亨格瑞管理会计英文第15版练习答案05解析.

亨格瑞管理会计英文第15版 答案 10-12章

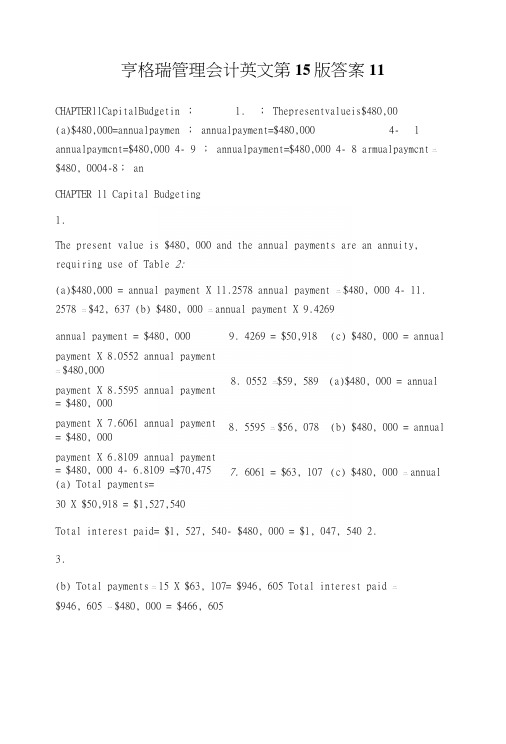

CHAPTER 11Capital Budgeting11-A1 (15-25 min.) Answers are printed in the text at the end of the assignment material.11-29 (10-15 min.)1. The present value is $480,000 and the annual payments are an annuity, requiringuse of Table 2:(a)$480,000 = annual payment × 11.2578annual payment = $480,000 ÷ 11.2578 = $42,637(b)$480,000 = annual payment × 9.4269annual payment = $480,000 ÷ 9.4269 = $50,918(c)$480,000 = annual payment × 8.0552annual payment = $480,000 ÷ 8.0552 =$59,5892. (a)$480,000 = annual payment × 8.5595annual payment = $480,000 ÷ 8.5595 = $56,078(b)$480,000 = annual payment × 7.6061annual payment = $480,000 ÷ 7.6061 = $63,107(c)$480,000 = annual payment × 6.8109annual payment = $480,000 ÷ 6.8109 =$70,4753. (a) Total payments= 30 × $50,918 = $1,527,540Total interest paid= $1,527,540- $480,000 = $1,047,540(b) Total payments= 15 × $63,107= $946,605Total interest paid = $946,605 - $480,000 = $466,60511-36 (10 min.)Buy. The net present value is positive.Initial outlay * $(21,000)Present value of cash operating savings, from12-year, 12% column of Table 2, 6.1944 × $5,000 30,972Net present value $ 9,972* The trade-in allowance really consists of a $5,000 adjustment of the sellingprice and a bona fide $10,000 cash allowance for the old equipment. Therelevant amount is the incremental cash outlay, $21,000. The book value isirrelevant.11-39 (10-15 min.)Copyright ©2011 Pearson Education 1Copyright ©2011 Pearson Education21. NPV @ 10% = 10,000 × 3.7908 = $37,908 - $36,048 = $1,860 NPV @ 12% = 10,000 × 3.6048 = $36,048 - $36,048 = $0NPV @ 14% = 10,000 × 3.4331 = $34,331 - $36,048 = $(1,717)2.The IRR is the interest rate at which NPV = $0; therefore, from requirement 1 we know that IRR = 12%.3.The NPV at the company’s cost of capital, 10%, is positive, so the project should be accepted.4.The IRR (12%) is greater than the company’s cost of capital (10%), so the project should be accepted. Note that the IRR and NPV models give the same decision.11-46 (10-15 min.)Annual addition to profit = 40% × $25,000 = $10,000.1.Payback period is $36,000 ÷ $10,000 = 3.6 years. It is not a good measure of profitability because it ignores returns beyond the payback period and it does not account for the time value of money.2. NPV = $5,114. Accept the proposal because NPV is positive. Computation: NPV = ($10,000 × 4.1114) - $36,000= $41,114 - $36,000 = $ 5,1143. ARR = (Increase in average cash flow – Increase in depreciation) ÷ Initialinvestment= ($10,000 - $6,000) ÷ $36,000 = 11.1%11-51 (30-35 min.)1.Annual Operating Cash FlowsXeroxCannon Difference Salaries $49,920(a) $41,600(b) $ 8,320 Overtime 1,728(c) -- 1,728 Repairs and maintenance 1,800 1,050 750Toner, supplies, etc. 3,6003,300 300 Total annual cash outflows $57,048 $45,950 $11,098(a) ($ 8 × 40 hrs.) × 52 weeks × 3 employees = $320 × 52 × 3 = $49,920 (b) ($10 × 40 hrs.) × 52 weeks × 2 employees = $400 × 52 × 2 = $41,600 (c) ($12 × 4 hrs.) × 12 months × 3 machines = $ 48 × 12 × 3 = $ 1,728Initial Cash FlowsXeroxCannon Difference Purchase of Cannon machines $ -- $50,000 $50,000Sale of Xerox machines -- -3,000 -3,000 Training and remodeling -- 4,000 4,000 Total $ -- $51,000 $51,000Copyright ©2011 Pearson Education 3EXHIBIT 11-50All numbers are expressed in Mexican pesos.2. 18% Total Sketch of Relevant Cash Flows(inthousands)PresentPVFactor Value 0 1 2 3 4 5Cash operating savings:* .8475 83,902 99,000108,90078,212.718272,904119,790.608667,966 131,769 .5158.4371 63,356 144,946Total366,340Income tax savings fromdepreciation not changedby inflation, see 1 3.1272 105,074 33,600 33,600 33,600 33,600 33,600471,414TotalRequired outlay at time zero 1.0000 (420,000) (420,000)Net present value 51,414*Amounts are computed by multiplying (150,000 × .6) = 90,000 by 1.10, 1.10 2, 1.10 3, etc.Copyright ©2011 Pearson Education 461PV PresentofValue$1.00ofCashFlows Annual Cash FlowsDiscountedat 12% 0 1 2 3 4 5T OTAL P ROJECT A PPROACH:Cannon:Init. cash outflow 1.0000 $ (51,000)Oper. cash flows 3.6048 (165,641) (45,950) (45,950) (45,950) (45,950) (45,950)Total $(216,641)Xerox:Oper. cash flows 3.6048 $(205,647) (57,048) (57,048) (57,048) (57,048) (57,048)Difference in favor ofretaining Xerox $ (10,994)I NCREMENTAL A PPROACH:Initial investment 1.0000 $(51,000)Annual operatingcash savings 3.6048 40,006 11,098 11,098 11,098 11,098 11,098Net present valueof purchase $(10,994)2. The Xerox machines should not be replaced by the Cannon equipment.Net savings = (Present value of expenditures to retain Xerox machines) less (Present value of expenditures toconvert to Cannon machines)= $205,647 - $216,641 = $(10,994)3. a. How flexible is the new machinery? Will it be useful only for the presently intended functions, or can it be easilyadapted for other tasks that may arise over the next 5 years?b. What psychological effects will it have on various interested parties?Copyright ©2011 Pearson Education 46211-71 (60-90 min.)This is a complex problem because it requires comparing three alternatives. It reviews Chapter 6 as well as covering several of the topics of Chapter 11. The following answer uses the total project approach. The total net future cash outflows are shown for each alternative.1. Alternative A: Continue to manufacture the parts with the current tools.Annual cash outlaysVariable cost, $92 × 8,000 $(736,000)Fixed cost, 1/3 × $45 × 8,000 × .6 (72,000)Tax savings, .4 × ($736,000 + $72,000) 323,200After-tax annual cost $(484,800)Present value, 3.6048 × $484,800 $(1,747,607)PV of remaining tax savings on MACRS:11.52% × $2,000,000 × .4 × .8929 82,2905.76% × $2,000,000 × .4 × .7972 36,735Total present value of costs, Alternative A $(1,628,582)Alternative B: Purchase from outside supplierAnnual cash outlaysPurchase cost, $110 × 8,000 $(880,000)Tax savings, $880,000 × .4 352,000After-tax annual cost $(528,000)Copyright ©2011 Pearson Education 463Present value, $528,000 × 3.6048 $(1,903,334)Sale of old equipment:Sales price $ 400,000Book value [(11.52% + 5.76%) × $2,000,000] 345,600Gain $ 54,400Taxes @ 40% (21,760)Total after-tax effect ($400,000 - $21,760) 378,240Total present value of costs, Alternative B $(1,525,094)Copyright ©2011 Pearson Education 464Alternative C: Purchase new toolsInvestment $(1,800,000) Annual cash outlaysVariable cost, $73 × 8,000 $(584,000)Fixed cost (same as A) (72,000)Tax savings, .4 × ($584,000 + $72,000) 262,400After-tax annual cost $(393,600)Present value, $393,600 × 3.6048 (1,418,849)Tax savings on new equipment* 579,217Effect of disposal of new equipmentSales price $ 500,000Book value 0Gain $500,000Taxes @ 40% 200,000Total after-tax effect $ 300,000Present value, $300,000 × .5674 170,220Effect of disposal of old equipment (see Alternative B) 