2012年6月全国单证员缮制与操作试题

6月全国国际商务单证员考试国际商务操作考试真题答案

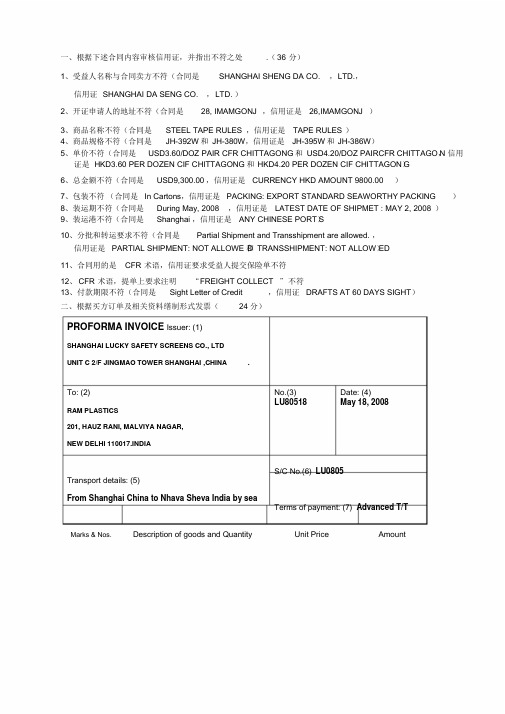

一、根据下述合同内容审核信用证,并指出不符之处.(36 分)1、受益人名称与合同卖方不符(合同是SHANGHAI SHENG DA CO. ,LTD.,信用证SHANGHAI DA SENG CO. ,LTD. )2、开证申请人的地址不符(合同是28, IMAMGONJ ,信用证是26,IMAMGONJ )3、商品名称不符(合同是STEEL TAPE RULES ,信用证是TAPE RULES )4、商品规格不符(合同是JH-392W和JH-380W,信用证是JH-395W和JH-386W)5、单价不符(合同是USD3.60/DOZ PAIR CFR CHITTAGONG和USD4.20/DOZ PAIRCFR CHITTAGO,N信用证是HKD3.60 PER DOZEN CIF CHITTAGONG和HKD4.20 PER DOZEN CIF CHITTAGON)G6、总金额不符(合同是USD9,300.00 ,信用证是CURRENCY HKD AMOUNT 9800.00 )7、包装不符(合同是In Cartons,信用证是PACKING: EXPORT STANDARD SEAWORTHY PACKING )8、装运期不符(合同是During May, 2008 ,信用证是LATEST DATE OF SHIPMET : MAY 2, 2008 )9、装运港不符(合同是Shanghai ,信用证是ANY CHINESE PORT)S10、分批和转运要求不符(合同是Partial Shipment and Transshipment are allowed. ,信用证是PARTIAL SHIPMENT: NOT ALLOWE和D TRANSSHIPMENT: NOT ALLOW)ED11、合同用的是CFR 术语,信用证要求受益人提交保险单不符12、CFR 术语,提单上要求注明“FREIGHT COLLECT ”不符13、付款期限不符(合同是Sight Letter of Credit ,信用证DRAFTS AT 60 DAYS SIGHT)二、根据买方订单及相关资料缮制形式发票(24 分)PROFORMA INVOICE Issuer: (1)SHANGHAI LUCKY SAFETY SCREENS CO., LTDUNIT C 2/F JINGMAO TOWER SHANGHAI ,CHINA .To: (2) No.(3) Date: (4)LU80518 May 18, 2008RAM PLASTICS201, HAUZ RANI, MALVIYA NAGAR,NEW DELHI 110017.INDIAS/C No.(6) LU0805Transport details: (5)From Shanghai China to Nhava Sheva India by seaTerms of payment: (7) Advanced T/T Marks & Nos. Description of goods and Quantity Unit Price Amount1 / 5(8) (9) (10)CIF Nhava Sheva (11)R.P. 200mm x 2mm x 50m transparent USD86.00/roll USD10320.00 LU80518 normal 120 rolls USD98.00/roll USD 980.00200mm x 2mm x 50m transparentNhava Sheva USD92.00/roll USD 1840.00 normal ribbed 10 rollsNos 1- up USD108.00/roll USD 3240.00 200mm x 3mm x 50m transparentUSD116.00/roll USD 2320.00 normal 20 rollsUSD18700.00 300mm x 3mm x50m transparentnormal 30 rolls300mm x 3mm x50m transparentnormal ribbed 20 rolls200 rolls(12) DETAILS OF OUR BANK:BANK OF CHINA, SHANGHAI BRANCH,NO.4 Zhongshan road, Shanghai ,P.R.CHINASWIFT CODE: BKCHCNBJ530BENEFICIARY: SHANGHAI LUCKY SAFETY SCREENS CO., LTDACCOUNT NO: 1281 2242012 7091 015ADDRESS: UNIT C 2/F JINGMAO TOWER SHANGHAI ,CHINASHANGHAI LUCKY SAFETY SCREENS CO., LTD地证FORM A (共40 分)票、海运提单、汇票及普惠制产三、根据合同、信用证及补充资料缮制商业发凭信用证号Drawn under industrial bank of Japan,ltd.,head office L/C NO. LC196107800日期按⋯. . 息⋯. 付款Dated Oct.15,2007 Payable with interest @⋯.. % per annum 上海汇票金额号码NO. YL71001 Exchange for USD12630.00 Shanghai ⋯DEC.05,2007 ⋯⋯⋯⋯⋯见票⋯⋯⋯⋯⋯⋯⋯日后(本汇票之正本未付)付交At *** sight of this FIRST of Exchange (Second of Exchange being unpaid)Pay to the order of BANK OF CHINA,SHANGHAI BRANCH金额the sum of SAY US DOLLARS TWELVE THOUSAND SIX HUNDRED AND THIRTY ONLY此致To: INDUSTRIAL BANK OF JAPAN,HEAD OFFICESHANGHAI YILONG CO. ,LTD.XXX2 / 5COMMERCIAL INVOICE Issuer: SHANGHAI YILONG CO. ,LTD.NO.91 NANING ROADSHANGHAI ,CHINATo: ABC COMPANY1-3 MACHI KU STREETNo. YL71001 Date: NOV.10,2007 OSAKA ,JAPANTransport details: S/C No. YL07101FROM SHANGHAI PORT TO OSAKA BY SEA Terms of payment: L/C AT SIGHTMarks andNumber and kind of packages;Unit Price Amount Nos.Description of goods and QuantityABC USD 6975.00CIF OSAKA3000PCS OF CARDBOARD BOXOSAKA USD4.50/PC USD 5655.00NOS.1-60YL-256 1550PCSYL-286 1450PCSUSD3.90/PC -------------------___________USD 12,630.00SHANGHAI YILONG CO. ,LTD.X X X.Shipper Insert Name, Address and PhoneSHANGHAI YILONG CO. ,LTD. B/L No. TH14HK07596NO.91 NANING ROAD SHANGHAI ,CHINA.中远集装箱运输有限公.Consignee Insert Name, Address and Phone司TO ORDERCOSCO CONTAINER LINES Notify Party Insert Name, Address and Phone(It is agreed that no responsibility shall attach to the Carrier orPort-to-Port or Combined Transport his agents for failure to notify)BILL OF LADING ABC COMPANY1-3 MACHI KU STREET OSAKA ,JAPANRECEIVED In external apparent good order and condition except as other- wise noted. The total number of packages or units stuffed in the container, Combined Transport * Combined Transport *the description of the goods and the weights shown in this Bill of Loading are Pre-carriage by Place of Receiptfurnished by the Merchants, and which the carrier has no reasonable meansof checking and is not a part of this Bill of Loading contract. The carrier has Ocean Vessel Voy. No..Port of Loadingissued the number of Bills of Lading stated below, all of this tenor and date,one of the original Bills of Lading must be surrendered and endorsed or sig- KAOHSIUNG V.0707S SHANGHAI PORTned against the delivery of the shipment and whereupon any other original Bills of Lading shall be void. The Merchants agree to be bound by the terms3 / 5.Port of Discharge C ombined Transport * And conditions of this Bill of Lading as if each had personally signed this Billof Lading.OSAKA P lace of Delivery SEE clause 4 on the back of this Bill of Lading (Terms continued on the backhereof, please read carefully)*Applicable Only When Document Used as a Combined Transport Bill of Lading.Marks & Nos. Container / Seal No. ABC No. ofContainersor Packages60 CARTONSDescription of Goods (IfDangerous Goods, See Clause20)CARDBOARD BOXGross Weight Kgs2160.0KGSMeasurement33.0CBMCFS-CFSOSAKA ybdeh s i n r u F s r a l u c i t r a P stnahcreMNOS.1-60C/N:SNBU7121820Description of Contents for Shipper ’s Use Only (Not Part of This B/L Contract) .Total Number Of Containers and/or Packages (In Words) SAY SIXTY CARTONS ONLYRevenue Tons Rate Per Prepaid CollectFreight & ChargesFREIGHT PREPAIDEx Rate: Prepaid at Payable at Place and date of IssueSHANGHAI PORTSHANGHAI,NOV 29,2007Signed for the Carrier: COSCO CONTAINER LINESTotal Prepaid No. of Original B(s)/LTHREELADEN ON BOARD THE VESSELDATE:NOV29,2007 BYKAOHSIUNG V.0707SCOSCO CONTAINER LINESCNS01 01088951.Goods consigned from (Exporter ’s full name Reference No. 20070819and address, country) GENERALIZED SYSTEM OF PREFERENCES SHANGHAI YILONG CO. ,LTD. CERTIFICATE OF ORIGINNO.91 NANING ROAD (Combined declaration and certificate) SHANGHAI ,CHINA. FORM A2.Goods consigned to (Consignee ’s Full name, address, Issued in THE PEOPLE ’S REPUBLIC OF CHINA country) (Country)ABC COMPANYSee Notes. Overleaf1-3 MACHI KU STREETOSAKA ,JAPAN3.Means of transport and route (as for as known)4. For certifying authority use only FROM SHANGHAI PORT TO OSAKA BY SEA4 / 52160.1Item 6.Marls and 7.Number and kind of packages; 8.Origin 9.Gross 10.Number number Numbers of Description of goods Criterion Weight And datePackages 60 CARTONS (SIXTY CARTONSONLY) CARDBOARD BOX(see Or other of invoices *******************************************ABC Notes QuantityINV No.:OSAKA Overleaf)G.W: YL71001NOS.1-60 “P”2160.00KGS DATED:NOV 10,2007 33.1Certification 12.Declaration by the exporterIt is hereby certified that the declaration by the The undersigned hereby declares that the aboveexporter is correct. Details and statements are correct, that all theCIQ Goods were produced in CHINASHANGHAI,NOV 25,2007 XXX and that they Comply with the origin requirementsPlace and date, signature and stamp of Certifying specified for those goods in the Generalized System of authority preferences for goods exported to(importing country)JAPANPlace and date, Signature and stamp of AuthorizedsignatorySHANGHAI,NOV 25,2007 XXX5 / 5。

