博迪投资学第九版英文答案

博迪的投资学第一章练习题(英)

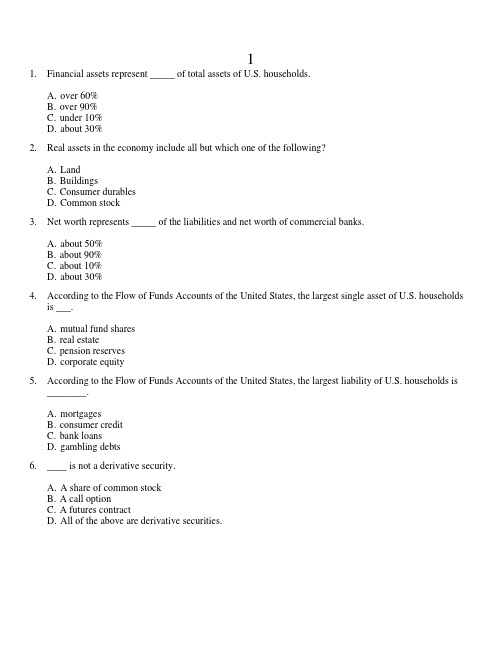

11.Financial assets represent _____ of total assets of U.S. households.A. over 60%B. over 90%C. under 10%D. about 30%2.Real assets in the economy include all but which one of the following?A. LandB. BuildingsC. Consumer durablesD. Common stock worth represents _____ of the liabilities and net worth of commercial banks.A. about 50%B. about 90%C. about 10%D. about 30%4.According to the Flow of Funds Accounts of the United States, the largest single asset of U.S. householdsis ___.A. mutual fund sharesB. real estateC. pension reservesD. corporate equity5.According to the Flow of Funds Accounts of the United States, the largest liability of U.S. households is________.A. mortgagesB. consumer creditC. bank loansD. gambling debts6.____ is not a derivative security.A. A share of common stockB. A call optionC. A futures contractD. All of the above are derivative securities.7.According to the Flow of Funds Accounts of the United States, the largest financial asset of U.S.households is ____.A. mutual fund sharesB. corporate equityC. pension reservesD. personal trusts8.Active trading in markets and competition among securities analysts helps ensure that __________.I. security prices approach informational efficiencyII. riskier securities are priced to offer higher potential returnsIII. investors are unlikely to be able to consistently find under- or overvalued securitiesA. I onlyB. I and II onlyC. II and III onlyD. I, II and III9.The material wealth of society is determined by the economy's _________, which is a function of theeconomy's _________.A. investment bankers, financial assetsB. investment bankers, real assetsC. productive capacity, financial assetsD. productive capacity, real assets10.Which of the following is not a money market security?A. U.S. Treasury billB. Six month maturity certificate of depositC. Common stockD. Banker's acceptance11.__________ assets generate net income to the economy and __________ assets define allocation of incomeamong investors.A. Financial, financialB. Financial, realC. Real, financialD. Real, real12.Which of the following are financial assets?I. Debt securitiesII. Equity securitiesIII. Derivative securitiesA. I onlyB. I and II onlyC. II and III onlyD. I, II and III13.__________ are examples of financial intermediaries.A. Commercial banksB. Insurance companiesC. Investment companiesD. All of the above are financial intermediaries14.Asset allocation refers to the _________.A. allocation of the investment portfolio across broad asset classesB. analysis of the value of securitiesC. choice of specific assets within each asset classD. none of the answers define asset allocation15.Which one of the following best describes the purpose of derivatives markets?A. Transferring risk from one party to anotherB. Investing for a short time period to earn a small rate of returnC. Investing for retirementD. Earning interest income16.__________ was the first to introduce mortgage pass-through securities.A. Chase ManhattanB. CiticorpC. FNMAD. GNMA17.Security selection refers to the ________.A. allocation of the investment portfolio across broad asset classesB. analysis of the value of securitiesC. choice of specific securities within each asset classD. top down method of investing18._____ is an example of an agency problem.A. Managers engage in empire buildingB. Managers protect their jobs by avoiding risky projectsC. Managers over consume luxuries such as corporate jetsD. All of the answers provide examples of agency problems19._____ is a mechanism to mitigate potential agency problems.A. Tying income of managers to success of the firmB. Directors defending top managementC. Anti takeover strategiesD. Straight voting method of electing the board of directors20.__________ are real assets.A. BondsB. Production equipmentC. StocksD. Commercial paper21.__________ portfolio construction starts with selecting attractively priced securities.A. Bottom-upB. Top-downC. Upside-downD. Side-to-side22.In a capitalist system capital resources are primarily allocated by ____________.A. governmentsB. the SECC. financial marketsD. investment bankers23. A __________ represents an ownership share in a corporation.A. call optionB. common stockC. fixed-income securityD. preferred stock24.The value of a derivative security _________.A. depends on the value of other related securityB. affects the value of a related securityC. is unrelated to the value of a related securityD. can only be integrated by calculus professors25. A bond issue is broken up so that some investors will receive interest payments while others will receiveprincipal payments. This is an example of _________.A. bundlingB. credit enhancementC. securitizationD. unbundling26.__________ portfolio management calls for holding diversified portfolios without spending effort orresources attempting to improve investment performance through security analysis.A. ActiveB. MomentumC. PassiveD. Market timing27.Financial markets allow for all but which one of the following?A. Shift consumption through time from higher income periods to lowerB. Price securities according to their riskinessC. Channel funds from lenders of funds to borrowers of fundsD. Allow most participants to routinely earn high returns with low risk28.Financial intermediaries exist because small investors cannot efficiently _________.A. diversify their portfoliosB. gather informationC. monitor their portfoliosD. all of the answers provide reasons why29.Methods to encourage managers to act in shareholders' best interest includeI. Threat of takeoverII. Proxy fights for control of the Board of DirectorsIII. Tying managers' compensation to stock price performanceA. I onlyB. I and II onlyC. II and III onlyD. I, II and III30.Firms that specialize in helping companies raise capital by selling securities to the public are called_________.A. pension fundsB. investment banksC. savings banksD. REITs31.In securities markets, there should be a risk-return trade-off with higher-risk assets having _________expected returns than lower-risk assets.A. higherB. lowerC. the sameD. Can't tell from the information given32.__________ are an indirect way U.S. investors can invest in foreign companies.A. ADRsB. IRAsC. SDRsD. CPCs33.Security selection refers to _________.A. choosing specific securities within each asset-classB. deciding how much to invest in each asset-classC. deciding how much to invest in the market portfolio versus the riskless assetD. deciding how much to hedge34.An example of a derivative security is _________.A. a common share of General MotorsB. a call option on Intel stockC. a Ford bondD. a U.S. Treasury bond35.__________ portfolio construction starts with asset allocation.A. Bottom-upB. Top-downC. Upside-downD. Side-to-side36.Which one of the following firms falsely claimed to have a $4.8 billion bank account at Bank of Americaand vastly understated its debts, eventually resulting in the firm's bankruptcy?A. WorldComB. EnronC. ParmalatD. Global Crossing37.Debt securities promise _________.I. a fixed stream of incomeII. a stream of income that is determined according to a specific formulaIII. a share in the profits of the issuing entityA. I onlyB. I or II onlyC. I and III onlyD. II or III only38.The Sarbanes-Oxley Act tightened corporate governance rules by requiring all but which one of thefollowing?A. Required corporations to have more independent directorsB. Required the CFO to personally vouch for the corporation's financial statementsC. Required that firms could no longer employ investment bankers to sell securities to the publicD. The creation of a new board to oversee the auditing of public companies39.The success of common stock investments depends on the success of _________.A. derivative securitiesB. fixed income securitiesC. the firm and its real assetsD. government methods of allocating capital40.The historical average rate of return on the large company stocks since 1926 has beenA. 5%B. 8%C. 12%D. 20%41.The average rate of return on U.S. Treasury bills since 1926 was _________.A. 0.5%B. 2.4%C. 3.8%D. 6.0%42.An example of a real asset is _________.I. a college educationII. customer goodwillIII. a patentA. I onlyB. II onlyC. I and III onlyD. I, II and III43.The 2002 law designed to improve corporate governance is titled theA. Pension Reform ActB. ERISAC. Financial Services Modernization ActD. Sarbanes-Oxley Act44.Which of the following is not a financial intermediary?A. a mutual fundB. an insurance companyC. a real estate brokerage firmD. a savings and loan company45.The combined liabilities of American households represent approximately __________ percent ofcombined assets.A. 11%B. 21%C. 25%D. 33%46.In 2008 real assets represented approximately __________ percent of the total asset holdings of Americanhouseholds.A. 37%B. 42%C. 48%D. 55%47.In 2008 mortgages represented approximately __________ percent of total liabilities and net worth ofAmerican households.A. 12%B. 15%C. 28%D. 42%48.Liabilities equal approximately _____ of total assets for nonfinancial U.S. businesses.A. 10%B. 25%C. 44%D. 75%49.Which of the following is not an example of a financial intermediary?A. Goldman SachsB. Allstate InsuranceC. First Interstate BankD. IBM50.Real assets represent about ____ of total assets for financial institutions.A. 1%B. 15%C. 25%D. 40%51.Money Market securities are characterized by ________.I. maturity less than one yearII. safety of the principal investmentIII. low rates of returnA. I onlyB. I and II onlyC. I and III onlyD. I, II and III52.After much investigation an investor finds that Intel stock is currently under priced. This is an example of______.A. asset allocationB. security analysisC. top down portfolio managementD. passive management53.After considering current market conditions an investor decides to place 60% of their funds in equities andthe rest in bonds. This is an example ofA. asset allocationB. security analysisC. top down portfolio managementD. passive management54.Suppose an investor is considering one of two investments which are identical in all respects except forrisk. If the investor anticipates a fair return for the risk of the security they invest in they can expect toA. earn no more than the Treasury bill rate on either securityB. pay less for the security that has higher riskC. pay less for the security that has lower riskD. earn more if interest rates are lower55.The efficient markets hypothesis suggests that _______.A. active portfolio management strategies are the most appropriate investment strategiesB. passive portfolio management strategies are the most appropriate investment strategiesC. either active or passive strategies may be appropriate, depending on the expected direction of the marketD. a bottom up approach is the most appropriate investment strategy56.In a perfectly efficient market the best investment strategy is probably a/anA. active strategyB. passive strategyC. asset allocationD. market timing57.An important trend that has changed the contemporary investment market is _________.A. financial engineeringB. globalizationC. securitizationD. all three of the other answers58.Securitization refers to the creation of new securities by _________.A. selling individual cash flows of a security or loanB. repackaging individual cash flows of a security or loan into a new payment patternC. taking an illiquid asset and converting it into a marketable securityD. selling financial services overseas as well as in the U.S.59.Brady bonds were an example of _________.A. securitizationB. mortgagizationC. bundlingD. pass through securities60.Individuals may find it more advantageous to purchase claims from a financial intermediary rather thandirectly purchasing claims in capital markets becauseI. intermediaries are better diversified than most individualsII. intermediaries can exploit economies of scale in investing that individual investors cannotIII. intermediated investments usually offer higher rates of return than direct capital market claimsA. I onlyB. I and II onlyC. II and III onlyD. I, II and III61.Surf City Software Company develops new surf forecasting software. It sells the software to Microsoft inexchange for 1000 shares of Microsoft common stock. Surf City Software has exchanged a _____ asset fora _____ asset in this transaction.A. real, realB. financial, financialC. real, financialD. financial, real62.Stone Harbor Products takes out a bank loan. It receives $100,000 and signs a promissory note to pay backthe loan over 5 years.A. A new financial asset was created in this transaction.B. A financial asset was traded for a real asset in this transaction.C. A financial asset was destroyed in this transaction.D. A real asset was created in this transaction.63.Which of the following firms was not engaged in a major accounting scandal between 2000 and 2005?A. General ElectricB. ParmalatC. EnronD. WorldCom64.Accounting