chapter_3_financial_ratios

financialratios(accounting)

IntroductionFinancial statements obviously play an important role in a fundamental approach to security analysis. Among the items of potential interest to analysts are financial ratios relating key parts of the financial statement. Financial Ratio is a measure of the relationship which exists between two figures shown in a set of financial statements, which indicates performance and financial situation of a company. Financial ratios could assess the profit of investments during the different years, and it can be also used to analyze trends and to compare the firm’s financials to those of other firms. Thus, financial ratios could compare the benefits and risks of different companies, which help investors and creditors to make rational decision. Moreover, this can evaluate the finance condition, operating results and cash flows for a business as well. Financial ratios can be classified according to the information they provide. There are some types of ratios: Liquidity ratios, Profitability rations, Efficiency ratios and Gearing ratios. However, financial ratios relate to both benefits and limitations in evaluating the performance and management of firms. This assignment is going to analyzing the EasyJet plc annual report and accounts in 2003 to discuss the usefulness and limitations of financial ratios.The ratios analysis is one of the most powerful tools of financial management. It can be computed from any pair of numbers. Given the large quantity of variables included in financial statements, a very long list of meaningful ratios can be derived. A standard list of ratios or standard computation of them does not exist. Financial ratios are used by bankers, investors, and business analysts to assess a company’s financial status. Financial ratio analysis can be used in two different but equally useful ways. Business can use them to examine the current performance of your company in comparison to past periods of time, from the prior quarter two years ago. Frequently, this can help you identify problems that need fixing. Even better, it can direct company attention to potential problems that can be avoided.Financial ratio plays an important role in financial statements, so there are some benefits of financial ratios. First of all, most of the rations become much more meaningful when used as a basis for comparison, which make a company very easy to compare firms against each other. Besides, it also makes possible comparison of the performance of different divisions of the business. Secondly, financial ratio provides information for inter-firm comparison. It highlights the factors associated with successful and unsuccessful firm, and it also reveal strong firms and weak firms, overvalued and undervalued firms. There are no firm has all the strength points, but ratio analysis can create co-ordination between strength points and weak points. Thirdly, it simplifies the comprehension of financial statements, which is able to illustrate the financial condition of a company by the number. For example, a company’s gross profit in 2011 is 25.3% and in 2012, it is 27.5%. According to this ratio, people can understand whether their company is growing or falling. In addition, financial ratio helps in planning and forecasting as well. This means it could be used to assess the risk factor involved for an investor and predict the bankruptcy of acompany. Thus, financial ratio is an early warning system for businesses that are heading into financial distress.Although ratio analysis is an extremely useful and powerful tool for the analysis and interpretation of financial statements, but it still has some limitations. Firstly, there are no two companies are exactly the same. This means many large firms operate different divisions in different industries, so it is difficult to find a meaningful set of industry –average ratios. Additionally, inflation might be damage of balance sheets of a company, which will be affected profits of a company as well. After that, small companies tend to pay more debt than large companies, and this will affect the interest coverage ratio formula as a way needs to be explained. Moreover, ratio analysis explains relationships between past information while users are more concerned about current and future information. Therefore, it is only the reference value for the future decision making. What is more, some accounting ratios might be defined in more than one way. This means, different companies may choose different accounting procedure, and each operators have different calculation methods that lead to different interpretations of data. It is very important that users should be aware of this problem when basing important economic decisions on information provided in the form of ratio analysis. Furthermore, a statement of financial position shows only a snapshot of a company’s financial position on a single date, whilst a statement of comprehensive income covers an entire accounting period. Therefore, if the company’s assets and liabilities end of the period are not typical of the period as a whole, any ratio which combines a figure drawn from the statement of financial position with a figure drawn from the statement of comprehensive income might produce a misleading result. Last but not least, financial ratio just able to show the data of company to the analysts or managers, but it cannot explain the problems and deal with them.EasyJet is a British airline carrier based at London Luton Airport. This is helpful to take a look at what information is obvious from the financial statement. There is some information to interpretation of the ratios, which from the EasyJet plc annual report and accounts in 2013. On the one hand, the non-current assets increased by about 26% (from 2191 pounds to 2964 pounds) between 2009 and 2013. This may be due to the fact that the company invested in some property, such as plane, airline, staffs and so on. Moreover, the number of revenue keep grew up between the 2009 and 2013. Companies use selling products or providing services to achieve the revenue, so the high revenue means the increase of assts or decrease of liabilities in a company. At the same time,there was a significantly increased in the number of profit during the 5 years, which were from 71million pounds in 2009 to 398 million pounds in 2013. Obviously, this means EasyJet Company getting better continually during the year. Return on capital employed is an important ratio expresses a company’s profit as a percentage of the amount of capital invested in the company. This version of ROCE interprets “capital employed”as the total amount of money in the long-term, regardless of whether that money has been supplied by shareholders or lenders. This amount is then compared with the return achieved on that capital. According to theinformation from the EasyJet report, there was a remarkable jumped in the number of the return on capital employed from 3.6% to 17.4% during the five years. Generally, the higher the rate of return on capital employed of the company has more growth in the future.Financial information can be “massaged” in several ways to the figures used for ratios more attractive. For example, many businesses delay payments to trade creditors at the end of the financial year to make the cash balance higher than normal and the creditor days figure higher too.these ratios to compare the performance of the company against that of competitors or other members of same industry Performing a ratio analysis on a single set of financial statements is usually a fairly pointless exercise. For example, if the company's inventory turnover ratio of 1 to 4 this year when it was 1 to 3 last year, this means that inventory levels are building in the current year. The increase in the ratio is an indication that sales are slowing or that inventory levels (which are expensive to maintain) are growing. The ratio change alerts the business manager to a pending cash crunch in time to avert it.If you are evaluating two businesses to hire as subcontractors, their respective debt-to-asset ratios will give you an idea about which of these two companies is the more stable choice. The company with a higher debt-to-asset ratio could be more likely to go out of business as a result of defaulting on interest and principal repayments. However, if your primary objective is investing in a business, and you are seeking high returns, the company with the higher ratio may be a better bet. Firms that borrow heavily are high-risk, high-return investments and tend to do either very well or fail spectacularlyA company can burn through its cash reserves quickly during tough economic times or industry contraction. Financial ratios can operate as an early warning system for businesses that are heading into financial distress. Ratios such as the quick ratio (how much money will there be to pay current debts?), gross margin (how much is the company making on every widget it sells?), and accounts receivable ratio (how quickly are sales being paid for?) tell the company's owners if the money is going to run out and how quickly. The sooner the cash flow problem is identified, the sooner it can be corrected.. The liquidity and non-bank credit ratio are used for assessing the companies going through a hard time. The non-bank ratio is used by a firm where the firm cannot afford to get more credit from banks. This ratio means the greater risk as if the company cannot repay the loan to the bank, it may be charge a higher interest. Therefore, good financial ratio analysing can help business to avoid unnecessary risks.The positive use of financial ratios has been of two types: by accountants and analysts to forecast future financial variables.。

