财务管理-AnalysisandValuation(财务报表分析,台湾中

财务管理英语知识

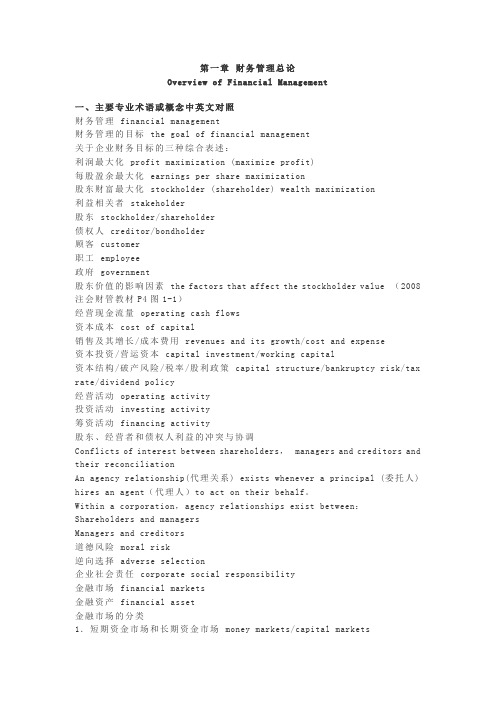

第一章财务管理总论Overview of Financial Man agement一、主要专业术语或概念中英文对照财务管理financial management财务管理的目标the goal of financial management关于企业财务目标的三种综合表述:利润最大化profit maximization (maximize profit)每股盈余最大化earnings per share maximization股东财富最大化stockholder (shareholder) wealth maximization利益相关者stakeholder股东stockholder/shareholder债权人creditor/bondholder顾客customer职工employee政府government股东价值的影响因素the factors that affect the stockholder value (2008注会财管教材P4图1-1)经营现金流量operating cash flows资本成本cost of capital销售及其增长/成本费用revenues and its growth/cost and expense资本投资/营运资本capital investment/working capital资本结构/破产风险/税率/股利政策capital structure/bankruptcy risk/tax rate/dividend policy经营活动operating activity投资活动investing activity筹资活动financing activity股东、经营者和债权人利益的冲突与协调Conflicts of interest between shareholders,managers and creditors and their reconciliationAn agency relationship(代理关系) exists whenever a principal (委托人) hires an agent(代理人)to act on their behalf。

