中南财经政法大学 中级会计学 英文版 5The Statement of Cash Flows

中级财务会计 英文

Intermediate Financial AccountingIntroductionFinancial accounting is a fundamental component of a company’s management and reporting process. It involves the recording, analysis, and reporting of a company’s financial transactions. A strong foundation in financial accounting is essential for any individual looking to pursue a career in finance or accounting. This document aims to provide an overview of intermediate financial accounting concepts and principles.The Accounting CycleThe accounting cycle is a series of steps that are followed in the financial accounting process to ensure accurate and reliable financial reporting. The cycle begins with the recording of transactions and ends with the preparation of financial statements. The key steps in the accounting cycle include:1.Identifying and Analyzing Transactions: This step involvesidentifying relevant financial transactions and analyzing their impact on the company’s financial position.2.Recording Journal Entries: Journal entries are recorded todocument the financial transactions. These entries are made in the generaljournal, which is a chronological record of all transactions.3.Posting to General Ledger: The information from the journal entriesis transferred to the general ledger accounts, which are used to summarizetransactions for each account.4.Preparing Trial Balance: A trial balance is prepared to ensure thatall debit and credit balances in the general ledger are equal. If there are noerrors, the total debits will equal the total credits.5.Adjusting Entries: Adjusting entries are made at the end of theaccounting period to record any transactions that have not been previouslyrecorded, such as accruals and prepayments.6.Preparing Financial Statements: Financial statements, including theincome statement, balance sheet, and cash flow statement, are prepared toreport the company’s financial performance and position.7.Closing Entries: Closing entries are made to transfer balances fromtemporary accounts (such as revenue and expense accounts) to permanentaccounts (such as retained earnings).8.Preparing Post-Closing Trial Balance: A post-closing trial balance isprepared to ensure that all temporary accounts have been closed and that the accounting records are ready for the next accounting period.Financial Statement AnalysisFinancial statement analy sis involves the examination of a company’s financial statements to assess its financial performance and position. It helps in understanding the company’s profitability, liquidity, solvency, and efficiency. The key tools and techniques used in financial statement analysis include:•Horizontal Analysis: Horizontal analysis compares financial statement items over multiple periods to identify trends and changes.•Vertical Analysis: Vertical analysis involves expressing each financial statement item as a percentage of a base amount, such as total assets or netsales, to assess the relative importance of each item.•Ratio Analysis: Ratio analysis involves calculating and interpreting financial ratios to assess the company’s liquidity, solvency, profitability, and efficiency.•Common Size Ratios: Common size ratios are used to compare the relative percentages of different items within a financial statement.•DuPont Analysis: DuPont analysis decomposes the return on equity (ROE) into its components to assess the company’s profitability, efficiency, and leverage.Revenue Recognition and Expense RecognitionThe principles of revenue recognition and expense recognition are fundamental to financial accounting. These principles determine when revenue and expenses should be recognized in the financial statements. The generally accepted accounting principles (GAAP) provide guidelines for revenue recognition and expense recognition.•Revenue Recognition: Revenue is generally recognized when it is earned and realizable. It is earned when the company has delivered goods or services to the customer, and it is realizable when the company can reasonably expect to collect the amount. There are specific criteria for recognizing revenue from different sources, such as sales of goods, provision of services, andinterest and dividends.•Expense Recognition: Expenses are recognized when they are incurred and have a cause-and-effect relationship with revenue. The matching principle requires expenses to be recognized in the same period as the revenuethey help generate. There are different methods of expense recognition, such as the accrual basis and the cash basis.Inventory Valuation MethodsInventory valuation is a crucial aspect of financial accounting, as it impacts the company’s profitability, assets, and financial ratios. There are different methods used to value inventory, including:•FIFO (First-In, First-Out): The FIFO method assumes that the first units of inventory purchased or produced are the first to be sold or used. Itresults in the cost of goods sold being based on the oldest inventory.•LIFO (Last-In, First-Out): The LIFO method assumes that the last units of inventory purchased or produced are the first to be sold or used. Itresults in the cost of goods sold being based on the most recent inventory.•Weighted Average Cost: The weighted average cost method calculates the average cost of inventory based on the average cost per unit. It is calculated by dividing the total cost of goods available for sale by the total units available for sale.Each inventory valuation method has its advantages and disadvantages, and the choice of method can have a significant impact on the company’s f inancial statements and taxes.ConclusionIntermediate financial accounting plays a vital role in providing accurate and reliable financial information for decision-making and reporting. Understanding the accounting cycle, financial statement analysis, revenue recognition and expense recognition principles, and inventory valuation methods is essential for anyone seeking to excel in the field of finance or accounting. By acquiring a solid foundation in these concepts, individuals can enhance their ability to interpret financial data and contribute to the success of their organizations.。

中级财务会计习题(英文)