378,240Total present value of costs, Alternative C $(2,091,172)* Using the MACRS schedule for tax depreciation, the depreciation rate for each year of a 3-year asset's life is shown inExhibit 11-6:Depreciation Tax PV PresentYear Rate Savings Factor Value1 33.33% .3333 × $1,800,000 × .40 = $239,976 .8929 $214,2752 44.45% .4445 × 1,800,000 × .40 = 320,040 .7972 255,1363 14.81% .1481 × 1,800,000 × .40 = 106,632 .7118 75,9014 7.41% .0741 × 1,800,000 × .40 = 53,352 .6355 33,905Total present value of tax savings $579,217Using Exhibit 11-7, we get .8044 × $1,800,000 × .4 = $579,168, which differs from $579,217 by a $49 rounding error.The alternative with the lowest present value of cost is Alternative B, purchasing from the outside supplier.Copyright ©2011 Pearson Education 4652. Among the major factors are (1) the range of expected volume (both large increases and decreases in volume make thepurchase of the parts relatively less desirable), (2) the reliability of the outside supplier, (3) possible changes inmaterial, labor, and overhead prices, (4) the possibility that the outside supplier can raise prices before the end of five years, (5) obsolescence of the products and equipment, and (6) alternate uses of available capacity (alternative uses make Alternative B relatively more desirable).Copyright ©2011 Pearson Education 466Copyright ©2011 Pearson Education467CHAPTER 12 Cost Allocation12-30 (10-15 min.) 1. Rate = [$2,500 + ($.05 × 100,000)] ÷ 100,000 = $.075 per copy Cost allocated to City Planning in August = $.075 × 42,000 = $3,150. 2. Fixed cost pool allocated as a lump sum depending on predicted usage:To City Planning: (36,000 ÷ 100,000) × $2,500 = $900 per monthVariable cost pool allocated on the basis of actual usage: $.05 × number of copies Cost allocated to City Planning in August: $900 + ($.05 × 42,000) = $3,000. 3. The second method, the one that allocated fixed- and variable-cost pools separately, is preferable. It better recognizesthe causes of the costs. The fixed cost depends on the size of the photocopy machine, which is based on predicted usage and is independent of actual usage. Variable costs, in contrast are caused by actual usage.Exhibit 12-34Customer Type 1Customer Type 2 Customer Type 3 Sales Gross price profit per margin Gross Gross Gross Product unit per unit Units Revenue profit Units Revenue profit Units Revenue profitA $11.031$ 4.14 200 $ 2,206 $ 828 2,200 $ 24,266 $ 9,108 500 $ 5,515 $ 2,070 B 20.47 4.09 100 2,047 409 1,200 24,564 4,908 3,000 61,410 12,270 C 51.38 10.28 50 2,569 514 400 20,552 4,112 5,000 256,900 51,400D 90.00 39.38 400 36,000 15,752 800 72,000 31,504 400 36,000 15,752Total 750 $42,822 17,5034,600 $141,382 49,632 8,900 $359,825 81,492 Cost to serve 7,36845,193 87,439 Operating income $10,135 $4,439 ($5,947) Customer gross margin percentage 40.9% 35.1% 22.6% Cost to serve percentage 17.2% 32.0% 24.3%Customer operating income percentage 23.7%3.1% (1.7%)1$32,000 ÷ 2,900 units; etc. The rounded numbers from the first two columns are used in subsequent calculations.5. The chart below shows customer profitability for the three customer types and suggested strategies for profit improvement.Grow business with this customer type byfocused sales efforts and quantity discounts.Work with customers to lowerthe cost to serve. Seek internalprocess improvements to lowerthose elements of the cost toserve controllable by thecompany.Copyright ©2011 Pearson Education 46912-35 (15-20 min.)of1. AllocationCostsGallons Weighting Joint$300,000 $180,000×A 9,000 9/15SolventSolvent B 6,000 6/15 × $300,000 120,00015,000 $300,0002. Relative Sales Allocation ofCostsValue at Split-off* Weighting JointSolvent A $270,000 27/54 × $300,000 $150,000Solvent B 270,000 27/54 × $300,000 150,000$540,000 $300,000 * $30 × 9,000 and $45 × 6,00012-42 (25-30 min.)There a several ways to organize an analysis that provides product costs. We like to focus first on determining total activity-cost pools and activity cost per driver unit. Then, an analysis similar to the one shown in Exhibit 12-8 can be used.Schedule a: Activity center cost poolsResources Supporting the Allocated Setup/Maintenance Activity Center Allocation Calculation Cost Assembly supervisors $90,000 × 2% $ 1,800 Assembly machines $247,000 × (400 ÷ 1,900) 52,000 Facilities management $95,000 × (400 ÷ 1,900) 20,000 Power $54,000 × (10 ÷ 90) 6,000Total assigned cost $79,800Cost per driver unit (setup) $79,800 ÷ 40 $ 1,995 Resources Supporting the Allocated Setup/Maintenance Activity Center Allocation Calculation Cost Assembly supervisors $90,000 × 98% $ 88,200 Assembly machines $247,000 × (1,500 ÷ 1,900) 195,000 Facilities management $95,000 × (1,500 ÷ 1,900) 75,000 Power $54,000 × (80 ÷ 90) 48,000Total assigned cost $406,200Cost per driver unit (machine hour) $406,200 ÷ 1,500 $ 270.80Copyright ©2011 Pearson Education 470Exhibit 12-42 Contribution to cover other value-chain costs by productStandardDeluxe Custom Cost per Driver unit Driver Driver Driver Activity/Resource (Schedule a) Units Cost Units Cost Units Cost Setup/Maintenance $1,995 20 $ 39,900 12 $ 23,940 8 $ 15,960 Assembly $270.80 1,000 270,800 400 108,320 100 27,080 Parts 1,003,800 115,080 15,980Direct labor 298,00072,000 68,000 Total $1,612,500$319,340 $127,020 Units 100,000 10,000 1,000 Cost per display $16.125 $31.934 $127.02Selling price 20.00050.000 250.00 Unit gross profit $ 3.875$18.066 $122.98 Total gross profit $387,500$180,660 $122,980The total contribution of these products is $387,500 + $180,660 + $122,980 = $691,140.12-43 (25-30 min.) See solution to problem 12-42.12-55 (100 – 200 min.)1. Exhibits 12-55A and 12-55B show the calculation of customer gross margin percentage and customer cost-to-serve percentage for the 4 customer types. Exhibit 12-55C shows a plot of customer gross margin percentage versus customer cost-to-serve percentage for the 4 customer types.2. Suggested strategies for profit improvement for the 4 customer types follow.•Customer type 1 - Mega stores. These stores have the lowest cost-to-serve.Profitability can be improved by focusing on a better product mix. A quarter ofthe sales (cases) to these stores are from bulk and singles products – both ofwhich have a negative gross margin. A shift in mix towards more regular andfragile product types would improve profitability.