Chaper131

Chapter11_PPT

– Sever problems

• Prevent normal execution – Notification – Termination

2002 Prentice Hall. All rights reserved.

4

11.2

Exception Handling Overview

• Program detects error

2002 Prentice Hall. All rights reserved.

7

11.2

• Finally block

Exception Handling Overview

– Appears after last Catch handler – Optional (if one or more catch handlers exist) – Encloses code that always executes

The appropriate error message dialog is displayed for the user

2002 Prentice Hall.

All rights reserved.

Outline

10

DivideByZeroTest .vb

2002 Prentice Hall.

33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63

' Convert.ToInt32 generates FormatException if argument ' is not an integer Dim numerator As Integer = _ Convert.ToInt32(txtNumerator.Text) Dim denominator As Integer = _ Convert.ToInt32(txtDenominator.Text) ' division generates DivideByZeroException if ' denominator is 0 Dim result As Integer = numerator \ denominator lblOutput.Text = result.ToString() ' process invalid number format Catch formattingException As FormatException MessageBox.Show("You must enter two integers", _ "Invalid Number Format", MessageBoxButtons.OK, _ MessageBoxIcon.Error) ' user attempted to divide by zero Catch dividingException As DivideByZeroException MessageBox.Show(dividingException.Message, _ "Attempted to Divide by Zero", _ MessageBoxButtons.OK, MessageBoxIcon.Error) End Try End Sub ' cmdDivide_Click End Class ' FrmDivideByZero

