FRM一级练习题(1)

frm一级题库 2023

frm一级题库2023

一、单项选择题

1.在2023年FRM考试中,一级考试的合格分数线是多少?

2. A. 400

3. B. 500

4. C. 600

5. D. 700

6.FRM一级考试中,风险管理基础占比多少?

7. A. 15%

8. B. 25%

9. C. 35%

10. D. 45%

11.FRM一级考试中,数量分析占比多少?

12. A. 10%

13. B. 15%

14. C. 20%

15. D. 25%

16.FRM一级考试中,金融市场与产品占比多少?

17. A. 20%

18. B. 25%

19. C. 30%

20. D. 35%

21.FRM一级考试中,估值与风险建模占比多少?

22. A. 15%

23. B. 20%

24. C. 25%

25. D. 30%

二、多项选择题

1.下列哪些科目是FRM一级考试的重要内容?

2. A. 风险管理基础

3. B. 数量分析

4. C. 公司金融

5. D. 金融市场与产品

6. E. 估值与风险建模

7.在FRM一级考试中,下列哪些知识点是考生需要掌握的?

8. A. 市场风险的管理方法

9. B. 信用风险的计算方式

10. C. 操作风险的识别与评估

11. D. 企业价值的评估方法

12. E. 对冲策略的有效性分析

三、简答题

1.请简述FRM一级考试的主要目的。

2.在FRM一级考试中,考生应具备哪些基本能力?。

FRM一级模考

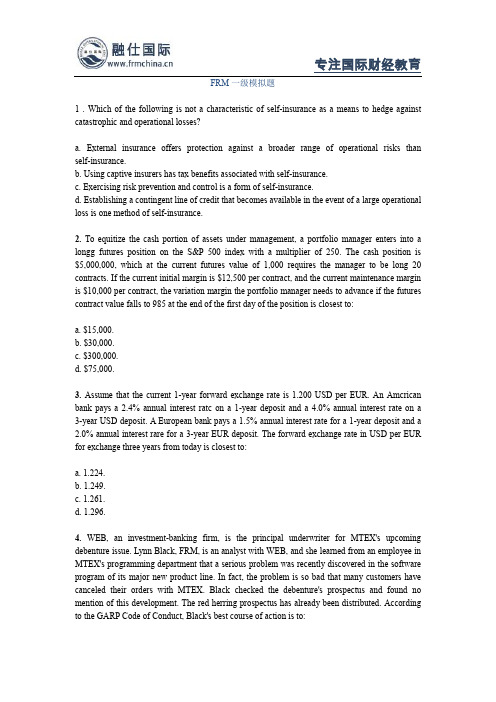

FRM一级模拟题1 . Given the following 1-year transition matrix, what is the probability that a Baa rated firm will default over a 2-year period?a. 5.00%.b. 9.75%.c. 14.50%.d. 20.00%.2. Isabelle Burns, FRM, is an investment advisor for a firm whose client base is composed of high net worth individuals. In her personal portfolio, Burns has an investment in Torex, a company that has developed software to speed up internet browsing. Burns has thoroughly researched Torex and believes the company is financially strong yet currently significantly undervalued. According to the GARP Code of Conduct, Burns may:a. not recommend Torex as long as she has a personal investment in the stock.b. not recommend Torex to a client unless her employer gives written consent to do so.c. recommend Torex to a client, but she must disclose her investment in Torex to the client.d. recommend Torex to a client without disclosure as long as it is a suitable investment for the client.3. Donaldson Capital Management, a regional money management firm, manages nearly $400 million allocated among three investment managers. All portfolios have the same objective, which is to produce superior risk-adjusted returns (by beating the market) for their clients. You have been hired as a consultant to measure the performance of the portfolio managers. You have collected the following information based on the last ten years of returns.During the same time period the annual rate of return on the marker portfolio was 13% with astandard deviation of 19%. In order to assess the portfolio performance of the above managers, you should use:a. the Treynor measure of performance.b. the Sharpe measure of performance.c. the Jensen measure of performance.d. none of the above.4. Which of the following statements about the central limit theorem is least likely correct?a. The variance of the distribution of sample means is s2 / n.b. The central limit theorem has limited usefulness for skewed distributions.c. The mean of the population and the mean of all possible sample means are equal.d. When the sample size n is large, the sampling distribution of the sample means is approximately normal.5. Bank regulators are examining the loan portfolio of a large, diversified lender. The regulators main concern is that the bank remains solvent during turbulent economic times. Which of the following is most likely the area that the regulator will want to focus on?a. Expected loss, since each asset can expect, on average, to decline in value from a positive probability of default.b. Expected loss, given the increase in underwriting standards of new loans.c. Unexpected loss, since the bank will need to set aside additional capital for the unlikely event that recovery rates are larger than expected.d. Unexpected loss, since the bank will need to set aside additional capital for the unlikely event that default losses are larger than expected.。

FRM一级模考

FRM一级模拟题1 . The current price of a stock is $25. A put option with a $20 strike price that expires in six months is available. N(-d1) = 0.0263 and N(-d2) = 0.0349. If the underlying stock exhibits an annual standard deviation of 25%, and the current continuously compounded risk-free rate is 4.25%, the Black-Scholes-Merton value of the put is closest to:a. $5.00.b. $3.00.c. $1.00.d. $0.03.2. What are the minimum values of an American-style and a European-style 3-month call option with a strike price of $80 on a non-dividend-paying stock trading at $86 if the risk-free rate is 3%?American Europeana. $6.00 $6.00b. $6.00 $5.96c. $6.59 $6.00d. $6.59 $6.593. An analyst is testing the hypothesis that the variance of monthly returns for Index A equals the variance of monthly returns for Index B based on samples of 50 monthly observations. The sample variance of Index A returns is 0.085, whereas the sample variance of Index B returns is 0.084. Assuming the samples are independent and the returns are normally distributed, which of the following represents the most appropriate test statistic?a.b.c.d.4. For a given portfolio, the expected return is 10% with a standard deviation of 15%. The beta of the portfolio is 0.75. The expected return of the market is 11% with a standard deviation of 18%.The risk-free rate is 4%. The portfolio's Treynor measure is:a. 0.060.b. 0.012.c. 0.040.d. 0.080.5. An analyst gathers the following data about the mean month returns of four securities.Which security has the lowest and highest level of relative risk as measured by the coefficient of variation?Lowest Highesta. W Yb. W Zc. X Yd. X Z。

20110416 FRM一级模考题第一套答案

Standard deviation = 160, 000 = 400; 400 / 100 = 40 The researcher is correct that a

possible consequence of increasing the sample size is sampling more than one population. In addition, increasing sample size will increase its costs. The need for additional precision must be balanced with cost and the risk of sampling more than one population.

15. Answer: B Indemnified bonds will hedge adverse internal firm events, such as a large underwriting loss for an insurance company, so Statement II is incorrect. Catastrophe options are traded on the Chicago Board of Trade so Statement III is incorrect.

14. Answer: D The expected value of the portfolio after two years is: (10)(1 - 0.03)(1 - 0.03) ($1,000,000) = $9,409,000. Therefore, the expected cumulative loss is: $10,000,000 - $9,409,000 = $591,000.

FRM一级模考

专注国际财经教育FRM一级模拟题1. An analyst gathered the following information about the return distributions for two portfolios during the same time period:Portfolio Skewness KurtosisA -1. 6 1.9B 0.8 3.2The analyst states that the distribution for Portfolio A is more peaked than a normal distribution and that the distribution for Portfolio B has a long tail on the lef-t side of the distribution, Which of the following is correct?A . The analyst's assessment is correct.B . The analyst's assessment is correct for Portfolio A and incorrect for portfolio B.C . The analyst's assessment is incorrect for Portfolio A but is correct for portfolio BD . The analyst is incorrect in his assessment for both portfolios.Common text for questions 2 and 3:A risk manager for Bank XYZ. Mark, is considering writing a 6-month American put option on a non-dividend-pay- ing stock ABC. The current stock price is USD 50 and the strika price of the option is USD 52. In order to find the no-arbitrage pnce of the option Mark uses a two-step binomial tree model. The stock price can go up or down by 20% each period. Mark's view is that the stock price has an 80% probability of going up each period and a 20% probability of going down The annual risk-free rate is 12% with continuous compounding2 . What is the risk-neutral probability of the stock price going up in a single step?a. 34.5%b. 57. 6Yoc. 65.5Yod. 80. 0%3 . The no-arbitrage price of the option is closest toa. USD 2.00b. USD 2.93c- USD 5.22d. USD 5.86。

FRM一级练习题(1)

