaggerates the implications of holding the CFA designation.7. A CFA candidate was responsible for developing presentations regarding New Vision Asset Managers’ investment process and historical investment perform ance. When the candidate moved to another firm, he brought with him the presentation he developed for New Vision, changed the name of the company and presented it to a client of his new employer. The client asked the candidate if he had New Vision’s permission to use their presentation. The candidate responded, “I created the presentation in my last month working there. It was, after my resignation, so it’s mine to use. Besides the investment performance is what I achieved for my clients at New Vision.” Acc ording to the Standards of Practice Handbook, the CFA candidate is least likely to have violated the CFA Institute Standards of Professional Conduct that relate to:A. Loyalty.B. Misrepresentation.C. Communication with Clients and Prospective Clients.Answer: C “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, pp. 29-30, 69-71, 84-85 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity. It is not evident that the candidate did not disclose the basic format and general principles of the investment processes, use reasonable judgment in identifying which factors are import to their investment recommendations or distinguish between fact andopinion. However, it is evident that the candidate did violate Standard IV(A)-Duties to Employers, Loyalty as the candidate did not act for the benefit of either his former or current employer since the candidate could perceivably have caused harm to both by removing an asset from his former employer and using it at his new employer, which reflects badly on the new employer. In addition, the candidate implied that the performance at New Vision was the performance of his new employer, which is a misrepresentation (Standard I(C)- Professionalism, Misrepresentation) of his new employer’s historical investment performance.8. As the Managing Director of a commercial bank, a CFA charterholder sat in on a board meeting of a publicly listed company that the bank had lent a large sum of money. The purpose of the board meeting was to renegotiate the terms of the commercial loan due to the pending restructuring of the company. The next day all of the Managing Director’s shares of the publicly listed company are sold on the stock exchange, the sell order having been given two days prior to the meeting. According to the Standards of Practice Handbook, the CFA charterholder was least likely in violation of which CFA Institute Standards of Professional Conduct?A. Disclosure of Conflicts.B. Priority of Transactions.C. Material Nonpublic Information.Answer: B “Guidance for Standards I-VII,” CFA Institute 2009 Modular Level I, Volume 1, pp. 36-38, 89-91, 94-95 Study Session 1-2-a Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity. The Candidate did not violate Standard VI(B)-Priority of Transactions as he was only trading on his own account, not those of his clients or employer.。