scandals can often be attributed to a particular concept in the study of finance known as theA. agency problemB. risk - return trade - offC. allocation of riskD. securitization65.An intermediary that pools and manage funds for many investors is called a/an ______.A. investment companyB. savings and loanC. investment bankerD. ADR66.Financial institutions that specialize in assisting corporations in primary market transactions are called_______.A. mutual fundsB. investment bankersC. pension fundsD. globalization specialists67.WEBS allow investors to _______.A. invest in U.S. mortgage backed securitiesB. invest in an individual foreign stockC. invest in a portfolio of foreign stocksD. avoid any exposure to foreign exchange risk68.In 2008 the largest corporate bankruptcy in the U.S. history involved the investment banking firm of______.A. Goldman SachsB. Lehman BrothersC. Morgan StanleyD. Merrill Lynch69.The inability of shareholders to influence the decisions of managers, despite overwhelming shareholdersupport, is a breakdown in what process or mechanism?A. AuditingB. Public financeC. Corporate governanceD. Public reporting70.Real assets are ______.A. are assets used to produce goods and servicesB. always the same as financial assetsC. always equal to liabilitiesD. claims on company's income71. A major cause of mortgage market meltdown in 2007 and 2008 was linked to ________.A. globalizationB. securitizationC. negative analyst recommendationsD. online trading72.In recent years the greatest dollar amount of securitization occurred for which type loan?A. Home mortgagesB. Credit card debtC. Automobile loansD. Equipment leasing73.The process of securitizing poor quality bank loans made to developing nations resulted in the creation of__________.A. Pass-throughsB. Brady bondsC. WEBSD. FHLMC participation certificates74.U.S. Treasury bonds pay interest every six months and repay the principal at maturity. The U.S.Treasury routinely sells individual interest payments on these bonds to investors. This is an example of ___________.A. unbundlingB. bundlingC. securitizationD. security selection75.An investment advisor has decided to purchase gold, real estate, stocks, and bonds in equal amounts. Thisdecision reflects which part of the investment process?A. Asset allocationB. Investment analysisC. Portfolio analysisD. Security selection1 Key1.Financial assets represent _____ of total assets of U.S. households.A. over 60%B. over 90%C. under 10%D. about 30%Bodie - Chapter 01 #1Difficulty: Easy2.Real assets in the economy include all but which one of the following?A. LandB. BuildingsC. Consumer durablesD. Common stockBodie - Chapter 01 #2Difficulty: Easy worth represents _____ of the liabilities and net worth of commercial banks.A. about 50%B. about 90%C. about 10%D. about 30%Bodie - Chapter 01 #3Difficulty: Medium 4.According to the Flow of Funds Accounts of the United States, the largest single asset of U.S.households is ___.A. mutual fund sharesB. real estateC. pension reservesD. corporate equityBodie - Chapter 01 #4Difficulty: Medium 5.According to the Flow of Funds Accounts of the United States, the largest liability of U.S. households is________.A. mortgagesB. consumer creditC. bank loansD. gambling debtsBodie - Chapter 01 #5Difficulty: Medium6.____ is not a derivative security.A. A share of common stockB. A call optionC. A futures contractD. All of the above are derivative securities.Bodie - Chapter 01 #6Difficulty: Easy 7.According to the Flow of Funds Accounts of the United States, the largest financial asset of U.S.households is ____.A. mutual fund sharesB. corporate equityC. pension reservesD. personal trustsBodie - Chapter 01 #7Difficulty: Medium8.Active trading in markets and competition among securities analysts helps ensure that __________.I. security prices approach informational efficiencyII. riskier securities are priced to offer higher potential returnsIII. investors are unlikely to be able to consistently find under- or overvalued securitiesA. I onlyB. I and II onlyC. II and III onlyD. I, II and IIIBodie - Chapter 01 #8Difficulty: Hard 9.The material wealth of society is determined by the economy's _________, which is a function of theeconomy's _________.A. investment bankers, financial assetsB. investment bankers, real assetsC. productive capacity, financial assetsD. productive capacity, real assetsBodie - Chapter 01 #9Difficulty: Medium10.Which of the following is not a money market security?A. U.S. Treasury billB. Six month maturity certificate of depositC. Common stockD. Banker's acceptanceBodie - Chapter 01 #10Difficulty: Medium11.__________ assets generate net income to the economy and __________ assets define allocation ofincome among investors.A. Financial, financialB. Financial, realC. Real, financialD. Real, realBodie - Chapter 01 #11Difficulty: Medium12.Which of the following are financial assets?I. Debt securitiesII. Equity securitiesIII. Derivative securitiesA. I onlyB. I and II onlyC. II and III onlyD.I, II and IIIBodie - Chapter 01 #12Difficulty: Hard13.__________ are examples of financial intermediaries.A. Commercial banksB. Insurance companiesC. Investment companiesD. All of the above are financial intermediariesBodie - Chapter 01 #13Difficulty: Easy14.Asset allocation refers to the _________.A.allocation of the investment portfolio across broad asset classesB. analysis of the value of securitiesC. choice of specific assets within each asset classD. none of the answers define asset allocationBodie - Chapter 01 #14Difficulty: Easy15.Which one of the following best describes the purpose of derivatives markets?A.Transferring risk from one party to anotherB. Investing for a short time period to earn a small rate of returnC. Investing for retirementD. Earning interest incomeBodie - Chapter 01 #15Difficulty: Medium16.__________ was the first to introduce mortgage pass-through securities.A. Chase ManhattanB. CiticorpC. FNMAD. GNMABodie - Chapter 01 #16Difficulty: Easy17.Security selection refers to the ________.A. allocation of the investment portfolio across broad asset classesB. analysis of the value of securitiesC.choice of specific securities within each asset classD. top down method of investingBodie - Chapter 01 #17Difficulty: Medium18._____ is an example of an agency problem.A. Managers engage in empire buildingB. Managers protect their jobs by avoiding risky projectsC. Managers over consume luxuries such as corporate jetsD. All of the answers provide examples of agency problemsBodie - Chapter 01 #18Difficulty: Easy19._____ is a mechanism to mitigate potential agency problems.A. Tying income of managers to success of the firmB. Directors defending top managementC. Anti takeover strategiesD. Straight voting method of electing the board of directorsBodie - Chapter 01 #19Difficulty: Hard20.__________ are real assets.A. BondsB. Production equipmentC. StocksD. Commercial paperBodie - Chapter 01 #20Difficulty: Easy21.__________ portfolio construction starts with selecting attractively priced securities.A. Bottom-upB. Top-downC. Upside-downD. Side-to-sideBodie - Chapter 01 #21Difficulty: Easy22.In a capitalist system capital resources are primarily allocated by ____________.A. governmentsB. the SECC. financial marketsD. investment bankersBodie - Chapter 01 #22Difficulty: Easy23. A __________ represents an ownership share in a corporation.A. call optionmon stockC. fixed-income securityD. preferred stockBodie - Chapter 01 #23Difficulty: Easy24.The value of a derivative security _________.A.depends on the value of other related securityB. affects the value of a related securityC. is unrelated to the value of a related securityD. can only be integrated by calculus professorsBodie - Chapter 01 #24Difficulty: Easy 25. A bond issue is broken up so that some investors will receive interest payments while others willreceive principal payments. This is an example of _________.A. bundlingB. credit enhancementC. securitizationD.unbundlingBodie - Chapter 01 #25Difficulty: Easy 26.__________ portfolio management calls for holding diversified portfolios without spending effort orresources attempting to improve investment performance through security analysis.A. ActiveB. MomentumC.PassiveD. Market timingBodie - Chapter 01 #26Difficulty: Easy27.Financial markets allow for all but which one of the following?A. Shift consumption through time from higher income periods to lowerB. Price securities according to their riskinessC. Channel funds from lenders of funds to borrowers of fundsD. Allow most participants to routinely earn high returns with low riskBodie - Chapter 01 #27Difficulty: Moderate28.Financial intermediaries exist because small investors cannot efficiently _________.A. diversify their portfoliosB. gather informationC. monitor their portfoliosD. all of the answers provide reasons whyBodie - Chapter 01 #28Difficulty: Easy29.Methods to encourage managers to act in shareholders' best interest includeI. Threat of takeoverII. Proxy fights for control of the Board of DirectorsIII. Tying managers' compensation to stock price performanceA. I onlyB. I and II onlyC. II and III onlyD. I, II and IIIBodie - Chapter 01 #29Difficulty: Easy 30.Firms that specialize in helping companies raise capital by selling securities to the public are called_________.A. pension fundsB.investment banksC. savings banksD. REITsBodie - Chapter 01 #30Difficulty: Easy 31.In securities markets, there should be a risk-return trade-off with higher-risk assets having _________expected returns than lower-risk assets.A. higherB. lowerC. the sameD. Can't tell from the information givenBodie - Chapter 01 #31Difficulty: Easy32.__________ are an indirect way U.S. investors can invest in foreign companies.A. ADRsB. IRAsC. SDRsD. CPCsBodie - Chapter 01 #32Difficulty: Easy33.Security selection refers to _________.A. choosing specific securities within each asset-classB. deciding how much to invest in each asset-classC. deciding how much to invest in the market portfolio versus the riskless assetD. deciding how much to hedgeBodie - Chapter 01 #33Difficulty: Easy34.An example of a derivative security is _________.A. a common share of General MotorsB. a call option on Intel stockC. a Ford bondD. a U.S. Treasury bondBodie - Chapter 01 #34Difficulty: Easy35.__________ portfolio construction starts with asset allocation.A. Bottom-upB. Top-downC. Upside-downD. Side-to-sideBodie - Chapter 01 #35Difficulty: Easy 36.Which one of the following firms falsely claimed to have a $4.8 billion bank account at Bank ofAmerica and vastly understated its debts, eventually resulting in the firm's bankruptcy?A. WorldComB. EnronC. ParmalatD. Global CrossingBodie - Chapter 01 #36Difficulty: Medium37.Debt securities promise _________.I. a fixed stream of incomeII. a stream of income that is determined according to a specific formulaIII. a share in the profits of the issuing entityA. I onlyB.I or II onlyC. I and III onlyD. II or III onlyBodie - Chapter 01 #37Difficulty: Medium 38.The Sarbanes-Oxley Act tightened corporate governance rules by requiring all but which one of thefollowing?A. Required corporations to have more independent directorsB. Required the CFO to personally vouch for the corporation's financial statementsC. Required that firms could no longer employ investment bankers to sell securities to the publicD. The creation of a new board to oversee the auditing of public companiesBodie - Chapter 01 #38Difficulty: Medium39.The success of common stock investments depends on the success of _________.A. derivative securitiesB. fixed income securitiesC. the firm and its real assetsD. government methods of allocating capitalBodie - Chapter 01 #39Difficulty: Easy40.The historical average rate of return on the large company stocks since 1926 has beenA. 5%B. 8%C.12%D. 20%Bodie - Chapter 01 #40Difficulty: Medium41.The average rate of return on U.S. Treasury bills since 1926 was _________.A. 0.5%B. 2.4%C. 3.8%D. 6.0%Bodie - Chapter 01 #41Difficulty: Medium42.An example of a real asset is _________.I. a college educationII. customer goodwillIII. a patentA. I onlyB. II onlyC. I and III onlyD. I, II and IIIBodie - Chapter 01 #42Difficulty: Medium43.The 2002 law designed to improve corporate governance is titled theA. Pension Reform ActB. ERISAC. Financial Services Modernization ActD. Sarbanes-Oxley ActBodie - Chapter 01 #43Difficulty: Easy44.Which of the following is not a financial intermediary?A. a mutual fundB. an insurance companyC. a real estate brokerage firmD. a savings and loan companyBodie - Chapter 01 #44Difficulty: Medium 45.The combined liabilities of American households represent approximately __________ percent ofcombined assets.A. 11%B.21%C. 25%D. 33%Bodie - Chapter 01 #45Difficulty: Medium 46.In 2008 real assets represented approximately __________ percent of the total asset holdings ofAmerican households.A. 37%B. 42%C. 48%D. 55%Bodie - Chapter 01 #46Difficulty: Medium。