•Customer type 2 – Local small stores. These stores have a product mix that contains a substantial amount (32%) of the negative gross margin products. Thesame change in sales focus that applies to mega stores can be applied to localsmall stores.But unlike mega stores, small stores are very costly to serve. From Exhibit 12-55 B, the largest single cost to serve local small stores is truck deliveries. Theaverage number of cases per order (the same as per truck delivery) is 6,000,000 ÷ 80,000 = 75. Compare this to mega stores that average 7,680,000 ÷ 32,000 = 240 cases per order (delivery). This is a significant factor causing the high cost-to-serve.For example, suppose that the average order size could be increased from 75,000 to 150,000 cases. If the total annual cases sold is unchanged (6,000,000), a totalof 40 orders, a 50% reduction, would be made. An estimate of the cost savingsand the impact on the cost-to-serve percentage can be made as follows:Cost per Driver Unit Reduction in Driver Cost Savings(Exhibit 12-55B) Units of 50% (000) Truck delivery $167.55 34,000 $5,696.70 Order processing 27.49 40,000 1,099.60 Regular scheduling 5.83 36,000 209.88 Expedited scheduling 19.44 4,000 77.76 Total cost savings (000) $7,083.94 Cost savings as a percent of revenue 24.9%New cost-to-serve as a percent of revenue 60.1%In addition to the above savings, other activities would also be impacted by thereduction in orders such as customer service. So while the total impact ofCopyright ©2011 Pearson Education 472focusing on increasing order size can only be estimated, it is reasonable to expect dramatic cost savings from the current 85% of revenue.Other factors that should be investigated include the high level of corporatesupport and customer service.•Customer type 3 – Local large stores. Local large stores generate $68,400 ÷ $136,230 = 50% of DSI’s total revenue and with a net margin of 58% - 47% = 11%. The key to local large store profitability is sales of a large percentage (80%) of regular product. The cost-to-serve percentage is 47%. This could be reduced as for customer type 2 by increasing the order size from the current level of14,400,000 ÷ 120,000 = 120 cases per order. But a dramatic improvementshould not be expected. In general, local large stores are sustaining DSI’sbusiness and their loyalty should be cultivated.•Customer type 4 – Specialty stores. Specialty stores have a low gross margin of 22% coupled with a very large cost-to-serve percent of 106%! Although thesestores do not account for a significant portion of DSI’s revenue the companyshould rationalize their business. Several actions could be suggested. One is to charge a premium for all high-security products. The vast majority of theseproducts are sold to specialty stores with only marginal sales to mega and local small stores. Another action is to adopt a customer loyalty program based onvolume of sales. The list price of $7.25 per case would apply to customers with sales volumes less than a specified level. Most of DSI’s customers would qualify for discounts (similar to those currently existing) so prices would not besignificantly different. For specialty stores, prices would increase dramatically.This may result in losing specialty-store business so DSI needs to decide is this isa direction they wish to consider.Copyright ©2011 Pearson Education 473Exhibit 12-55A (Units and dollars are in thousands.)C u s t o m e r T y p eProductRegular Short Fragile Bulk HighSecurity Singles Total Gross Profit PercentageProduct mix percentage 60% 5% 5% 20% 5% 5% 100% Cases sold 4,608 384 384 1,536 384 3847,680Total Revenue$ 21,888 $ 1,824$ 1,824$7,296$ 1,824 $ 1,824 $36,480Gross Profit per Case $ 3.28 $ 1.58 $ 2.74 $(1.44)$ 0.54 $ (5.30)1Total Gross Profit$ 15,114 $ 607 $ 1,052 $(2,212)$ 207 $(2,035)$12,733 35%Product mix percentage 50% 5% 5% 30% 8% 2% 100% Cases sold3,000 300 300 1,800 480 120 6,000 Total Revenue @ 4.75/case $ 14,250 $ 1,425 $ 1,425 $ 8,550 $ 2,280 $ 570 $28,500 Gross Profit per Case $ 3.28 $ 1.58 $ 2.74 $ (1.44) $ 0.54 $ (5.30)2Total Gross Profit$ 9,840 $ 474 $ 822 $(2,592) $ 259 $ (636)$ 8,167 29%Product mix percentage 80% 0% 10% 10% 0% 0% 100%Cases sold 11,520 -1,4401,440--14,400Total Revenue @ 4.75/case $ 54,720 $ - $ 6,840 $ 6,840 $ - $ - $68,400Gross Profit per Case $ 3.28 $ 1.58 $ 2.74 $ (1.44) $ 0.54 $ (5.30)3Total Gross Profit$ 37,786 $ - $ 3,946 $(2,074) $ - $ - $39,658 58%Product mix percentage 10% 20% 0% 0% 70% 0% 100% Cases sold 60 120 - - 420-600Total Revenue @ 4.75/case $ 285 $ 570 $ - $ - $ 1,995 $ - $ 2,850 Gross Profit per Case $ 3.28 $ 1.58 $ 2.74 $ (1.44)$ 0.54 $ (5.30)4Total Gross Profit $ 197$ 190$ -$ -$ 227$ - $ 61322%Exhibit 12-55B (Units and dollars are in thousands.)ActivityO r d e r P r o c e s s i n gC u s t o m e r S e r v i c eO r d e r C h a n g e sC o r p o r a t e S u p p o r tR e g u l a r S c h e d u l i n gE x p e d i t e d S c h e d u l i n gS h i p p i n gT r u c k D e l i v e r yP a r c e l D e l i v e r y Cost DriverO r d e r sL a b o r H o u r sN u m b e r o f C h a n g e sL a b o r H o u r sO r d e r sO r d e r sP a l l e t sD e l i v e r i e sD e l i v e r i e sC u s t o m e r T y p eCost/DriverUnit $27.49 $43.34$32.63$51.66$5.83 $19.44 $6.60 $167.55 $23.89Total Driver Units3218.73.2 - 29 3 41625.6 1.6 Cost to Serve $879.68 $810.46$104.42-$169.07$58.32$2,745.6$4,289.28$38.22$9,095.05Revenue (See Exhibit 12-55A) $36,480.001 Cost-to-Serve Percentage24.9%Driver Units 80 100 8 20 72 8 640 68 8Cost to Serve $2,199.2 $4,334$261.04$1,033.2 $419.76$155.52$4,224$11,393.4$191.12$24,211.24Revenue (See Exhibit 12-55A) $28,500.02Cost-to-Serve Percentage85.0%Exhibit 12-55B (continued)ActivityO r d e r P r o c e s s i n gC u s t o m e r S e r v i c eO r d e r C h a n g e sC o r p o r a t e S u p p o r tR e g u l a r S c h e d u l i n gE x p e d i t e d S c h e d u l i n gS h i p p i n gT r u c k D e l i v e r y P a r c e l D e l i v e r y Cost DriverO r d e r sL a b o r H o u r sN u m b e r o f C h a n g e sL a b o r H o u r sO r d e r sO r d e r sP a l l e t sD e l i v e r i e sD e l i v e r i e sC u s t o m e r T y p eCost/DriverUnit $27.49 $43.34$32.63$51.66$5.83 $19.44 $6.60 $167.55 $23.89TotalDriver Units 120 70 2.4 80 108 12 840 90 6Cost to Serve$3,298.8 $3,033.8 $78.31$4,132.8 $629.64 $233.28 $5,544$15,079.5$143.34$32,173.47Revenue (See Exhibit 12-55A) $68,400.03 Cost-to-Serve Percentage47.0%Driver Units 12 30 1.2 0 10 2 60 4.8 2.4Cost to Serve $329.88$1,300.2 $39.16- $58.3 $38.88 $396 $804.24 $57.34$3,023.99Revenue (See Exhibit 12-55A) $2,850.004 Cost-to-Serve Percentage106.1%CUSTOMER PROFITABILITYCT3, 47%, 58%0%10%20%30%40%50%60%70%80%90%100%0%10%20%30%40%50%60%70%80%90%100%110%120%COST-TO-SERVE PERCENTAGEG R O S S P R O F I T P E R C E N T A G EExhibit 12-55CCopyright ©2011 Pearson Education 478。

亨格瑞管理会计英文第15版练习答案01

