4_Financial_Markets_and_Institutions_students

金融市场1financial market and institutions

Financial Markets andInstitutionsW.L. WuEmail:wuwenli@1929年夏天,股市不但支配着新闻,也笼罩着文化。

少数自诩对神学、心理分析及精神医学感兴趣的附庸风雅者,现在也在谈论联合公司和钢铁公司的股票。

每个地方总有那么一个人能够准确地把握买卖股票的时机,他们被奉为圣人,即便在画家、剧作家、诗人和美丽的情妇面前,他们也突然变得光彩照人。

他们说的话几乎字字千金,听众个个全神贯注,惟恐因错过重要消息而丧失赚钱的机会。

------《1929年大崩盘》(The Great Crash 1929 )加尔布雷思(1908-2006),美国经济学家,新制度学派主要代表人物。

美国加利福尼亚大学研究农业经济学博士。

此后相继在哈佛大学和普林斯顿大学任教。

1941~1943年担任美国物价管理局副局长。

1961~1963年任美国驻印度大使。

1972年被选为美国经济学协会主席。

当你试图不去谈论股票的时候,反而让人感觉是缺乏勇气和决心,在那些总是轻而易举挣大钱的榜样映衬之下,还没有投身证券市场的人在内心中竟然平添了几分匪夷所思的自卑感。

------------中国证券报:不在泡沫中疯狂就在泡沫中崩溃2007年08月27日用了一个简单比喻说明“泡沫”的形成机制:猴子看,猴子学。

他说,没有什么事比眼看着一个朋友变富更困扰人们的头脑和判断力的了。

--------------金德尔伯格, 《金融危机史》Finance•1866年,英国词典(Webster)出现Finance一词,定义为“筹集或提供资本的活动”(To Raise or Provide Funds or Capital )。

•华尔街日报在其新开的公司金融(Corporate Finance)的固定版面中将(公司)金融定义为“为业务提供融资的业务(Business of Financing Businesses)”,这一定义基本上代表了金融实业界的看法。

Financial Instruments, Financial Markets, and Financial Institutions

• Financial development is linked to economic growth. • The role of the financial system is to facilitate production, employment, and consumption. • Resources are funneled through the system so resources flow to their most efficient uses.

3-6

Uses of Financial Instruments

• Three functions:

• Act as a means of payment (like money). • Employees take stock options as payment for working. • Act as stores of value (like money). • Generate increases in wealth that are larger than from holding money. • Can be used to transfer purchasing power into the future. • Allow for the transfer of risk (unlike money). • Futures and insurance contracts allows one person to transfer risk to another.

Financial Markets and Institutions

• •

Well-functioning markets promote economic growth. Economies with well-developed markets perform better than economies with poorly-functioning markets.

2-2

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, or duplicated, or posted to a publicly accessible website, in whole or in part.

How is capital transferred between savers and borrowers?

• • •

Direct transfers

Investment banks

Financial intermediaries

2-3

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, or duplicated, or posted to a publicly accessible website, in whole or in part.

What is a market?

•

•

A market is a venue where goods and services are exchanged. A financial market is a place where individuals and organizations wanting to borrow funds are brought together with those having a surplus of funds.

Foundations of Financial Markets and Institutions 金融市场与机构基础

Common stock Preferred stock Foreign stock

Debt vs. Equity

Debt Instruments

Fixed dollar payments (‘fixed income’) Examples include loans, bonds

Equity Claims

Equity holders bear inflation risk Debt holders bear default risk Both may bear exchange rate risk

Role of (Financial) Markets

Provide liquidity: buyers and sellers all in one ‘place’. price discovery efficient resource allocation Reduce transactions costs:

search costs information costs (market efficiency)

Financial Market Participants

Households Business units Federal, state, and local governments Government agencies International organizations (e.g. World bank) Regulators (broader definition)

Classification of Global Financial Markets

Internal Market (= national market)