FRM一级练习题(1)1、An investment manager is given the task of beating a benchmark. Hence the risk shoul d be measured in terms ofA. Loss relative to the initial investmentB. Loss relative to the expected portfolio valueC. Loss relative to the benchmarkD. Loss attributed to the benchmark2、Based on the risk assessment of the CRO, Bank United's CEO decid ed to make a large investment in a levered portfolio of CDOs. The CRO had estimated that the portfolio had a 1% chance of l osing $1 billion or more over one year, a loss that would make the bank insolvent. At the end of the first year the portfolio has lost $2 billion and the bank was cl osed by regulator. Which of the foll owing statement is correct?A. The outcome d emonstrates a risk management failure because the bank did not eliminate the possibility of financial distress.B. The outcome demonstrates a risk management failure because the fact that an extremely unlikely outcome occurred means that the probability of the outcome was poorly estimated.C. The outcome demonstrates a risk management failure because the CRO failed to go to regulators to stop the shutd own.D. Based on the information provid ed, one cannot determine whether it was a risk management failure.3、An analyst at CARM Research Inc. is projecting a return of 21% on Portfolio A. The market risk premium is 11%, the volatility of the market portfolio is 14%, and the risk-free rate is 4.5%. Portfolio A has a beta of 1.5. According to the capital asset pricing model which of the foll owing statements is true?A. The expected return of Portfolio A is greater than the expected return of the market portfolio.B. The expected return of Portfolio is less than the expected return of the market portfolio.C. The return of Portfolio A has l ower volatility than the mark t portfolio.D. The e peered return of Portfolio A is equal to the expected return of the market portfolio.4、Suppose Portfolio A has an expected return of 8%, volatility of 20%, and beta of 0.5. Suppose the market has an expected return of 10% and volatility of 25%. Finally suppose the risk-free rate is 5%. What is Jensen’s Alpha for Portfolio A?A. 10.0%B. 1.0%C. 0.5%D. 15%5、Which of the foll owing statement about the Sharpe ratio is false?A. The Sharpe ratio consid ers both the systematic and unsystematic risk of a portfolio.B. The Sharpe ratio is equal to the excess return of a portfolio over the risk-free rate divided by the total risk of the portfolio.C. The Sharpe ratio cannot be used to evaluate relative performance of undiversified portfolios.D. The Sharpe ratio is derived from the capital market line.6、A portfolio manager returns 10% with a volatility of 20%. The benchmark returns 8% with risk of 4%. The correlation between the two is 0.98. The risk-free rate is 3%. Which of the foll owing statement is correct?A. The portfolio has higher SR than the benchmark.B. The portfolio has negative IR.C. The IR is 0.35.D. The IR is 0.29.7、In perfect markets risk management expenditures aimed at reducing a firm' diversifiable risk serve toA. Make the firm more attractive to sharehol ders as long as costs of risk management are reasonable.B. Increase the firm's value by lowering its cost of equity.C. Decrease the firm's value whenever the costs o f such risk management are positive.D. Has no impact on firm value.8、By reducing the risk of financial distress and bankruptcy, a firm's use of d erivatives contracts to hedge it cash fl ow uncertainty willA. Lower its value due to the transaction costs of derivative trading.B. Enhance its value since investors cannot hedge such risks by themselves.C. Have no impact on its value as investor costless diversify this risk.D. Have no impact as only systematic risks can be hedged with derivatives.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。

FRM一级模考

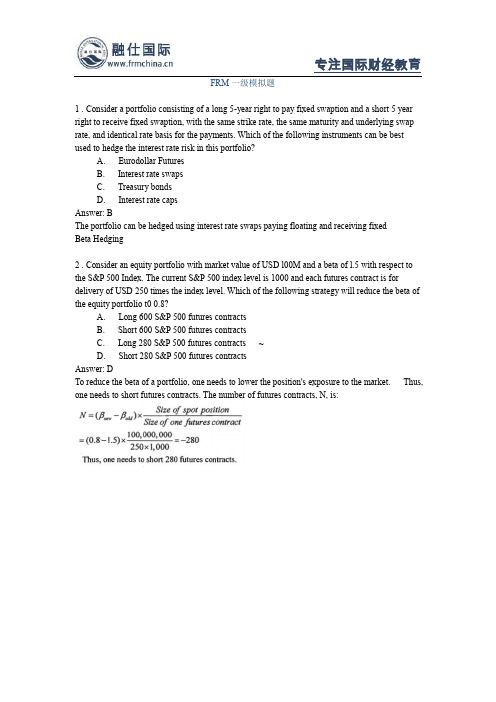

FRM一级模拟题1 . You are given the following information about an interest rate swap:. 2-year term. Semi-annual payment. Fixed rate=6%. Floating rate=LIBOR+50 basis points. Notional principal USD 10 millionCalculate the net coupon exchange for the first period if LIBOR is 5% at the beginning of the period and 5.6% at the end of the period.A. Fixed-rate payer pays USDOB. Fixed-rate payer pays USD25,000C. Fixed-rate payer pays USD50,000D. Fixed-rate payer receives USD25,000Answer: BA. Incorrect. The candidate incorrectly uses the LIBOR rate at the end of the period.B. Correct. Fixed rate payer pays USD25,000. See BELOW for details.C. Incorrect. The candidate forgets to add the 50 basis points to the beginning LIBOR rate.D. Incorrect. The candidate is confused about the cash flow direction. A net positive payment ispaid by the fixed rate payer, not receiving.Computational Details for Numerical Answer:. Fixed rate payer pays 6%, therefore (0.06 1 2) x 10 million = USD 300,000.. Interest rate swaps have payments in arrears. Floating rate payer pays LJBOR rate at the beginning of period + 0.50%, i.e. 5 % + 0.50% = 5.5 %.Therefore the floating rate payment = (0.055 1 2) x 10 million = USD 275,000.The net payment of USD 25,000 is paid by the fixed rate payer.2 . Assume that swap rates are identical for all swap tenors. A swap dealer entered into a plain vanilla swap one year ago as the receive-fixed party, when the price of the swap was 7%. Today, this swap dealer will face credit risk exposure from this swap only if the value of the swap for the dealer is:A. negative, which will occur if new swaps are being priced at 6%.B. negative, which will occur if new swaps are being priced at 8%.C. positive, which will occur if new swaps are being priced at 6%.D. positive, which will occur if new swaps are being priced at 8%.Answer: CCredit exposure only exists if the value of the swap is positive, This can only occur lf new swaps are being priced at a lower fixed rate.3 . It has been 90 days since the last coupon payment on a default swap. The notional principal is $10,000,000 and the reference price is 100%. The final price is estimated at 40% and the annual coupon rate was 8%. What is the cash amount to settle the swap?A. $5,800,000B. $9,040,000C. $5,200,000D. $4,600,000Answer: AThe settlement of the default swap is the notional principle times the reference amount minus the final and accrued interest. 'Settlement amount =$10,000,000 x (100% - [40% + 8% x 90 / 360] ) = $5,800,000 .4 . A stock currently trades at $10. At the end of three months, the stock will either be $11 or $9. The continuously compounded risk-free rate of interest is 3.5% per year. The value of a 3-month European call option with a strike price of $10 is closest to:A. $0.11B. $0.54C. $0.65D. $1.015 .。

