CPA会计英语教学课件8

大学课程《会计英语》PPT课件:Chapter 8 Unit 1

证券交易委员会

Forms of Business Organizations

The element of owners’ equity will differ depending on the nature of the organization. A business enterprise may be organized as: a single proprietorship a partnership a corporation.

(4) Unlimited Liabilities

Each partner is personally responsible for all the debts of the firm. The lack of any ceiling on the liability of a partner may deter a wealthy person from entering a partnership.

A proprietorship itself is not subject to taxation of income. Rather, the income or loss derived from the proprietorship is included and taxed in the personal tax return of the proprietor.

Chapter 8

Unit 1 Forms of Business Organizations Unit 2 Accounting for Owners’ Equity in

Different Forms of Organizations

CPA(英文介绍)PPT演示幻灯片

Chinese CPA system establishment and development

Certified Public accountants hereinafter referred to as CPA (Certified Public Accountant) is one of the accounting industry professional qualification examination.

CPA (Certified public accountant)

09注会(3)班 韩晓璐05 黄馨瑶09 张梦瑶44

1

Encyclopedia card

Certified public accountant ---is a certified public accountant certificate obtained according to law and accept entrust engaged in auditing accounting consulting and accounting services of the practicing personnel accounting firm is established according to law and undertakes the orgnaization of business of certified public accountants registered accountants executive business shall join a public accounting firm

3

• The law of the People's Republic of certified public accountants law in on October 31, 1993, the eighth National People's Congress standing committee meeting through the fourth time, on October 31, 1993, the People's Republic of ZhuXiLing st by 13, 1994 on January 1. By the end of 2010, the total nearly 154000 candidates all through the subject's test, and our country need to register accountant about 350000 people. With college degree or above school graduates, accounting or related field with the title of technology of intermediate above, can the unified national examination for certified public accountants.

会计专业英语PPT

Management accounting:

use both historical data in assisting management daily operations and in planning future operations.

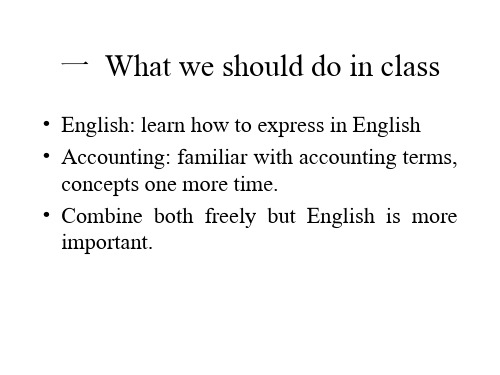

concepts one more time. • Combine both freely but English is more

important.

二 Improve English by ….

– Read textbook in class and after class – Remember new words – Answer questions in exercise is important – Overlook some parts while emphasizing some

• Financial accounting: provides external reports o outsiders, financial information.

2 Reporting management information to internal users

Internal users are senior management-level personnel.

• What do you think?

二 Functions

1 Reporting financial information to outside interested users

• Outside users are:investors,banks and other creditors,government agencies,general publics

会计英语 Unit (8)

45 units

What is the unit cost of the 35 units on hand at the end of the period as determined the perpetual inventory system by the lifo costing method?

Beginning inventory 40 units at $20

First purchase

50 units at $21

Second purchase

50 units at $22

Third purchase

50 units at $23

What is the unit cost of the 35 units on hand at the end of

the order in which they were incurred.

Exercises

Unit Eight

III. Choose the best answer.

1. If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an:

√D.Understatement of net income for the year by $7,500.

2. The inventory costing method that is based on the assumption that costs should be charged against revenue in the order in which they were incurred is:

会计英语八章 优质课件

Few companies that grant credit to customer get away from suffering credit losses. The losses due to uncollected accounts from customers are generally described as bad debts.

The answer is clear that granting credit results in high inventory turnover and increasing sales volume. Even though bad debits incurred, most of the product cost is recovered, and the return of income offsets the uncollectible accounts enough.