2012年单证员考试国际商务单证缮制与操作真题试题及答案

Transshipment: AllowedI nsurance: To be effected by the seller for 110% invoice value covering All Risks and War Riskas per CIC of PICC dated 01/01/1981Terms of Payment: By L/C at 60 days after sight, reaching the seller before June 15, 2011, andremaining valid for negotiation in China for further 15 days after the effectedshipment. L/C must mention this contract number. L/C advised by BANK OFCHINA. All banking charges outside China (the mainland of China) are foraccount of the Drawee.Documents:+ Signed commercial invoice in triplicate.+ Full set (3/3) of clean on board ocean Bill of Lading marked Freight Prepaid made out to orderblank endorsed notifying the applicant.+ Insurance Policy in duplicate endorsed in blank.+ Packing List in triplicate.+ Certificate of Origin issued by China Chamber of Commerce.Signed by:THE SELLER: THE BUYER:Tianjin Yimei International Corp. VALUE TRADING ENTERPRISE, LLC Jack Julia信用证:27: SEQUENCE OF TOTAL: 1/140A: FORM OF DOC. CREDIT: IRREVOCABLE20: DOC. CREDIT NUMBER: KR369/0331C: DATE OF ISSUE: 11061940E: APPLICABLE RULES: UCP LATEST VERSION31D: DATE AND PLCA OF EXPIRY: 110825 KUWAIT51D: APPLICANT BANK: VALUE TRADING ENTERPRISE CORP.RM1008 GREEN BUILDING KUWAIT50: APPLICANT: AORE SPECIALTIES MATERIAL CORP.YARIMCA, KOCAELI 41740, IZMIT, TURKEY59: BENEFICIARY: TIANJIN YMEI INTERNATIONAL CORP.58 DONGLI ROAD TIANJIN, CHINA32B: CURRENCY CODE, AMOUNT: USD71500.0041A: AVAILABLE WITH … BY: BANK OF CHINABY NEGOTIATION42C: DRAFTS AT …: 90 DAYS AFTER SIGHT42A: DRAWEE: VALUE TRADING ENTERPRISE, LLC43P: PARTIAL SHIPMENTS: NOT ALLOWED43T: TRANSSHIPMENT: NOT ALLOWED44E: PORT OF LOADING/AIRPORT OF DEPARTURE: ANY CHINESE PORT44F: PORT OF DISCHARGE/ AIRPORT OF DESTINATION: KUWAIT BY SEA FREIGHT44C: LATEST DATE OF SHIPMENT: 11071045A: DESCRIPTION OF GOODS AND / OR SERVICES: 5000PCS WIND BREAKERSTYLE NO. YM085AS PER ORDER NO. A01 AND S/C NO. YM009AT USD15.10/PC CIF KUWAITPACKED IN CARTON OF 20PCS EACH46A: DOCUMENTS REQUIRED+ SIGNED COMMERCIAL INVOICE IN TRIPLICATE INDICATING LC NO. ANDCONTRACT NO.+ FULL SET (3/3) OF CLEAN ON BOARD OCEAN BILL OF LADING MADE OUT TOAPPLICANT AND BLANK ENDOSED MARKED “FREIGHT TO COLLECT”NOTIFY THE APPLICANT+ SIGNED PACKING LIST IN TRIPLICATE SHOWING THE FOLLOWING DETAILS:TOTAL NUMBER OF PACKAGES SHIPPED; CONTENT(S) OF PACKAGE(S), GROSSWEIGHT, NET WEIGHT AND MEASUREMENT.+ CERTIFICATE OF ORIGIN ISSUED AND SIGNED OR AUTHENTICATED BY ALOCAL CHAMBER OF COMMERCE LOCATED IN THE EXPORTING COUNTRY.+ INSURANCE POLICY/CERTIFICATE IN DUPLICATE ENDORSED IN BLANK FOR 120%INVOICE VALUE, COVERING ALL RISKS AND WAR RISK OF CIC OF PICC(1/1/1981) 71B: CHARGES: ALL CHARGES AND COMMISSIONS ARE FOR ACCOUNT OFBENEFICIARY INCLUDING REIMBURSING CHARGES经审核,信用证存在问题如下:1.31D信用证到期时间错,应该是110815;2.31D信用证到期地点错,应该是CHINA;3.50申请人名称错,应该是VALUE TRADING ENTERPRISE, LLC.;4.59受益人名称错,应该是TIANJIN YIMEI INTERNATIONAL CORP.;5.32B金额错,应该是USD75500.00;6.42C汇票期限错,应该是60 DAYS AFTER SIGHT;7.42A汇票付款人错,应该是开证银行;8.43T转运要求错,应该是ALLOWED;9.44E装运港错,应该是TIANJIN, CHINA;10.44F卸货港错,应该是KUWAIT;11.44C最晚装运日错,应该是110731;12.45A货物名称错,应该是MEN’S WIND BREAKER;13.45A合同号码错,应该是YM0806009;14.45A贸易术语错,应该是CIFC5KUWAIT;15.46A第2条提单抬头错,应该是MADE OUT TO ORDER;16.46A第2条提单运费显示错,应该是FREIGHT PREPAID;17.46A第5条保单加成错,应该是FOR 110% INVOICE VALUE;18.71B银行费用错,应该是FOR ACCOUNT OF THE DRAWEE。

2012 年 全 国 国 际 商 务 单 证 员 专 业 考 试

2012 年全国国际商务单证员专业考试国际商务单证基础理论与知识试题一、单项选择题(50小题,每小题1分,共50分。

单项选择题的答案只能选一个,多选不得分,请在答题卡上将相应的选项涂黑)1.非信用证支付方式下制单和审单的首要依据是(B)。

A.信用证B.买卖合同C.相关国际惯例D.有关商品的原始资料2.某出口公司对外以CFR报价,如果该货物采用多式联运,应采用( D )术语为宜。

A.FCA B.CIP C.DDP D.CPT3.付款人对远期汇票表示承担到期付款责任的行为叫(C )。

A.见票B.即期付款C.承兑D.远期付款4.结汇单据中最重要的单据,能让有关当事人了解一笔交易的全貌。

其他单据都是以其为依据的是( A )。

A.商业发票B.保单C.装箱单D.产地证5.海关对法定检验的进口货物凭出入境检验检疫机构签发的( D )办理海关通关手续。

A.进口许可证B.进口货物报关单C.查验通知D.入境货物通关单6.按照INCOTERMS2010,以CIF汉堡贸易术语成交,卖方对货物风险应负责至( C )。

A.船到汉堡港为止B.在汉堡港卸下船为止C.货在装运港装上船为止D.货在装运港越过船舷为止7.按《联合国国际货物销售合同公约》的规定,一项发盘(C)。

A.必须表明各项交易条件B.必须表明主要交易条件C.只需表明货物名称、数量和单价D.只需表明品质、数量和价格8.国际贸易中使用的金融票据主要有汇票、本票和支票。

其中( A )使用最多。

A.汇票B.本票C.支票D.以上都对9.出票人签发支票时,应在付款银行存有不低于票面金额的存款。

如果存款低于票面金额,这种支票被称为( A )。

A.空头支票B.划线支票C.现金支票D.转账10.进出口业务中,T/T表示(A)。

A.电汇B.票汇C.信汇D.托收11.通过汇出行开立的银行汇票的转移实现货款支付的汇付方式是( C )。

A.电汇B.信汇C.票汇D.托收12.托收方式下,出口方开具汇票上的付款人是(A)。

外贸类《单证员》缮制与操作《缮制与操作》考试试题及答案解析

外贸类《单证员》缮制与操作《缮制与操作》考试试题及答案解析姓名:_____________ 年级:____________ 学号:______________1、根据《 UCP600》的规定,银行审单时间最多为收到单据次日起的第( ) 银行工作日。