财金英语教程参考答案

财金英语教程参考答案Chapter 1: Introduction to Finance1. What is finance?- Finance is the management of money and includesactivities such as investing, borrowing, lending, budgeting, saving, and forecasting.2. What are the three main functions of finance?- The three main functions of finance are planning, acquiring, and managing financial resources.3. What is the time value of money?- The time value of money is the concept that a sum of money is worth more now than the same sum in the future dueto its potential earning capacity.4. How does inflation affect the value of money?- Inflation erodes the purchasing power of money over time, meaning that the same amount of money will buy fewer goodsand services in the future.5. What is the difference between a bond and a stock?- A bond is a debt instrument where an investor lends money to an entity in exchange for interest payments, while a stock represents ownership in a company and offers thepotential for capital gains and dividends.Chapter 2: Financial Statements1. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, cash flow statement, and statement of changes in equity.2. What is the purpose of a balance sheet?- The balance sheet provides a snapshot of a company's financial position at a specific point in time, showing its assets, liabilities, and equity.3. How is net income calculated?- Net income is calculated by subtracting all expensesfrom the total revenue of a company during a specific period.4. What does the cash flow statement show?- The cash flow statement shows the inflow and outflow of cash within a business over a period of time, categorizedinto operating, investing, and financing activities.5. What is the statement of changes in equity?- The statement of changes in equity shows the changes in the equity accounts of a company over a period of time, including retained earnings, capital contributions, and other comprehensive income.Chapter 3: Financial Analysis1. What are the main types of financial analysis?- The main types of financial analysis are ratio analysis,horizontal analysis, vertical analysis, and trend analysis.2. What is the purpose of ratio analysis?- Ratio analysis is used to evaluate a company's financial health by comparing various financial ratios such asliquidity, profitability, and leverage ratios.3. What is horizontal analysis?- Horizontal analysis involves comparing financial statement items over multiple periods to identify trends and changes in performance.4. What is vertical analysis?- Vertical analysis, also known as common-size analysis,is a method of financial statement analysis where each itemis expressed as a percentage of a base figure, typicallytotal assets or total revenue.5. What is trend analysis?- Trend analysis involves examining the historical data of financial metrics over time to predict future trends and performance.Chapter 4: Risk Management1. What is risk management?- Risk management is the process of identifying, assessing, and prioritizing potential risks to an investment or project, and taking steps to mitigate or avoid these risks.2. What are the types of risks in finance?- The types of risks in finance include market risk,credit risk, liquidity risk, operational risk, and legal risk.3. What is diversification?- Diversification is a risk management strategy that involves spreading investments across various financial instruments, industries, or geographic regions to reduce overall risk.4. What is hedging?- Hedging is a risk management technique used to reducethe risk of price fluctuations in an asset by taking an offsetting position in a related security.5. What is the role of insurance in risk management?- Insurance is a risk management tool that providesfinancial protection against potential losses or damages by transferring the risk to an insurance company in exchange for a premium.Chapter 5: Investment Strategies1. What are the different types of investment strategies?- Types of investment strategies include passive investing, active investing, value investing, growth investing, and income investing.2. What is the difference between passive and active investing?- Passive investing involves a "set it and forget it" approach, typically using index funds, while active investingrequires regular buying and selling of individual securities based on market research and analysis.3. What is value investing?- Value investing is an investment strategy that involves buying stocks that are considered undervalued by the market, with the expectation that their true value will eventually be recognized.4. What is growth investing?- Growth investing focuses on companies that are expected to grow at an above-average rate compared to the market, often investing in companies with strong competitive advantages and high growth potential.5. What is income investing?- Income investing is an investment strategy aimed at generating a steady stream of income from investments, typically through dividends or interest payments.Chapter 6: International Finance1. What is international。

3财务管理chapter 3(new)

b. Analysis on debt to total assets : * From the standpoint of the creditors, debt ratio is the lower the better. * From the standpoint of the shareholders, when return on capital is higher than borrowing rate, debt ratio is the higher the better. * From the standpoint of the managers,high , debt ratio means high risks. But if the debt ratio is too low, they will be accused of hanging back and lack of confidence in the future. So they must be trade-off between the two.

(2)Equity ratio

a. Formula equity ratio=(total liabilities÷ shareholders’ equity) *100% b. Analysis on equity ratio * It reflects the relationship between capital from creditors and that from shareholders, and reflects the stability of the company’s basic financial structure. * It also reflects the degree of capital from creditors’ protection by shareholders’ equity.

chapter3internationalfinancialmarkets练习答案+详解

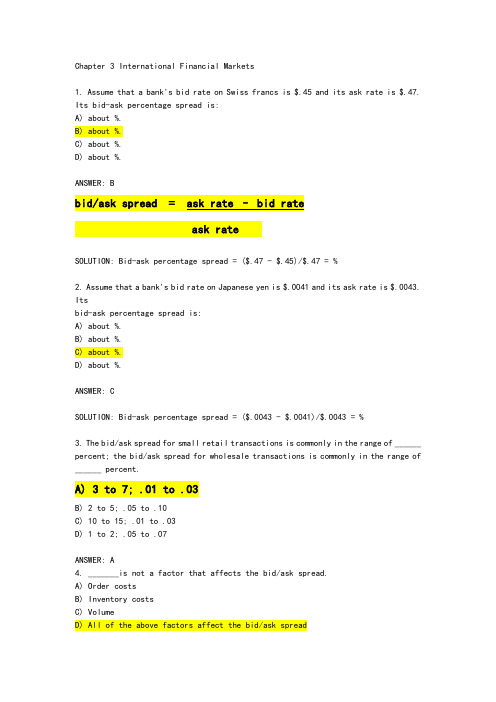

Chapter 3 International Financial Markets1. Assume that a bank's bid rate on Swiss francs is $.45 and its ask rate is $.47. Its bid-ask percentage spread is:A) about %.B) about %.C) about %.D) about %.ANSWER: Bask rateSOLUTION: Bid-ask percentage spread = ($.47 - $.45)/$.47 = %2. Assume that a bank's bid rate on Japanese yen is $.0041 and its ask rate is $.0043. Itsbid-ask percentage spread is:A) about %.B) about %.C) about %.D) about %.ANSWER: CSOLUTION: Bid-ask percentage spread = ($.0043 - $.0041)/$.0043 = %3. The bid/ask spread for small retail transactions is commonly in the range of ______ percent; the bid/ask spread for wholesale transactions is commonly in the range of ______ percent.A) 3 to 7; .01 to .03B) 2 to 5; .05 to .10C) 10 to 15; .01 to .03D) 1 to 2; .05 to .07ANSWER: A4. _______is not a factor that affects the bid/ask spread.A) Order costsB) Inventory costsC) VolumeD) All of the above factors affect the bid/ask spreadANSWER: D5. The forward rate is the exchange rate used for immediate exchange of currencies.A) true.B) false.ANSWER: B6. The ask quote is the price for which a bank offers to sell a currency.A) true.B) false.ANSWER: A7. According to the text, the forward rate is commonly used for:A) hedging.B) Eurocurrency transactions.C) Eurocredit transactions.D) Eurobond transactions.ANSWER: A8. If a U.S. firm desires to avoid the risk from exchange rate fluctuations, and it is receiving100,000 in 90 days, it could:A) obtain a 90-day forward purchase contract on euros.B) obtain a 90-day forward sale contract on euros.C) purchase euros 90 days from now at the spot rate.D) sell euros 90 days from now at the spot rate.ANSWER: B9. If a U.S. firm desires to avoid the risk from exchange rate fluctuations, and it will needC$200,000 in 90 days to make payment on imports from Canada, it could:A) obtain a 90-day forward purchase contract on Canadian dollars.B) obtain a 90-day forward sale contract on Canadian dollars.C) purchase Canadian dollars 90 days from now at the spot rate.D) sell Canadian dollars 90 days from now at the spot rate.ANSWER: A10. Assume the Canadian dollar is equal to $.88 and the Peruvian Sol is equal to $.35. Thevalue of the Peruvian Sol in Canadian dollars is:A) about .3621 Canadian dollars.B) about .3977 Canadian dollars.C) about Canadian dollars.D) about Canadian dollars.ANSWER: BSOLUTION: $.35/$.88 = .397711. Which of the following is not true with respect to spot market liquidity?现货市场流动性A) The more willing buyers and sellers there are, the more liquid a market is.B) The spot markets for heavily traded currencies such as the Japanese yen are very liquid.C) A currency's liquidity affects the ease with which an MNC can obtain or sell that currency.D) If a currency is illiquid, an MNC is typically able to quickly purchase that currency at a reasonable exchange rate.ANSWER: D12. Forward markets for currencies of developing countries are:A) prohibited.B) less liquid than markets for developed countries.C) more liquid than markets for developed countries.D) only available for use by government agencies.发展中国家现货市场流动性较低ANSWER: B13. A forward contract can be used to lock in the __________ of a specified currency for afuture point in time.A) purchase priceB) sale priceC) A or BD) none of the aboveANSWER: C14. The forward market:A) for euros is very illiquid.B) for Eastern European countries is very liquid.C) does not exist for some currencies.D) none of the aboveANSWER: C15. _______ is not a bank characteristic important to customers in need of foreign exchange.A) Quote competitivenessB) Speed of executionC) Forecasting adviceD) Advice about current market conditionsE) All of the above are important bank characteristics to customers in need of foreign exchange.ANSWER: E16. The Basel II accord would:A) replace the Basel Accord.B) reduce the amount of capital banks are required to hold.C) require banks to take more risks and to document their risk.D) correct some inconsistencies that still exist. Operation riskANSWER: D17. The international money market primarily concentrates on:A) short-term lending (one year or less). IMM短期借款B) medium-term lending.C) long-term lending.D) placing bonds with investors.E) placing newly issued stock in foreign markets.ANSWER: A18. The international credit market primarily concentrates on:A) short-term lending (less than one year).B) medium-term lending.C) long-term lending. 欧洲信用贷款市场D) providing an exchange of foreign currencies for firms who need them.E) placing newly issued stock in foreign markets.ANSWER: B19. The main participants in the international money market are:A) consumers.B) small firms.C) large corporations.D) small European firms needing European currencies for international trade.ANSWER: C20. LIBOR is: 同业拆借利率A) the interest rate commonly charged for loans between banks.B) the average inflation rate in European countries.C) the maximum loan rate ceiling on loans in the international money market.D) the maximum deposit rate ceiling on deposits in the international money market.E) the maximum interest rate offered on bonds that are issued in London. ANSWER: A21. A syndicated Eurocredit loan:A) represents a loan by a single bank to a syndicate of corporations.B) represents a loan by a single bank to a syndicate of country governments.C) represents a direct loan by a syndicate of oil-producing exporters to a less developedcountry.D) represents a loan by a group of banks to a borrower.E) A and BANSWER: D22. The international money market is primarily served by:A) the governments of European countries, which directly intervene in foreign currencymarkets.B) government agencies such as the International Monetary Fund that enhance development of countries.C) several large banks that accept deposits and provide loans in various currencies.D) small banks that convert foreign currency for tourists and business visitors. ANSWER: C。

