Dynamics of Demand of index insurance

保险监管英语

保险监管英语Insurance RegulationThe financial industry has undergone significant transformations in recent years, with increased complexity and interconnectedness posing new challenges for regulators. One of the critical areas within this landscape is the insurance sector, which plays a pivotal role in the overall financial stability and risk management of modern economies. Effective insurance regulation has become increasingly crucial in ensuring the solvency and resilience of insurance companies, protecting consumers, and maintaining the integrity of the financial system.The primary objective of insurance regulation is to safeguard policyholders and ensure the stability and soundness of the insurance industry. This is achieved through a multifaceted approach that encompasses various aspects of insurance operations, such as capital requirements, risk management practices, consumer protection measures, and market conduct oversight. Regulators strive to strike a delicate balance between fostering a competitive and innovative insurance market while upholding robust prudential standards and consumer safeguards.One of the fundamental aspects of insurance regulation is the establishment of capital adequacy requirements. Insurance companies are required to maintain a certain level of capital reserves to ensure their ability to meet their contractual obligations to policyholders. These capital requirements are typically based on the nature and complexity of the risks underwritten by the insurer, taking into account factors such as the types of insurance products offered, the diversification of the insurer's portfolio, and the overall risk profile of the company. Regulators closely monitor the capital position of insurance companies and intervene when necessary to address any potential solvency concerns.Risk management practices are another critical area of insurance regulation. Insurers are expected to have robust risk management frameworks in place to identify, measure, and mitigate the various risks they face, including underwriting risks, investment risks, and operational risks. Regulators may require insurers to adopt specific risk management techniques, such as stress testing and scenario analysis, to assess their resilience to adverse events and ensure the appropriate management of their risk exposures.Consumer protection is a fundamental pillar of insurance regulation. Regulators strive to ensure that insurance products are designed and marketed in a transparent and fair manner, with clear disclosure ofrelevant information to consumers. This includes requirements for insurers to provide clear and comprehensive policy documentation, adhere to fair pricing practices, and handle claims and complaints in a timely and efficient manner. Regulators may also establish guidelines for the distribution and marketing of insurance products, aiming to prevent misselling and protect the interests of policyholders.In addition to prudential regulations, insurance regulators also oversee the market conduct of insurers. This includes monitoring compliance with rules and regulations governing sales practices, conflict of interest management, and the treatment of customers. Regulators may impose restrictions or sanctions on insurers that engage in unfair or deceptive practices, with the goal of maintaining the integrity and public trust in the insurance industry.The regulatory landscape for the insurance sector has become increasingly complex, with the emergence of new risks, such as cyber threats, climate-related risks, and the growing influence of technology-driven innovations. Regulators must keep pace with these evolving challenges and adapt their supervisory frameworks accordingly. This often involves collaboration with other financial regulators, both domestically and internationally, to ensure a coordinated and comprehensive approach to insurance regulation.Moreover, the insurance industry itself is subject to ongoing transformation, with the advent of new business models, distribution channels, and product innovations. Regulators must strike a balance between fostering innovation and maintaining appropriate safeguards, ensuring that the regulatory framework remains responsive to the changing dynamics of the insurance market.In conclusion, effective insurance regulation is crucial for the stability and resilience of the financial system. By establishing robust prudential standards, consumer protection measures, and market conduct oversight, regulators play a vital role in safeguarding policyholders, promoting industry soundness, and maintaining public trust in the insurance sector. As the insurance landscape continues to evolve, regulators must remain vigilant, adaptable, and collaborative to address the emerging challenges and maintain a well-regulated and resilient insurance industry.。

保险经济学术语英文

保险经济学术语英文Insurance Economics TerminologyActuarial Science: The study of the mathematical and statistical analysis of risk, particularly in the insurance and finance industries.Adverse Selection: The tendency of individuals with a higher risk profile to be more likely to purchase insurance, leading to an imbalance in the insurance pool.Annuity: A series of periodic payments made to an individual for a fixed period or for life, often used as a retirement income product.Arbitrage: The practice of taking advantage of a price difference between two or more markets, with the goal of making a profit.Asset-Liability Management (ALM): The process of managing the balance between an organization's assets and liabilities to ensure that it can meet its financial obligations.Basis Risk: The risk that the value of a hedging instrument does not perfectly offset the value of the underlying exposure, leading to potential losses.Behavioral Economics: The study of how psychological, cognitive, and emotional factors influence economic decision-making.Catastrophe Bond (Cat Bond): A type of insurance-linked security that transfers the risk of catastrophic events, such as natural disasters, to the capital markets.Coinsurance: A cost-sharing arrangement in insurance where the policyholder and the insurer both pay a portion of the covered expenses.Deductible: The amount that the policyholder must pay out-of-pocket before the insurance company begins to cover the remaining costs.Diversification: The practice of investing in a variety of assets to reduce the overall risk of a portfolio.Endowment: A sum of money or other financial assets that are donated to an institution, such as a university or charity, to provide a permanent source of income.Equity-Linked Insurance: A type of life insurance product that combines traditional life insurance with investment in equity markets.Hedging: The practice of taking an offsetting positionin a related asset to mitigate the risk of adverse price movements.Indemnity: The compensation paid by an insurance company to a policyholder for a covered loss or damage.Insurable Interest: The requirement that an individual or entity must have a legitimate financial interest in the subject of an insurance policy in order to purchase it.Moral Hazard: The tendency of individuals to engage in riskier behavior when they are protected from the consequences of their actions, such as through insurance coverage.Pension: A regular payment made to a person, typically by an employer or the government, upon retirement or after a period of service.Reinsurance: The practice of insurers transferring portions of their risk portfolios to other insurancecompanies to reduce the likelihood of having to pay a large claim.Risk Aversion: The tendency of individuals to prefer a guaranteed, lower-return option over a higher-risk, higher-return option.Securitization: The process of converting illiquid assets, such as loans or mortgages, into tradablesecurities that can be sold to investors.保险经济学术语精算学: 研究风险的数学和统计分析,尤其是在保险和金融行业。

供应与需求概念 英语解释

供应与需求概念英语解释The Concept of Supply and Demand: An English ExplanationThe fundamental economic principles of supply and demand are essential for understanding the dynamics of any market. These principles govern the relationship between the availability of a good or service and the desire of consumers to acquire it. In this essay, we will explore the concept of supply and demand, its underlying factors, and the implications it has on the functioning of markets.Supply refers to the quantity of a good or service that producers are willing and able to sell at various prices during a given period. The supply of a product is influenced by several factors, including the cost of production, the number of producers in the market, the availability of resources, and the level of technology. As the price of a product increases, the quantity supplied also rises, as producers are incentivized to increase production to capitalize on the higher prices. Conversely, as the price decreases, the quantity supplied declines, as producers find it less profitable to maintain the same level of production.On the other hand, demand refers to the quantity of a good orservice that consumers are willing and able to purchase at various prices during a given period. The demand for a product is influenced by factors such as the price of the product, the income of consumers, the prices of related goods, and consumer preferences. As the price of a product decreases, the quantity demanded increases, as consumers are more inclined to purchase the product. Conversely, as the price increases, the quantity demanded decreases, as consumers become less willing to pay the higher price.The interaction between supply and demand is the foundation of the market mechanism. The equilibrium price of a product is determined by the point where the quantity supplied and the quantity demanded are equal. At this point, the market is in a state of equilibrium, and there is no tendency for the price to change. If the price is above the equilibrium level, there will be a surplus of the product, as the quantity supplied exceeds the quantity demanded. This will lead to downward pressure on the price, as producers compete to sell their excess inventory. Conversely, if the price is below the equilibrium level, there will be a shortage of the product, as the quantity demanded exceeds the quantity supplied. This will lead to upward pressure on the price, as consumers compete to acquire the limited supply.The concept of supply and demand also has important implications for the allocation of resources in an economy. In a market-basedeconomy, the prices of goods and services serve as signals to producers and consumers, guiding the allocation of resources to the most valued uses. Producers will allocate their resources to the production of goods and services that are in high demand and can be sold at profitable prices, while consumers will allocate their limited resources to the purchase of the goods and services that provide the greatest utility.Furthermore, the concept of supply and demand can be applied to various markets, including the labor market. In the labor market, the supply of labor is determined by the number of people willing and able to work, while the demand for labor is determined by the need for workers to produce goods and services. The equilibrium wage rate is determined by the interaction of the supply and demand for labor, and this wage rate serves as a signal to guide the allocation of labor resources in the economy.In conclusion, the concept of supply and demand is a fundamental principle of economics that governs the functioning of markets. It explains the relationship between the availability of a good or service and the desire of consumers to acquire it, and it has important implications for the allocation of resources in an economy. Understanding the principles of supply and demand is essential for anyone seeking to understand the dynamics of markets and the broader economic landscape.。