Chapter 1 A. An example of a business stakeholder is the federal government.B. A corporation is a business that is legally separate and distinct from its owners.C. Accounting is a service that provides many different users with financial information to make economic decisions.D. Small ethical lapses are harmless in and of themselves.E. Managerial accounting is primarily concerned with the recording and reporting of economic data and activities of an entity for use by owners, creditors, governmental agencies, and the public.F. The unit of measurement concept requires that economic data be recorded in a common unit of measurement.G. If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000.H. The owner’s rights to the assets rank ahead of the creditors’ rights to the assets.I. Business transactions are economic events that directly or indirectly change an entity’s financial condition or results f rom operations.J. If net income for a proprietorship was $25,000, the owner withdrew $10,000 in cash and the owner invested $5,000 in cash, the capital of the owner increased by $20,000. K. The owner is only allowed to withdraw cash from the business.L. Receiving a bill or otherwise being notified that an amount is owed is amount is paid.M. The principal financial statements of a proprietorship are the income statement, statement of owner’s equity, and the balance sheet.N. An income statement is a summary of the revenues and expenses of a business as of a specific date.O. A low ratio of liabilities to owner’s equity indicates that a business is near bankruptcy. 1. Profit is the difference betweena. assets and liabilitiesb. the incoming cash and outgoing cashc. the assets purchased with cash contributed by the owner and the cash spent to operate the businessd. the assets received for goods and services and the amounts used to provide the goods and services2. Which of the items below is not a business organization form?a. entrepreneurshipb. proprietorshipc. partnershipd. corporation3. Which of the following is not a step in providing accounting information to stakeholders? a. design the accounting information systemb. prepare accounting surveysc. identify stakeholdersd. record economic data4. For accounting purposes, the business entity should be considered separate from its owners if the entity isa. a corporationb. a proprietorshipc. a partnershipd. all of the above5. Which of the following is not a business transaction?a. make a sales offerb. sell goods for cashc. receive cash for services to be rendered laterd. pay for supplies6. The Reynolds Company estimated that the value of its land had increased from $10,000 to $16,000 and therefore wrote up the land account to $16,000. Which accounting concept(s) was (were) violated?a. cost conceptb. objectivity conceptc. all of the aboved. none of the above7. Goods purchased on account for future use in the business, such as supplies, are called a. prepaid liabilities b. revenuesc. prepaid expensesd. liabilities8. All of the following are financial statement(s) of a proprietorship except thea. statement of retained ear ningsb. statement of owner’s equityc. income statementd. statement of cash flowsChapter 2 A. A chart of accounts is a listing of accounts that make up the journal.B. Drawings are an example of an expense.C. To determine the balance in an account, always subtract credits from debits.D. The double-entry accounting system records each transaction twice.E. The increase side of all accounts is the normal balance.F. The journal is the book of original entry.G. Journalizing transactions using the double-entry bookkeeping system will eliminate fraud. H. The process of transferring the data from the journal to the ledger accounts is posting. I. The post reference notation used in the journal is the page number.J. When a business receives a bill from the utility company, no entry should be made until the invoice is paid.K. A proof of the equality of debits and credits in the ledger at the end of an accounting period is called a balance sheet.L. Even when a trial balance is in balance, there may be errors in the individual accounts. M. Posting a part of a transaction to the wrong account will cause the trial balance totals to be unequal.N. Horizontal analysis is used to compare the financial statements of the same company for different periods. 1. A group of related accounts that comprise a complete unit is called aa. Journalb. liability2.3.4.5.6. c. ledger d. transaction Which statement(s) concerning cash is (are) true? a. cash will always have more debits than credits b. cash will never have a credit balance c.cash is increased by debiting d. all of the above Which of the following types of accounts have a normal credit balance? a. assets and liabilities b. liabilities and expenses c. revenues and liabilities d. capital and drawing Which of the following entries records the receipt of cash from patients on account? a. Accounts Payable, debit; Fees Earned, credit b. Accounts Receivable, debit; Fees Earned, credit c. Accounts Receivable, debit; Cash, credit d. Cash, debit; Accounts Receivable, credit If the two totals of a trial balance are not equal, it could be due to a. failure to record a transaction b. recording the same erroneous amount for both the debit and the credit parts of a transaction c. an error in determining the account balances, such as a balance being incorrectly computed d. recording the same transaction more than once Which of the following errors, each considered individually, would cause the trial balance totals to be unequal?a. a transaction was not postedb. a payment of $96 for insurance was posted as a debit of $46 to Prepaid Insurance and a credit of $46 to Cashc. a payment of $311 to a creditor was posted as a debit of $3,111 to Accounts Payable and a debit of $311 to Accounts Receivabled. cash received from customers on account was posted as a debit of $140 to Cash and a credit of $140 to Accounts PayableChapter 3 1. The accrual basis of accounting requires revenue be recorded when cash is received from customers.2. The matching concept requires expenses be recorded in the same period that the related revenue is recorded.3. Adjusting entries are made at the end of an accounting period to adjust accounts on the balance sheet.4. The difference between deferred revenue and accrued revenue is that accrued revenue has been recorded and needs adjusting and deferred revenue has never been recorded.5. The systematic allocation of land’s cost to expense is called depreciation.6. The difference between the balance of a fixed asset account and the balance of its related accumulated depreciation account is termed the book value of the asset.7. If the adjustment for accrued salaries at the end of the period is inadvertently omitted, both liabilities and owner’s equity will be overstated for the period.8. The financial statements are prepared from the unadjusted trial balance.9. Vertical analysis compares each item in a statement with another item in the same statement.The correct: 2,6,91. Which account would normally not require an adjusting entry?a. Wages Expenseb. Accounts Receivablec. Accumulated Depreciationd. Smith, Capital2. What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid insurance account balance before adjustment, $15,500, and unexpired amounts per analysis of policies, $4,500?a. debit Insurance Expense, $4,500; credit Prepaid Insurance, $4,500b. debit Insurance Expense, $15,500; credit Prepaid Insurance, $15,500c. debit Prepaid Insurance, $11,500; credit Insurance Expense, $11,500d. debit Insurance Expense, $11,000; credit Prepaid Insurance, $11,0003. Depreciation Expense and Accumulated Depreciation are classified, respectively, asa. expense, contra assetb. asset, contra liabilityc. revenue, assetd. contra asset, expense4. If there is a balance in the unearned subscriptions account after adjusting entries are made, it represents a(n)a. deferralb. accrualc. drawingd. revenue5. What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid insurance account balance before adjustment, $15,500, and unexpired amounts per analysis of policies, $4,500?a. debit Insurance Expense, $4,500; credit Prepaid Insurance, $4,500b. debit Insurance Expense, $15,500; credit Prepaid Insurance, $15,500c. debit Prepaid Insurance, $11,500; credit Insurance Expense, $11,500d. debit Insurance Expense, $11,000; credit Prepaid Insurance, $11,0006. Depreciation Expense and Accumulated Depreciation are classified, respectively, asa. expense, contra assetb. asset, contra liabilityc. revenue, assetd. contra asset, expense7. If there is a balance in the unearned subscriptions account after adjusting entries are made, it represents a(n)a. deferralb. accrualc. drawingd. revenueMultiple choice: d d a aChapter 41. The most important output of the accounting cycle is the financial statements.2. A net loss is shown on the work sheet in the credit columns of both the Income Statement columns and the Balance Sheet columns.3. The difference between a classified balance sheet and one that is not classified is that the classified one has subheadings.4. Since the adjustments are entered on the work sheet, it is not necessary to record them in the journal or post them to the ledger.5. The post-closing trial balance will generally have fewer accounts than the trial balance.6. Solvency is essentially the ability of an organization to pay its bills.7. Working capital is current assets plus current liabilities.ANS:T F T F T T F1. The worksheeta. is an integral part of the accounting cycleb. eliminates the need to rewrite the financial statementsc. is a working paper that is requiredd. is used to summarize account balances and adjustments for the financial statements2. Which one of the fixed asset accounts listed below will not have a related contra asset account? a. Office Equipment b. Land c. Delivery Equipment d. Building3. Which of the accounts below would be closed by making a debit to the account?a. Unearned Revenueb. Fees Earnedc. Jeff Ritter, Drawingd. Rent Expense4. Which of the following accounts ordinarily appears in the post-closing trial balance?a. Bill Smith, Drawingb. Supplies Expensec. Fees Earnedd. Unearned Rent5. A fiscal yeara. ordinarily begins on the first day of a month and ends on the last day of the following twelfth monthb. for a business is determined by the federal governmentc. always begins on January 1 and ends on December 31 of the same yeard. should end at the height of the business’s annual operating cycle6. A current ratio of 4.3 means thata. there are $4.30 in current assets available to pay each dollar of current liabilitiesb. the company cannot pay its debts as they come duec. there are $4.30 in current assets for every $4.30 in current liabilitiesd. there are $4 in current assets for every $3 in current liabilitiesANS: dbbdaaChapter 61. In a merchandise business, sales minus operating expenses equals net income.2. In a perpetual inventory system, the Merchandise Inventory account is only used to reflect the beginning inventory.3. The single-step income statement is easier to prepare, but a criticism of this format is that gross profit and income from operations are not readily available.4. Under the perpetual inventory system, when a sale is made, both the retail and cost values are recorded.5. Sales Discounts is a revenue account with a credit balance.6. Discounts taken by the buyer for early payment of an invoice are credited to Cash Discounts by the buyer.7. If the ownership of merchandise passes to the buyer when the seller delivers the merchandise for shipment, the terms are stated as FOB destination.8. If merchandise costing $2,500, terms FOB destination, 2/10, n/30, with prepaid transportation costs of $100, is paid within 10 days, the amount of the purchases discount is $50.9. The adjusting entry to record inventory shrinkage would generally include a debit to Cost of Merchandise Sold. 1. The primary difference between a periodic and perpetual inventory system is that aa. periodic system determines the inventory on hand only at the end of the accounting periodb. periodic system keeps a record showing the inventory on hand at all timesc. periodic system provides an easy means to determine inventory shrinkaged. periodic system records the cost of the sale on the date the sale is made2. A sales invoice included the following information: merchandise price, $4,000; transportation, $300; terms 1/10, n/eom, FOB shipping point. Assuming that a credit for merchandise returned of $600 is granted prior to payment, that the transportation is prepaid by the seller, and that the invoice is paid within the discount period, what is the amount of cash received by the seller? a.$3,366 b.$3,400c.$3,666d.