Cost15EChapter01_Solutions 成本会计课后习题答案

成本会计课后习题答案

成本会计课后习题答案成本会计是管理会计的一个重要分支,它主要关注企业在生产经营过程中产生的各种成本,并通过适当的方法进行核算和控制。

对于学习成本会计的同学来说,进行课后习题的练习是巩固知识、提高能力的重要途径。

下面是一些成本会计课后习题的答案,希望对大家有所帮助。

1. 问题:某公司在某一期间的生产成本为10,000元,销售成本为8,000元,期末库存为2,000元,计算该期间的期初库存。

答案:期初库存 = 期末库存 + 生产成本 - 销售成本= 2,000 + 10,000 - 8,000= 4,000元2. 问题:某公司在某一期间的生产成本为15,000元,销售成本为12,000元,期初库存为3,000元,计算该期间的期末库存。

答案:期末库存 = 期初库存 + 生产成本 - 销售成本= 3,000 + 15,000 - 12,000= 6,000元3. 问题:某公司在某一期间的直接材料成本为6,000元,直接人工成本为4,000元,制造费用为2,000元,计算该期间的制造成本。

答案:制造成本 = 直接材料成本 + 直接人工成本 + 制造费用= 6,000 + 4,000 + 2,000= 12,000元4. 问题:某公司在某一期间的制造成本为10,000元,期初库存为2,000元,期末库存为3,000元,计算该期间的销售成本。

答案:销售成本 = 制造成本 + 期初库存 - 期末库存= 10,000 + 2,000 - 3,000= 9,000元5. 问题:某公司在某一期间的销售成本为8,000元,期初库存为2,000元,期末库存为4,000元,计算该期间的制造成本。

答案:制造成本 = 销售成本 + 期末库存 - 期初库存= 8,000 + 4,000 - 2,000= 10,000元以上是一些常见的成本会计课后习题,通过计算,可以对成本会计的核算方法和概念有更深入的理解。

在实际工作中,成本会计的应用非常广泛,可以帮助企业合理控制成本,提高经营效益。

成本会计 课后练习第一章(答案)

第一章 概 论1.实际成本是指按现行规章制度在成本计划和成本核算中应用的成本,一般可称为财务成本或实际应用成本。

2. 生产成本是企业为生产一定数量和种类的产品所发生的以货币表现的各种生产耗费。

生产成本是对象化的生产费用。

3. 制造成本是指产品在制造过程中所发生的各项产品成本。

在我国现行会计制度中,其成本项目主要包括直接材料、直接人工和制造费用。

4. 直接成本是指与某一特定产品之间具有直接联系的成本。

它是为某一特定产品所消耗,因而可以直接计入该产品成本。

5. 间接成本是指与某一特定产品没有直接联系的成本。

它是为几种产品所消耗,不能直接计入,需要按适当的标准分配计入各种产品的成本。

6. 生产费用是企业在一定时期所发生各种生产耗费的总和,是计算产品成本的基础。

7. 成本预测是在认真分析企业现有经济技术条件、市场状况及其发展趋势的基础上,根据与成本有关的各种数据,采用一定的专门方法,对企业未来的成本水平及其变化趋势所进行的科学测算。

8. 成本决策是根据成本预测提供的数据和其他有关资料,制订出优化成本的各种备选方案,运用决策理论和方法,对各个备选方案进行比较分析,从中选择最优方案确定目标成本的过程。

9. 成本核算是指运用各种专门的成本计算方法,按照规定的成本项目,通过费用的归集和分配,计算出各种产品的总成本和单位成本,并进行相应的账务处理。

1.× 2.√ 3. × 4.× 5. √ 6.√ 7.√ 8.√ 9.× 10.√ 11.√ 12.× 13.√ 14.√ 15.× 16.× 17. × 18.×19.× 20.×名词解释判断问题1. D 2.C 3.D 4.D 5.B 6.B 7.C 8.C 9.C 10.C 1.B D E 2.A D E F 3. A C E F 4.C D E F1. 简述成本的概念。

成本会计课后习题答案

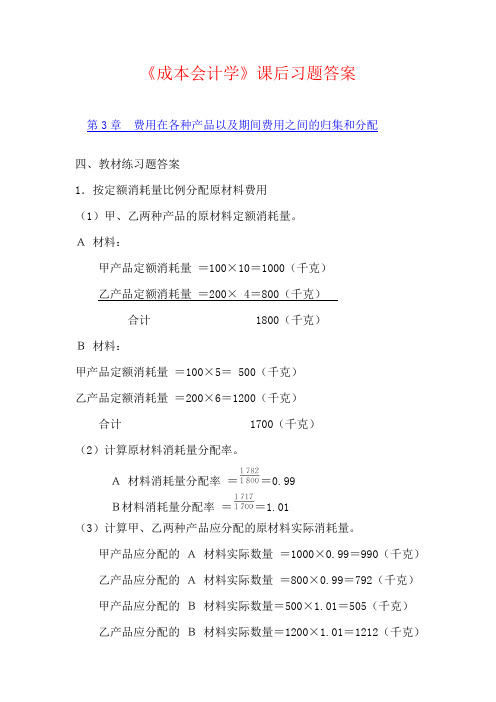

《成本会计学》课后习题答案第3章费用在各种产品以及期间费用之间的归集和分配四、教材练习题答案1.按定额消耗量比例分配原材料费用(1)甲、乙两种产品的原材料定额消耗量。

A材料:甲产品定额消耗量=100×10=1000(千克)乙产品定额消耗量=200× 4=800(千克)合计1800(千克)B材料:甲产品定额消耗量=100×5= 500(千克)乙产品定额消耗量=200×6=1200(千克)合计 1700(千克)(2)计算原材料消耗量分配率。

A材料消耗量分配率==0.99B材料消耗量分配率==1.01(3)计算甲、乙两种产品应分配的原材料实际消耗量。

甲产品应分配的A材料实际数量=1000×0.99=990(千克)乙产品应分配的A材料实际数量=800×0.99=792(千克)甲产品应分配的B材料实际数量=500×1.01=505(千克)乙产品应分配的B材料实际数量=1200×1.01=1212(千克)(4)计算甲、乙两种产品应分配的原材料计划价格费用。

甲产品应分配的A材料计划价格费用=990×2=1980(元)甲产品应分配的B材料计划价格费用=505×3=1515(元)合计3495(元)乙产品应分配的A材料计划价格费用= 792×2=1584(元)乙产品应分配的B材料计划价格费用=1212×3=3636(元)合计5220(元)(5)计算甲、乙两种产品应负担的原材料成本差异。