External Market (= international, offshore or Euromarket): securities

商业银行管理彼得S.罗斯第八版课后答案chapter_01

CHAPTER 1AN OVERVIEW OF BANKS AND THE FINANCIAL-SERVICES SECTORGoal of This Chapter: In this chapter you will learn about the many roles financial service providers play in the economy today. You will examine how and why the banking industry and the financial services marketplace as a whole is rapidly changing, becoming new and different as we move forward into the future. You will also learn about new and old services offered to the public.Key Topics in This Chapter•Powerful Forces Reshaping the Industry•What is a Bank?•The Financial System and Competing Financial-Service Institutions•Old and New Services Offered to the Public•Key Trends Affecting All Financial-Service Firms•Appendix: Career Opportunities in Financial ServicesChapter OutlineI. I ntroduction: P owerful Forces Reshaping the IndustryII. W hat Is a Bank?A. D efined by the Functions It Serves and the Roles It Play:B. B anks and their Principal CompetitorsC. Legal Basis of a BankD. D efined by the Government Agency That Insures Its DepositsIII.The Financial System and Competing Financial-Service InstitutionsA.Savings AssociationsB.Credit UnionsC.Money Market FundsD.Mutual FundsE.Hedge FundsF.Security Brokers and DealersG.Investment BankersH.Finance CompaniesI.Financial Holding CompaniesJ.Life and Property/Casualty Insurance CompaniesIV. T he Services Banks and Many of Their Closest Competitors Offer the PublicA. S ervices Banks Have Offered Throughout History1.Carrying Out Currency Exchanges2.Discounting Commercial Notes and Making Business Loans3.Offering Savings Deposits4.Safekeeping of Valuables and Certification of Value5.Supporting Government Activities with Credit6.Offering Checking Accounts (Demand Deposits)7.Offering Trust ServicesB. S ervices Banks and Many of Their Financial-Service Competitors HaveOffered More Recently1.Granting Consumer Loans2.Financial Advising3.Managing Cash4.Offering Equipment Leasing5.Making Venture Capital Loans6.Selling Insurance Policies7.Selling Retirement PlansC. Dealing in Securities: Offering Security Brokerage and Investment Banking Services1. Offering Security Underwriting2. Offering Mutual Funds and Annuities3. Offering Merchant Banking Services4. Offering Risk Management and Hedging ServicesV. Key Trends Affecting All Financial-Service FirmsA. S ervice ProliferationB. R ising CompetitionC. G overnment DeregulationD. A n Increasingly Interest-Sensitive Mix of FundsE. T echnological Change and AutomationF. C onsolidation and Geographic ExpansionG. C onvergenceH. G lobalizationVI. T he Plan of This BookVII. S ummaryConcept Checks1-1. What is a bank? How does a bank differ from most other financial-service providers?A bank should be defined by what it does; in this case, banks are generally those financial institutions offering the widest range of financial services. Other financial service providers offer some of the financial services offered by a bank, but not all of them within one institution.1-2. Under U.S. law what must a corporation do to qualify and be regulated as a commercial bank?Under U.S. law, commercial banks must offer two essential services to qualify as banks for purposes of regulation and taxation, demand (checkable) deposits and commercial loans. More recently, Congress defined a bank as any institution that could qualify for deposit insurance administered by the FDIC.1-3.Why are some banks reaching out to become one-stop financial service conglomerates? Is this a good idea in your opinion?There are two reasons that banks are increasingly becoming one-stop financial service conglomerates. The first reason is the increased competition from other types of financial institution s and the erosion of banks’ traditional service areas. The second reason is the Financial Services Modernization Act which has allowed banks to expand their role to be full service providers.1-4. Which businesses are banking’s closest and toughest com petitors? What services do they offer that compete directly with banks’ services?Among a bank’s closest competitors are savings associations, credit unions, money market funds, mutual funds, hedge funds, security brokers and dealers, investment banks, finance companies, financial holding companies, and life andproperty-casualty insurance companies. All of these financial service providers are converging and embracing each other’s innovations. The Financial Services Modernization Act has allowed many of these financial service providers to offer the public one-stop shopping for financial services.1-5. What is happening to banking’s share of the financial mark etplace and why? What kind of banking and financial system do you foresee for the future if present trends continue?The Financial Services Modernization Act of 1999 allowed many of the banks’ closest competitors to offer a wide array of financial services thereby taking away market share from “traditional” banks. Banks and their closest competitors are converging into one-stop shopping for financial services and this trend should continue in the future1-6. What different kinds of services do banks offer the public today? What services do their closest competitors offer?Banks offer the widest range of services of any financial institution. They offer thrift deposits to encourage saving and checkable (demand) deposits to provide a means of payment for purchases of goods and services. They also provide credit through direct loans, by discounting the notes that business customers hold, and by issuing credit guarantees. Additionally, they make loans to consumers for purchases of durable goods, such as automobiles, and for home improvements, etc. Banks also manage the property of customers under trust agreements and manage the cash positions of their business customers. They purchase and lease equipment to customers as an alternative to direct loans. Many banks also assist their customers with buying and selling securities through discount brokerage subsidiaries, the acquisition and sale of foreign currencies, the supplying of venture capital to start new businesses, and the purchase of annuities to supply future funding at retirement or for other long-term projects such as supporting a college education. All of these services are also offered by their closest competitors. Banks and their closest competitors are converging and becoming the financial department stores of the modern era.1-7. What is a financial department store? A universal bank? Why do you think these institutions have become so important in the modern financial system? Financial department store and universal bank refer to the same concept. A financial department store is an institution where banking, fiduciary, insurance, and security brokerage services are unified under one roof. A bank that offers all these services is normally referred to as a universal bank. These have become important because of convergence and changes in regulations that have allowed financial service providers to offer all services under one roof1-8. Why do banks and other financial intermediaries exist in modern society, according to the theory of finance?There are multiple approaches to answering this question. The traditional view of banks as financial intermediaries sees them as simultaneously fulfilling the financial-service needs of savers (surplus-spending units) and borrowers(deficit-spending units), providing both a supply of credit and a supply of liquid assets. A newer view sees banks as delegated monitors who assess and evaluate borrowers on behalf of their depositors and earn fees for supplying monitoring services. Banks also have been viewed in recent theory as suppliers of liquidity andtransactions services that reduce costs for their customers and, through diversification, reduce risk. Banks are also critical in the payment system for goods and services and have played an increasingly important role as a guarantor and a risk management role for customers.1-9. How have banking and the financial services market changed in recent years? What powerful forces are shaping financial markets and institutions today? Which of these forces do you think will continue into the future?Banking is becoming a more volatile industry due, in part, to deregulation which has opened up individual banks to the full force of the financial marketplace. At the same time the number and variety of banking services has increased greatly due to the pressure of intensifying competition from nonbank financial-service providers and changing public demand for more conveniently and reliably provided services. Adding to the intensity of competition, foreign banks have enjoyed success in their efforts to enter countries overseas and attract away profitable domestic business and household accounts.1-10. Can you explain why many of the forces you named in the answer to the previous question have led to significant problems for the management of banks and other financial firms and their stockholders?The net result of recent changes in banking and the financial services market has been to put greater pressure upon their earnings, resulting in more volatile returns to stockholders and an increased bank failure rates. Some experts see banks' role and market share shrinking due to restrictive government regulations and intensifying competition. Institutions have also become more innovative in their service offerings and in finding new sources of funding, such as off-balance-sheet transactions. The increased risk faced by institutions today, therefore, has forced managers to more aggressively utilize a wide array of tools and techniques to improve and stabilize their earnings streams and manage the various risks they face. 1-11. What do you think the financial services industry will look like 20 years from now? What are the implications of your projections for its management today? There appears to be a trend toward continuing consolidation and convergence. There are likely to be fewer financial service providers in the future and many of these will be very large and provide a broad range of financial services under one roof. In addition, global expansion will continue and will be critical to the survival of many financial service providers. Management of financial service providers willhave to be more technologically astute and be able to make a more diverse set of decisions including decisions about mergers, acquisitions and global expansion as well as new services to add to the firm.Problems and Projects1. You have just been hired as the marketing officer for the new First National Bank of Vincent, a suburban banking institution that will soon be serving a local community of 120,000 people. The town is adjacent to a major metropolitan area with a total population of well over 1 million. Opening day for the newly chartered bank is just two months away, and the president and the board of directors are concerned that the new bank may not be able to attract enough depositors and good-quality loan customers to meet its growth and profit projections. There are 18 other financial-service competitors in town, including two credit unions, three finance companies, four insurance agencies, and two security broker offices. Your task is to recommend the various services the bank should offer initially to build up an adequate customer base. You are asked to do the following:a.Make a list of all the services the new bank could offer, according to current regulations.b.List the type of information you will need about the