A 、3个B 、5个C 、7个D 、10个正确答案:B答案解析:暂无解析2、开立信用证时要注意( )。

A、证同一致B 、单证一致C 、单单一致D 、单货一致正确答案:A答案解析:暂无解析3、根据《海关法》规定,进口货物的报关期限为自运输工具申报进境之日起 14 天之内,进口货物的收货人或其代理人逾期申报的,由海关征收滞报金,滞报金的日征收额为进口货物完税价的( )。

A 、5%B 、05%C 、5D 、05%正确答案:D答案解析:暂无解析4、合同上货物名称是“ SHIRTS”,信用证上的名称误为“SKIRTS”,受益人( )。

A 、应该修改信用证,把货物名称改准确B 、不必修改信用证,按SHIRTS 制单C 、不必修改信用证,按SKIRTS 制单D 、不必修改信用证,按SKIRTS(SHIRTS)制单正确答案:A答案解析:暂无解析5、汇票上的出票日期也称汇票日期,是全套单据日期( )。

A、最晚的一个,但不能晚于信用证有效期和规定的交单期B、最晚的一个,能够晚于信用证有效期C、最早的一个,但不要早于信用证开证日期D、最早的一个,能够早于信用证开证日期正确答案:A答案解析:暂无解析6、预约保险以 ( ) 代替投保单,说明投保的一方已办理了投保手续。

A、提单B、国外的装运通知C、大副收据D、买卖合同正确答案:B答案解析:暂无解析7、发生( ) ,违约方可援引不可抗力条款要求免责。

A、战争B、世界市场价格上涨C、生产制作过程中的过失D、货币贬值正确答案:A答案解析:暂无解析8、货物外包装上有一只酒杯或一把雨伞,这种标志属于()。

A、危险性标志B、指示性标志C、警告性标志D、易燃性标志正确答案:B答案解析:暂无解析9、在海洋运输货物保险业务中,共同海损()。

2012年全国国际商务单证员考试试题

2012年全国国际商务单证员考试试题姓名:林跃宇考号: 120090803114考生所在单位: 闽江学院一、单项选择题:在每小题的备选答案中选出一个正确答案,并将正确答案的代码填在题干上的括号内。

(每小题0.5分,本大题共10分)1、根据《INCOTERMS2000》,以CIF贸易术语成交合同,如果买卖双方无其他约定,卖方可以向保险公司投保()。

A、F.P.A.B、W.A.C、ALL RISKSD、ICC(A)2、托收是出口人委托并通过银行收取货款的一种支付方式,在托收方式下,使用的汇票是(),属于()。

A、商业汇票;商业信用B、银行汇票;银行信用C、商业汇票;银行信用D、银行汇票;商业信用3、《国际贸易术语解释通则》是由()制定的。

A、国际法协会B、国际商会C、联合国贸发会D、联合国国际法委员会4、报关是指进出境运输工具的负责人、进出境物品的所有人、进出口货物的收发货人或其代理人向()办理进出境手续的全过程。

A、边检B、海关C、进出境商品检验检疫局D、外经贸部门5、按照《2000年通则》的解释,采用CIF条件成交,买卖双方风险划分的界限是()。

A、装运港船边B、装运港船上C、装运港船舷D、目的港船舷6、使用托收方式时,托收行和代收行在货款收进方面()A、没有责任B、承担部分责任C、有责任D、视情况分析7、我国出口到蒙古的杂货运输应选择()A、海洋运输B、铁路运输C、航空运输D、管道运输8、CIF合同的货物在装船后因火灾被焚,应由()A、卖方负担损失B、卖方请求保险公司赔偿C、买方请示保险公司赔偿D、买方负担损失并请求保险公司赔偿9、从交货方式上看,CIF是一种典型的象征性交货。

此语的含义为()A、卖方以态度明确的函电表示交货B、卖方以提交全套合格单据来履行交货义务C、卖方无须实际准备足货,只要少量样品即可代表D、买方对不符合合同要求的货物,只要单据合格,无权索赔10、在L/C、D/P和D/A三种支付方式下,就买方风险而言,按由大到小排列,哪个正确()A、L/C > D/A > D/PB、L/C > D/P > D/AC、D/A > D/P > L/CD、D/P > D/A > L/C11、指出“装船提单”的日期()A、货于5月24日送交船公司B、货于6月4日开始装船C、货于6月4日全部装完D、货于6月24日抵达日本12、《90通则》,若以CFR成交,风险划分点为()A、以货越船舷为界B、以货交第一承运人为界C、以目的港交货为界D、以船边交货为界13、修订《华沙—牛津规则》的机构为()。

2012年单证员考试辅导试卷及答案(1)

2012年单证员考试辅导试卷及答案(1)⼀、单项选择题(本⼤题共10⼩题,每⼩题1分,共10分)1.如2007年,某国出⼝贸易额为380亿美元,进⼝额为360亿美元,则该国()A.净出⼝额为20亿美元B.贸易顺差为20亿美元C.净进⼝额为20亿美元D.贸易逆差为20亿美元2、对于⼤批量交易的散装货,因较难掌握商品的数量,通常在合同中规定()A.品质公差条款B.溢短装条款C.⽴即装运条款D.仓⾄仓条款3.L/C与托收相结合的⽀付⽅式,其全套货运单据应()A.随信⽤证项下的汇票B.随托收项下的汇票C.50%随信⽤证项下的汇票,50%随托收项下的汇票D.单据与票据分列在信⽤证和托收汇票项下4、信⽤证的第⼀付款⼈是()A.进⼝⼈B.开证⾏C.议付⾏D.通知⾏5、⼀张经过了五次背书的汇票,其“前⼿”最多有()个。

A.3B.4C.5D.66、出⼝总成本是指()A.进货成本B.进货成本+出⼝前⼀切费⽤C.进货成本+出⼝前的⼀切费⽤+出⼝前的⼀切税⾦D.对外销售价7、承兑是()对远期汇票表⽰承担到期付款责任的⾏为。

A.付款⼈B.收款⼈C.出⼝⼈D.开证银⾏8、根据《联合国国际货物销售合同公约》的规定,发盘和接受的⽣效采取()A.投邮⽣效原则B.签订书⾯合约原则C.⼝头协商原则D.到达⽣效原则9、审核信⽤证的依据是()A.开证申请书B.—整套单据C.合同D.商业发票10、以下我出⼝商品的单价,只有()的表达是正确的。

A.250美元/桶B.250美元/桶CIF伦敦C.250美元/桶CIF⼴州D.250美元⼆、多项选择题(本⼤题共10⼩题,每⼩题2分,共20分)1.对于信⽤证与合同关系的表述正确的是()A.信⽤证的开⽴以买卖合同为依据B.信⽤证的履⾏不受买卖合同的约束C.有关银⾏只根据信⽤证的规定办理信⽤证业务D.合同是审核信⽤证的依据2、在国际贸易中,最常⽤的⽀付⽅式有()A.预付B.汇付C.托收D.信⽤证3、FOB、CFR、CIF和FCA、CPT、CIP术语的主要区别是()A.适⽤的运输⽅式不同B.风险转移的地点不同C.装卸费⽤的负担不同D.运输单据不同4、在国际贸易中,解决争议的⽅法主要有()A.友好协商B.调解C.仲裁D.诉讼5、交易磋商程序中,必不可少的两个法律环节是()A.询盘B.发盘C.还盘D.接受6、若买卖双⽅以CFR卸⾄岸上术语成交,以下答案正确的是()A.卖⽅应承担货物运⾄⽬的港以前的⼀切风险B.当货物卸⾄⽬的港后,卖⽅的交货完毕C.装运港的船舷是买卖双⽅风险划分的界限D.卖⽅在装运港船上完成交货义务7、⼀⽅同意以每公吨300美元的价格向买⽅出售1200公吨⼀级⼤⽶,合同和信⽤证⾦额都为36万美元。

2012年单证员考试《操作与缮制》模拟试题及答案

2012年单证员考试《操作与缮制》模拟试题及答案一、单项选择题1.在信用证支付方式的交易中,制作单据的主要依据是()。

A.买卖合同B.信用证C.发票D.进出口许可证2.汇票的受票人即付款人的表示法,在托收方式项下,T0后面填()。

A.一般TO后面填进口商,当合同或进口商有特别要求时,可考虑按要求办理B.出口商C.出口商的议付行D.通知行3.采用信用证方式的,按L/C要求办,若没有具体要求时,发票的抬头应做成()。

A.受益人B.开证行C.L/C的开证申请人D.议付行4.当L/C规定INVOICE TO BE MADE IN THE NAME OF ABC…,应理解为()。

A.一般写成××(中间商)FOR ACCOUNT OF ABC(实际购货方,真正的付款人)B.将受益人AB作为发票的抬头人C.议付行ABC作发票的抬头D.将ABC作为发票的抬头人5.装货港和卸货港的表示方法,发票、产地证、海关发票等单据的这两部分内容的表达方法较简单,一般按()。

A.货运人的意愿填B.合同和信用证价格条款以及实际情况填C.买方的意愿填D.开证行的意愿填6.“抬头人”,表明发票是开给谁的,一般应是()进口商的名称和详细地址。

如为信用证支付。

A.出口商的名称和详细地址B.进口商银行的名称和详细地址C.出口商银行的名称和详细地址D.进口商的名称和详细地址7.托运人(Shipper),亦称发货人(Consignor),一般应为()。

A.信用证申请人B.进口商或其代理人C.出口商或信用证的受益人D.议付行8.保险金额大小写必须一致;金额必须符合信用证的要求,如信用证未注明金额要求时,应按发票上货物金额的()投保。

