Journalizing

英语会计知识点总结

英语会计知识点总结IntroductionAccounting is a systematic process of recording, analyzing, and interpreting financial information of a business. It is an essential tool for business managers to make decisions, monitor performance, and report to stakeholders. This summary aims to highlight key accounting concepts, principles, and practices that are crucial for understanding and applying accounting knowledge.Accounting PrinciplesThere are generally accepted accounting principles (GAAP) that guide the preparation of financial statements and reports. These principles ensure consistency, comparability, and transparency in financial reporting. The basic accounting principles include:1. Going Concern Assumption: The assumption that a business will continue to operate in the foreseeable future.2. Accrual Basis: Recording revenues and expenses when they are earned or incurred, regardless of when cash is received or paid.3. Consistency: Using the same accounting methods and procedures from one period to another for comparability.4. Materiality: Reporting financial information that is significant and relevant to users.5. Cost Principle: Recording assets at their historical cost, not their current market value.6. Dual Aspect Principle: Every transaction has two aspects – a debit and a credit, which must be recorded in the accounting system.Financial StatementsFinancial statements are the end products of the accounting process. They provide a summary of the financial performance and position of a business. The main financial statements include:1. Income Statement: A report of revenues, expenses, and net income or loss for a specific period.2. Balance Sheet: A snapshot of the assets, liabilities, and equity of a business at a specific point in time.3. Cash Flow Statement: A report of cash inflows and outflows from operating, investing, and financing activities.4. Statement of Changes in Equity: A summary of changes in equity capital, including share capital, retained earnings, and other reserves.Accounting CycleThe accounting cycle is a series of steps that are performed to process financial transactions and produce financial statements. The steps in the accounting cycle include:1. Analyzing Transactions: Identifying and analyzing the financial effects of business transactions.2. Journalizing: Recording transactions in a chronological order in the general journal.3. Posting to Ledger: Transferring journal entries to individual accounts in the general ledger.4. Adjusting Entries: Making adjusting entries at the end of the accounting period to reflect accruals, deferrals, and estimates.5. Trial Balance: Preparing a trial balance to ensure that total debits equal total credits in the general ledger.6. Financial Statements: Preparing income statement, balance sheet, and other financial reports based on the trial balance.7. Closing Entries: Recording closing entries to transfer revenue and expense account balances to the income summary account.8. Post-Closing Trial Balance: Preparing a post-closing trial balance to ensure that temporary accounts have been closed and permanent accounts have the correct balances. Inventory Valuation MethodsInventory valuation is important for determining the cost of goods sold and the value of ending inventory. There are several inventory valuation methods, including:1. First-In, First-Out (FIFO): Assuming that the oldest units are sold first and the newest units remain in ending inventory.2. Last-In, First-Out (LIFO): Assuming that the newest units are sold first and the oldest units remain in ending inventory.3. Weighted Average Cost: Calculating the average cost per unit based on the total cost of goods available for sale.4. Specific Identification: Identifying the actual cost of each specific unit in the inventory. Depreciation MethodsDepreciation is the process of allocating the cost of a tangible asset over its useful life. Common depreciation methods include:1. Straight-Line Method: Allocating an equal amount of depreciation expense each accounting period.2. Declining Balance Method: Allocating a higher depreciation expense in the early years of an asset’s life.3. Units of Production Method: Allocating depreciation expense based on the actual usage or production of the asset.Revenue RecognitionRevenue recognition is the process of recording revenue when it is earned and realizable. The key principles of revenue recognition include:1. Recognition Criteria: Revenue should be recognized when it is earned, measurable, and collectible.2. Performance Obligation: Revenue should be allocated to each distinct performance obligation in a contract.3. Time of Transfer: Revenue should be recognized at the time of transfer of goods or services to the customer.4. Principal versus Agent: Revenue should be recognized based on whether the entity is a principal or an agent in a transaction.Financial AnalysisFinancial analysis involves using financial information to assess the performance and financial position of a business. Common financial analysis techniques include:1. Ratio Analysis: Calculating and interpreting financial ratios to evaluate liquidity, profitability, solvency, and efficiency.2. Trend Analysis: Analyzing the trend of key financial indicators over multiple periods to identify patterns and changes.3. Vertical Analysis: Comparing each line item on the financial statements to a common base, such as total revenue or total assets.4. Horizontal Analysis: Comparing financial data from different periods to identify changes and trends.ConclusionAccounting knowledge is fundamental for business managers, investors, creditors, and other stakeholders to understand and evaluate the financial health of a business. This summary provides an overview of key accounting concepts, principles, and practices that are essential for effective financial management and decision-making. By understanding and applying these accounting principles, individuals can make informed financial decisions and contribute to the success of their business endeavors.。

ODI_学习笔记

AIMDO.060P UBLISH U SER R EFERENCEM ANUALODI学习笔记Author: Derek.JaaCreation Date: January 1, 2009Last Updated: January 29, 2009Document Ref: ODI090101Version: 1.0Approvals:<Approver 1><Approver 2>Copy Number _____Document ControlChange RecordReviewersDistributionNote To Holders:If you receive an electronic copy of this document and print it out, please write your nameon the equivalent of the cover page, for document control purposes.If you receive a hard copy of this document, please write your name on the front cover, fordocument control purposes.ContentsDocument Control (2)Part 1 – Overview (4)1. ETL & E-LT (4)2. Oracle Data Integrator架构 (4)3. Knowledge Modules [知识模型] (6)Part 2 – ODI设置&简单数据整合 (7)1. 完成Getting Start (7)2. 创建Repository Storage Space (7)3. 创建Master Repository (8)4. 连接至Master Repository (9)5. 创建Work Repository (10)6. 连接至Work Repository (11)7. 创建Oracle Data Server (12)8. 创建Physical Schema [物理架构] (13)9. 创建Logical Schema [逻辑架构] (14)10. 创建Project [项目] (15)11. 导入Knowledge Module (15)12. 创建Data Module & Reverse-engineer (16)13. 创建 & 执行Interface (17)14. 为Datastore启用简单CDC (18)15. 为Datastore启用一致性CDC (19)16. 创建Physical Agent [物理代理] & Logical Agent[逻辑代理] (21)17. 创建Scenario并使用Agent运行 (22)18. Interface/Package调试及KM分析 (23)Appendix (24)ODI连接Microsoft SQL Server 2005 (24)Open and Closed Issues for this Deliverable (25)Open Issues (25)Closed Issues (25)Part 1 – Overview阅读:An Introduction to Real-Time Data Integration1. ETL & E-LTContent无论是ETL还是E-LT,其基本目标是通过Extract/Transformation/Load这几个过程达到将源数据整合并放入目标数据库/数据仓库的过程。

财务英语试题及答案

财务英语试题及答案一、选择题(每题2分,共20分)1. What is the term for the process of recording, summarizing, and reporting financial transactions?A. BudgetingB. AccountingC. AuditingD. Forecasting答案:B2. Which of the following is a financial statement that showsa company's financial position at a specific point in time?A. Income StatementB. Balance SheetC. Cash Flow StatementD. Statement of Retained Earnings答案:B3. The difference between the purchase price and the fair market value of an asset is known as:A. DepreciationB. AmortizationC. GoodwillD. Capital Gains答案:C4. What is the term for the systematic allocation of the cost of a tangible asset over its useful life?A. DepreciationB. AmortizationC. AccrualD. Provision答案:A5. Which of the following is not a type of revenue recognition?A. Cash basisB. Accrual basisC. Installment methodD. All of the above答案:D6. The process of estimating the cost of completing a project is known as:A. BudgetingB. Cost estimationC. Project managementD. Cost accounting答案:B7. Which of the following is a non-current liability?A. Accounts payableB. Wages payableC. Long-term debtD. Income tax payable答案:C8. The term used to describe the process of adjusting the accounts at the end of an accounting period is:A. Closing the booksB. JournalizingC. PostingD. Adjusting entries答案:D9. What is the term for the financial statement that shows the changes in equity of a company over a period of time?A. Balance SheetB. Income StatementC. Statement of Changes in EquityD. Cash Flow Statement答案:C10. The process of verifying the accuracy of financial records is known as:A. BudgetingB. AuditingC. ForecastingD. Valuation答案:B二、填空题(每空1分,共10分)1. The __________ is the process of determining the value of an asset or liability.答案:valuation2. A __________ is a type of financial instrument that represents a creditor's claim on a company's assets.答案:bond3. The __________ is the difference between the cost of an asset and its depreciation.答案:book value4. __________ is the process of converting non-cash items into cash equivalents.答案:Liquidation5. A __________ is a financial statement that provides information about a company's cash inflows and outflows during a specific period.答案:Cash Flow Statement6. The __________ is the process of estimating the useful life of an asset.答案:depreciation schedule7. __________ is the practice of recording revenues and expenses when they are earned or incurred, not when cash is received or paid.答案:Accrual accounting8. __________ is the process of recording transactions in the order they are received.答案:Journalizing9. __________ is the practice of matching expenses with the revenues they helped to generate.答案:Matching principle10. A __________ is a document that provides evidence of a transaction.答案:voucher三、简答题(每题5分,共20分)1. What are the main components of a balance sheet?答案:The main components of a balance sheet are assets, liabilities, and equity.2. Explain the concept of "double-entry bookkeeping."答案:Double-entry bookkeeping is a system of recording financial transactions in which every entry to an account requires a corresponding and opposite entry to another account, ensuring that the total of debits equals the total of credits.3. What is the purpose of an income statement?答案:The purpose of an income statement is to summarize a company's revenues, expenses, and profits or losses over a specific period of time.4. Describe the role of a financial controller in anorganization.答案:A financial controller is responsible for overseeing the financial operations of an organization, including budgeting, financial reporting, and ensuring compliance with financial regulations and policies.四、论述题(每题15分,共30分)1. Discuss the importance of financial planning in business management.答案:Financial planning is crucial in business management as it helps in setting financial goals。

