IRS_FATCA_Summary of Key FATCA Provisions

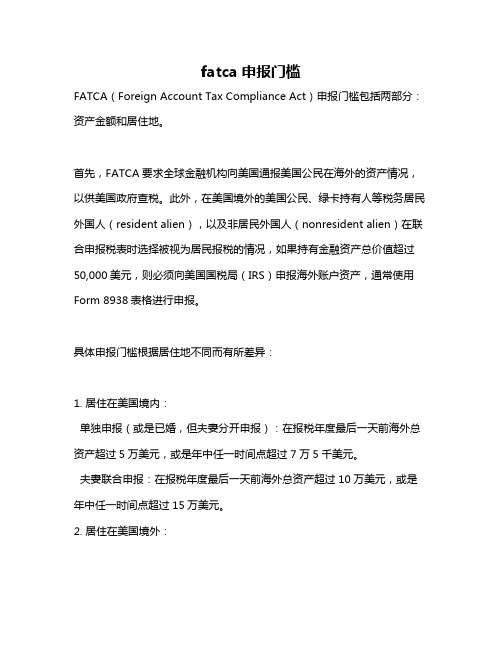

fatca申报门槛

fatca申报门槛

FATCA(Foreign Account Tax Compliance Act)申报门槛包括两部分:资产金额和居住地。

首先,FATCA要求全球金融机构向美国通报美国公民在海外的资产情况,以供美国政府查税。

此外,在美国境外的美国公民、绿卡持有人等税务居民外国人(resident alien),以及非居民外国人(nonresident alien)在联合申报税表时选择被视为居民报税的情况,如果持有金融资产总价值超过50,000美元,则必须向美国国税局(IRS)申报海外账户资产,通常使用Form 8938表格进行申报。

具体申报门槛根据居住地不同而有所差异:

1. 居住在美国境内:

单独申报(或是已婚,但夫妻分开申报):在报税年度最后一天前海外总资产超过5万美元,或是年中任一时间点超过7万5千美元。

夫妻联合申报:在报税年度最后一天前海外总资产超过10万美元,或是年中任一时间点超过15万美元。

2. 居住在美国境外:

单独申报:在报税年度最后一天前海外总资产超过20万美元,或是年中任一时间点超过30万美元。

夫妻联合申报:在报税年度最后一天前海外总资产超过40万美元,或是年中任一时间点超过60万美元。

需要注意的是,如果当年不需要申报个人所得税,即使海外资产价值超过申报门槛,也无需申报Form 8938表格。

美国《海外账户纳税法案》(FATCA)对持有绿卡的中国公民以及中国金融机构的影响

Things turn out best for the people who make the best of the way things turn out. John Wooden美国《海外账户纳税法案》(FATCA)对持有绿卡的中国公民以及中国金融机构的影响美国于2010年3月18日通过了《海外账户纳税法案》(Foreign Account Tax Compliance Act,以下简称“FATCA”)。

FATCA主要目的在于加强对美国人(包括美国公民和绿卡持有者1)的海外投资的税收征管,防止美国人通过海外账户逃避纳税。

其中,一百万美元以上的个人账户、外资企业将成为美国政府重点关注对象。

FATCA要求协议合作的外国金融机构(Foreign Financial Institutions,以下简称“FFIs”)提供美国人个人账户信息或其所拥有的境外实体的账户信息。

FATCA实施后,美国以外地区拥有高额资产的美国人很可能需要缴纳大额税金;就金融机构而言,根据相关机构的预测,FATCA将使其增加大约3000万美元的合规成本。

FATCA原计划于2013年1月1日正式生效,然而美国财政部及美国国税局(Internal Revenue Service,以下简称“IRS”)分别于2012年10月26日及2013年7月12日宣布推迟FATCA的生效日期,现定于2014年7月1日正式施行。

截至2013年7月12日,美国已与英国、丹麦、墨西哥、爱尔兰、瑞士、挪威、西班、德国和日本九个政府之间签署协议,支持FATCA施行,另与近百个国家和地区正处洽谈之中。

根据外交部官方网站2公布的《第五轮中美战略与经济对话框架下经济对话联合成果情况说明》,“中美双方承诺尽最大努力在法定截止期2014年1月前就FATCA的实施达成政府间协议。

为寻求FATCA实施的合作方案,美国财政部、IRS、中国财政部、税务总局和中国人民银行承诺在2013年夏天尽早开展下一轮讨论。

FATCA(海外账户纳税法案)对中国金融机构的影响_发出版本_20150325_CL

Things turn out best for the people who make the best of the way things turn out. John Wooden《美国〈海外账户纳税法案〉(FATCA)与中国》之三FATCA(海外账户纳税法案)对中国金融机构的影响2015年3月25日随着中国政府与美国政府就FATCA实质性达成一致,中国金融机构将不可避免地受到FATCA的影响,我们将在下文简要分析FATCA对中国金融机构的影响。

一、FATCA对中国金融机构的主要影响对中国金融机构而言,最大的风险是可能被扣缴30%预提税,即如果中国金融机构未取得全球中介机构识别号码(Global Intermediary Identification Number,以下简称“GIIN”),当支付方把来源于美国的款项支付给中国金融机构时则应该扣缴该款项30%的预提税。

美国国税局开发了专门的网上注册系统。

外国金融机构在线注册后即可拿到GIIN。

获得GIIN参加FATCA的外国金融机构有如下主要义务:(1)判断在其开设的账户是否为美国账户;(2)对于账户持有人进行尽职调查,鉴别其是否为美国人;(3)每年向IRS汇报在其设立的美国账户的信息。

关于向美国政府汇报美国账户信息的义务,按照中美的政府间协议,中国金融机构不直接向IRS汇报美国账户信息,而是通过中国政府间接向IRS汇报美国账户信息。

参加FATCA的中国金融机构也负有其他义务。

其中,比较重要的一个义务是把来源于美国的款项支付给非合作账户(recalcitrant account)、未参加FATCA的外国金融机构等时,应该代为扣缴30%预提税。

