会计学 教程与案例

会计学教程及案例讲解中英文对照Ch01第一章

Operating Information 操作信息

➢ Needed to conduct day-to-day activities. ➢ Largest quantity of accounting data. ➢ Examples:

Hours worked by employees for payroll purposes. Automobiles available for sale to customers. Amounts owed by customers. Parts and accessories on hand. 需要进行日常活动。 最大数量的会计数据。 例子: 员工为工资的目的而工作的时间。 可供销售给客户的汽车。 客户欠下的。

➢ Accountants in industry.会计行业。 ➢ Professional organization is the Institute of Management Accountants (IMA).专业机构是管理会计师协会(IMA)。

Administers the Certified Management Accountant (CMA) program.管理注册会计师(CMA)项目。 Professional designation for auditors employed in industry is Certified Internal Auditor (CIA). 在行业中被雇佣的审计师的专业名称是经过认证的内部审计师(CIA)。 ➢ Many accounting faculty at universities belong to the American Accounting Association (AAA). ➢ 许多大学的会计系属于美国会计协会(AAA)。 ➢ Controller is the high level officer in organizations responsible for financial and management accounting. ➢ Controller是负责财务和管理会计的组织的高级官员。

自学会计怎么入门教程

自学会计怎么入门教程一、入门教程会计是一个综合性非常强的学科,也是企业运营管理中非常重要的一环。

因此,自学会计成为了很多人的选择。

但是,如何自学会计呢?一、了解会计基础知识首先,学会计需要先了解会计的基础知识,如会计的定义、会计要素和会计凭证等等。

建议初学者先了解一些会计基础知识,为学习打下基础。

二、零基础学会计从零基础开始学习会计需要理解会计科目、会计制度、会计分录和账簿等等。

初学者可以通过购买一些会计基础课程来学习。

例如,可以到知名的在线教育平台上购买课程,如慕课网、Coursera 网等。

这些教育平台提供的课程内容设计严谨,讲解深入浅显易懂,且通常都是免费的。

三、跟进最新的财务政策法规学会计还需要了解相关财务政策和法规。

当前,财务领域发生的变化非常快,因此学习财务政策和法规需要保持及时跟进。

特别是当前的新商法,财务会计管理制度,税收政策以及市场监管架构的建立和完善,对企业会计业务带来的影响非常大。

因此,加强对新财务政策法规的学习和理解,可以帮助学生更好地理解财务会计的需要和发展。

四、进行实践训练练习会计知识是学好会计必不可少的过程,可以通过实现的方式进行训练。

例如,我们可以选用一份企业财务报表作为练习的对象,从中分析、计算和归纳财务数据。

同时,重点分析财务数据的内涵和图形展现方式,让自己更加深入学习、理解。

五、坚持学习学会计的过程其实也是一个不断深挖和不断巩固的过程。

因此,在学习过程中,需要坚持不断学习,不断深化自己对会计知识的理解和认识。

以上五个方面是学会计入门的基础教程,初学者可以根据自己的情况来选择学习的内容,建立起完整的财务知识体系,提高知识水平,以更好地应对实际工作需要。

二、案例分析1、公司A的会计凭证审核公司A的会计人员负责审核和处理公司的财务会计凭证,公司A的领导对会计人员的审核要求非常高,需要严格深入地核对每个项目和金额的准确性和合理性。

因此,会计人员需要具备高度的财务专业知识和细心的工作习惯,每张会计凭证都需要仔细核对几遍,确保不会出现任何错误或不合理数值。

Accounting会计学教程与案例讲义中英文对照Ch04第四章

2

The Account

Device used for calculating net change Simplest form is T-account. Increases listed on one side; decreases listed on other side. Balanced periodically. 用于计算净变化的设备 最简单的形式是丁字式帐户。 在一边的增加;减少在其他方面的上市。 定期平衡。

4-12

要真正理解“借”“贷”的含义,必须了解借贷 记账法账户的结构。 (二)借贷记账法的账户结构 账户的基本结构和资金变动方向的两种情况(增 加和减少)相适应,分为两部份,左边用“借”表 示,称为借方;右边用“贷”表示,称为贷方。 究竟哪一部分记增加,哪一部分记减少,要根据 账户的性质确定。 对于资产、负债、所有者权益账户,借贷

不同的部分形成了记账符号。 记账符号表示将经济业务记入账户的方向。“借” 表示记入账户的左边;“贷”表示记入账户的右边。 而账户的方向又和“增加”,“减少”相联系。 将一项资产记入“借”方,表示资产增加;记入“贷” 方,表示资产的减少。 “借”“贷”作为单纯的记账符号已经失去了其文字本 身的含义,即不能按汉语词典对“借”“贷”的解释来 理解作为记账符号的“借”“贷”的含义。

Chapter 4 Accounting Records and Systems 会计记录和系统

1

Why learn basic record keeping procedures? 为什么要学习基本的记录保存程 序?

Accounting

is best learned by doing. Debit-credit mechanism provides an analytical framework. 会计是最好的学习方法。 债务信用机制提供了一个分析框架。

