财务会计英语版课后答案

财务会计英语 练习及答案ch03

36.If the adjustment to recognize expired insurance at the end of the period is inadvertently omitted, the assets at the end of the period will be understated.

ANS:TDIF:2OBJ:02

13.An adjusting entry would adjust an expense account so the expense is reported when incurred.

ANS:TDIF:2OBJ:02

14.An adjusting entry to accrue an incurred expense will affect total liabilities.

ANS:TDIF:2OBJ:02

15.The difference between deferred revenue and accrued revenue is that accrued revenue has been recorded and needs adjusting and deferred revenue has never been recorded.

ANS:TDIF:4OBJ:03

34.The balance in the prepaid insurance account before adjustment at the end of the year is $4,000. The amount of the journal entry required to record insurance expense will be $2,500 if the amount of unexpired insurance applicable to future periods is $1,500.

财务会计英文影印版第十版课后练习题含答案 (2)

财务会计英文影印版第十版课后练习题含答案简介本文档为《财务会计英文影印版第十版》的课后练习题及答案。

该书是一本介绍财务会计的教材,涵盖了财务会计理论和实践,适用于财务会计初学者。

练习题Chapter 11.1 Expln the difference between management accounting and financial accounting.1.2 Expln the purpose of financial statements.1.3 Expln the role of the audit committee.1.4 Expln the difference between the balance sheet and the income statement.Chapter 22.1 Expln the difference between revenue and profit.2.2 Expln the difference between cash basis accounting and accrual basis accounting.2.3 Expln the purpose of the statement of cash flows.Chapter 33.1 Expln the difference between current and non-current assets.3.2 Expln the difference between current and non-current liabilities.3.3 Expln the difference between financing activities and investing activities.Chapter 44.1 Expln the purpose of the double-entry accounting system.4.2 Expln the difference between debits and credits.4.3 Expln the purpose of the trial balance.Chapter 55.1 Expln the difference between the cost of goods sold and operating expenses.5.2 Expln the purpose of the income statement.5.3 Expln the difference between gross profit and net profit.答案Chapter 11.1 Management accounting is concerned with providing information for internal decision-making, while financial accounting is concerned with providing information to external users.1.2 The purpose of financial statements is to provide information about an entity’s financial performance, financial position, and cash flows.1.3 The audit committee is responsible for overseeing the financial reporting process and ensuring the integrity of financial statements.1.4 The balance sheet shows an entity’s financial position at a specific point in time, while the income statement shows an entity’s financial performance over a period of time.Chapter 22.1 Revenue represents the amounts earned from the sale of goods or services, while profit represents the difference between revenue and expenses.2.2 Cash basis accounting recognizes revenue and expenses when cash is received or pd, while accrual basis accounting recognizes revenue and expenses when they are earned or incurred, regardless of when cash is received or pd.2.3 The statement of cash flows is used to show the inflows and outflows of cash from operating, investing, and financing activities.Chapter 33.1 Current assets are expected to be converted to cash within one year, while non-current assets are expected to be held for more than one year.3.2 Current liabilities are expected to be pd within one year, while non-current liabilities are expected to be pd after one year.3.3 Financing activities involve obtning funds from external sources and paying dividends to shareholders, while investing activities involve acquiring and disposing of property, plant, and equipment, and other long-term investments.Chapter 44.1 The double-entry accounting system ensures that everytransaction is recorded in two accounts, with equal debits and credits,in order to mntn the equality of debits and credits in the accounting equation.4.2 Debits are used to record increases in assets and expenses and decreases in liabilities and equity, while credits are used to record increases in liabilities and equity and decreases in assets and expenses.4.3 The trial balance is a list of all the accounts in the ledgerwith their balances, used to ensure that the total of the debits equals the total of the credits.Chapter 55.1 The cost of goods sold represents the cost of the goods or services sold by a company, while operating expenses represent the other costs of running a business.5.2 The income statement shows a company’s revenue, expenses, andnet income or loss for a period of time.5.3 Gross profit represents revenue minus the cost of goods sold, while net profit represents gross profit minus operating expenses.结论本文档为《财务会计英文影印版第十版》课后练习题及答案,涵盖了财务会计的基本理论和实践。

财务会计课后习题答案(英文原版)第3单元

2A

Simple

3A 4A 5A

Moderate Moderate Moderate

*6A*

Moderate

1B

Simple

2B

Simple

3B 4B 5B

Moderate Moderate Moderate

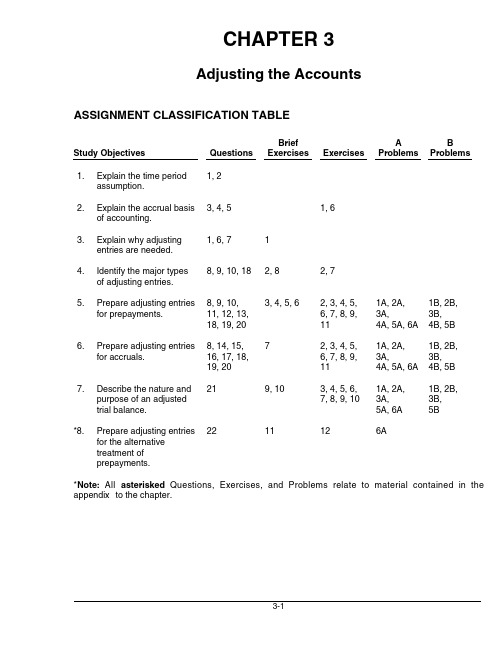

3-2

Correlation Chart between Bloom’s Taxonomy, Study Objectives and End-of-Chapter Exercises and Problems

1A, 2A, 3A, 4A, 5A, 6A 1A, 2A, 3A, 4A, 5A, 6A 1A, 2A, 3A, 5A, 6A 6A

1B, 2B, 3B, 4B, 5B 1B, 2B, 3B, 4B, 5B 1B, 2B, 3B, 5B

*6.