公司理财罗斯英文原书第九版第三章

3-17

Potential Problems

There is no underlying theory, so there is no way to know which ratios are most relevant. Benchmarking (标杆学习) is difficult for diversified firms. Globalization and international competition makes comparison more difficult because of differences in accounting regulations. Firms use varying accounting procedures. Firms have different fiscal years. Extraordinary, or one-time, events

2904 + (196 + 457) – 98 = 3465 3465 / 967 = 3.6 times

3-13

EV Multiple(企业倍数) = EV / EBITDA

Using Financial Statements

Ratios are not very helpful by themselves: they need to be compared to something Time-Trend Analysis(时间趋势分析 )

98 / 540 = .18 times

3-6

Computing Leverage Ratios

Total Debt Ratio = (TA – TE) / TA (负债比 率)

Financial_Ratios

4

Profitability Ratios

3 elements of the profitability analysis: • Analysing on sales and trading margin

– focus on gross profit

• Analysing on the control of expenses

• Dividend payout ratio = Dividends per share *100 Earnings per share • Price Earnings ratio = Market price per share Earnings per share

14

Horizontal analysis/Trend analysis

• Quick Ratio = Current Assets – Inventory – Prepayments Current Liabilities – Bank Overdraft

8

Asset Management or Activity Ratios

• Efficiency of asset usage

6

Liquidity or Short-Term Solvency ratios

Short-term funds management • Working capital management is important as it signals the firm’s ability to meet short term debt obligations. For example: Current ratio • The ideal benchmark for the current ratio is RM2 : RM1 where there are two Ringgit of current assets (CA) to cover RM1 of current liabilities (CL). The acceptable benchmark is RM1 : RM1, but a ratio below RM1CA : RM1CL represents liquidity riskiness as there is insufficient current assets to cover RM1 of current liabilities.

财务管理基础斯坦利布洛克Chapter (12)

Delete Depreciation FC = ($60,000 − $20,000) = $40,000 = 33,333

• Break-Even analysis based on cash flows

P − VC $2.00 − $0.80 $1.20

Q=(FC-D)/(p-v)

Cash Break-Even Analysis Chart

Q2

Q1

2.2 Operating Leverage

Definition: •Operating leverage reflects the extent to which fixed assets and associated fixed costs are utilized in business. •A firm with relatively high fixed operating costs will experience more variable operating income if sales change.

财务管理基础斯坦利布洛克Chapter (3)

Profitability Ratios -DuPont System of Analysis(cont’d)

Profitability Ratios -DuPont System of Analysis(cont’d)

The difference of ROA and ROE • The big factor that separates ROE and ROA is financial leverage, or debt. – If a company carries no debt, its shareholders' equity and its total assets will be the same. – If ROE>ROA, financial leverage or debt

Ratio Analysis

Chapter 3- financial ratio analysis II. Interpreting ratios

think of the factors which would make distortions on the financial reporting of the firm. Industry average or the best one of this industry. Suitable to d company. Inflation impact. Seasonal reasons. Using different accounting methods.

Q: How to use Financial Ratios?

• Stockholders & Potential investors – profitability, with secondary consideration given to debt utilization, liquidity, and other ratios. Since stockholders are the ultimate owners of the firm, they are primarily concerned with profits or the return on their investment. • Financial managers – All the ratios. Profitability, liquidity, debt, asset.