二、中国金融机构的首要对策中国金融机构首先需确认本机构是否属于FATCA下的“外国金融机构”。

FATCA中所提及“外国金融机构”并不仅限于银行。

根据FATCA的规定,金融机构主要有以下三种类型:(1)银行(bank),商业银行(commercial bank),储蓄银行(savingbank)及信用社(credit union)等存贷款为经常性业务的公司;(2)证券经纪公司(broker-dealers),信托公司(trust companies)等以为他人持有金融财产为主要业务的公司;(3)PE基金(private equity funds)以及其他基金(funds)等主要从事或受托从事投资、再投资、买卖证券等业务的公司,此外,有些保险公司也被包括在内。

表格W-8BEN-E填写说明

表格 W-8BEN-E 填写说明(于 2017 年 7 月修订)美国财政部美国国税局在美纳税与报税受益方身份证明(实体)除非另有说明,请参见《国内税收法》。

未来发展关于表格 W-8BEN-E 及其填写说明的最新进展,例如在该表格和说明发布后颁布的相关法律法规,请访问/ FormW8BENE。

最新进展有限 FFI 和有限分支机构。

有限 FFI 和有限分支机构身份已于 2016 年 12 月 31 日到期,并且已从此表格和填写说明中删除。

获赞助 FFI 和获赞助直接申报 NFFE。

自 2017 年 1 月 1 日起,登记视同遵守 FATCA 的获赞助 FFI 和获赞助直接申报NFFE 必须获得自己的 GIIN 以便在此表格上提供,并且不可再提供赞助实体的 GIIN。

此表格已经更新以反映这一要求。

非申报 IGA FFI。

此表格和这些填写说明已经更新以反映财政部法规中要求预扣款代理人证明非申报 IGA FFI 的要求。

这些填写说明还澄清是获赞助实体的非申报 IGA FFI 应提供自己的 GIIN(如有要求)并且不应提供赞助实体的GIIN。

参见第 12 部分的填写说明。

此外,这些填写说明规定:受托人提供证明文件的信托的外国受托人应提供其登记为参与 FATCA 的 FFI(包括模式 2 申报 FFI)或模式1 申报 FFI 时收到的 GIIN。

外国纳税人身份编号 (TIN)。

这些填写说明已更新以要求在一家金融机构的美国办事处或分支机构持有金融账户的特定外国账户持有人在此表格上提供外国 TIN(某些情况除外)。

请参见第 9b 行的填写说明了解这一要求的例外情况。

提醒注意。

如果您居住于 FATCA 合伙人辖区(即具有互惠的IGA 模式 1 辖区),特定纳税账户信息可提供给居住辖区。

一般说明关于本说明中所用术语的定义,请参阅下文的定义部分内容。

表格用途本表格供外籍实体证明第 3 章、第 4 章及本说明下文中描述的《国内税收法》其他特定条款规定的身份。

FATCA法案介绍及对我国商业银行的影响

FATCA法案介绍及对我国商业银行的影响作者:张德晓来源:《商情》2014年第52期【摘要】为了增加财政收入,近年来美国政府将追查海外偷漏税作为一条增收途径。

2010年3月18日,美国总统奥巴马签署《促进就业法案》(HIRE Act),以改善就业市场,而该法案包含一个条例,即《外国账户税务合规法案》(Foreign Account Tax Compliance Act,简称FATCA),该法案于2013年1月开始实施。

其相关条款要求所有非美国金融机构(FFI),其中包括银行、投资银行、信托公司等,和非美国非金融机构(NFFE)鉴别并披露其“美国账户”持有人和成员,并按要求向美国国税局报告“美国账户”持有人的详细信息并承担代扣代缴义务,否则,该金融机构任何来源于美国的收入款项和销售或处分美国证券所得都将被强行征收一项新的30%的预提税。

【关键词】FATCA,商业银行一、美国政府实施FATCA的背景介绍FATCA法案旨在打击美国纳税义务人利用海外金融账户和投资进行避税,并掌握其海外资产,其实质上是一种新的监管合规和报告机制,要求特定外国实体披露持有海外“金融账户”的美国人士的信息。

FATCA的申报对象为美国公民,其中包括在海外有个人账户达5万美元以上和企业账户25万美元以上的持有美国绿卡和双重国籍者。

对于某些非金融机构来说,一旦其拥有超过10%以上的美国股东,该非金融机构就必须定期向美国国税局申报公司持股人国籍资料和持股比例。

FATCA法案通过对直接或间接不遵守法案规定的相关方支付的可扣缴款项征收30%的惩罚税收,来促使特定外国实体遵守合规要求。

该法案的意图是让包括中国商业银行在内的全球金融机构承担主动申报所持有的美国客户的账户资料(包含收入、所得、资本利得等信息)的责任,以单方面保障美国政府的税收收入。

FATCA法案片面保护美国利益,并对海外金融机构强加了宽泛的域外识别、信息申报和扣缴义务,因此法案一经推出便引起了各国政府以及全球金融机构的强烈关注。

fatca申请书

尊敬的美国税务局(IRS):您好!我是[您的全名],居住在[您的居住国家/地区],根据美国海外账户纳税法案(Fatca)的相关规定,我需要向您提交此申请书,以说明我的情况并请求您的批准。

以下是我的详细情况说明:一、个人信息1. 姓名:[您的全名]2. 性别:[您的性别]3. 出生日期:[您的出生日期]4. 国籍:[您的国籍]5. 居住国家/地区:[您的居住国家/地区]6. 联系电话:[您的联系电话]7. 电子邮箱:[您的电子邮箱]二、账户信息1. 银行名称:[开户银行名称]2. 银行地址:[开户银行地址]3. 账户类型:[账户类型,如储蓄账户、投资账户等]4. 账户号码:[账户号码]5. 账户余额:[截至申请之日账户余额]三、Fatca合规情况1. 已知悉Fatca的相关规定,并了解其在全球范围内的实施情况。