甲产品应负担的原材料成本差异=3495×(-2%)=-69.9(元)乙产品应负担的原材料成本差异=5220×(-2%)=-104.4(元)(6)计算甲、乙两种产品的实际原材料费用。

甲产品实际原材料费用=3495-69.9=3425.1(元)乙产品实际原材料费用=5220-104.4=5115.6(元)(7)根据以上计算结果可编制原材料费用分配表(见表3—12)。

《成本会计》四版答案

《成本会计》习题参考答案一、客观题答案第一章、总论一、单项选择1. A2. D3. B4. C 5.A二、多项选择1. ABD2. CE3. BCD4. ACE 5.CDE三、判断题1.V 2。

X 3。

V 4。

V 5。

X第二章生产费用的归集与分配一、单项选择1.D 2。

B 3。

B 4。

D 5。

C 6。

C 7。

B 8。

A 9。

A 10。

D二、多项选择1.AD 2。

ADE 3。

BCDE 4。

ABCE 5。

ACDE 6。

AE 7。

AB 8。

BCD 三、判断题1.X 2。

V 3。

X 4。

V 5。

V 6。

V 7。

V 8。

V 9。

X 10。

X 第三章产品成本计算方法概述一、单选题:1 D2 B3 B4 C5 A二、多选题:1 ACD 2 BC 3 ADE 4 AC 5 AB三、判断题:1× 2√ 3√ 4√ 5× 6√ 7 X第四章产品成本计算的品种法一、单选:1.A 2.A 3.B 4.A 5.D二、多选:1.BD 2.AE 3.ABC 4.ABE 5.ADE三、判断:×××√√第五章产品成本计算的分批法一、单选题:1 A2 D3 D4 A5 C6 A7 D 8B 9D二、多选题:1CDE 2CE 3ABCDE 4ABD 5ABD 6AB 7ACDE三、判断题:1√ 2× 3× 4 V 5√ 6√ 7√ 8×第六章产品成本计算的分步法一、单选题:1 D2 C3 C4 D5 C6 B7 B8 C9 B二、多选题:1 ABD2 ABCDE3 ACDE4 ADE5 ABCD6 AD7 BCDE8 CDE三、判断题:1√ 2√ 3√ 4× 5√ 6×7√8√9× 10√11√12×第七章产品成本计算的辅助方法一、单选题:1 B2 C3 D4 C二、多选题:1 AB2 ABCDE 3ACDE 4 CDE 5BCD三、判断题:1√ 2√ 3√ 4√ 5×第八章成本报表和成本分析一、单选题:1.B 2。

成本会计课后习题答案,成本会计课后习题答案

成本会计课后习题答案,成本会计课后习题答案一、名词解释1.工资总额是企业在一定时期内支付给全体职工的劳动报酬总额。

2.交互分配法是一种“亲兄弟、明算账,算账后,再对外”的分配方法,即所归集的辅助生产费用先在辅助生产车间之间进行交互分配,计算出交互分配后的辅助生产费用再在辅助生产车间以外的受益对象之间进行分配。

3.直接分配法是一种“团结一致,共同对外”的分配方法,即所归集的辅助生产费用只对辅助生产车间以外的受益对象之间进行分配。

4.不可修复废品是指在技术上无法修复,或修复成本过大,在经济上不合算而放弃修复的废品。

5.废品损失是指在产品生产过程中因出现废品而发生的无价值的耗费。

6.品种法是以产品的品种作为成本计算对象,归集生产费用,计算产品成本的方法。

7.分批法是以产品批别作为成本计算对象,归集生产费用,计算产品成本的方法。

8.分步法是以产品的生产步骤作为成本计算对象,归集生产费用,计算产品成本的方法。

9.产品成本计算对象是指企业为了计算产品成本而确定的归集和分配生产费用的各个对象,即生产费用的承担者。

10.逐步结转分步法,又称计列半成品成本分步法。

它是按照产品的生产步骤逐步计算并结转半成品成本,直到最后一个步骤算出完工产品成本的分步法。

11.平行结转分步法,又称不计列半成品成本分步法。

它是各步骤不计算半成品成本,而只归集各个步骤本身所发生的费用和计算各步骤应计入完工产品成本的份额,将各步骤应计入完工产品成本的份额平行加以汇总,计算出完工产品成本的一种方法。

12.脱离定额差异是指生产过程中各项生产费用的实际支出脱离现行定额或预算的数额。

13.定额变动差异是指因修订消耗定额或生产耗费的计划价格而产生的新旧定额之间的差额。

14.联产品是指使用同种原材料,经过同一加工过程而同时生产出来的具有同等地位的两种或两种以上的主要产品。

15.副产品是指在同一生产过程中,使用同种原料,在生产主要产品的同时附带生产出来的非主要产品。

成本会计习题答案-完整版

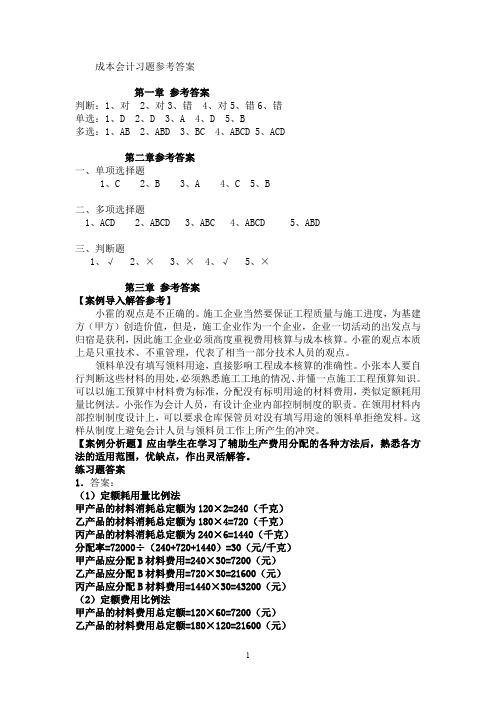

成本会计习题参考答案第一章参考答案判断:1、对 2、对3、错 4、对5、错6、错单选:1、D 2、D 3、A 4、D 5、B多选:1、AB 2、ABD 3、BC 4、ABCD 5、ACD第二章参考答案一、单项选择题1、C2、B3、A4、C5、B二、多项选择题1、ACD2、ABCD3、ABC4、ABCD5、ABD三、判断题1、√2、×3、×4、√5、×第三章参考答案【案例导入解答参考】小霍的观点是不正确的。