关于财务管理的英文单词

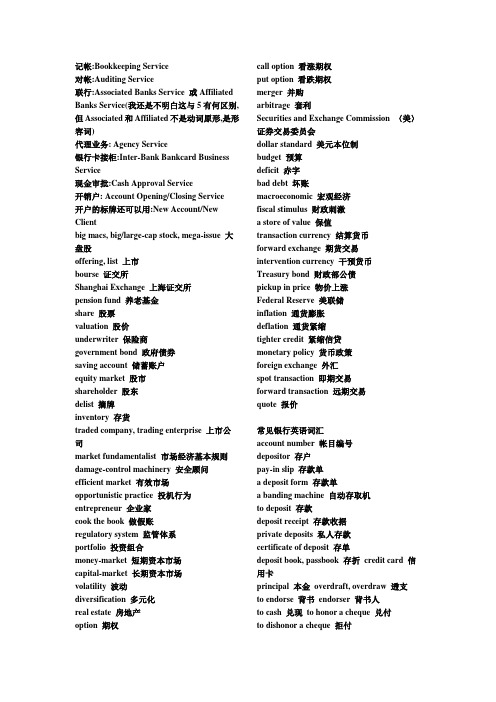

记帐:Bookkeeping Service对帐:Auditing Service联行:Associated Banks Service 或Affiliated Banks Service(我还是不明白这与5有何区别,但Associated和Affiliated不是动词原形,是形容词)代理业务: Agency Service银行卡接柜:Inter-Bank Bankcard Business Service现金审批:Cash Approval Service开销户: Account Opening/Closing Service开户的标牌还可以用:New Account/New Clientbig macs, big/large-cap stock, mega-issue 大盘股offering, list 上市bourse 证交所Shanghai Exchange 上海证交所pension fund 养老基金share 股票valuation 股价underwriter 保险商government bond 政府债券saving account 储蓄账户equity market 股市shareholder 股东delist 摘牌inventory 存货traded company, trading enterprise 上市公司market fundamentalist 市场经济基本规则damage-control machinery 安全顾问efficient market 有效市场opportunistic practice 投机行为entrepreneur 企业家cook the book 做假账regulatory system 监管体系portfolio 投资组合money-market 短期资本市场capital-market 长期资本市场volatility 波动diversification 多元化real estate 房地产option 期权call option 看涨期权put option 看跌期权merger 并购arbitrage 套利Securities and Exchange Commission 〈美〉证券交易委员会dollar standard 美元本位制budget 预算deficit 赤字bad debt 坏账macroeconomic 宏观经济fiscal stimulus 财政刺激a store of value 保值transaction currency 结算货币forward exchange 期货交易intervention currency 干预货币Treasury bond 财政部公债pickup in price 物价上涨Federal Reserve 美联储inflation 通货膨胀deflation 通货紧缩tighter credit 紧缩信贷monetary policy 货币政策foreign exchange 外汇spot transaction 即期交易forward transaction 远期交易quote 报价常见银行英语词汇account number 帐目编号depositor 存户pay-in slip 存款单a deposit form 存款单a banding machine 自动存取机to deposit 存款deposit receipt 存款收据private deposits 私人存款certificate of deposit 存单deposit book, passbook 存折credit card 信用卡principal 本金overdraft, overdraw 透支to endorse 背书endorser 背书人to cash 兑现to honor a cheque 兑付to dishonor a cheque 拒付to suspend payment 止付cheque,check 支票cheque book 支票本crossed cheque 横线支票blank cheque 空白支票rubber cheque 空头支票cheque stub, counterfoil 票根cash cheque 现金支票traveler's cheque 旅行支票cheque for transfer 转帐支票outstanding cheque 未付支票canceled cheque 已付支票forged cheque 伪支票Bandar's note 庄票,银票banker 银行家president 行长savings bank 储蓄银行Chase Bank 大通银行National City Bank of New York 花旗银行Hongkong Shanghai Banking Corporation 汇丰银行Chartered Bank of India, Australia and China 麦加利银行Banque de I'IndoChine 东方汇理银行central bank, national bank, banker's bank 中央银行bank of issue, bank of circulation 发行币银行commercial bank 商业银行,储蓄信贷银行member bank, credit bank 储蓄信贷银行discount bank 贴现银行exchange bank 汇兑银行requesting bank 委托开证银行issuing bank, opening bank 开证银行advising bank, notifying bank 通知银行negotiation bank 议付银行confirming bank 保兑银行paying bank 付款银行associate banker of collection 代收银行consigned banker of collection 委托银行clearing bank 清算银行local bank 本地银行domestic bank 国内银行overseas bank 国外银行unincorporated bank 钱庄branch bank 银行分行trustee savings bank 信托储蓄银行trust company 信托公司financial trust 金融信托公司unit trust 信托投资公司trust institution 银行的信托部credit department 银行的信用部commercial credit company(discount company) 商业信贷公司(贴现公司)neighborhood savings bank, bank of deposit 街道储蓄所credit union 合作银行credit bureau 商业兴信所self-service bank 无人银行land bank 土地银行construction bank 建设银行industrial and commercial bank 工商银行bank of communications 交通银行mutual savings bank 互助储蓄银行post office savings bank 邮局储蓄银行mortgage bank, building society 抵押银行industrial bank 实业银行home loan bank 家宅贷款银行reserve bank 准备银行chartered bank 特许银行corresponding bank 往来银行merchant bank, accepting bank 承兑银行investment bank 投资银行import and export bank (EXIMBANK) 进出口银行joint venture bank 合资银行money shop, native bank 钱庄credit cooperatives 信用社clearing house 票据交换所public accounting 公共会计business accounting 商业会计cost accounting 成本会计depreciation accounting 折旧会计computerized accounting 电脑化会计general ledger 总帐subsidiary ledger 分户帐cash book 现金出纳帐cash account 现金帐journal, day-book 日记帐,流水帐bad debts 坏帐investment 投资surplus 结余idle capital 游资economic cycle 经济周期economic boom 经济繁荣economic recession 经济衰退economic depression 经济萧条economic crisis 经济危机economic recovery 经济复苏inflation 通货膨胀deflation 通货收缩devaluation 货币贬值revaluation 货币增值international balance of payment 国际收支favourable balance 顺差adverse balance 逆差hard currency 硬通货soft currency 软通货international monetary system 国际货币制度the purchasing power of money 货币购买力money in circulation 货币流通量note issue 纸币发行量national budget 国家预算national gross product 国民生产总值public bond 公债stock, share 股票debenture 债券treasury bill 国库券debt chain 债务链direct exchange 直接(对角)套汇indirect exchange 间接(三角)套汇cross rate, arbitrage rate 套汇汇率foreign currency (exchange) reserve 外汇储备foreign exchange fluctuation 外汇波动foreign exchange crisis 外汇危机discount 贴现discount rate, bank rate 贴现率gold reserve 黄金储备money (financial) market 金融市场stock exchange 股票交易所broker 经纪人commission 佣金bookkeeping 簿记bookkeeper 簿记员an application form 申请单bank statement 对帐单letter of credit 信用证strong room, vault 保险库equitable tax system 等价税则specimen signature 签字式样banking hours, business hours 营业时间(Consumer Price Index) 消费者物价指数business 企业商业业务financial risk 财务风险sole proprietorship 私人业主制企业partnership 合伙制企业limited partner 有限责任合伙人general partner 一般合伙人separation of ownership and control 所有权与经营权分离claim 要求主张要求权management buyout 管理层收购tender offer 要约收购financial standards 财务准则initial public offering 首次公开发行股票private corporation 私募公司未上市公司closely held corporation 控股公司board of directors 董事会executove director 执行董事non- executove director 非执行董事chairperson 主席controller 主计长treasurer 司库revenue 收入profit 利润earnings per share 每股盈余return 回报market share 市场份额social good 社会福利financial distress 财务困境stakeholder theory 利益相关者理论value (wealth) maximization 价值(财富)最大化common stockholder 普通股股东preferred stockholder 优先股股东debt holder 债权人well-being 福利diversity 多样化going concern 持续的agency problem 代理问题free-riding problem 搭便车问题information asymmetry 信息不对称retail investor 散户投资者institutional investor 机构投资者agency relationship 代理关系net present value 净现值creative accounting 创造性会计stock option 股票期权agency cost 代理成本bonding cost 契约成本monitoring costs 监督成本takeover 接管corporate annual reports 公司年报balance sheet 资产负债表income statement 利润表statement of cash flows 现金流量表statement of retained earnings 留存收益表fair market value 公允市场价值marketable securities 油价证券check 支票money order 拨款但、汇款单withdrawal 提款accounts receivable 应收账款credit sale 赊销inventory 存货property,plant,and equipment 土地、厂房与设备depreciation 折旧accumulated depreciation 累计折旧liability 负债current liability 流动负债long-term liability 长期负债accounts payout 应付账款note payout 应付票据accrued espense 应计费用deferred tax 递延税款preferred stock 优先股common stock 普通股book value 账面价值capital surplus 资本盈余accumulated retained earnings 累计留存收益hybrid 混合金融工具treasury stock 库藏股historic cost 历史成本current market value 现行市场价值real estate 房地产outstanding 发行在外的a profit and loss statement 损益表net income 净利润operating income 经营收益earnings per share 每股收益simple capital structure 简单资本结构dilutive 冲减每股收益的basic earnings per share 基本每股收益complex capital structures 复杂的每股收益diluted earnings per share 稀释的每股收益convertible securities 可转换证券warrant 认股权证accrual accounting 应计制会计amortization 摊销accelerated methods 加速折旧法straight-line depreciation 直线折旧法statement of changes in shareholders’equity 股东权益变动表source of cash 现金来源use of cash 现金运用operating cash flows 经营现金流cash flow from operations 经营活动现金流direct method 直接法indirect method 间接法bottom-up approach 倒推法investing cash flows 投资现金流cash flow from investing 投资活动现金流joint venture 合资企业affiliate 分支机构financing cash flows 筹资现金流cash flows from financing 筹资活动现金流time value of money 货币时间价值simple interest 单利debt instrument 债务工具annuity 年金future value 终至present value 现值compound interest 复利compounding 复利计算pricipal 本金mortgage 抵押credit card 信用卡terminal value 终值discounting 折现计算discount rate 折现率opportunity cost 机会成本required rate of return 要求的报酬率cost of capital 资本成本ordinary annuity普通年金annuity due 先付年金financial ratio 财务比率deferred annuity 递延年金restrictive covenants 限制性条款perpetuity 永续年金bond indenture 债券契约face value 面值financial analyst 财务分析师coupon rate 息票利率liquidity ratio 流动性比率nominal interest rate 名义利率current ratio 流动比率effective interest rate 有效利率window dressing 账面粉饰going-concern value 持续经营价值marketable securities 短期证券liquidation value 清算价值quick ratio 速动比率book value 账面价值cash ratio 现金比率marker value 市场价值debt management ratios 债务管理比率intrinsic value 内在价值debt ratio 债务比率mispricing 给……错定价格debt-to-equity ratio 债务与权益比率valuation approach 估价方法equity multiplier 权益乘discounted cash flow valuation 折现现金流量模型long-term ratio 长期比率undervaluation 低估debt-to-total-capital 债务与全部资本比率overvaluation 高估leverage ratios 杠杆比率option-pricing model 期权定价模型interest coverage ratio 利息保障比率contingent claim valuation 或有要求权估价earnings before interest and taxes 息税前利润promissory note 本票cash flow coverage ratio 现金流量保障比率contractual provision 契约条款asset management ratios 资产管理比率par value 票面价值accounts receivable turnover ratio 应收账款周转率maturity value 到期价值inventory turnover ratio 存货周转率coupon 息票利息inventory processing period 存货周转期coupon payment 息票利息支付accounts payable turnover ratio 应付账款周转率coupon interest rate 息票利率cash conversion cycle 现金周转期maturity 到期日asset turnover ratio 资产周转率term to maturity 到期时间profitability ratio 盈利比率call provision赎回条款gross profit margin 毛利润call price 赎回价格operating profit margin 经营利润sinking fund provision 偿债基金条款net profit margin 净利润conversion right 转换权return on asset 资产收益率put provision 卖出条款return on total equity ratio 全部权益报酬率indenture 债务契约return on common equity 普通权益报酬率covenant 条款market-to-book value ratio 市场价值与账面价值比率trustee 托管人market value ratios 市场价值比率protective covenant 保护性条款dividend yield 股利收益率negative covenant 消极条款dividend payout 股利支付率positive covenant 积极条款financial statement财务报表secured deht担保借款profitability 盈利能力unsecured deht信用借款viability 生存能力creditworthiness 信誉solvency 偿付能力collateral 抵押品collateral trust bonds 抵押信托契约debenture 信用债券bond rating 债券评级current yield 现行收益yield to maturity 到期收益率default risk 违约风险interest rate risk 利息率风险authorized shares 授权股outstanding shares 发行股treasury share 库藏股repurchase 回购right to proxy 代理权right to vote 投票权independent auditor 独立审计师straight or majority voting 多数投票制cumulative voting 积累投票制liquidation 清算right to transfer ownership 所有权转移权preemptive right 优先认股权dividend discount model 股利折现模型capital asset pricing model 资本资产定价模型constant growth model 固定增长率模型growth perpetuity 增长年金mortgage bonds 抵押债券。

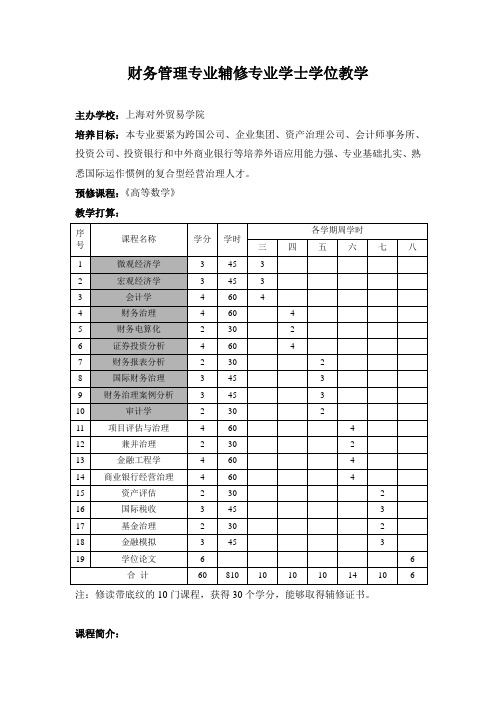

财务管理专业辅修专业学士学位教学

财务管理专业辅修专业学士学位教学主办学校:上海对外贸易学院培养目标:本专业要紧为跨国公司、企业集团、资产治理公司、会计师事务所、投资公司、投资银行和中外商业银行等培养外语应用能力强、专业基础扎实、熟悉国际运作惯例的复合型经营治理人才。

