WHY DID CREDIT RATING FAIL IN CREDIT CRISIS

穆迪 评级方法

Rating Methodology Request for CommentBank Financial Strength Ratings: Revised MethodologySummaryThis report details Moody’s proposal to revise our rating methodology for assigning Bank Financial Strength Ratings (BFSRs) globally.1 This revision does not change the main factors that Moody’s considers in rating banks. However,the revised approach provides a single, global methodology instead of separate methodologies for mature and develop-ing markets. It also establishes specific ranges for each factor that relate to different rating categories. The updated methodology is intended to provide investors and issuers with a transparent set of guidelines allowing them to better understand our rating process and how we reach our decisions.T o this end, we have developed a rating scorecard that uses a common set of globally available financial metrics together with key qualitative factors that Moody’s analysts consider critical in evaluating a bank’s intrinsic financial strength and specific weights for each factor. This scorecard will be used by Moody’s analysts as the first step in deter-mining BFSRs. It should also enable investors and issuers to independently estimate a BFSR for most banks within two notches. This report describes the scorecard and discusses some of its limitations as well as some of the further adjust-ments that Moody’s analysts may employ in assigning BFSRs.The revised methodology is also intended to improve the consistency of Moody’s BFSRs. As previously announced, Moody’s intends to incorporate joint-default analysis (JDA) into our assessment of external support for banks later this year.2 We believe the updated BFSR methodology will help ensure that existing BFSRs are indeed “pure” measures of stand-alone financial strength and do not include external support. This is important in order to avoid double counting external support when we implement JDA for banks. We are requesting comments because we believe that the implementation of this methodology could lead to changes in the BFSRs for a significant number of banks, although we do not expect most of those to exceed 2 notches.Readers should note that this methodology is not an exhaustive treatment of every factor considered by Moody’s in assigning bank financial strength ratings, but it should enable our constituents to better understand how and why we arrive at a BFSR. Moody’s welcomes comments or suggestions on this proposal from market participants. Comments should be sent to cpc@ by September 29, 2006.1.Moody's current approach is outlined in the following Rating Methodology reports: "Bank Credit Risk -- An Analytical Framework for Banks in Developed Markets," April 1999 and "Bank Credit Risk in Emerging Markets -- An Analytical Framework," July 1999.2.Please see "Request for Comment: Incorporation of Joint-Default Analysis for Systemic Support into Moody's Bank Rating Methodology ," October 2005; "Update to Proposal to Incorporate Joint-Default Analysis into Moody's Bank Rating Methodology ," April 2006; and "Bank Joint Default Analysis: Rating Methodology Update," August 2006.New YorkDavid Fanger 1.212.553.1653Rosemarie Conforte Jeanne Del Casino Greg Bauer Laura Levenstein LondonLynn Exton 44.20.7772.5454Adel Satel Antonio Carballo MadridMaria Cabanyes 34.91.310.14.54TokyoMutsuo Suzuki 81.3.5408.4000Yasunobu Doi SingaporeDeborah Schuler 65.6398.8300Hong KongJerry Chien 852.2916.1121 Contact PhoneSeptember 2006About Moody’s Bank Financial Strength RatingsBank credit risk is a function of a bank’s (i) intrinsic financial strength, (ii) the likelihood that it would benefit from external support in the case of need, and (iii) the risk that it would fail to make payments owing to the actions of a sov-ereign. Moody’s assigns credit risk ratings to banks and their debt obligations using a multi-step process that incorpo-rates both a bank’s intrinsic risk profile and specific external support and risk elements that can affect its overall credit risk.Moody’s Bank Financial Strength Ratings (BFSRs) represent Moody’s opinion of a bank’s intrinsic safety and soundness. Assigning a BFSR is the first step in Moody’s bank credit rating process.Unlike Moody’s deposit and debt ratings, BFSRs do not address either the probability of timely payment (i.e. default risk) or the loss that an investor may suffer in the event of a missed payment (i.e. severity of loss). Instead, BFSRs are a measure of the likelihood that a bank will require assistance from third parties such as its owners, its industry group, or official institutions, in order to avoid a default. BFSRs do not take into account the probability that the bank will receive such external support, nor do they address the external risk that sovereign actions may interfere with a bank’s ability to honor its domestic or foreign currency obligations.In order to differentiate Moody’s BFSRs from our bank deposit and debt ratings, we use different rating symbols. Moody’s BFSRs range from A to E, with “A” for banks with the greatest intrinsic financial strength and “E” for banks with the least intrinsic financial strength. A “+” modifier may be appended to ratings below the “A” category and a “-”modifier may be appended to ratings above the “E” category to identify those banks which are placed higher (+) or lower (-) in a rating category.Moody’s introduced BFSRs in 1995, and currently assigns them to almost a thousand banks and deposit-taking financial institutions worldwide. The factors considered in the assignment of BFSRs were described in Moody’s last bank rating methodologies published in 1999, and continue to form the basis of our updated approach as described in this report. These include bank-specific elements such as financial fundamentals, franchise value, and business and asset diversification, as well as risk factors in the bank’s operating environment, such as the strength and prospective performance of the economy, the structure and relative fragility of the financial system, and the quality of banking reg-ulation and supervision.The following diagram shows how BFSRs fit into Moody’s overall approach to assigning bank credit ratings. The left side shows the principal factors that are used to determine a bank’s BFSR. This report describes how these are measured and analyzed to derive a BFSR.2Moody’s Rating MethodologyThe right side of the diagram summarizes the specific external support and risk elements that are combined with the BFSR to determine Moody’s local currency and foreign currency deposit and debt ratings. In October 2005 Moody’s proposed to incorporate joint-default analysis (JDA) into how it evaluates external support factors for banks; we published updates on this proposal in April and August 2006. We expect to publish and implement a final method-ology incorporating JDA into Moody’s bank credit ratings later this year.The BFSR will be mapped directly to the baseline credit assessment in Moody’s JDA framework. Like the BFSR, a baseline credit assessment is a measure of an issuer’s stand-alone default risk assuming there is no systemic or other external support. For banks, the baseline credit assessment reflects what the local currency deposit rating would be without any assumed external support from a government or other third party. In the October 2005 request for com-ment we published a mapping showing how Moody’s BFSRs translate into a baseline credit assessment for banks using Moody’s traditional alphanumeric rating scale.A more detailed discussion of how Moody’s evaluates the risk elements that affect foreign currency ratings for banks can be found in the 1999 bank rating methodologies, as well as in more recent publications.3About the Rated UniverseMoody’s currently assigns BFSRs to 959 financial institutions globally (as of August 21, 2006). These financial institu-tions generally fall under the category of deposit-taking institutions, including commercial banks, savings banks, build-ing societies, cooperative banks, thrifts, and government-owned banks. Moody’s BFSRs may also be assigned to other types of financial institutions such as multilateral development banks, government-sponsored financial institutions and national development financial institutions.In a number of countries Moody’s also assigns BFSRs to a variety of other financial institutions (such as mortgage banks or other specialized banks) that, although they do not take deposits, are still chartered and regulated as banks and usually obtain some funding from the interbank market.BFSRs are generally assigned to individual banks, including those that are subsidiaries or affiliates of another bank. Therefore, there are some banking groups that have a number of banks with different BFSRs.The rated universe is spread throughout the world, with the highest concentrations in Europe, followed by the Americas, Asia (excluding Japan), Japan and the Middle East. Rated banks range in size from over $1 trillion in total assets to as small as $150 million. Some may be truly diversified global institutions, while others may operate on an extremely limited scale in a small local market.Distribution of Moody’s Bank Financial Strength Ratings3.Please see "Revised Country Ceiling Policy," June 2001; "Emerging Market Bank Ratings in Local and Foreign Currency: The Implications of Country Risk and Insti-tutional Support," December 2001; "The Implications of Highly Dollarized Banking Systems for Sovereign Credit Risk," March 2003; and "Piercing the Country Ceil-ing: An Update," January 2005.Moody’s Rating Methodology3The inherent riskiness of the banking business – as characterized by high leverage (equity capital of only 5-10% of total assets), illiquid assets (loans) financed by short-term liabilities (deposits), and a cyclical business environment –makes it difficult for all but a select number of banks that are generally extremely large and diversified to achieve and maintain a BFSR in the range from A to a high B. Solid, diversified and sustainable franchises and excellent manage-ment are also necessary attributes of A and B BFSRs.However, barring systemic stress and provided there is reasonable client confidence, banking, if conservatively managed without excessive risk-taking, is also a business allowing a stable generation of interest and fee income, albeit perhaps at a lower level of overall profitability. Therefore, BFSRs in the C category are generally available to a large number of banks even if they have limited scale and franchises, and average financials. Many institutions fall under this category. BFSRs of D are generally assigned to those that either are exhibiting modest capital, earnings, or business franchise, thus limiting their ability to deal with asset quality problems or other potential balance sheet risks, or are subject to unpredictable and unstable operating environments. BFSRs of E are typically restricted to those institutions that are under pressure to maintain their capital due to external and internal factors such as a highly volatile operating environment, recurring losses and asset quality problems, or a very high risk profile. However, regulatory forbearance can allow even insolvent banks to operate for an extended period of time, until the regulatory authorities arrange for either a rescue or a restructuring, or place the bank into liquidation.Industry Overview and Current Risk CharacteristicsThe global banking industry is made up of a highly varied group of firms offering a wide range of products and pursu-ing a wide range of business models and customers. While most banks face the same fundamental risks -- credit risk, liquidity risk, market risk, interest rate risk, and operational risk -- the extent of such risks vary considerably depending upon the products sold, the bank’s funding profile, and the markets in which it operates.General vs. Specific RisksBanking risk can be broadly divided into general risks, which apply to all banks within a system and derive to a large extent from a country’s economic strength, and specific risks, which are the product of the bank itself. In mature mar-kets, it is rare for serious difficulties experienced by a bank to be solely attributable to general risks, even though such risks certainly do have an impact on the bank’s performance. In most cases, bank failure in mature markets is the result of factors such as mismanagement, risky strategies, structurally poor performance, and franchise collapse. It is, in gen-eral, the weak banks and the highly risky banks that are the first to suffer in a shrinking or increasingly competitive market.In developing markets, general risks loom larger. Not only can general risks be more severe, but it may also be dif-ficult for any bank to avoid the consequences of a severe economic shock (such as a massive currency devaluation) or a deep economic recession. Clearly, banks which are better managed and have stronger earnings, franchises, and balance sheets are better placed to cope with general risks. However, in cases where general risks present a significant threat to the banking system of the country in question, it may well be that no bank can be assigned a BFSR at the upper end of the scale.4Moody’s Rating MethodologyFive Broad Categories of BankingOverall, the diversity of the sector can be broken down into five broad categories of banking institutions. Many banks may actually pursue a combination of these models, but we believe it is useful to address each of them separately to clarify the different risks that different banks can face.1. Wholesale banks: These banks focus on serving large corporate or institutional customers. While many wholesale banks have traditionally focused primarily on lending (and, in some countries, making equity investments), they fre-quently offer a much broader array of services to their customers, including not just loans but also treasury manage-ment and transaction services, foreign exchange services, trade finance, derivatives, debt and equity underwriting and market-making, and insurance. Because their customers are often very large entities, wholesale banks, especially smaller ones, can have significant customer concentration risks; they may also have industry concentration risks, espe-cially if they operate primarily within a particular region or market. Also, while a portion of their activities may be funded with corporate customer deposits, typically such banks are heavily reliant upon wholesale funding from both the interbank and capital markets. Such funding can be highly confidence-sensitive, exposing the bank to substantial liquidity risk if