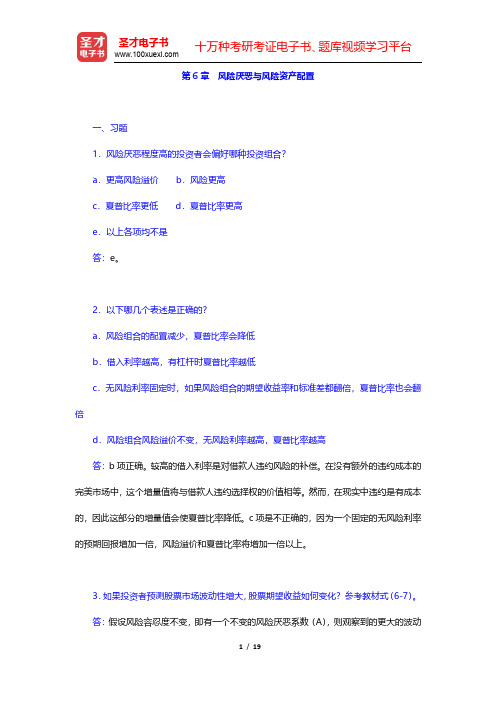

博迪《投资学》(第9版)课后习题-风险厌恶与风险资产配置(圣才出品)

第6章风险厌恶与风险资产配置一、习题1.风险厌恶程度高的投资者会偏好哪种投资组合?a.更高风险溢价b.风险更高c.夏普比率更低d.夏普比率更高e.以上各项均不是答:e。

2.以下哪几个表述是正确的?a.风险组合的配置减少,夏普比率会降低b.借入利率越高,有杠杆时夏普比率越低c.无风险利率固定时,如果风险组合的期望收益率和标准差都翻倍,夏普比率也会翻倍d.风险组合风险溢价不变,无风险利率越高,夏普比率越高答:b项正确。

较高的借入利率是对借款人违约风险的补偿。

在没有额外的违约成本的完美市场中,这个增量值将与借款人违约选择权的价值相等。

然而,在现实中违约是有成本的,因此这部分的增量值会使夏普比率降低。

c项是不正确的,因为一个固定的无风险利率的预期回报增加一倍,风险溢价和夏普比率将增加一倍以上。

3.如果投资者预测股票市场波动性增大,股票期望收益如何变化?参考教材式(6-7)。

答:假设风险容忍度不变,即有一个不变的风险厌恶系数(A),则观察到的更大的波动会增加风险投资组合的最优投资方程(教材式6-7)的分母。

因此,投资于风险投资组合的比例将会下降。

4.考虑一个风险组合,年末现金流为70000美元或200000美元,两者概率相等。

短期国债利率为6%。

a.如果追求风险溢价为8%,你愿意投资多少钱?b.期望收益率是多少?c.追求风险溢价为12%呢?d.比较a和c的答案,关于投资所要求的风险溢价与售价之间的关系,投资者有什么结论?答:a.预期现金流入为(0.5×70000)+(0.5×200000)=135000(美元)。