(2) notes receivable

(3) other receivable

Accounts receivable are amount due from customers. They arise from selling goods or services on credit. Accounts receivable are expected to be collected within one year and are classified as current assets on the balance sheet.

That is, bad debt is recorded only when actual loss is confirmed.

会计英语第八单元课件

二 Income Statement

1 Definition : ► Shows: ► (1)the results of operations for a business ► (2)matching revenue and the related expenses ► (3)for a particular accounting period (during a given time)

2 sources: ► BS/IS: TB ► CFS: account balances/changes/entries 3 style : ► BS/IS: manual or computerized ► CFS: hand prepare 4 format : Direct preparation Approach Indirect preparation Approach

►5

What the definition of cash flow statement? And how often dose it prepare? ► 6 Grasp the preparation of cash flow statement: format, heading and body, classifications ► 7 Prepare the statement of Owner’s Equity.

三 Cash flow statement:

1 Definition: ► cash--------- currency. (the amount of founds that can be accessed by the company at any time, or on demand) ► cash on hand/on deposit/short term investment ► cash equivalents ---------- investments which readily convertible to known amount of cash and be subject to an insignificant risk of changes in value.

注会综合·英语专题班·第八讲

18. 持续经营假设Both directors and auditors of an entity have responsibilities regarding going concern. ISA 570 states that the auditor needs to consider the appropriateness of management’s use of the going concern assumption. The auditors need to assess the risk that the company may not be a going concern. Where there are going concern issues, the auditor needs to ensure that the directors have made sufficient disclosure of such matters in the notes to the financial statements.管理层和审计人员对企业的持续经营都负有责任。

审计人员需要考虑管理层使用持续经营假设是否适当。

审计人员需要评价企业也许不是一个持续经营实体的风险。

当存在影响持续经营的事件,审计人员需要确定管理层在报表相关附注中就这类事件做出了充分披露。

19. 书面说明A written representation is a written statement by management provided to the auditor to confirm certain matters or to support other audit evidence.书面声明,是指管理层向注册会计师提供的书面陈述,用以确认某些事项或支持其他审计证据。

Unfortunately, written representations are internal sources of evidence, and are therefore subject to bias. They are therefore potentially unreliable forms of audit evidence. They do not,on their own, constitute appropriate evidence. They do not, on their own, constitute sufficient evidence.书面声明是内部证据,有可能存在偏见,因此本身是不可靠的审计证据,其本身不构成适当、充分的证据。

会计学英语电子版课件08

EFFECTS OF DIRECT WRITEOFF METHOD

THE ALLOWANCE METHOD

Allowance method

Required when bad debts are deemed to be material in amount

Uncollectible accounts are estimated At the end of each period Expense for the uncollectible accounts is

10

Review

a. b. c.

d.

Accounts receivable include Interest receivable. Advances to employees. Amounts customers owe from purchasing goods and/or services. Income taxes receivable.

9

RECOGNIZING ACCOUNTS RECEIVABLE

General Journal Date July 5 Account Titles Sales Returns and Allowances Accounts Receivable – Polo Company Debit 100 Credit

16

DIRECT WRITE-OFF METHOD

Direct write-off method

An entry is made for bad debts expense when an account is determined to be uncollectible at which time the loss is charged to Bad Debts Expense