亨格瑞管理会计英文第15版练习答案01CHAPTER 1COVERAGE OF LEARNING OBJECTIVESLEARNING OBJECTIVE LO1: Describe the major users and uses of accounting information. LO2: Describe the cost-benefit and behavioral issues involved in designing an accounting system. LO3: Explain the role of budgets and performance reports in planning and control. LO4: Discuss the role accountants play in the company’s value chain functions. LO5: Explain why accounting is important in a variety of career paths. LO6: Identify current trends in management accounting. LO7: Explain why ethics and standards of ethical conduct are important to accountants. FUNDA- CRITICAL CASES, MENTAL THINKING EXCEL, ASSIGN-EXERCISES COLLAB., & MENT AND INTERNET MATERIAL EXERCISES PROBLEMS EXERCISES A1, B1 28, 29, 33 39, 40, 42 55 41, 43 A2, B2 32 45 53A1, B1 30, 31, 34, 35, 39, 42, 44 36 30, 31 52, 55 A3, B3 37, 38 47, 48, 49 54 51, 52, 55 1 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.CHAPTER 1Managerial Accounting, the Business Organization, and Professional Ethics1-A1 (10-15 min.)Information is often useful for more than one function, so the following classifications for each activity are not definitive but serve as a starting point for discussion: 1. Scorekeeping. A depreciation schedule is used in preparing financial statementsto report the results of activities. 2. Problem solving. Helps a manager assess the impact of a purchase decision. 3. Scorekeeping. Reports on the results of an operation. Could also be attentiondirecting if scrap is an area that might require management attention. 4. Attention directing. Focuses attention on areas that need attention. 5. Attention directing. Helps managers learn about the information contained in aperformance report. 6. Scorekeeping. The statement reports what has happened. Could also be attentiondirecting if the report highlights a problem or issue. 7. Problem solving. Assuming the cost comparison is to help the manager decidebetween two alternatives, this is problem solving. 8. Attention directing. Variances point out areas where results differ fromexpectations. Interpreting them directs attention to possible causes of the differences. 9. Problem solving. Aids a decision about where to make parts. 10. Attention directing and problem solving. Budgeting involves making decisionsabout planned activities -- hence, aiding problem solving. Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has a scorekeeping dimension.2 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-A2 1. 2.(15-20 min.)Room rental FoodEntertainment Decorations TotalBudgeted Amounts $ 140 700 600 220 $1,660 Actual Amounts $ 140865 600 260 $1,865 Deviations or Variances $ 0 165U 0 40U $205U Because of the management by exception rule, room rental and entertainment require no explanation. The actual expenditure for food exceeded the budgetby $165. Of this $165, $150 is explained by attendance of 15 persons morethan budgeted (at a budget of $10 per person for food) and $15 is explained by expenditures above $10 per person.Actual expenditures for decorations were $40 more than the budget. The decorations committee should be asked for an explanation of the excess expenditures.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard: 1. The General Mills manager must respect the confidentiality standard. He or sheshould not disclose any information about the new cereal. 2. Felix must address his level of competence for the assignment. If his supervisorknows his level of expertise and wants an analysis from a “layperson” point of view, he should do it. However, if the supervisor expects an expert analysis, Felix must disclose his lack of competence. 3. The credibility standard should cause Mary Sue to decline to omit the informationfrom the budget. It is relevant information, and its omission may mislead readers of the budget.3 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-B1 (15-20 min.)Information is often useful for more than one function, so the following classifications for each activity are not definitive but serve as a starting point for discussion: 1. Problem solving. Provides information for deciding between two alternativecourses of action. 2. Scorekeeping. Recording what has happened. If amounts are compared withexpectations, this could also serve an attention-directing function. 3. Problem solving. Helps a manager decide among alternatives. 4. Attention directing. Directs attention to the use of overtime labor. Alsoscorekeeping. 5. Problem solving. Provides information to managers for deciding whether to movecorporate headquarters. 6. Attention directing. Directs attention to why nursing costs increased. 7. Attention directing. Directs attention to areas where actual results differed fromthe budget. 8. Problem solving. Helps the vice-president decide which course of action is best. 9. Problem solving. Produces information to help the marketing department make adecision about a marketing campaign. 10. Scorekeeping. Records actual overtime costs. If results are compared withexpectations, also attention directing. 11. Attention directing. Directs attention to stores with either high or low ratios ofadvertising expenses to sales. 12. Attention directing. Directs attentionto causes of returns of the drug. 13. Attention directing or problem solving, depending on the use of the schedule. If itis to identify areas of high fuel usage it is attention directing. If itis to plan for purchases of fuel, it is problem solving. 14. Scorekeeping. Records items needed for financial statements.4 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-B2 (10-15 min.)1 & 2. Budget Actual Variance Sales $75,000 $74,600 $ 400U Costs: Fireworks $36,000 $35,500 $500F Labor 15,000 18,000 3,000U Other 8,000 7,910 90F Total cost 59,000 61,410 2,410U Profit $16,000 $13,190 $2,810U 3. The cost of fireworks was $500 ÷ $36,000 = 1.4%under budget while sales wasjust 400 ÷ $75,000 = .5% under budget. Did fireworks suppliers lowertheir prices? Were selling prices set higher than expected? There should be some explanation for the lower cost of fireworks. The labor cost was $3,000÷ $15,000 =20% over budget. Sales and other costswere close to budget in percentage terms. Why was labor cost much higherthan expected?1-B3 (15 - 20 min.) 1. A code of conduct is a document specifying theethical standards of anorganization. 2. Different companies include different elements intheir codes of conduct. Some ofthe items included in companies’ codes of condu ct include maintaining adress code, avoiding illegal drugs, following instructions of superiors, being reliable and prompt, maintaining confidentiality, not accepting personal gifts fromstakeholders as a result of company role, avoiding racial or sexual discrimination, avoiding conflict of interest, complying with laws and regulations, not using organization’s property for personal use, andreporting illegal or questionable activity. Some companies have a simple code with little detail, and others have long lists of rules and regulations regarding appropriate conduct. The key is that the code of conduct must fit with the corporate culture. 3. Simply having a code of conduct does not guarantee ethical behavior byemployees. Most important is top management’s ethical example and its support of the code of conduct. A company’s performance evaluation and reward system must be consistent with its code of conduct. If unethical actions are rewarded, they will be encouraged even if they violate the code of conduct.5 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.感谢您的阅读,祝您生活愉快。