罗斯公司理财Chap003全英文题库及答案

Chapter 03 Financial Statements Analysis and Long-Term Planning Answer KeyMultiple Choice Questions1. One key reason a long-term financial plan is developed is because:A. the plan determines your financial policy.B. the plan determines your investment policy.C. there are direct connections between achievable corporate growth and the financial policy.D. there is unlimited growth possible in a well-developed financial plan.E. None of the above.Difficulty level: EasyTopic: LONG-TERM PLANNINGType: DEFINITIONS2. Projected future financial statements are called:A. plug statements.B. pro forma statements.C. reconciled statements.D. aggregated statements.E. none of the above.Difficulty level: EasyTopic: PRO FORMA STATEMENTSType: DEFINITIONS3. The percentage of sales method:A. requires that all accounts grow at the same rate.B. separates accounts that vary with sales and those that do not vary with sales.C. allows the analyst to calculate how much financing the firm will need to support the predicted sales level.D. Both A and B.E. Both B and C.Difficulty level: MediumTopic: PERCENTAGE OF SALESType: DEFINITIONS4. A _____ standardizes items on the income statement and balance sheet as a percentage of total sales and total assets, respectively.A. tax reconciliation statementB. statement of standardizationC. statement of cash flowsD. common-base year statementE. common-size statementDifficulty level: EasyTopic: COMMON-SIZE STATEMENTSType: DEFINITIONS5. Relationships determined from a firm's financial information and used for comparison purposes are known as:A. financial ratios.B. comparison statements.C. dimensional analysis.D. scenario analysis.E. solvency analysis.Difficulty level: EasyTopic: FINANCIAL RATIOSType: DEFINITIONS6. Financial ratios that measure a firm's ability to pay its bills over the short run without undue stress are known as _____ ratios.A. asset managementB. long-term solvencyC. short-term solvencyD. profitabilityE. market valueDifficulty level: EasyTopic: SHORT-TERM SOLVENCY RATIOSType: DEFINITIONS7. The current ratio is measured as:A. current assets minus current liabilities.B. current assets divided by current liabilities.C. current liabilities minus inventory, divided by current assets.D. cash on hand divided by current liabilities.E. current liabilities divided by current assets.Difficulty level: EasyTopic: CURRENT RATIOType: DEFINITIONS8. The quick ratio is measured as:A. current assets divided by current liabilities.B. cash on hand plus current liabilities, divided by current assets.C. current liabilities divided by current assets, plus inventory.D. current assets minus inventory, divided by current liabilities.E. current assets minus inventory minus current liabilities.Difficulty level: EasyTopic: QUICK RATIOType: DEFINITIONS9. The cash ratio is measured as:A. current assets divided by current liabilities.B. current assets minus cash on hand, divided by current liabilities.C. current liabilities plus current assets, divided by cash on hand.D. cash on hand plus inventory, divided by current liabilities.E. cash on hand divided by current liabilities.Difficulty level: MediumTopic: CASH RATIOType: DEFINITIONS10. Ratios that measure a firm's financial leverage are known as _____ ratios.A. asset managementB. long-term solvencyC. short-term solvencyD. profitabilityE. market valueDifficulty level: EasyTopic: LONG-TERM SOLVENCY RATIOSType: DEFINITIONS11. The financial ratio measured as total assets minus total equity, divided by total assets, is the:A. total debt ratio.B. equity multiplier.C. debt-equity ratio.D. current ratio.E. times interest earned ratio.Difficulty level: EasyTopic: TOTAL DEBT RATIOType: DEFINITIONS12. The debt-equity ratio is measured as total:A. equity minus total debt.B. equity divided by total debt.C. debt divided by total equity.D. debt plus total equity.E. debt minus total assets, divided by total equity.Difficulty level: EasyTopic: DEBT-EQUITY RATIOType: DEFINITIONS13. The equity multiplier ratio is measured as total:A. equity divided by total assets.B. equity plus total debt.C. assets minus total equity, divided by total assets.D. assets plus total equity, divided by total debt.E. assets divided by total equity.Difficulty level: MediumTopic: EQUITY MULTIPLIERType: DEFINITIONS14. The financial ratio measured as earnings before interest and taxes, divided by interest expense is the:A. cash coverage ratio.B. debt-equity ratio.C. times interest earned ratio.D. gross margin.E. total debt ratio.Difficulty level: MediumTopic: TIMES INTEREST EARNED RATIOType: DEFINITIONS15. The financial ratio measured as earnings before interest and taxes, plus depreciation, divided by interest expense, is the:A. cash coverage ratio.B. debt-equity ratio.C. times interest earned ratio.D. gross margin.E. total debt ratio.Difficulty level: MediumTopic: CASH COVERAGE RATIOType: DEFINITIONS16. Ratios that measure how efficiently a firm uses its assets to generate sales are known as _____ ratios.A. asset managementB. long-term solvencyC. short-term solvencyD. profitabilityE. market valueDifficulty level: EasyTopic: ASSET MANAGEMENT RATIOSType: DEFINITIONS17. The inventory turnover ratio is measured as:A. total sales minus inventory.B. inventory times total sales.C. cost of goods sold divided by inventory.D. inventory times cost of goods sold.E. inventory plus cost of goods sold.Difficulty level: MediumTopic: INVENTORY TURNOVERType: DEFINITIONS18. The financial ratio days' sales in inventory is measured as:A. inventory turnover plus 365 days.B. inventory times 365 days.C. inventory plus cost of goods sold, divided by 365 days.D. 365 days divided by the inventory.E. 365 days divided by the inventory turnover.Difficulty level: MediumTopic: DAYS' SALES IN INVENTORYType: DEFINITIONS19. The receivables turnover ratio is measured as:A. sales plus accounts receivable.B. sales divided by accounts receivable.C. sales minus accounts receivable, divided by sales.D. accounts receivable times sales.E. accounts receivable divided by sales.Difficulty level: MediumTopic: RECEIVABLES TURNOVERType: DEFINITIONS20. The financial ratio days' sales in receivables is measured as:A. receivables turnover plus 365 days.B. accounts receivable times 365 days.C. accounts receivable plus sales, divided by 365 days.D. 365 days divided by the receivables turnover.E. 365 days divided by the accounts receivable.Difficulty level: MediumTopic: DAYS' SALES IN RECEIVABLESType: DEFINITIONS21. The total asset turnover ratio is measured as:A. sales minus total assets.B. sales divided by total assets.C. sales times total assets.D. total assets divided by sales.E. total assets plus sales.Difficulty level: EasyTopic: TOTAL ASSET TURNOVERType: DEFINITIONS22. Ratios that measure how efficiently a firm's management uses its assets and equity to generate bottom line net income are known as _____ ratios.A. asset managementB. long-term solvencyC. short-term solvencyD. profitabilityE. market valueDifficulty level: EasyTopic: PROFITABILITY RATIOSType: DEFINITIONS23. The financial ratio measured as net income divided by sales is known as the firm's:A. profit margin.B. return on assets.C. return on equity.D. asset turnover.E. earnings before interest and taxes.Difficulty level: EasyTopic: PROFIT MARGINType: DEFINITIONS24. The financial ratio measured as net income divided by total assets is known as the firm's:A. profit margin.B. return on assets.C. return on equity.D. asset turnover.E. earnings before interest and taxes.Difficulty level: EasyTopic: RETURN ON ASSETSType: DEFINITIONS25. The financial ratio measured as net income divided by total equity is known as the firm's:A. profit margin.B. return on assets.C. return on equity.D. asset turnover.E. earnings before interest and taxes.Difficulty level: EasyTopic: RETURN ON EQUITYType: DEFINITIONS26. The financial ratio measured as the price per share of stock divided by earnings per share is known as the:A. return on assets.B. return on equity.C. debt-equity ratio.D. price-earnings ratio.E. Du Pont identity.Difficulty level: EasyTopic: PRICE-EARNINGS RATIOType: DEFINITIONS27. The market-to-book ratio is measured as:A. total equity divided by total assets.B. net income times market price per share of stock.C. net income divided by market price per share of stock.D. market price per share of stock divided by earnings per share.E. market value of equity per share divided by book value of equity per share.Difficulty level: MediumTopic: MARKET-TO-BOOK RATIOType: DEFINITIONS28. The _____ breaks down return on equity into three component parts.A. Du Pont identityB. return on assetsC. statement of cash flowsD. asset turnover ratioE. equity multiplierDifficulty level: MediumTopic: DU PONT IDENTITYType: DEFINITIONS29. The External Funds Needed (EFN) equation does not measure the:A. additional asset requirements given a change in sales.B. additional total liabilities raised given the change in sales.C. rate of return to shareholders given the change in sales.D. net income expected to be earned given the change in sales.E. None of the above.Difficulty level: MediumTopic: EXTERNAL FUNDS NEEDEDType: DEFINITIONS30. To calculate sustainable growth rate without using return on equity, the analyst needs the:A. profit margin.B. payout ratio.C. debt-to-equity ratio.D. total asset turnover.E. All of the above.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS31. Growth can be reconciled with the goal of maximizing firm value:A. because greater growth always adds to value.B. because growth must be an outcome of decisions that maximize NPV.C. because growth and wealth maximization are the same.D. because growth of any type cannot decrease value.E. None of the above.Difficulty level: MediumTopic: GROWTHType: DEFINITIONS32. Sustainable growth can be determined by the:A. profit margin, total asset turnover and the price to earnings ratio.B. profit margin, the payout ratio, the debt-to-equity ratio, and the asset requirement or asset turnover ratio.C. Total growth less capital gains growth.D. Either A or B.E. None of the above.Difficulty level: MediumTopic: SUSTAINABLE GROWTHType: DEFINITIONS33. Which of the following will increase sustainable growth?A. Buy back existing stockB. Decrease debtC. Increase profit marginD. Increase asset requirement or asset turnover ratioE. Increase dividend payout ratioDifficulty level: MediumTopic: SUSTAINABLE GROWTHType: DEFINITIONS34. The main objective of long-term financial planning models is to:A. determine the asset requirements given the investment activities of the firm.B. plan for contingencies or uncertain events.C. determine the external financing needs.D. All of the above.E. None of the above.Difficulty level: MediumTopic: LONG TERM PLANNINGType: DEFINITIONS35. On a common-size balance sheet, all _____ accounts are shown as a percentage of _____.A. income; total assetsB. liability; net incomeC. asset; salesD. liability; total assetsE. equity; salesDifficulty level: MediumTopic: COMMON-SIZE BALANCE SHEETType: DEFINITIONS36. Which one of the following statements is correct concerning ratio analysis?A. A single ratio is often computed differently by different individuals.B. Ratios do not address the problem of size differences among firms.C. Only a very limited number of ratios can be used for analytical purposes.D. Each ratio has a specific formula that is used consistently by all analysts.E. Ratios can not be used for comparison purposes over periods of time.Difficulty level: MediumTopic: RATIO ANALYSISType: DEFINITIONS37. Which of the following are liquidity ratios?I. cash coverage ratioII. current ratioIII. quick ratioIV. inventory turnoverA. II and III onlyB. I and II onlyC. II, III, and IV onlyD. I, III, and IV onlyE. I, II, III, and IVDifficulty level: MediumTopic: LIQUIDITY RATIOSType: DEFINITIONS38. An increase in which one of the following accounts increases a firm's current ratio without affecting its quick ratio?A. accounts payableB. cashC. inventoryD. accounts receivableE. fixed assetsDifficulty level: MediumTopic: LIQUIDITY RATIOSType: DEFINITIONS39. A supplier, who requires payment within ten days, is most concerned with which one of the following ratios when granting credit?A. currentB. cashC. debt-equityD. quickE. total debtDifficulty level: MediumTopic: LIQUIDITY RATIOSType: DEFINITIONS40. A firm has a total debt ratio of .47. This means that that firm has 47 cents in debt for every:A. $1 in equity.B. $1 in total sales.C. $1 in current assets.D. $.53 in equity.E. $.53 in total assets.Difficulty level: MediumTopic: LONG-TERM SOLVENCY RATIOSType: DEFINITIONS41. The long-term debt ratio is probably of most interest to a firm's:A. credit customers.B. employees.C. suppliers.D. mortgage holder.E. shareholders.Difficulty level: MediumTopic: LONG-TERM SOLVENCY RATIOSType: DEFINITIONS42. A banker considering loaning a firm money for ten years would most likely prefer the firm have a debt ratio of _____ and a times interest earned ratio of _____.A. .75; .75B. .50; 1.00C. .45; 1.75D. .40; 2.50E. .35; 3.00Difficulty level: MediumTopic: LONG-TERM SOLVENCY RATIOSType: DEFINITIONS43. From a cash flow position, which one of the following ratios best measures a firm's ability to pay the interest on its debts?A. times interest earned ratioB. cash coverage ratioC. cash ratioD. quick ratioE. Interval measureDifficulty level: MediumTopic: LONG-TERM SOLVENCY RATIOSType: DEFINITIONS44. The higher the inventory turnover measure, the:A. faster a firm sells its inventory.B. faster a firm collects payment on its sales.C. longer it takes a firm to sell its inventory.D. greater the amount of inventory held by a firm.E. lesser the amount of inventory held by a firm.Difficulty level: MediumTopic: ASSET MANAGEMENT RATIOSType: DEFINITIONS45. Which one of the following statements is correct if a firm has a receivables turnover measure of 10?A. It takes a firm 10 days to collect payment from its customers.B. It takes a firm 36.5 days to sell its inventory and collect the payment from the sale.C. It takes a firm 36.5 days to pay its creditors.D. The firm has an average collection period of 36.5 days.E. The firm has ten times more in accounts receivable than it does in cash.Difficulty level: MediumTopic: ASSET MANAGEMENT RATIOSType: DEFINITIONS46. A total asset turnover measure of 1.03 means that a firm has $1.03 in:A. total assets for every $1 in cash.B. total assets for every $1 in total debt.C. total assets for every $1 in equity.D. sales for every $1 in total assets.E. long-term assets for every $1 in short-term assets.Difficulty level: MediumTopic: ASSET MANAGEMENT RATIOSType: DEFINITIONS47. Puffy's Pastries generates five cents of net income for every $1 in sales. Thus, Puffy's has a _____ of 5%.A. return on assetsB. return on equityC. profit marginD. Du Pont measureE. total asset turnoverDifficulty level: MediumTopic: PROFITABILITY RATIOSType: DEFINITIONS48. If a firm produces a 10% return on assets and also a 10% return on equity, then the firm:A. has no debt of any kind.B. is using its assets as efficiently as possible.C. has no net working capital.D. also has a current ratio of 10.E. has an equity multiplier of 2.Difficulty level: MediumTopic: PROFITABILITY RATIOSType: DEFINITIONS49. If shareholders want to know how much profit a firm is making on their entire investment in the firm, the shareholders should look at the:A. profit margin.B. return on assets.C. return on equity.D. equity multiplier.E. earnings per share.Difficulty level: MediumTopic: PROFITABILITY RATIOSType: DEFINITIONS50. BGL Enterprises increases its operating efficiency such that costs decrease while sales remain constant. As a result, given all else constant, the:A. return on equity will increase.B. return on assets will decrease.C. profit margin will decline.D. equity multiplier will decrease.E. price-earnings ratio will increase.Difficulty level: MediumTopic: PROFITABILITY RATIOSType: DEFINITIONS51. The only difference between Joe's and Moe's is that Joe's has old, fully depreciated equipment. Moe's just purchased all new equipment which will be depreciated over eight years. Assuming all else equal:A. Joe's will have a lower profit margin.B. Joe's will have a lower return on equity.C. Moe's will have a higher net income.D. Moe's will have a lower profit margin.E. Moe's will have a higher return on assets.Difficulty level: MediumTopic: PROFITABILITY RATIOSType: DEFINITIONS52. Last year, Alfred's Automotive had a price-earnings ratio of 15. This year, the price earnings ratio is 18. Based on this information, it can be stated with certainty that:A. the price per share increased.B. the earnings per share decreased.C. investors are paying a higher price for each share of stock purchased.D. investors are receiving a higher rate of return this year.E. either the price per share, the earnings per share, or both changed.Difficulty level: MediumTopic: MARKET VALUE RATIOSType: DEFINITIONS53. Turner's Inc. has a price-earnings ratio of 16. Alfred's Co. has a price-earnings ratio of 19. Thus, you can state with certainty that one share of stock in Alfred's:A. has a higher market price than one share of stock in Turner's.B. has a higher market price per dollar of earnings than does one share of Turner's.C. sells at a lower price per share than one share of Turner's.D. represents a larger percentage of firm ownership than does one share of Turner's stock.E. earns a greater profit per share than does one share of Turner's stock.Difficulty level: MediumTopic: MARKET VALUE RATIOType: DEFINITIONS54. Which two of the following are most apt to cause a firm to have a higher price-earnings ratio?I. slow industry outlookII. high prospect of firm growthIII. very low current earningsIV. investors with a low opinion of the firmA. I and II onlyB. II and III onlyC. II and IV onlyD. I and III onlyE. III and IV onlyDifficulty level: MediumTopic: MARKET VALUE RATIOSType: DEFINITIONS55. Vinnie's Motors has a market-to-book ratio of 3. The book value per share is $4.00. Holding market-to-book constant, a $1 increase in the book value per share will:A. cause the accountants to increase the equity of the firm by an additional $2.B. increase the market price per share by $1.C. increase the market price per share by $12.D. tend to cause the market price per share to rise.E. only affect book values but not market values.Difficulty level: MediumTopic: MARKET VALUE RATIOSType: DEFINITIONS56. Which one of the following sets of ratios applies most directly to shareholders?A. return on assets and profit marginB. quick ratio and times interest earnedC. price-earnings ratio and debt-equity ratioD. market-to-book ratio and price-earnings ratioE. cash coverage ratio and times equity multiplierDifficulty level: MediumTopic: MARKET VALUE RATIOSType: DEFINITIONS57. The three parts of the Du Pont identity can be generally described as:I. operating efficiency, asset use efficiency and firm profitability.II. financial leverage, operating efficiency and asset use efficiency.III. the equity multiplier, the profit margin and the total asset turnover.IV. the debt-equity ratio, the capital intensity ratio and the profit margin.A. I and II onlyB. II and III onlyC. I and IV onlyD. I and III onlyE. III and IV onlyDifficulty level: MediumTopic: DU PONT IDENTITYType: DEFINITIONS58. If a firm decreases its operating costs, all else constant, then:A. the profit margin increases while the equity multiplier decreases.B. the return on assets increases while the return on equity decreases.C. the total asset turnover rate decreases while the profit margin increases.D. both the profit margin and the equity multiplier increase.E. both the return on assets and the return on equity increase.Difficulty level: MediumTopic: DU PONT IDENTITYType: DEFINITIONS59. Which one of the following statements is correct?A. Book values should always be given precedence over market values.B. Financial statements are frequently the basis used for performance evaluations.C. Historical information has no value when predicting the future.D. Potential lenders place little value on financial statement information.E. Reviewing financial information over time has very limited value.Difficulty level: MediumTopic: EVALUATING FINANCIAL STATEMENTSType: DEFINITIONS60. It is easier to evaluate a firm using its financial statements when the firm:A. is a conglomerate.B. is global in nature.C. uses the same accounting procedures as other firms in its industry.D. has a different fiscal year than other firms in its industry.E. tends to have one-time events such as asset sales and property acquisitions.Difficulty level: MediumTopic: EVALUATING FINANCIAL STATEMENTSType: DEFINITIONS61. Which two of the following represent the most effective methods of directly evaluating the financial performance of a firm?I. comparing the current financial ratios to those of the same firm from prior time periodsII. comparing a firm's financial ratios to those of other firms in the firm's peer group who have similar operationsIII. comparing the financial statements of the firm to the financial statements of similar firms operating in other countriesIV. comparing the financial ratios of the firm to the average ratios of all firms located in the same geographic areaA. I and II onlyB. II and III onlyC. III and IV onlyD. I and IV onlyE. I and III onlyDifficulty level: MediumTopic: EVALUATING FINANCIAL STATEMENTSType: DEFINITIONS62. In the financial planning model, external funds needed (EFN) is equal to changes inA. assets - (liabilities - equity).B. assets - (liabilities + equity).C. (assets + liabilities - equity).D. (assets + equity - liabilities).E. assets - equity.Difficulty level: MediumTopic: EXTERNAL FUNDS NEEDEDType: DEFINITIONS63. Which of the following represent problems encountered when comparing the financial statements of one firm with those of another firm?I. Either one, or both, of the firms may be conglomerates and thus have unrelated lines of business.II. The operations of the two firms may vary geographically.III. The firms may use differing accounting methods for inventory purposes.IV. The two firms may be seasonal in nature and have different fiscal year ends.A. I and II onlyB. II and III onlyC. I, III, and IV onlyD. I, II, and III onlyE. I, II, III, and IVDifficulty level: MediumTopic: EVALUATING FINANCIAL STATEMENTSType: DEFINITIONS64. A firm's sustainable growth rate in sales directly depends on its:A. debt to equity ratio.B. profit margin.C. dividend policy.D. asset efficiency.E. All of the above.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS65. The sustainable growth rate will be equivalent to the internal growth rate when:A. a firm has no debt.B. the growth rate is positive.C. the plowback ratio is positive but less than 1.D. a firm has a debt-equity ratio exactly equal to 1.E. net income is greater than zero.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS66. The sustainable growth rate:A. assumes there is no external financing of any kind.B. is normally higher than the internal growth rate.C. assumes the debt-equity ratio is variable.D. is based on receiving additional external debt and equity financing.E. assumes that 100% of all income is retained by the firm.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS67. If a firm bases its growth projection on the rate of sustainable growth, and shows positive net income, then the:A. fixed assets will have to increase at the same rate, regardless of the current capacity level.B. number of common shares outstanding will increase at the same rate of growth.C. debt-equity ratio will have to increase.D. debt-equity ratio will remain constant while retained earnings increase.E. fixed assets, debt-equity ratio, and number of common shares outstanding will all increase.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS68. Marcie's Mercantile wants to maintain its current dividend policy, which is a payout ratio of 40%. The firm does not want to increase its equity financing but is willing to maintain its current debt-equity ratio. Given these requirements, the maximum rate at which Marcie's can grow is equal to:A. 40% of the internal rate of growth.B. 60% of the internal rate of growth.C. the internal rate of growth.D. the sustainable rate of growth.E. 60% of the sustainable rate of growth.Difficulty level: MediumTopic: SUSTAINABLE GROWTH RATEType: DEFINITIONS69. One of the primary weaknesses of many financial planning models is that they:A. rely too much on financial relationships and too little on accounting relationships.B. are iterative in nature.C. ignore the goals and objectives of senior management.D. are based solely on best case assumptions.E. ignore the size, risk, and timing of cash flows.Difficulty level: MediumTopic: FINANCIAL PLANNING MODELSType: DEFINITIONS70. Financial planning, when properly executed:A. ignores the normal restraints encountered by a firm.B. ensures that the primary goals of senior management are fully achieved.C. reduces the necessity of daily management oversight of the business operations.D. helps ensure that proper financing is in place to support the desired level of growth.E. eliminates the need to plan more than one year in advance.Difficulty level: MediumTopic: FINANCIAL PLANNINGType: DEFINITIONS71. When examining the EBITDA ratio, lower numbers are:A. considered good.B. considered mediocre.C. considered poor.D. indifferent to higher numbers.E. it is impossible to garner information from this ratio.Difficulty level: MediumTopic: EBITDA RATIOType: DEFINITIONS。