it is not conservatively managed.4Since their customers tend to be concentrated in larger cities and economic regions, wholesale banks generally do not require as substantial a physical presence as most retail banks. With fewer fixed costs, this often means a more flex-ible cost structure. However, customers can develop strong relationships with individual bankers (instead of with the bank itself), making retention of personnel a critical element to long-term success.As discussed below, both globalization and the growth of local capital markets can pose significant challenges for wholesale banks, as more of their customers have the ability to tap the capital markets directly for funding. This can lead to greater earnings volatility, as wholesale banks increase their capital markets activities in order to retain their customers, and also expand into potentially riskier lending businesses to replace lost lending opportunities.2. Retail banks: These banks focus primarily on serving individuals and/or small and middle market businesses. They may offer a wide array of products, including deposit-taking and lending, asset management and insurance, cash man-agement and transaction services, and even trade finance and foreign exchange services. A defining feature of such banks is that they are often locally or regionally focused. This reflects the retail nature of the customer base. While some functions may be centralized, direct customer interaction remains an important part of the service most retail banks provide. Given the wide dispersion of potential customers (both individuals and businesses), and their preference for local interaction, this requires a physical presence in the form of retail branches. Many retail banks also site their branches in clusters to benefit from classic network economies, although this is not always the case. (This is especially true for retail banks serving individuals; retail banks serving only small and middle market businesses may have less need for clusters of branches, but are still likely to require more branches than a wholesale bank.) As retail banks grow, they may develop more and more clusters of branches, growing from merely a local or regional presence into a national or even international one. Nonetheless, even an international retail bank can usually best be thought of as a combination of local retail banks.Given the need to have a significant physical infrastructure and to support significant daily customer transaction volumes, most retail banks have fairly inflexible cost structures. This makes stable revenue generation critical. T o address this need, most retail banks focus on generating recurring business with relationship customers and increasing the level of cross-selling of products including insurance products. Because their customers are small, retail banks do not usually have significant customer concentration risks; however, they may still have industry concentration risks since they frequently operate within a particular region.5Retail banks are often funded primarily with customer deposits. However, pressure to grow assets and earnings, especially in more mature markets, can lead to loan growth that far outstrips deposit growth. Such banks must rely more heavily upon wholesale funding, which can pressure net interest margins, reducing the bank’s profitability, while at the same time also exposing it to greater liquidity risk and interest rate risk.As discussed below, both de-regulation and technological innovation can pose a significant threat to retail banks because they provide their customers with greater access to competing products through alternative distribution chan-nels, and may also reduce competitors’ costs to provide those products. While retail banking has not traditionally pos-sessed much in the way of economies of scale, to the extent that such technological innovations create economies of scale, it may pose even greater challenges to the smaller retail providers.4.Please see discussion of Liquidity Management under Rating Factor 2.5.Please see discussion on Credit Risk Concentrations under Rating Factor 2.Moody’s Rating Methodology53. Universal banks: These banks are not so much a separate business model from either retail banks or wholesale banks, but rather are usually characterized by a combination of retail banking and wholesale banking, frequently also combined with activities such as private banking, asset management, or insurance. Universal banks often rank among the largest banks in a country. Universal banking can potentially provide greater earnings diversification as well as a more stable funding profile (to the extent that the more deposit-rich retail banking activities provide funding for some of the wholesale activities) than either retail banking or wholesale banking can provide on their own. However, the complexity of managing a universal bank can require considerable managerial resources. Furthermore, the disparate activities of a universal bank can at times pose conflicts of interest which, if not carefully managed, can cause reputation damage, harming the franchise. In some jurisdictions, the complexity of a universal bank also raises questions about the depth or effectiveness of regulatory oversight over such disparate activities.4. Policy banks: Moody’s defines policy banks as state-owned institutions that have explicit or implicit public policy mandates. Some state-owned banks have specific public policy mandates. These banks are often heavily dependent on government-directed business, which may or may not be profitable. Other state-owned banks, while not subject to specific public policy mandates, may still have to contend with bureaucratic controls and pressure from politicians that forces them to lend to certain favored industries or regions. Even though such banks may have substantial market shares, they frequently have weak earnings, lack strong management, and suffer from poor asset quality and controls. This usually translates into low BFSRs, although such banks also usually benefit from regulatory forbearance or other forms of government assistance, providing support to their deposit and debt ratings. Even when well run, policy banks usually still have substantial industry concentrations, reflecting their reason for being or the limitations of their char-ters.5. Specialized banks: These are niche players, most often specialized lenders such as mortgage banks, development banks, public-sector lenders, credit card banks, or export-finance entities. Some are the legacy of past government pol-icies and regulatory barriers that disappeared following deregulation and liberalization, while others were formed as a direct result of deregulation and technological innovation. Because they often have limited product offerings and/or a limited customer base, specialized banks can be more vulnerable to competitive pressures or changing economic con-ditions. However, some specialized banks, either by virtue of still-strong regulatory barriers or through substantial economies of scale and a dominant market share, usually combined with a focus on less volatile loan products such as public sector lending or mortgages, can still support high BFSRs. As with wholesale banks, specialized banks are typi-cally heavily reliant upon wholesale funding. Such funding can be highly confidence-sensitive, exposing the bank to substantial liquidity risk if it is not conservatively managed.Although the risks are somewhat different, we also include captive banks in this category. Captives are usually owned or controlled by an industrial corporation and are used to provide financing for customers purchasing products sold by the corporation, and/or to provide internal financing to the corporate and its affiliates, serving in essence as the corporate’s treasury function. Similar to other specialized banks, captives tend to have limited product offerings and a limited customer base. Even when they are lending to customers rather than to the corporate itself, their performance can still be significantly affected by the performance of the corporate.Key Industry Risks: Transformation Will Continue, Whether Banks are Ready or NotThe global banking industry is in the midst of a significant transformation, driven by substantial changes in the busi-ness environment. This transformation, begun in some countries well over a decade ago, is now occurring at different rates of change in most countries around the world. While much of the change is occurring in mature markets, devel-oping markets are also affected. These developments pose significant challenges and risks for all banks. Many banks are struggling to adjust to the substantial changes already underway. Moody’s expects that many banks will not succeed in making the transformation, and will either be driven to consolidate with a more successful competitor or will gradu-ally weaken as its franchise and earnings power are eroded away. Six major catalysts are driving this transformation. •Deregulation – is breaking down barriers within the banking industry in many countries and enabling banks to adopt diversification strategies and to compete against each other on a level playing field. In some countries it is also allowing for the entrance of new specialized competitors.•Disintermediation – a byproduct of deregulation, it is brought about by financial liberalization and the expansion of capital markets, allowing both borrowers and investors to bypass banks in favor of capital market products. The growing trend towards privatization of pension funds is also creating a growing pool of funds managed by invest-ment professionals, helping to fuel this trend.•Technological Innovation – is reducing transaction and information costs, facilitating the creation of new distri-bution channels, and allowing for innovation in retail lending (data mining), funding (securitization), and risk management (derivatives). At the same time, such technologies may also be creating potential economies of scale where none previously existed.6Moody’s Rating Methodology•Globalization – pressures banks to follow their business customers around the world, and forces them to compete with other banks globally for those customers’ business. Globalization gives banks in developing markets access to growing pools of funding due to the growth of global capital markets. However, many banks obtaining first-time access to wholesale funding have shown themselves to be ill-equipped for the liquidity risks such funding can pose. •Privatization – Governments are increasingly seeking to get out of the business of banking. While this is clearly not universal, and in some cases is being done with great reluctance, nonetheless the privatization of formerly state-owned banks could potentially reduce subsidized competition, benefiting all banks competing in the same market. However, the social or political costs of such actions may be more than some governments are willing to tolerate. And for the management of formerly state-owned banks it can be a considerable challenge to develop a credit culture based on analyzing a client’s ability to repay loans, as opposed to relying on imputed state guaran-tees.•Increased shareholder power – with more banks being owned by private investors and with more investment funds being managed by professional investors, banks globally are facing increasing pressure from powerful insti-tutional shareholders for higher returns. T o remain competitive in this more unforgiving market, banks are increasingly shifting to shareholder value-creation strategies, which may not always benefit bondholders. Framework for Assigning Bank Financial Strength RatingsMoody’s bank ratings reflect our opinion of long-term relative risk and are, of necessity, forward-looking in nature because they apply to liabilities that may pay out over long periods of time. Historical experience has shown that look-ing only at the current financial condition of a bank is not always an accurate predictor of its future financial perfor-mance and financial strength. We believe there are significant qualitative factors which play an important role in determining the stability and predictability of a bank’s financial performance over time. Thus Moody’s analytical approach includes significant qualitative analysis in addition to quantitative analysis, and incorporates the opinions and judgments of experienced analysts.As noted above, the factors considered in the assignment of Bank Financial Strength Ratings were described in Moody’s last bank rating methodologies published in 1999, and remain at the basis of the updated methodology. We focus on five key rating factors that we believe are critical to understanding a bank’s financial strength and risk pro-file. They are:1. Franchise Value2. Risk Positioning3. Regulatory Environment4. Operating Environment5. Financial FundamentalsIn the following sections we review the five key rating factors, discuss why each factor is important to our BFSRs, and explain the relevant metrics or “sub-factors” that we use to measure performance for each key rating factor. Some of the metrics that we consider important are purely quantitative, while others include elements of qualitative judg-ment or – where hard data is not reasonably accessible — educated estimates. For those involving a qualitative assess-ment, we have provided qualitative descriptions that we believe help to differentiate among risk profiles at different banks. T o dampen the cyclical nature of the industry, most of the financial metrics we use are three-year averages.For each of these factors, the methodology outlines in a summary mapping table either the range of financial met-rics or the qualitative description that would typically correspond with a given BFSR level, ranging from A to E. Evaluating OutliersIt is unlikely that every bank’s BFSR will be consistent with the rating level guidelines for every rating factor. This is because a bank typically has a variety of strengths and weaknesses which combine to reflect its overall financial risk profile. For those banks that show up as frequent outliers for their respective rating category, there could be several different explanations. The most obvious one would be that there is likely pressure on its BFSR, either up or down. But there also may be unique characteristics of the bank’s accounting, regulatory or market environment that limit the comparability of certain key factors and metrics. And finally, some elements of the bank’s business or financial profile may receive greater weight in our analysis.Moody’s Rating Methodology7。

