会计学英文版经典教程 (4)

基础会计学四单元课件英文版PPT课件

Salaries payable

Unearned consulting revenue

C. Taylor, Capital

C. Taylor, Withdrawals

200

Consulting revenue

Rental revenue

Depreciation expense-Equipment

375

Debit

Cash

$ 4,350

Accounts receivable

1,800

Supplies

8,670

Prepaid insurance

2,300

Equipment

26,000

Accumulated depreciation-Equip.

Accounts payable

Salaries payable

8,670

Prepaid insurance

2,300

Equipment

26,000

Accumulated depreciation-Equip.

Accounts payable

Salaries payable

Unearned consulting revenue

C. Taylor, Capital

balance columns

4 Extend adjusted trial balance amounts to the F/S

columns

5 Total F/S columns, compute net income or loss, and

complete the worksheet

4-7

Unearned consulting revenue

大学课程《会计英语》PPT课件:Chapter 10 Unit 4

Cash Defined in the Context of the

Cash Flow Statement

Cash is a non-productive asset, and therefore companies strive to keep their immediately accessible cash balance at a minimum. Instead of carrying large cash balances, companies place their cash in term deposits, or other money market instruments so that they can earn interest. For purposes of the cash flow statement, therefore, cash includes cash on hand ,cash on deposit, and highly liquid short-term investments——cash equivalents.

The Uses of a Cash Flow Statement

The cash flow statement reveals not only the operating cash flow of the company, but also enables the user to reconcile the cash flows to net income. Users can thereby see just how a company can have a cash flow that is different from the reported net income.

理论力学梁昆淼答案

理论力学梁昆淼答案【篇一:大学课本答案大全】【大学四年100万份资料大集合】/forum.php?mod=viewthreadtid=7083fromuid=461166 新视野大学英语课后习题答案1-4册全集/forum.php?mod=viewthreadtid=6423fromuid=461166 《毛泽东思想和中国特色社会主义理论体系概论》有史以来最全面的复习资料!!!/forum.php?mod=viewthreadtid=5900fromuid=461166 中国近现代史纲要课后题答案/forum.php?mod=viewthreadtid=5310fromuid=461166 新视野大学英语第四册答案(第二版)/forum.php?mod=viewthreadtid=5161fromuid=461166 新视野大学英语视听说第三册答案/forum.php?mod=viewthreadtid=2647fromuid=461166 《物理化学》习题解答(天津大学, 第四版,106张)/forum.php?mod=viewthreadtid=2531fromuid=461166 新视野大学英语听说教程1听力原文及答案下载/forum.php?mod=viewthreadtid=2006fromuid=461166 西方宏观经济高鸿业第四版课后答案/forum.php?mod=viewthreadtid=1282fromuid=461166 大学英语综合教程 1-4册练习答案/forum.php?mod=viewthreadtid=1275fromuid=461166 新视野大学英语课本详解(四册全)/forum.php?mod=viewthreadtid=805fromuid=461166 新视野大学英语读写教程3册的课后习题答案/forum.php?mod=viewthreadtid=514fromuid=461166 毛邓三全部课后思考题答案(高教版)/毛邓三课后答案/forum.php?mod=viewthreadtid=384fromuid=461166/forum.php?mod=viewthreadtid=305fromuid=461166 《会计学原理》同步练习题答案/forum.php?mod=viewthreadtid=304fromuid=461166 《管理学》课后答案(周三多)计》习题及答案(自学推荐,23页)/forum.php?mod=viewthreadtid=300fromuid=461166 《成本会计》配套习题集参考答案/forum.php?mod=viewthreadtid=294fromuid=461166 《现代西方经济学(微观经济学)》笔记与课后习题详解(第3版,宋承先) /forum.php?mod=viewthreadtid=290fromuid=461166 《国际贸易》课后习题答案(海闻 p.林德特王新奎)/forum.php?mod=viewthreadtid=289fromuid=461166 《西方经济学》习题答案(第三版,高鸿业)可直接打印/forum.php?mod=viewthreadtid=283fromuid=461166《微观经济学》课后答案(高鸿业版)/forum.php?mod=viewthreadtid=280fromuid=461166 《管理学》经典笔记(周三多,第二版)/forum.php?mod=viewthreadtid=277fromuid=461166 《教育心理学》课后习题答案(皮连生版)/forum.php?mod=viewthreadtid=268fromuid=461166 《信号与系统》习题答案(第四版,吴大正)/forum.php?mod=viewthreadtid=262fromuid=461166 《计算机操作系统》习题答案(汤子瀛版,完整版)/forum.php?mod=viewthreadtid=260fromuid=461166 高等数学习题答案及提示/forum.php?mod=viewthreadtid=258fromuid=461166 《生物化学》复习资料大全(3套试卷及答案+各章习题集)/forum.php?mod=viewthreadtid=249fromuid=461166 《概率论与数理统计》8套习题及习题答案(自学推荐)/forum.php?mod=viewthreadtid=244fromuid=461166 《线性代数》9套习题+9套相应答案(自学,复习推荐)/forum.php?mod=viewthreadtid=236fromuid=461166 《高分子化学》课后习题答案(第四版,潘祖仁主编)/forum.php?mod=viewthreadtid=232fromuid=461166 《电工学》课后习题答案(第六版,上册,秦曾煌主编)/forum.php?mod=viewthreadtid=217fromuid=461166 《大学物理》完整习题答案理》课后习题答案及每章总结(樊昌信,国防工业出版社,第五版)/forum.php?mod=viewthreadtid=195fromuid=461166 《化工原理答案》课后习题答案(高教出版社,王志魁主编,第三版)/forum.php?mod=viewthreadtid=191fromuid=461166 《工程力学》课后习题答案(梅凤翔主编)/forum.php?mod=viewthreadtid=186fromuid=461166 《中国近代史纲要》课后习题答案/forum.php?mod=viewthreadtid=182fromuid=461166 《概率论与数理统计》优秀学习资料/forum.php?mod=viewthreadtid=181fromuid=461166 《中国近现代史》选择题全集(共含250道题目和答案)/forum.php?mod=viewthreadtid=178fromuid=461166 《概率论与数理统计及其应用》课后答案(浙江大学盛骤谢式千编著)/forum.php?mod=viewthreadtid=174fromuid=461166 《数字信号处理——基于计算机的方法》习题答案(第二版)/forum.php?mod=viewthreadtid=173fromuid=461166 《数据结构习题集》答案(c版,清华大学,严蔚敏)/forum.php?mod=viewthreadtid=172fromuid=461166 《大学物理基础教程》课后习题答案(第二版,等教育出版社)/forum.php?mod=viewthreadtid=170fromuid=461166c语言资料大全(有课后答案,自学资料,c程序等)/forum.php?mod=viewthreadtid=168fromuid=461166 《新编大学英语》课后答案(第三册)/forum.php?mod=viewthreadtid=164fromuid=461166 《电力电子技术》习题答案(第四版,王兆安,王俊主编)/forum.php?mod=viewthreadtid=163fromuid=461166 《中级财务会计》习题答案(第二版,刘永泽)/forum.php?mod=viewthreadtid=162fromuid=461166 《常微分方程》习题解答(王高雄版)/forum.php?mod=viewthreadtid=161fromuid=461166 《c++程序设计》课后习题答案(第2版,吴乃陵,高教版)/forum.php?mod=viewthreadtid=158fromuid=461166 《机械制图》习题册答案(近机类、非机类,清华大学出版社)学》习题答案(南大,第五版)/forum.php?mod=viewthreadtid=142fromuid=461166 《高频电子线路》习题参考答案(第四版)/forum.php?mod=viewthreadtid=138fromuid=461166 《宏观经济学》课后答案(曼昆,中文版)/forum.php?mod=viewthreadtid=137fromuid=461166 《电路》习题答案上(邱关源,第五版)/forum.php?mod=viewthreadtid=136fromuid=461166《信息论与编码》辅导ppt及部分习题答案(曹雪虹,张宗橙,北京邮电大学出版社)/forum.php?mod=viewthreadtid=122fromuid=461166 《分析化学》课后习题答案(第五版,高教版)/forum.php?mod=viewthreadtid=112fromuid=461166 《电工学》习题答案(第六版,秦曾煌)/forum.php?mod=viewthreadtid=102fromuid=461166 《离散数学》习题答案(高等教育出版社)/forum.php?mod=viewthreadtid=96fromuid=461166 《机械设计》课后习题答案(高教版,第八版,西北工业大学)/forum.php?mod=viewthreadtid=90fromuid=461166 《数字电子技术基础》习题答案(阎石,第五版)/forum.php?mod=viewthreadtid=85fromuid=461166 曼昆《经济学原理》课后习题解答/forum.php?mod=viewthreadtid=83fromuid=461166 《流体力学》习题答案/forum.php?mod=viewthreadtid=81fromuid=461166 《中国近代史纲要》完整课后答案(高教版)/forum.php?mod=viewthreadtid=78fromuid=461166 《全新版大学英语综合教程》(第四册)练习答案及课文译文/forum.php?mod=viewthreadtid=77fromuid=461166 《全新版大学英语综合教程》(第三册)练习答案及课文译文/forum.php?mod=viewthreadtid=76fromuid=461166《全新版大学英语综合教程》(第二册)练习答案及课文译文/forum.php?mod=viewthreadtid=75fromuid=461166 《全新版大学英语综合教程》(第一册)练习答案及课文译文线性系统分析》习题答案及辅导参考(吴大正版)/forum.php?mod=viewthreadtid=69fromuid=461166 《有机化学》习题答案(汪小兰主编)/forum.php?mod=viewthreadtid=66fromuid=461166 高等数学上下《习题ppt》/forum.php?mod=viewthreadtid=63fromuid=461166 