advanced accounting Chapter 13 - Solution Manual

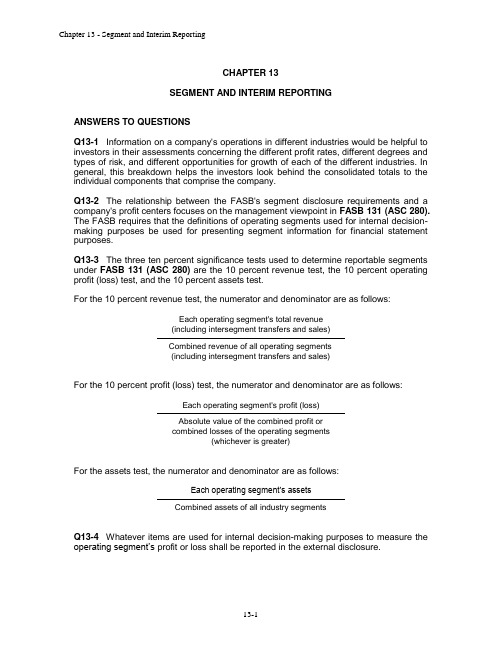

CHAPTER 13SEGMENT AND INTERIM REPORTINGANSWERS TO QUESTIONSQ13-1 Information on a company's operations in different industries would be helpful to investors in their assessments concerning the different profit rates, different degrees and types of risk, and different opportunities for growth of each of the different industries. In general, this breakdown helps the investors look behind the consolidated totals to the individual components that comprise the company.Q13-2 The relationship between the FASB's segment disclosure requirements and a company's profit centers focuses on the management viewpoint in FASB 131 (ASC 280). The FASB requires that the definitions of operating segments used for internal decision-making purposes be used for presenting segment information for financial statement purposes.Q13-3 The three ten percent significance tests used to determine reportable segments under FASB 131 (ASC 280) are the 10 percent revenue test, the 10 percent operating profit (loss) test, and the 10 percent assets test.For the 10 percent revenue test, the numerator and denominator are as follows:Each operating segment's total revenue(including intersegment transfers and sales)Combined revenue of all operating segments(including intersegment transfers and sales)For the 10 percent profit (loss) test, the numerator and denominator are as follows:Each operating segment's profit (loss)Absolute value of the combined profit orcombined losses of the operating segments(whichever is greater)For the assets test, the numerator and denominator are as follows:Each operating segment’s assetsCombined assets of all industry segmentsQ13-4 Whatever items are used for internal decision-making purposes to measure the operating segment’s profit or loss shall be reported in the external disclosure.Q13-5 Any segments passing one of the 10 percent tests would also be disclosed. The lower limit for the number of segments to be disclosed is set by the 75 percent revenue test. If the assumption is made that the largest four segments fail the 75 percent test and the largest five segments pass the 75 percent test, then the five segments should be separately reported. The remaining segments, if they fail the 10 percent tests, are combined under the heading of "Other Segments" and not defined further.Q13-6 First, FASB 131 (ASC 280)specifies that all companies should disclose revenues and long-lived, productive assets domestically and, in total, for all foreign activities. The two materiality tests applied to country-based foreign operations are the 10 percent revenue test and the 10 percent long-lived asset test. The profit or loss test is not used for foreign operations because of the many differences in tax structures and accounting practices in different geographic areas.Q13-7 A company must disclose for each of its significant customers the amount of sales to these customers and the associated industry segment. The names of the individual customers need not be disclosed, although some companies do disclose the names of the customers.Q13-8 Interim reports can be used by investors to identify a company's seasonal trends by identifying the pattern of revenue and expenses as they occur each interim period.Q13-9 The discrete view of interim reporting holds each interim period as a basic accounting period to be evaluated as if it were an annual accounting period. Any end-of-period adjustments and deferrals would be determined using the same accounting principles used for the annual report. The integral view of interim reporting holds each interim period as an installment of an annual period. Recognition and adjustment of certain income or expense items may be affected by judgments about the expected results of the entire year's operations. APB Opinion 28 (ASC 270 and 740) uses the integral view of interim reporting.Q13-10 Revenue from products sold or services rendered should be recognized as earned during an interim period on the same basis as followed for the full year. Revenue from seasonal businesses cannot be manipulated to eliminate seasonal trends.Q13-11 Those costs and expenses that are associated directly with or allocated to the products sold or to the services rendered for annual reporting purposes should be treated similarly for interim reporting purposes. The following practical modifications are allowed to the general rule:a. Estimated gross profit rates may be used to determine an interim period's cost ofgoods sold.b. Temporary reductions of inventories expected to be replaced by the end of thefiscal year should not be expensed through cost of goods sold at historical cost if the company uses the LIFO inventory valuation method. The expected replacement cost of the liquidated portion of the LIFO base should be used for the interim period's cost of goods sold.c. Inventory losses due to a decline in market prices are recognized in the period ofdecline using the lower-of-cost-or-market valuation method. Recoveries of market prices in later interim periods of the same fiscal year should be recognized as gains (recoveries of prior losses) in the later interim period.d. Companies using a standard cost system for inventories should use the sameprocedures for computing and reporting variances in an interim period as used for the fiscal year. Purchase price variances or volume or capacity variances that are expected to be absorbed by the end of the fiscal year should be deferred at the interim period and should not be included in the interim income.Costs and expenses other than product costs should be charged to income in interim periods as incurred or be allocated among interim periods based on an estimate of the time expired, benefit received, or activity associated with the periods.Q13-12 The application of the lower-of-cost-or-market valuation method differs between interim statements and annual statements when temporary market declines are expected to reverse by the end of the fiscal year. When a temporary market decline is experienced, the decline need not be recognized at the interim date because no loss is expected for the fiscal year.Q13-13 The integral theory of interim reporting would allocate the expenditure over the interim periods benefited. Thus, a portion of the $200,000 might be recognized over one or more interim periods. The discrete theory of interim reporting would recognize the entire $200,000 in the interim period when the expenditure was made.Q13-14 At the end of the second interim period, the company should make its best estimate of the effective tax rate expected to be applicable for the full fiscal year. The rate so determined should be used in providing for income taxes on a current year-to-date basis. The effective annual tax rate should reflect anticipated investment tax credits, foreign tax rates, percentage depletion, capital gains rates, and other available tax planning alternatives. In arriving at this effective annual tax rate, no effect should be included for the tax related to significant unusual or extraordinary items that will be separately reported or reported net of their related tax effect in reports for the interim period or for the fiscal year.Q13-15 If the future realizability of the tax benefit is not assured beyond a reasonable doubt, the tax benefit is not shown in the interim statements.Q13-16 Extraordinary items should be disclosed separately, included in the determination of net income for the interim period in which they occur, and shown net of applicable taxes. In determining materiality, extraordinary items should be related to the estimated income for the full fiscal year.Q13-17 A change in accounting principle made in an interim period is reported using the retrospective application process. The balance sheet for the earliest period presented (usually an annual period) is adjusted for the cumulative amount of the change as of the beginning of that year. Then, all subsequent annual and interim financial statements shall be adjusted to the newly adopted accounting principle. In the example of an inventory change, all the financial statements presented must be adjusted to the new method, the average cost method. The balance sheet for the earliest period presented must include the cumulative effect as of the change computed as of the beginning of that first period presented.SOLUTIONS TO CASESC13-1 Segment Disclosures [CMA Adapted]a. The purpose for requiring segment information to be disclosed in financial statements is to assist financial statement users in analyzing and understanding the enterprise's financial statements by permitting better assessment of the enterprise's past performances and future prospects.b. The determination of the segments appropriate for an enterprise is the responsibility of management; that is, management should use its judgment in deciding how to report its segment information. Specific characteristics or sets of characteristics management can use in determining how to group its products into segments include the following:1. Use of existing profit centers.2. A segment shall be regarded as significant and identified as a reportablesegment if one or more of the following are satisfied:i. 10% or more of the total revenue is derived from one segment.ii. 10% or more of the greater in absolute amount of the aggregate profitsor aggregate losses is contributed by the segment.iii. 10% of the combined assets can be associated with the segment.3. Management has the ability to define the breakdown of the segments, but thesegment definitions used for external purposes must be the same as used for internal decision making purposes.c. The options available to Chemax Industries are as follows:1. Segment by product line — antihistamines. This single product meets the 10percent test and can be anticipated as a significant product line in the future.2. Segment by product group —pharmaceutical, medical instruments, andmedical supplies. Antihistamines can be carried as a part of the pharmaceutical group.3. Disaggregate pharmaceutical into ethical and proprietary drugs and carryantihistamines under whichever industry segment is appropriate (probably proprietary drugs, in this case).C13-2 Matching Revenue and Expenses for Interim Periodsa. Revenue, product costs, gains, and losses should be recognized for interim periods on the same bases as for an annual period. These items should be recognized in the period earned or incurred and should not be deferred or allocated to other interim periods.b. Cost of goods sold and inventory valuation requires several estimations because physical counts typically are not made for interim periods. Cost of goods sold may be estimated using the gross profit method. Temporary liquidations of LIFO layers are priced using the replacement costs of the goods, not the LIFO cost. Temporary reductions in the market value below cost under the lower-of-cost-or-market rule do not need to be recognized in an interim period. However, reductions in value that may be permanent must be recognized. A loss recovery is allowed for recoveries of market value from one interim to another.c. Period costs are those such as depreciation or other amortizations and allocations. These should be allocated to each interim period based on a reasonable allocation method such as straight-line or percentage of the interim period's revenue to expected annual revenue.d. Accounting treatment for interim statements:1. Long-term contracts — These contracts are accounted for on the same basis as forthe annual period. Percentage-of-completion estimates are made each interim and gross profit is recognized. If the completed contract method is used, then profit is recognized only for projects completed within the interim period.2. Advertising costs — These costs may be capitalized and allocated to the interimperiods that benefit. However, no advertising costs are deferred beyond the end of the annual fiscal period. The allocation should be on a reasonable basis such as the percentage of interim revenue to expected annual revenue. Advertising costs or other costs that will benefit more than one interim period may be deferred under the integral approach used for interim reporting.3. Seasonal revenue —Revenue must be recognized in the period earned. Thecompany may not defer revenue from one interim to another in an attempt to smooth the revenue stream.4. Flood loss — Extraordinary items must be recognized in the interim period in whichthe event occurs.5. Annual major repairs and maintenance — Unusually large and nonrecurring costsmay be capitalized to the asset and carried past the end of the fiscal period.However, normal maintenance and repairs may not be carried beyond the end of the fiscal year. Some accountants account for repairs on an interim basis by charging each of the interim periods with a proportionate amount of the annual repair cost and establishing an allowance for repairs contra account to the plant and equipment account. The expenditure is then charged against the allowance account. Other accountants would charge the entire cost off in the interim period in which the expenditure is made.C13-3Segment Disclosures in the Financial Statements [CMA Adapted]a. A subdivision of an entity is a reportable segment if one of the following tests is met:1. Revenue, both unaffiliated and intersegment revenue, is ten percent or more oftotal revenue, which includes intersegment revenue. For each of Bennett's segments, divide the sum of the unaffiliated sales and intersegment sales by total company sales of $63,000. If the result is ten percent or more, the revenue test is met for that specific segment.2. The absolute value of profit or loss is ten percent or more of the greater of eitherthe total profit of segments that did not incur a loss or the total, in absolute amounts, of the segments that did incur a loss. For each segment, divide the absolute value of the profit or loss by the sum of the segment profits of $6,200. If the result is ten percent or more, the segment profit or loss test is met for that specific segment.3. Assets are ten percent or more of total assets. For each segment, divide the valueof the assets by total assets of $100,000. If the result is ten percent or more, the assets test is met for that specific segment.The calculations for the segments of Bennett Inc. yield results that show that all segments are reportable with the exception of Security Systems, which does not meet any of the tests. See the results of all the tests in the table below.Bennett Inc.Results of Required Tests for Determining Segment ReportingFor the Year Ended December 31, 20X5Power Fastening Household Plumbing SecurityTools Systems Products Products Systems Revenue 0.67 0.16 0.08 0.06 0.03 Profit 0.73 0.16 0.10 0.11 0.02 Assets 0.50 0.23 0.17 0.06 0.04 Reportable Yes Yes Yes Yes Nob. For the reportable segments of Bennett Inc. to represent a substantial portion of total operations, the combined revenue from sales to unaffiliated customers of all reportable segments must be at least 75 percent of the total sales for the company as a whole. Since the sales to unaffiliated customers of Bennett's reportable segments are $44,300 and represent approximately 96 percent of the company's total sales ($44,300 / $46,300), this criterion would be met.C13-4 Determining Industry and Geographic Segmentsa. This is an actual case adapted from experiences with a large, publicly-held U.S. company. The U.S. company's management was reluctant to disclose information about the Canadian operation's profitability because of the desire to maintain its economic competitiveness, and because of fear that Canadian authorities might want to increase regulation of non-Canadian owned companies operating in Canada.b. Under FASB 131 (ASC 280), the U.S. company must present its segmental disclosures based on the definition of operating segments as used for internal decision making. Therefore, if the management of the company felt that the two product lines were sufficiently comparable, management could aggregate the two product lines in the same operating segment for internal decision-making purposes. Then, because the two product lines were in one operating segment for internal decision-making purposes, they would be considered one operating segment for external disclosure purposes under FASB 131 (ASC 280). However, FASB 131 (ASC 280)also requires separate disclosure of revenues by product line. The company could still be required to disclose revenue information about the pasta product line.One interpretation the company could use to postpone separately disclosing detailed information about its pasta business is to argue that the pasta business passed one of the 10 percent tests in the current year because of some unusual, one-time events that are not expected to continue. Thus, if a segment becomes reportable in a single period because of some significant one-time events, the company may choose not to include it as a separately reportable segment. However, if in the next year, the pasta business continues to meet the separately reportab le segment tests, then the company’s management would not be able to use this argument.c. FASB 131 (ASC 280)requires separate disclosure of total revenues from external customers attributed to the domestic operations and the total attributed to all foreign operations. In addition, disclosure is required of the total of long-lived assets located in the country of the domestic operations and the total long-lived assets in all foreign countries. If the revenues or the long-lived assets in any individual country are material, then separate disclosure of the material revenues or significant amount of long-lived assets must be made for those specific countries. FASB 131 (ASC 280)did not specifically state a measure of materiality to be used in assessing foreign operations. Management does have the flexibility to determine the basis of assigning revenues to specific countries. For example, in this case, management may argue that the revenues should be based on the point-of-sale to the eventual consumer. Thus, sales of the pasta products in the U.S. would be assignable to the U.S. domestic market even though the product may have been manufactured in Canada.C13-5 Segment Reportinga. A great amount of information can be found on a company’s homepage ranging fr om financial information to product information and company profiles. The internet address for many companies includes their company name. Your students may simply use a web browser to do a search for a specific company.b. EDGAR is a comprehensive database of SEC filings for all publicly held firms. The URL is http://www.se and EDGAR can be accessed from there. All SEC filings for publicly held firms are available in this database and the filings can be easily printed off for further use, if required.C13-6 Interim Reportinga & b.Internet URL: /info/edgar.shtmlThe above Internet address provides access to the SEC’s EDGAR database. From thi s page, the user is able to select "Search for Filings” on the left-hand side of the page. The user then selects the link to search by “Company or fund name…" This link takes you to EDGAR Company Search page at which you will enter the Company name. After clicking on the “Find Companies” button at the bottom of the screen, students will be taken to a listing of the companies with that name, and can select their specific company which will then take them to the listing of all SEC filings for that company and they can then quickly scroll down to find a Form 10-Q.In comparison to the Form 10-K, several differences in Form 10-Q are noted. The interim financial statements and footnotes are entirely unaudited. As the interim financial statements are unaudited, no report from the independent public accountants is provided in the Form 10-Q.C13-7 Defining Segments for DisclosureMEMOTo: Randy Rivera, CFO, Stanford CorporationFrom:Re: Segment DisclosuresFor the current annual reporting period, Stanford Corporation has identified four operating segments that meet the quantitative thresholds to be considered reportable segments under FASB Statement No. 131 (FASB 131; ASC 280).Neither the cereals segment nor the sports beverage segment meets any of the three quantitative thresholds in the current period. [FASB 131, Par. 18; ASC 280-10-50-12]However, the FASB 131 (ASC 280) quantitative thresholds are intended to insure that information about significant business segments is included in the disclosures, not to limit the information that can be provided.The cereals segment, which was disclosed as a reportable segment last year, can continue to be reported this year if its disclosure provides significant information for the users of the financial statements, even though the segment does not meet the specific criteria for separate disclosure specified in paragraph 22 of FASB 131 (ASC 280).In addition, the segment disclosure standard allows companies to designate additional operating segments as reportable segments. Management may decide to provide separate disclosure of segment information for other segments that management feels that the disclosure would be of information value to the users of the financial statements.Finally, paragraph 24 of FASB 131 (ASC 280-10-50-18) addresses the possibility that identification of too many reportable segments might result in overly detailed segment information. As a general guideline, the standard suggests that a reasonable limit of 10 segments should be used and smaller, somewhat comparable segments can then be combined for purposes of the footnote disclosure.As a result of my research, I conclude that it would be acceptable for Stanford to report information about six segments, including the cereals and sports beverage segments. Disclosure of information for six segments does not approach the practical limit on the number of segments suggested in FASB 131 (ASC 280). The continuing significance of the cereals segment and the developing significance of the sports beverage segment make their inclusion appropriate even though these segments do not meet the FASB 131 (ASC 280) quantitative thresholds in the current year.Primary referencesFASB 131, Par. 22; ASC 280-10-50-16FASB 135, Par. 4 (x) [replaces a section of FAS 131, Par. 18]Other referencesFASB 131, Par. 24; ASC 280-10-50-18C13-8 Income Tax Provision in Interim PeriodsMEMOTo: Andrea Meyers, Controller's Department, Vanderbilt CompanyFrom:Re: Income Tax Provision in Interim PeriodsIn computing the income tax provision for interim periods, APB 28 (ASC 270 and 740) states that the company should make its best estimate of the effective tax rate expected to be applicable for the year. [APB 28, Para. 19; ASC 740-270-30-6] This estimate should reflect all expected tax credits, and other tax rates, such as foreign taxes. Therefore, anticipated tax credits available to Vanderbilt should be included in the computation of the expected effective annual tax rate.However, the first quarter calculation of this tax rate cannot include the anticipated energy tax credit benefits because the tax law providing the energy tax credit has not yet been enacted into law.Vanderbilt's first quarter estimate of the effective annual tax rate should not include the expected tax benefits of the energy tax credit. Changes in the tax rate are to be recognized as changes in estimate, according to APB 28 (ASC 270 and 740). If the legislation is enacted as expected, the effect of the tax credit should be factored into the estimate of the effective annual tax rate made at the end of the third quarter, which would reduce the income tax provision for the third quarter of 20X5.Primary referencesAPB 28, Par. 19; ASC 740-270-30-6FAS 109, Par. 288(h) [replaces a sentence of APB 28, Par. 20]; ASC 740-20-45-11Other referencesAPB 28, Par. 26; ASC 270-10-45-14C13-9 Questions about Interim Reporting1. In their third-quarter 10-Q, a company would have the following four income statements for the respective reporting periods:a. An income statement for the third quarter and a comparative income statement for thethird quarter of the prior year.b. An income statement for the cumulative first three quarters of the current year and acomparative cumulative income statement for the first three quarters of the prior year. 2. FASB 154 (ASC 250) requires that a change in depreciation method be accounted for as a change in accounting estimate affected by a change in accounting principle. The current and prospective application is used and prior financial statements are not restated. Thus, the third quarter and subsequent periods would report with the new depreciation method.3. The company would report a condensed balance sheet as of the end of the third quarter and a condensed balance sheet as of the end of the prior fiscal year. However, a company should also provide a comparative, condensed balance sheet as of the end of the third quarter of the prior fiscal year if it is necessary for understanding the seasonal fluctuations on the company’s financial condition.4. No, interim financial statements do not need to be audited. However, some companies choose to have their interims audited. Summary amounts from the interim reports are included in the annual financial report and are subject to audit review at that time.5. FASB 131 (ASC 280) requires segment disclosures in each interim report. However, the level of detail of information required in the interim report is less than that required in the annual report.6. Publicly owned companies classified as accelerated filers must file their 10-Q within 35 days after the end of each of their first three quarters. Companies not meeting the criteria of accelerated files must file within 45 days after the end of each of their first three quarters.7. The methods of computing revenues for interim reporting should be the same as those used for the annual financial statements. The reason for this is so that financial statement users may properly determine the revenue patterns during the year. However, if a company makes a change in accounting principle that affects the computation of its revenues, the company must retroactively apply the new accounting principle to all prior interims.8. A company is not required to take a physical inventory at the end of each quarter although a physical inventory is required as part of the annual audit procedures. A company usually estimates ending inventory for each quarter based on beginning inventory plus purchases, less the cost of sales. The cost of sales is estimated using the normal mark-up percentages from cost to retail.9. Many companies allocate costs incurred in a quarter that benefit the entire year. A common example of this are the costs associated with retooling efforts during the short period the company is shut down each year for retooling to take place. Several allocation methods are allowed such as allocating a fourth of the retooling cost to each quarter or relating the retooling cost to proportional sales revenue during the year. The key point to selecting an allocation method is that the method must be rational and relate to the benefits received from the cost.C13-9 (continued)10. This is a change in accounting principle for which FASB 154 (ASC 250)requires a retrospective application. All prior periods, including prior interims, are restated to the new accounting principle (percentage-of-completion) for the direct effects of the change. This presumes that the company is able to determine the effects of the change on previous interim periods. Otherwise the company must wait until the first day of the next fiscal year to make the change.11. This is a change in estimate and is treated currently and prospectively. Prior interims are not restated for this change in estimates. The change in estimate would be made effective as of the first day of the interim period in which the change is made.。