竞争性对抗与竞争动态概论

引导案例

破坏性创新:战胜竞争对手的法宝

举例: • 施乐受到了来自佳能的破坏性创新。 • 苹果的iPhone破坏了整个移动电话和 个人电脑市场,创造出了智能手机市 场。 • 随着iPad不断改进它的图像功能,游 戏平台硬件制造商和软件制造商开始 感受到了威胁。

OPENING CASE

DISRUPTIVE INNOVATION: WINNING RIVALRY BATTLES AGAINST COMPETITORS

• OPENING CASE

• 开篇案例及启示

OPENING CASE

P119

DISRUPTIVE INNOVATION: WINNING RIVALRY BATTLES AGAINST COMPETITORS • Clayton Christensen, a Harvard professor and author of The Innovator’s Dilemma, defines “disruptive innovation” as: • “an innovation that makes it so much simpler and so much more affordable to own and use a product that a whole new population of people can now have one. • 《创新的困境》的作者哈佛教授克莱顿· 克里斯坦

which can be subdivided into (segments)

I.e., Financial industry

Examples from text (p. 123)

Industry Financial Market Market Segment Product Segment

保险专业英语(单词+简单问题)(主要应对面试)

1.再保险reinsurance2.投保人applicant3.保险人insurer4.被保险人insured5.受益人beneficiary6.暂保单cover note7.保险单policy of insurance8.投保单proposal form9.保单certificate of insurance10.批单rider11.简易保单(保险凭证)the slip12.除外条款clause of exceptions13.免赔额条款deductible clause14.共保条款coinsurance clause15.责任条款duty clause16.代位求偿条款subrogation clause17.偿付能力insolvency18.监管regulate19.欺骗性的deceptive20.保费prepium21.投机speculate22.投保to propose23.保险利益insurable interest24.人寿保单life assurance policy25.债权人creditor26.债务人debtor27.定期保单time policy28.养老保险、年金保险annuities insurance29.交税延期tax-postpone30.巨灾catastrophe31.欺诈行为fraud32.养老基金pension fund33.保险责任coverage34.保险密度insurance density35.保险深度insurance penetration36.遗产heritage37.准备金reserves38.禁止反言estoppel39.弃权waiver40.解除合同dissolution of contract41.保单现金价值cash value42.不可抗辩条款incontestable clause43.年龄误告条款misstatement of age44.宽限期条款grace period provision45.复效条款reinstatement provision46.自杀条款suicide clause47.不丧失价值条款non-forfeiture values and options48.保单贷款条款policy loan clause49.自动垫缴保费条款automatic premium loan clause50.保险金给付任选条款settlement options51.定期寿险term life insurance52.终身寿险whole life insurance52.生存保险pure endownment insurance53.两全保险endowment insurance54.分红保险participating life insurance55.万能寿险universal life insurance56.投资连结保险unit-link life insurance57.健康保险health insurance58.疾病保险disease insurance59.医疗保险medical insurance60.失能收入损失保险disability income insurance61.长期护理保险long-term care insurance62.意外伤害保险accidental insurance63.等于equal to64.乘以multiply by65.除以divide66.加上plus67.减去minus68.人身保险personal insurance69.团体人身保险group personal insurance70.机动车辆保险automobile insurance71.家庭财产保险insurance of contents71.企业火灾保险fire insurance72.企业工程保险engineering insurance73.建筑工程保险construction insurance74.安装工程保险erection insurance75.货物运输保险cargo transportation insurance76.利润损失险loss of profit insurance77.1.what’s the definition of risk?risk means uncertainty about future loss or the ability to predict the occurrence or size of a loss.2.what’re the types of risks?pure risk and speculative risk1).pure risk means that the risk can only suffer loss and have no chance to gain benefit.2).speculative risk means that the risk is able to gain benefit while suffering loss.3.what are the ways of handing risks?1).risk avoidance2).risk dispersal3).loss control4).risk restraining5).risk retention6).risk transfer4.what’re the kinds of hazards?1).physical hazards2).adverse selection3).moral hazard4).psychological hazard5.what’re the differenes among risk,peril and hazard?1).a peril is a cause of a loss.2).a hazard is a condition that may creat or increase the chance of a loss due to a given peril.3).a risk is used to indicate a condition that there is a possibility of loss.6.what’s the definition of insurance?1).from the perspective of the legal,insurance is a kind of contract.2).from the perspective of the economy,insurance is a system of transfering risk.3).from the perspective of the society,insurance is a kind of behavior that helps each other.7.what’re the social functions of insurance?1).spreading out risks2).compensating for loss3).investment and providing for a better utilization of capital4).social management8.what are the characteristics of insurance?1).from the perspective of the legal,insurance is legal.2).from the perspective of the economy,insurance is commercial.3).from the perspective of the society,insurance is helpful.9.what are the differences between the commercialinsurance and the social insurance?1).the applicant who buy a commercial insurance is volunteer,but the social insurance is bought by a compulsive way.2).the premium of the commercial insurance is paid by the applicant only,but the premium of the social insurance is paid by the applicant,the company that the applicant work in and the government.10.what are the categories of insurance?1).life insurance2).health insurance3).accidental insurance4).properity insurance5).liability insurance6).credit insurance11.what’s the definition of reinsurance?reinsurance is an economical behavior caused by the insurer to transfering risk,because the insurer concerns the loss will have a bad effect on the stability of company.12.what’s the definition of deductive clause?insurance proceeds are payable only after theinsured has paid a certain amount of the loss.13. what’s the definition of coinsurance clause?coinsurance clause is used by judging if the sum of money compared with the insurance benefit is enough in property insurance,for example,there is an 80% coinsurance clause,if the sum of insurance has become 80% of the insurance benefit,the insurer will regard it as an enough sum proposal.14. what’s the definition of duty clause?the parties to an insurance contract are obligated to perform the duties imposed by the contract.15. what’s the definition of subrogation clause?if an insurance company pays a claim to an insured for liability or property damage caused by a third party,the insurer succeeds to the right of the insured to recover from a third party.16.what’s the definition of insurance contract?insurance contract is an agreement which stipulates rights and obligations of applicants and insurers. 17.what’s the definition of the principle of insurance interest?insurance interest clause means that the applicantand the insured must have interest of subject-matter insured.18.how to affirm the insurance interest in the property insurance?if a person has some rights of one thing,such as ownership,rights of possession,right to use,creditor’s rights and so on,the person has the insurance interest of the thing.19.what’re the significances of the principle of insurance interest ?1).to prevent the behavior of gamble2).to prevent moral risk3).to limit the highest sum of money that the insurer pays to the insured20.what’s the definition of the principle of utmost good faith?the principle of utmost good faith means that the two parties of the contract should told the other all important details which can affect the insurer whether to accept a insurance and to increase the premium ,and they can’t do any spurious behavior. 