风险溢价为8%,无风险利率为6%,则必要回报率为14%。

因此资产组合的现值为:135000/1.14=118421(美元)。

b.如果资产组合以118421美元买入,给定预期的收入为135000美元,则期望收益率E(r)满足:118421×[1+E(r)]=135000(美元)。

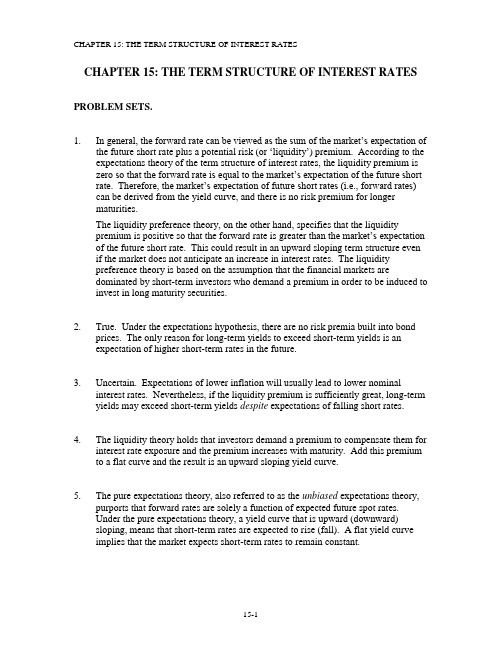

博迪投资学第九版 Investment Chap015 习题答案

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.1. In general, the forward rate can be viewed as the sum of the market‟s expectation ofthe future short rate plus a potential risk (or …liquidity‟) premium. According to the expectations theory of the term structure of interest rates, the liquidity premium is zero so that the forward rate is equal to the market‟s expectation of the future short rate. Therefore, the market‟s expectation of future short rates (i.e., forward rates) can be derived from the yield curve, and there is no risk premium for longermaturities.The liquidity preference theory, on the other hand, specifies that the liquiditypremium is positive so that the forward rate is greater than the market‟s expectation of the future short rate. This could result in an upward sloping term structure even if the market does not anticipate an increase in interest rates. The liquiditypreference theory is based on the assumption that the financial markets aredominated by short-term investors who demand a premium in order to be induced to invest in long maturity securities.2. True. Under the expectations hypothesis, there are no risk premia built into bondprices. The only reason for long-term yields to exceed short-term yields is anexpectation of higher short-term rates in the future.3. Uncertain. Expectations of lower inflation will usually lead to lower nominalinterest rates. Nevertheless, if the liquidity premium is sufficiently great, long-term yields may exceed short-term yields despite expectations of falling short rates.4. The liquidity theory holds that investors demand a premium to compensate them forinterest rate exposure and the premium increases with maturity. Add this premium to a flat curve and the result is an upward sloping yield curve.5. The pure expectations theory, also referred to as the unbiased expectations theory,purports that forward rates are solely a function of expected future spot rates.Under the pure expectations theory, a yield curve that is upward (downward)sloping, means that short-term rates are expected to rise (fall). A flat yield curveimplies that the market expects short-term rates to remain constant.6. The yield curve slopes upward because short-term rates are lower than long-term rates. Since market rates are determined by supply and demand, it follows thatinvestors (demand side) expect rates to be higher in the future than in the near-term. 7. Maturity Price YTM Forward Rate1 $943.40 6.00%2 $898.47 5.50% (1.0552/1.06) – 1 = 5.0% 3 $847.62 5.67% (1.05673/1.0552) – 1 = 6.0% 4$792.166.00%(1.064/1.05673) – 1 = 7.0%8.The expected price path of the 4-year zero coupon bond is shown below. (Note that we discount the face value by the appropriate sequence of forward rates implied by this year‟s yield curve.) Beginning of YearExpected PriceExpected Rate of Return 1 $792.16($839.69/$792.16) – 1 = 6.00% 2 69.839$07.106.105.1000,1$=⨯⨯($881.68/$839.69) – 1 = 5.00% 3 68.881$07.106.1000,1$=⨯($934.58/$881.68) – 1 = 6.00%458.934$07.1000,1$= ($1,000.00/$934.58) – 1 = 7.00% 9.If expectations theory holds, then the forward rate equals the short rate, and the one year interest rate three years from now would be43(1.07)1.08518.51%(1.065)-==10. a.A 3-year zero coupon bond with face value $100 will sell today at a yield of 6% and a price of:$100/1.063 =$83.96Next year, the bond will have a two-year maturity, and therefore a yield of 6% (from next year‟s forecasted yield curve). The price will be $89.00, resulting in a holding period return of 6%.b. The forward rates based on today‟s yield curve are as follows: Year Forward Rate2 (1.052/1.04) – 1 = 6.01% 3(1.063/1.052) – 1 = 8.03%Using the forward rates, the forecast for the yield curve next year is: Maturity YTM 1 6.01% 2 (1.0601 × 1.0803)1/2 – 1 = 7.02%The market forecast is for a higher YTM on 2–year bonds than your forecast. Thus, the market predicts a lower price and higher rate of return.11. a. 86.101$08.1109$07.19$P 2=+=b.The yield to maturity is the solution for y in the following equation:86.101$)y 1(109$y 19$2=+++ [Using a financial calculator, enter n = 2; FV = 100; PMT = 9; PV = –101.86; Compute i] YTM = 7.958%c.The forward rate for next year, derived from the zero-coupon yield curve, is the solution for f 2 in the following equation:0901.107.1)08.1(f 122==+ ⇒ f 2 = 0.0901 = 9.01%.Therefore, using an expected rate for next year of r 2 = 9.01%, we find that the forecast bond price is:99.99$0901.1109$P ==d.If the liquidity premium is 1% then the forecast interest rate is:E(r 2) = f 2 – liquidity premium = 9.01% – 1.00% = 8.01% The forecast of the bond price is:92.100$0801.1109$=12. a.The current bond price is:($85 × 0.94340) + ($85 × 0.87352) + ($1,085 × 0.81637) = $1,040.20 This price implies a yield to maturity of 6.97%, as shown by the following: [$85 × Annuity factor (6.97%, 3)] + [$1,000 × PV factor (6.97%, 3)] = $1,040.17b.If one year from now y = 8%, then the bond price will be:[$85 × Annuity factor (8%, 2)] + [$1,000 × PV factor (8%, 2)] = $1,008.92 The holding period rate of return is:[$85 + ($1,008.92 – $1,040.20)]/$1,040.20 = 0.0516 = 5.16%13. Year Forward Rate PV of $1 received at period end 1 5% $1/1.05 = $0.95242 7% $1/(1.05⨯1.07) = $0.890138%$1/(1.05⨯1.07⨯1.08) = $0.8241a. Price = ($60 × 0.9524) + ($60 × 0.8901) + ($1,060 × 0.8241) = $984.14b.To find the yield to maturity, solve for y in the following equation: $984.10 = [$60 × Annuity factor (y, 3)] + [$1,000 × PV factor (y, 3)] This can be solved using a financial calculator to show that y = 6.60%c.Period Payment received at end of period:Will grow by a factor of: To a future value of: 1 $60.00 1.07 ⨯ 1.08 $69.34 2 $60.00 1.08 $64.80 3 $1,060.00 1.00 $1,060.00$1,194.14$984.10 ⨯ (1 + y realized )3 = $1,194.141 + y realized = 0666.110.984$14.194,1$3/1=⎪⎭⎫⎝⎛ ⇒ y realized = 6.66%d.Next year, the price of the bond will be:[$60 × Annuity factor (7%, 2)] + [$1,000 × PV factor (7%, 2)] = $981.92 Therefore, there will be a capital loss equal to: $984.10 – $981.92 = $2.18 The holding period return is:%88.50588.010.984$)18.2$(60$==-+14. a.The return on the one-year zero-coupon bond will be 6.1%. The price of the 4-year zero today is:$1,000/1.0644 = $780.25Next year, i f the yield curve is unchanged, today‟s 4-year zero coupon bond will have a 3-year maturity, a YTM of 6.3%, and therefore the price will be:$1,000/1.0633 = $832.53The resulting one-year rate of return will be: 6.70%Therefore, in this case, the longer-term bond is expected to provide the higher return because its YTM is expected to decline during the holding period. b.If you believe in the expectations hypothesis, you would not expect that the yield curve next year will be the same as today‟s curve. The u pward slope in today's curve would be evidence that expected short rates are rising and that the yield curve will shift upward, reducing the holding period return on the four-year bond. Under the expectations hypothesis, all bonds have equal expected holding period returns. Therefore, you would predict that the HPR for the 4-year bond would be 6.1%, the same as for the 1-year bond.15. The price of the coupon bond, based on its yield to maturity, is:[$120 × Annuity factor (5.8%, 2)] + [$1,000 × PV factor (5.8%, 2)] = $1,113.99 If the coupons were stripped and sold separately as zeros, then, based on the yield to maturity of zeros with maturities of one and two years, respectively, the coupon payments could be sold separately for:08.111,1$06.1120,1$05.1120$2=+ The arbitrage strategy is to buy zeros with face values of $120 and $1,120, and respective maturities of one year and two years, and simultaneously sell the coupon bond. The profit equals $2.91 on each bond.16. a.The one-year zero-coupon bond has a yield to maturity of 6%, as shown below:1y 1100$34.94$+=⇒y 1 = 0.06000 = 6.000% The yield on the two-year zero is 8.472%, as shown below:22)y 1(100$99.84$+=⇒y 2 = 0.08472 = 8.472% The price of the coupon bond is:51.106$)08472.1(112$06.112$2=+Therefore: yield to maturity for the coupon bond = 8.333%[On a financial calculator, enter: n = 2; PV = –106.51; FV = 100; PMT = 12]b. %00.111100.0106.1)08472.1(1y 1)y 1(f 21222==-=-++=c.Expected price 90.100$11.1112$==(Note that next year, the coupon bond will have one payment left.) Expected holding period return =%00.60600.051.106$)51.106$90.100($12$==-+This holding period return is the same as the return on the one-year zero.d.If there is a liquidity premium, then: E(r 2) < f 2 E(Price) =90.100$)r (E 1112$2>+E(HPR) > 6%17. a.We obtain forward rates from the following table: Maturity YTM Forward Rate Price (for parts c, d) 1 year 10%$1,000/1.10 = $909.09 2 years 11% (1.112/1.10) – 1 = 12.01% $1,000/1.112 = $811.62 3 years 12% (1.123/1.112) – 1 = 14.03%$1,000/1.123 = $711.78b.We obtain next year‟s prices and yields by discounting each zero‟s face value at the forward rates for next year that we derived in part (a): Maturity PriceYTM1 year $1,000/1.1201 = $892.78 12.01%2 years$1,000/(1.1201 × 1.1403) = $782.9313.02%Note that this year‟s upward sloping yield curve implies, according t o the expectations hypothesis, a shift upward in next year‟s curve.c.Next year, the 2-year zero will be a 1-year zero, and will therefore sell at a price of: $1,000/1.1201 = $892.78Similarly, the current 3-year zero will be a 2-year zero and will sell for: $782.93 Expected total rate of return:2-year bond: %00.1011000.1162.811$78.892$=-=-3-year bond:%00.1011000.1178.711$93.782$=-=-d.The current price of the bond should equal the value of each payment times the present value of $1 to be received at the “maturity” of th at payment. The present value schedule