BEC中级单词

BCE中级词汇整理1. absence n.缺席, 离开2. absent adj.不在,不参与3. absenteeism n。

(经常性)旷工, 旷职4. absorb v。

吸收, 减轻(冲击、困难等)作用或影响5. abstract n。

摘要6. access n.接近(或进入)的机会,享用权v.获得使用计算机数据库的权利7. accommodation n.设施, 住宿8. account n.会计帐目9. accountancy n.会计工作10. accountant n。

会计11. accounts n.往来帐目12. account for 解释,说明13. account executive n.(广告公司)客户经理14. *accruals n。

增值, 应计15. achieve v。

获得或达到,实现,完成16. acknowledge v.承认,告知已收到(某物), 承认某人17. acquire v.获得,得到18. *acquisition n。

收购, 被收购的公司或股份19. acting adj.代理的20. activity n.业务类型21. actual adj.实在的,实际的,确实的22. adapt v。

修改, 适应23. adjust v.整理,使适应24. administration n。

实施, 经营, 行政25. administer v.管理,实施26. adopt v。

采纳, 批准,挑选某人作候选人27. advertise v.公布,做广告28. ad n.做广告, 登广告29. advertisement n.出公告,做广告30. advertising n。

广告业31. after-sales service n.售后服务32. agenda n。

议事日程33. agent n.代理人, 经纪人34. allocate v。

分配, 配给35. amalgamation n.合并, 重组36. ambition n.强烈的欲望,野心37. *amortise v。

中英:信用评分及模型原理解析

中英:信用评分及模型原理解析本系列博文将针对消费贷款领域的信用评分及其模型进行相关研究探讨。

虽然人人都可以通过对借款方在Lending Club和Prosper上的历史借贷数据进行分析,但我相信,了解消费信贷行为、评分机制和贷款决策背后的工作原理可以帮助投资人更好的在市场中进行决策,获得收益。

This series of blog posts tries to cover the theory behind credit scoring and models typically used in consumer lending domain. While anyone can perform statistics gymnastics given the historical loan data from Lending Club and Prosper, I believe, understanding the theory behind consumer credit behavior, scoring and lending decision making is important to profit from the opportunities in the marketplace lending.消费信贷一直是推动世界领先国家经济转型的主要力量。

在过去的50年里,消费开支也因此有所增加。

根据纽约联邦储备银行家庭债务和信用季度报告,2014年8月,消费者负债总额为11.63万亿美元,其中74%为按揭和净值贷款,10%为学生贷款,8%为汽车贷款,以及6%为信用卡债务。

消费信贷需求增长率极高,自动化风险评估系统势在必行。

The consumer credit has been the driving force behind the economies of leading nations. It has been responsible for growth in consumer spending in last 50 years. According to Federal Reserve Bank of New York’s Quarterly Rep ort on Household Debt and Credit Report, August 2014, the total consumer indebtedness stands at $11.63 trillion with 74% in mortgage and home equity line of credit, 10% in student loans, 8% in auto loans, and 6% in credit card debt. The demand for consumer credit is growing at extremely high rate creating opportunity forautomated risk assessment systems.信用评分Credit Scoring信用评分最早始于上世纪50年代初。

催款外贸信函

催款外贸信函催款外贸信函催款外贸信函外贸信函之:如何催款外贸的大部分工作都是通过电子邮件来完成的。

因为,做外贸应该掌握各种外贸函电的书写格式和要点。

一般的客户开发邮件、客户维护邮件我们见得比较多,也很熟悉了。

今天特意找了一篇催款函文范文。

虽然此类函电不常用,但是也有必要了解,最好掌握。

催款,有一点全世界都通用,那就是得客气。

外贸催款函电也属于外贸商务书信范畴,因此,也应当遵守外贸商务信函的一般规则,那就是间明扼要。

不能拖泥带水,一是节省双方时间,二是以求把主题表达明确。

如果太过啰嗦,则有可能出现说多错多。

subject demanding overdue paymentdear sirs,acas you are usually very prompt in settling your acs, we wonder whether there is any special reason why we have not received payment of the above ac, already a month overdue. we think you may not have received the statement of ac we sent you on 30th august showing the balance of us$ 80,000 you owe. we send you a copy and hope it may have your early attention. yours faithfully,xxx催款函主题:索取逾期账款亲爱的先生:第8756号账单鉴于贵方总是及时结清项目,而此次逾期一个月仍未收到贵方上述账目的欠款,我们想知道是否有何特殊原因。

我们猜想贵方可能未及时收到我们8月30日发出的80,000美元欠款的账单。

现寄出一份,并希望贵方及早处理。

你真诚的xxxsubject urging paymentdear sirs,acnot having received any reply to our e-mail of september 8 requesting settlement of the above ac, we are writing again to remind you that the amount still owing isus$ 80,000. no doubt there is some special reason for delay in payment and we should welcome an explanation and also your remittance,yours faithfully,xxx催款函主题:再次索取欠款原文来自必克英语http:///外贸英语函电催款函范文催款函是卖放在规定期限内未收到货款,提醒或催促买方付款的函件。

纯正地道英语口语听力

纯正地道英语口语听力纯正地道的美语口语听力,我们可以仔细地研磨研磨。

下面是店铺给大家整理的纯正地道英语口语听力,供大家参阅!纯正地道英语口语听力:信用不佳Having Bad Credit 信用不佳Alisha: This is the second time I’ve been turned down for a credit card in a month. I don’t knowwhat I’m doing wrong.这是我一个月之内第二次信用卡被拒了。

我不知道自己做错了什么。

James: Have you checked your credit report recently? Maybe you have a bad credit rating.你最近有没有查看信用记录?或许你的信用评级不好。

Alisha: I have a full-time job with a good income, which they can easi ly verify, and I don’t haveany outstanding debt, so what could be the problem?我有一份收入良好的全职工作,他们很容易证实,我也没有未偿付债务,那可能是什么问题呢?James: Have you had a credit card before?你以前有没有信用卡呢?Alisha: Yes.有。

James: Did you always make your payments on time?你有没有及时支付呢?Alisha: Well, no.哦,没有。

James: Then that may be your answer. Your payment history makes a big difference with thecredit bureau. If you’ve missed payments or been late, that’s a big strike against you.可能就是这个问题了。

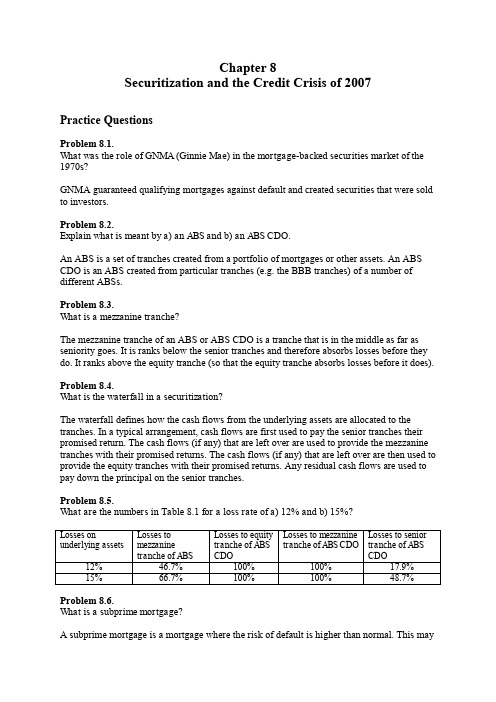

期权期货与其他衍生产品第九版课后习题与答案Chapter (8)

