会计英语课后题

(完整版)会计英语课后习题参考答案解析

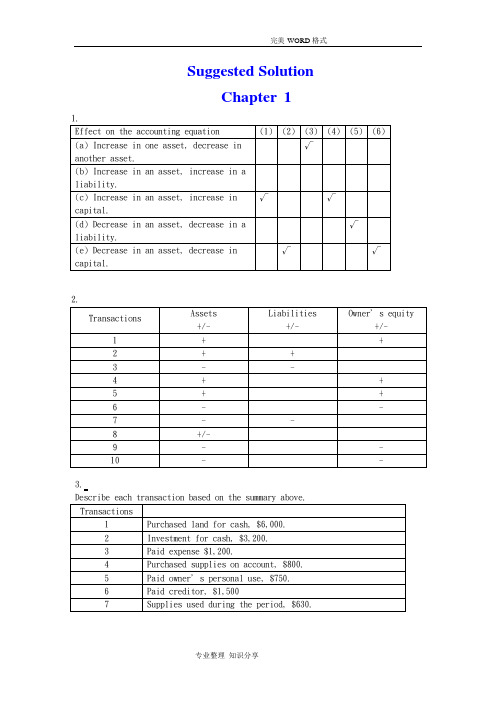

Suggested SolutionChapter 11.3.4.5.(a)(b) net income = 9,260-7,470=1,790(c) net income = 1,790+2,500=4,290Chapter 21.a.To increase Notes Payable -CRb.To decrease Accounts Receivable-CRc.To increase Owner, Capital -CRd.To decrease Unearned Fees -DRe.To decrease Prepaid Insurance -CRf.To decrease Cash - CRg.To increase Utilities Expense -DRh.To increase Fees Earned -CRi.To increase Store Equipment -DRj.To increase Owner, Withdrawal -DR2.a.Cash 1,800Accounts payable ........................... 1,800 b.Revenue ..................................... 4,500Accounts receivable ................... 4,500 c.Owner’s withdrawals ........................ 1,500Salaries Expense ....................... 1,500 d.Accounts Receivable (750)Revenue (750)3.Prepare adjusting journal entries at December 31, the end of the year.Advertising expense 600Prepaid advertising 600Insurance expense (2160/12*2) 360Prepaid insurance 360Unearned revenue 2,100Service revenue 2,100Consultant expense 900Prepaid consultant 900Unearned revenue 3,000Service revenue 3,000 4.1. $388,4002. $22,5203. $366,6004. $21,8005.1. net loss for the year ended June 30, 2002: $60,0002. DR Jon Nissen, Capital 60,000CR income summary 60,0003. post-closing balance in Jon Nissen, Capital at June 30, 2002: $54,000Chapter 31. Dundee Realty bank reconciliationOctober 31, 2009Reconciled balance $6,220 Reconciled balance $6,2202. April 7 Dr: Notes receivable—A company 5400Cr: Accounts receivable—A company 540012 Dr: Cash 5394.5Interest expense 5.5Cr: Notes receivable 5400June 6 Dr: Accounts receivable—A company 5533Cr: Cash 553318 Dr: Cash 5560.7Cr: Accounts receivable—A company 5533Interest revenue 27.73. (a) As a whole: the ending inventory=685(b) applied separately to each product: the ending inventory=6254. The cost of goods available for sale=ending inventory + the cost of goods=80,000+200,000*500%=80,000+1,000,000=1,080,0005.(1) 24,000+60,000-90,000*0.8=12000(2) (60,000+24,000)/( 85,000+31,000)*( 85,000+31,000-90,000)=18828Chapter 41. (a) second-year depreciation = (114,000 – 5,700) / 5 = 21,660;(b) second-year depreciation = 8,600 * (114,000 – 5,700) / 36,100 = 25,800;(c) first-year depreciation = 114,000 * 40% = 45,600second-year depreciation = (114,000 – 45,600) * 40% = 27,360;(d) second-year depreciation = (114,000 – 5,700) * 4/15 = 28,880.2. (a) weighted-average accumulated expenditures (2008) = 75,000 * 12/12 + 84,000 * 9/12 + 180,000 * 8/12 + 300,000 * 7/12 + 100,000 * 6/12 = 483,000(b) interest capitalized during 2008 = 60,000 * 12% + ( 483,000 – 60,000) * 10% =49,5003. (1) depreciation expense = 30,000(2) book value = 600,000 – 30,000 * 2=540,000(3) depreciation expense = ( 600,000 – 30,000 * 8)/16 =22,500(4) book value = 600,000 – 30,000 * 8 – 22,500 = 337,5004. Situation 1:Jan 1st, 2008 Investment in M 260,000Cash 260,000June 30 Cash 6000Dividend revenue 6000Situation 2:January 1, 2008 Investment in S 81,000Cash 81,000June 15 Cash 10,800Investment in S 10,800December 31 Investment in S 25,500Investment Revenue 25,5005. a. December 31, 2008 Investment in K 1,200,000Cash 1,200,000June 30, 2009 Dividend Receivable 42,500Dividend Revenue 42,500December 31, 2009 Cash 42,500Dividend Receivable 42,500 b. December 31, 2008 Investment in K 1,200,000Cash 1,200,000December 31, 2009 Cash 42,500Investment in K 42,500 Investment in K 146,000 Investment revenue 146,000 c. In a, the investment amount is 1,200,000net income reposed is 42,500In b, the investment amount is 1,303,500Net income reposed is 146,000Chapter 51.a. June 1: Dr: Inventory 198,000Cr: Accounts Payable 198,000 June 11: Dr: Accounts Payable 198,000Cr: Notes Payable 198,000 June 12: Dr: Cash 300,000Cr: Notes Payable 300,000b. Dr: Interest Expenses (for notes on June 11) 12,100Cr: Interest Payable 12,100 Dr: Interest Expenses (for notes on June 12) 8,175Cr: Interest Payable 8,175c. Balance sheet presentation:Notes Payable 498,000Accrued Interest on Notes Payable 20,275d. For Green:Dr: Notes Payable 198,000 Interest Payable 12,100Interest Expense 7,700Cr: Cash 217,800For Western:Dr: Notes Payable 300,000Interest Payable 8,175Interest Expense 18,825Cr: Cash 327,0002.(1) 20⨯8 Deferred income tax is a liability 2,400 Income tax payable 21,60020⨯9 Deferred income tax is an asset 600Income tax payable 26,100(2) 20⨯8: Dr: Tax expense 24,000Cr: Income tax payable 21,600 Deferred income tax 2,400 20⨯9: Dr: Tax expense 25,500Deferred income tax 600Cr: Income tax payable 26,100 (3) 20⨯8: Income statement: tax expense 24,000Balance sheet: income tax payable 21,600 20⨯9: Income statement: tax expense 25,500Balance sheet: income tax payable 26,1003.a. 1,560,000 (20000000*12 %* (1-35%))b. 7.8% (20000000*12 %* (1-35%)/20000000)4.5.Notes Payable 14,400 Interest Payable 1,296 Accounts Payable 60,000+Unearned Rent Revenue 7,200 Current Liabilities 82,896Chapter 61. Mar. 1Cash 1,200,000Common Stock 1,000,000Paid-in Capital in Excess of Par Value 200,000Mar. 15Organization Expense 50,000Common Stock 50,000Mar. 23Patent 120,000Common Stock 100,000Paid-in Capital in Excess of Par Value 20,000The value of the patent is not easily determinable, so use the issue price of $12 per share on March 1 which is the issuing price of common stock.2. July.1Treasury Stock 180,000Cash 180,000The cost of treasury purchased is 180,000/30,000=60 per share.Nov. 1Cash 70,000Treasury Stock 60,000Paid-in Capital from Treasury Stock 10,000Sell the treasury at the cost of $60 per share, and selling price is $70 per share. The treasury stock is sold above the cost.Dec. 20Cash 75,000Paid-in Capital from Treasury Stock 15,000Treasury Stock 90,000The cost of treasury is $60 per share while the selling price is $50 which is lower than the cost.3. a. July 1Retained Earnings 24,000Dividends Payable—Preferred Stock 24,000b.Sept.1Dividends Payable—Preferred Stock 24,000Cash 24,000c. Dec.1Retained Earnings 80,000Dividends Payable—Common Stock 80,000d. Dec.31Income Summary 350,000Retained Earnings 350,0004.a. Preferred stock gives its owner certain advantages over common stockholders. These benefits include the right to receive dividends before the common stockholders and the right to receive assets before the common stockholders if the corporation liquidates. Corporation pay a fixed amount of dividends on preferred stock.The 7% cumulative term indicates that the investors earn 7% fixed dividends.b. 7%*120%*20,000=504,000c. If corporation issued debt, it has obligation to repay principald. The date of declaration decrease the stockholders’ equity; the date of record and the date of payment have no effect on stockholders.5.a. Jan. 15Retained Earnings 35,000Accumulated Depreciation 35,000To correct error in prior year’s depreciation.b. Mar. 20Loss from Earthquake 70,000Building 70,000c. Mar. 31Retained Earnings 12,500Dividends Payable 12,500d. Apirl.15Dividends Payable 12,500Cash 12,500e. June 30Retained Earnings 37,500Common Stock 25,000Additional Paid-in Capital 12,500To record issuance of 10% stock dividend: 10%*25,000=2,500 shares;2500*$15=$37,500f. Dec. 31Depreciation Expense 14,000Accumulated Depreciation 14,000Original depreciation: $40,000/40=$10,000 per year. Book value on Jan.1, 2009 is $350,000(=$400,000-5*$10,000). Deprecation for 2009 is $14,000(=$350,000/25). g. The company does not need to make entry in the accounting records. But the amount of Common Stock ($10 par value) decreases 275,000, while the amount of Common Stock ($5 par value) increases 275,000.Chapter 71.Requirement 1If revenue is recognized at the date of delivery, the following journal entries would be used to record the transactions for the two years:Year 1Inventory............................................... 480,000 Cash/Accounts payable ............................... 480,000 To record purchase of inventoryInventory............................................... 