2018美国市场消费者信心报告(英文版)

美国消费者的看法英语作文

美国消费者的看法英语作文As an American consumer, I think it's important to have choices when it comes to products and services. I like being able to compare different options and find the best value for my money. It's also nice to have the convenience of shopping online and having things delivered right to my door.When it comes to customer service, I expect to be treated with respect and courtesy. It's frustrating when I encounter rude or unhelpful employees, and it can make me think twice about doing business with a company in the future. On the other hand, good customer service can make me a loyal and repeat customer.I appreciate it when companies are transparent about their pricing and policies. Hidden fees and complicated terms and conditions can be a major turn-off. I want to know exactly what I'm getting and how much it will cost me before making a purchase.As a consumer, I also care about the ethical and environmental practices of the companies I support. I prefer to buy from companies that are committed to sustainability and social responsibility. It's important to me that the products I buy are not only high quality, but also produced in a way that is ethical and environmentally friendly.When it comes to advertising, I prefer when companies are honest and upfront about their products. I don't like feeling like I'm being manipulated or deceived by flashy ads. I appreciate it when companies focus on the actual benefits and features of their products rather than trying to create a false sense of urgency or scarcity.。

市场趋势预测英文版

1CX hits a wallC ustomer experience CX became the centerpiece of business strategy as companies adjusted to the experience economy.But according to Forrester’s 2017 CX Index, CX quality plateaued or declined for most industries and companies. Why CX initiatives tackled low-hanging fruit to put early points on the board, and most CX initiatives had too little clout to force meaningful operational change.PREDICTIONS Customers’ expectations will outpace companies’ ability to evolve or invent experiences, and the deferred transformation in 2017 means that companies can’t adjust fast enough or well enough.In 2018, 30% of companies will see further declines in CX performance, and those declines will translate into a net loss of a point of growth.Smart executives will intervene to make CX an internal disruptive force, one that is underpinned by the fundamentals of CX management with customer trust at the core; too many executives will continue to ignore evidence of market disruption and procrastinate until the evidence is overwhelming, putting their rms at risk as we enter 2019.PREDICTIONS3Talent widens the digital divideThose strugglingto attract scarcetalent will spendup to 20% above market.T he news reports of a digital talent crisis are overblown. Continued use of H-1B, the gig economy bench, and technical training for the existing workforce have strengthened supply for commodity technical skills. The 2% to 4% growth in wages suggests a relatively balanced market.The real story is the lack of specialized roles like data scientists, information security analysts, high-end software developers, and experience designers that are critical to CX and digital transformation.PREDICTIONSThese professionals want to work for rms further along in their digitaltransformation effort and with more ambitious strategies. They will work for laggards as a last resort or due to geographic necessity. Executives at digital leaders have 90% of the talent they need, while those at self-described digital laggards have only 19% of the talent they need.In 2018, talent issues will widen the divide between digital predator and prey; laggards will need to more aggressively set up digital incubation centers in talent hotspots and pay up to 20% above the market rate to change the game.4 The empowered machine Intelligent agentswill directly in uence 10%of purchasedecisions.PREDICTIONS25% of brandswill lack expertise in thelingua franca of intelligent T he algorithm is foundational to digital platforms like Google and Amazon. It is how platforms make sense of customer preferences, recommend actions, learn, and act. The algorithm is the languageagents.of platforms.Ye t brands have been slow to understand the lingua franca of platformalgorithms, especially when the brand is not part of the customer’sexisting preference and the algorithm is choosing whether to introducethat brand to the customer. It is akin to not understanding search PREDICTIONSalgorithms — but with far greater consequences.It is one thing to be disintermediated by the platform and its associatedintelligent agent; it is another to not understand or have any realin uence on that relationship.In 2018, CMOs will need to source talent to interpret and in uenceAI-driven platforms. Twenty-ve percent of CMOs will fail, resulting intheir brand becoming undifferentiated and silenced in the market.6The intelligent agent cocoon Consumers,representing$24B in spend,will use intelligentagents to escapethe noise. PREDICTIONSAll the signals are clear: customers avoiding ads; the cost of wasted or bad ads; major brands announcing massive cuts in ad spending; and agencies providing downward guidance to Wall Street.This is not an advertising budget crisis but simply changing priorities.CMOs can’t defend underperforming media spend focused on customer acquisition as churn rates escalate or stand idly by as digitalPREDICTIONS platforms threaten to disintermediate their relationship with customers. Instead of plowing money into traditional ad spending, CMOs will increase spend on:1. Revitalizing CX to drive af nity and stem churn.2. Synchronizing loyalty programs to customer expectations.3. Understanding how to decode digital platform algorithms.4. Advancing martech to deliver individualized experiences at scale.The result: Ad spend will be at in 2018 and cause a painful correction in the agency and adtech markets.8The GDPR challengeGDPR challenges how companies balance risk and cost. Full compliancewith all aspects of GDPR, including the ePrivacy Directive, is a highand expensive bar to clear. Non- or partial compliance could createextraordinary costs and damage to the brand. Companies are weighing what it means to fully or partially comply. We predict that 80% of rms affected by GDPR will not comply withPREDICTIONS the regulation by May 2018. Of those noncompliant rms, 50% will intentionally not comply — meaning they have weighed the cost and risk and are taking a path that presents the best position for their rms. The other 50% are trying to comply but will fail.This will be a uid environment; any successful case against awell-known giant will change the risk/cost balance.The sleeper issue of 2018 will not be compliance but how consumer advocate groups use GDPR to prosecute their agendas by using the regulation’s“right to be forgotten” clause — exhausting companies’resources and damaging their brands.More than 50% of banks will start becoming an unintentional utility.PREDICTIONS67% of retailers will be unprepared to exploit intelligent agents.PREDICTIONS11The AI resetA I is rapidly changing how companies create personalized experiencesat scale; how consumers balance privacy and value with brazendemocratization of their data; and how employees shape theirprofessional paths to include greater interaction with machines.The focus of the AI conversation has centered on using AI technologiesto augment intelligence or create conversational interfaces. Ideally, theseinvestments would test how AI reinvents businesses, enabling rms toenter new markets, create new products and services, and drive growth PREDICTIONSthrough a reimagined operating model and an expanded view of digitalecosystems and partnerships.But 2017 investments have focused on discrete use cases and projectsto prove immediate business value. Those bene ts are too narrow andwill be short-lived.In 2018, 75% of AI projects will underwhelm because they fail to modeloperational considerations, causing business leaders to reset the scopeof AI investments — and place their rms on a path to realizing theexpected bene ts.30% of proofs of concept will create a true foundation for blockchain.PREDICTIONS13 Securit y for pro tC ompanies face increasing cyberthreats from hackers who seek tocommit cyberwarfare or industrial sabotage. There is no rest for theweary: The same security, risk, and privacy teams battling hackersencounter internal pushback that security measures negatively affectcustomer experiences.But what if security investments directly enhance customer experiencesand drive growthPREDICTIONSIn 2018, we will start to see security for pro t measures driven bysecurity, risk, and privacy teams with the support of their marketingand product peers. Central to this is identity management.Security and privacy teams need to know exactly who is accessingwhat and resolve identities across entry points. Marketing can use thatsame capability in the martech stack for personalization — transforminga security mandate into a CX enhancement. In the coming year,10% of rms will crack this code and gain new and powerfulinvestment leverage.淘宝店铺“Vivian研报”收集整理获取最新报告及后续更新服务请淘宝搜索“Vivian研报”For more information on the data and research that underpins these predictions, visit 2018-predictions or email usat.Follow Forrester: Become a client:CONTACT US。