会计学教程与案例财务会计分册第十12版第3章答案

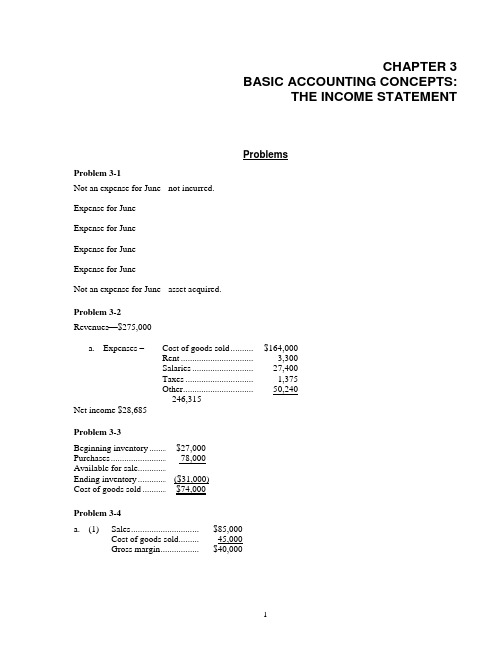

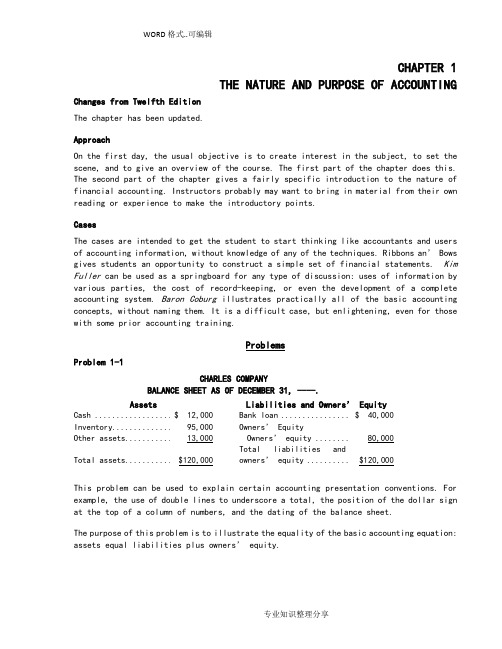

CHAPTER 3BASIC ACCOUNTING CONCEPTS:THE INCOME STATEMENTProblemsProblem 3-1Not an expense for June - not incurred.Expense for JuneExpense for JuneExpense for JuneExpense for JuneNot an expense for June - asset acquired.Problem 3-2Revenues $275,000a.Expenses –Cost of goods sold ...............$164,000Rent .....................................3,300Salaries ................................27,400Taxes ...................................1,375Other ....................................50,240246,315Net income $28,685Problem 3-3Beginning inventory ............$27,000Purchases ............................. 78,000Available for sale .................Ending inventory .................($31,000)Cost of goods sold ...............$74,000Problem 3-4a.(1) Sales ...................................$85,000Cost of goods sold..............45,000Gross margin ......................$40,0001Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/Merchant(2)47 percent gross margin ($40,000 / $85,000)(3)11 percent profit margin (9000/85000)The Woden Corporation had a tax rate of 40 percent ($6,000 / $15,000) on its pretax profit that represented 17.7 percent of its sales ($15,000 / $85,000). The company’s operating expenses were 82.3 percent of sales ($70,000 / $85,000) and its cost of goods sold was 53 percent of sales. The company’s gross margin was 47 percent of sales ($40,000 / $85,000).Problem 3-5Depreciation. Each year for the next 5 years depreciation will be charged to income.No income statement charge. Land is not depreciated.Cost of goods sold. $3,500 charged to current year’s income. $3,500 charged to next year’s income. Subscription expense. $36 charged to current year. $36 charged to next year. Alternatively, $72 charged to current year on grounds $72 is immaterial.Problem 3-6Asset value:October 1, 20X5 $30,000December 31, 20X5 26,250December 31, 20X6 11,250December 31, 20X7 0Expenses:20X5 $3,750 ($1,250 x 3 months)20X6 $15,000 ($1,250 x 12 months)20X7 $11,250 ($1,250 x 9 months)One month’s insurance charge is $1,250 ($30, 000 / 24 months)2©2007 McGraw-Hill/Irwin Chapter 3Problem 3-7QED ELECTRONICS COMPANYIncome Statement for the month of April, ----.Sales ...................................................$33,400Expenses:Bad debts .......................................$ 645Parts ...............................................2,100Interest (880)Wages ............................................10,000Utilities (800)Depreciation ..................................2,700Selling ............................................1,900Administrative ...............................4,700 ______26,925Profit before taxes .............................. 8,075Provision for taxes .............................. 2,800.Net income $6,875Truck purchase has no income statement effect. It is an asset.Sales are recorded as earned, not when cash is received. Bad debt provision of 5 percent related to sales on credit ($33,400 - $20,500) must be recognized. Wages expense is recognized as incurred, not when paid.March’s utility bill is an expense of March when the obligation was incurred.Income tax provision relates to pretax income. Must be matched with related income.Problem 3-8First calculate sales:Sales ($45,000 / (1 - .45)) .................$81,818+Beginning inventory .........................$35,000Purchases ..........................................$40,000Total available ..................................75,000Ending inventory .............................. 30,000Cost of goods sold ............................$45,000Gross margin ....................................$36,818If the gross margin percentage is 45 percent, the cost of goods sold percentage must be 55 percent.Once sales are determined, calculate net income:Net income ($81,818 x .1) $8,1823Accounting: Text and Cases 12e – Instructor’s Manual Anthony/Hawkins/Merchant4Next, prepare balance sheet:Assets LiabilitiesCurrent assets ($50,000 x 1.6) ............................ $ 80,000 Current liabilities .........................$ 50,000 Other assets ($218,182 - $50,000) ................... 138,182 Long term debt 40,000 Total liabilities ............................$ 90,000Owners’ equityBeginning balance .......................$120,000 Plus net income ........................... 8,182 Ending balance ............................$128,182Total assets ..................... $218,182+Total liabilitiesand owners’ equity ......................$218,182+Total assets = Total liabilities and Owner’s equity.Problem 3-9Sales LC 26,666,667 [LC 20,000,000 x (200 / 150)] January cash LC 1,000,000 [LC 500,000 x (200 / 100)] December cash LC 600,000At year-end the company was more liquid in terms of nominal currency (LC 600,000 versus LC 500,000) but in terms of the purchasing power of its cash it was worse off (LC 1,000,000 versus LC 600,000).CasesCase 3-1: Maynard Company (B)Note: This case is unchanged from the Eleventh Edition. Question 1 See below.Question 2This question brings out the difference between cash accounting and accrual accounting. Cash increased by $31,677 whereas net income was $19,635. Explaining the exact difference may be too difficult at this stage, but students should see that:1. The bank loan, a financing transaction, increased cash by $20,865 but did not affect net income.Cash collected on credit sales made last period ($21,798) also increased cash, but did not affect net income this period. (The same is true of the collection of the $11,700 note receivable from Diane Maynard, but it was offset by the payments of the $11,700 dividend to Diane Maynard, the sole shareholder.)©2007 McGraw-Hill/Irwin Chapter 32.MAYNARD COMPANYINCOME STATEMENT, JUNESales ($44,420 cash sales + $26,505 credit sales) .....................$70,925 Less: Cost of sales * ............................................................ 39,345Gross Margin .............................................................................31,580ExpensesWages($5,660+$2,202-$1,974) ..........................................$5,888Utilities (900)Supplies ($5,559+$1,671-$6,630) (600)Insurance($3,150-$2,826) (324)Depreciation ($157,950-$156,000)+($5,928-$5,304) .........2,574Miscellaneous ..................................................................... 135 10,421Income before income tax .........................................................21,159 Income tax expense ($7,224 - $5,700) ................................1,524Net Income ................................................................................19,635 Less: Dividends ................................................................... 11,700Increase in retained earnings .....................................................$ 7,935*Cost of sales:Merchandise purchased for cash .........................................$14,715Merchandise purchased on credit ........................................21,315 [$21,315+($8,517-$8,517)] Inventory, June 1 ................................................................. 29,835Total goods available during June ................................65,865Inventory, June 30 ............................................................... 26,520Cost of Sales .................................................................$39,3453.The purchase of equipment ($23,400) and other assets ($408) decreased cash but did not affectnet income (at least not by this full amount) this period.4.Credit sales made this period ($26,505) increased net income, but did not affect cash.5.Noncash expenses such as depreciation ($2,574) and insurance ($324) decreased net income butdid not affect cash as they relate largely, if not wholly, to cash outflows made for asset acquisition in prior periods. (Exception: such expenses on an entity’s first income statement are not related to prior period expenditures but they will be a much smaller amount than the first accounting period’s expenditures.Question 3(a)$14,715 is incorrect because it is the amount of cash purchases rather than the cost of sales. Thecost of cash purchases and cost of sales amounts would be equal for a period in which all purchases were for cash, and in which the dollar amount of beginning inventory was the same as the dollar amount of ending inventory, since Cost of Sales = Beginning Inventory + Purchases - Ending Inventory.(b)$36,030 is the sum of cash purchases ($14,715) and credit purchases ($21,315). As explainedabove, purchases equal cost of sales for the period only if beginning and ending inventory amounts are the same.5Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/MerchantCase 3-2: Lone Pine Café (B)Note:This case is updated from the Eleventh Edition.ApproachThis case introduces students to preparation of an income statement based on analyzing transactions. At this stage, students are not expected to set up accounts in the formal sense. However, in effect they do so for those income statement items that did not coincide exactly with cash flows.Question 1A suggested income statement as required by Question 1 is shown below. The following notes applyto the income statement.1.The student needs to refer back to Lone Pine Café (A) in order to construct the income statementon the accrual basis. Amounts for sales on credit, purchases on credit, beginning and ending inventory, beginning and ending prepaid operating license, and depreciation expense are to be found there. Specifically:a.Sales revenues = $43,480 cash sales + $870 credit sales to ski instructors = $44,350.b.Food and beverage expense = $2,800 beginning inventory + $10,016 cash purchases + $1,583credit purchases - $2,430 ending inventory = $11,969.2.Since the entity is unincorporated, it is also correct (though less meaningful for evaluativepurposes) to treat the $23,150 partners’ salaries as owners’ drawings. This treatment would result in an income of $12,296 and a decrease in equity (after drawings) of $10,854.LONE PINE CAFE (B)INCOME STATEMENT FOR NOVEMBER 2, 2005, THROUGHMARCH 30, 2006Sales ...........................................................................$ 44,350Expenses:Salaries to partners ................................................$23,150Part-time employee wages .....................................5,480Food and beverage supplies ...................................l1,969Telephone and electricity ......................................3,270Rent expense ..........................................................7,500Depreciation ..........................................................2,445Operating license expense (595)Interest (540)Miscellaneous expenses (255)Total expenses ............................................................55,204(Loss) ..........................................................................$(10,854)6©2007 McGraw-Hill/Irwin Chapter 3Question 2The income statement tells Mrs. Antoine that the partnership has suffered a $10,854 loss for the first five months of operation. This $10,854 loss is the correct figure for evaluative purposes, not the $12,296 income before partners’ salaries. This assumes, of course, that nonowner salaries for the cook and table servers would also have been $23,150, which is questionable. It would appear that Lone Pine Cafe cannot support three partners, even at a bare level of sustenance ($23,150 was only an average of $1,543 per partner/employee per month). Of course the three owner/employees did receive room and board, for which no value has been imputed here.Case 3-3: Dispensers of California, Inc.Note: This is a new case for the Twelfth Edition.ApproachThe case can be used for two class sessions. The first day is devoted to analyzing the accounting transactions, including a preliminary discussion of Hynes’ accounting policy d ecisions. The second class deals with preparing the financial statements and an analysis of how they may change if alternative accounting procedures had been adopted by Hynes.The first class should start with the case Question 1. Its purpose is to give the students a sense of the managerial purpose of profit plans and a context for the later accounting discussions.The use of the asset equals liability plus equity structure to answer Question 2 is recommended so that the instructor can 1) highlight the retained earnings link between net income and the balance sheet 2) illustrate how any accounting transaction can be analyzed using the basic accounting equation and 3) to lay the foundation for the debit-credit framework material in Chapter 4. (At this point in the course debit and credit terminology and analysis should not be used.)Questions 3 and 4 require the preparation of an income statement and balance sheet, respectively. Some instructors prefer to end the first class with a discussion of the balance sheet, including a completed balance sheet. Typically, these instructors want to leave time in the second class to discuss the relationship between net income and the change in cash on the balance sheet.Question 5 is designed to illustrate the role of judgment in accounting for transactions.Answers to QuestionsQuestion 1Profit plans are used for a variety of purposes. These include:▪To force short range planning▪As a basis for evaluating performance and determining compensation.▪To encourage coordination and communication between different organization units and levels.▪As a challenge to improve performance.