思想道德修养与法律基础课后习题答案/forum.php?mod=viewthreadtid=61fromuid=461166 新编大学英语4(外研版)课后练习答案/forum.php?mod=viewthreadtid=60fromuid=461166 西方经济学(高鸿业版)教材详细答案/forum.php?mod=viewthreadtid=59fromuid=461166 《c语言程序与设计》习题答案(谭浩强,第三版)/forum.php?mod=viewthreadtid=58fromuid=461166 《数字信号处理》课后答案及详细辅导(丁美玉,第二版)/forum.php?mod=viewthreadtid=57fromuid=461166 《概率论与数理统计》习题答案/forum.php?mod=viewthreadtid=55fromuid=461166 《理论力学》课后习题答案/forum.php?mod=viewthreadtid=52fromuid=461166 《自动控制原理》课后题答案(胡寿松,第四版)/forum.php?mod=viewthreadtid=50fromuid=461166 《物理学》习题分析与解答(马文蔚主编,清华大学,第五版)/forum.php?mod=viewthreadtid=48fromuid=461166 《毛泽东思想和中国特色社会主义理论体系概论》习题答案(2008年修订版的) /forum.php?mod=viewthreadtid=47fromuid=461166 完整的英文原版曼昆宏观、微观经济学答案/forum.php?mod=viewthreadtid=46fromuid=461166 离散数学习题解答(第四版)清华大学出版社/forum.php?mod=viewthreadtid=45fromuid=461166 《电机与拖动基础》课后习题答案(第四版,机械工业出版社,顾绳谷主编)/forum.php?mod=viewthreadtid=44fromuid=461166 《现代通信原理》习题答案(曹志刚版)/forum.php?mod=viewthreadtid=43fromuid=461166 《土力学》习题解答/课后答案/forum.php?mod=viewthreadtid=42fromuid=461166 《模拟电子技术基础》详细习题答案(童诗白,华成英版,高教版)/forum.php?mod=viewthreadtid=41fromuid=461166 《模拟电子技术基础简明教程》课后习题答案(杨素行第三版)/forum.php?mod=viewthreadtid=38fromuid=461166《数学物理方法》习题解答案详细版(梁昆淼,第二版)/forum.php?mod=viewthreadtid=37fromuid=461166 《马克思主义基本原理概论》新版完整答案/forum.php?mod=viewthreadtid=36fromuid=461166 《单片机原理及应用》课后习题答案(张毅刚主编,高教版)/forum.php?mod=viewthreadtid=35fromuid=461166 机械设计课程设计——二级斜齿圆柱齿轮减速器(word+原图)/forum.php?mod=viewthreadtid=34fromuid=461166 《管理运筹学》第二版习题答案(韩伯棠教授)/forum.php?mod=viewthreadtid=31fromuid=461166 《材料力学》详细辅导及课后答案(pdf格式,共642页)/forum.php?mod=viewthreadtid=29fromuid=461166 《统计学》课后答案(第二版,贾俊平版)/forum.php?mod=viewthreadtid=28fromuid=461166 谢希仁《计算机网络教程》(第五版)习题参考答案(共48页)/forum.php?mod=viewthreadtid=25fromuid=461166 《大学基础物理学》课后答案(共16个单元)/forum.php?mod=viewthreadtid=23fromuid=461166 机械设计基础(第五版)习题答案[杨可桢等主编]/forum.php?mod=viewthreadtid=22fromuid=461166 流体力学课后答案(高教版,张也影,第二版)/forum.php?mod=viewthreadtid=21fromuid=461166 《模拟电子技术基础》课后习题答案(共10章)/forum.php?mod=viewthreadtid=20fromuid=461166 《液压传动》第2版思考题和习题解答(共36页)/forum.php?mod=viewthreadtid=18fromuid=461166 高等数学(同济第五版)课后答案(pdf格式,共527页)/forum.php?mod=viewthreadtid=17fromuid=461166 《线性代数》(同济第四版)课后习题答案(完整版)/forum.php?mod=viewthreadtid=16fromuid=461166 《新视野大学英语读写教程(第二版)第三册》课后答案/forum.php?mod=viewthreadtid=15fromuid=461166 《新视野大学英语读写教程(第二版)第二册》课后答案/forum.php?mod=viewthreadtid=14fromuid=461166 新视野大学英语读写教程(第二版)第一册》课后答案/forum.php?mod=viewthreadtid=13fromuid=461166 统计学原理作业及参考答案/forum.php?mod=viewthreadtid=9fromuid=461166 大学英语精读第3册答案(外教社)/forum.php?mod=viewthreadtid=8fromuid=461166 大学数学基础教程课后答案(微积分)/forum.php?mod=viewthreadtid=7fromuid=461166 21世纪大学英语读写教程(第四册)课后答案/forum.php?mod=viewthreadtid=6fromuid=461166【篇二:大学所有科目习题答案文件大全】txt>第 2 页共 163 页第 3 页共 163 页第 4 页共 163 页第 5 页共 163 页【篇三:大学教材课后习题答案大集合】第一部分:【经济金融】/forum-19-1.html/thread-305-1-1.html [pdf格式]《会计学原理》同步练习题答案/thread-301-1-1.html [word格式]《成本会计》习题及答案(自学推荐,23页) /thread-300-1-1.html [word格式]《成本会计》配套习题集参考答案/thread-299-1-1.html [word格式]《实用成本会计》习题答案 /thread-296-1-1.html [word格式]《会计电算化》教材习题答案(09年) /thread-295-1-1.html [jpg格式]会计从业《基础会计》课后答案 /thread-294-1-1.html [word格式]《现代西方经济学(微观经济学)》笔记与课后习题详解(第3版,宋承先)/thread-293-1-1.html [word格式]《宏观经济学》习题答案(第七版,多恩布什) /thread-290-1-1.html [word格式]《国际贸易》课后习题答案(海闻 p.林德特王新奎) /thread-289-1-1.html [pdf格式]《西方经济学》习题答案(第三版,高鸿业)可直接打印/thread-288-1-1.html [word格式]《金融工程》课后题答案(郑振龙版) /thread-286-1-1.html [word格式]《宏观经济学》课后答案(布兰查德版) /thread-285-1-1.html [jpg格式]《投资学》课后习题答案(英文版,牛逼版)/thread-284-1-1.html [pdf格式]《投资学》课后习题答案(博迪,第四版) /thread-283-1-1.html [word格式]《微观经济学》课后答案(高鸿业版) /thread-282-1-1.html [word格式]《公司理财》课后答案(英文版,第六版) /thread-281-1-1.html [word格式]《国际经济学》教师手册及课后习题答案(克鲁格曼,第六版)/thread-279-1-1.html [word格式]《金融市场学》课后习题答案(张亦春,郑振龙,第二版) /thread-278-1-1.html [pdf格式]《金融市场学》电子书(张亦春,郑振龙,第二版) /thread-254-1-1.html [word格式]《微观经济学》课后答案(平狄克版) /thread-163-1-1.html [word格式]《中级财务会计》习题答案(第二版,刘永泽) /thread-155-1-1.html [pdf格式]《国际经济学》习题答案(萨尔瓦多,英文版) /thread-138-1-1.html [jpg格式]《宏观经济学》课后答案(曼昆,中文版) /thread-134-1-1.html [pdf格式]《宏观经济学》答案(曼昆,第五版,英文版)pdf格式 /thread-109-1-1.html [word格式]《技术经济学概论》(第二版)习题答案/thread-85-1-1.html [word格式]曼昆《经济学原理》课后习题解答/thread-60-1-1.html [pdf格式]西方经济学(高鸿业版)教材详细答案 /thread-47-1-1.html [word格式]完整的英文原版曼昆宏观、微观经济学答案《财务报表分析与证券定价》第二版答案(英文版)【人大-高鸿业版】【西方经济学(宏观部分)第四版】课后习题答案(pdf)【人大-高鸿业版】【西方经济学(微观部分)第四版】课后习题答案(word/txt)《财务管理》系统答案(人大出版,全)第二部分:【化学物理】/forum-26-1.html/thread-274-1-1.html[word格式]《固体物理》习题解答(方俊鑫版)/thread-271-1-1.html[word格式]《简明结构化学》课后习题答案(第三版,夏少武)/thread-258-1-1.html[word格式]《生物化学》复习资料大全(3套试卷及答案+各章习题集)/thread-245-1-1.html[pdf格式]《光学教程》习题答案(第四版,姚启钧原著)/thread-242-1-1.html[word格式]《流体力学》实验分析答案(浙工大版)/thread-236-1-1.html[word格式]《高分子化学》课后习题答案(第四版,潘祖仁主编)/thread-235-1-1.html[pdf格式]《化工热力学》习题与习题答案(含各种版本)/thread-230-1-1.html[word格式]《材料力学》习题答案/thread-226-1-1.html[word格式]《量子力学导论》习题答案(曾谨言版,北京大学)/thread-217-1-1.html [word格式]《大学物理》完整习题答案/thread-213-1-1.html [ppt格式]流体输配管网习题详解(重点)/thread-212-1-1.html [pdf格式]《结构化学基础》习题答案(周公度,北大版) /thread-205-1-1.html [pdf格式]《物理化学》习题答案与课件集合(南大)/thread-200-1-1.html [word格式]《传热学》课后习题答案(第四版) /thread-196-1-1.html [word格式]《控制电机》习题答案 /thread-195-1-1.html [pdf格式]《化工原理答案》课后习题答案(高教出版社,王志魁主编,第三版) /thread-191-1-1.html [pdf格式]《工程力学》课后习题答案(梅凤翔主编)/thread-188-1-1.html [pdg格式]《工程电磁场导论》习题详解/thread-187-1-1.html [pdf格式]《材料力学》习题答案(单辉祖,北京航空航天大学)/thread-184-1-1.html [word格式]《热工基础》习题答案(张学学主编,第二版,高等教育出版社) /thread-175-1-1.html [word格式]《大学物理实验》实验题目参考答案(第2版,中国林业出版社) /thread-172-1-1.html [word格式]《大学物理基础教程》课后习题答案(第二版,等教育出版社) /thread-165-1-1.html [word格式]《水力学》习题答案(李炜,徐孝平主编,武汉水利电力大学出版社) /thread-160-1-1.html[pdf格式]《普通物理学教程电磁学》课后习题答案(梁灿斌,第2版) /thread-153-1-1.html [word格式]《激光原理与激光技术》习题答案完整版(北京工业大学出版社) /thread-152-1-1.html[word格式]《固体物理》习题解答(阎守胜版) /thread-145-1-1.html [ppt格式]《仪器分析》课后答案(第三版,朱明华编)/thread-144-1-1.html [word格式]《高分子化学》习题答案(第四版) /thread-143-1-1.html [pdf格式]《物理化学》习题答案(南大,第五版) /thread-142-1-1.html [ppt格式]《高频电子线路》习题参考答案(第四版) /thread-141-1-1.html [pdf格式]《原子物理学》习题答案(褚圣麟版) /thread-140-1-1.html [ppt格式]《分析力学》习题答案 /thread-139-1-1.html [word格式]《分析化学》习题答案(第三版,上册,高教版) /thread-133-1-1.html [ppt格式]《普通物理》习题答案(磁学,电学,热学) /thread-124-1-1.html [pdf格式]《材料力学》课后习题答案(单辉祖,第二版,高教出版社)/thread-122-1-1.html [word格式]《分析化学》课后习题答案(第五版,高教版) /thread-121-1-1.html [word格式]《分析化学》习题解答 /thread-119-1-1.html [word格式]《理论力学》课后习题答案(赫桐生,高教版) /thread-114-1-1.html [word格式]《大学物理学》习题解答。