敦煌网分享2018年美国假日季电商数据

敦煌网分享2018年美国假日季电商数据目录一、美国消费者信心指数 (1)二、2018年美国电商销售增长 (2)三、假日季期间有更多的消费者选择网购 (3)四、黑五周的电商销售表现 (4)五、年终购物季跟亚马逊Prime Day的战绩相比如何? (6)六、美国黑五周的零售总额 (6)七、2018年美国假日季预测 (7)八、60%的消费者计划在电商平台上购物 (8)根据美国电商研究机构Internet Retailer迄今对美国假日季的分析结果,包括黑五周销售额、消费者购买习惯和2018年假日季预测。

得益于强劲的电商销售增长、高涨的消费者信心指数以及强烈的消费者网购意愿,2018年有望以一场“声势浩大”的假日购物季完美谢幕。

Internet Retailer有关2018美国假日季电商数据的分析,接下来将结合10张图向你娓娓道来。

一、美国消费者信心指数消费者信心指数是指消费者对当前经济状况的评价,以及对未来6个月经济生活变化的预期。

根据世界大型企业联合会(Conference Board)有关消费者信心指数的调查显示,美国消费者信心指数在今年10月攀升到了137.9,创下了18年以来的最高水平。

一般来说,当人们相信经济运行良好时,他们会更有安全感并且更愿意消费。

据估计,美国消费者信心指数在年底前都会持续保持高水平状态。

二、2018年美国电商销售增长根据对Internet Retailer对美国商务部数据的分析,美国电商销售额在2018年前三季度同比增长了15.5%,该数字超过了前三年的增长率。

2017年前三个季度里,美国电商销售额同比增长率为15.2%。

而在2016年的同一时期,美国电商销售额同比增长率仅为14.6%。

(图为2015年-2018年,前三季度美国电商销售额年同比增长率)三、假日季期间有更多的消费者选择网购根据Internet Retailer和评级平台Bizrate Insights在2018年11月对消费者进行的调查(如下图),60%的消费者计划将超过一半的假日时间用于网购,超过80%的人计划至少利用1/4的假日时间用于上网。

Avionos:2018年消费趋势报告

Avionos:2018年消费趋势报告Avionos提供的《2018年消费趋势报告》显示,美国已经有超过55%的消费者通过Facebook和Instagram等社交媒体购物过,但有超过60%的消费者从未购买过由网红或者社媒名人推广的产品。

报告还指出,在接受调查的1409名美国消费者中,超过66%的消费者表示上网冲浪时,他们会先在亚马逊或者谷歌上进行搜索。

这表明,主流引擎搜索已经取代了传统的网页浏览模式。

谈及实体店零售的地位时,约有63%的受访者表示愿意在实体店购买电子产品或者家具等昂贵物品,而52%则表示会使用电脑或者手机在网上搜索这些产品。

也许这份报告最大的收获就是,得出了通过社交媒体购物的消费者数量。

除了让零售商更有信心通过社交媒体推广产品、与消费者互动之外,社交媒体作为购物渠道,也给零售商带来了巨大商机。

因为,实际上,在社交媒体购物的消费者比那些不在社交媒体购物的消费者要花费得更多。

Avionos还发现,当消费者在社交媒体购物或者通过其他方式网购时,他们希望能了解产品信息。

比如说,调查发现,有54%的受访者表示,如果从网上零售商那里获得产品详情,他们网购时会更有信心;而49%表示,在网购一款产品前,如果能顺着这款产品的listing找到其他对购买有帮助的相关内容,他们会更放心。

在社交媒体的推送和搜索结果上,能做到这一点更为重要。

因为这样一来,消费者就不再需要去零售网站上搜索所有相关产品的详细信息。

“传统的进店购物体验已经远远不够用了。

消费者希望,与零售商和品牌的互动无论在何时何地都能更快捷、个性化和信息化”Avionos的总裁Scott Webb 在一份声明中说道。

“亚马逊已经改变游戏规则了,尤其是提高了消费者的预期标准。

这导致了零售商改变了他们的整体策略,把重点放在了购物体验为主的交易上,专注于在各种购物渠道上为消费者提供有趣的内容和个性化的消费体验。

”。

美国特种纸市场报告2018目录—英文版

美国特种纸市场报告2018目录—英文版Published by QYResearchMar. 2018United States Specialty Paper Market Report 2018Hard Copy: 3800 USDPDF Copy (single user): 3800 USDEnterprise wide License: 7600 USDPages: 152Tables and Figures: 199Published Date: June 2018Publisher: QYR Chemical & Material Research CenterSummaryThe United States Specialty Paper market is valued at 7963.63 million USD in 2017 and is expected to reach 8578.20 million USD by the end of 2025, growing at a CAGR of 0.93% between 2018 and 2025.This report studies the Specialty Paper development status and future trend in United States, focuses on top players in United States, also splits Specialty Paper by type and by applications, to fully and deeply research and reveal the market general situation and future forecast.The major players in United States market includeKapStoneGlatfelterInternational PaperDomtarSMWGeorgia-PacificAhlstrom-MunksjöKohlerUPMOji GroupMondiStora EnsoSappiFedrigoniNippon PaperOnyx Specialty PapersWausau Coated Products, Inc.On the basis of product, the Specialty Paper market is primarily split intoDecor PaperRelease Liner PaperPackaging PaperPrinting PaperOthersOn the basis on the end users/applications, this report coversPackaging & LabelingBuilding & ConstructionFood ServiceBusiness and CommunicationIndustrialPrinting and PublishingOthersTable of Contents1 Specialty Paper Overview (1)1.1 Product Overview and Scope of Specialty Paper (1)1.2 Classification of Specialty Paper by Product Category (1)1.2.1 United States Specialty Paper Sales (K MT) Comparison by Types (2013-2025) (1)1.2.2 United States Specialty Paper Sales (K MT) Market Share by Types (ProductCategory) in 2018 (2)1.2.3 Decor Paper (2)1.2.4 Release Liner Paper (3)1.2.5 Packaging Paper (3)1.2.6 Printing Paper (4)1.3 United States Specialty Paper Market by Applications/End Users (5)1.3.1 United States Specialty Paper Sales (K MT) and Market Share Comparison byApplications (2013-2025) (5)1.3.2 Packaging & Labeling (6)1.3.3 Building & Construction (6)1.3.4 Food Service (7)1.3.5 Business and Communication (8)1.3.6 Industrial (8)1.3.7 Printing and Publishing (9)1.4 United States Specialty Paper Market by Regions (9)1.4.1 United States Specialty Paper Market Size (Million USD) Comparison by Regions(2013-2025) (10)1.4.2 The West Specialty Paper Status and Prospect (2013-2025) (10)1.4.3 Southwest Specialty Paper Status and Prospect (2013-2025) (11)1.4.4 The Middle Atlantic Specialty Paper Status and Prospect (2013-2025) (12)1.4.5 New England Specialty Paper Status and Prospect (2013-2025) (13)1.4.6 The South Specialty Paper Status and Prospect (2013-2025) (14)1.4.7 The Midwest Specialty Paper Status and Prospect (2013-2025) (15)1.5 United States Market Size (Sales and Revenue) of Specialty Paper (2013-2025) (16)1.5.1 United States Specialty Paper Sales and Growth Rate (2013-2025) (16)1.5.2 United States Specialty Paper Revenue (Million USD) and Growth Rate(2013-2025) (17)2 United States Specialty Paper Market Competition by Players/Manufacturers (18)2.1 United States Specialty Paper Sales and Market Share of Key Players/Manufacturers(2013-2018) (18)2.2 United States Specialty Paper Revenue and Share by Players/Manufacturers (2013-2018) (21)2.3 United States Specialty Paper Average Price by Players/Manufacturers (2013-2018) (24)2.4 United States Specialty Paper Market Competitive Situation and Trends (26)2.4.1 United States Specialty Paper Market Concentration Rate (26)2.4.2 United States Specialty Paper Market Share of Top 3 and Top 5Players/Manufacturers in 2017 (26)2.5 United States Players/Manufacturers Specialty Paper Manufacturing Base Distribution,Sales Area (27)3 United States Specialty Paper Sales and Revenue by Regions (2013-2018) (29)3.1 United States Specialty Paper Sales and Market Share by Regions (2013-2018) (29)3.2 United States Specialty Paper Revenue (Million USD) and Market Share by Regions(2013-2018) (31)3.3 United States Specialty Paper Price by Regions (2013-2018) (33)4 United States Specialty Paper Sales and Revenue by Type/ Product Category (2013-2018) (34)4.1 United States Specialty Paper Sales and Market Share by Type/ Product Category(2013-2018) (34)4.2 United States Specialty Paper Revenue (Million USD) and Market Share by Type(2013-2018) (36)4.3 United States Specialty Paper Price (USD/MT) by Type (2013-2018) (37)4.4 United States Specialty Paper Sales Growth Rate by Type (2013-2018) (38)5 United States Specialty Paper Sales by Application (2013-2018) (39)5.1 United States Specialty Paper Sales and Market Share by Applications (2013-2018) (39)5.2 United States Specialty Paper Sales Growth Rate by Applications (2013-2018) (41)5.3 Market Drivers and Opportunities (41)6 United States Specialty Paper Players/Manufacturers Profiles and Sales Data (43)6.1 KapStone (43)6.1.1 Company Basic Information, Manufacturing Base and Competitors (43)6.1.2 Specialty Paper Product Description (44)6.1.3 KapStone Specialty Paper Sales (K MT), Revenue (Million USD), Price (USD/MT)and Gross Margin (2013-2018) (45)6.1.4 Main Business/Business Overview (46)6.2 Glatfelter (47)6.2.1 Company Basic Information, Manufacturing Base and Competitors (47)6.2.2 Specialty Paper Product Description (47)6.2.3 Glatfelter Specialty Paper Sales (K MT), Revenue (Million USD), Price (USD/MT)and Gross Margin (2013-2018) (48)6.2.4 Main Business/Business Overview (50)。