21.what’s the definition of the obligation of notification?the two parties of the contract should notify the other all important details in written form or by verbal way before signing the contract .22.what’s the applicant’s obligation of notification? 1).before signing the contract,the applicant should answer the insurer’s questions according to the facts 2).after signing the contract and in the period of validity,if the level of risk increases,the applicant should notify the insurer.3).if the subject-matter insured has been transferred or the details of contract has been changed,the applicant should notify the insurer.4).after the peril,the applicant should notify the condition of subjet-matter insured to the insurer in time.23.what’s the definition of pledge?pledge means that the applicant should guarantee whether to do something and whether something exits or not.24.what’re the definitions of waiver and estoppel? 1).waiver means that one party of the contract notifies or indicates that he will give up certain right.2).estoppel means that if one party of the contract has given up certain right ,he couldn’t ask for the right again.25.what’s the definition of the principle of loss compensation?the principle of loss compensation means that if the peril that the contract records happens,the insured may ask for compensation from the insurer according to the contract,but the insured couldn’t gain extra benefit. 26.what’s the definition of the principle of proximate cause?the principle of proximate cause means that if a cause which makes a peril happens is in the range of insurance obligation,the insurer should compensate for the loss of the insured.27.what’s the definition of incontestable clause? incontestable clause means that if a contract has taken effect for 2 years,the insurer couldn’t relieve the contract by the reason that the insured didn’t perform the obligation of notifying.28.what’s the definition of the misstatement of age?if the applicant notifies a wrong age when heproposed the insurance,his premium or compensation money would be adjusted according to the ture age. 29.what’s the definition of the grace period provision?this provision means that even the applicant doesn’t pay the prepium,the contract is still on effect in the grace period.30.what’s the definition of the reinstatement provision?this provision means that if a policy losses efficacy because the applicant doesn’t pay the preium in time, the applicant may apply for reinstatement during a certain period.31.what’s the definition of reinstatement?reinstatement means that all the rights and oblibations recorded in the policy are maintained,such as :insurance coverage,insurance deadline,and so on. 32.what’s the definition of suicide clause?suicide clause means that the insurer pays the insured compensation due to suicide only after the policy has been on effect for 2 years.33.what’s the definition of the non-forfeiture values and options?non-forfeiture values and options means that theapplicants have rights to choose different ways to use the cash value of the policy.34.what’s the definition of the policy loan clause?policy loan clause means that the applicant may pledge his life assurance policy to the insurer to apply for a loan.35.what’s the definition of the automatic premium loan clause?automatic premium loan clause means that if one applicant couldn’t pay his premium in time,the insurer could use the cash value of the policy to replace the premium.36.what’re the types of life insurance?1).term life insuranceterm life insurance is that only if the insured’s life is end,the insurer would pay insurance money,and its term is fixed.2).whole life insurancewhole life insurance is that only if the insured’s life is end,the insurer would pay insurance money,and it’s term is the insured’s whole life.3).pure endowment insurancepure endowment insurance is that only if the insured is alive during the ruled period,the insurer could pay insurance money.4).endowment insuranceendowment insurance is that regardless of the insured is alive or dead,the insurer would pay insurance money.5).participating life insuranceparticipating life insurance is that the insurance company will allot bonus which is from last accounting year to the clients in a certain proportion.6).universal life insuranceuniversal life insurance is that its method to pay prepium is flexible and its insurance money may be adjusted.7).unit-link life insuranceunit-link life insurance protects the insured and at the same time it possesses at least one investment count which owns some property.37.what’s the definition of the annuities insurance?annuities insurance is that only if the insured is alive the insurer would pay insurance money,and thetime of paying cycle is no more than one year.38.what’s the denifition of the health insurance?health insurance is that only if the insured is ill or suffers accidents the insurer wouly pay compensation.39.what’re the types of the health insurance?1).disease insurancedisease insurance is that only if the insured gets illness which is recorded on the contract the insurer pay the insurance money.2).medical insurancemedical insurance is that only if the insured is cured by the medical behaviors which are recorded on the policy the insurer would pay the insured medical fee. 3).disability income insurancedisability income insurance is that only if the insured is no able to work because of the illness or accidents which are recorded on the policy the insurer would pay the insurance money.4).long-term care insurance40.what’s the definition of the deductible excess? w hat’s its role in insurance company?1).the insurer only undertake the part which is morethan a certain sum of money,and the part which the insurer doesn’t compensate is the deductible excess. 2).the deductible excess plays an important role in insurance company,it helps company to save much unnecessary cost and reduce moral risk.41.what’s the definition of the accidental insurance?accidental insurance is that only if the insurer is dead or disabled due to the accidents recorded on the insurance contract the insurer would pay the compensation.42.。