施工企业当然要保证工程质量与施工进度,为基建方(甲方)创造价值,但是,施工企业作为一个企业,企业一切活动的出发点与归宿是获利,因此施工企业必须高度重视费用核算与成本核算。

小霍的观点本质上是只重技术、不重管理,代表了相当一部分技术人员的观点。

领料单没有填写领料用途,直接影响工程成本核算的准确性。

小张本人要自行判断这些材料的用处,必须熟悉施工工地的情况、并懂一点施工工程预算知识。

可以以施工预算中材料费为标准,分配没有标明用途的材料费用,类似定额耗用量比例法。

小张作为会计人员,有设计企业内部控制制度的职责。

在领用材料内部控制制度设计上,可以要求仓库保管员对没有填写用途的领料单拒绝发料。

这样从制度上避免会计人员与领料员工作上所产生的冲突。

【案例分析题】应由学生在学习了辅助生产费用分配的各种方法后,熟悉各方法的适用范围,优缺点,作出灵活解答。

练习题答案1.答案:(1)定额耗用量比例法甲产品的材料消耗总定额为120×2=240(千克)乙产品的材料消耗总定额为180×4=720(千克)丙产品的材料消耗总定额为240×6=1440(千克)分配率=72000÷(240+720+1440)=30(元/千克)甲产品应分配B材料费用=240×30=7200(元)乙产品应分配B材料费用=720×30=21600(元)丙产品应分配B材料费用=1440×30=43200(元)(2)定额费用比例法甲产品的材料费用总定额=120×60=7200(元)乙产品的材料费用总定额=180×120=21600(元)丙产品的材料费用总定额=240×180=43200(元)分配率=72000÷(7200+21600+43200)=1甲产品应分配B材料费用=7200×1=7200(元)乙产品应分配B材料费用=21600×1=21600(元)丙产品应分配B材料费用=43200×1=43200(元)2.答案:分配率=20000÷(18000+23000+9000)=0.4(元/小时)甲产品应分配电费=18000×0.4=7200(元)乙产品应分配电费=23000×0.4=9200(元)丙产品应分配电费=9000×0.4=3600(元)借:生产成本——甲产品 7200——乙产品 9200——丙产品 3600制造费用 2200管理费用 2800贷:银行存款 250003.答案:A产品年度计划产量的定额工时:50 000×2.2=110 000(工时)B产品年度计划产量的定额工时:30 000×2.5= 75 000(工时)制造费用年度计划分配率=2 220 000÷(110 000+75 000)=12(元/工时)本月A产品应分配制造费用=9 000×12=108 000(元)本月B产品应分配制造费用=6 000×12= 72 000(元)借:生产成本——A产品 108 000——B产品 72 000贷:制造费用 180 000(本月实际发生的制造费用与按计划分配率分配费用之间的差额:183 918-180 000=3 918(元)对于本月形成的差异,暂不处理。

《成本会计》习题集及参考答案(完整版)

《成本会计》习题集第一章总论一、单项选择题1.成本会计是会计的一个分支,是一种专业会计,其对象是()。

A.企业B.成本C.资金D.会计主体2.成本会计最基本的职能是()。

A.成本预测B.成本决策C.成本核算D.成本考核3.成本会计的环节,是指成本会计应做的几个方面的工作,其基础是()。

A.成本控制B.成本核算C.成本分析D.成本考核4.成本会计的一般对象可以概括为()。

A.各行业企业生产经营业务的成本B.各行业企业有关的经营管理费用C.各行业企业生产经营业务的成本和有关的经营管理费用D.各行业企业生产经营业务的成本、有关的经营管理费用和各项专项成本5.实际工作中的产品成本是指()。

A.产品的生产成本B.产品生产的变动成本C.产品所耗费的全部成本D.生产中耗费的用货币额表现的生产资料价值6.产品成本是指()。

A.企业为生产一定种类、一定数量的产品所支出的各种生产费用的总和B.企业在一定时期内发生的,用货币额表现的生产耗费C.企业在生产过程已经耗费的、用货币额表现的生产资料的价值D.企业为生产某种、类、批产品所支出的一种特有的费用7.按产品的理论成本,不应计入产品成本的是()。

A.生产管理人员工资B.废品损失C.生产用动力D.设备维修费用8.所谓理论成本,就是按照马克思的价值学说计算的成本,它主要包括()。

A.已耗费的生产资料转移的价值B.劳动者为自己劳动所创造的价值C.劳动者为社会劳动所创造的价值D.已耗费的生产资料转移的价值和劳动者为自己劳动所创造的价值9.正确计算产品成本,应该做好的基础工作是()。

A.各种费用的分配B.正确划分各种费用界限C.建立和健全原始记录工作D.确定成本计算对象10.集中核算方式和分散核算方式是指()的分工方式。

A.企业内部各级成本会计机构B.企业内部成本会计职能C.企业内部成本会计对象D.企业内部成本会计任务二、多项选择题1.产品的理论成本是由产品生产所耗费的若干价值构成,包括()。

成本会计(第三版)各章节课后全部习题参考答案

《成本会计》(第三版)(揭志锋)各章节课后全部习题参考答案第一章一、单项选择题1.【解析】:B成本会计是以成本为对象,以提供成本信息为主的一个会计分支。

2.【解析】:C成本核算是成本会计最基本的内容,它反映成本的生成过程,是成本计划的实施结果,是对成本决策目标是否实现的检验。

3.【解析】:D成本会计是以成本为对象,是对各行业企业生产经营业务成本、有关经营管理费用和各项专项成本进行归集与分配。

4.【解析】:D在马克思主义政治经济学中,商品价值(W)包括生产中耗费的不变资本价值(C)、可变资本价值(V)与剩余价值(M),C+V即为成本。

5.【解析】:C产品成本是指可以计入存货价值的成本,包括按特定目的分配给一项产品的成本总和。

在会计中,按照配比原则划分产品成本和期间成本,为此要求收入和为取得收入而支出的费用要在同一会计期间确认,即产品的生产成本。

选项B,季节性停工损失属于生产产品的必需支出,应当计入成本中;选项C,应在实际发生时直接计入当期损益。

二、多项选择题1.【解析】:CD在马克思主义政治经济学中,商品价值(W)包括生产中耗费的不变资本价值(C)、可变资本价值(V)与剩余价值(M),C+V即为成本。

2.【解析】:ABC管理费用、财务费用与销售费用与产品生产无直接关系,无法具体划分到产品成本中。

3.【解析】:CD材料费用按照用途若为直接材料则直接计入产品“生产成本”,若为生产车间多种产品生产所需则须先计入“制造费用”科目。

4.【解析】:BDA和C计入管理费用。

构成产品实体的原材料费用可直接或者经过分配直接计入“生产成本——基本生产成本”科目借方,而车间生产人员工资通过“制造费用”贷方转入“生产成本——基本生产成本”科目借方。