《管理会计》英文版课后习题答案

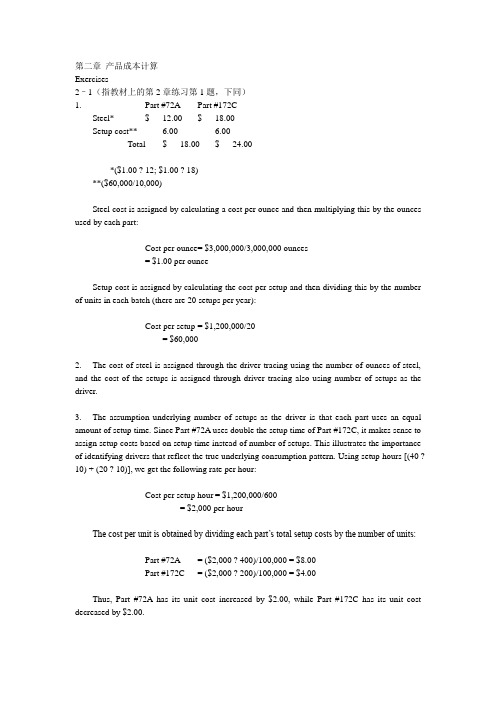

第二章产品成本计算Exercises2–1(指教材上的第2章练习第1题,下同)1. Part #72A Part #172CSteel* $ 12.00 $ 18.00Setup cost** 6.00 6.00Total $ 18.00 $ 24.00*($1.00 ? 12; $1.00 ? 18)**($60,000/10,000)Steel cost is assigned by calculating a cost per ounce and then multiplying this by the ounces used by each part:Cost per ounce= $3,000,000/3,000,000 ounces= $1.00 per ounceSetup cost is assigned by calculating the cost per setup and then dividing this by the number of units in each batch (there are 20 setups per year):Cost per setup = $1,200,000/20= $60,0002. The cost of steel is assigned through the driver tracing using the number of ounces of steel, and the cost of the setups is assigned through driver tracing also using number of setups as the driver.3. The assumption underlying number of setups as the driver is that each part uses an equal amount of setup time. Since Part #72A uses double the setup time of Part #172C, it makes sense to assign setup costs based on setup time instead of number of setups. This illustrates the importance of identifying drivers that reflect the true underlying consumption pattern. Using setup hours [(40 ?10) + (20 ? 10)], we get the following rate per hour:Cost per setup hour = $1,200,000/600= $2,000 per hourThe cost per unit is obtained by dividing each part’s total setup costs by the number of units:Part #72A = ($2,000 ? 400)/100,000 = $8.00Part #172C = ($2,000 ? 200)/100,000 = $4.00Thus, Part #72A has its unit cost increased by $2.00, while Part #172C has its unit cost decreased by $2.00.problems2–51. Nursing hours required per year: 4 ? 24 hours ? 364 days* = 34,944*Note: 364 days = 7 days ? 52 weeksNumber of nurses = 34,944 hrs./2,000 hrs. per nurse = 17.472Annual nursing cost = (17 ? $45,000) + $22,500= $787,500Cost per patient day = $787,500/10,000 days= $78.75 per day (for either type of patient)2. Nursing hours act as the driver. If intensive care uses half of the hours and normal care the other half, then 50 percent of the cost is assigned to each patient category. Thus, the cost per patient day by patient category is as follows:Intensive care = $393,750*/2,000 days= $196.88 per dayNormal care = $393,750/8,000 days= $49.22 per day*$525,000/2 = $262,500The cost assignment reflects the actual usage of the nursing resource and, thus, should be more accurate. Patient days would be accurate only if intensive care patients used the same nursing hours per day as normal care patients.3. The salary of the nurse assigned only to intensive care is a directly traceable cost. To assign the other nursing costs, the hours of additional usage would need to be measured. Thus, both direct tracing and driver tracing would be used to assign nursing costs for this new setting.2–61. Bella Obra CompanyStatement of Cost of Services SoldFor the Year Ended June 30, 2006Direct materials:Beginning inventory $ 300,000Add: Purchases 600,000Materials available $ 900,000Less: Ending inventory 450,000*Direct materials used $ 450,000Direct labor 12,000,000Overhead 1,500,000Total service costs added $ 13,950,000Add: Beginning work in process 900,000Total production costs $ 14,850,000Less: Ending work in process 1,500,000Cost of services sold $ 13,350,000*Materials available less materials used2. The dominant cost is direct labor (presumably the salaries of the 100 professionals). Although labor is the major cost of providing many services, it is not always the case. For example, the dominant cost for some medical services may be overhead (e.g., CAT scans). In some services, the dominant cost may be materials (e.g., funeral services).3. Bella Obra CompanyIncome StatementFor the Year Ended June 30, 2006Sales $ 21,000,000Cost of services sold 13,350,000Gross margin $ 7,650,000Less operating expenses:Selling expenses $ 900,000Administrative expenses 750,000 1,650,000Income before income taxes $ 6,000,0004. Services have four attributes that are not possessed by tangible products: (1) intangibility, (2) perishability, (3) inseparability, and (4) heterogeneity. Intangibility means that the buyers of services cannot see, feel, hear, or taste a service before it is bought. Perishability means that services cannot be stored. This property affects the computation in Requirement 1. Inability to store services means that there will never be any finished goods inventories, thus making the cost of services produced equivalent to cost of services sold. Inseparability simply means that providers and buyers of services must be in direct contact for an exchange to take place. Heterogeneity refers to the greater chance for variation in the performance of services than in the production of tangible products.2–71. Direct materials:Magazine (5,000 ? $0.40) $ 2,000Brochure (10,000 ? $0.08) 800 $ 2,800Direct labor:Magazine [(5,000/20) ? $10] $ 2,500Brochure [(10,000/100) ? $10] 1,000 3,500Manufacturing overhead:Rent $ 1,400Depreciation [($40,000/20,000) ? 350*] 700Setups 600Insurance 140Power 350 3,190Cost of goods manufactured $ 9,490*Production is 20 units per printing hour for magazines and 100 units per printing hour for brochures, yielding monthly machine hours of 350 [(5,000/20) + (10,000/100)]. This is also monthly labor hours, as machine labor only operates the presses.2. Direct materials $ 2,800Direct labor 3,500Total prime costs $ 6,300Magazine:Direct materials $ 2,000Direct labor 2,500Total prime costs $ 4,500Brochure:Direct materials $ 800Direct labor 1,000Total prime costs $ 1,800Direct tracing was used to assign prime costs to the two products.3. Total monthly conversion cost:Direct labor $ 3,500Overhead 3,190Total $ 6,690Magazine:Direct labor $ 2,500Overhead:Power ($1 ? 250) $ 250Depreciation ($2 ? 250) 500Setups (2/3 ? $600) 400Rent and insurance ($4.40 ? 250 DLH)* 1,100 2,250Total $ 4,750Brochure:Direct labor $ 1,000Overhead:Power ($1 ? 100) $ 100Depreciation ($2 ? 100) 200Setups (1/3 ? $600) 200Rent and insurance ($4.40 ? 