2. 已向开户银行了解Fatca合规要求,并积极配合银行完成相关信息登记。

3. 我国的税收协定与Fatca存在冲突,根据我国政府的相关政策,我需要向美国税务局申请Fatca合规豁免。

4. 我已向开户银行提交了以下文件,以证明我的合规性:a. 我国税务机关出具的证明文件,证明我在我国纳税;b. 我国的居民身份证明文件;c. 其他有助于证明我合规性的文件。

四、申请理由1. 我居住在我国,根据我国政府的相关政策,我需要申请Fatca合规豁免。

2. 我已向开户银行提交了合规证明文件,并积极配合银行完成相关信息登记。

3. 我愿意遵守美国税务局的要求,提供必要的个人信息和账户信息。

五、承诺1. 我保证所提供的信息真实、准确、完整。

2. 我将积极配合美国税务局的调查和审查工作。

3. 我将遵守美国税务局的相关规定,及时更新个人信息和账户信息。

综上所述,我特此申请Fatca合规豁免,并承诺将积极配合美国税务局的工作。

请贵局予以审批,并给予支持与帮助。

此致敬礼!申请人:[您的全名]申请日期:[申请日期]。

【以诺财富】加拿大和美国加入全球金融账户信息交换制度('CRS') 会怎么样?

【以诺财富】加拿大和美国加入全球金融账户信息交换制度('CRS') 会怎么样?网上有不少关于美国或加拿大或将成为下一个避税天堂的新闻和讨论。

有的说全球金融账户信息交换制度(“CRS”)实施后美国或加拿大将取代瑞士成为下一个全球最大的避税地,但也有的说CRS实施以后美国或加拿大不再是富人的避税地。

不妨做一个小讨论。

目前有96个国家已经承诺加入OECD主导的CRS体系,换句话说,在未来的两三年,这些国家之间的涉税金融账户信息交换网络将逐步建立,富人的资产在这张大网里面将很难藏身。

但是美国并非CRS的参与国,并且一直在“拉拢”其他国家加入其所倡导的FATCA双边机制。

CRS虽然建立在FATCA的基础上,而且大体法规内容都一致,但是在很多具体问题的判定上仍存在差异。

这种差异一方面给金融机构,尤其是跨国金融机构造成了合规上的更大负担,另一方面也给“心机者”规避这两种制度以可乘之机。

尽管OECD在其CRS Commentary以及指导各国制定本地法的CRS Implementation Handbook中多处强调CRS与FATCA的一致性,但是由于FATCA中更多地融入了美国税法自己的特色,导致金融机构在两种制度下同时进行合规工作的混乱,尤其是在2015年已经向美国国税局(IRS)报送过第一批信息的金融机构,可能面临在CRS下一些重复的甚至是相反的合规要求。

鉴于传统的著名避税地如开曼群岛、英属维尔京群岛,巴巴多斯,列支敦士登等等都已经承诺加入CRS,那么美国的缺席是否会导致其成为下一个富人避税的宝地呢?富人在境外隐匿资产的方式五花八门,包括设立境外资产持有公司、基金或者信托等等,在此无意对所有情况进行全面的分析。

但鉴于投资类公司、基金或者信托等实体在FATCA 和CRS下的分类大体一致,所以我们不妨就以投资类公司为例进行一个小讨论。

分类用简单但不严谨的话来说,在FATCA或者CRS下, 通常投资类公司会被划分为“金融机构”或者“非金融机构”两种。

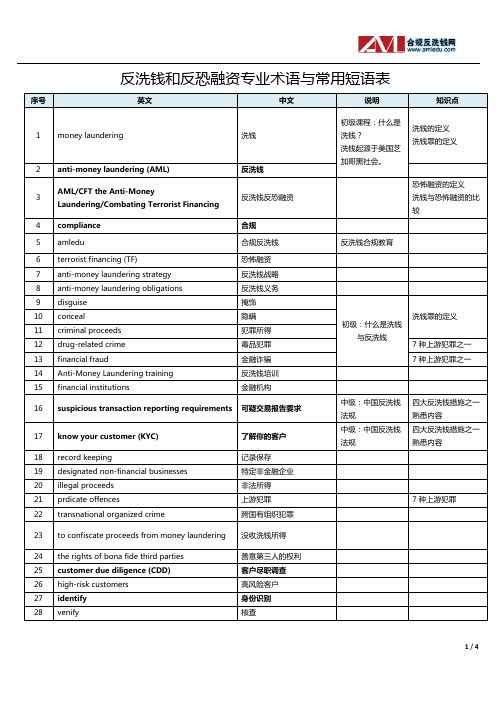

反洗钱考试辅助 反洗钱专业术语中英文对照表

79

公认反洗钱协会

Specialists (ACAMS)

全称“当代 ACAMS 反洗钱合规教育中 心”专业反洗钱教 育网站

全球最大的反洗钱 协会

Basel Committee on Banking Supervision 80

(BCBS)

巴塞尔银行监管委员会

中级:国际反洗钱、 西方十国央行的俱乐 反恐融资主要组织 部

国际货币基金组织

中级:国际反洗钱、 世界银行

反恐融资主要组织

Organization for Economic Co-operation and 87

Development (OECE)

经济合作与发展组织

4/4

欧盟理事会

中级:国际反洗钱、 预防

反恐融资主要组织

83 Federal Reserve 84 Financial Intelligence Units (FIU) 85 Interal Revenue Service (IRS)

联邦储备委员会 金融情报处理中心 美国国税局

86 Interal Monetary Fund (IMF)

四大反洗钱措施乊一 熟悉内容 四大反洗钱措施乊一 熟悉内容

7 种上游犯罪

23 to confiscate proceeds from money laundering 没收洗钱所得

24 the rights of bona fide third parties 25 customer due diligence (CDD) 26 high-risk customers 27 identify 28 venify