$3,9503. The net sales to asset s ratio measures a company’sa. working capitalb. net worthc. effective use of sales to support the purchase of new assetsd. effective use of assets to generate salesThe correct: 3,4,8,9 Multiple choice: a c dChapter 74. A customer’s c heck received in settlement of an account receivable is considered cash.5. If the balance in Cash Short and Over at the end of a period is a credit, it indicates that cash shortages have exceeded cash overages for the period.6. A voucher system is an example of an internal control procedure over cash payments.7. A remittance advice is the notification accompanying the check issued to a creditor that states the specific invoice being paid.8. The amount of the "adjusted balance" appearing on the bank reconciliation as ofa given date is the amount that is shown on the balance sheet for that date.9. When the petty cash fund is replenished, the petty cash account is credited for the total of all expenditures made since the fund was last replenished.10. Cash equivalents are short -term investments that will be converted to cash within 120 days.11. The doomsday ratio is almost always less than one.ANS:T F T T T F F T1. Credit memorandums from the banka. decrease a bank custom er’s accountb. are used to show a bank service chargec. show that a company has deposited a customer’s NSF checkd. show the bank has collected a note receivable for the customer2. Journal entries based on the bank reconciliation are required in the depositor’s accounts for a. outstanding checks b. deposits in transitc. bank errorsd. book errorsANS: d dChapter 81. Receivables from company owners and officers should be disclosed separately on the balance sheet.2. Since those responsible for receivables record keeping and credit approval do not handle cash, these duties do not need to be separated to maintain good internal control.3. Of the two methods of accounting for uncollectible receivables, the allowance method provides inadvance for uncollectible receivables.4. Although Allowance for Doubtful Accounts normally has a credit balance, it may have either a debit or a credit balance before adjusting entries are recorded at the end of the accounting period.5. At the end of a period, before the accounts are adjusted, Allowance for Doubtful Accounts has a debit balance of $2,000. If the estimate of uncollectible accounts determined by aging the receivables is $30,000, the current provision to be made for uncollectible accounts expense is $30,000.6. The due date of a 60-day note dated July 10 is September 10.7. If the maker of a note fails to pay the debt on the due date, the note is said to be dishonored.8. The discounting of a note receivable creates a contingent liability that continues in effect until the due date of the note. ANS: T F T T F F T T 1. Allowance for Doubtful Accounts has a debit balance of $500 at the end of the year (before adjustment), and uncollectible accounts expense is estimated at 3% of net sales. If net sales are $600,000, the amount of the adjusting entry to record the provision for doubtful accounts is a. $18,500 b. $17,500 c. $18,000 d. none of the above 2. On the balance sheet, the amount shown for the Allowance for Doubtful Accounts is equal to the a. Uncollectible accounts expense for the year b. total of the accounts receivables written-off during the year c. total estimated uncollectible accounts as of the end of the year d. sum of all accounts that are past due. 3. What is the type of account and normal balance of Allowance for Doubtful Accounts? a. Contra asset, credit b. Asset, debit c. Asset, credit d. Contra asset, debit 4. If the direct write-off method of accounting for uncollectible receivables is used, what general ledger account is credited to write off a customer’s account as uncollectible? a. Uncollectible Accounts Expense b. Accounts Receivable c. Allowance for Doubtful Accounts d. Interest Expense 5. A 90-day, 12% note for $10,000, dated May 1, is received from a customer on account. Thematurity value of the note isa. $10,000b. $10,300c. $450d. $9,550ANS: c c a b bChapter 91. 2. 3. 4. A business using the perpetual inventory system, with its detailed subsidiary records, does not need to take a physical inventory. Purchased goods in transit, shipped FOB destination, should be excluded from ending inventory. Unsold consigned merchandise should be included in the consignee’s inventory. Of the three widely used inventory costing methods (FIFO, LIFO, and average), the LIFO method of costing inventory is based on the assumption that costs are charged against revenues in the reverse order in which they were incurred.During inflationary periods, the use of the FIFO method of costing inventory will yield an inventory amount for the balance sheet approximating the current replacement cost.When using the FIFO inventory costing method, the most recent costs are assigned to the cost of goods sold.The use of the lower-of-cost-or-market method of inventory valuation increases net income for the period in which the inventory replacement price declined. Generally, the lower the number of days’ sales in inventory, the better.ANS: F F F T T F F TTaking a physical count of inventorya. is not necessary when a periodic inventory system is usedb. is a detective controlc. has no internal control relevanced. is not necessary when a perpetual inventory system is usedMerchandise inventory at the end of the year was inadvertently overstated. Which of the following statements correctly states the effect of the error on net income, assets, and owner’s equity?a. net income is overstated, assets are overstated, owner’s equity is understatedb. net income is overstated, assets are overstated, ow ner’s equity is overstatedc. net income is understated, assets are understated, owner’s equity is understatedd. net income is understated, assets are understated, owner’s equity is overstated Inventory costing methods place primary emphasis on assumptions abouta. flow of goodsb. flow of costsc. flow of goods or costs depending on the methodd. flow of valuesIf merchandise inventory is being valued at cost and the purchase price is steadily falling, which method of costing will yield the largest net income?a. average costb. LIFO 5. 6. 7. 8. 1. 2. 3. 4.c. FIFOd. weighted average 5. On the basis of the following data, what is the estimated cost of the merchandise inventory on October 31 by the retail method? Oct. 1 Merchandise Inventory $225,000 $324,500 Oct. 1-31 Purchases (net) 335,000 475,500 Oct. 1-31 Sales (net) 700,000 a. $372,000 b. $140,000 c. $100,000 d. $ 70,000 6. If the estimated rate of gross profit is 40%, what is the estimated cost of the merchandise inventory on June 30, based on the following data? June 1 Merchandise inventory $ 75,000 June 1-30 Purchases (net) 150,000 June 1-30 Sales (net) 135,000 a. $144,000 b. $140,000 c. $ 81,000 d. $ 54,500 7. Too much inventory on handa. reduces solvencyb. increases the cost to safeguard the assetsc. increases the losses due to price declinesd. all of the aboveANS: b b b b d a dChapter 10 1. The acquisition costs of property, plant, and equipment should include all normal, reasonable and necessary costs to get the asset in place and ready for use.2. Land acquired as a speculation is reported under Investments on the balance sheet.3. Standby equipment held for use in the event of a breakdown of regular equipment is reported as property, plant, and equipment on the balance sheet.4. As a company depreciates a piece of equipment, it cash flow goes up.5. All property, plant, and equipment assets are depreciated over time.6. The declining-balance method is an accelerated depreciation method.7. The cost of replacing an engine in a truck is an example of ordinary maintenance.8. The cost of new equipment is called a revenue expenditure because it will help generate revenues in the future.9. A gain can be realized when a fixed asset is discarded.10. When exchanging equipment, if the trade-in allowance is greater than the book value a loss results.11. The cost of a patent with a remaining legal life of 10 years and an estimated useful life of 7 years is amortized over 10 years.12. The method used to calculate the depletion of a natural resource is the straight line method.13. The higher the ratio of fixed assets to long-term liabilities the greater the margin of safety.ANS: T T T F F T F F F F F F T1. Factors contributing to a decline in the usefulness of a fixed asset may be divided into the following two categoriesa. salvage and functionalb. physical and functionalc. residual and salvaged. functional and residual2. Accumulated Depreciationa. is used to show the amount of cost expiration of intangiblesb. is the same as Depreciation Expensec. is a contra asset accountd. is used to show the amount of cost expiration of natural resources3. Equipment with a cost of $80,000, an estimated residual value of $5,000, and an estimated life of 15 years was depreciated by the straight-line method for 5 years. Due to obsolescence, it was determined that the useful life should be shortened by 5 years and the residual value changed to zero. The depreciation expense for the current and future years isa. $5,500b. $11,000c. $10,000d. $5,0004. A fixed asset with a cost of $42,000 and accumulated depreciation of $38,500 is traded for a similar asset priced at $60,000. Assuming a trade-in allowance of $5,000, the cost basis of the new asset isa. $58,000b. $58,500c. $60,000d. $61,5005. A machine with a cost of $65,000 has an estimated residual value of $5,000 and an estimated life of 4 years or 18,000 hours. What is the amount of depreciation for the second full year, using the declining-balance method at double the straight-line rate?a. $15,000b. $30,000c. $16,250d. $32,500ANS: b c b b cChapter 11 1. For a current liability to exist, the following two tests must be met. The liability must be due usually within a year and must be paid out of current assets.2. For an interest bearing note payable, the amount borrowed is equal to the face value of the note.3. The proceeds of a discounted note are equal to the face value of the note.4. Obligations that depend on past events and that are based on future transactions are contingent liabilities.5. The journal entry to record the cost of warranty repairs that were incurred during the current period, but related to sales made in prior years, includes a debit to Warranty Expense.6. Generally, all deductions made from an employee’s gross pay are required by law.7. FICA tax is a payroll tax that is paid only by employers.8. The higher the quick ratio, the more liquid a company is.ANS: T T F F F F F T1. On June 8, Acme Co. issued an $80,000, 6%, 120-day note payable to Still Co. Assume that the fiscal year of Acme Co. ends June 30. What is the amount of interest expense recognized by Acme in the current fiscal year?a. $293.33b. $400.00c. $391.11d. $1,600.002. Proceeds of $48,750 were received from discounting a $50,000, 90-day note at a bank. The discount rate used by the bank in computing the proceeds wasa. 6.25%b. 10.00%c. 10.26%d. 9.75%3. Pilgrim Company sells merchandise with a one year warranty. In 2005, sales consisted of 1,500 units. It is estimated that warranty repairs will average $10 per unit sold, and 30% of the repairs will be made in 2005 and 70% in 2006. In the 2005 income statement, Pilgrim should show warranty expense ofa. $4,500b. $10,500c. $15,000d. $0ANS: a b cChapter 12 1. A corporation is a separate entity for accounting purposes but not for legal purposes.2. Double taxation is a disadvantage of a corporation because the same party has to pay taxes twice on the income.3. The two main sources of stockholders’ equity are investments contributed by stockholders and net income retained in the business.4. The balance in retained earnings should be interpreted as representing surplus cash left over for dividends.5. Preferred stock with a preferential right to dividends in arrears is referred to asparticipating preferred.6. If 50,000 shares are authorized, 37,000 shares are issued, and 2,000 shares are reacquired, the number of outstanding shares is 39,000.7. When a corporation issues stock at a premium, it reports the premium as an other income item on the income statement.8. If 100 shares of treasury stock were purchased for $50 per share and then sold at $60 per share, $1,000 of income is reported in the income statement.9. Since a stock split changes information of a business, this transaction needs to be recorded.10. If 20,000 shares are authorized, 14,000 shares are issued, and 500 shares are held as treasury stock, a cash dividend of $1 per share would amount to $14,000.11. The declaration and issuance of a stock dividend does not affect the total amount of a corporation’s assets, liabilities, or stockholders’ equity.12. The dividend yield indicates the rate of return to stockholders in terms of cash dividend distributions.ANS: F F T F F F F F F F T T1. The outstanding stock is composed of 10,000 shares of $100 par, cumulative preferred $8 stock, and 50,000 shares of no-par common stock. Preferred dividends have been paid every year except for the preceding year and the current year. If $380,000 is to be distributed as a dividend for the current year, what total amount will be distributed to the common stockholders? a. $380,000b. $220,000c. $80,000d. $160,0002. A corporation issues 2,000 shares of common stock for $ 32,000. The stock has a stated value of $10 per share. The journal entry to record the stock issuance would include a credit to Common Stock fora. $20,000b. $32,000c. $12,000d. $2,0003. When common stock is issued in exchange for a noncash asset, the transaction should be recorded ata. the par value of the stock issuedb. the fair market value of the stockc. the fair market value of the asset acquiredd. the fair market value of the asset acquired or the fair market value of the stock, whichever canbe determined more objectively.4. Treasury stock that had been purchased for $5,400 last month was reissued this month for $7,500. The journal entry to record the reissuance would include a credit。