2018年国内外宏观经济形势回顾及2019年预判

2019 年第 1 期

09

E 独家观察 Exclusive Observation

预测范围

实际 2017 年

表 1 2018- 2019 年世界及主要经济体 GDP 增速预测

世界银行 (2019 年 1 月 )

IMF (2018 年 10 月 )

OECD (2018 年 11 月 )

2018 年

2019 年

9 世界 美国 欧元区 英国 日本 新兴经济体和发展中经济体

6

3

0

-3

-6

年份 图 1 世界 GDP 年度增速走势

澳、日也先后推出了减税计划,但规模相对较小, 对私人消费和企业投资的刺激作用有限。 1.1.2 贸易保护政策导致大部分经济体出口下滑

美国推行贸易保护主义,不断宣布对进口商 品加征关税,贸易紧张局势持续加剧,抑制了包 括美国自身在内的世界大部分主要经济体的商品 出口增速。

关键词:2019 年 世界经济 中国经济 经济政策

1 世界经济形势分析及预判 1.1 2018 年平稳增长,预计增速 3.1%,大体持平 于 2017 年

因主要经济体财政政策趋于宽松,世界经济 自 2013 年步入稳步复苏通道,2017 年出现强劲 复苏势头。2018 年初以来,美国贸易保护主义加 剧,中美贸易摩擦持续升级,中断了世界经济快 速复苏势头。第一、二、三季度世界 GDP 增速分 别为 3.1%,3.5% 和 2.6%,估计全年为 3.1%,大 体持平于 2017 年。

美国经济数据解释及公布时间资料

2018/10/19

美国经济数据解释及公布时间

二、国内生产总值(GDP):指某一国在一定时期其境内 生产的全部最终产品和服务的总值。反映一个国家总体经 济形势的好坏,与经济增长密切相关,被大多数西方经济 学家视为“最富有综合性的经济动态指标”。主要由消费、 私人投资、政府支出、净出口额四部分组成。数据稳定增 长,表明经济蓬勃发展,国民收入增加;反之,则利淡。 一般情况下,如果GDP连续两个季度下降,则被视为衰退。 此值。一般在每季度末的某日北京时间 21:30公布前一 个季度的终值。

2018/10/19

美国经济数据的解释补充

五. 净资本流入 :经济学上的资本净流入和外商投 资没有直接关系 ;由于各国经济发展水平和生产 成本不同以及利差的存在,资本为追逐利润而形 成了资本的国际流动,同时国内政治、经济风险 的存在也促使了国际资本的流动;在当今世界中, 国际资本流动成为非常引人注目的经济现象,对 全球经济的稳定和发展发挥着重要的影响。

2018/10/19

美国经济数据的解释补充

二. GDP:港台地区被称为国内生产毛额、本地生 产总值 ;GDP是宏观经济中最受关注的经济统计 数字,因为它被认为是衡量国民经济发展情况最 重要的一个指标 ;第一,国内生产总值是用最终 产品来计量的,即最终产品在该时期的最终出售 价值 ;第二,国内生产总值是一个市场价值的概 念;第三,国内生产总值一般仅指市场活动导致 的价值 ;第四,GDP是计算期内生产的最终产品 价值,因而是流量而不是存量 。

2018/10/19

美国经济数据的解释补充

六. 贸易赤字:国际贸易是指不同国家(和/或地区)之间的 商品和劳务的交换活动。国际贸易是商品和劳务的国际转 移。国际贸易也叫世界贸易。 国际贸易由进口贸易和出 口贸易两部分组成,故有时也称为进出口贸易。

