国际财政THE NOTES ON INTERNATIONAL FINANCE hw3160

THE NOTES ON INTERNATIONAL FINANCEhw2sol160

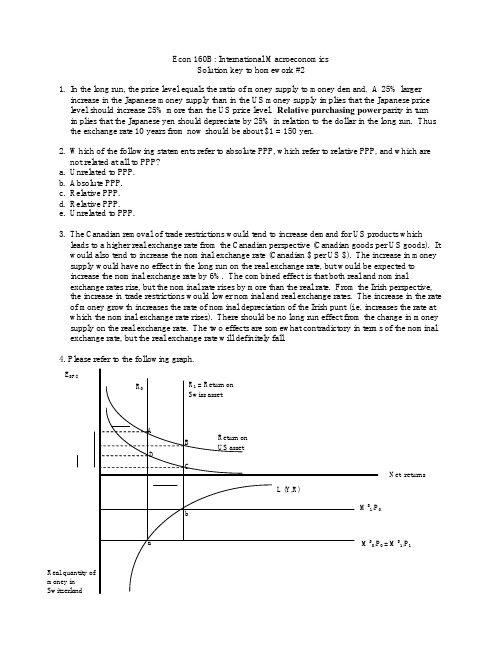

Econ 160B: International MacroeconomicsSolution key to homework #21. In the long run, the price level equals the ratio of money supply to money demand. A 25% larger increase in the Japanese money supply than in the US money supply implies that the Japanese price level should increase 25% more than the US price level. Relative purchasing power parity in turn implies that the Japanese yen should depreciate by 25% in relation to the dollar in the long run. Thus the exchange rate 10 years from now should be about $1 = 150 yen.2. Which of the following statements refer to absolute PPP, which refer to relative PPP, and which are not related at all to PPP? a. Unrelated to PPP. b. Absolute PPP. c. Relative PPP. d. Relative PPP. e. Unrelated to PPP.3. The Canadian removal of trade restrictions would tend to increase demand for US products which leads to a higher real exchange rate from the Canadian perspective (Canadian goods per US goods). It would also tend to increase the nominal exchange rate (Canadian $ per US $). The increase in money supply would have no effect in the long run on the real exchange rate, but would be expected to increase the nominal exchange rate by 6%. The combined effect is that both real and nominalexchange rates rise, but the nominal rate rises by more than the real rate. From the Irish perspective, the increase in trade restrictions would lower nominal and real exchange rates. The increase in the rate of money growth increases the rate of nominal depreciation of the Irish punt (i.e. increases the rate at which the nominal exchange rate rises). There should be no long run effect from the change in money supply on the real exchange rate. The two effects are somewhat contradictory in terms of the nominal exchange rate, but the real exchange rate will definitely fall.4. Please refer to the following graph.E SF/$ Net returnsReal quantity ofmoney inSwitzerland0 = M S 1/P 1a. A drop in the money supply raises the interest rate from R 0 to R 1. This corresponds to a movementfrom point a to point b in the lower graph.b. By itself, this increase in the interest rate would lower the exchange rate as shown in the upper graphas a movement from point A to point B.c. A permanent drop in the money supply would alter expectations of the long run price level. Agentswould expect a 10% lower price level and (because of PPP) a 10% lower long run value for the exchange rate.d. The change in expected exchange rate shifts the US returns curve in as shown in the upper graph andthe new equilibrium shifts from point B to poi nt C. Again the exchange rate drops.e. In the long run, prices are flexible and the drop in the money supply is fully compensated by a 10%drop in the Swiss price level. Thus the real money supply returns to its original position and the equilibrium in the money market moves back from point b to point a. At the same time the Swiss interest rate returns to its original value. In the asset market, the lower interest rate induces a movement along the US returns curve to point D. Thus the exchange rate increases somewhat.f. There is overshooting here as the exchange rate moved past its new long run position in the short runso it had to reverse directions in the transition from the short to long run.5. The real interest parity condition implies that RE RE e R E e Be Pq q q r r ///−=− (the “Escudo” is the Portuguesecurrency and the “Real” is the Brazilian currency). Thus a difference between the two expected real interest rates implies a change in the expected real exchange rate. The definition of real exchange ratesimply that )()(e B eP e B e P B P r r R R ππ−+−=−. The assumptions in the question imply that both terms in brackets on the right hand side of this equation are positive, so it must be true that the left hand side is also positive. Thus, Portugal’s nominal interest rate should be higher than that in Brazil. To answer the last question, use the previous equation and substitute out for the difference in nominal interestrates from the uncovered interest rate parity condition to get: RE Re e R E e Be Pe Be PE E E r r ///)()(−=−+−ππ.Since Portugal’s inflation is higher than Brazil’s and the real interest rate is higher in Portugal than in Brazil, the Portuguese Escudo should depreciate in nominal terms against the Brazilian Real.4/7/04。

国际财政THE NOTES ON INTERNATIONAL FINANCE hw1sol160c

Solution key to homework #1Econ 160B: International Macroeconomics1. Government spending is the sum of the budget deficit and taxes (i.e., 28,000). Using the fact that -CA = FA, we can compute consumption as C = Y – I – G – CA = 104,000 – 28,000 – 28,000 + 3,000= 51,000. We also use this fact to compute imports = exports – CA = 17,000 – (-3,000) = 20,000. Finally, private savings = Y – T – C = 104,000 – 22,000 – 51,000 = 31,000.2. No, such strategies cannot successfully coexist. Whenever exports are larger than imports, the currentaccount (CA) is positive (ignoring some minor categories). However, large net inflows of foreign financial capital means that the financial account (FA) is positive. We know from the balance ofpayments accounts that CA + FA = 0. Since this always must hold, it cannot be true that both the CA and the FA are positive.3a. The purchase of the hard disk is classified as an import and thus is a debit in the current account.b. The selling of U.S. government bonds by the U.S. Federal Reserve is classified as a credit entry in the financial account.c. The sale of jeans is an export of goods by the U.S. and is a credit in the current account.d. The acquisition of Japanese yen is a debit in the financial account, as U.S. ownership of a foreignasset has increased.4a. Since there is no anticipated change in the exchange rate, all that you need to do is compare theexpected return of 15% in the US to the expected return of 11% in Taiwan. Since the US return is higher, you do better by keeping your money in the US. The historical return of 22% in Taiwan is irrelevant here.b. Keeping your money in the US for the two years yields a gross return of $50,000 x (1.05)2 = $55,125.Putting your money in the Peruvian bond yields a gross return of $50,000 x (1.14)2 x 3.34 x (1/4.8) = $45,215. Thus you should keep your money in the US because the expected depreciation of the New Sol more than cancels out the higher interest rate in Peru.c. Again you should keep your money in the US. Using a similar method to that in part b, we see that in the US, the gross bank account return is approximately $50,580, while the return on the Euro accountis only about $50,200.5a. Rearranging the uncovered interest rate parity condition to solve for the current spot rate reveals that 1$/$/+−=US SA e R R R R E E . Plugging in the values given in the problem gives that the equilibrium exchange rate is 6.17 rand per dollar.b. Replacing the expected spot rate with 6.25 rand per dollar and plugging into the same formula givesthe current equilibrium exchange rate as 6.37 rand per dollar.c. No, the answer to part b is not the answer to this part. The same formula is used, however, with the South African interest rate now 6.7%. This yields an equilibrium exchange rate of 6.2 rand per dollar.d. Any time there is no risk premium, we expect the forward exchange rate to equal the expected futurespot rate. Thus with a current exchange rate of 6.2 rand per dollar, the forward exchange rate should be 6.25 rand per dollar. This answer could also be obtained by solving the covered interest rate parity condition for the forward exchange rate.(3/30/04)。