FRM一级在线模考题答案

FRM一级模考试题(一)——答案1.Answer: CThe historical simulation method may not recognize changes in volatility and correlations from structural changes.2.Answer: CThe dirty price of the bond is calculated as N = 10; I/Y = 2.5; PMT = 30; FV = 1,000; CPT→PV = 1,043.76. Adjusting the PV for the fact that there are only 90 days until the receipt of the first coupon gives $1,043.76×(l.025)90/180 = $1,056.73. Clean price = dirty price - accrued interest = $1056.73 - $30(90/180) = $1,041.73.3.Answer: BGamma (not theta) represents the expected change in delta for a change in the value of the underlying. In-the-money options are more sensitive to changes in rates (rho is higher) than out-of-the-money options.4.Answer: AAssuming no default risk, the domestic return is 7.35%. The return on the UK investments, however, is equal to the amount invested today, (USD$2,000,000)/(USD1.62GBP)= GBP1,234,568, which turns into GBP1,234,568×1.08 = GBP1,333,333 one year from now. Since the forward contract guarantees the exchange rate in the future, this translates into GBP1,333,333 ×USD1.5200/GBP = USD2,026,666. This is a dollar return to the bank of USD2,026,666/ USD2,000,000-1 = 1.33%. Hence, the weighted average return to the bank’s investments is (0.5)×(7.35%) + (0.5)×(1.33%) = 4.34%. Since the cost of funds for the bank is 5.5%, the net interest margin for the bank is 4.34-5.50 = -1.16%.5.Answer: DAll of the statements are correct except choice d: the value of the firm’s equity should be the present value of its expected free cash flows (not net income).6.Answer: D± So youWith a known variance, the 95% confidence interval is constructed as Xknow that 33.23307.Answer: DA 6% rate compounded annually is approximately equivalent to a 5.8269% rate (rounded to four decimal places) compounded continuously. In (1 + 0.06) = 0.058268908 Using put-call parity:0.0582690 4.1027.5025$5.04rTp c XeS e −−=+−=+−=8.Answer: AV AR measures the expected amount of capital one can expect to lose within a given confidence level over a given period of time. One of the problems with V AR is that it does not provide information about the expected size of the loss beyond the V AR. V AR is often complemented by the expected shortfall, which measures the expected loss conditional on the loss exceeding the V AR. Note that since expected shortfall is based on V AR, changing the confidence level may change both measures. A key difference between the two measures is that V AR is not sub-additive, meaning that the risk of two funds separately may be lower than the risk of a portfolio where the two funds are combined. Violation of the sub-additive assumption is a problem with V AR that does not exist with expected shortfall. 9.Answer: CThe fixed payments made by Cooper are (0.07/2)×$2,000,000 = $70,000. The present value of the fixed payments =0.0650.50.0681.0(0.0751.5)($70,000)($70,000)($70,000$2,000,000)$67,762$65,398$1,849,747$1,982,907e e e −×−×−×+++×=++=The value of the floating rate payments received by Cooper at the payment date is the value of the notional principal, or $2,000,000.The value of the swap to Cooper is ($2,000,000-$1,982,907) = $17,093. 10.Answer: CA stack is a bundle of futures contracts with the same expiration. Over time, a firm may acquire stacks with various expiry dates. To hedge a long-term risk exposure, a firm would close out each stack as it approaches expiry and enter into a contract with a more distant delivery, known as a roll. This strategy is called a stack-and-roll hedge and is designed to hedge long-term risk exposures with short-term contracts. Using short-term futures contracts with a larger notional value than the long-term risk they are meant to hedge could result in over hedging” depending on the hedge ratio. 11.Answer: BThe duration of a portfolio of bonds is the weighted average (using market value weights) of thedurations of the bonds in the portfolio. First let’s find the weights.Bond Price as Percentage of Par Face Value $ Market Value $1 95.5000 2,000,000 1,910,0002 88.6275 3,000,000 2,658,8253 114.8750 5,000,000 5,743,750 Total 10,312,575The weights based on market values are:Weight of bond 1 = 1,910,000 / 10,312,575 = 0.1852Weight of bond 2 = 2,658,825 / 10,312,575 = 0.2578Weight of bond 3 = 5,743,750 / 10,312,575 = 0.5570Bond Weights Duration WeightedDuration1 0.1852 6.95 1.28712 0.2578 9.77 2.51873 0.5570 14.81 8.2492Total 12.055012.Answer: CTo increase the beta of the portfolio from the market beta (1.0) to 1.5, the portfolio manager should take a long position:# of contracts =$250,000,000(1.5 1.0)4171,200250−×=×contracts13.Answer: BThe concessionality of a MYRA is defined as the difference between the present value of the loans before and after the restructuring.14.Answer: BThe formula is JB =2222(3)180(43)1[][0]30[]7.5 64644n KS−−+=+==Note that excess kurtosis is equal to K-3 so excess kurtosis of 1 means that kurtosis is 4.15.Answer: CThe rogue traders for both Daiwa and Barings had dual roles as both the head of trading and the head of the back-office support function. This operational risk oversight allowed them to hide millions in losses from senior management. In the Allied Irish Bank case, John Rusnak did not run the back-office operations. The Drysdale Securities case did not deal with a rogue trader.16.Answer: AThe fact that mean> median> mode is consistent with a distribution that is positively skewed. For all normal distributions, kurtosis = 3. Excess kurtosis = kurtosis-3, which is 0 for a normal distribution. In this case, excess kurtosis = 2, which means kurtosis = 5. This means that the distribution being examined is more peaked than the normal distribution and is said to be leptokurtic. 17.Answer: CA change from a Ba to Baa rating is an example of a credit upgrade. A credit upgrade will decrease the likelihood of default (EDF) reducing expected loss. Note that expected loss is an estimate of average future loss. Actual loss is by definition equal to zero until a credit event occurs. 18.Answer: BThe CAPM assumes that the market portfolio should be the portfolio with the highest Sharpe ratio of all possible portfolios and should include all investable assets. It also assumes that the expected excess returns for the market are assumed to be known in that investors have access to the same information. As well, it assumes that returns are normally distributed and investors’ expectations for risk and return ate identical. 19.Answer: CThe 3-month forward rate is calculated as follows:1()(0.0650.05)0.250,()$19$19.07r T T T F S e e δ−−==×=20.Answer: CThe farmer needs to be short the futures contracts. The two sources of basis risk confronting the farmer will result from the fact that he is using a cattle contract to offset the price movement of his buffalo herd, Cattle prices and buffalo prices may not be perfectly positively correlated. As a result, the correlation between buffalo and cattle prices will have an impact on the basis of the cattle futures contract and spot buffalo meat. The delivery date is a problem in this situation, because the farmer’s hedge horizon is winter, which probably will not commence until December or January. In order to maintain a hedge during this period, the farmer will have to enter into another futures contract, which will introduce an additional source of basis risk. 21.Answer: BA scattergram can help determine whether a relationship is positive or negative. Since the population and sample coefficients are almost always different, the residual will very rarely equal the corresponding population error term.Answer: C0.02(0.25)0.04(0.25)01,1001,08025.26qT rT S e Ke e e −−−−−=−=23.Answer: DPractitioners primarily use structural models, while academics are the primary users of statistical models. There are three types of structural models and one of them includes the need to forecast both factor returns and exposures. Factors in structural models are intuitive and well-known, while factors in statistical models are implied factors derived through a statistical operation. Structural models assume an underlying economic relationship between factors and stock returns. 24Answer: ABecause catastrophe bonds are riskier than straight bonds issued by the same firm, they usually have maturities less than three years and are usually non-investment-grade bonds. They also have potentially useful diversification qualities as their returns, being linked to operational losses, are not highly correlated with market returns. 25.Answer: AFor a risk management activity to have value, the firm must be able to do something for shareholders that they cannot do themselves. The risk of bankruptcy cannot be hedged by shareholders (as beta risk and output-price risk can), thus, it may be value increasing for the firm to hedge this risk. Note that it is not a question that bankruptcy costs are too expensive to hedge; they are impossible to hedge. Although Choices b and c may be correct, they are less relevant to the situation and are, therefore, not the best answers. 26.Answer: BIn this case, U = 1.1, D = 0.9, r = 0.035, and the value of the option is $1 if the stock increases and $0 if the stock decreases. The probability of an up movement, ∏U, can be calculated as0.0353/12(0.9)/(1.10.9)0.5439e ×−−=The value of the call option is therefore (0.0353/12)(0.5439$1)/$0.54e××=27.Answer: CStandards 2.1 and 2.2—Conflicts of Interest. Members and candidates must act fairly in all situations and must fully disclose any actual or potential conflict to all affected parties. Sell-side members and candidates should disclose to their clients any ownership in a security that they are recommending.28.Answer: BThe Treynor measure is most appropriate for comparing well-diversified portfolios. That is the Treynor measure is the best to compare the excess returns per unit of systematic risk earned by portfolio managers, provided all portfolios are well-diversified.All three portfolios managed by Donaldson Capital Management are clearly less diversified than the market portfolio. Standard deviation of returns for each of the three portfolios is higher than the standard deviation of the market portfolio, reflecting a low level of diversification.Jensen’s alpha is the most appropriate measure for comparing portfolios that have the same beta. The Sharpe measure can be applied to all portfolios because it uses total risk and it is more widely used than the other two measures. Also, the Sharpe ratio evaluates the portfolio performance based on realized returns and diversification. A less-diversified portfolio will have higher total risk and vice versa.29.Answer: DThe central limit theorem holds for any distribution (skewed or not) as long as the sample size is large (i.e., n >30). The mean of the population and the mean of the distribution of all sample means are equal. The standard deviation of the mean many observations is less than the standard deviation of a single observation.30.Answer: CUnexpected loss is a measure of the variation in expected loss. As a precaution, the bank needs to set aside sufficient capital in the event that actual losses exceed expected losses with a reasonable likelihood. For example, smaller recovery rates would be indicative of larger actual losses.31.Answer: CGiven that the economy is good, the probability of a poor economy and a bull market is zero. The other statements are true. The P(normal market) = (0.60×0.30) + (0.40×0.30) = 0.30. P(good economy and bear market)= 0.60×0.20 = 0.12. Given that the economy is poor, the probability of a normal or bull market = 0.30 + 0.20 = 0.50.32.Answer: DNone of the statements are correct. The historical approach uses historic data from past crisis events, the prospective scenario conditional approach includes correlations between risk factors, and the factor push method is a prospective approach not a historical approach.33.Answer: BRisk management activities can increase firm value when the firm’s claimholders cannot takeactions to replicate the results of hedging activity. Claimholders are willing to pay for the firm to do something they cannot do on their own accounts.34.Answer: CTop-down models rely primarily on aggregate historical data. Therefore, they are relatively simple and do not differentiate between high-frequency low-severity events and low-severity, high-frequency events because both are pooled together in the data. The aggregated nature of the data also limits the amount of data used in these models. A limitation of aggregated data, however, is that top-down models do not have diagnostic capabilities like bottom-up models that dissect processes into individual components.35.Answer: CBuying a call (put) option with a low strike price, buying another call (put) option with a higher strike price, and selling two call (put) options with a strike price halfway between the low and high strike options will generate the butterfly payment pattern. Two other wrong answer choices deal with bull and bear spreads, which can also be replicated with either calls or puts. A bull spread involves purchasing a call (put) option with a low strike price and selling a call (put) option with a higher exercise price. A bear spread is the exact opposite of the bull spread.36.Answer: DCaptive insurers are off-shore, wholly owned subsidiaries that may deduct for tax purposes the discounted value of all future expected losses stemming front a claim spanning several years. Essential this allows self-insurers to deduct losses before they have even occurred. Incurring costs to manage and control operational risk achieves the same result in principle as self-insurance. A contingent line of credit is a form of self-insurance that provides liquidity in the event of a loss rather than building up cash reserves in anticipation of a loss.37.Answer: DThe futures contract ended at 985 on the first day. This represents a decrease in value in the position of (1,000-985)×$250×20 = $75,000. The initial margin placed by the manager was $12,500×20 = $250,000. The maintenance margin for this position requires $10,000×20 = $200,000. Since the value of the position declined $75,000 on the first day, the margin account is now worth $175,000 (below the $200,000 maintenance margin) and will require a variation margin of $75,000 to bring the position back to the initial margin. It is not sufficient just to bring the position back to the maintenance margin.38.Answer: CWe are given that the forward exchange rate in one year is 1.200 and are asked to find the exchange rate in three years. This means we need to apply the 2-year forward rate one year fromtoday.The 2-year forward rate in the United States is:1.04811 4.81%==−=The 2-year forward rite in Europe is:1.022512.25%==−=Finally, we can apply interest rate parity:221.04811.200 1.2611.0225t F =×= 39.Answer: AStandards 3.1 and 3.2 relate to the preservation of confidentiality. The simplest, most conservative, and most effective way to comply with these Standards is to avoid disclosing any information received from a client, except to authorized fellow employees who are also working for the client. If the information concerns illegal activities by MTEX, Black may be obligated to report activities to authorities. 