2004-2018年美国消费指数月度数据

月份CPI指数(未经季调) 2004年1月185.22004年2月186.22004年3月187.42004年4月1882004年5月189.12004年6月189.72004年7月189.42004年8月189.52004年9月189.92004年10月190.92004年11月1912004年12月190.32005年1月190.72005年2月191.82005年3月193.32005年4月194.62005年5月194.42005年6月194.52005年7月195.42005年8月196.42005年9月198.82005年10月199.22005年11月197.62005年12月196.82006年1月198.32006年2月198.72006年3月199.82006年4月201.52006年5月202.52006年6月202.92006年7月203.52006年8月203.92006年9月202.92006年10月201.82006年11月201.52006年12月201.82007年1月202.416 2007年2月203.499 2007年3月205.352 2007年4月206.686 2007年5月207.949 2007年6月208.352 2007年7月208.299 2007年8月207.917 2007年9月208.492007年10月208.936 2007年11月210.177 2007年12月210.036 2008年1月211.082008年2月211.693 2008年3月213.5282008年9月218.783 2008年10月216.573 2008年11月212.425 2008年12月210.228 2009年1月211.143 2009年2月212.193 2009年3月212.709 2009年4月213.24 2009年5月213.856 2009年6月215.693 2009年7月215.351 2009年8月215.834 2009年9月215.969 2009年10月216.177 2009年11月216.33 2009年12月215.949 2010年1月216.687 2010年2月216.741 2010年3月217.631 2010年4月218.009 2010年5月218.178 2010年6月217.965 2010年7月218.011 2010年8月218.312 2010年9月218.439 2010年10月218.711 2010年11月218.803 2010年12月219.179 2011年1月220.223 2011年2月221.309 2011年3月223.467 2011年4月224.906 2011年5月225.964 2011年6月225.722 2011年7月225.922 2011年8月226.545 2011年9月226.889 2011年10月226.421 2011年11月226.23 2011年12月225.672 2012年1月226.665 2012年2月227.663 2012年3月229.392 2012年4月230.085 2012年5月229.815 2012年6月229.478 2012年7月229.104 2012年8月230.379 2012年9月231.4072013年3月232.773 2013年4月232.531 2013年5月232.945 2013年6月233.504 2013年7月233.596 2013年8月233.877 2013年9月234.149 2013年10月233.546 2013年11月233.069 2013年12月233.049 2014年1月233.916 2014年2月234.781 2014年3月236.293 2014年4月237.072 2014年5月237.9 2014年6月238.343 2014年7月238.25 2014年8月237.852 2014年9月238.031 2014年10月237.433 2014年11月236.151 2014年12月234.812 2015年1月233.707 2015年2月234.722 2015年3月236.119 2015年4月236.599 2015年5月237.805 2015年6月237.684 2015年7月238.053 2015年8月238.028 2015年9月237.506 2015年10月237.781 2015年11月238.016 2015年12月237.817 2016年1月237.833 2016年2月237.469 2016年3月238.038 2016年4月238.827 2016年5月239.464 2016年6月240.167 2016年7月240.15 2016年8月240.602 2016年9月241.051 2016年10月241.691 2016年11月242.029 2016年12月242.772 2017年1月243.78 2017年2月243.961 2017年3月243.7492017年9月246.418 2017年10月246.587 2017年11月247.332 2017年12月247.9 2018年1月248.884 2018年2月249.369 2018年3月249.498 2018年4月249.956 2018年5月250.646 2018年6月251.134 2018年7月251.597 2018年8月251.879 2018年9月252.01 2018年10月252.794 2018年11月252.76 2018年12月252.723。

美国人财务困境分析报告(3篇)

第1篇一、引言近年来,美国经济持续增长,但与此同时,许多美国人的财务状况却面临着严重的困境。

财务困境不仅影响个人的生活质量,还可能引发一系列社会问题。

本报告旨在分析美国人财务困境的现状、原因以及应对策略,以期为相关决策者提供参考。

二、美国人财务困境的现状1. 债务负担加重近年来,美国人的债务负担逐年加重。

根据美国消费者金融保护局(CFPB)的数据,2019年美国人的总债务达到14.15万亿美元,其中信用卡债务为1.02万亿美元,学生贷款债务为1.6万亿美元,汽车贷款债务为1.35万亿美元,房屋贷款债务为10.7万亿美元。

2. 收入不稳定美国人的收入不稳定现象日益严重。

根据美国劳工统计局(Bureau of Labor Statistics)的数据,2019年美国失业率为3.6%,尽管处于较低水平,但仍有大量人群面临就业困难。

此外,许多美国人的工作时间不稳定,加班工资较低,导致收入难以满足生活需求。

3. 医疗费用负担美国医疗费用高昂,许多美国人因医疗费用而陷入财务困境。

据美国凯撒家庭基金会(Kaiser Family Foundation)的报告,2019年美国人均医疗费用为1.3万美元,其中个人自付费用占医疗费用的29%。

4. 退休储蓄不足随着美国人口老龄化加剧,退休储蓄不足成为一大问题。

根据美国个人退休账户协会(National Retirement Security Council)的报告,2019年美国有超过40%的退休人员面临财务困难。

三、美国人财务困境的原因1. 经济全球化带来的冲击经济全球化使得美国国内就业市场受到冲击,许多传统产业和岗位被外包到国外,导致美国工人收入下降,生活成本上升。

2. 金融体系的漏洞美国金融体系存在漏洞,导致金融风险在金融市场中不断累积。

金融危机爆发后,许多美国人因投资失利而陷入财务困境。

3. 社会保障体系不完善美国社会保障体系不完善,老年人、残疾人等弱势群体在面临财务困境时缺乏有力保障。

Fluent:2018年消费者概览

Fluent:2018年消费者概览

199IT原创编译

Fluent发布了“2018年消费者概览”报告。

美国人对2018年的个人前景持乐观态度,但他们认为这个国家面临着一些关键问题。

消费者最担心的是恐怖主义,其次是医疗改革和经济。

85%的美国人认为自己是幸福的或非常幸福。

65%的美国人认为当前的医疗系统非常好,能满足他们的医疗需求。

尽管股市飙升,但是一半以上的美国人担心经济走向了错误的方向,特别是女性、年轻人和低收入家庭。

57%的美国人认为个人经济状况正朝着正确的方向发展。

千禧一代和Z世代更担心国家经济和枪支暴力。

56%的美国人认为国家经济正朝着错的方向发展。

受这种担忧影响,美国人在花钱方面将更小心谨慎。

从整体来看,75%的美国人用“稍微谨慎”来描述他们的消费习惯,只有7%的受访者随意花钱。

但是千禧一代和Z世代则对自己的经济形势更加自信、更愿意随意花钱。

45%的美国人相信他们的经济状况将有所改变。

那些有工作的美国人对他们的职业感到满意(87%),而那些找工作的人则对2018年找到工作的可能性表示乐观。

74%的求职者认为求职前景是乐观的。

Fluent还调查了2018年美国人将广泛采用哪些技术,通用互联网排在首位,42%的美国人希望2018年Wi-Fi的覆盖范围更广。

其次是智能家居系统(30%)、自动驾驶汽车(22%)、无人机快递(22%)和可再生能源电力(19%)。

。

美国2018Q2经济情况分析及政策展望

美国2018Q2经济情况分析及政策展望王健Dr.Jian Wang, 郭晓声Erin Guo, 郭晓敏Melody Guo, 魏昕宇Xinyu Wei总结美国经济在二季度持续稳步增强。

通胀水平也有了明显改善,向美联储的目标进一步靠近。

预计美联储在6月FOMC会议上会加息25个基准点,并会给出进一步加息的信号。

受美国通胀预期上升影响,长期国债利率在第二季度出现了明显的攀升。

虽然长期国债利率在6月有所回调,但随着通胀预期的上行,长期利率在下半年预计会持续原有的上升趋势。

随着实体经济的扩张和通胀预期上行,美联储预计下半年会采用更快速的加息路线,2018年加息次数预计从原来的3次提高到4次。

受美元利率上行影响,存在双赤字(贸易赤字和财政赤字)的新兴市场已经开始出现金融市场动荡。

防范国际金融风险将是这些新兴市场下半年的主要挑战。

实体经济美国一季度GDP增速同比继续稳步扩张,消费者信心持续改善。

2018年第一季度实际国内生产总值增长率二次估计为2.2%(图1),自2017年第四季度增速下降后进一步下滑,下降0.7个百分点,但与去年同期相比有明显改善,实际GDP增速同比上升1个百分点。

和首次估计相比,2018第一季度GDP增速二次预估下调0.1个百分点,主要反映了个人消费支出、私人存货投资、住宅投资等估计下调。

非住宅投资在2018Q1成为拉动GDP增长的主要因素,上推GDP1.1个百分点,并有持续扩张趋势。

其他私人投资部门中,住宅投资增长率下滑幅度较大,而私人存货投资增长率在2018年第一季度扭负为正,某种程度上抵消了住宅投资的负影响,投资部门整体呈上扬趋势。

作为GDP月度数据替代的零售业销售额在2018年4月达4391.4亿,环比上升0.36%,较去年同期上涨4.81%,第二季度开端实体经济已经奠定了强劲的涨势。

第一季度消费对实际GDP增长贡献率下滑2.1个百分点至0.7%,实际个人消费支出增速较2017Q4有所放缓,与2017Q4密歇根消费者信心指数下滑走势相一致,但2018Q1实际PCE同比增长2.6%,这一结果说明季节性因素是2018年第一季度消费增速减慢的主要原因,未来消费走势依旧增强。