local community tohelp you decide which of the possible services are likely to have sufficientdemand to make them profitable.c.Divide the possible services into two groups--those you think are essentialto customers and should be offered beginning with opening day, and thosethat can be offered later as the bank grows.d. Briefly describe the kind of advertising campaign you would like to run tohelp the public see how your bank is different from all the other financialservice providers in the local area. Which services offered by the nonblankservice providers would be of most concern to the new bank’smanagement?Banks can offer, if they choose, a wide variety of financial services today. These services are listed below. However, unless they are affiliated with a larger bank holding company and can offer some of these services through that company, it may be more limited in what it can offer.Regular Checking Accounts Management Consulting Services NOW Accounts Letters of CreditPassbook Savings Deposits Business Inventory Loans Certificates of Deposit Asset-Based Commercial Loans Money Market Deposits Discounting of Commercial Paper Automobile Loans Plant and Equipment Loans Retirement Savings Plans Venture Capital LoansNonauto Installment Loans to IndividualsResidential Real Estate Loans Leasing Plans for Business Property and EquipmentHome Improvement Loans Security Dealing and Underwriting Personal Trust Management Services Discount Security BrokerageCommercial Trust Services Institutional Trust Services Foreign Currency Trading and ExchangePersonal Financial Advising Personal Cash-Management ServicesInsurance Policy Sales (Mainly Credit-Life)Insurance Today (Except in Some States)) Standby Credit Guarantees Acceptance FinancingTo help the new bank decide which services to offer it would be helpful to gather information about some of the following items in the local community:School Enrollments and Growth in School EnrollmentsEstimated Value of Residential and Commercial PropertyRetail SalesPercentage of Home Ownership Among Residents in the AreaNumber and Size (in Sales and Work Force) of Local Business Establishments Major Population Locations (i.e., Major Subdivisions, etc.) and Any Projected Growth AreasPopulation Demographics (i.e., Age Distribution of the Area)Projected Growth Areas of Industries in the AreaEssential services the bank would probably want to offer right from the beginning includes:Regular Checking Accounts Home Improvement Loans Automobile and other Consumer-type Money Market Deposit Accounts Installment Loans Retirement Savings PlansNOW Accounts Business Inventory LoansPassbook Savings Deposits Discounting of High-QualityCommercial NotesResidential Real Estate LoansCertificates of DepositAs the bank grows, opportunities for the profitable sale of additional services usually increase, especially for trust services for individuals and smaller businesses and personal financial advising as well as some commercial (plant and equipment) loans and leases. Further growth may result in the expansion of commercial trust services as well as a widening variety of commercial loans and credit guarantees.The bank would want to develop an advertising campaign that sends a message to potential customers that the new bank is, indeed, different from its competitors. Small banks often have the advantage of offering highly personalized services in which their customers are known and recognized and services are tailored to each individual customer's special financial needs. Quality and reliability of banking service are often more important to individual customers than is price. A new bank must try to sell prospective customers, most of who will come from other banks in the area, on personalized services, quality, and reliability - all three of which should be emphasized in its advertising program.2. Leading money center banks in the United States have accelerated their investment banking activities all over the globe in recent years, purchasing corporate debt securities and stock from their business customers and reselling those securities to investors in the open market. Is this a desirable move by these banking organizations from a profit standpoint? From a risk standpoint? From the public interest point of view? How would you research their question? If you were managing a corporation that had placed large deposits with a bank engaged in such activities, would you be concerned about the risk to your company's funds? What could you do to better safeguard those funds?In the 1970's and early 1980's investment banking was so profitable that commercial bankers were lured into the investment banking business largely because of its greater profit potential than possessed by more traditional commercial banking activities. Later foreign banks, particularly the British and Japanese banking firms, began to attract away large corporate customers from U.S. banks, who were restrained by regulation from offering many investment banking services. Thus, U.S. banks ran into severe difficulty in simply trying to hold onto their traditional corporate credit and deposit accounts because they could not compete service-wise in the investment banking field. Today, banks are allowed to underwrite securities through either a subsidiary or through a holding company structure. This change occurred as part of the Gramm-Leach-Bliley Act (Financial Services Modernization Act).Unfortunately, if investment banking is more profitable than traditional banking product lines, it is also more risky, consistent with the basic tenet of finance that risk and return are directly related. That is why the Federal Reserve Board has placed such strict limits on the type of organization that can offer these services. Currently, the underwriting of most corporate securities must be done through a subsidiary or as a separate part of the holding company so that, in theory at least, the bank is not responsible for any losses incurred. For this reason there may be little reason for depositors (including large corporate depositors) to be concerned about risk exposure from investment banking. Moreover, the ability to offer such services may make U.S. banks more viable in the long run which helps their corporate customers who depend upon them for credit.On the other hand, opponents of investment banking powers for bank operations inside the U.S. have some reasonable concerns that must be addressed. There are, for example, possible conflicts of interest. Information gathered in the investment banking division could be used to the detriment of customers purchasing other bank services. For example, a customer seeking a loan may be told that he or she must buy securities from the bank's investment banking division in order to receive a loan. Moreover, banks could gain effective control over some nonblank industrial corporations which might subject them to added risk exposure and place industrial firms not allied with banks at a competitive disadvantage. As a result theGramm-Leach-Bliley Act has built in some protections to prevent this from happening.3. The term bank has been applied broadly over the years to include a diverse set of financial-service institutions, which offer different financial service packages.Identify as many o f the different kinds of “banks” as you can. How do the “banks” you have identified compare to the largest banking group of all – the commercial banks? Why do you think so many different financial firms have been called banks? How might this terminological confusion affect financial-service customers?The general public tends to classify anything as a bank that offers some sort of financial service, especially deposit and loan services. Other institutions that are often referred to as a bank without being one are savings associations, credit unions, money market funds, mutual funds, hedge funds, security brokers and dealers, investment banks, finance companies, financial holding companies and life and property/casualty insurance companies. All of these institutions offer some of the services that a commercial bank offers, but generally not the entire scope of services. Since providers of financial services are normally called banks by the general public they are able to take away business from traditional banks and it is of utmost importance for commercial banks to clarify their unique position among financial services providers.4. What advantages can you see to banks affiliating with insurance companies? How might such an affiliation benefit a bank? An insurer? Can you identify any possible disadvantages to such an affiliation? Can you cite any real world examples of bank-insurer affiliations? How well do they appear to have worked out in practice?Before Glass-Steagall banks used to sell insurance services to their customers on a regular basis. in particular, banks would sell life insurance companies to loan customers to ensure repayment of the loan in case of death or disablement. These reasons still exist today and the right to sell insurances to customers again benefits banks in allowing them to offer their customers complete financial packages from financing the home or car to insure it, from giving investment advice to selling life insurance policies and annuities for retirement planning. Generally, a bank customer who is already purchasing a service from a bank might feel compelled to purchase an insurance product, as well. On the other hand, insurance companies sometimes have a negative image, which makes it more difficult to sell certain insurance products. Combining their products with the trust that people generally have in banks will make it easier for them to sell their products. The most prominent example of a bank-insurer affiliation is the merger of Citicorp and Traveler’s Insurance to Citigroup. However, given that Citigroup has sold Traveler’s Insurance indicates that the anticipated synergy effects did not materialize.5. Explain the difference between consolidation and convergence. Are these trends in banking and financial services related? Do they influence each other? How? Consolidation refers to increase in the size of financial institutions and the decline in the number of small independently owned banks and financial service providers. Convergence is the bringing together of firms from different industries to createconglomerate firms offering multiple services. Clearly, these two trends are related. In their effort to compete with each other, banks and their closest competitors have acquired other firms in their industry as well across industries to provide multiple financial services in multiple markets.6. What is a financial intermediary? What are their key characteristics? Is a bank a type of financial intermediary? Why? What other financial-services companies are financial intermediaries? What important role within the financial system do financial intermediaries play?A financial intermediary is a business that interacts with deficit spending individuals and institutions and surplus spending individuals and institutions. For that reason any financial service provider (including banks) is considered a financial intermediary. In their function as intermediaries they act as a bridge between the deficit and surplus spending units by offering financial services to the surplus spending individuals and then loaning those funds to the deficit spending individuals. Financial intermediaries accelerate economic growth by increasing the pool of available funds and lowering the risk of investments through diversification.。