124,000 Cash/Accounts payable ............................... 124,000 To record refurbishment of inventoryAccounts receivable ..................................... 310,000 Sales revenue ....................................... 310,000 To record sale of goods on accountCost of goods sold ...................................... 220,000 Inventory ........................................... 220,000 To record the cost of the goods sold as an expenseSales returns (I/S) ..................................... 15,500* Allowance for sales returns (B/S) ................... 15,500 To record provision for return of goods sold under 30-day return period* 5% of $310,000Warranty expense ........................................ 31,000* Provision for warranties (B/S) ...................... 31,000 To record provision, at time of sale, for warranty expenditures* 10% of $310,000Allowance for sales returns ............................. 12,400 Accounts receivable ................................. 12,400 To record return of goods within 30-day return period.It is assumed the returned goods have no value and are disposed of.Provision for warranties (B/S) .......................... 18,600 Cash/Accounts payable ............................... 18,600 To record expenditures in year 1 for warranty workCash ................................................... 297,600*Accounts receivable ................................. 297,600 To record collection of Accounts Receivable* $310,000 – $12,400Year 2Provision for warranties (B/S) .......................... 8,400 Cash/Accounts payable ............................... 8,400 To record expenditures in year 2 for warranty workRequirement 2If revenue is recognized only when the warranty period has expired, the following journal entries would be used to record the transactions for the two years:Year 1Inventory............................................... 480,000 Cash/Accounts payable ............................... 480,000 To record purchase of inventoryInventory............................................... 124,000 Cash/Accounts payable ............................... 124,000 To record refurbishment of inventoryAccounts receivable ..................................... 310,000 Inventory ........................................... 220,000 Deferred gross margin ............................... 90,000 To record sale of goods on accountDeferred gross margin ................................... 12,400 Accounts receivable ................................. 12,400 To record return of goods within the 30-day return period. It is assumed the goods have no value and are disposed of.Deferred warranty costs (B/S) ........................... 18,600 Cash/Accounts payable ............................... 18,600 To record expenditures for warranty work in year 1. The warranty costs incurred are deferred because the related revenue has not yet been recognizedCash ................................................... 297,600* Accounts receivable ................................. 297,600 To record collection of Accounts receivable* $310,000 – $12,400Year 2Deferred warranty costs ................................. 8,400 Cash/Accounts payable ............................... 8,400 To record warranty costs incurred in year 2 related to year 1 sales. The warranty costs incurred are deferred because the related revenue has not yet been recognized.Deferred gross margin ................................... **77,600Cost of goods sold ...................................... 220,000 Sales revenue ....................................... 297,600* To record recognition of sales revenue from year 1 sales and related cost of goods sold at expiry of warranty period* $310,000 – $12,400** ($90,000 – $12,400)Warranty expense ........................................ 27,000* Deferred warranty costs ............................. 27,000 To record recognition of warranty expense at same time as related sales revenue recognition* $18,600 + $8,400Requirement 3Allied Auto Parts Inc. might choose to recognize revenue only after the warranty period has expired if they are not able to make a good estimate, at the time of sale, of the amount of warranty work that will be required under the terms of the one-year warranty. If Allied is not able, at the time of sale, to make a good estimate of the warranty work that will be required, then the measurability criterion of revenue recognition is not met at the time of sale. The measurability criterion means that the amount of revenue can be reliably measured. If the seller is not able to estimate the amount of work that will have to be done under the warranty agreement, then it is not able to reasonably measure the profit that it will eventually earn on the sales. The performance criteria might also be invoked here. The performancecriterion means that the seller has transferred the significant risks and rewards of ownership to the buyer. As long as there is warranty work to be performed after the sale that is the responsibility of the seller, you might argue that performance is not substantially complete. However, if the seller was able to reliably estimate the amount of warranty work, then performance would be satisfied on the assumption that we could measure the risk that remains with the seller, and make a provision for it.2.Percentage-of-completion method:The first step in applying revenue recognition using the percentage-of-completion method (using costs incurred to date compared to estimated total costs to determinethe percentage of completion) is to estimate the percentage of completion of the project at the end of each year. This is done in the following table (in $000s):End of 2005 End of 2006 End of 2007Total costs incurred $ 5,400 $ 12,950 $ 18,800 Total estimated costs 18,000 18,500 18,800 % completed 30% 70% 100%Once the percentage of completion at the end of each year has been calculated as above, the next step is to allocate the appropriate amount of revenue to each year, based on the percentage completed to date, less what has previously been recordedin revenue. This is done in the following table (in $000s):2005 2006 20072005 $20,000 × 30%$ 6,0002006 $20,000 × 70%$ 14,0002007 $20,000 × 100%$ 20,000 Less: Revenue recognized in prior years (0) (6,000) (14,000) Revenue for year $ 6,000 $ 8,000 $ 6,000Therefore, the profit to be recognized each year on the construction project would be:2005 2006 2007 TotalRevenue recognized $ 6,000 $ 8,000 $ 6,000 $ 20,000 Construction costs incurred (expenses) (5,400) (7,550) (5,850) (18,800) Gross profit for the year $ 600 $ 450 $ 150 $ 1,200The following journal entries are used to record the transactions under the percentage-of-completion method of revenue recognition:2005 2006 20071. Costs of construction:Construction in progress ....... 5,400 7,550 5,850 Cash, payables, etc. 5,400 7,550 5,850 2. Progress billings:Accounts receivable ..... 3,100 4,900 12,000 Progress billings ... 3,100 4,900 12,000 3. Collections on billings:Cash .................... 2,400 4,000 12,400 Accounts receivable . 2,400 4,000 12,400 4. Recognition of profit:Construction in progress 600 450 150Construction expense .... 5,400 7,550 5,850 Revenue from long-termcontract .......... 6,000 8,000 6,000 5. To close construction in progress:Progress billings ....... 