公司理财精要版原书第12版习题库答案Ross12e_Chapter03_TB

Fundamentals of Corporate Finance, 12e (Ross)Chapter 3 Working with Financial Statements1) Which one of the following is a source of cash for a tax-exempt firm?A) Increase in accounts receivableB) Increase in depreciationC) Decrease in accounts payableD) Increase in common stockE) Increase in inventory2) Which one of the following is a use of cash?A) Decrease in fixed assetsB) Decrease in inventoryC) Increase in long-term debtD) Decrease in accounts receivablesE) Decrease in accounts payable3) Which one of the following is a source of cash?A) Repurchase of common stockB) Acquisition of debtC) Purchase of inventoryD) Payment to a supplierE) Granting credit to a customer4) Which one of the following is a source of cash?A) Increase in accounts receivableB) Decrease in common stockC) Increase in fixed assetsD) Decrease in accounts payableE) Decrease in inventory5) On the statement of cash flows, which one of the following is considered a financing activity?A) Increase in inventoryB) Decrease in accounts payableC) Increase in net working capitalD) Dividends paidE) Decrease in fixed assets6) On the statement of cash flows, which one of the following is considered an operating activity?A) Increase in net fixed assetsB) Decrease in accounts payableC) Purchase of equipmentD) Dividends paidE) Repayment of long-term debt7) According to the statement of cash flows, an increase in inventory will ________ the cash flow from ________ activities.A) increase; operatingB) decrease; financingC) decrease; operatingD) increase; financingE) increase; investment8) According to the statement of cash flows, an increase in interest expense will ________ the cash flow from ________ activities.A) decrease; operatingB) decrease; financingC) increase; operatingD) increase; financingE) Increase; investment9) Activities of a firm that require the spending of cash are known as:A) sources of cash.B) uses of cash.C) cash collections.D) cash receipts.E) cash on hand.10) The sources and uses of cash over a stated period of time are reflected on the:A) income statement.B) balance sheet.C) tax reconciliation statement.D) statement of cash flows.E) statement of operating position.11) A common-size income statement is an accounting statement that expresses all of a firm's expenses as a percentage of:A) total assets.B) total equity.C) net income.D) taxable income.E) sales.12) Which one of the following standardizes items on the income statement and balance sheet relative to their values as of a chosen point in time?A) Statement of standardizationB) Statement of cash flowsC) Common-base year statementD) Common-size statementE) Base reconciliation statement13) On a common-size balance sheet all accounts for the current year are expressed as a percentage of:A) sales for the period.B) the base year sales.C) total equity for the base year.D) total assets for the current year.E) total assets for the base year.14) On a common-base year financial statement, accounts receivables for the current year will be expressed relative to which one of the following?A) Current year salesB) Current year total assetsC) Base-year salesD) Base-year total assetsE) Base-year accounts receivables15) Which one of the following ratios is a measure of a firm's liquidity?A) Cash coverage ratioB) Profit marginC) Debt-equity ratioD) Quick ratioE) NWC turnover16) An increase in current liabilities will have which one of the following effects, all else held constant? Assume all ratios have positive values.A) Increase in the cash ratioB) Increase in the net working capital to total assets ratioC) Decrease in the quick ratioD) Decrease in the cash coverage ratioE) Increase in the current ratio17) An increase in which one of the following will increase a firm's quick ratio without affecting its cash ratio?A) Accounts payableB) CashC) InventoryD) Accounts receivableE) Fixed assets18) A supplier, who requires payment within 10 days, should be most concerned with which one of the following ratios when granting credit?A) CurrentB) CashC) Debt-equityD) QuickE) Total debt19) A firm has an interval measure of 48. This means that the firm has sufficient liquid assets to do which one of the following?A) Pay all of its debts that are due within the next 48 hoursB) Pay all of its debts that are due within the next 48 daysC) Cover its operating costs for the next 48 hoursD) Cover its operating costs for the next 48 daysE) Meet the demands of its customers for the next 48 hours20) Ratios that measure a firm's liquidity are known as ________ ratios.A) asset managementB) long-term solvencyC) short-term solvencyD) profitabilityE) book value21) Which one of the following statements is correct?A) If the total debt ratio is greater than .50, then the debt-equity ratio must be less than 1.0.B) Long-term creditors would prefer the times interest earned ratio be 1.4 rather than 1.5.C) The debt-equity ratio can be computed as 1 plus the equity multiplier.D) An equity multiplier of 1.2 means a firm has $1.20 in sales for every $1 in equity.E) An increase in the depreciation expense will not affect the cash coverage ratio.22) If a firm has a debt-equity ratio of 1.0, then its total debt ratio must be which one of the following?A) 0B) .5C) 1.0D) 1.5E) 2.023) The cash coverage ratio directly measures the ability of a company to meet its obligation to pay:A) an invoice to a supplier.B) wages to an employee.C) interest to a lender.D) principal to a lender.E) a dividend to a shareholder.24) All-State Moving had sales of $899,000 in 2017 and $967,000 in 2018. The firm's current accounts remained constant. Given this information, which one of the following statements must be true?A) The total asset turnover rate increased.B) The days' sales in receivables increased.C) The net working capital turnover rate increased.D) The fixed asset turnover decreased.E) The receivables turnover rate decreased.25) The Corner Hardware has succeeded in increasing the amount of goods it sells while holding the amount of inventory on hand at a constant level. Assume that both the cost per unit and the selling price per unit also remained constant. This accomplishment will be reflected in the firm's financial ratios in which one of the following ways?A) Decrease in the inventory turnover rateB) Decrease in the net working capital turnover rateC) Increase in the fixed asset turnover rateD) Decrease in the day's sales in inventoryE) Decrease in the total asset turnover rate26) RJ's has a fixed asset turnover rate of 1.26 and a total asset turnover rate of .97. Sam's has a fixed asset turnover rate of 1.31 and a total asset turnover rate of .94. Both companies have similar operations. Based on this information, RJ's must be doing which one of the following?A) Utilizing its fixed assets more efficiently than Sam'sB) Utilizing its total assets more efficiently than Sam'sC) Generating $1 in sales for every $1.26 in net fixed assetsD) Generating $1.26 in net income for every $1 in net fixed assetsE) Maintaining the same level of current assets as Sam's27) Ratios that measure how efficiently a firm manages its assets and operations to generate net income are referred to as ________ ratios.A) asset managementB) long-term solvencyC) short-term solvencyD) profitabilityE) turnover28) If a company produces a return on assets of 14 percent and also a return on equity of 14 percent, then the firm:A) may have short-term, but not long-term debt.B) is using its assets as efficiently as possible.C) has no net working capital.D) has a debt-equity ratio of 1.0.E) has an equity multiplier of 1.0.29) Which one of the following will decrease if a firm can decrease its operating costs, all else constant?A) Return on equityB) Return on assetsC) Profit marginD) Total asset turnoverE) Price-earnings ratio30) Al's has a price-earnings ratio of 18.5. Ben's also has a price-earnings ratio of 18.5. Which one of the following statements must be true if Al's has a higher PEG ratio than Ben's?A) Al's has more net income than Ben's.B) Ben's is increasing its earnings at a faster rate than Al's.C) Al's has a higher market value per share than does Ben's.D) Ben's has a lower market-to-book ratio than Al's.E) Al's has a higher earnings growth rate than Ben's.31) Tobin's Q relates the market value of a firm's assets to which one of the following?A) Initial cost of creating the firmB) Current book value of the firmC) Average asset value of similar firmsD) Average market value of similar firmsE) Today's cost to duplicate those assets32) The price-sales ratio is especially useful when analyzing firms that have:A) volatile market prices.B) negative earnings.C) positive PEG ratios.D) a high Tobin's Q.E) increasing sales.33) Mortgage lenders probably have the most interest in the ________ ratios.A) return on assets and profit marginB) long-term