注会英语课件

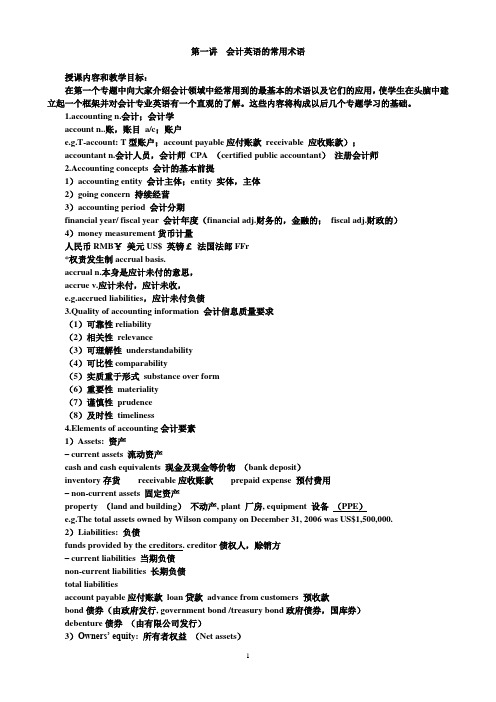

第一讲会计英语的常用术语授课内容和教学目标:在第一个专题中向大家介绍会计领域中经常用到的最基本的术语以及它们的应用,使学生在头脑中建立起一个框架并对会计专业英语有一个直观的了解。

这些内容将构成以后几个专题学习的基础。

1.accounting n.会计;会计学account n..账,账目a/c;账户e.g.T-account: T型账户;account payable应付账款receivable 应收账款);accountant n.会计人员,会计师CPA (certified public accountant)注册会计师2.Accounting concepts 会计的基本前提1)accounting entity 会计主体;entity 实体,主体2)going concern 持续经营3)accounting period 会计分期financial year/ fiscal year 会计年度(financial adj.财务的,金融的;fiscal adj.财政的)4)money measurement货币计量人民币RMB¥美元US$ 英镑£法国法郎FFr*权责发生制accrual basis.accrual n.本身是应计未付的意思,accrue v.应计未付,应计未收,e.g.accrued liabilities,应计未付负债3.Quality of accounting information 会计信息质量要求(1)可靠性reliability(2)相关性relevance(3)可理解性understandability(4)可比性comparability(5)实质重于形式substance over form(6)重要性materiality(7)谨慎性prudence(8)及时性timeliness4.Elements of accounting会计要素1)Assets: 资产– current assets 流动资产cash and cash equivalents 现金及现金等价物(bank deposit)inventory存货receivable应收账款prepaid expense 预付费用– non-current assets 固定资产property (land and building)不动产, plant 厂房, equipment 设备(PPE)e.g.The total assets owned by Wilson company on December 31, 2006 was US$1,500,000.2)Liabilities: 负债funds provided by the creditors. creditor债权人,赊销方– current liabilities 当期负债non-current liabilities 长期负债total liabilitiesaccount payable应付账款loan贷款advance from customers 预收款bond债券(由政府发行, government bond /treasury bond政府债券,国库券)debenture债券(由有限公司发行)3)Owners’ equit y: 所有者权益(Net assets)funds provided by the investors. Investor 投资者– paid in capital (contributed capital)实收资本– shares /capital stock (u.s.)股票retained earnings 留存收益同时记住几个单词dividend 分红beginning retained earnings ending retained earnings– reserve 储备金(资产重估储备金,股票溢价账户)e.g.The company offered/issued 10,000 shares at the price of US$2.30 each.4)Revenue: 收入sales revenue销售收入interest revenue利息收入rent revenue租金收入5)Expense: 费用cost of sales销售成本, wages expense工资费用6)Profit (income, gain):利润net profit, net income5.Financial statement 财务报表1)balance sheet 资产负债表2)income statement 利润表3)statement of retained earnings 所有者权益变动表4)cash flow statement 现金流量表6.Accounting cycle1)journal entries 日记账general journal总日记账general ledger总分类账trial balance试算平衡表adjusting entries 调整分录adjusted trial balance调整后的试算平衡表Financial statements 财务报表closing entry 完结分录2)Dr.—Debit 借Cr.—Credit 贷Double-entry system 复式记账7.Exercise 练习1)purchases of inventory in cash for RMB¥3,000 现金人民币3,000元购买存货Dr.inventory 3,000借:存货3,000Cr.cash 3,000 贷:现金3,0002)sales on account of US$10,000 赊销方式销售,收入10,000美元Dr.account receivable 10,000借:应收账款10,000Cr.sales revenue 10,000 贷:销售收入10,0003)paid RMB¥50,000 in salaries & wages 支付工资人民币50,000元Dr.wages & salaries expense 50,000 借:职工薪酬50,000Cr.bank deposit 50,000贷:银行存款50,0004)cash sale of US$1,180 销售收入现金1,180美元Dr.cash 1,180 借:现金1,180Cr.sales revenue 1,180贷:销售收入1,1805)pre-paid insurance for US$12,000 预付保险费12,000美元Dr.prepaid insurance 12,000借:预付保险12,000Cr.bank deposit 12,000贷:银行存款12,000第二讲存货授课内容和教学目标:本专题主要讲授与存货有关的英文术语,如期初和期末的存货的表达方式,以及不同的企业中的各种存货形式。