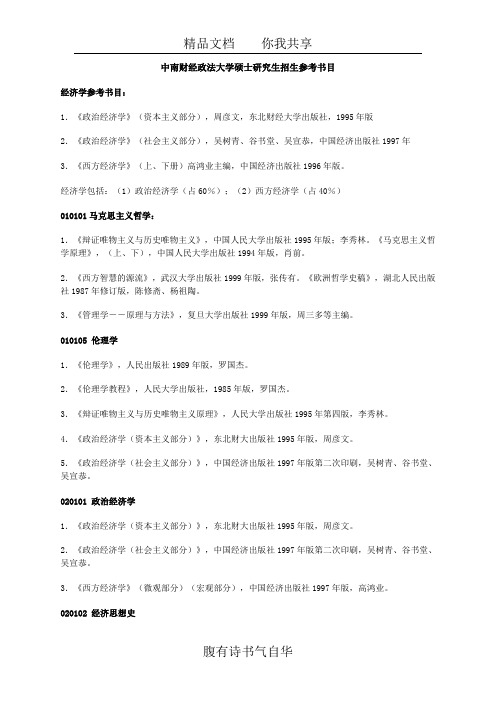

中级财务会计英文版.课后答案(chap2)

Exercise 2-4Requirement 1Sales price = 100 units x $600 = $60,000 x 70% = $42,000Requirement 2Exercise 7-4 (concluded)Requirement 3Requirement 1, using the net method:Requirement 2, using the net method:Exercise 2-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000Less: Actual returns (450,000)Remaining estimated returns $10,000Note: another series of journal entries that produce the same end result would be:Exercise 2-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 2-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2011 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 2-9Requirement 1To record the write-off of receivables.To reinstate an account previously written off and to record the collection.Allowance for uncollectible accounts:Balance, beginning of year $32,000Deduct: Receivables written off (21,000) Add: Collection of receivable previously written off 1,200Balance, before adjusting entry for 2011 bad debts 12,200Required allowance: 10% x $625,000 (62,500) Bad debt expense $50,300 To record bad debt expense for the year.Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 2-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2011 $20,030 Exercise 2-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388Exercise 2-12Requirement 1Requirement 22011 income before income taxes would be understated by $900 2012 income before income taxes would be overstated by $900.Exercise2-13Requirement 1Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 2-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year $ 2,200= 10% rate Divided by value of note $ 22,000 Requirement 2To record sale of stock in exchange for note receivable.To accrue interest on note receivable for twelve months.Exercise 2-15Exercise 2-16Exercise 2-17Exercise 2-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet of Mountain High, and they must record a liability.Exercise 2-19Step 1: Accrue interest earned.Step 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21Requirement 1Step 1: To accrue interest earned for two months on note receivableStep 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21 (concluded)Requirement 2To accrue interest earned on note receivable.。

中级会计学_中南财经政法大学中国大学mooc课后章节答案期末考试题库2023年

中级会计学_中南财经政法大学中国大学mooc课后章节答案期末考试题库2023年1.下列各项中,属于反映企业财务状况的会计要素是()。

答案:资产2.企业出现的现金短款,无法查明原因时,按照管理权限经批准后,应计入()。

答案:管理费用3.资产负债表日的应收账款的预期信用损失大于坏账准备的期初余额时,应贷记的会计科目为()。

答案:坏账准备4.蓝星公司对其发出材料采用先进先出法计价,2022年12月1日库存A材料15 000千克,实际成本为150 000元;12月2日购买A材料120 000千克,单价11元;12月18日购买A材料90 000千克,单价12元;12月6日发出A材料90 000千克。

2022年12月31日蓝星公司结存A材料金额为()元。

答案:1 575 0005.甲公司对其固定资产采用年数总和法计提折旧时,年折旧额()。

答案:逐年递减6.企业在无形资产研究阶段发生的职工薪酬应当()。

答案:计入管理费用7.甲公司于2022年12月5日从证券市场上购入乙公司发行在外的股票100万股作为以公允价值计量且其变动计入当期损益的金融资产,每股支付价款5元(含已宣告但尚未发放的现金股利1元),另支付相关交易费用8万元,甲公司确认为以公允价值计量且其变动计入当期损益的金融资产的入账价值为()万元。

答案:4008.甲公司增值税采用一般计税方法,其发生的下列税费中,不应计入相应资产成本的是()。

答案:购置用于不动产扩建工程的工程材料支付的增值税9.下列各项中,属于流动资产的是()。

答案:货币资金10.下列各项中,应确认为工业企业其他业务收入的是()。

答案:材料销售收入11.委托加工应纳消费税物资(非金银首饰)收回后,若将其用于连续生产应税消费品时,由受托方代扣代缴的消费税应记入的科目是()。

答案:应交税费——应交消费税12.甲公司2022年1月1日取得乙公司40%的股权,对乙公司财务与经营政策有重大影响,并准备长期持有。

(精品中级财务会计英文版.课后答案(chap2)

