Topic Evaluation of an Accounting Model for Grid Infrastructures

会计信息质量检查与审计质量

会计信息质量检查与审计质量一、本文概述Overview of this article随着经济全球化的发展和我国市场经济的深入,会计信息质量对于企业的决策、投资者的利益以及国家宏观经济的调控都具有至关重要的影响。

然而,由于各种内外部因素的影响,会计信息失真、舞弊等问题屡见不鲜,严重影响了会计信息的真实性和可靠性。

因此,会计信息质量检查与审计质量成为了当前会计领域研究的热点和难点。

With the development of economic globalization and the deepening of China's market economy, the quality of accounting information has a crucial impact on the decision-making of enterprises, the interests of investors, and the macroeconomic regulation of the country. However, due to various internal and external factors, problems such as accounting information distortion and fraud are common, seriously affecting the authenticity and reliability of accounting information. Therefore, the quality inspection of accounting information and audit quality has become a hot and difficult research topicin the current accounting field.本文旨在探讨会计信息质量检查与审计质量之间的关系,分析会计信息失真的原因,探讨有效的会计信息质量检查方法和审计策略,以提高会计信息质量和审计质量,保护投资者利益,维护市场经济秩序。

管理会计第14版(charles 查尔斯)英文影印版课后答案

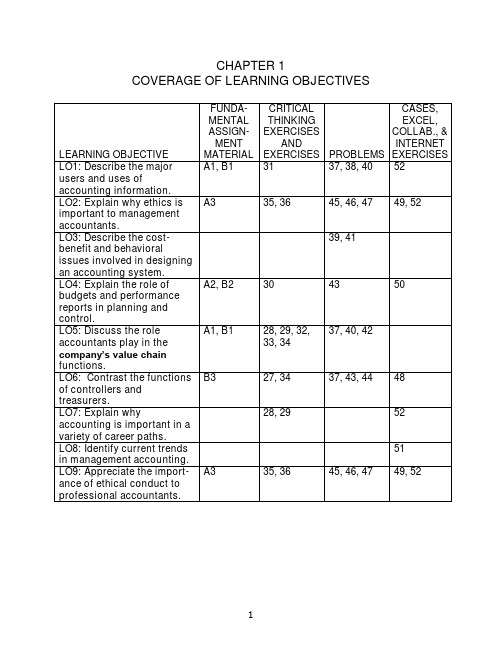

COVERAGE OF LEARNING OBJECTIVESManagerial Accounting and the Business Organization1-A1 (10-15 min.)Because the accountant's duties are often not sharply defined, some of these answers could be challenged:1. Attention directing and problem solving. Budgeting involves makingdecisions about planned activities -- hence, aiding problem solving.Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has ascorekeeping dimension.2. Problem solving. Helps a manager assess the impact of a decision.3. Scorekeeping. Reports on the results of an operation. Could also beattention direction if scrap is an area that might require management decisions.4. Attention directing. Focuses attention on areas that need attention.5. Attention directing. Helps managers learn about the informationcontained in a performance report.6. Scorekeeping. The statement merely reports what has happened.7. Problem solving. The cost comparison is apparently useful becausethe manager wishes to decide between two alternatives. Thus, it aids problem solving.8. Attention directing. Variances point out areas where results differfrom expectations. Interpreting them directs attention to possiblecauses of the differences.9. Problem solving. Aids a decision about where the parts should bemade.10. Scorekeeping. Determining a depreciation schedule is simply anexercise in preparing financial statements to report the results ofactivities.1. Budgeted Actual DeviationsAmounts Amounts or Variances Room rental $ 140 $ 140 $ 0Food 800 1,008 208UEntertainment 600 600 0Decorations 220 190 30FTotal $1,760 $1,938 $178U2. Because of the management by exception rule, room rental andentertainment require no explanation. The actual expenditure forfood exceeded the budget by $208. Of this $208, $150 is explained by attendance of 15 persons more than budgeted (at a budget of $10 per person) and $58 is explained by expenditures above $10 per person.Actual expenditures for decorations were $30 less than the budget. If all desired decorations were purchased, the decorations committee should be commended for their savings.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard:1. The General Mills manager must respect the confidentiality standard.He or she should not disclose any information about the new cereal.2. Roberto must address his level of competence for the assignment. Ifhis supervisor knows his level of expertise and wants an analysisfrom a “layperson” point of view, he should do it. However, if thesupervisor expects an expert analysis, Roberto must admit his lackof competence.3. The objectivity standard should cause Helen to decline to omit theinformation from her budget. It is relevant information, and itsomission may mislead readers of the budget.Because the accountant’s duties are often not sharply defined, some of these answers could be challenged:1. Scorekeeping. Records events.2. Scorekeeping. Simply recording of what has happened.3. Problem solving. Helps a manager decide between alternatives.4. Attention directing. Directs attention to the use of overtime labor.5. Problem solving. Provides information to managers for decidingbetween alternatives.6. Attention directing. Directs attention to why nursing costs increased.7. Attention directing. Directs attention to areas where actual resultsdiffered from the budget.8. Problem solving. Helps the vice-president to decide which course ofaction is best.9. Scorekeeping. Records costs in the department to which theybelong.10. Scorekeeping. Records actual overtime costs.11. Attention directing. Directs attention to stores with either high or lowratios of advertising expenses to sales.12. Attention directing. Directs attention to causes of returns of the drug.13. Attention directing or problem solving, depending on the use of theschedule. If it is to identify areas of high fuel usage it is attentiondirecting. If it is to plan for purchases of fuel, it is problem solving. 14. Problem solving. Provides information for deciding between twoalternative courses of action.15. Scorekeeping. Records items needed for financial statements.1 & 2. Budget Actual VarianceSales $75,000 $74,860 $ 140UCosts:Fireworks $35,000 $39,500 $4,500ULabor 15,000 13,000 2,000FOther 8,000 8,020 20UProfit $17,000 $14,340 $2,660U3. The cost of fireworks was $4,500 ÷ $35,000 = 13% over budget. Didfireworks suppliers raise their prices? Did competition cause retailprices to be lower than expected? There should be someexplanation for the extra cost of fireworks. Also, the labor cost was$2,000 ÷ $15,000 =13% below budget. It would be useful to discover why this cost was saved. Both sales and other costs were very close to budget.1-B3 (10 - 15 min.)1. Treasurer. Analysts affect the company's ability to raise capital,which is the responsibility of the treasurer.2. Controller. Advising managers aids operating decisions.3. Controller. Advice on cost analysis aids managers' operatingdecisions.4. Controller. Divisional financial statements report on operations.Financial statements are generally produced by the controller'sdepartment.5. Treasurer. Financing the business is the responsibility of thetreasurer.6. Controller. Tax returns are part of the accounting process overseenby the controller.7. Treasurer. Insurance, as with other risk management activities, isusually the responsibility of the treasurer.8. Treasurer. Allowing credit is a financial decision.1-1 Decision makers within and outside an organization use accounting information for three broad purposes:1. Internal reporting to managers for planning and controllingoperations.2. Internal reporting to managers for special decision-making and long-range planning.3. External reporting to stockholders, government, and other interestedparties.1-2 The emphasis of financial accounting has traditionally been on the historical data presented in the external reports. Management accounting emphasizes planning and control purposes.1-3 The branch of accounting described in the quotation is management accounting.1-4 Scorekeeping is the recording of data for a later evaluation of performance. Attention directing is the reporting and interpretation of information for the purpose of focusing on inefficiencies of operation or opportunities for improvement. Problem solving presents a concise analysis of alternative courses of action.1-5 GAAP applies to publicly issued annual financial reports. Internal accounting reports are not restricted by GAAP.1-6 Yes, but it covers more than that. The Foreign Corrupt Practices Act applies to all publicly-held companies and covers the quality of internal accounting control as well as bribes and other matters.1-7 Users cannot easily observe the quality of accounting information. Thus, they rely on the integrity of accountants to be sure the information is accurate. Information that is unreliable is worthless, so if accountants do not have a reputation for integrity, the information they produce will not have value.1-8 Three examples of service organizations are banks, insurance companies, and public accounting firms. Such organizations tend to be labor intensive, have outputs that are difficult to define and measure, and have both inputs and outputs that are difficult or impossible to store.1-9 Two considerations are cost-benefit balance and behavioral effects. Cost-benefit balance refers to how well an accounting system helps achieve management's goals in relation to the cost of the system. The behavioral consideration specifies that an accounting system should be judged by how it will affect the behavior (that is, decisions) of managers.1-10 Yes. The act of recording events has become as much a part of operating activities as the act of selling or buying. For example, cash receipts and disbursements must be traced, and receivables and payables must be recorded, or else gross confusion would ensue.1-11 A budget is a prediction and guide; a performance report is a tabulation of actual results compared with the budget; and a variance reconciles the differences between budget and actual.1-12 No. Management by exception means that management spends more effort on those areas that seem to be out of control and less on areas that are functioning as planned. This method is an efficient way for managers to decide where to put their time and effort.1-13 No. There is no perfect system of automatic control, nor does accounting control anything. Accounting is a tool used by managers in their control of operations.1-14 Information that is relevant for decisions about a product depends on the product's life-cycle stage. Therefore, to prepare and interpret information, accountants should be aware of the current stage of a product's life cycle.1-15 The six functions are: (1) research and development – generation and experimentation with new ideas; (2) product and service process design – detailed design and engineering of products; (3) production – use of resources to produce a product or service; (4) marketing - informing customers of the value and features of products or services; (5) distribution – delivering products or services to customers; and (6) customer service –support provided to customers.1-16 No. Not all of the functions are of equal importance to the success of a company. Measurement and reporting should focus on those functions that enable a company to gain and maintain a competitive edge.1-17 Line managers are directly responsible for the production and sale of goods or services. Staff managers have an advisory function – they support line managers.1-18 Management accountants are the information specialists, even in non-hierarchical companies. However, in such companies they are more directly involved with managers and are often parts of cross-functional teams.1- 19 A treasurer is concerned mainly with the company's financial matters, the controller with operating matters. In large organizations, there are sufficient activities associated with both financial and operating matters to justify two separate positions. In a small organization the same person might be both treasurer and controller.1-20 The four parts of the CMA examination are: (1) economics, finance, and management, (2) financial accounting and reporting, (3) management reporting, analysis, and behavioral issues, and (4) decision analysis and information systems.1-21 This is not true. About one-third of CEOs come from finance or accounting backgrounds. Accounting is excellent preparation for top management positions because accountants are often exposed to many parts of the company early in their careers.1-22 Changes in technology are affecting how accountants operate. They must be able to account for e-commerce transactions efficiently and safely, they often must integrate their accounting systems into ERP systems, and an increasing number are beginning to use XBRL to communicate information electronically.1-23 The essence of the just-in-time philosophy is the elimination of waste, accomplished by reducing the time products spend in the production process and trying to eliminate the time spent in processes that do not add value to the product.1-24 Moving tools and products that are in process from one location to another in a plant is an activity that does not add value to the product. So changing the plant layout to eliminate wasted movement and time improves production efficiency.1-25 The four major responsibilities are: (1) competence - develop knowledge; know and obey laws, regulations, and technical standards; and perform appropriate analyses, (2) confidentiality - refrain from disclosing or using confidential information, (3) integrity - avoid conflicts of interest, refuse gifts that might influence actions, recognize limitations, and avoid activities that might discredit the profession, and (4) objectivity - communicate information fairly, objectively, and completely, within confidentiality constraints.1-26 Standards do not always provide the needed guidance. Sometimes an action borders on being unethical, but it is not clearly an ethical violation. Other times two ethical standards conflict. In situations such as these, accountants must make ethical judgments.1-27 (5-10 min.)Typical activities associated with the treasurer function include:❑Provision of capital❑Investor relations❑Short-term financing❑Banking and custody❑Credits and collections❑Investments❑Risk managementTypical activities associated with the controller function include:❑Planning for control❑Reporting and interpreting❑Evaluating and consulting❑Tax administration❑Government reporting❑Protection of assets❑Economic appraisal1-28 (5-10 min.)Activities 2, 4, 5, and 6 are primarily associated with marketing decisions. The management accountant would assist in these decisions as follows: Boeing Company’s pricing decision requires cost data relevant to the new method of distributing spare parts. will need to know the costs of the advertising program as well as the additional costs of other value chain functions resulting from