教育部办公厅关于公布2007年度普通高等教育精品教材书目的通知

教高厅函〔2007〕46号

教育部办公厅关于公布2007年度普通

高等教育精品教材书目的通知

各省、自治区、直辖市教育厅(教委),新疆生产建设兵团教育局,部属各高等学校,有关出版社:

为进一步提高高等教育教材质量,推动优秀教材进课堂,我部决定在已出版的“十一五”国家级规划教材中评选精品。

经出版社申报、专家评审,确定了218种教材为2007年度普通高等教育精品教材。

现将精品教材书目予以公布,供各高等学校选用教材时参考。

附件:2007年度普通高等教育精品教材书目

教育部办公厅

二○○七年七月二日

2007年度普通高等教育精品教材书目。

管理会计CO教程4朗泽topsap培训系列

风险管理

管理会计通过分析数据和信息 ,帮助企业识别和应对风险,

提高风险管理水平。

管理会计的历史与发展

历史回顾

管理会计起源于20世纪初的工业 革命时期,随着企业规模扩大和 市场竞争加剧而逐渐发展起来。

发展趋势

未来管理会计将更加注重战略价 值创造、数字化转型、组织变革 等方面的研究和实践。

CO教程介绍

THANKS.

SAP系统提供了销售管理、库存管理 和财务管理等功能,帮助零售企业实 现精细化管理。

SAP系统的实施与管理

项目管理

SAP系统的实施需要专业的项目 管理团队进行全程跟踪和管理,

确保项目按时按质完成。

定制化开发

根据企业的实际需求,SAP系统可 以进行定制化开发,满足企业的特 殊需求。

培训与推广

为了使员工更好地适应SAP系统, 企业需要进行系统的培训和推广工 作,提高员工的操作技能和意识。

SAP系统介绍

03

SAP系统的功能与特点

集成化企业资源规划

SAP系统集成了企业各个业务 模块的信息,实现了资源的优

化配置和管理。

高度自动化

SAP系统通过预设的流程和规 则,实现了业务流程的自动化 处理,提高了工作效率。

实时数据分析

SAP系统提供了强大的数据分 析工具,能够帮助企业实时了 解经营状况,做出科学决策。

管理会计co教程4朗泽 topsap培训系列

contents

目录

• 管理会计概述 • CO教程介绍 • SAP系统介绍 • 管理会计与SAP系统的结合应用定义

管理会计是一门以现代管理理论为基础,运用一系列专门方法和技术,对会计 信息进行加工、整理、分析和报告,旨在为组织内部管理者提供决策支持的会 计学科。

西方财务会计培训教程(英文版)PPT课件( 68页)

LO 1 Discuss the characteristics of the corporate form of organization.

The Corporate Form of Organization

Variety of Ownership Interests

Corporate Capital

No-Par Stock

Reasons for issuance: Avoids contingent liability. Avoids confusion over recording par value versus fair market value.

Some states require that no-par stock have a stated value.

Corporate Capital

Stock Issued with Other Securities

Two methods of allocating proceeds: 1. the proportional method and 2. the incremental method.

LO 3 Explain the accounting procedures for issuing shares of stock.

The Corporate Form of Organization

State Corporate Law

Corporation must submit articles of incorporation to the state in which incorporation is desired.

会计类高等数学教材推荐

会计类高等数学教材推荐高等数学是会计专业的基础课程之一,对会计学生来说,选择一本适合的高等数学教材是非常重要的。

本文将向你推荐几本经典的会计类高等数学教材,帮助你在学习过程中更好地掌握数学知识。

一、《高等数学(第七版)》《高等数学(第七版)》是由同济大学出版社出版的经典教材。

该教材内容全面,结构清晰,注重数学概念的理解和应用。

教材以示例为主线,每个章节都有大量的例题和习题供学生练习。

同时,教材还提供了详细的解答和习题答案,方便学生自我检验。

该教材在会计专业中应用广泛,被广大学生和教师所推崇。

二、《高等数学(第八版)》《高等数学(第八版)》是清华大学出版社出版的教材。

该教材对数学基本概念进行了详细的讲解,并且通过大量的例题和习题帮助学生巩固所学知识。

与其他教材相比,该教材更加注重数学的应用能力培养,通过实际问题的分析和解决,培养学生的数学思维和创新能力。

该教材内容丰富,覆盖了会计专业所需的各个数学概念和知识点,是一本非常实用的教材。

三、《应用高等数学》《应用高等数学》是北京航空航天大学出版社出版的教材。

该教材以应用为导向,注重数学知识的实际应用。

该教材的特点是理论与实践相结合,通过大量的案例和实际应用问题的分析来教授数学知识,能够更好地帮助学生理解和掌握所学内容。

该教材内容全面,适合会计专业学生使用。

四、《高等数学应用教程》《高等数学应用教程》是人民邮电出版社出版的教材。

该教材是以教材为主,辅以实例分析和应用案例,通过实例和案例的讲解,帮助学生更好地理解数学知识和应用技巧。

该教材的特点是案例丰富,内容多样,注重实际应用和问题解决能力的培养。

对于会计专业的学生来说,该教材是一本不可多得的好教材。

综上所述,对于会计类高等数学教材的选择,我们推荐《高等数学(第七版)》、《高等数学(第八版)》、《应用高等数学》和《高等数学应用教程》这四本经典教材。

无论你是初学者还是已经有一定数学基础的人,这些教材都可以帮助你更好地掌握会计类高等数学知识。

大学期间各科目的课后习题答案与模拟卷及往年原题

《新视野大学英语读写教程(第二版)第三册》课后答案新视野大学英语读写教程(第二版)第一册》课后答案《马·克思主·义大体原理概论》新版完整答案《毛·泽东思想和中国特色社会主·义理论体系概论》习题答案(2020年修订版的)21世纪大学实用英语综合教程(第一册)课后答案及课文翻译西方经济学(高鸿业版)教材详细答案《新视野大学英语读写教程(第二版)第二册》课后答案思想道德修养与法律基础课后习题答案《中国近代史纲要》完整课后答案(高教版)《全新版大学英语综合教程》(第三册)练习答案及课文译文《全新版大学英语综合教程》(第一册)练习答案及课文译文《会计学原理》同步练习题答案《微观经济学》课后答案(高鸿业版)《统计学》课后答案(第二版,贾俊平版)《西方经济学》习题答案(第三版,高鸿业)可直接打印毛邓三全部课后思考题答案(高教版)/毛邓三课后答案新视野大学英语听说教程1听力原文及答案下载西方宏观经济高鸿业第四版课后答案《管理学》经典笔记(周三多,第二版)《中国近代史纲要》课后习题答案《理论力学》课后习题答案《线性代数》(同济第四版)课后习题答案(完整版)高等数学(同济第五版)课后答案(PDF格式,共527页)中国近现代史纲要课后题答案曼昆《经济学原理》课后习题解答21世纪大学英语读写教程(第三册)参考答案谢希仁《计算机网络教程》(第五版)习题参考答案(共48页)《概率论与数理统计》习题答案《模拟电子技术基础》详细习题答案(童诗白,华成英版,高教版)《机械设计》课后习题答案(高教版,第八版,西北工业大学)《大学物理》完整习题答案《管理学》课后答案(周三多)机械设计基础(第五版)习题答案[杨可桢等主编]程守洙、江之永主编《普通物理学》(第五版)详细解答及辅导新视野大学英语课本详解(四册全)21世纪大学英语读写教程(第四册)课后答案新视野大学英语读写教程3册的课后习题答案新视野大学英语第四册答案(第二版)《中国近现代史》选择题全集(共含250道题目和答案)《电工学》课后习题答案(第六版,上册,秦曾煌主编)完整的英文原版曼昆宏观、微观经济学答案《数字电子技术基础》习题答案(阎石,第五版)《电路》习题答案上(邱关源,第五版)《电工学》习题答案(第六版,秦曾煌)21世纪大学英语读写教程(第三册)课文翻译《生物化学》复习资料大全(3套试卷及答案+各章习题集)《模拟电子技术基础》课后习题答案(共10章)《概率论与数理统计及其应用》课后答案(浙江大学盛骤谢式千编著)《理论力学》课后习题答案(赫桐生,高教版)《全新版大学英语综合教程》(第四册)练习答案及课文译文《化工原理答案》课后习题答案(高教出版社,王志魁主编,第三版)《国际贸易》课后习题答案(海闻P.林德特王新奎)大学英语综合教程1-4册练习答案《流体力学》习题答案《传热学》课后习题答案(第四版)高等数学习题答案及提示《高分子化学》课后习题答案(第四版,潘祖仁主编)马·克思主·义大体原理概论答案《计算机网络》课后习题解答(谢希仁,第五版)《概率论与数理统计》优秀学习资料《离散数学》习题答案(高等教育出版社)《模拟电子技术基础简明教程》课后习题答案(杨素行第三版)《信号与线性系统分析》习题答案及辅导参考(吴大正版)《教育心理学》课后习题答案(皮连生版)《理论力学》习题答案(动力学和静力学)选修课《中国现当代文学》资料包机械设计课程设计——二级斜齿圆柱齿轮减速器(WORD+原图)《成本会计》配套习题集参考答案《概率论与数理统计》8套习题及习题答案(自学推荐)《现代西方经济学(微观经济学)》笔记与课后习题详解(第3版,宋承先)《计算机操作系统》习题答案(汤子瀛版,完整版)《毛·泽东思想和中国特色社会主·义理论体系概论》有史以来最全面的温习资料!!!《线性代数》9套习题+9套相应答案(自学,复习推荐)《管理理论与实务》课后题答案(手写版,中央财经大学,赵丽芬)统计学原理作业及参考答案机械设计课程设计——带式运输机的传动装置的设计《物理学》习题分析与解答(马文蔚主编,清·华大学,第五版)《新编大学英语》课后答案(第三册)《通信原理》课后习题答案及每章总结(樊昌信,国防工业出版社,第五版)《c语言程序与设计》习题答案(谭浩强,第三版)《微生物学》课后习题答案(周德庆版)新视野第二版全四册听说教程答案《宏观经济学》课后答案(曼昆,中文版)《电力电子技术》习题答案(第四版,王兆安,王俊主编)《土力学》习题解答/课后答案《公司法》课后练习及参考答案《全新版大学英语综合教程》(第二册)练习答案及课文译文新视野大学英语视听说第三册答案《工程力学》课后习题答案(梅凤翔主编)《理论力学》详细习题答案(第六版,哈工大出版社)《成本会计》习题及答案(自学推荐,23页)《自动控制原理》课后题答案(胡寿松,第四版)《复变函数》习题答案(第四版)《信号与系统》习题答案(第四版,吴大正)《有机化学》课后答案(第二版,高教版,徐寿昌主编)《电工学——电子技术》习题答案(下册)《财务管理学》章后练习参考答案(人大出版,第四版)现代汉语题库(语法部分)及答案《概率论与数理统计》习题详解(浙大二、三版通用)《有机化学》习题答案(汪小兰主编)《微机原理及应用》习题答案《管理运筹学》第二版习题答案(韩伯棠教授)《古代汉语》习题集(附习题答案)福建人民出版社《金融市场学》课后习题答案(张亦春,郑振龙,第二版)《公共关系学》习题及参考答案(复习必备)现代汉语通论(邵敬敏版)词汇语法课后练习答案《国际经济学》教师手册及课后习题答案(克鲁格曼,第六版)《教育技术》课后习题答案参考(北师大)《金融市场学》课后答案(郑振龙版)《组织行为学》习题集答案(参考下,还是蛮好的)《分析化学》课后习题答案(第五版,高教版)大学英语精读第3册答案(外教社)《国际经济学》习题答案(萨尔瓦多,英文版)《复变函数与积分变换》习题答案《信息论与编码》辅导PPT及部分习题答案(曹雪虹,张宗橙,北京邮电大学出版社)《宏观经济学》习题答案(第七版,多恩布什)《物理化学》习题解答(天津大学, 第四版,106张)新视野大学英语视听说教程第一册《机械制造技术》习题集与答案解析新视野大学英语听说教程2册听力原文及答案下载管理学试题(附答案)《材料力学》详细辅导及课后答案(PDF格式,共642页)六级词汇注解《大学基础物理学》课后答案(共16个单元)《管理学——原理与方式》课后习题答案新视野2版第三册(大2上学期用)曼昆《经济学原理》中文第四版.课后习题答案-清晰图片版《数据库系统概论》课后习题(第四版)大学数学基础教程课后答案(微积分)《投资学》课后习题答案(博迪,第四版)流体力学课后答案(高教版,张也影,第二版)《语言学概论》习题答案(自考,新版教材)《统计学》各章练习题答案《数字电子技术基础》课后习题答案(完整答案版)《积分变换》习题答案(配套东南大学张元林编的)《中级财务会计》习题答案(第二版,刘永泽)《计算机网络》课后习题答案(第5版和第4版)《单片机原理及应用》课后习题答案(张毅刚主编,高教版)《金融工程》课后题答案(郑振龙版)《液压传动》第2版思考题和习题解答(共36页)《动物学》习题集与答案(资料相当丰富)《高频电子线路》习题参考答案(第四版)《国际经济法》课后参考答案大学英语四级十年真题+听力《信号与系统》习题详解(奥本海姆版)《电路分析》课后答案及学习指导(第二版,胡翔骏,高教版)《C语言设计》(谭浩强,第三版)227页新视野大学英语课后习题答案1-4册全集《数字电路与逻辑设计》课后习题答案,讲解详细《电路》第五版课后答案《材料力学》详细习题答案及辅导(第四版,刘鸿文)《传播学教程》课后答案(郭庆光主编,完整版)《物理化学》习题答案与课件集合(南大)《金融市场学》电子书(张亦春,郑振龙,第二版)毛邓三95%考点高等教育出版社《毛·泽东思想和中国特色社会主·义道路》(09版,原毛邓三)课后题答案《线性代数》课后习题答案(陈维新,科学出版社)自动控制原理习题集(自学辅导推荐)《现代通信原理》习题答案(曹志刚版)高等数学上下《习题PPT》《数据结构习题集》答案(C版,清·华大学,严蔚敏)《大学物理学》习题解答《物理化学》习题答案(南大,第五版)《机械原理》复习精要与习题精解(第7版,西北大学)《宏观经济学》答案(曼昆,第五版,英文版)pdf格式《化工热力学》习题与习题答案(含各种版本)《材料力学》习题答案教育统计与测量管理心理学(自考必备资料,牛逼打印版)离散数学习题解答(第四版)清·华大学出版社货币银行学《技术经济学概论》(第二版)习题答案《毛·泽东思想和社会主·义建设理论题概论》精炼考试题目,耐心整理《数字信号处理》课后答案及详细辅导(丁美玉,第二版)《语言学概论练习题》答案《会计电算化》教材习题答案(09年)《数据库系统概论》习题答案(第四版)《微观经济学》课后答案(平狄克版)《控制工程基础》课后习题解答(清·华版)《高分子化学》习题答案(第四版)《电机与拖动基础》课后习题答案(第四版,机械工业出版社,顾绳谷主编)《机械工程测试技术基础》(第三版,熊诗波等主编)课后答案《宏观经济学》课后答案(布兰查德版)《机械原理》习题答案和超多例题(西北工业大学,第六版)《大学物理基础教程》课后习题答案(第二版,等教育出版社)简明乐谱基础知识《语言学教程》课后答案《公司理财》课后答案(英文版,第六版)《信息论与编码》学习辅导及习题详解(傅祖芸版)《遗传学》课后习题答案(朱军主编,完整版)现代人心理实战700题处世韬略《自动控制原理》习题答案《普通动物学》完整课后答案(刘凌云,郑光美版)《微机原理》作业答案(李继灿版)尼尔·波兹曼《娱乐至死》《电力电子技术》习题答案(第4版,西安交通大学)大学英语四级(CET-4)历年真题大全[89-07年39套](精品级)753页word 《通信原理》习题答案《普通化学(第五版)》习题详解(配套浙大编的)经济法课后复习及思考答案《结构化学基础》习题答案(周公度,北大版)财务管理学课后答案荆新王化成《C++程序设计》课后习题答案(第2版,吴乃陵,高教版)药用植物的两份习题(自己感觉比较有用)《数学物理方法》习题解答案详细版(梁昆淼,第二版)《机械制图》习题册答案(近机类、非机类,清·华大学出版社)《控制工程基础》习题答案(第二版,燕山大学)《画法几何》资料包(含习题答案,自学辅导课件)《畜禽解剖学与组织胚胎学》习题答案参考《统计学》课后习题答案(周恒彤编)《西方经济学简明教程》课后习题全解(尹伯成,上海人民出版社)《汽车理论》课后答案详细解答(余志生,机械工业出版社)《数学物理方法》(第三版)习题答案新视野听力原文及课后答案新编大学英语4(外研版)课后练习答案《材料力学》习题答案(单辉祖,北京航空航天大学)大学英语精读第3册课文及课后答案《自动控制原理》课后习题答案———胡寿松,第五版《数据库系统原理与设计》课后答案(第四版,王珊,萨师煊)《数字电子技术基础》详细习题答案(阎石第四版)财经应用文笔记《管理学》课后习题答案(罗宾斯,人大版,第7版)《概率论与数理统计》习题答案(复旦大学出版社)《数字信号处理——基于运算机的方式》习题答案(第二版)《传热学》课后答案(杨世铭,陶文铨主编,高教版)C语言资料大全(有课后答案,自学资料,C程序等)毛邓三重点归纳《电力拖动自动控制系统》习题答案逄锦聚《政治经济学》(第3版)笔记和课后习题详解《概率论与数理统计》课后习题解答(东南大学出版社)《有机化学》课后习题答案(胡宏纹,第三版)《常微分方程》习题解答(王高雄版)▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆【因为太多了,没方法再粘贴到那个地址了,更多答案,直接进入下面那个搜索就好】源地址:||。