预修课程:《高等数学》教学打算:注:修读带底纹的10门课程,获得30个学分,能够取得辅修证书。

课程简介:课程名称:微观经济学课程简介:本课程介绍西方经济学的差不多概念、差不多理论和差不多方法。

微观经济学以单个经济行为者的经济行为为研究对象,分析在市场机制作用下的资源配置作用。

要紧内容:均衡价格决定理论、消费者行为理论、生产理论、厂商均衡理论、生产要素价格决定和收入分配理论、微观经济决策等。

课程名称:宏观经济学课程简介:本课程介绍西方经济学的差不多概念、差不多理论和差不多方法。

宏观经济学是以整个国民经济为研究对象,分析资源利用问题。

要紧内容有:国际收入核算理论,简单国民收入决定理论,产业市场和货币市场的均衡,总需求和总供给模型,通货膨胀理论,经济周期与经济增长理论,宏观经济政策,开放条件下的宏观经济模型。

课程名称:会计学课程简介:本课程要紧讲述会计总论,包括会计差不多前提和一样原则、会计要素与会计科目、复式记账与账户、会计凭证与账簿、会计核算程序等;会计要素专论,包括资产、负债、资本、收入与费用、利润等运算与分配;会计报表,包括会计报表的意义和种类、会计报表的编制与分析等。

课程名称:财务治理课程简介;财务治理的环境,汇率的确定及均衡关系;汇率的推测;外汇风险的测定;外汇风险的治理;跨国公司短期资金筹集分析;国际现金治理;应收账款和库存治理;跨国财务系统治理;国际税收治理;跨国公司投资策略分析;跨国资本规划;政治风险治理;对外投资成本;跨国融资策略;融资场所。

课程名称:财务电算化课程简介:随着财务软件的普及,财务类人员能否熟练把握其使用变得越来越重要。

这门课程以教师教授与学生上机实践相结合,要紧介绍了财务软件中账务处理模块、报表生成模块、应收账款治理模块、应对账款治理模块、存货治理模块、财务分析模块、资金治理模块等的使用。

财务报表分析-英文

Introduction and Basic Concepts

Business Partnership Vision Strategy Budget Forecast

Others Treasury M&A Risk Management Insurance Auditing Compliance Hedging ….

Introduction and Basic Concepts

Minimize Working Capital Maintain Strong Cash Flow

Pay Debts As They Are Due Increase Liquidity

Maintain Strong Financial Position

Introduction and Basic Concepts

导言及基本概念 Introduction and Basic Concepts Introduction Finance Organization Finance Activity Other topics

This training will allow you to understand: Finance Function Concept of Financial KPIs (Revenue, DM, DL, VOH, FOH, SG&A, OI, OCF, EBITDA, DOH, DSO, DPO, Incremental, etc.) BS, P&L and Cash Flow Statements Concepts of Financial Statement Evaluation and Investment Appraisal

财务报表分析中英文对照外文翻译文献编辑

财务报表分析中英文对照外文翻译文献编辑Introduction:Financial statement analysis is an essential tool used by businesses and investors to evaluate the financial performance and position of a company. It involves the examination of financial statements such as the balance sheet, income statement, and cash flow statement to assess the company's profitability, liquidity, solvency, and efficiency. In this document, we will provide a detailed analysis and translation of foreign literature related to financial statement analysis.1. Importance of Financial Statement Analysis:Financial statement analysis provides valuable insights into a company's financial health and helps stakeholders make informed decisions. It enables investors to assess the profitability and growth potential of a company before making investment decisions. Additionally, it helps creditors evaluate the creditworthiness and repayment capacity of a company before extending credit. Furthermore, financial statement analysis assists management in identifying areas of improvement and making strategic decisions to enhance the company's performance.2. Key Elements of Financial Statement Analysis:a) Balance Sheet Analysis:The balance sheet provides a snapshot of a company's financial position at a specific point in time. It presents the company's assets, liabilities, and shareholders' equity. By analyzing the balance sheet, stakeholders can assess the company's liquidity, solvency, and financial stability.b) Income Statement Analysis:The income statement, also known as the profit and loss statement, presents the company's revenues, expenses, and net income over a specific period. It helps stakeholders evaluate the company's profitability, revenue growth, and cost management.c) Cash Flow Statement Analysis:The cash flow statement details the inflows and outflows of cash during a specific period. It provides insights into the company's operating, investing, and financing activities. By analyzing the cash flow statement, stakeholders can assess the company's ability to generate cash, meet its financial obligations, and fund its growth.3. Financial Ratios for Analysis:Financial ratios are essential tools used in financial statement analysis to assess a company's performance and compare it with industry benchmarks. Some commonly used financial ratios include:a) Liquidity Ratios:- Current Ratio: Measures a company's ability to meet short-term obligations.- Quick Ratio: Measures a company's ability to meet short-term obligations without relying on inventory.b) Solvency Ratios:- Debt-to-Equity Ratio: Measures the proportion of debt to equity in a company's capital structure.- Interest Coverage Ratio: Measures a company's ability to meet interest payments on its debt.c) Profitability Ratios:- Gross Profit Margin: Measures the profitability of a company's core operations.- Net Profit Margin: Measures the profitability of a company after all expenses, including taxes.d) Efficiency Ratios:- Inventory Turnover Ratio: Measures how quickly a company sells its inventory.- Accounts Receivable Turnover Ratio: Measures how quickly a company collects cash from its customers.4. Translation of Foreign Literature:In this section, we will provide a translation of key points from foreign literature related to financial statement analysis. The literature emphasizes the importance of accurate financial reporting, the use of financial ratios for analysis, and the interpretation of financial statements to make informed decisions.Conclusion:Financial statement analysis is a crucial process for evaluating a company's financial performance and position. It provides valuable insights into a company's profitability, liquidity, solvency, and efficiency. By analyzing financial statements and using financial ratios, stakeholders can make informed decisions regarding investments, credit extension, and strategic planning. Accurate translation and understanding of foreign literature related to financial statement analysis can further enhance the effectiveness of this process.。

财务管理财务分析中英文对照外文翻译文献

独资企业的资产也可以卖给其他公司,只要它还存在。经营者的寿命终止,那么独资企业的寿命终止,虽然资产经营可以通过经营者的继承人。

合伙企业

合伙企业是在两个或更多的人签订协议来经营业务,合伙是相似于个人独资企业,除了所有者替代经营者,这里是不止一个。事实上,有超过一个经营者,介绍了一些问题:谁说在日常经营业务吗?谁是承担经济责任(也就是说最终的责任,)为企业债务?如何分配企业收入? 如何产生纳税收入? 这些问题和合伙协议一起被解决,有些是通过法律进行解决。合伙协议描述损益在合伙人中如何都是分担,它详细企业管理责任。

图例。数学概念利用表格和插图在视觉上被仔细谨慎动态的描述。例如我们指出银行的资产负债增长率通过复利的方式,在数学上表示为次数和柱状图。

实用性。尽可能的,我们要通过实务例子提出的概念和数学公式。例如,我们首先提出财务分析要通过假设一个公司的简化财务报表。最后,你会学到基础的使用假设的公司数据,我们通过沃尔玛超市的数据来证明分析工具,真实的案例帮助我们更好的理解和记住主要的概念和工具。我们对本书中100个真实的公司的案例求积,你不会希望错过它们。考虑到本书案例和研究问题和难题,你将看到无数的真实公司数据。

通过对本书的学习,你将了解我们是如何理解财务的。我们所说的财务决策作为公司所做决策的一部分,不是一个被分离出来的功能。财务决策的做出协调了企业会计部、市场部和生产部。