Chapter 8Securitization and the Credit Crisis of 2007Practice QuestionsProblem 8.1.What was the role of GNMA (Ginnie Mae) in the mortgage-backed securities market of the 1970s?GNMA guaranteed qualifying mortgages against default and created securities that were sold to investors.Problem 8.2.Explain what is meant by a) an ABS and b) an ABS CDO.An ABS is a set of tranches created from a portfolio of mortgages or other assets. An ABS CDO is an ABS created from particular tranches (e.g. the BBB tranches) of a number of different ABSs.Problem 8.3.What is a mezzanine tranche?The mezzanine tranche of an ABS or ABS CDO is a tranche that is in the middle as far as seniority goes. It is ranks below the senior tranches and therefore absorbs losses before they do. It ranks above the equity tranche (so that the equity tranche absorbs losses before it does). Problem 8.4.What is the waterfall in a securitization?The waterfall defines how the cash flows from the underlying assets are allocated to the tranches. In a typical arrangement, cash flows are first used to pay the senior tranches their promised return. The cash flows (if any) that are left over are used to provide the mezzanine tranches with their promised returns. The cash flows (if any) that are left over are then used to provide the equity tranches with their promised returns. Any residual cash flows are used to pay down the principal on the senior tranches.Problem 8.5.What are the numbers in Table 8.1 for a loss rate of a) 12% and b) 15%?Problem 8.6.What is a subprime mortgage?A subprime mortgage is a mortgage where the risk of default is higher than normal. This maybe because the borrower has a poor credit history or the ratio of the loan to value is high or both.Problem 8.7.Why do you think the increase in house prices during the 2000 to 2007 period is referred to as a bubble?The increase in the price of houses was caused by an increase in the demand for houses by people who could not afford them. It was therefore unsustainable.Problem 8.8.Why did mortgage lenders frequently not check on information provided by potential borrowers on mortgage application forms during the 2000 to 2007 period?Subprime mortgages were frequently securitized. The only information that was retained during the securitiza tion process was the applicant’s FICO score and the loan-to-value ratio of the mortgage.Problem 8.9.How were the risks in ABS CDOs misjudged by the market?Investors underestimated how high the default correlations between mortgages would be in stressed market conditions. Investors also did not always realize that the tranches underlying ABS CDOs were usually quite thin so that they were either totally wiped out or untouched. There was an unfortunate tendency to assume that a tranche with a particular rating could be considered to be the same as a bond with that rating. This assumption is not valid for the reasons just mentioned.Problem 8.10.What is meant by the term “agency costs”? How did agency costs play a role in the credit crisis?“Agency costs” is a term used to describe the costs in a situation where the interests of two parties are not perfectly aligned. There were potential agency costs between a) the originators of mortgages and investors and b) employees of banks who earned bonuses and the banks themselves.Problem 8.11.How is an ABS CDO created? What was the motivation to create ABS CDOs?Typically an ABS CDO is created from the BBB-rated tranches of an ABS. This is because it is difficult to find investors in a direct way for the BBB-rated tranches of an ABS.Problem 8.12.Explain the impact of an increase in default correlation on the risks of the senior tranche of an ABS. What is its impact on the risks of the equity tranche?As default correlation increases, the senior tranche of a CDO becomes more risky because it is more likely to suffer losses. As default correlation increases, the equity tranche becomes less risky. To understand why this is so, note that in the limit when there is perfect correlationthere is a high probability that there will be no defaults and the equity tranche will suffer no losses.Problem 8.13.Explain why the AAA-rated tranche of an ABS CDO is more risky than the AAA-rated tranche of an ABS.A moderately high default rate will wipe out the tranches underlying the ABS CDO so that the AAA-rated tranche of the ABS CDO is also wiped out. A moderately high default rate will at worst wipe out only part of the AAA-rated tranche of an ABS.Problem 8.14.Explain why the end-of-year bonus is sometimes r eferred to as “short-term compensation.”The end-of-year bonus usually reflects performance during the year. This type of compensation tends to lead traders and other employees of banks to focus on their next bonus and therefore have a short-term time horizon for their decision making.Problem 8.15.Add rows in Table 8.1 corresponding to losses on the underlying assets of (a) 2%, (b) 6%, (c) 14%, and (d) 18%.Further QuestionsProblem 8.16.Suppose that the principal assigned to the senior, mezzanine, and equity tranches is 70%, 20%, and 10% for both the ABS and the ABS CDO in Figure 8.3. What difference does this make to Table 8.1?‘‘Resecuritization was a badly flawed idea. AAA tranches created from the mezzanine tranches of ABSs are bound to have a higher probability of default than the AAA-rated tranches of ABSs.’’ Discuss this point of view.When the AAA-rated tranches of an ABS experiences defaults, the mezzanine tranches of the ABSs must have been wiped out. As a result the AAA tranche of the ABS CDO has also wiped out. If the portfolios underlying the different ABSs have the same default rates, it must therefore be the case the AAA-rated tranche of the ABS is safer than the AAA-rated tranche of the ABS CDO. If there is a wide variation if the default rates, it is possible for theAAA-rated tranche of the ABS CDO to fare better than some (but not all) AAA rated tranches of the underlying ABSs.Resecuritization can only be successful if the default rates of the underlying ABS portfolios are not highly correlated. The best approach would seem to be to obtain as much diversification as possible in the portfolio of assets underlying the ABS. Resecuritization then has no value.Problem 8.18.Suppose that mezzanine tranches of the ABS CDOs, similar to those in Figure 8.3, are resecuritized to form what is referred to as a “CDO squared.” As in the case of tranches created from ABSs in Figure 8.3, 65% of the principal is allocated to a AAA tranche, 25% to a BBB tranche, and 10% to the equity tranche. How high does the loss percentage have to be on the underlying assets for losses to be experienced by a AAA-rated tranche that is created in this way. (Assume that every portfolio of assets that is used to create ABSs experiences the same loss rate.)For losses to be experienced on the AAA rated tranche of the CDO squared the loss rate on the mezzanine tranches of the ABS CDOs must be greater than 35%. This happens when the loss rate on the mezzanine tranches of ABSs is 10+0.35×25 = 18.75%. This loss rate occurs when the loss rate on the underlying assets is 5+0.1875×15 = 7.81%Problem 8.19.Investigate what happens as the width of the mezzanine tranche of the ABS in Figure 8.3 is decreased with the reduction of mezzanine tranche principal being divided equally between the equity and senior tranches. In particular, what is the effect on Table 8.1?The ABS CDO tranches become similar to each other. Consider the situation where the tranche widths are 12%, 1%, and 87% for the equity, mezzanine, and senior tranches. The table becomes:Suppose that the structure in Figure 8.1 is created in 2000 and lasts 10 years. There are no defaults on the underlying assets until the end of the eighth year when 17% of the principal is lost because of defaults during the credit crisis. No principal is lost during the final two years. There are no repayments of principal until the end. Evaluate the relative performance of the tranches. Assume a constant LIBOR rate of 3%. Consider both interest and principal payments.The cash flows per $100 of principal invested in a tranche are roughly as followsThe internal rates of return for the senior, mezzanine and equity tranches are approximately 3.6%, -6%, and 16.0%. This shows that the equity tranche can fare quite well if defaults happen late in the life of the structure.。

借钱不还的英语作文

借钱不还的看法英语作文1It is a common phenomenon that people sometimes fail to repay the money they borrowed. This behavior is highly unethical and can have severe consequences.Take the relationship between friends for example. Imagine a situation where one friend borrows a considerable amount of money from another with a promise to return it promptly. However, as time passes and the due date comes and goes, the borrower shows no sign of repaying. This can lead to a breakdown in trust and ultimately destroy the friendship.In the business world, the consequences of not repaying debts can be even more dire. A company that owes a large sum of money to its creditors and fails to honor its obligations may find itself in financial distress. This could result in layoffs, loss of reputation, and even bankruptcy.Honesty and integrity are of utmost importance in any financial transaction. When we borrow money, we make a commitment to repay it. Failing to do so not only violates this commitment but also reflects poorly on our character. We should always strive to keep our word and honor our financial obligations, as this is the foundation of a trustworthy and respectful society.It is a common phenomenon that some people fail to repay the money they borrowed. There are several reasons behind this behavior. One of the main causes is excessive personal consumption. Some individuals spend money beyond their means and borrow without a clear plan for repayment. For instance, they might be lured by the temptation of buying the latest electronic devices or fashionable clothes, and end up borrowing money but being unable to pay it back.Another reason is the lack of an effective supervision system in society. When there are no strict regulations and punishments for those who fail to fulfill their debt obligations, debtors may feel less pressured and act without scruples.This issue not only causes harm to the creditors but also has a negative impact on the overall social credit environment. To address this problem, it is essential to establish a sound credit system. This system should include comprehensive records of individuals' borrowing and repayment behaviors, as well as clear and strict consequences for those who default on their debts.In conclusion, only by establishing a sound credit system can we effectively prevent the occurrence of borrowing without repayment and maintain a healthy and stable social economic order.When it comes to the issue of not repaying borrowed money, it is a matter that deserves serious reflection. The act of borrowing money and then failing to return it brings numerous harms. Firstly, for the individual, their credit is damaged. Once their reputation for not repaying debts spreads, it becomes extremely difficult for them to obtain loans in the future when they are truly in need. This not only affects their own financial situation but also limits their development opportunities.Take a look at society as a whole. If such behavior becomes widespread, trust among people will diminish rapidly. The normal operation of the economy will be disrupted as people become hesitant to engage in financial transactions. No one would be willing to lend money or conduct business with others, leading to a stagnation of economic activities.To avoid such a situation, it is crucial for us to establish a correct view of money. We should understand that borrowing money is a responsibility and must be honored. Only by maintaining integrity and fulfilling our financial obligations can we build a healthy and prosperous social and economic environment. Let us all strive to be trustworthy individuals and contribute to a society based on honesty and mutual assistance.It is a common phenomenon that people sometimes fail to repay the money they borrowed, which has caused many problems and negative impacts in our lives. I have witnessed such incidents around me. For instance, one of my neighbors borrowed a considerable amount of money from my family with the promise of returning it within a specified period. However, as time passed, he disappeared without a trace, leaving us in a state of anxiety and disappointment. This incident not only caused financial losses to my family but also damaged the friendly relationship we once had with him.Another example is a colleague at work who owed money to several colleagues but refused to pay it back. This created a tense and uncomfortable atmosphere in the workplace, affecting everyone's mood and teamwork. People began to lose trust in him, and his reputation was severely damaged.The issue of borrowing money and not repaying it is not only a matter of financial transaction but also reflects a person's integrity and moral character. It is essential for us to be responsible and keep our promises when borrowing money. At the same time, we should also be cautious when lending money to others and ensure that there is a clear agreement and guarantee to avoid unnecessary disputes and losses.In today's globalized society, the issue of borrowing money and not repaying it is a common concern that varies in different countries. In some countries, there are strict legal sanctions in place to deal with this problem. For instance, severe fines and even imprisonment may be imposed on those who fail to fulfill their financial obligations. This approach acts as a powerful deterrent, making people think twice before borrowing and ensuring they do their best to repay.On the other hand, in other nations, credit rating systems play a crucial role. A person's credit score can be significantly affected if they do not repay borrowed money. This can lead to difficulties in obtaining loans, renting properties, or even getting certain jobs. Such systems encourage individuals to maintain a good credit history and honor their debts.However, despite these measures, the problem persists. To improve this situation, we need to raise public awareness about the importance of financial integrity. Schools and families should educate young people on the responsibilities that come with borrowing. Moreover, financial institutions could provide better guidance and support to borrowers, helping them manage their debts effectively.In conclusion, a combination of strict legal measures, effective credit rating systems, and enhanced education is needed to address the issue of borrowing money and not repaying it, creating a more trustworthy andstable financial environment for all.。