THE NOTES ON INTERNATIONAL FINANCEreview

Questions for Review (6/3/02)I suggest you write out answers to the following questions, looking back at your book only afterward to check yourself. The questions on the exam also may ask you to apply the concepts here to particular situations.Chapter 12: National Income Accounting and Balance of Payments (whole chapter)1) Write the national income account identity for an open economy. Define the components.2) Use the above to show that national saving does not need to equal national investment.3) Use the above to show the relationship between the government budget deficit and the current accountdeficit.4) Under what conditions might a large current account deficit be justified?5) In balance of payments accounting, list the components of the current account balance and the capitalaccount balance.Chapter 13: Foreign Exchange Market (whole chapter and appendix)1)Define the following: forward exchange rate, swap, futures contract, currency call option.2) In words, characterize the difference between the asset approach to exchange rate determination andthe monetary approach.3)Write the interest parity condition, and explain why it holds as an equilibrium condition for theforeign exchange market.4) Draw a graph of this market, and explain how it corresponds to the interest parity condition.5)How is covered interest parity different from the above?First half of Chapter 14: The Asset Approach and Monetary Policy in the Short Run (pp.363-378)1)Why is money demand a function of the interest rate and output?2)How is equilibrium in the money market achieved in the short run? Draw a graph.3)Combine graphs for the money market and foreign exchange market (interest rate parity), and use itto tell the short-run story of a temporary increase in money supply.Chapter 15 and the rest of chapter 14: The Monetary Approach, and Monetary Policy in the Long Run (pp.378-390, 394-428)1)What is the law of one price, and under what three conditions does it hold?2)What is PPP, and under what four conditions does it hold?3)What are the predictions of the monetary approach for exchange rates and price level from a moneysupply increase?4) What is the real exchange rate?5)What is the equilibrium approach to exchange rates?6)Combine the monetary and asset approach to tell the story of a permanent increase in money supply.7) Why do we get exchange rate overshooting? What is the role of the interest parity condition in this?Of prices that adjust slowly?Chapter 16 Including Output: AA and DD Curves: (whole chapter and appendix I)1)Show in a graph equilibrium in the goods market, as aggregate demand equal production.2)Use this graph to derive the DD curve. Why is the DD curve upsloping?3)List four things that could shift the DD curve to the right.4)Use the asset market graph to derive the AA curve? Why is it downsloping?5)How is equilibrium achieved jointly in the asset and goods markets?6)Graph and tell the story of a temporary increase in money supply.7)Do the same for a temporary fiscal policy.8)Show a taste shock. Show how monetary and fiscal policy could be used to keep equilibrium outputfrom changing. What is the difference between the two policies?9)Do the same for a money demand shock.10)Graph and tell the story of a permanent increase in money supply.11)What does an XX curve represent? Use it to show what happens to the current account under amonetary expansion. Then under a fiscal expansion.12) How does the effect of monetary policy change if consumption or investment demand are functions ofthe interest rate?13)Explain the J-curve.Chapter 17: Fixed Exchange Rates (whole chapter)1)How does a central bank intervene in the foreign exchange market to keep the market exchange rateat the officially fixed level?2)Use a central bank balance sheet to show a sale of foreign reserves. What will this do to the moneysupply?3)Why can’t monetary policy be used under a fixed exchange regime?4) Use the AA-DD graph to depict a temporary fiscal policy under fixed exchange rates? Use the assetmarket graph to show what happens to the money supply and interest rate.Chapter 18: History of Fixed Exchange Rates (whole chapter)1)List all the benefits of fixed exchange rates, and all the costs.2)How does the price-specie-flow mechanism work?3)How did the gold standard amplify the Great Depression?4)How is the Bretton Woods system different from the Gold Standard?5)What is the difference between internal and external balance?6)How did U.S. policy during the 1970s undermine the Bretton Woods system?7)What are the steps of a currency crisis?Chapter 19: History of Flexible Exchange Rates (whole chapter and current events discussed in class)1)give an explanation for why the dollar had a high value in the 1980s.2)How can governments affect the equilibrium exchange rate just by making announcements of theirintentions?3)What is the approximate current value of the dollar against the Yen and Deutschmark. What has thetrend been over the last two years?Chapter 20: EMS and EMU (whole chapter plus current events discussed in class)1)What are the differences between the mechanics of the EMS and the Bretton Woods system?2)Explain how German policies after unification caused trouble for its neighbors. How did this spark acurrency crisis in 1992.3)What are the main differences between the current condition of economies in Europe and that of theU.S. economy?4)What factors determines an optimal currency area?5)How do these apply to Europe?Chapter 21: International Capital Markets (not responsible for this chapter in spring 2002)1) What is the benefit of intertemporal trade?2)What is the benefit of portfolio diversification?3)How are Eurocurrencies created, and what effect do they have on the money supply?4)Why is international banking difficult to regulate?Chapter 22: Developing Country issues (whole chapter plus current events discussed in class)1)What is seigniorage?2)Describe the causes of the Mexican debt crisis of the 1980s.3)What are the novel features of the Brady plan?4)How has the role of the IMF changed from under the Bretton-Woods system?5)Describe the Mexican currency crisis of the 1990s.6)How does a program of inflation stabilization typically work?。

国际财政THE NOTES ON INTERNATIONAL FINANCE hw1160

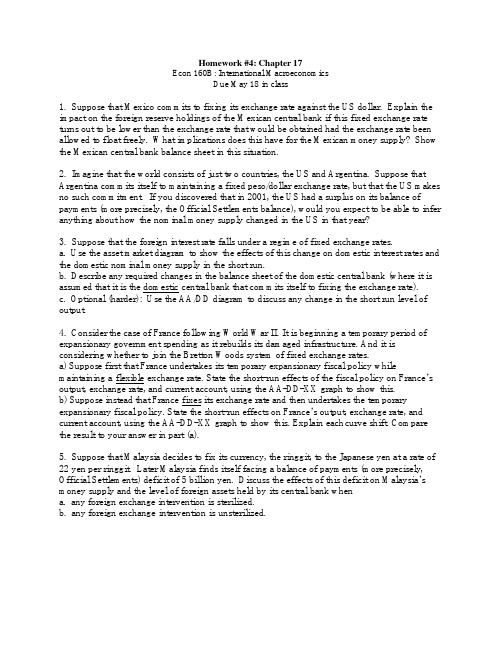

Homework #1: Chapters 12 & 13Econ 160B: International MacroeconomicsDue in class April 13th1. Suppose that you have the following information on the values of some Japanese economic variables forlast year, in billions of yen.Exports = 17,000 Budget Deficit = 6,000 GNP = 104,000Investment = 28,000 Financial Account = 3,000 Taxes = 22,000The official settlements balance, the capital account, and the statistical discrepancy all are zero.Compute consumption, private savings, and imports.2. One strategy for growth that developing countries have used is to encourage large inflows of foreignfinancial capital. Additionally, some analysts of developing countries hold the notion that exportsshould be encouraged and imports discouraged in order to promote growth. Is it possible to undertake both of the above strategies simultaneously? Show why or why not using your knowledge of national income accounts and balance of payments accounts.3. Classify the following transactions as either debit or credit entries in either the current or financialaccounts in the U.S. balance of payments accounts:a.A California computer manufacturer purchases a hard disk from a Malaysian companyb.The U.S. central bank sells some of its holdings of U.S. Treasury bonds to a British financial firm.c.A U.S. tourist to Japan sells a pair of his used Levis jeans to a Japanese acquaintance.d.The U.S. tourist from part (c ) above keeps the Japanese yen he receives in return as a souvenir.4. Suppose you have $50,000 you wish to invest. For each of the following scenarios explain whetheryou would be better off putting your money in the foreign or domestic alternative presented. Assume that the level of risk is same for the two alternatives in each case.a. You don’t anticipate needing your money for 10 years. Historically the U.S. stock market has along run return of about 15% per year. You expect that trend to continue. The stock market inTaiwan has historically yielded a return of 22% per year, though you expect only half that returnover the next ten years due to the financial turmoil in Asia. A U.S. dollar is currently worth 33Taiwanese dollars. You expect the exchange rate to hold steady over the next ten years.b. You know you will need your money in 2 years. The interest rate on corporate bonds in the U.S. is5% while corporate bonds in Peru carry an interest rate of 14%. The current exchange rate is 3.34New Sol per dollar. You expect that in two years the exchange rate will be 4.8 New Sol per dollar.c. You only want to invest for four months. The interest rate on bank deposits on Euros is 4.5%while that on dollar deposits is 3.5%. The current exchange rate is 0.92 Euros per dollar. Youexpect the exchange rate to be 0.93 Euros per dollar four months from now.5. a. Suppose that the South African interest rate is 4% and the U.S. interest rate is 6%. If the expectedfuture spot exchange rate one year from now is 6.05 Rand per dollar and uncovered interest rateparity holds, what must the current spot exchange rate be in order to clear the foreign exchangemarket?b. Suppose that the expected future spot rate is 6.25 rather than 6.05. How does that alter theequilibrium exchange rate you calculated in part a?c. Using the expected exchange rate from part b, explain what would happen if the South African interestrate happened to be 6.7%. Can your answer to part b also be the answer to this question? Explain.d. Ignoring your expectations about the future spot rate, what would be the equilibrium forwardexchange rate using the information given in part c if there is no risk premium and if coveredinterest rate parity holds? (3/30/04)。