20,000 Construction in progress 20,0002005 2006 2007Balance sheetCurrent assets:Accounts receivable $ 700 $ 1,600 $ 1,200 Inventory:Construction in process 6,000 14,000Less: Progress billings (3,100) (8,000)Costs in excess of billings 2,900 6,000Income statementRevenue from long-term contracts $ 6,000 $ 8,000 $ 6,000 Construction expense (5,400) (7,550) (5,850) Gross profit $ 600 $ 450 $ 1503.a. The three criteria of revenue recognition are performance, measurability, andcollectibility.Performance means that the seller or service provider has performed the work.Depending on the nature of the product or service, performance may mean quitedifferent points of revenue recognition. For example, for the sale of products,IAS18 defines performance as the point when the seller of the goods hastransferred the risks and rewards of ownership to the buyer. Normally, this meansthat performance is done at the time of sale. Although the seller may haveperformed much of the work prior to the sale (production, selling efforts, etc.),there is still significant risk to the seller that a buyer may not be found.Therefore, from a reliability point of view, revenue recognition is delayed untilthe point of sale. Also, there may be significant risks remaining with the sellerof the product even after the sale. Warranties given by the seller are a riskthat remains with the seller. However, if this risk can be reliably estimatedat the time of sale, revenue can be recognized at the point of sale. Performanceis quite different under a long-term construction contract. Here, performancereally is considered to be a measure of the work done. Revenue is recognizedover the production period as the work is performed. It is intended to reflectthe amount of effort expended by the seller (contractor). Although legal titlewon’t transfer to the buyer until the project is completed, revenue can berecognized because there is a known and committed buyer. If the contractor is not able to estimate how much of the work has been done (perhaps because he or she can’t reliably estimate how much work must still be done), then profit would not be recognized until the extent of performance is known.Measurability means that the seller or service provider must be able to reliably estimate the amount of the revenue from the sale or service. For the sale of products this is generally known at the time of sale (the sales price is set).However, if the seller provides a return period, it may be necessary to estimate the volume of returns at the time of sale in order to measure the revenue that will be recognized.Collectibility means that the seller or the service provider has reasonable assurance that the sales price will actually be collected. In most cases for the sales of products, the seller is able to recognize revenue at the time of sale even if the sale is on account. This is because the seller has experience with its customers and is able to estimate reliably the risk of non payment.As long as the seller is able to make this estimate, it is appropriate to recognize the revenue but to offset it with a provision for possible non collection. If the seller is unable to make reliable estimates of future collection of amounts owing, the recognition of revenue would be delayed until the cash is actually received. This is what is done using the instalment sales method of revenue recognition.b. Because of the performance criterion of revenue recognition, it would seem to be most appropriate to recognize most revenue as the seller or service provider performs the work. This would be the best measure of performance. This would mean, for example, that sellers of products would recognize their revenue over the whole production, selling, and post sales servicing periods. As we saw above, this is not commonly done because, in many cases, there are still significant risks that are retained by the seller (risk of not being able to sell the product, for example). There are also measurement risks (knowing the selling price) that exist prior to the sale. The percentage-of-completion method of revenue used for some long-term construction contracts would seem to most closely recognize revenue as the work is performed. As mentioned in Part 1, we are able to recognize revenue on this basis since a contract exists which commits the purchaser to buy the project (assuming certain conditions are met) and the sales price is known because of the existence of the contract.4.If all revenue is recognized when a student registers for the course, profit for 2007 would be:Sales Revenue1:Manuals and initial lessons (200 × $100)$ 20,000 Additional lessons ((200 × 8) × $30)48,000 Examinations ((200 × 80%) × $130)20,800 Total sales revenue 88,800Cost of sales:Manuals and initial lessons (200 × ($15 + $3))3,600 Additional lessons ((200 × 8) × $3))4,800 Examinations ((200 × 80%) × $30)4,800 Total cost of sales 13,200Depreciation of development costs:$180,000 × (200/1,000)36,000Profit $ 39,6005.FINISH ENTERPRISESIncome Statementfor the year ending December 31, 2005Continuing operations (excluding the chemical division)Sales ($35,000,000 – $5,500,000) $ 29,500,000Cost of sales ($15,000,000 – $2,800,000) (12,200,000)Gross profit 17,300,000Selling & administration expenses($18,000,000 – $3,200,000) (14,800,000)Profit from operations 2,500,000Income tax expense (40%) 1,000,000Profit after tax $ 1,500,000Discontinuing operations (Chemical division)Sales 5,500,000Cost of sales (2,800,000)Gross profit 2,700,000Selling & administration expenses (3,200,000)Loss from operations (500,000)Income tax expense(40%) 200,000Loss after tax (300,000) Gain on discontinuance of the Chemical division 3,500,000Tax thereon (1,400,000)After-tax gain on discontinuance of the Chemical division2,100,000$ 3,300,000Chapter 81.Payment of account payable. operatingIssuance of preferred stock for cash. financingPayment of cash dividend. financingSale of long-term investment. investingAmortization of bond discount. no effectCollection of account receivable. operatingIssuance of long-term note payable to borrow cash. financing Depreciation of equipment. no effectPurchase of treasury stock. financingIssuance of common stock for cash. financingPurchase of long-term investment. investingPayment of wages to employees. operatingCollection of cash interest. investingCash sale of land. InvestingDistribution of stock dividend. no effectAcquisition of equipment by issuance of note payable. no effect Payment of long-term debt. financingAcquisition of building by issuance of common stock. no effect Accrual of salary expense. no effect2.(a) Cash received from customers = 816,000(b) Cash payments for purchases of merchandise. =468,000(c) Cash payments for operating expenses. = 268,200(d) Income taxes paid. =36,9003.Cash sales …………………………………………... $9,000 Payment of accounts payable ………………………. -48,000Payment of income tax ………………………………-13,000Payment of interest ……………………………..…..-16,000 Collection of accounts receivable ……………………93,000 Payment of salaries and wages ………………………..-34,000 Cash flows from operating activitiesby the direct method -9,0004.Operating activities:Net loss -200,000 Add: loss on sale of land 250,000 Add: depreciation 300,000Add: amortization of patents 20,000Less: increases in current assets other than cash -750,000 Add: increases in current liabilities 180,000 Net cash flows from operating-200,000Investing activitiesSale of land -50,000 Purchase of PPE -1,500,000Net cash flows from investing-1,550,000Financing activitiesIssuance of common shares 400,000 Payment of cash dividend -50,000 Issuance of non-current liabilities 1,000,000 Net cash flows from financing1,350,000Net changes in cash-400,0005.。

会计英语课后习题参考答案解析(可编辑修改word版)