2009年中国工商银行CFA二级培训项目

10 5--10594䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Published “Security Analysis”(1934): 4 approaches to determine the value of a security based on an analysis of the firm’s income statement and balance sheet.¾Fourth edition of “Security Analysis”(1962): the analyst should estimate a stock’s intrinsic value independent of its market by multiplying earnings power by an appropriate capitalization factor.¾According to Graham and Dodd, investment involved purchasing an asset that was trading at or around its intrinsic value, and the concept that earnings power should provide a “margin of safety”.1. Benjamin Graham and David Dodd’s workLOS 33595䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU2. John Burr Williams’work¾Published “The Theory of Investment Value”(1938)¾Advancing the notion that the value of a stock could be determined by discounting future dividend ¾1962, the modern dividend discount and free cash flow models came outTherefore, the work of these three men forms the framework of fundamental equity analysis.LOS 33Equity InvestmentsReading 34: The Equity Valuation ProcessLOS a.define valuation and discuss the uses of valuation models;b.contrast quantitative and qualitative factors in valuation;c.discuss the importance of quality of inputs in valuation;d.discuss the importance of the interpretation of footnotes to accounting statements and other disclosures;e.calculate alpha;f.contrast the going-concern and non-going-concern assumptions in valuation;g.contrast absolute valuation models to relative valuation models;h.discuss the role of ownership perspective in valuation.598䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDUThe Equity Valuation Process -Framework 1.Valuation2.Quantitative and Qualitative factors in valuation3.Quality of inputs4.Footnotes of accounting statements and other disclosures5.Alpha6.Assumptions7.Models8.Perspectives599䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU1. Valuation¾Definition : estimation of an asset’s value1.based on variables perceived to be related to future investment returns, or2.based on comparisons with closely similar assets ¾Objectives1.Selecting stock2.Estimating market expectations3.Evaluating corporate events4.Fairness opinions5.Evaluating business strategies and modelsmunication among management, shareholders, and analysts7.Assessment of private businessLOS 34.a¾Valuation in portfolio managementplanning, execution and feedback ė3 steps in the portfoliomanagement process (valuation is most closely associated with the planning and execution steps)1.Planning9identification and specification the investment objectives andconstraints ėwriting detail on the investment strategy of securities selection9Valuation on individual security is not apply to Indexing strategybut active management.2.Execution9Portfolio selection9Portfolio implementation 3.Feedback1. ValuationLOS 34.a ¾Valuation process1.Understanding the business;9Industry structure;9Relative competitive position with the industry;9Competitive strategy;9Execution of strategy.2.Forecasting company performance;9Economic forecasting;9Financial forecasting.3.Selecting the appropriate valuation model;9Absolution valuation model;9Relative valuation model.4.Converting forecasts to a valuation;5.Making the investment decision.1. ValuationLOS 34.a602䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU2. Quantitative and qualitative factors in valuation¾Quantitative factorskey source from company’s accounting information and financial disclosuresincluding: balance sheet, income statement, cash flow statement,as well as the footnotes¾Qualitative factorspurpose: to measure industry performance, such as legal and regulatory environmentincluding: quality of the firm’s management team; the transparency of its performance; the analyst’s confidence in the firm’s; industry’s accounting practicesStep 2603䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU3. Quality of inputs¾Quality of inputsanalysts can forecast firm’s future economic value based on current facts¾Requirementthe financial factors must be disclosed in sufficient detail and accuracy the investigation of issues relating to accuracy is often broadly referred to as quality of earnings analysis, namely the scrutiny of all financial statementsStep 24. Footnotes of accounting statements and other disclosuresCategory ObservationExampleRevenues and gainsRecognizing revenue early Accelerating or premature recognition of incomeReclassifying gains and non-operating incomeExpenses and lossesDelay of recognition of expensesExpense recognition and losses Amortization, depreciation, and discount ratesBalance sheet issuesOff-balance-sheet issuesSPEsLOS 34.d ¾Indicators of selected quality of earnings 5. Intrinsic value and alpha¾Intrinsic value is the value of an asset give a hypothetically completeunderstanding of the assets’investment characteristics. Valuation is a part of the active manager’s attempt to production positive excess return.¾Alpha,an excess risk-adjusted return, also called an abnormal return ¾Formula :ex ante alpha = expected holding period return –required return ex post alpha = actual holding period return –contemporaneous required return ¾the difference between intrinsic value (V) and market value (P) ėperceive mispricing ėbecomes part of the manager’s forecast of expected return ėinfluence the total return on the asset ėnamely influence alphaLOS 34.e606䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU6. Assumptions in valuation models¾A company has one value if it is immediately dissolved, and another value if it continues in operation.¾Going-concern assumptionIt is based on the assumption that the company will maintain its business activities into the foreseeable future.going-concern value of the company is the value under a going-concern assumption ¾Non-going-concern assumptionNon-going-concern value is based on the assumption that the company will finish operating and all assets will be sold out.Also called liquidation value due to liquidation should be concerned in this assumption ¾going-concern value ˚liquidation value607䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU7. Types of valuation models¾The two board types of going-concern models of valuation are:Absolute valuation models; and Relative valuation models ¾Absolute valuation modelsthe model that specifies an asset’s intrinsic value which is inorder to be compared with the asset’s market price (does not need consider about the value of other firms). Two types:9Present value model or discounted cash flow model•DDM•FCF model•Residual income model9Asset-based model: sometime is used to value the company that own or control natural resources, such as oilfields, coal deposits and other mineral claims¾Relative valuation models (method of comparable)the model that specifies an asset’s value relative to that of another assetIt is typically implemented using price multiplesFor example: P/E1<P/E2 ėstock is relatively undervalued7. Types of valuation modelsLOS 34.g 8. Issues in valuation model –ownership perspectives¾Criteria for selecting a valuation modelConsistent with the characteristics of the company being valued; Appropriate given the availability and quality of data; andConsistent with the purpose of valuation, including ownership perspective.¾Ownership perspective influence the choice of valuation approach in 3 aspects:Control premiumsMarketability discounts Liquidity discountsLOS 34.h610䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU8. Issues in valuation model –ownership perspectives¾Control premiumsthe ability of controlling ownership position in the company & can determine how the assets of the firm are deployed and financed by making operating and financing decisionthe strong controlling power ėthe shares are more valuable ¾Marketability discountsThe price of non-publicly traded stocks will be discounted due to they can not be as freely traded in a timely manner ¾Liquidity discountsLack of liquidity = lack of marketabilitySuch as the non-publicly-traded shares or the size of the position in relation to its normal trading volume ėthe price will be discountedLOS 34.h611䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDUEquity InvestmentsReading 35: Equity: Market andInstrumentsLOSa.explain the origins of different national market organizations;b.differentiate between an order-driven market and a price-driven market, and explain the risks and advantages of each;c.calculate the impact of different national taxes on the return of an international investment;d.discuss the various components of execution costs (i.e., commissions and fees, market impact, and opportunity cost) and explain ways to reduce execution costs, and discuss the advantages and disadvantages of each;e.describe an American Depositary Receipt (ADR), and differentiate among the various forms of ADRs in terms of trading and information supplied by the listed company;f.explain why firms choose to be listed abroad and calculate the cost tradeoff between buying shares listed abroad and buying ADRs;g.state the determinants of the value of a closed-end country fund;h.discuss the advantages of exchange-traded funds (ETFs) and explain the pricing of international ETFs in relation to their net asset value (NAV);i.discuss the advantages and disadvantages of the various alternatives to direct international investing.Equity: Market and Instruments -Framework 1.Stock exchange basic types 2.Two different markets 3.Tax aspects 4.Execution costs5.Alternatives to direct international investing614䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU1. Stock exchange basic types¾There are 3 types of stock exchanges:Private bourses; Public bourses; and Bankers’bourses¾Private boursesPrivate bourses are established by private individuals and entities for the purpose of securities tradingThere are several private stock exchanges within a country, and they may compete with each otherMixture public regulation (government supervision) and self-regulation Developed from and directly influenced by British exchanges Most popular model today615䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU1. Stock exchange basic types¾Public boursesPublic bourses are public institutions, with brokers appointed by the government and enjoying a monopoly over all transactionsThe brokerage firms gain the fixed commissions, which regulated by government officialNowadays, most public bourses have shifted to private bourses ¾Bankers’boursesIn some countries, the banks are the major, even are the only securities tradersBankers’bourses may be either private or semipublic organizations Usually, they are regulated by government, but sometimes tradingtakes place directly between banks without involving the official bourse at allIn 1990s, most bankers’bourses had developed into private bourses2. Two different markets DifferentiatingFactorsOrder-Driven Market Price-Driven MarketDefinitionAll trades are entered into acentral order book, and neworders are matched with limit orders previously submittedMarket makers stand ready to buy and sell at listed prices Market makers publicly postbid-ask prices to encourage orders MarketsParis Bourse, Frankfurt XETRA, Tokyo Nikkei U.S. NasdaqTypeContinues marketPeriodic call markets to improve liquidityContinues marketTrades occur anytime the market is openElementsElectronic order drivenCentral order book maintainsall limit orders postedAutomated system posts firm quotes by market makers LOS 35.b 2. Two different marketsDifferentiatingFactorsOrder-Driven Market Price-Driven MarketAdvantageTraders view all standingorders, and trades areexecuted via the central orderbookTraders can monitor andprovide liquidity at lower cost High speed and low cost of tradingLittle human intervention Efficient system for small security tradesPurchases are made at the lowest offering price, and sales occur at the highest bid price More efficient for large block trades LOS 35.b618䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU2. Two different markets DifferentiatingFactorsOrder-Driven MarketPrice-Driven MarketDisadvantageTrades quickly due to lack of market depthLack of developed marketmaking requires placing market orders as opposed to limit orders (transparency risk)Both expose traders to the risk of getting “picked off ”or forced to trade at an unattractive priceNo centralized book of limit ordersMarket maker does not know what trades will be generated when posting a quote, which reduces the anonymity of the trade619䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU3. Tax aspects¾Foreign investment may be taxed in 2 locations: investor’s country and investment’s country;¾Taxes are applied in 3 areas:Transaction;Capital gain; and Income.¾Transaction taxestransaction taxes are taxes imposed on tradesMarket makers are usually exempted from these taxes when they trade for their own accountsMost countries have eliminated, or drastically reduced the transaction taxes¾Capital gains taxesCapital gains are taxed in the country where the investor resides Domestic and international investments are taxed the same way¾Income taxThere are the conflict of jurisdiction existed between the two countries The international convention on taxing income is to make certain that taxes are paid by the investor in at least one country, which is why withholding taxes are levied on dividend paymentsThe home country taxes the gross amount of the dividends but gives the investor a tax credit equal to the foreign country withholding ėthe investor pays the percentage tax rate that applies in the investor’s home country ¾With international tax treaties, double taxes between the countries are avoided.3. Tax aspectsLOS 35.c 4. Execution costs¾Execution costs also can be referred to the transaction cost, which includes tangible and intangible trading costs. The costs would reduce the expected returnreduce the benefits from diversification.