遗传学复习大纲1

护理131-134

• 考试时间:6月10日6-7节

• 考试地点:待定

考试题型:

• • • • 一、名词解释6(30%) 二、单选10(20%) 三、是非10(20%) 四、简答计算3(30%)

第一章 绪论

基因 等位基因

复等位基因

遗传病

Chapter02 基因与染色体

• (全球共有,国际合作,即时公布,免费 共享)的百慕大原则

Chapter04 单基因遗传病

系谱

先证者 常染色体显性遗传(AD)

常染色体显性遗传-完全显性 病例举例: 短指(趾)、 并指Ⅰ型、 家族性多发性结肠息肉症 多囊肾病、 进行性舞蹈病、 多发性神经纤维瘤等。

常染色体显性遗传的遗传系谱特征

1.男女发病机率均等。由于致病基因在常染色体上,因而致病 基因的传递与性别无关。 2.连续传递。即系谱中每代都可能出现患者。 3.患者双亲之一常常是患者,而且大多数为杂合子。致病基因 是由双亲向后代传递,因此,双亲无病时,子女一般不患病。 如果双亲无病而子女患病,则可能是由于新基因突变引起的。 4.患者的子女(或患者的同胞中)约有1/2的机率患病。1/2的 患病机率在一个小家庭中很难体现,把许多患病类似的家庭 累计起来分析,我们发现正常个体约占1/2,患病个体约占 1/2。

四、不规则显性遗传 (irregular dominant inheritance)

在AD遗传中,杂合子(Aa)在不同的条件下,有的 表现显性性状,也有的表现隐性性状,或虽均表现显性 性状,但表现程度不同,使显性性状的传递不规则。 例:多指(趾), Marfan综合征

外显率(penetrance): 是指一个群体中 有致病基因的个体表现出相应病理表型 的百分率。

CHAPTER 核物理基础 截面与反应率

一立方厘米物质中全部原子核的微观截面之和称为宏观截面, 用Σ表示:

Σ = N *σ

N为核密度。Σ的单位是cm-1 ,表示中子在物质中每穿行一厘米 与原子核发生核反应的几率。

微观截面

Microscopic cross section

R

I

NA

# cm2s

宏观截面

Macroscopic cross section

N

[cm1] [# / cm3 ][cm2 ]

N为单位体积内原子核的数目。 表征了一个中子和单位体积内所有的原子核发

生反应的概率大小。 为一个中子在介质内穿行单位距离与原子核发

生反应的概率大小。

宏观截面的物理解释

λ= 1 / Σ

散射平均自由程: s 1 s

吸收平均自由程: a 1 a

总自由程: t 1 t

111

t s a

核反应率

反应率: 单位时间、单位体积内发生某种核反 应的次数,是反应堆工程中最关心的量。

R = N σ n v (cm-3 sec-1)

令 ∑=N σ,则 R =∑ n v =n v /∑-1 =n v/λ N:物质原子核密度,cm-3 n:中子密度,cm-3 v:中子飞行速度,cm/sec σ:微观截面, [σ] = [R N-1n-1v-1] = [cm2] ∑:宏观截面,[∑] = [cm-3 cm2] = [ cm-1 ] λ=∑-1:平均自由程,[λ]=[ cm ]

1原子质量单位(amu)= 1.66 x 10-24 克

核(分子)密度 ––– 单位体积的核子(分子)数 N = Na *ρ/A,

Na = 0.6022*1024是阿伏伽德罗常数( A克该物质的 核子(分子)数),ρ为该物质的密度(克/立方厘米 ),A为该物质的原子量(分子量)。 例:水的分子密度,一氧化二氢

威尼斯商人每幕英文概括

威尼斯商人每幕英文概括【篇一:威尼斯商人每幕英文概括】chapter 1:威尼斯商人安东尼欧是个宽厚为怀的富商,与另外一位犹太人夏洛克的高利贷政策恰恰相反。

他的一位好朋友因要向贝尔蒙一位继承了万贯家财的美丽女郎——波西亚——求婚,而向他告贷三千块金币,而安东尼欧身边已无余钱,只有向夏洛克以他那尚未回港的商船为抵押品,借三千块金币。

没想到夏洛克对安东尼欧往日与自己作对耿耿于怀,于是利用此一机会要求他身上的一磅肉代替商船。

在一番口舌之后,安东尼欧答应了,与他定了合约。

chapter 2:巴珊尼(安东尼欧的朋友)欢天喜地的到贝尔蒙脱去求亲了,在贝尔蒙脱,他的侍从葛来西安诺喜欢上了波西亚的侍女聂莉莎,两对新人在一个意外事件来临时,匆匆同时结了婚。

chapter 3:安东尼欧写了一封信来,信中说明了他的商船行踪不明,他立刻就要遭到夏洛克索取一磅肉的噩运,因这一磅肉可能会导致他性命不保,所以,他希望见到巴珊尼的最后一面……听到这个消息,巴珊尼与葛来西安诺赶紧奔回威尼斯,波西亚与聂莉莎也偷偷地化装成律师及书记,跟着去救安东尼欧。

chapter 4:在法庭上,波西亚聪明地答应夏洛克可以剥取安东尼欧的任何一磅肉,只是,如果流下一滴血的话(合约上只写了一磅肉,却没有答应给夏洛克任何一滴血),就用他的性命及财产来补赎,因此,安东尼欧获救,并且,庭上宣布以谋害威尼斯市民的罪名,没收其财产的三分之一,另外二分之一则给安东尼欧,而后者却把这笔意外的财产让给了夏洛克的女婿——罗伦佐,罗伦佐也是安东尼欧的朋友之一,又是个基督徒。

夏洛克见阴谋失败,也只好答应了,并遵依判决,改信基督教。

chapter 5:波西亚及聂莎莉戏弄了她们的丈夫,要回结婚戒指做为替安东尼欧辩护的代价,然后再回到家中,等她们丈夫回来时责备他们忽视了结婚戒指的意义,并咬定他们一定是把它们送给了别的女人,一连发窘的解释后,终于真象大白,除了夏洛克外,每个人都有一个满意的结局(安东尼欧的船只也顺利地到达港口里了)。

Chapter_11_12_Verb_tense_and_aspect

3. A future happening according to a definite plan or arrangement. He is leaving china in a few weeks. I’m going to Shanghai for the summer holiday.