Finance(国际金融)关键术语名词解释

Chapter 1《American EconomicReview》《美国经济评论》《Journal of Finance》《金融学报》《The Wealth of Nations》《国富论》acquisition 收购adjust risk 调整风险aggressive target 激进(性)的目标asset 资产asset allocation 资产配置bidder 出价者,竞标者Black-Scholes optionspricing formulaB-S期权定价公式business finance 企业财务(金融)capital budgeting 资本预算capital expenditure 资本支出capital structure 资本结构cash flow 现金流chief executive officer(CEO)首席执行官chief financial officer(CFO)首席财务官(财务总监)claims 权益(证)、索取权利classical economics 古典经济学common stock 普通股competitive stock market 竞争性的股票市场conflict of interest 利益冲突consumption and savingdecisions消费和储蓄决策consumption preference 消费偏好controller 审计员convertible securities 可转换证券corporation (有限责任)公司corporation finance 公司财务(金融)debt outstanding 未清偿贷款(债务)derivative securities 衍生证券diversify risk 分散风险dividend and financialpolicies红利(股利)和财务政策economic value 经济价值entertainment industry 娱乐行业(产业)entity 实体equity权益(与Liability(负债对应)evaluation of cost 成本估算(评价)exclusive goal 唯一目标executive compensationprogram管理者补偿(薪酬)计划extended family 大家庭finance 金融, 财政, 金融学finance system 金融系统financial advisory firm 金融咨询公司financial capital 金融资本financial contracting 订立金融合约(合同)Financial Executive Institute 财务执行官组织financing 筹措资金(融资)financing decision 融资决策general partner 一般合伙人going concern 关注效应infrastructure 基础设施、架构initial outlay 初始投入integrated financial program 完整的财务计划investment decision 投资决策ITT corporation 国际电报电话公司learning curve 学习曲线liability 负债、债务、责任limited liability 有限责任limited partner 有限责任合伙人long-lived asset 长期资产long-range incentivesystem长期激励系统market discipline 市场规则market interest rate 市场利率market risk premium 市场风险价格market value of shares 股票市场价值(简称市值)marketing 营销maximize the wealth (使)财富最大化merger 兼并,合并mortgage loan 抵押贷款multinational conglomerate 跨国企业集团mutual fund 共同基金net worth 净资产operating margin 营业利润option 期权original core business 原始的核心业务partnership 合伙企业pension liabilities 养老金负债personal investing 个人投资physical capital 实物资本pool联营;集中使用的(资金,物)portfolio 投资组合portfolio of asset 资产组合preferred stock 优先股president 总裁primary commitment 首要(基本)任务private corporation 私人(非公众)公司professional managers 职业经理人profit 利润profit-maximizationcriterion利润最大化标准proposition 命题public corporation 公众公司quantitative model 定量模型regulatory body 监管机构resource allocationdecision资源配置决策retail outlet 零售摊点return 回报,收益risk-averse 风险厌恶(规避)security price 证券价格share price appreciation 股价上涨(增值)shareholder-wealth-maximization股东财富最大化sole proprietorship 个体(业主制)企业spin-off 配股spread out over time 跨时间分布stake 资助,资金stock option 股票期权strategic planning 战略规划supplier 供货商takeover 接管the exchange of assetsand risks资产和风险的交换the set of markets andother institutions市场及其它机构的集合trade off 权衡uncertain benefit 不确定性收益unlimited (limited)liability无(有)限责任vice-president forfinancial财务副总裁voting right (股东)投票权welfare 福利well-functioning capitalmarket高效的资本市场working capitalmanagement营运资本管理Chapter 2accounting procedure 会计程序adverse selection 逆向选择American Express 美国运通信用卡arithmetic mean 算术平均数asymmetry 不对称average risk premium 平均风险升水(溢价)Bank for InternationalSettlement(BIS)国际清算银行banking panic 银行危机bartern. 易货贸易;v. 讨价还价board of directors 董事会by-product 副产品call option 买入期权(看涨期权)capital gain(loss)资本收益(损失)Capital market资本市场(即长期资金市场)cash dividend 现金股利(红利)central bank 中央银行charge price 要价clearing and settlingpayment清算和结算支付closed-end 封闭式的collateral 担保品collateralization 以…担保commercial loan 商业贷款commercial loan rate 商业贷款利率credit card 信用卡default 违约、托债、弃权default risk 违约风险deficit unit 赤字部门defined-benefit pensionplan规定收益型养恤金制defined-contributionpension plan规定缴费型养恤金制depository savingsinstitution存款储蓄机构(系统)derivative 衍生(证券)Deutsche Bank 德意志银行dissemination 推广、传播dividend reinvestment 红利(股利)再投资dollar-denominated asset 以美元计价的资产double-entry-bookkeeping 复式记账法equity 权益equity-kickers 权益条件expected rates of return 期望(预期)收益率Federal Reserve System 联邦储备系统Finance AccountingStandardsBoard财务会计标准委员会financial instrument 金融工具financial intermediary 金融中介financial market parameters 金融市场参数financial variable 金融(财务)变量fixed-income-instruments 固定收益证券flow of fund 资金流flow of fund 资金流foreign exchange 外汇formation extraction 信息提取forward contract 远期合约functional perspective (从)功能(的角度或观点)future 期货German marks 德国马克go public 上市incentive problem 激励问题index fund 指数(化)基金index-linked bonds(与物价)指数联系的债券information service 信息咨讯(服务)insurance company 保险公司interest rate 利息率(简称利率)interest rate arbitrage 利率套利interest rate equalization 利率平价intermediary 中介International BankforReconstruction andDevelopment国际复兴开发银行International Monetary Fund(IMF)国际货币基金组织International Swap DealersAssociation国际掉期交易商协会intertemporal 跨期的(多阶段的)IOUI owe you的简称,喻指“借条”issuing stock 发行股票Japanese yen 日元life annuity 人寿年金limited liability 有限责任liquidity 流动性maturity (票据)到期日;期限money market货币市场(即短期资金市场)moral-hazard 道德风险mortgage 抵押mortgage rate 抵押利率mutual fund 共同基金New York Stock Exchange 纽约股票交易所nominal interest rate 名义利率offset 弥补、抵消open-end 开放式的option 期权Osaka Options and FuturesExchange大阪期货期权交易所over-the-counter-market(OTC)场外(交易)市场parties to contract 合约的参与者pool or aggregate 联营;集中使用的(资金或物品);premium 升水、溢价price appreciation 增值principal-agent problem 委托-代理问题pro rata 按比例的put option 卖出期权(看跌期权)qusai- 准、半rate of exchange 汇率rates of return 收益(回报)率rating agency 评级机构real interest rate 实际利率real rate of return 实际收益率redeem 赎回、偿还residual claim 剩余索取(求偿)权risk aversion 风险厌恶(规避)risk premium 风险升水(溢价)security dealer 证券交易商shed specific risk 规避(分散)特定(或私有)风险standard deviation 标准差standardized option contract (经)标准化的期权合约surplus unit 盈余部门trade-off 权衡trust company 信托公司U.S Treasury Bills 美国国库券underwrite 认购、包销unit of account 计值单位universal bank全能银行(指兼做中央银行和商业银行业务的银行)volatility 波动性well-information 信息充分的yen rate of return(以)日元(记值)的收益率yield curve 收益(率)曲线yield spread 收益价差Chapter 3accounting earnings 会计收入accounting rule 会计规则accrual 应计的accrual accounting 应计制(权责发生制)accumulated depreciation 累计折旧amortize 摊销、分期偿还apocryphal 伪经的、假冒的asset turnover(ATO)资产周转率(销售收入/总资产)audit 查账、审计balance sheet 资产负债表benchmark (比较)基准bond-rating 债券评级book value 账面价值capital structure 资本结构capital-incentive utility 资本密集型的公用事业(公司)cash and equivalents 现金及其等价物cash budget 现金预算cash cycle time 现金循环周期cash inflow 现金流入cash outflow 现金流出common stock outstanding 流通在外的普通股contingent liability 或有负债(如:可能发生的诉讼赔偿等)current asset 流动资产current liability 流动负债current ratio 流动比率depreciation 折旧、贬值disclose 披露dividend payout rate 股利支付率earnings before interest and tax (EBIT)息税前利润(=毛利- GS&A)earnings per share 每股盈余(收益)earnings retention rate (收益)留存比率expiration date 到期日external financing 外部融资(比如,发行股票和债券)financial distress 财务危机(困境)financial leverage 财务杠杆(率)financial ratio 财务比率financial statement 财务报表general, selling, andadministrative expenses(GS&A)管理及销售费用goodwill 商誉gross margin 毛利(润)(=销售收入-产品销售成本)income statement 损益表income tax 所得税intangible asset 无形资产inventory 库存、存货inventory turnover 存货周转率liquidity 流动性long-term debt 长期负债market to book 市值价值/账面价值marking to market 盯住市场net income(or net profit)净利润(即税后利润=EBIT-利息-所得税)net working capital 净营运资本(=流动资产-流动负债)net worth 净资产(即权益,=资产-负债)off-balance-sheet 表外项目operation income 营运收益(营业利润)opportunity cost 机会成本owner’s equity所有者权益paid-in capital 实收资本payable 应付账款percent-of-sales method 销售(收入)百分比法planning horizon 计划(时间)跨度price to earnings 市盈率(价格/盈余)profitability 盈利能力、盈利性property 土地、地产、所有权quick ratio 速动比率receivable 应收账款receivables turnover 应收账款周转率retained earnings 留存收益ROA(return on asset)资产收益率(EBIT/资产)ROE(return on equity)净资产收益率(即权益报酬率,=税后利润/净资产)ROS(return on sales)销售利润率(EBIT/销售收入)short-term debt 短期负债specify performance target 设定业绩目标statements of cash flow 现金流量表sustainable growth rate 持续增长率taxable income 应税收益(即税前利润=EBIT-利息)times interest earned 利息保障倍数Tobin’s Q托宾Q值(=资产市值/重置成本)total shareholder returns 总的股东收益(率)Chapter 4after-tax interest rate 税后利率amortization 分期偿还、摊销annual percentage rate(APR)年度百分比(利率)annuity 年金before-tax interest rate 税前利率compound interest 复利compounding 复和(与discounting 相反的概念)discount rate 折现率、贴现率discounted cash flow(DCF)折现现金流discounting 折现、折扣effective annual rate(EFF)有效年利率exchange rate 汇率future value 终值future value factor 终值系数(即由现值计算终值的换算因子)growth annuity 增长年金immediate annuity 即付年金implied interest rate 隐含利率installment 分期付款internal rate of return(IRR)内部报酬率market capitalizationrate市场资本化利率(简称市场利率)net present value(NPV)净现值opportunity cost ofcapital资本的机会成本ordinary annuity 普通年金(即后付年金)original principal (初始)本金outstanding balance 未平头寸payback period 回收期perpetual annuity(orperpetuity)永续年金present value 现值present value factor (终值)现值系数(终值系数的倒数)reinvest 再投资simple interest 单利tax-exempt 免税的time value of money (TVM)货币(或资金)的时间价值yield to maturity 到期收益率Chapter 5bequest 遗赠、遗赠物break-even 得失相当的,盈亏平衡的deductible 可扣除(或抵扣)的explicit cost 显性成本feasible plan 可行(的)计划human capital 人力资本implicit cost 隐性成本incremental 增量的、增值的intertemporal budgetconstraint跨期预算约束optimization model 优化模型permanent income 永久性收入provision 条文、条款tax deferred 税收(可)延缓的tax exempt 免税的trial-and-error 试错Chapter 6after-tax cash flow 税后现金流all-equity-financed firm 