100 DLH)* 440 940Total $ 1,940*Rent and insurance cannot be traced to each product so the costs are assigned using direct labor hours: $1,540/350 DLH = $4.40 per direct labor hour. The other overhead costs are traced according to their usage. Depreciation and power are assigned by using machine hours (250 for magazines and 100 for brochures): $350/350 = $1.00 per machine hour for power and $40,000/20,000 = $2.00 per machine hour for depreciation. Setups are assigned according to the time required. Since magazines use twice as much time, they receive twice the cost: Letting X = the pro?portion of setup time used for brochures, 2X + X = 1 implies a cost assignment ratio of 2/3 for magazines and 1/3 for brochures.Exercises3–11. Resource Total Cost Unit CostPlastic1 $ 10,800 $0.027Direct labor andvariable overhead2 8,000 0.020Mold sets3 20,000 0.050Other facility costs4 10,000 0.025Total $ 48,800 $0.12210.90 ? $0.03 ? 400,000 = $10,800; $10,800/400,000 = $0.0272$0.02 ? 400,000 = $8,000; $8,000/400,000 = $0.023$5,000 ? 4 quarters = $20,000; $20,000/400,000 = $0.054$10,000; $10,000/400,000 = $0.0252. Plastic, direct labor, and variable overhead are flexible resources; molds and other facility costs are committed resources. The cost of plastic, direct labor, and variable overhead are strictly variable. The cost of the molds is fixed for the particular action figure being produced; it is a step cost for the production of action figures in general. Other facility costs are strictly fixed.3–3High (1,400, $7,950); Low (700, $5,150)V = ($7,950 – $5,150)/(1,400 – 700)= $2,800/700 = $4 per oil changeF = $5,150 – $4(700)= $5,150 – $2,800 = $2,350Cost = $2,350 + $4 (oil changes)Predicted cost for January = $2,350 + $4(1,000) = $6,350problems3–61. High (1,700, $21,000); Low (700, $15,000)V = (Y2 – Y1)/(X2 – X1)= ($21,000 – $15,000)/(1,700 – 700) = $6 per receiving orderF = Y2 – VX2= $21,000 – ($6)(1,700) = $10,800Y = $10,800 + $6X2. Output of spreadsheet regression routine with number of receiving orders as the independent variable:Constant 4512.98701298698Std. Err. of Y Est. 3456.24317476605R Squared 0.633710482694768No. of Observations 10Degrees of Freedom 8X Coefficient(s) 13.3766233766234Std. Err. of Coef. 3.59557461331427V = $13.38 per receiving order (rounded)F = $4,513 (rounded)Y = $4,513 + $13.38XR2 = 0.634, or 63.4%Receiving orders explain about 63.4 percent of the variability in receiving cost, providing evidence that Tracy’s choice o f a cost driver is reasonable. However, other drivers may need to be considered because 63.4 percent may not be strong enough to justify the use of only receiving orders.3. Regression with pounds of material as the independent variable:Constant 5632.28109733183Std. Err. of Y Est. 2390.10628259277R Squared 0.824833789433823No. of Observations 10Degrees of Freedom 8X Coefficient(s) 0.0449642991356633Std. Err. of Coef. 0.0073259640055344V = $0.045 per pound of material delivered (rounded)F = $5,632 (rounded)Y = $5,632 + $0.045XR2 = 0.825, or 82.5%Pounds of material delivered explains about 82.5 percent of the variability in receiving cost. This is a better result than that of the receiving orders and should convince Tracy to try multiple regression.4. Regression routine with pounds of material and number of receiving orders as the independent variables:Constant 752.104072925631Std. Err. of Y Est. 1350.46286973443R Squared 0.951068418023306No. of Observations 10Degrees of Freedom 7X Coefficient(s) 0.0333883151096915 7.14702865269395Std. Err. of Coef. 0.00495524841198368 1.68182916088492V1 = $0.033 per pound of material delivered (rounded)V2 = $7.147 per receiving order (rounded)F = $752 (rounded)Y = $752 + $0.033a + $7.147bR2 = 0.95, or 95%Multiple regression with both variables explains 95 percent of the variability in receiving cost. This is the best result.5–21. Job #57 Job #58 Job #59Balance, 7/1 $ 22,450 $ 0 $ 0Direct materials 12,900 9,900 35,350Direct labor 20,000 6,500 13,000Applied overhead:Power 750 600 3,600Material handling 1,500 300 6,000Purchasing 250 1,000 250Total cost $ 57,850 $ 18,300 $ 58,2002. Ending balance in Work in Process = Job #58 = $18,3003. Ending balance in Finished Goods = Job #59 = $58,2004. Cost of Goods Sold = Job #57 = $57,850problems5–31. Overhead rate = $180/$900 = 0.20 or 20% of direct labor dollars.(This rate was calculated using information from the Ladan job; however, the Myron and Coe jobs would give the same answer.)2. Ladan Myron Coe Walker WillisBeginning WIP $ 1,730 $1,180 $2,500 $ 0 $ 0Direct materials 400 150 260 800 760Direct labor 800 900 650 350 900Applied overhead 160 180 130 70 180Total $ 3,090 $2,410 $3,540 $ 1,220 $ 1,840Note: This is just one way of setting up the job-order cost sheets. You might prefer to keep the detail on the materials, labor, and overhead in beginning inventory costs.3. Since the Ladan and Myron jobs were completed, the others must still be in process. Therefore, the ending balance in Work in Process is the sum of the costs of the Coe, Walker, and Willis jobs.Coe $3,540Walker 1,220Willis 1,840Ending Work in Process $6,600Cost of Goods Sold = Ladan job + Myron job = $3,090 + $2,410 = $5,5004. Naman CompanyIncome StatementFor the Month Ended June 30, 20XXSales (1.5 ? $5,500) $8,250Cost of goods sold 5,500Gross margin $2,750Marketing and administrative expenses 1,200Operating income $1,5505–201. Overhead rate = $470,000/50,000 = $9.40 per MHr2. Department A: $250,000/40,000 = $6.25 per MHrDepartment B: $220,000/10,000 = $22.00 per MHr3. Job #73 Job #74Plantwide:70 ? $9.40 = $658 70 ? $9.40 = $658Departmental:20 ? $6.25 $ 125.00 50 ? $6.25 $ 312.5050 ? $22 1,100.00 20 ? $22 440.00$ 1,225.00 $ 752.50Department B appears to be more overhead intensive, so jobs spending more time in Department B ought to receive more overhead. Thus, departmental rates provide more accuracy.4. Plantwide rate: $250,000/40,000 = $6.25Department B: $62,500/10,000 = $6.25Job #73 Job #74Plantwide:70 ? $6.25 = $437.50 70 ? $6.25 = $437.50Departmental:20 ? $6.25 $ 125.00 50 ? $6.25 $ 312.5050 ? $6.25 312.50 20 ? $6.25 125.00$ 437.50 $ 437.50Assuming that machine hours is a good cost driver, the departmental rates reveal that overhead consumption is the same in each department. In this case, there is no need for departmental rates, and a plantwide rate is sufficient.5–41. Overhead rate = $470,000/50,000 = $9.40 per MHr2. Department A: $250,000/40,000 = $6.25 per MHrDepartment B: $220,000/10,000 = $22.00 per MHr3. Job #73 Job #74Plantwide:70 ? $9.40 = $658 70 ? $9.40 = $658Departmental:20 ? $6.25 $ 125.00 50 ? $6.25 $ 312.5050 ? $22 1,100.00 20 ? $22 440.00$ 1,225.00 $ 752.50Department B appears to be more overhead intensive, so jobs spending more time in Department B ought to receive more overhead. Thus, departmental rates provide more accuracy.4. Plantwide rate: $250,000/40,000 = $6.25Department B: $62,500/10,000 = $6.25Job #73 Job #74Plantwide:70 ? $6.25 = $437.50 70 ? $6.25 = $437.50Departmental:20 ? $6.25 $ 125.00 50 ? $6.25 $ 312.5050 ? $6.25 312.50 20 ? $6.25 125.00$ 437.50 $ 437.50Assuming that machine hours is a good cost driver, the departmental rates reveal that overhead consumption is the same in each department. In this case, there is no need for departmental rates, and a plantwide rate is sufficient.5–51. Last year’s unit-based overhead rate = $50,000/10,000 = $5This year’s unit-based overhead rate = $100,000/10,000 = $10Last Year This YearBike cost:2 ? $20 $ 40 $ 403 ? $12 36 36Overhead:5 ? $5 255 ? $10 50Total $101 $126Price last year = $101 ? 