2023年10月纽约联储消费者调查报告英文版

2023年10月纽约联储消费者调查报告英文版全文共3篇示例,供读者参考篇1Consumer Confidence Remains Steady in October 2023: New York Fed SurveyThe latest consumer survey conducted by the Federal Reserve Bank of New York in October 2023 indicates that consumer confidence remains steady despite ongoing economic uncertainties. The survey, which gathers data on consumer attitudes and expectations regarding the economy, employment, and personal finances, provides valuable insights into consumer sentiment and future spending behavior.Overall, the survey results suggest that consumers are cautiously optimistic about the economic outlook, with the Consumer Confidence Index holding steady at 96.7 in October, unchanged from the previous month. This stability in consumer confidence reflects a combination of positive and negative factors influencing consumer sentiment.On the positive side, respondents expressed confidence in the labor market, with a significant majority (62%) reporting thatjobs are plentiful. This reflects the strong job market conditions, with unemployment at a historic low and job creation continuing to outpace expectations. Additionally, respondents indicated a slight improvement in their own financial situations, with 45% reporting that their income had increased over the past year.However, there are also factors contributing to concerns among consumers. Inflation remains a key issue, with 68% of respondents reporting that prices have increased significantly over the past year. Rising prices for everyday goods and services, such as food, gasoline, and housing, are putting pressure on household budgets and eroding purchasing power.Despite these challenges, consumers are generally optimistic about the future, with 52% expecting their financial situation to improve over the next year. This positive outlook is supported by expectations of continued job growth and wage increases, which should help offset the impact of inflation on household budgets.The survey also highlighted differences in consumer sentiment across different demographic groups. Younger consumers, aged 18-34, were more optimistic about the economy and their personal finances compared to older age groups. This may be due to their greater flexibility in the labormarket and higher exposure to technology-driven industries, which have been growing rapidly.In terms of regional differences, consumers in urban areas tended to be more optimistic than those in rural areas. This may reflect the stronger job market conditions and higher levels of economic activity in urban centers, compared to more rural and economically disadvantaged areas.Looking ahead, the survey results suggest that consumer spending is likely to remain resilient in the coming months, supported by strong job market conditions and improving personal finances. However, the impact of inflation on purchasing power remains a key concern, and policymakers will need to closely monitor price developments to ensure that inflationary pressures do not undermine consumer confidence.Overall, the October 2023 consumer survey conducted by the New York Fed provides valuable insights into consumer sentiment and expectations, highlighting the complex interplay of factors shaping consumer confidence in the current economic environment. By monitoring consumer attitudes and behaviors, policymakers can make informed decisions to support economic growth and stability in the months ahead.篇2Federal Reserve Bank of New York Consumer Survey ReportOctober 2023IntroductionThe Federal Reserve Bank of New York conducts a monthly consumer survey to gauge the sentiment and outlook of consumers in the New York region. This report provides an overview of the key findings from the October 2023 survey.Consumer SentimentConsumer sentiment in October remained relatively stable compared to the previous month. The overall sentiment index stood at 85.6, showing a slight increase from September. Consumers expressed cautious optimism about the economy, with many citing improvements in the job market and overall economic conditions.Income ExpectationsIncome expectations among consumers also improved in October. The survey revealed that a majority of respondents expected their incomes to increase in the next 12 months. Thispositive outlook is likely driven by the continued strength in the labor market and rising wages.Spending IntentionsConsumers' spending intentions showed a notable increase in October. The survey found that a larger proportion of respondents planned to make major purchases in the coming months, such as homes, cars, and appliances. This increase in spending intentions bodes well for economic growth in the region.Inflation ConcernsInflation remained a top concern for consumers in October. The survey showed that a majority of respondents were worried about rising prices and their impact on their purchasing power. However, many consumers also expressed confidence in the Federal Reserve's ability to control inflation and keep it at a manageable level.Housing MarketThe housing market continued to be a bright spot in the economy, with strong demand for homes driving up prices. The survey found that a significant number of respondents were considering buying a home in the near future, citing lowmortgage rates and attractive property prices as key factors influencing their decision.Employment OutlookThe labor market showed signs of improvement in October, with job creation picking up pace across various industries. The survey revealed that a growing number of respondents were optimistic about their job prospects, with many expecting to see wage increases and more job opportunities in the coming months.ConclusionOverall, the October 2023 consumer survey paints a positive picture of consumer sentiment and economic outlook in the New York region. Despite lingering concerns about inflation, consumers are optimistic about the future, with strong income expectations and increased spending intentions driving economic growth. The Federal Reserve Bank of New York will continue to monitor consumer sentiment closely to inform its policy decisions and support the region's economic recovery.篇3New York Fed Consumer Survey Report – October 2023IntroductionThe New York Federal Reserve Bank conducts a monthly consumer survey to gauge the sentiment and behavior of American consumers. The survey covers a wide range of topics including personal finances, spending habits, economic outlook, and job market perceptions. The data collected from the survey provides valuable insights into consumer confidence, which is a key driver of economic growth.Key Findings1. Consumer Confidence: In October 2023, consumer confidence remained strong, with the index tracking at 110. This indicates that the majority of consumers are optimistic about the economy and their own financial situations.2. Spending Habits: The survey found that consumers are continuing to increase their spending on goods and services. In particular, spending on non-essential items such as travel, entertainment, and dining out has shown a significant uptick.3. Personal Finances: Despite the overall positive sentiment, there are concerns about personal finances. Many consumers reported feeling increased financial pressure due to rising costs of living, such as housing, healthcare, and education.4. Job Market: The job market continues to be a major focus for consumers. While there is optimism about the availability of jobs, concerns remain regarding job security and wage growth.5. Inflation Expectations: Inflation expectations have risen, with consumers anticipating prices to continue to increase in the coming months. This has led to a more cautious approach to spending and saving.6. Economic Outlook: Overall, consumers are divided on the future direction of the economy. While some are optimistic about continued growth, others are concerned about potential economic challenges, such as trade tensions and geopolitical risks.ImplicationsThe findings from the October 2023 consumer survey highlight the complex dynamics of consumer behavior in the current economic environment. While consumer confidence remains high, there are underlying concerns about personal finances and inflation that could impact spending patterns in the future. Understanding these nuances is crucial for policymakers, businesses, and investors as they make decisions that affect the overall health of the economy.ConclusionThe October 2023 New York Fed Consumer Survey provides valuable insights into the sentiment and behavior of American consumers. While consumer confidence remains strong, underlying concerns about personal finances, inflation, and the job market indicate a complex economic landscape. By monitoring these trends and addressing consumer concerns, policymakers can help ensure the continued prosperity of the economy.。

【最新2018】希望对方配合的信函-优秀word范文 (10页)

(三)另外,从内容和用途上,还可以分为商洽事宜函,通知事宜函,催办事宜函,邀请函、请示答复事宜函,转办函,催办函,报送材料函等等。

五、函的结构、内容和写法

由于函的类别较多,从制作格式到内容表述均有一定灵活机动性。主要介绍规范性公函的结构、内容和写法。

为避免影响设计工期,和促进项目的顺利进行,在此恳请贵司能予以相应理解,尽快安排支付定金(RMB 万元)。

再次感谢贵司的信任和理解!顺祝商祺!