¾Execution costs compriseCommission, fee and taxes; (tangible costs) Market impact; and (intangible costs)9the difference between the actual execution price and benchmark priceOpportunity costs (intangible costs)9the loss or gain incurred as the result of delay or failure to complete an individual trade¾There is a cost tradeoff between market impact and opportunity costThe slower an order is complete ėhigher opportunity costs, but the market impact cost is lowerExecuting large orders ėhigher market impact costs, but opportunity cost is lowerLOS 35.d622䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU4. Execution costs¾Comparison of 3 execution costs Commissions, fees andtaxes Market impact Opportunity cost paid to brokers for the services Negotiatedexplicit and easily measurable Soft dollarthe size of the impact depends on the order size, market liquidity, and desired execution speed the bid-ask spread is the largest component of the market impact cost in a price-driven markethigher for institutional investors, especially the immediacy tradingare significant for investors usingcrossing networks or order-driven systemnon-execution may lead to high costs sincefailure to fulfill the order can leave the portfolio manager without the security623䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Approaches to reduce execution costs (for large trade)Program trading: managers offer simultaneously a basket of securityfor sale rather than trading stock by stockInternal crossing:managers will attempt to execute the oppositeorder with another client for the same securityExternal crossing:managers use an electronic crossing network(ECN), which matches buy and sell market ordersPrincipal trades:managers find a dealer who acts as a principal totake the opposite side of the order for a firm priceAgency trades:the fund manager finds a broker, who tries to get thebest price. Namely, this broker has ability to reduce total execution costs and the search for the best execution is delegated to the managerIndications of interest (IOI):includes dealers who search the marketfor counterparties willing to engage in an opposing tradeFuture contract usage:managers use future to hedge the risk ofdelay in execution of the large trade4. Execution costs4. Execution costs¾Advantages and disadvantages of the approachesLOS 35.d Approach Advantages DisadvantagesProgram trading less riskysmaller bid-ask quoted higher market impact costs Internal crossing minimizes execute cost non-execution riskExternal crossinglower execution costs assured anonymous It takes long time before an opposite order is entered. Exposed to opportunity cost.Principal trades Assured tradinglower opportunity cost large entire execution cost less anonymity Agency tradesthe best execution minimize the conflictbetween opportunity cost and market impact cost higher commission paid less anonymityIOI low execution cost less anonymity Future contractusagelower opportunity costadditional risk5. Alternatives to direct international investing ¾American Depositary Receipt (ADRs) –conceptForeign shares are deposited with a U.S. bank, which in turn issues ADRs in the name of the foreign company.To avoid unusual share prices, ADRs may represent a combination of several foreign shares; Types9Unsponsored ADR:an ADR program created without the company’s involvement 9Sponsored ADRan ADR program created with the assistance of the foreign companyLOS 35.e626䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Classification of sponsored ADRs.Level Ithe company does not comply with SEC registration and reporting requirements, and the shares can be traded only on the OTC market (but not NASDAQ) ėcan raise capital in the U.S., but it must be done through a private placement Level IIthe company registers with SEC and complies with its reporting requirements. The shares can be listed on an official U.S. stock exchange (NYSE, ASE) or NASDAQ Level IIIthe company’s ADRs are traded on a U.S. stock exchange or NASDAQ and the company may raise capital in the United States through a public offering of the ADRs5. Alternatives to direct international investing627䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Motivations for listed aboardBroader diversificationBroader capital markets exposure Additional advertising opportunitiesConcern over take-overs by domestic competitors is minimized by global diversification of the company’s shares ¾Domestic purchase or ADRsPrice levels, transaction costs, taxes and administrative costs should be major determinants of whichever market the invest chooses. Reading page 79, example 7.5. Alternatives to direct international investing¾Closed-end country fund -concepta closed-end fund that invests in stocks from a single country Motivation9simple way to access the local market and benefit from international diversification9Some countries traditionally restricted foreign investment Closed-end fund market price = NAV + premium, or ( –discount);5. Alternatives to direct international investingLOS 35.g ¾Determinants of value of closed-end country fundForeign investment restrictions:9The stricter the restriction, the higher the premium;9If lift foreign investment restriction, the premium on a local-country fund dropsVolatility of the country fund:9The volatility of premium is larger than that of NAV in developed country funds;9Volatility results that closed-end country fund less attractive toinvest in developed countries. buy open-end funds or buy a portfolio directly on the foreign market in order to avoid the additional volatility of closed-end country fundsCorrelation with U.S. markets:9it was proved that the pricing of country closed-end funds listed in the U.S. are often strongly correlated with U.S. stock market 9the market prices react slowly to changes in NAV ėboth areconsistent with market inefficiency ėneed develop the behavioral finance models to explain.5. Alternatives to direct international investingLOS 35.g630䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Exchange traded funds (ETF)Open-end fund with special characteristics and it traded on stock market;It usually indexing;Allow redemption in a basket of securities or in cash based on NAV. For international ETFs, the effect of non-overlapping time zonesshould be taken into account when comparing the ETF price with NAV. (see example 9 in page 85 of readings)5. Alternatives to direct international investingLOS 35.h631䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU5. Alternatives to direct international investing LOS 35. h& iInstruments AdvantagesDisadvantagesADRseasy and direct approach to invest in some foreign companies lower execution costlimited number of companies have issued ADRsMore costly than directinvestment in foreign market.Closed-end countryfund simple way to accessforeign markets no need to worry aboutredemptionsInferior substitute for direct investment in foreign stock markets.ETFefficiency internationaldiversification for individuals Liquidity with lower cost tax efficiencypractice in active asset allocation strategies not benefits for large institutional investors ¾Comparison of alternatives of foreign investing Equity InvestmentsReading 36: Return ConceptLOSa.distinguish among the following return concepts: holding period return, realized return and expected return, required return, discount rate, the return from convergence of price to intrinsic value (given that price does not equal value), and internal rate of return;b.explain the equity risk premium and its use in required return determination, and demonstrate the use of historical and forward-looking estimation approaches;c.discuss the strengths and weaknesses of the major methods of estimating the equity risk premium;d.explain and demonstrate the use of the capital asset pricing model (CAPM), Fama–French model (FFM), the Pastor–Stambaugh model (PSM), macroeconomic multifactor models, and the build-up method (including bond yield plus risk premium method) for estimating the required return on an equity investment;e.discuss beta estimation for public companies, thinly traded public companies, and nonpublic companies634䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDULOSf.analyze the strengths and weaknesses of the major methods of estimating the required return on an equity investment;g.discuss international considerations in required return estimation;h.explain and calculate the weighted average cost of capital for a company;i.explain the appropriateness of using a particular rate of return as a discount rate, given a description of the cash flow to be discounted and other relevant facts.635䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDUReturn Concept –framework 1.Return concept;2.Equity risk premium;3.Required return on equity;4.Weighted average cost of capital;5.Selecting appropriate discount rate in relation to cash flow.1. Return concepts¾Holding period returnHolding period return is the return earned from investing an asset over a specified time period. The formula:Annualized HPR.¾Realized and expected returnRealized return is the same with HPR. It is backward-looking context. In forward-looking, an investor can form an expectation concerning the dividend and selling price and thereby have an expected return .LOS 36.a return on appreciati price yield dividend 1000P P P P D P P D r H H H H 1. Return concepts¾Required returnIt is the minimum level of expected return that an investor requires in order to invest in the asset over a specific time period, given the assets’riskiness. It represents9the opportunity cost for investing in an assets;9A threshold value for being fairly compensated for the risk of the asset.9If investor’s expected return > required return, the asset is undervalued; and vice versa.Expected alpha (ex ante alpha), is the difference between expected return and required return.9Expected alpha = expected return –required return.Realized alpha = actual HPR –contemporaneous required return.LOS 36.a638䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU1. Return concepts¾Discount rateIt is rated used in finding the PV of a future cash flow;It used to determine the intrinsic value depends on the characteristics of the investment rather than that of purchaser;¾Internal rate of return (IRR)An IRR computed under the assumption of market efficiency has been used to estimate the required return on equity.639䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU1. Return concepts¾Expected return estimates from intrinsic value estimatesWhen a asset is mispriced, price of assets converges to its intrinsic value in a period time. The investor’s expected rate of return comprises:9Required return; and9A return from convergence of price to value.Where,Vo, there intrinsic value of the stock;Po, the current price of the stockr T ,required return during the convergence time period0)(P P V r R E T|2. Equity risk premium¾The equity risk premium is the incremental return (premium) that investors require for holding equities rather than a risk-free asset.Required return on equity = Current expected risk-free return+ Equity risk premiumRequired return on share i = Current expected risk-free return+˟i (Equity risk premium)Required return on share i = Current expected risk-free return+ Equity risk premiums Other risk premium/discounts appropriate for I ¾2 board approaches are used to estimate the ERPHistorical estimate; and Forward-looking estimate.LOS 36.b 2. Equity risk premium¾Historical estimate –conceptual frameworkUse the mean value of differences between index return andgovernment debt return (risk free return, RFR) over selected period; Issues in historical estimate9Select an appropriate index. An index is frequently adjusted. In driving the return, it should be stationary.9Time period. The longer the period used, the more precise the estimate. Precision is irrelevant to splitting into sub-periods.9Arithmetic mean or geometric mean in estimating the return;9Long term bond or short tem bill is an appropriate proxy for the risk-free assets.9Adjustments are usually made to the historical estimate.LOS 36.b642䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Historical estimate –Arithmetic return or geometric return?Arithmetic mean of return is in a sing period context while the geometric mean of return is in multiple period context;The ERP with arithmetic return is usually higher than that with geometric return. But in practice 2 returns are widely used. Arguments for using arithmetic return9It is a single period concept. And most of financial models, such as CAPM, are in single period context.9Statistical argument. The unbiased estimate of the expected terminal value of an investment is found by compounding forward at the arithmetic return.Arguments for using geometric return9It is a multiple periods concept and discounting method is also in multiple context.9Do not introduce bias in calculating of terminal value. The using of geometric return is increasing.643䓉䄖㎕䓵➺➺⭥㵗㧌CopyRight 2009By GFEDU¾Historical estimate –long term or short term risk free return?In choice of proxy for RFR, return on long term bond or short term bill should be considered;The ERP relative to bond is usually lower than that to bill due to normal upward sloping yield curve.The ERP relative to bond produce a more plausible required return in a context of multiple period valuation.In calculating ERP, we should match the duration of RFR measure to the duration of the asset being valued. If the investment is short term, ERP relative to bill could be used.If current YTM on a long term government bond is used to calculate the ERP, we should consider:9The current YTM only reflect current inflation expectation;9Current YTM might be mitigated by liquidity issue.2. Equity risk premium¾Historical estimate –adjustmentsAdjustments are usually made to historical estimate on ERP. There 2 types of adjustments:1.To offset the bias resulting from a series of data being used;2.Take account of an independent estimate; Issues in regarding with adjustments9Survivorship bias. Poor performing companies are removed from index. That results the over-estimate return on index and the ERP. Downward adjustment is used to offset the bias.9Un-expected positive or negative event (outlier) will distort the return on index.LOS 36.b 2. Equity risk premium¾Forward-looking (Ex ante) estimate –conceptual frameworkERP is based on expectations for economic and financial variables from the present going forward. It is logical to estimate ERP directly based on current information and expectation.It is not subject to the issues such as non-stationary or data series in historical estimate. But it is subject to potential errors related to models and behavioral bias. 3 approaches9Gordon growth model (GGM) estimate;9Macroeconomics model estimate; and 9Survey estimate.LOS 36.b。