Horizontal analysis

Horizontal analysis(水平分析):将本期报表与前期报表的相同项目进行比较的一种财务分析方法。

Ideal standards(理想标准):只有在没有时间浪费、没有机器故障、没有材料损耗的理想经营状况下才能达到的标准。

也称为理论标准。

Income from operations (operating income)(营业利润):一个利润中心或投资中心的收入减去经营费用和服务部门费用。

Income statement(损益表):总括列示一个企业在某一特定期间(如一个月或一年)收入与费用项目的报表。

Income summary(收益汇总):期末将收入账户和费用账户余额转入的账户。

Indirect method(间接法):报告经营活动现金流量的一种方法,这种方法在净利润的基础上进行调整来计算经营活动现金流量,调整项目包括过去现金收付的递延项目和未来现金收付的应计项目。

Inflation(通货膨胀):总物价水平上升并且货币购买力下降的期间。

Initial public offering (IPO)(首次公开招股):公司第一次向投资公众发行普通股。

Intangible assets(无形资产):对企业经营有用的、非待售的且没有实物形态的长期资产。

Internal controls(内部控制):用来保护企业资产、确保企业信息的准确性以及确保企业遵守有关法规的政策和程序。

Internal rate of return method(内含回报率法):运用现值概念来计算投资项目预计未来现金流量的收益率的一种评价备选投资项目的方法。

Inventory shrinkage(存货损耗):存货账户记录的可供销售商品金额大于实际盘点商品金额的部分。

Inventory turnover(存货周转率):用于衡量销售商品和存货数量关系,等于商品销售成本除以平均存货。

Investment center(投资中心):一个分权单位,其负责人有权利和责任做出决策从而影响该中心的收入、成本以及可获得的固定资产。

会计英语第四版参考答案

会计英语第四版参考答案Chapter 1: Introduction to Accounting1. What is accounting?- Accounting is the systematic recording, summarizing, and reporting of financial transactions and events of a business entity.2. What are the main functions of accounting?- The main functions of accounting are to providefinancial information for decision-making, ensure compliance with laws and regulations, and facilitate the management of a business.3. What are the two main branches of accounting?- The two main branches of accounting are financial accounting and management accounting.4. What is the purpose of financial accounting?- The purpose of financial accounting is to provide an accurate and fair representation of an entity's financial position and performance to external users.5. What is the double-entry bookkeeping system?- The double-entry bookkeeping system is a method of recording financial transactions in which every transactionis recorded twice, once as a debit and once as a credit, to maintain the equality of the accounting equation.Chapter 2: Accounting Concepts and Principles1. What are the fundamental accounting concepts?- The fundamental accounting concepts include the accrual basis of accounting, going concern, consistency, and materiality.2. What is the accrual basis of accounting?- The accrual basis of accounting records transactions when they occur, regardless of when cash is received or paid.3. What is the going concern assumption?- The going concern assumption is the premise that a business will continue to operate for the foreseeable future.4. What is the principle of consistency?- The principle of consistency requires that an entity should apply accounting policies consistently over time.5. What is the principle of materiality?- The principle of materiality states that only items that could potentially affect the decisions of users of financial statements are included in the financial statements.Chapter 3: The Accounting Equation and Financial Statements1. What is the accounting equation?- The accounting equation is Assets = Liabilities +Owner's Equity.2. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, statement of changes in equity, and cashflow statement.3. What is the purpose of the balance sheet?- The balance sheet provides a snapshot of an entity's financial position at a specific point in time.4. What is the purpose of the income statement?- The income statement reports the revenues, expenses, and net income of an entity over a period of time.5. What is the purpose of the cash flow statement?- The cash flow statement reports the cash inflows and outflows of an entity over a period of time.Chapter 4: Recording Transactions1. What is a journal entry?- A journal entry is the initial recording of atransaction in the general journal.2. What are the steps in the accounting cycle?- The steps in the accounting cycle are analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries.3. What is the difference between a debit and a credit?- A debit is an increase in assets or a decrease inliabilities or equity, while a credit is an increase in liabilities or equity or a decrease in assets.4. What are adjusting entries?- Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are recorded in the correct period.5. What is the purpose of closing entries?- Closing entries are made to transfer the balances of temporary accounts to the owner's equity account and to prepare the accounts for the next accounting period.Chapter 5: Accounting for Merchandising Businesses1. What is a merchandise inventory?- A merchandise inventory is the stock of goods held by a business for sale to customers.2. What is the cost of goods sold?- The cost of goods sold is the direct cost of producing the merchandise sold during an accounting period.3. What is the gross profit?- The gross profit is the difference between the sales revenue and the cost of goods sold.4. What is the difference between a perpetual and a periodic inventory system?- A perpetual inventory system updates inventory records in real-time with each sale or purchase, while a periodicinventory system updates inventory records at specific intervals, such as at the end of an accounting period.5. What is the retail method of inventory pricing?- The retail method of inventory pricing is a method of estimating the cost of ending inventory by applying a cost-to-retail ratio to the retail value of the inventory.Chapter 6: Accounting for Service Businesses1. What are the main differences in accounting for service businesses compared to merchandise businesses?- Service businesses do not have inventory and their primary expenses are typically labor and overhead costs.2. What is the main source of revenue for service businesses? - The main source of revenue for service businesses is the fees charged for the services provided.3. What are the typical expenses。