5. If he cooks, I always wash up. If you heat metal, it expands. [a woman is talking about the relationship with her husband.] If he’s cooking for example a roast meal, or any kind of meal, I can sometimes sort of do the typical, you know, wife bit of going in the kitchen and saying, “Oh, I’ll take over.’

Use of past progressive p134

1. An action in progress at a definite point or period of past time 2. A past habitual action 3. To denote futurity in the past 4. To make polite requests and express hypothetical meanings

1. To denote an action in progress at the moment of speaking What are you doing? I’m writing a letter. 2. An action in progress at a period of time including the present He is studying law while her sister is dong physics. I teach English at the college, but I’m now teaching in a middle school.

柴油机应急处理和运转管理

第十二章柴油机应急处理和运转管理船舶经常在复杂的海域和恶劣的气候下航行,柴油机一旦运行失常,使船舶失去控制将会造成十分严重的后果。

轮机管理人员除了应能对运行中的柴油机进行正确的管理以及维修保养之外,尚需在紧急事故突发之际能正确地进行相应的应急处理,使这在最短时间内恢复其运转以保证船舶航行安全。

下面介绍几种常见故障的应急处理。

第一节封缸运行柴油机运行中若一个或一个以上的气缸发生故障而一时无法修复,此时可采取停止故障气缸运转的措施,即封缸运行。

根据我国船规的规定,六缸以下柴油机应能保证在停掉一个气缸的情况下继续运转;六缸以上应能保证在停掉两个气缸的情况下继续运转。

一、封缸运行的三种情况及措施1.停止该缸供油发火如果有一个气缸发生故障,如喷射系统故障、气阀咬死、气缸漏气等,这些故障只是使气缸不能发火而运动部件尚可运转。

在此情况下,根据柴油机的具体情况可提起喷油泵滚轮,使喷油泵停止工作或打开喷油器的回油阀,使燃油停止喷入气缸。

但要避免关闭喷油泵进〖出〗口阀,造成喷油泵偶件干磨而咬死。

此种封缸亦称减缸运行或停缸运行。

如果是直流二冲程柴油机,在停止喷油的同时还应〖×将排气阀锁定在开启位置,以减少活塞消耗的压缩功。

〗【尽可能将排气阀锁定在关闭位置,以保护十字头轴承,减少不正常振动。

】2.活塞组件拆出,十字头和连杆尚在机内如果是活塞、气缸造成气缸裂纹或损坏而无法修复使用,但连杆和十字头尚能正常工作,则必须拆掉活塞组件(含填料函),并采取下列措施:(1)提起喷油泵滚轮停止泵油;(2)弯流扫气者专用工具封住气缸套排气口,直流扫气者或四冲程柴油机将气阀锁住在正常关闭位置;(3)用专用工具封住活塞杆填料函孔;(4)在十字头上安装专用封盖;(5)封闭活塞冷却系统;(6)拆下气缸起动阀控制空气管并封住;(7)拆下气缸起动阀起动空气管并封住;(8)关闭该缸气缸冷却水的进出口阀;(9)该缸气缸油注油管减至最小;(10)活塞组件拆除后重新安装气缸盖。

【免费下载】C Primer英文版第5版

C++ Primer英文版(第5版)《C++ Primer英文版(第5版)》基本信息作者: (美)李普曼(Lippman,S.B.) (美)拉乔伊(Lajoie,J.) (美)默Moo,B.E.) 出版社:电子工业出版社ISBN:9787121200380上架时间:2013-4-23出版日期:2013 年5月开本:16开页码:964版次:5-1所属分类:计算机 > 软件与程序设计 > C++ > C++内容简介计算机书籍 这本久负盛名的C++经典教程,时隔八年之久,终迎来史无前例的重大升级。

除令全球无数程序员从中受益,甚至为之迷醉的——C++大师Stanley B. Lippman的丰富实践经验,C++标准委员会原负责人Josée Lajoie对C++标准的深入理解,以及C++先驱Barbara E. Moo在C++教学方面的真知灼见外,更是基于全新的C++11标准进行了全面而彻底的内容更新。

非常难能可贵的是,《C++ Primer英文版(第5版)》所有示例均全部采用C++11标准改写,这在经典升级版中极其罕见——充分体现了C++语言的重大进展极其全面实践。