××××设计有限公司

二〇一×年×月×日

篇三:工作、询问和答复问题,或者向有关主管部门请求批准事项时所使用的公文。 函是应用写作实践中的一种常用文体。

(三)结尾。一般用礼貌性语言向对方提出希望。或请对方协助解决某一问题,或请对方及时复函,或请对方提出意见或请主管部门批准等。

(四)结语。通常应根据函询、函告、函商或函复的事项,选择运用不同的结束语。如“特此函询(商)”、“请即复函”、“特此函告”、“特此函复”等。有的函也可以不用结束语,如属便函,可以像普通信件一样,使用“此致”、“敬礼”。

(五)结尾落款。一般包括署名和成文时间两项内容。

署名机关单位名称,写明成文时间年、月、日;并加盖公章。

五、撰写函件应注意的问题

函的写作,首先要注意行文简洁明确,用语把握分寸。无论是平行机关或者是不相隶属的行文,都要注意语气平和有礼,不要倚势压人或强人所难,也不必逢迎恭维、曲意客套。至于复函,则要注意行文的针对性,答复的明确性。 其次,函也有时效性的问题,特别是复函更应该迅速、及时。像对待其他公文一样,及时处理函件,以保证公务等活动的正常进行。

为提升公司管理质量,给业主提供更好的质量服务,我司一直在实行ISO9000管理体系,其中项目管理规定:签订合同和收到定金后,方能启动项目。而在本项目中,为表合作诚意和考虑双方友好关系,通过特批流程同意在未签订合同前,已启动项目工作。虽然目前合同已签订,但定金尚未支付。因此,如果在×月×日前仍未收到定金,我司会按合同有关规定,延期提交设计成果或考虑暂停本项目的设计工作。待收到定金后,双方再商议重新启动的事宜。