教育部高等教育司关于公布2008年度普通高等教育精品教材书目的通知

教育部高等教育司关于公布2008年度普通高等教育精

品教材书目的通知

文章属性

•【制定机关】教育部

•【公布日期】2008.09.09

•【文号】教高司函[2008]194号

•【施行日期】2008.09.09

•【效力等级】部门规范性文件

•【时效性】现行有效

•【主题分类】高等教育

正文

教育部高等教育司关于公布2008年度普通高等教育精品教材

书目的通知

(教高司函[2008]194号)

各省、自治区、直辖市教育厅(教委),新疆生产建设兵团教育局,部属各高等学校,有关出版社:

为进一步加强高等教育教材建设,促进“十一五”规划教材质量不断提高,我司对已出版的普通高等教育“十一五”规划教材进行了评审。

经出版社申报、专家评审,确定了292种教材为2008年度普通高等教育精品教材。

现将精品教材书目予以公布,供各高等学校选用教材时参考。

附件:2008年度普通高等教育精品教材书目

教育部高等教育司

二○○八年九月九日附件:

2008年度普通高等教育精品教材书目。

大学课后习题答案大全

▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆《新视野大学英语读写教程(第二版)第三册》课后答案/viewthread.php?tid=16&fromuid-14755-1-1新视野大学英语读写教程(第二版)第一册》课后答案/viewthread.php?tid=14&fromuid-14755-1-1《马·克思主·义基本原理概论》新版完整答案/viewthread.php?tid=37&fromuid-14755-1-1《毛·泽东思想和中国特色社会主·义理论体系概论》习题答案(2008年修订版的)/viewthread.php?tid=48&fromuid-14755-1-121世纪大学实用英语综合教程(第一册)课后答案及课文翻译/viewthread.php?tid=4&fromuid-14755-1-1西方经济学(高鸿业版)教材详细答案/viewthread.php?tid=60&fromuid-14755-1-1《新视野大学英语读写教程(第二版)第二册》课后答案/viewthread.php?tid=15&55-14755-1-1思想道德修养与法律基础课后习题答案/viewthread.php?tid=63&fromuid-14755-1-1《中国近代史纲要》完整课后答案(高教版)/viewthread.php?tid=81&fromuid=14755-1-1《全新版大学英语综合教程》(第三册)练习答案及课文译文/viewthread.php?tid=77&fromuid=14755-1-1《全新版大学英语综合教程》(第一册)练习答案及课文译文/viewthread.php?tid=75&fromuid=14755-1-1《会计学原理》同步练习题答案/viewthread.php?tid=305&fromuid=14755-1-1《微观经济学》课后答案(高鸿业版)/viewthread.php?tid=283&fromuid=14755-1-1《统计学》课后答案(第二版,贾俊平版)/viewthread.php?tid=29&fromuid=14755-1-1《西方经济学》习题答案(第三版,高鸿业)可直接打印/viewthread.php?tid=289&fromuid=14755-1-1毛邓三全部课后思考题答案(高教版)/毛邓三课后答案/viewthread.php?tid=514&fromuid=14755-1-1新视野大学英语听说教程1听力原文及答案下载西方宏观经济高鸿业第四版课后答案/viewthread.php?tid=2006&fromuid=14755-1-1《管理学》经典笔记(周三多,第二版)/viewthread.php?tid=280&fromuid=14755-1-1《中国近代史纲要》课后习题答案/viewthread.php?tid=186&fromuid=14755-1-1《理论力学》课后习题答案/viewthread.php?tid=55&fromuid=14755-1-1《线性代数》(同济第四版)课后习题答案(完整版)/viewthread.php?tid=17&fromuid=14755-1-1高等数学(同济第五版)课后答案(PDF格式,共527页)/viewthread.php?tid=18&fromuid=14755-1-1中国近现代史纲要课后题答案/viewthread.php?tid=5900&fromuid=14755-1-1曼昆《经济学原理》课后习题解答/viewthread.php?tid=85&fromuid=14755-1-1 21世纪大学英语读写教程(第三册)参考答案/viewthread.php?tid=5&fromuid=14755-1-1谢希仁《计算机网络教程》(第五版)习题参考答案(共48页)/viewthread.php?tid=28&fromuid=14755-1-1《概率论与数理统计》习题答案/viewthread.php?tid=57&fromuid=14755-1-1《模拟电子技术基础》详细习题答案(童诗白,华成英版,高教版)/viewthread.php?tid=42&fromuid=14755-1-1《机械设计》课后习题答案(高教版,第八版,西北工业大学)/viewthread.php?tid=96&fromuid=14755-1-1《大学物理》完整习题答案/viewthread.php?tid=217&fromuid=14755-1-1《管理学》课后答案(周三多)/viewthread.php?tid=304&fromuid=14755-1-1机械设计基础(第五版)习题答案[杨可桢等主编]/viewthread.php?tid=23&fromuid=14755-1-1程守洙、江之永主编《普通物理学》(第五版)详细解答及辅导/viewthread.php?tid=3&fromuid=14755-1-1新视野大学英语课本详解(四册全)/viewthread.php?tid=1275&fromuid=14755-1-1 21世纪大学英语读写教程(第四册)课后答案/viewthread.php?tid=7&fromuid=14755-1-1新视野大学英语读写教程3册的课后习题答案/viewthread.php?tid=805&fromuid=14755-1-1新视野大学英语第四册答案(第二版)/viewthread.php?tid=5310&fromuid=14755-1-1《中国近现代史》选择题全集(共含250道题目和答案)《电工学》课后习题答案(第六版,上册,秦曾煌主编)/viewthread.php?tid=232&fromuid=14755-1-1完整的英文原版曼昆宏观、微观经济学答案/viewthread.php?tid=47&fromuid=14755-1-1《数字电子技术基础》习题答案(阎石,第五版)/viewthread.php?tid=90&fromuid=14755-1-1《电路》习题答案上(邱关源,第五版)/viewthread.php?tid=137&fromuid=14755-1-1《电工学》习题答案(第六版,秦曾煌)/viewthread.php?tid=112&fromuid=14755-1-121世纪大学英语读写教程(第三册)课文翻译/viewthread.php?tid=6&fromuid=14755-1-1《生物化学》复习资料大全(3套试卷及答案+各章习题集)/viewthread.php?tid=258&fromuid=14755-1-1《模拟电子技术基础》课后习题答案(共10章)/viewthread.php?tid=21&fromuid=14755-1-1《概率论与数理统计及其应用》课后答案(浙江大学盛骤谢式千编著)/viewthread.php?tid=178&fromuid=14755-1-1《理论力学》课后习题答案(赫桐生,高教版)/viewthread.php?tid=119&fromuid=14755-1-1《全新版大学英语综合教程》(第四册)练习答案及课文译文/viewthread.php?tid=78&fromuid=14755-1-1《化工原理答案》课后习题答案(高教出版社,王志魁主编,第三版)/viewthread.php?tid=195&fromuid=14755-1-1《国际贸易》课后习题答案(海闻P.林德特王新奎)/viewthread.php?tid=290&fromuid=14755-1-1大学英语综合教程1-4册练习答案/viewthread.php?tid=1282&fromuid=14755-1-1《流体力学》习题答案/viewthread.php?tid=83&fromuid=14755-1-1《传热学》课后习题答案(第四版)/viewthread.php?tid=200&fromuid=14755-1-1高等数学习题答案及提示/viewthread.php?tid=260&fromuid=14755-1-1《高分子化学》课后习题答案(第四版,潘祖仁主编)/viewthread.php?tid=236&fromuid=14755-1-1马·克思主·义基本原理概论答案/viewthread.php?tid=6417&fromuid=14755-1-1《计算机网络》课后习题解答(谢希仁,第五版)/viewthread.php?tid=3434&fromuid=14755-1-1《概率论与数理统计》优秀学习资料/viewthread.php?tid=182&fromuid=14755-1-1《离散数学》习题答案(高等教育出版社)/viewthread.php?tid=102&fromuid=14755-1-1《模拟电子技术基础简明教程》课后习题答案(杨素行第三版)/viewthread.php?tid=41&fromuid=14755-1-1《信号与线性系统分析》习题答案及辅导参考(吴大正版)/viewthread.php?tid=74&fromuid=14755-1-1《教育心理学》课后习题答案(皮连生版)/viewthread.php?tid=277&fromuid=14755-1-1《理论力学》习题答案(动力学和静力学)/viewthread.php?tid=221&fromuid=14755-1-1选修课《中国现当代文学》资料包/viewthread.php?tid=273&fromuid=14755-1-1机械设计课程设计——二级斜齿圆柱齿轮减速器(WORD+原图)/viewthread.php?tid=35&fromuid=14755-1-1《成本会计》配套习题集参考答案/viewthread.php?tid=300&fromuid=14755-1-1《概率论与数理统计》8套习题及习题答案(自学推荐)/viewthread.php?tid=249&fromuid=14755-1-1《现代西方经济学(微观经济学)》笔记与课后习题详解(第3版,宋承先)/viewthread.php?tid=294&fromuid=14755-1-1《计算机操作系统》习题答案(汤子瀛版,完整版)/viewthread.php?tid=262&fromuid=14755-1-1《毛·泽东思想和中国特色社会主·义理论体系概论》有史以来最全面的复习资料!!!/viewthread.php?tid=6423&fromuid=14755-1-1《线性代数》9套习题+9套相应答案(自学,复习推荐)/viewthread.php?tid=244&fromuid=14755-1-1《管理理论与实务》课后题答案(手写版,中央财经大学,赵丽芬)/viewthread.php?tid=287&fromuid=14755-1-1统计学原理作业及参考答案/viewthread.php?tid=13&fromuid=14755-1-1机械设计课程设计——带式运输机的传动装置的设计/viewthread.php?tid=222&fromuid=14755-1-1《物理学》习题分析与解答(马文蔚主编,清·华大学,第五版)/viewthread.php?tid=50&fromuid=14755-1-1《新编大学英语》课后答案(第三册)/viewthread.php?tid=168&fromuid=14755-1-1《通信原理》课后习题答案及每章总结(樊昌信,国防工业出版社,第五版)/viewthread.php?tid=203&fromuid=14755-1-1《c语言程序与设计》习题答案(谭浩强,第三版)/viewthread.php?tid=59&fromuid=14755-1-1《微生物学》课后习题答案(周德庆版)/viewthread.php?tid=291&fromuid=14755-1-1新视野第二版全四册听说教程答案/viewthread.php?tid=6959&fromuid=14755-1-1《宏观经济学》课后答案(曼昆,中文版)/viewthread.php?tid=138&fromuid=14755-1-1《电力电子技术》习题答案(第四版,王兆安,王俊主编)/viewthread.php?tid=164&fromuid=14755-1-1《土力学》习题解答/课后答案/viewthread.php?tid=43&fromuid=14755-1-1《公司法》课后练习及参考答案/viewthread.php?tid=307&fromuid=14755-1-1《全新版大学英语综合教程》(第二册)练习答案及课文译文/viewthread.php?tid=76&fromuid=14755-1-1新视野大学英语视听说第三册答案/viewthread.php?tid=5161&fromuid=14755-1-1《工程力学》课后习题答案(梅凤翔主编)/viewthread.php?tid=191&fromuid=14755-1-1《理论力学》详细习题答案(第六版,哈工大出版社)/viewthread.php?tid=2445&fromuid=14755-1-1《成本会计》习题及答案(自学推荐,23页)/viewthread.php?tid=301&fromuid=14755-1-1《自动控制原理》课后题答案(胡寿松,第四版)/viewthread.php?tid=52&fromuid=14755-1-1《复变函数》习题答案(第四版)/viewthread.php?tid=118&fromuid=14755-1-1《信号与系统》习题答案(第四版,吴大正)/viewthread.php?tid=268&fromuid=14755-1-1《有机化学》课后答案(第二版,高教版,徐寿昌主编)/viewthread.php?tid=3830&fromuid=14755-1-1《电工学——电子技术》习题答案(下册)/viewthread.php?tid=237&fromuid=14755-1-1《财务管理学》章后练习参考答案(人大出版,第四版)/viewthread.php?tid=292&fromuid=14755-1-1现代汉语题库(语法部分)及答案/viewthread.php?tid=211&fromuid=14755-1-1《概率论与数理统计》习题详解(浙大二、三版通用)/viewthread.php?tid=80&fromuid=14755-1-1《有机化学》习题答案(汪小兰主编)/viewthread.php?tid=69&fromuid=14755-1-1《微机原理及应用》习题答案/viewthread.php?tid=261&fromuid=14755-1-1《管理运筹学》第二版习题答案(韩伯棠教授)/viewthread.php?tid=34&fromuid=14755-1-1《古代汉语》习题集(附习题答案)福建人民出版社/viewthread.php?tid=1277&fromuid=14755-1-1《金融市场学》课后习题答案(张亦春,郑振龙,第二版)/viewthread.php?tid=279&fromuid=14755-1-1《公共关系学》习题及参考答案(复习必备)/viewthread.php?tid=308&fromuid=14755-1-1现代汉语通论(邵敬敏版)词汇语法课后练习答案/viewthread.php?tid=1429&fromuid=14755-1-1《国际经济学》教师手册及课后习题答案(克鲁格曼,第六版)/viewthread.php?tid=281&fromuid=14755-1-1《教育技术》课后习题答案参考(北师大)/viewthread.php?tid=199&fromuid=14755-1-1《金融市场学》课后答案(郑振龙版)/viewthread.php?tid=24&fromuid=14755-1-1《组织行为学》习题集答案(参考下,还是蛮好的)/viewthread.php?tid=297&fromuid=14755-1-1《分析化学》课后习题答案(第五版,高教版)/viewthread.php?tid=122&fromuid=14755-1-1大学英语精读第3册答案(外教社)/viewthread.php?tid=9&fromuid=14755-1-1《国际经济学》习题答案(萨尔瓦多,英文版)/viewthread.php?tid=155&fromuid=14755-1-1《复变函数与积分变换》习题答案/viewthread.php?tid=70&fromuid=14755-1-1《信息论与编码》辅导PPT及部分习题答案(曹雪虹,张宗橙,北京邮电大学出版社)/viewthread.php?tid=136&fromuid=14755-1-1《宏观经济学》习题答案(第七版,多恩布什)/viewthread.php?tid=293&fromuid=14755-1-1《物理化学》习题解答(天津大学,第四版,106张)/viewthread.php?tid=2647&fromuid=14755-1-1新视野大学英语视听说教程第一册/viewthread.php?tid=5901&fromuid=14755-1-1《机械制造技术》习题集与答案解析/viewthread.php?tid=219&fromuid=14755-1-1新视野大学英语听说教程2册听力原文及答案下载/viewthread.php?tid=2532&fromuid=14755-1-1管理学试题(附答案)/viewthread.php?tid=1087&fromuid=14755-1-1《材料力学》详细辅导及课后答案(PDF格式,共642页)/viewthread.php?tid=31&fromuid=14755-1-1六级词汇注解/viewthread.php?tid=4893&fromuid=14755-1-1《大学基础物理学》课后答案(共16个单元)/viewthread.php?tid=25&fromuid=14755-1-1《管理学——原理与方法》课后习题答案/viewthread.php?tid=303&fromuid=14755-1-1新视野2版第三册(大2上学期用)/viewthread.php?tid=1438&fromuid=14755-1-1曼昆《经济学原理》中文第四版.