increased sales. TexMex Foods will need to know the incremental revenues and incremental costs associated with the special order. Target Stores needs to know the impact on both revenues and costs of closing one of its stores.Activities 1, 7, and 8 are primarily associated with production decisions. The management accountant would assist in these decisions as follows. Porsche Motor Company needs an analysis of the costs associated with purchasing the part compared to the costs of making the part. Dell will need to know the costs of the training program and the savings associated with increased efficiencies in the setup and changeover activities. General Motors needs to know the costs and salvage values of the replacement equipment, the proceeds of the sale of the old equipment, and the operating savings associated with the use of the new equipment.1-30 (5 min.)1. Management 4. Management 7. Financial2. Management 5. Management3. Financial 6. Financial1. Performance ReportBudget Actual Variance Explanation Revenues $220,000 $228,000 $8,000 F Additional salesfrom newproducts* Advertising cost 15,000 16,500 (1,500) U New advertisingCampaignNet $6,500 F* From the New Products Report, seven new products were added. This exceeded the plan to add six.2.Factors that may not have been considered include:a.The costs of new products may have exceeded their price.b.Customer satisfaction with new products may not have been partof the new products report.petitors’ reactions to the Starbucks store’s actions may nothave been anticipated.d.External uncontrollable factors such as increases in operatingcosts, adverse weather, changes in the overall economy, newcompetitors entering the market, or key employee turnover mayhave decreased efficiency.1-32 (5 min.)1. Line, support 3. Staff, marketing 5. Staff, support2. Staff, support 4. Line, marketing 6. Line, productionMicrosoft is a company that most students will know and have some understanding of what functions its managers perform. Nevertheless, this may not be an easy exercise for those who have little knowledge of how companies operate.Research & development – Because software companies must continually come out with new products and upgrades to their current products this is a critical function for Microsoft. More than one-fourth of Microsoft’s operating expenses are devoted to R&D.Design of products, services, or processes – For Microsoft the design and R&D process probably overlap considerably. Product design is critical; process design is probably not. One essential part of design is beta testing – that is, field testing of new software. This quality-control step is essential to prevent customer dissatisfaction with new products.Production – Microsoft produces disks and CD-ROMs and the manuals and packaging to go with them. However, they are increasingly delivering software over the Internet, which takes an initial process design and then few resources. It is not likely a major focus for Microsoft.Marketing – Microsoft spends more on sales and marketing than on any other operating expense. Increasing competition in software sales makes marketing essential to the company’s future. This function includes advertising and direct marketing activities, but it also includes activities of the company’s sales force. Distribution – This function is becoming simpler for Microsoft as it delivers more and more software over the Internet. Although the company must stay abreast of competitors in delivery methods, this is not likely to create a major competitive advantage or disadvantage for Microsoft.Customer service – Customer service is important, but Microsoft tries to minimize its costs in this area by product design – making things work right without needing deep computer expertise. Still, poor customer service can severely impact a company, so Microsoft must attend to it.Support functions – Most of the time these are not a major focus. There is one exception recently for Microsoft. Legal support has been front and center. The very future of the company was based on court judgments for which good legal support was essential.The management accountant's major purpose is to provide information that helps line managers in making decisions regarding the planning and controlling of operations. The accountant supplies information for scorekeeping, attention directing, and problem solving. In turn, managers use this and other information for routine and non-routine decisions and for evaluating subordinates and the performance of sub-parts of the organization. Management accountants must walk a delicate line between (1) making sure that managers are properly using the pertinent information and (2) making sure that the managers, not the accountants, are doing the actual managing.1-35(5 min.)Other costs of a poor ethical environment include legal costs and costs due to high employee turnover. Other benefits of a good ethical environment include low employee turnover, low loss from internal theft, and improved customer satisfaction resulting from better quality and service (that result from a more productive work environment).1-36(5 min.)There are numerous examples.“You understand how important it is to record this sale before year end, don’t you?”“Doing it this way is common for all companies in our business, so don’t worry!”“Trust me, the inventory is at the warehouse.”This problem can form the basis of an introductory discussion of the entire field of management accounting.1. The focus of management accounting is on helping internal users tomake better decisions, whereas the focus of financial accounting ison helping external users to make better decisions. Managementaccounting helps in making a host of decisions, including pricing,product choices, investments in equipment, making or buying goods and services, and manager rewards.2. Generally accepted accounting standards or principles affect bothinternal and external accounting. However, change in internalaccounting is not inhibited by generally accepted principles. Forexample, if an organization wants to account for assets on the basisof replacement costs for internal purposes, no outside agency canprohibit such accounting. Of course, this means that organizationsmay have to keep more than one set of records. There is nothingimmoral or unethical about having multiple sets of books, but theyareexpensive. Accounting data are commodities, just like butter or eggs.Innovations in internal accounting systems must meet the samecost-benefit tests that other commodities endure. That is, theirperceived increases in benefits must exceed their perceivedincreases in costs. Ultimately, benefits are measured by whetherbetter decisions are forthcoming in the form of increased net profitsor cost savings.3. Budgets, the formal expressions of management plans, are a majorfeature of management accounting, whereas they are not asprominent in financial accounting. Budgets are major devices forcompelling and disciplining management planning.4. An important use of management accounting information is theevaluation of performance, which often takes the form of comparisonof actual results against budgets, providing incentives and feedback to improve future decisions.5.Accounting systems have an enormous influence on the behavior ofindividuals affected by them. Management accounting is moreconcerned with the likely behavioral effects of various accountingalternatives that may be adopted than is financial accounting.1-38(10 min.)The main point of this question is that cost information is crucial for decisions regarding which products and services should be emphasized or de-emphasized. The incentives to measure costs precisely are far greater when flat fees are being received instead of reimbursements of costs.Note, too, that nonprofit organizations and profit-seeking organizations have similar desires regarding management accounting. Accountability is now in fashion for many purposes, including justification of prices, cost control, and response to criticisms by investors (whether they be donors, taxpayers, or others).When somebody's money is at stake, accounting systems get much love and attention. In a survey of 550 hospitals, hospital financial executives said that improved cost accounting systems "are crucial to responding to changes in hospital payment mechanisms and that better cost information is essential for more profitable and efficient operations." Hospitals will increasingly identify costs by product (type of case), not just by departments.1-39 (10 min.)Paperwork and systems often seem to become ends in themselves. However, the rationale that should underlie systems design is the cost-benefit philosophy or approach that is implied in the quotation. The aim is to get the managers and their subordinates collectively to make better decisions under one system versus another system -- for a given level of costs.Marks & Spencer should look at each of the management accounting reports it produces with an eye toward how it helps managers make better decisions. Does it provide needed scorekeeping? Does it direct attention to aspects of operations that might need altering? Does it provide information for specific management decisions? These types of questions will help identify the benefit of the information in the report.Then the company must consider the cost – not just the cost of collecting the data and preparing the reports, but the cost of educating managers to use the information and the cost of the time to read, digest, and act on the information. Too much information may be costly because it makes it time-consuming (and thus costly) to sift through the reams of information to find the few items that are important. And one cost may be the loss of important information because the total volume of information makes it too difficult to ferret out the important items.1-40(10 min.) Financial information is important in all companies. But how managers get and use financial information can differ depending on the culture and philosophies of the company.Top executives of a company often represent a functional area that is critical to the comparative economic advantage of the company. If technology is crucial, engineers generally hold important executive positions. If marketing differentiates the company from others, marketing executive s usually dominate. But regardless of the source of a company’s competitive advantage, its success will eventually be measured in economic terms. They must attend to financial aspects to thrive and often even to survive.Management accountants must work with the dominant managers in any organization. The modern trend toward use of cross-functional teams places management accountants at the center of the action regardless of what type of managers and executives dominate. Most companies realize that there is a financial dimension to almost every major decision, so they want the financial experts, management accountants, involved in the decisions. But to be accepted as an important part of these teams, the management accountants must know how to help managers in various functional areas. In General Mills, if accountants can’t talk the language of marketing, they will not have great influence. In ArvinMeritor, if they do not understand the information needs of engineers they will not provide value.1-41(10-15 min.)1. Boeing's competitive environment and manufacturing processeschanged greatly during the 1990s. An accounting system that served them well in their old environment would not necessarily be optimal in the 2000s. Boeing's management probably thought that changes in the accounting system were necessary to produce the kind of information necessary to remain competitive.2. A cost-benefit criterion was probably used. Boeing's management maynot have quantified the costs and the benefits, but they certainlyassessed whether the new system would help decisions enough towarrant the cost of the system.Many of the benefits of a better accounting system are hard to measure.They affect many strategic decisions of an organization. Withoutaccurate product costs, management will find it difficult to assess the consequences of their decisions. An accurate accounting system will help to price airplanes and other products competitively.3. More accurate product costs will usually result in better managementdecisions. But if the cost of the accounting system that produces the more accurate costs is too high, it may be best to forego the increased accuracy. The benefit of better decisions must exceed the added cost of the system for a change to be desirable.1-42(10 min.)1. There are many possible activities for each function of Nike's valuechain. Some possibilities are:Research and development -- Determining changes in customers'tastes and preferences for shoes and sportswear to come up withnew products (maybe the next "Air Jordans").Product and service process design -- Design a shoe to meet theincreasing demands of competitive athletes.Production -- Determine where to produce products and negotiatecontracts with the companies producing them.Marketing -- Signing prominent athletes to endorse Nike's products.Distribution -- Select the best locations for warehouses fordistribution to retail outlets.Customer service -- Formulate return policies for products thatcustomers perceive to be defective.2. Accounting information that aids managers' decisions includes:Research and development -- Trends in sales for various products, to determine which are becoming more and less popular.Product and service process design -- Production costs of variousshoe designs.Production -- Measure total costs, including both purchase cost and transportation costs, for production in various parts of the world.Marketing -- The added profits generated by the added sales due toproduct endorsements.Distribution -- Storage and shipping costs for different alternativewarehouse locations.Customer service -- The net cost of returned merchandise, to becompared with the benefits of better customer relations.。