5.【解析】:ABCD销售费用主要包括与产品销售有关的营销成本、配送成本与客户服务成本等。

三、判断题1.×2.×3.×4.√5.√第二章一、单项选择题1.【解析】:B分配率=2240×13/(1.6×300+200×1.8)=34.67(元/千克)。

成本会计课后习题参考答案

帐务处理——

①结转废品的生产成本

借:废品损失——A产品

2990

贷:基本生产成本——A产品 2990

②回收残料入库

借:原材料

500

贷:废品损失——A产品 500

③将废品损失2990-500=2490元转入合格产品成本

借:基本生产成本——A产品 2490

贷:废品损失——A产品

帐务处理——

借:辅助生产成本——修理车间 750

辅助生产成本——运输车间 950

贷:辅助生产成本——修理车间 950

辅助生产成本——运输车间 750

交互分配后的实际费用:

修理车间:19000+750-950=18800 运输车间:20000+950-750=20200

(2)对外分配

计算分析题17——约当产量比例法

(1)在产品完工程度 第一道工序:160×50%÷400=20% 第二道工序:(160+240×50%)÷400=70%

管理费用

2610

贷:辅助生产成本——修理车间 4510

辅助生产成本——运输车间 7920

计算分析题8——交互分配法

(1)对内交互分配

修理车间的劳务单位成本=19000÷20000=0.95 运输车间的劳务单位成本=20000÷40000=0.5

运输车间应分摊的修理费用=1000×0.95=950 修理车间应分摊的运输费用=1500×0.5=750

31573

管理部门应分摊的修理费

=3000× 0.9895=2968.5

管理部门应分摊的运输费

《成本会计》习题集答案21世纪经济管理专业应用型精品教材word精品文档23页

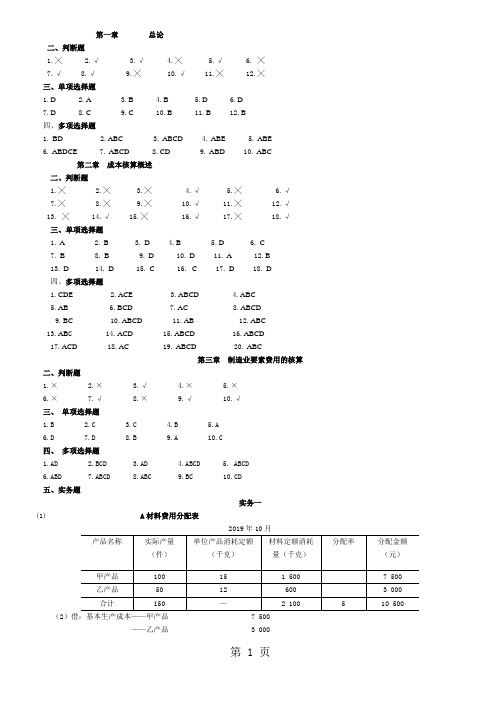

第一章总论二、判断题1.╳2.√3.√4.╳5.√6. ╳7.√ 8.√ 9.╳ 10.√ 11.╳ 12.╳三、单项选择题1.D2.A3.B4.B5.D6.D7.D 8.C 9.C 10.B 11.B 12.B四、多项选择题1. BD2.ABC3. ABCD4. ABE5. ABE6. ABDCE7. ABCD8.CD9. ABD 10. ABC第二章成本核算概述二、判断题1.╳2.╳3.╳4.√5.╳6.√7.╳ 8.╳ 9.╳ 10.√ 11.╳ 12.√13. ╳ 14.√ 15.╳ 16.√ 17.╳ 18.√三、单项选择题1. A2. B3. D4.B5.D6. C7. B 8. B 9. D 10. D 11. A 12.B13. D 14. D 15. C 16. C 17. D 18. D四、多项选择题1.CDE2.ACE3.ABCD4.ABC5.AB6.BCD7.AC8.ABCD9.BC 10.ABCD 11.AB 12.ABC13.AB C 14.ACD 15.ABCD 16.ABCD17.ACD 18.AC 19. ABCD 20. ABC第三章制造业要素费用的核算二、判断题1.×2.×3.√4.×5.×6.×7.√8.×9.√ 10.√三、单项选择题1.B2.C3.C4.B5.A6.D7.D8.B9.A 10.C四、多项选择题1.AD2.BCD3.AD4.ABCD5. ABCD6.ABD7.ABCD8.ABC9.BC 10.CD五、实务题实务一(1) A材料费用分配表2019年10月(2)借:基本生产成本——甲产品 7 500——乙产品 3 000贷:原材料——A材料 10 500实务二(1)燃料费用分配率=32 800÷(60×10+80×13)=20101产品应负担的燃料费用=60×10×20=12 000(元)102产品应负担的燃料费用=80×13×20=20 800(元)(2)借:基本生产成本——101产品 12 000——102产品 20 800辅助生产成本 4 500管理费用 5 700制造费用 3 800贷:燃料 46 800实务三(1)工资费用分配表2019年7月单位:元会计分录:借:基本生产成本——甲产品 7 350——乙产品 12 250——丙产品 8 400制造费用 4 200管理费用 6 000营业费用 8 400贷:应付职工薪酬 46 600 (2)借:基本生产成本——甲产品 1 029——乙产品 1 715——丙产品 1 176制造费用 588管理费用 840营业费用 1 176贷:应付职工薪酬——应付福利费 6 524实务四(1)年初预付财产保险费,借:待摊费用 12 000贷:银行存款 12 000 1~12月摊销财产保险费,借:制造费用 600辅助生产成本 100管理费用 300贷:待摊费用 1 000 (2)7~11月预提大修理支出,借:制造费用 300 12月实际支付大修理费用,借:预提费用 15 000制造费用 2 600贷:银行存款 17 600第四章辅助生产费用和制造费用的核算二、判断题1.×2.×3.×4.×5.√6.√7.×8.√9.× 10.×三、单项选择题1.A2.C3.B4.C5.D6.B7.C8.B9.D 10.A四、多项选择题1.CD2.AD3.ABC4.BD5.CD6.BC7.ABC8.ABCD9.ABC 10.CD五、实务题实务一辅助生产费用分配表2019年12月(1)账务处理:借:基本生产成本——甲产品 14 225制造费用 79 150管理费用 14 625贷:辅助生产成本——供电 18 000——供暖 90 000(2)辅助生产费用分配表2019年12月账务处理:交互分配:借:辅助生产成本——供电 10 000——供暖 720贷:辅助生产成本——供电 720——供暖 10 000对外分配:借:基本生产成本——甲产品 21 559制造费用 72 628管理费用 13 813贷:辅助生产成本——供电 27 280——供暖 80 720(3)假设供电车间的电费为x元/度,供暖车间的供暖费为y元/小时。