▪As a means for training managers▪As an early warning system and▪As a guide to spending.7Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/MerchantQuestion 2TN-Exhibit 1 presents an analysis of the planned transactions using the basic accounting equation framework. This analysis follows Hynes’ accounting policy.Question 3TN-Exhibit 2 presents Hynes’ profit plan using the Question 1 transaction analysis.The instructor should expect that most students will not calculate the cost of goods sold figure correctly. The instructor will have to explain that the components of the cost of manufactured goods includes direct materials and their conversion costs, including manufacturing equipment depreciation.The distinction between operating and finance costs in the income statement is another accounting practice most students will miss. Again, the instructor will have to explain this format and its rationale, which is to permit statement users to evaluate how well management has operated the company before considering the impact of their financing decisions.Question 4TN-Exhibit 3 presents the year-end balance sheet using the Question 1 transaction analysis.Equipment is reported net. Most students will follow this presentation. A better presentation is:Equipment (cost) $85,000Accumulated depreciation (8,500)Equipment (net) $76,500The patent is reported net. This is the correct presentation for intangible assets.TN-Exhibit 4 presents a reconciliation of beginning (zero) and ending ($47,500) retained earnings. The instructor may want to share this exhibit with the students. It links the income statement to the balance sheet. It also illustrates that dividends are distributions of capital and not an expense.The instructor should point out to students that many intra period transactions, such as the borrowing and repaying of the bank loan, do not appear on the end of the period balance sheet.Question 5There are three accounting decisions that require Hynes to exercise judgment. They are: ▪Patent valuation▪Patent amortization period▪Equipment depreciation periodStudents might believe Hynes must exercise judgment in the accounting for the redesign and incorporation costs. Under current GAAP this is not the case. Redesign and organization costs must be expensed as incurred.8©2007 McGraw-Hill/Irwin Chapter 3 The patent can not be valued directly. There is no current liquid market for this type of patent. Hynes must value it indirectly. He chose to use the value of the comp any’s equity he received based on the cash paid by the investors for their equity interest to value the patent. This is an acceptable approach.Hopefully, the patent amoralization and depreciation periods represent Hynes’ best estimate of the related asse ts’ useful life (useful to Dispensers of California.)Students should be asked what would be the impact on the balance sheet and income statement if different lives had been used. So that students do not get the impression that differences in judgment are driven by a desire to manage earnings, the instructor should be careful during the discussion to remind the students that different reasonable life estimates can be made by responsible managers acting in good faith.Cash Flow AnalysisIf the instructor wishes to incorporate some aspect of cash flows in the case discussion, TN-Exhibit 5 and 6 present two analysis of cash flows. TN-Exhibit 5 uses a cash receipts and distribution format. TN-Exhibit 6 uses a direct method statement of cash flows format. Instructors should not use the indirect method at this point in the course. It confuses students. Chapter 11 introduces students to indirect method statement of cash flows.9Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/MerchantExhibit 1Dispensers of California, IncBalance Sheet Transaction Analysis* Beginning component parts inventory $0 **Component parts used $197,000Purchases 212,100 Manufacturing payroll 145,000Total available 212,100 Other manufacturing costs 62,000Ending component parts inventory 15,100 Depreciation 8,500Components parts used 197,000 Cost of goods sold 412,50010Exhibit 2Dispensers of California, Inc.12-month Profit PlanSales $598,500Cost of goods soldComponents $197,000Mfg payroll 145,000Other Mfg. 62,000Depreciation 8,500 412,500 Gross margin $186,000Selling, general andAdministration 63,000Patent 20,000Redesign costs 25,000Incorporation costs 2,500Operating profit $75,500Interest 500Profit before taxes $75,000Tax expense 22,500Net Income $52,500Exhibit 3Dispensers of California, Inc.Projected Year-end Balance SheetAssets LiabilitiesCash $78,400 Taxes payable $22,500 Components inventory 15,100 Current liabilities $22,500 Current assets $93,500Equipment (net) 76,500 Owner’s EquityPatent (net) 100,000 Capital stock $200,000___ Retained earnings 47,500$270,000 $270,000Exhibit 4Dispensers of California, Inc.Change in Retained EarningsBeginning retained earnings $0Net income 52,500Dividends (5,000)Ending retained earnings $47,500Exhibit 5Dispensers of California, Inc.Cash ReconciliationReceipts Disbursements New equity capital $80,000Incorporation $2,500Equipment 85,000Redesign 25,000Component parts 212,100Bank loan 30,000Bank loan 30,000Loan interest 500Manufacturing payroll 145,000Other manufacturing 62,000S G & A 63,000Sales 598,500Dividend 5,000Total $708,500 $630,100 Cash ReconciliationReceipts $708,500Disbursements 630,100Ending Balance $78,400Exhibit 6Dispensers of California, Inc.Statement of Cash Flows (Direct Method)Collections from customers $598,500Payments to suppliers (212,100)Payments to employees (295,000)Legal payments (2,500)Interest (500)Operating cash flow $89,400Equipment purchases (85,000)Investing cash flow $(85,000)Bank loan 30,000Repayment of bank loan (30,000)Capital 80,000Dividends (5,000)Financing cash flow $75,000Change in cash $78,400Beginning cash 0Ending cash $78,400Case 3-4: Pinetree MotelNote: This case is updated from the Eleventh Edition.ApproachThis case treats the transition from cash to accrual accounting; also, the inherent difficulties in comparison of data with industry averages are illustrated. The case does not require a full 80 minutes of class time, so I use the final portion of time for review.Comments on QuestionsThe operating statement called for in Question I is shown below. For many terms—e.g., revenues, advertising, depreciation is no difficulty in fitting Pinetree’s account names with the journal’s standard format; but for other items, there are problems:1.Th e Kims’ drawings conceptually should be divided between payroll costs andadministrative/general, since the Kims’apparently perform both operating and administrative tasks.2.Some students may treat replacement of glasses, bed linens, and towels as general expense ratherthan as direct operating expense (although I feel the latter is more appropriate).3.Some students may treat payroll taxes and insurance as a general expense; nevertheless, itproperly is part of payroll costs.Question 2Based on profit as a percent of sales, Pinetree Motel is only about one-third as profitable as the survey average return on sales. The key percentage disparity is on payroll costs, which may reflect two things: (1) the Kims’ tasks could be done by two employees who would work for less than $86,100 a year (which is equivalent to saying the Kims’ drawings reflect both a fair salary and a distribution of entity profits); or (2) the survey data are dominated by motels having twice as many rooms as Pinetree Motel does, thus spreading fixed labor costs over a higher volume (e.g., a motel of 20 units and one of 40 units each needs only one desk clerk). Of course, there is probably a lot of ―noise‖ in the survey data for payroll and administrative/general costs: owner-operators respond ing to the journal’s survey would encounter the same problems as a student does in answering Question 1.PINETREE MOTELOPERATING STATEMENT FOR 2005(in industry trade journal format)Dollars Percentages* Revenues:Room rentals ($236,758- $1,660) .........................................................$235,098 96.8 Other revenue ....................................................................................... 7,703 3.2 Total Revenues ..............................................................................242,801 100.0 Operating Expenses:Payroll costs($86,100+$26,305+$2,894-$795-$84+$1,128+$126) ..........................115,674 47.6 Administrative and general...................................................................——Direct operating expense ($8,800 + $1,660 + $6,820) .........................17,280 7.1 Fees and commissions ..........................................................................——Advertising and promotion($2,335 - $600 + $996) ..............................2,731 1.1 Repairs and maintenance ......................................................................8,980 3.7 Utilities20,767 8.6 ($12,205+$2,789+$5,611-$933-$105-$360+$840+$75+$153+492) .......................................................................................................Total ...............................................................................................165,432 68.1 Fixed expenses:Property taxes, fees ($9,870 - $1,005 + $1,119)...................................9,984 4.1 Insurance ($11,584 - $2,025) ................................................................9,559 3.9 Depreciation .........................................................................................30,280 12.5 Interest ($10,605 - $687 + $579) ..........................................................10,497 4.3 Rent ......................................................................................................——Total ............................................................................................... 60,320 24.8 Profit(pretax) ..............................................................................................$ 17,049 7.1*May not add exactly owing to rounding.As a rough composition that attempts to adjust for the Kims’ (and probably other survey respondents’) dual roles as owners and operators, I suggest adding three accounts:Pinetree AveragePayroll costs .............................47.6 22.5Administrative/general .............— 4.2Profit ......................................... 7.1 20.7Total .........................................54.7 47.4This tends to substantiate the hypothesis that hired employees would perform the Kims’ task for less than $86,100.Pinetree’s other operating costs do not seem to be out of line compared with the survey averages. the higher-than-average utilities may reflect a location with cold winters. Insurance and taxes are essentially uncontrollable. Repairs and maintenance may be below average because the Kims’ personally do some of this work, whereas other motels pay outsiders to do it.Note that both rent and depreciation are shown in the journal’s survey data. This also causes comparison problems. For Pinetree, there is no rent, but the motel buildings are depreciated, whereas for some motels the depreciation would include only furnishings. Adding the rent and depreciation percentages may be more meaningful than working at either one in isolation; but, of course, building depreciation is only a very rough proxy for fair rental value.No final conclusion on the success of their operation can be made as information on the following is lacking:Capital (re: the average) Occupancy rateLocation Seasonality (re: Florida annual season vs. New England)Pricing Efficiency in using their own timeCheck on income calculation:Receipts in 2005 ...........................................................................$244,461Less: 2004 revenue collected ................................................. 1,660Revenues in 2005 .........................................................................$242,801Checks written in 2005 ................................................................196,558Plus: 2005 expenses not paid .......................................................5,508Depreciation .................................................................... 30,280232,346Less: 2004 expenses paid....................................................... 6,594Expenses in 2005 .........................................................................225,752Profit ............................................................................................$ 17,049Case 3-5: National Association of AccountantsNote:This case has been updated since the Eleventh Edition.ApproachThis case describes a typical problem in the management of membership associations and of many other nonprofit organizations. Each year a new governing board is elected and becomes responsible for the operations of the organization for that year. As a general rule, the governing board should so conduct affairs that the organization breaks even financially. If it operates at a deficit, it is eating into resources intended for future members, as suggested in the case. If it operates at a surplus, it is not providing the members with as many services as they are entitled to.Thus, the difference between the concept of income described in the text for business organization and the income concept appropriate for a nonprofit membership organization is that a business organization should earn satisfactory net income, while the membership organization should break even. The measurement of revenues and expenses follows the same principles in both types of organizations (at least with respect to the transactions given in this case.)The case is based, loosely, on experiences of the American Accounting Association, and instructors may wish to refer to the AAA financial statements. The case relates to the ―general fund,‖ which is the portion of the financial statements that reports normal operations. The other columns in these statements can be disregarded. (The NAA is no longer in existence.)In the interest of simplicity, students are not given balance sheets. The case can be made more complicated by assuming a beginning balance sheet, perhaps showing only cash and equity of $55,000 each. Students can then be asked to set up assets and liabilities that result from the transactions described in the case.Answers to QuestionVarious ―correct‖ answers are possible. One set is given in Exhibit A and dis cussed below.1.The grant relates to services to be performed in 2006, so it should not be counted as 2005 revenue.However, the $2,700 already spent must be matched against the grant in some way. This can be done either by subtracting it from 2005 expenses and setting it up as a prepaid asset or, more simply, by transferring $51,300 of the grant to 2006 revenue. The effect on the bottom line is the same. The fact that the president obtained the grant is irrelevant. The principle is to recognize the revenue in the period in which the services are performed. The legal question is probably also irrelevant; the intention was to perform the services in 2006, and that probably would be the governing factor. This is a debatable point, however, because it gives no credit to the 2005 president for the fine work he or she has done in obtaining the grant.2.The desktop publishing system is not an expense of 2005. It will be an expense of future yearsand is therefore an asset on December 31, 2005. Because it was acquired so near the end of the year, there is no need to deal with depreciation. The question can be asked about depreciation in future years, and this raises the question of estimating the future life. Desktop publishing systems are a ―hot‖ item. They are likely t o improve in performance and decrease in price fairly rapidly.The useful life is therefore probably not more than five years. Note that although this is not an expense of 2005, and the 2005 board has created a depreciation cost that will affect the surplus of future boards.。