无论企业的形式和规模如何,财务原理和财务工具均适用。就像对小规模的私营企业而言存在如何筹资的问题,大企业面临所有权和经营权分离时出现的代理问题。不管公司的规模和形式是如何的,公司财务管理的基本原理是一样的。例如,无论是独资企业做出的决策还是大企业做出的决策,今天一美元的价值都高于未来一美元的价值。

mba财务管理参考题目方向

mba财务管理参考题目方向英文回答:1. Financial Statement Analysis.Vertical and horizontal analysis.Common-size financial statements.Trend analysis.DuPont analysis.Ratio analysis.2. Working Capital Management.Cash conversion cycle.Inventory management.Accounts receivable management. Accounts payable management.3. Capital Budgeting.Net present value (NPV)。

Internal rate of return (IRR)。

Payback period.Profitability index.4. Risk Management.Financial risk.Operational risk.Market risk.5. Investment Analysis.Bond valuation.Stock valuation.Portfolio management.6. Financial Planning and Forecasting. Financial planning process.Forecasting techniques.Sensitivity analysis.7. Management Accounting.Cost accounting.Budgeting.Performance measurement.Transfer pricing.8. Corporate Finance.Capital structure.Dividend policy.Mergers and acquisitions.9. Financial Ethics.Fiduciary duty.Conflicts of interest.insider trading.10. International Financial Management.Foreign exchange risk.Currency hedging.International investment.中文回答:1. 财务报表分析。

财务报表分析课程简介

“财务报表分析”课程简介

课程名称:财务报表分析

英文名称:FinancialStatementsAnalysis

课程代码:182035

开设专业:财务管理

课程类型:专业基础课

先行课程:宏观经济学(181007)、财务会计(182029)、财务管理(182030)

内容简介:《财务报表分析》是一门是为培养学生基本理论知识和应用能力而设置的一门专业课。

本课程主要阐述了财务报表分析的基本原理、基本知识和基本方法。

本课程的任务是通过教学,使学生能够系统掌握财务报表分析的基本知识和基本方法,具有较强的财务报表分析能力,

为未来在实际工作中分析会计信息、使用会计信息打下坚实的基础。

教材:

张新民、钱爱民《财务报表分析》第三版,中国人民出版社

参考教材:

1、崔也光主编《财务务报表分析》,天津:南开大学出版社出版,2003年

2、张先治、陈友邦编著《财务分析》(第一版),大连:东北财经大学出版社2004年。

3.金中泉《财务务报表分析》(第一版),北京:中国财政经济出版社出版,2001年。

4.曹冈主编《财务务报表分析》(第一版),北京:经济科学出版社出版,2002年。

声明:此资源由本人收集整理于网络只用于交流学习。

如有侵权请联系删除处理。

《财务管理》(一)(双语)课程教学大纲

《财务管理》(一)(双语)课程教学大纲课程代码:FINM2005课程性质:大类基础课程授课对象:财务管理专业开课学期:秋总学时:54学时学分:3学分讲课学时:54学时实验学时:实践学时:指定教材:《现代企业财务管理》,复旦大学出版社,2012年;James C.Van Home,《Fundamentals of Financial Management》(Thirteenth Edition)(影印本),清华大学出版社,2009年参考书目:1.财务管理-实务与案例.陈玉菁。

中国人民大学出版社,2011年2.财务成本管理(第1版).中国注册会计师协会.财经出版社,2010年3.财务管理.陈玉菁、赵洪进、顾晓安.中国人民大学出版社,2008年4.金融理财原理(上、下).中国金融教育发展基金会金融理财标准委员会组织.中信出版社,2007年5.公司金融.薛斐.立信会计出版社,2005年6.现代财务管理(原书第11版,中译本第1版).(美)麦圭根(McGuigan,G.R.), 克雷洛(Kretlow,W.J.),王满译,机械工业出版社,2010年7.公司财务管理(原书第2版,中译本第1版),(美)埃默瑞(Emery,D.R.),芬纳蒂(Finnerty,J.D.)著,荆新,王化成等译.中国人民大学出版社,2008年8.经理人财务管理——如何创造价值(原书第3版,中译本第1版).(美)哈瓦维尼(Hawawini,G.)维埃里(Viallet,C.)著,胡玉明,江伟译.中国人民大学出版社,2008年9.财务管理(中译本第1版).(美)韦佛(Weawer,S.C.), 韦斯顿(Weston,J.F.)著,刘力,黄慧馨译. 中国财政经济出版社,2003年10.公司理财(原书第6版).[美]罗斯等著.吴世农等译.机械工业出版社,2012年教学目的:本课程介绍企业财务管理的基本理论、基本知识和基本方法。

内容主要包括:财务管理的基本概念,财务管理的目标,财务管理的环境,财务管理的一般方法,资金时间价值及其初步运用,资金成本的基本计算和运用,筹资管理的基本原理和方法,投资管理基本原理和方法,分配管理基本原理和方法,财务预测和财务决策原理,财务计划和财务控制原理,基本财务指标分析等。