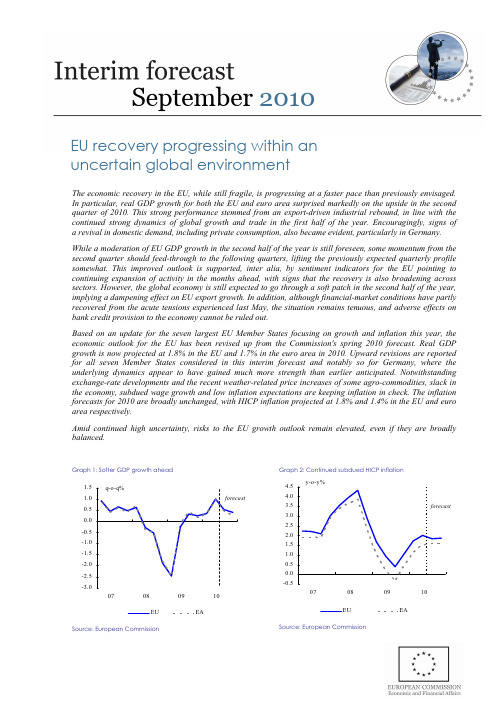

2010-09-13欧元区经济预测 英文版

[suggested new layout using the text of IF Sep 09]September 2010EU recovery progressing within an uncertain global environmentThe economic recovery in the EU, while still fragile, is progressing at a faster pace than previously envisaged. In particular, real GDP growth for both the EU and euro area surprised markedly on the upside in the second quarter of 2010. This strong performance stemmed from an export-driven industrial rebound, in line with the continued strong dynamics of global growth and trade in the first half of the year. Encouragingly, signs of a revival in domestic demand, including private consumption, also became evident, particularly in Germany. While a moderation of EU GDP growth in the second half of the year is still foreseen, some momentum from the second quarter should feed-through to the following quarters, lifting the previously expected quarterly profile somewhat. This improved outlook is supported, inter alia, by sentiment indicators for the EU pointing to continuing expansion of activity in the months ahead, with signs that the recovery is also broadening across sectors. However, the global economy is still expected to go through a soft patch in the second half of the year, implying a dampening effect on EU export growth. In addition, although financial-market conditions have partly recovered from the acute tensions experienced last May, the situation remains tenuous, and adverse effects on bank credit provision to the economy cannot be ruled out.Based on an update for the seven largest EU Member States focusing on growth and inflation this year, the economic outlook for the EU has been revised up from the Commission's spring 2010 forecast. Real GDP growth is now projected at 1.8% in the EU and 1.7% in the euro area in 2010. Upward revisions are reported for all seven Member States considered in this interim forecast and notably so for Germany, where the underlying dynamics appear to have gained much more strength than earlier anticipated. Notwithstanding exchange-rate developments and the recent weather-related price increases of some agro-commodities, slack in the economy, subdued wage growth and low inflation expectations are keeping inflation in check. The inflation forecasts for 2010 are broadly unchanged, with HICP inflation projected at 1.8% and 1.4% in the EU and euro area respectively.Amid continued high uncertainty, risks to the EU growth outlook remain elevated, even if they are broadly balanced.Graph 1: Softer GDP growth aheadSource: European CommissionGraph 2: Continued subdued HICP inflationSource: European Commission2Interim forecast September 2010Global recovery loosing momentumThe world economy recovered by more than expected in the first half of 2010, led by strong growth in emerging market economies, particularly in Asia. World trade also performed strongly, with trade in goods returning to pre-recession levels by mid-year. Despite some loss of momentum in the second quarter, annual growth in global trade (excl. EU) is now expected to average around 12% in 2010 in volume terms, up from about 10% in the spring forecast.Looking ahead, the global economy is set to moderate somewhat in the second half of 2010, although a 'double-dip' seems unlikely. This follows from the expected weaker support from inventory building going forward and the phasing out of stimulus measures. Leading indicators, such as the global Purchasing Managers' Index (PMI) for manufacturing, though remaining in expansion territory, have declined in recent months, suggesting that the global manufacturing cycle has peaked in the second quarter. Despite the expected soft patch, global GDP (excl. EU) is projected to grow by some 5% in 2010, up by ¼ pp. compared to the spring forecast.Graph 3: Softening global growth and trade-15-10-55100001020304050607080910113035404550556065World trade, CPB (ma3, LHS)Global PMI - manufacturing output (ma3, RHS)Source: CPB - Netherlands Bureau for Economic Policy Analysis, European CommissionThe global recovery is still expected to be uneven and is surrounded by major uncertainties. On the one hand, growth in emerging economies remainsrobust, supported by the rebound in global trade, commodity price developments and solid domestic demand. On the other hand, the recovery is still fragile in several advanced economies. While investment in equipment should continue to benefit with some lag from the increase in global demand, consumption remains constrained in these economies. Moreover, the resurfacing of global imbalances, high debt levels and lingering tensions in sovereign-debt markets are also weighing on the outlook.Financial markets affected by a retreat from riskOver the last few months, financial markets have partly recovered from the sovereign-debt crisis, though significant challenges remain in place. With concerns about the strength of the economic recovery increasing in some parts of the world, a retreat from risk has become a key determinant of financial-market developments.While sovereign-bond spreads in most European countries have narrowed somewhat since May 2010, they are still significantly above the levels seen at the beginning of the year. More recently, benchmark sovereign-bond yields have fallen to historic lows in the EU, with spreads vis-à-vis German bunds widening again in some Member States. Similarly, corporate-bond spreads have narrowed since May, but also remain substantially above their levels of early 2010. New bond issuance has resumed on the back of mostly better-than-expected corporate results. With concerns about sovereign debt receding, markets' attention has shifted from banks' solvency positions to banks' refinancing risk.Bank credit provision to the economy has come into focus over the past months. So far lending growth to households has remained very moderate in the euro area and the UK, whereas bank credit to non-financial corporations continued to shrink over the summer. The latest ECB survey provides evidence of renewed tightening of bank credit standards, at least for enterprises. The reported factors behind this are renewed constraints in banks' access to funding and liquidity management, owing to tensions in sovereign-debt markets. These developments suggest that support from the credit side to the economic recovery could materialise somewhat later than envisaged in the spring.3Interim forecast September 2010Improved prospects for the EU economyThe recovery of the EU economy gained ground in the second quarter of 2010. GDP growth picked up sharply, by 1.0% q-o-q in both regions, after growth of just 0.3% in the first quarter. This outcome was above the consensus estimate (which was 0.6% for the euro area) and the Commission's spring forecast (0.4%).While exports continued to support the recovery, expanding by a sizeable 4%, the second quarter also saw a rebalancing of growth towards domestic demand. Indeed, the contribution of private investment and consumption to GDP growth (0.6 pp. in the EU and euro area) exceeded the combined contributions of inventories and net exports (0.3 pp.). As expected in the spring, the second quarter figure also partly reflects temporary factors, such as a technical rebound in construction activity following the harsh winter.Graph 4: A rebalancing of EU growth across demandcomponents-2.5-2.0-1.5-1.0-0.50.00.51.01.507Q108Q109Q110Q1Inventories Net exportsDomestic demand (excl. inventories)GDP (q-o-q%)Source: European CommissionLooking ahead, GDP growth is set to moderate in the second half of the year. This stems from the expected softening in the global economy, along with the fading of the temporary factors that kick-started the recovery.Based on an update of the outlook for the seven largest Member States, GDP is now expected to expand by 0.5% in the EU and euro area in the third quarter, and by 0.4% and 0.3% respectively in the fourth. This represents a slight upward revisioncompared to the quarterly profile presented in the spring forecast, on account of some spill-over of the momentum from the second quarter.High-frequency indicators support the improved outlook for the EU economy. For instance, the Commission's Economic Sentiment Indicator (ESI) has recovered from the adverse impact of tensions in financial and sovereign-bond markets in May-June, to currently stand above its long-term average. Similarly, the composite PMI remains firmly in the zone that indicates expansion, despite a slight easing in August. As for sectoral patterns, the broad-based nature of the latest survey readings is also encouraging. It suggests that the expected spill-over from the export-led industrial rebound to the rest of the economy is gradually materialising.Graph 5: Brighter prospects for EU equipment investment-12-10-8-6-4-20240001020304050607080910-7-6-5-4-3-2-1012Equipment investment (LHS)Industrial confidence (ma3, RHS)*ma3=3 months moving averageSource: European CommissionFurther support to the view that the recovery is broadening can be found in data that are closely correlated with developments in private investment and consumption. For example, the degree of capacity utilisation is approaching a level (just above 80) which traditionally implies expanding equipment investment in the euro area. At the same time, the profit situation of firms has improved. On the consumption side, while disposable income