课后习题答案-清晰图片版/viewthread.php?tid=1131&fromuid=14755-1-1《数据库系统概论》课后习题(第四版)/viewthread.php?tid=240&fromuid=14755-1-1大学数学基础教程课后答案(微积分)/viewthread.php?tid=8&fromuid=14755-1-1《投资学》课后习题答案(博迪,第四版)/viewthread.php?tid=284&fromuid=14755-1-1流体力学课后答案(高教版,张也影,第二版)/viewthread.php?tid=22&fromuid=14755-1-1《语言学概论》习题答案(自考,新版教材)/viewthread.php?tid=313&fromuid=14755-1-1《统计学》各章练习题答案/viewthread.php?tid=458&fromuid=14755-1-1《数字电子技术基础》课后习题答案(完整答案版)/viewthread.php?tid=197&fromuid=14755-1-1《积分变换》习题答案(配套东南大学张元林编的)/viewthread.php?tid=103&fromuid=14755-1-1《中级财务会计》习题答案(第二版,刘永泽)/viewthread.php?tid=163&fromuid=14755-1-1《计算机网络》课后习题答案(第5版和第4版)/viewthread.php?tid=132&fromuid=14755-1-1《单片机原理及应用》课后习题答案(张毅刚主编,高教版)/viewthread.php?tid=36&fromuid=14755-1-1《金融工程》课后题答案(郑振龙版)/viewthread.php?tid=288&fromuid=14755-1-1《液压传动》第2版思考题和习题解答(共36页)/viewthread.php?tid=20&fromuid=14755-1-1《动物学》习题集与答案(资料相当丰富)/viewthread.php?tid=315&fromuid=14755-1-1《高频电子线路》习题参考答案(第四版)/viewthread.php?tid=142&fromuid=14755-1-1《国际经济法》课后参考答案/viewthread.php?tid=306&fromuid=14755-1-1大学英语四级十年真题+听力/viewthread.php?tid=2454&fromuid=14755-1-1《信号与系统》习题详解(奥本海姆版)/viewthread.php?tid=79&fromuid=14755-1-1《电路分析》课后答案及学习指导(第二版,胡翔骏,高教版)/viewthread.php?tid=177&fromuid=14755-1-1《C语言设计》(谭浩强,第三版)227页/viewthread.php?tid=129&fromuid=14755-1-1新视野大学英语课后习题答案1-4册全集/viewthread.php?tid=7083&fromuid=14755-1-1《数字电路与逻辑设计》课后习题答案,讲解详细/viewthread.php?tid=233&fromuid=14755-1-1《电路》第五版课后答案/viewthread.php?tid=1678&fromuid=14755-1-1《材料力学》详细习题答案及辅导(第四版,刘鸿文)/viewthread.php?tid=88&fromuid=14755-1-1《传播学教程》课后答案(郭庆光主编,完整版)/viewthread.php?tid=252&fromuid=14755-1-1《物理化学》习题答案与课件集合(南大)/viewthread.php?tid=205&fromuid=14755-1-1《金融市场学》电子书(张亦春,郑振龙,第二版)/viewthread.php?tid=278&fromuid=14755-1-1毛邓三95%考点/viewthread.php?tid=6802&fromuid=14755-1-1高等教育出版社《毛·泽东思想和中国特色社会主·义道路》(09版,原毛邓三)课后题答案/viewthread.php?tid=6874&fromuid=14755-1-1《线性代数》课后习题答案(陈维新,科学出版社)/viewthread.php?tid=156&fromuid=14755-1-1自动控制原理习题集(自学辅导推荐)/viewthread.php?tid=53&fromuid=14755-1-1《现代通信原理》习题答案(曹志刚版)/viewthread.php?tid=44&fromuid=14755-1-1高等数学上下《习题PPT》/viewthread.php?tid=66&fromuid=14755-1-1《数据结构习题集》答案(C版,清·华大学,严蔚敏)/viewthread.php?tid=173&fromuid=14755-1-1《大学物理学》习题解答/viewthread.php?tid=114&fromuid=14755-1-1《物理化学》习题答案(南大,第五版)/viewthread.php?tid=143&fromuid=14755-1-1《机械原理》复习精要与习题精解(第7版,西北大学)/viewthread.php?tid=179&fromuid=14755-1-1《宏观经济学》答案(曼昆,第五版,英文版)pdf格式/viewthread.php?tid=134&fromuid=14755-1-1《化工热力学》习题与习题答案(含各种版本)/viewthread.php?tid=235&fromuid=14755-1-1《材料力学》习题答案教育统计与测量管理心理学(自考必备资料,牛逼打印版)/viewthread.php?tid=264&fromuid=14755-1-1离散数学习题解答(第四版)清·华大学出版社/viewthread.php?tid=46&fromuid=14755-1-1货币银行学/viewthread.php?tid=5074&fromuid=14755-1-1《技术经济学概论》(第二版)习题答案/viewthread.php?tid=109&fromuid=14755-1-1《毛·泽东思想和社会主·义建设理论题概论》精炼考试题目,耐心整理/viewthread.php?tid=6062&fromuid=14755-1-1《数字信号处理》课后答案及详细辅导(丁美玉,第二版)/viewthread.php?tid=58&fromuid=14755-1-1《语言学概论练习题》答案/viewthread.php?tid=312&fromuid=14755-1-1《会计电算化》教材习题答案(09年)/viewthread.php?tid=296&fromuid=14755-1-1《数据库系统概论》习题答案(第四版)/viewthread.php?tid=86&fromuid=14755-1-1《微观经济学》课后答案(平狄克版)/viewthread.php?tid=254&fromuid=14755-1-1《控制工程基础》课后习题解答(清·华版)/viewthread.php?tid=127&fromuid=14755-1-1《高分子化学》习题答案(第四版)/viewthread.php?tid=144&fromuid=14755-1-1《电机与拖动基础》课后习题答案(第四版,机械工业出版社,顾绳谷主编)/viewthread.php?tid=45&fromuid=14755-1-1《机械工程测试技术基础》(第三版,熊诗波等主编)课后答案/viewthread.php?tid=27&fromuid=14755-1-1《宏观经济学》课后答案(布兰查德版)/viewthread.php?tid=286&fromuid=14755-1-1《机械原理》习题答案和超多例题(西北工业大学,第六版)/viewthread.php?tid=239&fromuid=14755-1-1《大学物理基础教程》课后习题答案(第二版,等教育出版社)/viewthread.php?tid=172&fromuid=14755-1-1简明乐谱基础知识/viewthread.php?tid=762&fromuid=14755-1-1《语言学教程》课后答案/viewthread.php?tid=309&fromuid=14755-1-1《公司理财》课后答案(英文版,第六版)/viewthread.php?tid=282&fromuid=14755-1-1《信息论与编码》学习辅导及习题详解(傅祖芸版)/viewthread.php?tid=238&fromuid=14755-1-1《遗传学》课后习题答案(朱军主编,完整版)现代人心理实战700题处世韬略/viewthread.php?tid=770&fromuid=14755-1-1《自动控制原理》习题答案/viewthread.php?tid=117&fromuid=14755-1-1《普通动物学》完整课后答案(刘凌云,郑光美版)/viewthread.php?tid=316&fromuid=14755-1-1《微机原理》作业答案(李继灿版)/viewthread.php?tid=218&fromuid=14755-1-1尼尔·波兹曼《娱乐至死》/viewthread.php?tid=5129&fromuid=14755-1-1《电力电子技术》习题答案(第4版,西安交通大学)/viewthread.php?tid=130&fromuid=14755-1-1大学英语四级(CET-4)历年真题大全[89-07年39套](精品级)753页word /viewthread.php?tid=809&fromuid=14755-1-1《通信原理》习题答案/viewthread.php?tid=190&fromuid=14755-1-1《普通化学(第五版)》习题详解(配套浙大编的)/viewthread.php?tid=94&fromuid=14755-1-1经济法课后复习及思考答案/viewthread.php?tid=5406&fromuid=14755-1-1《结构化学基础》习题答案(周公度,北大版)/viewthread.php?tid=212&fromuid=14755-1-1财务管理学课后答案荆新王化成/viewthread.php?tid=5414&fromuid=14755-1-1《C++程序设计》课后习题答案(第2版,吴乃陵,高教版)/viewthread.php?tid=161&fromuid=14755-1-1药用植物的两份习题(自己感觉比较有用)/viewthread.php?tid=270&fromuid=14755-1-1《数学物理方法》习题解答案详细版(梁昆淼,第二版)/viewthread.php?tid=38&fromuid=14755-1-1《机械制图》习题册答案(近机类、非机类,清·华大学出版社)/viewthread.php?tid=158&fromuid=14755-1-1《控制工程基础》习题答案(第二版,燕山大学)/viewthread.php?tid=126&fromuid=14755-1-1《画法几何》资料包(含习题答案,自学辅导课件)/viewthread.php?tid=216&fromuid=14755-1-1《畜禽解剖学与组织胚胎学》习题答案参考/viewthread.php?tid=314&fromuid=14755-1-1《统计学》课后习题答案(周恒彤编)/viewthread.php?tid=3022&fromuid=14755-1-1《西方经济学简明教程》课后习题全解(尹伯成,上海人民出版社)/viewthread.php?tid=2569&fromuid=14755-1-1《汽车理论》课后答案详细解答(余志生,机械工业出版社)/viewthread.php?tid=123&fromuid=14755-1-1《数学物理方法》(第三版)习题答案/viewthread.php?tid=101&fromuid=14755-1-1新视野听力原文及课后答案/viewthread.php?tid=1401&fromuid=14755-1-1新编大学英语4(外研版)课后练习答案/viewthread.php?tid=61&fromuid=14755-1-1《材料力学》习题答案(单辉祖,北京航空航天大学)/viewthread.php?tid=187&fromuid=14755-1-1大学英语精读第3册课文及课后答案/viewthread.php?tid=1640&fromuid=14755-1-1《自动控制原理》课后习题答案———胡寿松,第五版/viewthread.php?tid=1740&fromuid=14755-1-1《数据库系统原理与设计》课后答案(第四版,王珊,萨师煊)/viewthread.php?tid=150&fromuid=14755-1-1《数字电子技术基础》详细习题答案(阎石第四版)/viewthread.php?tid=167&fromuid=14755-1-1财经应用文笔记/viewthread.php?tid=1088&fromuid=14755-1-1《管理学》课后习题答案(罗宾斯,人大版,第7版)/viewthread.php?tid=302&fromuid=14755-1-1《概率论与数理统计》习题答案(复旦大学出版社)/viewthread.php?tid=82&fromuid=14755-1-1《数字信号处理——基于计算机的方法》习题答案(第二版)/viewthread.php?tid=174&fromuid=14755-1-1《传热学》课后答案(杨世铭,陶文铨主编,高教版)/viewthread.php?tid=33&fromuid=14755-1-1C语言资料大全(有课后答案,自学资料,C程序等)/viewthread.php?tid=170&fromuid=14755-1-1毛邓三重点归纳/viewthread.php?tid=6816&fromuid=14755-1-1《电力拖动自动控制系统》习题答案/viewthread.php?tid=115&fromuid=14755-1-1逄锦聚《政治经济学》(第3版)笔记和课后习题详解/viewthread.php?tid=2185&fromuid=14755-1-1《概率论与数理统计》课后习题解答(东南大学出版社)/viewthread.php?tid=206&fromuid=14755-1-1《有机化学》课后习题答案(胡宏纹,第三版)/viewthread.php?tid=72&fromuid=14755-1-1《常微分方程》习题解答(王高雄版)/viewthread.php?tid=162&fromuid=14755-1-1▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆▆【因为太多了,没办法再粘贴到这里了,更多答案,直接进入下面这个搜索就好】/?fromuid=14755-1-1好东西,齐分享!!!——果皮。