合规

合规反洗钱

恐怖融资 反洗钱战略 反洗钱义务 掩饰 隐瞒 犯罪所得 毒品犯罪 金融诈骗 反洗钱培训 金融机构

fatca pffi 机构分类英文

fatca pffi 机构分类英文The Foreign Account Tax Compliance Act (FATCA) was enacted by the United States Congress in 2010 to combat tax evasion by U.S. taxpayers holding assets in offshore accounts. FATCA requires foreign financial institutions (FFIs) to report information about their U.S. account holders to the Internal Revenue Service (IRS). To comply with FATCA, FFIs need to classify themselves into different categories based on their level of compliance and reporting obligations. This classification helps determine the extent of their reporting requirements and the penalties for non-compliance. In this essay, we will discuss the various categories of FFIs under FATCA and the requirements associated with each category.The first category of FFIs under FATCA is the Participating Foreign Financial Institution (PFFI). PFFIs are foreign financial institutions that enter into an agreement with the IRS to comply with FATCA reporting requirements. These institutions are required to reportinformation about their U.S. account holders directly to the IRS or through their local tax authorities. PFFIs must also withhold and pay over to the IRS any applicable withholding taxes on certain U.S. source income paid tonon-compliant account holders.The second category is the Registered Deemed-Compliant Foreign Financial Institution (RDCFFI). RDCFFIs are FFIs that are deemed compliant with FATCA requirements without having to enter into an agreement with the IRS. These institutions include certain local banks, retirement plans, and non-profit organizations. RDCFFIs have reducedreporting obligations compared to PFFIs but still need to provide information about their U.S. account holders to their local tax authorities.The third category is the Certified Deemed-Compliant Foreign Financial Institution (CDCFFI). CDCFFIs are FFIs that are deemed compliant with FATCA requirements based on their status under local laws or regulations. These institutions include certain small banks, local investment entities, and governmental entities. CDCFFIs have evenlower reporting obligations compared to RDCFFIs and generally do not need to report directly to the IRS.The fourth category is the Limited FFI. Limited FFIs are FFIs that have been granted a limited exemption from FATCA reporting requirements. These institutions are typically located in jurisdictions that have entered into intergovernmental agreements (IGAs) with the United States. Under these agreements, the local tax authorities agree to provide the required information about U.S. account holders to the IRS on behalf of the Limited FFIs.The fifth category is the Nonparticipating Foreign Financial Institution (NPFFI). NPFFIs are FFIs that have not entered into an agreement with the IRS and do not meet the criteria for deemed compliance. These institutions face the highest level of FATCA reporting requirements and are subject to a 30% withholding tax on certain U.S. source income.In conclusion, FATCA requires foreign financial institutions to classify themselves into differentcategories based on their compliance with reporting requirements. The categories include Participating Foreign Financial Institutions, Registered Deemed-Compliant Foreign Financial Institutions, Certified Deemed-Compliant Foreign Financial Institutions, Limited FFIs, and Nonparticipating Foreign Financial Institutions. Each category has different reporting obligations and penalties for non-compliance. By classifying FFIs, FATCA aims to increase transparency and reduce tax evasion by U.S. taxpayers holding offshore accounts.。

全新版大学英语综合教程第四册Unit2

• Benz奔驰

• Hummer 悍马 (原意为“蜂鸟”,悍马 多数为大型吉普车、房 车)

• Cadillac凯迪拉克 the Cadillac of sth一流 的,最好的,顶级的

How much do you know about smart cars?

Warm-up discussion

1. Smart is short for Swatch Mercedes ART. 2. Smart car is a vehicle equipped with multimedia digital

systems, such as sensors, in-car navigational systems, Global Positioning Systems, small radars to make driving safe and fast, so it’s versatile. 3. It is an application of artificial intelligence in vehicles. 4. It plays an important role in Intelligent Transport Systems (ITS).

Terms of smart cars:

• sensor(L10) • monitor(L24) • bumper(L25) • dashboard(L33) • orbiting satellite(L40) • receiver(L49) • navigation(L53) • microchip(L56) • radio transmitter(L65) • rear-view mirror

• What do you imagine a smart car can do? talk to the driver? drive on its own? warn the driver of dangers? locate the car? sense the driving conditions nearby?