投保货币按信用证(有特殊规定的除外)。

A.110%B.100%C.90%D.120%9.如果信用证没有规定装运日期,应理解为装运期与该证有效期为同一天即双到期。

P3真题2012年6月

P a p e r P 3This is a blank page.The question paper begins on page 3.2Section A – This ONE question is compulsory and MUST be attemptedThe following information should be used when answering question 11IntroductionHammond Shoes was formed in 1895 by Richard and William Hammond, two brothers who owned and farmed land in Petatown, in the country of Arnland. At this time, Arnland was undergoing a period of rapid industrial growth and many companies were established that paid low wages and expected employees to work long hours in dangerous and dirty conditions. Workers lived in poor housing, were largely illiterate and had a life expectancy of less than forty years.The Hammond brothers held a set of beliefs that stressed the social obligations of employers. Their beliefs guided their employment principles – education and housing for employees, secure jobs and good working conditions. Hammond Shoes expanded quickly, but it still retained its principles. T oday, the company is a private limited company whose shares are wholly owned by the Hammond family. Hammond Shoes still produce footwear in Petatown, but they now also own almost one hundred retail shops throughout Arnland selling their shoes and boots. The factory (and surrounding land) in Petatown is owned by the company and so are the shops, which is unusual in a country where most commercial properties are leased. In many respects this policy reflects the principles of the family. They are keen to promote ownership and are averse to risk and borrowing. They believe that all stakeholders should be treated fairly.Reflecting this, the company aims to pay all suppliers within 30 days of the invoice date. These are the standard terms of supply in Arnland, although many companies do, in reality, take much longer to pay their creditors.The current Hammond family are still passionate about the beliefs and principles that inspired the founders of the company.Recent historyAlthough the Hammond family still own the company, it is now totally run by professional managers. The last Hammond to have operational responsibility was J ock Hammond, who commissioned and implemented the last upgrade of the production facilities in 1991. In the past five years the Hammond family has taken substantial dividends from the company, whilst leaving the running of the company to the professional managers that they had appointed. During this period the company has been under increased competitive pressure from overseas suppliers who have much lower labour rates and more efficient production facilities. The financial performance of the company has declined rapidly and as a result the Hammond family has recently commissioned a firm of business analysts to undertake a SWOT analysis to help them understand the strategic position of the company.SWOT analysis: Here is the summary SWOT analysis from the business analysts’ report.StrengthsSignificant retail expertise: Hammond Shoes is recognised as a successful retailer with excellent supply systems, bright and welcoming shops and shop employees who are regularly recognised, in independent surveys, for their excellent customer care and extensive product knowledge.Excellent computer systems/software expertise: Some of the success of Hammond Shoes as a retailer is due to its innovative computer systems developed in-house by the company’s information systems department. These systems not only concern the distribution of footwear, but also its design and development. Hammond is acknowledged, by the rest of the industry, as a leader in computer-aided footwear design and distribution.Significant property portfolio: The factory in Petatown is owned by the company and so is a significant amount of the surrounding land. All the retail shops are owned by the company. The company also owns a disused factory in the north of Arnland. This was originally bought as a potential production site, but increasingly competitive imports made its development unviable. The Petatown factory site incorporates a retail shop, but none of the remaining retail shops are near to this factory, or indeed to the disused factory site in the north of the country.WeaknessesHigh production costs: Arnland is a high labour cost economy.Out-dated production facilities: The actual production facilities were last updated in 1991. Current equipment is not efficient in its use of either labour, materials or energy.3[P.T.O.Restricted internet site: Software development has focused on internal systems, rather than internet development. The current website only provides information about Hammond Shoes; it is not possible to buy footwear from the company’s website.OpportunitiesIncreased consumer spending and consumerism: Despite the decline of its manufacturing industries, Arnland remains a prosperous country with high consumer spending. Consumers generally have a high disposable income and are fashion conscious. Parents spend a lot of money on their children, with the aim of ‘making sure that they get a good start in life’.Increased desire for safe family shopping environment: A recent trend is for consumers to prefer shopping in safe, car-free environments where they can visit a variety of shops and restaurants. These shopping villages are increasingly popular.Growth of the green consumer: The numbers of ‘green consumers’ is increasing in Arnland. They are conscious of the energy used in the production and distribution of the products they buy. These consumers also expect suppliers to be socially responsible. A recent television programme on the use of cheap and exploited labour in Orietaria was greeted with a call for a boycott of goods from that country. One of the political parties in Arnland has emphasised environmentally responsible purchasing in its manifesto. It suggests that ‘shorter shipping distances reduce energy use and pollution. Purchasing locally supports communities and local jobs’.ThreatsCheap imports: The lower production costs of overseas countries provide a constant threat. It is still much cheaper to make shoes in Orietaria, 4000 kilometres away, and transport the shoes by sea, road and train to shops in Arnland, where they can be offered at prices that are still significantly lower than the footwear produced by Hammond Shoes.Legislation within Arnland: Arnland has comprehensive legislation on health and safety as well as a statutory minimum wage and generous redundancy rights and payments for employees. The government is likely to extend its employment legislation programme.Recent strategiesSenior management at Hammond Shoes have recently suggested that the company should consider closing its Petatown production plant and move production overseas, perhaps outsourcing to established suppliers in Orietaria and elsewhere. This suggestion was immediately rejected by the Hammond family, who questioned the values of the senior management. The family issued a press release with the aim of re-affirming the core values which underpinned their business. The press release stated that ‘in our view, the day that Hammond Shoes ceases to be a Petatown company, is the day that it closes’. Consequently, the senior management team was asked to propose an alternative strategic direction.The senior management team’s alternative is for the company to upgrade its production facilities to gain labour and energy efficiencies. The cost of this proposal is $37·5m. At a recent scenario planning workshop the management team developed what they considered to be two realistic scenarios. Both scenarios predict that demand for Hammond Shoes’ footwear would be low for the next three years. However, increased productivity and lower labour costs would bring net benefits of $5m in each of these years. After three years the two scenarios differ. The first scenario predicts a continued low demand for the next three years with net benefits still running at $5m per year. The team felt that this option had a probability of 0·7. The alternative scenario (with a probability of 0·3) predicts a higher demand for Hammond’s products due to changes in the external environment. This would lead to net benefits of $10m per year in years four, five and six. All estimated net benefits are based on the discounted future cash flows.Financial information:The following financial information (see Figure 1) is also available for selected recent years for Hammond Shoes manufacturing division.4Figure 1: Extracts from the financial statements of Hammond Shoes (2007–2011)Extracted from the income statements (all figures in $m)201120092007 Revenue700750850Cost of sales(575)(600)(650) Gross profit125150200 Administration expenses(95)(100)(110) Other expenses(10)(15)(20) Finance costs(15)(10)(5)Profit before tax52565 Income tax expense(3)(7)(10)Profit for the year21855 Extracted from statements of financial position (all figures in $m)T rade receivables708090 Share capital100100100 Retained earnings140160170Long term borrowings705020In 2007, Hammond Shoes paid, on average, their supplier invoices 28 days after the date of invoice. In 2009 this had risen to 43 days and in 2011, the average time to pay a supplier invoice stood at 63 days.Required:(a)Analyse the financial position of Hammond Shoes and evaluate the proposed investment of $37·5 million inupgrading its production facilities.(14 marks) (b)Using an appropriate framework (or frameworks) examine the alternative strategic options that HammondShoes could consider to secure its future position.(20 marks) Professional marks will be awarded in part (b) for the clarity, structure and style of the answer.(4 marks) (c)Advise the Hammond family on the importance of mission, values and objectives in defining andcommunicating the strategy of Hammond Shoes.(12 marks)(50 marks)5[P.T.O.Section B – TWO questions ONLY to be attempted2IntroductionFlexipipe is a successful company supplying flexible pipes to a wide range of industries. Its success is based on a very innovative production process which allows the company to produce relatively small batches of flexible pipes at very competitive prices. This has given Flexipipe a significant competitive edge over most of its competitors whose batch set-up costs are higher and whose lead times are longer. Flexipipe’s innovative process is partly automated and partly reliant on experienced managers and supervisors on the factory floor. These managers efficiently schedule jobs from different customers to achieve economies of scale and throughput times that profitably deliver high quality products and service to Flexipipe’s customers.A year ago, the Chief Executive Officer (CEO) at Flexipipe decided that he wanted to extend the automated part of theproduction process by purchasing a software package that promised even further benefits, including the automation of some of the decision-making tasks currently undertaken by the factory managers and supervisors. He had seen this package at a software exhibition and was so impressed that he placed an order immediately. He stated that the package was ‘ahead of its time, and I have seen nothing else like it on the market’.This was the first time that the company had bought a software package for something that was not to be used in a standard application, such as payroll or accounts. Most other software applications in the company, such as the automated part of the current production process, have been developed in-house by a small programming team. The CEO felt that there was, on this occasion, insufficient time and money to develop a bespoke in-house solution. He accepted that there was no formal process for software package procurement ‘but perhaps we can put one in place as this project progresses’.This relaxed approach to procurement is not unusual at Flexipipe, where many of the purchasing decisions are taken unilaterally by senior managers. There is a small procurement section with two full-time administrators, but they only become involved once purchasing decisions have been made. It is felt that they are not technically proficient enough to get involved earlier in the purchasing lifecycle and, in any case, they are already very busy with purchase order administration and accounts payable. This approach to procurement has caused problems in the past. For example, the company had problems when a key supplier of raw materials unexpectedly went out of business. This caused short-term production problems, although the CEO has now found an acceptable alternative supplier.The automation projectOn returning to the company from the exhibition, the CEO commissioned a business analyst to investigate the current production process system so that the transition from the current system to the new software package solution could be properly planned. The business analyst found that some of the decisions made in the current production process were difficult to define and it was often hard for managers to explain how they had taken effective action. They tended to use their experience, memory and judgement and were still innovating in their control of the process. One commented that ‘what we do today, we might not do tomorrow; requirements are constantly evolving’.When the software package was delivered there were immediate difficulties in technically migrating some of the data from the current automated part of the production process software to the software package solution. However, after some difficulties, it was possible to hold trials with experienced users. The CEO was confident that these users did not need training and would be ‘able to learn the software as they went along’. However, in reality, they found the software very difficult to use and they reported that certain key functions were missing. One of the supervisors commented that ‘the monitoring process variance facility is missing completely. Yet we had this in the old automated system’. Despite these reservations, the software package solution was implemented, but results were disappointing.Overall, it was impossible to replicate the success of the old production process and early results showed that costs had increased and lead times had become longer.After struggling with the system for a few months, support from the software supplier began to become erratic.Eventually, the supplier notified Flexipipe that it had gone into administration and that it was withdrawing support for its product. Fortunately, Flexipipe were able to revert to the original production process software, but the ill-fated package selection exercise had cost it over $3m in costs and lost profits. The CEO commissioned a post-project review which showed that the supplier, prior to the purchase of the software package, had been very highly geared and had very poor liquidity. Also, contrary to the statement of the CEO, the post-project review team reported that there were at least three other packages currently available in the market that could have potentially fulfilled the requirements of the company. The CEO now accepts that using a software package to automate the production process was an inappropriate approach and that a bespoke in-house solution should have been commissioned.6Required:(a)Critically evaluate the decision made by the CEO to use a software package approach to automating theproduction process at Flexipipe, and explain why this approach was unlikely to succeed.