金融市场学双语题库及答案(第二十章)米什金《金融市场与机构》

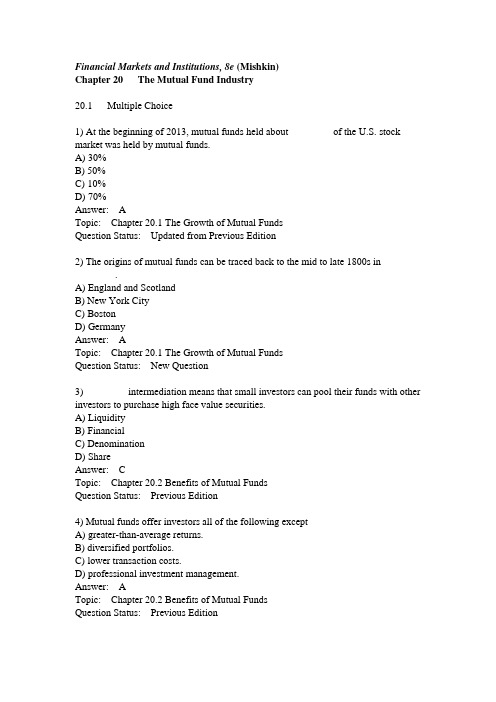

Financial Markets and Institutions, 8e (Mishkin)Chapter 20 The Mutual Fund Industry20.1 Multiple Choice1) At the beginning of 2013, mutual funds held about ________ of the U.S. stock market was held by mutual funds.A) 30%B) 50%C) 10%D) 70%Answer: ATopic: Chapter 20.1 The Growth of Mutual FundsQuestion Status: Updated from Previous Edition2) The origins of mutual funds can be traced back to the mid to late 1800s in________.A) England and ScotlandB) New York CityC) BostonD) GermanyAnswer: ATopic: Chapter 20.1 The Growth of Mutual FundsQuestion Status: New Question3) ________ intermediation means that small investors can pool their funds with other investors to purchase high face value securities.A) LiquidityB) FinancialC) DenominationD) ShareAnswer: CTopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition4) Mutual funds offer investors all of the following exceptA) greater-than-average returns.B) diversified portfolios.C) lower transaction costs.D) professional investment management.Answer: ATopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition5) Mutual fundsA) pool the resources of many small investors by selling these investors shares and using the proceeds to buy securities.B) allow small investors to obtain the benefits of lower transaction costs in purchasing securities.C) provide small investors a diversified portfolio that reduces risk.D) do all of the above.E) do only A and B of the above.Answer: DTopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition6) ________ enables mutual funds to consistently outperform a randomly selected group of stocks.A) Managerial expertiseB) DiversificationC) Denomination intermediationD) None of the aboveAnswer: DTopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition7) At the end of 2012 there were over ________ separate mutual funds with total assets over ________.A) 800; $10 trillionB) 7,500; $13 trillionC) 10,000; $10 trillionD) 1,000; $7 trillionAnswer: BTopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Updated from Previous Edition8) Most mutual funds are structured in two ways. The most common structure is a(n) ________ fund, from which shares can be redeemed at any time at a price that is tied to the asset value of the fund. A(n) ________ fund has a fixed number of nonredeemable shares that are traded in the over-the-counter market.A) closed-end; open-endB) open-end; closed-endC) no-load; closed-endD) no-load; loadE) load; no-loadAnswer: BTopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition9) Which of the following is an advantage to investors of an open-end mutual fund?A) Once all the shares have been sold, the investor does not have to put in more money.B) The investors can sell their shares in the over-the-counter market with low transaction fees.C) The fund agrees to redeem shares at any time.D) The market value of the fund's shares may be higher than the value of the assets held by the fund.Answer: CTopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition10) The net asset value of a mutual fund isA) determined by subtracting the fund's liabilities from its assets and dividing by the number of shares outstanding.B) determined by calculating the net price of the assets owned by the fund.C) calculated every 15 minutes and used for transactions occurring during the next 15-minute interval.D) calculated as the difference between the fund's assets and its liabilities. Answer: ATopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition11) ________ funds are the simplest type of investment funds to manage.A) BalancedB) Global equityC) GrowthD) IndexAnswer: DTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition12) The majority of mutual fund assets are now owned byA) individual investors.B) institutional investors.C) fiduciaries.D) business organizations.E) retirees.Answer: ATopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition13) Capital appreciation funds select stocks of ________ and tend to be ________ risky than total return funds.A) large, established companies that pay dividends regularly; moreB) large, established companies that pay dividends regularly; lessC) companies expected to grow rapidly; moreD) companies expected to grow rapidly; lessAnswer: CTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition14) From largest to smallest in terms of total assets, the four classes of mutual funds areA) equity funds, bond funds, hybrid funds, money market funds.B) equity funds, money market funds, bond funds, hybrid funds.C) money market funds, equity funds, hybrid funds, bond funds.D) bond funds, money market funds, equity funds, hybrid funds.Answer: BTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition15) Measured by assets, the most popular type of bond fund is the ________ bond fund.A) state municipalB) strategic incomeC) governmentD) high-yieldAnswer: BTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition16) People who take their money out of insured bank deposits to invest in uninsured money market mutual funds have ________ risk because money market funds invest in ________ assets.A) high; long-termB) low; short-termC) high; short-termD) low; long-termAnswer: BTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition17) The largest share of assets held by money market mutual funds isA) Treasury bills.B) certificates of deposit.C) commercial paper.D) repurchase agreements.Answer: CTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition18) Which of the following is a feature of index funds?A) They have lower fees.B) They select and hold stocks to match the performance of a stock index.C) They do not require managers to select stocks and decide when to buy and sell.D) All of the above.Answer: DTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition19) A deferred-load mutual fund charges a commissionA) when shares are purchased.B) when shares are sold.C) both when shares are purchased and when they are sold.D) when shares are redeemed.Answer: DTopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition20) Over the past twenty years, mutual fund fees have ________, largely because________.A) fallen; SEC fee disclosure rules have led to greater competitionB) risen; investors have learned that funds with high fees provide better performanceC) risen; there has been collusion between large mutual fund companiesD) fallen; advances in information technology have lowered transaction costs Answer: ATopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition21) Which of the following is most likely to be a no-load fund?A) Value fundsB) Hedge fundsC) Growth fundsD) Index fundsAnswer: DTopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition22) When investors switch between funds within the same fund family, mutual funds may chargeA) a contingent deferred sales charge.B) a redemption fee.C) an exchange fee.D) 12b-1 fees.E) an account maintenance fee.Answer: CTopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition23) The Securities Acts of 1933 and 1934 did notA) regulate the activities of investment funds.B) require funds to register with the SEC.C) include antifraud rules covering the purchase and sale of fund shares.D) apply to investment funds.Answer: BTopic: Chapter 20.6 Regulation of Mutual FundsQuestion Status: Previous Edition24) The largest share of total investment in mutual funds is inA) stock funds.B) hybrid funds.C) bond funds.D) money market funds.Answer: ATopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition25) Over ________ of the total daily volume in stocks is due to institutions initiating trades.A) 70%B) 50%C) 25%D) 90%Answer: ATopic: Chapter 20.6 Regulation of Mutual FundsQuestion Status: New Question26) Hedge funds areA) low risk because they are market-neutral.B) low risk if they buy Treasury bonds.C) low risk because they hedge their investments.D) high risk because they are market-neutral.E) high risk, even though they may be market-neutral.Answer: ETopic: Chapter 20.7 Hedge FundsQuestion Status: Previous Edition27) The near collapse of Long Term Capital Management was caused byA) the high management fees charged by the fund's two Nobel Prize winners.B) the fund's high leverage ratio of 20 to 1.C) a sharp decrease in the spread between corporate bonds and Treasury bonds.D) a sharp increase in the spread between corporate bonds and Treasury bonds.E) the fund's shift away from a market-neutral investment strategy.Answer: DTopic: Chapter 20.7 Hedge FundsQuestion Status: Previous