企业成本控制分析外文翻译

必属精品

免费下载

成本控制

成本控制,也被称为遏制成本或管理成本,一个广阔的成本管理技术,它的经济增长目标是降低成本提高企业效率。企业使用的成本控制方法,监测,评价,并最终提升效率的具体领域,如部门、产品线。

20世纪90年代的成本控制措施,受到了美国企业的首要关注。一般而言,外包企业重组、撤资的外围活动,大规模裁员等成本控制战略被认为是升提升企业利润和维持企业竞争优势的需要。其目的往往是降低企业的生产成本,这样该企业给出的销售价格就比其竞争对手具更大的利润。

Cost control, also known as cost management or cost containment, is a broad set of cost accountingmethods and management techniques with the common goal of improving business cost-efficiency by reducing costs, or at least restricting their rate of growth. Businesses use cost control methods to monitor, evaluate, and ultimately enhance the efficiency of specific areas, such as departments, divisions, or product lines, within their operations.

成本控制是一个持续的过程,与拟议的年度预算配合使用。该预算有助于:(1)组织、协调生产和销售、服务和管理职能;(2)采取最大程度地利用现有的机会。根据财政历年的进步形式,将预算与实际结果作比,生成新的计划和经验教训,用以评价目前的行动。

会计专业评估作文英语

会计专业评估作文英语Title: The Significance of Accounting Profession: An Evaluation。

Introduction:The field of accounting plays a crucial role in the global economy by providing financial information that facilitates decision-making for businesses, investors, and other stakeholders. In this essay, we will delve into the significance of the accounting profession, its evolution, challenges, and future prospects.Importance of Accounting:Accounting serves as the language of business, enabling organizations to communicate their financial health and performance to various stakeholders. It involves the recording, summarizing, and analyzing of financial transactions to produce financial statements such asbalance sheets, income statements, and cash flow statements. These statements provide insights into a company's profitability, liquidity, and overall financial health, guiding stakeholders in making informed decisions.Evolution of Accounting:The accounting profession has evolved significantlyover the years, adapting to changes in technology, regulations, and business practices. From its roots in ancient civilizations, where simple record-keeping was practiced, to the double-entry system pioneered by Luca Pacioli in the 15th century, accounting has continuously evolved to meet the needs of modern businesses. The adventof computers and accounting software has further revolutionized the profession, making data processing more efficient and enabling real-time financial reporting.Challenges Facing the Accounting Profession:Despite its importance, the accounting profession faces several challenges. One major challenge is maintainingethical standards and integrity in financial reporting. The occurrence of financial scandals, such as Enron and WorldCom, has raised concerns about the credibility of financial information provided by companies. Additionally, globalization and the increasing complexity of financial transactions pose challenges for accountants in ensuring compliance with international accounting standards and regulations.Another challenge is the rapid pace of technological advancement, which requires accountants to continually update their skills to remain relevant. Automation and artificial intelligence are reshaping the accounting landscape, automating routine tasks and data analysis. While these technologies offer opportunities for increased efficiency, they also raise concerns about job displacement and the need for accountants to develop new skills in data analysis and interpretation.Future Prospects of the Accounting Profession:Despite these challenges, the accounting professionremains indispensable in the global economy. As businesses continue to expand globally, the demand for skilled accountants who can navigate complex financial environments is expected to increase. Moreover, advancements in technology present opportunities for accountants to provide higher-value services such as financial analysis, strategic planning, and risk management.Conclusion:In conclusion, the accounting profession plays a vital role in the global economy by providing financialinformation that facilitates decision-making for businesses, investors, and other stakeholders. Despite facingchallenges such as maintaining ethical standards and adapting to technological advancements, the profession remains resilient and continues to evolve to meet the needs of modern businesses. As we look to the future, the demand for skilled accountants is expected to grow, underscoringthe significance of this profession in driving economic prosperity.。

会计盈余数字的实证评价

市场月报酬率的估计。 该等式中的残差就是实际回报与预期回报的差。 如果市场可以很快和有效地对信息做出反应,那 么这里的残差就完全可以代表被研究公司新信息收益和EPS(每股收益)

✓ 样本数据 盈余数据来源于标准普尔的Compustat数据库。 年报披露来源于《华尔街日报》。 股价数据来源于芝加哥大学的CRSP 数据库。 样本的最后选择是1957-1965年9年纽约证券交易 所261家上市公司的数据。

➢ 在现实中,我们注意到盈余数字对于投资者来说 是至关重要的,它是投资者决策的重要标准,那 么会计盈余就会反映在股价中。Beaver(1968) 、 Samuelson(1965)