会计英语单词

会计英语单词Accounting 会计economic event 经纪业务Balance sheet资产负债表Bookkeeping 簿记source document原始凭证prepaid exoense待摊费用Relevance 相关性external transaction 外部业务accrued expense 预提费用Objectivity 客观性internal transaction 内部业务cash in blank 银行存款Feasibility 可行性temporary account 暂时账户transfer voucher 转账凭证Liquidity 流动性payment voucher 付款凭证Going-concern 持续经营rdebit借方general ledger 总分类帐receipt voucher 收款凭证Asset 资产Tax accounting 税务会计Accounting Equation 会计等式Liability 负债nominal account 虚账户Managerial accounting 管理会计Revenue收入normal balance 正常余额journalizing 记日记账Expense费用adjustment 账项调整debt ratio 负债比率Income 收益accounting cycle 会计循环trial balance 试算表Depreciation 折旧financial leverage 财务杠杆time period 会计期间posting 过账Accrued items 应计项目contra account 备抵账户withdrawal 提存Entity concept 会计主体closing entries 结账分录credit 贷方Income summary 收益汇总unearned revenue 预收收入account 账户Worksheet 工作底稿Business transaction 经济业务cash 现金Financial accounting财务会计general journal 普通日记investment 投资prepaid expense 预付费用chart of account 科目表closing结账Double-entry system 复式记账real account 实账户receivable 应收账款Cost principle 成本原则Cash flow statement 现金流量表payable 应付账款Ethics of accounting会计职业道德tangible fixed asset 固定资产bad debts 坏账working capital 营运资本long-term investment 长期投资voucher 记账凭证shareholders’equity股东权益intangible fixed asset 无形资产write off 注销contributed capital 缴入资本common shares 普通股股本maker 出票人retained earnings 留存收益Owner’s equity/Capital 所有者权益payee 受款人current ratio 流动比率accrual basis 应计制、权责发生制treasury bills 国库券cash equivalent 现金等价物cash basis 现金制、收付实现制petty cash fund 备用金internal controls 内部控制bank statement 银行对账单service charges 手续费deposit in transit 在途存款debit memorandum 借项通知单allowance method 备抵法outstanding checks 未兑支票credit memorandum 贷项通知单promissory note 期票temporary investment 短期投资bad debt recovery 坏账回收maturity date 到期日cost of goods sold 销售成本deferred expenses 递延费用proceeds 贴现所得sales revenue销售收入return on asset 资产报酬率gross profit 毛利contingent liability 或有负债subsequentexpenditures后续支出transportation costs 运费operating expense 营业费用merchandise inventory 商品存货raw materials 原材料trade discounts 商品折扣asset turnover 资产周转率gross margin 毛利purchase discounts 购货折扣inventory shrinkage存货减值equity method 权益法sales discounts销售折扣inventory shrinkage 存货短缺replacement costs 重置成本work in process 生产成本net realizable value 可变现净值finished goods 完工产品manufacturing overhead 制造成本transportation-in 运输费用cost method 成本法gross profit method 毛利率法capital expenditure 资本性支出patents 专利权changes in estimate 估计变更revenue expenditure 收益性支出copyrights 版权debt security 债券证券pre-operating expenses 开办费franchise 特许权equity securities 股权证券operating lease 经营租赁goodwill 商誉carrying value 账面余额land improvements 土地改良trademarks 商标权financing lease 筹资租赁residual value 残值par value 面值nor-par value 无面值outstanding shares 发行在外股份depletion 折耗future value 终值future value of an annuity 年金终值amortization 摊销present value 现值present value of an annuity 年金现值registered bonds 记名债券coupon bonds 不记名债券term bonds 到期还本债券serial bonds 分期还本债券convertible bonds 可转换债券callable bonds 可赎回债券contingency 或有事项contingent asset 或有资产contingent liability 或有负债stock split 股票分割earning per share 每股收益price-earnings ratio 市盈率dividend yield 股利报酬率prior period adjustments 前期损益调整secured bond 有担保债debenture bonds 无担保债券或风险债券authorized stock 核定股本coupon rate or nominal rate 票面利率或名义利率sole proprietorships 独资企业marker or effective rate 市场利率或实际利率partnerships 合伙企业discount on bonds payable 应付债券折价stock subscriptions 股票认购premium on bonds payable 应付债券溢价capital surplus 资本公积loss on redemption of bonds 赎回债券损失donated capital 捐赠资本times interest earned 利息保障倍数treasury stock 库藏股common stock&preferred stock 普通股与优先股stock buyout 股票回收noncumulative-dividend preference 非累积优先股retained earnings 留存收益cumulative-dividend preference 累积优先股bonds payable 应付债券advances from customers /unearned revenue 预收账款reserve fund 盈余公积participating-dividend preference 参加优先股cash dividends 现金股利nonparticipating-dividend preference 参加优先股stock dividends 股票股利appropriated(or Restricted) retained earning 拨定留存收益temporary differences 临时性差异permanent differences 永久性差异non-depreciable assets 非折旧资产substance over form 实质重于形式non-monetary exchange 非货币性交易purchase returns and allowances 购货退回和折让inventory turnover 存货周转率number of day’s sales in inventory 存货周转天数periodic inventory system 定期盘存制perpetual inventory system 永续盘存制the straight-line(SL)method 直线法accelerated methods 加速折旧法sum-of-the years’-digits method 年数总和法declining-balance method 余额递减法accounts receivable turnover 应收账周转率dishonored note receivable 应收票据拒付bank reconciliation 银行余额调节表discounting note receivable 应收票据贴现work-in-process inventory 在产品provision for decline in value of inventory 存货跌价准备construction in progress 在建工程double-declining-balance method 双倍余额递减法impairment of long-term assets长期资产的减值return on assets 资产报酬率unearned items 预收项目Stable-monetary-unit 货币计量单位fixed assets pending disposal 固定资产清理assets turnover 资产周转率time value of money 货币的时间价值prodection method (activity method ) 工作量法simple versus compound interest 单利与复利discount on notes payables 应付票据折价rules of debits and credits 借贷规则post-closing trial balance 结账后试算表Income statement/Profit and loss account 利润表adjusted trial balance 调整后试算表current maturities of long-term obligation 一年之内到期的长期负债。

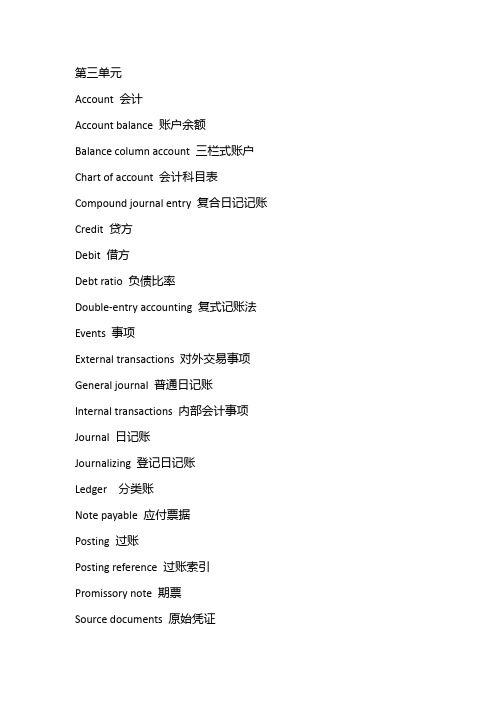

会计原理3、4单元单词

第三单元Account会计Account balance 账户余额Balance column account三栏式账户Chart of account 会计科目表Compound journal entry复合日记记账Credit贷方Debit借方Debt ratio 负债比率Double-entry accounting复式记账法Events事项External transactions对外交易事项General journal普通日记账Internal transactions内部会计事项Journal日记账Journalizing登记日记账Ledger分类账Note payable应付票据Posting过账Posting reference过账索引Promissory note期票Source documents原始凭证T-account T型账户Trial balance试算平衡表Unearned revenue预收收入第四单元Account form balance sheet账户式资产负债表Accouting basis accounting权责发生制会计Accrued expenses应计费用Accrued revenues应计收入Adjusted trial balance 调整后试算平衡表Adjusting entry调整分录Annual financial statements年度财务报表Book value 账面价值Cash basis accounting收付实现制会计Contra account备抵账户Depreciation折旧Fiscal year会计年度Interim financial statements中期财务报表Matching principle配比原则Natural business year自然营业年度Plant and equipment固定资产Prepaid expense预付费用Profit margin 利润率Report form balance sheet报告式资产负债表Straight-line depreciation method直线折旧法Time period principle会计分期原则Unadjusted trial balance未经调整的试算平衡表Unearned revenues预收收入。