can be taken directly from the prices of zero-coupon bonds calculated above.Current price = ($120 × 0.90909) + ($120 × 0.81162) + ($1,120 × 0.71178)= $109.0908 + $97.3944 + $797.1936 = $1,003.68Similarly, the expected prices of zeros one year from now can be used to calculate the expected bond value at that time:Expected price 1 year from now = ($120 × 0.89278) + ($1,120 × 0.78293)= $107.1336 + $876.8816 = $984.02Total expected rate of return =%00.101000.068.003,1$)68.003,1$02.984($120$==-+18. a.Maturity (years) Price YTM Forward rate 1 $925.93 8.00% 2 $853.39 8.25% 8.50% 3 $782.92 8.50% 9.00% 4 $715.00 8.75% 9.50% 5$650.009.00%10.00%b.For each 3-year zero issued today, use the proceeds to buy:$782.92/$715.00 = 1.095 four-year zerosYour cash flows are thus as follows:Time Cash Flow0 $ 03 -$1,000 The 3-year zero issued at time 0 matures;the issuer pays out $1,000 face value4 +$1,095 The 4-year zeros purchased at time 0 mature;receive face valueThis is a synthetic one-year loan originating at time 3. The rate on thesynthetic loan is 0.095 = 9.5%, precisely the forward rate for year 4.c. For each 4-year zero issued today, use the proceeds to buy:$715.00/$650.00 = 1.100 five-year zerosYour cash flows are thus as follows:Time Cash Flow0 $ 04 -$1,000 The 4-year zero issued at time 0 matures;the issuer pays out $1,000 face value5 +$1,100 The 5-year zeros purchased at time 0 mature;receive face valueThis is a synthetic one-year loan originating at time 4. The rate on thesynthetic loan is 0.100 = 10.0%, precisely the forward rate for year 5.19. a. For each three-year zero you buy today, issue:$782.92/$650.00 = 1.2045 five-year zerosThe time-0 cash flow equals zero.b. Your cash flows are thus as follows:Time Cash Flow0 $ 03 +$1,000.00 The 3-year zero purchased at time 0 matures;receive $1,000 face value5 -$1,204.50 The 5-year zeros issued at time 0 mature;issuer pays face valueThis is a synthetic two-year loan originating at time 3.c.The effective two-year interest rate on the forward loan is:$1,204.50/$1,000 1 = 0.2045 = 20.45%d.The one-year forward rates for years 4 and 5 are 9.5% and 10%, respectively. Notice that:1.095 × 1.10 = 1.2045 =1 + (two-year forward rate on the 3-year ahead forward loan)The 5-year YTM is 9.0%. The 3-year YTM is 8.5%. Therefore, another way to derive the 2-year forward rate for a loan starting at time 3 is:%46.202046.01085.109.11)y 1()y 1()2(f 3533553==-=-++= [Note: slight discrepancies here from rounding errors in YTM calculations]CFA PROBLEMS1. Expectations hypothesis: The yields on long-term bonds are geometric averages ofpresent and expected future short rates. An upward sloping curve is explained by expected future short rates being higher than the current short rate. A downward-sloping yield curve implies expected future short rates are lower than the current short rate. Thus bonds of different maturities have different yields if expectations of future short rates are different from the current short rate.Liquidity preference hypothesis: Yields on long-term bonds are greater than the expected return from rolling-over short-term bonds in order to compensate investors in long-term bonds for bearing interest rate risk. Thus bonds of different maturities can have different yields even if expected future short rates are all equal to the current short rate. An upward sloping yield curve can be consistent even with expectations of falling short rates if liquidity premiums are high enough. If,however, the yield curve is downward sloping and liquidity premiums are assumed to be positive, then we can conclude that future short rates are expected to be lower than the current short rate. 2. d. 3.a.(1+y 4 )4 = (1+ y 3 )3 (1 + f 4 ) (1.055)4 = (1.05)3 (1 + f 4 )1.2388 = 1.1576 (1 + f 4 ) ⇒ f 4 = 0.0701 = 7.01%b.The conditions would be those that underlie the expectations theory of the term structure: risk neutral market participants who are willing to substitute among maturities solely on the basis of yield differentials. This behavior would rule out liquidity or term premia relating to risk.c.Under the expectations hypothesis, lower implied forward rates wouldindicate lower expected future spot rates for the corresponding period. Since the lower expected future rates embodied in the term structure are nominal rates, either lower expected future real rates or lower expected future inflation rates would be consistent with the specified change in the observed (implied) forward rate.4.The given rates are annual rates, but each period is a half-year. Therefore, the per period spot rates are 2.5% on one-year bonds and 2% on six-month bonds. The semiannual forward rate is obtained by solving for f in the following equation:030.102.1025.1f 12==+This means that the forward rate is 0.030 = 3.0% semiannually, or 6.0% annually. 5.The present value of each bond‟s payments can be derived by discounting each cash flow by the appropriate rate from the spot interest rate (i.e., the pure yield) curve:Bond A: 53.98$11.1110$08.110$05.110$PV 32=++= Bond B:36.88$11.1106$08.16$05.16$PV 32=++=Bond A sells for $0.13 (i.e., 0.13% of par value) less than the present value of itsstripped payments. Bond B sells for $0.02 less than the present value of its stripped payments. Bond A is more attractively priced. 6. a.Based on the pure expectations theory, VanHusen‟s conclusion is incorrect. According to this theory, the expected return over any time horizon would be the same, regardless of the maturity strategy employed.b. According to the liquidity preference theory, the shape of the yield curveimplies that short-term interest rates are expected to rise in the future. Thistheory asserts that forward rates reflect expectations about future interest ratesplus a liquidity premium that increases with maturity. Given the shape of theyield curve and the liquidity premium data provided, the yield curve would stillbe positively sloped (at least through maturity of eight years) after subtractingthe respective liquidity premiums:2.90% – 0.55% = 2.35%3.50% – 0.55% = 2.95%3.80% – 0.65% = 3.15%4.00% – 0.75% = 3.25%4.15% – 0.90% = 3.25%4.30% – 1.10% = 3.20%4.45% – 1.20% = 3.25%4.60% – 1.50% = 3.10%4.70% – 1.60% = 3.10%7. The coupon bonds can be viewed as portfolios of stripped zeros: each coupon canstand alone as an independent zero-coupon bond. Therefore, yields on couponbonds reflect yields on payments with dates corresponding to each coupon. When the yield curve is upward sloping, coupon bonds have lower yields than zeroswith the same maturity because the yields to maturity on coupon bonds reflect the yields on the earlier interim coupon payments.8. The following table shows the expected short-term interest rate based on theprojections of Federal Reserve rate cuts, the term premium (which increases at arate of 0.10% per 12 months), the forward rate (which is the sum of the expectedrate and term premium), and the YTM, which is the geometric average of theforward rates.Time Expectedshort rateTermpremiumForwardrate (annual)Forward rate(semi-annual)YTM(semi-annual)0 5.00% 0.00% 5.00% 2.500% 2.500% 6 months 4.50 0.05 4.55 2.275 2.387 12 months 4.00 0.10 4.10 2.050 2.275 18 months 4.00 0.15 4.15 2.075 2.225 24 months 4.00 0.20 4.20 2.100 2.200 30 months 5.00 0.25 5.25 2.625 2.271 36 months 5.00 0.30 5.30 2.650 2.334 This analysis is predicated on the liquidity preference theory of the term structure, which asserts that the forward rate in any period is the sum of the expected short rate plus the liquidity premium.9. a. Five-year Spot Rate:5544332211)y 1(070,1$)y 1(70$)y 1(70$)y 1(70$)y 1(70$000,1$+++++++++= 55432)y 1(070,1$)0716.1(70$)0605.1(70$)0521.1(70$)05.1(70$000,1$+++++= 55)y 1(070,1$08.53$69.58$24.63$67.66$000,1$+++++= 55)y 1(070,1$32.758$+= 32.758$070,1$)y 1(55=+⇒%13.71411.1y 55=-= Five-year Forward Rate:%01.710701.11)0716.1()0713.1(45=-=-b. The yield to maturity is the single discount rate that equates the present valueof a series of cash flows to a current price. It is the internal rate of return. The short rate for a given interval is the interest rate for that interval available at different points in time.The spot rate for a given period is the yield to maturity on a zero-coupon bond that matures at the end of the period. A spot rate is the discount rate for each period. Spot rates are used to discount each cash flow of a coupon bond in order to calculate a current price. Spot rates are the rates appropriate fordiscounting future cash flows of different maturities.A forward rate is the implicit rate that links any two spot rates. Forward rates are directly related to spot rates, and therefore to yield to maturity. Some would argue (as in the expectations hypothesis) that forward rates are the market expectations of future interest rates. A forward rate represents abreak-even rate that links two spot rates. It is important to note that forward rates link spot rates, not yields to maturity.Yield to maturity is not unique for any particular maturity. In other words, two bonds with the same maturity but different coupon rates may havedifferent yields to maturity. In contrast, spot rates and forward rates for each date are unique.c.The 4-year spot rate is 7.16%. Therefore, 7.16% is the theoretical yield to maturity for the zero-coupon U.S. Treasury note. The price of the zero-coupon note discounted at 7.16% is the present value of $1,000 to be received in 4 years. Using annual compounding: 35.758$)0716.1(000,1$PV 4==10. a.The two-year implied annually compounded forward rate for a deferred loan beginning in 3 years is calculated as follows: %07.60607.0111.109.11)y 1()y 1()2(f 2/1352/133553==-⎥⎦⎤⎢⎣⎡=-⎥⎦⎤⎢⎣⎡++=b. Assuming a par value of $1,000, the bond price is calculated as follows: 10.987$)09.1(090,1$)10.1(90$)11.1(90$)12.1(90$)13.1(90$)y 1(090,1$)y 1(90$)y 1(90$)y 1(90$)y 1(90$P 543215544332211=++++=+++++++++=。