Suggested SolutionChapter 12.3.Describe each transaction based on the summary above.4.5.(a)(b) net income = 9,260-7,470=1,790(c) net income = 1,790+2,500=4,290Chapter 21.a.To increase Notes Payable -CRb.To decrease Accounts Receivable-CRc.To increase Owner, Capital -CRd.To decrease Unearned Fees -DRe.To decrease Prepaid Insurance -CRf.To decrease Cash - CRg.To increase Utilities Expense -DRh.To increase Fees Earned -CRi.To increase Store Equipment -DRj.To increase Owner, Withdrawal -DR2.a.Cash 1,800Accounts payable ............................ 1,800 b.Revenue ......................................Accounts receivable ....................c. 4,5004,500Owner’s withdrawals........................ 1,500Salaries Expense ....................... 1,500d.Accounts Receivable (750)Revenue (750)3.Prepare adjusting journal entries at December 31, the end of the year.Advertising expense 600Prepaid advertising 600Insurance expense (2160/12*2) 360Prepaid insurance 360Unearned revenue Service revenue 2,1002,100Consultant expense Prepaid consultant 9009004. Unearned revenueService revenue3,0003,0001. $388,4002. $22,5203. $366,6004. $21,8005.1. net loss for the year ended June 30, 2002: $60,0002. DR Jon Nissen, Capital 60,000CR income summary 60,0003. post-closing balance in Jon Nissen, Capital at June 30, 2002: $54,000Chapter 31.Dundee Realty bank reconciliationOctober 31, 2009Reconciled balance $6,220 Reconciled balance $6,2202.April 7 Dr: Notes receivable—A company 5400Cr: Accounts receivable—A company 540012 Dr: Cash 5394.5Interest expense 5.5Cr: Notes receivable 5400June 6 Dr: Accounts receivable—A company 5533Cr: Cash 553318 Dr: Cash 5560.7Cr: Accounts receivable—A company 5533Interest revenue 27.73.(a) As a whole: the ending inventory=685(b)applied separately to each product: the ending inventory=6254.The cost of goods available for sale=ending inventory + the cost of goods=80,000+200,000*500%=80,000+1,000,000=1,080,0005.(1) 24,000+60,000-90,000*0.8=12000(2) (60,000+24,000)/( 85,000+31,000)*( 85,000+31,000-90,000)=18828Chapter 41. (a) second-year depreciation = (114,000 – 5,700) / 5 = 21,660;(b) second-year depreciation = 8,600 * (114,000 – 5,700) / 36,100 = 25,800;(c)first-year depreciation = 114,000 * 40% = 45,600second-year depreciation = (114,000 – 45,600) * 40% = 27,360;(d) second-year depreciation = (114,000 – 5,700) * 4/15 = 28,880.2.(a) weighted-average accumulated expenditures (2008) = 75,000 * 12/12 + 84,000 * 9/12 + 180,000 * 8/12 + 300,000 * 7/12 + 100,000 * 6/12 = 483,000 (b) interest capitalized during 2008 = 60,000 * 12% + ( 483,000 – 60,000) * 10% =49,5003.(1) depreciation expense = 30,000(2) book value = 600,000 – 30,000 * 2=540,000(3) depreciation expense = ( 600,000 – 30,000 * 8)/16 =22,500(4) book value = 600,000 – 30,000 * 8 – 22,500 = 337,5004.Situation 1:Jan 1st, 2008 Investment in M 260,000Cash 260,000June 30 Cash 6000Dividend revenue 6000Situation 2:January 1, 2008 Investment in S 81,000Cash 81,000June 15 Cash 10,800Investment in S 10,800December 31 Investment in S 25,500Investment Revenue 25,5005.a. December 31, 2008 Investment in K 1,200,000Cash 1,200,000June 30, 2009 Dividend Receivable 42,500Dividend Revenue 42,500December 31, 2009 Cash 42,500Dividend Receivable 42,500 b. December 31, 2008 Investment in K 1,200,000Cash 1,200,000 December 31, 2009 Cash42,500Investment in K 42,500Investment in K 146,000Investment revenue 146,000 c. In a, the investment amount is 1,200,000net income reposed is 42,500In b, the investment amount is 1,303,500Net income reposed is 146,000Chapter 51.a. June 1: Dr: Inventory198,000 Cr: Accounts Payable198,000 June 11: Dr: Accounts Payable198,000Cr: Notes Payable198,000 June 12: Dr: Cash300,000Cr: Notes Payable300,000 b. Dr: Interest Expenses (for notes on June 11) 12,100 Cr: Interest Payable12,100 Dr: Interest Expenses (for notes on June 12) 8,175 Cr: Interest Payable8,175 c. Balance sheet presentation:dFor Western: Dr: Notes Payable 300,000 Interest Payable 8,175 Interest Expense 18,825Cr: Cash 327,0002.(1) 20⨯8 Deferred income tax is a liability2,400Income tax payable21,600 20⨯9 Deferred income tax is an asset600 Income tax payable 26,100 (2) 20⨯8: Dr: Tax expense24,000Cr: Income tax payable 21,600 Deferred income tax2,400 20⨯9: Dr: Tax expense25,500 Deferred income tax 600Cr: Income tax payable 26,100 (3) 20⨯8: Income statement: tax expense24,000 Balance sheet: income tax payable21,600 20⨯9: Income statement: tax expense25,500 Balance sheet: income tax payable 26,1003.a. 1,560,000 (20000000*12 %* (1-35%))Notes Payable498,000 Accrued Interest on Notes Payable20,275 . For Green:Dr: Notes Payable198,000 Interest Payable12,100 Interest Expense 7,700 Cr: Cash 217,800b. 7.8% (20000000*12 %* (1-35%)/20000000)4.5.Notes Payable 14,400 Interest Payable 1,296 Accounts Payable 60,000+Unearned Rent Revenue 7,200 Current Liabilities 82,896Chapter 61.Mar. 1Cash 1,200,000Common Stock 1,000,000Paid-in Capital in Excess of Par Value 200,000Mar. 15Organization Expense 50,000Common Stock 50,000Mar. 23Patent 120,000Common Stock 100,000Paid-in Capital in Excess of Par Value 20,000 The value of the patent is not easily determinable, so use the issue price of $12 per share on March 1 which is the issuing price of common stock.2.July.1Treasury Stock 180,000Cash 180,000The cost of treasury purchased is 180,000/30,000=60 per share.Nov. 1Cash 70,000Treasury Stock 60,000Paid-in Capital from Treasury Stock 10,000Sell the treasury at the cost of $60 per share, and selling price is $70 per share. The treasury stock is sold above the cost.Dec. 20Cash 75,000Paid-in Capital from Treasury Stock 15,000Treasury Stock 90,000The cost of treasury is $60 per share while the selling price is $50 which is lower than the cost.3.a. July 1Retained Earnings 24,000Dividends Payable—Preferred Stock 24,000b.Sept.1Dividends Payable—Preferred Stock 24,000Cash 24,000c. Dec.1Retained Earnings 80,000Dividends Payable—Common Stock 80,000d.Dec.31Income Summary 350,000Retained Earnings 350,0004.a. Preferred stock gives its owner certain advantages over common stockholders. These benefits include the right to receive dividends before the common stockholders and the right to receive assets before the common stockholders if the corporation liquidates. Corporation pay a fixed amount of dividends on preferred stock.The 7% cumulative term indicates that the investors earn 7% fixed dividends.b. 7%*120%*20,000=504,000c. If corporation issued debt, it has obligation to repay principald. The date of dec laration decrease the stockholders’ equity; the date of record and the date of payment have no effect on stockholders.5.a. Jan. 15Retained Earnings 35,000Accumulated Depreciation 35,000 To correct error in prior year’s depreciation.b. Mar. 20Loss from Earthquake 70,000Building 70,000c. Mar. 31Retained Earnings 12,500Dividends Payable 12,500d. Apirl.15Dividends Payable 12,500Cash 12,500e. June 30Retained Earnings 37,500Common Stock 25,000Additional Paid-in Capital 12,500To record issuance of 10% stock dividend: 10%*25,000=2,500 shares;2500*$15=$37,500f. Dec. 31Depreciation Expense 14,000Accumulated Depreciation 14,000Original depreciation: $40,000/40=$10,000 per year. Book value on Jan.1, 2009 is $350,000(=$400,000-5*$10,000). Deprecation for 2009 is $14,000(=$350,000/25).g. The company does not need to make entry in the accounting records. But the amount of Common Stock ($10 par value) decreases 275,000, while the amount of Common Stock ($5 par value) increases 275,000.Chapter 71.Requirement 1If revenue is recognized at the date of delivery, the following journal entries would be used to record the transactions for the two years:Year 1Inventory ............................................... 480,000 Cash/Accounts payable................................ 480,000 To record purchase of inventoryInventory ............................................... 124,000 Cash/Accounts payable................................ 124,000 To record refurbishment of inventoryAccounts receivable ..................................... 310,000 Sales revenue........................................ 310,000 To record sale of goods on accountCost of goods sold ...................................... 220,000 Inventory............................................ 220,000 To record the cost of the goods sold as an expenseSales returns (I/S) ..................................... 15,500* Allowance for sales returns (B/S).................... 15,500 To record provision for return of goods sold under 30-day return period* 5% of $310,000Warranty expense ........................................ 31,000* Provision for warranties (B/S)....................... 