西方财务会计双语单词

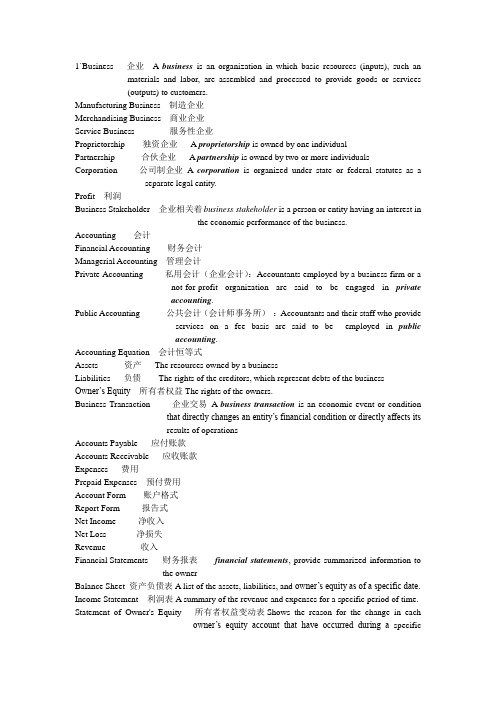

1`Business 企业 A business is an organization in which basic resources (inputs), such an materials and labor, are assembled and processed to provide goods or services(outputs) to customers.Manufacturing Business 制造企业Merchandising Business 商业企业Service Business 服务性企业Proprietorship 独资企业 A proprietorship is owned by one individualPartnership 合伙企业 A partnership is owned by two or more individuals Corporation 公司制企业A corporation is organized under state or federal statutes as a separate legal entity.Profit 利润Business Stakeholder 企业相关着business stakeholder is a person or entity having an interest inthe economic performance of the business.Accounting 会计Financial Accounting 财务会计Managerial Accounting 管理会计Private Accounting 私用会计(企业会计):Accountants employed by a business firm or anot-for-profit organization are said to be engaged in privateaccounting.Public Accounting 公共会计(会计师事务所):Accountants and their staff who provideservices on a fee basis are said to be employed in publicaccounting.Accounting Equation 会计恒等式Assets 资产The resources owned by a businessLiabilities 负债The rights of the creditors, which represent debts of the business Owner’s Equity所有者权益The rights of the owners.Business Transaction 企业交易A business transaction is an economic event or conditionthat directly changes an entity’s financial condition or directly affects itsresults of operationsAccounts Payable 应付账款Accounts Receivable 应收账款Expenses 费用Prepaid Expenses 预付费用Account Form 账户格式Report Form 报告式Net Income 净收入Net Loss 净损失Revenue 收入Financial Statements 财务报表financial statements, provide summarized information tothe ownerBalance Sheet 资产负债表A list of the assets, liabilities, and owner’s equity as of a specific date. Income Statement 利润表A summary of the revenue and expenses for a specific period of time. Statement of Owner's Equity 所有者权益变动表Shows the reason for the change in eachowner’s equity account that have occurred during a specificperiod of time.Generally Accepted Accounting Principles (GAAP) 公认会计原则Statement of Cash Flows 现金流量表A summary of the cash receipts and disbursements for a specific period of time.Certified Public Accountant (CPA) 注册会计师2`Account 账户An account is a separate record to show the increase and decrease of each financial statement item.Ledger 分类账A group of accounts for a business entity is called a ledgerChart of Accounts 科目表A list of the accounts in the ledger is called a chart of account Revenues 收入类账户Expenses 资产消耗Drawing 提款账户Balance of the Account 账户余额Debits 借方金额Credits 贷方金额T Account T 型帐 An account can be drawn to resemble the letter T, it is called a T account. Double-Entry Accounting 复式记账会计Journal Entry 日记账分录Journal 日记账Journalizing 日记簿记账2Posting 过账Two-Column Journal 二栏式日记账Unearned Revenue 预收收入The liability created by receiving the cash in advance of providing the service is called unearned revenve.Trial Balance 试算平衡3`Cash Basis 现今制(收付实现制)period in which cash is received or paidAccrual Basis 应计制(权责发生制)period in which they are earnedAdjusting Process 调整程序Accruals 应计项目Deferrals 递延项Deferred Expenses 递延费用(预付费用)have been initially recorded as assets but areexpected to become expensesAccrued Expenses 应计费用(accrued liabilities)Deferred Revenues 递延收入(预收收入)have ben initially recorded as liability bu areexpected to become revenuesAccrued Revenues 应计收入(accrued assets)Prepaid Expenses 预付费用Adjusting Entries 调整账户Unearned Expenses 预收费用?Adjusted Trial Balance 调整试算平衡Accumulated Depreciation累计折旧Depreciation 折旧Book Value of the Asset 资产账面价值Depreciation Expense 折旧费用Contra Accounts 备抵账户accumulated depreciation accountsFixed Assets 固定资产(plant assets)4`Accounting Cycle 会计循环Work Sheet 工作底稿Current Assets 流动资产Cash and other assets that are expected to be converted into cash,sold, or used up usually in less than a year are current assets.Current Liabilities 流动负债Long-Term Liabilities 长期负债Post-Closing Trial Balance 结账后试算表Closing Entries 结账分录Real Account 实账户Temporary Accounts (Nominal Accounts ) 虚账户(类似过渡账户)Income Summary 损益表(反应某一特定时期收入费用状况的报表)5`Accounting System 会计系统General Ledger 总分类账Accounts Payable Subsidiary Ledger 应付账款明细账Accounts Receivable Subsidiary Ledger 应收账款明细账Purchases Journal 赊购日记账The purchases journal is designed for recording allpurchases on account.Cash Payments Journal 现金支出日记账Revenue Journal 赊销日记账Cash Receipts Journal 现金收入日记账All transactions that involve the receipt of cash arerecorded in the cash receipts journalSpecial Journals 特种日记账Controlling Account 控制账户General Journal 普通日记账6` Multiple-Step Income Statement 多步式损益表Single-Step Income Statement 单步式损益表Sales 销售额Sales Discounts 销售折扣Sales Returns & Allowances 销售退回及折让Purchase 购买额Purchase Discount 购货折扣Purchase Returns & Allowances 购货退回或折让Periodic Method 实地盘存制Perpetual Method 永续盘存制Merchandise Inventory 商品存货Cost of Merchandise Sold 商品销售成本Gross Profit 毛利润Administrative Expenses管理费用Selling Expenses 销售费用Income from Operations 营业收入Other Expense 其他费用Other Income 其他收益Invoice 发票Credit Memorandum 贷项通知单Debit Memorandum 借项通知单FOB Destination 目的地交货FOB Shipping Point 船上交货Trade Discounts 商业折扣7` Cash 现金Bank Reconciliation 银行存款余额调节表Check 支票Remittance advice 汇款通知Transactions register 交易登记册(交易账簿)Deposit ticket 存款票据Signature card 签名卡Drawee 付款人Drawer 发票人Payee 收款人8` Accounts Receivable 应收账款Notes Receivable 应收票据Allowance Method 备抵法Uncollectible Accounts Expense 坏账损失Direct Write-Off Method 直接冲销法Aging the Receivables 应收账款账龄分析法Net Realizable Value 可变现价值Maturity Value 到期价值Promissory Note 本票9`Inventory 存货Periodic Inventory System 实地盘存制Perpetual Inventory System 永续盘存制Average Cost Method 加权平均法First-in, First-out (FIFO) Method 先进先出法Last-in, First-out (LIFO) Method 后进先出法Lower-of-Cost-or-Market (LCM) Method 成本与市价孰低法Gross Profit Method 毛利率法Retail Inventory Method 零售价法10`Fixed assets 固定资产损失Depreciation 折旧Residual Value 剩余价值Book Value 账面价值Accelerated Depreciation Method 加速折旧法Straight-Line Method 直线法Declining-Balance Method 余额递减法Units-of-Production Method 工作量法Trade-in Allowance 交换折价Depletion 折耗Amortization 摊销Intangible Assets 无形资产Copyright 版权Patents 专利Goodwill 商誉Trademark 商标Boot 补价(附得利益)11`Discount 折价Discount Rate 贴现率Proceeds 应收票据贴现率Gross Pay 毛工资Net Pay 净薪资Payroll 薪酬Defined Contribution Plan 确定投入计划Defined Benefit Plan 确定收益计划12`Stock 股份Stockholders 股东Stockholders’Equity 股东权益Retained Earnings 留存收益Paid-in Capital 实收资本Common Stock 普通股Preferred Stock 优先股Par 平价Cumulative Preferred Stock 累积优先股Nonparticipating Preferred StockStated Value 设定价值Outstanding Stock发行在外股票Premium 溢价Treasury Stock 库藏股票Stock Split 股票分割Cash Dividend 现金股利Stock Dividend 股票股利。

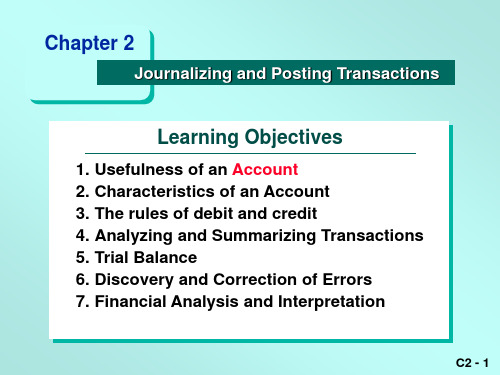

02journalizing and posting 会计英语

To assist you in learning, an account can be drawn to resemble the letter T.

C2 - 11

The T-Account TCash

The T-account has a title. T.

C2 - 12

The T-Account TCash

C2 - 7

Major Account Classifications

Owner’s equity is the owner’s right to the assets of the business. Revenues are increases in owner’s equity as a result of selling services or products. Expenses are the using up of assets or consuming of services to generate revenue.

NetSolutions

Chart of Accounts Balance Sheet Assets Cash Accounts Receivable Supplies Prepaid Insurance Land Office Equipment Income Statement 4. Revenue 41 Fees Earned 5. 51 52 54 55 59 Expenses Wages Expense Rent Expense Utilities Expense Supplies Expense Miscellaneous Expense

C2 - 2

Accounts are used to record business transactions. An account is simply a record of all the increases and decreases in a financial statement item (such as cash, supplies, and accounts payable).