大学英语4U4 课文+翻译

The credit card trap1 I have a confession. Several years ago, I was standing in a queue to collect some theatre tickets for my family, and my friend was doing the same for hers. I got mine, and paid for them by credit card, feeling contented by the convenience of this cash- free transaction. It was then her turn to pay. The whole operation passed as smoothly as mine, but my delight soon turned to abject shame. My credit card was a fairly pathetic, status-free dark blue, whereas hers was a 11. 有一件事我得坦白。

几年前,我排队为家人取戏票时,我的朋友也在为她的家人取票。

我拿到了票,用信用卡付了账,对这种非现金交易的便利感到很满意。

然后就轮到她付款了,整个交易也进行得同样顺利,但我的高兴劲儿很快就变成了莫大的羞耻:我的信用卡太寒酸了,是不显示身份地位的深蓝色卡,而她的信用卡则是高级的金卡。

very exclusive gold one.2 How did she do this? How could this be? I knew I earned more than her, my car was newer, and my house was smarter. How did she get to appear more flash than me?3 Now, I had a job which was as steady as any job was in those days –that’s to say, not very, but you know, no complaints. I had a mortgage on my house, but then who didn’t? I paid off all my credit debt at the end of the month, so although technically, I was in debt to the credit card company, it was only for a matter of a few weeks. So I assumed I had a good credit rating.2她是怎样弄到金卡的?怎么会这样呢?我知道我挣得比她多,我的车比她的车新,我的家比她的家漂亮,她怎么看起来显得比我光鲜呢?3我有一份跟那时候任何工作相比还算安定的工作——虽然不是非常安定,不过我也没什么可抱怨的。