cfa一级计划表

cfa一级计划表CFA一级计划表CFA(Chartered Financial Analyst,特许金融分析师)是全球范围内最为知名和有影响力的金融资格认证之一。

它由国际特许金融分析师协会(CFA Institute)颁发,被誉为金融界的"黄金学位"。

CFA一级是CFA考试的起点,也是最基础的一级,考察金融和投资的基本知识和技能。

为了帮助考生进行系统的备考,制定一份合理的CFA一级计划表是非常重要的。

一、确定备考时间确定备考时间是制定计划表的第一步。

考生可以根据个人情况和学习能力,大致规划出备考的时间段。

一般来说,备考时间建议控制在4-6个月左右,这样可以保证充足的时间复习和巩固知识。

二、确定备考阶段和分配时间备考CFA一级可以分为三个阶段:基础知识学习、习题练习和模拟考试。

根据考试大纲,将各个知识点分配到不同的阶段,制定出具体的备考计划。

1. 基础知识学习阶段(约2-3个月)在这个阶段,考生需要系统地学习CFA一级的各个知识点。

根据考试大纲,将各个主题按照重要性和难度进行排序,合理安排每个主题的学习时间。

每天安排2-3个小时的学习时间,将重点放在理解概念和原理上,掌握基础知识。

2. 习题练习阶段(约1-2个月)在基础知识学习阶段结束后,考生需要进行大量的习题练习,提高解题能力和应试技巧。

根据每个主题的重要性和难度,逐步增加习题的难度。

每天安排2-3个小时的习题练习时间,将重点放在解题思路和答题技巧上。

3. 模拟考试阶段(约1个月)在距离考试前一个月左右,考生需要进行模拟考试,检验自己的备考效果。

可以选择一些官方出版的模拟试题或者在线模拟考试平台进行模拟考试。

每周进行一次全真模拟考试,并在考后进行详细的答案解析和错题总结。

三、每周安排在制定计划表时,还需要将每周的学习时间进行具体的安排。

根据个人情况和实际时间安排,将每周的学习时间划分为不同的阶段,并设定每天的学习目标。

在每周的计划中,可以适当安排一天或半天的休息时间,让自己得到充分的休息和放松。

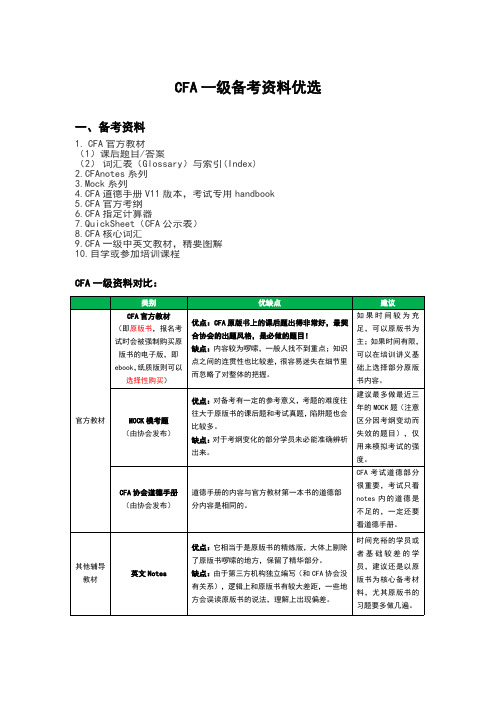

CFA考试备考常用资料

CFA考试备考常用资料(CFA必备)1.CFA官方教材CFA考试官方教材有两种,一种是电子版e-book,一种是纸质版2.Study Notes是备考CFA一级明确、高效的学习补充资料.3.CFA Quicksheet买Notes一般会送Quicksheet,quick如其名,就是用来偷懒的表.三张A4纸正反面布满了一些比较general的公式,但很不全,真正齐全的公式表是Notes最后的几页Formulas 4.handbook道德手册考试只看study notes内的道德是不足的,一定还要看道德手册5.MOCK系列临近考试做一些mock exam非常有必要.6.CFA官方考纲每年的CFA考纲都是会发生一些变化的7.CFA指定计算器CFA协会指定了两款计算器供考生选择,分别是TI BAII PLUS 以及HP12C,普通版和专业版均可,TI BAII PLUS在中国的使用率远远超过HP12C.其他型号的计算器均不得带入CFA考场!8.CFA核心词汇CFA核心词汇是依照CFA协会颁布的最新CFA考试大纲和指定教材编写9.CFA题库原版教材、历年模拟考题、notes考题和知识点梳理紧贴CFA考试大纲让每位学员顺利通关!中博课程9大特点高效学习科学备考面授、直播、网课同步学习汇聚300+名师教研心血,支持多方学习双语教学模式全球一流的中英双语CFA课程全天候高品质答疑专业学服团队跟踪服务,随时解答疑虑专属学习计划一步到位搞定听学练测,直面通关独家官方教材为学生提供原汁原味且由官方认证的原版教材配备外教讲师中博联合Wiley组建了强大外教讲师团队免费重修任意科目不过,免费重修学游一体服务学员面授课程皆可选择中博任意CFA开课的分部学习。

奖学金机制参加中博任意形式的培训课程而通过的,且满足申请条件,均可申领中博奖Wiley与中博教育的合作通过与Wiley的强强联合,优势互补,共谋发展,从而为中博的学员提供更专业的知识和更优质的服务。

CFA二级公式表

^

H0 : b 0 ˆ t b , df n k 1 sb

Reject h0 if | t | critical t or p-value <

ˆ (t s ) Confidence Interval: b j c bj

Currency appreciates due to: (1) Lower relative income growth rate. (2) Lower relative inflation rate. (3) Higher domestic real interest rate. (4) Improved investment climate. 9. Unanticipated shift to exp. Monetary Policy: Higher income, accelerated inflation, lower real interest rates, leads to currency dept, current acct surplus, and financial acct deficit. 10. Unanticipated shift to exp. Fiscal Policy: currency appr, current acct deficit, & financial account surplus. 11. Purchasing Power Parity: Law of one price: a single, clearly comparable good should have same real price in all countries. Relative PPP: Countries with high inflation rates should see their currencies depreciate.