成本会计配套习题集参考答案

第二部分练习题参考答案第一章总论一、填空题1.C+V理论2.生产资料自己资金3.开支围法规制度4.制造产品当期损益5.补偿综合质量6.产品生产成本期间费用7.生产经营业务成本期间费用8.财务成本管理成本9.成本核算10.集中工作分散工作二、名词解释1.成本的经济实质:生产经营过程中所耗费的生产资料转移的价值和劳动者为自己劳动所创造的价值的货币表现,也就是企业在生产经营中所耗费的资金的总和。

2.产品的制造成本:是指为制造产品而发生的各种费用总和,包括原材料、生产工人工资和全部制造费用。

3.产品的生产成本:为生产一定种类、一定数量产品而发生的各种生产费用支出的总和。

4.期间费用:包括销售费用、管理费用和财务费用,这些费用与产品生产没有直接联系,而是按发生的期间归集,直接计入当期损益,故统称期间费用。

5.集中工作方式:是指企业的成本会计工作,主要由厂部成本会计机构集中进行;车间等其他单位的成本会计机构或人员只负责原始记录和原始凭证的填制,并对它们进行初步的审核、整理和汇总,为厂部成本会计机构进一步工作提供基础资料。

6.分散工作方式:是指成本会计工作中的计划、控制、核算和分析分散由车间等其他单位的成本会计机构或人员分别进行;成本考核工作由上一级成本会计机构对下一级成本会计机构逐级进行。

厂部会计机构除对全厂成本进行综合的计划、控制、分析和考核以及汇总核算外,还应负责对各下级成本会计机构或人员进行业务上的指导和监督。

三、判断题1.√2.×3.√4.×5.×6.√7.√8.√9.×10.×四、单项选择题1.D 2.D 3.A 4.D 5.D6.C 7.C 8.B 9.B 10.B五、多项选择题1.ACD 2.ABC 3.ABCD 4.ABCD 5.ABCD6.ABD 7.ABD 8.ABD六、简答题1.答:实际工作中的成本开支围与理论成本容的差别,主要是将劳动者为社会劳动所创造的价值,如财产保险费等,以及一些不形成产品价值的损失性支出,如工业企业的废品损失、季节性和修理期间的停工损失等也计入了成本。

成本会计习题参考答案

第一章总论一、简答题(要点)1.成本概念中最具典型意义的是产品成本。

企业的生产过程既是产品的制造过程,也是物化劳动和活劳动的消耗过程。

从理论上说,产品成本是指企业为生产一定种类和数量的产品而发生的生产耗费。

所以成本的经济内涵可以概括为:成本是生产经营过程中所耗费的生产资料转移的价值和劳动者为自己劳动所创造价值的货币表现,是企业在生产过程中所耗费的资金的综合。

2.成本会计的形成和发展表现为以下几个方面:(1)成本会计起源于英国,最初只是反映生产过程的各种耗费,形成了记录型成本会计。

(2)随着泰罗制的产生,成本会计的职能不断扩大,不仅能够计算成本,还能够控制和分析成本。

(3)在传统成本会计阶段,会计核算、会计控制、会计理论等方面都取得了辉煌的成就,成本会计的应用范围也从工业企业扩大到各种行业。

(4)在现代成本会计阶段,计算机等各种科学技术成就在成本会计中得到了广泛应用,形成了新型的着重管理的经营型成本会计。

(5)随着当前企业内部环境和外部环境的变化,成本会计必须适应新的制造环境,不断创新成本管理理论与方法。

3.会计人员职业道德主要有:爱岗敬业、诚实守信、廉洁自律、坚持准则、客观公正、精通业务、保守秘密。

4.成本的作用主要有:(1)成本可以反映企业的综合管理水平;(2)成本是管理当局确定产品价格的重要依据;(3)成本可以为企业的管理当局进行成本预测、决策提供资料;(4)成本是生产耗费的补偿尺度;(5)成本可以为编制财务报表提供所必需的成本资料。

5.成本会计的任务主要有:(1)正确计算产品成本,及时提供成本信息;(2)加强成本预测,优化成本决策;(3)制定目标成本,强化成本控制;(4)建立成本责任制度,严格成本业绩考核。

6.成本会计职能包括成本预测、成本决策、成本计划、成本控制、成本核算、成本分析和成本考核。

成本会计的各项职能之间是相互联系、相辅相成的,它们贯穿于企业生产经营的全过程,构成现代成本管理的整体框架。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