31,000 To record provision, at time of sale, for warranty expenditures* 10% of $310,000Allowance for sales returns ............................. 12,400 Accounts receivable.................................. 12,400 To record return of goods within 30-day return period.It is assumed the returned goods have no value and are disposed of.Provision for warranties (B/S) ..........................Cash/Accounts payable................................ 18,60018,600To record expenditures in year 1 for warranty workCash .................................................... 297,600*Accounts receivable.................................. 297,600 To record collection of Accounts Receivable* $310,000 – $12,400Year 2Provision for warranties (B/S) .......................... 8,400 Cash/Accounts payable................................ 8,400 To record expenditures in year 2 for warranty workRequirement 2If revenue is recognized only when the warranty period has expired, thefollowing journal entries would be used to record the transactions for the two years:Year 1Inventory ...............................................Cash/Accounts payable................................ To record purchase of inventory 480,000480,000Inventory ...............................................Cash/Accounts payable................................ To record refurbishment of inventory 124,000124,000Accounts receivable .....................................Inventory............................................ 310,000220,000Deferred gross margin................................To record sale of goods on account90,000Deferred gross margin ...................................Accounts receivable.................................. 12,40012,400To record return of goods within the 30-day return period.goods have no value and are disposed of.It is assumed theDeferred warranty costs (B/S) ........................... 18,600 Cash/Accounts payable................................ 18,600 To record expenditures for warranty work in year 1. The warranty costs incurred are deferred because the related revenue has not yet been recognizedCash .................................................... 297,600* Accounts receivable.................................. 297,600 To record collection of Accounts receivable* $310,000 – $12,400Year 2Deferred warranty costs ................................. 8,400 Cash/Accounts payable................................ 8,400 To record warranty costs incurred in year 2 related to year 1 sales. Thewarranty costs incurred are deferred because the related revenue has not yet been recognized.Deferred gross margin ................................... **77,600Cost of goods sold ...................................... 220,000 Sales revenue........................................ 297,600* To record recognition of sales revenue from year 1 sales and related cost of goods sold at expiry of warranty period* $310,000 – $12,400** ($90,000 – $12,400)Warranty expense ........................................ 27,000* Deferred warranty costs.............................. 27,000 To record recognition of warranty expense at same time as related sales revenue recognition* $18,600 + $8,400Requirement 3Allied Auto Parts Inc. might choose to recognize revenue only after thewarranty period has expired if they are not able to make a good estimate, at the time of sale, of the amount of warranty work that will be required under the terms of the one-year warranty. If Allied is not able, at the time of sale, to make a good estimate of the warranty work that will be required, then the measurability criterion of revenue recognition is not met at the time of sale.The measurability criterion means that the amount of revenue can be reliably measured. If the seller is not able to estimate the amount of work that will have to be done under the warranty agreement, then it is not able to reasonably measure the profit that it will eventually earn on the sales. The performance criteria might also be invoked here. The performance criterion means that the seller has transferred the significant risks and rewards of ownership to the buyer. As long as there is warranty work to be performed after the sale that is the responsibility of the seller, you might argue that performance is notsubstantially complete. However, if the seller was able to reliably estimate the amount of warranty work, then performance would be satisfied on theassumption that we could measure the risk that remains with the seller, andmake a provision for it.2.Percentage-of-completion method:The first step in applying revenue recognition using the percentage-of-completion method (using costs incurred to date compared to estimated totalcosts to determine the percentage of completion) is to estimate the percentageof completion of the project at the end of each year. This is done in thefollowing table (in $000s):End of 2005 End of 2006 End of 2007Total costs incurred $ 5,400 $ 12,950 $ 18,800 Total estimated costs 18,000 18,500 18,800 % completed 30% 70% 100%Once the percentage of completion at the end of each year has been calculatedas above, the next step is to allocate the appropriate amount of revenue toeach year, based on the percentage completed to date, less what has previously been recorded in revenue. This is done in the following table (in $000s):2005 2006 20072005 $20,000 × 30% $ 6,0002006 $20,000 × 70% $ 14,0002007 $20,000 × 100% $ 20,000Less: Revenue recognized in prior years (0) (6,000) (14,000) Revenue for year $ 6,000 $ 8,000 $ 6,000Therefore, the profit to be recognized each year on the construction projectwould be:2005 2006 2007 TotalRevenue recognized $ 6,000 $ 8,000 $ 6,000 $ 20,000 Construction costs incurred (expenses) (5,400) (7,550) (5,850) (18,800) Gross profit for the year $ 600 $ 450 $ 150 $ 1,200The following journal entries are used to record the transactions under the percentage-of-completion method of revenue recognition:2005 2006 20071. Costs of construction:Construction in progress ....... 5,400 7,550 5,850 Cash, payables, etc. . 5,400 7,550 5,8502. Progress billings:Accounts receivable ..... 3,100 4,900 12,000 Progress billings .... 3,100 4,900 12,000 3. Collections on billings:Cash .................... 2,400 4,000 12,400 Accounts receivable .. 2,400 4,000 12,400 4. Recognition of profit:Construction in progress 600 450 150Construction expense .... 5,400 7,550 5,850Revenue from long-termcontract ........... 6,000 8,000 6,0005.To close construction in progress:Progress billings ....... 20,000Construction in progress 20,0002005 2006 2007Balance sheetCurrent assets:Accounts receivable $ 700 $ 1,600 $ 1,200 Inventory:Construction in process 6,000 14,000Less: Progress billings (3,100) (8,000)Costs in excess of billings 2,900 6,000Income statementRevenue from long-term contracts $ 6,000 $ 8,000 $ 6,000 Construction expense (5,400) (7,550) (5,850) Gross profit $ 600 $ 450 $ 1503.a.The three criteria of revenue recognition are performance, measurability,and collectibility.Performance means that the seller or service provider has performed thework. Depending on the nature of the product or service, performance maymean quite different points of revenue recognition. For example, for thesale of products, IAS18 defines performance as the point when the seller ofthe goods has transferred the risks and rewards of ownership to the buyer.Normally, this means that performance is done at the time of sale. Althoughthe seller may have performed much of the work prior to the sale(production, selling efforts, etc.), there is still significant risk to theseller that a buyer may not be found. Therefore, from a reliability pointof view, revenue recognition is delayed until the point of sale. Also,there may be significant risks remaining with the seller of the producteven after the sale. Warranties given by the seller are a risk that remainswith the seller. However, if