书中丰富的教学辅助内容、醒目的知识点提示,以及精心组织的编程示范,让这本书在C++领域的权威地位更加不可动摇。

无论是初学者入门,或是中、高级程序员提升,本书均为不容置疑的首选。

目录《c++ primer英文版(第5版)》prefacechapter 1 getting started 11.1 writing a simple c++program 21.1.1 compiling and executing our program 31.2 afirstlookat input/output 51.3 awordaboutcomments 91.4 flowofcontrol 111.4.1 the whilestatement 111.4.2 the forstatement 131.4.3 readinganunknownnumberof inputs 141.4.4 the ifstatement 171.5 introducingclasses 191.5.1 the sales_itemclass 201.5.2 afirstlookatmemberfunctions 231.6 thebookstoreprogram. 24chaptersummary 26definedterms 26part i the basics 29chapter 2 variables and basic types 312.1 primitivebuilt-intypes 322.1.1 arithmetictypes 322.1.2 typeconversions 352.1.3 literals 382.2 variables 412.2.1 variabledefinitions 412.2.2 variabledeclarations anddefinitions 44 2.2.3 identifiers 462.2.4 scopeof aname 482.3 compoundtypes 502.3.1 references 502.3.2 pointers 522.3.3 understandingcompoundtypedeclarations 57 2.4 constqualifier 592.4.1 references to const 612.4.2 pointers and const 622.4.3 top-level const 632.4.4 constexprandconstantexpressions 652.5 dealingwithtypes 672.5.1 typealiases 672.5.2 the autotypespecifier 682.5.3 the decltypetypespecifier 702.6 definingourowndatastructures 722.6.1 defining the sales_datatype 722.6.2 using the sales_dataclass 742.6.3 writing our own header files 76 chaptersummary 78definedterms 78chapter 3 strings, vectors, and arrays 813.1 namespace usingdeclarations 823.2 library stringtype 843.2.1 defining and initializing strings 843.2.2 operations on strings 853.2.3 dealing with the characters in a string 90 3.3 library vectortype 963.3.1 defining and initializing vectors 973.3.2 adding elements to a vector 1003.3.3 other vectoroperations 1023.4 introducingiterators 1063.4.1 usingiterators 1063.4.2 iteratorarithmetic 1113.5 arrays 1133.5.1 definingandinitializingbuilt-inarrays 113 3.5.2 accessingtheelementsof anarray 1163.5.3 pointers andarrays 1173.5.4 c-stylecharacterstrings 1223.5.5 interfacingtooldercode 1243.6 multidimensionalarrays 125chaptersummary 131definedterms 131chapter 4 expressions 1334.1 fundamentals 1344.1.1 basicconcepts 1344.1.2 precedenceandassociativity 1364.1.3 orderofevaluation 1374.2 arithmeticoperators 1394.3 logical andrelationaloperators 1414.4 assignmentoperators 1444.5 increment anddecrementoperators 1474.6 thememberaccessoperators 1504.7 theconditionaloperator 1514.8 thebitwiseoperators 1524.9 the sizeofoperator 1564.10 commaoperator 1574.11 typeconversions 1594.11.1 thearithmeticconversions 1594.11.2 other implicitconversions 1614.11.3 explicitconversions 1624.12 operatorprecedencetable 166 chaptersummary 168definedterms 168chapter 5 statements 1715.1 simple statements 1725.2 statementscope 1745.3 conditional statements 1745.3.1 the ifstatement 1755.3.2 the switchstatement 1785.4 iterativestatements 1835.4.1 the whilestatement 1835.4.2 traditional forstatement 1855.4.3 range forstatement 1875.4.4 the do whilestatement 1895.5 jumpstatements 1905.5.1 the breakstatement 1905.5.2 the continuestatement 1915.5.3 the gotostatement 1925.6 tryblocks andexceptionhandling 1935.6.1 a throwexpression 1935.6.2 the tryblock 1945.6.3 standardexceptions 197 chaptersummary 199definedterms 199chapter 6 functions 2016.1 functionbasics 2026.1.1 localobjects 2046.1.2 functiondeclarations 2066.1.3 separatecompilation 2076.2 argumentpassing 2086.2.1 passingargumentsbyvalue 2096.2.2 passingargumentsbyreference 2106.2.3 constparametersandarguments 2126.2.4 arrayparameters 2146.2.5 main:handlingcommand-lineoptions 218 6.2.6 functionswithvaryingparameters 2206.3 return types and the returnstatement 222 6.3.1 functionswithnoreturnvalue 2236.3.2 functionsthatreturnavalue 2236.3.3 returningapointer toanarray 2286.4 overloadedfunctions 2306.4.1 overloadingandscope 2346.5 features forspecializeduses 2366.5.1 defaultarguments 2366.5.2 inline and constexprfunctions 2386.5.3 aids for debugging 2406.6 functionmatching 2426.6.1 argumenttypeconversions 2456.7 pointers tofunctions 247 chaptersummary 251definedterms 251chapter 7 classes 2537.1 definingabstractdatatypes 2547.1.1 designing the sales_dataclass 2547.1.2 defining the revised sales_dataclass 256 7.1.3 definingnonmemberclass-relatedfunctions 260 7.1.4 constructors 2627.1.5 copy,assignment, anddestruction 2677.2 accesscontrol andencapsulation 2687.2.1 friends 2697.3 additionalclassfeatures 2717.3.1 classmembersrevisited 2717.3.2 functions that return *this 2757.3.3 classtypes 2777.3.4 friendshiprevisited 2797.4 classscope 2827.4.1 namelookupandclassscope 2837.5 constructorsrevisited 2887.5.1 constructor initializerlist 2887.5.2 delegatingconstructors 2917.5.3 theroleof thedefaultconstructor 2937.5.4 implicitclass-typeconversions 2947.5.5 aggregateclasses 2987.5.6 literalclasses 2997.6 staticclassmembers 300chaptersummary 305definedterms 305contents xipart ii the c++ library 307chapter 8 the io library 3098.1 the ioclasses 3108.1.1 nocopyorassignfor ioobjects 3118.1.2 conditionstates 3128.1.3 managingtheoutputbuffer 3148.2 file input and output 3168.2.1 using file stream objects 3178.2.2 file modes 3198.3 stringstreams 3218.3.1 using an istringstream 3218.3.2 using ostringstreams 323chaptersummary 324definedterms 324chapter 9 sequential containers 3259.1 overviewof the sequentialcontainers 3269.2 containerlibraryoverview 3289.2.1 iterators 3319.2.2 containertypemembers 3329.2.3 begin and endmembers 3339.2.4 definingandinitializingacontainer 3349.2.5 assignment and swap 3379.2.6 containersizeoperations 3409.2.7 relationaloperators 3409.3 sequentialcontaineroperations 3419.3.1 addingelements toasequentialcontainer 3419.3.2 accessingelements 3469.3.3 erasingelements 3489.3.4 specialized forward_listoperations 3509.3.5 resizingacontainer 3529.3.6 containeroperationsmayinvalidateiterators 353 9.4 how a vectorgrows 3559.5 additional stringoperations 3609.5.1 other ways to construct strings 3609.5.2 other ways to change a string 3619.5.3 stringsearchoperations 3649.5.4 the comparefunctions 3669.5.5 numericconversions 3679.6 containeradaptors 368chaptersummary 372definedterms 372chapter 10 generic algorithms 37510.1 overview. 37610.2 afirstlookat thealgorithms 37810.2.1 read-onlyalgorithms 37910.2.2 algorithmsthatwritecontainerelements 380 10.2.3 algorithmsthatreordercontainerelements 383 10.3 customizingoperations 38510.3.1 passingafunctiontoanalgorithm 38610.3.2 lambdaexpressions 38710.3.3 lambdacapturesandreturns 39210.3.4 bindingarguments 39710.4 revisiting iterators 40110.4.1 insert iterators 40110.4.2 iostream iterators 40310.4.3 reverse iterators 40710.5 structureofgenericalgorithms 41010.5.1 thefive iteratorcategories 41010.5.2 algorithmparameterpatterns 41210.5.3 algorithmnamingconventions 41310.6 container-specificalgorithms 415 chaptersummary 417definedterms 417chapter 11 associative containers 41911.1 usinganassociativecontainer 42011.2 overviewof theassociativecontainers 423 11.2.1 defininganassociativecontainer 423 11.2.2 requirements onkeytype 42411.2.3 the pairtype 42611.3 operations onassociativecontainers 428 11.3.1 associativecontainer iterators 429 11.3.2 addingelements 43111.3.3 erasingelements 43411.3.4 subscripting a map 43511.3.5 accessingelements 43611.3.6 awordtransformationmap 44011.4 theunorderedcontainers 443 chaptersummary 447definedterms 447chapter 12 dynamicmemory 44912.1 dynamicmemoryandsmartpointers 45012.1.1 the shared_ptrclass 45012.1.2 managingmemorydirectly 45812.1.3 using shared_ptrs with new 46412.1.4 smartpointers andexceptions 46712.1.5 unique_ptr 47012.1.6 weak_ptr 47312.2 dynamicarrays 47612.2.1 newandarrays 47712.2.2 the allocatorclass 48112.3 usingthelibrary:atext-queryprogram 484 12.3.1 designof thequeryprogram 48512.3.2 definingthequeryprogramclasses 487 chaptersummary 491definedterms 491part iii tools for class authors 493chapter 13 copy control 49513.1 copy,assign, anddestroy 49613.1.1 thecopyconstructor 49613.1.2 thecopy-assignmentoperator 50013.1.3 thedestructor 50113.1.4 theruleofthree/five 50313.1.5 using = default 50613.1.6 preventingcopies 50713.2 copycontrol andresourcemanagement 51013.2.1 classesthatactlikevalues 51113.2.2 definingclassesthatactlikepointers 51313.3 swap 51613.4 acopy-controlexample 51913.5 classesthatmanagedynamicmemory 52413.6 movingobjects 53113.6.1 rvaluereferences 53213.6.2 moveconstructor andmoveassignment 53413.6.3 rvaluereferencesandmemberfunctions 544 chaptersummary 549definedterms 549chapter 14 overloaded operations and conversions 551 14.1 basicconcepts 55214.2 input andoutputoperators 55614.2.1 overloading the output operator [[55714.2.2 overloading the input operator ]]. 55814.3 arithmetic andrelationaloperators 56014.3.1 equalityoperators 56114.3.2 relationaloperators 56214.4 assignmentoperators 56314.5 subscriptoperator 56414.6 increment anddecrementoperators 56614.7 memberaccessoperators 56914.8 function-calloperator 57114.8.1 lambdasarefunctionobjects 57214.8.2 library-definedfunctionobjects 57414.8.3 callable objects and function 57614.9 overloading,conversions, andoperators 57914.9.1 conversionoperators 58014.9.2 avoidingambiguousconversions 58314.9.3 functionmatchingandoverloadedoperators 587 chaptersummary 590definedterms 590chapter 15 object-oriented programming 59115.1 oop:anoverview 59215.2 definingbaseandderivedclasses 59415.2.1 definingabaseclass 59415.2.2 definingaderivedclass 59615.2.3 conversions andinheritance 60115.3 virtualfunctions 60315.4 abstractbaseclasses 60815.5 accesscontrol andinheritance 61115.6 classscopeunder inheritance 61715.7 constructors andcopycontrol 62215.7.1 virtualdestructors 62215.7.2 synthesizedcopycontrol andinheritance 62315.7.3 derived-classcopy-controlmembers 62515.7.4 inheritedconstructors 62815.8 containers andinheritance 63015.8.1 writing a basketclass 63115.9 textqueriesrevisited 63415.9.1 anobject-orientedsolution 63615.9.2 the query_base and queryclasses 63915.9.3 thederivedclasses 64215.9.4 the evalfunctions 645chaptersummary 649definedterms 649chapter 16 templates and generic programming 65116.1 definingatemplate. 65216.1.1 functiontemplates 65216.1.2 classtemplates 65816.1.3 templateparameters 66816.1.4 membertemplates 67216.1.5 controlling instantiations 67516.1.6 efficiency and flexibility 67616.2 templateargumentdeduction 67816.2.1 conversions andtemplatetypeparameters 67916.2.2 function-templateexplicitarguments 68116.2.3 trailing return types and type transformation 683 16.2.4 functionpointers andargumentdeduction 68616.2.5 templateargumentdeductionandreferences 68716.2.6 understanding std::move 69016.2.7 forwarding 69216.3 overloadingandtemplates 69416.4 variadictemplates 69916.4.1 writingavariadicfunctiontemplate 70116.4.2 packexpansion 70216.4.3 forwardingparameterpacks 70416.5 template specializations 706chaptersummary 713definedterms 713part iv advanced topics 715chapter 17 specialized library facilities 71717.1 the tupletype 71817.1.1 defining and initializing tuples 71817.1.2 using a tuple toreturnmultiplevalues 72117.2 the bitsettype 72317.2.1 defining and initializing bitsets 723 17.2.2 operations on bitsets 72517.3 regularexpressions 72817.3.1 usingtheregularexpressionlibrary 729 17.3.2 thematchandregex iteratortypes 73417.3.3 usingsubexpressions 73817.3.4 using regex_replace 74117.4 randomnumbers 74517.4.1 random-numberengines anddistribution 745 17.4.2 otherkinds ofdistributions 74917.5 the iolibraryrevisited 75217.5.1 formattedinput andoutput 75317.5.2 unformattedinput/outputoperations 761 17.5.3 randomaccess toastream 763 chaptersummary 769definedterms 769chapter 18 tools for large programs 77118.1 exceptionhandling 77218.1.1 throwinganexception 77218.1.2 catchinganexception 77518.1.3 function tryblocks andconstructors 777 18.1.4 the noexceptexceptionspecification 779 18.1.5 exceptionclasshierarchies 78218.2 namespaces 78518.2.1 namespacedefinitions 78518.2.2 usingnamespacemembers 79218.2.3 classes,namespaces,andscope 79618.2.4 overloadingandnamespaces 80018.3 multiple andvirtual inheritance 80218.3.1 multiple inheritance 80318.3.2 conversions andmultiplebaseclasses 805 18.3.3 classscopeundermultiple inheritance 807 18.3.4 virtual inheritance 81018.3.5 constructors andvirtual inheritance 813 chaptersummary 816definedterms 816chapter 19 specialized tools and techniques 819 19.1 controlling memory allocation 82019.1.1 overloading new and delete 82019.1.2 placement newexpressions 82319.2 run-timetypeidentification 82519.2.1 the dynamic_castoperator 82519.2.2 the typeidoperator 82619.2.3 usingrtti 82819.2.4 the type_infoclass 83119.3 enumerations 83219.4 pointer toclassmember 83519.4.1 pointers todatamembers 83619.4.2 pointers tomemberfunctions 83819.4.3 usingmemberfunctions ascallableobjects 84119.5 nestedclasses 84319.6 union:aspace-savingclass 84719.7 localclasses 85219.8 inherentlynonportablefeatures 85419.8.1 bit-fields 85419.8.2 volatilequalifier 85619.8.3 linkage directives: extern "c" 857chaptersummary 862definedterms 862appendix a the library 865a.1 librarynames andheaders 866a.2 abrieftourof thealgorithms 870a.2.1 algorithms tofindanobject 871a.2.2 otherread-onlyalgorithms 872a.2.3 binarysearchalgorithms 873a.2.4 algorithmsthatwritecontainerelements 873a.2.5 partitioningandsortingalgorithms 875a.2.6 generalreorderingoperations 877a.2.7 permutationalgorithms 879a.2.8 setalgorithms forsortedsequences 880a.2.9 minimumandmaximumvalues 880a.2.10 numericalgorithms 881a.3 randomnumbers 882a.3.1 randomnumberdistributions 883a.3.2 randomnumberengines 884本图书信息来源:中国互动出版网。