CHAPTER 1THE MANAGER AND MANAGEMENT ACCOUNTINGSee the front matter of this Solutions Manual for suggestions regarding your choices of assignment material for each chapter.1-1 Management accounting measures, analyzes, and reports financial and nonfinancial information that helps managers make decisions to fulfill the goals of an organization. It focuses on internal reporting and is not restricted by generally accepted accounting principles (GAAP).Financial accounting focuses on reporting to external parties such as investors, government agencies, and banks. It measures and records business transactions and provides financial statements that are based on generally accepted accounting principles (GAAP).Other differences include (1) management accounting emphasizes the future (not the past), and (2) management accounting influences the behavior of managers and other employees (rather than primarily reporting economic events).1-2Financial accounting is constrained by generally accepted accounting principles. Management accounting is not restricted to these principles. The result is that•management accounting allows managers to charge interest on owners’ capital to helpjudge a division’s performance, even though such a charge is not allowed under GAAP,•management accounting can include assets or liabilities (such as “brand names”developed internally) not recognized under GAAP, and•management accounting can use asset or liability measurement rules (such as presentvalues or resale prices) not permitted under GAAP.1-3 Management accountants can help to formulate strategy by providing information about the sources of competitive advantage—for example, the cost, productivity, or efficiency advantage of their company relative to competitors or the premium prices a company can charge relative to the costs of adding features that make its products or services distinctive.1-4The business functions in the value chain are•Research and development—generating and experimenting with ideas related to new products, services, or processes.•Design of products and processes—the detailed planning, engineering, and testing of products and processes.•Production—procuring, transporting, storing, and assembling resources to produce a product or deliver a service.•Marketing—promoting and selling products or services to customers or prospective customers.•Distribution—processing orders and shipping products or services to customers.•Customer service—providing after-sales service to customers.1-5Supply chain describes the flow of goods, services, and information from the initial sources of materials and services to the delivery of products to consumers, regardless of whether those activities occur in the same organization or in other organizations.Cost management is most effective when it integrates and coordinates activities across all companies in the supply chain as well as across each business function in an individual company’s value chain. Attempts are made to restructure all cost areas to be more cost-effective. 1-6 “Management accounting deals only with costs.” This statement is misleading at best, and wrong at worst. Management accounting measures, analyzes, and reports financial and nonfinancial information that helps managers define the organization’s goals and make decisions to fulfill those goals. Management accounting also analyzes revenues from products and customers in order to assess product and customer profitability. Therefore, while management accounting does use cost information, it is only a part of t he organization’s information recorded and analyzed by management accountants.1-7Management accountants can help improve quality and achieve timely product deliveries by recording and reporting an organization’s current quality and timeliness levels and by analyzing and evaluating the costs and benefits—both financial and nonfinancial—of new quality initiatives, such as TQM, relieving bottleneck constraints, or providing faster customer service.1-8The five-step decision-making process is (1) identify the problem and uncertainties; (2) obtain information; (3) make predictions about the future; (4) make decisions by choosing among alternatives; and (5) implement the decision, evaluate performance, and learn.1-9Planning decisions focus on selecting organization goals and strategies, predicting results under various alternative ways of achieving those goals, deciding how to attain the desired goals, and communicating the goals and how to attain them to the entire organization.Control decisions focus on taking actions that implement the planning decisions, deciding how to evaluate performance, and providing feedback and learning to help future decision making.1-10The three guidelines for management accountants are as follows:1.Employ a cost-benefit approach.2.Recognize technical and behavioral considerations.3.Apply the notion of “different costs for different purposes.”1-11 Agree. A successful management accountant requires general business skills (such as understanding the strategy of an organization) and people skills (such as motivating other team members) as well as technical skills (such as computer knowledge, calculating costs of products, and supporting planning and control decisions).1-12 The new controller could reply in one or more of the following ways:(a) Demonstrate to the plant manager how he or she could make better decisions if theplant controller was viewed as a resource rather than a deadweight. In a related way,the plant controller could show how the plant manager’s time and resources could besaved by viewing the new plant controller as a team member.(b) Demonstrate to the plant manager a good knowledge of the technical aspects of theplant. This approach may involve doing background reading. It certainly will involvespending much time on the plant floor speaking to plant personnel.(c) Show the plant manager examples of the new plant controller’s past successes inworking with line managers in other plants. Examples could include•assistance in preparing the budget,•assistance in analyzing problem situations and evaluating financial and nonfinancial aspects of different alternatives, and•assistance in submitting capital budget requests.(d) Seek assistance from the corporate controller to highlight to the plant manager theimportance of many tasks undertaken by the new plant controller. This approach is alast resort but may be necessary in some cases.1-13The controller is the chief management accounting executive. The corporate controller reports to the chief financial officer, a staff function. Companies also have business unit controllers who support business unit managers or regional controllers who support regional managers in major geographic regions.1-14 The Institute of Management Accountants (IMA) sets standards of ethical conduct for management accountants in the following four areas:•Competence•Confidentiality•Integrity•Credibility1-15 Steps to take when established written policies provide insufficient guidance are as follows:(a) Discuss the problem with the immediate superior (except when it appears that thesuperior is involved).(b)Clarify relevant ethical issues by confidential discussion with an IMA EthicsCounselor or other impartial advisor.(c)Consult your own attorney as to legal obligations and rights concerning the ethicalconflicts.1-16 (15 min.) Value chain and classification of costs, computer company.Cost Item Value Chain Business Functiona.b.c.d.e.f.g.h. ProductionDistributionDesign of products and processes Research and development Customer service or marketing Design of products and processes (or research and development) MarketingProduction1-17 (15 min.)Value chain and classification of costs, pharmaceutical company.Cost Item Value Chain Business Functiona.b.c.d.e.f.g.h. MarketingDesign of products and processes Customer serviceResearch and development MarketingProductionMarketingDistribution1-18 (15 min.) Value chain and classification of costs, fast-food restaurant.Cost Item Value Chain Business Functiona.b.c.d.e.f.g.h. ProductionDistributionMarketingMarketingMarketingProductionDesign of products and processes (or research and development) Customer service1-19 (10 min.)Key success factors.Change in Operations/Management Accounting Key Success Factora.b.c.d.e. InnovationCost and efficiency and quality TimeTime and cost and efficiency Cost and efficiency1-20 (10 min.)Key success factors.Change in Operations/Management Accounting Key Success Factora.b.c.d.e. Time and cost and efficiency Time and cost and efficiency Quality and cost and efficiency Innovation and qualityCost and efficiency1-21(10–15 min.) Planning and control decisions.Action Decisiona.b.c.d.e. Planning Control Control Planning Planning1-22(10–15 min.) Planning and control decisions.Action Decisiona.b.c.d.e. Planning Control Planning Planning Control1-23 (15 min.) Five-step decision-making process, manufacturing.Action Step in Decision-Making Processa.b.c.d.e.f.g. Obtain information.Make predictions about the future.Identify the problem and uncertainties.Implement the decision, evaluate performance, and learn. Make predictions