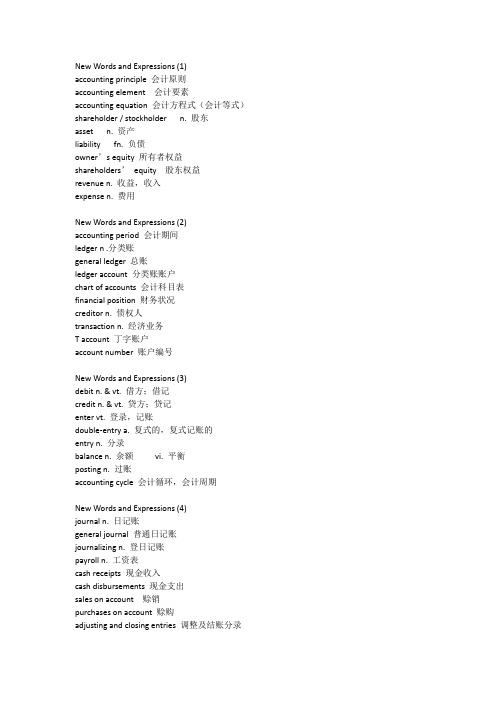

会计英语词汇

accounting principle 会计原则accounting element 会计要素accounting equation 会计方程式(会计等式)shareholder / stockholder n. 股东asset n. 资产liability fn. 负债owner’s equity 所有者权益shareholders’equity 股东权益revenue n. 收益,收入expense n. 费用New Words and Expressions (2)accounting period 会计期间ledger n .分类账general ledger 总账ledger account 分类账账户chart of accounts 会计科目表financial position 财务状况creditor n. 债权人transaction n. 经济业务T account 丁字账户account number 账户编号New Words and Expressions (3)debit n. & vt. 借方;借记credit n. & vt. 贷方;贷记enter vt. 登录,记账double-entry a. 复式的,复式记账的entry n. 分录balance n. 余额vi. 平衡posting n. 过账accounting cycle 会计循环,会计周期New Words and Expressions (4)journal n. 日记账general journal 普通日记账journalizing n. 登日记账payroll n. 工资表cash receipts 现金收入cash disbursements 现金支出sales on account 赊销purchases on account 赊购adjusting and closing entries 调整及结账分录现金Cash银行存款Cash in bank现金等价物cash equivalents银行汇票Bank draft信用卡Credit card短期投资Short-term investmentsNew Words and Expressions (2)股票stock债券bonds基金funds应收账款Accounts receivable应收票据Notes receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable坏账准备allowance for bad debts预付项目prepaid存货Inventories原材料Raw materials低值易耗品Low-value consumption goods半成品Semi-Finished goods产成品Finished goods商品进销差价Differences between purchasing and selling price 本金Principal利息Interest证券交易所Securities ExchangeSection 1New Words and Expressionsasset n. 资产enterprise n. 企业tangible assets 有形资产economic benefit 经济利益rental n. 租赁,租金额administrative 管理的,行政的accounting year 会计年度fixed assets 固定资产Section 1New Words and Expressionsproperty n. 财产,地产,资产warehouse n. 库房exchange n. 交换issuance of securities 发行股票donation n. 捐助long-term assets 长期资产lump sum purchase 整批购买recognition criteria确认条件historical cost 历史成本,原始成本Section 1acquisition cost 购置成本original cost 原始成本actual cost 实际成本,原始成本additional cost 附加费用expenditure n. 支出,花费,开销intended use 预定可使用状态installation cost 安装费professional fees 专业人员服务费overhead cost 管理费building permit fee 建设许可费Section 2economic value 经济价值useful life 使用寿命depreciation n. 折旧estimated net residual value 预计净残值net salvage value 净残值depreciation rate折旧率depreciable amount应计折旧额Section 2disposal n. 处置,处理deduct vt. 扣除straight-line method 年限平均法(直线法)units of production method 工作量法double declining balance method 双倍余额递减法sum-of-the-years-digits method 年数总和法conservative a. 保守的,守旧的depreciation expense 折旧费depreciation charge 折旧费wear and tear 磨损,损耗Section 2straight-line rate 直线折旧率book value 账面价值double straight-line rate双倍直线折旧率SYD 年数总和depreciation base折旧基数functional value功能价值annual depreciation amount 年折旧额disposal expenses 弃置费用Section 3intangible assets 无形资产identifiable a.可以确认的physical substance 实物形态privilege n. 特权,特别待遇finite intangibles 使用寿命有限的无形资产indefinite intangibles 使用寿命不确定的无形资产Section 3franchise n. 特许权,公民权license n. 营业执照,许可证Internet domain name 互联网域名construction permit 建筑许可证land utilization right 土地使用权assessed value 评估价格amortization n. 摊销Section 3impairment test 减值测试amortization charge 摊销费profit and loss 损益provision n. 条款,规定common practice惯例disposal proceeds处置收益accumulated amortization累计摊销额organization cost 开办费Section 1New Words and Expressions短期负债Current liability透支overdraft应付票据Notes payable应付账款Account payable预收账款unearned revenue应付工资Accrued wages应付股利Dividends payableSection 1应交税金Tax payable应交增值税value added tax payable应交消费税Consumption tax payable应交所得税Income tax payable应交个人所得税Personal income tax payable其他应付款Other payables预提费用Drawing expense in advance或有负债Contingent LiabilitiesSection 2New Words and Expressions长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year 一年后到期的长期借款Long-term loans due over one year 债券debentures , bondsSection 2应付债券Bonds payable债券面值Face value, Par value到期日the maturity date债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest或有负债contingent liability未履行责任defaultNew Words and Expressionspartnership n. 合伙partner n. 合伙人proprietorship n. 独资corporation n. 公司distribution n. 分配divide v. 划分share v. 分配分享issuance 发行Common stock n. 普通股Preferred stock n. 优先股Shareholder(Stockholder) n. 股东dividend 股利股息owner’s equity 所有者权益par value stock 有面值股票no-par value stock 无面值股票paid-in capital 实收资本additional paid-in capital 多收资本,增收资本capital surplus 资本公积retained earnings 留存收益cash dividend 现金股利stock dividend 股票股利declaration of dividend 股利宣布股利公告dividend distribution 股利分配reserve 计提准备金准备金stockholders’equity 股东权益appropriation of retained earnings 留存收益的分拨appropriated retained earnings 拨定的留存收益reserve found / surplus reserve 盈余公积stock split 股票分割charter 宪章章程bylaw 附则、细则、公司章程New Words and Expressionssales revenue 销售收入cash discount 现金折扣sales allowances 销售折让trade discount 商业折扣service revenue 劳务收入proportion of A to B A占B的比例prime operating revenue 主营业务收入render 提供(服务等)period expense 期间费用operating/sales expense 营业/销售费用administrative expense 行政管理费用financial expense 财务费用freight charges 运输费advertising expenses 广告费direct material cost 直接材料成本direct labor cost 直接人工成本manufacturing overhead 制造费用leasing charge 租赁费maintenance 维修费allocate 分摊New Words and Expressionsfinancial position财务状况operating results经营成果the balance sheet资产负债表the income statement 利润表multiple-step income statement多步式利润表single-step income statement单步式利润表accounts payable应付账款long-term assets长期资产net income净收益net loss净损失the cost of goods sold商品销售成本gross profit毛利income tax expenses所得税费用the statement of cash flows现金流量表cash receipts现金收入cash payments现金支出cash equivalents现金等价物operating activities经营活动financing activities筹资活动(融资行为)New Words and Expressionsauditing 审计,查账,审计学examination of financial statements 财务报表审查audit report/ auditor’s report 审计报告,审计师报告internal auditing 内部审计external auditing 外部审计governmental auditing 政府审计audit fee 审计费audit process 审计程序,审计过程system of internal control 内部控制系统Statement of Auditing Standards 审计准则公告engagement letter 审计委托书audit working paper 审计工作底稿test of compliance 符合性测试substantive test 实质性测试audit procedure 审计程序unqualified opinion 无保留意见书,无保留意见qualifield audit report 保留意见的审计报告adverse opinion 否定意见书,否定意见disclaimer 无法发表意见的(审计)报告。

会计学原理专业英语词汇对照(第一二章)

会计学原理专业英语词汇对照第一章:必知词汇accounting会计recordkeeping or bookkeeping簿记shareholders股东board of directors董事会auditors审计suppliers供应商creditor债权人ethics职业道德GAAP公认会计原则(美国)SEC证券交易委员会(美国)FASB财务会计准则委员会(美国)IASB国际会计准则理事会(国际)IFRS国际财务报告准则(国际)Relevant相关Reliable可靠Comparable可比Principles原则The measurement principle/ the cost principle计量原则/ 成本原则The revenue recognition principle收入确认原则The expense recognition principle/ the matching principle支出确认原则/配比原则Sale on credit/ on account 赊销Purchase on credit/on account赊购The full disclosure principle充分披露原则Assumptions假设The going-concern assumption持续经验假设The monetary unit assumption货币计量假设The time period assumption会计分期假设The business entity assumption会计主体假设Sole proprietorship独资企业Unlimited liability无限责任Partnership合伙企业Corporation公司Double taxation双重课税Expanded accounting equation扩展会计等式Assets资产Liabilities负债Owners, equity 所有者权益Net assets净资产Owners, capital所有者资本Owners, withdrawals所有者提取/所有者抽回投资Expenses费用Revenue收入Net income净利润Net loss净损失Income statement利润表Statement of owners, equity所有者权益表/所有者权益变动表Balance sheet资产负债表Statement of cash flows现金流量表第二章:必知词汇(上文有的不再重复)Accounting books/books会计帐簿Source documents原始凭证Account账户General ledger总分类账Ledger分类账Account receivable应收账款Note receivable应收票据Prepaid accounts/ prepaid expenses预付账款/待摊费用Account payable应付账款Note payable应付票据Unearned revenue预收账款Accrued liabilities应计负债Increase增加Decrease减少Chart of accounts会计科目表T-account T形账户Debit借方(Dr.)Credit贷方(Cr.)Account balance账户余额Normal balance正常余额Double entry accounting 复式记账法Journalizing登记日记账Journal日记账General journal普通日记账Journal entry日记账分录Posting过账Balance column account三栏式账户PR(posting reference)过账索引Trial balance试算平衡表Unadjusted statements调整前的财务报表必记口诀:有借必有贷,借贷必相等。