1.40 = $141.40/dayPrice this year = $126 ? 1.40 = $176.40/dayThis is a $35 increase over last year, nearly a 25 percent increase. No doubt the Carsons arenot pleased and would consider looking around for other recreational possibilities.2. Purchasing rate = $30,000/10,000 = $3 per purchase orderPower rate = $20,000/50,000 = $0.40 per kilowatt hourMaintenance rate = $6,000/600 = $10 per maintenance hourOther rate = $44,000/22,000 = $2 per DLHBike Rental Picnic CateringPurchasing$3 ? 7,000 $21,000$3 ? 3,000 $ 9,000Power$0.40 ? 5,000 2,000$0.40 ? 45,000 18,000Maintenance$10 ? 500 5,000$10 ? 100 1,000Other$2 ? 11,000 22,000 22,000Total overhead $50,000 $50,0003. This year’s bike rental overhead rate = $50,000/10,000 = $5Carson rental cost = (2 ? $20) + (3 ? $12) + (5 ? $5) = $101Price = 1.4 ? $101 = $141.40/day4. Catering rate = $50,000/11,000 = $4.55* per DLHCost of Estes job:Bike rental rate (2 ? $7.50) $15.00Bike conversion cost (2 ? $5.00) 10.00Catering materials 12.00Catering conversion (1 ? $4.55) 4.55Total cost $41.55*Rounded5. The use of ABC gives Mountain View Rentals a better idea of the types and costs of activities that are used in their business. Adding Level 4 bikes will increase the use of the most expensive activities, meaning that the rental rate will no longer be an average of $5 per rental day. Mountain View Rentals might need to set a Level 4 price based on the increased cost of both the bike and conversion cost.分步成本法6–11. Cutting Sewing PackagingDepartment Department DepartmentDirect materials $5,400 $ 900 $ 225Direct labor 150 1,800 900Applied overhead 750 3,600 900Transferred-in cost:From cutting 6,300From sewing 12,600Total manufacturing cost $6,300 $12,600 $14,6252. a. Work in Process—Sewing 6,300Work in Process—Cutting 6,300b. Work in Process—Packaging 12,600Work in Process—Sewing 12,600c. Finished Goods 14,625Work in Process—Packaging 14,625 3. Unit cost = $14,625/600 = $24.38* per pair6–21. Units transferred out: 27,000 + 33,000 – 16,200 = 43,8002. Units started and completed: 43,800 – 27,000 = 16,8003. Physical flow schedule:Units in beginning work in process 27,000Units started during the period 33,000Total units to account for 60,000Units started and completed 16,800Units completed from beginning work in process 27,000Units in ending work in process 16,200Total units accounted for 60,0004. Equivalent units of production:Materials ConversionUnits completed 43,800 43,800Add: Units in ending work in process:(16,200 ? 100%) 16,200(16,200 ? 25%) 4,050 Equivalent units of output 60,000 47,8506–31. Physical flow schedule:Units to account for:Units in beginning work in process 80,000Units started during the period 160,000Total units to account for 240,000Units accounted for:Units completed and transferred out:Started and completed 120,000From beginning work in process 80,000 200,000 Units in ending work in process 40,000Total units accounted for 240,0002. Units completed 200,000Add: Units in ending WIP ? Fraction complete(40,000 ? 20%) 8,000Equivalent units of output 208,0003. Unit cost = ($374,400 + $1,258,400)/208,000 = $7.854. Cost transferred out = 200,000 ? $7.85 = $1,570,000Cost of ending WIP = 8,000 ? $7.85 = $62,8005. Costs to account for:Beginning work in process $ 374,400Incurred during June 1,258,400Total costs to account for $ 1,632,800Costs accounted for:Goods transferred out $ 1,570,000Goods in ending work in process 62,800Total costs accounted for $ 1,632,8006–31、Units t0 account for:Units in beginning work in process(25% completed) 10000Units started during the period 70000 Total units to account for 80000 Units accounted forUnits completed and transferred outStarted and completed 50000From beginning work in process 10000 60000 Units in ending work in process(60% completed) 20000 Total units accounted for 80000 2、60000+20000×60%=72000(units)3、Unit cost for materials:($/unit)Unit cost for convension:($/unit)Total unit cost:5+1.13=6.13($/unit)4、The cost of units of transferred out:60000×6.13=367800($)The cost of units of ending work in process:20000×5+20000×20%×1.13=113560($)作业成本法4–21. Predetermined rates:Drilling Department: Rate = $600,000/280,000 = $2.14* per MHrAssembly Department: Rate = $392,000/200,000= $1.96 per DLH*Rounded2. Applied overhead:Drilling Department: $2.14 ? 288,000 = $616,320Assembly Department: $1.96 ? 196,000 = $384,160Overhead variances:Drilling Assembly TotalActual overhead $602,000 $ 412,000 $ 1,014,000Applied overhead 616,320 384,160 1,000,480Overhead variance $ (14,320) over $ 27,840 under $ 13,5203. Unit overhead cost = [($2.14 ? 4,000) + ($1.96 ? 1,600)]/8,000= $11,696/8,000= $1.46**Rounded4–31. Yes. Since direct materials and direct labor are directly traceable to each product, their cost assignment should be accurate.2. Elegant: (1.75 ? $9,000)/3,000 = $5.25 per briefcaseFina: (1.75 ? $3,000)/3,000 = $1.75 per briefcaseNote: Overhead rate = $21,000/$12,000 = $1.75 per direct labor dollar (or 175 percent of direct labor cost).There are more machine and setup costs assigned to Elegant than Fina. This is clearly a distortion because the production of Fina is automated and uses the machine resources much more than the handcrafted Elegant. In fact, the consumption ratio for machining is 0.10 and 0.90 (using machine hours as the measure of usage). Thus, Fina uses nine times the machining resources as Elegant. Setup costs are similarly distorted. The products use an equal number of setups hours. Yet, if direct labor dollars are used, then the Elegant briefcase receives three times more machining costs than the Fina briefcase.3. Overhead rate = $21,000/5,000= $4.20 per MHrElegant: ($4.20 ? 500)/3,000 = $0.70 per briefcaseFina: ($4.20 ? 4,500)/3,000 = $6.30 per briefcaseThis cost assignment appears more reasonable given the relative demands each product places on machine resources. However, once a firm moves to a multiproduct setting, using only one activity driver to assign costs will likely produce product cost distortions. Products tend to make different demands on overhead activities, and this should be reflected in overhead cost assignments. Usually, this means the use of both unit- and nonunit-level activity drivers. In this example, there is a unit-level activity (machining) and a nonunit-level activity (setting up equipment). The consumption ratios for each (using machine hours and setup hours as the activity drivers) are as follows:Elegant FinaMachining 0.10 0.90 (500/5,000 and 4,500/5,000)Setups 0.50 0.50 (100/200 and 100/200)Setup costs are not assigned accurately. Two activity rates are needed—one based on machine hours and the other on setup hours:Machine rate: $18,000/5,000 = $3.60 per MHrSetup rate: $3,000/200 = $15 per setup hourCosts assigned to each product:Machining: Elegant Fina$3.60 ? 