about the future.Make decisions by choosing among alternatives. Obtain information.1-24(15 min.) Five-step decision-making process, service firm.Action Step in Decision-Making Processa.b.c.d.e.f. Make decisions by choosing among alternatives.Identify the problem and uncertainties.Obtain information and/or make predictions about the future. Obtain information and/or make predictions about the future. Make predictions about the future.Obtain information.1-25 (10–15 min.) Professional ethics and reporting division performance.1. Mendez’s ethical responsibilities are well summarized in the IMA’s “Standards of Ethical Conduct for Management Accountants”(Exhibit 1-7 of text). Areas of ethical responsibility include the following:•Competence•Confidentiality•Integrity•CredibilityThe ethical standards related to Mendez’s current dilemma are integrity, competence, and credibility. Using the integrity standard, Mendez should carry out duties ethically and communicate unfavorable as well as favorable information and professional judgments or opinions. Competence demands that Mendez perform her professional duties in accordance with relevant laws, regulations, and technical standards and provide decision support information that is accurate. Credibility requires that Mendez report information fairly and objectively and disclose deficiencies in internal controls in conformance with organizational policy and/or applicable law. Mendez should refuse to book the $200,000 of sales until the goods are shipped. Both financial accounting and management accounting principles maintain that sales are not complete until the title is transferred to the buyer.2. Mendez should refuse to follow Dalton’s orders. If Dalton persists, the incident should be reported to the corporate controller. Support for line management should be wholehearted, but it should not require unethical conduct.1-26 (10–15 min.) Professional ethics and reporting division performance.1. Wilson’s ethical responsibilities are well summarized in the IMA’s “Standards of Ethical Conduct for Management Accountants” (Exhibit1-7 of text). Areas of ethical responsibility include the following:•Competence•Confidentiality•Integrity•CredibilityThe ethical standards related to Wilson’s current dilemma are integrity, competence, and credibility. Using the integrity standard, Wilson should carry out duties ethically and communicate unfavorable as well as favorable information and professional judgments or opinions. Competence demands that Wilson perform his professional duties in accordance with relevant laws, regulations, and technical standards and provide decision support information that is accurate. Credibility requires that Wilson report information fairly and objectively and disclose deficiencies in internal controls in conformance with organizational policy and/or applicable law. Wilson should refuse to include the $150,000 of defective inventory. Both financial accounting and management accounting principles maintain that once inventory is determined to be unfit for sale, it must be written off. It may be just a timing issue, but reporting the $150,000 of inventory as an asset would be misleading to the users of the company’s financial statements.2. Wilson should refuse to follow Leonard’s orders. If Leonard persists, the incident should be reported to the corporate controller of Garman Enterprises. Support for line management should be wholehearted, but it should not require unethical conduct.1-27(15 min.) Planning and control decisions, Internet company.1. Planning decisionsa. Decision to raise monthly subscription feec. Decision to upgrade content of online services (later decision to inform subscribersand upgrade online services is an implementation part of control)e. Decision to decrease monthly subscription fee starting in November.Control decisionsb.Decision to inform existing subscribers about the rate of increase—an implementationpart of control decisionsd. Dismissal of VP of Marketing—performance evaluation and feedback aspect ofcontrol decisions2. Other planning decisions that may be made at : decision to raise or lower advertising fees; decision to charge a fee from on-line retailers when customers click-through from to the retailers’ websites.Other control decisions that may be made at : evaluating how customers like the new format for the weather information, working with an outside vendor to redesign the website, and evaluating whether the waiting time for customers to access the website has been reduced.1-28 (20 min.) Strategic decisions and management accounting.1. The strategies the companies are following in each case are:a.b.c.d. Cost leadership or low price strategy Product differentiation strategy Cost leadership or low price strategy Product differentiation strategy2. Examples of information the management accountant can provide for each strategic decision follow.a.b.c.d. Cost to manufacture and sell the cell phoneProductivity, efficiency, and cost advantages relative to competitionPrices of competitive cell phonesSensitivity of target customers to price and qualityThe production capacity of Pedro Phones and its competitorsHow the market for cell phones with standard features is growingCost to develop, produce, and sell new softwarePremium price that customers would be willing to pay due to product uniqueness Price of basic softwarePrice of closest competitive softwareCash needed to develop, produce, and sell new softwareCost of producing the “store-brand” lip glossProductivity, efficiency, and cost advantages relative to competitionPrices of competitive productsSensitivity of target customers to price and qualityThe production capacity of Celine Cosmetics and its competitorsHow the market for lip gloss is growingCost to produce and sell new line of gourmet bolognaPremium price that customers would be willing to pay due to product uniqueness Price of basic meat productPrice of closest competitive productCash available to develop, produce, and sell special line of gourmet bologna1-29 (20 min.) Strategic decisions and management accounting.1. The strategies the companies are following in each case area.b.c.d. Cost leadership strategy Product differentiation strategy Cost leadership strategy Product differentiation strategy2. Examples of information the management accountant can provide for each strategic decision follow.a.b.c.d. Cost related to training the new cooksProductivity and efficiency advantages relative to competition Sensitivity of target customers to price and qualityCost of delivery servicePremium price that customers would be willing to pay for the service Price of closest competitive productCost to develop new software to check in customersEfficiency and cost advantages relative to competitionSensitivity of target customers to change in serviceCost to hire horticultural specialistPremium price that customers would be willing to pay for expert advice Price of closest competitive product1-30(15 min.) Management accounting guidelines.1.Cost-benefit approach2.Behavioral and technical considerations3.Different costs for different purposes4.Cost-benefit approach5.Behavioral and technical considerations6.Cost-benefit approach7.Behavioral and technical considerations8.Different costs for different purposes9.Behavioral and technical considerations1-31(15 min.) Management accounting guidelines.1.Cost-benefit approach2.Behavioral and technical considerations3.Different costs for different purposes4.Cost-benefit approach or behavioral and technical considerations, for example, howemployees will react to the new technology5.Behavioral and technical considerations6.Cost-benefit approach7.Behavioral and technical considerations or different costs for different purposes. The goal ofdetermining the loss in future business because of poor quality beyond the cost of scrap and waste reported in financial statements is to influence behavior toward improving quality by recognizing its high cost.1-32 (15 min.)Role of controller, role of chief financial officer.1.Activity Controller CFO Managing the company’s long-term investments XPresenting financial statements to the board of directors XStrategic review of different lines of businesses XBudgeting funds for a plant upgrade XManaging accounts receivable XNegotiating fees with auditors XAssessing profitability of various products XEvaluating the costs and benefits of a new product design X2. As CFO, Jimenez will be interacting much more with the senior management of the company, the board of directors, auditors, and the external financial community. Any experience he can get with these aspects will help him in his new role as CFO. George Jimenez can be better positioned for his new role as CFO by participating in strategy discussions with senior management, by preparing the external investor communications and press releases under the guidance of the current CFO, by attending courses that focus on the interaction and negotiations between the various business functions and outside parties such as auditors and, either formally or on the job, getting training in issues related to investments and corporate finance.1-33 (30 min.) Pharmaceutical company, budgeting, ethics.1.The overarching principles of the IMA Statement of Ethical Professional Practice are Ho nesty, Fairness, Objectivity and Responsibility. The statement’s corresponding “Standards for Ethical Conduct…” require management accountants to•Perform professional duties in accordance with relevant laws, regulations, and technical standards.