会计英语词汇英文解释

1.Accounting(会计)The process of indentifying,recording, summarizing and reporting economic information to decision makers.2.Financial accounting(财务会计)The field of accounting that serves external decision makers,such as stockholders,suppliers, banks and government agencies.3.Management accounting(管理会计)The field of accounting that serves internal decision makers,such as top executives,department headsand people at other management levels within an organization.4.Annual report(年报)A combination of financial statements,management discussion and analysis and graphs and charts that is provided annually to investors.5.Balance sheet (statement of financial position,statement of financial condition)(资产负债表)A financial statement that shows the financial status of a business entity at a particular instant in time.6.Balance sheet equation(资产负债方程式)Assets = Liabilities + Owners' equity.7.Assets(资产)Economic resources that are expected to help generate future cash inflows or help reduce future cash outflows.8.Liabilities (负债)Economic obligations of the organization to outsiders ,or claims against its assets by outsiders.9.Owners’ equity (所有者权益)The residual interest in the organization’s assets after deducting liabilities.10.Notes payable (应付票据)Promissory notes that are evidence of a debt and state the terms of payment.11.Entity (实体)An organization or a section of an organization that stands apart from other organization and individuals as a separate economics unit.12.Transaction (交易)Any event that both affects the financial position of an entity and be reliably recorded in money terms.13.Inventory (存货)Goods held by a company for the purpose of sale to customers.14.Account (帐户)A summary record of the changes in a particular assets,liability,or owne r’ equity.15.Account payable (应付帐款)A liability that results from a purchase of goods or services on account.17.Creditor (债权人)A person or entity to whom money is owed.18.Debtor (债务人)A person or entity that owes money to another.19.Sole proprietorship (个体经营、独资经营)A separate organization with a single owner.20.Partnership (合伙)A form of organization that joins two or more individuals together as co-owners(共有人).21.Corporation (公司)A business organization that is created by individual state laws.22.Limited liability (有限责任)A feature of the corporate form of organization whereby corporate creditors ordinarily have claims against the corporate assets only.23.Publicly owned (公有)A corporation in which shares in the ownership are sold to thepublic.24.Privately owned (私有)A corporation owned by a family,a small group of shareholders,or a single individual,in which shares of ownership are not publicly sold.25.Stockholders’ equity (shareholders’ equity) (股东权益)Own ers’ equity of a corporation.The excess of assets over liabilities of a corporation.26.Paid-in capital(实际投入资本)The total capital investment in a corporation by its owners both at and subsequent to the inception of business.27.Par value(票面值)The nominal dollar amount printed on stock certificates.29.Auditor (审计师)A person who examines the information used by managers to prepare the financial statements and attests to the credibility of those statements.31.Audit (审计)An examination of transactions and financial statement made in accordance with generally accepted auditing standards.33. Fiscal year (会计、财政年度)The year established for accounting purposes.34.Interim periods (中期)The time spans established for accounting purposes that are less than a year.35.Revenues(sales) (收入OR商品销售收入)Increases in owners’ equity arising from increases in assets received in exchange for the delivery of goods or services to customers.36.Expenses (费用)Decreases in owners’ equity that arise because goods or services are delivered to customers.37.Income (profit ,earnings) (收益、利润)The excess of revenues over expenses.39.Accrual basis (应计制、权责发生制)Accounting method that recognizes the impact of transactions on the financial statements in the time periods when revenues and expenses occur.40.Cash basis (收付实现制)Accounting method that recognizes the impact of transactions on the financial statements only when cash is received or disbursed.43.Cost of goods sold (cost of sales) (销售成本)The original acquisition cost of the inventory that was sold to customers during the reporting period.44.Matching (配比)The recording of expenses in the same time period as the related revenues are recognized.47.Depreciation (折旧)The systematic allocation of the acquisition cost of long-lived of fixed assets to the expenses accounts of particular periods that benefit from the use of the assets. income (净利润)The remainder after all expenses has been deducted from revenues.49.Income statement (statement of earnings, operating statement) (收益表)A report of all revenues and expenses pertaining to a specific time period.50.Statement of cash flows (cash flow statement) (现金流量表)A required statement that reports the cash receipts and cash payments of an entity during a particular period. loss (净损失)The difference between revenues and expenses when expenses exceed revenues.52.Cash dividends (现金股利)Distribution of cash to stockholders that reduce retained income.53.Statement of retained income (利润分配表)A statement that lists the beginning balance in retained income, followed by a description of any changes that occurred during the period, and the ending balance.54.Statement of income and retained income (收入及利润分配表)A statement that included a statement of retained income at the bottom of an income statement.55.Earnings per share (EPS) (每股收益)Net income divided by average number of common shares outstanding.56.Price-earnings ratio (P-E) (市盈率)Market price per share of common stock divided by earnings per share of common stock.57.Dividend-yield ratio (股息率)Common dividends per share dividend by market price per share.58.Dividend-payout ratio (派息率)Common dividends per share dividend by earnings per share.59.Double-entry system (复试记账法)The method usually followed for recording transactions, whereby at least two accounts are always affected by each transaction.60.Ledger (分类账)The records for a group of related accounts kept current in asystematic manner.61.General ledger (总分类账)The collection of accounts that accumulates the amounts reported in the major financial statements.62.T-account (T形账户)Simplified version of ledger accounts that takes the form of the capital letter T.63.Balance (余额)The difference between the total left-side and right-side amounts in an account at any particular time.64.Debit (借方)An entry or balance on the left side of an account.65.Credit (贷方)An entry or balance on the right side of an account.66.Charge (Debit)A word often used instead of debit.67.Source documents (原始凭证)The supporting original records of any transactions.68.Book of original entry (原始分录帐本)A formal chronological record of how the entity’s transactions affect the balances in pertinent accounts.69.General journal (普通日记账)The most common example of a book of original entry; a complete chronological record of transactions.70.Trial balance (试算表)A list of all accounts in the general ledger with their balance.71.Journalizing (记入分类帐)The process of entering transactions into the journal.72.Journal entry (日记帐分录)An analysis of the affects of a transaction on the accounts, usually accompanied by an explanation.81.Accumulated depreciation (allowance for depreciation) (累计折旧)The cumulative sum of all depreciation recognized since the date of acquisition of the particular assets described.82.Data processing 数据处理The totality to the procedures used to record, analyze store, and report on chosen activities.83.Explicit transactions (显性交易)Events such as cash receipts and disbursements, credit purchases, and credit sales that trigger nearly all day-to-day routine entries.84.Implicit transactions (非显性交易)Events (such as the passage of time) that do not generate source documents or visible evidence of the event and are not recognized in the accounting records until the end of an accounting period.85.Adjustments (adjusting entries) (调帐)End-of-period entries that assign the financial effects of implicit transactions to the appropriate time periods.86.Accrue (应计)To accumulate a receivable or payable during a given period eventhough no explicit transactions occurs.87.Unearned revenue (revenue received in advance, deferred revenue, deferred credit) (未实现收入)Revenue received and recorded before it is earned.88.Pretax income (税前利润)Income before income taxes.89.Classified balance sheet (分类资产负债表)A balance sheet that groups the accounts into subcategories to help readers quickly gain a perspective on the company’s financial position.90.Current assets (流动资产)Cash plus assets that are expected to be converted to cash or sold or consumed during the next 12 months or within the normal operating cycle if longer that a year.91.Current liabilities (流动负债)Liabilities that fall due within the coming year or within the normal operating cycle if longer than a year.92.Working capital (营运资金、资本)The excess of current assets over current liabilities.93.Solvency (偿付能力)An entity’s ability to meet its immediate financial obligations as they become due.94.Current ratio (working capital ratio) (流动比率)Current assets divided by current liabilities.Current ratio = Current assets / Current liabilities.95.Report format (报表格式之一)A classified balance sheet with the assets at the top. Example:Balance Sheet, January 31,20X2Assets 1999 1998Current assetsCashAccounts receivable……Total current assetsLong-term assetsStore equipmentAccumulated depreciationTotal assetsLiabilities and Owners’ Equity 1999 1998 Current liabilitiesNote payableAccounts payable…Total current liabilities Stockholder’s equityPaid-in capitalRetained incomeTotal liabilities and owners’ equity96.Account format (报表格式之二)A classified balance sheet with the assets at the left. Example:Balance Sheet, January 31,20X2Assets Liabilities and Owners’ EquityCurrent assets Current liabilitiesCash Note payableAccounts receivable Accounts payable… …Total current assets Total current liabilitiesLong-term assets Stockholder’s equityStore equipment Paid-in capitalAccumulated depreciation Retained incomeTotal Total97.Single-step income statement (单一步骤收入表)An income statement that groups all revenues together and then lists and deducts all expenses together without drawing any intermediate subtotals.98.Multiple-step income statement (复合步骤收入表)An income statement that contains one or more subtotals that highlight significant relationships.99.Gross profit (gross margin) (毛利)The excess of sales revenue over the cost of the inventory that was sold.100.Operating income (operating profit) (营业收入)Gross profit less all operating expenses.101.Profitability (收益能力)The ability of a company to provide investors with a particular rate of return on their investment.102.Gross profit percentage (gross margin percentage) (毛利率)Gross profit divided by sales.Gross profit percentage=Gross profit / Sales103.Return on sales ratio (销售收益率)Net income divided by sales,104.Return on stockholders’ equity ratio (股东权益收益率)Net income divided by invested capital (measured by average stockholder’s equity)。