2019年金融分析师考试必备资料CFA 2019 - Level 1 Schweser's Quicksheet

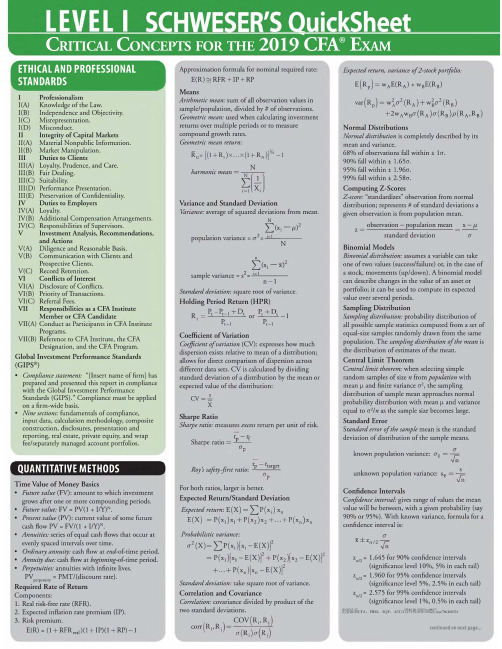

/C r it ic a l C o n c e pt s f o r t h e2019C F A®E x a mETHICAL AND PROFESSIONAL STANDARDSI Professionalism1(A) KnowledgeoftheLaw.1(B) IndependenceandObjectivity.1(C) Misrepresentation.1(D) Misconduct.II IntegrityofCapitalMarkets11(A) Material Nonpublic Information.11(B) Market Manipulation.III DutiestoClientsIII (A) Loyalty, Prudence, and Care.III(B) Fair Dealing.III(C) Suitability.III(D) Performance Presentation.III(E) Preservation of Confidentiality.IV DutiestoEmployersIV(A) Loyalty.IV(B) Additional Compensation Arrangements. IV(C) Responsibilities of Supervisors.V InvestmentAnalysis,Recommendations, and ActionsV(A) Diligence and Reasonable Basis.V(B) Communication with Clients andProspective Clients.V(C) Record Retention.VI ConflictsofInterestVI(A) Disclosure of Conflicts.VI (B) Priority of T ransactions.VI(C) Referral Fees.VII Responsibilities as a CFA InstituteMember or CFA CandidateVII(A) Conduct as Participants in CFA Institute Programs.VII(B) Reference to CFA Institute, the CFADesignation, and the CFA Program. Global Investment Performance Standards (GIPS®)• Compliance statement: “[Insert name of firm] has prepared and presented this report in compliance with the Global Investment PerformanceStandards (GIPS).” Compliance must be applied on a firm-wide basis.• Nine sections: fundamentals of compliance,input data, calculation methodology, composite construction, disclosures, presentation andreporting, real estate, private equity, and wrapfee/separately managed account portfolios. QUANTITATIVE METHODSTime Value of Money Basics• Future value (FV): amount to which investment grows after one or more compounding periods.• Future value: FV = PV(1 + I/Y)N.• Present value (PV): current value of some futurecash flow PV - FV/(1 + I/Y)N.• Annuities: series of equal cash flows that occur at evenly spaced intervals over time.• Ordinary annuity: cash flow at end-oFume. period.• Annuity due: cash flow at beginning-of-time period.• Perpetuities: annuities with infinite lives.PV .=PMT/(discountrate).perpetuity vRequired Rate of ReturnComponents:1.Real risk-free rate (RFR).2.Expected inflation rate premium (IP).3.Risk premium.E(R) = (1 + RFRreal)(l + IP)(1 + RP) — 1Approximation formula for nominal required rate:E(R) = RFR + IP + RPMeansArithmetic mean: sum of all observation values insample/population, divided by # of observations.Geometric mean: used when calculating investmentreturns over multiple periods or to measurecompound growth rates.Geometric mean return:Y*Rc=[(l + R1)x...x(l + RN)]/N — 1harmonic mean =NNEi=l,x[,Variance and Standard DeviationVariance: average of squared deviations from mean.N£(Xi—M)2population variance = cr2= —--------------NnE(x i-x)2sample variance = s =2 i=ln — 1Standard deviation: square root of variance.Holding Period Return (HPR)R P r-Pr-t+D ror _!Pt-1Pt-1Coefficient of V ariationCoefficient o f v ariation (C V): expresses how muchdispersion exists relative to mean of a distribution;allows for direct comparison of dispersion acrossdifferent data sets. CV is calculated by dividingstandard deviation of a distribution by the mean orexpected value of the distribution:CV = =XSharpe RatioSharpe ratio: measures excess return per unit of risk.c, •rP-r fbnarpe ratio = —------a…Roy's safety-first ratio:rp ^targetFor both ratios, larger is better.Expected Return/Standard DeviationExpected return: E(X) = ^^P(x j) xnE(X) =P(x1)x1+P(x2)x2+... + P(xn)x nProbabilistic variance:^2(x)=E p(xi)h-E(x)f= P(x1)[x1-E(X)f + P(x2)[x2-E(X)]:+ ... + P(xn)[x…—E(x)fStandard deviation: take square root of variance.Correlation and CovarianceCorrelation: covariance divided by product of thetwo standard deviations.corr R^R: =COV (Rj, RjExpected return, variance o f2-stock portfolio.E(R P) = w a E(Ra) +w b E(Rb)var(R p) = w2cr2(R A) + w2cr2(R B)+2w Aw B cr(RA)cr(R B)p(R A,R B)Normal DistributionsNormal distribution is completely described by itsmean and variance.68% of observations fall within ±I ct.90% fall within ±1.65a.95% fall within ±1.96a.99% fall within ± 2.58a.Computing Z-ScoresZ-score: “standardizes” observation from normaldistribution; represents # of standard deviations agiven observation is from population mean.observation — population meanz =x —flstandard deviation aBinomial ModelsBinomial distribution: assumes a variable can takeone of two values (success/failure) or, in the case ofa stock, movements (up/down). A binomial modelcan describe changes in the value of an asset orportfolio; it can be used to compute its expectedvalue over several periods.Sampling DistributionSampling distribution: probability distribution ofall possible sample statistics computed from a set ofequal-size samples randomly drawn from the samepopulation. The sampling distribution o f t he mean isthe distribution of estimates of the mean.Central Limit TheoremCentral lim it theorem: when selecting simplerandom samples of size n from population withmean p and finite variance a2, the samplingdistribution of sample mean approaches normalprobability distribution with mean p and varianceequal to a1 In as the sample size becomes large.Standard ErrorStandard error o f t he sample mean is the standarddeviation of distribution of the sample means.known population variance: a^ =aunknown population variance: s* =Confidence IntervalsConfidence interval: gives range of values the meanvalue will be between, with a given probability (say90% or 95%). With known variance, formula for aconfidence interval is:x ± zaa llZ aJ2Z =a llZ =a ll1.645 for 90% confidence intervals(significance level 10%, 5% in each tail)1.960 for 95% confidence intervals(significance level 5%, 2.5% in each tail)2.575 for 99% confidence intervals(significance level 1%, 0.5% in each tail)continued on next page...需要最新CFA、FRM、AQF、ACCA资料欢迎添加微信zyz786468331QUANTITATIVE METHODS continued...Null and Alternative HypothesesNull hypothesis (H{)): hypothesis that contains the equal sign (=, <, >); the hypothesis that is actually tested; the basis for selection of the test statistics. Alternative hypothesis (Ha): concluded if there is sufficient evidence to reject the null hypothesis. Difference Between One- and Two-Tailed Tests One-tailed test: tests whether value is greater than or less than a given number.Two-tailed test: tests whether value is equal to a given number.• One-tailed test: H0: p < 0 versus Ha: p > 0.• Two-tailed test: H0: p = 0 versus Ha p * 0.Type I and Type II Errors• Type I error: rejection of null hypothesis when it is actually true.• Type II error: failure to reject null hypothesis when it is actually false.Types of Hypothesis TestsUse t-statistic for tests involving the population mean (location of mean, difference in means, paired comparisons).Use chi-square statistic for tests of a single population variance.Use F-statistic for tests comparing two population variances.Technical AnalysisReversal p atterns: head and shoulders, inverse H&S, double/triple top or bottom.Continuation patterns: triangles, rectangles, pennants, flags.Price-based indicators: moving averages, Bollinger bands, momentum oscillators (rate of change, RSI, stochastic, MACD).Sentiment indicators: opinion polls, put/call ratio, VIX, margin debt, short interest ratio.Flow o f f unds indicators: TRIN, margin debt, mutual fund cash position, new equity issuance, secondary offerings.ECONOMICS1 ElasticityOwn price elasticity %A quantity demanded%A priceIf absolute value >1, demand is elastic.If absolute value <1, demand is inelastic.On a straight line dem and curve, total revenue is maximized where price elasticity = —1.%A quantity demanded%A incomeIf positive, the good is a normal good.If negative, the good is an inferior good.....%A quantity demanded Cross p rice elasticity=---------------------------------%A price of related goodIf positive, related good is a substitute.If negative, related good is a complement. Breakeven and ShutdownBreakeven: total revenue = total cost.Operate in short run if total revenue is greater than total variable cost but less than total cost.Shut down in short run if total revenue is less than total variable cost.Income elasticityMarket StructuresPerfect competition: Many firms with no pricing power; very low or no barriers to entry; homogeneous product.M onopolistic competition: Many firms; some pricing power; low barriers to entry; differentiated products; large advertising expense.Oligopoly: Few firms that may have significantpricing power; high barriers to entry; products maybe homogeneous or differentiated.Monopoly: Single firm with significant pricingpower; high barriers to entry; advertising used tocompete with substitute products.In all market structures, profit is maximized atthe output quantity for which marginal revenue =marginal cost.Gross Domestic ProductReal GDP = consumption spending + investment +government spending + net exports.Savings, Investment, Fiscal Balance, and TradeBalanceFiscal budget deficit (G - T) = excess of saving overdomestic investment (S - I) - trade balance (X - M)Equation of ExchangeMV = PY, where M = real money supply, V =velocity of money in transactions, P = price level,and Y = real GDP.Business Cycle PhasesExpansion; peak; contraction; trough.Economic IndicatorsLeading: Turning points occur ahead of peaks andtroughs (stock prices, initial unemployment claims,manufacturing new orders)Coincident: Turning points coincide with peaksand troughs (nonfarm payrolls, personal income,manufacturing sales)Lagging: Turning points follow peaks and troughs(average duration of unemployment, inventory/sales ratio, prime rate)Factors Affecting Aggregate DemandConsumers’ wealth; business expectations;consumers’ income expectations; capacityutilization; monetary and fiscal policy; exchangerates; global economic growth.Factors Affecting SR Aggregate SupplyInput prices; labor productivity; expectations foroutput prices; taxes and subsidies; exchange rates;all factors that affect LR aggregate supply.Factors Affecting LR Aggregate SupplySize of labor force; human capital; supply ofnatural resources; stock of physical capital; level oftechnology.Typ e s of UnemploymentFrictional: time lag in matching qualified workerswith job openings.Structural: unemployed workers do not have theskills to match newly created jobs.Cyclical: economy producing at less than capacityduring contraction phase of business