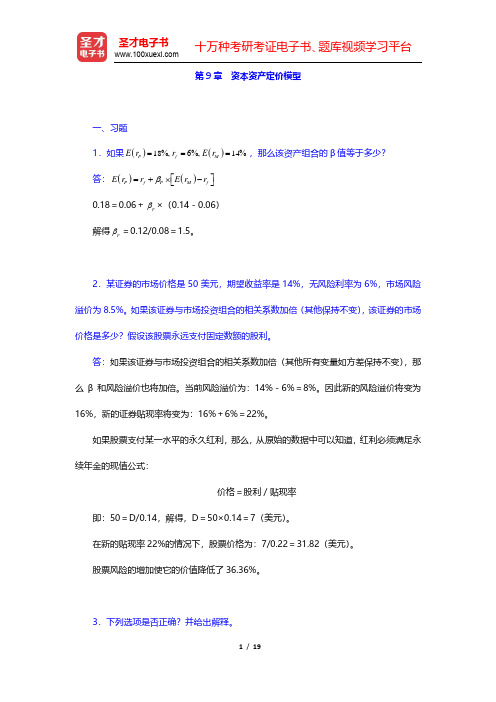

博迪《投资学》(第9版)课后习题-资本资产定价模型(圣才出品)

第9章 资本资产定价模型一、习题1.如果()()1814P f M E r r E r =%, =6%, =%,那么该资产组合的β值等于多少?答:()()P f P M f E r r E r r β⎡⎤=+⨯−⎣⎦0.18=0.06+p β×(0.14-0.06)解得p β=0.12/0.08=1.5。

2.某证券的市场价格是50美元,期望收益率是14%,无风险利率为6%,市场风险溢价为8.5%。

如果该证券与市场投资组合的相关系数加倍(其他保持不变),该证券的市场价格是多少?假设该股票永远支付固定数额的股利。

答:如果该证券与市场投资组合的相关系数加倍(其他所有变量如方差保持不变),那么β和风险溢价也将加倍。

当前风险溢价为:14%-6%=8%。

因此新的风险溢价将变为16%,新的证券贴现率将变为:16%+6%=22%。

如果股票支付某一水平的永久红利,那么,从原始的数据中可以知道,红利必须满足永续年金的现值公式:价格=股利/贴现率即:50=D/0.14,解得,D =50×0.14=7(美元)。