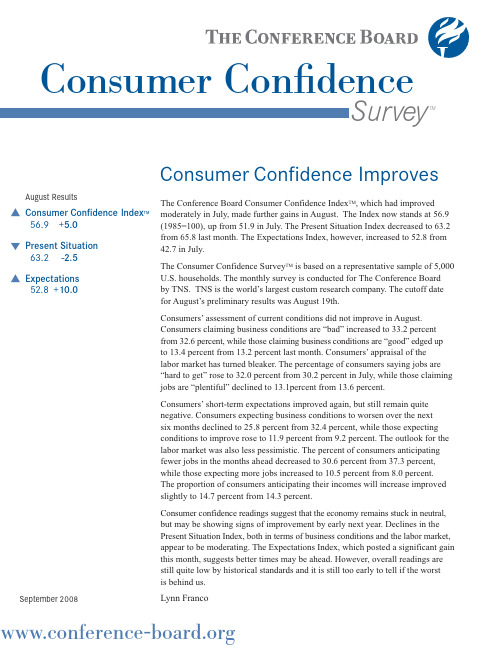

美国消费者信心指数

The Conference Board Consumer Confidence Index TM , which had improved moderately in July, made further gains in August. The Index now stands at 56.9(1985=100), up from 51.9 in July. The Present Situation Index decreased to 63.2from 65.8 last month. The Expectations Index, however, increased to 52.8 from 42.7 in July.The Consumer Confidence Survey TM is based on a representative sample of 5,000U.S. households. The monthly survey is conducted for The Conference Board by TNS. TNS is the world’s largest custom research company. The cutoff date for August’s preliminary results was August 19th.Consumers’assessment of current conditions did not improve in August.Consumers claiming business conditions are “bad” increased to 33.2 percent from 32.6 percent, while those claiming business conditions are “good” edged up to 13.4 percent from 13.2 percent last month. Consumers’appraisal of the labor market has turned bleaker. The percentage of consumers saying jobs are “hard to get” rose to 32.0 percent from 30.2 percent in July, while those claiming jobs are “plentiful” declined to 13.1percent from 13.6 percent.Consumers’short-term expectations improved again, but still remain quite negative. Consumers expecting business conditions to worsen over the next six months declined to 25.8 percent from 32.4 percent, while those expecting conditions to improve rose to 11.9 percent from 9.2 percent. The outlook for the labor market was also less pessimistic. The percent of consumers anticipating fewer jobs in the months ahead decreased to 30.6 percent from 37.3 percent,while those expecting more jobs increased to 10.5 percent from 8.0 percent. The proportion of consumers anticipating their incomes will increase improved slightly to 14.7 percent from 14.3 percent.Consumer confidence readings suggest that the economy remains stuck in neutral,but may be showing signs of improvement by early next year. Declines in the Present Situation Index, both in terms of business conditions and the labor market,appear to be moderating. The Expectations Index, which posted a significant gain this month, suggests better times may be ahead. However, overall readings are still quite low by historical standards and it is still too early to tell if the worst is behind us.Lynn FrancoSeptember 2008August ResultsL Consumer Confidence Index TM56.9+5.0M Present Situation63.2-2.5L Expectations52.8+10.0Consumer Con fidenceSurveyTMConsumer Confidence Improves20072008 All series seasonally adjusted Aug.Sep. Oct. Nov. Dec.Jan.Feb. Mar.Apr.May June July(r) Aug.(p)C o m p o s i t e S e r i e s:I n d e x N u m b e r s,1985=100C o n s u m e r C o n f i d e n c e I n d e x T M105.699.595.287.890.687.376.465.962.858.151.051.956.9P r e s e n t S i t u a t i o n130.1121.2118.0115.7112.9114.3104.090.681.974.265.465.863.2E x p e c t a t i o n s89.285.080.069.175.869.358.049.450.047.341.442.752.8A p p r a i s a l o f P r e s e n t S i t u a t i o n:P e r c e n tB u s i n e s sC o n d i t i o n sGood26.225.723.222.521.220.619.115.615.413.011.513.213.4 Bad16.317.816.618.918.820.121.325.526.529.731.932.633.2 Normal57.556.560.258.660.059.359.658.958.157.356.654.253.4E m p l o y m e n tJobs plentiful27.525.624.123.323.623.821.519.217.116.114.113.613.1 Jobs not so plentiful52.852.053.155.353.755.655.156.355.055.656.256.254.9 Jobs hard to get19.722.422.821.422.720.623.424.527.928.329.730.232.0E x p e c t a t i o n s f o r S i x M o n t h s H e n c e:P e r c e n tB u s i n e s sC o n d i t i o n sBetter15.015.714.012.413.811.59.78.610.110.68.59.211.9 Worse10.211.913.916.614.116.321.626.027.432.933.532.425.8 Same74.872.472.171.072.172.268.765.462.556.558.058.462.3E m p l o y m e n tMore jobs12.913.413.310.610.910.58.98.08.89.08.08.010.5 Fewer jobs15.218.720.222.819.921.928.029.332.932.335.737.330.6 Same71.967.966.566.669.267.663.162.758.358.756.354.758.9I n c o m eIncrease19.820.019.919.420.218.118.016.115.514.113.114.314.7 Decrease8.58.89.110.910.49.810.613.713.514.615.915.916.1 Same71.771.271.069.769.472.171.470.271.071.371.069.869.2P l a n s t o B u y W i t h i n S i x M o n t h s:P e r c e n tA u t o m o b i l eYes 6.3 5.3 6.6 4.8 6.3 6.7 5.4 5.4 5.8 5.1 5.1 5.0 5.3 New 3.2 2.8 3.4 2.1 2.8 3.0 2.2 2.6 2.6 2.2 2.2 2.3 2.5 Used 2.5 1.8 2.3 1.8 2.4 3.2 2.2 2.2 2.4 2.1 2.3 2.1 2.3 Uncertain0.00.70.90.9 1.10.5 1.00.60.80.80.60.60.0H o m eYes 3.6 3.0 2.7 2.6 2.5 2.5 2.9 3.4 2.5 2.4 2.4 2.8 3.3 New 1.00.80.70.70.50.70.70.90.70.50.50.50.7 Lived in 1.8 1.3 1.2 1.2 1.3 1.2 1.5 1.7 1.3 1.3 1.4 1.8 1.6 Uncertain0.80.90.80.70.70.60.70.80.50.60.50.5 1.0 M a j o r a p p l i a n c e sTotal plans29.729.826.330.028.130.632.130.132.133.628.328.631.6 Refrigerator 4.1 4.6 4.2 4.0 3.9 5.0 4.9 4.2 4.1 4.6 3.8 4.0 4.0 Washing machine 3.7 3.1 3.5 3.9 3.4 3.9 3.3 3.6 3.6 3.7 3.4 3.7 3.7 TV Set8.28.98.09.28.99.711.011.111.412.610.010.311.2 Vacuum Cleaner 5.8 5.6 3.7 5.0 4.7 4.1 4.4 4.8 4.7 5.0 3.6 3.9 4.9 Range 2.1 3.0 3.1 2.3 2.4 2.8 3.4 2.3 2.8 2.9 2.1 2.2 2.6 Clothes dryer 3.6 2.6 2.4 3.6 3.0 3.4 3.1 3.1 3.8 3.3 3.4 2.9 3.5 Air conditioner 2.2 2.0 1.4 2.0 1.8 1.7 2.0 1.0 1.7 1.5 2.0 1.6 1.7 Carpet 4.5 4.7 4.7 3.4 4.1 5.0 4.4 3.9 4.0 4.5 3.6 4.0 4.0V a c a t i o n I n t e n d e d W i t h i n S i x M o n t h s:P e r c e n tV a c a t i o n I n t e n d e d41.745.844.543.039.636.237.4D e s t i n a t i o nU.S.35.137.435.635.733.430.130.9 Foreign country8.39.39.79.68.27.78.1 M e a n s o f T r a v e lAutomobile21.722.822.322.419.919.119.2 Airplane18.918.918.419.320.117.816.1 Other 3.2 4.3 4.7 3.9 3.1 2.8 3.9 (p) - preliminary (r) - revisedC o n s u m e r C o n f i d e n c e a n d B u y i n g P l a n sB a s e d o n s u r v e y s c o n d u c t e d b y T N SPercentage of households = 100%A monthly report fromThe Consumer Research CenterCopyright © 2008by The Conference Board,Inc.All rights reserved.ISSN 1046-1876The Conference Board,845Third Avenue,New York,NY10022-6679/ 2127590900The Conference Board Europe,Chaussée de La Hulpe 130,Box 11,B-1000 Brussels,Belgium 3226755405The Conference Board of Canada,255Smyth Road,Ottawa,Ontario,K1H-8M7,Canada 613 5263280B u s i n e s s E m p l o y m e n t I n c o m eThe Conference Board and the torch logo are registered trademarks of The Conference Board,Inc.The Conference Board Consumer Confidence Survey TM September20083 mos.20072008PercentAll series seasonally adjustedAug.Sep.Oct.Nov.Dec.Jan.Feb.Mar.Apr.MayJuneJuly(r)Aug.(p)Change*C o n s u m e r C o n f i d e n c e I n d e xT M, 1985 = 100A g e o f H o u s e h o l d H e a d Under 35104.4115.1110.299.0100.998.687.782.979.268.467.568.574.0-8.935-54107.393.091.289.190.883.977.268.765.260.449.354.458.0-16.855 and over 102.698.892.581.485.284.668.454.350.749.844.642.849.3-11.6H o u s e h o l d I n c o m e Under $15,00072.171.669.062.469.655.858.050.548.745.032.631.947.1-22.6$15,000-24,99985.682.475.469.773.279.250.652.346.145.239.936.137.7-20.8$25,000-34,99992.288.194.079.975.073.168.651.151.847.431.248.743.2-18.1$35,000-49,999106.599.694.885.491.282.080.556.559.454.041.453.554.5-12.0*Percent Change: Average of last three months shown as compared with preceding three months. Age and Income data have been adjusted for seasonal variations.Not Seasonally 20072008AdjustedAug.Sep.Oct.Nov.Dec.Jan.Feb.Mar.Apr.MayJuneJuly(r)Aug.(p)E x p e c t a t i o n s f o r T w e l v e M o n t h s H e n c e : P e r c e n tI n f l a t i o n R a t e Average 5.1 5.0 5.1 5.7 5.5 5.3 5.4 6.1 6.87.77.77.5 6.7I n t e r e s t R a t e s Higher 56.751.244.743.844.143.631.935.437.338.443.346.645.5Same 31.629.833.333.130.930.431.127.028.331.830.031.031.9Lower 11.719.022.023.125.026.037.037.634.429.826.722.422.6S t o c k P r i c e s Increase 30.729.033.926.729.625.519.918.121.824.421.718.222.3Same 40.141.442.340.839.140.037.133.032.530.830.126.933.2Decrease29.229.623.832.531.334.543.048.945.744.848.254.944.5S t o c k P r i c e sI n t e r e s t R a t e s I n f l a t i o n The Conference Board Consumer Confidence Survey TM September 2008The Conference Board Consumer Confidence Survey TM September2008Consumer Confidence by RegionSeasonally unadjusted3-MONTH AVG.Index numbers: 20072008June,July,Aug. Percent U.S. Average, 1985 = 100July Aug.Sep.Oct.Nov.Dec.Jan.Feb.Mar.Apr.May June July(r)Aug.(p)20072008 ChangeN e w E n g l a n dConsumer Confidence Index TM105.9105.484.162.073.071.970.557.557.843.749.726.651.439.4102.639.1-61.9 Present Situation130.3128.0111.676.596.799.593.183.175.852.556.836.264.433.2126.744.6-64.8 Expectations89.790.465.852.457.253.555.440.445.737.845.020.142.843.686.635.5-59.0M i d d l e A t l a n t i cConsumer Confidence Index TM99.183.893.786.878.872.572.259.651.949.745.440.933.641.089.038.5-56.8 Present Situation126.0116.8118.7116.6107.796.286.376.868.358.153.949.240.246.3120.045.2-62.3 Expectations81.161.877.067.059.556.862.948.141.044.139.735.429.237.568.434.0-50.3E a s t N o r t h C e n t r a lConsumer Confidence Index TM75.870.262.759.957.965.859.146.038.241.434.728.328.838.073.331.7-56.8 Present Situation82.476.165.662.765.773.164.840.137.139.734.127.932.629.680.330.0-62.6 Expectations71.466.360.858.052.760.955.350.038.942.535.128.626.343.668.732.8-52.2W e s t N o r t h C e n t r a lConsumer Confidence Index TM104.8116.4112.292.893.9108.096.276.573.079.555.164.058.559.3108.860.6-44.3 Present Situation136.4144.0147.6130.5127.3137.1114.3104.598.1100.875.5101.482.380.2140.487.9-37.4 Expectations83.798.088.667.771.788.684.257.856.365.341.539.042.745.487.842.4-51.7S o u t h A t l a n t i cConsumer Confidence Index TM121.9114.1109.2103.197.885.692.487.367.964.358.551.353.455.8115.853.5-53.8 Present Situation152.9140.8136.5130.1131.2111.1113.2116.188.783.974.763.464.761.9145.063.3-56.3 Expectations101.396.391.085.175.668.678.668.054.151.347.843.345.951.896.347.0-51.2E a s t S o u t h C e n t r a lConsumer Confidence Index TM116.1101.6120.8106.481.297.2100.787.268.577.063.456.857.563.6108.259.3-45.2 Present Situation140.5124.2141.2122.798.2117.2116.2103.597.495.675.075.771.778.0129.475.1-42.0 Expectations99.986.6107.295.669.884.090.476.349.364.555.744.348.154.194.048.8-48.1W e s t S o u t h C e n t r a lConsumer Confidence Index TM131.5118.9121.0127.7122.6119.5125.3106.397.591.382.682.880.092.8125.285.2-31.9 Present Situation166.3152.0155.3159.0167.1160.2162.8137.0132.9131.1119.7125.0124.8123.7155.9124.5-20.2 Expectations108.396.998.2106.892.992.4100.385.873.964.758.054.650.272.2104.759.0-43.6M o u n t a i nConsumer Confidence Index TM137.6129.9119.9140.1119.6114.0122.8102.197.567.574.969.269.080.8132.373.0-44.8 Present Situation174.2165.8163.0181.4156.1159.4171.5142.5137.496.2102.7102.996.392.5168.497.2-42.3 Expectations113.2106.091.3112.695.383.790.375.170.948.456.446.850.973.1108.356.9-47.5P a c i f i cConsumer Confidence Index TM111.3115.6107.3120.1100.098.680.784.565.958.157.151.648.448.6114.949.5-56.9 Present Situation151.8150.0140.7156.8146.6135.1117.6110.185.375.373.862.954.953.8151.957.2-62.4 Expectations84.292.785.095.669.074.356.167.452.946.745.944.144.145.290.244.4-50.8*Percent Change: Average of last three months shown as compared with the same period a year ago. Regional data are not adjusted for seasonal variation.。