新约哥罗森书第一章解释

新约哥罗森书第一章解释(中英文实用版)Chapter 1: An Explanation of the Book of ColossiansIn the first chapter of the New Testament, the Book of Colossians addresses issues that were prevalent in the early Christian church.The author, Paul, writes to the Colossian believers to encourage them in their faith and to warn them against false teachings.The book of Colossians emphasizes the preeminence of Jesus Christ.Paul declares that Jesus is the Creator, Sustainer, and Redeemer of the universe.He emphasizes that all things were created in Jesus and for Jesus, and that in Him all the fullness of Deity dwells.One of the key themes in Colossians is the unity of the church.Paul writes about the importance of unity among believers, stressing that they should be characterized by love, forgiveness, and harmony.He encourages them to live lives that are pleasing to God and to beware of false teachers who may lead them astray.Another important theme in Colossians is the Christian"s spiritual armor.Paul writes about the need for believers to put on the full armor of God in order to stand firm against the schemes of the devil.This armor includes the belt of truth, the breastplate of righteousness, the shoes of peace, the shield of faith, the helmet of salvation, and the sword of the Spirit.Overall, the Book of Colossians is a powerful letter that emphasizes the importance of faith in Jesus Christ and the need for unity and spiritual preparedness among believers.It serves as a reminder of the surpassing greatness of Jesus Christ and the hope that we have in Him.。