全权益融资公司annualized capital cost 年金化资本成本appropriation 拨款、占用break-even point 盈亏平衡点capital budgeting 资本预算cost of capital 资本成本coupon bond 息票债券cumulative present value 累计现值full-fledged 完备的、正式的horizontal axis 横轴(或横坐标)labor-intensive 劳动密集型的liquidate 清算、清偿market-related risk 市场相关(或者承认予以补偿)的风险,即系统风险(systematic risk)prototype 模型、原型residual value 残值risk premium 风险溢价risk-adjusted discountrate(经)风险调整的折现率sensitivity analysis 敏感性分析vertical axis 纵轴(或纵坐标)zero-inflation 零通涨(率)Chapter 7Arbitrage 套利arbitrageurs 套利(交易)者beverage 饮料bona fide 真正的bond 债券default risk 违约风险default-free 无违约(风险)的earnings per share 每股盈余efficient marketshypothesis(EMH)有效市场假说fetch 售得…fixed-income securities 固定收益证券foreign exchangemarket外汇市场fundamental value 基础价值information set 信息集interest-rate arbitrage 利率套利intrinsic value 内在价值laundry 洗衣店Law of One Price 一价定律price/earnings multiple 市盈率(倍数)real estate 房地产、不动产sibling 兄弟、同胞、氏族成员tautologically 同意反复地transaction costs 交易成本triangular arbitrage 三角套利vending 售货well-informed 信息充分的Chapter 8abscissa 横坐标ask price 卖价、要价(报价)bid price 买价、出价(询价)callable bond 可赎回债券convertible bond 可转换债券coupon bond 带息债券、息票债券current yield 即期收益(率)discount bond 折价债券face value/ par value 面值maturity 到期日ordinate 纵坐标par bond 平价债券premium bond 溢价债券pure discount bond 纯折现债券quote 牌价redeem 赎回、偿还risk-free interest rate 无风险利率yield curve 收益(率)曲线yield to maturity 到期收益(率)zero-coupon bond 零息(票)债券Chapter 9New York StockExchange纽约股票交易所cash dividend 现金股利(或红利、分红)closing price 收盘价Constant-Growth-RateDDM不变增长率股利折现模型current/existingstockholders现有股东、老股东discounted-dividendmodel(DDM)股利折现模型dividend policy 股利政策dividend yield 分利收益率ex-dividend price 除息(即股息)价格expected rate of return 期望收益率(或报酬率)infinite 无穷(或无限)的internal equity financing 内部权益融资Investment opportunity 投资机会market capitalization rate 市场资本化利率odd lots 零星(交易量)per se 亲自、亲身perpetual 永久的price/earnings ratio 市盈率Reinvested earnings 再投资收益required rate of return 必要报酬率(或收益率)risk-adjusted discountrate(经)风险调整折现率round lots 整批(交易量)share repurchase 股票回购skeptical 怀疑的stock dividend 股票股利stock splits 股票分割Chapter 10actuary 精算师caterer 酒席承办人colossal 巨大的、异常的confidence intervals 置信区间consortium 社团、合伙continuous probability distribution 连续概率分布diversification 分散化(投资)diversifying 分散化、多样化dunce 笨蛋、书呆子ex ante 事先的ex post 事后的expected rate of return 期望收益率(报酬率)flexibility 灵活性、柔性forward contract 远期合约hedger (套期)保值者、对冲者hedging 保值、对冲、对两方下注以防止(赌博、冒险等)的损失insuring 投保、给…保险jurisdiction 司法、权力、权限layoff 解雇、失业materialize 实现mean 均值normal distribution 正态分布overview 概述perverse 故意作对的、任性的portfolio 投资组合precautionary saving 预防性储蓄probability distribution 概率分布quadruple adj. 四倍的;v. 使…(增加)四倍recrimination 反责refund 退还risk assessment 风险评估risk aversion 风险规避risk avoidance 风险避免risk exposure 风险暴露risk identification 风险识别risk management 风险管理risk retention 风险保留risk transfer 风险转移sinful 有罪的、过错的、不道德的speculator 投机者square root 平方根stakeholder 利益相关者standard deviation 标准差swap 互换volatility 波动率Chapter 11American-type option 美式期权call option 买入期权(简称“买权”)cap (利率)上限condominium 公寓私有的共有方式co-payment 共同支付counterparty 交易对手credit guarantee 信用担保credit risk 信用风险deductible/deduction 免赔额delivery 交割delivery date 交割日derivative 衍生工具diversifiable risk 可分散的风险diversification principle 分散化(或多元化)原则European-type option 欧式期权exclusion 除外责任expiration date 到期日expire 到期face value 面值fictitious 虚构的firm-specific risk (公司)私有(或特有)风险forward contract 远期合约forward price 远期价格future contract 期货合约guarantee 保证、保证人、担保、担保品loan guarantee 债务保单long position 多头market risk 市场风险non-diversifiable risk 不可分散的风险premium 保险费、附加费、溢价proceed n. 盈利put option 卖出期权(简称“卖权”)rolling over 滚动(式)的short position 空头shortfall 不足之数、赤字spot price 即期价格standardized (经)标准化的strike price/ exerciseprice执行价格、行权价swap contract 互换合约、调期合约Chapter 12decision horizon 决策(修正)期限efficient portfolio 有效组合efficient portfolio frontier 有效组合前沿expected return 期望收益率mean-variance model 均值-方差模型minimum-varianceportfolio最小方差组合mutual fund 共同基金optimal combination ofrisky assets风险资产最优组合planning horizon 计划期、规划期point of tangency 切点portfolio selection (投资)组合选择risk premium 风险溢价risk tolerance 风险容忍(度)riskless asset 无风险资产risky-asset portfolio 风险资产组合set of……的集合tangency portfolio 切线组合target expected return 目标期望收益率trade-off 权衡、平衡trading horizon 交易(间隔)期限Chapter 13active investmentstrategies积极投资策略active portfolio selectionstrategy积极的组合选择策略Arbitrage Pricing Theory (APT)套利(定价)理论beat the market 打败市场benchmark 基准benchmark portfolio 基准组合Capital Asset PricingModel(CAPM)资本资产定价模型capital market line(CML)资本市场线consensus 一致、一致同意cost of capital 资本成本covariance 协方差equilibrium asset price 均衡(的)资产价格equilibrium expectedreturn均衡(的)期望收益率equilibrium price 均衡价格equilibrium risk premium 均衡风险溢价indexing 指数化irreducible 不能减少的、难复位的marginal contribution 边际贡献market portfolio 市场组合market-related risk 市场相关的(或承认的)风险multifactor IntertemporalCapital Asset PricingModel(ICAPM)多因子、跨期资本资产定价模型mutual fund 共同基金non-market risk 非市场风险passive investing 消极投资passive portfolio selectionstrategy消极的组合选择策略pension fund 养老基金regression coefficient 回归系数reward-to-risk ratio 风险补偿比率security market line(SML)证券市场线short-sale 卖空systematic risk 系统风险unsystematic risk 非系统风险Chapter 14arbitrageur 套利者bountiful 慷慨的、充足的casino 卡西诺赌场、小别墅closing out(one’s/a)position平仓continuouscompounding连续复利cost of carry 持有成本daily marking to market 逐日盯市(即每日无负债清算制度)delivery 交割delivery date 交割日delivery price 交割价格expectationshypothesis期望假说financial future 金融期货(即标的物为金融产品的期货合约)foreign-exchangeparity relation汇率平价关系forward contract 远期合约forward price 远期价格forward-spotprice-parity relation 远期-即期价格间的平价关系future contract 期货合约future price 期货价格future spot price 将来的现货价格hedger 套期保值者intrinsic value 内在价值margin 保证金open interest 未平仓合约数、头寸开放权益数position 头寸posting of margin (对)保证金(进行)过帐quasi-arbitrage 准套利(机会)replicate 复制speculator 投机者spoilage 损坏spot price 即期价格、现货价格spread 价差、差额the wall street journal 《华尔街日报》Chapter 15American-typeoption美式期权arrear 应付欠款、储备物at the money option 两平期权Black-Scholes model 布莱克-斯科尔斯期权定价模型boom 繁荣的bullish 乐观的call (option)买入期权(简称买权)、看涨期权capital-gain 资本(性)收益cash settlement 现金结算Chicago BoardOptions Exchange(CBOE)芝加哥期权交易所commission 佣金Contingent Claims 或有权益(简称或有权、或然权)credit guarantee 信用保证(或承诺)de facto 实际的、实际上decision tree 决策树delinquency 失职、违法行为dividend yield 股利收益率dividend-adjusted option formula 股利调整期权(定价)公式embedded option 嵌入式期权European put option 欧式卖权European-typeoption欧式期权evasion 逃避、躲避Exchange-traded option 场内(即在交易所交易的)期权exercise price/strikeprice执行价格/敲定价格expirationdate/maturity date到期日explicit 外生的flexibility 灵活性、柔性FutureOptions/Option onFutures期货期权growth option 增长期权guarantor 保证人hedge ratio 对冲比率、套期比率implicit 内生的implied volatility 隐含波动率in the money option 虚值期权incremental 增量的、增加的index option 指数期权intrinsicvalue/tangible value内在价值、执行价值junk bond 垃圾债券litigation 诉讼、争论mainline 主流的、传统的natural logarithm 自然对数normal distribution 正态分布Option 期权out of the moneyoption实值期权Over-the-counteroption场外(交易的)期权payoff diagrams 支付图plaintiff 起诉人provision 条文、条款put (option)卖出期权(简称卖权)、看跌期权put-call parityrelation买(权)与卖(权)间的平价关系real option 实物期权recession 衰退self-financinginvestment strategy自融资投资策略sequel 续篇、后果shortfall 不足之数、赤字stochastic 随机的 swap 互换 time value 时间价值 truncate截断two-state (binomial )option pricing model 两状态(二项式)期权定价模型 underlying asset 标的资产、基础资产Chapter 16account payable 应付账款accrued wage应计工资adjusted present value (APV )(经)调整的现值 after-tax incremental cash flow 税后增量现金流agency cost 代理成本 allegiance 忠诚、忠贞 all-equtiy financing 全权益融资 bankruptcy cost破产成本bankruptcy proceeding 破产程序、破产诉讼 Capital Structure资本结构capital structure irrelevance proposition 资本结构无关性定理 circumvent 绕过、智胜 collateral 担保品 common stock 普通股 corporate income tax公司所得税cost of financial distress 财务危机(危难)成本 debt financing 债务融资 entity实体、本质、存在 equity financing 权益融资 external financing外部融资(筹资) fiduciary受信托的 financial distress财务危机(危难) financing instrument 金融工具 franchise 特许权 free cash flow自由现金流 frictionless 无摩擦的gourmet供美食家的享用的、美食家imminent 临近的、迫在眉睫的 interest tax shield (债务)利息税盾 internal financing 内部融资(筹资) issuing new stock 发行新股leveraged investment 杠杆投资(即投资额中有部分债务融资) long-term lease 长期租赁 M & M proposition MM 定理market debt-to-equity ratio(用)市场(价值表示的)债务-权益比率market-value/economic balance sheet (用)市场价值(表示的)资产负债表 Modigliani & Miller (M 莫迪里阿尼和米勒& M )optimal capital structure 最优资本结构 pension liability 养老金(形式的)债务 perk额外补贴 personal income tax 个人所得税 preferred stock优先股学习必备欢迎下载prestige 威信、声望pro rata 按比例的realized capital gains 已实现资本收益redeploy 重新部署(布置、调派)repurchase stock 回购股票residual claim 剩余索取权(求偿权)retained earning 留存收益scrutiny 细致检查secured debt 安全债务stock option 股票期权subsidy 津贴、财政援助、特别津贴voting right 投票权warrant 认股权证、认股权weighted average costof capital(WACC)加权资本成本Chapter 17acquisition 收购bargain v. 讲价、讨价还价;n. 便宜货、交易、协定breakup 分散、中止、崩溃consolidation 合并、联合、巩固consummate 完成、使…完美contest 竞争、争夺corroborate 加强证实、巩固、支持discretion 决定权、谨慎、判断力divest 使…脱去information set 信息集loss carry-forward 亏损递延malevolence 恶意、坏影响merger 兼并opaqueness 不透明real option 实物期权spin-off 派生出、让产易股、抽资脱离synergy 协同增效takeover 接管。