Edition28) Conflicts arise in the mutual funds industry because ________ cannot effectively monitor ________.A) investment advisers; directorsB) directors; shareholdersC) shareholders; investment advisersD) investment advisers; stocks that will outperform the overall marketAnswer: CTopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition29) Late trading is the practice of allowing orders received ________ to trade at the ________ net asset value.A) before 4:00 PM; 4:00 PMB) after 4:00 PM; 4:00 PMC) after 4:00 PM; next day'sD) before 4:00 PM; previous day'sAnswer: BTopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition30) Market timingA) takes advantage of time differences between the east and west coasts of the United States.B) takes advantage of arbitrage opportunities in foreign stocks.C) takes advantage of the time lag between the receipt and execution of orders.D) is discouraged by the stiff fees mutual funds charge every investor for buying and then selling shares on the same day.Answer: BTopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition31) Late trading and market timingA) allow large, favored investors in a mutual fund to profit at the expense of other investors in the fund.B) hurt ordinary investors by increasing the number of fund shares and diluting the fund's net asset value.C) are both A and B of the above.D) are none of the above.Answer: CTopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund Industry Question Status: Previous Edition32) Which of the following is not a proposal to deal with abuses in the mutual fund industry?A) Strictly enforce the 4:00 PM net asset value rule.B) Make redemption fees mandatory.C) Disclose compensation arrangements for investment advisers.D) Increase the number of dependent directors.Answer: DTopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition33) ________ means the investors can convert their investment into cash quickly at a low cost.A) Liquidity intermediationB) Denomination intermediationC) DiversificationD) Managerial expertiseAnswer: ATopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition34) At the start of 2014, one share of Berkshire Hathaway's A-shares was trading at over $150,000. ________ in an mutual fund gives a small investor access to these shares.A) Liquidity intermediationB) Denomination intermediationC) DiversificationD) Managerial expertiseAnswer: BTopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition35) Mutual fund companies frequently offer a number of separate mutual funds called ________.A) indexesB) complexesC) componentsD) actuariesAnswer: BTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition36) Equity funds can be placed in which class according to the Investment Company Institute?A) Capital appreciation fundsB) World fundsC) Total return fundsD) All of the aboveAnswer: DTopic: Chapter 20.4 Investment Objective Classes Question Status: Previous Edition37) Government bonds are essentially default risk-free, ________ returns.A) and will yield highB) and will yield the highestC) but will have relatively lowD) none of the aboveAnswer: CTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition38) ________ bonds combine stocks into one fund.A) HybridB) Money marketC) MunicipalD) EquityAnswer: ATopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition39) All ________ are open-end investment funds that invest only in money market securities.A) Stock fundsB) Bond fundsC) Money market mutual fundsD) all of the aboveAnswer: CTopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition20.2 True/False1) The larger the number of shares traded in a stock transaction, the lower the transaction costs per share.Answer: TRUETopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition2) The increase in the number of defined contribution pension funds has slowed the growth of mutual funds.Answer: FALSETopic: Chapter 20.1 The Growth of Mutual FundsQuestion Status: Previous Edition3) Mutual funds accounted for $5.3 trillion, or 27%, of the $19.5 trillion U.S. retirement market at the beginning of 2013.Answer: TRUETopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Updated from Previous Edition4) Among the investors in mutual funds, only about 25% cite preparing for retirement as one of their main reasons for holding shares.Answer: FALSETopic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Updated from Previous Edition5) Open-end mutual funds are more common than closed-end funds.Answer: TRUETopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition6) The net asset value of a mutual fund is the average market price of the stocks, bonds, and other assets the fund owns.Answer: FALSETopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition7) A mutual fund's board of directors picks the securities that will be held and makes buy and sell decisions.Answer: FALSETopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition8) Money market mutual funds originated when the brokerage firm Merrill Lynch offered its customers an account from which funds could be taken to purchase securities and into which funds could be deposited when securities were sold. Answer: TRUETopic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition9) A deferred load is a fee charged when shares in a mutual fund are redeemed. Answer: TRUETopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition10) Several academic research studies show that investors earn higher returns by investing in mutual funds that charge higher fees.Answer: FALSETopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition11) Hedge funds have a minimum investment requirement of between $100,000 and$20 million, with the typical minimum investment being $1 million.Answer: TRUETopic: Chapter 20.7 Hedge FundsQuestion Status: New Question12) SEC research suggests that about three-fourths of mutual funds let privileged shareholders engage in market timing.Answer: TRUETopic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition13) One factor explaining the rapid growth in mutual funds is that they are financial intermediaries that are not regulated by the federal government.Answer: FALSETopic: Chapter 20.1 The Growth of Mutual FundsQuestion Status: Previous Edition14) Whether a fund is organized as a closed- or an open-end fund, is will have the same basic organizational structure.Answer: TRUETopic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition15) The primary purpose of loads is to provide compensation for sales brokers. Answer: TRUETopic: Chapter 20.5 Fee Structure of Investment FundsQuestion Status: Previous Edition16) Mutual funds are regulated under four federal laws designed to protect investors. Answer: TRUETopic: Chapter 20.6 Regulation of Mutual FundsQuestion Status: Previous Edition20.3 Essay1) What benefits do mutual funds offer investors?Topic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: Previous Edition2) How is a mutual fund's net asset value calculated?Topic: Chapter 20.3 Mutual Fund StructureQuestion Status: Previous Edition3) How did money market mutual funds originate and why did they become especially popular in the late 1970s and early 1980s?Topic: Chapter 20.1 The Growth of Mutual FundsQuestion Status: Previous Edition4) How does the governance structure of mutual funds lead to asymmetric information and conflicts of interest?Topic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition5) Describe the practices of late trading and market timing and explain how these practices harm a mutual fund's shareholders.Topic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition6) Discuss the proposals that have been made to reduce the conflict of interest abuses in the mutual funds industry.Topic: Chapter 20.8 Conflicts of Interest in the Mutual Fund IndustryQuestion Status: Previous Edition7) How is an index fund different from the other four primary investment objective classes for mutual funds?Topic: Chapter 20.4 Investment Objective ClassesQuestion Status: New Question8) Discuss the four primary classes of mutual funds available to investors.Topic: Chapter 20.4 Investment Objective ClassesQuestion Status: Previous Edition9) What are the five benefits of mutual funds?Topic: Chapter 20.2 Benefits of Mutual FundsQuestion Status: New Question10) What is the difference between an open-end and a closed-end mutual fund? Topic: Chapter 20.3 Mutual Fund StructureQuestion Status: New Question11) What are two key differences between a traditional mutual fund and a hedge fund?Topic: Chapter 20.7 Hedge FundsQuestion Status: New Question。