医学英语教程Chapter 3

Chapter 3.I. IntroductionThis chapter has three purposes. The first purpose is to teach many of the most common suffixes in the medical language. As you work through the entire book, the suffixes mastered in this chapter will appear often. An additional group of suffixes is presented in Chapter 6. The second purpose is to introduce new combining forms and use them to make works with suffixes. Your analysis of the terminology in Section III of this chapter will increase tour medical language wocabulary.The third purpose is to expand your understanding ofterminology beyond basic word analgsis. The appendices in Section IV present illustrations and additional explanations of new terms. Your should refer to these appendices as your complete the meanings of terms in Section III.II. Combining FormsRead this list and underline those combining forms that are unfamiliarCombining FormsCombining Form MeaningAbdomin/o abdomenAcr/o extremities, top, extreme pointAcu/o sharp, severe, suddenAden/o glandAgor/a marketplaceAmni/o amnionAngi/o vesselArteri/o arteryArthr/o jointAxill/o armpitBlephar/o eyelidBronch/o bronchial tubesCarcin/o cancerChem/o drug, chemicalChondr/o cartilageChron/o timeCol/o colonCyst/o urinary bladderEncephal/o brainHydr/o water, fluidInguin/o groinIsch/o to hold backLapar/o abdomen, abdominal wallLaryng/o larynxLymph/o lymphLymph, a clear fluid that bathes tissue spaces, is contained inspecial lymph vessels and nodes throughout the bodyMamm/o breastMast/o breastMorph/o shape, formMuc/o mucusMy/o muscleMyel/o spinal cord, bone marrowContext of usage indicates the meaning intendedNecr/o deathNephr/o kidneyNeur/o nerveNeutr/o neurophilOphthalm/o eyeOste/o boneOt/o earPath/o diseasePeritone/o peritoneumPhag/o to eat, swallowPhleb/o veinPlas/o formation, developmentPleur/o pleuraPneumon/o lungsPulmon/o lungsRect/o rectumRen/o kidneySarc/o fleshSplen/o spleenStaphyl/o clystersStrept/o twisted chainsThorac/o chestThromb/o clotTonsill/o tonsilsTrache/o tracheaVen/o veinIII. Suffixes and TerminologyNoun SuffixesThe following list includes common noun suffixes. After the meaning of each suffix, terminology illustrates the use of the suffix in various words. Remember the basic rule for building a medical term: Use a combining vowel, such as o, to connect the root to the suffix. However, drop the combining vowel if the suffix begins with a vowel. For example: gastr/it is, not gastr/o/it is. Numbers after certain terms direct you to the Appendices that follow this list. These Appendices contain additional information to help you understand the terminology.Suffix Meaning Terminology Meaning-algia pain arthralgia _________________________otalgia ____________________________neuralgia __________________________myalgia ___________________________-cele hernia rectocele ___________________________cystocele __________________________-centesis surgical puncture to remove fluid thoracentesis __________________________Notice that this term is shortened fromthoracocentesisamniocentesis__________________________abdominocentesis ________________________This procedure is more commonly known as aparacentesis. A tube is placed through anincision of the abdomen and fluid is removedtfrom the peritoneal cavity .-coccus berry-shaped, bacterium streptococcus _________________________staphylocci ___________________________ -cyte cell erythrocyte __________________________leukocyte ___________________________thrombocyte _________________________-dynia pain pleurodynia _________________________Pain in the chest wall muscles that isaggravated by breathing-ectomy excision, removal, resection laryngectomy _______________________mastectomy _________________________ -ectomy blood condition anemia ___________________________ischemia _________________________-genesis condition of producing, forming carcinogenesis _____________________pathogenesis ________________________angiogenesis ________________________-genic pertaining to, producing, carcinogenic_________________________ produced by, or inosteogenic ___________________________An osteogenic sarcoma is a tumor producedin bone tissue-gram record electroencephalogram __________________myelogram _________________________Myle/o means spinal cord in this term. This isan x-ray record taken after contrast material isinjected into membranes around the spinalcordmammogram _________________________ -graph instrument for recording electroencephalograph _________________ -graphy process of recording electroencephalography ________________angiography _________________________ -itis inflammation bronchitis ___________________________tonsillitis ____________________________thrombophlebitis ______________________Also called phlebitis-logy study of ophthalmology _______________________morphology__________________________ -lysis breakdown, destruction, separation hemolysis ___________________________Breakdown of red blood cells with release ofhemoglobin-malacia softening osteomalacia _______________________chondromalacia ______________________ -megaly enlargement acromegaly _________________________splenomegaly _______________________-oma tumor, mass, collection of fluid myoma __________________________A benign tumormyosarcoma _______________________A malignant tumor. Muscle is a type of fleshtissuemyltiple myeloma ____________________Myel/o means bone marrow in this term. Thismaligant tumor occurs in bone marrow tissuethroughout the bodyhematoma _______________________-opsy to view biopsy _____________________________necropsy __________________________This is an autopsy or postmortemexamination-osis condition, usually abnormal necrosis ___________________________hydronephrosis ______________________leukocytosis _________________________ -pathy disease condition cardiomyopathy _____________________Primary disease of the heart muscle in theabsence of a known underlying etiology-penia deficiency erythropenia ______________________neutropenia ________________________In this term, neutr/o means neutrophilthrombocytopenia___________________-phobia fear acrophobia ________________________Fear of heightsagoraphobia _______________________An anxiety disorder maked by fear ofventuring out into a crowded place-plasm development, formation, growth achondroplasia _____________________ -plasty surgical repair angioplasty ________________________A cardiologist opens a narrowed bloodvessel using a ballon that is inflated afterinsertion into the vessel. Stents, or slottedtubes, are then put in place to keep theartery open-ptosis drooping, sagging, prolapse blepharoptosis _____________________Physcians use ptosis alone, to indicateprolapse of the upper eyelidnephroptosis ________________________ -sclerosis hardening arteriosclerosis _____________________In atherosclerisis deposits of fat collect inan artery-scope instrument for visual examination laparoscope _______________________ -scopy process of visual examination laparoscopy _______________________ -stasis stopping, controlling metastasis ________________________Meta- means beyond. A metastasis is thespread of a malignant tumor beyond itsoriginal site to a secondary organ orlocationhemostasis ________________________Blood flow is stopped naturally byclotting or artificially by compression orwsuturing of a wound-stomy opening to form a mouth colostomy ________________________tracheostomy ______________________ -therapy treatment hydrotherapy ______________________chemotherapy ______________________radiotherapy _____________________-tomy incision, to cut into laparotomy _____________________This is a large incision through theabdominal wallphlebotomy ______________________ -trophy development, nourishment hypertrophy ______________________Cells increase in size, not number.Muscles of weight lifters often hypertrophyatrophy ___________________________Cells decrease in size. Muscles atrophywhen immobilized in a cast and not in use The following are shorter noun suffixes that are usually attached to roots in wordsSuffix Meaning Terminology Meaning-er one who radiographer _______________________A technologist who assists in the making ofdiagnostic x-ray pictures-ia condition leukemia __________________________pneumonia ________________________-ist specialist nephrologist _______________________-ole little, small arteriole __________________________-ule little, small venule ____________________________ -um, -ium structure, tissue, thing pericardium _______________________This membrane surrounds the heart-y condition, process nephropathy _______________________Adjective SuffixesThe following are adjectival suffixes. No simple rule will tell you which suffix meanin “pertaining to” should be used with a specific combining form. Your job is to recongnize the suffix in each term and know the meaning of the entire termSuffix Meaning Terminology Meaning-ac, -iac pertaining to cardiac _________________________-al pertaining to peritoneal _______________________inguinal _________________________pleural __________________________-ar pertaining to tonsillar __________________________-ary pertaining to pulmonary ________________________axillary ___________________________-eal pertaining to laryngeal __________________________-ic, -ical pertaining to chronic ____________________________Acute is the opposite of chronic. It describes adisease that is of rapid onset and has severesymptoms and brief durationpathological __________________________-oid resembling adenoids __________________________-ose pertaining to, full of adipose ___________________________-ous pertaining to mucous ___________________________Mecous membranes produce the stickysection called mucus-tic pertaining to necrotic _____________________________IV. AppendicesAppendix A.A hernia is protrusion of an organ or the muscular wall of an organ througg the cavity that normally contains it. A hiatal hernia occurs when the stomach protrudes upward into the mediastinum through the esophageal opening in the diaphragm, and an inguinal hernia occurs when part of the intestine protrudes downward into the groin region and commonly into the scrotal sac in the male. A rectocele is the protrusion of a portion of the rectum toward the vagina through a weak part of the vaginal wall muscles. An omphalocele is a herniation of the intestines through the navel occurring in infants at birth. A cystocele occurs when part of the urinary bladder herniates through the vaginal wall due to weakened pelvic musclesAppendix B: AmniocentesisThe amnion is the sac that surrounds the embbryo in the uterus. Fluid accumulates within the sac and can be withdrawn for analysis between the 12th and 18th weeks of pregnancy. The fetus sheds cells into the fluid, and these cells are grown for microscopic analysis. A karyotype is made to analyze chromosomes, and the fluid can be examined for high levels of chemicals that indicate defects in the developing spinal cord and spinal column of the fetusAppendix C: PluralsWords ending in –us commonly form their plural by dropping the –us and adding –i. Thus, nucleus becomes nuclei and coccus becomes cocci. For additional information on formation of plurals, please refer to Appendix I, page 949, at the end of the book.Appendix D: Streptococcus and StaphylococcusStreptococcus, a berry-shaped bacterium, grows in twisted chains. One group of streptocoocci causes such conditions as “strep” throat, tonsillitis, rheumatic fever, and certain kidney ailments, whereas another group causes infections in teeth, in the sinuses of the nose and face, and in the valves of the heart.Staphylococci, other berry-shaped bacteria, grow in small clusters, like grapes. Staphylococcal lesions may be external or internal. An abscess is a collection of pus, white blood cells, and protein that is present at the site of infection.Examples of diplococci are pneumococci and gonococci. Pneumococci cause bacterial pneumonia, and gonococci invade the reproductive organs causing gonorrhea. Figure 3-3 illustrates the different growth patterns of streptococci, staphylococci, and diplococci.Appendix E: Blood CellsStudy Figure 3-4 as you read the following to note the differences among the three different types of cells in the blood.Erythrocytes. These cells are made in the bone marrow. They carry oxygen from the lungs through the blood to all body cells. The body cells use oxygen to burn food and release energy. Hemoglobin, an important protein in erythrocytes, carries the oxygen through the bloodstream. Leukocytes. There are five different leukocytes:Granulocytes contain dark-staining granules in their gytoplasm and have a multilobed nucleus. They are formed in the bone marrow and there are three types:1.Eosinophils are active and elevated in allergic conditions such as asthma. About 3 percent ofleukocytes are eosinophils2.Basophils. The function of basophils is not clear, but they play a role in inflammation. Lessthan 1 percent of leukocytes are basophils3.Neutrophils are important disease-fighting cells. They are phagocytes because they engulf anddigest bacteria. They are the most numerous disease-fighting “soldiers”, and are referred to as “polys” or polymorphonuclear leukocytes because of their multilobed nucleusMononuclear leukocytes have one large nucleus and only a few granules in their cytoplasm.They are produced in lymph nodes and the spleen. There are two types of mononuclear leukocytes4. Lymphocytes fight disease by producing antibodies and thus destroying foreign cells. Theymay also attach directly to foreign cells and destroy them. Two types of lymphocytes are T cells and B cells. About 32 percent of leukocytes are lymphocytes5. Monocyte: Engulf and destroy cellular debris after neutrophils have attacked foreign cells.Monocytes leave the bloodstream and enter tissues (such as lung and liver) to become macrophages, which are large phagocytes. Monocytes make up about 4 percent of all leukocytes.Appendix F: Pronunciation CluePronunciation clue: The letters g and c are soft when followed by an i or e, and are hard when followed by an o or aAppendix G: AnemiaAnemia literally means no blood. However, in medical language and usage, anemia is a condition of reduction in the number of erythrocytes or amount of hemoglobin in circulating blood. Anemias are classified according to the different problems that arise with red blood cells. Aplastic (a = no, plas/o = formation) anemia, a severe type, occurs when bone marrow fails to produce not only erythrocytes but leukocytes and thrombocytes as well.Appendix H: IschemiaIschemia litterally mens to hold back (isch/o) blood (-emia) from a part of the body. Tissue that becomes ischemic loses its normal flow of blood and becomes deprived of oxygen. The ischemia can be caused by mechanical injury to a blood vessel, by blood clots lodging in a vessel, or by the progressive and gradual closing off (occusion) of a vessel caused by collection of faty material. Appendix I: TonsillitisThe tonsils are lymphatic tissue in back of the throat. They contain white blood cells (lymphocytes), which filter and fight bacteria. However, tonsils can also become infected and inflamed. Streptococcal infection of the throat causes tonsillitis, which may require tonsillectomy.Appendix J: AcromegalyAcromegaly is an endocrine disorder. It occurs when the pituitary gland, attached to the base of the brain, produces an excesive amount of growth hormone after the completion of puberty. The excess grouth hormone most often results from benign tumor of the pituitary gland. A person with acromegaly is of normalheight beccause the long bones have stopped growth after puberty, but bones and soft tissue in the hands, feet, and facegrow abnormally. High levels of growth hormone before completion of puberty produce excessive growth of long bones (gigantism) as well as acromegaly.Appendix K: SplenomegalyThe speen is an organ in the left upper quadrant (LUQ) of the abdomen (below the diaphragm and to the side of the stomach). Composed of lymph lymph tissue and blood vessels, it disposes of dying red blood cells and manugactures white blood cells (lymphocytes) to fight disease. If the speen is removed (dplenectomy), other organs carry out these functions.Appendix L: LeukocytosisWhen –osis is a suffix with blood cells, it is an abnormal condition of increase normal circulating blood cells. Thus, in leukocytosis an elevation in numbers of normal white blood cells occurs in response to the presence of infection. When –emia is a suffix with blood cells, the condition is an abnormally high, excessive increase in number of cancerous blood cells.Appendix M: AchondroplasiaAchondroplasia is an inherited disorder in which the bones of the arms and legs fail to grow to normal size because of a defect in both cartilage and bone. It results in a type of dwarfism characterized by short limbs, a normal-sized head and body, and normal intelligence.Appendix N: -ptosis = blepharoptosisThe suffix –ptosis is pronounced. When two consonants begin a word, the first is silent. If the two consonants are found in the middle of a word, both are pronounced for example, blepharoptosis. This condition occurs when eyelid muscles weaken, and a person has difficulty lifting the eyelid to keep it open.Appendix O: Laparoscopy = peritoneoscopy = MIS, mingmally invasive surgeryLaparoscopy is visual examination of the abdominal cavity using a laparoscope. The laparoscope, a lighted telescopic instrument, is inserted through an incision in the abdomen near the navel, and gas is infused into the peritoneal cavity to prevent injury to abdominal structures during surgery. Surgeons use laparosocopy to examine abdominal viscera for evidence of disease or for procedures such as removal of the appendix, gallbladder, adrenal gland, spleen, or colon, and repair of hernias. It is also used to clip and collapse the fallopain tube, which prevents sperm cells from reaching eggs that leave the ovary.Appendix P: Arteriole, capillary, venuleNotice the relationship among an artery, arterioles, capillaries, venules, and a vein as illustrated in Figure 3-8Appendix Q: AdenoidsThe adenoids are lymphatic tissue in the part of the pharynx (throat) near the nose and nasal passages. The literal meaning “resembling glands”is appropriate because they are neither endocrine nor exocrine glands. Enlargement of adenoids may cause blockage of the airway from the nose to the pharynx, and adenoidectomy may be advised. The tonsils are also lymphatic tissue, and their location as well as that of the adenoids is indicated in Figure 3-9.V. Practical ApplicationsMatch the diagnostic or treatment procedures with their descriptions:amniocentesis colostomy mastectomy tonsillectomy angiography laparoscopy paracentesis tracheotomy angioplasty laparotomy thoracentesis1.removal of abdominal fluid from the peritoneal space. ____________________rge abdominal incision to remove an ovarian adenocarcinoma ________________3.removal of an adnocarcinoma of the breast. ______________________4. a method used to determine the karyotype of a fetus _______________________5.establishment of an emergency airway path _______________________6.surgical procedure to remove pharyngeal lymphatic tissue _____________________7.surgical precdedure to open clogged coronary arteties. _______________________8.method of removing fluid from the chest (pleural effusion) _______________________9.procedure to drain feces from the body after bowel resection. ______________________10.X-ray procedure used to examine blood vessels before surgery ______________________11.minimally invasive surgery within the abdomen. _______________________VI. ExercisesRemember to check your answers carefully with those given in Section VII, Answers to ExerciseA.give the meanings for the following suffixes.1.– cele ______________2.– emia ______________3.– coccus ______________4.–gram ______________5.–cyte __________________6.–algia____________________7.–ectomy ________________8.–centesis _______________9.–genesis _________________10.– graph _________________11.–it is ____________________12.– graphy _______________ing the following combining forms and your knowleges of suffixes, build the followingmedical terms.amni/o isch/o ot/o angi/o laryng/o rect/o arthr/o mast/o staphyl/o bronch/o my/o strept/o carcin/o myel/o thorac/o cyst/o1.Hernia of the urinary bladder ____________________2.pain of muscle ______________________________3.process of produsing cancer ___________________4.record (x-ray) of the spinal cord ________________5.berry-shaped bacteria in twisted chains _____________6.surgical puncture to remove fluid from the chest ________________7.removal of the breast _____________________8.inflammation of the tubes leading from the windpipe to the lungs _________________9.to hold back blood from cells ____________________10.process of recording (x_ray) blood vessels _________________11.visual examination of joints _______________________12.berry-shaped bacteria in clusters _________________13.resection of the voice box ___________________14.surgical procedure to remove fluid from the sac around the fetus _________________C.Match the following terms, which describe blood cells, with their meanings below.Basophil eosinophil erythrocyte lymphocyte monocytethrombocyte erythrocyte1.granulocytic white blood cell (granules stain purple) that destroys foreign cells byengulfing and disgesting them; also called a polymorphonuclear leukocyte _________________________2.mononuclear white blood cell that destroys foreign cells by making antibodies___________________3.cloting cell; also called a platelet ___________________4.leukocyte with reddish –staining granules and numbers elevated in allergic reactions_______________5.red blood cell ____________________6.mononuclear white blood cell that engulfs and digests cellular debris; contains one largenucleus __________7.granulocytic (granules stain blue) white blood cell prominent in inflammatory reaction_______________D.give the mening of the following suffixes.1.– logy ________________2.–lysis ________________3.–pathy ______________4.–penia _______________5.–malacia _______________6.–osis ________________7.–phobia _______________8.–megaly __________________9.–oma ___________________10.–opsy ________________11.–plasia _________________12.–plasty ________________13.–sclerosis _______________14.–stasis ____________________ing the following combining forms and your knowledge of suffixes, build the followingmedical terms.Acr/o agor/o arteri/o bi/o blephar/o cardi/ochondr/o hem/o hydr/o morph/o my/o myel/onephr/o phleb/o sarc/o splen/o1.fear of the marketplace (crowds) ______________2.enlargement of the spleen ________________3.study of the shape (of cells) _______________4.softening of cartilage ______________________5.abnomal condition of water (fluid) in the kidney ________________6.disease conditionof heart muscle ____________________7.hardening of arteries ___________________8.tumor (benign ) of muscle ____________________9.flesh tumor (malignant ) of muscle _____________________10.surgical reqair of the nose ________________11.tumor of bone marrow _______________12.fear of heights ____________________13.view of living tissue upder the microscope ________________14.stoppage of the flow of blood ( by mechanical or natural means ) _________________15.inflamation of the eyelid __________________16.incision of vein ________________________F.Match the following terms with their meanings below.Achondroplasia acromegly atrophychemotherapy colostomy hydrotherapyhypertrophy laparoscope laparoscopymetastasis necrosis osteomalacia1.treatment using drogs ____________________2.conditiono f death (of cells ) ______________3.softening of bone _________________4.opening of the large intestine to the outside of the body ________________5.no development; shrinkage of cells ________________6.beyond control; spread of a cancerous tumor to another organ _______________7.instrument to visually examine the abdomen ____________________8.enlargement of extremities; an endocrine disorder that causes excess growth hormone tobe produced by the pituitary gland after puberty __________________9.condition of improper formation of cartilage in the embryo that leads to short bones anddwarr-like deformities _______10.process of viewing the peritoneal (adbominal ) cavity _________________11.treatment using water _______________12.excessive development of cells (increase in size of individual cells )____________G.give the menaing of the following suffixes.1.–ia _________2.–trophy ___________3.–stasis ____________4.–stomy ________________5.–tomy _____________6.–ole __________________7.–um ________________8.–ule _________________9.–y ___________________10.– oid_______________11.–genic ________________12.– ptosis ______________ing the following combining forms and suffixes, build the following medical terms.Combining Formsarteri/o pleur/o lapar/o pneumon/o mamm/o radi/onephr/o ven/oSuffixes-dynia -ole -therapy -ectomy -pathy -tomy -gram -plasty -ule -ia -scopy1.incision of the abdomen _____________2.process of visual examination of the abdomen _____________3. a small artery ________________4.condition of the lungs ______________5.treamtent using x-rays ______________6.recod (x-ray) of the breast ________________7.pain of the chest wall and the membranes surrounding the lungs ______________8. a small vein __________________9.disease condition of the kidney ___________________10.surgical repair of the breast _________________I.Underline the suffix in the following terms and give the menaing of the entire term.ryngeal _____________2.inguinal ______________3.chronic _______________4.pulmonary _____________5.adipose ________________6.peritoneal ______________7.axillary _________________8.necrotic ________________9.mucoid _________________10.mucous _______________J.Select from the following terms relating to blood and blood vessels to eomplete the sentences below.Anemia angioplasty arterioles hematoma hemolysis hemostasis ischemia leukemia leukocytosis multiple myeloma thromocytopenia venules1.Billy was diagnosed with excessively high numbers of cancerous white blood cells, or__________________. His doctor prescribed chemotherapy and expected an excellent prognosis.2.Mr. Clark’s angiogram showed that he had serious atherosclerosis of one of the arteriessupplying bood to his heart. His doctor recommended that _________________ would be helpful to open up his clogged artery by threading a catheter (tube) through his artery and opening a ballon at the end of the catheter to widen the artery.3.Mrs. Jackson’s blood count showed a reduced number of red blood cells, indicating____________________. Her erythrocytes were being destroyed by __________________________4.Doctors refused to operate on Joe Hite becausse of his low platelet count, a conditioncalled ________________.5.Blockage of an artery leading to Mr. Stein’s brain led to the holding back of blood flowto nerve tissue in his brain. This condition, called __________________, could lead to necrosis of tissue and a cerebrovascular accident.6.Small arteries, or ___________________, were broken under Ms. Bein’s scalp when shewas struck on the head with a rock. She soon developed a mass of blood, a (an) _________________, under the skin in that region of her head.7.Sarah Jones had a staphylococcal infection causing elevation of her white blood cellcount. She was treated with antibiotics and the ________________________ returned to normal.8.Within the body, the bone marrow (soft tissue within bones) is the “factory” for makingblood cells. Mr. Scott developed ____________________, a malignant condition of the bone marrow cells in his hip, upper arm, and thigh bones.9.During operations, surgeons use clamps to close off blood vessels and prevent blood loss.Thus, they maintain _________________ and avoid blood transfusions.10.Small vessels that carry blood toward the heart from capillaries and tissues are_______________.。