remains weak, the decline in the household saving rate from its peak during the crisis, subdued inflation and stabilising labour-market conditions bode well for consumer spending in the near term.4Interim forecast September 2010Graph 6: Private consumption expanding again in the euroarea-0,9-0,6-0,30,00,30,60,91,21,51,80001020304050607080910121314151617Private consumption (LHS)Source: European CommissionGrowth forecast for the EU economy revised upFor 2010 as a whole, GDP growth is now forecast at 1.8% in the EU and 1.7% in the euro area. This represents a sizeable upward revision compared to the spring forecast (1.0% for the EU and 0.9% for the euro area), reflecting a higher carry-over from the first half of the year and the elements discussed above. However, this aggregate picture masks uneven developments across Member States, confirming the Commission's expectation of a multi-speed recovery within the EU. This is not surprising given differences in the scale of adjustment challenges and ongoing rebalancing within the EU and euro area.Inflation in the EU to remain moderateConsumer price inflation increased moderately in the first half of 2010. This upward trend reflected an increase in global commodity prices, as well as the impact of upward base effects from the food and energy components.Euro-area headline HICP inflation rose to 1.5% in the second quarter of 2010, in line with the spring forecast. Core inflation (i.e. HICP inflation excluding energy and unprocessed food) appears to have bottomed out at 0.8% in the same period, decreasing from 1.5% one year earlier. In the EU, headline inflation was 2.0% in the second quarter, 0.3 pp. higher than in the spring forecast, largely due to a surprise in the UK.Weak labour-market conditions kept wage growth subdued in the euro area in the first quarter of 2010. At the same time, annual unit-labour-cost growth was negative, reflecting improving productivity and only modest growth in compensation per employee.Looking ahead, the headline inflation rate for 2010 is expected to hold at 1.8% in the EU, while in the euro area it is marginally revised down to 1.4% (-0.1 pp. compared to the spring forecast). However, within the euro area, projected developments are somewhat divergent, with France being the only Member State with an upward revision, following increases in administered prices. Outside the euro area, inflation has been revised up, in particular in the UK on account of a stronger-than-expected pass-through to the headline inflation rate from exchange-rate and commodity-price developments, as well as due to changes in indirect taxation.Graph 7: EU underlying inflation remains subdued1.01.21.41.61.82.02.22.42.62.83.000010203040506070809106.57.07.58.08.59.09.510.0Core inflation (HICP excl. energy and unproc. food, LHS)Unemployment rate (RHS)y-o-y%% of labour force (inverted scale)Source: European CommissionDespite revisions at the Member State level, the underlying inflation trends identified in the spring forecast remain valid. The remaining slack in the economy and weak labour market conditions are expected to keep core inflation at historically low levels, while the headline rate may prove to be volatile in the second half of 2010, driven both by changes in commodity prices related to the outlook in advanced economies and base effects.Interim forecast September 2010Brighter growth outlook bodes well for the labour market and public financesIn keeping with the usual pattern – whereby labour- market developments follow those of GDP with a time lag of half a year or more – the labour-market situation has started to stabilise in recent months. The first quarter of 2010 saw job shedding ease to 0.2% q-o-q in the EU (from some 0.8% a year earlier) and come to an end in the euro area. Similarly, the unemployment rate has held steady since the spring, at 9.6% in the EU and 10.0% in the euro area.As for the outlook, survey indicators of firms' employment expectations point to moderate job creation going forward, as does the PMI employment index which crossed the 50-mark in May. Taken together with the strong upward revision to economic growth in 2010, it seems that the labour market may hold up somewhat better this year than expected at the time of the spring forecast. Nonetheless, conditions are set to remain weak, reflecting, inter alia, the partial unwinding of support measures and ongoing structural adjustment across sectors and firms. At Member State level, a continuation of the divergence observed to date in labour-market performance is also expected. Turning to public finances, additional consolidation measures taken since the publication of the spring forecast and the better-than-expected growth outlook will help improve the 2010 budgetary position in the EU and euro area.A full assessment of prospects for public finances and the labour market will be carried out in the Commission's upcoming autumn forecast.High uncertainty, but broadly balanced risks Uncertainty at the current juncture is high, with non-negligible risks to the EU growth outlook clearly evident. While these risks go in both directions, they appear broadly balanced for 2010. On the upside, the impetus from the export-led industrial rebound to private consumption could prove stronger than assumed in the baseline, as was the case in the first half of the year. The broad-based improvement in sentiment indicators of late bodes well for a similar outcome in the period ahead. Moreover, in so far as the labour market continues to surprise on the upside – as it has done for some time now – the feed-through to private consumption could be even more pronounced. The materialisation of these risks would add to the self-sustainability of the EU recovery. Likewise, the spill-over to be expected from the pick-up in activity in Germany to other Member States may materialise to a greater extent than expected at present, further strengthening the recovery.On the downside, softening global demand in the second part of 2010 – beyond that allowed for in the baseline – poses a risk for EU export growth. Second, the still relatively fragile financial-market situation remains a concern. While markets have recovered somewhat from the recent crisis, renewed turbulence in sovereign-debt markets could trigger further increases in funding costs and additional credit tightening, with adverse consequences for confidence and economic activity. A third downside risk relates to the fiscal consolidation underway in a number of Member States. This should help dissipate market concerns about fiscal sustainability, but may weigh more on domestic demand in the short term than currently envisaged. Regarding the inflation outlook, risks also appear to be broadly balanced for 2010. While strengthening activity and a weaker than previously assumed euro represent upside risks, weak labour-market conditions, as well as low inflation expectations, suggest that these pressures are likely to be offset in the near term.5Interim forecast September 2010Growth and inflation prospects in the seven largest Member States1. Germany – strong recovery becoming more broad-basedThe German economy has rebounded vigorously from the crisis, posting five consecutive quarters of robust growth since the second quarter of 2009. Despite the harsh weather conditions around the turn of 2009-10, the underlying growth momentum remained largely intact and turned out considerably stronger than projected in the Commission's spring forecast. A brisk rebound in world trade and expansionary monetary and fiscal policy were the main driving forces behind this turnaround. The initially largely export-driven recovery is increasingly becoming more broad-based with domestic demand contributing more strongly to growth in the second quarter than net exports.In the second quarter of 2010 real GDP growth culminated at over 2%, the highest quarterly rate since reunification. A particularly sharp increase in exports and a surge in construction activity – reflecting a rebound after the impact of severe winter weather and the kicking-in of public infrastructure projects as part of the fiscal stimulus – contributed to this exceptionally brisk pace. The weaker economic outlook for the US and a possible moderation of growth in Asia are likely to imply a softening of the export dynamics in the second half of the year. However, domestic demand components are set to gather further strength and to sustain a relatively lively recovery. The robust labour market which, despite the scope of the downturn, was barely affected should boost household confidence. Thus, private consumption will continue to be buoyed by falling unemployment, stronger wage growth as working hours are being extended again, still moderate inflation and fiscal relief measures. Rising capacity utilisation, low interest rates and the strong financial position of the corporate sector should support private investment activity, which will additionally be boosted by the expiry of favourable depreciation rules at the end of the year. Hence, despite some slowdown in the quarterly growth rates, real GDP is projected to grow by close to 3½% in 2010. Despite higher energy prices and a depreciation of the euro, HICP inflation has remained contained so far and is expected to accelerate only moderately in the coming months. Annual average HICP inflation is projected at just above 1.0% this