会计英语—基础会计模板

chart of accounts 会计科目表

balance 余额

19

Chapter 5

20

accounting cycle 会计循环

entry 会计分录

general journal 普通日记账

journalizing 记日记账

21

ledger 分类账

posting 过账

累计折旧

adjusting entries 调整分录

adjusted trial balance

调整后试算平衡

contra-asset account 备抵账户

25

closing entries 结账分录

capital stock 股本

depreciation expense

会计标准

会计主体

accounting assumptions

会计假设

going concern 持续经营

8

monetary unit 货币计量

accounting period 会计分期

cash-basis 现金收付制

accrual-basis 权责发生制〔应计制〕

9

cost principle 本钱原那么

根本会计要素

drawing 提款,资本撤回

14

net income 净收益

net loss 净损失

expense 费用

revenue 收入

15

Chapter 4

16

account 账户

T-account T形账户

double-entry accounting

复式记账制

financing activity 融资活动

34

会计英语试题及答案

会计英语试题及答案一、选择题(每题2分,共20分)1. What is the term for the systematic, periodic assessmentof the performance and financial position of a business?A. AuditingB. BudgetingC. Financial AnalysisD. Forecasting答案:C. Financial Analysis2. Which of the following is not a basic accounting principle?A. Accrual Basis AccountingB. ConsistencyC. Cash Basis AccountingD. Going Concern答案:C. Cash Basis Accounting3. The process of recording transactions in a journal isknown as:A. PostingB. JournalizingC. ClosingD. Adjusting答案:B. Journalizing4. What does the term "Double Entry" refer to in accounting?A. Recording transactions twiceB. Recording transactions in two different accountsC. Recording transactions in two different waysD. Recording transactions in two different periods答案:B. Recording transactions in two different accounts5. The financial statement that provides a snapshot of a company's financial condition at a specific point in time is:A. Income StatementB. Balance SheetC. Cash Flow StatementD. Statement of Changes in Equity答案:B. Balance Sheet二、填空题(每题2分,共20分)6. The __________ is the accounting equation that shows the relationship between assets, liabilities, and equity.答案:Accounting Equation7. In accounting, the term __________ refers to theallocation of the cost of a tangible asset over its useful life.答案:Depreciation8. The __________ is the process of summarizing the transactions recorded in the ledger accounts and presentingthem in a more condensed form.答案:Trial Balance9. __________ is the method of accounting where revenues and expenses are recognized when they are earned or incurred, not necessarily when cash is received or paid.答案:Accrual Accounting10. The __________ is the financial statement that shows the changes in a company's cash and cash equivalents during a period.答案:Cash Flow Statement三、简答题(每题10分,共30分)11. Explain the purpose of a balance sheet in a business context.答案:The purpose of a balance sheet is to provide stakeholders with a snapshot of a company's financialposition at a specific point in time. It lists the company's assets, liabilities, and equity, and is used to assess the company's liquidity, solvency, and overall financial health.12. What are the main differences between an income statement and a statement of cash flows?答案:The income statement reports a company's financial performance over a period, focusing on revenues and expenses to determine net income. The statement of cash flows, on the other hand, shows the inflows and outflows of cash during thesame period, highlighting how the company generates and uses cash.13. Describe the concept of "matching principle" in accounting.答案:The matching principle in accounting requires that expenses be recognized in the same accounting period as the revenues they helped generate. This principle ensures that the financial statements reflect the actual economic activity of the period, providing a more accurate picture of the company's financial performance.四、计算题(每题15分,共30分)14. Given the following trial balance figures, calculate the total current assets and total current liabilities.| Account | Debit ($) | Credit ($) ||||-|| Cash | 12,000 | || Accounts Receivable | | 8,000 || Inventory | | 15,000 || Prepaid Expenses | 2,000 | || Accounts Payable | | 5,000 || Wages Payable | 1,000 | || Total Current Liabilities | | 6,000 |答案:Total current assets = Cash + Accounts Receivable + Inventory + Prepaid Expenses = 12,000 + 8,000 + 15,000 +2,000 = 37,000Total current liabilities = Accounts Payable + Wages Payable + Total Current Liabilities = 5,000 + 1,000 + 6,000 = 12,00015. If a company has a net income of $50,000 and an increase in retained earnings of $75,000, calculate the dividends paid by the company.答案:Dividends paid = Increase in retained earnings - Net income = 75,000 -。

会计英语实训考试题及答案

会计英语实训考试题及答案一、选择题(每题2分,共20分)1. What is the basic accounting equation?A. Assets = Liabilities + EquityB. Revenue – Expenses = Net IncomeC. Assets = Liabilities – EquityD. Liabilities = Assets – Equity答案:A2. Which of the following is not an accounting principle?A. ConsistencyB. MaterialityC. TimelinessD. Flexibility答案:D3. What is the purpose of adjusting entries?A. To correct past errorsB. To update the financial records for the current periodC. To prepare for the next accounting periodD. To estimate future revenues答案:B4. What is the term for the process of recording transactions in the general journal?A. JournalizingB. PostingC. ClosingD. Adjusting答案:A5. Which of the following is a type of liability?A. Common stockB. Retained earningsC. Accounts payableD. Dividends payable答案:C6. What is the accounting term for the cost of goods sold?A. COGSB. CGSC. COSD. SGA答案:A7. What is the purpose of a trial balance?A. To summarize the financial statementsB. To prove the accuracy of the accounting recordsC. To calculate the net incomeD. To determine the value of assets答案:B8. What is the accounting term for the amount of money a company owes to its suppliers?A. Accounts receivableB. Accounts payableC. Notes payableD. Accrued liabilities答案:B9. What is the term for the process of transferring journal entries to the ledger accounts?A. JournalizingB. PostingC. ClosingD. Adjusting答案:B10. Which of the following is not a financial statement?A. Balance sheetB. Income statementC. Cash flow statementD. Budget答案:D二、简答题(每题10分,共30分)1. Explain the difference between revenue and income.答案:Revenue refers to the inflow of cash or other assets from normal business operations. Income, on the other hand,is the net result of revenues and gains minus the expensesand losses. It is a measure of profitability over a period of time.2. What are the steps involved in the accounting cycle?答案:The accounting cycle involves the following steps: 1) Identifying and recording transactions, 2) Journalizing, 3) Posting to the ledger accounts, 4) Preparing a trial balance, 5) Adjusting entries, 6) Posting adjustments, 7) Preparing an adjusted trial balance, 8) Closing entries, and 9) Preparing financial statements.3. What is the purpose of depreciation in accounting?答案:Depreciation is the systematic allocation of thecost of a tangible asset over its useful life. It is used to match the expense of using the asset with the revenue it generates over time, in accordance with the matchingprinciple.三、案例分析题(每题25分,共50分)1. Assume you are the accountant for a company that has just purchased a piece of equipment for $50,000. The equipment is expected to have a useful life of 5 years and no residual value. Calculate the annual depreciation expense using the straight-line method.答案:The annual depreciation expense using the straight-line method is calculated as follows:Cost of the equipment = $50,000Useful life = 5 yearsAnnual depreciation expense = (Cost of the equipment –Residual value) / Useful lifeAnnual depreciation expense = ($50,000 – $0) / 5 = $10,0002. A company has the following transactions for the month of January:- Purchased inventory on credit for $20,000.- Sold inventory on credit for $30,000.- Paid cash for office supplies of $1,000.- Received cash from customers for $25,000.- Paid cash for salaries of $15,000.Prepare the journal entries for these transactions.答案:a) Purchase of inventory on credit:Dr. Inventory $20,000Cr. Accounts Payable $20,000b) Sale of inventory on credit:Dr. Accounts Receivable $30,000Cr. Sales Revenue $30,000c) Payment for office supplies。

英文解释簿记循环流程的含义

英文解释簿记循环流程的含义English:Journalizing a recurring transaction process means recording the same type of transaction on a regular basis. This type of cycle involves capturing the details of transactions such as sales, purchases, or expenses consistently to keep accurate financial records. By following this routine, a company can maintain an organized and efficient system to track its financial activities over time. The journal entries for recurring transactions typically follow a standardized format to ensure consistency and clarity in the accounting records. This process allows businesses to easily identify trends, monitor expenses, analyze cash flow, and make informed decisions based on up-to-date financial information. Implementing a journalizing cycle for recurring transactions also streamlines the reconciliation process, as it creates a systematic approach to recording financial data and reduces the risk of errors or discrepancies in the accounting records.中文翻译:簿记循环流程的含义是定期记录相同类型的交易。

财务英语中英文对照表(部分)