ACCA财务管理英语中英文对照

ACCA--财务管理英语sole propsietorship 独资企业partnership 合伙企业corporate finance 公司财务corporate 公司closely held 私下公司public company 公众公司Goldman Sachs 高盛银行pension fund 养老基金insurance company 保险公司board of director 董事会separation of ownership and management 所有权与管理权的分离limited liability 有限责任articles of incorporation 公司章程real asset 实物资产financial asset 金融资产security 证券financial market 金融市场capital market 资本市场money market 货币市场investment decision 投资决策capital budgeting decision 资本预算决策financing decision 融资决策financial manager 财务经理treasurer 司库controller 总会计师CFO 首席财务官principal-agent problem 委托代理问题principal 委托人agent 代理人agency cost 代理成本information asymmetry 信息不对称signal 信号efficient markets hypothesis 有效市场假说present value 现值discount factor 贴现因子rate of return 收益率discount rate 贴现率hurdle rate 门坎比率opportunity cost of capital 资本机会成本net present value 净现值cash outflow 现金支出net present value rule 净现值法则rate-of-return rule 收益率法则profit maximization 利润最大化doing well 经营盈利doing good 经营造益collateral 抵押品warrant 认股权证convertible bond 可转换债券primary issue 一级发行prinary market 一级市场secondary tansaction 二级交易secondary market 二级市场over-the-counter (OTC) 场外交易financial intermediary 金融中介zero-stage 启动阶段business plan 创业计划书first-stage financing 第一阶段融资after-the-money valuation 注资后的价值paper gain 账面利润mezzanine financing 引渡融资angel investor 天使投资者venture capital fund 创业投资基金limited private partnership 有限合伙企业general partner 普通合伙人limited partner 有限合伙人small-business investment companies(SBIC)小企业投资公司initial public offering (IPO) 首次公开发行primary offering 首次发行secondary offering 二次发行underwriter 承销商syndicate of underwriter 承销辛迪加registration statement 注册说明书prospectus 招股说明书road show 路演greenshoe option 绿鞋期权spread 差价offering price 发售价格underpricing 抑价winner’s curse 成功者灾难bookbuilding 标书登记fixed price offer 定价发售auction 拍卖discrimination auction 差价拍卖uniform-price auction 一价拍卖general cash offer 一般现款发行right issue 附权发行shelf registration 上架注册prior approval 事前许可bought deal 买方交易seasoned issue 新增发行knowledgeable invertor 成熟的投资者qualified institutional buyer 有资格的机构买者record date 登记日with dividend 附有红利cum dividend 附息ex dividend 除息legal capital 法定资本regular cash dividend 正常现金红利extra 额外的special dividend 特别红利stock dividend 股票红利automatic dividend reinvestment plans (DRIP) 红利自动转投计划transfer of value 价值转移capital structure 资本结构MM’s proposition MM定理weighted-average cost of capital (WACC) 加权平均资本成本margin debt 保证金借款floating-rate note 浮动利率票据money-market fund 货币市场基金interest-rate ceiling 利率上限trade-off theory 权衡理论right to default 违约权leverage buy-out (LBO) 杠杆收购asymmetric information 信息不对称financial slack 银根宽松cost of debt 负债成本cost of equity 权益成本terminal value 清算价值cash flow to equity 权益现金流rebalancing 重整project financing 项目融资adjusted cost of capital 调整资本成本equivalent loan 等值贷款offsetting transaction 反向交易depreciable basis 折旧基数adjusted present value (APV) 调整现值call option 看涨期权exercise price 执行价格strike price 敲定价格exercise date 到期日European call 欧式看涨期权American call 美式看涨期权position diagram 头寸图put option 看跌期权Salomon Brothers 所罗门兄弟公司term stucture of interest rate 利率期限结构annuity 年金perpetuity 永久年金annuity factor 年金因子annuity due 即期年金future value 终值conmpound interest 复利simple interest 单利continuously compounded rate 连续复利率Consumer Price Index (CPI) 消费物价指数current dollar 当期货币nominal dollar 名义货币constant dollar 不变货币real dollar 实际货币real rate of return 实际收益率inflation rate 通货膨胀率principal 本金deflation 滞胀yield to maturity 到期收益率market capitalization rate 市场资本化率dividend yield 红利收益率cost of equity capital 权益资本成本payout ratio 红利发放率earnings per share (EPS) 每股收益return on equity (ROE) 权益收益率discount cash flow 贴现现金流growth stock 成长股income stock 绩优股present value of growth opportunity (PVGO) 成长机会的现值price-earnings ratio (P/E) 市盈率free cash flow (FCF) 自由现金流量book rate of return 账面收益率capital investment 资本投资operating expense 经营费用payback period 回收期discounted-payback rule 贴现回收期法则discounted-cash-flow rate of return 贴现现金流量的收益率internal rate of return (IRR) 内部收益率lending 贷出borrowing 借入profitability measure 盈利指标standard of pfofitability 赢利标准modified internal rate of return 修正内部收益率mutually exclusive projects 互相排斥的项目capital rationing 资本约束profitability index 盈利指标soft rationing 软约束hard rationing 硬约束incremental payoff 增量收入net working capital 净营运资本sunk cost 沉没成本sunk-cost fallacy 沉没成本悖论overhead cost 间接费用salvage value 残值straight-line depreciation 直线法折旧Internal Revenue Service 国内税收署tax shield 税盾accelerated cost recovery system 加速成本回收折旧法alternative minimum tax 另类最低税tax preference 税收优惠accelerated depreciation 加速折旧project analysis 项目分析equivalent annual cash flow 等价年度现金流marginal investment 边际投资default risk 违约风险risk premium 风险溢酬standard error 标准误差standard deviation 标准差market portfolio 市场组合market returm (rm) 市场收益率variance 方差the loss of a dgree of freedom 自由度损失Delphic 德尔菲unique risk 独特风险unsystematic risk 非系统风险residual risk 剩余风险specific risk 特定风险diversifiable risk 可分散风险market risk 市场风险systematic risk 系统风险undiversifiable risk 不可分散风险convariance 协方差well-diversified 有效分散value additivity 价值可加性efficient portfolio 有效投资组合quadratic programming 二次规划best efficient portfolio 最佳有效投资组合capital asset pricing model (CAPM) 资本资产定价模型separation theorem 分离定理security market line 证券市场线market capitalization 市场资本总额small-cap stocks 小盘股book-to-market ration 账面-市值比data mining 数据挖掘data snooping 数据侦察consumption beta 消费贝塔consumption CAPM 消费型资本资产定价模型risk aversion 风险厌恶arbitrage pricing theory 套利定价理论sensitivity of each stock to these factors 每种股票对这些因素的敏感度three-factor model 三因素模型company cost of capital 公司资本成本industry beta 行业贝塔firm value 公司价值debt value 负债价值asset value 资产价值blue-chip firm 蓝筹股financial leverage 财务杠杆gearing 举债经营financial risk 财务风险unlever 消除杠杆relative market values of debt (E/V) 负债的相对市场价值taxable income 应税利润after-tax cost 税后成本marginal corporate tax rate 公司边际税率after-tax weighted-average cost of capital 税后加权平均资本成本cyclicality 周期性cyclical firms 周期性公司operating leverage 经营杠杆revenue 收入fixed costs 固定成本variable costs 可变成本rate of output 产出率certainty equivalent 确定性等价值certainty-equivalent cash flow 确定性等价现金流risk-adjusted discount rate 风险相应贴现率underlying variables 基础变量sample 抽样real option 实物期权decision tree 决策树timing qption 安排期权production option 生产性期权option to bail out 清算选择权economic rent 经济租金future market 期货市场capital budget 资本预算strategic planning 战略规划appropriation request 拨款申请postaudit 事后审计stock options 股票期权private benefit 私下利益perks 特权享受perquisite 特权享受overinvestment 过度投资generally accepted accounting principle (GAAP) 公认会计原则qualified doption 保留意见delegated 委托economic value added (EV A) 经济附加值trade loading 贸易超载economic depreciation 经济折旧national income and product accounts 国民收入与产出账户cap 上限合约strip 本息剥离债券swap 互换bookrunner 股份登记员efficient capital market 有效资本市场random walk 随机游走positive drift 正漂移autocorelation coefficient 自相关系数weak form of efficiency 弱有效性semistrong form of efficiency 半强有效性strong form of efficiency 强有效性market model 市场模型acquiring firm 兼并公司acquired firm 被兼并公司superior profit 超常利润overreaction 反应过度underreaction 反应不足index arbitrageur 指数套利者portfolio insurance scheme 证券组合保险策略superior rates of return 超常收益exchange-rate policy 汇率政策application date 申购日long-term asset 长期资产retained earnings 留存收益financial deficit 资金缺口internal fund 内部资金debt policy 负债政策dividend policy 红利政策long-term financing 长期融资total capitalization 资本总额reserve 准备金issued and outsanding 已发行流通股份issued but not outsanding 已发行未流通股份authorized share capital 法定股本总额financial institution 金融机构cash-flow right 现金流要求权control right 控制劝dominant stockholder 控股股东majority voting system 多数投票制cumulative voting 累计投票制supermajority 绝对多数制proxy contest 投票代理权角逐minority stockholder 小股东reverse stock split 逆股票拆细master limited partnership 业主有限责任合伙企业real estate investment trust (REIT) 房地产信托投资基金preferred stock 优先股cumulative preferred stock 红利累积优先股line of credit 授信额度fixed-rate 固定利率floating-rate 浮动利率coupon 息票London Interbank Offered Rate (LIBOR) 伦敦银行间拆借利率eurobond 欧洲债券eurocurrency 欧洲货币euro 欧元senior 优级junior 次级subordinated 从属secured 有担保的collateral 抵押品warrant 认股权证convertible bond 可转换债券primary issue 一级发行prinary market 一级市场secondary tansaction 二级交易secondary market 二级市场over-the-counter (OTC) 场外交易financial intermediary 金融中介zero-stage 启动阶段business plan 创业计划书first-stage financing 第一阶段融资after-the-money valuation 注资后的价值paper gain 账面利润mezzanine financing 引渡融资angel investor 天使投资者venture capital fund 创业投资基金limited private partnership 有限合伙企业general partner 普通合伙人limited partner 有限合伙人small-business investment companies(SBIC)小企业投资公司initial public offering (IPO) 首次公开发行primary offering 首次发行secondary offering 二次发行underwriter 承销商syndicate of underwriter 承销辛迪加registration statement 注册说明书prospectus 招股说明书road show 路演greenshoe option 绿鞋期权spread 差价offering price 发售价格underpricing 抑价winner’s curse 成功者灾难bookbuilding 标书登记fixed price offer 定价发售auction 拍卖discrimination auction 差价拍卖uniform-price auction 一价拍卖general cash offer 一般现款发行right issue 附权发行shelf registration 上架注册prior approval 事前许可bought deal 买方交易seasoned issue 新增发行knowledgeable invertor 成熟的投资者qualified institutional buyer 有资格的机构买者record date 登记日with dividend 附有红利cum dividend 附息ex dividend 除息legal capital 法定资本regular cash dividend 正常现金红利extra 额外的special dividend 特别红利stock dividend 股票红利automatic dividend reinvestment plans (DRIP) 红利自动转投计划transfer of value 价值转移capital structure 资本结构MM’s proposition MM定理weighted-average cost of capital (WACC) 加权平均资本成本margin debt 保证金借款floating-rate note 浮动利率票据money-market fund 货币市场基金interest-rate ceiling 利率上限trade-off theory 权衡理论right to default 违约权leverage buy-out (LBO) 杠杆收购asymmetric information 信息不对称financial slack 银根宽松cost of debt 负债成本cost of equity 权益成本terminal value 清算价值cash flow to equity 权益现金流rebalancing 重整project financing 项目融资adjusted cost of capital 调整资本成本equivalent loan 等值贷款offsetting transaction 反向交易depreciable basis 折旧基数adjusted present value (APV) 调整现值call option 看涨期权exercise price 执行价格strike price 敲定价格exercise date 到期日European call 欧式看涨期权American call 美式看涨期权position diagram 头寸图put option 看跌期权色诺芬在《经济论》中首次提出“经济”一词(1)著作:《居鲁士的教育》、《居鲁士远征记》、《经济论》、《雅典的收入》(2)主要经济思想:a)重农思想。