40.Answer: AThe liquidity preference theory suggests that the shape of the term structure is determined by the fact that most investors prefer short-term liquid assets, holding return constant. 41.Answer: AIn general, bond prices will tend to increase with maturity when coupon rates are above relevant forward rates. When short-term rates are below the forward rates utilized by bond prices, the investors who invest in longer-term investments will tend to outperform investors who roll over shorter-term investments. 42.Answer: CThe forward rate can be calculated as [(98.2240/96.7713)-1]×2 = 3%. 43.Answer: BThe price is calculated as $15 (0.992556) + $15 (0.982240) + $1,015 (0.967713) = $1,011.85. 44.Answer: AUnique among swaps, equity swap payments may be floating on both sides (and the payments not known until the end of the settlement period). Similar to options, premiums for swaptions are dependent on the strike rate specified in the swaption. The most common reason for entering into commodity swap agreements is to control the costs of purchasing resources, such as oil and electricity. A negative index return requires the fixed-rate payer to pay the percentage decline in the index. 45.Answer: BThe GARCH (1,1) estimate of volatility will be:220.000005(0.13)(0.03)(0.85)(0.022)0.0005330.0231 2.31%volatility ++====46.Answer: B0.04250.5($200.0349)($250.0263)$0.02582$0.03P e −×=××−×=≈47Answer: DThe minimum value for a European-style call option, c T is given by3/12max[0,/(1)]max[0,8680/(1.03)]$6.59T T F S X R −+=−=An American style call option must be worth at least as much as an otherwise identical European-style call option and has the same minimum value Note that this fact alone limits the possible correct responses to Choices a and d. Since the American style call is in the money and therefore must be worth more than the $6 difference between the strike price and the exercise price, you can eliminate Choice a and select Choice d without calculating the exact minimum value. 48.Answer: AThe appropriate test is an F-test, where the larger sample variance (Index A) is placed in the numerator. 49.Answer: DThe formula for the Treynor measure is ()[p FPE R R β−. Thus, the value for the Treynor measurein this case is (0.10 - 0.04)/0.75 = 0.08 50.Answer: DThe coefficient of variation, CV = standard deviation/arithmetic mean, is a common measure of relative dispersion (risk) CV W = 0.4/0.5 = 0.80, CV X = 0.7/0.9 = 0.78; CV Y = 4.7/l.2 = 3.92 and CV Z = 5.2/1.5=3.47 Because a lower relative risk, Security X has the lowest relative risk and Security Y has the highest relative risk.51.Answer: AThe probability of rescheduling sovereign debt is positively related to the debt-service ratio, the import ratio, the variance of export revenue, and the domestic money supply growth.52.Answer: BAccording to the cash-and-carry Formula, the futures price should be:(0.02750.01)0.25e−=1,010$1,014.43Hence, the futures is overvalued, indicating it should he sold and the index be purchased for a risk-free profit of $1,020 —$1,014.43 = $5.57.53.Answer: DHoffman has violated both Standard 1.2-independence and objectivity, which specially mentions that CARP Members must not offer, solicit, or accept any gift, benefit, compensation, or consideration that could be reasonably expected to compromise their own or another’s independence and objectivity, and Standard 2.2-Conflicts of Interest, which states the Members should make full and fair disclosure of all matters that could reasonably be expected to impair independence and objectivity or interfere with respective duties to their employer, clients, and prospective clients.54.Answer: DThe variability in the receipt of payments from the floating-rate asset is eliminated, as the floating payment of the floating rate leg of the swap offsets the receipt of the floating rate on the asset. The floating-rate payer is effectively left with a fixed-rate asset.55.Answer: DExpected value = (0.4)(10%) + (0.4)(12.5%) + (0.2)(30%) = 15%Variance = (0.4)(10-15)2 + (0.4)(12.5 -15)2 + (0.2)(30 - 15)2 = 57.5Standard deviation =56.Answer: D,,220.05 1.250.2S FS F F Cov HR Beta σ====57.Answer: AOption-free bonds have positive convexity and the effect of (positive) convexity is to increase the magnitude of the price increase when yields fall and to decrease the magnitude of the price decrease when yields rise. 358.Answer: CThe standard normal random variable, denoted Z, has mean equal to 0 and standard variation (and variance) equal to 1. Also, a multivariate distribution is meaningful only when the behavior of each random variable in the group is in some way dependent upon the behavior of others.59.Answer: DThe critical z-value for a one-tailed test of significance at the 0.01 level will be either +2.33 or -2.33. The test statistic for hypotheses concerning equality of variances is 2122S F S = The statement regarding p-value is true. A Type II error is failing to reject the null hypothesis when it is actually false.60.Answer: BThe Taylor Series does not provide good approximations of price changes when the underlying asset is a callable bond or mortgage-backed security. The Taylor Series approximation only works well for “well-behaved” quadratic functions that can be approximated by a polynomial of order two.61.Answer: DLTCM believed that, although yield differences between risky and riskless fixed-income instruments varied over time, the risk premium (or credit spread) tended to revert (decrease) to average historical levels. This was similar to their equity volatility strategy. Also, their balance sheet leverage was actually in line with other large investments banks (but their true leverage, economic leverage, was not considered).62.Answer: BThe benchmark returns are not important here. The average of the portfolio returns is(6+9+4+12)14=31/4=7.75.0.4743==63.Answer: D Neither statement is correct. The appropriate number of contracts for the hedge is:$10,000,000() 1.0()36 1,100250portfolio portfolio value contracts futures price multiplierβ×=×≈×× However, since the manager is long the portfolio, he will want to take a short position in the 36 contracts.Change in value of portfolio = -0.01($10,000,000) = -$100,000.Change in value of futures position = 36(1,100 — 1,090)(250) = $90,000.Net payoff= -$100,000 + $90,000 = -$10,000 The net impact is a loss of $10,00064.Answer: CAt the end of year 1 there is a 0% chance of default and a 90% chance that the firm will maintain an Aaa rating. In year 2, there is a 0% chance of default if the firm was rated Aaa after 1 year (90%×0% = 0%), There is a 5% chance of default if the firm was rated Baa after 1 year (10%×5% = 0.5%). Also, there is a 15% chance of default if the firm was rated Caa after 1 year (0%× 15% = 0%) The probability of default is 0% from year 1 plus 0.5% chance of default from year 2 for a total probability of default over a 2-year period of 0.5%.65.Answer: AThe beta factors used in the standardized approach for operationa1 risk are as follows: trading and sales 18%, retail banking 12% agency and custody services 15%, asset management: 12%.66.Answer: AAccording to put-call parity:000rT c Xe p S −+=+The left-hand side=$4+$45e -0.06×0.5 = $47.67The right-hand side = $4 + $43 = $47Since the value of the fiduciary call is not equal to the value of the protective put, put-call parity is violated and there is an arbitrage opportunity.Sell overpriced and buy underpriced. That is, sell the fiduciary call and buy the protective put. Therefore, sell the call for $4, sell the Treasury bill for $43.67 (i.e., borrow at therisk-free rate), buy the put for $4 and buy the underlying asset for $43. The arbitrageprofit is $0.67.67.Answer: BThe 5-3-2 spread tells us the amount of profit that can be locked in by buying five barrels of oil and producing three barrels of gasoline and two barrels of heating oil.(61.5×3) + (58.5×2) - (55×5) = $26.50 for 5 barrels; $5.30/barrel68.Answer: CUse interest-rate parity to solve this problem. 1.1565 = Se (0.02-0.04)0.25, so S = 1.1623.69.Answer: AUnsystematic risk is asset-specific and, therefore, a diversifiable risk. The market risk premium is also known as the price of risk and is calculated as the excess of the expected return on the market over the risk-free rate of return. The risk premium of an asset is calculated as beta times the excess of the expected return on the market over the risk-free rate of return.70.Answer: C12[()][()] 6.523.56.520.325.88 3.5i i j j i j ij i j i j R E R R E R Cov Cov r σσσσ−×−========××Σ71.Answer: DMoral hazard refers to the fact that an insured party may engage in risky behavior (or at least behave in a less risk-averse manner) knowing that an insurance policy will insulate the party against the consequences of such behavior. The way that Eggenton can mitigate the moral hazard problem is to include a deductible or co-insurance feature that would force JT Cola to pay a portion of the cost should a claim be made against the policy. If a deductible feature were not included in the policy, JT Cola management would have been free to act in any manner they would choose, including manipulating the global cola market, and Federal Insurance Group would have assumed all of the risk.72.Answer: BWe can calculate the expected loss as follows.EL = AE×EDF×LGDMaximum lossAdjusted exposure = OS + (COM U - OS)×UGD= $8,000,000 + ($12,000,000)×(0.75)= 17,000,000EL = ($17,000,000)×(0.02)×(0.80) = $272,000Minimum lossAdjusted exposure = OS + (COM U - OS)×UGD= $8,000,000 + ($12,000,000)×(0.5)= $14,000,000EL = ($14,000,000)×(0.01)×(0.80) = $112,000Therefore, the difference between maximum and minimum loss is:$272,000 - $112,000 = $160,000.73.Answer: ASince the current position is short gamma, the action that must be taken is to go long the option in the ratio of the current gamma exposure to the gamma of the instrument to be used to create the gamma-neutral position (5,000/2 = 2,500). However, this will change the delta of the portfolio from zero to (2,500×0.7) = 1,750. This means that 1,750 of the underlying stock position will need to be said to maintain both gamma and delta neutrality.74.Answer: BYou have purchased a bull spread. You will exercise the call chat you purchased for a net profit of (34 - 25) - 3 = $6 per share. The call that you sold will not be exercised, so your net profit is the cost of $1 per share. Your total net profit is 6 + 1 = $7 per share.75.Answer: AIf the investor has written 15,000 call options, he must go long delta times the short option position to create a delta-neutral position. or buy $15,000×0.50 = 7,500 shares. Note that the delta of a call option, which is exactly at-the-money, is 0.5.76.Answer: BThe historical simulation V AR for 5% is the fifth lowest return, which is -1.59%; therefore, the correct V AR is: -79,500 = (-0.0159)×(5,000,000).77.Because firms tend to release good news more readily than bad news, downgrades may be more of a surprise, so downgrades affect stock prices more than upgrades when the firm reveals the good news associated with the upgrade prior to its occurrence.The “underrating” and “overrating” is seen more with the use of the through-the-cycle approach. As well, the ratings delivered by more specialized and regional agencies tend to be less homogeneous than those delivered by major players like S&P and Moody’s.78.Answer: BOperational risk economic capital is the difference between the loss at a given confidence level and the expected loss. In this case, $500,000 - $50,000 = $450,000.79.Answer: AThe head of the government bond trading desk at Kidder Peabody, Joseph Jett, misreported trades, which allowed him to report substantial artificial profits. After these errors were detected, $350 million in falsely reported gains had to he reversed.80.Answer: BThe R2 of the regression is calculated as ESS/TSS = (92.648/117.160) = 0.79, which means that the variation in industry returns explains 79% of the variation in the stock return. By taking the square root of R2, we can calculate that the correlation coefficient (r) = 0.889. The t-statistic for the industry return coefficient is 1.91/0.31 = 6.13, which is sufficiently large enough for the coefficient to be significant at the 99% confidence interval. Since we have the regression coefficient and intercept, we know that the regression equation is R stock= l.9X + 2.1. Plugging in a value of 4% for the industry return, we get a stock return of 1.9 (4%) + 2.1 = 9.7%.81.Answer: BFixed-rate coupon = 150,000,000×0.055 = $8,250,000B fixed = 8.25e-0.0575+158.25e-0.0625×2 = $147,440,000B floating = $150,000,000V swap= $150,000,000 - $147,440,000 = $2,560,00082.Answer: BThe rate of sampling error has no relation to the sample size; all things being equal, the likelihood of sampling error will be the same regardless of sample size. According to the central limit theorem, the sample mean for large sample sizes will be distributed normally regardless of the distribution of the underlying population.83.。