this risk can be reliably estimated at thetime of sale, revenue can be recognized at the point of sale. Performanceis quite different under a long-term construction contract. Here,performance really is considered to be a measure of the work done. Revenue is recognized over the production period as the work is performed. It is intended to reflect the amount of effort expended by the seller(contractor). Although legal title won’t transfer to the buyer until the project is completed, revenue can be recognized because there is a known and committed buyer. If the contractor is not able to estimate how much of the work has been done (perhaps because he or she can’t reliably estimate how much work must still be done), then profit would not be recognizeduntil the extent of performance is known.Measurability means that the seller or service provider must be able toreliably estimate the amount of the revenue from the sale or service. For the sale of products this is generally known at the time of sale (the sales price is set). However, if the seller provides a return period, it may be necessary to estimate the volume of returns at the time of sale in order to measure the revenue that will be recognized.Collectibility means that the seller or the service provider has reasonable assurance that the sales price will actually be collected. In most cases for the sales of products, the seller is able to recognize revenue at the time of sale even if the sale is on account. This is because the seller has experience with its customers and is able to estimate reliably the risk of non payment. As long as the seller is able to make this estimate, it isappropriate to recognize the revenue but to offset it with a provision for possible non collection. If the seller is unable to make reliable estimates of future collection of amounts owing, the recognition of revenue would be delayed until the cash is actually received. This is what is done using the instalment sales method of revenue recognition.b.Because of the performance criterion of revenue recognition, it would seem to be most appropriate to recognize most revenue as the seller or service provider performs the work. This would be the best measure of performance. This would mean, for example, that sellers of products would recognize their revenue over the whole production, selling, and post sales servicing periods. As we saw above, this is not commonly done because, in many cases, there are still significant risks that are retained by the seller (risk of not being able tosell the product, for example). There are also measurement risks (knowing the selling price) that exist prior to the sale. The percentage-of-completion method of revenue used for some long-term construction contracts would seem to most closely recognize revenue as the work is performed. As mentioned in Part 1, we are able to recognize revenue on this basis since a contract exists which commits the purchaser to buy the project (assuming certain conditions are met) and the sales price is known because of the existence of the contract.4.If all revenue is recognized when a student registers for the course, profit for 2007 would be:Sales Revenue1:Manuals and initial lessons (200 × $100)$ 20,000 Additional lessons ((200 × 8) × $30)48,000 Examinations ((200 × 80%) × $130) 20,800 Total sales revenue 88,800Cost of sales:Manuals and initial lessons (200 × ($15+ $3)) 3,600 Additional lessons ((200 × 8) × $3))4,800 Examinations ((200 × 80%) × $30) 4,800 Total cost of sales 13,200Depreciation of development costs:$180,000 × (200/1,000) 36,000 Profit $ 39,6005.FINISH ENTERPRISESIncome Statementfor the year ending December 31, 2005Continuing operations (excluding the chemical division)Sales ($35,000,000 – $5,500,000) $ 29,500,000Cost of sales ($15,000,000 – $2,800,000) (12,200,000)Gross profit 17,300,000Selling & administration expenses($18,000,000 – $3,200,000) (14,800,000)Profit from operations 2,500,000Income tax expense (40%) 1,000,000Profit after tax $ 1,500,000Discontinuing operations (Chemical division)Sales 5,500,000Cost of sales (2,800,000)Gross profit 2,700,000Selling & administration expenses (3,200,000)Loss from operations (500,000)Income tax expense(40%) 200,000Loss after tax (300,000) Gain on discontinuance of the Chemical division 3,500,000Tax thereon (1,400,000)After-tax gain on discontinuance of the Chemical division2,100,000Enterprise net profit $3,300,000Chapter 81.Payment of account payable. operatingIssuance of preferred stock for cash. financingPayment of cash dividend. financingSale of long-term investment. investingAmortization of bond discount. no effectCollection of account receivable. operatingIssuance of long-term note payable to borrow cash. financing Depreciation of equipment. no effectPurchase of treasury stock. financingIssuance of common stock for cash. financingPurchase of long-term investment. investingPayment of wages to employees. operatingCollection of cash interest. investingCash sale of land. InvestingDistribution of stock dividend. no effectAcquisition of equipment by issuance of note payable. no effect Payment of long-term debt. financingAcquisition of building by issuance of common stock. no effect Accrual of salary expense. no effect2.(a)Cash received from customers = 816,000(b)Cash payments for purchases of merchandise. =468,000(c)Cash payments for operating expenses. = 268,200(d)Income taxes paid. =36,9003.Cash sales..................................... $9,000Payment of accounts payable ………………………. -48,000Payment of income tax ……………………………… -13,000Payment of inter est ……………………………..….. -16,000 Collection of accounts receivable .................. 93,000 Payment of salaries and wages ………………………..-34,000 Cash flows from operating activitiesby the direct method -9,0004.Operating activities:Net loss -200,000 Add: loss on sale of land 250,000 Add: depreciation 300,000Add: amortization of patents 20,000Less: increases in current assets other than cash -750,000 Add: increases in current liabilities 180,000 Net cash flows from operating - 200,000Investing activitiesSale of land -50,000 Purchase of PPE -1,500,000Net cash flows from investing - 1,550,000Financing activitiesIssuance of common shares 400,000 Payment of cash dividend -50,000 Issuance of non-current liabilities 1,000,000 Net cash flows from financing1,350,000Net changes in cash - 400,0005.。

会计英语课后题

Unlimited liability is an advantage of a sole proprietorship. ×A sole proprietorship is a business owned by one or more persons. ×As a general rule, revenues should not be recognized in the accounting records until it is received in cash. ×In the partnership form of business, the owners are called stockholders. ×The area of accounting aimed at serving the decision making needs of internal users is:A Financial accounting.B Managerial accounting.C External auditing.D SEC reporting.E Bookkeeping.The accounting concept that requires financial statement information to be supported by independent, unbiased evidence other than someone's belief or opinion is:A Business entity assumption.B Monetary unit assumption.C Going-concern assumption.D Time-period assumption.E ObjectivityExternal users of accounting information include all of the following except:A Shareholders.B Customers.C Purchasing managers.D Government regulators.E Creditors.The accounting assumption that requires every business to be accounted for separately from other business entities, including its owner or owners is known as the:A Time-period assumption.B Business entity assumption.C Going-concern assumption.D Revenue recognition principle.E Cost principle.If a parcel of land that was originally acquired for $85,000 is offered for sale at $150,000, is assessed for tax purposes at $95,000, is recognized by its purchasers as easily being worth $140,000, and is sold for $137,000, the land should be recorded in the purchaser's