大学生必备资料下载-百度文库

资料打开方法: 资料打开方法:按住 Ctrl 键,在你需要的资料上用鼠标左键单击

• • • • • • • • • • • • • • • • • • • • • • • • • • • • •

[Word 版答案]新视野大学英语听说教程 1 听力原文及答案下载 [PDF 版答案]《西方经济学》习题答案(第三版,高鸿业)可直接打印 [Word 版答案]《微观经济学》课后答案(高鸿业版) [PDF 版答案]谢希仁《计算机网络教程》(第五版)习题参考答案(共 48 页) [Word 版答案]《统计学》课后答案(第二版,贾俊平版) [Word 版答案]《大学物理》完整习题答案 [Word 版答案]《中国近代史纲要》完整课后答案(高教版) [Word 版答案]新视野大学英语第四册答案(第二版) [PDF 版答案]《线性代数》(同济第四版)课后习题答案(完整版) [Word 版答案]《管理学》经典笔记(周三多,第二版) [Word 版答案]新视野大学英语视听说第三册答案 [PDF 版答案]大学数学基础教程课后答案(微积分) [Word 版答案]新视野大学英语读写教程 3 册的课后习题答案 [Word 版答案]高等数学习题答案及提示 [PPT 版答案]《概率论与数理统计》习题答案 [Word 版答案]《电工学》课后习题答案(第六版,上册,秦曾煌主编) [Word 版答案]《中国近代史纲要》课后习题答案 [PDF 版答案]统计学原理作业及参考答案 [Word 版答案]机械设计基础(第五版)习题答案[杨可桢等主编] [PDF 版答案]程守洙、江之永主编《普通物理学》(第五版)详细解答及辅导 [Word 版答案]中国近现代史纲要课后题答案 [PDF 版答案]高等数学(同济第五版)课后答案(PDF 格式,共 527 页) [PDF 版答案]毛邓三全部课后思考题答案(高教版)/毛邓三课后答案 [PDF 版答案]《管理学》课后答案(周三多) [Word 版答案]《模拟电子技术基础》详细习题答案(童诗白,华成英版,高教版) [Word 版答案]《新编大学英语》课后答案(第三册) [Word 版答案]《成本会计》配套习题集参考答案 [Word 版答案]曼昆《经济学原理》课后习题解答 [Word 版答案]《全新版大学英语综合教程》(第四册)练习答案及课文译文

会计学英文版ppt课件

accounts within the chart of accounts are numbered for use

as references.