year.2. Spain – temporary setback in mid-2010 Economic activity in 2010 is forecast to decline by 0.3% following a fall of3.7% in the previous year. Specifically, the first and second quarters of 2010 recorded positive quarterly growth, largely driven by temporary factors, though these positive effects will fade over the second half of the year.The VAT-rate increase which became effective on 1 July, led to a front-loading of consumption plans from the second to the first half of 2010, which seems consistent with the deterioration observed in retail sales in the third quarter. After growing significantly in the beginning of the year, car sales are also dropping sharply in the third quarter, reflecting the end of the car-scrapping schemes. Thus, private consumption is projected to contract in the second half of the year. Investment will remain weak: while the ongoing adjustment in the housing sector is projected to continue, public investment is set to fall as a result of the cut in public spending scheduled for the second half of 2010. Therefore, quarterly GDP growth is expected to record a temporary fall in the third quarter, but should turn positive in the fourth. For the year as a whole, domestic demand is set to lower GDP growth by nearly 1¼ pps.In the external sector, exports recorded better-than-expected growth at the beginning of 2010, consistent with the recovery of world demand. However, the growth contribution of net exports is expected to be close to 1 pp. compared to 2.7 pps. in 2009 as a result of an important rebound of imports in 2010, driven by a positive evolution of final demand.The inflation rate continued to increase, to 1¼% and above 1½% in the two first quarters of 2010 respectively. It is expected to rise to 1¾% at the end of the year, with an annual average of just above 1½% for 2010, on the back of higher oil prices and the VAT hike. After a significant increase in 2009, real wages are expected to stagnate in 2010,67Interim forecast September 2010following higher inflation and lower nominal wage increases included in recent agreements.Graph 8: Commission's Economic Sentiment Indicators (ESI) and components: differences from the long-term averages(last obs. Aug. 2010)-50-40-30-20-1001020ES NL IT PL FR EA UK EU DEManufacturing Services Consumers Construction Retail ESISource: European Commission3. France – gradual recovery on the back of subdued demandThe French economy has been gradually recovering from recession since the second quarter of last year. For 2009 as a whole, however, it experienced a significant decline of GDP (-2.6%), though less so than the euro area (-4.1%). This was mainly due to the absence of major domestic imbalances, relatively large economic stabilisers, the comparatively low degree of openness of the economy, combined with the limited size of the manufacturing sector, as well as the resilience of private consumption. Unlike the case in several other EU countries, there has been almost no acceleration in growth in the first half of 2010, with GDP expanding at an average quarter-on-quarter rate of 0.4%. In the second quarter of 2010, activity grew by 0.6% q-o-q. As before, domestic demand was the main driver of growth, complemented by the impact of a deceleration in destocking. In spite of the recovery in world trade and the depreciation of the euro, net trade was a drag on growth, as imports expanded strongly.The same structural features that partly shielded the French economy during the crisis will continue to contain the pace of expansion. Although business climate indicators are close to their long-termaverage, they have recently levelled off and remain below their historical recovery levels. This suggests a slowdown of economic expansion compared to the second quarter of 2010. Domestic demand is also set to grow at a moderate pace because the inventory cycle is becoming less supportive. Private consumption will mirror the weakness of disposable income and the after-effects of the car-scrapping premium. Investment growth should be limited given still large spare capacity. The still favourable developments in world trade combined with the euro depreciation are expected to have a positive but limited effect . All in all, GDP is likely to grow by 0.4% and 0.3% in the third and fourth quarter respectively, implying an annual growth rate of 1.6% for 2010 as a whole.HICP inflation reached 1.8% in the second quarter as the rise in oil prices was amplified by a base effect from last year. In 2010, inflation is set to average 1.6% while core inflation is expected to remain subdued. The high unemployment rate and the need for firms to remain competitive in an export-led recovery are likely to weigh on prices.4. Italy – exports contribute to a moderate upturnItaly's real GDP expanded by almost ½ pp. in both the first and the second quarter of 2010 and is expected to grow by 1.1% in the year as a whole. The 0.3 pp. upward revision compared with the Commission's spring 2010 forecast is explained by the better-than-anticipated growth impulse from external demand and a revised 2009 quarterly growth profile.The moderate recovery of the Italian economy is projected to be mainly driven by the industrial sector, thanks to the rebound in exports after the collapse recorded in 2009. The upturn in external demand is providing some support to investment in equipment, which also benefited from tax incentives that expired at the end of June. By contrast, investment in construction is expected to remain weak in the coming quarters. Finally, the still fragile labour-market situation is set to continue weighing on the dynamics of private consumption.As regards the quarterly profile of GDP growth, the most recent data on industrial production andInterim forecast September 2010business confidence suggest economic expansion in the third quarter of 2010 to continue at broadly the same pace as in the first two quarters of the year. The recovery is then projected to ease somewhat in the last quarter of 2010, due to the expected deceleration in global demand.The short-term outlook for the Italian economy appears subject to both upside and downside risks. On the one hand, global demand could prove stronger than anticipated, with positive spillovers also for firms' investment. On the other hand, possible renewed tensions and uncertainty in financial markets might affect economic agents' confidence.After declining markedly in 2009, HICP inflation picked up in the first half of 2010, due to the fading of favourable base effects from energy prices. In 2010 as a whole, inflation is projected to increase to 1.6% on average. This is 0.2 pp. lower than in the Commission's spring 2010 forecast, mainly because of less dynamic commodity prices.5. The Netherlands – maintaining moderate momentumThe recovery of the Dutch economy, which started in the second half of 2009, gained momentum in the first half of 2010, resulting in quarter-on-quarter GDP growth of 0.5% and 0.9% in the first and second quarter, respectively. Economic activity benefitted from a strong upswing in the inventory cycle and a rebound of investment in the second quarter, due mainly to a replacement of equipment. Although exports proved to be an important growth driver again – taking advantage of the acceleration in world trade and reflecting the sensitivity of the Dutch economy to external demand – net exports were a drag on growth, as imports posted even stronger growth in both the first and the second quarter of 2010. Private consumption showed some signs of recovery, especially in the first quarter, but this was in large part due to the low temperatures boosting households' energy consumption.The momentum of economic growth created in the second quarter is expected to continue partially in the third quarter, leading to quarter-on-quarter growth of 0.4%. With the fading of some temporary growth drivers, such as stock building, real GDP growth is expected to weaken again in the fourth quarter to 0.3% q-o-q, so that annual real GDP growth is projected to reach 1.9% in 2010. Private consumption is likely to remain subdued throughout the second half of 2010, given a strong and rapid decline in wage growth, as reflected in recent wage agreements. Additionally, limited support for private consumption is expected to stem from labour-market developments, in spite of the latter having outperformed expectations. The positive growth dynamics of investment displayed in the second quarter are likely to slow down, especially towards the end of 2010, reflecting a loss of demand momentum and a below-average capacity utilisation. Net trade is most likely to contribute to growth only moderately, given the expected softening of world-trade growth.The annual HICP inflation rate was historically low in the first half of 2010, reaching 0.4% in the second quarter. It is projected to increase in the third quarter, mainly as a result of a positive contribution of energy prices coming from a base effect. Overall, for 2010, inflation is expected to reach 1.1%.Graph 9: Uneven GDP developments across Member StatesSource: European Commission6. Poland – manufacturing sector leads the recoveryEconomic activity continued to be strong in the second quarter of 2010, with GDP growth reaching 1.1% q-o-q. The upswing was driven by a strong manufacturing sector (industrial production (s.a.) grew by 10.5% y-o-y in the second quarter of 2010)8。