➢ 本文首次采用实证方法将会计盈余与股票回报联 系起来,通过研究会计盈余数字的信息含量和时 效性来验证会计信息是有用的

二、论证过程

➢ 不足 盈利的信息含量被分类为好消息和坏消息是一种 比较粗糙的分类。

四、文章拓展

本文的研究为后来多方面研究提供了基础: ➢ 公司公告的信息含量研究

比如股利公告等事件研究。 ➢ 盈余公告漂移现象的深入探讨

本文是首次发现了盈余公告的漂移现象,从而为 后来Bernard和Thomas(1989)等研究漂移现象奠 定了基础。 ➢ 会计实证研究方法的兴起 该论文开创了会计与资本市场结合研究的先河。

a.可能是市场收益指数在一些公司报告出他们的 盈余数据之前都是不确定的

b.可能是在公告日的随机误差

c.可能是初步公告没有被市场完全反应

➢ 稳健性分析

由于检验的残差中的新信息的存在并不一定是盈 余公告信息提供的,可能包含了其他来源的信息, 因此作者最后给出了一个稳健性检验,建立了总 信息、盈余信息和其他信息模型。检验结果发现 盈余数字提供的信息含量占了每个公司提供所有 信息含量的一半以上,同样证明了盈余数字是具 有信息含量的。

香港会计准则应用指南

`1MEMBERS' HANDBOOKCONTENTS OF VOLUME III(Updated to December 2012)Issue/ReviewdatePreface (Amended) Amended Preface to the Hong Kong Quality Control, Auditing, Review, Other Assurance and Related Services Prouncements...................................................07/12Glossary (Clarified) Glossary of Terms Relating to Hong Kong Standards on Quality Control,Auditing, Review, Other Assurance and Related Services ....................................12/12 HONG KONG STANDARDS ON QUALITY CONTROLHKSQC 1 (Clarified) Quality Control for Firms that Perform Audits and Reviews of FinancialStatements, and Other Assurance and Related Services Engagements ..............07/10Framework HONG KONG FRAMEWORK FOR ASSURANCE ENGAGEMENTS..................12/12 HONG KONG STANDARDS ON AUDITINGHKSA 200 – 299 GENERAL PRINCIPLES AND RESPONSIBILITIESHKSA 200 (Clarified) Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Hong Kong Standards on Auditing .............................................07/10HKSA 210(Clarified)Agreeing The Terms of Audit Engagements ..........................................................12/12HKSA 220(Clarified)Quality Control for an Audit of Financial Statements .............................................07/10HKSA 230(Clarified)Audit Documentation ..............................................................................................07/10HKSA 240 (Clarified) The Auditor’s Responsibilities Relating to Fraud in an Audit of FinancialStatements .............................................................................................................07/10HKSA 250(Clarified)Consideration of Laws and Regulations in an Audit of Financial Statements........07/10HKSA 260(Clarified)Communication with Those Charged with Governance.........................................12/12HKSA 265 (Clarified) Communicating Deficiencies in Internal Control to Those Charged withGovernance and Management...............................................................................07/10HKSA 300 – 499 RISK ASSESSMENT AND RESPONSE TO ASSESSED RISKSHKSA 300(Clarified)Planning an Audit of Financial Statements.............................................................12/12HKSA 315 (Clarified) Identifying and Assessing the Risks of Material Misstatement throughUnderstanding the Entity and Its Environment.......................................................07/12HKSA 315 (Revised) Identifying and Assessing the Risks of Material Misstatement throughUnderstanding the Entity and Its Environment.......................................................12/12HKSA 320(Clarified)Materiality in Planning and Performing an Audit ....................................................07/10HKSA 330 (Clarified) The Auditor’s Responses to Assessed Risks.........................................................12/12HKSA 402(Clarified)Audit Considerations Relating to an Entity Using a Service Organization.............07/10HKSA 450(Clarified)Evaluation of Misstatements Identified during the Audit ........................................07/10HKSA 500 – 599 AUDIT EVIDENCEHKSA 500(Clarified)Audit Evidence........................................................................................................07/10HKSA 501(Clarified)Audit Evidence - Specific Considerations for Selected Items ................................07/10HKSA 505(Clarified)External Confirmations ...........................................................................................06/10HKSA 510(Clarified)Initial Audit Engagements - Opening Balances......................................................07/10HKSA 520(Clarified)Analytical Procedures.............................................................................................07/09HKSA 530(Clarified)Audit Sampling .......................................................................................................07/10HKSA 540 (Clarified) Auditing Accounting Estimates, Including Fair Value Accounting Estimates,and Related Disclosures.........................................................................................07/10HKSA 550(Clarified)Related Parties.......................................................................................................07/10HKSA 560(Clarified)Subsequent Events ................................................................................................07/10HKSA 570(Clarified)Going Concern .......................................................................................................07/10HKSA 580(Clarified)Written Representations.........................................................................................07/10 HKSA 600 – 699 USING THE WORK OF OTHERSHKSA 600 (Clarified) Special Considerations – Audits of Group Financial Statements (Including theWork of Component Auditors)................................................................................07/10HKSA 610(Clarified)Using the Work of Internal Auditors........................................................................07/12HKSA 610(Revised)Using the Work of Internal Auditors........................................................................12/12HKSA 620(Clarified)Using the Work of an Auditor’s Expert ...................................................................07/10HKSA 700 – 799 AUDIT CONCLUSIONS AND REPORTINGHKSA 700(Clarified)Forming an Opinion and Reporting on Financial Statements ................................10/10HKSA 705(Clarified)Modifications to the Opinion in the Independent Auditor’s Report .........................07/10HKSA 706 (Clarified) Emphasis of Matter Paragraphs and Other Matter Paragraphs in theIndependent Auditor’s Report.................................................................................07/10HKSA 710 (Clarified) Comparative Information – Corresponding Figures and ComparativeFinancial Statements..............................................................................................07/10HKSA 720 (Clarified) The Auditor’s Responsibilities Relating to Other Information in DocumentsContaining Audited Financial Statements ..............................................................07/10HKAS 800 - 899 SPECIALIZED AREASHKSA 800 (Clarified) Special Considerations – Audits of Financial Statements Prepared inAccordance with Special Purpose Frameworks.....................................................07/10HKSA 805 (Clarified) Special Considerations – Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement..........................................07/10HKSA 810(Clarified)Engagements to Report on Summary Financial Statements .................................03/11HONG KONG STANDARDS ON REVIEW ENGAGEMENTSHKSRE 2400 Engagements to Review Financial Statements......................................................12/12 HKSRE 2400(Revised)Engagements to Review Historical Financial Statements.....................................12/12HKSRE 2410 Review of Interim Financial Information Performed by the IndependentAuditor of the Entity ................................................................................................3/08HONG KONG STANDARDS ON ASSURANCE ENGAGEMENTSHKSAE 3000 Assurance Engagements Other Than Audits or Reviews of HistoricalFinancial Information ..............................................................................................10/04 HKSAE 3402 Assurance Reports on Controls at a Service Organization ....................................12/12 HKSAE 3410 Assurance Engagements on Greenhouse Gas Statements .................................11/12HONG KONG STANDARDS ON INVESTMENT CIRCULAR REPORTINGENGAGEMENTSHKSIR 300 Accountants’ Reports on Pro Forma Financial Information in InvestmentCirculars..................................................................................................................3/06 HKSIR 400 Comfort Letters and Due Diligence Meetings.........................................................12/12 HONG KONG STANDARDS ON RELATED SERVICESHKSRS 4400 Engagements to Perform Agreed-upon Procedures Regarding FinancialInformation..............................................................................................................11/04 HKSRS 4410 Engagements to Compile Financial Statements ....................................................07/12 HKSRS 4410(Revised)Compilation Engagements .....................................................................................07/12PRACTICE NOTESPN 600.1 Reports by the auditor under the Hong Kong Companies Ordinance ...................12/11 PN 620.2 Communications between auditors and the Insurance Authority ..........................9/04 PN 720 Acting as Scrutineer at a General Meeting of a Listed Issuer ...............................7/05 PN 730 Guidance for Auditors Regarding Preliminary Announcements of AnnualResults ...................................................................................................................12/05 PN 740 Auditor's Letter on Continuing Connected Transactions under the Hong KongListing Rules...........................................................................................................6/10 PN 810.1 Insurance brokers - compliance with the minimum requirements specified bythe Insurance Authority under sections 69(2) and 70(2) of the InsuranceCompanies Ordinance ...........................................................................................9/04PN 810.2 The duties of auditors under the Insurance Companies Ordinance .....................9/04 PN 820 The audit of licensed corporations and associated entities ofintermediaries ........................................................................................................12/10 PN 830 Reports by the Auditor Under the Banking Ordinance ..........................................12/11 PN 840 The audit of solicitors' accounts under the Solicitors' Accounts Rules and theAccountant's Report Rules ....................................................................................9/04 PN 850 Review of flag day accounts ..................................................................................9/04 PN 851 Review of the Annual Financial Reports of Non-governmentalOrganisations ........................................................................................................9/04 PN 852 Review of lottery accounts .....................................................................................9/04 PN 860.1 The audit of retirement schemes ...........................................................................9/04 PN 870 The assessments of Certification Authorities under the ElectronicTransactions Ordinance ........................................................................................9/04 PN 871 Engagement to report on compliance with the Billing and Metering IntegrityScheme of OFTA ...................................................................................................9/04PN 900 (Clarified) Audit of Financial Statements Prepared in Accordance with the Small andMedium-sized Entity Financial Reporting Standard ...............................................6/10 AUDITING GUIDELINESAG 3.283 Guidance for internal auditors ...............................................................................9/04 AG 3.340 Prospectuses and the reporting accountant ..........................................................9/04 AG 3.341 Accountants' report on profit forecasts ..................................................................9/04 HONG KONG AUDITING PRACTICE GUIDANCEHKAPG 1000 Special Considerations in Auditing Financial Instruments .....................................12/12。