books at:A $95,000.B $137,000.C $138,500.D $140,000.E $150,000.The Maxim Company acquired a building for $500,000. Maxim had the building appraised, and found that the building was easily worth $575,000. The seller had paid $300,000 for the building 6 years ago. Which accounting principle would require Maxim to record the building on its records at $500,000?A Monetary unit assumption.B Going-concern assumption.C Cost principle.D Business entity assumption.E Revenue recognition principle.If the liabilities of a business increased $75,000 during a period of time and the owner's equity in the business decreased $30,000 during the same period, the assets of the business must have:A Decreased $105,000.B Decreased $45,000.C Increased $30,000.D Increased $45,000.E Increased $105,000.If the assets of a business increased $89,000 during a period of time and its liabilities increased $67,000 during the same period, equity in the business must have:A Increased $22,000.B Decreased $22,000.C Increased $89,000.D Decreased $156,000.E Increased $156,000. If a company paid $38,000 of its accounts payable in cash, what was the effect on the assets, liabilities, and equity?A Assets would decrease $38,000, liabilities would decrease $38,000, and equity would decrease $38,000.B Assets would decrease $38,000, liabilities would decrease $38,000, and equity would increase $38,000.C Assets would decrease $38,000, liabilities would decrease $38,000, and equity would not change.D There would be no effect on the accounts because the accounts are affected by the same amount.E None of these.How would the accounting equation of Boston Company be affected by the billing of a client for $10,000 of consulting work completed?A +$10,000 accounts receivable, -$10,000 accounts payable.B +$10,000 accounts receivable, +$10,000 accounts payable.C +$10,000 accounts receivable, +$10,000 cash.D +$10,000 accounts receivable, +$10,000 revenue.E +$10,000 accounts receivable, -$10,000 revenueAssets created by selling goods and services on credit are:A Accounts payable.B Accounts receivable.C Liabilities.D Expenses.E Equity.On June 30 of the current year, the assets and liabilities of Phoenix, Inc. are as follows: Cash $20,500; Accounts Receivable, $7,250; Supplies, $650; Equipment, $12,000; Accounts Payable, $9,300. What is the amount of owner's equity as of June 30 of the current year?A $8,300B $13,050C $20,500D $31,100E $40,400The excess of expenses over revenues for a period is:A Net assets.B Equity.C Net loss.D Net income.E A liability.The accounting equation implies that: Assets + Liabilities = Equity.×owner's equity are the owner's claim on assets.√Increases in liability accounts are recorded as debits.×Crediting an expense account decreases it.√If insurance coverage for the next three years is paid for in advance, the amount of the payment is debited to an asset account called Prepaid Insurance.√The purchase of supplies on credit should be recorded with a debit to Supplies and a credit to Accounts Payable.√If a company provides services to a customer on credit the selling company should credit Accounts Receivable.×A record of the increases and decreases in a specific asset, liability, equity, revenue, or expense is a(n):A Journal.B Posting.C Trial balance.D Account.E Chart of accounts. Which of the following statements is correct?A When a future expense is paid in advance, the payment is normally recorded in a liability account called Prepaid Expense.B Promises of future payment by the buyer are called accounts receivable.C Increases and decreases in cash are always recorded in the owner's capital account.D An account called Land is commonly used to record increases and decreases in both the land and buildings owned by a business.E Accrued liabilities include accounts receivable.Prepaid expenses are:A Payments made for products and services that do not ever expire.B Classified as liabilities on the balance sheet.C Decreases in equity.D Assets that represent prepayments of future expenses.E Promises of payments by customers.A debit:A Always increases an account.B Is the right-hand side of a T-account.C Always decreases an account.D Is the left-hand side of a T-account.E Is not need to record a transaction.Which of the following statements is incorrect?A The normal balance of accounts receivable is a debit.B The normal balance of owner's withdrawals is a debit.C The normal balance of unearned revenues is a credit.D The normal balance of an expense account is a credit.E The normal balance of the owner's capital account is a credit.The first step in the processing of a transaction is to analyze the transaction and source documents.√Preparation of a trial balance is the first step in the analyzing and recording process.×Source documents provide evidence of business transactions and are the basis for accounting entries.√A revenue account normally has a debit balance.×Accounts are normally decreased by debits.×All of the following statements regarding a sales invoice are true except:A A sales invoice is a type of source document.B A sales invoice is used by sellers to record the sale.C A sales invoice is used by buyers to record purchases.D A sales invoice gives rise to an entry in the accounting process.E A sales invoice does not provide objective evidence about a transaction.The accounting process begins with:A Analysis of business transactions and source documents.B Preparing financial statements and other reports.C Summarizing the recorded effect of business transactions.D Presentation of financial information to decision-makers.E Preparation of the trial balance.Source documents include all of the following except:A Sales tickets.B Ledgers.C Checks.D Purchase orders.A ledger is:A A record containing increases and decreases in a specific asset, liability, equity, revenue, or expense item.B A journal in which transactions are first recorded.C A collection of documents that describe transactions and events entering the accounting process.D A list of all accounts with their debit balances at a point in time.E A record containing all accounts and their balances used by a company.Robert Haddon contributed $70,000 in cash and land worth $130,000 to open a new business, RH Consulting. Which of the following general journal entries will RH Consulting make to record this transaction?A Debit Assets $200,000; credit Haddon, Capital, $200,000.B Debit Cash and Land, $200,000; credit Haddon, Capital, $200,000.C Debit Cash $70,000; debit Land $130,000; credit Haddon, Capital, $200,000.D Debit Haddon, Capital, $200,000; credit Cash $70,000, credit Land, $130,000.On January 1 a company purchased a five-year insurance policy for $1,800 with coverage starting immediately. If the purchase was recorded in the Prepaid Insurance account, and the company records adjustments only at year-end, the adjusting entry at the end of the first year is:A Debit Prepaid Insurance, $1,800; credit Cash, $1,800.B Debit Prepaid Insurance, $1,440; credit Insurance Expense, $1,440.C Debit Prepaid Insurance, $360; credit Insurance Expense, $360.D Debit Insurance Expense, $360; credit Prepaid Insurance, $360.E Debit Insurance Expense, $360; credit Prepaid Insurance, $1,440.A company had no office supplies available at the beginning of the year. During the year, the company purchased $250 worth of office supplies. On December 31, $75 worth of office supplies remained. How much should the company report as office supplies expense for the year?A $75.B $125.C $175.D $250On April 1, a company paid the $1,350 premium on a three-year insurance policy with benefits beginning on that date. What will be the insurance expense on the annual income statement for the year ended December 31?A $1,350.00.B $450.00.C $1,012.50.D $337.50.If throughout an accounting period the fees for legal services paid in advance by clients are recorded in an account