必备的外贸词汇

必备的外贸词汇Aabroad adv. 在国外,出国,广泛流传absence n. 缺席,离开absent adj. 不在,不参与absenteeism n. (经常性)旷工,旷职absorb v. 吸收,减轻(冲击、困难等)作用或影响abstract n. 摘要access n. 接近(或进入)的机会,享用权v. 获得使用计算机数据库的权利accommodation n. 设施,住宿account n. 会计帐目accountancy n. 会计工作accountant n. 会计accounts n. 往来帐目account for 解释,说明account executive n. (广告公司)客户经理accruals n. 增值,应计achieve v. 获得或达到,实现,完成acknowledge v. 承认,告知已收到(某物),承认某人acquire v. 获得,得到acquisition n. 收购,被收购的公司或股份acting adj. 代理的activity n. 业务类型actual adj. 实在的,实际的,确实的adapt v. 修改,适应adjust v. 整理,使适应administration n. 实施,经营,行政administer v. 管理,实施adopt v. 采纳,批准,挑选某人作候选人advertise v. 公布,做广告ad n. 做广告,登广告advertisement n. 出公告,做广告advertising n. 广告业after-sales service n. 售后服务agenda n. 议事日程agent n. 代理人,经纪人allocate v. 分配,配给amalgamation n. 合并,重组ambition n. 强烈的欲望,野心amortise v. 摊还analyse v 分析,研究analysis n. 分析,分析结果的报告analyst n. 分析家,化验员annual adj. 每年的,按年度计算的annual general meeting (AGM)股东年会anticipate v. 期望anticipated adj. 期待的appeal n. 吸引力apply v. 申请,请求;应用,运用applicant n. 申请人application n. 申请,施用,实施appointee n. 被任命人appraisal n. 估量,估价appreciate v. 赏识,体谅,增值appropriate v. 拨出(款项)approve v. 赞成,同意,批准aptitude n. 天资,才能arbitrage n. 套利arbitration n. 仲裁arrears n. 欠帐assemble v. 收集,集合assembly-line n. 装配线,流水作业线assess v. 评定,估价asset n. 资产current asset n. 流动资产fixed asset n. 固定资产frozen asset n. 冻结资产intangible assets n. 无形资产liquid assets n. 速动资产tangible assets n. 有形资产assist v. 援助,协助,出席audit n. 查账,审计automate v. 使某事物自动操作average n. 平均,平均水准awareness n. 意识;警觉Bbacking n. 财务支持,赞助backhander n. 贿赂backlog n. 积压(工作或订货)bad debt 死账(无法收回的欠款)balance n. 收支差额,余额balance of payments n. 贸易支付差额balance sheet n. 资产负债表bankrupt adj. 破产的bankruptcy n. 破产bank statement n. 银行结算清单(给帐户的),银行对账单bar chart n. 条形图,柱状图bargain v. 谈判,讲价base n. 基地,根据地batch n. 一批,一组,一群batch production 批量生产bear market n. 熊市beat v. 超过,胜过behave v. 表现,运转behaviour n. 举止,行为,运转情况below-the-line advertising 线下广告,尚未被付款的广告benchmark n. 衡量标准benefit n. 利益,补助金,保险金得益fringe benefits n. 附加福利sickness benefit n. 疾病补助费bid n. 出价,投标takeover bid n. 盘进(一个公司)的出价bill n. 账单,票据billboard n. (路边)广告牌,招贴板black adj. 违法的in the black 有盈余,贷方black list 黑名单,禁止贸易的(货物、公司及个人)名单black Monday n. 黑色星期一,指1987年10月国际股票市场崩溃的日子blue chips n. 蓝筹股,绩优股blue-collar adj. 蓝领(工人)的Board of Directors n. 董事会Bond n. 债券bonus n. 津贴,红利books n. 公司帐目book value n. 账面价值,(公司或股票)净值bookkeeper n. 簿记员,记帐人boom n. 繁荣,暴涨boost v. 提高,增加,宣扬bottleneck n. 瓶颈,窄路,阻碍bottom adj. 最后的,根本的v. 到达底部,建立基础bounce v. 支票因签发人无钱而遭拒付并退回brainstorm n./v. 点子会议,献计献策, 头脑风暴branch n. 分支,分部brand n. 商标,品牌brand leader n. 占市场最大份额的品牌,名牌brand loyalty n. (消费者)对品牌的忠实break even v. 收支相抵,不亏不盈break even point 收支相抵点, 盈亏平衡点breakthrough n. 突破brief n. 摘要brochure n. 小册子broker n. 经纪人,代理人bull market 牛市budget n. 预算bulk n. 大量(货物) adj. 大量的bust adj. 破了产的buyout n. 买下全部产权CCAD(=Computer Aided Design) n. 计算机辅助设计call n. 打电话call on v. 呼吁,约请,拜访campaign n. 战役,运动candidate n. 求职者,候选人canteen n. 食堂canvass v. 征求意见,劝说capacity n. 生产额,(最大)产量caption n. 照片或图片下的简短说明capital n. 资本,资金capture v. 赢得cash n. 现金,现付款v. 兑现cash flow n. 现金流量case study n. 案例分析catalogue n. 目录,产品目录catastrophe n. 大灾难,大祸CEO n. Chief Executive Officer(美)总经理chain n. 连锁店challenger n. 挑战者channel n. (商品流通的)渠道charge n. 使承担,要(价),把……记入(账册等)chart n. 图表checkout n. 付款台chief adj. 主要的,首席的,总的CIF, c.i.f. 成本保险费加运费circular n. 传阅的小册子(传单等)circulate v. 传阅claim n./v. 要求,索赔client n. 委托人,顾客cold adj. 没人找上门来的,生意清淡的commercialise v. 使商品化commission n. 佣金commitment n. 承诺commodity n. 商品,货物company n. 公司limited (liability) company (ltd.) 股份有限公司public limited company (plc) n. 股票上市公司compensate v. 补偿,酬报compensation n. 补偿,酬金compete v. 比赛,竞争competition n. 比赛,竞争competitor n. 竞争者,对手competitive adj. 竞争性的component n. 机器元件、组件、部件,部分concentrated marketing n. 集中营销策略condition n. 条件,状况configuration n. 设备的结构、组合conflict n. 冲突,争论conglomerate n. 综合商社,多元化集团公司consolidate v. 帐目合并consortium n. 财团constant adj. 恒定的,不断的,经常的consultant n. 咨询人员,顾问,会诊医生consumables n. 消耗品consumer durables n. 耐用消费品(如:洗衣机)consumer goods n. 消费品,生活资料contingency n. 意外事件continuum n. 连续时间contract n. 合同,契约contractor n. 承办商,承建人contribute v. 提供,捐献contribution n. 贡献,捐献,税conversion n. 改装,改造conveyor n. 运送,传递,转让core time n. (弹性工作制的)基本上班时间(员工于此段时间必须上班,弹性只对除此以外的时间有效)cost n. 成本fixed costs 固定成本running costs 日常管理费用variable costs 可变成本cost-effective adj. 合算的,有效益的costing n. 成本计算,成本会计credit n. 赊购,赊购制度credit control 赊销管理(检查顾客及时付款的体系)letter of credit 信用证credit limit 赊销限额credit rating 信贷的信用等级,信誉评价creditor n. 债权人,贷方creditworthiness n. 信贷价值,信贷信用crisis n. 危机,转折点critical adj. 关键的critical path analysis n. 关键途径分析法currency n. 货币,流通current adj. 通用的,现行的Current account 往来帐户,活期(存款)户current assets n. 流动资产current liabilities n. 流动负债customise v. 按顾客的具体要求制造(或改造等);顾客化cut-throat adj. 残酷的,激烈的cut-price a. 削价(出售)的CV(=curriculum vitae) n. 简历,履历cycle time n. 循环时间Ddamages n. 损害,损失deadline n. 最后期限deal n. 营业协议,数量 v. 交易dealer n. 商人debit n. 借方,欠的钱 v. 记入帐户的借方debt n. 欠款,债务to get into debt 负债to be out of debt 不欠债to pay off a debt 还清债务debtor n. 债务人aged debtors 长期债务人declare v. 申报,声明decline n./v. 衰退,缓慢,下降decrease v. 减少deduct v. 扣除,减去default n. 违约,未履行defect n. 缺陷defective adj. 有缺点的defer v. 推迟deferred payments n. 延期支付deficit n. 赤字delivery cycle n. 交货周期demand management n. 需求规化demotivated adj. 消极的,冷谈的deposit n. 储蓄,预付(定金)depot n. 仓库depreciate v. 贬值,(对资产)折旧depressing adj. 令人沮丧的deputy n. 代理人,副职,代理devalue v. 货币贬值(相对于其它货币)diet n. 饮食,食物,特种饮食differentiation n. 区分,鉴别dimensions n. 尺寸,面积,规模direct v 管理,指导director n. 经理,主管Managing Director n. 总经理direct cost n. 直接成本direct mail n. (商店为招揽生意而向人们投寄的)直接邮件direct selling n. 直销,直接销售directory n. 指南,号码簿discount n. 折扣,贴现dismiss v. 让……离开,打发走dismissal n. 打发走dispatch n./v. 调遣display n./v. 展出,显示dispose v. 安排,处理(事务)dispose of 去掉,清除distribution n. 分配,分发,分送产品diversify v. 从事多种经营;多样化divest v. 剥夺dividend n. 股息,红利,年息division n. 部门dog n. 滞销品down-market a./ad. 低档商品的down-time/downtime n. 设备闲置期DP(=Data Processing) n. 计算机数据处理,计算机数据处理部门dramatic adj. 戏剧性的drive n. 积极性,能动性due adj. 应付的,预期的dynamic adj. 有活力的Eearnings n. 工资efficiency n. 效率endorse v. 背书,接受engage v. 雇用entitle v. 授权entitlement n. 应得的权利holiday entitlement n. 休假权equity n. 股东权益equity capital n. 股本equities 普通股,股票estimated demand n. 估计需求evaluate v. 估价,评价eventual adj. 最终的exaggerate v. 夸张exceed v. 超过exhibit n. 展览,表现expenditure n. 花费,支出额expense n. 费用,支出expense account n. 费用帐户expenses n. 费用,业务津贴expertise n. 专长,专门知识和技能exposure n. 公众对某一产品或公司的知悉;广告所达到的观众总数Ffacilities n. 用于生产的设备、器材facilities layout n. 设备的布局规化、计划facilities location n. 设备安置factoring n. 折价购买债券fail-safe system n. 安全系统feasibility study n. 可行性研究feedback n. 反馈,反馈的信息field n. 办公室外边,具体业务file n. 文件集,卷宗,档案,文件 v. 把文件(或资料)归档fill v. 充任finance n. 资金,财政 v. 提供资金financial adj. 财政的financing n. 提供资金,筹借资金finished goods n. 制成品firm n. 公司fire v. 解雇fix v. 确定,使固定在fix up v. 解决,商妥fiscal adj. 国库的,财政的flagship n. 同类中最成功的商品,佼佼者flexible adj. 有弹性的,灵活的flextime n. 弹性工作时间制flier(=flyer) n. 促销传单float v. 发行股票flop n. 失败flow shop n. 车间fluctuate v. 波动,涨落,起伏FOB, f.o.b n. 离岸价follow-up n. 细节落实,接连要做的事forecast v. 预测four P’s 指产品PRODUCT、价格PRICE、地点PLACE、促销PROMOTIONframework n. 框架,结构franchise n. 特许经销权 v. 特许经销,给予特许经销权franchisee n. 特许经营人franchiser n. 授予特许经营权者fraud n. 欺骗freebie n. (非正式的)赠品,免费促销的商品freelance n.& adj. 自由职业者(的)funds n. 资金,基金futures n. 期货交易Ggap n. 缺口,空隙gearing n. 配称(即定息债务与股份资本之间的比率)gimmick n. 好主意,好点子goal n. 目标going adj. 进行的,运转中的going rate n. 产品的市场价格goods n. 货物,商品goodwill n. 声誉go public v. 首次公开发行股票grapple with v. 与……搏斗,尽力解决grievance n. 申诉,抱怨gross adj. 总的,毛的gross margin n. 毛利率gross profit n. 毛利gross yield n. 毛收益gradually adv. 逐渐地group n. (由若干公司联合而成的)集团grow v. 增长,扩大growth n. 增长,发展guarantee n. 保证,保单guidelines n. 指导方针,准则Hhand in v. 呈送hand in one’s notice 递交辞呈handle v. 经营hands on adj. 有直接经验的hard sell n. 强行推销hazard n. 危险,危害行为head n. 主管,负责health and safety n. 健康和安全hedge n. 套期保值hidden adj. 隐藏的,不明显的hierarchy n. 等级制度,统治集团,领导层hire v. 雇用hire purchase n. 分期付款购物法hit v. 击中,到达holder n. 持有者holding company n. 控股公司hostile adj. 不友好的,恶意的HRD n. 人力资源发展部human resources n. 人力资源hype n. 天花乱坠的(夸张)广告宣传Iimpact n. 冲击,强烈影响implement v. 实施,执行implication n 隐含意义incentive n. 刺激;鼓励income n. 工资或薪金收入,经营或投资的收入earned income 劳动收入,劳动所得unearned income 非劳动收入,投资所得increment v. 