THE NOTES ON INTERNATIONAL FINANCElec1

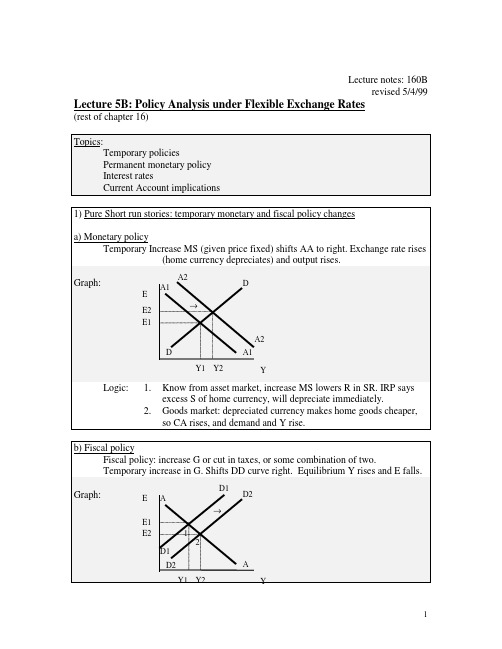

Lecture notes: 160Brevised 3/29/04 Lecture 1: National Income AccountsChapter 121) National income accountinga) Recall variables from closed economy macro classes:Y = Gross National Product (GNP), total value of all final goods and services produced by a country’s factors of production.“final goods and services”: because the price you pay for the dominos pizza includes the cost dominos paid for the flour, to count the four separately would be doublecounting“produced by a country’s factors”: so if a Ford factory in Mexico is owned by the US company, the profits go back to the US, reflecting the role that the US-ownedcapital played in producing the final output. (If count what produced within USborders regardless of ownership, is called GDP).C = consumption: Purchases by private sector for current wants. (includes durables,nondurables, and services)I = investment : part of current output used to increase in the capital stock and producemore output in futurenote the economic definition of investment is a little different from the common usage. If buy stocks and bonds, is saving not investment. When company you boughtstock from uses the money you gave them to buy capital, machinery to makemore output, this is called investment.G = government purchases: goods and services purchased by the public sectorexample: government buys tanks for a war. But government spending on welfare payments does not get counted here, because money is given to people whouse it for consumption, and it will be counted there.b) In a closed economy, what is relationship between these variables?Y=C+I +GWe defined the variables on the right here so this is true, we created subcategories of output because these parts of output tend to behave in different ways. Sincethis equation is true by definition, we call it an identity.The idea here is that in a closed economy each item produced is going to be utilized for something within the country. It will be consumed by private households orgovernment, or it will be classified as investment, to produce future output or beinventory used for consumption next period.Rearrange this as: Y – C – G = IOr: S = I, where S is total national saving.So the accounting identity tells us that in a closed economy, total saving must equal investment.c) In an open economyHow does this change in an open economy? Now goods can flow across national borders, so the goods produced within the US do not need to be utilized withinthe US.First, exports: Y = C + I + G + EXWhy: If Chrysler makes a car bought by a European, it is in our GNP, but no in domestic consumption, investment or government expenditure. Need list itseparately.Similarly for Imports: A Toyota made in Japan and bought by your cousin will appear in the US consumption, but it is not part of our national product, so it needs to besubtracted out. : Y = C + I + G + EX - IMRecall from last class that Exports less imports can roughly be referred to as the current account: CA = EX - IM, where this includes exports and imports ofmerchandise, factor services and other services. So the open economy identityis:Y = C + I + G + CAOr Y – C -G = I + CAS = I + CAIt no longer is true that saving must equal investment in an open economy. In fact this gives us a way to compute the current account, as the difference betweennational saving and investment.CA = S - I2) US current account deficit:b) What this means:If the current account is in deficit, how is the U.S. paying for its imports in excess of exports? It is selling off its assets, the wealth created by past production.Example: Suppose consumers in the U.S. purchase a million Toyotas from Japan and give Toyota in Japan dollars in exchange. Japanese will use some of thesedollars to buy Fords from the U.S., but suppose they only want half a millionFords. What will they do with the remaining dollars? They may use them topurchase real estate in the U.S. or U.S. government bonds which aregovernment IOUS. In a sense, the U.S. is borrowing from rest of world.This will be represented as a fall in the U.S. net foreign asset position, the value of foreign assets owned by U.S. citizens minus the value of U.S. assets owned byforeign citizens.The loss of net wealth may mean that there are future sacrifices to pay back the debt c) Evaluation:So is the fall in the U.S. CA and the resulting rise in U.S. indebtedness to the rest of the world a bad thing? Hard to say - depends on what is causing it.Reconsider the accounting identity:CA = S – I = Y – C – G - IPossible explanations for large U.S. CA deficit:1) Current account could be negative because consumption is high this year relative tooutput. This may be unwise if U.S. consumers don’t realize this comes at thecost of lower than usual consumption in the future when they pay back the debt.2) Or it could be because of investment spending is high. This could be sensible, sinceinvestment implies higher output in the future, which could be used to pay off thedebt then. Some say this is the story of Mexico when oil was discovered.Needed to import machinery to exploit the oil. Could have loweredconsumption a lot, but why? Borrow the money, and then pay it back lateronce receiving income from oil production. This was the idea in any case.3) The CA deficit could also be because of increased government expenditure. Candebate whether this is a good reason to run a deficit.Some economists have noted that the U.S. federal government has run significant budget deficits during this time, and they claim that the U.S. current accountdeficit has been caused by the government budget deficit. This theory is oftencalled the “Twin Deficits Hypothesis.”d) Understanding the “Twin Deficits Hypothesis”:We can rearrange accounting identity to get better insight into twin deficits claim: Y - C - I - G = CAintroduce taxes in a way that does not alter the validity of the equation:(Y-T) –C –I – (G-T) = CAor defineYd =Y-T: disposable income is what private sector has left after taxesthen rearrange:(Yd - C) + (T-G) - I = CAorSp + Sg - I = CA where we define private saving: Sp = Yd – Cand we define government saving: Sg = T - GorSp - def - I = CA where we define the government budget deficit: def = G – T Conclude: “All else constant,” a worsening budget deficit (def) will lead to a fall in the current account balance (CA). But note that the other variables in the equation,like private saving and investment, can also change and potentially cause currentaccount deficits as well.3) BOP (Balance of Payments) Accountinga) Accounting rulesDefinition of Balance of Payments: record of transactions with the rest of the world: buyand sell: goods, services, assets of various types. Keeps track both ofpayments to foreigners and receipts from foreigners.Rule 1: A transaction resulting in a payment to foreigners is recorded as a debit and isgiven a negative sign. Example: an American buys a Rolls Royce fromUK, then is a debit for U.S, negative sign.Any transaction resulting in a receipt from foreigners is entered as a credit and isgiven a positive sign. Example: British person buys a Chevy: is a creditfor U.S., positive sign.Rule 2: Transactions are divided into two types:If the transaction involves the export or import of goods or services, it entersdirectly into the current account (CA). Example: British person buys aChevrolet truck, then is a credit in U.S. current account.If the transaction involves the purchase or sale of assets, it instead enters financialaccount (FA). An asset is any form in which wealth can be held, suchas money, stocks, factories, government bonds, land, etc.If British person buys stock in Chevrolet motor company, then is a credit inU.S. capital account (asset, not the product)Rule 3: Every international transaction automatically enters the BOP accounts twice:once as a credit and once as a debit.Example: If U.S. person buys a Rolls Royce, paying dollars to seller in U.K. This isa debit in U.S. current account.The British person then must do something with the dollarsa) buy a Chevy with them: is a credit in current accountb) buys stock in U.S. company: is a credit in financial accountc) holds on to U.S. cash - is a U.S. asset, so is a credit in financialaccountSince every transaction gives rise to two offsetting entries in the balance of payments, acurrent account debit will necessarily be offset by a credit, either incurrent account or in financial account.So we know that if we add up the CA and FA, we will get zero:Current Account + Financial Account = 0Note: in some accounting schemes an additional category, the “capital account”, isalso included in this identity. This category is extremely small for theU.S. and just is used to cover some technical transactions relating tochanges in ownership of assets. So we will abstract from this accountingcategory in this course. Sometimes I may lump just these two assetaccounts together as the “capital and financial account.”Recall that the current account is how much more are spending than producing, orsaving minus investment.If you are spending more than producing, say have a current account deficit, whichmust finance this somehow.We could sell assets in our country to pay for the goods we want. This wouldgenerate a financial account credit to balance the current account deficit.Or we could issue debt which sell to foreigners, another way of borrowing, and alsowould be a financial account credit. Can refer to this as a “financialinflow” (also sometimes called a “capital inflow”) to finance the currentaccount deficit.b) Current accountNow we give more detail about how to compute each account.Three categories:1.Exports - credit2.Imports - debit3.TransfersExports and imports each divided into three categories:1.merchandise: export and import of goods, like Chevys and Rolls Royces2.services: legal assistance, shipping fees, tourism3.investment income: interest and dividend payments and earnings of domesticallyowned firms operating abroad.One additional category in CA: net unilateral transfers. Defined: international gifts, needto account for corresponding entry in BOPc) Financial accountRecall that this account measures the change in net holdings of foreign assets.Break down into:1) change in U.S. ownership of assets located abroad (increase is a debit, acapital outflow), and2) change in foreign ownership of assets located in U.S. (increase is a credit, acapital inflow)Each category includes assets that are official reserve assetsCentral banks hold foreign assets. They buy and sell them as a way of influencingthe financial markets.The “official settlements balance” is defined as the sum of the Current account, thestatistical discrepancy, and the part of the financial account excludingthe official reserve transactions. It thus indicates how much of a gap wasleft in the balance of payments after private transactions were made,and how much the central banks had to intervene to fill in this gap.In 1994 financial account was in surplus $188.9 billion.Means U.S. net wealth fell by 188.9. This helped finance current account deficit- isa financial inflow.But notice there is a statistical discrepancy. The two accounts do not exactly cancel.This is due to error in collecting statistics. Much of problem lies with thefinancial account – it is harder to keep track of the many, complicatedfinancial transactions.。