财务分析-财务状况分析(英文版) 精品

Financial Statement AnalysisTo develop techniques for evaluating firms using financial statement analysis for equity and credit analysis.Integrates financial statement analysis with corporate finance, accounting and fundamental analysis.Adopts activist point of view to investing: the market may be inefficient and the statements may not tell all the truth.What Will You Learn From the Course• How statements are generated• The role of financial statements in determining firms’ values• How to pull ap art the financial statements to get at the relevant information• How ratio analysis aids in valuation• The relevance of cash flow and accrual accounting information • How to calculate what the P/E ratio should be ?• How to calculate what the price-to-book ratio ?Need for financial statement analysisGAAP – plexEconomic events about the firm to be reported to the public Relevance vs ReliabilityReporting: Recognition vs Disclosure (where)Users of Firms’ Financial InformationEquity InvestorsInvestment analysisLong term earnings powerManagement performance evaluationAbility to pay dividendRisk – especially marketDebt InvestorsShort term liquidityProbability of defaultLong term asset protectionCovenant violationsUsers of Firms’ Financial InformationManagement: Strategic planning; Investment in operations;Performance EvaluationLitigants - Disputes over value in the firmCustomers - Security of supplyGovernments: Policy making and Regulation– Taxation– Government contractingEmployees: Security and remunerationInvestors and management are the primary users of financial statementsFundamental AnalysisStep 1 - Knowing the Business•The Products; The Knowledge Base•The petition’ The Regulatory ConstraintsStep 2 - Analyzing Information•In Financial Statements•Outside of Financial StatementsStep 3 - Forecasting Payoffs•Measuring Value Added•Forecasting Value AddedStep 4 - Convert Forecasts to a ValuationStep 5 - Trading on the Valuation•Outside Investor: pare Value with Price to; BUY, SELL, or HOLD•Inside Investor: pare Value with Cost to; ACCEPT or REJECT StrategyA valuation model guides the process: Forecasting is at the heart of the process and a valuation model specifies what is to be forecasted (Step 3) and how a forecast is converted to a valuation (Step 4). What is to be forecasted (Step 3) dictates the information is implied?Balance Sheet•Assets (SFAC6): “probable future economic benefits obtained or controlled by a particular entity as a resultof past transaction or events-- no reference to risk (eg, assets sold but in which entityretains a risk)•Liabilities (SFAC6): ‘probable future sacrifice of economic benefits arising from present obligations of a particularentity to transfer assets or provide services to other entities in the future as a result of past transactions or events”-- not always followed (eg, certain leases and, until recently, pension benefits)•Equity (SFAC6): the residual interest in the net assets of an entity that remains after deducting i ts liabilities”-- does not handle situations where a source of capitalhas elements of debt & equity (eg, convertibles)•Classified by liquidityCA : converted to cash or used within 1-year oroperating cycle (if longer)CL: obligations expected to be settled within 1-year oroperating cycle•Tangible A&L reported above intangibles (goodwill, contingent liabilities)Measurement of Assets & Liabilities•Historical Cost, for most ponents of Balance Sheet•May be at market under “lower of cost or market rule”•Reversals of prior write downs allowed for marketable equity securities but not for inventories•Financial service firms (banks, brokerage, insurance) report certain A&L at market•A&L of foreign affiliates reported at end-of-period X-rate or a bination of it and specified historical X-rates •Intangible assets have uncertain and hard to measure benefits and are reported only when acquired via a“purchase method” acquisition-- brand names-- when reported, called Goodwill, Patents, etc.Two Fundamental shortings of the Balance Sheet Elusiveness of valueValue cannot be assigned to all assetsOther Balance Sheet issues: Book Value vs. Market ValueInflation: The correct way to think about inflation is that inflation represents a decline in the value of one good – the currency of denomination (i.e., the U.S. dollar in our case). When the value of the currency declines, prices of all other goods & services rise because those prices are measured in terms of dollarsWeakness of Historical Cost Accounting: it ignores the impact of changes in the purchasing power of the currency. The net impact of not considering inflation is that book value understates the market value.Obsolescence causes book value to overstate market valueHow to Measure Effect of Obsolescencea. Observe difference between market value & book value (after adjustingfor inflation)b. Estimate the value of the asset’s earning power. But this is simply thediscounted cash flow approach & thus it represents circular reasoning.Inflation & ObsolescenceInflation causes book value to understate market valueObsolescence causes book value to overstate market valueThe effect of inflation & obsolescence may not be apparent in an examination of book values because they offset one anotherOrganizational Capitala. The whole is worth more than the sum of the partsb. Returns to Entrepreneurshipc. Difficult to separate from the firm as a going concernd. Can be estimated only by examining the earning power of the panySources of Organizational Capital Valuesa. Long-term relationshipsb. Reputational “brand name” capitalc. Growth optionsd. Network of suppliers and distributorsMore on Organizational Capitala. It is difficult to separate the firm’s organizational capital from the firm as anongoing concernb. The value of a brand name is not reflected in the replacement cost of assetsc. Can only be estimated by examining the earning power of the pany (DCF)Adjustments to Book ValueEstimate Replacement CostEstimate Liquidation ValueDrawbacksDo adjusted book values reflect market values?Adjusted book values do not consider organizational capital Drawbacks of AdjustmentsIt is often difficult to determine if we have made the correct adjustments Adjustments often fail to consider the value of off-balance sheet itemsReplacement CostNo universal agreementCan use price indexCPI, PPI, GDP implicit deflatorIgnores organizational capitalLiquidation ValueSecondary markets do not existAsset specificityContestable marketsIne statementNet SalesCost of Goods SoldGross ProfitSelling & Administrative expensesAdvertisingLease paymentsDepreciation and amortizationRepairs and maintenanceOperating ProfitOther ine (expense)Interest ineInterest expenseEarnings before Ine taxesIne taxesNet earningsStatement of Consolidated Retained Earnings Retained earnings at beginning of yearNet earningsCash DividendsRetained earnings at end of yearIne Statement•Based on Accrual accounting•Based on Matching Principle•Revenues(SFAC6) “inflows of an entity from delivering or producing goods, rendering services, or carrying out otheractivities that constitute the entities ongoing major or centraloperations”•Expenses(SFAC6) “outflows from delivering or producing goods, rendering services, or carrying out other activities thatconstitute the entities ongoing major or central operations”•PREHENSIVE INE CONCEPT“the change in equity from transactions from non-owner sources. It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners”•Gains“Increases in equity from peripheral or incidental transactions of an entity except those that result from revenues or investment by owners.”•Losses“Decreases in equity from p eripheral or incidental transactions of an entity except those that result from revenues or investment by owners.”Revenues+ Other ine and revenues- E xpenses= Ine from CONTINUING OPERATIONS∀Unusual or infrequent events= Pre tax earnings from continuing operations- I ne tax expense= After tax earnings from continuing operations*∀Discontinued operations (net of tax)*∀Extraordinary operations (net of tax)*∀Cumulative effect of accounting changes (net of tax) * = Net Ine ** Per share amounts are reported for each of these items High quality ine statement reflect repeatable ine statement Gain from non-recurring items should be ignoredwhen examining earningsHigh quality earnings result from the use of conservative accounting principles that do not overstate revenues or understate costsLow Quality of Earnings Indicators1.Unstable Ine Statement Elements unrelated to normalbusiness operations2 Earnings that reflect dubious adjustments to estimatedliability accounts3 Earnings that have been determined using liberal accountingpolicies (methods and estimates) because of the resultingoverstatement of net ine. Such overstatement also results in the overstatement of future earnings projections ine based on ultraconservative accounting policiessince the resulting net ine is misleading as a basis forpredicting future earningsWhat to do?pare the pany’s accounting polices to the prevalentaccounting policies in the industry5.Unreliable and inaccurate accounting estimatesWhat to watch for?Prior estimates materially differ from actualexperience, such as where the pany’s assumed interest rate onpension fund assets significantly differs from the actual interestrate earned as reflected by significant actuarial gains and losses.What to do?Restate net ine as if realistic accounting estimates were used.6. Earnings that have been artificially smoothed or managed.What to watch for?a. Revenue reflected earlier or later than the realistic time periodb. Shifting of expense among reporting periodsc. Smoothly rising earnings trendd. Sharp increase or decrease in sales in the last quarter of the yearsas reflected in the 4th quarter ine statemente. Trading of investment securities among affiliated paniesf. Significant modification in estimated liability accounts in the lastquarterg. Writing down a good asset (inventory) and selling it next year toshow higher earningsh. The “big bath”, in which everything is written off in a really badyear so that it will be easier to show good profits in the followingyears. This sometimes occurs when new management takes overand wishes to blame old management for poor profits or whenearnings are already so low that their further reduction my nothave significant impactWhat to do?Look at the functional relationship of sales and net ine over time. An inconsistent relationship may be a manipulatorindicator. Restate earnings by taking out profit increments orreductions due to ine management ploys7.Deferral of costs that do not have future economic benefitWhat to watch fora. Inventory of unsalable items in view of current environment (8track tapes, typewriters, large automobiles during oil shortage)b. Sudden write-offs of inventoryc. Goodwill on the balance sheet but the pany has none (operating atlosses, significant decline in market share, bad publicity)d. Costs that are currently capitalized when in prior years, they wereexpensed (e.g. Tooling costs in inventory)What to doRestate net ine as if the unrealistic deferral had not been made.8. Unjustified Changes in Accounting Principles and EstimatesWhat to watch fora. A firm has a past history of making frequent accounting changesb. Accounting changes that create earnings growthc. The pany fires the auditor and hires another one because of adisagreement over a proposed accounting change.What to doa. Determine whether the accounting change is justified by seeing if itconfirms to requirements in FASB statements, Industry Audit Guides& IRS regulationsb. Ascertain whether the accounting change is preferable, given nature ofbusiness (e.g., decreasing the life of a puter because of newtechnological advances in the industry)c. Does change make sense? (Lowering bad debt expense as % ofaccounts receivable does NOT make sense when customer defaultsare rising)d. If accounting change results in increasing net ine, restate earnings asthey would have been if the old method had been retained.9.Premature or Belated Revenue RecognitionWhat to watch fora. Accruing unbilled salesb. Is there a sufficient provision for future losses in connection withthe recognition of revenue?c. Improper deferral of revenue to a later periodd. Reversal of previously recorded profitsWhat to do- Restate revenue as if proper revenue recognition were made10.Underaccrual or Overaccrual of ExpensesWhat to watch fora. Failure to incur necessary maintenance expendituresb. Inadequate warranty provisionWhat to do- Adjust net ine for difference between expenseprovided & normal expense11.Improper Accounting PoliciesWhat to watch fora. Reduction of expense for overly anticipated recoveries of excesscosts due to modifications in government contractsb. Substantial provision for future costs in present year (e.g.warranties) because firm was remiss in making sufficientprovisions in prior yearsWhat to do-restate