定期增加incur v 招致,承担indemnity n. 偿还,赔偿index n. 指数,索引retail price index 零售价格指数indirect costs n. 间接成本induction n. 就职industrial adj. 工业的industrial action n. (罢工、怠工等)劳工行动industrial relations n. 劳资关系inefficiency n. 低效率,不称职inflate v. 抬高(物价),使通货等)膨胀inflation n. 通货膨胀infringe v. 违法,违章initial adj. 初步的innovate v. 革新input n. 投入insolvent adj. 无清偿力的installment n. 部分,分期付款insure v. 给……保险,投保insurance n. 保险interest n. 利息,兴趣interest rate n. 利率interim n. 中期,过渡期间intermittent production n. 阶段性生产interview n./v. 面试interviewee n. 被面试的人interviewer n. 主持面试的人,招聘者introduce v. 介绍,提出inventory n. 库存buffer inventory n. 用于应付突发性需求的存货capacity inventory n. 用于将来某时使用的存货cycle inventory n. 循环盘存decoupling inventory n. 保险性存货(以应付万一)finished goods inventory n. 制成品存货(盘存)pipeline inventory n. 在途存货raw materials inventory n. 原材料存货work-in-progress inventory n. 在制品盘存(存货)invest v. 投资investment n. 投资investor n. 投资者invoice n. 发票 v. 给(某人)开发票irrevocable adj. 不可撤消的,不能改变的issue n. 发行股票rights issue n. 优先认股权IT=Information Technology 信息技术item n. 货物,条目,条款Jjob n. 工作job description 工作说明,职务说明job lot n. 一次生产的部分或少数产品job mobility 工作流动job rotation 工作轮换job satisfaction 工作的满意感(自豪感)job shop n. 专门车间jobbing n. 为一次性的或小的订货需求而特设的生产制度joint adj. 联合的joint bank account (几个人的)联合银行存款帐户journal n. 专业杂志jurisdiction n. 管辖(权)junk bonds n. 低档(风险)债券,垃圾债券junk mail n. (未经收信人要求的)直接邮寄的广告宣传just-in-time n. 无库存制度Kkey adj. 主要的,关键的knockdown adj. (价格)很低的know-how n. 专门技术Llabel n. 标签,标牌 v. 加标签,加上标牌labour n. 劳动,工作,劳动力labour market 劳动力市场labour relations 劳资关系labour shortage 劳动力短缺launch v. 在市场推出一种新产品n. 新产品的推出lay-off/layoff n./v. 临时解雇layout n. 工厂的布局lead v. 领先,领导lead time n. 完成某项活动所需的时间leaflet n. 广告印刷传单lease n. 租借,租赁物legal adj. 合法的lend v. 出借,贷款lessee n. 承租人lessor n. 出租人ledger n. 分类帐nominal ledger n. 记名帐purchase ledger n. 进货sales ledger n. 销货帐leverage n. 杠杆比率liability n. 负债liabilities n. 债务licence(US: license) n. 许可证license v. 许可,批准life cycle n. 寿命周期likely adj. 可能的line process 流水线(组装)link n. 关系,联系,环liquid adj. 易转换成现款的liquidate v. 清算liquidity n. 拥有变现力liquidation n. 清理(关闭公司),清算liquidator n. 清算人,公司资产清理人listed adj. 登记注册的listing n. 上市公司名录literature n. (产品说明书之类的)印刷品,宣传品litigate v. 提出诉讼loan n./v. 贷款,暂借logo n. 企业的特有标记lose v. 亏损loser n. 失败者loss n. 损失lot n. 批,量loyalty n. 忠诚,忠实Mmagazine n. 杂志,期刊mailshot n. 邮购maintain v. 维持,保持maintenance n. 维持,坚持major adj. 重大的,主要的,较大的majority shareholding 绝对控股make n. 产品的牌子或型号make-to-order adj. 根据订货而生产的产品make-to-stock adj. 指那些在未收到订货时就已生产了的产品management n. 管理,管理部门middle management n. 中层管理人员senior management n. 高层管理人员managerial adj. 管理人员的,管理方面的manager n. 经理plant manager n. 工厂负责人line manager n. 基层负责人staff manager n. 部门经理助理management accounts n. 管理帐目matrix management n. 矩阵管理management information system(MIS) n. 管理信息系统manning n. 人员配备manpower n. 劳动力manpower resources n. 劳动力资源manual adj. 体力的,人工的,蓝领的manufacture v. (用机器)制造manufacturer n. 制造者(厂、商、公司)manufacturing adj. 制造的manufacturing industry 制造业margin n. 利润gross margin n. 毛利率net margin n. 净利润mark-up v. 标高售价,加价market n. 市场;产品可能的销量down market adv./adj. 低档商品/地的up market adj./adv. 高档商品的/地marketing mix n. 综合营销策略,指定价、促销、产品等策略的配合market leader n. 市场上的主导公司market niche n. 小摊位,专业市场的一个小部分market penetration n. 市场渗入market segmentation 市场划分market share n. 市场占有率,市场份额mass-marketing n. 大众营销术master production schedule n. 主要生产计划material requirements planning(MRP) n. 计算生产中所需材料的方法materials handling n. 材料管理,材料控制maximise v. 使增至最大限度、最大化measure n. 措施,步骤media n. 新闻工具,传媒mass media 大众传媒(如电视、广播、报纸等)merchandising n. (在商店中)通过对商品的摆放与促销进行经营merge v. 联合,合并merger n. (公司,企业等的)合并merit n. 优点,值得,应受method study n. 方法研究middleman n. 中间人,经纪人full milk n. 全脂牛奶skimmed milk n. 脱脂乳minimise v. 使减至最小限度,最小化mission n. 公司的长期目标和原则mobility n. 流动性,可移性moderately adv. 中等地,适度地monopoly n. 垄断,独占mortgage n./v. 抵押motivate v. 激励,激发……的积极性motivated adj. 有积极性的motivation n. 提供动机,积极性,动力motive n. 动机Nnegotiate v. 谈判negotiable adj. 可谈判的,可转让的net adj. 净的,纯的network n. 网络niche n. 专业市场中的小摊位notice n. 通知,辞职申请,离职通知Oobjective n. 目标,目的obsolete adj. 过时的,淘汰的,废弃的offer n. 报价,发盘offer v. 开价off-season adj./adv. 淡季的off-the-shelf adj. 非专门设计的off-the-peg adj. 标准的,非顾客化的opening n. 空位operate v. 操作,经营,管理operating profits 营业利润operations chart n. 经营(管理)表operations scheduling n. 生产经营进度表opportunity n. 机会optimize v. 优化option n. 选择权share option n. 期权organigram n. 组织图organisation chart n. 公司组织机构图orient v. 定向,指引orientation n. 倾向,方向;熟悉,介绍情况outcome n. 结果outlay n. 开销,支出,费用outlet n. 商店a retail outlet 零售店outgoings n. 开支,开销outlined adj. 概括,勾勒的草图output n. 产量outsource v. 外购产品或由外单位制做产品outstanding adj. 未付款的,应收的over-demand n. 求过于供overdraft n. 透支overdraft facility 透支限额overdraw v. 透支overhead costs n. 营业成本overheads n. 企业一般管理费用overpay n. 多付(款)overtime n. 加班overview n. 概述,概观owe v. 欠钱,应付Pp.a.(=per annum) n. 每年packaging n. 包装物;包装parent company n. 母公司,总公司part-time adj. 部分时间工作的,业余的participate v. 参加,分享 (in)partnership n. 合伙(关系),合伙,合伙企业patent n. 专利pay n. 工资,酬金v. 付钱,付报酬take-home pay 实得工资payroll n. 雇员名单,工资表peak n. 峰值,顶点penetrate v. 渗透,打入(市场)penetration n. 目标市场的占有份额pension n. 养老金,退休金perform v. 表现,执行performance n. 进行,表现工作情况performance appraisal n. 工作情况评估perk n. 额外待遇(交通、保健、保险等)personnel n. 员工,人员petty cash n. 零用现金phase out n. 分阶段停止使用pick v. 提取生产用零部件或给顾客发货picking list n. 用于择取生产或运输订货的表格pie chart n. 饼形图pilot n. 小规模试验pipeline n. 管道,渠道plant capacity n. 生产规模,生产能力plot v. 标绘,策划plough back n. 将获利进行再投资point of sale (POS) n. 销售点policy n. 政策,规定, 保险单portfolio n. (投资)组合portfolio management n. 组合证券管理post n. 邮件,邮局;职位position n. 职位potential n. 潜在力,潜势power n. 能力purchasing power 购买力PR=Public Relations 公共关系preference shares n. 优先股price n. 价格market price 市场价,市价retail price 零售价probation n. 试用期product n. 产品production cycle n. 生产周期production schedule n. 生产计划product life cycle n. 产品生命周期product mix n. 产品组合(种类和数量的组合)productive adj. 生产的,多产的profile n. 简介形象特征profit n. 利润operating profit n. 营业利润profit and loss account n. 损益帐户project v. 预测promote v . 推销promotion n. 提升,升级proposal n. 建议,计划prospect n. 预期,展望prospectus n. 计划书,说明书prosperity n. 繁荣,兴隆prototype n. 原型,样品publicity n. 引起公众注意public adj. 公众的,公开的go public 上市public sector 公有企业publicity n. 公开场合,名声,宣传publics n. 公众,(有共同兴趣的)一群人或社会人士punctual adj. 准时的punctuality n. 准时purchase v. & n. 购买purchaser n. 买主,采购人QC(=Quality Circle) n. 质检人员qualify v. 有资格,胜任qualified adj. 有资格的,胜任的,合格的qualification n. 资格,资格证明quality n. 质量quality assurance n. 质量保证quality control 质量控制,质量管理quarterly adj./adv. 季度的,按季度questionnaire n. 调查表,问卷quote n. 报价,股票牌价quotation n. 报价,股票牌价R&D Research and Development 研究与开发radically adv. 根本地,彻底地raise n. (美)增加薪金 v. 增加,提高;提出,引起range n. 系列产品rank n./v. 排名rapport n. 密切的关系,轻松愉快的气氛rate n. 比率,费用fixed rate 固定费用,固定汇率going rate 现行利率,现行汇率rating 评定结果ratio n. 比率rationalise v. 使更有效,使更合理raw adj. 原料状态的,未加工的raw material n. 原材料receive v. 得到receipt n. 收据receiver n. 接管人,清算人accounts receivable 应收帐receivership n. 破产管理recession n. 萧条reckon v. 估算,认为recognise v. 承认reconcile v. 使……相吻合,核对,调和recoup v. 扣除,赔偿recover v. 重新获得,恢复recovery n. 重获,恢复recruit v. 招聘,征募 n. 新招收的人员recruitment n. 新成员的吸收red n. 红色in the red 赤字,负债reduce v. 减少reduction n. 减少redundant adj. 过多的,被解雇的redundancy n. 裁员,解雇reference n. 参考,参考资料reference number (Ref. No.) 产品的参考号码refund n./v. 归还,偿还region n. 地区reimburse v. 偿还,报销reject n./v. 拒绝reliability n. 可靠性relief n. 减轻,解除,救济relocate v. 调动,重新安置remuneration n. 酬报,酬金rent v. 租 n. 租金rep (代表)的缩写report to v. 低于(某人),隶属,从属reposition v. (为商品)重新定位represent v. 代表,代理representative n. 代理人,代表reputation n. 名声,声望reputable adj. 名声/名誉好的reserves n. 储量金,准备金resign v. 放弃,辞去resignation n. 辞职resistance n. 阻力,抵触情绪respond v. 回答,答复response n. 回答,答复restore v. 恢复result/results n. 结果,效果retail n./v. 零售retailer n. 零售商retained earnings n. 留存收益retire v. 退休retirement n. 退休return n. 投资报酬return on investment (ROI) n. 投资收入,投资报酬revenue n. 岁入,税收review v./n. 检查reward n./v. 报答,报酬,奖赏rework v. (因劣质而)重作risk capital n. 风险资本rival n. 竞争者,对手adj. 竞争的rocket v. 急速上升,直线上升,飞升ROI Return on Investment 投资利润roughly adv. 粗略地round adj. 整数表示的,大约round trip 往返的行程royalty n. 特许权,专利权税run v. 管理,经营running adj. 运转的Ssack v. 解雇sales force 销售人员sample n. 样品v. 试验;抽样检验saturation n. (市场的)饱和(状态)saturate v. 饱和save v. 节省,储蓄savings n. 存款scale n. 刻度,层次scapegoat n. 替罪羊scare adj. 