500 $ 1,800$3.60 ? 4,500 $ 16,200Setups:$15 ? 100 1,500 1,500Total $ 3,300 $ 17,700Units ÷3,000 ÷3,000Unit overhead cost $ 1.10 $ 5.904:Elegant Unit overhead cost:[9000+3000+18000*500/5000+3000/2]/3000=$5.1 Fina Unit overhead cost:[3000+3000+18000*4500/5000+3000/2]/3000=$7.94–51. Deluxe Percent Regular PercentPrice $900 100% $750 100%Cost 576 64 600 80Unit gross profit $324 36% $150 20%Total gross profit:($324 ? 100,000) $32,400,000($150 ? 800,000) $120,000,0002. Calculation of unit overhead costs:Deluxe gularUnit-level:Machining:$200 ? 100,000 $20,000,000$200 ? 300,000 $60,000,000Batch-level:Setups:$3,000 ? 300 900,000$3,000 ? 200 600,000Packing:$20 ? 100,000 2,000,000$20 ? 400,000 8,000,000Product-level:Engineering:$40 ? 50,000 2,000,000$40 ? 100,000 4,000,000Facility-level:Providing space:$1 ? 200,000 200,000$1 ? 800,000 800,000Total overhead $25,100,000 $73,400,000Units ÷100,000 ÷800,000Overhead per unit $251 $91.75Deluxe Percent Regular PercentPrice $900 100% $750.00 100%Cost 780* 87*** 574.50** 77***Unit gross profit $120 13%*** $175.50 23%***Total gross profit:($120 ? 100,000) $12,000,000($175.50 ? 800,000) $140,400,000*$529 + $251**$482.75 + $91.753. Using activity-based costing, a much different picture of the deluxe and regular products emerges. The regular model appears to be more profitable. Perhaps it should be emphasized.4–61. JIT Non-JITSalesa $12,500,000 $12,500,000Allocationb 750,000 750,000a$125 ? 100,000, where $125 = $100 + ($100 ? 0.25), and 100,000 is the average order size times the number of ordersb0.50 ? $1,500,0002. Activity rates:Ordering rate = $880,000/220 = $4,000 per sales orderSelling rate = $320,000/40 = $8,000 per sales callService rate = $300,000/150 = $2,000 per service callJIT Non-JITOrdering costs:$4,000 ? 200 $ 800,000$4,000 ? 20 $ 80,000Selling costs:$8,000 ? 20 160,000$8,000 ? 20 160,000Service costs:$2,000 ? 100 200,000$2,000 ? 50 100,000Total $1,160,000 $340,0 0For the non-JIT customers, the customer costs amount to $750,000/20 = $37,500 per order under the original allocation. Using activity assign?ments, this drops to $340,000/20 = $17,000 per order, a difference of $20,500 per order. For an order of 5,000 units, the order price can be decreased by $4.10 per unit without affecting customer profitability. Overall profitability will decrease, however, unless the price for orders is increased to JIT customers.3. It sounds like the JIT buyers are switching their inventory carrying costs to Emery without any significant benefit to Emery. Emery needs to increase prices to reflect the additional demands on customer-support activities. Furthermore, additional price increases may be needed to reflectthe increased number of setups, purchases, and so on, that are likely occurring inside the plant. Emery should also immediately initiate discussions with its JIT customers to begin negotiations for achieving some of the benefits that a JIT supplier should have, such as long-term contracts. The benefits of long-term contracting may offset most or all of the increased costs from the additional demands made on other activities.4–71. Supplier cost:First, calculate the activity rates for assigning costs to suppliers:Inspecting components: $240,000/2,000 = $120 per sampling hourReworking products: $760,500/1,500 = $507 per rework hourWarranty work: $4,800/8,000 = $600 per warranty hourNext, calculate the cost per component by supplier:Supplier cost:Vance FoyPurchase cost:$23.50 ? 400,000 $ 9,400,000$21.50 ? 1,600,000 $ 34,400,000Inspecting components:$120 ? 40 4,800$120 ? 1,960 235,200Reworking products:$507 ? 90 45,630$507 ? 1,410 714,870Warranty work:$600 ? 400 240,000$600 ? 7,600 4,560,000Total supplier cost $ 9,690,430 $ 39,910,070Units supplied ÷400,000 ÷1,600,000Unit cost $ 24.23* $ 24.94**RoundedThe difference is in favor of Vance; however, when the price concession is considered, the cost of Vance is $23.23, which is less than Foy’s component. Lumus should accept the contractual offer made by Vance.4–7 Concluded2. Warranty hours would act as the best driver of the three choices. Using this driver, the rate is $1,000,000/8,000 = $125 per warranty hour. The cost assigned to each component would be:Vance FoyLost sales:$125 ? 400 $ 50,000$125 ? 7,600 $ 950,000$ 50,000 $ 950,000Units supplied ÷400,000 ÷1,600,000Increase in unit cost $ 0.13* $ 0.59**Rounded$0.075 per unitCategory II: $45/1,000 = $0.045 per unitCategory III: $45/1,500 = $0.03 per unitCategory I, which has the smallest batches, is the most undercosted of the three categories. Furthermore, the unit ordering cost is quite high relative to Category I’s selling price (9 to 15 percent of the selling price). This suggests that something should be done to reduce the order-filling costs.3. With the pricing incentive feature, the average order size has been increased to 2,000 units for all three product families. The number of orders now processed can be calculated as follows:Orders = [(600 ? 50,000) + (1,000 ? 30,000) + (1,500 ? 20,000)]/2,000= 45,000Reduction in orders = 100,000 – 45,000 = 55,000Steps that can be reduced = 55,000/2,000 = 27 (rounding down to nearest whole number)There were initially 50 steps: 100,000/2,000Reduction in resource spending:Step-fixed costs: $50,000 ? 27 = $1,350,000Variable activity costs: $20 ? 55,000 = 1,100,000$2,450,000预算9-4Norton, Inc.Sales Budget For the Coming YearModel Units Price Total SalesLB-1 50,400 $29.00 $1,461,600LB-2 19,800 15.00 297,000WE-6 25,200 10.40 262,080 WE-7 17,820 10.00 178,200 WE-8 9,600 22.00 211,200 WE-9 4,000 26.00 104,000 Total $2,514,080二、1. Raylene’s Flowers and GiftsProduction Budget for Gift BasketsFor September, October, November, and DecemberSept. Oct. Nov. D ec.Sales 200 150 180 250Desired ending inventory 15 18 25 10Total needs 215 168 205 260Less: Beginning inventory 20 15 18 25 Units produced 195 153 187 2352. Raylene’s Flowers and GiftsDirect Materials Purchases BudgetFor September, October, and NovemberFruit: Sept. Oct. Nov.Production 195 153 187? Amount/basket (lbs.) ? 1 ? 1 ?1Needed for production 195 153 187Desired ending inventory 8 9 12Needed 203 162 200Less: Beginning inventory 10 8 9Purchases193 154 190Small gifts: Sept. Oct. Nov.Production 195 153 187 ? Amount/basket (items) ? 5 ? 5 ? 5Needed for production 975 765 935Desired ending inventory 383 468 588Needed 1,358 1,233 1,523Less: Beginning inventory 488 383 468Purchases 870 850 1,055Cellophane: Sept. Oct. Nov.Production 195 153 187。

亨格瑞管理会计英文第15版练习答案06