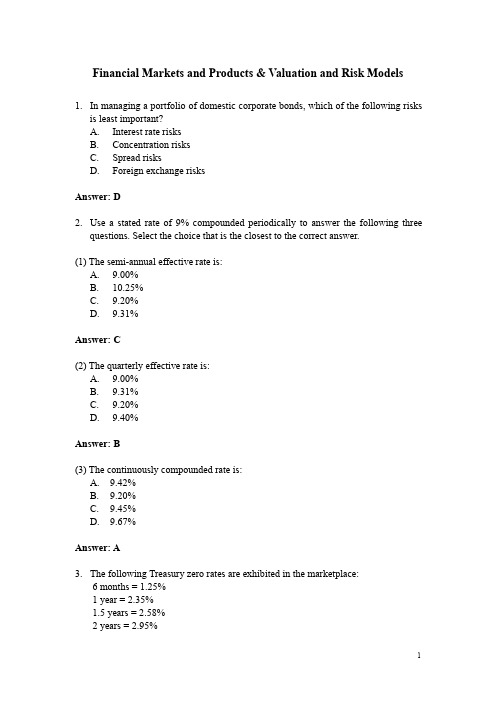

FRM一级_金融市场与产品&估值和风险模型习题及答案(★★)

Financial Markets and Products & Valuation and Risk Models1.In managing a portfolio of domestic corporate bonds, which of the following risksis least important?A.Interest rate risksB.Concentration risksC.Spread risksD.Foreign exchange risksAnswer: De a stated rate of 9% compounded periodically to answer the following threequestions. Select the choice that is the closest to the correct answer.(1) The semi-annual effective rate is:A.9.00%B.10.25%C.9.20%D.9.31%Answer: C(2) The quarterly effective rate is:A.9.00%B.9.31%C.9.20%D.9.40%Answer: B(3) The continuously compounded rate is:A.9.42%B.9.20%C.9.45%D.9.67%Answer: A3.The following Treasury zero rates are exhibited in the marketplace: 6 months = 1.25% 1 year = 2.35%1.5 years =2.58% 2 years = 2.95%Assuming continuous compounding, the price of a 2-year Treasury bond that paysa 6 percent semiannual coupon is closest to:A.105.20B.103.42C.108.66D.105.90Answer: D4. A two-year zero-coupon bond issued by corporate XYZ is currently rated A. Oneyear from now XYZ is expected to remain at A with 85% probability, upgraded to AA with 5% probability, and downgraded to BBB with 10% probability. The risk free rate is flat at 4%. The credit spreads are flat at 40, 80, and 150 basis points for AA, A, and BBB rated issuers, respectively. All rates are compounded annually.Estimate the expected value of the zero-coupon bond one year from now (for USD 100 face amount). Fixed Income Securities:D 92.59D 95.33D 95.37D 95.42Answer: C5.Assuming the long-term yield on a perpetual note is 5%, compute the dollar valueof a 1 bp. Increase in the yield (DV01) for a perpetual note paying a USD 1,000,000 annual coupon.A.-20,000B.-30,000C.-40,000D.-50,000Answer: C6.Given the following portfolio of bonds:What is the value of the portfolio’s DV01 (Dollar value of 1 basis point)?A.8,019B.8,294C.8,584D.8,813Answer: C7.Assuming other things constant, bonds of equal maturity will still have differentDV01 per USD 100 face value. Their DV01 per USD 100 face value will be in the following sequence of highest value to lowest value:A.Premium bonds, par bonds, zero coupon bondsB.Zero coupon bonds, Premium bonds, par bondsC.Premium bonds, zero coupon bonds, par bondsD.Zero coupon bonds, par bonds, Premium bondsAnswer: A8.Which of the following statements about standard fixed rate government bondswith no optionality is TRUE?I.Higher coupon implies shorter duration.II.Higher yield implies shorter duration.III.Longer maturity implies larger convexity.A.I and II onlyB.II and III onlyC.I and III onlyD.I, II, and IIIAnswer: D9.Which of the following is not a property of bond duration?A.For zero-coupon bonds, Macaulay duration of the bond equals its years tomaturity.B.Duration is usually inversely related to the coupon of a bond.C.Duration is usually higher for higher yields to maturity.D.Duration is higher as the number of years to maturity for a bond selling atpar or above increases.Answer: C10.Estimated price changes using only duration tend to:A.Overestimate the increase in price that occurs with a decrease in yield forlarge changes in yield.B.Underestimate the decrease in price that occurs with a increase in yield forlarge changes in yield.C.Overestimate the increase in price that occurs with a decrease in yield forsmall changes in yield.D.Underestimate the increase in price that occurs with a decrease in yield forlarge changes in yield.Answer: D11.A portfolio consists of two positions: One position is long $100M of a two yearbond priced at 101 with a duration of 1.7; the other position is short $50M of a five year bond priced at 99 with a duration of 4.1. What is the duration of the portfolio?A.0.68B.0.61C.-0.68D.-0.61Answer: D12.A zero-coupon bond with a maturity of 10 years has an annual effective yield of10%. What is the closest value for its modified duration?A.9B.10C.100D.Insufficient InformationAnswer: A13.A portfolio manager uses her valuation model to estimate the value of a bondportfolio at USD 125.482 million.The term structure is ing the same model,she estimates that the value of the portfolio would increase to USD 127.723 million if all the interest rates fell by 30bp and would decrease to USD 122.164 million if all the interest rates rose by ing these estimates,the effective duration of the bond is closest to :A. 8.38B. 16.76C. 7.38D. 14.77Answer: C14.A portfolio manager has a bond position worth USD 100 million. The position hasa modified duration of eight years and a convexity of 150 years. Assume that theterm structure is flat. By how much does the value of the position change if interest rates increase by 25 basis points?D -2,046,875D -2,187,500D -1,953,125D -1,906,250Answer: C15.An investment in a callable bond can be analytically decomposed into a:A.Long position in a non-callable bond and a short position in a put optionB.Short position in a non-callable bond and a long position in a call optionC.Long position in a non-callable bond and a long position in a call optionD.Long position in a non-callable and a short position in a call optionAnswer: D16.A European bank exchanges euros for USD, lends them at the U.S. risk-free rate,and simultaneously enters into a forward contract to sell the loan proceeds for euros at loan maturity. If the net effect of these transactions is to earn the risk-free euro rate, it is an example of:A.ArbitrageB.Spot-forward equalityC.Interest rate parityD.The law of one priceAnswer: C17.At the inception of a six-month forward contract on a stock index, the value of theindex was $1,150, the interest rate was 4.4%, and the continuous dividend was1.8%. Three months later, the value of the index is $1,075. Which of the followingstatement is True? The value of the:A.long position is $82.41.B.long position is $47.56.C.short position is $47.56.D.long position is -$82.41.Answer: D18.Assuming the 92-day and 274 day interest rate is 8% (act/360, money market yield)compute the 182-day forward rate starting in 92 days (act/360, money market yield).A.7.8%B.8.0%C.8.2%D.8.4%Answer: B19.The 1-year US dollar interest rate is 3% and the 1-year Canadian dollar interestrate is 4.5%. The current USD/CAD spot exchange rate is 1.5000. Calculate the 1-year forward rate.A. 1.5225B. 1.5218C. 1.5207D. 1.5199Answer: B20.The price of a three-year zero coupon government bond is 85.16. The price of asimilar four-year bond is 79.81. What is the one-year implied forward rate form year 3 to year 4?A. 5.4%B. 5.5%C. 5.8%D. 6.7%Answer: D21.The clearinghouse in a futures contract performs all but which of the followingroles? The clearing house:A.guarantees traders against default from another party.B.splits each trade and acts as a buyer to futures sellers and as a seller tofutures buyers.C.allows traders to reverse their position without having to contract the otherside of the position.D.guarantees the physical delivery of the underlying asset to the buyer offuture contracts.Answer: D22.A weakening of the basis is a consequence of the:A.Spot price increasing faster than the futures price over time.B.Spot price moving according to hyper-arithmetic Brownian motion.C.Futures price increasing faster than the spot price over time.D.Futures price moving according to hyper-arithmetic Brownian motion. Answer: C23.Which of the following statements best describes marking-to-market of a futurescontract? At the:A.End of the day, the maintenance margin is increased for traders who lost anddecreased for traders who gained.B.Conclusion of each trade, the gains or losses from all previous trades in thefutures contract are tallied.C.Maturity of the futures contract, the gains or losses are tallied to the trader’saccount.D.End of the day, the gains or losses are tallied to the trader’s account. Answer: D24.A trader buys one wheat contract (underlying = 5,000 bushels) at a price of $3.05per bushel. The initial margin on the contract is $4,500 and the maintenance margin is $3,750. At what price will the trader receive a maintenance margin call?A.$2.30B.$2.90C.$3.20D.$3.80Answer: B25.The S&P 500 index is trading at 1,025. The S&P 500 pays an expected dividendyield of 1.2% and the current risk-free rate is 2.75%. The value of a 3-month futures contract on the S&P 500 index is closest to:A.$1,028.98B.$1,108.59C.$984.86D.$1,025.00Answer: A26.The current spot price of gold is $325/oz and the price of 90-day gold futurescontract (nominal amount of 100 oz) is $315. If 90-day Treasury bills are trading at yields of 3.55% - 3.58% and storage and delivery costs are ignored, what is the potential arbitrage profit per contract?A.$1,266B.$1,286C.$1,334D.$1,344Answer: C27.Which of the following statements describing the role of a convenience yield inpricing commodity futures is true? The convenience yield:I.will cause contango in the futures pricing relationship.II.Effectively reduces the cost of carry in the futures pricing relationship.III.Eliminates the potential for arbitrage between the futures and spot price.IV.Accounts for additional costs for storing an asset in the futures pricing relationship.A.I onlyB.II onlyC.II, III, and IV onlyD.I and II onlyAnswer: B28.A firm is going to buy 10,000 barrels of West Texas Intermediate Crude Oil. Itplans to hedge the purchase using the Brent Crude Oil futures contract. The correlation between the spot and futures prices is 0.72. The volatility of the spot price is 0.35 per year. The volatility of the Brent Crude Oil futures price is 0.27 per year. What is the hedge ratio for the firm?A. 0.9333B. 0.5554C. 0.8198D. 1.2099Answer: A29.The hedge ratio is the ratio of derivatives to a spot position (or vice versa thatachieves an objective such as minimizing or eliminating risk. Suppose that the standard deviation of quarterly changes in the price of a commodity is 0.57, the standard deviation of quarterly changes in the price of a futures contract on the commodity is 0.85, and the covariance between the two changes is 0.3876. What is the optimal hedge ratio for a 3.-month contract?A.0.1893B.0.2135C.0.2381D.0.2599Answer: D30.Consider an equity portfolio with market value of USD 100M and a beta of 1.5with respect to the S&P 500 Index. The current S&P 500 index level is 1000 and each futures contract is for delivery of USD 250 times the index level. Which of the following strategy will reduce the beta of the equity portfolio to 0.8?A.Long 600 S&P 500 futures contractsB.Short 600 S&P 500 futures contractsC.Long 280 S&P 500 futures contractsD.Short 280 S&P 500 futures contractsAnswer: D31.Corporates normally use FRAs to:A.Lock-in the cost of borrowing in the futureB.Lock-in the cost of lending in the futureC.Hedge future currency exposuresD.Create future currency exposuresAnswer: A32.An investor has entered into a forward rate agreement(FRA) where she hascontracted to pay a fixed rate of 5 percent on $5,000,000 based on the quarterly rate in three months. If interest rates are compounded quarterly, and the floating rate is 2 percent in three months, what is the payoff at the end of the sixth month?The investor will:A.make a payment of $37,500.B.receive a payment of $37,500.C.make a payment of $75,000.D.receive a payment of $75,000.Answer: A33.Consider the following 6x9 FRA ,Assume the buyer of the FRA agrees to acontract rate of 6.35% on a notional amount of 10 million USD ,Calculate the settlement amount of the seller if the settlement rate is 6.85%. Assume a 30/360 day count basis.A.–12,500B.–12,290C.+12,500D.+12,290Answer: B34.XYZ Corporation plans to issue a 10-year bond 6 months from now. XYZ wouldlike to hedge the risk that interest rates might rise significantly over the next 6 months. In order to effect this, the treasurer is contemplating entering into a swap transaction. Under the swap, she should:A.Pay fixed and receive LIBORB.Pay LIBOR and receive fixedC.Either swap (a or b above) will workD.Neither swap (a or b above) will workAnswer: A35.Consider the following plain vanilla swap. Party A pays a fixed rate 8.29% perannum on a semiannual basis (180/360), and receives from Party B LIBOR+30 basis point. The current six-month LIBOR rate is 7.35% per annum. The notional principal is $25M. What is the net swap payment of Party AA.$20,000B.$40,000C.$80,000D.