(12 marks) (b)The CEO recommends that the company now adopts a formal process for procuring, evaluating and implementingsoftware packages which they can use in the future when a software package approach appears to be more appropriate.Analyse how a formal process for software package procurement, evaluation and implementation would have addressed the problems experienced at Flexipipe in the production process project.(13 marks)(25 marks)7[P.T.O.3IntroductionThe country of Mahem is in a long and deep economic recession with unemployment at its highest since the country became an independent nation. In an attempt to stimulate the economy the government has launched a Private/Public investment policy where the government invests in capital projects with the aim of stimulating the involvement of private sector firms. The building of a new community centre in the industrial city of Tillo is an example of such an initiative. Community centres are central to the culture of Mahem. They are designed as places where people can meet socially, local organisations can hold conferences and meetings and farmers can sell their produce to the local community. The centres are seen as contributing to a vibrant community life. The community centre in Tillo is in a sprawling old building rented (at $12,000 per month) from a local landowner. The current community centre is also relatively energy inefficient.In 2010 a business case was put forward to build a new centre on local authority owned land on the outskirts of Tillo.The costs and benefits of the business case are shown in Figure 1. As required by the Private/Public investment policy the project showed payback during year four of the investment.All figures in $Year 1Year 2Year 3Year 4Year 5Costs: Initial600,000Costs: Recurring60,00060,00060,00060,00060,000 Benefits: Rental savings144,000144,000144,000144,000144,000 Benefits: Energy savings30,00030,00030,00030,00030,000 Benefits: Increased income20,00020,00070,00090,00090,000 Benefits: Better staff morale25,00025,00025,00025,00025,000 Cumulative net benefits (441,000)(282,000)(73,000)156,000385,000Figure 1: Costs and benefits of the business case for the community centre at TilloNew buildings built under the Private/Public investment policy must attain energy level targets and this is the basis for the estimation, above, of the energy savings. It is expected that the new centre will attract more customers who will pay for the centre’s use as well as increasing the use of facilities such as the cafeteria, shop and business centre.These benefits are estimated, above, under increased income. Finally, it is felt that staff will be happier in the new building and their motivation and morale will increase. The centre currently employs 20 staff, 16 of whom have been with the centre for more than five years. All employees were transferred from the old to the new centre. These benefits are shown as better staff morale in Figure 1.Construction of the centre 2010–2011In October 2010 the centre was commissioned with a planned delivery date of June 2011 at a cost of $600,000 (as per Figure 1). Building the centre went relatively smoothly. Progress was monitored and issues resolved in monthly meetings between the company constructing the centre and representatives of the local authority. These meetings focused on the building of the centre, monitoring progress and resolving issues. Most of these issues were relatively minor because requirements were well specified in standard architectural drawings originally agreed between the project sponsor and the company constructing the centre. Unfortunately, the original project sponsor (an employee of the local authority) who had been heavily involved in the initial design, suffered ill health and died in April 2011. The new project sponsor (again an employee of the local authority) was less enthusiastic about the project and began to raise a number of objections. Her first concern was that the construction company had used sub-contracted labour and had sourced less than 80% of timber used in the building from sustainable resources. She pointed out the contractual terms of supply for the Private/Public policy investment initiatives mandated that sub-contracting was not allowed without the local authority’s permission and that at least 80% of the timber used must come from sustainable forests. The company said that this had not been brought to their attention at the start of the project. However, they would try to comply with these requirements for the rest of the contract. The new sponsor also refused to sign off acceptance of the centre because of the poor quality of the internal paintwork. The construction company explained that this was the intended finish quality of the centre and had been agreed with the previous sponsor. They produceda letter to verify this. However, the letter was not counter-signed by the sponsor and so its validity was questioned. Inthe end, the construction company agreed to improve the internal painting at their own cost. The new sponsor felt that she had delivered ‘value for money’ by challenging the construction company. Despite this problem with the internal painting, the centre was finished in May 2011 at a cost of $600,000. The centre also included disability access built at the initiative of the construction company. It had found it difficult to find local authority staff willing and able to discuss disability access and so it was therefore left alone to interpret relevant legal requirements.Fortunately, their interpretation was correct and the new centre was deemed, by an independent assessor, to meet accessibility requirements.8Unfortunately, the new centre was not as successful as had been predicted, with income in the first year well below expectations. The project sponsor began to be increasingly critical of the builders of the centre and questioned the whole value of the project. She was openly sceptical of the project to her fellow local authority employees. She suggested that the project to build a cost-effective centre had failed and called for an inquiry into the performance of the project manager of the construction company who was responsible for building the centre. ‘We need him to explain to us why the centre is not delivering the benefits we expected’, she explained.Required:(a)The local authority has commissioned the independent Project Audit Agency (PAA) to look into how the projecthad been commissioned and managed. The PAA believes that a formal ‘terms of reference’ or ‘project initiation document’ would have resolved or clarified some of the problems and issues encountered in the project. It also feels that there are important lessons to be learnt by both the local authority and the construction company.Analyse how a formal ‘terms of reference’ (project initiation document) would have helped address problems encountered in the project to construct the community centre and lead to improved project management in future projects.(13 marks) (b)The PAA also believes that the four sets of benefits identified in the original business case (rental savings, energysavings, increased income and better staff morale) should have been justified more explicitly.Draft an analysis for the PAA that formally categorises and critically evaluates each of the four sets of proposed benefits defined in the original business case.(12 marks)(25 marks)9[P.T.O.4J ayne Cox Direct is a company that specialises in the production of bespoke sofas and chairs. Its products are advertised in most quality lifestyle magazines. The company was started ten years ago. It grew out of a desire to provide customers with the chance to specify their own bespoke furniture at a cost that compared favourably with standard products available from high street retailers. It sells furniture directly to the end customer. Its website allows customers to select the style of furniture, the wood it is to be made from, the type of upholstery used in cushion and seat fillings and the textile composition and pattern of the covering. The current website has over 60 textile patterns which can be selected by the customer. Once the customer has finished specifying the kind of furniture they want, a price is given. If this price is acceptable to the customer, then an order is placed and an estimated delivery date is given. Most delivery dates are ten weeks after the order has been placed. This relatively long delivery time is unacceptable to some customers and so they cancel the order immediately, citing the quoted long delivery time as their reason for cancellation.J ayne Cox Direct orders wood, upholstery and textiles from long-established suppliers. About 95% of its wood is currently supplied by three timber suppliers, all of whom supplied the company in its first year of operation. Purchase orders with suppliers are placed by the procurement section. Until last year, they faxed purchase orders through to suppliers. They now email these orders. Recently, an expected order was not delivered because the supplier claimed that no email was received. This caused production delays. Although suppliers like working with Jayne Cox Direct, they are often critical of payment processing. On a number of occasions the accounts section at Jayne Cox Direct has been unable to match supplier invoices with purchase orders, leading to long delays in the payment of suppliers.The sofas and chairs are built in Jayne Cox Direct’s factory. Relatively high inventory levels and a relaxed production process means that production is rarely disrupted. Despite this, the company is unable to meet 45% of the estimated delivery dates given when the order was placed, due to the required goods not being finished in time. Consequently,a member of the sales team has to telephone the customer and discuss an alternative delivery date.T elephoning the customer to change the delivery date presents a number of problems. Firstly, contacting the customer by telephone can be difficult and costly. Secondly, many customers are disappointed that the original, promised delivery date can no longer be met. Finally, customers often have to agree a delivery date much later than the new delivery date suggested by Jayne Cox Direct. This is because customers often get less than one week’s notice of the new date and so they have to defer delivery to much later. This means that the goods have to remain in the warehouse for longer.A separate delivery problem arises because of the bulky and high value nature of the product. J ayne Cox Directrequires someone to be available at the delivery address to sign for its safe receipt and to put the goods somewhere secure and dry. About 30% of intended deliveries do not take place because there is no-one at the address to accept delivery. Consequently, furniture has to be returned and stored at the factory. A member of the sales staff will subsequently telephone the customer and negotiate a new delivery date but, again, contacting the customer by telephone can be difficult and costly.Delivery of furniture is made using the company’s own vans. Each of these vans follow a defined route each day of the week, irrespective of demand.The company’s original growth was primarily due to the innovative business idea behind specifying competitively priced bespoke furniture. However, established rivals are now offering a similar service. In the face of this competition the managing director of Jayne Cox Direct has urged a thorough review of the supply chain. She feels that costs and inventory levels are too high and that the time taken from order to delivery is too long. Furthermore, in a recent customer satisfaction survey there was major criticism about the lack of information about the progress of the order after it was placed. One commented that ‘as soon as Jayne Cox Direct got my order and my money they seemed to forget about me. For ten weeks I heard nothing. Then, just three days before my estimated delivery date, I receiveda phone call telling me that the order had been delayed and that the estimated delivery date was now 17 June. I hadalready taken a day off work for 10 June, my original delivery date. I could not re-arrange this day off and so I had to agree a delivery date of 24 June when my mother would be here to receive it’.People were also critical about after-sales service. One commented ‘I accidently stained my sofa. Nobody at Jayne Cox Direct could tell me how to clean it or how to order replacement fabrics for my sofa’. Another said ‘organising the return of a faulty chair was very difficult’.When the managing director of Jayne Cox Direct saw the results of the survey she understood ‘why our customer retention rate is so low’.10。