四种审计意见(英文版)

审计报告意见类型有以下四种:无保留意见、保留意见、否定意见和无法表示意见(原为拒绝表示意见)。

下面对这四种意见作了简要解释。

AUDIT REPORTINGAudit Reports are categorized into four categories. Each type is briefly described as follows:UNQUALIFIED OPINION(无保留意见)An unqualified opinion states that the financial statements are presented fairly in conformity with GAAP. However, in some instances, the standard unqualified report may be modified without affecting the unqualified opinion issued on the financial statements.QUALIFIED OPINION. (保留意见)A qualified opinion is issued when the financial statements present the entity's financial position, results of operations, and cash flows in conformity with GAAP except for the matter of the qualification. Qualified opinions are issued, in some cases, when: (1) a scope limitation, or (2) a departure from GAAP exists.ADVERSE OPINION. (否定意见)When issuing an adverse opinion, the auditor concludes that the financial statements do not present the entity's financial position, results of operations, and cash flows in conformity with GAAP. This type of opinion is only issued when the financial statements contain very material departures from GAAP.DISCLAIMER OF OPINION.(无法表示意见)A disclaimer of opinion is issued when the auditor is unable to form an opinion on an entity's financial statements. A disclaimer may be issued in cases when: (1) the auditor is not independent with respect to the entity under audit, (2) a material scope limitation exists, or (3) a significant uncertainty exists.SAS No. 58 suggests seven principal reasons why an independent auditor my depart from the wording of the standard report. These are:1. Limitations on the scope of the auditor's examination.2. Division of responsibility.3. Lack of conformity with GAAP.4. A departure from an accounting principle set by the body designated to establish such principles.5. Lack of consistency.6. Uncertainties.7. Emphasizing a matter.AUDPORT: Expert System EvaluationThis knowledged-based system uses the criteria contained in Statement on Auditing Standards No. 58 to determine the type of audit opinion that should be rendered by anexternal auditor after conducting a financial audit under generally accepted auditing standards (GAAS). Assessment of the educational impact of the Audport expert system is described in a paper by L. Murphy Smith and R. Stephen McDuffie, "Impact of an Audit Reporting Expert System on Learning Performance: A Teaching Note" (forthcoming in Accounting Education). This Web-based HTM (hypertext m arkup language) approach was developed by Professors Smith and McDuffie, with assistance from Ms. Jennifer Calhoun.Answer the questions that appear on the screen by clicking on the correct answer. Based upon your answers, the criteria contained in SAS No. 58 will be evaluated. As each criterion is evaluated you will be provided with information on the screen either that a particular type of audit opinion should be rendered by the auditor or that additional evaluation is necessary.If the type of audit opinion to be rendered has been determined, you have completed the evaluation and can then quit the consultation. If additional evaluation is necessary to determine the type of audit opinion to render, this will be indicated to you and you will need to continue the consultation. The system only considers one audit problem for each consultation. However, many potential problems can be evaluated by the system.Two sets of terms are important when using this system, material versus pervasive and significant versus severe. Pervasive is of more concern than material, and severe is of more concern than significant. For example, a departure from generally accepted accounting principles that is not immaterial and is not justified either has a material affect on the financial statements or a pervasive affect on the financial statements, but not both. Depending on the situation, either a qualified opinion or an adverse opinion will be rendered.Significant and severe are used in describing a circumstance-imposed scope limitation. One or the other terms can be used to describe a situation but both terms can not be used to describe the sam e situation.A list of the questions that make up the AUDPORT Web-based expert system are available for you to review under 'AUDPORT questions' below. At any time during the consultation you may quit the consultation and return to the AUDPORT homepage.。

n empirical evaluation of accounting income number 全文翻译

会计收益数据的经验评价雷·鲍尔* 菲利普·布朗+会计理论家们大体上通过会计实务与特定分析模型的相符程度来评价其有用性。

这种会计分析模式可能仅仅由一些主张或断言组成,或者,它可能是一种经过严格推理的理论。

无论哪种情况,会计研究方法一直是将现行惯例和由模型推出的更为可取的操作或由模型推出的所有会计实践都应拥有的标准进行对比。

这种方法的缺点是它忽视了世界上知识的一个重要来源,就是模型预测符合观测行为的程度。

在某个探析的假设均能被经验验证这样的基础上为该探析辩护是不够的。

因为,如何能得知一个理论包含了所有相关的有证据支持的假设?同时,如何解释基于无法证实的前提,如效用函数最大化,得出的结论的预测能力?此外,如何分析在考虑了世界不同方面后产生的结论之间的差异?对会计实务的有用性进行完全分析方法的局限由会计数据本质上不能被定义的争论来说明。

会计数据本质上不能被定义是因为它们缺乏“意义”,从而它们的作用令人质疑。

1争论中心在一定程度上源自为适应新经济环境,相应出现会计实务的发展。

仅举一些出现问题的领域。

随着实务的发展,会计人员需要处理合并、租赁、并购、研发费用、物价波动和税项支出等实务。

因为会计缺少一个统一的理论框架,所以在这些会计实务中出现了不一致的现象。

其结果是,净收益是不同质部分的累计。

因而,净收益被认为是一个“无意义”的数字,跟27张桌子和8把椅子之间的差别没什么不同。

在这种观点下,净盈余只能被定义为一系列程序{}12,,X X 运用到一系列事件{}12,,Y Y 后得到的结果,没有什么实质内涵。

Canning 观察到:净盈余的计量结果在任何意义上都不能认为是真实的,除了它是一个数字,是会计人员中止他所采用的程序的应用后得出的结果。

2 尝试提高计量方式解释能力的分析方法的价值是无争议的。

有争议的是这样一个事实:一个分析模型本身没有评估脱离它所隐含计量方式的意义。

因此,在没有进行经验检验的基础上,根据会计分析模式得出由于会计收益数据缺乏实质内涵导致它缺乏有用性的结论是不妥的。

审计英语讲义

2008年注册会计师审计考试英语辅导讲义一、相关背景1、2008年注册会计师全国统一考试将在会计、审计和财务成本管理三门课程中增加10分的英语附加题。

这一变化主要是为了满足中国经济和行业发展对国际型人才的需要。

财政部CPA考试委员会将逐步推广英文附加题到其他考试科目中。

据此看来,在CPA各科考试中加试英语将是一个趋势。

2、增加英语附加题后,会计、审计、财务成本管理的总分为110分,及格分仍为60分,总体考试时间不变。

英语附加题要求用英语回答,所以考生朋友们一定要根据本人英语水平选择作答。

有一定英语基础(大学英语四、六级水平,掌握一定的财经英语词汇),打算选答英语附加题的考生朋友应该合理规划和安排时间,在考试时认真阅读试卷首页的特别提示和答题导语,争取尽可能多的在英语附加题上拿分。