cycle.Policy Multipliersmoney multiplier =-------------------------reserve requirementfiscal multiplier =--------------------l-M P C(l-t)where MPC = marginal propensity to consume,t = tax rate.Expansionary and Contractionary PolicyM onetary policy is expansionary when the policyrate is less than the neutral interest rate (real trendrate of economic growth + inflation target) andcontractionary when the policy rate is greater thanthe neutral interest rate.Fiscal p olicy is expansionary when a budgetdeficit is increasing or surplus is decreasing, andcontractionary when a budget deficit is decreasingor surplus is increasing.Balance of PaymentsCurrent account: merchandise and services; incomereceipts; unilateral transfers.Capital account: capital transfers; sales/purchases ofnonfinancial assets.Financial account: government-owned assetsabroad; foreign-owned assets in the country.Regional Trading AgreementsFree trade area: Removes barriers to goods andservices trade among members.Customs union: Members also adopt common tradepolicies with non-members.Common market: Members also remove barriers tolabor and capital movements among members.Economic union: Members also establish commoninstitutions and economic policy.M onetary union: Members also adopt a commoncurrency.Foreign Exchange RatesFor the exam, FX rates are expressed as pricecurrency / base currency and interpreted as thenumber of units of the price currency for each unitof the base currency.Real Exchange Ratebase currency CPI= nominal FX rate Xprice currency CPI yNo-Arbitrage Forward Exchange Rateforward 1 + price currency interest ratespot 1 + base currency interest rateExchange Rate RegimesFormal dollarization: country adopts foreigncurrency.M onetary union: members adopt common currency.Fixed p eg: ± 1 % margin versus foreign currency orbasket of currencies.Target zone: Wider margin than fixed peg.Crawling p eg: Pegged exchange rate adjustedperiodically.Crawling bands: Width of margin increases overtime.M anaged f loating: Monetary authority acts toinfluence exchange rate but does not set a target.Independently f loating: Exchange rate is market-determined.F in a n c ia l r e p o r t in g a n d.ANALYSISRevenue RecognitionTwo requirements: (1) completion of earningsprocess and (2) reasonable assurance of payment.Revenue Recognition Methods• Percentage-of-completion method.• Completed contract method.• Installment sales.• Cost recovery method.Converged Standards Issued May 2014Five-step revenue recognition model:1. Identify contracts2.Identify performance obligations3.Determine transaction price4.Allocate price to obligations5.Recognize when (as) obligations are satisfiedUnusual or Infrequent Items• Gains/losses from disposal of a business segment.• Gains/losses from sale of assets or investments insubsidiaries.• Provisions for environmental remediation.continued on next page...需要最新CFA、FRM、AQF、ACCA资料欢迎添加微信zyz786468331FINANCIAL REPORTING AND ANALYSIS continued...•Impairments, write-offs, write-downs, and restructuring costs.•Integration expenses associated with businesses recently acquired.Discontinued OperationsTo be accounted for as a discontinued operation, a business—assets, operations, investing, financing activities—must be physically/operationally distinct from rest of firm. Income/losses are reported net of tax after net income from continuing pute Cash Flows From Operations (CFO)Direct method : start with cash collections (cash equivalent of sales); cash inputs (cash equivalent of cost of goods sold); cash operating expenses; cash interest expense; cash taxes.Indirect method: start with net income, subtracting back gains and adding back losses resulting from financing or investment cash flows, adding back all noncash charges, and adding and subtracting asset and liability accounts that result from operations.Free Cash FlowFree cash flow (FCF) measures cash available for discretionary purposes. It is equal to operating cash flow less net capital expenditures.Critical RatiosCommon-size financial statement analysis:•Common-size balance sheet expresses all balance sheet accounts as a percentage of total assets.•Common-size incom e statement expresses all income statement items as a percentage of sales.•Common-size cash flow statement expresses each line item as a percentage of total cash inflows (outflows), or as a percentage of net revenue.Horizontal common-size f inancial statement analysis: expresses each line item relative to its value in a common base period.Liquidity ratios:current assetscurrent ratio =------------—7-77—current liabilitiescash + marketable securities + receivablescurrent liabilities cash + marketable securitiescurrent liabilities.... . cash + mkt. sec. + receivables defensive interval =--------------------------------------daily cash expendituresReceivables, inventory, payables turnover, and days'supply ratios—all o f w hich are used in the cash conversion cycle:. . . annual sales receivables turnover =------------------------quick ratio =cash ratio =inventory turnover =average receivables cost of goods sold average inventorypayables turnover ratio =purchases average trade payables days of sales outstanding =365days of inventory on hand = 7receivables turnover365number of days of payables =inventory turnover 365payables turnover ratiocash conversion cycle =days of inventoryon hand+days of sales number of days outstandingof payablesTotal asset, fixed-asset, and working capital turnover ratios:total asset turnover =revenueaverage total assets fixed asset turnover =revenue average fixed assetsworking capital turnover =revenueaverage working capitalGross, operating, and net p rofit margins:f, . gross profit gross profit margin = --------------revenue. operating profit EBIToperating profit margin =--------------------—revenue net sales net income net profit margin =revenueReturn on assets [return on total capital (ROTC)J:return on assets _ EBIT(total capital) average total capital Debt to equity ratio and total debt ratio:total debt debt-to-equity ratio =total equitytotal-debt-ratio =total debt total assetsInterest coverage andfix ed charge coverage:EBITinterest coverage = 7interestf, . .EBIT +lease paymentsfixed charge coverage = --------------------1------------interest + lease paymentsGrowth rate (g): g = RR x ROEdividends declaredretention rate — 1 —operating income after taxesLiquidity ratios indicate company’s ability to pay its short-term liabilities.Operating p erform ance ratios indicate how well management operates the business.DuPont AnalysisTraditional DuPont equation:return on equity =net income salesassetsk salesk assets,, equity,net profit asset equity margin turnover /multiplierYou may also see it presented as:return on equity =Extended DuPont equation further decomposes net profit margin:ROE =net income v ' EBT v ' EBIT 'EBT /A EBIT V /Arevenue xrevenue v avg. total assets avg. total assets A avg. equityYou may also see it presented as:ROE = tax burden x interest burden xEBIT margin x asset turnover x leverage Marketable Security ClassificationsHeld-for-trading: fair value on balance sheet; dividends, interest, realized and unrealized G/L recognized on income statement.Available-for-sale: fair value on balance sheet; dividends, interest, realized G/L recognized on income statement; unrealized G/L is other comprehensive income.Held-to-maturity: amortized cost on balancesheet; interest, realized G/L recognized on income statement.Inventory AccountingIn periods of rising prices and stable or increasing inventory quantities:LIFO results in: FIFO results in:Higher COGS Lower COGS Lower gross profit Higher gross profit Lower inventory Higher inventory balances balances Basic and Diluted EPSBasic EPS calculation does not consider effects of any dilutive securities in computation of EPS:net income — preferred dividends basic EPS =wtd. avg. no. of common shs. outstanding ... . adj. income avail, for common sharesdiluted EPS =------------------------------------------------—wtd. avg. common shares plus potentialcommon shares outstanding Therefore, diluted EPS is:net _ pfd income div convertible +preferred +dividends convertible'debt interest(1-t)wtdshares from sh ’ s from shares aw sh s +conversion of conv. pfd. sh’s +conversion conv. debt +issuable from stock options Long-Lived Assets Capitalizing vs. Expensing Capitalizing: lowers income variability andincreases near-term profits. Increase assets, equity. Expensing: opposite effect.Depreciationcost — residual valueStraight-line: ----------------------------useful lifeDouble declining balance:(cost — accum. depreciation)V useful life /Units o f p roduction:cost — salvage value * •useful life in unitsx output unitsRevaluation of Long-Lived AssetsIFRS: revaluation gain recognized in net income only to the extent it reverses previously recognized impairment loss; further gains recognized in equity as revaluation surplus. (For investment p roperty, all gains and losses from marking to fair value are recognized as income.)U.S. GAAP: revaluation is not permitted.Deferred Taxes•Created when taxable income (on tax return) ^pretax income (on financial statements) due to temporary differences.• D eferred tax liabilities are created when taxable income < pretax income. Treat DTL as equity if not expected to reverse.• D eferred tax assets are created when taxable income > pretax income. Must recognize valuation allowance if more likely than not that DTA will not be realized.Long-Term Liabilities• Premium bond: coupon rate > market rate at issuance.• Discount bond: coupon rate < market rate at issuance.• Interest expense equals book value at the beginning of the year multiplied by the market rate of interest at the time the bonds were issued.需要最新CFA 、FRM 、AQF 、ACCA 资料欢迎添加微信zyz786468331FINANCIAL REPORTING AND ANALYSIS continued.• •LeasesFinancial statement/ratio impact of lease accounting from the lessee perspective: capital leases result in:• Higher: assets, liabilities, CFO, debt/equity.• Lower: net income (early years), CFF, currentratio, working capital, asset turnover, ROA,ROE.• Same: total cash flow.PensionsD efined contribution: employer contribution expensed in period incurred.D efined benefit: overfunded plan recognized as asset, underfunded plan recognized as liability. CORPORATE FINANCEWeighted Average Cost of CapitalWACC = (wd)[kd(l-t)] + (wps)(kps) + (wce)(ks) Cost of Preferred StockPCost of Equity Capital■D,k« = y i+si0Cost of Equity Using CAPMk c= RFR + /}(Rm kl - RFR)Capital BudgetingNPV - CF0 + CFl . + CFz …+...