IRS FATCA 注册系统指南说明书

Global IRW NewsbriefIRS opens FATCA online registration system to provide a beneficial user testing periodAugust20,2013In briefThe Internal Revenue Service(IRS)announced the opening of the Foreign Account Tax Compliance Act (FATCA)registration system on August19,2013.The registration system will enable financial institutions(FIs)to register and obtain a global intermediary identification number(GIIN).FIs are requested to submit the required information online as final on or after January1,2014–no GIINs will be issued before this date.Between now and December31,2013,FIs are permitted to establish their online account,input preliminary information,refine such information,and become familiar with the system thereby resulting in a user testing period.The IRS release included:∙A75-page User Guide and Overview which provides instructions for completing the online registration process including step-by-step instructions for each question and the registrationinformation required for each type of FI as well as information on how to edit and delete aregistration.∙Tips for Logging into the FATCA Registration System which provides helpful hints for accessing the system.∙A GIIN Composition document which explains the components of the19-character GIIN.The IRS also released the final Form8957(Foreign Account Tax Compliance Act(FATCA)Registration), including instructions.This form is substantially similar to the draft dated April17,2013which did not have instructions.The IRS is strongly encouraging the use of the online registration system in lieu of paper registration requests on Form8957,but will accept registrations made on this form beginning January1,2014.The IRS notes that registrations using Form8957will experience slower processing times than online registration.Consequently,FIs registering by paper will wait longer for a GIIN.The available testing period and new IRS guidance are long awaited and welcome developments for stakeholders.The ability to gain a practical understanding of the registration system before the information is formally submitted is intended to enable the registration process to be conducted in a more orderly fashion.The IRS is encouraging preparedness by suggesting that registrants input andedit information early during the testing period so they are ready to submit the final information starting in January2014.It should be noted that the user guide does not contain information about registering sponsored entities,and that guidance is forthcoming.The registration site and materials also make reference to the FFI Agreement in which a significant number of foreign financial institutions(FFIs)are expected to enter.However,stakeholders are still awaiting a draft of such agreement. In detailOnline registration promotes efficiencyFI registration with the IRS is an important cornerstone of the FATCA regime for entities wanting to achieve compliance.The IRS intends for its secure,web-based system to enable FIs to satisfy their FATCA registration requirements efficiently and effectively in a paperless manner.The registration system is intended to be a one-stop shop that enables the registrant and its related entities(e.g., members and branches)to handle the administrative and compliance matters relating to obtaining a GIIN–a critical step in avoiding the30% FATCA withholding. Observation:According to the Form8957instructions,FIs must finalize their registration by April 25,2014in order to be included in the June2014FFI List.Registering FIs will receive a notice of registration acceptance and will be issued a GIIN.Although the form instructions are silent on this issue, it may be possible to submit a paper Form8957by April25,2014 and still be included in the June List.Entities eligible to registerBroadly speaking,the FATCAregistration system should be used byan FI to register itself(and itsbranches,if any)as a participatingforeign financial institution(PFFI),aregistered deemed-complaint FFI(RDCFFI),a limited FFI,or asponsoring entity.Note that RDCFFIsinclude reporting FFIs under a Model1intergovernmental agreement(IGA).Registration will enable the entity toobtain a GIIN and to accomplish thefollowing:∙An FFI,non-US branch of an FFI,or USFI that is treated as areporting FI under a Model1IGAcan authorize one or more pointsof contact(POCs)to receiveinformation related to registrationon the FI’s behalf.∙An FFI,or foreign branch of anFFI,that is treated as a reportingFI under a Model2IGA,canauthorize one or more POCs toreceive information related toregistration on the FI’s behalf,andconfirm that it will comply with theterms of an FFI Agreement,asmodified by the applicable Model2IGA.∙An FFI,or branch of an FFI,otherthan one covered by an IGA,canenter into an FFI Agreement to betreated as a PFFI,agree to meet therequirements to be treated as anRDCFFI,or confirm that it willcomply with the terms applicableto a limited FFI or a limitedbranch.∙An FI(including a USFI)seeking toact as a sponsoring entity,canagree to perform the due diligence,reporting,and withholdingresponsibilities on behalf of one ormore sponsored FFIs.∙An FI,including a foreign branchof a USFI,currently acting as aqualified intermediary(QI),withholding foreign partnership(WP),or withholding foreign trust(WT),can renew its QI,WP,or WTAgreement.∙A USFI wishing to act as a lead FI(defined below)for purposes ofregistering its member FIs,canidentify itself as such.Observation:The new IRSguidance provides clarity on how aUSFI will register and serve aseither a sponsoring or lead entity.The IRS guidance also provides animportant distinction when a USFIhas a foreign branch under a Model1or2IGA.Specifically,branchesunder a Model1IGA must register.The registration appears necessaryas they will need to provideinformation directly to localgovernments and in some cases filea nil return.However,a foreignbranch of a USFI located in a Model2IGA country does not need toregister unless such foreign branchneeds to renew its QI,WP,or WTagreement.Lead FIs and EAG relationshipsclarifiedA key requirement under theregistration process is that an FI mustselect one of the four registrationtypes:Single(not a member of anexpanded affiliated group(EAG)),lead(within an EAG),member(withinan EAG),and FI sponsoring entity.The term‘lead FI’includes a USFI,FFI,or a compliance FI that agrees tocarry out FATCA registration for eachof its member FIs that is a PFFI,RDCFFI,or limited FFI and that isauthorized to carry out most aspectsof its members’FATCA registrations.A compliance FI is defined as a lead FIthat agrees to establish and maintain aconsolidated compliance program andto perform a consolidated periodic review on behalf of one or more members FIs that are part of its EAG (the compliance group).A compliance FI must also have the authority to terminate the FATCA status of each member FI within its compliance group.The new IRS guidance presents additional clarity surrounding the‘lead FI’type.A lead FI is not, however,required to act as a lead FI for all members within an EAG.As a result,an EAG may include more than one lead FI that will carry out FATCA registration for a portion of its members.The particular lead FI will perform FATCA registration for each of its members through the website. Observation:The final Form8957 instructions and the User Guide provide a number of helpful definitions for reference such as‘lead FI.’The instructions make clear however,that the definitions should be used only for registration purposes and that FIs should refer to definitions under an IGA or FATCA regulations to determine their obligations.Creating an online FATCA account and home pageThe first step in the FATCA registration process is to create an online FATCA account.This may be done only by a single,lead,or sponsoring entity.An FI must create an access code(password)along with certain‘challenge questions’in case the access code is lost.Once submitted,the online system will provide a six-character FATCA ID used to identify the FI only for registration purposes.The FATCA ID is a different number than the19-character GIIN,although the FATCA ID will be the first six characters of the GIIN.Observation:In order to access the registration site for on-going use,the access code and FATCA ID mustbe used.The login credentials canbe shared by the responsible officer(RO)and up to five POCs–no othercontacts may access theregistration system.If anauthorized contact forgets thecredentials,that person may‘reset’the access code by answeringchallenge questions correctly.From a practical perspective,coordination and sharing mustoccur among users of a specificFATCA account.Once the FATCA account is created,the FI home page provides a centrallocation for accessing all relevantinformation about the FATCAregistration account.The system maybe used for on-going accountmanagement and will include featuressuch as a message board.As a result,most communications between theIRS and FI will occur electronically.The individual identified as the RO inQuestion10may likely be the onlyindividual who will receive emailsfrom the IRS related to the FI’sFATCA account.However,a POC isalso an individual authorized toreceive FATCA related informationfrom the IRS and to take FATCA-related actions on behalf of the FIupon the request of the IRS.The FI’s account status will belocated on the registration home page.According to the User Guide,there arenine potential account statuses for anFI.These include(i)Initiated,(ii)Registration submitted,(iii)Registration incomplete,(iv)Registration under review,(v)Registration rejected,(vi)Agreementcancelled,(vii)Agreement terminated,and(viii)Approved.This lattercategory is generally the desiredcategory where a notice of registrationand GIIN is awarded by the IRS.Theninth and final status is Limitedconditional,which denotes an FI thatwill not receive a GIIN and will notappear on the next published FFI List.Observation:The initialregistration to obtain a GIIN maybe performed by the sponsoringentity without providing significantdetail about their sponsoredentities.Additional guidance isexpected related to sponsored FFIsand how they can provideinformation about their sponsoredentities.Notice of registration acceptanceand GIIN compositionWhen a registration is finalized andapproved in2014,a registering FI willbe given a notice of registrationacceptance and issued a unique GIIN.The first IRS FFI list of GIINs will beposted online by June2,2014and isexpected to be updated monthlythereafter.An FI will use its GIIN toidentify itself to withholding agentsand to tax administrators for FATCAreporting.A separate GIIN will beissued by an FI to identify eachjurisdiction in which the FI maintainsa branch that is participating orregistered deemed-complaint.GIINs are alphanumeric and arecomprised of19-characters.There arefour sections within the GIIN,eachseparated by a period:∙1through6characters=theFATCA ID–randomly generatedsix-character alphanumeric string.For member FIs,the first sixcharacters will follow that of thelead FI or sponsoring entity∙7is a character representing aperiod∙8through12characters=theFI type–depends on the type offinancial entity.For example,leadand sponsoring entities are fivezeros∙13is a character representinga period∙14through 15characters =the category code based onfinancial institution or branch category (lead,single,member,branch,and sponsoring)∙16is a character representing a period ∙17through 19characters =the country identifier ,chosen by viewing Appendix D in the User Guide;Over 250countries arelisted but registrants should choose the number 999if their specific country is not included.The takeawayThe new IRS guidance is consistent with the revised timelines announced by the IRS in July of this year for implementing various provisions under FATCA.See previous Global IRW Newsbrief on this topic.The delay in FATCA implementation provides a unique opportunity for stakeholders to have more time togather complete and accurateinformation about their entities,make necessary key business decisions,and conduct the registration process in an orderly manner.However,the registration process continues to demand that taxpayers work through their FATCA strategy upfront –how they are going to prepare for their compliance requirements going forward and avoid potentially costly FATCA withholding.A detailed analysis of the registration process and required data should occurbefore registration ,including but not limited to the following:∙Given the broad definition of FFI,determining the specific types of entities that may qualify as FFIs.In addition,identifying entities which will be responsible for reporting tasks (e.g.,what sponsoring entities should be designated as such).∙Registering FIs must gather and organize the required registrationinformation.This will improve the accuracy of the registration process and make take longer than anticipated.∙FIs that have not designated an RO must appoint one soon.An RO is required to establish an FI account and complete the FFI registration.This requirement is part of the larger issue of who throughout the organization is affected and should be involved with FATCA compliance.∙Evaluate the use of technology and automation.What specific efficiencies can be gained by effective use of technology in gathering and exchanging documentation?How could technology help leverage knowledge between related companies?Additional backgroundAccess to the FATCA registration system and related support information can be found on the IRS FATCA page .Additional FATCA information can be found on the US Treasury FATCA Resource Center .For additional thought leadership regarding FATCA guidance and implementation,please see our Global IRW Newsbrief archive .How do you plan to keep up-to-date with the release of the FATCA IGAs and some of their unique differences?Access our FATCA IGA Monitor Website that includes:∙a high-level overview of signed IGAs ∙the latest IGA developments∙potential actions to think about as you look at the impact of the IGAs to your FATCA program.Let’s talkFor more information on how FATCA might impact you,please contact a member of the Global GIR Network .To view FATCA contacts for over 30countries worldwide,click here .PwC contactsIf you would like further advice or information in relation to the issues outlined above, please call your local PwC contact or any of the individuals listed below:Martin VinkT:+31(0)887926369 ******************.com Clark NoordhuisT:+31(0)887927244**********************.comRemco van der Linden T:+31(0)887927485*********************.com。