财务英语中英文对照表Aaccount 账户account payable 应付账款accounting system 会计系统Accounting Principle Board (APB) (美国)会计准则委员会accrual basis 权责发生制(应计制)accumulated depreciation 累计折旧account FORMat 账户格式accrue 应计accounting cycle 会计循环accounts receivable 应收账款accounts receivable turnover 应收账款周转率accelerated depreciation 加速折旧adjusting entries 调整分录adjustment 调整aging of accounts receivable 应收账款账龄分析法allowance for bad debts 坏账准备allowance for doubtful accounts 坏账准备allowance for uncollectible 坏账准备allowance method 备抵法allowance for depreciation 折旧备抵账户amortization 摊销annual report 年度报告annuity 年金assets 资产audit 审计auditor’s opinion 审计意见书auditor 审计师audit committee 审计委员会average collection period 平均收账期AICPA 美国注册会计师协会APB Opinions 会计准则委员会意见书Bbalance 余额bad debt recoveries 坏账收回bad debts 坏账bad debts expense 坏账费用balance sheet 资产负债表balance sheet equation 资产负债表等式basket purchase 一揽子采购betterment 改造投资,改造工程投资bearer instrument 不记名票据bonds 债券book of original entry 原始分录账簿book value 账面价值Ccapital 资本capital stock certificate 股本证明书cash basis 收付实现制(现金收付制)cash dividends 现金股利cash flow statement 现金流量表carrying amount 账面价值carrying value 账面价值callable bonds 可赎债券,可提前兑回债券call premium 提前兑回溢价capital lease 资本租赁(指融资租赁)cash discounts 现金折扣cash equivalents 现金等价物capital improvement 资本改造支出capitalized 资本化callable bonds 可赎债券,可提前兑回债券call premium 提前兑回溢价capital lease 资本租赁(指融资租赁)certified public accountant(CPA)注册会计师charge ①费用;②赊账,指赊欠而采用记账的方式;③留置权chart of account 会计科目表closing entries 结账分录closing the books 结账classified balance sheet 分类资产负债表compound interest 复利compound interest method 复利法contingent liability 或有负债contractual rate 合同比率convertible bonds 可兑换债券coupon rate 息票利率covenant 合同条款common stock 普通股compound entry 复合分录corporation 公司cost of goods sold 销售成本cost of sales 销售成本cost recovery 成本收回compound entry 复合分录continuity convention 持续经营惯例contra account 抵减账户contra asset 抵减资产cost—benefit criterion 成本—效益标准compensating balances 补偿性存款额conservatism 稳健性,保守性comparative financial statement 比较财务报表consistency 一致性cost of goods available for sale可供销售的商品成本cost valuation 成本计价consignment 寄销copyright 版权creditor 债权人credit 贷方cross-referencing 对照检录cutoff error 截止错误,截账误差current assets 流动资产current liabilities 流动负债current ratio 流动比率current yield 本期收益率Ddata processing 数据处理过程days to collect account receivable 应收账款收回天数debtor 债务人depreciation 折旧debit 借方deferred credit 递延贷项deferred revenue 递延收入debenture 公司债券debt-to-equity ratio 债务股本比debt—to—total—assets ratio 债务全部资产比deferred charges 递延费用depletion 折耗depreciable value 应计折旧depreciation schedule 折旧计划表discount amortization 债券折价摊销discount on bonds 债券折价discount rates 贴现率disposal value 残值double-entry system 复式记账系统double-declining-balance depreciation (DDB)双倍余额递减法Eearnings 收益(利润)economic life 经济寿命effective—interest amortization 实际利率摊销法effective interest rate 实际利率entity 主体(会计主体)explicit transactions 明计交易expenses费用expenditures 支出Fface amount 票面值FASB Statement 财务会计委员会公告financial accounting 财务会计Financial Accounting Standards Board (FASB) (美国)财务会计准则委员会fiscal year ①会计年度(财务年度);②财政年度financing lease 融资租赁法finished goods inventory 产成品存货fixed assets 固定资产franchises 特许经营权,专营权first—in, first-out(FIFO) 先进先出F.O.B。

财务会计单词表

VOCABULARYaccount.n.帐,帐户;帐单。

vi.讲明;计价。

accountingn.会计;会计学。

accountant.n.会计师;会计人员。

record-keepingn.记录,记账。

certify.vi.证实;执业。

summarizevi汇总;概括。

transaction.n.交易,事项,会计事项,经济业务。

finance.n财政;金融;筹资;融通资金;财务,理财。

vi.筹资;融通资金。

evaluation.n.评价,评估。

auditing.n审计;审计学。

review.vi&n检查;回忆;评论。

measuren量度;量具;措施。

vi.计量。

processn.步骤;工序;过程v.处理;加工。

assumptionn.假设,假定。

accountingentity会计实体。

soleproprietorship独资。

partnershipn合伙。

corporationn股份公司。

goingconcern接着经营。

liquidatevi清理〔破产地企业〕;清偿;往除。

. moneymeasurement货币计量。

inflationn通货膨胀。

deflationn通货紧缩。

accountingperiod会计期间。

financialstatement财务报表historicalcost历史本钞票。

objectivityn客瞧性invoicesn发票;发货单。

physicalcount实地计数。

bias-freeevidence无偏见的证据。

materialityn重要性。

conservationn稳健性,慎重性。

consistencyn一致性,一贯性。

fulldisclosure充分披露matchingn配比性,配合性。

elementn要素。

assetsn资产,财产。

liabilityn负债,债务;责任。

owner’sequity业务权益,所有者权益。

revenuen营业收进。

expensesn费用,支出。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

LIABILITIES

Equipment 5,000

=

Accounts Payable 5,000

OWNER’S EQUITY

13

Business Transactions

c. Feb. 5 received cash of ¥2,000 for providing service to customers

=

OWNER’S EQUITY

15

Business Transactions

c. Feb. 5 received cash of ¥2,000 for providing service to customers

ASSETS

LIABILITIES

Cash 2,000

=

OWNER’S EQUITY

Fees Earned 2,000

29

Business Transactions

h. Feb. 28 paid the following expenses during the month: Utilities, ¥300, and Miscellaneous, ¥200.

ASSETS

LIABILITIES

Cash (500)

=

ASSETS

LIABILITIES

=

OWNER’S EQUITY

11

Business Transactions

b. Feb. 2 purchased equipment (printers, copiers, and fax machine) for ¥5,000 and agreed to pay the supplier in the near future.

16

Business Transactions

d. Feb. 14 paid the part-time assistant ¥1,000 for one month’s wages.

ASSETS

LIABILITIES

=

OWNER’S EQUITY

17

Business Transactions

d. Feb. 14 paid the part-time assistant ¥1,000 for one month’s wages.

7

Business Transactions

a. Feb. 1 opened a business account with a deposit of ¥10,000 from personal funds.

ASSETS LIABILITIES

=

OWNER’S EQUITY

8

Business Transactions

2. Master the accounts used in American accounting.

3. Compare with the process of journalizing in Chinese Accounting that you have learnt.

5

Operations: Print, Copy, Fax, Graphic Designing

ASSETS

LIABILITIES

Cash (1,000)

=

OWNER’S EQUITY

18

Business Transactions

d. Feb. 14 paid the part-time assistant ¥1,000 for one month’s wages.

ASSETS

LIABILITIES

ASSETS

LIABILITIES

Accounts Receivable 6,000

=

OWNER’S EQUITY

Fees Earned 6,000

25

Business Transactions

g. Feb. 27 paid rent on the work place for the month, ¥2,500.

OWNER’S EQUITY

30

Business Transactions

h. Feb. 28 paid the following expenses during the month: Utilities, ¥300, and Miscellaneous, ¥200.

ASSETS

LIABILITIES

ASSETS LIABILITIES

Cash 10,000

=

OWNER’S EQUITY

l 10,000

10

Business Transactions

b. Feb. 2 purchased equipment (printers, copiers, and fax machine) for ¥5,000 and agreed to pay the supplier in the near future.

Principles of

Accounting

TEACHING ARRANGEMENTS

1 2 3

PURPOSES OF THIS BILINGUAL COURSE

MAIN CONTENT OF THIS CLASS

TEACHING (LEARNING) OBJECTIVES

2

PURPOSES OF THIS BILINGUAL COURSE

ASSETS

LIABILITIES

=

OWNER’S EQUITY

14

Business Transactions

c. Feb. 5 received cash of ¥2,000 for providing service to customers

ASSETS

LIABILITIES

Cash 2,000

a. Feb. 1 opened a business account with a deposit of ¥10,000 from personal funds.

ASSETS LIABILITIES

Cash 10,000

=

OWNER’S EQUITY

9

Business Transactions

a. Feb. 1 opened a business account with a deposit of ¥10,000 from personal funds.

6

Brilliant Sunshine A Sole Proprietorship

“ On February 1, 2014, I established a business called Brilliant Sunshine to manage Print&Copy Service. The business progressed smoothly in the first month of operation. Some selected transactions that I completed during the month are as follows.”

ASSETS

LIABILITIES

=

OWNER’S EQUITY

26

Business Transactions

g. Feb. 27 paid rent on the work place for the month, ¥2,500.

ASSETS

LIABILITIES

Cash (2,500)

=

OWNER’S EQUITY

ASSETS

LIABILITIES

Equipment 5,000

=

OWNER’S EQUITY

12

Business Transactions

b. Feb. 2 purchased equipment (printers, copiers, and fax machine) for ¥5,000 and agreed to pay the supplier in the near future.

Business Transactions

h. Feb. 28 paid the following expenses during the month: Utilities, ¥300, and Miscellaneous, ¥200.

ASSETS

LIABILITIES

=

OWNER’S EQUITY

BASIC PURPOSE:

to build a bridge between your English and your specialty

MAIN OBJECTIVES:

to train your reading ability (reading English accounting literature directly), to train your accounting skills in English, and to rethink the accounting knowledge you have learnt.

Cash (1,000)

=

OWNER’S EQUITY

Wages Expense (1,000)

19

Business Transactions

e. Feb. 18 paid creditors on account ¥3,000.

ASSETS

LIABILITIES

=

OWNER’S EQUITY

20

Business Transactions

e. Feb. 18 paid creditors on account ¥3,000.

ASSETS