货币金融学financialmarketandinstitutions-米什金-英文ch11原版

▪ Before we do that, let’s examine some of the current rates offered in the U.S. money markets. Some of these rates have been discussed in previous chapters. Other rates will be explored throughout this chapter.

© 2012 Pearson Education. All rights reserved.

11-5

The Money Markets Defined: Cost Advantages

▪ Even today, the cost structure of banks limits their competitiveness to situations where their informational advantages outweighs their regulatory costs.

11-13

Money Market Instruments (cont.)

▪ We will examine each of these in the following slides (continued):

─ Commercial Paper ─ Banker’s Acceptance ─ Eurodollars

Financial Markets and Institutions

Cash Reinvested

Cash

Investors

2-6 The Flow of Savings to Corporations

Corporation Reinvestment

Financial markets

Stock markets Fixed-income markets Money markets Markets for • Commodities • Foreign exchange • Derivatives

2- 14

Total U.S. Financing

% Holdings of Corporate Equities (Qtr 3, 2007)

1.4

28.3

Hale Waihona Puke 27.112.622.3

8 0.3

Households Rest of world Banks Insurance Cos Pension Funds Mutual Funds Other

2-15 Function of Financial Markets

Transporting cash across time Risk transfer and diversification Liquidity Payment mechanism Provide information

2- 1

Chapter 2

Financial Markets and Institutions

2- 2

Topics Covered

The Importance of Financial Markets and Institutions

The Flow of Savings to Corporations Functions of Financial Markets and

Financial Markets and Institutions 金融市场与结构 第三章

Yield Curve Shapes

Normal

Level or Flat

Inverted

Factors Affecting Security Yields

Special Provisions

Call Feature: enables borrower to buy back the bonds before maturity at a specified price

Factors Affecting Security Yields

Term to maturity

Interest rates typically vary by maturity. The term structure of interest rates defines the relationship between maturity and yield.

Forward

rate: market’s forecast of the future interest

rate

The Term Structure of Interest Rates

UpwardSloping Yield Curve

DownwardSloping Yield Curve

Factors Affecting Security Yields

The Liquidity of a security affects the yield/price of the security A liquid investment is easily converted to cash At minimum transactions cost Investors pay more (lower yield) for liquid investment Liquidity is associated with short-term, low default risk, marketable securities

5_Financial_Markets_and_Institutions_students

Comparison of single-payment yield, bond equivalent yield, and EAR

• You purchase a $1 million jumbo CD that is 105 days from maturity. The CD has a quoted annual interest rate of 5.16% for a 360-day year. • The bond equivalent yield is: ibey = ispy × (365/360) = 5.16% × (365/360) = 5.232% • The EAR on the CD is calculated as: EAR = [1+ 5.232%× (105/365)] 365/105 -1 = 5.33%

Comparison of discount yield, bond equivalent yield, and EAR

• You purchase a $1 million Treasury bill that is selling on a discount basis (with no interest payments) at 94.5 percent of its face value. The T-bill is 179 days from maturity. Calculate its discount yield, bond equivalent yield, and EAR.