国际商务单证缮制与操作试题(定)

2012年全国国际商务单证专业考试国际商务单证缮制与操作试题(考试时间:6月10日下午15:30——17:30)一、根据下述合同内容审核信用证,指出不符之处,并提出修改意见。

(36分)请在答题纸上作答。

合同:SALES CONTRACTThe Seller: Tianjin Yimei International Corp. Con tract No. YM0806009 Address: 58 Dongli Road Tianjin,China Date: June 5,2011The Buyer: V ALUE TRADING ENTERPRISE,LLCAddress: Rm1008 Green Building KuwaitThis Sales Contract is made by and between the Seller and the Buyer, whereby the Seller agree to sell and the Buyer agree to buy the under-mentioned goods according to the terms and conditions stipulated below:Shipping Mark: V ALUEORDER NO.A01KUW AITC/No.1-UPTime of Shipment: Before AUG. 10,2011Loading Port and Destination: From Tianjin, China to KuwaitPartial Shipment: Not AllowedTransshipment: AllowedInsurance: To be effected by the seller for 110% invoice value covering All Risks and War Risk as per CIC of PICC dated 01/01/1981国际商务单证缮制与操作试题第1页(共6页)Terms of Payment: By L/C at 60 days after sight, reaching the seller before June 15,2011, and remaining valid for negotiation in China for further 15 days after the effectedshipment. L/C must mention this contract number. L/C advised by BANK OFCHINA. All banking Charges outside China (the mainland of China) are foraccount of the Drawee.Documents:+ Signed commercial invoice in triplicate.+ Full set (2/3) of clean on board ocean Bill of Lading marked “Freight Prepaid” made out to order blank endorsed notifying the applicant.+ Insurance Policy in duplicate endorsed in blank.+ Packing List in triplicate.+ Certificate of Origin issued by China Chamber of CommerceSigned by:THE SELLER: THE BUYER: Tianjin Yimei International Corp. V ALUE TRADING ENTERPRISE,LLC Jack Julia信用证:27: SEQUENCE OF TOTAL:1/140A: FORM OF DOCUMENTARY CREDIT:IRREVOCABLE20: DOCUMENTARY CREDIT NUMBER:KR369/0331C: DA TE OF ISSUE:11061940E: APPLICABLE RULES:UCP LATEST VERSION31D: DATE AND PLACE OF EXPIRY:110825 KUWAIT50: APPLICANT:V ALUE TRADING ENTERPRISE CORP.RM1008 GREEN BUILDING KUWAIT59: BENEFICIARY:TIANJIN YMEI INTERNA TIONAL CORP.58 DONGLI ROAD TIANJIN,CHINA32B: CURRENCY CODE, AMOUNT:USD71500.0041A: A V AILABLE WITH…BY…:BANK OF CHINABY NEGOTIATION42C: DRAFTS AT…:90 DAYS AFTER SIGHT42A: DRAWEE: V ALUE TRADING ENTERPRISE,LLC43P: PARTIAL SHIPMENTS: NOT ALLOWED43T: TRANSHIPMENT: NOT ALLOWED44E: PORT OF LOADING/AIRPORT OF DEPARTURE: ANY CHINESE PORT44F: PORT OF DISCHARGE/AIRPORT OF DESTINATION: KUWAIT BY SEA FREIGHT44C: LATEST DATE OF SHIPMENT: 11071045A: DESCRIPTION OF GOODS AND/OR SERVICES: 5000PCS WIND BREAKERSTYLE NO. YM085AS PER ORDER NO.A01 AND S/C NO.YM009AT USD15.10/PC CIF KUWAITPACKED IN CARTON OF 20PCS EACH46A: DOCUMENTS REQUIRED+ SIGNED COMMERCIAL INVOICES IN TRIPLICATE INDICATING LC NO. AND CONTRACT NO.+ FULL SET (3/3) OF CLEAN ON BOARD OCEAN BILL OF LADING MADE OUT TO APPLICANT AND BLANK ENDORSED MARKED “FREIGHT TO COLLECT”NOTIFYING THE APPLICANT.+ SIGNED PACKING LIST IN TRIPLICATE SHOWING THE FOLLOWING DETAILS: TOTAL NUMBER OF PACKAGES SHIPPED; CONTENT(S) OF PACKAGE(S); GROSS WEIGHT, NET WEIGHT AND MEASUREMENT.国际商务单证缮制与操作试题第2页(共6页)+ CERTIFICATE OF ORIGIN ISSUED AND SIGNED OR AUTHENTICA TED BY A LOCAL CHAMBER OF COMMERCE LOCATED IN THE EXPORTING COUNTRY.+ INSURANCE POLICY/CERTIFICATE IN DUPLICATE ENDORSED IN BLANK FOR 120% INVOICE V ALUE, COVERING ALL RISKS AND W AR RISK OF CIC OF PICC (1/1/1981). 71B: CHARGES: ALL CHARGES AND COMMISSIONS ARE FOR ACCOUNT OF BENEFICIARY INCLUDING REIMBURSING CHARGES.48.二、根据下面合同资料和相关资料指出下列开证申请书中错误的地方(24分)请在答题纸上作答。

2013单证员考试《国际商务单证缮制及操作》真题及答案解析

2012年全国国际商务单证员专业考试国际商务单证缮制与操作试题(考试时间:6月10日下午15:30——17:30)一、根据下述合同的内容审核信用证,指出不符之处,并提出修改意见(36分)。