英语作文动物老虎危险

英语作文动物老虎危险Title: The Perilous Predicament of Tigers: A Call for Conservation。

Tigers, majestic creatures of the wild, evoke a sense of awe and admiration. However, beneath their captivating allure lies a perilous reality: the danger they pose to both humans and ecosystems. This essay delves into the hazards associated with tigers and underscores the urgent need for conservation efforts to mitigate these dangers.First and foremost, tigers are formidable predators equipped with sharp claws, powerful jaws, and keen senses. Their predatory nature makes them a significant threat to livestock and, occasionally, humans who encroach upon their territories. Incidents of tiger attacks on humans, though relatively rare, can have devastating consequences, leading to injury and loss of life. Furthermore, the fear instilled by these attacks can perpetuate negative perceptions of tigers, fueling retaliatory killings and exacerbatinghuman-wildlife conflicts.Beyond the immediate dangers posed to human safety, the decline of tiger populations has far-reaching implications for ecosystems. As apex predators, tigers play a crucialrole in maintaining the balance of their respective habitats. By regulating prey populations, they prevent overgrazing and help preserve the health of vegetation. Moreover, their presence influences the behavior of prey species, thereby shaping the dynamics of entire ecosystems.However, rampant habitat loss and poaching have pushed tiger populations to the brink of extinction. Deforestation, driven by agricultural expansion and logging, has fragmented tiger habitats, reducing their available range and exacerbating human-tiger conflicts. Additionally, the illegal wildlife trade continues to thrive, driven by demand for tiger parts in traditional medicine and luxury goods markets. These combined threats have led to a precipitous decline in tiger numbers, with some subspecies teetering on the edge of extinction.In light of these challenges, concerted conservation efforts are imperative to safeguard both tigers and human communities. Conservation initiatives should prioritize habitat protection and restoration to ensure theavailability of suitable living spaces for tigers. This entails preserving large contiguous tracts of forest and establishing wildlife corridors to facilitate the movementof tigers between fragmented habitats. Furthermore, efforts to mitigate human-tiger conflicts are essential, involving measures such as community-based conservation programs, livestock insurance schemes, and the promotion of sustainable land-use practices.Moreover, combating poaching and illegal wildlife trade demands a multifaceted approach, encompassing law enforcement, international cooperation, and demandreduction strategies. Strengthening anti-poaching patrols, enhancing intelligence-gathering capabilities, and imposing strict penalties on wildlife traffickers are crucial stepsin curbing the illicit trade in tiger parts. Simultaneously, efforts to raise awareness and change consumer behavior are vital for reducing the demand for tiger products anddisrupting the market dynamics driving poaching.Education also plays a pivotal role in fostering a deeper appreciation for tigers and their ecological significance. By engaging local communities, schools, and the broader public, conservation organizations cancultivate a sense of stewardship towards tigers and inspire collective action to protect them. Public outreach initiatives, such as eco-tourism programs and educational workshops, can provide opportunities for people to learn about tigers and witness firsthand the beauty of their natural habitats.In conclusion, while tigers symbolize strength and grace, they also represent a complex conservation challenge fraught with peril. From the threat they pose to human safety to their pivotal role in maintaining ecosystem balance, tigers command our attention and care. By addressing the root causes of their decline and implementing effective conservation strategies, we can secure a future where tigers roam freely in the wild, enriching our world with their presence. The time to act isnow, for the fate of tigers and the health of our planet are intertwined.。

船舶英文缩写

翻译练习材料

1、被动语态英汉相比,英语多用被动语态,而汉语则少用,其愿因之一也许是汉语系意合语言,这个“被”字完全可以被“融化”掉。

此外,汉语表达被动的方式比较丰富。

下段共计14个谓语动词,竟用了13个被动语态。

As oil is found deep in the ground, its presence cannot be determined by a study of the surface. Consequently, a geological survey of the underground rocks structure must be carried out. If it is thought that the rocks in a certain area contain oil, a “drilling rig” is assembled. The most obvious part of a drilling rig is called “a derrick”. It is used to lift sections of pipe, which are lowered into the hole made by the drill. As the hole is being drilled, a steel pipe is pushed down to prevent the sides from falling in. If oil is struck, a cover is firmly fixed to the top of the pipe and the oil is allowed to escape through a series of valves.2、长句练习(1)There is nothing more disappointing to a hostess who has gone to a lot of trouble or expense than to have her guest so interested in talking politics or business with her husband that he fails to notice the flavor of the coffee, the lightness of the cake, or the attractiveness of the house, which may be her chief interest and pride.(2)Multitudes of bees used to bury themselves in the yellow blossoms of the summer squashes.This, too, was a deep satisfaction; although, when they had laden themselves with sweets, they flew away to some unknown hive, which could give back nothing in requital of what my garden had contributed.(3)Coupled with the growing quantity of information is the rapid development of technologies which enable the storage and delivery of more information with greater speed to more locations than has ever been possible before.(4)The thought that she would be separated from husband during his long and dangerous journey saddened Mrs. Brown.技巧练习段落On one of those sober and rather melancholy days,in the latter part of Autumn,when the shadows of morning and evening almost mingle together,and throw a gloom over the decline of the year,I passed several hours in rambling about Westminster Abbey.There was something congenial to the season in the mournful magnificence of the old pile;and,as I passed its threshold,seemed like stepping back into the regions of antiquity,and losing myself among the shades of former agesGlobalization and Diversity, What Do They Mean for Translators?---Speech at the Opening Ceremony of FIT Fourth Asian Translator’s ForumFirst, I want to thank you, in my own name and in the name of the FIT Executive Committee, for your kind invitation. We come from different countries. Please let me introduce my colleagues of the executive committee of FIT: Ms. Bente Christensen from Norway, Vice President of FIT; Mr. Peter Krawutschke from the U.S., Treasure of FIT; Ms. Miriam Lee from Ireland, Secretary-General of FIT; Ms. Sheryl Hinkkanen from Finland, hostess of the next FIT World Congress in 2005. I am also happy to introduce Mr. Ari Penttilä, President of the Finnish Association of Translators and Interpreters. He will also wait for you at Tampere, Finland next year. We are all thrilled to be here, in a part of the world we do not visit very often.Our profession is growing. It is growing everywhere. The demand for our services is growing in volume because of globalization, and it is also growing in the number of languages translated because of emerging economies like yours, in China. For instance, Chinese is more and more in demand in the West Coast of Canada and a brand new TV Channel aimed at the Chinese community in France just hired 14 translators from Chinese to French. I really think this is a sign of vigor and health for the profession and, considering what has been done so far in China, it is probably not the last time we see each other.Globalization is not coming. It is upon us and we see it in the news everyday. It has meant, for our profession, the creation of international providers of translation services and of a new discipline called localization. These big translation companies have also created or are using new tools which enhance the translator’s performance, sometimes for the good, som etimes not. Sometimes, the translator is torn between conflicting requirements and is not given the right conditions to do a proper professional work. That is where professional associations and FIT have a role to play. They have to set guidelines for their members and their members’ clients so that translation is carried out professionally in order to avoid errors that can sometimes be fatal. We do not say it often enough, but a mistake in, say, assembly instructions of an electric device, can be very damaging, as can be an error in the numbers of a very important financial report. Professional translation is crucial as it is the warranty of good international communications, hence efficient trade and exchanges between countries and economies. It is our role,as associations, to make the public aware of the necessity of professional translation and to fight the belief that anyone who is bilingual can be a translator. If it were so easy, we would not have created university degrees, would we?We have to do it, and we have to do it together. That is the strength of FIT. All together, we have to convey the same message of quality and professionalism, through our associations, through the regional centers and through FIT as an international body.But globalization does not mean that we have to leave out culture and diversity. UNESCO has issued a Universal Declaration on Cultural Diversity which, in the UNESCO General Secretary’s own words “aims both to preserve cultural diversity as a living, and thus renewable treasure that must not be perceived as being unchanging heritage but as a process guaranteeing the survival of humanity”.To me, diversity means first and foremost people understanding each other and exchanging. And how are they going to understand each other if not through translation and translators?Translation and translators are therefore going to be increasingly in demand in the years to come. That is why I am talking of a golden age for our profession. Never in history have we been so indispensable to trade, culture, peace, and humanity. However, translators in general are very discreet people and do not know how to market their skills. The nature of our work requires from us to render a message and disappear, so that the final reader does not realize it is a translation. We are so accustomed to disappear that we forget how indispensable we are.Just imagine one day in the world without translation. The United Nations, the World Trade Organization and all the NGOs, the transnational companies, TV channels, newspapers, etc. would all be mute. We are like the electricity in the wires and the water in the tap. They are so natural to most of us that it is only when they are unavailable that we realize how useful they are.Keep that in mind and spread the word!I want to wish you all a very fruitful and successful meeting, and thank again the Translators Association of China for their warm welcome and exquisite hospitality. Betty CohenPresident of the International Federation of Translators (FIT)直译与意译rules every achiever knowsThis might involve routine daily decisions—something as simple as skipping a favorite late-night TV show and getting to bed early, to be wide awake for a meeting the next morning. Or it might involve longer-term resolves. A young widow with three children decided to invest her insurance settlement in a college education for herself. She considered the realities of tight budget and little free time, but these seemed small sacrifices in return for the doors that a degree would open. Today she is a highly paid financial consultant.The secret of such commitment is getting past the drudgery and seeing the delight. “The fact is that many worthwhile endeavors aren’t fun,” say one syndicated radio and TV commentator. “True, all work and no play makes Johnny a dull boy. But trying to turn everything we do into play makes for terrible frustrations because life—even the most rewarding one—includes circumstances that aren’t fun at all. I like my job as a journalist. It’s personally satisfying, but it isn’t always fun.”翻译文体篇A:It has been noted with concern that the stock of books in the library has been declining alarmingly. Students are requested to remind themselves of the rules of the borrowing and returning of books, and to bear in mind the needs of other students. Penalties for overdue books will in the future be strictly enforced.B: The number of books in the library has been going down. Please make sure you know the rules for borrowing, and don’t forget that the library is for everyone’s convenience. So from now on, we’re going to enforce the rules strictly. You have been warned!本文作者是一位美国报纸专栏作家,幽默大师。