会计学教程与案例财务会计分册第十12版第2章答案

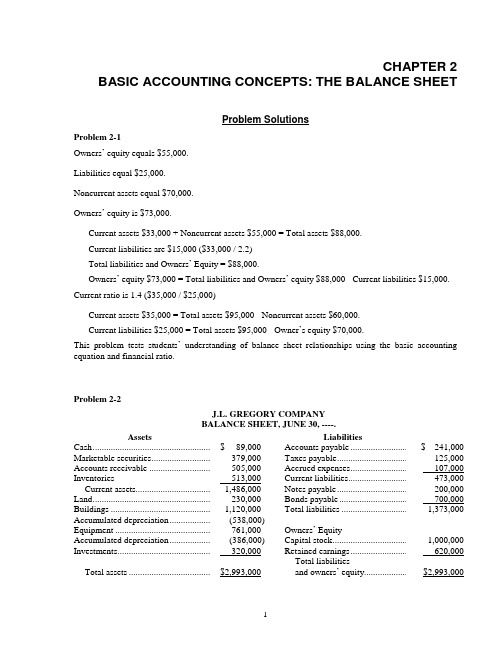

CHAPTER 2 BASIC ACCOUNTING CONCEPTS: THE BALANCE SHEETProblem SolutionsProblem 2-1Owners’ equity equals $55,000.Liabilities equal $25,000.Noncurrent assets equal $70,000.Owners’ equity is $73,000.Current assets $33,000 + Noncurrent assets $55,000 = Total assets $88,000.Current liabilities are $15,000 ($33,000 / 2.2)Total liabilities and Owners’ Equity = $88,000.Owners’ equity $73,000 = Total liabilities and Owners’ equity $88,000 - Current liabilities $15,000. Current ratio is 1.4 ($35,000 / $25,000)Current assets $35,000 = Total assets $95,000 - Noncurrent assets $60,000.Current liabilities $25,000 = Total assets $95,000 - Owner’s equity $70,000.This problem tests students’understanding of balance sheet relationships using the basic accounting equation and financial ratio.Problem 2-2J.L. GREGORY COMPANYBALANCE SHEET, JUNE 30, ----.Assets LiabilitiesCash ........................................................$ 89,000 Accounts payable .............................$ 241,000 Marketable securities ..............................379,000 Taxes payable ...................................125,000 Accounts receivable ...............................505,000 Accrued expenses ............................. 107,000 Inventories 513,000 Current liabilities ..............................473,000 Current assets.....................................1,486,000 Notes payable ...................................200,000 Land ........................................................230,000 Bonds payable .................................. 700,000 Buildings ................................................1,120,000 Total liabilities .................................1,373,000 Accumulated depreciation ......................(538,000)Equipment ..............................................761,000 Owners’ EquityAccumulated depreciation ......................(386,000) Capital stock .....................................1,000,000 Investments ............................................. 320,000 Retained earnings ............................. 620,000$2,993,000Total liabilitiesand owners’ equity.......................$2,993,0001Accounting: Text and Cases 12e – Instructor’s Manual Anthony/Hawkins/Merchant2 Some students may want to test the notes payable as a current liability. Notes payable are usually debt instruments longer than one year, but in the absence of any details listing them as a current liability is acceptable. Problem 2-3Cash + $100,000; Capital stock + $100,000. Bonds payable - $25,000; Capital stock + $25,000. Retained earnings (Depreciation expense) - $8,500.Accumulated depreciation on plant and equipment + $8,500. Cash - $15,900; Inventory + $15,900.Inventory + $9,400; Accounts payable + $9,400.Inventory - $4,500; Accounts receivable + $7,200; Retained earnings + $2,700 Cash + $3,500; Accounts receivable - $3,500.Dividends payable + $3,000; Retained earnings - $3,000. Cash - $3,000; Dividends payable - $3,000. No effect.Some students may simply show the net effect on assets, liabilities, and owners ’ equity without reference to the specific accounts. While this is acceptable, students should be pushed to identify both the net effect and the particular accounts involved. This will help students to become familiar with the balance sheet account names. Problem 2-4CARSON LEGATT PARTNERSHIP BALANCE SHEET AS OF JUNE 1, ----.Assets Capital AccountsCash ....................................................$ 50,000 Carson ...................................................$ 50,000 Inventory ............................................ 50,000 Legatt..................................................... 50,000 Total assets ....................................$100,000Total capital ......................................$100,000CARSON LEGATT PARTNERSHIP BALANCE SHEET AS OF JUNE 30, ----.AssetsLiabilitiesCash ....................................................$ 22,100Bank loan ..............................................$ 50,000 Inventory ............................................58,500 Capital - Carson .....................................51,550 Land ....................................................25,000 Capital - Legatt ......................................54,050 Building .............................................. 50,000 ________ $155,600$155,600©2007 McGraw-Hill/Irwin Chapter 2CARSON LEGATT PARTNERSHIPACCOUNTS, JUNE 30, ----.CarsonCapital - June 1 .........................$50,000Additions ..................................7,750Withdrawals ..............................( 6,200 )Capital - June 30 .......................$51,550LegattCapital - June 1 .........................$50,000Additions ..................................7,750Withdrawals ..............................( 3,700 )Capital - June 30 .......................$54,050Problem 2-5Jan. 4: Retained earnings (Sales) + $12,000; Cash + $12,000 Inventory - $7,000 ;Retained earnings (Cost of goods sold) - $7,000Jan. 6: No effect.Jan. 8: Inventory + $7,000; Accounts Payable + $7,000Jan. 11: Inventory - $1,500; Cash + $2,500; Retained earnings (Sales) + $2,500; Retained earnings (Cost of goods sold) - $1,500Jan. 16: Inventory - $2,000; Retained earnings (Cost of goods sold) - $2,000; Accounts receivable + $3,400; Retained earnings (Sales) + $3,400Jan. 26: Cash - $4,200; Retained earnings (Wages) - $4,200Jan. 29: Cash - $20,000; Land + $20,000Jan. 31: Cash - $2,800; Prepaid insurance + $2,800MARVIN COMPANYBALANCE SHEET AS OF JANUARY 31, ----.Assets LiabilitiesCash .......................................................$12,500 Accounts payable .............................$ 7,000 Accounts receivable ..............................3,400 Total current liabilities .....................$7,000 Inventory ............................................... 46,500Current assets ........................................62,400 Notes payable .................................. 20,000 Land .......................................................20,000 Total liabilities .................................27,000 Prepaid insurance ..................................2,800 Owner’s EquityCapital ..............................................55,000_______ Retained earnings ............................ 3,200 Total assets ......................................$85,200 Total liabilitiesand owners’ equity ...................$85,200Problem 2-6BRIAN COMPANYCURRENT ASSETS AND LIABILITIES AS OF DECEMBER 31, ----.Current Assets Current LiabilitiesCash .......................................................$ 2,000 Accounts payable .............................$5,0003Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/Merchant Marketable securities .............................3,500 Wages payable .................................1,500 Accounts receivable............................... 7,000 Bonds due – current portion ............ 2,000 Current assets ........................................$12,500 Current liabilities .............................$8,500 Current ratio = ...............$12,500 $8,500 = 1.47The current ratio is an indication of an entity’s ability to meet its current obligations.CasesCase 2-1: Maynard Company (A)Note: This case is unchanged from Eleventh Edition.Answers to QuestionsQuestion 1Two suggested balance sheets as required by Question 1 are shown below.Question 2This question provides an opportunity for students to step back and think about the information in a financial statement, rather than focusing on the details of constructing a financial statement. Students can begin to analyze and use the information that the financial statements contain. Students can be asked to identify which accounts have changed significantly between the beginning and ending balance sheets. These would include accounts receivable, note receivable, equipment, accounts payable, taxes payable, and the bank note payable, in addition to the cash account. The only ratio explained in Chapter 2 of the text is the current ratio, so students should be encouraged to ascertain what has happened to the current ratio between June 1 and June 30. Cash has increased largely due to increased accounts and notes payable, as well as cash generated by operations. Cash appears to have been increased by the collection of4©2007 McGraw-Hill/Irwin Chapter 2the note receivable, but as explained in Question 3 below, this was offset by the declaration of an identical dividend, so that the net effect on cash of these two transactions was zero. Equipment purchaseswere a major use of cash. As a result of these events, the June 30 current ratio has fallen to 2.15 from itsJune 1 level of 4.35. Even though the leverage ratios have not yet been introduced in the text, the instructor might want to encourage students to observe that the proportion of liabilities on the right-handside of the balance sheet has increased, with a complementary decrease in the proportion of equities. The capitalization ratio Total Liabilities/Total Liabilities + Equities has increased from 4% on June 1 to 9% onJune 30. While these ratios are still very low, students can be made aware of the importance of identifying trends early.Question 3Retained Earnings has not increased by the amount of net income for the month, $19,635, since Diane Maynard as the sole shareholder declared a dividend of $11,700, which she then used to cancel her loanof $11,700 from the company. Hence, Retained Earnings increased by $7,935 during the month of June. Question 4This question is intended to emphasize early in the course that shareholder’s equity does not necessarily reflect what the entity is worth. Time permitting, the instructor can have students estimate the cash proceeds of piecemeal sale of the assets by a liquidation company, which, net of liabilities, will certainlybe less than $619,446. Then the value of the company as a going concern can be discussed; if June’s $19,635 net income is typical, the firm would be worth more than $619,446 as a going concern. Capitalizing June’s net income on an annual basis ($19,635 x 12) at 10 times earning gives the company avalue in excess of $2 million. The company’s return on equity is very high. On an annual basis it may beas high as 32%. This figure is 12 months’ income ($19,635 x 12) divided by projected year-end equity ($619,446 + $19,635 x 6). This is not a typical business. It is better.MAYNARD COMPANYBALANCE SHEETS AS OF JUNE 1 AND JUNE 30AssetsCurrent Assets: As of June I As of June 30:Cash ...................................................................................$ 34,983 $ 66,660Accounts receivable ..........................................................21,798 26,505Note receivable ..................................................................11,700 0 Merchandise inventory ......................................................29,835 26,520Supplies on hand ...............................................................5,559 6,630Prepaid insurance .............................................................. 3,150 2,826 Total current assets .......................................................$107,025 $129,141 Noncurrent assets:Land ...................................................................................89,700 89,700 Building .............................................................................585,000 585,000 Less: Accumulated depreciation ...................................(156,000 )429,000 ( 157,950 )427,050 Equipment .........................................................................13,260 36,660 Less: Accumulated depreciation ...................................( 5,304 )7,956 ( 5,928 )30,732 Other noncurrent assets ..................................................... 4,857 5,265 Total noncurrent assets ................................................. 531,513 552,747 Total assets ............................................................$638,538 $681,8885Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/MerchantLiabilities and Shareholders’ EquityCurrent liabilities:Accounts payable...............................................................$8,517 $ 21,315Bank notes payable ............................................................8,385 29,250Taxes payable ....................................................................5,700 7,224Accrued wages payable ..................................................... 1,974 2,202 Total current liabilities..................................................$ 24,576 $ 59,991 Other noncurrent liabilities ................................................ 2,451 2,451 Total liabilities ..............................................................27,027 62,442 Shareholders’ Equity:Capital stock ......................................................................390,000 390,000Retained earnings ..............................................................221,511 229,446 Total shareholder’s equity ............................................ 611,511 619,446 Total liabilities and shareholders’ equity .................