debt and times interest earnedC) price-earnings and debt-equityD) market-to-book and times interest earnedE) return on equity and price-earnings34) Relationships determined from a company's financial information and used for comparison purposes are known as:A) financial ratios.B) identities.C) dimensional analysis.D) scenario analysis.E) solvency analysis.35) DL Farms currently has $600 in debt for every $1,000 in equity. Assume the company uses some of its cash to decrease its debt while maintaining its current equity and net income. Which one of the following will decrease as a result of this action?A) Equity multiplierB) Total asset turnoverC) Profit marginD) Return on assetsE) Return on equity36) Which one of these identifies the relationship between the return on assets and the return on equity?A) Profit marginB) Profitability determinantC) Balance sheet multiplierD) DuPont identityE) Debt-equity ratio37) Which one of the following accurately describes the three parts of the DuPont identity?A) Equity multiplier, profit margin, and total asset turnoverB) Debt-equity ratio, capital intensity ratio, and profit marginC) Operating efficiency, equity multiplier, and profitability ratioD) Return on assets, profit margin, and equity multiplierE) Financial leverage, operating efficiency, and profitability ratio38) An increase in which of the following must increase the return on equity, all else constant?A) Total assets and salesB) Net income and total equityC) Total asset turnover and debt-equity ratioD) Equity multiplier and total equityE) Debt-equity ratio and total debt39) Which one of the following is a correct formula for computing the return on equity?A) Profit margin × ROAB) ROA × Equity multiplierC) Profit margin × Total asset turnover × Debt-equity ratioD) Net income/Total assetsE) Debt-equity ratio × ROA40) The DuPont identity can be used to help managers answer which of the following questions related to a company's operations?I. How many sales dollars are being generated per each dollar of assets?II. How many dollars of assets have been acquired per each dollar in shareholders' equity? III. How much net profit is being generating per dollar of sales?IV. Does the company have the ability to meet its debt obligations in a timely manner?A) I and III onlyB) II and IV onlyC) I, II, and III onlyD) II, III and IV onlyE) I, II, III, and IV41) The U.S. government coding system that classifies a company by the nature of its business operations is known as the:A) Centralized Business Index.B) Peer Grouping codes.C) Standard Industrial Classification codes.D) Governmental ID codes.E) Government Engineered Coding System.42) Which one of the following statements is correct?A) Book values should always be given precedence over market values.B) Financial statements are rarely used as the basis for performance evaluations.C) Historical information is useful when projecting a company's future performance.D) Potential lenders place little value on financial statement information.E) Reviewing financial information over time has very limited value.43) The most acceptable method of evaluating the financial statements is to compare the company's current financial:A) ratios to the company's historical ratios.B) statements to the financial statements of similar companies operating in other countries.C) ratios to the average ratios of all companies located within the same geographic area.D) statements to those of larger companies in unrelated industries.E) statements to the projections that were created based on Tobin's Q.44) All of the following issues represent problems encountered when comparing the financial statements of two separate entities except the issue of the companies:A) being conglomerates with unrelated lines of business.B) having geographically varying operations.C) using differing accounting methods.D) differing seasonal peaks.E) having the same fiscal year.45) Which one of these is the least important factor to consider when comparing the financial situations of utility companies that generate electric power and have the same SIC code?A) Type of ownershipB) Government regulations affecting the firmC) Fiscal year endD) Methods of power generationE) Number of part-time employees46) At the beginning of the year, Brick Makers had cash of $183, accounts receivable of $392, accounts payable of $463, and inventory of $714. At year end, cash was $167, accounts payables was $447, inventory was $682, and accounts receivable was $409. What is the amount of the net source or use of cash by working capital accounts for the year?A) Net use of $16 cashB) Net use of $17 cashC) Net source of $17 cashD) Net source of $15 cashE) Net use of $15 cash47) During the year, Al's Tools decreased its accounts receivable by $160, increased its inventory by $115, and decreased its accounts payable by $70. How did these three accounts affect the sources of uses of cash by the firm?A) Net source of cash of $120B) Net source of cash of $205C) Net source of cash of $45D) Net use of cash of $115E) Net use of cash of $2548) Lani's generated net income of $911, depreciation expense was $47, and dividends paid were $25. Accounts payables increased by $15, accounts receivables increased by $28, inventory decreased by $14, and net fixed assets decreased by $8. There was no interest expense. What was the net cash flow from operating activity?A) $776B) $865C) $959D) $922E) $98549) For the past year, Jenn's Floral Arrangements had taxable income of $198,600, beginning common stock of $68,000, beginning retained earnings of $318,750, ending common stock of $71,500, ending retained earnings of $316,940, interest expense of $11,300, and a tax rate of 21 percent. What is the amount of dividends paid during the year?A) $157,280B) $159,935C) $163,200D) $153,555E) $158,70450) The Floor Store had interest expense of $38,400, depreciation of $28,100, and taxes of $19,600 for the year. At the start of the year, the firm had total assets of $879,400 and current assets of $289,600. By year's end total assets had increased to $911,900 while current assets decreased to $279,300. What is the amount of the cash flow from investment activity for the year?A) −$51,150B) $21,850C) $29,300D) −$70,900E) −$89,40051) Williamsburg Market is an all-equity firm that has net income of $96,200, depreciation expense of $6,300, and an increase in net working capital of $2,800. What is the amount of the net cash from operating activity?A) $91,300B) $99,700C) $93,400D) $105,300E) $113,70052) The accounts payable of a company changed from $136,100 to $104,300 over the course of a year. This change represents a:A) use of $31,800 of cash as investment activity.B) source of $31,800 of cash as an operating activity.C) source of $31,800 of cash as a financing activity.D) source of $31,800 of cash as an investment activity.E) use of $31,800 of cash as an operating activity.53) Oil Creek Auto has sales of $3,340, net income of $274, net fixed assets of $2,600, and current assets of $920. The firm has $430 in inventory. What is the common-size statement value of inventory?A) 12.22 percentB) 44.16 percentC) 16.54 percentD) 13.36 percentE) 46.74 percent54) Pittsburgh Motors has sales of $4,300, net income of $320, total assets of $4,800, and total equity of $2,950. Interest expense is $65. What is the common-size statement value of the interest expense?A) .89 percentB) 1.51 percentC) 1.69 percentD) 2.03 percentE) 1.35 percent55) Last year, which is used as the base year, a firm had cash of $52, accounts receivable of $223, inventory of $509, and net fixed assets of $1,107. This year, the firm has cash of $61,accounts receivable of $204, inventory of $527, and net fixed assets of $1,216. What is this year's common-base-year value of inventory?A) .67B) .91C) .88D) 1.04E) 1.1856) Duke's Garage has cash of $68, accounts receivable of $142, accounts payable of $235, and inventory of $318. What is the value of the quick ratio?A) 2.25B) .53C) .71D) .89E) 1.3557) Uptown Men's Wear has accounts payable of $2,214, inventory of $7,950, cash of $1,263, fixed assets of $8,400, accounts receivable of $3,907, and long-term debt of $4,200. What is the value of the net working capital to total assets ratio?A) .31B) .42C) .47D) .51E) .5658) DJ's has total assets of $310,100 and net fixed assets of $168,500. The average daily operating costs are $2,980. What is the value of the interval measure?A) 31.47 daysB) 47.52 daysC) 56.22 daysD) 68.05 daysE) 104.62 days59) Corner Books has a debt-equity ratio of .57. What is the total debt ratio?A) .36B) .30C) .44D) 2.27E) 2.7560) SS Stores has total debt of $4,910 and a debt-equity ratio of 0.52. What is the value of the total assets?A) $16,128.05B) $7,253.40C) $9,571.95D) $11,034.00E) $14,352.3161) JK Motors has sales of $96,400, costs of $53,800, interest paid of $2,800, and depreciation of $7,100. The tax rate is 21 percent. What is the value of the cash coverage ratio?A) 15.21B) 12.14C) 17.27D) 23.41E) 12.6862) Terry's Pets paid $2,380 in interest and $2,200 in dividends last year. The times interest earned ratio is 2.6 and the depreciation expense is $680. What is the value of the cash coverage ratio?A) 1.42B) 2.72C) 2.94D) 2.89E) 2.4663) The Up-Towner has sales of $913,400, costs of goods sold of $579,300, inventory of $123,900, and accounts receivable of $78,900. How many days, on average, does it take the firm to sell its inventory assuming that all sales are on credit?A) 74.19 daysB) 84.69 daysC) 78.07 daysD) 96.46 daysE) 71.01 days64) Flo's Flowers has accounts receivable of $4,511, inventory of $1,810, sales of $138,609, and cost of goods sold of $64,003. How many days does it take the firm to sell its inventory and collect the payment on the sale assuming that all sales are on credit?A) 11.88 daysB) 22.20 daysC) 16.23 daysD) 14.50 daysE) 18.67 days65) The Harrisburg Store has net working capital of $2,715, net fixed assets of $22,407, sales of $31,350, and current liabilities of $3,908. How many dollars' worth of sales are generated from every $1 in total assets?A) $1.08B) $1.14C) $1.19D) $84E) $9366) TJ's has annual sales of $813,200, total debt of $171,000, total equity of $396,000, and a profit margin of 5.78 percent. What is the return on assets?A) 8.29 percentB) 6.48 percentC) 9.94 percentD) 7.78 percentE) 8.02 percent67) Frank's Used Cars has sales of $807,200, total assets of $768,100, and a profit margin of 6.68 percent. The firm has a total debt ratio of 54 percent. What is the return on equity?A) 13.09 percentB) 12.04 percentC) 11.03 percentD) 8.56 percentE) 15.26 percent68) Bernice's has $823,000 in sales. The profit margin is 4.2 percent and the firm has 7,500 shares of stock outstanding. The market price per share is $16.50. What is the price-earnings ratio?A) 3.58B) 3.98C) 4.32D) 3.51E) 4.2769) Hungry Lunch has net income of $73,402, a price-earnings ratio of 13.7, and earnings per share of $.43. How many shares of stock are outstanding?A) 13,520B) 12,460C) 165,745D) 171,308E) 170,70270) A firm has 160,000 shares of stock outstanding, sales of $1.94 million, net income of $126,400, a price-earnings ratio of 21.3, and a book value per share of $7.92. What is the market-to-book ratio?A) 2.12B) 1.84C) 1.39D) 2.45E) 2.6971) Taylor's Men's Wear has a debt-equity ratio of 48 percent, sales of $829,000, net income of $47,300, and total debt of $206,300. What is the return on equity?A) 19.29 percentB) 11.01 percentC) 15.74 percentD) 18.57 percentE) 14.16 percent72) Nielsen's has inventory of $29,406, accounts receivable of $46,215, net working capital of $4,507, and accounts payable of $48,919. What is the quick ratio?A) 1.55B) .49C) 1.32D) .94E) .9273) The Strong Box has sales of $859,700, cost of goods sold of $648,200, net income of $93,100, and accounts receivable of $102,300. How many days of sales are in receivables?A) 57.60 daysB) 40.32 daysC) 54.53 daysD) 29.41 daysE) 43.43 days74) Corner Books has sales of $687,400, cost of goods sold of $454,200, and a profit margin of 5.5 percent. The balance sheet shows common stock of $324,000 with a par value of $5 a share, and retained earnings of $689,500. What is the price-sales ratio if the market price is $43.20 per share?A) 4.28B) 12.74C) 6.12D) 4.07E) 14.5175) Gem Jewelers has current assets of $687,600, total assets of $1,711,000, net working capital of $223,700, and long-term debt of $450,000. What is the debt-equity ratio?A) .87B) .94C) 1.21D) 1.15E) 1.0676) Russell's has annual sales of $649,200, cost of goods sold of $389,400, interest of $23,650, depreciation of $121,000, and a tax rate of 21 percent. What is the cash coverage ratio for the year?A) 8.43B) 10.99C) 11.64D) 5.87E) 18.2277) Lawn Care, Inc., has sales of $367,400, costs of $183,600, depreciation of $48,600, interest of $39,200, and a tax rate of 25 percent. The firm has total assets of $422,100, long-term debt of $102,000, net fixed assets of $264,500, and net working capital of $22,300. What is the return on equity?A) 24.26 percentB) 15.38 percentC) 38.96 percentD) 29.96 percentE) 17.06 percent78) Frank's Welding has net fixed assets of $36,200, total assets of $51,300, long-term debt of $22,000, and total debt of $29,700. What is the net working capital to total assets ratio?A) 12.18 percentB) 16.82 percentC) 14.42 percentD) 17.79 percentE) 9.90 percent79) The Green Fiddle has current liabilities of $28,000, sales of $156,900, and cost of goods sold of $62,400. The current ratio is 1.22 and the quick ratio is .71. How many days on average does it take to sell the inventory?A) 128.13 daysB) 74.42 daysC) 199.81 daysD) 147.46 daysE) 83.53 days80) Green Yard Care has net income of $62,300, a tax rate of 21 percent, and a profit margin of 6.7 percent. Total assets are $1,100,500 and current assets are $328,200. How many dollars of sales are being generated from every dollar of net fixed assets?A) $2.83B) $1.37C) $.84D) $1.20E) $1.2381) Jensen's Shipping has total assets of $694,800 at year's end. The beginning owners' equity was $362,400. During the year, the company had sales of $711,000, a profit margin of 5.2 percent, a tax rate of 21 percent, and paid $12,500 in dividends. What is the equity multiplier at year-end?A) 1.67B) 1.72C) 1.93D) 1.80E) 1.8682) Western Gear has net income of $12,400, a tax rate of 21 percent, and interest expense of $1,600. What is the times interest earned ratio for the year?A) 9.63B) 7.75C) 10.81D) 14.97E) 10.9783) Big Tree Lumber has earnings per share of $1.36. The firm's earnings have been increasing at an average rate of 2.9 percent annually and are expected to continue doing so. The firm has 21,500 shares of stock outstanding at a price per share of $23.40. What is the firm's PEG ratio?A) 2.27B) 11.21C) 4.85D) 3.94E) 5.9384) Townsend Enterprises has a PEG ratio of 5.3, net income of $49,200, a price-earnings ratio of 17.6, and a profit margin of 7.1 percent. What is the earnings growth rate?A) 2.48 percentB) 1.06 percentC) 3.32 percentD) 5.20 percentE) 10.60 percent85) A firm has total assets with a current book value of $71,600, a current market value of $82,300, and a current replacement cost of $90,400. What is the value of Tobin's Q?A) .85B) .87C) .90D) .94E) .9186) Dixie Supply has total assets with a current book value of $368,900 and a current replacement cost of $486,200. The market value of these assets is $464,800. What is the value of Tobin's Q?A) .79B) .76C) .96D) 1.26E) 1.0587) Dandelion Fields has a Tobin's Q of .96. The replacement cost of the firm's assets is $225,000 and the market value of the firm's debt is $101,000. The firm has 20,000 shares of stock outstanding and a book value per share of $2.09. What is the market-to-book ratio?A) 2.75 timesB) 3.18 timesC) 3.54 timesD) 4.01 timesE) 4.20 times88) The Tech Store has annual sales of $416,000, a price-earnings ratio of 18, and a profit margin of 3.7 percent. There are 12,000 shares of stock outstanding. What is the price-sales ratio?A) .97B) .67C) 1.08D) 1.15E) .8689) Lassiter Industries has annual sales of $328,000 with 8,000 shares of stock outstanding. The firm has a profit margin of 4.5 percent and a price-sales ratio of 1.20. What is the firm's price-earnings ratio?A) 21.9B) 17.4C) 18.6D) 26.7E) 24.390) Drive-Up has sales of $31.4 million, total assets of $27.6 million, and total debt of $14.9 million. The profit margin is 3.7 percent. What is the return on equity?A) 6.85 percentB) 9.15 percentC) 11.08 percentD) 13.31 percentE) 14.21 percent91) Corner Supply has a current accounts receivable balance of $246,000. Credit sales for the year just ended were $2,430,000. How many days on average did it take for credit customers to pay off their accounts during this past year?A) 44.29 daysB) 55.01 daysC) 55.50 daysD) 36.95 daysE) 41.00 days92) BL Industries has ending inventory of $302,800, annual sales of $2.33 million, and annual cost of goods sold of $1.41 million. On average, how long did a unit of inventory sit on the shelf before it was sold?A) 47.43 daysB) 22.18 daysC) 78.38 daysD) 61.78 daysE) 83.13 days93) Billings Inc. has net income of $161,000, a profit margin of 7.6 percent, and an accounts receivable balance of $127,100. Assume that 66 percent of sales are on credit. What is the days' sales in receivables?A) 21.90 daysB) 27.56 daysC) 33.18 daysD) 35.04 daysE) 36.19 days94) Stone Walls has a long-term debt ratio of .6 and a current ratio of 1.2. Current liabilities are $800, sales are $7,800, the profit margin is 6.5 percent, and return on equity is 15.5 percent. What is the amount of the firm's net fixed assets?A) $8,880.15B) $8,017.43C) $7,666.67D) $5,848.15E) $8,977.43。

03. Financial Ratio Analysis 财务分析 国外MBA课程英文版 之 比率分析