英语基础较薄弱的考生朋友不要慌乱,心态要放平和,力争前面的100分,如果时间允许可尝试做英语附加题。

二、可能的题型因为只有10分的英语题,所以估计出客观题的可能性不大,很有可能是主观题,并且是专业题。

题型可能包括:名词解释,英汉互译,问答(理论性的或业务性的)。

从2007年会计、审计两门课的英语加试题判断,出业务核算和以计算为主的专业题的可能性较大。

三、审计英语讲解Auditing一、鉴证业务与外部审计Assurance engagements and external auditAn assurance engagement is one in which a practitioner expresses a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the outcome of the evaluation or measurement of a subject matter against criteria.Assurance service: external auditPractitioner = AuditorSubject matter = Financial statementsResponsible party = ManagementIntended users = ShareholdersCriteria = Accounting standards/lawConclusion = Truth and fairnessLevel of assurance= High (rendered as “reasonable assurance”)Two general types of assurance engagement:An assertion based engagement where the account declares that a given assertion is either correct or not.A direct reporting engagement, where the accountant reports on issues that have come to his attention during his evaluation.An audit is an exercise to give an independent opinion on the truth and fairness of financial statements.1.重要性、真实和公允反应、合理保证Materiality, true and fair presentation, reasonable assurance Materiality is the magnitude of an omission or misstatement of accounting information that, in the light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the omission or misstatement. An auditor must consider materiality both in (1) planning the audit and designing audit procedures and (2)evaluating audit results. 2.注册会计师的聘用,解聘和辞职Appointment, removal and resignation of auditors3.审计意见类型:标准无保留意见、带强调事项段的无保留意见、保留意见、否定意见、无法表示意见Types of opinion: standard unqualified opinion, Unqual ified with emphasis of matter paragraph, qualified opinion, adverse opi nion, disclaimer of opinion.4.职业道德:独立、客观和公正,专业胜任能力,应有的关注,保密性,职业行为Professional ethics: independence, objectivity and integrity, professional competence, due care, confidentiality, professional behavior5.审计业务约定书Engagement letter二、审计计划和风险评估Planning and risk assessment1.一般原则General principles· Plan and perform audits with an attitude of professional skepticism · Audit risks = inherent risk × control risk × detection risk(1) Inherent risk refers to the likelihood of material misstatement of an assertion, assuming no related internal c ontrol. This risk differs by account and assertion.(2) Control risk is the likelihood that a material misstatement will not be prevented or de tected on a timely basis by internal control. Th is risk is assessed using the results of tests of control.(3) De tection risk is the likelihood that an auditor’s procedures lead to an improper conclusion that no material misstatement exists in an assertion when in fact such a misstatement does exist. The auditor’s substantive tests are primarily relied upon to restrict detection risk.审计风险=重大错报风险×检查风险Audit risks = material misstatement risk × detection risk练习:The auditors assessed a combined inherent risk and control risk at 0.50and said they wanted to achieve a 0.05 risk of failing to detect misstatements in an account equal to the ¥17,000 tolerable misstatement assigned to the account. What detection risk do the a uditors plan to use for planning the remainder of the audit work?· Risk-based approach:audit risk-based approach, business risk-based approach2.了解被审单位Understanding the entity and knowledge of the businessThe CPA should obt ain a level of knowledge of the client’s busine ss that will enable effective planning and performance of the audit in accordance with generally accepted auditing standards. This knowledge helps the auditor in(1) Identifying areas that may need special consideration(2) Assessing conditions under which accounting data are produced, processed, reviewed and accumulated(3) Evaluating accounting estimates for reasonableness (e.g., valuation of inventories, depreciation, allowance for doubtful accounts, percentage of completion of long-term contracts)(4) Evaluating the reasonableness of management representations(5) Making judgments about the appropriateness of the accounting principles applied and the adequacy of disclosures3.估计重大错报或舞弊的风险Assessing the risks of material misstatement and fraud重要性水平可容忍误差· Materiality (level) tolerable errorAuditors use materiality three ways:(1) as a guide to planning th e audit program—directing attention and audit work to the important, uncertain, or error-prone items and accounts; (2) as a guide t o evaluation of the evidence; (3) as a guide for making decisions about the audit report. Materiality in auditing is perceived in terms of both potential misstatement (in a planning sense) and known or estimated misstatement (in an evaluation and reporting decision sense).Auditors must examine both quantitative and qualitative factors when assessing materiality. Some of the common factors auditors use in making materiality judgments are: (1) Absolute Size; (2) Relative Size; (3) Nature of the item or issue; (4) Circumstances; (5) Uncertainty; (6) Cumulative EffectsThe tolerable misstatement is the amount by which a particular account may be misstated, yet still not cause the financia l statements taken as a whole to be materially misleading.练习:(1) Explain the relationship between Materiality, Audit risk and Auditevidence.(2) Discuss the criteria which would determine whether the following sale of an asset would be deemed to be material and require disclosure in the financial statements.AB, a public limited company, manufactures engineering parts, and is preparing its financial statements for the year ending 31 December 2007. AB has sold a building to one of its directors who retired on 31 December 2007. The selling price of the building wa s 500,000 a nd the company made profit of 200,000 on the transaction. If the building price index rises more than 50 percent in the next two years then a further 100,000 becomes payable by the director. The company does not normally sell building and this transaction is the first of its kind in the company records. The director was earning 400,000 per annum at the time of her retirement. The company normally makes profits of between 40 million and 50 million but the current year’s operating profits have drop ped to 3 million. The net assets of the company are 400 million and the carrying value of building in the balance sheet is 100 million.Answer:(a) Nature and incidence of the transactionThe company does not normally sell building and this transaction is the first of its kind.Also the transaction is with a related party.Although the profit on the transaction of 200,000 is unlikely to be material from the company’s point of view, it is likely to be material to the director, as the cost to the director exc eeds her annual salary. When considering materiality, the auditor has also to consider the needs of users and so it is likely that this transaction would be considered material by users.(b) SizeThe size of the profit (200,000) is material based on the op erating profit, as it accounts for 6.7% of operating profit. But the size of net assets makes the sale of building immaterial.(c) DisclosureUnder CAS××, the profit on sale of tangible non-current assets may be disclosed separately depending on size. As discussed above,the net profit on sale is 6.7% of operating profit and so could be deemed to be significant; particularly as this is the first transaction of its type carried out by the company.(d) ContingencyUnder CAS××, the auditors also need to consid er whether a provision needs to be made for the additional 100,000 that coul d become payable by the director, within the next two years. The contingency is likely to occur, otherwise the provision would not be included in the contract. However, is the contingent asset of 100,000 immaterial? Once again, it is down toprofessional judgment as to whether the contingency is material. Taking all the above items together, it is likely that the sale of the asset is material taking particular note of the nature and incidence of the transaction. Therefore it is likely to be disclosed in the accounts, probably in accordance with CAS ×× Related Party Disclosures.4.分析性复核程序Analytical proceduresAnalytical procedures are normally used at three stages of the audit: (1) planning, (2) substantive testing, and (3) overall review at the conclusion of an audit. They are required during the planning and overall review stages.Analytical procedures are used for 3 purposes:(1) Planning nature, timing, and extent of other auditing procedures(2) Substantive tests about particular assertions(3) Overall review in the final stage of audit5.制定审计计划Planning an audit6.审计记录:工作底稿Audit documentation: working papers7.利用其他人的工作Using the work of others· Rely on the work of experts· Rely on the work of internal audit三、内部控制Internal controlInternal control is a process effected by an entity’s boa rd of directors, management, and other personnel—designed to provide reasonable assurance regarding the achievement of objectives in the following categories: (1) reliability of financial reporting, (2) effectiveness and efficiency of operations, and (3) compliance with applicable laws and regulations.Five components of internal control(1) control environment(2) risk assessment(3) control activities(4) information and communication(5) monitoring1.内部控制系统评价内部控制系统评价The evaluation of internal control systems· Tests of control· Substantive procedures (time, nature, extent)交易循环:收入循环、采购循环、生产循环、融资与投资循环,等等Transaction cyclesRevenue and collection cycle, Purchase and expenditur e cycle, Production and payroll cycle, Finance and investment cycle.2.审计证据Audit evidence获取充分、适当的审计证据Obtain sufficient, appropriate audit evidence财务报表所包含的认定:完整性,发生,存在,计价,表达和披露,权利和义务,估价Assertions contained in the financial statements: completeness, occurrence, existence, measurement, presentation and disclosure, rights and obligations, valuation具体项目的审计The audit of specific items· Receivables: confirmation· Inventory: counting, cut-off, confirmation of inventory held by third parties· Payables: supplier statement reconcilia tion, confirmation· Bank and cash: bank confirmation审计抽样Auditing sampling: is the application of an audit procedure to less than 100% of the items within an account balance or class of transactions for the purpose of evaluating some characteristic of th e balance or class. Audit procedure: refers to actions described as general audit procedures (recalculation, physical observation, confirmation, verbal inquiry, document examination, scanning, and analytical procedures).An account balance: refers to a con trol account made up of many constituent items (for example, an account receivable control account representing the sum of customers’accounts, an inventory control account representing the sum of various goods in inventory, a sales account control account representing the sum of many sales invoices, or a long-term debt account representing the sum of several issues of outstanding bonds).A class of transactions: refers to a group of transactions having common characteristics, such as cash receipts or cash disbursements, but which are not simply added together and presented as an account balance in financial statements.Population(总体)is the set of all items that constitute an account balance or class of transactions.A sample(样本)is a set of sampling units.抽样风险(sampling risk)和非抽样风险(nonsampling risk)Sampling risk is defined as the probability that an auditor’s conclusion based on a sample might be different from the conclusion based on an audit of the entire population.控制测试中的抽样风险:信赖过度风险和信赖不足风险Sampling risk in test of controls includes overdependence risk and underdependence risk.细节测试中的抽样风险:误受风险和误拒风险Sampling risk in substantive test comprises the risk of incorrect acceptance and the risk of incorrect rejection.信赖过度风险和误受风险影响审计的效果,信赖不足风险和误拒风险影响审计的效率。