中级财务会计英文版.课后答案(c h a p2) Exercise 2-4Requirement 1Sales price = 100 units x $600 = $60,000 x 70% = $42,000November 17, 2011Accounts receivable ........................................................ 42,000Sales revenue .............................................................. 42,000 November 26, 2011Cash (98% x $42,000)........................................................ 41,160Sales discounts (2% x $42,000) (840)Accounts receivable .................................................... 42,000 Requirement 2Exercise 7-4 (concluded)Requirement 3Requirement 1, using the net method:Requirement 2, using the net method:Exercise 2-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000Less: Actual returns (450,000)Remaining estimated returns $10,000Note: another series of journal entries that produce the same end result would be:Exercise 2-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 2-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2011 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 2-9Requirement 1To record the write-off of receivables.To reinstate an account previously written off and to record the collection.Allowance for uncollectible accounts:Balance, beginning of year $32,000Deduct: Receivables written off (21,000)Add: Collection of receivable previously written off 1,200Balance, before adjusting entry for 2011 bad debts 12,200Required allowance: 10% x $625,000 (62,500)Bad debt expense $50,300To record bad debt expense for the year.Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 2-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2011 $20,030 Exercise 2-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388Exercise 2-12Requirement 1Requirement 22011 income before income taxes would be understated by $900 2012 income before income taxes would be overstated by $900.Exercise2-13Requirement 1Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 2-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year $ 2,200= 10% rate Divided by value of note $ 22,000Requirement 2To record sale of stock in exchange for note receivable.To accrue interest on note receivable for twelve months.Exercise 2-15Exercise 2-16Exercise 2-17Exercise 2-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet of Mountain High, and they must record a liability.Exercise 2-19Step 1: Accrue interest earned.Step 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21Requirement 1Step 1: To accrue interest earned for two months on note receivableStep 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21 (concluded)Requirement 2To accrue interest earned on note receivable.。

中南财经政法大学硕士研究生招生参考书目

中南财经政法大学硕士研究生招生参考书目经济学参考书目:1.《政治经济学》(资本主义部分),周彦文,东北财经大学出版社,1995年版2.《政治经济学》(社会主义部分),吴树青、谷书堂、吴宣恭,中国经济出版社1997年3.《西方经济学》(上、下册)高鸿业主编,中国经济出版社1996年版。

经济学包括:(1)政治经济学(占60%);(2)西方经济学(占40%)010101马克思主义哲学:1.《辩证唯物主义与历史唯物主义》,中国人民大学出版社1995年版;李秀林。

《马克思主义哲学原理》,(上、下),中国人民大学出版社1994年版,肖前。

2.《西方智慧的源流》,武汉大学出版社1999年版,张传有。

《欧洲哲学史稿》,湖北人民出版社1987年修订版,陈修斋、杨祖陶。

3.《管理学――原理与方法》,复旦大学出版社1999年版,周三多等主编。

010105 伦理学1.《伦理学》,人民出版社1989年版,罗国杰。

2.《伦理学教程》,人民大学出版社,1985年版,罗国杰。

3.《辩证唯物主义与历史唯物主义原理》,人民大学出版社1995年第四版,李秀林。

4.《政治经济学(资本主义部分)》,东北财大出版社1995年版,周彦文。

5.《政治经济学(社会主义部分)》,中国经济出版社1997年版第二次印刷,吴树青、谷书堂、吴宣恭。

020101 政治经济学1.《政治经济学(资本主义部分)》,东北财大出版社1995年版,周彦文。

2.《政治经济学(社会主义部分)》,中国经济出版社1997年版第二次印刷,吴树青、谷书堂、吴宣恭。

3.《西方经济学》(微观部分)(宏观部分),中国经济出版社1997年版,高鸿业。

020102 经济思想史1.《中国近代经济思想史》,中南财经大学(内部印刷),万安培。

2.《近代西方经济学史》,上海人民出版社1991年版,汤在新、傅殷才主编。

020103 经济史1.《中华人民共和国经济史纲要》,湖北人民出版社1996年第二版,赵德馨主编。

英文版会计学考试题及答案

英文版会计学考试题及答案English Accounting Exam Questions and AnswersQuestion 1: Define the term "Double Entry Bookkeeping" and explain its significance in accounting.Answer 1: Double Entry Bookkeeping is a system of recording financial transactions in which every entry to an account requires a corresponding and opposite entry to a different account. This ensures that the accounting equation (Assets = Liabilities + Owner's Equity) remains in balance. The significance of double entry bookkeeping lies in its ability to provide an accurate and comprehensive picture of a business's financial status, facilitating better decision-making and financial control.Question 2: What is the purpose of a trial balance, and how does it help in the preparation of financial statements?Answer 2: A trial balance is a report that lists the balances of all general ledger accounts at a particular point in time, with debit and credit amounts. It is used to ensure that the debits and credits have been recorded correctly. The trial balance helps in the preparation of financial statements by identifying any discrepancies in the accounting records, which can then be rectified before finalizing the statements.Question 3: Explain the difference between "AccrualAccounting" and "Cash Accounting."Answer 3: Accrual Accounting is a method of accounting where revenues and expenses are recognized when they are earned or incurred, not necessarily when cash is received or paid. This method provides a more accurate representation of a company's financial performance over a period. Cash Accounting, on the other hand, records transactions only when cash is exchanged. It is simpler and is often used by small businesses or those that operate on a cash basis.Question 4: Describe the process of preparing an income statement.Answer 4: Preparing an income statement involves several steps:1. List all the revenues for the period, such as sales and service income.2. Deduct all the expenses incurred to generate those revenues, including cost of goods sold, operating expenses, and taxes.3. Calculate the net income by subtracting total expenses from total revenues.4. The income statement should reflect the company's profitability over a specified period, typically a month, quarter, or year.Question 5: What are the main components of a balance sheet, and how do they relate to each other?Answer 5: The main components of a balance sheet are:1. Assets: What the company owns or controls with future economic benefit, divided into current assets (short-term) and non-current assets (long-term).2. Liabilities: Obligations the company owes to others, classified as current liabilities (due within one year) and long-term liabilities (due after one year).3. Owner's Equity: The residual interest in the assets of the entity after deducting liabilities, also known as shareholders' equity or net assets.These components are related through the fundamental accounting equation: Assets = Liabilities + Owner's Equity.Question 6: How does depreciation affect a company'sfinancial statements?Answer 6: Depreciation is a non-cash accounting method used to allocate the cost of tangible assets over their useful lives. It affects a company's financial statements in the following ways:1. It reduces the book value of the asset on the balance sheet.2. It increases the accumulated depreciation account, whichis a contra-asset account.3. It decreases net income on the income statement, as depreciation is an expense.4. It can lower taxable income, potentially reducing the company's tax liability.Question 7: What is the purpose of the statement of cash flows, and how does it differ from the income statement?Answer 7: The purpose of the statement of cash flows is to provide information about a company's cash receipts and payments during a period, showing how these cash flows affect the company's financial position. It differs from the income statement in that:1. It focuses on cash transactions, not accrual-basis accounting.2. It categorizes cash flows into operating, investing, and financing activities.3. It does not report net income but rather the net change in cash and cash equivalents.Question 8: Explain the concept of "Going Concern" and its importance in financial reporting.Answer 8: The Going Concern concept assumes that a businesswill continue to operate for the foreseeable future, allowing it to realize its assets and discharge its liabilities in the normal course of business. It is important in financial reporting because it underpins the accrual basis of accounting, which assumes that the business will continue to operate and therefore can recognize revenues and expensesover time.Question 9: What are the ethical considerations in accounting, and why are they important?Answer 9: Ethical considerations in accounting include honesty, integrity, objectivity, and confidentiality. Theyare important because they ensure the reliability andcredibility of financial information, which is crucial for stakeholders to make informed decisions. Ethical behavior also helps maintain public trust。

中级财务会计英文ch0757页

• Acquired intangibles should not be written off at acquisition.

Intangible Assets

Economic benefits last beyond the current period.

Chapter 7-4

Usually acquired for operational use.

Intangible Assets Classification Attributes

Chapter Patents

7-2

Copyrights

Franchises

Intangible Assets

Intangible assets are those noncurrent economic resources that are used in the operations of the business but have no physical existence.

costs. 10. Indicate the presentation of intangible assets and related items.

Chapter 7-1

Intangible Assets

Intangible assets are those noncurrent economic resources that are used in the operations of the business but have no physical existence.