在新的贴现率22%的情况下,股票价格为:7/0.22=31.82(美元)。

股票风险的增加使它的价值降低了36.36%。

3.下列选项是否正确?并给出解释。

a .β为零的股票提供的期望收益率为零。

b .资本资产定价模型认为投资者对持有高波动性证券要求更高的收益率。

c .你可以通过将75%的资金投资于短期国债,其余的资金投资于市场投资组合的方式来构建一个β为0.75的资产组合。

答:a .错误。

β=0意味着E (r )=r f ,不等于零。

b .错误。

只有承担了较高的系统风险(不可分散的风险或市场风险),投资者才要求较高期望收益;如果高风险债券的β较小,即使总风险较大,投资者要求的收益率也不会太高。

c .错误。

投资组合应当是75%的市场组合和25%的短期国债,此时β为:()()0.7510.2500.75p β=⨯+⨯=4.下表给出两个公司的数据。

博迪《投资学》(第9版)课后习题-宏观经济分析与行业分析(圣才出品)

第17章宏观经济分析与行业分析一、习题1.经济急剧衰退时,应该采取什么样的货币政策和财政政策?答:降低利率的扩张性(放松)货币政策将有助于刺激投资和对耐用消费品的支出。

扩张性财政政策(即降低税收,增加政府支出和福利转移支付)将直接刺激总需求。

2.如果你比其他投资者更相信美元会大幅贬值,那么你对美国汽车产业有何投资建议?答:美元的急剧贬值会使进口汽车变得更昂贵,美国的汽车对外国的消费者则变得更便宜了。

这将使得美国的汽车行业获益。

3.选择一个行业,列举决定其未来3年业绩的因素并预期其未来业绩。

答:答案不惟一。

4.证券评估“自下而上”和“自上而下”方法的差异是什么?“自上而下”方法的优势在哪里?答:证券评估“自上而下”的方法开始于全球和国内的经济分析。

在给定宏观经济的预期表现的情况下,遵循“自上而下”方法的分析家将会试图寻找一个可能表现良好的行业或部门。

最后,分析会集中于行业或部门内可能表现良好的特定企业。

“自下向上”的方法通常强调个别公司股票的基本面分析,它主要是基于这样一种信念,即无论行业或宏观经济的前景好坏,被低估的股票都将表现良好。

“自上而下”方法的主要优势是它提供了一种在每一水平下,将经济和金融变量的影响纳入到公司股票分析中的结构性方法。

特定行业的前景高度依赖于宏观经济变量。

同样,个别公司的股票表现可能受该公司经营的行业前景的影响很大。

5.公司的哪些特征会使其对经济周期更敏感?答:对经济周期有较大敏感性的公司一般属于生产耐用消费品或资本货物的行业。

耐用品(如汽车,大家电)的消费者更倾向于在经济扩张时购买这些东西,而在经济衰退时往往会推迟购买。

公司的资本货物(如购买生产产品的设备)的购买在经济衰退时会降低,因为在经济衰退时对公司最终产品的需求会下降。

6.与其他投资者不同,你认为美联储将实施宽松的货币政策。

那么你对下列行业有何投资建议?a.金矿开采b.建筑业答:a.金矿开采:传统上认为黄金可以对冲通胀风险。

博迪投资学第九版-Investment-Chap013-习题答案

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS PROBLEM SETS1. Even if the single-factor CCAPM (with a consumption-trackingportfolio used as the index) performs better than the CAPM, it is still quite possible that the consumption portfolio does notcapture the size and growth characteristics captured by the SMB(i.e., small minus big capitalization) and HML (i.e., high minuslow book-to-market ratio) factors of the Fama-French three-factor model. Therefore, it is expected that the Fama-French model with consumption provides a better explanation of returns than does the model with consumption alone.2. Wealth and consumption should be positively correlated and,therefore, market volatility and consumption volatility should also be positively correlated. Periods of high market volatility might coincide with periods of high consumption volatility. The‘conventional’ CAPM focuses on the covariance of security returns with returns for the market portfolio (which in turn tracksaggregate wealth) while the consumption-based CAPM focuses on the covariance of security returns with returns for a portfolio thattracks consumption growth. However, to the extent that wealth and consumption are correlated, both versions of the CAPM mightrepresent patterns in actual returns reasonably well.To see this formally, suppose that the CAPM and the consumption-based model are approximately true. According to the conventional CAPM, the market price of risk equals expected excess market return divided by the variance of that excess return. According to theconsumption-beta model, the price of risk equals expected excessmarket return divided by the covariance of R M with g, where g is the rate of consumption growth. This covariance equals the correlation of R M with g times the product of the standard deviations of thevariables. Combining the two models, the correlation between R M andg equals the standard deviation of R M divided by the standarddeviation of g. Accordingly, if the correlation between R M and g is relatively stable, then an increase in market volatility will beaccompanied by an increase in the volatility of consumption growth.Note: For the following problems, the focus is on the estimation procedure. To keep the exercise feasible, the sample was limited to returns on nine stocks plus a market index and a second factor over a period of 12 years. The data were generated to conform to a two-factor CAPM so that actual rates of return equal CAPMexpectations plus random noise, and the true intercept of the SCL is zero for all stocks. The exercise will provide a feel for the pitfalls of verifying social-science models. However, due to the small size of the sample, results are not always consistent withthe findings of other studies as reported in the chapter.3. Using the regression feature of Excel with the data presented inthe text, the first-pass (SCL) estimation results are:Stock:A B C D E F G H I R Square0.060.060.060.370.170.590.060.670.70ObservationBeta-0.470.590.42 1.380.90 1.780.66 1.91 2.08t-Alpha0.73-0.04-0.06-0.410.05-0.450.33-0.270.64t-Beta-0.810.780.78 2.42 1.42 3.830.78 4.51 4.814. The hypotheses for the second-pass regression for the SML are:•The intercept is zero; and,•The slope is equal to the average return on the index portfolio.5. The second-pass data from first-pass (SCL) estimates are:AverageBetaExcessReturnA 5.18-0.47B 4.190.59C 2.750.42D 6.15 1.38E8.050.90F9.90 1.78G11.320.66H13.11 1.91I22.83 2.08M8.12S The second-pass regression yields:Regression StatisticsMultiple R 0.7074R Square0.5004Adjusted RSquare0.4291Standard Error 4.6234 Observations9Coefficients StandardErrortStatisticfor β=0tStatisticforIntercept 3.92 2.54 1.54Slope 5.21 1.97 2.65-1.486. As we saw in the chapter, the intercept is too high (3.92% per yearinstead of 0) and the slope is too flat (5.21% instead of apredicted value equal to the sample-average risk premium: r M r f =8.12%). The intercept is not significantly greater than zero (thet-statistic is less than 2) and the slope is not significantlydifferent from its theoretical value (the t-statistic for thishypothesis is 1.48). This lack of statistical significance isprobably due to the small size of the sample.7. Arranging the securities in three portfolios based on betas fromthe SCL estimates, the first pass input data are:Year ABC DEG FHI115.0525.8656.692-16.76-29.74-50.85319.67-5.688.984-15.83-2.5835.41547.1837.70-3.256-2.2653.8675.447-18.6715.3212.508-6.3536.3332.1297.8514.0850.421021.4112.6652.1411-2.53-50.71-66.1212-0.30-4.99-20.10 Average 4.048.5115.28Std.Dev.19.3029.4743.96(continued on next page)The first-pass (SCL) estimates are:ABC DEG FHIR Square0.040.480.82Observation121212Alpha 2.580.54-0.34Beta0.180.98 1.92t-Alpha0.420.08-0.06t-Beta0.62 3.02 6.83Grouping into portfolios has improved the SCL estimates as is evident from the higher R-square for Portfolio DEG and Portfolio FHI. This means that the beta (slope) is measured with greater precision, reducing the error-in-measurement problem at the expense of leaving fewer observations for the second pass.The inputs for the second pass regression are:AverageExcessReturnBetaABC 4.040.18DEH8.510.98FGI15.28 1.92M8.12The second-pass estimates are:RegressionMultiple R0.9975R Square0.9949Adjusted RSquare0.9899Standard Error0.5693Observations3Coefficients StandardErrortStatisticfor β =0tStatisticfor βIntercept 2.620.58 4.55Slope 6.470.4614.03-3.58Despite the decrease in the intercept and the increase in slope, the intercept is now significantly positive, and the slope is significantly less than the hypothesized value by more than three times the standard error.8. Roll’s critique suggests that the problem b egins with the marketindex, which is not the theoretical portfolio against which thesecond pass regression should hold. Hence, even if therelationship is valid with respect to the true (unknown) index, we may not find it. As a result, the second pass relationship may be meaningless.9.Except for Stock I, which realized an extremely positive surprise, the CML shows that the index dominates all other securities, and the three portfolios dominate all individual stocks. The power of diversification is evident despite the very small sample size.10. The first-pass (SCL) regression results are summarized below:A B C D E F G H IR-Square0.070.360.110.440.240.840.120.680.71Observatio121212121212121212 nsIntercept9.19-1.89-1.00-4.480.17-3.47 5.32-2.64 5.66Beta M-0.470.580.41 1.390.89 1.790.65 1.91 2.08Beta F-0.35 2.330.67-1.05 1.03-1.95 1.150.430.48 t-Intercept0.71-0.13-0.08-0.370.01-0.520.29-0.280.59t-Beta M-0.770.870.75 2.46 1.40 5.800.75 4.35 4.65 t-Beta F-0.34 2.060.71-1.080.94-3.690.770.570.6311. The hypotheses for the second-pass regression for the two-factorSML are:•The intercept is zero;•The market-index slope coefficient equals the market-index average return; and,•The factor slope coefficient equals the average return on thefactor.(Note that the first two hypotheses are the same as those for the single factor model.)12. The inputs for the second pass regression are:AverageExcessReturnBeta M Beta FA 5.18-0.47-0.35B 4.190.58 2.33C 2.750.410.67D 6.15 1.39-1.05E8.050.89 1.03F9.90 1.79-1.95G11.320.65 1.15H13.11 1.910.43I22.83 2.080.48M8.12F0.60The second-pass regression yields:Regression StatisticsMultiple R0.7234R Square0.5233Adjusted RSquare0.3644Standard Error 4.8786Observations9Coefficients StandardErrortStatisticfor β =0tStatisticfor βtStatisticfor βIntercept 3.35 2.88 1.16Beta M 5.53 2.16 2.56-1.20Beta F0.80 1.420.560.14These results are slightly better than those for the single factor test; that is, the intercept is smaller and the slope on M is slightly greater. We cannot expect a great improvement since the factor we added does not appear to carry a large risk premium (average excess return is less than 1%), and its effect on mean returns is therefore small. The data do not reject the second factor because the slope is close to the average excess return and the difference is less than one standard error. However, with this sample size, the power of this test is extremely low.13. When we use the actual factor, we implicitly assume that investorscan perfectly replicate it, that is, they can invest in a portfolio that is perfectly correlated with the factor. When this is notpossible, one cannot expect the CAPM equation (the second passregression) to hold. Investors can use a replicating portfolio (aproxy for the factor) that maximizes the correlation with thefactor. The CAPM equation is then expected to hold with respect to the proxy portfolio.Using the bordered covariance matrix of the nine stocks and theExcel Solver we produce a proxy portfolio for factor F, denoted PF.To preserve the scale, we include constraints that require the nine weights to be in the range of [-1,1] and that the mean equal thefactor mean of 0.60%. The resultant weights for the proxy andperiod returns are:Proxy Portfolio for Factor F(PF)Weightson Universe YearPF HoldingPeriodReturnsA-0.141-33.51B 1.00262.78C0.9539.87D-0.354-153.56E0.165200.76F-1.006-36.62G0.137-74.34H0.198-10.84I0.06928.111059.5111-59.151214.22Average0.60This proxy (PF) has an R-square with the actual factor of 0.80.We next perform the first pass regressions for the two factor model using PF instead of P:A B C D E F G H I R-square0.080.550.200.430.330.880.160.710.72 Observations121212121212121212Intercept9.28-2.53-1.35-4.45-0.23-3.20 4.99-2.92 5.54 Beta M-0.500.800.49 1.32 1.00 1.640.76 1.97 2.12 Beta PF-0.060.420.16-0.130.21-0.290.210.110.08 t- 0.72-0.21-0.12-0.36-0.02-0.550.27-0.330.58 t-Beta M-0.83 1.430.94 2.29 1.66 6.000.90 4.67 4.77t-Beta PF-0.44 3.16 1.25-0.97 1.47-4.52 1.03 1.130.78Note that the betas of the nine stocks on M and the proxy (PF) are different from those in the first pass when we use the actual proxy.The first-pass regression for the two-factor model with the proxy yields:AverageExcessReturnBeta M Beta PFA 5.18-0.50-0.06B 4.190.800.42C 2.750.490.16D 6.15 1.32-0.13E8.05 1.000.21F9.90 1.64-0.29G11.320.760.21H13.11 1.970.11I22.83 2.120.08M8.12PF0.6The second-pass regression yields:Regression StatisticsMultiple R0.71R Square0.51Adjusted RSquare0.35Standard Error 4.95Observations9Coefficien ts StandardErrortStatisticfor β =0tStatisticfor βtStatisticfor βIntercept 3.50 2.99 1.17Beta M 5.39 2.18 2.48-1.25Beta PF0.268.360.03-0.04We can see that the results are similar to, but slightly inferior to, those with the actual factor, since the intercept is larger and the slope coefficient smaller. Note also that we use here an in-sample test rather than tests with future returns, which is more forgiving than an out-of-sample test.14. We assume that the value of your labor is incorporated in thecalculation of the rate of return for your business. It wouldlikely make sense to commission a valuation of your business atleast once each year. The resultant sequence of figures forpercentage change in the value of the business (including net cash withdrawals from the business in the calculations) will allow you to derive a reasonable estimate of the correlation between the rate of return for your business and returns for other assets. Youwould then search for industries having the lowest correlationswith your portfolio, and identify exchange traded funds (ETFs) for these industries. Your asset allocation would then be comprised of your business, a market portfolio ETF, and the low-correlation(hedge) industry ETFs. Assess the standard deviation of such aportfolio with reasonable proportions of the portfolio invested in the market and in the hedge industries. Now determine where youwant to be on the resultant CAL. If you wish to hold a less risky overall portfolio and to mix it with the risk-free asset, reducethe portfolio weights for the market and for the hedge industries in an efficient way.CFA PROBLEMS1. (i) Betas are estimated with respect to market indexes that areproxies for the true market portfolio, which is inherentlyunobservable.(ii) Empirical tests of the CAPM show that average returns are not related to beta in the manner predicted by the theory. Theempirical SML is flatter than the theoretical one.(iii) Multi-factor models of security returns show that beta, which is a one-dimensional measure of risk, may not capture the true risk of the stock of portfolio.2. a. The basic procedure in portfolio evaluation is to compare thereturns on a managed portfolio to the return expected on anunmanaged portfolio having the same risk, using the SML. Thatis, expected return is calculated from:E(r P ) = r f + βP [E(r M ) – r f ]where r f is the risk-free rate, E(r M ) is the expected return for the unmanaged portfolio (or the market portfolio), and βP is the beta coefficient (or systematic risk) of the managed portfolio. The performance benchmark then is the unmanaged portfolio. The typical proxy for this unmanaged portfolio is an aggregate stock market index such as the S&P 500.b. The benchmark error might occur when the unmanaged portfolioused in the evaluation process is not “optimized.” That is, market indices, such as the S&P 500, chosen as benchmarks are not on the manager’s ex ante mean/variance efficient frontier.c. Your graph should show an efficient frontier obtained fromactual returns, and a different one that represents (unobserved) ex-ante expectations. The CML and SML generated from actualreturns do not conform to the CAPM predictions, while thehypothesized lines do conform to the CAPM.d. The answer to this question depends on one’s prior beliefs.Given a consistent track record, an agnostic observer mightconclude that the data support the claim of superiority. Otherobservers might start with a strong prior that, since so manymanagers are attempting to beat a passive portfolio, a smallnumber are bound to produce seemingly convincing track records.e. The question is really whether the CAPM is at all testable.The problem is that even a slight inefficiency in the benchmarkportfolio may completely invalidate any test of the expectedreturn-beta relationship. It appears from Roll’s argumentthat the best guide to the question of the validity of the CAPMis the difficulty of beating a passive strategy.3. The effect of an incorrectly specified market proxy is that thebeta of Black’s portfolio is likely to be underestimated (i.e., too low) rel ative to the beta calculated based on the “true”market portfolio. This is because the Dow Jones Industrial Average (DJIA) and other market proxies are likely to have lessdiversification and therefore a higher variance of returns than the “true” market p ortfolio as specified by the capital asset pricing model. Consequently, beta computed using an overstated variance will be underestimated. This result is clear from the following formula:2Proxy Mark et Proxy Mark et Portfolio Portfolio )r ,r (Cov σ=βAn incorrectly specified market proxy is likely to produce a slope for the security market line (i.e., the market risk premium) that is underestimated relative to the “true” market portfolio. This results from the fact that the “true” market portfolio is likely to be more efficient (plotting on a higher return point for thesame risk) than the DJIA and similarly misspecified market proxies.Consequently, the proxy-based SML would offer less expected return per unit of risk..。

博迪《投资学》(第9版)课后习题-最优风险资产组合(圣才出品)

第7章最优风险资产组合一、习题1.以下哪些因素反映了单纯市场风险?a.短期利率上升b.公司仓库失火c.保险成本增加d.首席执行官死亡e.劳动力成本上升答:ae。

2.当增加房地产到一个股票、债券和货币的资产组合中,房地产收益的哪些因素影响组合风险?a.标准差b.期望收益c.和其他资产的相关性答:ac。

房地产被添加到组合中后,在投资组合中有四个资产类别:股票、债券、现金和房地产。

现在投资组合的方差包括房地产收益的方差项和房地产收益与其他三个资产类别之间的协方差项。

因此,房地产收益的方差(或标准差)和房地产收益与其他资产类别收益之间的相关性影响着投资组合的风险。

(注意房地产收益和现金收益之间的相关性很有可能为零。

)3.以下关于最小方差组合的陈述哪些是正确的? a .它的方差小于其他证券或组合 b .它的期望收益比无风险利率低 c .它可能是最优风险组合 d .它包含所有证券 答:a 。

4.用以下数据回答习题4~10:一个养老金经理考虑3个共同基金。

第一个是股票基金,第二个是长期政府和公司债基金,第三个是短期国债货币基金,收益率为8%。

风险组合的概率分布如表7-1所示。

表7-1基金的收益率之间的相关系数为0.1。

两种风险基金的最小方差投资组合的投资比例是多少?这种投资组合收益率的期望值与标准差各是多少?答:机会集的参数为:E (r S )=20%,E (r B )=12%,σS =30%,σB =15%,ρ=0.10。

根据标准差和相关系数,可以推出协方差矩阵(注意()ov ,S B S B C r r ρσσ=⨯⨯):债券 股票 债券 225 45 股票45900最小方差组合可由下列公式推出:w Min(S)=()()()222,225459002252452,B S BS B S BCov r rCov r rσσσ−−=+−⨯+−=0.1739w Min(B)=1-0.1739=0.8261最小方差组合的均值和标准差为:E(r Min)=(0.1739×0.20)+(0.8261×0.12)=0.1339=13.39%σMin=()122222w w2w w ov,S S B B S B S BC r rσσ/⎡⎤++⎣⎦=[(0.17392×900)+(0.82612×225)+(2×0.1739×0.8261×45)]1/2=13.92%5.制表并画出这两种风险基金的投资可行集,股票基金的投资比率从0~100%按照20%的幅度增长。