国际金融课件internationalfinance

06

中国国际金融的实践与展望

中国国际金融业在规模和业务范围上不断扩大,成为全球金融市场的重要参与者。

中国国际金融业在推动经济增长、促进国际贸易和投资等方面发挥了重要作用。

改革开放以来,中国国际金融业经历了从无到有、从小到大的发展历程,逐步建立起较为完善的金融机构体系和金融市场体系。

中国国际金融的发展历程与现状

Global financial markets facilitate the flow of capital across borders, allowing for the efficient allocation of resources and the hedging of risks.

Regional financial markets serve specific geographical regions and are often associated with trade blocs or economic unions.

01

国际金融危机的定义

由于国际金融市场上的过度投机、金融监管缺失等原因,导致国际金融市场出现大规模动荡,影响各国经济的稳定。

02

国际金融危机的传染机制

通过贸易、金融和信息等渠道,将危机从一个国家传递到另一个国家。

国际金融危机及其传染机制

1

2

3

通过监测和分析国际金融市场的相关信息,及时发现潜在的风险点,采取应对措施。

02

03

04

05

Main International Financial Centers and Their Characteristics 主要国际金融中心及其特点

ห้องสมุดไป่ตู้

国际财政THE NOTES ON INTERNATIONAL FINANCEfinal01

Final Exam: Economics 160B, Spring 2001You will have 120 minutes to complete this exam. It is divided into 115 points. Unless stated otherwise, assume the following: exchange rates are flexible, investment is exogenous, consumption is just a function of disposable income, and there is no risk premium in foreign exchange markets. Multiple Choice: (3 points each, 30 point total) Choose the best answer. Write answer on scantron.1) Which of the following could explain why the valueof the dollar currently is high relative to the yen:a)higher money supply growth in the U.S.b) higher income growth U.S. that is affectingmoney demand.c) a shift in tastes toward Japanese goods that hasaffected the real exchange rated) higher inflation rate in the U.S.2)Which of the following could lead to a currencycrisis in a country with a fixed exchange rate.a) a large current account deficit.b)expansionary fiscal policy.c)expansionary monetary policy.d)all of the above.3)According to the “Twin Deficits Hypothesis”, theupcoming U.S. tax cut should:a)worsen the current account deficitb)help balance the current account.c) have no effect on the current account deficit.d) worsen the current account but improve thetrade balance.4) If Mexico commits to fixing its exchange rate tothe dollar at a higher level (peso/dollar) thanwould be obtained had the rate been allowed tofloat freely, what will happen to the supply ofMexican currency in circulation and the holdingsof foreign reserves at the Mexican central bank?a)Currency in circulation rises and reserves fall.b)Currency in circulation rises and reserves rise.c)Currency in circulation falls and reserves fall.d)Currency in circulation falls and reserves rise.5) Purchasing Power Parity is more likely to hold inwhat context?a) Countries that consume very different typesof goods.b) Countries with large tariffs.c) Countries where the exchange rates are fixed.d) None of the above.6) If an American citizen receives earnings on hisshares of the Japanese company Sony, and usesthis to import a car from Germany, what will bethe net effect on the U.S. balance of paymentsaccounts:a) net increase in the current account and netdecrease in the capital account.b) net decrease in current account and the capitalaccount.c) net increase in the current account and netdecrease in the capital accountd) none of the above.7)A Gold Standard system of fixed exchange rates:a) requires only one country to hold gold reserves.b)was abandoned in 1973 by the industrializedcountriesc)is good at maintaining external balance.d)both a and b.8)All of the following contributed to the Asianfinancial crisis of 1997 except:a)Poor bank regulation.b)Contagion across countries.c)Excessive capital controlsd)IMF aid packages9) Which of the following is true about a currencyboard:a)it must hold sufficient reserves to back 100% ofthe domestic money base.b)It can hold no domestic assets.c)Unlike dollarization, it retains control overseigniorage revenue.d)Both a and b.10) The Latin American debt crisis of the mid-1980sa)slowed the GNP growth of the indebtedcountriesb)was triggered by the realization that the oilproducing nations of OPEC were in noposition to repay the loans they had taken outto pay for oil extracting capital equipment.c) was fully solved by IMF aid packagesd) was worsened by the Brady plan of debtforgiveness.Problem 1: Parity Conditions (20 points)Suppose that covered, uncovered and real interest rate parity conditions all hold, and you have the following information:- The interest rate on 1-year yen deposits is 2%.- Inflation is expected to be 2 percentage points higher in Europe than Japan during the next year.- The current nominal exchange rate is 100 yen/euro.- The forward exchange rate for one year from now is 95 yen/euro.Using this information, compute the following. Show your work in each case and name whichparity conditions you are using.a) The expected nominal exchange rate one year from now (yen/euro).b) The European nominal interest rate.c) The expected percentage change in the real exchange rate over the next year (Japanesegood/European good).Does your answer to ( c) above mean that Japanese goods are becoming more expensive in terms of European goods or less expensive?Problem 2: Temporary Shocks and Policies: (20 points)Consider Argentina, which has fixed exchange rate relative to the dollar using a currency board. Use the AA-DD-XX graph to illustrate each of the following scenarios. Be sure to label the axes and curves, and mark the equilibrium points and curve shifts. For each of the shocks state what happens to the following variables (rise, fall, no change, ambiguous): output, current account, consumption, money supply, and official foreign reserves.a) temporary rise in money demandb) temporary tax increasec) temporary terms of trade shock, in which world demand for Argentinian goods falls.Based on your graphs above, discuss the contrasts in how well fixed exchange rate regimes can deal with shocks, depending on whether they arise from the money market or the goods market. Problem 3: Permanent Monetary Policy (20 points)Suppose there is a permanent increase in Japanese money supply.a)Using the AA-DD graph, show a case where this would not lead to exchange rate overshooting. Besure to label the axes and curves, mark the initial equilibrium as 1, the short run equilibrium as 2 and the long run equilibrium as 3.b) What is the effect in the short run on the following Japanese variables: output, exchange rate(yen/dollar), and the interest rate (rise, fall, no change, ambiguous)?c) Suppose a case where the money demand function were more responsive to changes in income (achange in income affects money demand more). How would this affect your answer to part (b)above: for each variable, state if it moves more, less, the same, or it is ambiguous. Would this case be more likely or less likely to generate exchange rate overshooting?Problem 4: (25 points) Answer one of the following two questions (A or B) in three or four paragraphs.A) Capital Mobility and Developing Countries:List and explain the various benefits and costs of allowing capital mobility in the international capital market. Make an argument for how these costs and benefits apply to the case of typical developing countries, and whether these countries should allow capital mobility or should restrict capital flows. B) Optimal Currency Areas and AsiaList and explain the criteria for an optimal currency area. Some economists have proposed a currency union for the East Asian economies. Given the features of the newly developed East Asian economies given in class, discuss how the optimal currency area criteria would apply.6/13/01。