美国“国税局”:最令人闻风丧胆的政府部门

美国“国税局”:最令人闻风丧胆的政府部门作者:高荣伟来源:《检察风云》2018年第23期IRS被称为“美国最令人闻风丧胆的政府部门”,其能量甚至超过国防部、中情局。

美国人私下里讲,“惹谁也别惹国税局”,从中可以窥见其“强大威力”。

在美国,每年1月1日至4月15日是报税季节。

期间,每个公民都需要向一个部门提交自己的收入证明及纳税表格,包括合法收入以及非法收入——这个部门就是美国“国税局”(IRS)。

不要妄想逃税。

一旦逃税,IRS完全有能力查到。

毕竟,这里仅稽查人员就有4万人,占其职员总数的35%左右。

IRS被称为“美国最令人闻风丧胆的政府部门”,其能量甚至超过国防部、中情局。

美国人私下里讲,“惹谁也别惹国税局”,从中可以窥见其“强大威力”。

密不透风的机构设置“美国国税局”( Internal Revenue Service,简称IRS),也译为“美国国内收入署”,隶属于财政部,负责联邦政府的税务征收等工作。

1862年,林肯总统及当时的国会为支付战争费用,创立了国内税务局和所得税。

1913年美联储建立后,IRS开始正式运作,收缴高额税款直到今天。

IRS可以说是美国最大的政府机构,雇佣11.5万人。

美国实行联邦、州和市县三级税务管理体制。

美国被称为“万税国”。

联邦税以个人所得税、社会保险税、公司所得税为主,此外还有遗产税与赠予税、消费税(包括一般消费税及专项用途消费税)、暴利税、印花税等。

理论上,在美国所有收入都要缴纳联邦收入税。

个人所得税按照收入分级收取,最低联邦税率是收入的10%,最高达到35%。

去年年底,特朗普政府推出31年以来最为重大的减税改革,将联邦个人收入所得税率由之前的10%、15%、25%、28%、33%、35%、39.6%共7个档次减至4个档次,分别为12%、25%、35%和39.6%。