投资学第九版课后答案,博迪投资学第九版课后答案

投资学第九版课后答案,博迪投资学第九版课后答案CHAPTER1:THEINVESTMENTENVIRONMENTPROBLEMSETS1.Ultimately,itistruethatrealassetsdeterminethematerialwellbeingofaneconomy.Nevertheless,inpidualscanbenefitwhenfinancialengineeringcreatesnewproductsthatallowt hemtomanagetheirportfoliosoffinancialassetsmoreefficiently.Becausebundlingandunbundlingcreat esfinancialproductswithnewpropertiesandsensitivitiestovarioussourcesofrisk,itallowsinvestorstohe dgeparticularsourcesofriskmoreefficiently.2.Securitizationrequiresaccesstoalargenumberofpotentialinvestors.Toattracttheseinvestors,thecapitalmarketneeds:1.asafesystemofbusinesslawsandlowprobabilityofconfiscatorytaxation/regulation;2.awell-developedinvestmentbankingindustry;3.awell-developedsystemofbrokerageandfinancialtransactions,and;4.well-developedmedia,particularlyfinancialreporting.Thesecharacteristicsarefoundin(indeedmakefor)awell-developedfinancialmarket.3.Securitizationleadstodisintermediation;thatis,securitizationprovidesameansformarketparticipantstobypassintermediaries.Forexample,mortgage-backedsecuritieschannelfundstothehousingmarketwithoutrequiringthatbanksorthriftinstitutionsmakeloansfromtheirownportfolios. Assecuritizationprogresses,financialintermediariesmustincreaseotheractivitiessuchasprovidingshort-termliquiditytoconsumersandsmallbusiness,andfinancialservices.Financialassetsmakeiteasyforlargefirmstoraisethecapitalneededtofinancetheirinvestmentsinrealasse ts.IfFord,forexample,couldnotissuestocksorbondstothegeneralpublic,itwouldhaveafarmoredifficultt imeraisingcapital.Contractionofthesupplyoffinancialassetswouldmakefinancingmoredifficult,there byincreasingthecostofcapital.Ahighercostofcapitalresultsinlessinvestmentandlowerrealgrowth.4. 1-15.Evenifthefirmdoesnotneedtoissuestockinanyparticularyear,thestockmarketisstillimportanttothefinancialmanager.Thestockpriceprovidesimportantinformationabouthowthemarketvaluesthefirmsinvestmentprojects.Forexample,ifthestockpricerises considerably,managersmightconcludethatthemarketbelievesthefirmsfutureprospectsarebright.Thismightbeausefulsignaltothefirmtoproceedwithaninves tmentsuchasanexpansionofthefirmsbusiness.Inaddition,sharesthatcanbetradedinthesecondarymarke taremoreattractivetoinitialinvestorssincetheyknowthattheywillbeabletoselltheirshares.Thisinturnma kesinvestorsmorewillingtobuysharesinaprimaryoffering,andthusimprovesthetermsonwhichfirmsca nraisemoneyintheequitymarket.6.a.No.Theincreaseinpricedidnotaddtotheproductivecapacityoftheeconomy.b.Yes,thevalueoftheequit yheldintheseassetshasincreased.c.Futurehomeownersasawholeareworseoff,sincemortgageliabilitieshavealsoincreased.Inaddition,thishousingpricebubblewilleventuallyburstandsocietyasawhole(andmostlikelytaxpayers)willendurethedamage.7.a.ThebankloanisafinancialliabilityforLanni.(LannisIOUisthebanksfinancialasset.)ThecashLannirec eivesisafinancialasset.ThenewfinancialassetcreatedisLannispromissorynote(thatis,Lanni’sIOUtothebank).nnitransfersfinancialassets(cash)tothesoftwaredevelopers.Inreturn,Lannigetsarealasset,thecompletedsoftware.Nofinancialassetsarecreatedordestroyed;cashissimplytra nsferredfromonepartytoanother.nnigivestherealasset(thesoftware)toMicrosoftinexchangeforafinancialasset,1,500sharesofMicr osoftstock.IfMicrosoftissuesnewsharesinordertopayLanni,thenthiswouldrepresentthecreationofnew financialassets.nniexchangesonefinancialasset(1,500sharesofstock)foranother($120,000).Lannigivesafinancialasset($50,000cash)tothebankandgetsbackanotherfinancialasset(itsIOU).Theloanisdestroyedinthetransaction,sinceitisretiredwhenpaidoffandnolongerexists.1-28.a.LiabilitiesShareholders’equityCash$70,000Bankloan$50,000computersShareholders’equityTotal$100,000Total$100,000Ratioofrealassetstototalassets=$30,000/$100,000=0.30Assetsb.AssetsSoftwareproduct*computersTotal*ValuedatcostRatioofrealassetstototalassets=$100,000/$100,000=1.0c.AssetsMicrosoftsharescomputersTotalLiabilitiesShareholders’equity$120,000Bankloan$50,000Shareholders’equity$150,000Total$150,000LiabilitiesShareholders’equity$70,000Bankloan$50,000Shareholders’equity$100,000Total$100,000Ratioofrealassetstototalassets=$30,000/$150,000=0.20Conclusion:whenthefirmstartsupandraisesworkingcapital,itischaracterizedbyalowratioofrealassetst ototalassets.Whenitisinfullproduction,ithasahighratioofrealassetstototalassets.Whentheprojectshuts downandthefirmsellsitoffforcash,financialassetsonceagainreplacerealassets.9.Forcommercialbanks,theratiois:$140.1/$11,895.1=0.0118Fornon-financialfirms,theratiois:$12,538/$26,572=0.4719Thedifferenceshouldbeexpectedprimarilybecausethebulkofthebusinessoffinancialinstitutionsistomakeloans;whicharefinancialassetsforfinancialinstitutions.10.a.Primary-markettransactionb.Derivativeassetsc.Investorswhowishtoholdgoldwithoutthecomplicationandcostofphysicalstorage.1-311.a.Afixedsalarymeansthatcompensationis(atleastintheshortrun)independentofthefirmssuccess.Thissalarystructuredoesnottiethemanager’simmediatecompensationtothesuccessofthefirm.However,themanagermightviewthisasthesafestcom pensationstructureandthereforevalueitmorehighly.b.Asalarythatispaidintheformofstockinthefirmmeansthatthemanagerearnsthemostwhenthesharehol ders’wealthismaximized.Fiveyearsofvestinghelpsaligntheinterestsoftheemployeewiththelong-termperformanceofthefirm.Thisstructureisthereforemostlikelytoaligntheinterestsofmanagersandshareholders. Ifstockcompensationisoverdone,however,themanagermightviewitasoverlyriskysincethemanager’scareerisalreadylinkedtothefirm,andthisunpersifiedexposurewouldbeexacerbatedwithalargestockpo sitioninthefirm.c.Aprofit-linkedsalarycreatesgreatincentivesformanagerstocontributetothefirm’ssuccess.However,amanagerwhosesalaryistiedtoshort-termprofitswillberiskseeking,especiallyifthe seshort-termprofitsdeterminesalaryorifthecompensationstructuredoesnotbearthefullcostoftheproject’srisks.Shareholders,incontrast,bearthelossesaswellasthegainsontheproject,andmightbelesswillingtoassumethatrisk.12.Evenifaninpidualshareholdercouldmonitorandimprovemanagers’performance,andtherebyincreasethevalueofthefirm,thepayoffwouldbesmall,sincetheownershipshareinalargecorporationwouldbeverysmall.Forexample,ifyouown$10,000ofFordstocka ndcanincreasethevalueofthefirmby5%,averyambitiousgoal,youbenefitbyonly:0.05×$10,000=$500Incontrast,abankthathasamultimillion-dollarloanoutstandingtothefirmhasabigstakeinmakingsuretha tthefirmcanrepaytheloan.Itisclearlyworthwhileforthebanktospendconsiderableresourcestomonitort hefirm.13.Mutualfundsacceptfundsfromsmallinvestorsandinvest,onbehalfoftheseinvestors,inthenationalandinternationalsecuritiesmarkets.Pensionfundsacceptfundsandtheninvest,onbehalfofcurrentandfutureretirees,therebychannelingfund sfromonesectoroftheeconomytoanother.Venturecapitalfirmspoolthefundsofprivateinvestorsandinvestinstart-upfirms.Banksacceptdepositsfr omcustomersandloanthosefundstobusinesses,orusethefundstobuysecuritiesoflargecorporations.Treasurybillsserveapurposeforinvestorswhopreferalow-riskinvestment.Theloweraveragerateofreturncomparedtostocksisthepriceinvestorspayforpredictabilityofinvestmentperformanceandportfoliovalue.14.1-415.Witha“top-down”investingstyle,youfocusonassetallocationorthebroadcompositionoftheentireportfolio,whichisthemajordeterminantofoverallperformance.Moreover,top-downmanagementisthenaturalwaytoestablishaportfoliowithalevelofriskconsistentwithyourrisktoler ance.Thedisadvantageofanexclusiveemphasisontop-downissuesisthatyoumayforfeitthepotentialhig hreturnsthatcouldresultfromidentifyingandconcentratinginundervaluedsecuritiesorsectorsofthemar ket.Witha“bottom-up”investingstyle,youtrytobenefitfromidentifyingundervaluedsecurities.Thedisadva ntageisthatyoutendtooverlooktheoverallcompositionofyourportfolio,whichmayresultinanon-persifi edportfoliooraportfoliowitharisklevelinconsistentwithyourlevelofrisktolerance.Inaddition,thistechn iquetendstorequiremoreactivemanagement,thusgeneratingmoretransactioncosts.Finally,youranalysi smaybeincorrect,inwhichcaseyouwillhavefruitlesslyexpendedeffortandmoneyattemptingtobeatasimplebuy-and-holdstrategy.Youshouldbeskeptical.Iftheauthoractuallyknowshowtoachievesuchreturns,onemustquestionwhythe authorwouldthenbesoreadytosellthesecrettoothers.Financialmarketsareverycompetitive;oneoftheim plicationsofthisfactisthatrichesdonotcomeeasily.Highexpectedreturnsrequirebearingsomerisk,ando bviousbargainsarefewandfarbetween.Oddsarethattheonlyonegettingrichfromthebookisitsauthor.16.。

博迪投资学第九版InvestmentChap015习题答案