called Unearned Legal Fees, the end-of-period adjusting entry to record the portion of those fees that has been earned is:A Debit Cash and credit Legal Fees Earned.B Debit Cash and credit Unearned Legal Fees.C Debit Unearned Legal Fees and credit Legal Fees Earned.D Debit Legal Fees Earned and credit Unearned Legal Fees.E Debit Unearned Legal Fees and credit Accounts Receivable.The periodic expense created by allocating the cost of plant and equipment to the periods inwhich they are used, representing the expense of using the assets, is called:A Accumulated depreciation.B A contra account.C The matching principle.D Depreciation expense.An account linked with another account that has an opposite normal balance and that is subtracted from the balance of the related account is a(n):A Accrued expense.B Contra account.C Accrued revenue.D Intangible asset.On June 30 of the current calendar year, Apricot Co. paid $7,500 cash for management services to be performed over a two-year period. Apricot follows a policy of recording all prepaid expenses to asset accounts at the time of cash payment. The adjusting entry on December 31 for Apricot would include:A A debit to an expense for $5,625.B A debit to a prepaid expense for $5,625.C A debit to an expense for $1,875.D A debit to a prepaid expense for $1,875.On June 30 Apricot Co. paid $7,500 cash for management services to be performed over a two-year period. Apricot follows a policy of recording all prepaid expenses to asset accounts at the time of cash payment. On June 30 Apricot should record:A A credit to an expense for $7,500.B A debit to an expense for $7,500.C A debit to a prepaid expense for $7,500.D A credit to a prepaid expense for $7,500. If a company failed to make the end-of-period adjustment to remove from the Unearned Management Fees account the amount of management fees that were earned, this omission would cause:A An overstatement of net income.B An overstatement of assets.C An overstatement of liabilities.D An overstatement of equity.An adjusting entry could be made for each of the following except:A Prepaid expenses.B Depreciation.C Owner withdrawals.D Unearned revenues.Revenues are:A The same as net income.B The excess of expenses over assets.C Resources owned or controlled by a companyD The increase in equity from a company’s earning activities.E The costs of assets or services used.Another name for equity is:A Net income.B Expenses.C Net assets.D Revenue.E Net loss.A payment to an owner is called a(n):A Liability.B Withdrawal.C Expense.D Contribution.E Investmen The assets of a company total $700,000; the liabilities, $200,000. What are the claims of the owners?A 900,000.B $700,000.C $500,000.D 200,000.E It is impossible to determine unless the amount of this owners' investment is known. Photometer Company paid off $30,000 of its accounts payable in cash. What would be the effectsof this transaction on the accounting equation?A Assets, $30,000 increase; liabilities, no effect; equity, $30,000 increase.B Assets, $30,000 decrease; liabilities, $30,000 decrease; equity, no effect.C Assets, $30,000 decrease; liabilities, $30,000 increase; equity, no effect.D Assets, no effect; liabilities, $30,000 decrease; equity, $30,000 increase.E Assets, $30,000 decrease; liabilities, no effect; equity $30,000 decrease.Zion Company has assets of $600,000, liabilities of $250,000, and equity of $350,000. It buys office equipment on credit for $75,000. What would be the effects of this transaction on the accounting equation?A Assets increase by $75,000 and expenses increase by $75,000.B Assets increase by $75,000 and expenses decrease by $75,000.C Liabilities increase by $75,000 and expenses decrease by $75,000.D Assets decrease by $75,000 and expenses decrease by $75,000.E Assets increase by $75,000 and liabilities increase by $75,000.Every business transaction leaves the accounting equation in balance. √Owner's investments are increases in equity from a company's earnings activities. ×Owner’s withdrawals are expenses. ×Net income occurs when revenues exceed expenses. √In a double-entry accounting system, the total amount debited must always equal the total amount credited. √Increases in liability accounts are recorded as credits. √Asset accounts normally have credit balances and revenue accounts normally have debit balances. ×If a company purchases land paying cash, the journal entry to record this transaction will include a debit to Cash. ×If a company provides services to a customer on credit the selling company should debit cash. ×When a company bills a customer for $600 for services rendered, the journal entry to record this transaction will include a $600 debit to Services Revenue. ×A formal promise to pay (in the form of a promissory note) a future amount is a(n):A Unearned revenue.B Prepaid expense.C Credit account.D Note payable.A credit is used to record:A An increase in an expense account.B A decrease in an asset account.C A decrease in an unearned revenue account.D A decrease in a revenue account.Rocky Industries received its telephone bill in the amount of $300, and immediately paid it. Rocky's general journal entry to record this transaction will include aA Debit to Telephone Expense for $300.B Credit to Accounts Payable for $300.C Debit to Cash for $300.D Credit to Telephone Expense for $300. Management Services, Inc. provides services to clients. On May 1, a client prepaid Management Services $60,000 for 6-months services in advance. Management Services' general journal entry to record this transaction will include a:A Debit to Unearned Management Fees for $60,000.B Credit to Management Fees Earned for $60,000.C Credit to Cash for $60,000.D Credit to Unearned Management Fees for $60,000。

会计英语东北财经大学第四版课后习题答案

会计英语东北财经大学第四版课后习题答案一、语法精练1.My brother plays——football very well.A.a B.the C. all D. /2.Birds ——when there isn’t enough food for them.A. starve B.are starving C.starved D.starves3.I can see an apple ________ the apple tree and a bird ________ the banana tree.A.on, in B.in,in C.on,on D.in,on4.I have a red box.It’s full ________ toys,so it’s very ________.A.of, light B.for,big C.like,small D.of,heavy5.Your football shoes are under the chair.Please ________.A.put away it B.put it away C.put away them D.put them away6.Mom’s in a bad _____,so be nice to her.A.time B.trouble C. manner D.mood二、阅读理解Mr.White looks out of his window.There is a boy at the otherside of the street.The boy takes some bread out of a bag and begins eating it.There is a very thin dog in the street, too.The boy says to it, “I’ll give you some bread.” The dog is hungry and goes to the boy, but he does not give it any bread.He kicks the dog.It runs away, and the boy laughs.Then Mr.White comes out of his house and says to the boy.“I’ll give you a shilling (先令).”The boy is happy and says,“Yes.”“Come here.” Mr.White says.The boy goes to him,but Mr.White does not give him a shilling.He hits him with a stick. The boy cries and says, “Why do you hit me? I do not ask you for any money.” “No,” Mr.White says,“And the dog does not ask you for any bread,but you kick it.”1.Where is Mr.White at first?A.He is in the roomB.He is in the street.C.He is in front of the house.D.He stands close to the boy.2.Why does the dog go to the boy? Because__________.A.it wants to eatB.the boy asks it to do soC.the boy is the dog’s ownerD.the boy is friendly to it3.Why does the dog run away? Because__________.A.the boy gives some breadB.the dog doesn’t like breadC.the dog doesn’t like the boyD.the boy kicks the dog4.Why does Mr.White tell the boy to come up to him? Because he wants to__________.A.give him a shillingB.give him a good lesson(教训)C.give him some more breadD.help the boy5.What kind of man do you think Mr.White is? He is a __________man.A.cruel (粗鲁的)B.sympathetic (富有同情心的)C.friendlyD.polite (有礼貌的)一、语法精练1.D 解析:本题考查冠词的用法,在球类的名词前不加冠词。

会计专业英语习题答案.doc