国际财政THE NOTES ON INTERNATIONAL FINANCE midsol1160

Midterm 1 Solution KeyEconomics 160B (spring 2004)Regrade policy: If you would like your test regraded, please submit a written statement to explain why. Your entire test will be regraded, so there is a possibility that points could be lost not gained. Multiple Choices:1) a 2) e 3) c 4) b 5) d 6) a 7) d 8) c 9) b 10) cProblem 1: Exchange Rate Overshootinga) Short run analysisE W/Y Won returnsR01)/ E W/Y)/ E W/YM S KoBecause prices are fixed, the decrease in Korean nominal money supply lowers real money supply (M S1Ko/P0Ko <M S0Ko/P0Ko), and this makes the Korean interest rate rise in the short run to clear the money market. In the foreign exchange market, this shifts the won returns curve right. In addition, the expectation that in the long run the Korean price level will fall and the value of the won will rise relative to its starting point means that yen returns curve shifts left (expected yen returns are lower for any given spot exchange rate). Together these move the equilibrium point in the foreign exchange market from point 0 to point 1. In summary, thismeans that the current spot exchange rate (E w/y) falls, and the won interest rate is higher.b) Long run analysis:In the long run, the Korean price level P K falls in proportion to the money supply and clears the money market. So the interest rate returns to its original level and shifts the won returns curve back. The equilibrium in the foreign exchange market moves from point 1 to point 2. According to the monetary approach, which we take to hold here in the long run, the value of the Korean won appreciates in the long run in proportion to the price level, by 10 percent, relative to its value before the money supply change. This is less of an appreciation than in the short run.)/ E W/Y )/ E W/Yc) Yes. Exchange rate goes beyond its long-run value in the short-run.If the price level were fully flexible, we would move immediately to the long run solution above. So there would be no movement in the interest rate, and exchange rate would move 10% in the short run and stay there. So there would be no overshooting.Y W EE 0E 3E 2timeProblem 2: Interest Rate Parity and Purchasing Power Paritiesa) CIP: R P = R R + (F P/R – E P/R )/ E P/R = 0.07 + (3.3 - 3)/3 = 0.07 + 0.10 = 0.17b) Combining UIP & CIP says: E e P/R = F P/R = 3.3c) Relative PPP: Πe Mex - Πe Brazil = (E e P/R – E P/R )/ E P/R = (3.3 - 3)/3 = 0.10Inflation is expected to be 10% higher in Mexico.d) Combining UIP and relative PPP:R P - R R = (E e P/R – E P/R )/ E P/R = Πe Mex - Πe BrazilM S Ko E W/Y Won returns R 0W 1So R P - Πe Mex = R R - Πe BrazilUsing the definition of the real exchange rate (r e Mex = R P - Πe Mex): r e Mex = r e Brazil.But we only have information on the relative inflation between countries, not on their individual levels. So we can only conclude that the real interest rates are equal across the countries. We do not have enough information here to compute the real interest rate in Mexico individually.Discussion:Rearranging the national income accounting identity: Y = C + I + G + CAintroduce taxes: Y - T = C + I + G -T + CAthen rearrange: (Y -T - C) - (G - T) - I = CAor Sp - def - I = CA where Sp is private saving and def is the government budget deficit.The twin deficits hypothesis suggests that government budget deficits cause current account deficits. The equation above indicates that there indeed is a relationship between the two: a rise in def would tend to lower CA, if private saving and investment are constant. However, private saving or investment can move around, perhaps even in response to the rising budget deficit. So the twin deficits hypothesis does not necessarily hold.The hypothesis did seem be a useful explanation for the large U.S. current account deficit in the 1980s, when there was a large government budget deficit. But it does not seem to offer much explanation for the current account deficit in the 1990s and today, since thegovernment budget was balanced during part of this time. Instead it seems that a fallingprivate saving level has caused most of the current account deficit.(4/26/04)。

国际财政THE NOTES ON INTERNATIONAL FINANCE lec9b

Lecture notes: 160Brevised 5/17/04Lecture 9: European Monetary Arrangements(chapter 20)Topics:European Monetary SystemCrisisEMSEuropean Monetary UnionEuropean Central Bank1) European Monetary System (EMS)After Bretton Woods Break up, several European countries attempt various mechanisms to fix their exchange rates to each other.a) MechanicsIn 1979, eight European countries created a formal system of mutually fixed exchange rates, called the European Monetary system (EMS). The fixedtheir exchange rates relative to each other, floating jointly against thedollar.The bilateral exchange rates were not held exactly fixed. They were allowed to fluctuate within bands of an assigned par value with each of the othercurrencies. Called margins.Set like this: each currency has a central parity in terms of ECUs - European currency units, basket of member currencies. Can use central parities todetermine what bilateral central rates are. When first set up, each bilateralrate was only allowed to deviate from this by 2.25% above or below.If the French franc depreciates to its lower limit relative to the DM, it is obligated to sell DM reserves to make Franc appreciate. German centralbank is obligated to loan DM to France.If pressures of misallignment are strong and seems that a country can’t defend the set exchange rate, there are provisions for currencies to be reallignedif necessary.Initially had capital controls that limited the ability of private citizens to trade in foreign currencies. Prevent speculators from starting a currency crisis.These restrictions were relaxed in 1987 .Initially, the system worked better than most expected, and more countries joined along way.b) German Dominance:Was designed to be symmetric, but evolved so Germany had dominantposition.Germany had reputation for low inflation. Hyperinflation in inter-war years lead to fear of inflation. When created Bundesbank (German central bank)its primary goal was said to be to keep inflation low and keep value of DMhigh.Other countries wanted to import Germany’s reputation for low inflation. So they willingly used DM as their main reserve currency, and let theirmonetary policy mimic what Germany was doing. Evolved so that lookedlike Bretton Woods system, where Germany was the central country notUS.Lead to problems when Germany put its domestic interests ahead of itsinternational role, as Bretton Woods got into trouble when U.S. pursuedpolicy of the 1960s. Led to currency crisis in fall of 1992, which almostwrecked EMS.Pressure on the Lira caused it to devalue in September 11 1992. So speculators made profit, and showed them that EMS could indeed be cracked.September 16, Black Wednesday. Continued pressure for Lira to be devalued more and pressure on UK, costly draining of reserves. Ended up takingLira and Pound out of the EMS system, and allowed currencies to float.France also attacked, but managed to hang on. Many other currencies hadto be devalued: Spanish peseta, Irish punt, Portuguese Escuda Even for those still in system, bands were widened very much, from 2.25% to 15%. Not clear that was restricting very much. But E seem to have settleddown again for the most part at their new levels.This is referred to as a “Second Generation” type of currency crisis” .Although a country has enough foreign exchange reserves to be able todefend the peg, a crisis and devaluation occur nevertheless, becausedefending the currency peg is costly in terms of domestic monetary policyobjectives. Raising the interest rate causes a recession.c) Aftermath:Question if France was the unlucky/unwise one. France continued inrecession with very high unemployment.But UK and Italy did better. In part due to depreciated exchange rate made their goods more competitive, so CA improved. Lira dropped in valuealmost 50%, CA went from neg (over previous 10 years from 1992) to posin 1993. Also true for UK, Sweden and Ireland. Helped most of thesecountries to have improved output levels in 1993.Note that this came at cost of their European trading partners, especially France, which kept currency high and goods uncompetitively priced.Output fell much in France and unemployment rose. Are accounts offirms that closed up shop in France and moved across English channel touse cheaper British Labor. Worsened unemployment in France.Led to calls for protection, and threatened to undermine free trade agreements within the EU.Example of “beggar-thy-neighbor policy”3) European Monetary Uniona) IntroductionOn January 1 2002, 12 European countries finalized their monetary union. This meant that they had a common central bank in Frankfurt in Germany, atwhich all 12 countries had to agree on a common monetary policy.Why did these countries take this step. We look below at the various costs and benefits of a monetary union (also called a currency union.)b. Theory: Gains from monetary union.Lower uncertainty and transaction costs of cross-border tradeTransaction costs of exchanging currency. Imagine if every time someone bought agricultural products from California, they had to convert to dollarsfrom California pesos.Uncertainty is even a bigger issue. Example: if electronics store, risky to order shipment of Japanese TVs if not sure what the $ price will be when theyare delivered.Investment: Even worse for making long-term investment, where payoff is far in future. Not like uncertainty.(Same as for fixed rates)Note: size of all these gains depend on extent of trade.Another issue Is irrevocable.In EMS, as long as there is some chance E parities can be realligned, invites speculative attacks to undermine the system.The way to maintain fixed e is by selling reserves of foreign currencies and buying own currency from anyone who wishes to sell it at the official rate.If run out of reserves, must give up and let value of currency fall.So speculators can make money: borrow bunch of FF, go to central bank and sell for large # DM (FF overvalued), when reserves of DM depleted, bankallows value of FF to fall, then sell back your DM for large number of FF.Repay loan and have profit.Eliminate this possibility if is only one currency.c. Theory: Costs of monetary union:Main cost is cant use independent monetary policy (as with fixed exchange rate regime). But lets see how costly this cost is? - what depends on.Consider a recession in Spain alone: high unemployment and falling output.Previously Spain could use its monetary policy: increase money supply tolower interest rates, cheaper to borrow to buy car or build new factories, sostimulate demand for investment projects and consumption. This increaseddemand causes factories to produce more and hire more workers. So raiseGDP and lower unemploymentBut now Spain cant do this on own. ECB decides on common monetary policy to suit diverse interests of all the EU 11.Are some features that determine size of this cost:1) Symmetry of shocks: If rest of EMU countries all experiencing same shock- fall in tastes for all European goods. In that case, monetary union as awhole could increase money supply to restore full-employment output.But suppose Spain is the only one. Then stuck. This is a question of howasymmetric the shock is. If is asymmetric, hits one country more thanothers, so would want to use a country-specific policy if could.Shocks will tend to more symmetric if the national economies are moresimilar, producing same sorts of things in similar ways.2) Integrated factors markets: If unemployed workers in Spain can move toDenmark if there are more jobs there, then this helps alleviate stress ofasymmetric shocks.3) Fiscal Federalism: Also if there is a mechanism whereby if Spain is hurt bya shock, income would be transferred from Denmark to Spain tocompensate for lost welfare of higher unemployment. Example would bea federal system of taxation and welfare payments. Collect more taxesfrom where income is higher and pay more to where income is lower,similar economies.Seems that costs are low and benefits high if economies are highly integrated: high level of trade in goods, flow of labor, integrated fiscal administration.If these things true, say is an optimal currency area: costs are lower thangains.d) Evidence We can compare to U.S., which is a functioning common currency area?1) Extent of trade: If trade more, the gains of lower transaction costs will be big.Most European countries trade 10-20 percent of their GDP with otherEuropean countries. This is larger than trade between Europe and the US.But not as large as trade between regions within the US.However, there is a trend of increasing trade between European.2) Symmetry of Shocks:Studies have tended to find that shocks are more asymmetric in Europe.Partly due to fact that Northern Europe tends to produce more goods thatrequire capital and skilled labor than do southern European countries.Right now, Ireland is in boom, and France OK, but Germany on verge of recession. Output fell last quarter; one more and will be recession.But can also see some asymmetric shocks in US. Consider Recession in 1990-91. Hit Californian harder and longer than most of rest of country, becausewas partly due to cutback in defense spending, and many defensecontractors were based in California.3) Integration of Labor markets:Labor mobility is low in Europe, despite fact that have removed passport checks within Europe. Main reason is that countries have distinct cultures,making people less willing to relocate to find employment.Further, even within each European country there is less mobility than in the US. One study showed that in 1986 3% of US citizens changed state ofresidency, while in Germany only 1.1% changed from one German regionto another German region; Italy was 0.6%Labor mobility is an important means for US regions to adjust to asymmetric shocks. When California went through bigger recession, there wasoutflow of migration, say to Oregon and Washington whereunemployment was lower.Federalism:Fiscal4)Not highly developed in Europe - individual governments have not given up their separate authority over taxing and spending.Is highly developed fiscal federal system in US - national income tax and welfare system. This transfers much income to areas hit by asymmetricshock. For example, for every dollar California lost in income relative torest of country, 25 cents less was paid to the federal government, and 10cents more was received from the federal government. So offset perhaps35 percent of an asymmetric output shock.Conclusion: not optimal cur area: costs > benefits. So why move forward?e) Political benefits of EMU:1) Joint decision making Non-German countries want: In EMS, Germany isthe leader in deciding monetary policy, and other countries are followers.But if have one common central bank deciding monetary policy, Germanswill just be one among many members, others will also have a voice indeciding policy.What then is in it for Germany - why join?2) Next step toward political Integration: Seen as a necessary step towardpolitical integration, allowing more influence in international affairs.Something Germany has a hard time doing now because of its history.3) Prevent political opposition to free trade. Are large gains to free trade ingoods. If allow fluctuations in exchange rate to hurt export sectors on onecountry or another, will be an organized political force to demandprotectionism and undo free trade in goods. Recall outcry after UK andItaly leave EMS.Raises question of whether US is really an optimal currency area. Havemechanisms to help deal with asymmetric shocks, like California recessionin early 1990s.But wonder if California would have been better of if had had own currency.Could have used monetary policy to make California Peso depreciate -- California goods cheaper, improve California CA component of AD, raiseCalifornia output level toward full employment.4. European Central Banka) ECB design:ECB based in Frankfurt. Similar in some ways to Federal Reserve andbundesbank. Monetary policy decided by governing council, withrepresentatives from each member country.Designed to keep inflation low.Theory: if increase money supply, may lower unemployment in the short run, but will increase inflation in long run. More money chasing after samenumber of goods, bids up the price.There are natural tendencies to make politicians vote for too much money increase, because low unemployment increases votes. So tend to get toomuch inflationInflation is disliked, because makes it generates uncertainty, similar to changes in exchange rate. Don’t know how much nominal payment is worth in realterms.At time ECB charter written, most governments in Europe were conservative and thought it more important to keep inflation low than worry aboutunemployment. Especially disliked in Germany because of history. Soargued for design features to help ECB keep inflation low and not worryabout unemployment.features:Design1) ECB charter states that inflation is primary objective.2)Independence:Reps on governinc council prohibited from taking instructions fromgovernments.President has 8 year term. Immune from politics. (story about Duisenberg).3) Stability pact:deficits low: below 3%. Another reason tend to increase money Keepsupply, because use it to pay bills rather than taxes.Now that system is in place, some governments regret design. Governments now liberal, and place higher priority on unemployment. Germany in particularhas bad economy and is pressuring Duisenberg to incrrease money supply.Trying to find ways to pressure him. Unclear whether design will stand upto pressure.b) Current events:c) Implications for USEuropean economy little more efficient (good thing). Will be able to sell us cheaper goods, and be richer and buy more of our goods.Easier for our firms to conduct business there.Euro compete with dollar as an international reserve asset. Currently dollar is 60% of foreign reserves (European currencies only 1/4 of that). We get benefitbecause people want to hold US dollar. Euro may get some of thisbusiness.11。