2018美国车市常态下的希望与挑战

2018美国车市常态下的希望与挑战2018年的美国市场在寻常之中包含了些许意外,对于本土汽车制造商而言,压力不仅来源于本地市场,还有中国市场。

与多年维持上涨而2018年出现下跌的中国市场不同,美国市场自2016年达到1755万辆的“天花板”以来一直维持在涨跌波动都很细微的平稳状态。

刚刚出炉的2018年销售数据显示,全年美国市场实现销量1733万辆,同比微增0.6%,好于此前预测。

即使数据高于预期,但展望未来时却更加谨慎。

全美汽车经销商协会公布的年度预测报告中提到,2019年汽车制造商的乘用车销售量预计将为1680万辆,这会是自2014年首次年销量低于1700万辆。

美联储加息导致新车融资的平均利率已经上升了60到70个基点,加上轿车市场正遇上转型期,短暂的市场表现或许难以抵消美国乘用车市场需求下滑的影响。

好消息是,2018年的减税政策、2019年美联储加息或将放缓的信号以及就业和消费情况较为稳定将对汽车市场产生一定利好;坏消息是,作为美国经济晴雨表的股市出现大幅下跌,市场信心不足,美国长端国债和短端国债呈现“死亡交叉”、中美贸易战还未有定论等成为经济的不确定性因素。

未来,压力大于希望,2019年,1700万辆的年销量是美国汽车市场要守护的一个关口。

心情各不相同总体趋势还算平稳,但是汽车制造商们的日子并不好过。

从全年销量来看,除了菲亚特克莱斯勒外,榜单前几位的企业几乎都出现了不同程度的下跌。

有人会说,没有弱势的市场,只有弱势的车型。

在美国轿车领域,这一句话并不奏效。

榜单前十名的轿车车型都出现两位数跌幅,受此影响,除了专注于SUV、皮卡领域的品牌,其他都出现不同程度的下跌。

2018年全年,美国轻型卡车销量同比上升7.7%,创纪录的达到1197万辆,为一百多年来最高水平。

轿车市场却不容乐观,一方面是销量连续五年出现下跌,同比下降13%至536万辆,接近1958年的最低水平(460万辆);另一方面,轻卡的上涨与轿车的下跌对比,造成了2018年轿车在轻型车市场中的占比仅为31%。

2018消费者价格涨幅趋势英语作文

2018消费者价格涨幅趋势英语作文In 2018, the trend of consumer price increases has been a topic of great concern. From food to housing, the cost of living has been on the rise, affecting people's daily livesin various ways.First of all, the prices of daily necessities such as rice, vegetables, and meat have all seen significant increases. This means that consumers are spending more money on basic food items, leaving less for other expenses. As a result, many people are feeling the pinch on their wallets and have to carefully budget their spending.Secondly, the prices of services such as transportation and healthcare have also gone up. This puts additional pressure on consumers, especially those with lower incomes. People are now having to think twice before taking a taxi or visiting the doctor, as these costs can add up quickly.Furthermore, the housing market has experienced a boom in prices, making it more difficult for people to afford a home. Rent prices have skyrocketed in many cities, forcing some individuals to live in cramped conditions or move to cheaper areas far from their workplaces.In conclusion, the consumer price increase trend in 2018 has had a significant impact on people's lives. It is important for both consumers and policymakers to find ways to address these rising costs and ensure that everyone has access to affordable goods and services. Only by working together can we tackle the challenges posed by inflation and create a more prosperous society for all.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Up/down arrows indicate statistically significant difference (95% confidence)

Base: Total Market - 2015 (n=1285), 2016 (n=1250), 2017 (n=1270)

5

Hispanics were the most likely to say their income improved in 2017, but the 35% represented a decrease from 2016.

44%

38% 35% 33% 32% 32%

41%

41%

17%

20%

18%

15%

2017

Year Results

Improved

Stayed the same 32% 35% 34% 41% 41% 41% 36% 38% 50% 45% 19% 19%

Worsened 18% 22% 19% 17% 14% 16%

Conduct online, in-person and telephone research.

3

Our Services

QUANTIT A TIVE QUALITATIVE MIXED MODE

ONLINE MARKET RESEARCH COMMUNITIES

CONCEPTAND COPY TESTING

500

Hispanics

257

Non-Hisp

258

AsianAmericans

1,270

Total

2

Who We Are

An authority on creating and managing research products that help clients gather insights about rapidly changing consumer segments.

Research experience specifically in the Hispanic, African American, Asian and T otal markets. Experience in hard-to reach demographic sub-groups.

Only full-service market research company that owns & operates an inhouse Hispanic panel. Servicing Fortune 500 clients, ad agencies, nonprofits and other market research companies.

Recent Trends in Household Income

Total Market

39% 33% 33%

42% 38%

41%

22%

20%

19%

Improved

Stayed the same

Worsened

2015

2016

2017

Thinking of all of the sources of income that contribute to your household, compared to this same time last year would you say your household financial situation has:

Methodology

Survey Method › Online via XX Research’s

Omnibus Study

Regional Coverage

› National

Screening Criteria › 18-64 years of age

Field Timing › December,2017 Base Sizes

Total Market Consumer Sentiment with Comparisons to Previous Years

2018 Report

What isit?

XX is a national survey that examines the consumer sentiment of Americans. The study looks at the market as a whole and by key race/ethnic segments. Results from 2017 are compared to 2016 and 2015.

ADVERTISING EFFECTIVENESS

ONLINE PANEL BUILDING

ONLINE PANEL

INTERCEPTS

PHONE

Contact Us

info@ 818843-0220

WEBSITE USABILITY STUDIES

OMNIBUS SURVEYS

ATTITUDES & USAGE

BRAND TRACKING

PRODUCT TESTING

ONLINE & OFFLINE QUALIT A TIVE

4

Most Americans’ household income stayed the same in2017.

• Slightly more consumers report no major shifts in income this year over last, but fewer saw a significant improvement in income in 2017 over 2016.

• 2-in-10 Non-Hispanic Whites said their situation worsened. This was the highest of the race/ethnicsegments.

Recent Trends in Household Income

By Race/Ethnic Segment

2016 2015

43% 35%

39% 33%