中南财经政法大学成教学位英语考试真题

中南财经政法大学成教学位英语考试真题Title: Zhongnan University of Economics and Law School of Continuing Education Degree English Exam QuestionsIntroduction:Zhongnan University of Economics and Law (ZUEL) is a prestigious university located in Wuhan, China. The School of Continuing Education at ZUEL offers various degree programs for adult learners, including an English exam as part of the assessment process. This article will explore the English exam questions for the School of Continuing Education at ZUEL.Listening Section:1. Listen to the following conversation and answer the questions:Woman: Can you help me find the nearest post office?Man: Sure, it's just two blocks away. You can walk there.Question: Where is the nearest post office located?2. Listen to the weather report and complete the sentences:Today's weather will be __________ with a high of ________ degrees Celsius.Question: What will the weather be like today?Reading Comprehension:Read the following passage and answer the questions:Pandas are adorable animals that are native to China. They are known for their black and white fur and love of bamboo. Unfortunately, pandas are an endangered species due to deforestation and hunting.Questions:1. Where are pandas native to?2. Why are pandas endangered?Writing Section:Write an essay on the importance of environmental protection. Discuss the impact of human activities on the environment and propose solutions to address these issues.Speaking Section:1. Introduce yourself and talk about your hobbies and interests.2. Describe your favorite vacation destination and explain why you enjoy visiting that place.Overall, the English exam for the School of Continuing Education at ZUEL aims to assess students' listening, reading, writing, and speaking skills. By testing their English proficiency, the exam ensures that students are prepared to succeed in their degree programs at ZUEL. Good luck to all test takers!。

中南财经政法大学学位英语考试真题

中南财经政法大学学位英语考试真题全文共3篇示例,供读者参考篇1Central South University of Finance and LawEnglish Proficiency ExamQuestion: Write a persuasive essay on the following topic:"Social media has had significant negative impacts on society and should be more strictly regulated by governments. Social media companies have failed to protect user privacy, enable the spread of misinformation, and negatively impact mental health - especially among young people. Governments need to step in with new laws and regulations to rein in social media's harms."You should aim to write a multi-paragraph persuasive essay of around 2000 words in response to this statement. Be sure to acknowledge counterarguments but ultimately take a clear stance supporting or opposing the proposal put forth.Sample Student Essay:Social media has undoubtedly transformed the world in which we live over the past couple of decades. Platforms like Facebook, Twitter, Instagram and TikTok have connected billions and revolutionized how we communicate, access information, and spend our leisure time. However, I strongly agree that social media's negative impacts on society now outweigh its benefits and that new government regulations are desperately needed.Let's start with privacy - an issue that should concern every social media user. Despite their terms and policies, social media companies have proven themselves to be utterly untrustworthy when it comes to protecting our personal data. Time and again, major breaches and leaks have exposed user data to hackers, advertisers, and who knows who else. Our locations, messages, photos, browsing habits and more have been exploited for profit with minimal consent. Is it any wonder that changes like Europe's GDPR laws have garnered so much public support? I for one don't trust these companies to voluntarily implement sufficient privacy safeguards.Arguably even more disturbing is social media's role in spreading misinformation, hate speech and conspiracy theories on a massive scale. A few national governments have managed to counter anti-vax misinformation during the pandemic, but thisis just the tip of the iceberg. False information continues to rapidly proliferate on these platforms - whether it's related to elections, violence, discriminatory ideologies or pseudoscience. The algorithms designed to maximize engagement paradoxically reward outrageous, emotionally-charged falsehoods over facts. Simply put, social media has become a disinformation dystopia where fringe beliefs and tribalism reign. We cannot have a shared reality or rational discourse when everyone exists in their own filter bubble.As if that weren't bad enough, we're also now seeing major mental health impacts - particularly among young and teenage users. The constant pursuit of validation through likes and shares, addictive endless scrolling, relentless comparisons to perfected selfies and influencer lifestyles - it's no wonder rates of anxiety, depression, and even suicide have spiked since social media's meteoric rise. Do we really want our youth's formative years and self-esteem being shaped by these psychologically manipulative apps? I have friends who have deleted Instagram and Snapchat for their own wellbeing. Even former employees at these companies now admit to unease over the mental health consequences of social media. This level of harm demands intervention.Some may argue that government regulation could infringe on free speech and expression. I absolutely believe in those core democratic rights and values. However, we already have limitations and rules around yelling "fire" in a crowded theater, incitements to violence, defamation laws and so on. We must find reasonable ways to extend those principles to the social media age. Others may claim that social media is simply reflecting human nature - craving attention, tribalism, and outrage have existed long before Facebook. That may be partially true. But these platforms are also specifically engineered to exploit those impulses through endless newsfeeds, autoplay videos, and algorithms optimizing for engagement over truth and healthy discourse.So yes, while I admit there are complexities and valid concerns around excessive regulation, the status quo has become intolerable. We need governments to step up with common sense rules around user privacy, content moderation, and protecting the mental health of young people. Social media cannot be a total "Wild West" of privacy invasions, viral falsehoods, and psychological manipulation - especially not when it comes to kids. Tech companies have demonstrated they won't properly self-regulate.Perhaps we could implement data privacy laws with harsh penalties and required consent over use of personal information. Independent fact-checking oversight of viral posts could combat misinformation while still protecting free speech. Age restrictions, mental health disclosure requirements and ethical caps on attention-grabbing algorithms could help shield young minds from harm. Substantial fines or even temporary shutdowns could incentivize compliance.Whatever precise policy mix is enacted, one thing is clear - something must be done about social media's unchecked abuses. Core individual rights like privacy, access to truth, and mental wellbeing are being eroded on a generational scale for profit. The technology shaping our society and youth requires democratic, ethical oversight. We can't afford to be passive consumers about this any longer. Our humanity depends on reasonably governing these powerful platforms before it's too late.篇2The Postgraduate Entrance Exam: My Experience with the English SectionAs a fresh graduate eager to further my education, the postgraduate entrance exam loomed large on my horizon. Among the various sections, the English test was undoubtedly one of the most daunting challenges. With its reputation for being notoriously difficult, I knew I had to prepare diligently to stand a chance of securing a coveted spot in Zhongnan University of Economics and Law's prestigious graduate program.The weeks leading up to the exam were a whirlwind of intense study sessions, practice tests, and a constant battle against the nagging fear of underperformance. I pored over vocabulary lists, grammar rules, and past exam papers, determined to leave no stone unturned in my quest for mastery.Finally, the day of reckoning arrived, and I found myself seated in a vast examination hall, surrounded by hundreds of fellow test-takers, each of us united in our shared goal yet fiercely competitive. The air was thick with anticipation and apprehension.The English section kicked off with a reading comprehension passage that seemed deceptively straightforward at first glance. However, as I delved deeper into the intricacies of the text, I quickly realized that the questions were designed to test notonly our understanding of the material but also our ability to draw nuanced inferences and critically analyze the author's arguments.Next came the dreaded cloze test, a ruthless exercise that forced us to navigate the treacherous waters of vocabulary and grammar simultaneously. I found myself agonizing over each blank, meticulously weighing the subtle shades of meaning conveyed by different word choices. It was a mental gymnastics routine that left me utterly drained by the end.The writing section presented its own unique set of challenges. We were tasked with crafting a well-structured and logically sound essay on a thought-provoking prompt. As I scratched away furiously with my pen, trying to juggle coherent arguments and elegant phrasing, I couldn't help but feel a pang of envy for those who possessed an innate flair for the written word.But the true test of my English prowess came in the form of the listening comprehension section. The audio recordings, delivered in a dizzying array of accents and speech patterns, seemed to conspire against my auditory faculties. I found myself straining to catch every word, desperately scribbling notes as thespeakers rattled on, their voices fading in and out like a radio station with poor reception.As the exam drew to a close, I couldn't help but feel a mixture of relief and trepidation. Relief that the ordeal was finally over, but trepidation at the thought of how I had fared. Had my efforts been enough? Had I adequately demonstrated my command of the English language?In the end, the postgraduate entrance exam's English section proved to be a formidable foe, but one that I faced head-on with determination and resilience. It was a baptism by fire, a trial that tested not only my linguistic skills but also my mental fortitude and ability to perform under pressure.Looking back, I can't help but feel a sense of pride in having tackled such a daunting challenge. The experience has instilled in me a newfound respect for the complexities of the English language and a renewed appreciation for the dedication required to truly master it.As I anxiously await the results, I can take solace in the knowledge that, regardless of the outcome, I have emerged from this experience a stronger, more resilient individual, better equipped to face the academic and professional challenges that lie ahead.篇3The Trials and Tribulations of the Zhongnan University English Proficiency ExamAs students at Zhongnan University of Economics and Law, we all know that the English proficiency exam is a rite of passage. It's a test that strikes fear into the hearts of even the most diligent scholars. I still have nightmares about the time I took it last semester.I remember walking into the exam hall, clutching my pencils and feeling like I was marching to my doom. The room was deathly silent, except for the sound of nervous foot-tapping and pages turning. I took a deep breath and opened the exam booklet, bracing myself for the onslaught of questions.The first section was listening comprehension, which is always a doozy. They played these bizarre recordings of people with the strangest accents imaginable, talking about topics that ranged from quantum physics to artisanal cheese-making. I'm pretty sure one of the passages was in Klingon. I scribbled down my answers, praying that I hadn't just written "the quick brown fox jumps over the lazy dog" over and over again.Next up was the reading section, which is usually my strongest suit. But on that fateful day, the passages seemed to be written in some sort of indecipherable code. I struggled through dense paragraphs about international trade agreements and the mating habits of the Australian platypus. By the time I reached the end, my brain felt like it had been put through a blender.The writing section was equally brutal. The prompt asked us to argue whether or not pineapple belongs on pizza, which is a debate that has raged for centuries. I spent a good twenty minutes just staring at the page, trying to come up with a coherent thesis statement that didn't involve phrases like "unholy abomination" or "culinary sacrilege."But the true test of endurance was the speaking section. We had to record ourselves answering questions about our daily routines, our future plans, and our opinions on the geopolitical implications of the Skywalker saga. I'm pretty sure I just mumbled incoherently for most of it, occasionally throwing in words like "contingency" and "paradigm shift" to sound intelligent.By the time the exam was over, I felt like I had been through a war. I stumbled out of the hall, dazed and disoriented,wondering if I had just experienced some sort of elaborate hazing ritual.In the end, I passed the exam by the skin of my teeth. But the experience left me with a newfound respect for the English language and a burning desire to never again set foot in that cursed exam hall.To my fellow students who are gearing up to take the proficiency exam, I wish you the best of luck. Study hard, get plenty of rest, and remember: even if you bomb the test, at least you'll have a funny story to tell your grandchildren someday.And to the sadistic souls who create these exams, I have just one thing to say: You're monsters. Absolute monsters.。