earning of years affected so can determineproper earnings trend12.Modification in Loan Agreements Due to FinanciallyWeak BorrowersWhat to watch for - lowering of interest on loanWhat to do - downwardly adjust net ine for inclusion of accrued interest ine on risky loans13.Change in corporate policy for the current year, whichimpacts earnings (e.g., writing insurance renewal contracts in the 4th quarter of the current year rather than the 1stquarter of the next year).14.Unjustified Cutback in Discretionary CostsWhat to watch fora. Declining tend in discretionary costs as a % of net sales or toassets to which they applyb. Vacillation in the ratio of discretionary costs to sales over theyears as this may indicate management of earningsWhat to doa. Determine trend in discretionary costs over time throughuse of index numbersb. Determine ratio of discretionary costs to sales over last 5years. An example is ratio of repairs & maintenance tosales and/or to fixed assets15.Book Ine Substantially Exceeds Taxable IneWhat to watch for - A continual, significant rise in deferred ine tax credit account due to liberal accounting policies16.Residual Ine that is Substantially less than Net IneResidual Ine may be determined by deducting the imputed costof capital (weighted average cost of capital time total assets)from net ine.What to do - Determine ratio over time of residual ine to net ine17. A High Degree of Uncertainty Associated with IneStatement ponentsWhat to watch fora. Firm engaged in long-term activities requiring many estimates inine measurement processb. Significant future loss provisionsc. Estimates have been consistently materially different from actualexperienceWhat to doa. pare o ver time firm’s estimated liability provisions with actuallosses occurring. – e.g., warranty cost sb. Determine what percent of total assets are intangible, which bytheir nature require material estimates to be made18.Unreliably Reported EarningsWhat to watch fora. Poor system of internal control because it infers possibleerrors in reporting systemb. High turnover rate in auditorsc. pany has reputation for managing earnings and/or usingliberal accounting policiesd. Indications of lack of management integrity as evidenced bysuch things as bribesWhat to doa. Determine trend in audit fees over timeb. Examine for disclosure made by pany related to adjustmentsdue to prior years' accounting errorsc. Look at accounting, financial and brokerage researchpublications that note and give examples of panies withquestionable accounting policies.High Quality of Earnings Indicators: Ine Backed up by Cash Ine not involving the Inclusion of amortization costsrelated to questionable assets, such as deferred charges Ine that reflects Economic Reality4.Ine Statements ponents that are Recognized Close to thePoint of Cash Inflow and Cash OutflowPolicies that lower quality of earnings1. reduce expense for expected recovery of excess costs resultingfrom changes in government contract – only collected 65%2. unrealistic decline in percentage of sales allowance to sales3. provision for future costs (warranties) high becauseunderprovided in past4. “Big Bath”5. re-negotiate terms of loan with weak borrower6. transfer from 1 sub to another7. sell securities at a gain and buy them back at higher price- haveto recognize lossHow pany smoothes earnings Check list1Does level discretionary cost conform to past2Is there a drop in trend of discretionary costs as percentage of sales3Does cost cutting program involve significant cut in discretionary costs4Does cost cutting program eliminate fat?5Do discretionary costs show fluctuations relative to sales 6Is there a sizable jump in discretionary costs?Summary checklist of key pointsA. No single “real” net ine figure existsB. The analyst must adjust reported net ine to an earningsfigure that is relative to him/her.C. Earnings quality evaluation is important in investment,credit, audit & management decision making.D. Appraising the quality of earnings requires anexamination of accounting, financial, economic andpolitical factors.E. Earnings quality elements are both quantitative andqualitativeCash flow statement1. SCF (Statement of Cash Flows) adds in situations where Balance Sheetand Ine Statement provide limited insight2. SCF helps identify the categories into which panies fit3. Financial flexibility is a useful weapon to gain a petitive advantageand is best measured by studying the SCFThe key analytical lessonsThe cash flow statement – not the ine statement – provides the best information about a highly leveraged firm’s financial healthThere is no advantage in showing an accounting profit, the main consequence of which is incurring taxes, resulting, in turn, in reduced cash flowsCash Flow and pany Life CycleCash Flow and Start-up paniesLittle or no operating cash flowsLarge cash outflows for investing activitiesLarge need for external financing (mostly from issuing mon stock, issue long term debt)Cash Flows and Emerging Growth paniesSome operating cash flow (not enough to sustain growth)Large cash outflows to expand activitiesRequires cash flows from financingPay back some short-term debt, issue some mon stockCash Flows and Established Growth paniesFund growth from operating cash flowDepreciation is substantialRepayment of long term debt, begin to pay dividendCash Flows and Mature Industry paniesModest capital requirementsDepreciation and amortization is significantNet negative reinvestmentLarge dividend payout, reduction in long term debt Cash Flows and Declining Industry paniesNet cash user (similar to emerging growth)Lower dividends, Slim operating cash flowssell assetsCash Flows and Financial FlexibilitySafety of dividendFinance growth with internal fundsMeet other financial obligationsFinancial Ratios Analysis:Ratios are more informative than raw numbers1. Ratios provide meaningful relationships between individual values inthe financial statements2. Ratios help investors evaluate management3. Enable parison of a firm’s performance toThe aggregate economyIts industry or industriesIts major petitorsIts past performanceRatios and Financial Analysisparability among firms of different sizesProvides a profile of the firmCaution:Economic assumption of Linearity – ProportionalityNonlinearity can cause problems:Fixed costs, EOQ for inventoriesBenchmarks; Is high Current ratio good? For whom?Industry-wide norms.Accounting Methods; Timing & Window DressingLIMITATIONS1. No theory to define ‘good’2. Historical, not economic3. Most as of a single point in time4. Seasonal operations5. One-time effects6. Designed for manufacturersLiquidity Ratios: attempt to measure the ability to pay obligations such as current liabilities and the pool of assets available to cover the obligations. Liquidity is the ability of an asset to be converted to cash quickly at low cost. Converting an asset to cash occurs in one of two ways. Sell the asset, hoping it has reasonable liquidity, or in the case of a financial asset, like accounts receivable or Treasury bill, maturity brings cash. Working capital circulates from inventory to accounts receivable to cash, etc. Accounting value estimates of liquid assets are reasonable estimates of their value.Current assets (the pool of circulating cash assets available to be allocated to pay bills) minus current liabilities (the pool of obligations the business must pay in the near future) is an analytical amount called net working capital (NWC).NWC = current assets - current liabilitiesNWC/total asset ratio = net working capital / total assetsThe current ratio is the classic liquidity ratio, but is merely a variation of the idea above—what pool of circulating assets is available relative to the pool of current obligations:Current ratio = current assets / current liabilitiesQuick ratio =(cash + marketable securities + accounts receivable) /current liabilitiesCash ratio = (cash + marketable securities) / current liabilitiesCash flow from operation ratio = OCF / current liabilitiesLeverage ratios are two types: balance sheet ratios paring leverage capital to total capital or total assets, and coverage ratios which measure the earnings or cash-flow times coverage of fixed cost obligations.Balance sheet ratiosLong-term debt ratio = long-term debt / ( long-term debt + equity)Debt-equity ratio = long-term debt/equityTotal debt ratio = total liabilities / total assetsA coverage ratio, such as the times interest earned ratio, measures an amount available relative to amount owed. How many times is the obligation covered?Times interest earned = EBIT / interest expense= (EAT+Tax+Interest Exp)/ interest expenseTimes Cash flow coverage =(OCF+Tax+Interest Exp)/ interest expenseTotal assets turnover = Sales / Total assetsAccounts Receivable turnover = Sales / AR[Days A/R outstanding = 365 / Accounts Receivable turnover]Inventory turnover = Sales / Average Inventory, orCOGS / Average Inventory[Inventory Conversion = 365 / Inventory turnover]Payable turnover (deferral) = Purchase (or COGS) / AP[Days A/P outstanding = 365 / Payable turnover]Note: Cash Cycle = Inventory Conversion + Days A/R outstanding –Days A/P outstandingProfitability Ratios: refers to some measure of profit relative to revenue or an amount invested.The net profit margin measures the proportion of sales revenue that is profit available for sources of funds (EBIT-tax).Gross profit margin = gross profit / salesOperating profit margin = EBIT / salesNet profit margin = net ine / salesReturn on assets = (net ine + interest )/ average total assetsReturn on equity = net ine/ average equityPayout ratio = dividends / net earningsPlowback ratio = 1 - payout ratio= (earnings – dividends)/(net earnings) = (earnings retained in period)/( net earnings)Growth in equity = plowback ratio x ROEMarket Based Ratios•For pricing an IPO if business going public•P/E RatioWhat investors are willing to pay for a $ of earnings (Current/ Forecast)What creates a high P/E?•Market/BookUsually much different than 1.•Price/Cash FlowThe Du Pont System is a process of analyzing ponent ratios, (also called deposition) of the ROA and ROE to explain their level or changesRatio Pr 1 Leverage Turnover Asset y ofitabilit Equity Debt ROA EquityTA TA Sales Sales NI EquityTA TA NI Equity NI ROE ⨯⨯=⎪⎪⎭⎫ ⎝⎛+⨯=⨯⨯=⨯==Industry analysis:Definition of an industry: the group of firms producing products that are close substitutes for each other.Forces driving industry petition: There are five forces in determining the petitive structure of an industry, they are: (1)Entry, (2)Threats of substitutions, (3)bargaining power of buyers, (4)Bargaining power of suppliers, and (5)rivalry among current petitors, and can be pictured as:Five forces model:Potential EntrantsThreats of new entrants(Suppliers) (Buyers )0 bargaining power Industry petitors bargaining powerRivalry among existing firmsThreats of substitutesSubstitutesThreats of entry: new entrants bring to an industry new capacity, the desire to gain market share, and often substantial resources. Price can bid down or incumbent’s costs inflated as a result, reducing profitability.Barriers to entry:A. Economics of scales deter entry by forcing the entrants to e in at alarge scale and risk strong reaction from existing firms or e in at asmall scale and accept a cost disadvantage.B. Product differentiation: product differentiation means that establishedfirms have brand identification and customer loyalties. Differentiation creates a barrier to entry by forcing entrants to spend heavily to overe existing customer loyalties.C. Capital requirement: the need to invest large financial resources inorder to pete creates a barrier to entry, particularly if the capital is required for risky or unrecoverable up-front advertising or R&D.Capital requirement maybe also needed for customer credit, inventory start-up cost, as well as production cost.D. Switching costs: A barrier to entry is created by the switching cost,that is, one-time cost facing the buyer of switching from one supplier’s product to another’s.E. Access to distribution channels: the more limited the wholesale orretail channels for a product are and the more existing petitors have these tied up, obviously the tougher entry into the industry.F. Cost disadvantages independent of scale: proprietary producttechnology, favorable access to raw materials, favorable locations,government subsidy, and learning or experience curve.G. Government policy:Expected retaliation: conditions that signal the strong likelihood of retaliation to entry and hence to deter it are the following:A. A history of vigorous retaliation to entrants.B. Established firms with substantial resources to fight back.C. Established firms with great mitments to the industry andhighly illiquid assets employed in it.D. slow industry growth, which limits the ability of the industryto absorb a new firm without depressing the sales andfinancial performance of established firms.。