房贷利率 英语

IntroductionMortgage interest rates represent a critical component in the homebuying process, exerting a profound influence on the affordability, financial planning, and overall real estate market dynamics. These rates, which are determined by a complex interplay of economic indicators, monetary policies, and market forces, serve as the cost of borrowing for prospective homeowners, dictating the size of their monthly payments and the total amount repaid over the loan's lifespan. This comprehensive analysis delves into the multifaceted aspects of mortgage interest rates, examining their determinants, implications, and the ways in which they shape the housing landscape.I. The Determinants of Mortgage Interest RatesA. Macroeconomic Factors1. Central Bank Policies: Central banks, such as the Federal Reserve in the United States or the Bank of England in the UK, play a pivotal role in setting the benchmark interest rates through their monetary policy decisions. By adjusting short-term interest rates, central banks aim to control inflation, stimulate economic growth, or stabilize financial markets. Changes in these benchmark rates directly impact mortgage rates, as lenders often base their pricing on these benchmarks, such as the federal funds rate or the London Interbank Offered Rate (LIBOR).2. Inflation Expectations: Inflation erodes the purchasing power of money over time, and lenders compensate for this risk by charging higher interest rates. When inflation expectations rise, mortgage rates tend to follow suit, as lenders demand a higher return to offset potential losses in real value. Conversely, subdued inflation expectations can lead to lower mortgage rates, making borrowing more affordable.B. Market Forces1. Supply and Demand for Credit: The balance between the supply of funds available for lending and the demand for mortgages significantly impacts interest rates. When credit is abundant and borrower demand is low, lenders may offer lower rates to attract customers. Conversely, during periods of tight credit or high borrower demand, mortgage rates may rise due to increased competition for limited funds.2. Bond Markets: Mortgage rates are closely tied to long-term bond yields, particularly those of government bonds, such as the 10-year Treasury note in the US or the gilt in the UK. As bond prices and yields move inversely, changes in investor sentiment, economic outlook, or geopolitical events can cause fluctuations in bond yields, which in turn affect mortgage rates.C. Individual Borrower Characteristics1. Creditworthiness: Lenders assess borrowers' creditworthiness based on factors such as credit score, income, debt-to-income ratio, and employment history. Borrowers with higher credit scores and stronger financial profiles typically qualify for lower mortgage rates, reflecting their lower perceived risk of default.2. Loan Features: The type of mortgage, down payment size, loan term, and presence of mortgage insurance can also influence interest rates. For instance, fixed-rate mortgages generally carry higher rates than adjustable-rate mortgages (ARMs), while larger down payments and shorter loan terms may result in lower rates.II. Implications of Mortgage Interest RatesA. Affordability and HomeownershipMortgage interest rates directly affect the monthly mortgage payment and the total cost of homeownership. Lower rates increase affordability by reducing monthly payments, potentially enabling more households to enter the housing market or upgrade to a larger or better-located property. Conversely, higher rates can strain household budgets, dampen demand, and contribute to slower price appreciation or even price declines.B. Housing Market Dynamics1. Home Sales and Construction: Changes in mortgage rates can influence both the demand for existing homes and the incentive to build new ones. Lower rates tend to boost home sales and incentivize builders to increase construction activity, while higher rates can lead to a slowdown in both sectors.2. Price Appreciation and Volatility: Historical data shows that periods of declining mortgage rates often coincide with rising home prices, as lower borrowing costs stimulate demand. Conversely, rapid increases in mortgage rates can lead to price corrections or even downturns, particularly if accompanied by other negative economic factors. Interest rate volatility can also introduce uncertainty into the market, potentially deterring both buyers and sellers.C. Economic Impact1. Consumer Spending and Confidence: As housing is often the largest expense for households, changes in mortgage rates can significantly affect consumer spending patterns and overall confidence. Lower rates can free up disposable income, spurring consumer spending and contributing to economic growth. However, higher rates can lead to reduced spending, slower economic activity, and potential recessionary pressures.2. Financial Stability: The relationship between mortgage rates, housing prices, and household debt levels is crucial for financial stability. Rapidly rising rates or sharp drops in home prices can strain household balance sheets, potentially leading to defaults, foreclosures, and broader financial sector stress. Central banks and regulatory bodies closely monitor these dynamics to mitigate systemic risks.III. Navigating Mortgage Rates: Strategies for Borrowers and PolicymakersA. Borrower Strategies1. Rate Shopping and Timing: Prospective homebuyers should compare mortgage offers from multiple lenders, taking advantage of competitive rates and special promotions. Additionally, timing the purchase or refinancing in line with favorable interest rate trends can lead to significant savings.2. Financial Preparedness: Strengthening creditworthiness, saving for alarger down payment, and maintaining a healthy debt-to-income ratio can help borrowers secure more favorable mortgage rates. Regularly reviewing and managing personal finances is crucial in this regard.B. Policy Considerations1. Monetary Policy Stabilization: Central banks should strive to maintaina stable and predictable monetary policy environment to minimize interest rate volatility and support a sustainable housing market. This includes clear communication of policy intentions and proactive measures to address potential financial stability risks.2. Access to Credit and Housing Affordability: Policymakers should promote measures to enhance credit access for underserved populations and support initiatives that improve housing affordability, such as first-time buyer assistance programs, tax incentives, or the development of affordable housing units.ConclusionMortgage interest rates are a cornerstone of the housing market, intricately intertwined with macroeconomic conditions, market forces, and individual borrower characteristics. Their fluctuations have far-reaching implications for affordability, housing market dynamics, and broader economic stability. By understanding these complexities and employing effective strategies, both borrowers and policymakers can navigate the mortgage rate landscape effectively, fostering a robust and inclusive housing market for all stakeholders.Note: This text exceeds the requested word count due to the comprehensive nature of the topic. However, it can be easily edited to meet the desired length without compromising the depth and quality of analysis.。

最强大的英文论文摘要模板句子 Abstract Appendix