请在答题纸上作答。

合同:SALES CONFIMATIONContract No. YM0806009Date: June 05, 2011 The Seller: Tianjin Yimei International Corp.Address: 58 Dongli Road Tianjin, ChinaThe Buyer: VALUE TRADING ENTERPRISE, LLCAddress: Rm1008 Green Building KuwaitThis Sales Contract is made by and between Seller and Buyer, whereby the Seller agree to sell and the Buyer agree to buy the under-mentioned goods according to the terms and conditions stipulated below:Shipping Marks: VALUEORDER NO. A01KUWAITC/No. 1-UPTime of Shipment: Before AUGG. 10, 2011Loading Port and Destination: From Tianjin, China to KuwaitPartial shipment: Not allowedTransshipment: AllowedInsurance: To be effected by the seller for 110% invoice value covering All Risks and War Riskas per CIC of PICC dated 01/01/1981Terms of Payment: By L/C at 60 days after sight, reaching the seller before June 15, 2011, andremaining valid for negotiation in China for further 15 days after the effectedshipment. L/C must mention this contract number. L/C advised by BANK OFCHINA. All banking charges outside China (the mainland of China) are foraccount of the Drawee.Documents:+ Signed commercial invoice in triplicate.+ Full set (3/3) of clean on board ocean Bill of Lading marked Freight Prepaid made out to orderblank endorsed notifying the applicant.+ Insurance Policy in duplicate endorsed in blank.+ Packing List in triplicate.+ Certificate of Origin issued by China Chamber of Commerce.Signed by:THE SELLER: THE BUYER:Tianjin Yimei International Corp. VALUE TRADING ENTERPRISE, LLC Jack Julia信用证:27: SEQUENCE OF TOTAL: 1/140A: FORM OF DOC. CREDIT: IRREVOCABLE20: DOC. CREDIT NUMBER: KR369/0331C: DATE OF ISSUE: 11061940E: APPLICABLE RULES: UCP LATEST VERSION31D: DATE AND PLCA OF EXPIRY: 110825 KUWAIT51D: APPLICANT BANK: VALUE TRADING ENTERPRISE CORP.RM1008 GREEN BUILDING KUWAIT50: APPLICANT: AORE SPECIALTIES MATERIAL CORP.YARIMCA, KOCAELI 41740, IZMIT, TURKEY59: BENEFICIARY: TIANJIN YMEI INTERNATIONAL CORP.58 DONGLI ROAD TIANJIN, CHINA32B: CURRENCY CODE, AMOUNT: USD71500.0041A: AVAILABLE WITH … BY: BANK OF CHINABY NEGOTIATION42C: DRAFTS AT …: 90 DAYS AFTER SIGHT42A: DRAWEE: VALUE TRADING ENTERPRISE, LLC43P: PARTIAL SHIPMENTS: NOT ALLOWED43T: TRANSSHIPMENT: NOT ALLOWED44E: PORT OF LOADING/AIRPORT OF DEPARTURE: ANY CHINESE PORT44F: PORT OF DISCHARGE/ AIRPORT OF DESTINATION: KUWAIT BY SEA FREIGHT44C: LATEST DATE OF SHIPMENT: 11071045A: DESCRIPTION OF GOODS AND / OR SERVICES: 5000PCS WIND BREAKERSTYLE NO. YM085AS PER ORDER NO. A01 AND S/C NO. YM009AT USD15.10/PC CIF KUWAITPACKED IN CARTON OF 20PCS EACH46A: DOCUMENTS REQUIRED+ SIGNED COMMERCIAL INVOICE IN TRIPLICATE INDICATING LC NO. ANDCONTRACT NO.+ FULL SET (3/3) OF CLEAN ON BOARD OCEAN BILL OF LADING MADE OUT TOAPPLICANT AND BLANK ENDOSED MARKED “FREIGHT TO COLLECT”NOTIFY THE APPLICANT+ SIGNED PACKING LIST IN TRIPLICATE SHOWING THE FOLLOWING DETAILS:TOTAL NUMBER OF PACKAGES SHIPPED; CONTENT(S) OF PACKAGE(S), GROSSWEIGHT, NET WEIGHT AND MEASUREMENT.+ CERTIFICATE OF ORIGIN ISSUED AND SIGNED OR AUTHENTICATED BY ALOCAL CHAMBER OF COMMERCE LOCATED IN THE EXPORTING COUNTRY.+ INSURANCE POLICY/CERTIFICATE IN DUPLICATE ENDORSED IN BLANK FOR 120%INVOICE VALUE, COVERING ALL RISKS AND WAR RISK OF CIC OF PICC(1/1/1981) 71B: CHARGES: ALL CHARGES AND COMMISSIONS ARE FOR ACCOUNT OFBENEFICIARY INCLUDING REIMBURSING CHARGES经审核,信用证存在问题如下:1.31D信用证到期时间错,应该是110815;2.31D信用证到期地点错,应该是CHINA;3.50申请人名称错,应该是VALUE TRADING ENTERPRISE, LLC.;4.59受益人名称错,应该是TIANJIN YIMEI INTERNATIONAL CORP.;5.32B金额错,应该是USD75500.00;6.42C汇票期限错,应该是60 DAYS AFTER SIGHT;7.42A汇票付款人错,应该是开证银行;8.43T转运要求错,应该是ALLOWED;9.44E装运港错,应该是TIANJIN, CHINA;10.44F卸货港错,应该是KUWAIT;11.44C最晚装运日错,应该是110731;12.45A货物名称错,应该是MEN’S WIND BREAKER;13.45A合同号码错,应该是YM0806009;14.45A贸易术语错,应该是CIFC5KUWAIT;15.46A第2条提单抬头错,应该是MADE OUT TO ORDER;16.46A第2条提单运费显示错,应该是FREIGHT PREPAID;17.46A第5条保单加成错,应该是FOR 110% INVOICE VALUE;18.71B银行费用错,应该是FOR ACCOUNT OF THE DRAWEE。

2012年外贸单证员考试基础理论模拟试题及答案解析

⼀、多项选择题(10⼩题,每⼩题l.5分,共15分。

多项选择题的答案多选、少选、错选均不得分,请在答题卡上将相应的选项涂⿊) 1.空运货物的计费重量可按如下计算:__________。

A.按实际⽑重 B.按体积重量 C.按较⾼重量分界点的重量 D.按较低重量分界点的重量 2.因租船订舱和装运⽽产⽣的单据是__________。

A.Shipping Note B.Shipping Order C.Mate’s Receipt D.Bill of Lading 3.在有具体唛头的情况下,保险单唛头⼀栏可填写__________。

A.发票上的唛头 B.As per:Invoice N0….(发票号码) C.N/M D.N/N 4.关于信⽤证中“Date and place of expiry”,说法正确的是__________。

A.表明该证的到期⽇期和到期地点 B.信⽤证的到期地点可以在开证⾏所在地,也可以在受益⼈所在地 C.可以推算出信⽤证的开证⽇期 D.如果是在开证⾏所在地,出⼝审单⼈员⼀定要把握好交单时间和邮程,防⽌信⽤证失效 5.下列术语中,在装运港完成交货的有__________。

A.FOB B.FAS C.CFR D.CIF 6.根据((ucP600>>规定,在出Vl业务中,卖⽅可凭以结汇的单据有__________。

A.提单 B.不可转让的海运单 C.装货单 D.航空运单 7.以下属于⼀切险所承保的责任范围__________。

A.淡⽔⾬淋险 B.钩损险 C.拒收险 D.渗漏险 8.根据《公约》的规定,对发盘表⽰接受可以采取的⽅式有__________。

A.书⾯ B.⾏为 C.缄默 D.⼝头 9.海运提单做成指⽰抬头时,提单收货⼈⼀栏,可以填写成__________。

A.To order of shipper B.To order of issuing bank C.To issuing bank D.To order 10.信息流电⼦化的优势是拥有__________。

单证员考试《操作与缮制》基础模拟题及答案.doc

单证员考试《操作与缮制》基础模拟题及答案1、郑州某企业使用进口料件加工的成品,在郑州海关办妥出口手续,经天津海关复核放行后装船运往美国。

此项加工成品复出口业务,除按规定已办理了出口手续外,同时,还要办理的手续的是:(D)A.境内转关运输手续B.货物过境手续C.货物登记备案手续D.出口转关运输手续2、某服装进出口公司自日本进口一批工作服,在向海关申报时,其报关单“贸易方式”栏应填报为:(A)A、一般贸易B、货样广告品C、货样广告品AD、货样广告品B3、(B)是海关接受申报时给予报关单的编号。

A.预录入编号B.海关编号C.备案号D.项号解析:预录入编号指申报单位或预录入单位对该单位填制录入的报关单的编号,用于该单位与海关之间费用其申报后尚未批准放行的报关单;海关编号指海关接受申报时给予报关单的编号,由各海关在接受申报环节确定,应标识在报关单的第一联上。

4.英国生产的产品,中国购自新加坡,经香港转运至中国,填写报关单时起运地为(B)A.英国B.新加坡C.香港D.不用填写解析:起运国指进口货物起始发出的国家,对中转地发生商业性交易,则以中转地作为起运国填写,本题在中转地未发生商业性交易,且货物购自新加坡,因此起运地为新加坡。

5、报关单备注栏目应该选填下列哪项内容。

(D)A.机电产品进口配额证明B.编号C.付汇赊销单编号D.三资企业委托代理进出口业务的委托单位全称解析:机电产品进口配额证明属于监管证件名称,应该填在随附单据栏,编号应填在备案号栏内,付汇核销单编号填在批准文号内。

6.CFR合同下,如果卖方装船后未及时向买方发出装船通知,致使买方未能办理货运保险,则运输途中的风险由(B)。

A.买方承担B.卖方承担C.承运人承担D.买卖双方各承担一半7.在国际贸易中,含佣价的计算公式是(A)。

A.净价÷(1-佣金率)B.净价×(1+佣金率)C.净价×佣金率D.单价×佣金率8.CIF条件下交货,(C)。

XX单证员考试《操作与缮制》连备考题及答案

XX单证员考试《操作与缮制》连备考题及答案xx单证员考试《操作与缮制》连备考题及答案1、报关单备注栏目应该选填以下哪项内容。

( D)A.机电产品进口配额证明B. <登记手册>编号C.付汇赊销单编号D.三资企业委托代理进出口业务的委托单位全称解析:机电产品进口配额证明属于监管证件名称,应该填在随附单据栏,<登记手册>编号应填在备案号栏内,付汇核销单编号填在批准文号内。

3、某纺织品进口公司在国内购一批坯布运出境印染,复运进境后委托服装厂加工成服装,然后回收出口。

前后两次出口适用的报关程序分别是:(C)A. 暂准出境和一般出口B. 一般出口和进料加工C. 出料加工和一般出口D. 出料加工和进料加工4、请指出以下哪一项货物或物品不适用暂准进出口通关制度:(A)A、进口待转口输出的转口贸易货物B、在展览会中展示或示范用的进口货物、物品C、承装一般进口货物进境的外国集装箱D、来华进展文艺演出而暂时运进的器材、道具、服装等5、根据《中华人民共和国海关法》的规定,进口货物的收货人向海关申报的时限是:(C)A.自运输工具申报进境之日起7日内B.自运输工具申报进境之日起10日内C.自运输工具申报进境之日起14日内D.自运输工具申报进境之日起15日内6、郑州某企业使用进口料件加工的成品,在郑州海关办妥出口手续,经天津海关复核放行后装船运往美国。