$110,000Answer: C36.A trader executes a $420 million 5-year pay fixed swap(duration 4.433) with oneclient and a $385 million 10year receive fixed swap(duration 7.581) with another client shortly afterwards. Assuming that the 5-year rate is 4.15 % and 10-year rate is 5.38 % and that all contracts are transacted at par, how can the trader hedge his net delta position?A.Buy 4,227 Eurodollar contractsB.Sell 4,227 Eurodollar contractsC.Buy 7,185 Eurodollar contractsD.Sell 7,185 Eurodollar contractsAnswer: B37.Assume an investor with a short position is about to deliver a bond and has fourbonds to choose from which are listed in the following table. The last settlement price is $95.75 (this is the quoted futures price). Determine which bond is the cheapest-to-deliver.Bond Quoted Bond Price Conversion Factor1 99 1.012 125 1.243 103 1.064 115 1.14A. Bond 1B. Bond 2C. Bond 3D. Bond 4Answer: C38.What is the lower pricing bound for a European call option with a strike price of80 and one year until expiration? The price of the underlying asset is 90, and the1-year interest rate is 5% per annum. Assume continuous compounding of interest.A.14.61B.13.90C.10.00D. 5.90Answer: B39.According to Put-Call parity, buying a call option on a stock is equivalent to:A.Writing a put, buying the stock, and selling short bonds (borrowing).B.Writing a put, selling the stock, and buying bonds (lending).C.Buying a put, selling the stock, and buying bonds (lending).D.Buying a put, buying the stock, and selling short bonds (borrowing). Answer: D40.Jeff is an arbitrage trader, and he wants to calculate the implied dividend yield ona stock while looking at the over-the-counter price of a 5-year put and call (bothEuropean-style) on that same stock. He has the following data:• Initial stock price = USD 85• Strike price = USD 90• Continuous risk-free rate = 5%• Underlying stock volatility = unknown• Call price = USD 10• Put price = USD 15What is the continuous implied dividend yield of that stock?A. 2.48%B. 4.69%C. 5.34%D.7.71%Answer: C41.The current price of a stock is $55. A put option with $50 strike price thatexpires in 3 months is available. If N(d1)=0.8133, N(d2)=0.7779, the underlying stock exhibits an annual standard deviation of 25 percent, and current risk free rates are 3.25 percent, the Black-Scholes value of the put is closet to:A.$0.75B.$1.25C.$1.50D.$5.00Answer: A42.Which of the following is the riskiest form of speculation using options contracts?A.Setting up a spread using call optionsB.Buying put optionsC.Writing naked call optionsD.Writing naked put optionsAnswer: C43.A long position in a put option can be synthetically produced by:A.Long position in the underlying and a short position in a call.B.Short position in the underlying and a long position in a call.C.Long position in the underlying and a long position in a put.D.Short position in the underlying and a short position in a put.Answer: B44.ABEX Corporation common stock is selling for $50.00 per share. Both anAmerican call option and a European call option are available on ABEX common, and each have identical strike prices and expiration dates. Which of the following statements concerning these two options is TRUE?A.Because the American and European options have identical terms and arewritten against the same common stock, they will have identical optionpremiums.B.The greater flexibility allowed in exercising the American option willnormally result in a higher market value relative to an otherwise identicalEuropean option.C.The American option will have a higher option premium, because theAmerican security markets are larger than the European markets.D.The European option will normally have a higher option premium because oftheir relative scarcity compared to American options.Answer: B45.Put option values increase as a result of increases in which of the followingfactors?I.V olatilityII.DividendsIII.Stock PriceIV.Time to expirationA.I, II, and IV onlyB.I, III, and IV onlyC.II and IV onlyD.I and III onlyAnswer: A46.Your firm has no prior derivatives trades with its counterparty Super Bank. Yourboss wants you to evaluate some trades she is considering. in particular, she wants to know which of the following trades will increase your firm’s credit risk exposure to Super Bank:I.Buying a put optionII.Selling a put optionIII.Buying a forward contractIV.Selling a forward contractA.I and II onlyB.II and IV onlyC.III and IV onlyD.I, III, and IV onlyAnswer: D47.Which of the following statements about a floor is true?A.floor is a put option and protects against a fall in interest ratesB.floor is a call option and protects against a fall in interest ratesC.floor is a put option and protects against a rise in interest ratesD.floor is a call option and protects against a rise in interest ratesAnswer: A48.You are given the following information about a call option:• Time to maturity = 2 years• Continuous risk-free rate = 4%• Continuous dividend yield = 1%• N(d1) = 0.64Calculate the delta of this option.A.-0.64B.0.36C.0.63D.0.64Answer: C49.Call and put option values are most sensitive to changes in the volatility of theunderlying when:A.both calls and puts are deep in-the-money.B.both puts and calls are deep out-of-the-money.C.calls are deep out-of-the-money and puts are deep in-the-money.D.both calls and puts are at-the-money.Answer: D50.What is the reason for undertaking a Vega hedging? To minimize the:A.Possibility of counterparty default risk.B.Potential loss as a result of a change in the volatility of the underlying sourceof risk.C.Adverse effect due to the government regulation.D.Potential loss as a result of a large movement in the underlying source ofrisk.Answer: B51.Suppose an existing short option position is delta-neutral, but has a gamma of−600. Also assume that there exists a traded option with a delta of 0.75 and a gamma of 1.50. In order to maintain the position gamma-neutral and delta-neutral, which of the following is the appropriate strategy to implement?A. Buy 400 options and sell 300 shares of the underlying asset.B. Buy 300 options and sell 400 shares of the underlying asset.C. Sell 400 options and buy 300 shares of the underlying asset.D. Sell 300 options and buy 400 shares of the underlying asset.Answer: A52.W hich of the following is not an assumption of the BS options pricing model?A. The price of the underlying moves in a continuous fashionB. The interest rate changes randomly over timeC. The instantaneous variance of the return of the underlying is constantD. Markets are perfect,i.e.short sales are allowed,there are on transaction costs or taxes,andmarkets operate continuously.Answer: B53.If risk is defined as a potential for unexpected loss, which factors contribute to therisk of a short call option position?A.Delta, vega, rhoB.Vega, rhoC.Delta, vega, gamma, rhoD.Delta, vega, gamma, theta, rhoAnswer: C54.If risk is defined as a potential for unexpected loss, which factors contribute to therisk of a long straddle position?A.Delta, vega, rhoB.Vega, rhoC.Delta, vega, gamma, rhoD.Delta, vega, gamma, theta, rhoAnswer: B55.Long a call on a stock and short a call on the same stock with a higher strike priceand same maturity is called:A. A bull spreadB. A bear spreadC. A calendar spreadD. A butterfly spreadAnswer: A56.Consider a bullish spread option strategy of buying one call option with a $30exercise price at a premium of $3 and writing a call option with a $40 exercise price at a premium of $1.50. If the price of the stock increases to $42 at expiration and the option is exercised on the expiration date, the net profit per share at expiration (ignoring transaction costs) will be:A.$8.50B.$9.00C.$9.50D.$12.50Answer: A57.An investor sells a June 2008 call of ABC Limited with a strike price of USD 45for USD 3 and buys a June 2008 call of ABC Limited with a strike price of USD40 for USD 5. What is the name of this strategy and the maximum profit and lossthe investor could incur?A.Bear Spread, Maximum Loss USD 2, Maximum Profit USD 3B.Bull Spread, Maximum Loss Unlimited, Maximum Profit USD 3C.Bear Spread, Maximum Loss USD 2, Maximum Profit UnlimitedD.Bull Spread, Maximum Loss USD 2, Maximum Profit USD 3Answer: D58.Which of the following actions would be most profitable when a trader expects asharp rise in interest rates?A.Sell a payer swaption.B.Buy a payer swaption.C.Sell a receiver swaption.D.Buy a receiver swaption.Answer: B59.Initially, the call option on Big Kahuna Inc. with 90 days to maturity trades atUSD 1.40. The option has a delta of 0.5739. A dealer sells 200 call option contracts, and to delta-hedge the position, the dealer purchases 11,478 shares of the stock at the current market price of USD 100 per share. The following day, the prices of both the stock and the call option increase. Consequently, delta increases to 0.7040. To maintain the delta hedge, the dealer shouldA.sell 2,602 sharesB.sell 1,493 sharesC.purchase 1,493 sharesD.purchase 2,602 sharesAnswer: D60.A risk manager for bank XYZ, Mark is considering writing a 6 month American put optionon a non-dividend paying stock ABC. The current stock price is USD 50 and the strike price of the option is USD 52. In order to find the no-atbitrage price of the option, Mark uses a two-step binomial tree model. The stock price can go up or down by 20% each period. Mark’s view is that the stock price has an 80% probability of going up each period and a 20% probability of going down. The risk-free rate is 12% per annum with continuous compounding.What is the risk-neutral probability of the stock price going up in a single step?A. 34.5%B. 57.6%C. 65.5%D. 80.0%Answer: B61.Given the following 30 ordered simulated percentage returns of an asset, calculatethe VaR and expected shortfall (both expressed in terms of returns) at a 90% confidence level.-16, -14, -10, -7, -7, -5, -4, -4, -4, -3, -1, -1, 0, 0, 0, 1, 2, 2, 4, 6, 7, 8, 9, 11, 12, 12, 14, 18, 21, 23A.VaR (90%) = 10, Expected shortfall = 14B.VaR (90%) = 10, Expected shortfall = 15C.VaR (90%) = 14, Expected shortfall = 15D.VaR (90%) = 18, Expected shortfall = 22Answer: B62.What is the correct interpretation of a $3 million overnight VaR figure with 99%confidence level?A.The institution can be expected to lose at most $3 million in 1 out of next100 days.B.The institution can be expected to lose at least $3 million in 95 out of next100 days.C.The institution can be expected to lose at least $3million in 1 out of next 100days.D.The institution can be expected to lose at most $6 million in 2 out of next100 days.Answer: C63.In the presence of fat tails in the distribution of returns, VaR based on thedelta-normal method would (for a linear portfolio):A.underestimate the true VaRB.be the same as the true VaRC.overestimate the true VaRD.cannot be determined from the information providedAnswer: A64.Value at risk (VaR) measures should be supplemented by portfolio stress testingbecause:A.VaR does not indicate how large the losses will be beyond the specifiedconfidence level.B.stress testing provides a precise maximum loss level.C.VaR measures are correct only 95% of the time.D.stress testing scenarios incorporate reasonably probable events.Answer: A65.Assume we calculate a one-week VaR for a natural gas position by rescaling thedaily VaR using the square-root rule. Let us now assume that we determine the “true” gas price process to be mean reverting and recalculate the VaR. Which of the following statements is true?A.The recalculated VaR will be less than the original VaRB.The recalculated VaR will be equal to the original VaRC.The recalculated VaR will be greater than the original VaRD.There is no necessary relation between the recalculated VaR and the originalVaRAnswer: A66.If a portfolio with a VaR of 200 is combined with a portfolio with a VaR of 500,the VaR of the combination could be:I.Less than 200.II.Less than 500.III.More than 200.IV.More than 500.A.I and IIB.III and IVC.I, II and IVD.II, III and IVAnswer: D67.Consider the following portfolio consisting only of stock Alpha. Stock Alpha has amarket value of $635,000 and an annualized volatility of 28%. Calculate the VaR assuming normally distributed returns with a 99% confidence interval for a 10-day holding period and 252 business days in a year. The daily expected return is assumed to be zero.A.$56,225B.$69,420C.$82,525D.$96,375Answer: C68.Babson Bank is interested in knowing the risk exposure of their assets for variousprobabilities and time horizons. Babson has estimated that the annual variance (based on a 250 day year) of their $638 million asset portfolio is 151.29. If Z1%, Z5%, Z10%, are 2.32, 1.65, and 1.28, respectively, which of the following statements is false? The maximum dollar loss that can be expected to be exceeded:A.5% of the time in any six month period is $64.74 millionB.1% of the time on any given day is $11.51 millionC.10% of the time in any given quarter is $50.22 millionD.1% of the time in any given week is $25.25 millionAnswer: A69.The VaR on a portfolio using a 1-day horizon is USD 100 million. The VaR usinga 10-day horizon is:D 316 million if returns are not independently and identically distributedD 316 million if returns are independently and identically distributedD 100 million since VaR does not depend on any day horizonD 31.6 million irrespective of any other factorsAnswer: B70.If stock returns are independently, identically, normally distribution and the annualvolatility is 30%, then the daily VaR at the 99% confidence level of a stock market portfolio is approximately。