缺乏的,不足的scrap n. 废料或废品seasonal adj. 季节性的section n. 部门sector n. 部门securities n. 债券及有价证券segment n. 部分 v. 将市场划分成不同的部分segmentation n. 将市场划分成不同的部门semi-skilled adj. 半熟练的settle v. 解决,决定settlement n. 解决,清偿,支付service n. 服务,帮佣services n. 专业服务settle v. 安排,支付set up v. 创立share n. 股份shareholder n. 股东shelf-life n. 货架期(商品可以陈列在货架上的时间)shift n. 轮班showroom n. 陈列室simulation n. 模拟shop n. 商店closed shop 限制行业(只允许本工会会员)open shop 开放行业(非会员可从事的工作)shop steward 工会管事shopfloor 生产场所shortlist n. ……供最后选择的候选人名v. 把……列入最后的候选人名单sick adj. 病的sick leave 病假sick note 病假条sick pay 病假工资sickness 生病skill n. 技能,熟巧skilled employee n. 熟练工人skimming n. 高额定价,撇奶油式定价slogan n. 销售口号slump n. 暴跌a slump in sales 销售暴跌soft-sell n. 劝诱销售(术),软销售(手段)software n. 软件sole adj. 仅有的,单独的sole distributor 独家分销商solvent adj. 有偿付能力的sourcing n. 得到供货spare part n. 零部件specification n. 产品说明split v. 分离spokesman n. 发言人sponsor n. 赞助者(为了商品的广告宣传)spread n. (股票买价和卖价的)差额stable adj. 稳定的staff n. 职员stag n. 投机认股者 v. 炒买炒卖stagnant adj. 停滞的,萧条的statute n. 成文法statutory adj. 法定的steadily adv. 稳定地,平稳地stock n. 库存,股票stock exchange n. 证券交易所stockbroker n. 股票经纪人stock controller 库房管理者storage n. 贮藏,库存量strategy n. 战略streamline v. 精简机构,提高效率stress n. 压力,紧迫strike n. 罢工structure n. 结构,设备*subcontract v. 分包(工程项目),转包subordinate n. 下级adj. 下级的subscribe v. 认购subsidiary n. 子公司subsidise v. 补贴,资助subsidy n. 补助金substantially adv. 大量地,大幅度地summarise v. 概括,总结superior n. 上级,长官supervisor n. 监督人,管理人supervisory adj. 监督的,管理的supply n./v. 供给,提供survey n 调查SWOT analysis n. SWOT分析是分析一个公司或一个项目的优点、弱点、机会和风险*synergy n. 协作Ttactic n. 战术,兵法tailor v. 特制产品tailor made products 特制产品take on 雇用takeover n. 接管target n. 目标 v. 把……作为目标tariff n. 关税;价目表task n. 任务,工作task force n. 突击队,攻关小队(为完成某项任务而在一起的一组人)tax n. 税,税金capital gains tax n. 资本收益税corporation tax n. 公司税,法人税income tax n. 所得税value added tax 增值税tax allowance 免减税tax avoidance 避税taxable 可征税的taxation 征税tax-deductible 在计算所得税时予以扣除的telesales n. 电话销售,电话售货temporary adj. 暂时的temporary post 临时职位tender n./v. 投标territory n. (销售)区域tie n. 关系,联系throughput n. 工厂的总产量TQC(=Total Quality Control) n. 全面质量管理track record n. 追踪记录,业绩trade n./v. 商业,生意;交易,经商balance of trade 贸易平衡trading profit 贸易利润insider trading 内部交易trade mark 商标trade union 工会trainee n. 受培训者transaction n. 交易,业务transfer n./v. 传输,转让transformation n. 加工transparency n. (投影用)透明胶片treasurer n. 司库,掌管财务的人treasury n. 国库,财政部trend n. 趋势,时尚trouble-shooting n. 解决问题turnover n. 营业额,员工流动的比率staff turnover 人员换手率stock turnover 股票换手率Uundertake v. 从事、同意做某事undifferentiated marketing n. 无差异性营销策略uneconomical adj. 不经济的,浪费unemployment n. 失业unemployment benefit n. 失业津贴unit n. 单位unit cost n. 单位成本update v. 使现代化up to date adj./adv. 流行的,现行的,时髦的upgrade v. 升级,增加upturn n. 使向上,使朝上USP 唯一的销售计划Vvacancy n. 空缺vacant adj. 空缺的value n./v. 价值,估价valuation n. 价值value-added n. 增加值variable n. 可变物variation n. 变化,变更variety n. 多样化a variety of 多种多样的vary v. 改变,修改VAT Value Added Tax 增值税vendor n. 卖主(公司或个人)venture n. 冒险,投机venue n. 地点,集合地点viable adj. 可行的viability n. 可行性vision n. 设想,公司的长期目标vocation n. 行业,职业vocational adj. 行业的,职业的Wwage n. (周)工资wage freeze n. 工资冻结warehouse n. 仓库,货栈wealth n. 财富,资源wealthy adj. 富裕的,丰富的welfare n. 福利white-collar 白领阶层white goods n. 如冰箱和洗衣机等用在厨房中的产品wholesale n./adj./adv. 批发wholesaler 批发商wind up v. 关闭公司withdraw v. 拿走,收回,退出withdrawal n. 拿走,收回,退出wholesale n./a. 批发;批发的wholesaler n. 批发商work n. 工作working conditions n. 工作条件work-in-progress n. 工作过程workload n. 工作量work order n. (包括原料、半成品、成品的)全部存货总量work station 工作位置working capital n. 营运资本,营运资金write off v. 取消write-off n. 债务的取消Yyield n. 有效产量Zzero defect n. 合格产品zero inventory n. 零存货常见金融词汇financial turmoil/meltdown 金融危机Federal Reserve 美联储real estate 房地产share 股票valuation 股价shareholder 股东macroeconomic 宏观经济saving account 储蓄帐户go under 破产take a nosedive (股市)大跌tumble 下跌big macs,big/large-cap stock,mega-issue 大盘股offering,list 上市13.bourse 证交所Paris Bourse巴黎证券交易所Stock exchange (or market); securities house; Bourse证券交易所bourse transaction tax有价证券交易税corporate champion 龙头企业Shanghai Exchange 上海证交所pension fund 养老基金mutual fund 共同基金hedge mutual fund 对冲式共同基金underwriter 保险商government bond 政府债券subscription to government bond 认购公债amortization of government bond 政府公债分期偿还fixed rate government bond 固定利率公债budget 预算deficit 赤字delist 摘牌mongey-loser 亏损企业inventory 存货traded company,trading enterprise 上市公司state trading enterprise国营贸易企业stakeholder 利益相关者transparency 透明度market fundamentalist 市场经济基本规则damage-contral machinery 安全顾问efficient market 有效市场intellectual property 知识产权opportunistic practice 投机行为entrepreneur 企业家cook the book 做假帐regulatory system 监管体系portfolio 投资组合money-market 短期资本市场金融市场金融界capital-market 长期资本市场volatility 波动diversification 多元化多样化经营多样化option 期权call option 看涨期权购买选择权put option 看跌期权merger 并购arbitrage 套利Securities and Exchange Commission 〈美〉证券交易委员会安全与交换佣金, SEC (简称), 美国管理营业和公共销售安全的部门dollar standard 美元本位制bad debt 坏帐fiscal stimulus 财政刺激a store of value 保值transaction currency 结算货币forward exchange 期货交易intervention currency 干预货币Treasury bond 财政部公债current-account 经常项目pickup in rice 物价上涨Federal Reserve 美联储inflation 通货膨胀deflation 通货紧缩tighter credit 紧缩信贷monetary policy 货币政策foreigh exchange 外汇spot transaction 即期交易现货交易forward transaction 远期交易option forward transaction 择期交易swap transaction 调期交易互惠信贷交易quote 报价settlment and delivery 交割buying rate 买入价selling rate 卖出价selling rate卖价\卖出汇价\销售率\卖出价spread 差幅contract 合同at par 平价,按票面价格premium 升水discount 贴水direct quoation method 直接报价法indirect quoation method 间接报价法dividend 股息domestic currency 本币、本国货币floating rate 浮动利率parent company 母公司、总公司credit swap 互惠贷款venture capital 风险资本book value 帐面价值physical capital 实际资本IPO(initial public offering) 新股首发;首次公开发行welfare capitalism 福利资本主义collective market cap 市场资本总值golbal corporation 跨国公司transnational status 跨国优势transfer price 转让价格、内部调拨价格consolidation 兼并leverage 杠杆file for bankruptcy 申请破产bailout 救助take over 收购接收接管buy out 购买(某人的)产权或全部货物falter 摇摇欲坠on the hook 被套牢陷入圈套shore up confidence 提振市场信心stave off 挡开, 避开,liquidate assets 资产清算at fire sale prices 超低价sell-off 证券的跌价job machine 就业市场外贸常见英文缩略词CFR(cost and freight)成本加运费价D/P(document against payment)付款交单C.O (certificate of origin)一般原产地证CTN/CTNS(carton/cartons)纸箱DL/DLS(dollar/dollars)美元PKG(package)一包,一捆,一扎,一件等G.W.(gross weight)毛重C/D (customs declaration)报关单W (with)具有FAC(facsimile)传真EXP(export)出口MIN (minimum)最小的,最低限度M/V(merchant vessel)商船MT或M/T(metric ton)公吨INT(international)国际的INV (invoice)发票REF (reference)参考、查价STL.(style)式样、款式、类型RMB(renminbi)人民币PR或PRC(price) 价格S/C(sales contract)销售确认书B/L (bill of lading)提单CIF (cost,insurance&freight)成本、保险加运费价T/T(telegraphic transfer)电汇D/A (document against acceptance)承兑交单G.S.P.(generalized system of preferences)普惠制PCE/PCS(piece/pieces)只、个、支等DOZ/DZ(dozen)一打WT(weight)重量N.W.(net weight)净重EA(each)每个,各w/o(without)没有IMP(import)进口MAX (maximum)最大的、最大限度的M 或MED (medium)中等,中级的S.S(steamship)船运DOC (document)文件、单据P/L (packing list)装箱单、明细表PCT (percent)百分比EMS (express mail special)特快传递T或LTX或TX(telex)电传S/M (shipping marks)装船标记PUR (purchase)购买、购货L/C (letter of credit)信用证FOB (free on board)离岸价外贸术语解释交货条件交货delivery轮船steamship(缩写S.S)装运、装船shipment租船charter (the chartered ship)交货时间 time of delivery定程租船voyage charter;装运期限time of shipment定期租船time charter托运人(一般指出口商)shipper,consignor收货人consignee班轮regular shipping liner驳船lighter舱位shipping space油轮tanker报关clearance of goods陆运收据cargo receipt提货to take delivery of goods空运提单airway bill正本提单original B\L选择港(任意港)optional port选港费optional charges选港费由买方负担 optional charges to be borne by the Buyers 或 optional charges for Buyers' account一月份装船 shipment during January 或 January shipment一月底装船 shipment not later than Jan.31st.或shipment on or before Jan.31st.一/二月份装船 shipment during Jan./Feb.或 Jan./Feb. shipment 在......(时间)分两批装船 shipment during....in two lots 在......(时间)平均分两批装船 shipment during....in two equal lots分三个月装运 in three monthly shipments分三个月,每月平均装运 in three equal monthly shipments立即装运 immediate shipments即期装运 prompt shipments收到信用证后30天内装运 shipments within 30 days after receipt of L/C允许分批装船 partial shipment not allowed partial shipment not permitted partial shipment not unacceptable外贸价格术语价格术语trade term (price term)运费freight单价 price码头费wharfage。

自考国际商务英语