Balance Sheet Accounts

accounts.

Prepare an unadjusted trial

balance and explain how it can be used to discover errors.

Using Accounts to Record Transactions

As a result,accounting systems are designed to show the increases and decreases in each accounting equation element as a separate record.This record is

accounts.

Describe and illustrate

journalizing transaction using the double-entry

accounting system.

Describe and illustrate the journalizing and

posting of transactions to

Examples ——wages expense, rent expense, utilities expense, supplies expense, and miscellaneous expense.

A chart of accounts should meet the needs of a company’s

会计英语(第4版)教学大纲和期末复习题目

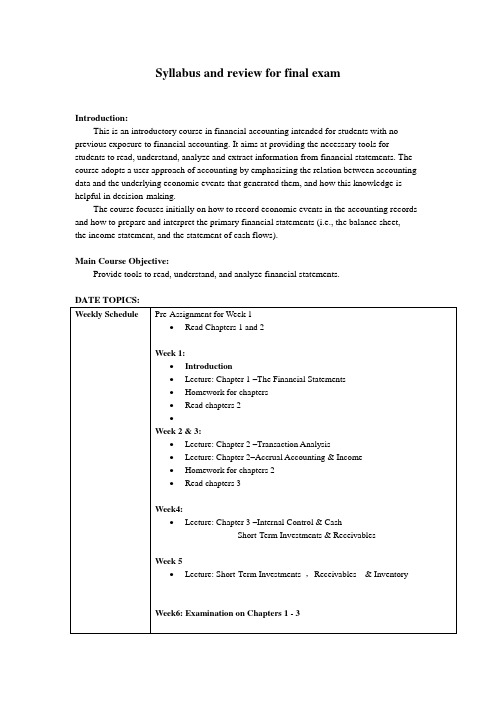

Syllabus and review for final examIntroduction:This is an introductory course in financial accounting intended for students with no previous exposure to financial accounting. It aims at providing the necessary tools for students to read, understand, analyze and extract information from financial statements. The course adopts a user approach of accounting by emphasizing the relation between accounting data and the underlying economic events that generated them, and how this knowledge is helpful in decision-making.The course focuses initially on how to record economic events in the accounting records and how to prepare and interpret the primary financial statements (i.e., the balance sheet,the income statement, and the statement of cash flows).Main Course Objective:Provide tools to read, understand, and analyze financial statements.Question 1 costing method for inventory Stylish Jeans Company markets blue jeans and uses a perpetual inventory system to account for its merchandise. The beginning balance of the inventory and transactions during the year were as follows:January 1: Balance: 350 units at €52 eachMarch 12: Purchased 175 units at €61 each.May 21: Sold 260 units for a selling price of €112 each.July 8: Purchased 300 units at €73.October 31: Sold 320 units for a selling price of €112 each.Required1. Calculate cost of goods available for sale and units available for sale for the year.2. Calculate units remaining in ending inventory.3. Calculate the currency value of cost of goods sold and ending inventory usinga) FIFOb) Weighted averageRound to two decimal places.1.Beg. 350 units @ €52= €18,200Mar. 12 175 units @ 61 = 10,675July 8 300 units @ 73 = 21,900UnitsAvailable 825 units €50,775Cost of goods available for sale2. Units in ending inventory:Units available 825Less: Units sold 580Ending Inventory 2453.(b) Weighted-average perpetualQuestion 2 accounting for bad debtsBeleVu Supplies showed the following selected adjusted balances at itsDecember 31, 2011 year end:During the year 2012, the following selected transactions occurred:1. Sales totalled €2,960,000, of which 25% were cash sales (cost of sales€1,804,000).2. Sales returns were €114,000, half regarding credit sales. The returnedmerchandise was scrapped.3. An account for €24,000 was recovered.4. Several accounts were written off; €39,000.5. Collections from credit customers totalled €1,880,000 (excluding the recovery in(3) above).Requireda. Prepare the December 31, 2012 adjusting entry to estimate bad debts, assuming that uncollectible accounts are estimated to be 1% of net credit sales.b. Show how accounts receivable will appear on the December 31, 2012 statement offinancial position.c. What will bad debts expense be on the statement of comprehensive income for theyear ended December 31, 2012?d. Prepare the December 31, 2012 adjusting entry to estimate bad debts, assumingthat uncollectible accounts are estimated to be 3% of outstanding receivables.e. Show how accounts receivable will appear on the December 31, 2012 statement offinancial position.f. What will bad debt expense be on the statement of comprehensive income for theyear ended December 31, 2012?a. Dec. 31 Bad Debt Expense 21,630 Allowance for Doubtful Accounts 21,630 2,220,000 – 57,000 = 2,163,000 2,163,000 × 1% = 21,630b. Current assets: Accounts receivable € 742,000 Less: Allowance for doubtful accounts (23,310) € 718,690 ORCurrent assets: Accounts receivable (net of €23,310 estimated uncollectible accounts) € 718,690c.d. Dec.31 Bad Debt Expense ................................................... 20,580 Allowance for Doubtful Accounts .................... 20,580 742,000 × 3% = 22,260 – 1,680 = 20,580Calculations:× 3%€22,260e.Current assets:Accounts receivable €742,000Less: Allowance for doubtful accounts (22,260) €719,740 ORCurrent assets:Accounts receivable (net of €22,260estimated uncollectible accounts) €719,740f. €20,580Question 3 accounting for trading investmentExtel Company’s fair value through profit or loss investments as of December 31, 2011 are as follows:Cost MarketKlondike ordinary shares €11,250 €14,875Kaffner ordinary shares 56,070 55,950IDEA ordinary shares 12,400 10,800Western ordinary shares 35,400 30,220RequiredPart 1Prepare the journal entries to record the adjustments to fair value for the fair value through profit or loss investments as per the requirements of IAS 39.Part 2Illustrate how the fair value through profit or loss investments will be reported on the statement of financial position on December 31, 2011.Illustrate what effect your adjustments would have on the Statement of Comprehensive Income for the year ended December 31, 2011.Part 1Cost Market Difference Klondike ordinary shares €11,250€14,875€3,625Kaffner ordinary shares 56,070 55,950 (120)IDEA ordinary shares 12,400 10,800 (1,600) Western ordinary shares 35,400 30,220 (5,180)2011Dec. 31 FVPL investments — Klondike shares 3,625Unrealized gain on FVPL investments 3,625€14,875 –€11,250 = €3,62531 Unrealized loss on FVPL investments (120)FVPL investments — Kaffner shares (120)€55,950 –€56,070 = (€120)31 Unrealized loss on FVPL investments ...................................... 1,600FVPL investments — IDEA shares .................................... 1,600 €10,800 –€12,400 = (€1,600)31 Unrealized loss on FVPL investments ...................................... 5,180FVPL investments — Western shares ................................ 5,180 €30,220 –€35,400 = (€5,180)Part 2Statement of Financial Position:Current assets:Fair value through profit or loss investments .................................... €111,845 Total fair or market values = €14,875 + €55,950 + €10,800 + €30,220Statement of Comprehensive Income:Other Income and Expenses:Unrealized loss on fair value through profit or loss investments....... €3,275Net unrealized loss = €3,625 –€120 –€1,600 –€5,180 = (€3,275)Question 4 accounting for fixed assetsShield Corporation purchased a used machine for €282,000 on January 7, 2007. It was repaired the next day at a cost of €12,500 and installed on a new platform that cost €2,000. The company predicted that the machine would be used for six years and would then have a €16,200 residual value. Depreciation was to be charged on a straight-line basis. A full year’s depreciation was charged on December 31, 2007. On June 25, 2012 it was retired.Required1. Prepare journal entries to record the purchase of the machine, the cost of repairingit, and the installation. Assume that cash was paid.2. Prepare entries to record depreciation on the machine on December 31 of its firstyear and on September 30 in the year of its disposal. (Round calculations to the nearest whole dollar.)3. Prepare entries to record the retirement of the machine under each of thefollowing unrelated assumptions:a) It was sold for €42,000;b) It was sold for €32,000; andc) It was stolen and the insurance company paid €37,500 in ful l settlement of theloss claim.4. Explain the purpose of recording depreciation. If depreciation is not recorded, whatis the effect on the statement of comprehensive income and statement of financial position?Part 12007Jan. 7 Machine ........................................................ 282,000Cash .................................................... 282,000 To record purchase of machine.8 Machine ........................................................ 12,500Cash .................................................... 12,500 To record capital repairs on machine.8 Machine ........................................................ 2,000Cash .................................................... 2,000 To record installation of machine.Part 2Dec. 31 Depreciation Expense, Machine .................. 46,717Accumulated Depreciation, Machine ........................................................46,717To record depreciation;(296,500 – 16,200)/6 = 46,717. 2012June. 25 Depreciation Expense, Machine .................. 23,359Accumulated Depreciation, Machine ........................................................23,359To record partial year’s depreciation; 46,717 × 6/12 = 23,359.Part 3(a)25 Accumulated Depreciation, Machine 1 ......... 256,944 Cash .............................................................. 42,000Gain on Disposal 2............................... 2,444 Machine .............................................. 296,500Sold machine for €42,000.Part 3(b)25 Accumulated Depreciation, Machine ........... 256,944 Cash .............................................................. 32,000 Loss on Disposal 3 ......................................... 7,556Machine .............................................. 296,500Sold machine for €32,000.Part 3(c)25 Accumulated Depreciation, Machine256,944 Cash37,500 Loss on Disposal4 2,056Machine296,500 Received insurance settlement.Dep. for 2007, 2008, 2009, 2010, and 2011.Dep. for 2012.1 Accumulated depreciation = (46,717 × 5 years) + 23,359 = 256,9442Gain (Loss) = Cash Proceeds – Book Value= 42,000 – (296,500 – 256,944) = 2,4443 Gain (Loss) = Cash Proceeds – Book Value= 32,000 – (296,500 – 256,944) = (7,556)4 Gain (Loss) = Cash Proceeds – Book Value= 3,7500 – (296,500 – 256,944) = (2,056)Part 4Depreciation is the process of allocating the cost of property, plant, and equipment in a rational and systematic manner over the assets’ useful life. It is required by the expense recognition principle. If depreciation is not recorded, net income will be overstated on the statement of comprehensive income. On the statement of financial position, assets and equity will be overstated.Question 5 accounting for bonds payableApplet Inc. issued bonds on January 1, 2011, that pay interest semi-annually on June30 and December 31. The par value of the bonds is €80,000, the annual contract rateis 8%, and the bonds mature in 10 years.RequiredFor each of these three situations, (a) determine the issue price of the bonds, and (b) show the journal entry that would record the issuance, assuming the market interestrate at the date of issuance was1. 6%2. 8%3. 10%Part 1a.Par value 0.5537 €80,000€44,296Interest (annuity) 14.8775 3,200 47,608Total €91,904Premium € 11,904* The table values are based on a discount rate of 3% (half the annual market rate)and 20 periods/payments.b.2011Jan. 1 Cash......................................................................... 91,904Premium on Bonds Payable .............................. 11,904Bonds Payable ................................................... 80,000 Sold bonds on original issue date.Part 2a.Par value 0.4564 €80,000 €36,512 Interest (annuity) 13.5903 3,200 43,488 Total €80,000* The table values are based on a discount rate of 4% (half the annual market rate)and 20 periods/payments.b.2011Jan. 1 Cash......................................................................... 80,000Bonds Payable ................................................... 80,000 Sold bonds on original issue date.Part 3a.Par value 0.3769 €80,000€30,152Interest (annuity) 12.4622 3,200 39,879Total €70,031Discount €9,969* The table values are based on a discount rate of 5% (half the annual market rate)and 20 periods/payments.b.2011Jan. 1 Cash ......................................................................... 70,031Discount on Bonds Payable .................................. 9,969Bonds Payable ................................................... 80,000 Sold bonds on original issue date.Entry for period 6 interestDR interest expense 3585CR cash 3200CR discount 385Question 6 accounting for shareholders equityMajestic Inc. was authorized to issue 250,000 €1.00 noncumulative preference shares and an unlimited number of ordinary shares. During Majestic’s first month of operations, May 2011, the following selected transactions occurred:May 1 10,000 preference shares were issued at €15.00 for cash.May 5 9,000 of the ordinary shares were issued for a total of €9,000 cash.May 6 14,000 ordinary shares were issued in exchange for land valued at €30,000.The shares were actively trading on this date at €2.00 per share.May 26 The corpora tion’s promoters were given 14,000 ordinary shares for their services in organizing the corporation. The directors valued the services at€70,000.May 31 The Board of Directors declared and paid a total dividend of €12,000.May 31 The €120,000 credit balan ce in the Income Summary account was closed. May 31 The cash dividends declared were closed to retained earnings.Required1.Prepare the journal entries to record the above transactions.2.Prepare the shareholders’ equity section of the company’s statemen t offinancial position as of May 31, 2011.Part 2Majestic Inc.Partial Statement of Financial PositionMay 31, 2011Shareholders’ EquityContributed capital:Preferred shares, €1.00, non-cumulativeAuthorized: 250,000Issued and outstanding: 10,000 € 150,000 Ordinary sharesAuthorized: unlimitedIssued and outstanding: 37,000 107,000 Total contributed capital ............................ €257,000 Retained earnings ............................................... 108,000 Total shareholders’ equity .......................................... €365,000Question 7 the statement of cash flowHolliday Corp.’s statement of financial position and statement ofcomprehensive income are as follows:HOLLIDAY CORP.Comparative Statement of Financial Position InformationDecember 31Assets 2012 2011Cash ............................................................................ €150,850 €214,550 Accounts receivable ..................................................... 182,000 138,950 Merchandise inventory ................................................. 766,500 707,000 Prepaid expenses ........................................................ 15,050 17,500 Equipment .................................................................. 446,600 308,000 Accumulated depreciation ........................................ (96,950) (123,200) Total assets ................................................................. €1,464,050 €1,262,800Liabilities and Shareholder s’ EquityAccounts payable ......................................................... €246,750 €326,550 Short-term notes payable ............................................. 28,000 17,500 Long-term notes payable ............................................. 262,500 150,500 Ordinary shares ........................................................... 563,500 437,500 Retained earnings ........................................................ 363,300 330,750 Total liabilities and shareholders’ equity ...................... €1,464,050 €1,262,800HOLLIDAY CORP.Statement of Comprehensive Incomefor year ended December 31, 2012Sales ............................................................................ €1,389,500 Cost of goods sold ....................................................... 700,000 Gross profit .................................................................. €689,500 Operating expenses:Depreciation expense ............................................. €52,500Other expenses ...................................................... 382,200Total operating expenses ....................................... 434,700 Income from operations ............................................... €254,800 Loss on sale of equipment ........................................... 14,350 Income taxes ............................................................... 33,950Net income ................................................................... €206,500 Other information regarding Holliday Corp.:a. All sales are credit sales.b. All credits to accounts receivable in the period are receipts from customers.c. Purchases of merchandise are on credit.d. All debits to accounts payable in the period result from payments formerchandise.e. The other operating expenses are cash expenses.f. The only decrease in income taxes payable is for payment of taxes.g. The other expenses are paid in advance and are initially debited to Prepaidexpenses.Additional information regarding Holliday Corp.’s activities during 2012:h. Loss on sale of equipment is €14,350.i. Equipment costing €131,250,with accumulated depreciation of €78,750, issold for cash.j. Equipment costing €269,850is purchased by paying cash of €70,000 and signing a long-term note payable for the balance.k. Borrowed €10,500 by signing a short-term note payable.l. Paid €87,850 to reduce a long-term note payable.m. Issued 7,000 ordinary shares for cash at €18 per share.n. Declared and paid cash dividends of €173,950.HOLLIDAY CORP.Statement of Cash FlowsNote A:The company purchased equipment for €269,850 by signing a €199,850 long-term note payable and paying €70,000 in cash.Note 2 retained earnings330,750+ profit 206,500 - 173,950(n) = 363,300Name______________ Student Number___________________HOLLIDAY CORP.Statement of Cash Flows。