+CFn(1 + k)1(1 + k):(1 + k)n IRR: discount rate that makes NPV equal to zero.Pure-Play Method Project BetaDelevered asset beta for comparable company:13a sset Passet ^equity X1 +(1-0DRelevered project beta for subject firm:DP nroiecr ^project asset Xi+(i-t)Measures of LeverageTotal leverage: percent change in net income from a given percent change in sales. Operating leverage: percent change in EBIT from a given percent change in sales.Financial leverage: percent change in net income from a given percent change in EBIT.breakeven quantity of sales =fixed operating & financing costsprice — variable costs per unitoperating breakeven quantity of sales =fixed operating costsprice — variable costs per unitWorking Capital ManagementPrimary sources ofiliquidity, cash balances,short-term funding, cash flow management of collections and payment.Secondary sources o f l iquidity, liquidating assets, negotiating debt agreements, bankruptcy protection.Cost of trade credit:1 +% discountl-% discount365days past discountCorporate GovernanceOne-tier board: Includes internal and externaldirectorsTwo-tier board: Supervisory board of externaldirectors, management board of internal directorsBoard committees:Audit: Financial reportingGovernance: Legal and ethics complianceNominations: Find Board candidatesRemuneration: Compensation for senior managersRisk: Firm risk tolerance and risk managementInvestment: Review large capital projects, assetpurchases, asset salesPORTFOLIO MANAGEMENTInvestment Policy StatementInvestment objectives:• Return objectives.• Risk tolerance.Constraints:• Liquidity needs.• Time horizon.• Tax concerns.• Legal and regulatory factors.• Unique needs and preferences.Combining Preferences with the Optimal Set ofPortfoliosMarkowitz efficient frontier is the set of portfoliosthat have highest return for given level of risk.Security Market Line (SML)Investors should only be compensated for riskrelative to market. Unsystematic risk is diversifiedaway; investors are compensated for systematic risk.The equation of the SML is the CAPM, which is areturn/systematic risk equilibrium relationship.total risk = systematic + unsystematic riskCAPM : E(R j) = RFR + (3- [E(Rmkt) - RFR]E(R.)The SML and EquilibriumIdentifying mispriced stocks:Consider three stocks (A, B, C) and SML.Estimated stock returns should plot on SML.• A return plot over the line is underpriced.• A return plot under the line is overpriced.E(R)Risk-Adjusted ReturnsSharpe ratio and M-squared measure excess returnper unit of total risk.Treynor measure and Jensens alpha measure excessreturn per unit of systematic risk.E(R)SECURITIES MARKETS,& EQUITY INVESTMENTSWell-Functioning Security Markets• Operational efficiency (lowest possibletransactions costs).• Informational efficiency (prices rapidly adjust tonew information).Margin PurchasesFor margin transactions:• Leverage factor =1 /margin percentage.• Levered return = HPR x leverage factor.Margin Call PriceP0 (1 — initial margin %)1 — maintenance margin%需要最新CFA、FRM、AQF、ACCA资料欢迎添加微信zyz786468331Securities Markets & Equity Investments continued... Computing Index Prices… . . , . T . stock pricesPrice-weighted Index =—-----------—----adjusted divisorValue-weighted Index^(current prices) (#shares)=-------------------^---------------------------X base valueXXbase year prices) (#base year shares)Types of OrdersExecution instructions: how to trade; e.g., market orders, limit orders.Validity instructions: when to execute; e.g., stop orders, day orders, fill-or-kill orders.Clearing instructions: how to clear and settle; for sell orders, specify short sale or sale of owned security. Market StructuresQuote-driven markets: investors trade with dealers. Order-driven markets: buyers and sellers matchedby rules.Brokered markets: brokers find counterparties. Forms of EMH• Weak f orm.Current stock prices f u lly reflectavailable security market info. Volumeinformation/past price do not relate to futuredirection of security prices. Investor cannotachieve excess returns using tech analysis.• Semi-strong f orm. Security prices instantly adjustto new public information. Investor cannot achieve excess returns using fundamental analysis.• Strong f orm. Stock prices fu lly reflect allinformation f rom public and p rivate sources.Assumes perfect markets in which all informationis cost free and available to everyone at the sametime. Even with inside info, investor cannotachieve excess returns..EQUITY INVESTMENTSIndustry Life Cycle StagesEmbryonic: slow growth, high prices, large investment needed, high risk of failure.Growth: rapid growth, falling prices, limited competition, increasing profitability.Shakeout: slower growth, intense competition, declining profitability, cost cutting, weaker firmsfail or merge.Mature: slow growth, consolidation, stable prices, high barriers to entry.Decline: negative growth, declining prices, consolidation.Five Competitive Forces1.Rivalry among existing competitors.2.Threat of entry.3.Threat of substitutes.4.Power of buyers.5.Power of suppliers.One-Period Valuation ModelP i(l+ kc)Be sure to use expected dividend Dj in calculation. Infinite Period Dividend Discount Models Supernormal g rowth m odel (multi-stage) DDM:V… =D,(1 +k_)++ D-+n(i+k e)n a+k erwhere: P… =D n+l" (k.-g e) Constant growth model:y=Do(1 + gc)=Di0 ke“gc ke~gc Critical relationship between k and g:•As difference between k and g c widens, value ofstock f alls.•As difference narrows, value of stock rises.•Small changes in difference between k and gcause large changes in stock’s value.Critical assumptions of infinite period DDM:•Stock pays dividends; constant growth rate.•Constant growth rate, g> never changes.• k must be greater than g c (or math will not work)Earnings Multiplier ModelDioEj k-payout ratiok^Price Multiplesleading P/E =price per sharetrailing P/E =forecast EPS next 12 mo,price per shareEPS previous 12 mo.P/B =P/S =price per sharebook value per shareprice per sharesales per shareP/CF =price per sharecash flow per shareFIXED INCOMEBasic Features of BondsIssuer. Sovereign, non-sovereign, quasi-government,supranational, corporate, SPE.Maturity. Money market (one year or less); capitalmarket (greater than one year).Par value. Bond’s principal value (face value).Coupon. Annual percent of par; fixed or floating.Divide by periodicity to get periodic rate.Currency. Single, dual, currency option.Indenture. Affirmative and negative covenants.Price, Yield, Coupon RelationshipsBond prices and yields are inversely related.Increase in yield decreases price; decrease in yieldincreases price.Coupon < yield: Discount to par value.Coupon > yield: Premium to par value.Constant-yield p rice trajectory: Price approachespar as bond nears maturity from amortization ofdiscounts and premiums. Capital gains and lossesare calculated relative to this trajectory.Cash Flow StructuresBullet: All principal repaid at maturity.Fully amortizing: Equal periodic payments includeboth interest and principal.Partially amortizing: Periodic payments includeinterest and principal, balloon payment at maturityrepays remaining principal.Sinking fu n d: Schedule for early redemption.Floating-rate: Coupon payments based on referencerate plus margin.Bond PricingThere are two equivalent ways to price a bond:•Constant discount rate applied to all cash flows(YTM) to find PV. This is a bond’s fla t p rice (doesnot include accrued interest).• Discount each cash flow using appropriate spotrate for each. This is a bond’s no-arbitrage price.Full p rice includes accrued interest. Governmentbonds use actual day counts; corporate bonds use30/360 method.full price = PV at last coupon date x (1 + YTM)r/Taccrued interest = coupon payment x (t/T)where:t = days from most recent coupon payment totrade settlementT = days in coupon payment periodMatrix p ricing: For illiquid bonds, use yields of bondswith same credit quality to estimate yield; adjust formaturity differences with linear interpolation.Bond MarketsNational bond market includes domestic bonds andforeign bonds.• Domestic bonds.Domestic issuer and currency.• Foreign bonds. Foreign issuer, domestic currency.Eurobond market is outside any one country, withbonds denominated in currencies other than thoseof countries in which bonds are sold.Global bonds trade in both a national bond marketand the eurobond market.Bond IssuanceUnderwritten offering: Investment banks buy entireissue, sell to public.Best efforts offering: Investment banks act as brokers.S helf r egistration: Register entire issue withregulators but sell over a period of time.Embedded OptionsCallable: Issuer may repay principal early. Increasesyield and decreases duration.Putable: Bondholder may sell bond back to issuer.Decreases yield and duration.Convertible: Bondholder may exchange bond forissuer’s common stock.Embedded warrants: Bondholder may buy issuer’scommon stock at exercise price.Yield MeasuresEffective y ield depends on periodicity. YTM =effective yield for annual-pay bonds.Semiannual bond basis: YTM = 2 x semiannualdiscount rate.Current y ield = annual coupon / price.Simple yield= current yield ±amortization.Yield to call is based on call date and call price.Yield to worst is lowest of a bond’s YTCs or YTM.M oney market y ields may be on a discount or addon basis and may use a 360- or 365-day year.Bond-equivalent yield is an annualized add-on yieldbased on a 365-day year.Forward and Spot RatesForward rate is a rate for a loan that begins at afuture date. “Iy3y” = 3-year forward rate 1 yearfrom today.Example of spot-forward relationship:(1 +s2)2=(1 +S^l+ly ly)Yield SpreadsG-spread: Basis points above government yield.I-spread: Basis points above swap rate.Z-spread: Accounts for shape of yield curve.Option-adjusted spread: Adjusts Z-spread for effectsof embedded options.Interest Rate RiskInterest rate risk has two components: reinvestment riskand market p rice risk from YTM changes. These riskshave opposing effects on an investor’s horizon yield.•Bond investors with short horizons are moreconcerned with market price risk.•Bond investors with long horizons are moreconcerned with reinvestment risk.•The horizon at which market price risk andreinvestment risk just offset is a bond’s Macaulayduration. This is the weighted average of timesuntil a bond’s cash flows are scheduled to be paid.continued on next page...。