Money market characteristics

• They are sold in large denominations (usually in units of $1 million to $10 million). • They can generally be issued only by highquality borrowers, so they have low default risk. • Their original maturity is one year or less.

financial markets and institutions

Factor markets

要素市场:分配土地、劳动力与资本等生产 要素的市场。 产品市场 :商品和服务进行交易的市场

产品市场 生产单位 (企业和 政府)

资金的流动 金融服务 收入与金融求偿权的流动

消费单位 (居民)

要素市场

• The purpose of financial markets is to efficiently allocate savings to ultimate users.

俄罗斯最大的石 油公司腊克 (Lukoil)石油公 司1995年的评估价 值是8.5亿美元 该公司拥有的油 田已被证实的储量 是160亿桶 英壳牌石油公司 1995年的市值为 940亿美元 该公司拥有的油 田已被证实的储量 是170亿桶 即它的石油每桶 超过5美元。

它的石油每桶只 值约5美分。

Demanders of funds (mainly business firms and governments)

Flow of loanable funds (savings) Flow of financial services, incomes, and financial claims

Suppliers of funds (mainly households)

Why Study Financial Markets?

• What’s financial market? • Do financial markets create value? • How financial markets create value?

Do financial markets create value?

2、宏观金融学(Macro Finance)

Lecture 2 Financial Markets and Institutions

Lecture 2Financial Markets and Institutions Function of Financial Markets∙将存款转换为投资∙跨期间使用资金eg.存款,养老金∙转移风险和多样化eg.保险,期货保值futures hedge∙资金流动性eg.存款V.S 股票市场,贷款∙支付机制eg.信用卡,电子交易(clearance清算&settlement 交付)∙提供信息eg.利率,市值,商品价格Financial Markets金融市场A.为公司和国家带来成长和利益/生产力eg.苹果公司1976年以$250,000成立公司=>2005留存收益$3.2 billion)B.融资决定实行的地方——交换(交易所, 银行借贷vs. 民间借贷)企业金融决定:•资金来源(股票/债券——风险不同)•资本结构(融资风险和资金基础)C.市场参与者∙企业(运营,年报,预估收益,电话会议)∙投资者(个人/机构,包括风险投资venture capital)∙证券公司Securities firms, CPA会计师事务所,律师行(具有经纪业务的券商Brokerage, 承销商Underwriter, 审计员Auditor, 律师)∙信息商Information vendor(金融分析,新闻,信用评级)D.交易平台∙股票市场(equity market)eg. NYSE, NASDAQ, OTCBB∙外汇市场∙债券市场(固定利息,现在不一定)∙货币市场(同业拆借市场、票据贴现市场、短期政府债券市场…)∙金融衍生品eg.期权options, 期货futures, 远期forward, 互换swap∙商品市场eg.煤炭、黄金、大豆∙金融市场(直接融资Direct Financing)eg.股票、债券、货币、期货、期权、外汇E.市场微结构1.一级市场行为:IPO首发,SPO/SEO再发∙询价圈购bookbuilding:承销商在现金增资前,先推广,由潜在投资者无拘束力的预购中得之市场对于释股的需求。

Financial Markets and Institutions (4)

Probability Return Probability Outcome 2 Return Outcome 1

50% 15% 50% 5%

100% 10%

EXAMPLE 2: Standard Deviation (b)

• What is the standard deviation of the returns on the Fly-by-Night Airlines stock and Feet-on-the-Ground Bus Company, with the return outcomes and probabilities described above? Of these two stocks, which is riskier?

• We learned in Chapter 3 that interest rates are negatively related to the price of bonds, so if we can explain why bond prices change, we can also explain why interest rates fluctuate. • Here we will apply supply-and-demand analysis to examine how bond prices and interest rates change. Topics include:

1. 2. 3. 4. Wealth, the total resources owned by the individual, including all assets. Expected return (the return expected over the next period) on one asset relative to alternative assets Risk (the degree of uncertainty associated with the return) on one asset relative to alternative assets Liquidity (the ease and speed with which an asset can be turned into cash) relative to alternative assets

financial markets and institutions 金融市场与机构

Overview of Financial Markets

Broad Classifications of Financial Markets

Money versus Capital Markets Primary versus Secondary Markets Organized versus Over-the-Counter Markets

Range of Issuer Quality

Debt Only

Debt and Equity

Primary Market Focus

Secondary Market Focus

Liquidity Market--Low Returns

Hale Waihona Puke Financing Investment-Higher Returns

Organized vs. Over-the-Counter Markets

Organized

Visible Marketplace

Members Trade

Securities Listed

OTC

Wired Network of Dealers

No Central, Physical Location

Debt vs. Equity Securities

Equity Securities: Claim with ownership rights and responsibilities

Investor receives dividends if declared Capital gain/loss when sold No maturity date—need market to sell

Institutions

financial-markets-and-institutions-金融市场与机构

Financial Markets and Institutions 6th Edition

By Jeff Madura Prepared by David R. Durst

The University of Akron

第1页,共78页。

CHAPTER

1

u Investor receives dividends if declared u Capital gain/loss when sold u No maturity date—need market to sell

第11页,共78页。

Valuation of Securities

n Value a function of:

第12页,共78页。

Investor Assessment of New Information

Economic Conditions

Industry Conditions

Impact of Future Cash

Flows

Evaluation of Security

Pricing

Investor Decision to

பைடு நூலகம்第21页,共78页。

Role of Nondepository Financial Institutions

n Focused on capital market n Longer-term, higher risk intermediation n Less focus on liquidity n Less regulation n Greater focus on equity investments

第15页,共78页。

Financial Markets and Institutions 第一章

Debt vs. Equity Securities

Equity Securities: Claim with ownership rights and responsibilities

Investor

receives dividends if declared Capital gain/loss when sold No maturity date—need market to sell

on a Stock Dividend Capital Income Gain (or Loss)

Total Dollar Return

Example:

Percent Returns

Total percent return is the return on an investment measured as a percentage of the original investment. The total percent return is the return for each dollar invested. Example, you buy a share of stock:

Annualizing Returns, II

1 + EAR = (1 + holding period percentage return)m m = the number of holding periods in a year.

In this example, m = 4 (12 months / 3 months). Therefore: 1 + EAR = (1 + .0556)4 = 1.2416.

Financial Markets and Institutions 第二章

Loanable Funds Theory

Government Demand for Loanable Funds

When planned expenditures exceed revenues from taxes, the government demands loanable funds Municipal (state and local) governments issue municipal bonds Federal government and its agencies issue Treasury securities and federal agency securities.