100篇英文经典文献

share with 各位会计、财务专业的同学...(P.S.读英文期刊绝对是体力活...开读前一定要吃好睡好...)这些是会计学的基础文献,是所有其他文献的参考文献~~~经典文献(The 100 articles with the highest citation index-until 1996)参考:Lawrence D. Brown, 1996, “Influential Accounting Articles, Individuals, Ph. D Granting Institutions and Faculties; A Citational Analysis”, Accounting, Organizations and Society, Vol.21, NO.7/8, P726-7281. Ball, R. an d Brown, P., 1968, “An Empirical Evaluation of Accounting Income Numbers”, journal of Accounting Research, Autumn, pp. 159-1781. 2.Watts R.L., Zimmerman J., 1978, “Towards a Positive Theory of theDetermination of Accounting Standards”, The Accounting Review, pp. 112-1342. 3.Healy P.M, 1985, “The Effect of Bonus Schemes on Accounting Decisions”,Journal of Accounting and Economics, April, 85-1073.Hopwood A. G., “Towards an Organizational Perspective for the Study ofAccounting and Information Systems”, Accounting, Organizations and Society (No.1, 1978) pp. 3-144.Collins, D. W., Kothari, S. P., 1989, “An Analysis of Intertemporal andCross-Sectional Determinants of Earnings Response Coefficients”, journal ofAccounting & Economics, pp. 143-1815.EastonP.D, Zmijewski M.E, 1989, “Cross-Sectional Variation in the Stock MarketResponse to Accounting Earnings Announcements”, Journal of Accou nting andEconomics, 117-1416.Beaver, W. H., 1968, “The Information Content of Annual EarningsAnnouncements”, journal of Accounting Research, pp. 67-927.Holthausen R.W., Leftwich R.W., 1983, “The Economic Consequences ofAccounting Choice: Implications of Costly Contracting and Monitoring”, journal of Accounting & Economics, August, pp77-1178.Patell J.M, 1976, “Corporate Forecasts of Earnings Per Share and Stock PriceBehavior: Empirical Tests. Journal of Accounting Research, Autumn, 246-2769.Brown L.D., Griffin P.A., Hagerman R.L., Zmijewski M.E, 1987, “An Evaluation ofAlternative Proxies for the Market’s Assessment of Unexpected Earnings”, Journal of Accounting and Economics, 61-8710.Ou J.A., Penman S.H., 1989, “Financial Statement Analysis a nd the Prediction ofStock Returns”, Journal of Accounting and Economics, Nov., 295-32911.William H. Beaver, Roger Clarke, William F. Wright, 1979, “The Associationbetween Unsystematic Security Returns and the Magnitude of Earnings ForecastErrors,” Journa l of Accounting Research, 17, 316-340.12.Burchell S., Clubb C., Hopwood, A., Hughes J., Nahapiet J., 1980, “The Roles ofAccounting in Organizations and Society”, Accounting, Organizations and Society, No.1, pp. 5-2813.Atiase, R.K., 1985, “Predisclosure Info rmation, Firm Capitalization, and SecurityPrice Behavior Around Earnings Announcements”, journal of Accounting Research, Spring, pp.21-36.ler P., O'Leary T., 1987, “Accounting and the Construction of the GovernablePerson”, Accounting, Organizations and Society, No. 3, pp. 235-26615.O'Brien P.C., 1988, “Analysts' Forecasts As Earnings Expectations”, journal ofAccounting & Economics, pp.53-8316.Bernard, V. L., 1987, “Cross-Sectional Dependence and Problems in Inference inMarket-Based Accounting Researc h”, Journal of Accounting Research, Spring, pp.1-4817.Brown L.D., Griffin P.A., Hagerman R.L., Zmijewski M.E, 1987, “An Evaluation ofAlternative Proxies for the Market’s Assessment of Unexpected Earnings”, Journal of Accounting and Economics, 61-8718.Freem an, R. N., 1987, “The Association Between Accounting Earnings and SecurityReturns for Large and Small Firms”, journal of Accounting & Economics, pp.195-22819.Collins, D. W. , Kothari, S. P. and Rayburn, J. D., 1987, “Firm Size and theInformation Content of Prices with Respect to Earnings”, journal of Accounting & Economics, pp. 111-13820.Beaver, W. H., Lambert, R. A. and Morse, D., 1980, “The Information Content ofSecurity Prices, Journal of Accounting & Economics”, March, pp. 3-2821.Foster G., 1977, “Quar terly Accounting Data: Time-Series Properties andpredictive-Ability Results”, The Accounting Review, pp. 201-23222.Christie A.A., 1987, “On Cross-Sectional Analysis in Accounting Research”, journalof Accounting & Economics, December, pp. 231-25823.Loft A., 1986, “Towards a Critica1 Understanding of Accounting: The Case of CostAccounting in theU.K.”, 1914-1925, Accounting, Organizations and Society, No.2, pp.137-17024.GonedesN.J., Dopuch N., 1974, “Capital Market Equilibrium, InformationProduction, and Selecting Accounting Techniques: Theoretical Framework and Review of Empirical Work”, journal of Accounting, 48-12925.Bowen, R. M. , Noreen, E. W. and Lacey, J. M., 1981, “Determinants of theCorporate Decision to Capitalize Interest”, Journal of Accounting & E conomics, August, pp151-17926.Hagerman R.L, Zmijewski M.E, 1979, “Some Economic Determinants of AccountingPolicy Choice”, Journal of Accounting and Economics, August, 141-16127.Burchell S., Clubb, C. and Hopwood, A. G., 1985, “Accounting in its Socia1 Conte xt:Towards a History of Value Added in theUnited Kingdom”, Accounting,Organizations and Society, No. 4, pp.381-41428.Leftwich R.W, 1981, “Evidence of the Impact of Mandatory Changes in AccountingPrinciples on Corporate Loan Agreements”, Journal of Accoun ting and Economics, 3-3629.Bernard, V. L. and Thomas, J . K., 1989, “Post-Earnings Announcement Drift:Delayed Price Response or Risk Premium?”, Journal of Accounting Research, pp.1-3630.WattsR.L., Zimmerman J.L., 1979, “The Demand for and Supply of Account ingTheories: The Market for Excuses”, The Accounting Review, April, pp. 273-305 31.Armstrong J.P., 1987, “the rise of Accounting Controls in British CapitalistEnterprises”, Accounting, Organizations and Society, May, pp. 415-43632.Beaver, W. H. , Lambert, R. A. and Ryan, S. G., 1987, “The Information Content ofSecurity Prices: A Second Look”, journal of Accounting & Economics, July, pp.139-15733.Chambers, A. E., Penman, S.H, 1984, “Timeliness of Reporting and the Stock PriceReaction to Earnings Announcemen ts”, journal of Accounting Research, Spring, pp.21-4734.Collins D.W., Rozeff M.S., Dhaliwal D.S., 1981, “The Economic Determinants of theMarket Reaction to Proposed Mandatory Accounting Changes in the Oil and Gas Industry: A Cross-Sectional Analysis”, Jou rnal of Accounting and Economics, 37-71 35.Holthausen R.W., 1981, “Evidence on the Effect of Bond Covenants andManagement Compensation Contracts on the Choice of Accounting Techniques: The Case of the Depreciation Switch-Back”, journal of Accounting & Economics, March, pp. 73-10936.ZmijewskiM.E., Hagerman R.L., 1981, “An Income Strategy Approach to thePositive Theory of Accounting Standard Settings/Choice”, Journal of Accounting and Economics, 129-14937.Lev B., Ohlson J.A, 1982, “Market-Based Empirical Research in Accounting: AReview, Interpretation, and Ext ension”, Journal of Accounting Research, 249-322 38.Ou J. and Penman S.H., 1989, “Financial Statement Analysis and the Prediction ofStock Returns”, Journal of Accounting and Economics, Nov., 295-32939.Bruns Jr. W.J, Waterhouse, J., 1975, “Budgetary Control a nd OrganizationStructure”, journal of Accounting Research, Autumn, pp. 177-20340.Tinker A.M., Merino B.D., Neimark M., 1982, “The Normative Origins of PositiveTheories: Ideology and Accounting Thought, Accounting, Organizations andSociety”, No. 2, pp. 167-20041.Foster, G., 1980, “Accounting Policy Decisions and Capital Market Research”,journal of Accounting & Economics March, pp. 29-6242.Gibbins M., 1984, “Propositions About the Psychology of Professional Judgement inPublic Accounting”, Journal of Account ing Research, Spring, pp. 103-12543.Hopwood A.G, 1983, “On Trying to Study Accounting in the Contexts in which itOperates”, Accounting, Organizations and Society, No. 2/3, pp. 287-30544.Abdolmohammadi M.J., Wright A., 1987, “An Examination of the Effects ofExperience and Task Complexity on Audit Judgments”, The Accounting Review, pp.1-1345.Berry, A. J., Capps, T., Cooper, D.,Ferguson, P., Hopper, T. and Lowe, E. A., 1985,“Management Control in an Area of the NCB: Rationales of Accounting Practices ina Pub lic Enterprise”, Accounting, Organizations