$638,538 $681,888 Case 2-2: Music Mart, Inc.Note: This case is unchanged from the Eleventh Edition.ApproachThis is a valuable type of problem. The student is in effect analyzing, journalizing, and posting transactions without knowing the technicalities, and hence without being encumbered by them. Some instructors prefer to make up similar transactions and give them in class, rather than, or in addition to,using the set given in this problem. If students can handle these events comfortably, they really understand the essentials of the balance sheet and of the balance sheet equation. They are urged to crossout old balances, rather than erasing them, both because this aids in tracing errors, and because this is analogous to what is done in the ledger.Preservation of the underlying equation in each transaction and the balance sheet should be emphasized throughout.For the accounts already established (e.g., Notes Payable), students should use the identical wording. Thishelps avoid sloppy habits when they start to journalize later on. For new accounts (e.g., Mortgage Payable), they should be given latitude in selecting a title, but having selected one, they must stick to it.6©2007 McGraw-Hill/Irwin Chapter 2MUSIC MART, INC.BALANCE SHEET AS OF _____________________Assets Liabilities and Owners’ Equity Current assets: Current liabilities:Cash ........................................................$25,636 Notes payable ...........................................$ 6,500 Accounts receivable ...............................2,620 Accounts payable ..................................... 5,000 Inventory ................................................4,700 Total current liabilities .........................11,500 Prepaid insurance ................................... 1,224Total current assets ............................34,180 Other liabilities:Mortgage payable ..................................... 9,000Total liabilities ................................20,500Owners’ equityProperty:Paid-in capital ...........................................25,000 Land ........................................................ 12,000 Retained earnings .. (680)$46,180 Total liabilitiesand owners’ equity ...............................$46,180Answers to Questions1.Increase Inventory, $5,000; increase Accounts Payable, $5,0002.Decrease Inventory, $1,500; increase Cash, $2,300; increase Retained Earnings, $8003.Decrease Inventory, $1,700; increase Accounts Receivable, $2,620; increase Retained Earnings, $920(Note that Retained Earnings increases whether or not the proceeds of the sale are received in cash.)4.Increase Prepaid Insurance (or similar), $1,224; decrease Cash, $1,224(Note that current practice is to treat this as a current asset even though the policy is in effect three years; the basis is materiality.)5.Increase Land, $24,000; decrease Cash, $6,000; increase Mortgage payable (noncurrent), $18,000(In view of what happens subsequently, it can be argued that the land is a current asset, or that $12,000 of it is. It depends on whether Smith plans to retain or to sell it. This point should be brought out, to avoid the tendency to classify land as a fixed asset without thinking.)6.Increase Cash, $3,000; decrease Mortgage Payable, $9,000; decrease Land, $12,000Note the decrease in the liability even though it was not “paid off” in cash.)7.No entry. Goodwill is recognized only when it is paid for.8.Decrease Retained Earnings, $1,000; decrease Cash, $1,000.9.Decrease Retained Earnings, $750; decrease Inventory, $750.(Note the basic similarity between #8 and #9; the equity of Smith in the business decreases whenever he, as an individual, takes out assets of the business. Students can of course handle this with a drawing account if they wish to get fancy.)7Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/Merchant 10.No entry, in accordance with the basic principle of value. I think students who argue for appreciationare on weak ground. They have no support from the text. This, together with #6 may be used to contrast accounting with what some would say is the “common sense” or “logical” way to record the events, although it is too much to expect that the arguments in favor of the cost basis of valuation will be fully comprehended at this point.11.Decrease Notes Payable, $6,000; decrease Cash, $6,000.12.No entry. This is not a transaction of the corporation, but rather a transaction between two outsideparties.Note also that the book value of the equity is not changed, even though there is clear evidence that book value is less than market value or “real” value.13.Decrease Inventory, $850; increase Cash, $1,310; increase Retained Earnings, $460.The final balance sheet is shown on the previous page, classified in perhaps more detail than is warranted for this simple set of items.Case 2-3: Lone Pine Cafe (A)Note: This case and its sequel in Chapter 3 are unchanged from the Eleventh Edition.LONE PINE CAFÉBALANCE SHEET AS OF NOVEMBER 2, 2005AssetsCurrent assets:Cash .......................................................................$10,172Inventory ...............................................................2,800Prepaid expense ..................................................... 1,428Tota1 current assets ..........................................$14,440Cafe equipment...................................................... 54,600Total assets .......................................................$69,000Liabilities and Owners’ EquityNote payable ..........................................................$21,000Owners’ equity: .....................................................Mrs. Landers ..........................................................$16,000Mr. Antoine ...........................................................16,000Mrs. Antoine .......................................................... 16,000 48,000Total liabilities and owners’ equity ..................$69,0008©2007 McGraw-Hill/Irwin Chapter 2LONE PINE CAFÉBALANCE SHEET AS OF MARCH 30, 2006AssetsCurrent assets:Cash .........................................................................$ 1,341Accounts receivable (870)Inventory .................................................................2,430Prepaid expense (833)Total current assets .............................................$5,474Noncurrent assets:Cafe equipment .......................................................54,600Less: Accumulated depreciation .............................( 2,445 ) 52,155Total assets .........................................................$57,629Liabilities and Owners’ EquityCurrent liabilities:Accounts payable ....................................................$1,583Other liabilities:Note payable ............................................................ 18,900Total liabilities ....................................................20,483Owners’ equity:Mrs. Landers............................................................$12,382Mr. Antoine .............................................................12,382Mrs. Antoine............................................................ 12,382 37,146Total liabilities and owners’ equity ....................$57,629ApproachThis case can be handled in either of two distinctly different ways: 1) It can be played straight; that is, students can be required to give the answers to questions, and they can be discussed. 2) The balance sheet for November 2 can be developed, and then the second balance sheet can be arrived at by changing the original balance sheet for each transaction. When the latter approach is used, the beginning balance sheet is put on the board (or on a Vugraph) leaving enough room between items so that the additional accounts can be added as needed. Then each fact described in the case is discussed in order, in terms of its effect on the balance sheet. The appropriate figures on the original balance sheet are erased and new figures are put in. (Or, instead of erasing the figures for each transaction, increases and decreases can be shown opposite the proper item, thus laying the ground work for the idea of the account.) A separate item should be set up for Retained Earnings, in which all profit and loss items are entered. The balance in this account is split among the three partners as the final step in the process. This is a lot easier than attempting to split each revenue or expense item among the three partners as it is recorded initially.The second approach is much more difficult than the first, but it has the advantage of emphasizing the effect of individual transactions on the balance sheet. It is particularly difficult to see that the decrease of $8,831 that is necessary to bring Cash down to its known balance of $1,341 is accompanied by a $6,731 decrease in Retained Earnings. This is a subtle point.Some of the points that are brought out by the case, and which either can be summed up explicitly by the instructor or left for the students to see for themselves, are the following:Even at the beginning of our study of accounting, the student can prepare a balance sheet.The dual aspect concept.9Accounting: Text and Cases 12e –Instructor’s Manual Anthony/Hawkins/Merchant There are a number of places in which different words can be used to describe the same basic fact. (I think it is unwise to require or even suggest the generally approved language for any item. Any term that the student wants to propose that is an adequate description of the item should, I think, be accepted and given as much praise as a more customary term. For example, if a student wants to say “owed to vendors” instead of “accounts payable,” I wouldn’t quarrel with that at this point.)There is also room for differences in interpretation of the facts. Even experienced accountants would disagree on how some of the items should be handled. These are mentioned below.The business has incurred a large loss, but there is no way from the information we have of finding out why this loss came about, and therefore no way of suggesting any corrective action. This leads into the usefulness of an income statement, which is the subject of the next chapter.It is easy to get into a discussion of the business entity idea (e.g., how about accounting for the value of the board and room of the partners?), but I doubt that it is desirable to take much time for this at this stage.Instructors may find it interesting to read the actual case from which Lone Pine Cafe wasconstructed. The name is Duncan v. Bartle and the reference is 216 P2d 1005. It should benoted, however, that the actual case is not identical with Lone Pine Cafe since several of thefacts have been omitted for purposes of simplification, and others have been changed in orderto make certain teaching points. Therefore, one cannot go by the actual decision indetermining a “right answer” to the case.Comments on QuestionsThe following notes apply to the balance sheet as of March 30, 2006:The net loss for the period was $10,854. This was divided one-third to each of the partners.The $1,428 paid for local operating licenses is set up as a prepaid expense with 5/12 of its original cost being amortized to the partnership. Due to the questionability of the partnership being able to secure a refund on the unused portion from the local municipality, and the immateriality of the fee, some students may argue that the total cost should be treated as an expense.Mr. Antoine’s clothes are not an asset to the business entity, and therefore are not included on the balance sheet. It might be argued, however, that these clothes included his cook’s uniforms, which could be a cafe asset; but there is no way from the information given to assign a value to such uniforms, even if they did exist.Accounting for the cash register will be troublesome to some students, since it and its contents have been removed from the cafépremises. Regardless of where these items are and that they were improperly removed, they nevertheless are still assets of the entity.The balance sheet as of March 30 shown in the manual is more detailed in format than the situation requires.Question 3 raises the issue of balance sheet values versus real values. If the business is notliquidated, Mrs. Antoine may have no choice but to give the other two partners the amountshown as their equity, since otherwise they might force liquidation, which Mrs. Antoine doesnot want. This is a good time to make the point that owners’ equity, which many people stillrefer to as “net worth,” is at best only a rough approximation of the true worth of a business.If the cafe were sold as a going concern (which in this case would mean transferring theentity name, tangible assets, license and facilities lease), it might be worth more than theindicated “book value” (assuming it had gained a reputation for serving tasty food). On theother hand, in liquidation the inventory is probably virtually worthless, the prepaid expense10©2007 McGraw-Hill/Irwin Chapter 2 has no value, and used restaurant equipment has a notoriously low value when sold at auction.Thus, in liquidation, the assets might scarcely bring enough cash to pay the liabilities.Note also that it will be difficult for Mrs. Antoine to pay each of the other partners his or her $12,382 equity. They may have to take a note payable from Mrs. Antoine and hope for the best. If the cafe assets’ liquidation value is only about $20,500 (enough to pay the liabilities), then Mr. Antoine and Mrs. Landers are no worse off with a note than if they forced liquidation.11。