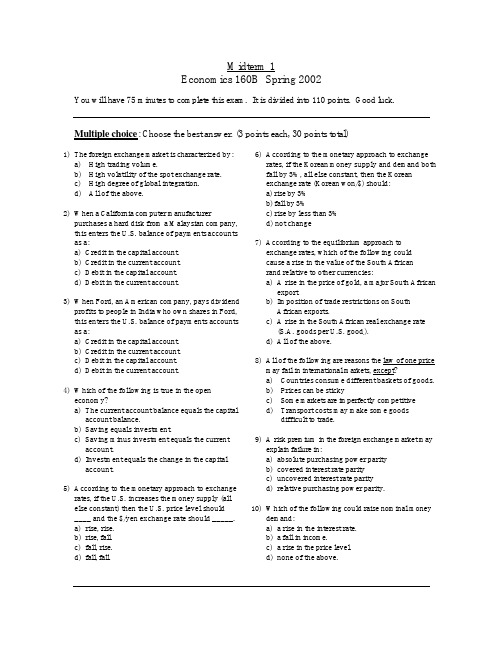

国际财政THE NOTES ON INTERNATIONAL FINANCE midterm102a

Midterm 1Economics 160B Spring 2002You will have 75 minutes to complete this exam. It is divided into 110 points. Good luck. Multiple choice: Choose the best answer. (3 points each, 30 points total)1) The foreign exchange market is characterized by:a)High trading volume.b)High volatility of the spot exchange rate.c)High degree of global integration.d)All of the above.2) When a California computer manufacturerpurchases a hard disk from a Malaysian company, this enters the U.S. balance of payments accounts as a:a)Credit in the capital account.b)Credit in the current account.c)Debit in the capital account.d)Debit in the current account.3) When Ford, an American company, pays dividendprofits to people in India who own shares in Ford, this enters the U.S. balance of payments accounts as a:a) Credit in the capital account.b) Credit in the current account.c) Debit in the capital account.d) Debit in the current account.4) Which of the following is true in the openeconomy?a)The current account balance equals the capitalaccount balance.b) Saving equals investment.c) Saving minus investment equals the currentaccount.d) Investment equals the change in the capitalaccount.5) According to the monetary approach to exchangerates, if the U.S. increases the money supply (allelse constant) then the U.S. price level should____ and the $/yen exchange rate should _____.a)rise, rise.b)rise, fall.c)fall, rise.d)fall, fall.6) According to the monetary approach to exchangerates, if the Korean money supply and demand both fall by 3%, all else constant, then the Koreanexchange rate (Korean won/$) should:a) rise by 3%b) fall by 3%c) rise by less than 3%d) not change7) According to the equilibrium approach toexchange rates, which of the following couldcause a rise in the value of the South Africanrand relative to other currencies:a) A rise in the price of gold, a major South Africanexport.b) Imposition of trade restrictions on SouthAfrican exports.c) A rise in the South African real exchange rate(S.A. goods per U.S. good.).d) All of the above.8) All of the following are reasons the law of one pricemay fail in international markets, except?a)Countries consume different baskets of goods.b)Prices can be stickyc)Some markets are imperfectly competitived)Transport costs may make some goodsdifficult to trade.9) A risk premium in the foreign exchange market mayexplain failure in:a) absolute purchasing power parityb) covered interest rate parityc) uncovered interest rate parityd) relative purchasing power parity.10) Which of the following could raise nominal moneydemand:a) a rise in the interest rate.b) a fall in income.c) a rise in the price level.d) none of the above.Problem 1: National Income and Balance of Payments Accounts(20 points total, 10 points each part)Suppose that you have the following information on the values of some Japanese economic variables for last year, in trillions of yen.Exports = 16 Budget Deficit = 4 GNP = 100Investment = 22 Capital Account = -2 Taxes = 20Both the Official Settlements Balance and the Statistical Discrepancy are zero.a) Compute the current account balance and private saving.b) Explain the “Twin Deficits Hypothesis” and discuss how well it applies in this case.Problem 2: Interest Rate Parity and PPP Conditions (30 points total, 6 points each) Suppose that the following conditions all hold: uncovered and covered interest rate parity, relativeand absolute purchasing power parity. And suppose you have the following information:- The interest rate on 1-year U.S. dollar deposits is 2%.- Inflation is expected to be 5 percentage points higher in Mexico than the U.S. during the next year. - The Mexican government has promised to keep the Mexican real interest rate at a level of zero.For each of the following, compute a value using the information above, or state if there is not enough information given above to do this. Show your work in each case and name which parity conditions you are using.a) The U.S. real interest rateb) The Mexican nominal interest ratec) The real exchange rated) The percentage expected change in the spot exchange rate over the next year. Is the pesoexpected to rise in value or fall?e) The level of the forward exchange rate for delivery of pesos one year from now(dollars/peso).Problem 3: Exchange Rate Overshooting (30 points total, 10 points each part)Suppose that the introduction of debit cards leads to a permanent fall in money demand in the U.S. Consider the effects this might have on the value of the dollar relative to the Japanese yen in the foreign exchange market. (Assume unless told otherwise that prices are fixed in the short run, output isexogenous, uncovered interest rate parity holds, and there is no change in the conditions of the Japanese domestic money market.)a)Show graphs of what happens in the U.S. domestic money market and foreign exchangemarket in the short run. (Label all curves and show with arrows in the graph how curves shift). State what direction the following U.S. variables move in the short run:- the current nominal spot exchange rate (U.S. dollar per yen),- the nominal U.S. interest rate, and- the real exchange rate (US goods per Japanese good).b)Now anal yze the long-run effects. Again show a graph as above, and state what happens tothe following variables: nominal exchange rate, nominal U.S. interest rate, and real exchange rate. (Note: state whether variables are higher or lower than before the change in monetary policy, and be as specific as possible about the magnitudes).c)Does the nominal exchange rate overshoot here? Explain why or why not.Discuss how this theory may or may not help you accurately predict movements of theexchange ahead of time, and how this may or may not help you make a profit by strategic investments in the foreign exchange market.4/24/02。

国际财政THE NOTES ON INTERNATIONAL FINANCE hw1160