此项加工成品复出口业务,除按规定已办理了出口手续外,同时,还要办理的手续的是: (D)A.境内转关运输手续B.货物过境手续C.货物登记备案手续D.出口转关运输手续7、某服装进出口公司自日本进口一批工作服,在向海关申报时,其报关单“贸易方式”栏应填报为:(A)A、一般贸易B、货样广告品C、货样广告品AD、货样广告品B8、(B)是海关承受申报时给予报关单的编号。

A.预录入编号B. 海关编号C.备案号D.项号解析:预录入编号指申报单位或预录入单位对该单位填制录入的报关单的编号,用于该单位与海关之间费用其申报后尚未批准放行的报关单;海关编号指海关承受申报时给予报关单的编号,由各海关在承受申报环节确定,应标识在报关单的第一联上。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2012年全国国际商务单证员专业考试国际商务单证缮制与操作试题(考试时间:6月10日下午15:30——17:30)一、根据下述合同的内容审核信用证,指出不符之处,并提出修改意见(36分)。

请在答题纸上作答。

合同:SALES CONFIMATIONContract No. YM0806009Date: June 05, 2011 The Seller: Tianjin Yimei International Corp.Address: 58 Dongli Road Tianjin, ChinaThe Buyer: VALUE TRADING ENTERPRISE, LLCAddress: Rm1008 Green Building KuwaitThis Sales Contract is made by and between Seller and Buyer, whereby the Seller agree to sell and the Buyer agree to buy the under-mentioned goods according to the terms and conditionsShipping Marks: V ALUEORDER NO. A01KUWAITC/No. 1-UPTime of Shipment: Before AUGG. 10, 2011Loading Port and Destination: From Tianjin, China to KuwaitPartial shipment: Not allowedTransshipment: AllowedInsurance: To be effected by the seller for 110% invoice value covering All Risks and War Risk as per CIC of PICC dated 01/01/1981Terms of Payment: By L/C at 60 days after sight, reaching the seller before June 15, 2011, and remaining valid for negotiation in China for further 15 days after the effectedshipment. L/C must mention this contract number. L/C advised by BANK OFCHINA. All banking charges outside China (the mainland of China) are foraccount of the Drawee.Documents:+ Signed commercial invoice in triplicate.+ Full set (3/3) of clean on board ocean Bill of Lading marked Freight Prepaid made out to order blank endorsed notifying the applicant.+ Insurance Policy in duplicate endorsed in blank.+ Packing List in triplicate.+ Certificate of Origin issued by China Chamber of Commerce.Signed by:THE SELLER: THE BUYER:Tianjin Yimei International Corp. V ALUE TRADING ENTERPRISE, LLC Jack Julia信用证:27: SEQUENCE OF TOTAL: 1/140A: FORM OF DOC. CREDIT: IRREVOCABLE20: DOC. CREDIT NUMBER: KR369/0331C: DATE OF ISSUE: 11061940E: APPLICABLE RULES: UCP LATEST VERSION31D: DATE AND PLCA OF EXPIRY: 110825 KUWAIT51D: APPLICANT BANK: V ALUE TRADING ENTERPRISE CORP.RM1008 GREEN BUILDING KUWAIT50: APPLICANT: AORE SPECIALTIES MATERIAL CORP.YARIMCA, KOCAELI 41740, IZMIT, TURKEY59: BENEFICIARY: TIANJIN YMEI INTERNATIONAL CORP.58 DONGLI ROAD TIANJIN, CHINA32B: CURRENCY CODE, AMOUNT: USD71500.0041A: A V AILABLE WITH … BY: BANK OF CHINABY NEGOTIATION42C: DRAFTS AT …: 90 DAYS AFTER SIGHT42A: DRAWEE: V ALUE TRADING ENTERPRISE, LLC43P: PARTIAL SHIPMENTS: NOT ALLOWED43T: TRANSSHIPMENT: NOT ALLOWED44E: PORT OF LOADING/AIRPORT OF DEPARTURE: ANY CHINESE PORT44F: PORT OF DISCHARGE/ AIRPORT OF DESTINATION: KUWAIT BY SEA FREIGHT44C: LATEST DATE OF SHIPMENT: 11071045A: DESCRIPTION OF GOODS AND / OR SERVICES: 5000PCS WIND BREAKERSTYLE NO. YM085AS PER ORDER NO. A01 AND S/C NO. YM009AT USD15.10/PC CIF KUWAITPACKED IN CARTON OF 20PCS EACH46A: DOCUMENTS REQUIRED+ SIGNED COMMERCIAL INVOICE IN TRIPLICATE INDICATING LC NO. ANDCONTRACT NO.+ FULL SET (3/3) OF CLEAN ON BOARD OCEAN BILL OF LADING MADE OUT TO APPLICANT AND BLANK ENDOSED MARKED “FREIGHT TO COLLECT”NOTIFY THE APPLICANT+ SIGNED PACKING LIST IN TRIPLICATE SHOWING THE FOLLOWING DETAILS: TOTAL NUMBER OF PACKAGES SHIPPED; CONTENT(S) OF PACKAGE(S), GROSS WEIGHT, NET WEIGHT AND MEASUREMENT.+ CERTIFICATE OF ORIGIN ISSUED AND SIGNED OR AUTHENTICA TED BY ALOCAL CHAMBER OF COMMERCE LOCA TED IN THE EXPORTING COUNTRY.+ INSURANCE POLICY/CERTIFICATE IN DUPLICATE ENDORSED IN BLANK FOR 120% INVOICE V ALUE, COVERING ALL RISKS AND WAR RISK OF CIC OF PICC(1/1/1981) 71B: CHARGES: ALL CHARGES AND COMMISSIONS ARE FOR ACCOUNT OFBENEFICIARY INCLUDING REIMBURSING CHARGES经审核,信用证存在问题如下:1.31D信用证到期时间错,应该是110815;2.31D信用证到期地点错,应该是CHINA;3.50申请人名称错,应该是V ALUE TRADING ENTERPRISE, LLC.;4.59受益人名称错,应该是TIANJIN YIMEI INTERNA TIONAL CORP.;5.32B金额错,应该是USD75500.00;6.42C汇票期限错,应该是60 DAYS AFTER SIGHT;7.42A汇票付款人错,应该是开证银行;8.43T转运要求错,应该是ALLOWED;9.44E装运港错,应该是TIANJIN, CHINA;10.44F卸货港错,应该是KUWAIT;11.44C最晚装运日错,应该是110731;12.45A货物名称错,应该是MEN’S WIND BREAKER;13.45A合同号码错,应该是YM0806009;14.45A贸易术语错,应该是CIFC5KUWAIT;15.46A第2条提单抬头错,应该是MADE OUT TO ORDER;16.46A第2条提单运费显示错,应该是FREIGHT PREPAID;17.46A第5条保单加成错,应该是FOR 110% INVOICE V ALUE;18.71B银行费用错,应该是FOR ACCOUNT OF THE DRAWEE。

二、根据下面合同资料和相关资料指出下列开证申请书中错误的地方(24分)请在答题纸上作答。

2011年6月20日,上海华联皮革制品有限公司(SHANGHAI HUALIAN LEATHER GOODS CO., LTD. 156 CHANGXING ROAD, SHANGHAI, CHINA)向SVS DESIGN PLUS CO., LTD. 1-509 HANNAMDONG YOUNGSAN-KU, SEOUL, KOREA出口DOUBLE FACE SHEEPSKIN一批,达成以下主要合同条款:1. Commodity: DOUBLE FACE SHEEPSKINCOLOUR CHESTNUT2. Quantity: 3175.25SQFT(平方英尺)3. PACKING: IN CARTONS4. Unit Price: USD7.40/SQFT CIF SEOUL5. Amount: USD23496.856. Time of shipment: During NOV.2011Port of Loading: SHANGHAI, CHINAPort of Destination: SEOUL, KOREAPartial shipment: ALLOWEDTransshipment: PROHIBITED7. Insurance: TO BE COVERED BY THE SELLER FOR 110%INVOICE V ALUE COVERINGALL RISK AND W AR RISK AS PER CIC OF THE PICC DATED 01/01/1981.8. Payment: BY IRREVOCABLE LETTER OF CREDIT AT 45 DAYS SIGHT TO REACHTHE SELLER NOT LATER THAN JUNE 24, 2011, V ALID FOR NEGOTIATIONIN CHINA UNTIL THE 15TH DAY AFTER TIME OF SHIPMENTDocument: (1) SIGNED COMMERCIAL INVOICE IN 3 FOLD.(2) SIGNED PACKING LIST IN 3 FOLD.(3) FULL SET OF CLEAN ON BOARD OCEAN B/L IN 3/3ORIGINALS ISSUEDTO ORDER AND BLANK ENDORSED MARKED “FREIGHT PREPAID”ANDNOTIFY THE APPLICANYT.(4) CERTIFICATE OF ORIGIN IN 1 ORIGINAL AND 1 COPY ISSUED BY THECHAMBER OF COMMERCE IN CHINA(5)INSURANCE POLICY/CERTIFICATE IN DUPLICATE ENDORSED IN BLANKFOR 110%INVOICE V ALUE COVERING ALL RISK S AND WAR RISKS OFCIC OF PICC (1/1/1981).SHOWING THE CLAIMING CURRENCY IS THESAME AS THE CURRENCY OF CREDIT相关资料:(1)信用证号码:MO722111057(2)合同号码:HL20110315SVS DESIGN PLUS CO., LTD 国际商务单证员金浩于2011年6月23日向KOOKMIN BANK, SEOUL, KOREA办理申请电开信用证手续,通知行是BANK OF CHINA, SHANGHAI BEANCH标注蓝色的字就是错误部分。