FRM一级模考

FRM一级模拟题1 . An investor is following the real-time changes in the price of options on a particular asset. She notices that both a European call and a European put on the same underlying asset each have an exercise price of $45. The two options have six months to expiration and are both selling for $4. She also observes that the underlying asset is selling for $43 and that the rate of return on a 1-year Treasury bill is 6%. According to put-call parity, what series of transactions would be necessary to take advantage of any mispricing in this case?a. Sell the call, sell a T-bill equal to the present value of $45, buy the put, and buy the underlying asset.b. Buy the call, buy a T-bill equal to the present value of $45, sell the put, and sell the underlying asset.c. Buy the call, sell a T-bill equal to the present value of $45, sell the put, and buy the underlying asset.d. Sell the call, buy a T-bill equal to the present value of $45, buy the put, and sell the underlying asset.2. Suppose we plan on buying crude oil in one month to produce gasoline and heating oil for sale in two months. The 1-month futures price for crude oil is currently $55.00/barrel. The 2-month futures prices for gasoline and heating oil are $61.50/barrel and $58.50/barrel, respectively. What is the 5-3-2 crack (commodity) sprcad?a. $5.30/barrel.b. $12.75/barrel.c. $26.50/barrel.d. $32.81/barrel.3. The forward rate of a 3-month EUR/USD foreign exchange contract is 1.1565 USD per EUR. USD LIBOR is 4% and EUR LIBOR is 2%. The spot USD per EUR exchange rate is closest to:a. 1.1507.b. 1.1302.c. 1.1601.d. 1.1720.4. Which of the following statements concerning the capital asset pricing model (CAPM) and the capital market line (CML) is true? According to the:a. CAPM, systematic risk determines the expected return and unsystematic risk does not.b. CAPM, unsystematic risk determines the expected return and systematic risk does not.c. CML, systematic risk determines the expected return and unsystematic risk does not.d. CML, unsystematic risk determines the expected return and systematic risk does not.5. An analyst obtains statistics on return information for Vay Industries and Ranch Meatpacking as follows:Based on this information, what is the covariance between the two sets of returns, and what is the correlation coefficient?Covariance Correlation coefficienta. 5.98 0.32b. 5.98 0.42c. 6.52 0.32d. 6.52 0.42。