案例讲解财务报告中的勾稽关系【会计实务操作教程】

(5)长期待摊费用摊销与长期待摊费用中本期摊销数一致;

(6)处置固定资产、无形资产和其他长期资产的损失与营业外收支中 非流动资产处置利得、损失一致; (7)公允价值变动损失与利润表中公允价值变动损失一致;

只分享有价值的会计实操经验,用有限的时间去学习更多的知识!

(8)财务费用与财务费用-利息支出一致; (9)投资损失与利润表中投资收益勾稽; (10)递延所得税资产减少=递延所得资产期初-期末; (11)递延所得税负债增加=递延所得负债期末-期初; (12)存货的减少=存货原值期初-期末; (13)经营性应收项目的减少跟应收账款、预付账款、其他应收款等 有个大致的关系(里面各种情况比较多); (14)经营性应付项目的增加与应付账款、预收账款、其他应付款、 应交税费、应付职工薪酬等有个大致的勾稽关系(里面各种情况比较 多); (15)经营活动产生的现金流量净额=现金流量表中经营活动产生的现 金流量净额。 11.关联方及关联交易 关联方应收应付款项中如果涉及在往来附注中有披露,两者应保持一 致。 12.非经常性损益 涉及营业外收入、营业外支出、投资收益、公允价值变动损益的与相 关科目附注中要核对一致。 四、 资金占用专项报告

资产。

5.递延所得税资产 (1)可抵扣暂时性差异中的资产减值准备应等于各科目资产减值之和 (包括坏账准备);

只分享有价值的会计实操经验,用有限的时间去学习更多的知识!