中南财经政法大学会计学院

中南财经政法大学会计学院School of Accounting, Zhongnan University of Economics & Law中级会计学(英文)课程(Intermediate Accounting)教学大纲(SYLLABUS)《中级财务会计》教学小组编写Teaching Team of Intermediate Accounting2006年2月修订(Feb.2006)Course NatureThis course is designed for undergraduate students majoring in accounting and auditing. It is arranged in the fourth or fifth semester. It is aimed to enhance students’ ability both in western accounting knowledge and professional English, and to improve competitive for their job.The teaching content and arrangements of this course should be strictly according to this teaching outline.Teaching ObjectiveAfter finishing learning this course, the students are required to understand the fundamenta western accounting theory, accounting concepts and the procedures and skills in dealing with the preparation of financial statements. By comparing the major differences of accounting treatment between U.S.A and China, the students are required to make comments on Chinese and US accounting standards and make research on them.Teaching ContentLesson 1 THE ENVIRONMENT OF FINANCIAL REPORTINGForewordsI. Accounting information: users, uses, and GAAP in U.S.A.2.The development of accounting standards in U.S.A.2.1 Brief history of development of accounting standards – CAP, APB, FASB2. 2 Financial Accounting Standards Board (FASB)2.2.1 Organization1.2.2 Statements issued by FASB3. Other organizations currently influencing GAAP in U.S.A.3.1 SEC, AICPA, EITF, CASB, IRS, AAA, IASC/IASB, GASB, professional organizations3.2 Relationship of organizations in current standard setting environment4.Ethics in the accounting environment5. Comparison of the development of accounting standards in China and in U.S.A. (Case)Lesson 2 FINANCIAL REPORTING:ITS CONCEPTUAL FRAMEWORK1.FASB conceptual framework1.1 General value of framework1.2 Nature and components of the FASB’s conceptual framework2.Objectives of financial reporting3.Qualitative characteristics of accounting information3. 1 Hierarchy of qualitative characteristics3.2 Pervasive constraint: benefits > cost3.3 Primary decision-specific qualities.3.3.1. Relevance3.3.2. Reliability3.4 Secondary decision-specific qualities- Comparability and consistency3.5 Threshold for recognition: materiality.4. Accounting assumptions and conventions4.1 Assumptions-- E ntity, Continuity (going-concern), Period of time, Monetary unit4. 2 Conventions-- Historical cost, Realization and recognition, matching and accrual accounting, Conservatism (prudence)5. Elements of financial statements5.1 Balance sheet – Asset, Liability, Equity5.2 Income statement – Revenue, Expenses, Gains, Losses5. 3 Statement of cash flows—Operating cash flows, Investing cash flows, Financing cash flows5.4 Statement of changes in equity—Investment by owners, Distribution to owners6. Comparison of accounting concepts in China and in U.S.A. (Case)Lesson 3 THE BALANCE SHEET AND STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITY1.Interrelationship of financial statements2.Elements of the balance sheet3. Measurement of the elements of the balance sheet4. Reporting classifications on the balance sheet4. 1 Asset and liability classifications4. 2 Conceptual guidelines for reporting assets and liabilities4. 3 Stockholders' equity classifications5. Limitations of the balance sheet6. Statement of changes in stockholders' equityII Other disclosure issues8. Reporting techniques9. Balance Sheet analysisLesson 4 THE INCOME STATEMENT AND INCOME RECOGNITION1. Concepts of income1. 1 Capital maintenance1. 2 Transactional approach2. Elements of the income statement3. Income statement content3.1 Income from continuing operations3.2 Results from discontinued operations3.3 Extraordinary items3.4 Effects of accounting changes3.5 Earnings per share4. Income statement formats4.1 Single-step4.2 Multiple-step5. Limitations of the income statement6. Income Statement analysis7. Comprehensive income8. Conceptual issues of revenue recognition8.1 Revenue recognition criteria8.2 E conomic substance versus legal form8.3 Transfer of risks and benefits8.4 Collectibility of receivable9. Revenue recognition alternatives9.1 Normal revenue recognition9. 2 Revenue recognition prior to the period of sale9. 3Revenue recognition after the period of saleLesson 5 THE STATEMENT OF CASH FLOWS1.Conceptual overview and uses of the Statement of Cash Flows2.Structure of the Statement of Cash Flows2.1 Three categories of cash flows.2.2 Supplemental disclosures3.Reporting Cash Flow From OperationsOperating cycleTwo methods3.2.1 Direct method--Illustration3.2.2 Indirect method-- Illustration4.Preparing a complete Statement of Cash FlowsA six-step process for preparing a statement of cash flows.ing cash flow data to assess financial strengthChapter 6 CASH AND RECEIVABLESI. Accounting for cash1.1 Measurement as a current asset1.2 Cash and cash equivalents1.3 Cash management1.4 Petty cash system2. Bank reconciliation3. Special topics3.1 Electronic funds transfer systems3.2 Compensating balances4. Receivables4.1 Classifications4.1.1 Current vs noncurrent4.1.2 Trade receivables4.1.3 Nontrade receivables4.2 Valuation issues4.2.1 Initial recording based on expected future cash flows4.2.2 Estimation of the probability of collection5. Accounts receivable5. 1 Cash (sales) discounts5.2 Sales returns and allowances6. Valuation of accounts receivable for uncollectible accounts6.1 Estimated bad debts method6.1.1 Income statement approach6.1.2 Balance sheet approach6.2 Recording bad debts6.3 Writing off uncollectible accounts6.4 Collection of an account previously written-off6.5 Direct write-off method7. Generating immediate cash from accounts receivable7.1 Conceptual issues7.2 Pledging7.3 Assignment7.4 Factoring of receivables7.5 Disclosure of financing agreements8. Notes receivable (short-term)Lesson 7 INVENTORIES1. Classifications of inventoryIII. A lternative inventory systems2. 1 Perpetual2. 2 Periodic3. Items to be included in inventory quantities4. Determination of inventory costs4.1Items included in inventory cost.4.2 Discounts as reductions in cost.4.3 Purchase returns and allowances.4.4 Summary5. Inventory valuation methods5. 1 Specific identification5. 2 First-in, first-out (FIFO)5. 3 Average cost5. 4 Last-in, first-out (LIFO)5. 5 Comparison6. Inventory valuation at other than cost6. 1 Lower of cost or market (LCM)6. 