CFA讲义之CFA与Excel结合的技巧

在前几天我们“CFA与Excel 结合的技巧”这篇文章中,我们介绍了如何的使用excel 计算某项投资的现值,重点讲解了NPV 与PV 两个函数。

在实务中,我们使用以上方法来计算某投资项目的净现值,以此来判断该项目是否值得投资,这种方法在投资项目筹划中经常用到。

除开计算净现值外,我们也要设定项目净现值为零的情况下计算项目的内部回报率是多少,并和该项目的资金成本(如项目的融资成本,或者公司的加权平均资金本成本等)做比较,以此判断项目内部回报率是否大于资金的成本,从而能为公司带来正的价值增值,下面我们融跃CFA 老师将介绍下如何使用excel 来计算项目的内部回报率。

下面是CFA 三级学长总结的CFA 学习资料大礼包,在CFA 考试前一套好的CFA 学习资料,会对你有很大的帮助。

01内部回报率内部回报率(IRR)即使是项目的净现值为零的复合收益率,设其为,则:在excel中我们可以使用IRR函数来计算投资项目的内部收益率,其语法如下:IRR(values, [guess])其中:values: 必需,表示投资项目的现金流,必须包含有一个正值或一个负值。

guess:可选,默认为10%,表示对内部收益率的估计值。

Excel使用迭代法计算内部收益率,从初始值开始不断修正计算结果,直至其精度小于 0.00001%。

如果迭代20 次仍未找到结果,则返回错误值 #NUM!下面我们看一个例子:例1:计算内部回报率现有一投资项目,其初始投资为800元,第一至第五年末分别带来的正现金流为200,250,300,350与400元,求该项目的内部回报率。

解:使用IRR函数计算该项目的内部回报率(如下图)。

可以看到,在一般的投资项目中,期初投资为现金流出即为负的现金流,而后期投资收益则为现金流入即为正的现金流,将这些现金流代入IRR函数,便可以计算出项目的内部收益率。

我们可以使用NPV函数来对以上的计算结果进行验证,可以发现在NPV函数中代入之前计算得到的内部回报率,得到项目的净现值为零,说明项目的内部回报率确为22.16%。

CFA一级备考资料优选【新手入门】

CFA一级备考资料优选

一、备考资料

1.CFA官方教材

(1)课后题目/答案

(2)词汇表(Glossary)与索引(Index)

2.CFAnotes系列

3.Mock系列

4.CFA道德手册V11版本,考试专用handbook

5.CFA官方考纲

6.CFA指定计算器

7.QuickSheet(CFA公示表)

8.CFA核心词汇

9.CFA一级中英文教材,精要图解

10.自学或参加培训课程

CFA一级资料对比:

二、学习顺序

对于一级学员来说,可以从Ethical and Professional Standards职业道德入门,这个科目大部分中国考生非常陌生,需要有个熟悉的过程。

先听视频课,力求理解,记忆的工作可以延后到考试前的一个月内(记得太早容易忘)。

如果没有财务基础或者基础薄弱,建议投入较多时间先学习财务,因为财务考试比重最大,内容多、要求高,需要早点开始学习。

其他科目学习顺序可以根据自己的情况而定。

如果是非经济或非金融背景,接下来建议先学数量分析和经济学,再之后是固定收益、股权投资、衍生工具、另类投资、组合管理、公司金融等模块。

2009年-CFA-一级-Mock题