(2)递延所得税资产/可抵扣暂时性差异=所得税税率。 6.递延收益 政府补助明细中“本期计入营业外收入金额”与营业外收入披露的政 府补助明细相关项目应该一致。 7.资产减值损失 资产减值损失各明细项目与对应的资产减值准备期末期初差额有勾稽 关系。 8.所得税费用 明细中的递延所得税费用=(递延所得资产期初-期末)+(递延所得税 负债期末-期初)。 9.现金流量表项目 收到的其他与经营活动有关的现金中利息收入与财务费用-利息收入有 勾稽关系。 10.现金流量表补充资料 (1)净利润=利润表中的净利润; (2)资产减值准备=利润表中的资产减值损失; (3)固定资产折旧、油气资产折耗、生产性生物资产折旧与相关资产 附注中折旧等本期计提数一致; (4)无形资产摊销与无形资产附注中本期摊销计提数一致;

会计学授课教案

会计学授课教案一、教学目标通过本次课程的学习,学生将能够: 1. 了解会计学的基本概念和原理; 2. 掌握基本的会计核算方法和技巧; 3. 熟悉财务报表的编制和分析; 4. 理解会计信息在企业决策中的作用。

二、教学内容和安排1. 会计学概述•会计学的定义和起源•会计学的发展和研究领域•会计环境和会计伦理2. 会计基础知识•会计等式和会计科目•借贷记账法和账户分类•金融会计和管理会计的区别3. 会计核算方法•资产、负债和所有者权益的核算•收入和费用的核算•成本和期末盈余的确定4. 财务报告和分析•财务报表的分类和编制•财务报表的分析指标和方法•利润表、资产负债表和现金流量表的分析5. 会计信息在企业决策中的应用•预算编制和控制•经营决策和投资决策•运营分析和绩效评估三、教学方法本课程采用多种教学方法相结合的方式进行教学,包括: - 讲授:通过课堂讲解,向学生传授会计学的基本概念和核心知识。

- 案例分析:选取实际会计案例,引导学生进行分析和解决问题,提高实际运用能力。

- 讨论和互动:通过小组讨论、学生提问等方式,鼓励学生参与课堂讨论和互动,提高学习效果。

- 实践操作:安排实际的会计软件操作实验,让学生亲自体验会计核算的过程。

四、评估方式本课程的评估方式主要包括以下几个方面: 1.课堂表现:根据学生的课堂参与情况、讨论表现、问题解决能力等进行评估。

2. 作业和实验报告:布置相关的作业和实验,要求学生按时完成并提交报告,根据报告质量进行评估。

3. 期中考试:设立期中考试,考察学生对于会计学概念和核算方法的理解和应用能力。

4. 期末考试:设立期末考试,考察学生对于财务报表分析和会计信息应用的理解和能力。

五、教学资源为了帮助学生更好地理解和学习会计学,本课程将提供以下教学资源: 1. 教材:选用经典的会计学教材作为参考书,供学生进行自主学习和复习。

2. 幻灯片:教师将提供精心制作的幻灯片,帮助学生掌握重点知识。

Accounting《会计学:教程与案例》财务会计答案解析 第一章

《会计学:教程与案例》财务会计答案第一章案例一:Case 1-1: Ribbons an’ Bows, Inc.Note: This case is unchanged from the Twelfth Edition.注:本案与第十二版持平。

Approach方法This is an introductory case and it should be taught as an introductory case. There will be plenty of time in the course for the students to learn the correct form of financial statements and details of accounting standards. In short, the instructor should be prepared to allow a variety of formats for the financial statements and tolerate some “not quite correct” accounting.这是一个介绍性案例,应该作为一个介绍性案例来教授。

课程中有足够的时间让学生学习财务报表的正确格式和会计准则的细节。

简言之,教师应准备好允许各种财务报表格式,并容忍一些“不太正确”的会计。

The instructor may want to have students discuss Carmen’s March 31 statement, but the bulk of the class should focus on the three case questions. Any discussion of the March 31 statement should deal with the nature of the various accounts (i.e. prepaid rent is rent paid in advance of using the property and it is an asset because it has future economic benefits for the company, etc), rather than the format of the statement. It is better to leave the beginning of the course’s instruction in financial statement formats to the assigned case question discussions.讲师可能希望学生讨论卡门3月31日的声明,但大部分的课应该集中在三个问题上。

会计信息系统操作案例教程 第05章 总账管理系统日常业务处理

13

第五章 总账管理系统日常业务处理

(一)日记账及资金日报表

1、日记账 日记账通常包括库存现金日记账和银行存款日

记账。出纳欲查询日记账,则库存现金和银行存款 科目必须在“会计科目”功能下的“指定科目”中 预先指定。

2、资金日报表 资金日报表主要用于查询、输出或打印资金日

报表,提供当日借、贷金额合计和余额及发生额的 业务量等信息。

19

第五章 总账管理系统日常业务处理

5、填制凭证的其他功能 生成和调用常用凭证 汇总凭证 查看凭证有关信息

11

第五章 总账管理系统日常业务处理

6、凭证记账

(1)记账

条件——期初余额试算平衡、凭证已审核、上月已经结账。 记账过程——选择记账范围、显示记账报告、自动记账,记账

过程一旦中断系统可自动恢复。

(2)取消记账

操作——执行【期末】/【对账】命令; 按 Ctrl+H 键,激活【恢复记账前状态】功能。 (以账套主管的身份进性操作)

12

第五章 总账管理系统日常业务处理

二、出纳管理

总账系统为出纳人 员提供了一个集成办公 环境,包括支票登记簿 功能,用来登记支票的 领用情况;查询现金日 记账、银行存款日记账 及资金日报表;进行银 行对账,并生成银行存 款余额调节表。

主要任务:

出纳签字 库存现金/银行日记账查询 资金日报 支票登记簿 银行对账

(2)“有痕迹”修改凭证 对象——已记账凭证 修改——红字冲销法或补充更正法

7

第五章 总账管理系统日常业务处理

3、作废和删除凭证 对象——未审核、未签字的凭证。 方法——执行〖作废/恢复〗命令; 对作废凭证进行“整理”即可删除。

注意! 作废凭证不能修改、不能审核 作废凭证应参与记账,否ห้องสมุดไป่ตู้月末无法结账

举例说明以前年度损益调整会计处理【会计实务操作教程】

案例一: 2001年 5月,税务部门在对某国有工业企业进行税务稽查时 发现,该企业 2000年度多提固定资产折旧 100万元(为便于计算,数据 已作简化处理,下同),因此责令企业作纳税调整,补交所得税 33万元 (该企业所得税税率 33%)。当时企业会计人员所作的会计处理如下: ①借: 所得税 33(万元)

只分享有价值的会计实操经验,用有限的时间去学习更多的知识!

举例说明以前年度损益调整会计处理【会计实务操作教程】 以前年度损益调整,是指企业对以前年度多计或少计的盈亏数额所进行 的调整。以前年度少计费用或多计收益时,应调整减少本年度利润总额; 以前年度少计收益或多计费用时,应调整增加本年度利润总额。

以前年度损益调整,是指企业对以前年度多计或少计的盈亏数额所进 行的调整。以前年度少计费用或多计收益时,应调整减少本年度利润总 额;以前年度少计收益或多计费用时,应调整增加本年度利润总额。

贷: 以前年度损益调整 300(万元) ②借: 以前年度损益调整 300(万元) 贷: 本年利润 300(万元) 需要特别说明的是: 在会计实务中,一般只有在企业“自查”中发现 的以前年度损益调整事项,才按上述程序处理。如果是在税务稽查或审 计检查中发现的以前年度损益调整事项,或许就不能按此程序处理了。 因为税务或审计人员为了防止税源流失、保护国家利益不受侵害,通常 会要求企业立即进行纳税调整,而非并入期末所得税计算中进行。此时 会计处理程序就应作相应调整:

以前年度损益调整的会计处理 一、本科目核算企业本年度发生的调整以前年度损益的事项以及本年 度发现的重要前期差错更正涉及调整以前年度损益的事项。企业在资产 负债表日至财务报告批准报出日之间发生的需要调整报告年度损益的事 项,也可以通过本科目核算。 二、以前年度损益调整的主要账务处理。 (一)企业调整增加以前年度利润或减少以前年度亏损,借记有关科 目,贷记本科目;调整减少以前年度利润或增加以前年度亏损做相反的会 计分录。 (二)由于以前年度损益调整增加的所得税费用,借记本科目,贷记 “应交税费——应交所得税”等科目;由于以前年度损益调整减少的所得 税费用做相反的会计分录。 (三)经上述调整后,应将本科目的余额转入“利润分配——未分配利 润”科目。本科目如为贷方余额,借记本科目,贷记“利润分配——未 分配利润”科目;如为借方余额做相反的会计分录。 三、本科目结转后应无余额。