CPA(英文介绍) PPT课件

About the exam

• Examination system

• The state shall unified national examination system certified public accountants. The unified national examination certified public accountants, formulated by the financial department of the state council formulated by the Chinese institute of certified public accountants implementation.

Founded in 1988, the China association of certified accountants is under the leadership of the Treasury a national association, and also the only one in China accounting professional groups. Since 1991, our country of a registered accountant unified national examination system. Since 1993, held once a year, has held 18 times,

• The examiners unit

• The Treasury was registered accountant exam commission , the organization leadership for the unified national examination certified public accountants. The Treasury will test committee set up a CPA examination committee office, organize the implementation of the unified national examination certified public accountants.

注册会计师-《会计》英语基础讲义-专题一 固定资产和无形资产(8页)

专题一固定资产和无形资产目录01 考情分析02 词汇归纳总结03 重点、难点讲解04 同步系统训练考情分析有关固定资产和无形资产的内容在注会考试中属于非常重要的基础知识,可能并不单独以主观题形式进行考查,但是专业阶段主观题所考查的知识点中一般都会穿插其相关内容。

如与借款费用、会计估计变更及差错更正等内容的结合。

因此,要给予一定的重视。

词汇归纳总结重点、难点讲解考点一:固定资产的初始计量Initial Measurement of Fixed Assets1.外购固定资产 Purchased fixed assets外购固定资产的成本,包括购买价款、相关税费、使固定资产达到预定可使用状态前所发生的可归属于该项资产的运输费、装卸费、安装费和专业人员服务费等。

The cost of a purchased fixed asset consists of purchase price, relevant taxes, freights, loading fees, installment fees, professional service fees and other expenses that bring the fixed asset to the expected conditions for use and that may be relegated to the fixed asset.购买固定资产的价款超过正常信用条件延期支付,实质上具有融资性质的,固定资产的成本以购买价款的现值为基础确定。

If the payment for a fixed asset is delayed beyond the normal credit conditions and it is of financing nature in effect, the cost of the fixed asset shall be ascertained based on the present value of the purchase price.会计分录:Journal entry:借:固定资产(购买价款的现值)未确认融资费用(差额,应在信用期内采用实际利率法进行摊销)贷:长期应付款等(实际应支付价款)Dr:Fixed assets (the present value of the purchase price)Unrecognized financing expenses(the balance,which should be amortized within the credit period using the effective interest method)Cr:Long-term payable(the actual purchase price that should be paid)企业可能以一笔款项购入多项没有单独标价的固定资产。