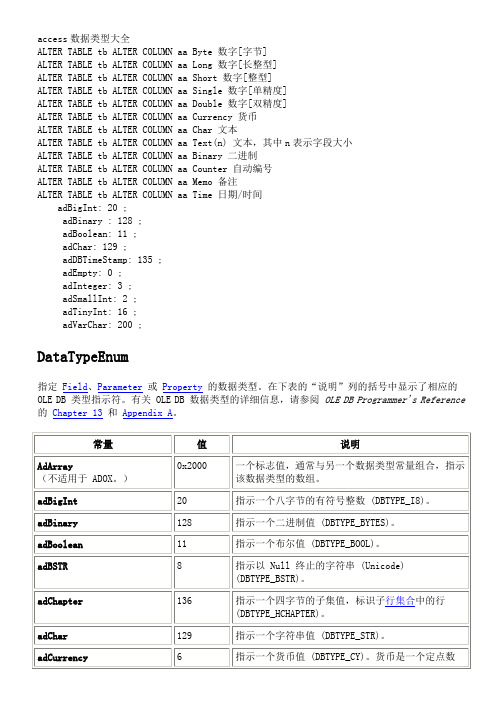

access数据类型大全

access数据类型大全ALTER TABLE tb ALTER COLUMN aa Byte 数字[字节]ALTER TABLE tb ALTER COLUMN aa Long 数字[长整型]ALTER TABLE tb ALTER COLUMN aa Short 数字[整型]ALTER TABLE tb ALTER COLUMN aa Single 数字[单精度]ALTER TABLE tb ALTER COLUMN aa Double 数字[双精度]ALTER TABLE tb ALTER COLUMN aa Currency 货币ALTER TABLE tb ALTER COLUMN aa Char 文本ALTER TABLE tb ALTER COLUMN aa Text(n) 文本,其中n表示字段大小ALTER TABLE tb ALTER COLUMN aa Binary 二进制ALTER TABLE tb ALTER COLUMN aa Counter 自动编号ALTER TABLE tb ALTER COLUMN aa Memo 备注ALTER TABLE tb ALTER COLUMN aa Time 日期/时间adBigInt: 20 ;adBinary : 128 ;adBoolean: 11 ;adChar: 129 ;adDBTimeStamp: 135 ;adEmpty: 0 ;adInteger: 3 ;adSmallInt: 2 ;adTinyInt: 16 ;adVarChar: 200 ;DataTypeEnum指定Field、Parameter或Property的数据类型。

在下表的“说明”列的括号中显示了相应的OLE DB 类型指示符。

有关 OLE DB 数据类型的详细信息,请参阅OLE DB Programmer's Reference 的Chapter 13和Appendix A。

一般最常使用解决不确定性决策问题的方法有下述五种

a2 : 21 132 147 147 147 147 147

132 0.7×147+0.3×132=142.5

a3 : 22 124 139 154 154 154 154

124 0.7×154+0.3×124=145

a4 : 23 116 131 146 161 161 161

116 0.7×161+0.3×116=147.5

作業研究.Chapter 10 決策理論

10-6

發生狀況 Q1

Q2

Q3

Q4

Q5 大中取

行動

20 21 22 23 24 小準則

a1 : 20 a2 : 21 a3 : 22 a4 : 23 a5 : 24

0

7 14 21 28

28

8

0

7 14 21

21

16 8

0

7 14

16*

24 16 8

0

7

24

140 147 154 161 168*

採用大中取大準則的決策者,對問題抱持樂觀的態度,又 稱為樂觀的準則 (Criterion of Optimism)。但須注意,可 能獲致最大報酬 168 元,因未來發生狀況未知,也有可能 只獲得最小報酬的 108 元。

作業研究.Chapter 10 決策理論

10-3

10-2

發生狀況 Q1 Q2 Q3 Q4 Q5 大中取

行動

20 21 22 23 24 大準則

a1 : 20 a2 : 21 a3 : 22 a4 : 23 a5 : 24

140 140 140 140 140 132 147 147 147 147 124 139 154 154 154 116 131 146 161 161 108 123 138 153 168

核医学专业介绍

主要研究方向及应用领域

主要研究方向

核医学的主要研究方向包括放射性核素 治疗、核医学影像诊断、核素示踪技术 等。

VS

应用领域