如何看财报经典书籍

如何看财报经典书籍如何阅读财报是每个投资者都需要掌握的基本技能。

了解财报背后的信息能够帮助我们更好地评估一家公司的财务状况和业绩表现,从而做出更明智的投资决策。

在这篇文章中,我将为你推荐一些经典的财报阅读书籍,希望能够帮助你提高财报阅读的能力。

1.《财务报表阅读与分析》(Financial Statement Analysis and Security Valuation)这本书是由斯蒂芬·佩内尔(Stephen Penman)所著,是一本介绍财报分析的经典教材。

书中详细讲解了财报的结构和内容,以及如何从财报中获取有用的信息来评估公司的价值。

2.《财务报表分析》(Analysis of Financial Statements)这本书是由利奥·斯特罗姆(Leopold A. Bernstein)和约翰·J.玛丽诺(John J. Wild)合著的。

书中通过具体的案例,向读者展示了如何从财务报表中提取必要的信息,以及如何进行财务比率分析和财务预测。

3.《财务报表分析与应用》(Financial Statement Analysis and Security Valuation)这本书是由斯蒂芬·佩内尔(Stephen Penman)所著,是一本财务报表分析的经典教材。

书中介绍了如何使用财务报表来评估公司的经营状况和财务表现,并且提供了一些实用的分析工具和方法。

4.《财务报表分析与应用》(Financial Statement Analysis and Security Valuation)这本书是由斯蒂芬·佩内尔(Stephen Penman)所著,是一本介绍财务报表分析和估值的经典教材。

书中详细介绍了财务报表的结构和内容,以及如何使用财务比率和现金流量分析来评估公司的价值。

5.《财务报表阅读与理解》(Financial Statements: A Step-by-Step Guide to Understanding and Creating Financial Reports)这本书是由托马斯·R.伯恩(Thomas R. Ittelson)所著,是一本介绍财务报表的入门读物。

财务报表分析(英文版)答案