《基础会计学教程与案例》课后习题答案

第一章绪论P41单选多选判断业务训练:训练1、属于当期收入或费用、1.2.3训练2、(1)会计处理不正确,违背了会计主体假设,主要违背了可靠性。

(2)假设a.该企业以美元作为记账本位币,那么会计处理合适,但要注意在期末对外报送会计资料时需换算成人民币。

b.该企业以人民币作为记账本位币,那么会计处理不合适,违背了货币计量假设,主要违背了可比性。

(3)不正确,一般来说以月份作为一个会计期间,违背会计分期假设,主要违背了可比性、可理解性。

(4)不正确,违背了一致性、可比性。

(5)不正确,违背了可靠性。

(6)不正确,违背了会计分期假设,可靠性。

(7)正确(8)不正确,违背了会计分期假设,可靠性。

训练3、(1)符合持续经营假设。

(2)违背了会计主体假设。

(3)符合会计分期假设。

(4)符合会计主体假设。

(5)违背了货币计量假设。

(6)违背了会计主体假设。

(7)违背了持续经营假设。

第二章会计要素、账户与复式记账P81业务训练:训练11.涉及的资产:库存现金银行存款账户性质:资产资产记账方位:借方贷方登记余额: 80000 800002.涉及的资产:原材料银行存款应付账款账户性质:资产资产负债记账方位:借方贷方贷方登记余额: 15000 10000 50003. 涉及的资产:银行存款库存现金应收账款账户性质:资产资产资产记账方位:借方借方贷方登记余额: 10000 500 10500训练2.资料(一)中的1235为负债,因为符合负债的定义,第4笔只是计划,是未来的交易事宜。

资料(二)中的第123笔属于收入。

训练3.训练4.(1)(2)(3)计入“固定资产”→资产类→借方记增加,贷方记减少,余额在借方(4))(5)计入“原材料”→资产类→借方记增加,贷方记减少,余额在借方(6)计入“生产成本”→借方记增加,贷方记减少,余额在借方(7)计入“库存商品”→借方记增加,贷方记减少,余额在借方(8)计入“银行存款”→资产类→借方记增加,贷方记减少,余额在借方。

零基础怎么开始学会计专业

零基础怎么开始学会计专业学习会计专业需要具备数学、逻辑思维和分析能力,初学者一般可以从以下步骤开始:1. 学习会计基础知识学习会计基础知识是学习会计的首要任务。

新手需要了解会计的基本概念和术语,掌握会计凭证的制作方法和会计账簿的记录方法,并学习会计报表的分析方法。

初学者可以选用专门的会计学习教材或上网查找相关视频教程进行自学。

2. 掌握会计软件应用现代会计工作主要依赖计算机或手机等终端设备,因此,初学者需要掌握常用的会计软件应用,如财务软件、电子表格等,以便进行会计凭证的制作、财务报表的制作和数据分析。

3. 学习会计法规和税法会计法规和税法是会计从业人员的必备知识。

初学者需要了解财务报表编制的相关规定,如会计准则、财务报表编制规范,以及了解税务部门的税收政策和法规,如税收计算方法、税收政策调整等。

4. 参加会计培训课程和考试参加会计培训课程和考试是学习会计的不二选择。

初学者可以找到本地职业学校或线上学习平台,报名参加相关培训课程和考试。

培训课程可以帮助学生系统掌握会计基础知识,考试是检验学习成果的有效途径。

5. 积极参加实习工作会计实习工作是学习会计最好的途径之一。

初学者可以通过实习工作熟悉会计工作流程,掌握会计报表编制,以及了解会计工作中的实际问题和应对方法,提高自己的职业技能。

以下是几个关于零基础怎么开始学会计专业的案例:案例一:小陆的会计学习之路小陆零基础学会计,在一个月之内通过网上自学和培训课程,掌握了会计基础知识和软件应用,顺利通过了初级会计实务考试。

他注重实践锻炼,在学习之余去做了一份会计实习工作,获得了实践经验和职业技能提升。

案例二:小张通过考试进入会计行业小张从事销售工作多年后,加入会计行业,他没有会计专业背景,但很快学会了会计基础知识,通过专业培训班和考试,成功地获得了初级会计职业资格证书。

他的职业技能和实践经验得到了进一步提升,成为了一名合格的会计从业者。

案例三:小王的实践经验贡献助力小王是一名大学生,学习会计专业并通过相关考试。

ACCOUNTING会计学教程与案例讲义中英文对照Ch06第六章

4

Methods of determining amounts in inventory 确定存货量的方法

Periodic inventory method or Perpetual inventory method. 定期盘存方法或 永续盘存法。 Measurement of inventories and cost of sales are related. 库存和销售成本的测量是相关的。

11

Merchandise companies 商品的公司

Inventories accounted for at cost. Cost includes cost of Acquiring merchandise (invoice cost of goods, freight-in) Making goods ready for sale. ( unpacking and marking) Adjust for: Returns and allowances Cash discounts from supplier. 存货以成本价计算。 成本包括成本的 购买商品(货物的发票成本,货物运输) 为销售做好准备。(拆包和标记) 调整为: 收益和津贴 现金折扣从供应商。

16

Periodic inventory method 定期盘存方法

Determine amount of ending inventory and deduce costs of goods sold. Count inventory (i.e., a physical inventory is taken) at the end of the period. Multiply count times cost for each item to determine total amount of inventory. Beginning inventory of current period = ending inventory of preceding period. COGS = COGA - End. Inventory 确定期末库存的数量,并推算出销售的货物的成本。 统计库存(即。在这段时间结束时,将会有一个实体的库存)。 每件商品的数量乘以成本,以确定库存的总数量。 开始存货盘点=期末库存。 COGA-End。库存

会计相关的专业文献

以下是一些与会计相关的专业文献:

《财务会计四大难题》:常勋著,中国财政经济出版社2005年1月第二版。

《金融企业会计制度操作指南》:经济科学出版社,2004年3月第一版。

《现代商业银行全面风险管理》:王卫东著,中国经济出版社2001年版。

《会计学四大难题》:娄尔行著,上海财经大学出版社2000年版。

《会计制度设计》:陈今池著,立信会计出版社1993年版。

《会计理论》:汤云为、钱逢胜著,上海财经大学出版社1997年版。

《会计学原理》:吴水澎著,辽宁人民出版社2001年版。

《会计案例》:乔世震著,中国财经出版社1999年版。

《会计学教程与案例》:安索尼、里斯、赫特斯坦著,北京大学出版社2000年版。

这些文献都是与会计学相关的重要著作,涵盖了财务会计、风险管理、商业银行、会计制度设计、会计理论等方面的内容,适合相关专业人士阅读和学习。

销售返利的税务处理案例【会计实务操作教程】

只分享有价值的会计实操经验,用有限的时间去学习更多的知识!

入。以后经销商实际享受返利时,转销该预计负债。主要是因为: 1. 将返利计入预计负债是符合权责发生制要求的。 2. 收入代表的经济利益流入应当是导致所有者权益增加的。但此处的

部分经济利益与应在未来享受的返利相关,需递延到以后确认,所以不 构成现在的收入,计提时应冲减当期收入。

只分享有价值的会计实操经验,用有限的时间去学习更多的知识!

借:预收账款 160000 贷:主营业务收入 160000 借:主营业务成本 137500(1100×5%×0.25) 贷:库存商品 137500

会计是一门很基础的学科,无论你是企业老板还是投资者,无论你是 税务局还是银行,任何涉及到资金决策的部门都至少要懂得些会计知 识。而我们作为专业人员不仅仅是把会计当作“敲门砖”也就是说,不 仅仅是获得了资格或者能力就结束了,社会是不断向前进步的,具体到 我们的工作中也是会不断发展的,我们学到的东西不可能会一直有用, 对于已经舍弃的东西需要我们学习新的知识来替换它,这就是专业能力 的保持。因此,那些只把会计当门砖的人,到最后是很难在岗位上立足 的。话又说回来,会计实操经验也不是一天两天可以学到的,坚持一天 学一点,然后在学习的过程中找到自己的缺陷,你可以针对自己的习惯 来制定自己的学习方案,只有你自己才能知道自己的不足。最后希望同 学们都能够大量的储备知识和拥有更好更大的发展。

3. 现金返利不属于无偿赠送,应冲减收入,不建议计入销售费用。 在实际工作中,往往是经销商已经达到了相关合同条款中规定的返利 条件,而企业尚未计提该项负债,惠而浦与经销商签订合同时,应该有 明确的返利政策,期末可以合理估计确定相关负债金额,惠而浦此次会 计差错因没有按照规定计提销售返利,导致收入虚增,利润浮盈。 例 1. 彤升公司与代理商协议,销售给代理商 10000元商品,年底完成 目标第二年返利 3510元。 (1)第一年的会计处理: 借:应收账款等 10000 贷:主营业务收入 8547 应交税费——应交增值税(销项税额) 1453 借:主营业务收入——折扣 3000 贷:预计负债 3000 注:企业所得税按照所有权转移作为纳税义务发生时间,会计上计提 的现金返利 3000元汇算清缴时要做纳税调增处理。 (2)第二年,实际开具红字折扣发票抵顶货款等时: 借:预计负债 3000 贷:应收账款等 3510

《会计学_教程和案例》财务会计答案与解析solutiontoAccounting_textandcases_Financialaccouting