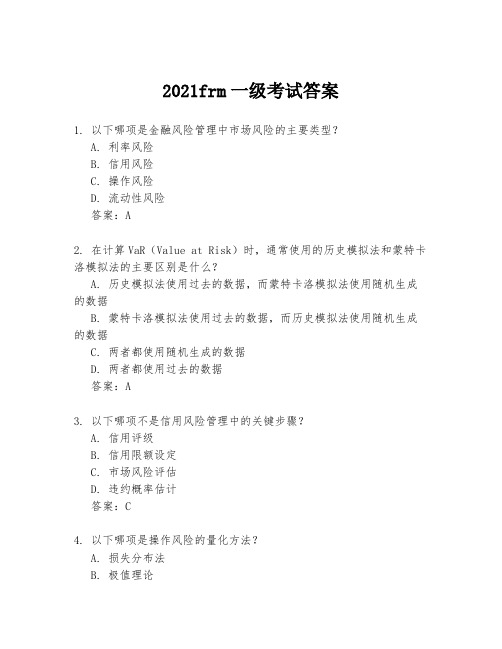

2021frm一级考试答案

2021frm一级考试答案1. 以下哪项是金融风险管理中市场风险的主要类型?A. 利率风险B. 信用风险C. 操作风险D. 流动性风险答案:A2. 在计算VaR(Value at Risk)时,通常使用的历史模拟法和蒙特卡洛模拟法的主要区别是什么?A. 历史模拟法使用过去的数据,而蒙特卡洛模拟法使用随机生成的数据B. 蒙特卡洛模拟法使用过去的数据,而历史模拟法使用随机生成的数据C. 两者都使用随机生成的数据D. 两者都使用过去的数据答案:A3. 以下哪项不是信用风险管理中的关键步骤?A. 信用评级B. 信用限额设定C. 市场风险评估D. 违约概率估计答案:C4. 以下哪项是操作风险的量化方法?A. 损失分布法B. 极值理论C. 敏感性分析D. 压力测试答案:A5. 金融衍生品的主要功能是什么?A. 提供流动性B. 风险转移C. 增加市场波动性D. 投机答案:B6. 以下哪项是利率衍生品?A. 股票期权B. 利率互换C. 信用违约互换D. 外汇远期合约答案:B7. 在计算债券的久期时,以下哪项是正确的?A. 久期是债券现金流的时间加权平均值B. 久期是债券现金流的金额加权平均值C. 久期是债券现金流的现值加权平均值D. 久期是债券现金流的利率加权平均值答案:C8. 以下哪项是市场风险管理中的关键因素?A. 风险识别B. 风险评估C. 风险监控D. 所有以上选项答案:D9. 以下哪项是流动性风险管理的主要策略?A. 资产负债匹配B. 信用风险管理C. 操作风险控制D. 市场风险评估答案:A10. 以下哪项是信用风险度量中的关键指标?A. 违约概率B. 预期损失C. 非预期损失D. 所有以上选项答案:D。

FRM一级每日一练

FRM一级每日一练1、Consid er a convertible bond that is trading at a conversion premium of 20 percent. If the value of the underlying stock rises by 25 percent, the value of the bond will:A.Rise by less than 25%.B.Rise by 25%.C.Rise by more than 25%.D.Remain unchanged.Correct answer: A解析:The convertible bond implicitly gives bondhol d ers a call option on the und erlying stock. The delta of this option will vary between 0 (when the option is extremely out of t e money) and 1 (when the option is extremely in the money). In this case, the bond is trading at a conversion premium of 20% so the delta must be somewhere between zero and one, and hence the price of the convertible bond will rise by less than the price of the und erlying stock.2、If a cash fl ow of $10,000 in two years’ time has a PV of $8,455, the annual percentage rate, assuming continuous compounding is CLOSEST to:A. 8.13%.B. 8.39%.C. 8.75%.D. 8.95%.Correct answer: B解析:Continuously compounded rate = In (FV/PV)/N = In (10000/8455)/ 2 =8.39%.3、The current values of a firm's assets and liabilities are 200 million and 160 million respectively. If the asset values are expected to grow by 40 million and liability values by 30 million within a year and if the annual standard deviation of these values is 50 million, the distance from default in the KMV model woul d be closest to:A. 0.8 standard deviations.B. 1.0 standard deviations.C. 1.2 standard deviations.D. Cannot not be determined.Correct answer: B解析:Distance from d efault = (Expected value of assets - Expected value of liabilities) / Standard deviation = (240 ~ 90)/ 50 = 1.0.4、What is the semiannual-pay bond equivalent yield on an annual-pay bond with a yiel d to maturity of 12.51 percent?A. 12.00%.B. 11.49%.C. 12.51%.D. 12.14%.Correct answer: D解析:The semiannual-pay bond equival ent yield of an annual-pay bond = 2 * [(1 + yield to maturity on the annual-pay bond) 0.5 - 1] = 12.14%.5、You want to test at the 0.05 l evel of significance that the mean price of luxury cars is greater than $80,000. A rand om sampl e of 50 cars has a mean price of $88,000. The population standard deviation is $15,000. What is the alternative hypothesis?A. The population mean is greater than or equal to $80,000.B. The population mean is l ess than $80,000.C. The population mean is not equal to $80,000.D. The population mean is greater than is $80,000.Correct answer: D解析:The alternate hypothesis is the statement which will be accepted if the null hypothesis is proven wrong. Therefore, we make whatever we are trying to test as the alternate hypothesis - in this case that the mean price of luxury cars is greater than $80,000, and the null hypothesis as the opposite ( the mean price of luxury cars is less than or equal to $80, 000). This probl em is a common example of how statisticians establish hypotheses by proving that the opposite (i.e. the null hypothesis) is false.6、Suppose that Gene owns a perpetuity, issued by an insurance company that pays $1,250 at the end of each year. The insurance company now wishes to replace it with a decreasing perpetuity of $1,500 decreasing at 1% p.a. without any change in the payment dates. At what rate of interest (assuming a flat yiel d curve) woul d Genebe indifferent between the choices?A. 4%.B. 5%.C. 6%.D. 9%.Correct answer: B解析:1,250 / r = 1,500 / (r + 1%) or, 1,250 x (r + 1 %) = 1,500 x r or, r = 12.5 / (1, 500 - 1,250) = 5%.7、Which of the foll owing is considered to be the responsibility of the legal risk manager?I. Inad equate d ocumentation of OTC d erivatives transactions.II. The enforceability of netting agreements in bankruptcy.III. Default on interest and principal payments.A.I only.B.II only.C.I and II only.D.I,II, and IIICorrect answer: D解析:Legal risk management is concerned with adequate documentation, public filings, compliance with regulatory entities, and some borrower impositions. The l egal manager is also involved in deciding if default has occurred and, of so, assisting with the enforcement of netting agreements.8、An analyst has constructed the foll owing t-test for a portfolio of financial securities whose returns are normally distributed:Number of securities = 40.HO: Mean return >=18 percent.Significance level = 0.1.What is the rejection point for this test?A. 1.304B. 1.684C. 2.021D. 2.023Correct answer: A解析:This is a one-tailed test with 39 degrees of freed om and significance l evel of 0.1. Looking up the Student's - distribution for DF = 39 and p = 0.1, we get the critical value or 1.304.9、Consid er an A-rated institution that funds itself in the wholesale market at LIBOR + 90bps. Which of the foll owing is the most attractive instrument for this firm to take exposure to an AAA – corporate issuer?A. Credit swap.B. Floating rate note.C. Credit-linked note.D. Fixed coupon bond.Correct answer: A解析:This firm has a fairly high funding cost. Funding itself at 90 bps over LIBOR and leading to AAA names at around LIBOR is a l oss making strategy, which rul es out the notes and the bond, The only way this firm can make money is by selling credit protection via a credit swap that does not require it to make a physical investment,10、Which of the foll owing statements about the Treynor ratio is correct?A. the Teynor ratio consid ers both systematic and unsystematic risk of a portfolio.B. the Teynor ratio is equal to the excess return of a portfolio over the risk - free rate divided by the total risk of the portfolio.C. the Teynor ratio can be used to appraise the performance of well - diversified portfolio.D. the Teynor ratio is derived from portfolio theory since it assesses a portfolio’s excess return relative to its risk.Correct answer: CA is incorrect - Treynor ratio consid ers only systematic risk of a well - diversified portfolio.B is incorrect - Treynor ratio denominator is beta of the portfolio.C is correct - this statement is correctD is correct - Treynor ratio is derived from CAPM and not portfolio theory.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。

V1_FRM一级习题(风险管理基础)