“作为一个美国公民,我必须申报在全球的收入,并进行纳税。

”的确,美国是经合组织(OECD)中唯一对其公民在全球任何其他地方获得的收入都进行征税的国家。

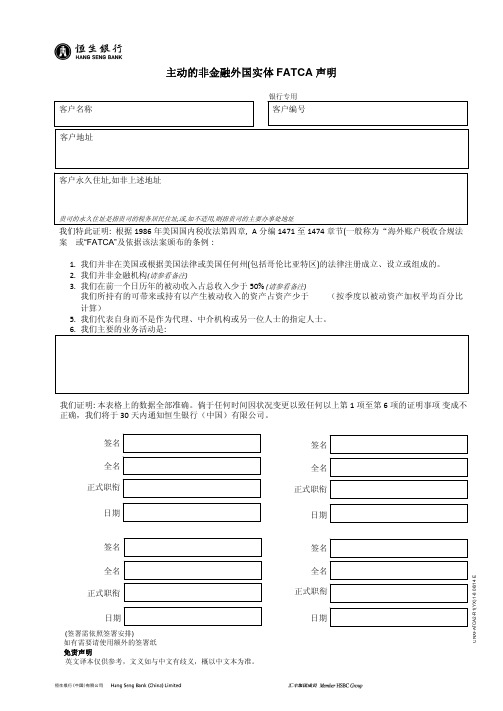

FATCA Form中文释义

主动的非金融外国实体FATCA 声明C N X F A T C A 2-R 1(Y X ) 2-8 06/14 EFATCA Declaration for Active Non-Financial Foreign EntitiesC N X F A T C A 2-R 1(Y X ) 3-8 06/14 EFATCA 声明 – 额外签署纸FATCA Declaration – Additional Signature Sheet(签署需依照签署安排)(Signed in accordance with the mandate)C N X F A T C A 2-R 1(Y X ) 5-8 06/14 E海外账户税收合规法案(FATCA )此为签署以下声明之备注:∙ 主动的非金融外国实体FATCA 声明 ∙ 非营利组织FATCA 声明重要: 本文件必须与作为其组成部分的免责声明一并阅读。

背景金融监管机构、政府及银行正作出多项重要改变,以确保能长远保障金融系统及客户利益。

其中一项变动为美国政府所颁布成为1986年美国国内税收法一部份的《海外账户税收合规法案》(“FATCA”)。

FATCA 旨在向美国税务机关申报由美国人士所拥有的金融资产。

FATCA 对恒生银行(中国)有限公司及阁下的影响?恒生银行(中国)有限公司(“恒生中国”)致力在所有经营地全面遵从FATCA 法案。

这代表我们需要向美国税务机关申报受影响的客户的收入和利润。

为此,我们需要从客户取得更多数据,以识别美国人士(USPs)和外国金融机构(FFIs)或其他客户。

银行及其他金融组织需每年申报美国人士直接或间接持有的金融账户的资料。

如我们无法从客户取得所需的数据或文件,银行可能需要从向客户或客户账户支付的若干款项中代扣美国税项,称为“可扣缴款项”。

我们也可能需要终止与客户的关系。

为了识别可能需按FATCA 进行申报的客户,我们将根据FATCA 法案列明的类别对客户进行分类。

外国账户税收遵从法FATCA

February 13, 2014Spanish | English | Russian外国账户税收遵从法 (FATCA)FATCA 和 IGA 简介外国账户税收遵从法 (FATCA) 是美国于 2010 年颁布的法律,属于 HIRE 法案的组成部分。

FATCA 最终规定于 2013 年 1 月 17 日颁发,2014 年 7 月 1 日生效,其中部分义务的履行期限为两年半。

根据美国财政部声明,我们预计不久后将发布 FATCA 修订法规和进一步的指导说明。

最后期限已经临近。

FATCA 面向持国外金融帐户的美国纳税人,专门打击其逃税行为。

它要求国外实体确认那些直接或间接持有特定国外金融帐户的美国纳税人,并向 IRS (国内收入署)汇报相关信息。

对于违规者,其来自美国的特定款项将代扣 30% 所得税,还可能违反当地国家法律。

美国政府与多个参与国签订了政府间协议 (IGA) 来消除某些法律障碍,减少当地财务机构的合规性负担并在其当地辖区内有效施行 FATCA 。

目前共制定了两套 IGA 范例 -Model 1 和 Model 2。

签署的 IGA 数量达到 22 个,有大约 40 个国家正与美国协商签订 IGA (见下表)。

FATCA 和 IGA 不仅影响到美国个人和实体,还要求众多国外实体遵守更多的披露与合规性要求,甚至还可能影响国外个人。

即使不涉及美国受益人或美国投资,FATCA 和 IGA 中的很多要求也仍然适用。

在等待后续指导说明的同时,我们会事先讨论 FATCA 和 IGA 可能产生的影响以及确保合规性所需的重要步骤和设施(见下面)。

FATCA 与 IGA 的重要方面FATCA 和 IGA 将美国以外的实体划分为国外金融机构 (FFI) 和非金融类国外实体 (NFFE)。

如下面所示,每一类都要履行不同的 FATCA/IGA 义务:外国金融机构 (FFI)非金融外国实体 (NFFE)FFI 可能需要向 IRS 登记以确认哪些帐户持有者是美国纳税人和美国所有的外国实体,并向 IRS 汇报其相关的财务信息,或是按照 1 型 IGA 的要求汇报给当地税务部门(LTA)。

金融机构fatca身份代码

金融机构fatca身份代码摘要:1.FATCA 身份代码的定义与重要性2.FATCA 身份代码与金融机构的关系3.FATCA 身份代码在全球范围内的应用4.FATCA 身份代码对我国金融机构的影响与应对措施正文:一、FATCA 身份代码的定义与重要性FATCA(Foreign Account Tax Compliance Act,外国账户税收合规法案)身份代码是由美国国税局(IRS)颁发的一种全球税收合规标识。