Businesses

choose projects by calculating the project’s Net Present Value Select all projects with +NPV’s

Loanable Funds Theory

Business Demand for Loanable Funds

Sum of sector demand (quantity) at varying levels of interest rates Sector cash receipts in period less than outlays = borrower Quantity demanded inversely related to interest rates Variables other than interest rate changes cause shift in demand curve

Example:

Economic conditions become more favorable Expected cash flows will increase > more positive NPV projects > increased demand for loanable funds

金融学 经典 十大书籍

金融学经典十大书籍金融学是现代社会非常重要的一门学科,涉及到金融市场、投资、风险管理等诸多领域。

对于想要深入了解金融学的人来说,阅读经典的金融学书籍是一种很好的学习途径。

下面是十本被公认为金融学经典之作的书籍,它们涵盖了金融学的各个方面,对于金融学的学习和研究具有重要的参考价值。

1.《金融市场与机构》(Financial Markets and Institutions)《金融市场与机构》是金融学领域的经典教材之一,作者是美国经济学家弗雷德里克·S·米什金。

本书对金融市场的运作、金融机构的功能和角色等进行了深入的分析和阐述,是理解金融市场和金融机构的基础。

2.《金融学原理》(Principles of Corporate Finance)《金融学原理》是美国经济学家理查德·A·布雷利、斯图尔特·C·迈尔斯和弗兰克林·艾伦的合著,是金融学领域的经典教材之一。

本书系统介绍了公司金融学的基本原理和方法,包括投资决策、融资决策和股东权益等内容,对于企业金融决策具有重要的指导意义。

3.《证券分析》(Security Analysis)《证券分析》是美国经济学家本杰明·格雷厄姆和大卫·杜杜勒的合著,被誉为价值投资的圣经。

本书介绍了证券分析的基本原理和方法,包括财务分析、估值方法等,对于投资者进行价值投资具有重要的指导意义。

4.《期权、期货和其他衍生品》(Options, Futures, and Other Derivatives)《期权、期货和其他衍生品》是美国经济学家约翰·C·哈尔的著作,是关于金融衍生品的经典教材。

本书介绍了期权、期货和其他衍生品的基本概念、定价模型和交易策略等内容,对于理解和应用金融衍生品具有重要的参考价值。

5.《金融工程》(Financial Engineering)《金融工程》是美国经济学家罗伯特·C·米顿的著作,是关于金融工程学的经典教材。

Foundations of Financial Markets and Institutions 金融市场与机构基础

Common stock Preferred stock Foreign stock

Debt vs. Equity

Debt Instruments

Fixed dollar payments (‘fixed income’) Examples include loans, bonds

Equity Claims

Classification of Financial Markets

Nature of asset: debt vs. equity markets Maturity: money (short) vs. capital (long) markets Seasoning: primary vs. secondary markets Structure: auction vs. over-the-counter (OTC).

search costs information costs (market efficiency)

Financial Market Participants

Households Business units Federal, state, and local governments Government agencies International organizations (e.g. World bank) Regulators (broader definition)

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

• Main roles:

• Regulate commercial banks • Control monetary policy

Ben S. Bernanke

• Adjusting the reserve requirement ratio

• The reserve requirement ratio is the proportion of bank deposits that must be held as reserves

• Set by the Board of Governors • Historically set between 8 and 12 percent • Sometimes changed to adjust the money supply as a reduction increases the proportion of bank deposits that can be lent out

Zhou Xiaochuan

The Chairman of US Fed and the Governor of the PBOC

Organization of the Fed

• Federal Open Market Committee (FOMC)

• The FOMC consists of the seven members of the Board of Governors and the presidents of five Fed district banks • Goals: promote high employment, economic growth, and price stability by controlling the money supply.

Monetary Policy Tools

• Open market operations

• When Fed purchases securities

• The total funds of commercial banks increase. • Leading to a loosening of the money supply • To force a decline in the Fed funds rate, the Trading Desk can also purchase Treasury securities • Other interest rates will decline as well.

Monetary Policy Tools

• Open market operations

• When Fed sells securities

• Traders sell government securities to government securities dealers to decrease the money supply. • As dealers pay, their account balances are reduced and the total amount of funds at commercial banks is reduced • Leading to a tightening of the money supply • To force an increase in the Fed funds rate, the Trading Desk can also sell Treasury securities

• Loans from the Fed serve as a backup source of funds • The discount rate no longer serves as a signal about the Fed’s monetary policy

Monetary Policy Tools

• The fed funds rate may decline • Banks with excess funds may offer new loans at a lower interest rate • The reduction in yields on debt securities lowers the cost of borrowing for the issuers of debt securities • It can encourage potential expenditures

• Six elected by member banks, and three appointed by the Board of Governors • The nine directors appoint the president of the district bank.

• District banks clear checks, replace old currency, provide loans to depository institutions, and conduct research

12 Federal Reserve district banks

Organization of the Fed

• ard of Governors

• The Board of Governors consists of seven members, which are appointed by the President and confirmed by the Senate • Members serve 14-year non-renewable terms

• Recently, the Fed has often adjusted the discount rate to keep it in line with changes in the targeted federal funds rate • In January 2003, the Fed set the discount rate at a level above the federal funds rate

Monetary Policy Tools

• Open market operations

• When Fed uses repurchase agreements

• Used to increase the aggregate level of bank funds for only a few days. E.g. during holidays to correct temporary imbalances. • The Trading Desk trades repurchase agreements. • Purchases of Treasury securities with an agreement to sell back at a specified date in the near future.

Monetary Policy Tools

• Open market operations

• FOMC specifies a target range for the money supply growth and a desired target for the federal funds rate. • The federal funds rate is the rate charged by banks on short-term loans to each other

Monetary Policy Tools

• Comparison of monetary policy tools

• The most frequent monetary policy tool is open market operations

• Open market operations can be used without signaling the Fed’s intentions and can be easily reversed • Adjustments in the discount rate only work if depository institutions respond to the adjustment • Adjustments in the reserve requirement ratio can cause erratic shifts in the money supply

Federal Reserve Components

Board of Governors •Regulates member banks and BHCs •Sets reserve requirements Federal Open Market Committee •Conducts open market operations

Monetary Policy Tools

• How open market operations affect interest rates

• When the Fed increase bank funds by buying securities, interest rates are affected because:

• The FOMC meets 8 times a year to determine target money supply growth level and interest rate level. • Members receive the Beige Book two weeks before to the meeting • Meeting is attended by the Board of Governors, the 12 presidents of the district banks, and staff members