and Society, No.1, pp.3-2846.Hoskin, K.W., Macve R.H, 1986, “Accounting and the Examination: A Genealogy ofDisciplinary Power”, Accounting, Organizations and Society, No. 2, pp. 105-136 47.Kaplan R.S, 1984, “The Evolution of Management Accounting”, The AccountingReview, 390-34148.Libby R., 1985, “Availability and the Generation of Hypotheses in Analytica1Review”, journal of Accounting Research, Autumn, pp. 648-66749.Wilson G.P., 1987, “The Incremental Information Con tent of the Accrual and FundsComponents of Earnings After Controlling for Earnings”, the Accounting Review, 293-32250.Foster, G., Olsen, C., Shevlin T., 1984, “Earnings Releases, Anomalies, and theBehavior of Security Returns”, The Accounting Review, Octo ber, pp.574-603 51.Lipe R.C., 1986, “The Information Contained in the Components of Earnings”,journal of Accounting Research, pp. 37-6852.Rayburn J., 1986, “The Association of Operating Cash Flows and Accruals WithSecurity Returns”, Journal of Accounting Re search, 112-13753.Ball, R. and Foster, G., 1982, “Corporate Financial Reporting: A MethodologicalReview of Empirical Research”, journal of Accounting Research, pp. 161-234 54.Demski J.S, Feltham G.A, 1978, “Economic Incentives in Budgetary ControlSystems”, The Accounting Review, 336-35955.Cooper D.J, Sherer M.J, 1984, “The Value of Corporate Accounting Reports:Arguments for a Political Economy of Accounting”, Accounting, Organizations and Society, No.3, 207-23256.Arrington, C. E., Francis J.R., 1989, “Letting the Chat Out of the Bag:Deconstruction privilege and Accounting Research”, Accounting Organization and Society, March, pp. 1-2857.Fried, D., Givoly, D., 1982, “Financial Analysts' Forecasts of Earnings: A BetterSurrogate for Market Expectations”, journal of Accounting & Economics, October, pp. 85-10758.Waterhouse J. H., Tiessen P., 1978, “A Contingency Framework for ManagementAccounting Systems Research”, Accounting, Organizations and Society, No.3,pp.65-7659.Ashton, R .H., 1974, “Experimental Study of In ternal Control Judgment journal ofaccounting Research”, 1974, pp. 143-15760.Collins D. W., Dent, W. T., 1979, “The Proposed Elimination of Full Cost Accountingin the Extractive Petroleum Industry: An Empirical Assessment of the MarketConsequences”, journ al of Accounting & Economics, March, pp. 3-4461.Watts R.L., Leftwich, R. W., 1977, “The Time Series of Annual Accounting Earnings,journal of Accounting Research”, Autumn, pp. 253-27162.Otley D.T, 1980, “The Contingency Theory of Management Accounting:Achievement and Prognosis”, Accounting, Organizations, and Society, NO. 4,413-42863.Hayes D.C, 1977, “The Contingency Theory of Managerial Accounting”, TheAccounting Review, January, 22-3964.Bea ver, W. H. ,Griffin, P. A. and Landsman, W. R., 1982, “The IncrementalInformation Content of Replacement Cost Earnings”, Journal of Accounting &Economics, July, pp. 15-3965.Libby R., Lewis B.L., 1977, “Human Information Processing Research in Accounting:The State of the Art”, Accounting, Organizations and Society, No.3, pp. 245-268 66.Schipper W., Thompson R., 1983, “The Impact Mergers-Related Regulations onthe Shareholders of Acquiring Firms”, Journal of Accounting Research, 184-221 67.Antle, R., Smith, A., 1986, “An Empirical Investigation of the Relative PerformanceEvaluation of Corporate Executives”, journal of Accounting Research, spring,pp.1-39.68.GonedesN.J., Dopuch N., Penman S.H., 1976, “Disclosure Rules,Information-Production, and Capital Market Equilibrium: The Case of ForecastDisclosure Rules”, Journal of Accounting Research, 89-13769.Ashton, A. H. and Ashton, R. H., 1998, “Sequential Belief Revision in Auditing”, TheAccounting Review, October, pp. 623-641rcker D.F, 1983, “The Association Be tween Performance Plan Adoption andCorporate Capital Investment”, Journal of Accounting and Economics, 3-3071.McNichols M., Wilson G.P., 1988, “Evidence of Earnings Management from theProvision for Bad Debts”, journal of Accounting Research, pp.1-3172.Tomk ins C., Groves R., 1983, “The Everyday Accountant and Researching HisReality”, Accounting, Organizations and Society, No 4, pp361-37473.Dye R.A, 1985, “Disclosure of Nonproprietary Information”, Journal of AccountingResearch, 123-14574.Biddle, G. C. and Li ndahl F. W., 1982, “Stock Price Reactions to LIFO Adoptions:The Association Between Excess Returns and LIFO Tax Savings”, Journal ofAccounting Research, 1982, pp. 551-58875.Joyce E.J., 1976, “Expert Judgment in Audit Program Planning”, journal ofAccounting Research, pp. 29-6076.Kaplan R.S, 1983, “Measuring Manufacturing Performance: A New Challenge forManagerial Accounting Research”, The Accounting Review, 686-70577.Ball R., 1972, “Changes in Accounting Techniques and Stock Prices”, journal ofAccounting Research, Supplement, pp. 1-3878.Ricks W.E, 1982, “The Market’s Response to the 1974 LIFO Adoptions”, Journal ofAccounting Research, 367-38779.Albrecht, W. S., Lookabill L. L., McKeown, J.C., 1977, “The Time-Series Propertiesof Annual Earnings”, journal of Accounting Research, Autumn, pp. 226-24480.DeAngelo L.E, 1981, “Auditor Size and Audit Quality”, Journal of Accounting andEconomics, 183-19981.Merchant K.A., 1981, “The Design of the Corporate Budgeting System: Influenceson Managerial Behavioral and Perfor mance”, The Accounting Review, October, pp.813-82982.Penman S.H, 1980, “An Empirical Investment of the Voluntary Disclosure ofCorporate Earnings Forecasts of Earnings”, Journal of Accounting Research,132-16083.Simunic D., 1980, “The Pricing of Audit Services: Theory and Evidence”, Journal ofAccounting Research, 161-19084.Waller W. S., Felix Jr. W.L., 1984, “The Auditor and Learning from Experience:Some Conjectures”, Accounting, Organizations and Society, No. 3, pp. 383-408 85.Dyckman T.R, Smith A.J, 1979, “Financial Accounting and Reporting by Oil and GasProducing Companies: A Study of Information Effects”, Journal of Accounting and Economics, 45-7586.Holthausen R.W., Verrecchia R.E., 1988, “The Effect of Sequential InformationReleases on the Variance of Price Changes in an Intertemporal Multi-Asset Market”, journal of Accounting Research, Spring, pp.82-10687.Hopwood A. G., 1978, “Towards an Organizational Perspective for the Study ofAccounting and Information Systems”, Accounting, Organizations and Society, No.1, pp. 3-1488.Leftwich R.W, 1983, “Accounting Information in Private Markets: Evidence fromPrivate Lending Agreements”. The Accounting Review, 23-4289.Otley D.T, 1978, “Budget Use and Managerial Performance”, Journal of AccountingResearch, Spring, 122-14990.Griffin, 1977, “The time-series Behavior of Quarterly Earnings: PreliminaryEvidence”, Journal of Accounting Research, spring, 71-8391.Brownell P., 1982, “The Role of Accounting Data in Performance Evaluation,Budgetary Participation, and Organizational Effectiveness”, journal of Accounting Research, Spring, pp. 12-2792.Dhaliwal D.S, Salamon G.L, Smith E.D, 1982, “The effect of Owner Vs ManagementControl on the Choice of Accounting and Economics”, 41-5393.Hopwood A.G., 1972, “An Empirical Study of the Role of Accounting Data inPerformance Evaluation”, journal of Accounting Research, pp. 156-18294.Foster, G., 1981, “Intra-Industry Information Transfers Associated with EarningsReleases”, journal of Accounting & Economics, December, pp. 201-23295.Chua, W. F., 1986, “Radical Developments in Accounting Thought”, TheAccounting Review, October, pp601-63296.Hughes P.J., 1986, “Signalling by Direct Disclosure Under Asymmetric Information”,journal of Accounting & Economics, June, pp. 119-14297.Kinney W.R. Jr., 1986, “Audit Technology and Preference for Auditing Standards”,Journal of Accounting and Economics, 73-8998.Titman S., Trueman B., 1986, “Information Quality and the Valuation of NewIssues”, journal of Accounting& Economics, pp. 159-17299.Wilson G.P., 1986, “The Relative Information Content of Accruals andCash Flows: Combined Evidence at the Announcement and Annual Report Release Date”, Journal of Accounting Research, 165-203。

谈谈你对会计的理解英文作文