•Refrain from engaging in any conduct that would prejudice carrying out duties ethically.•Communicate information fairly and objectively.•Disclose all relevant information that could reasonably be expected to influence an intended user’s understanding of the report s, analyses, or recommendations.The idea of capitalizing some of the company’s R&D expenditures is a direct violation of the IMA’s ethical standards above. This transaction would not be “in accordance with relevant laws, regulations, and technical standards.” GAAP requires research and development costs to be expensed as incurred. Even if Jackson believes his transaction is justifiable, it violates the profession’s technical standards and would be unethical.The other “year-end” actions occur in many org anizations and fall into the “gray” to “acceptable” area. Much depends on the circumstances surrounding each one, however, such as the following:a.Stop all research and development efforts on the drug Vyacon until after year-end.This change would delay the drug going to market by at least six months. It is alsopossible that in the meantime a BrisCor competitor could make it to market with asimilar drug. While this solution may solve the budget shortfall in this year, it couldresult in a significant loss of future profits for BrisCor in the long run, especially if acompetitor is able to obtain a patent on a similar drug before BrisCor.b.Sell off rights to the drug, Martek. The company had not planned on doing thisbecause, under current market conditions, it would get less than fair value. It would,however, result in a onetime gain that could offset the budget shortfall. Of course, allfuture profits from Martek would be lost.Again, this solution may solve thecompany’s short-term budget crisis, but could result in the loss of future profits forBrisCor in the long run.2.While it is not uncommon for companies to sacrifice long-term profits for short-term gains, it may not be in the best interest of the company’s shareholders. In the case of BrisCor, the CFO is primarily concerned with “maximizing shareholder wealth” in the immediate future (third quarter only) but not in the long term. Because this executive’s incentive pay and even employment may be based on his ability to meet short-term targets, he may not be acting in the best interest of the shareholders in the long run.Jackson definitely faces an ethical dilemma. It is not unethical on Jackson’s part to want to please his new boss, nor is it unethical that Jackson wants to make a good impression on his first days at his new job; however, Jackson must still act within the ethical standards required byhis profession. Taking illegal or unethical action by capitalizing R&D to satisfy the demands of his new supervisor, Ronald Meece, is unacceptable. Although not strictly unethical, I would recommend that Jackson not agree to slow down the R&D efforts on Vyacon or sell off the rights to Martek. Each of these appears to sacrifice the overall economic interests of BrisCor for short-run gain. Jackson should argue against doing this but not resign if Meece insists that these actions be taken. If, however, Meece asks Jackson to capitalize R&D, he should raise this issue with the chair of the audit committee after informing Meece that he is doing so. If the CFO still insists on Jackson capitalizing R&D, he should resign rather than engage in unethical behavior. 1-34 (30–40 min.) Professional ethics and end-of-year actions.1. The possible motivations for the snack foods division wanting to take end-of-year actions include:(a) Management incentives. Daniel Foods may have a division bonus scheme based onone-year reported division earnings. Efforts to front-end revenue into the current yearor transfer costs into the next year can increase this bonus.(b) Promotion opportunities and job security. Top management of Daniel Foods likelywill view those division managers who deliver high reported earnings growth rates asbeing the best prospects for promotion. Division managers who deliver “unwelcomesurprises” ma y be viewed as less capable.(c) Retain division autonomy. If top management of Daniel Foods adopts a “managementby exception” approach, divisions that report sharp reductions in their earningsgrowth rates may attract a sizable increase in top management supervision.2. The “Standards of Ethical Conduct . . . ” require management accountants to•Perform professional duties in accordance with relevant laws, regulations, and technical standards.•Refrain from engaging in any conduct that would prejudice carrying out duties ethically.•Communicate information fairly and objectively.Several of the “end-of-year actions” clearly are in conflict with these requirements and should be viewed as unacceptable by Butler.(b) The fiscal year-end should be closed on mid night of December 31. “Extending” theclose falsely reports next year’s sales as this year’s sales.(c) Altering shipping dates is falsification of the accounting reports.(f) Advertisements run in December should be charged to the current year. Theadvertising agency is facilitating falsification of the accounting records.The other “end-of-year actions” occur in many organizations and fall into the “gray” to “acceptable” area. However, much depends on the circumstances surrounding each one, such as the following:(a) If the independent contractor does not do maintenance work in December, there is notransaction regarding maintenance to record. The responsibility for ensuring thatpackaging equipment is well maintained is that of the plant manager. The divisioncontroller probably can do little more than observe the absence of a Decembermaintenance charge.(d) In many organizations, sales are heavily concentrated in the final weeks of the fiscalyear-end. If the double bonus is approved by the division marketing manager, thedivision controller can do little more than observe the extra bonus paid in December.(e) If TV spots are reduced in December, the advertising cost in December will bereduced. There is no record falsification here.(g)Much depends on the means of “persuading” carriers to accept the merchandise. Forexample, if an under-the-table payment is involved, or if carriers are pressured toaccept merchandise, it is clearly unethical. If, however, the carrier receives no extraconsideration and willingly agrees to accept the assignment because it sees potentialsales opportunities in December, the transaction appears ethical.Each of the (a), (d), (e), and (g) “end-of-year actions” may well disadvantage Daniel Foods in the long run. For example, lack of routine maintenance may lead to subsequent equipment failure. The divisional controller is well advised to raise such issues in meetings with the division president. However, if Daniel Foods has a rigid set of line/staff distinctions, the division president is the one who bears primary responsibility for justifying division actions to senior corporate officers.3. If Butler believes that Ray wants her to engage in unethical behavior, she should first directly raise her concerns with Ray. If Ray is unwilling to change his request, Butler should discuss her concerns with the Corporate Controller of Daniel Foods. She could also initiate a confidential discussion with an IMA Ethics Counselor, other impartial adviser, or her own attorney. Butler also may well ask for a transfer from the snack foods division if she perceives Ray is unwilling to listen to pressure brought by the Corporate Controller, CFO, or even President of Daniel Foods. In the extreme, she may want to resign if the corporate culture of Daniel Foods is to reward division managers who take “end-of-year actions” that Butler views as unethical and possibly illegal. It was precisely actions along the lines of (b), (c), and (f) that caused Betty Vinson, an accountant at WorldCom, to be indicted f or falsifying WorldCom’s books and misleading investors.1-35 (30 min.)Professional ethics and end-of-year actions.1. The possible motivations for Controller Rhett Gable to modify the division’s year-end earnings are(i) Job security and promotion. The company’s CFO will likely reward him for meeting thecompany’s performance expectations. Alternately, the Gable may be penalized, perhaps even by losing his job if the performance expectations are not met.(ii) Management incentives. Gable’s bonus may be based on the division’s ability to meet certain profit targets. If the House and Home division has already met its profit target for the year, the Controller may personally benefit if new printing equipment is sold off and replaced with the discarded equipment that no longer meets current safety standards, or if operating income is manipulated by questionable revenue and/or expense recognition.。