FATCA 身份代码的重要性在于,它关乎到金融机构是否能够合规地为其客户提供跨境金融服务,以及客户在全球范围内的资产是否得到合规的申报和纳税。

二、FATCA 身份代码与金融机构的关系金融机构在为客户提供跨境金融服务时,需要对其客户的FATCA 身份进行识别和分类。

金融机构需要向美国国税局申请FATCA 身份代码,以便在合规的前提下,完成客户信息的报送和税收义务。

同时,FATCA 身份代码也有助于金融机构在全球范围内建立合规的金融服务体系,降低合规风险。

三、FATCA 身份代码在全球范围内的应用FATCA 身份代码在全球范围内的应用十分广泛。

美国作为全球金融中心之一,其FATCA 法规对全球金融机构产生了深远的影响。

许多国家和地区的金融机构,为了合规地服务于拥有美国账户的客户,都需要申请FATCA 身份代码。

这使得FATCA 身份代码在全球范围内的金融服务市场中具有极高的地位。

四、FATCA 身份代码对我国金融机构的影响与应对措施我国金融机构在面临FATCA 身份代码的挑战时,需要采取一系列应对措施。

首先,金融机构需要提高自身的合规意识,了解并掌握FATCA 法规的具体要求。

其次,金融机构需要加强与美国国税局的沟通和合作,积极申请FATCA 身份代码。

最后,金融机构需要完善自身的信息系统和技术支持,确保在合规的前提下,为客户提供高效、便捷的跨境金融服务。

总之,FATCA 身份代码对金融机构在全球范围内的业务发展具有重要意义。

W-8BEN-E在美纳税与报税受益方身份证明(实体)20142

表格W-8BEN-E在美纳税与报税受益方身份证明(实体)X 此表仅限实体使用。

个人须使用 W-8BEN 表格。

X 参见国内税收法规。

X 关于表格 W-8BEN-E 及其单独说明的信息,请访问 /formw8bene 。

X 将此表格交给纳税代理人或支付方,不要交给美国国税局。

OMB 编号:1545-1621(2014 年 2 月)美国财政部美国国税局请勿将本表格用于以下对象: 而应使用以下表格:• 美国实体或美国公民或居民 W-9• 外籍人士 W-8BEN (个人) • 宣称所得与在美国的贸易或商业行为实际相关的外籍人士或外国实体 (要求享受税收协定优惠待遇的除外) W-8ECI• 外国合伙企业、外国简单信托或外国授予人信托(要求享受税收协定优惠待遇的除外)(参见说明中列举的例外情况) W-8IMY • 外国政府、国际组织、外国中央发行银行、外国免税机构、外国私人基金会,或者是美国的所属政府,这些机构宣称获得的收入是实际相关的美国收入或宣称适用于第 115(2)、501(c)、892、895 或 1443(b) 条的规定(要求享受税收协定优惠待遇的除外)(参见说明) W-8ECI 或 W-8EXP• 作为中间人的任何个人 W-8IMY 非参与 FATCA 的 FFI (包括受限 FFI 或与 IGA 申报 FFI 相关的 FFI ,登记视同遵守 FATCA 的 FFI 或参与 FATCA 的 FFI 除外)。

参与 FATCA 的 FFI 。

模式 1 申报 FFI 。

模式 2 申报 FFI 。

登记视同遵守 FATCA 的 FFI (模式 1 申报 FFI 或尚未取得 GIIN 的获赞助 FFI 除外)。

尚未取得 GIIN 的获赞助 FFI 。

请填写第 4 部分。

经认证视同遵守 FATCA 的未登记地方银行。

请填写第 5 部分。

经认证只拥有低价值账户的视同遵守 FATCA 的 FFI 。

请填写第 6 部分。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Summary of Key FATCA Provisions

The Foreign Account Tax Compliance Act (FATCA), enacted in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act, is an important development in U.S. efforts to combat tax evasion by U.S. persons holding investments in offshore accounts.

Under FATCA, certain U.S. taxpayers holding financial assets outside the United States must report those assets to the IRS. In addition, FATCA will require foreign financial institutions to report directly to the IRS certain information about financial accounts held by U.S. taxpayers, or by foreign entities in which U.S. taxpayers hold a substantial ownership interest.

Reporting by U.S. Taxpayers Holding Foreign Financial Assets

FATCA requires certain U.S. taxpayers holding foreign financial assets with an aggregate value exceeding $50,000 to report certain information about those assets on a new form (Form 8938) that must be attached to the taxpayer’s annual tax return. Reporting applies for assets held in taxable years beginning after March 18, 2010. For most taxpayers this will be the 2011 tax return they file during the 2012 tax filing season. Failure to report foreign financial assets on Form 8938 will result in a penalty of $10,000 (and a penalty up to $50,000 for continued failure after IRS notification). Further, underpayments of tax attributable to non-disclosed foreign financial assets will be subject to an additional substantial understatement penalty of 40 percent.

Reporting by Foreign Financial Institutions

FATCA will also require foreign financial institutions (“FFIs”) to report directly to the IRS certain information about financial accounts held by U.S. taxpayers, or by foreign entities in which U.S. taxpayers hold a substantial ownership interest. To properly comply with these new reporting requirements, an FFI will have to enter into a special agreement with the IRS by June 30, 2013. Under this agreement a “participating” FFI will be o bligated to:

(1) undertake certain identification and due diligence procedures with respect to its accountholders;

(2) report annually to the IRS on its accountholders who are U.S. persons or foreign entities with substantial U.S. ownership; and

(3) withhold and pay over to the IRS 30-percent of any payments of U.S. source income, as well as gross proceeds from the sale of securities that generate U.S. source income, made to (a) non-participating FFIs, (b) individual accountholders failing to provide sufficient information to determine whether or not they are a U.S. person, or (c) foreign entity accountholders failing to provide sufficient information about the identity of its substantial U.S. owners.

Notice 2011-53 provides the phased-in timeline of key FATCA implementation dates for FFIs. It is important to note that many details of the new reporting and withholding requirements pertaining to FFIs must be developed through Treasury regulations that are expected to be proposed by December 31, 2011. Published IRS Notices accessible from this FATCA internet site provide currently available information and guidance.

Page Last Reviewed or Updated: December 15, 2011。