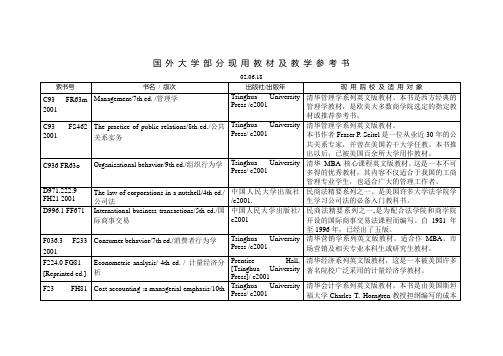

国外大学教材

国外大学生物学优秀教材。

本书几乎吸收了1999年以前国际上主要生态学杂志中发表的所有著名文献。是一本适合基础生态学教学的优秀教材,可作为大专院校本科生、研究生教材。

Q949.325.03 FB95

Methods in yeast genetics :a Cold Spring Harbor Laboratory course manual/2000 ed./酵母遗传实验方法:冷泉港实验课手册

清华MBA核心课程英文版教材。这是一本非常有特色的、跨学科的管理经济学教材。

F270.7 FD24 2001

Strategic management :concepts & cases/8th ed./战略管理:概念与案例

Tsinghua University Press /c2001.

清华MBA核心课程英文版教材。

F240 FD47 2001

Human resource management/8th ed./人力资源管理

Tsinghua University PreБайду номын сангаасs /c2001

清华管理学系列英文版教材。本书是一本优秀的人力资源管理教材,可供管理类专业本科生和研究生使用。

F27 FS28 2001

Effective small business management :an entrepreneurial approach/6th ed./有效的小企业管理:创业方法

F837.123 FS25

Financial institutions management :a modern perspective/3rd ed./金融机构管理:现代方法

西方财务会计培训教程(英文版)(ppt 68页)PPT学习课件

LO 1 Discuss the characteristics of the corporate form of organization.

The Corporate Form of Organization

Variety of Ownership Interests

LO 1 Discuss the characteristics of the corporate form of organization.

The Corporate Form of Organization

Capital Stock or Share System

In the absence of restrictive provisions, each share carries the following rights:

Corporate Capital

No-Par Stock

Reasons for issuance: Avoids contingent liability. Avoids confusion over recording par value versus fair market value.

Some states require that no-par stock have a stated value.

Preferred Stock or Common Stock. Additional Paid-in Capital

LO 3 Explain the accounting procedures for issuing shares of stock.

Corporate Capital

《会计英语—财务会计(双语版·第四版)》教师教学课件全编

c. Competence, judgment, and ethical behavior of individual accountants. d. All of the above.

Reading Comprehension (GAAP)

1.Assumption Accounting entity

Separate entity

会计主体 独立实体

Going concern

持续经营

Continue operation (or continuing concern)

Measuring unit Monetary unit Stable-money-unit

2.Divide into groups as instructed by your professor and discuss the following:

a. How does the description of accounting as the“language of business” relate to accounting as being useful for investors and creditors?

Words and Phrases

intuition rest on/upon =set up on account=on credit utility utility expense materiality encompass constraint hierarchy

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

25

Understand presentation requirements for Statement of Changes in Equity

Copyright ©2014 Pearson Education.

26

Key reconciling items

Copyright ©2014 Pearson Education.

• All financial statements, except cash flow info, to be prepared using accrual basis.

Copyright ©2014 Pearson Education.

13

Materiality and Aggregation

Copyright ©2014 Pearson Education.

14

Offsetting

• Not allowed to offset assets and liabilities, income and expenses

• Offsetting is different from netting

tool

• Top source of information for shareholders, lenders, potential investors etc.

• Provide information about the company from company visions, goals to financial information and changes in strategy.

Copyright ©2014 Pearson Education.

8

Know the general features of financial statements

Copyright ©2014 Pearson Education.

11

Complete set of financial statements

• Acknowledgement of responsibility for preparing financial statements by management

• Auditor’s report • 3 types of opinions:

Unqualified Qualified Adverse

• Cannot rectify inappropriate policies

▫ By notes or explanatory material

Байду номын сангаас

Copyright ©2014 Pearson Education.

12

Accrual basis and going concern

• Going concern: Entity intends to, and has ability to, operate into the foreseeable future.

Copyright ©2014 Pearson Education.

18

Statement of Financial Position

Copyright ©2014 Pearson Education.

19

Statement of Financial Position

• Liquidity • Current assets and current liabilities

Copyright ©2014 Pearson Education.

23

Categorizing expenses by nature

Copyright ©2014 Pearson Education.

24

Categorizing expenses by function

Copyright ©2014 Pearson Education.

Copyright ©2014 Pearson Education.

15

Frequency of reporting

• Entities are to present financial info at least annually

• Listed companies might have to publish interim reports

Copyright ©2014 Pearson Education.

28

Notes to the accounts

Copyright ©2014 Pearson Education.

29

Copyright ©2014 Pearson Education.

30

management personnel • Organization structure • Awards and accolades • Key markets and products • Operating Statistics and financial highlights

Copyright ©2014 Pearson Education.

Copyright ©2014 Pearson Education.

20

Statement of financial postion

• Account format

Assets

• Report format

Assets Liabilities Equities

Liabilities Equities

Copyright ©2014 Pearson Education.

16

Comparative information and

Consistency of presentation

• Numbers from previous periods must be disclosed

Minimum 2 years of information Under certain situations, 3 ears Comparatives made in narrative and descriptive

27

Accounting changes

• Dealt with in IAS 8 • Changes due to new accounting standards or

pronouncements • Changes in accounting estimates • Changes in accounting policies • Prior-period errors

Fair presentation and compliance with IFRS

• Faithful representation of effects of transactions

▫ Cannot selectively apply standards and proclaim compliance with IFRS

Appreciate the role of annual reports as a communication tool

Copyright ©2014 Pearson Education.

1

Chapter 4

Presentation of Financial Statements

Annual reports as a communication

Name of reporting entity

If consolidated or individual entity’s account

Date of the end of reporting period

Presentation currency used

Level of rounding

Copyright ©2014 Pearson Education.

Statement of financial

position

Statement of comprehensive

income

Statement of changes in

equity

Statement of cash flows

Notes

Proper labeling of financial statements

• Substance over form

Copyright ©2014 Pearson Education.

3

Typical structure of an annual report

Corporate

Analysis and

information commentaries

Other statements or

5

Analysis and commentaries

Copyright ©2014 Pearson Education.

6

Other statements and disclosure

Copyright ©2014 Pearson Education.

7

Financial Statements

• Accounts can be aggregated if they are immaterial • An item is material when its omission or

misstatement can influence the economic decisions of users based on financial statements.

information

• Firms are expected to maintain presentation and classification of items period to period