1.1 Application of LCM6.1.2 Conceptual evaluation of ceiling and floor6.1.3 Approaches to applying LCM6.1.4 Recording the reduction of inventory to market6.1.5 LCM and interim financial statements6.1.6 Conceptual evaluation of LCM6.2 Gross profit method6.3 Retail inventory method7. Effects of inventory errorsLesson 8 PROPERTY, PLANT, AND EQUIPMENT1. Classification as property, plant, and equipment (PPE)1.1 Characteristics1.2 Evaluation of use of historical cost2. Acquisition of PPE3. Assets acquired by exchange of other assets3.1 Definition of nonmonetary exchange3.2 Dissimilar productive asset exchanges3.3 Similar productive asset exchanges3.4 Comparison of accounting treatments in China and in U.S.A. (Case)4. Self-construction4.1 Interest during construction4.2 Fixed overhead costs5. Costs subsequent to acquisition6. Disposal of property, plant, and equipment7. Disclosure of property, plant, and equipment8. Depreciation and depletion8.1 Cost allocation terms8.2 Factors involved in depreciation8.3 Methods of cost allocation8.4 Conceptual evaluation of depreciation methods8.5 Disclosure requirements for depreciation8.6 Depreciation for partial periods8.7 Depletion9. Impairment of noncurrent assets9.1 Impairment test9.2 Measurement of loss9.3 Conceptual evaluationLesson 9 INTANGIBLES1. Accounting for intangibles1.1 Cost1.2 Amortization or impairment2. Research and development (R&D)2.1 Definitions2.2 Costs included as R&D2.3 Cost treatment2.4 Conceptual evaluation of accounting for R&D costs3.Identifiable intangible assets4. Unidentifiable intangibles5. Disclosure of intangibles5.1 In period intangible assets are acquired5.2 In each period company presents a balance sheet6. Conceptual evaluation of accounting for intangiblesLesson 10 CURRENT LIABILITIES AND CONTINGENCIES1. Conceptual overview of liabilities2. Nature and definition of current liabilities2.1 Liquidation expected within a year or an operating cycle, whichever is longer2.2 Liquidity and financial flexibility2.3 Classification3.Valuation of current liabilities4. Current liabilities having a contractual amount5. Current liabilities whose amounts depend on operations6. Current liabilities requiring amounts to be estimated7. Contingencies7.1 Definition in FASB Statement No. 57.2 Accrual of loss contingencies7.3 Disclosure of loss contingencies in notes to financial statements7.4 Disclosure of gain contingencies in notes to financial statements8. Other liability classification issues8.1 Short-term debt expected to be refinanced8.2 Classification of obligations that are callable by the creditor9. Presentation of current liabilities in the financial statementsLesson 11 LONG-TERM LIABILITIES AND RECEIVABLES1. Reasons for issuance of long-term liabilities2. Bonds payable2.1 Terms2.2 Bond selling prices2.3 Recording the issuance of bonds2.3.1 Premium on bonds payable: adjunct account2.3.2 Discount on bonds payable: contra account2.3.3 Carrying (book) value2 4. Bonds issued between interest payment dates2.5 Amortizing discounts and premiums2.5.1 Straight-line method2.5.2 Effective interest method3. Extinguishment of liabilities3.1 Bonds retired at maturity3.2 Bonds retired prior to maturity4. Bonds with equity characteristics5. Long-term notes payable5. 1 Notes payable issued for cash5. 2 Notes payable exchanged for cash and rights or privileges5.3 Notes payable exchanged for property, goods, or services5.4 Disclosure of long-term liabilitiesLesson 12 INVESTMENTS1. Investments: classification and valuation1.1 Trading securities1.2 Available-for-sale securities1.3 Held-to-maturity debt securities1.4 Definitions2. Investments in debt and equity trading securities3. Investments in available-for-sale debt and equity securities3.1 Recording initial cost3.2. Recording interest and dividend revenue3.3 Recognition of unrealized holding gains and losses3.4 Realized gains (losses) on sales of securities available-for-sale4. Investments in held-to-maturity debt securities4.1 Recording initial cost4.2 Recognition and amortization of bond premiums and discounts4.2.1 Methods4.2.1.1 Effective-interest method4.2.1.2 Straight-line method4.2.2 Premium amortization reduces investment account4.2.3 Discount amortization increases investment account4.3 Amortization for bonds acquired between interest dates4.4 Sale of investment in bonds before maturity5. Transfers and impairments5.1 Transfers of investments between categories (at fair value)5.2 Impairments6. Disclosures7. Financial statement classification8. Equity method8.1 Criteria for use8.2 Accounting procedures8.3 Financial statement disclosuresLesson 13 CONTRIBUTED CAPITAL1. Introduction2. Corporate capital structure2.1 Definitions2.2 Capital stock and stockholders' rights2.3 Basic terminology2.4 Legal capital2.5 Additional paid-in capital3. Issuance of capital stock3.1 Issuance for cash3.2. Stock issuance costs3.3 Stock subscriptions3.4 Combined sales of stock3.5 Nonmonetary issuance of stock3.6 Stock splits3.7 Stock rights to current stockholders4. Preferred stock characteristics4.1 Preference as to dividends4.2 Cumulative vs. noncumulative4.3 Participating4.4 Preference in liquidation4.5 Voting rights4.6 Disclosures5. Contributed capital section5.1 Segments5.2 Disclosure requirementsLesson 14 EARNINGS PER SHARE AND RETAINED EARNINGS1. Earnings and earnings per share2. Conceptual overview and uses of earnings per share information3. Basic earnings per share3.1 Basic earnings per share equation3.2 Numerator calculations3.2.1 Noncumulative preferred stock3.2.2 Cumulative preferred stock3.3 Denominator calculations3.4 Components of earnings per share4. Diluted earnings per share4.1 Definitions4.2 Two presentations4.2.1 Basic earnings per share4.2.2 Diluted earnings per share (DEPS)4.3 Computational steps4.4 Stock options and warrants4.5 Convertible securities4.6 Computation of tentative and final DEPS5. Content of retained earnings6. Dividends6.1 Cash dividends6.2 Property dividends6.3 Scrip dividends6.4 Stock dividends6.5 Liquidating dividends7. Prior period adjustments8. Appropriations of retained earnings9. Statement of retained earnings9.1 Prior period adjustments9.2 Net income9.3 Dividends9.4 Other deductions10. Accumulated other comprehensive incomeTeaching Arrangement1 Time allocationThe total class hour is 51, with 3 scores. Lectures in class are divided into 4 teaching units. The time allocation for each teaching unit is as follows:2 Teaching methodsThis course mainly adopts lecture in class, with the help of multimedia. We also allocates some presentations after group discussion out of classroom. It is taught either in English or in the combination of both English and Chinese.3. Exam form and requirementsAfter finishing the course, it will be tested in English, no matter the course is taught in English or in the combination of both English and Chinese. Normally , it adopts the close book test , if applied and allowed by the officers, it could be tested in other form according to the situation.The formats of the final exam paper includes multiple choice, translation both from English to Chinese and from Chinese to English , identification of true of false, case analysis writing, making journal entries, calculation, preparation of the worksheet for the financial statements , preparation of balance sheet, income statement and cash flow statements, and the analysis of the financial statements, ect.4. Scoring systemIt adopts 100% scoring system. The final score consists of 2 parts, one is the score of the final exam, the other is the score of daily performance, which including assignment, attendance and discussion performance etc. The proportion of this two parts depends on the requirement of university.Teaching Materials1. Textbook《中级会计学》(高等学校会计学类英文版教材),高等教育出版社,2005年1月第1版(Intermediate Accounting, 9E, by Loren A. Nikolai John D. Bazley)2. ReferencesA. 《中级会计学》(会计类原版教材影印系列),中国财政经济出版社,2002年11月第1版(Intermediate Accounting, 14E, by Earl Kay Stice, James D. Stice, K. Fred Skousen )B. Statements of Financial Accounting Standards, by FASBC. International Accounting Standards / International Financial Reporting StandardsD. Chinese Accounting Standards for Enterprises3. Related intenet web sitesA. FASB B. IASB C. the Nikolai and Bazley Intermediate Accounting web site )。

中级会计职称证书 英文版