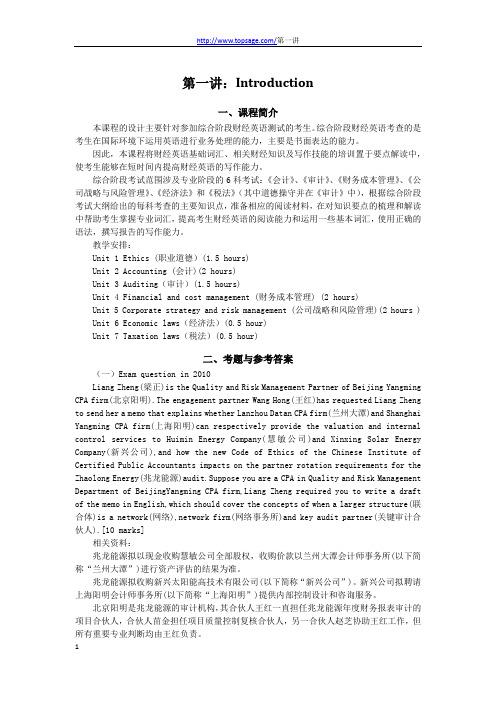

CPA综合英语课件

第一讲:Introduction一、课程简介本课程的设计主要针对参加综合阶段财经英语测试的考生。

综合阶段财经英语考查的是考生在国际环境下运用英语进行业务处理的能力,主要是书面表达的能力。

因此,本课程将财经英语基础词汇、相关财经知识及写作技能的培训置于要点解读中,使考生能够在短时间内提高财经英语的写作能力。

综合阶段考试范围涉及专业阶段的6科考试:《会计》、《审计》、《财务成本管理》、《公司战略与风险管理》、《经济法》和《税法》(其中道德操守并在《审计》中),根据综合阶段考试大纲给出的每科考查的主要知识点,准备相应的阅读材料,在对知识要点的梳理和解读中帮助考生掌握专业词汇,提高考生财经英语的阅读能力和运用一些基本词汇,使用正确的语法,撰写报告的写作能力。

教学安排:Unit 1 Ethics (职业道德)(1.5 hours)Unit 2 Accounting (会计)(2 hours)Unit 3 Auditing(审计)(1.5 hours)Unit 4 Financial and cost management (财务成本管理) (2 hours)Unit 5 Corporate strategy and risk management (公司战略和风险管理)(2 hours ) Unit 6 Economic laws(经济法)(0.5 hour)Unit 7 Taxation laws(税法)(0.5 hour)二、考题与参考答案(一)Exam question in 2010Liang Zheng(梁正)is the Quality and Risk Management Partner of Beijing Yangming CPA firm(北京阳明).The engagement partner Wang Hong(王红)has requestedLiang Zheng to send her a memo that explains whether Lanzhou Datan CPA firm(兰州大潭)and Shanghai Yangming CPA firm(上海阳明)can respectively provide the valuation and internal control services to Huimin Energy Company(慧敏公司)andXinxing Solar Energy Company(新兴公司),and how the new Code of Ethics of the Chinese Institute of Certified Public Accountants impacts on the partner rotation requirements for the Zhaolong Energy(兆龙能源)audit.Suppose you are a CPA in Quality and Risk Management Department of BeijingYangming CPA firm,Liang Zheng required you to write a draft of the memo in English,which should cover the concepts of when a larger structure(联合体)is a network(网络),network firm(网络事务所)and key audit partner(关键审计合伙人).[10 marks]相关资料:兆龙能源拟以现金收购慧敏公司全部股权,收购价款以兰州大潭会计师事务所(以下简称“兰州大潭”)进行资产评估的结果为准。

立信《会计专业英语》课件Lesson-Eight

A common example of a deferred credit is a government grant.

The grant is shown as a separate item or under creditors in the balance sheet, and an annual amount is transferred to the profit and loss account until the deferred credit balance is brought to nil.

An accrual is a current liability on the balance sheet and will be charged under expenses in the profit and loss account.

New words, Phrases and Special Terms

A basis of apportionment is always required. For example, local authority business rates for

premises are seldom incurred by individual cost centers, therefore floor area is often used as a basis of apportionment to share these costs between appropriate cost centers.

Lesson Eight

Adjusting Procedures

New words, Phrases and Special Terms

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Accounting English

Type 1---Apportioning recorded costs

Rent Expense Prepaid rent

580 580

1a.

Prepaid rent expired, $580.

Accounting English

Type 1---Apportioning recorded costs

Accounting English

Type 3--- Accruing unrecorded expenses

3b. Accrued advertising expense at the end of this month, $1,000.

Advertising Expense Accounts Payable

Accounting English

Based upon accrual accounting

Why is the adjusting step of the accounting cycle necessary?

Accounting English

Part 2 Presentation ---Purpose of adjusting (Why)

Accounting English

Lesson Eight

Adjusting Procedures

Lesson one

Steps in the accounting cycle

Close temporary accounts

Prepare financial statements

Adjust the general ledger accounts

Prepare adjusted trial balance

Accounting English

Part 2 Presentation ---Four Types of Adjusting Entries

1

2

3

4

Apportioning recorded costs

Apportioning recorded revenue

Accounting English

Part 1 Words and Phrases

• Accrue v.t., v.i. come as a natural growth or development. • If you keep your money in the Savings Bank, interest accrued. • Accrued interest is interest due, but not yet paid or received. • Accruing unrecorded expenses • Accruing unrecorded revenue

In order to achieve proper matching of costs and expenses with the relative revenue earned to determine a meaningful net income figure for each accounting period .

Depreciation Expense 700 Accumulated Depreciation 700

1b.

Depreciation for the month, $700.

Accounting English

Type 1---Apportioning recorded costs

Supplies Expense Supplies on Hand

Accruing unrecorded expenses

Accruing unrecorded revenue

Accounting English

Type 1---Apportioning recorded costs

Apportioning recorded costs

Assets

Expense

Accounting English

Terms --Accounting Basis

1

2

ac basis accounting

Accounting English

Terms --Accounting Basis

Accounting system

4

•Summary

Accounting English

Part 1 Words and Phrases

Words to Drill Apportion Accrue Expire Align

Terms Accrual basis accounting Cash basis accounting Periodic inventory system Perpetual inventory system

880 880

1c.

Supplies used during the month, $ 880.

Accounting English

Type 2--- Apportioning recorded revenue

Apportioning recorded revenue

liability

revenue

Post transaction to the ledger

Prepare trial balance Journalize and post adjusting entries Prepare financial statements

Journalize and post closing entries

Part 2

Presentation

a. Why is the adjusting step of the accounting cycle necessary? b. When does the adjusting step occur? c. How to journalize the adjusting entries?

Accounting English

Part 1 Words and Phrases

• Apportion---- v.t. divide; distribute; give as a share • I have apportioned you different duties each day of the week. • This sum of money is to be apportioned among the six boys. • Apportioning recorded costs to periods benefited. • Apportioning recorded revenue to periods in which it is earned.

Perpetual inventory system

Accounting English

Terms –Inventory Accounting System

Purchases are recorded as they occur, but the ending balance of inventory and the cost of good sold are not determined Text until the end of the period after counting inventory.

Accrual basis

Cash basis

are recognized when cash is collected; Expenses are recognized when cash is paid for the Accounting English goods and services.

Post to general ledger accounts

Record in journals

Analyze transactions from source documents

Accounting English

Lesson Eight Adjusting Procedures

1 2 3

•Words and Phrases presentation •Exercises

Accounting English

1,000 1,000

Type 4--- Accruing unrecorded revenue

Interest Receivable Interest Revenue

Accounting English

Part 1 Words and Phrases

• Expire v.i. (of a period of time )come to an end • When does your driving license expire? • At the end of each accounting period, the estimated portion of the outlay that has expired during the period or that has benefited the period must be transferred from an asset account to an expense account.

Accounting English

Part 1 Words and Phrases

• Align v.t. bring, come, into agreement, close cooperation etc (with) • Adjusting entries made to align revenue and expense with the appropriate periods consist of four types: (1) Apportioning recorded costs . (2) Apportioning recorded revenue. (3) Accruing unrecorded expenses. (4) Accruing unrecorded revenue.