Prepare adjusting entries for accruals.

7

*7.

Describe the nature and purpose of an adjusted trial balance. Prepare adjusting entries for the alternative treatment of prepayments.

9, 10

*8.

22

11

12

Study Objective Q3-1 Q3-3 Q3-4 Q3-1 Q3-6 Q3-8 Q3-9 Q3-8 Q3-9 Q3-10 Q3-11 Q3-12 Q3-13 Q3-19 Q3-20 Q3-17 Q3-18 BE3-3 BE3-4 BE3-5 BE3-6 E3-2 E3-3 E3-4 E3-5 E3-6 E3-7 E3-8 E3-9 E3-11 P3-1A P3-2A P3-3A Q3-10 Q3-18 BE3-2 BE3-8 E3-7 E3-2 P3-4A E3-11 P3-5A P3-6A P3-1B P3-2B P3-3B P3-4B P3-5B Q3-7 BE3-1 Q3-5 E3-6 Q3-2 E3-1 Knowledge Comprehension Application Analysis Synthesis Evaluation

财务会计英文影印版第十版课后练习题含答案

Financial and Managerial Accounting English Version Photocopy Tenth Edition Exercise Questions withAnswersIntroductionThe Financial and Managerial Accounting English Version Photocopy Tenth Edition Exercise Questions with Answers is a comprehensive guide for accounting students to practice and sharpen their skills infinancial and managerial accounting. This guide includes a wide range of exercise questions with detled answers to help students better understand complex accounting concepts. The guide is designed to be an essential study tool for accounting students and professionals who are preparing for certification exams or looking to improve their accounting skills.FeaturesThe guide contns the following features:prehensive coverage of financial and managerialaccounting topics.2.A wide range of exercise questions with detled answers.3.Clear and concise explanations of complex accountingconcepts.4.Easy-to-use format.5.All questions are organized by chapter and topic for easyreference.ContentsThe guide includes the following chapters:1.Accounting in Action2.The Recording Process3.Adjusting the Accountspleting the Accounting Cycle5.Accounting for Merchandising Operations6.Inventories7.Fraud, Internal Control, and Cash8.Accounting for Receivables9.Plant Assets, Natural Resources, and Intangible Assets10.Liabilities11.Corporations: Organization, Stock Transactions, andDividends12.Long-Term Liabilities: Bonds and Notes13.Investments and Fr Value Accounting14.Statement of Cash Flows15.Financial Statement Analysis16.Managerial Accounting Concepts and Principles17.Job Order Costing18.Process Costing19.Cost Behavior and Cost-Volume-Profit Analysis20.Budgeting21.Performance Evaluation Using Variances from StandardCosts22.Performance Evaluation for Decentralized Operations23.Differential Analysis and Product PricingEach chapter includes a series of exercise questions with answers.How to Use the GuideThe guide is designed to be an essential study tool for accounting students and professionals who are preparing for certification exams or looking to improve their accounting skills. Students can use the guide to practice and sharpen their accounting skills. The guide can be used in conjunction with textbooks, lectures, and other study materials. Students are encouraged to work through e ach chapter’s exercises in order, starting with the easier exercises and progressing to the more difficult exercises.ConclusionThe Financial and Managerial Accounting English Version Photocopy Tenth Edition Exercise Questions with Answers is a comprehensive guide for accounting students to practice and sharpen their skills infinancial and managerial accounting. This guide includes a wide range of exercise questions with detled answers to help students better understand complex accounting concepts. The guide is an essential study tool for accounting students and professionals who are preparing for certification exams or looking to improve their accounting skills.。

中级财务会计英文版.课后答案(Chap03)

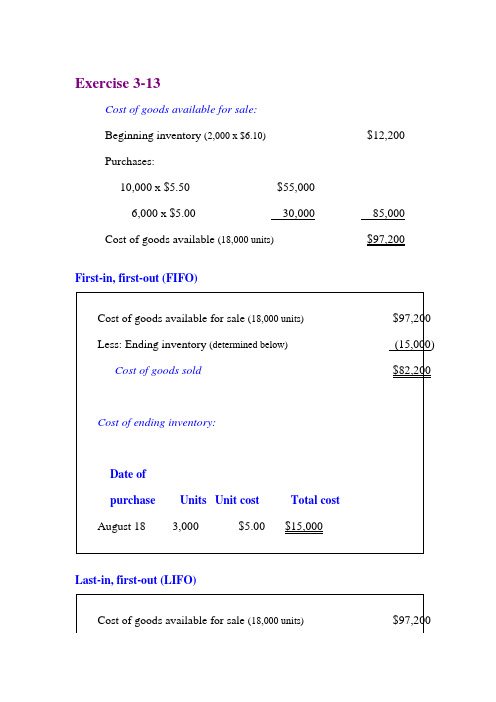

Cost of goods available for sale:

Beginning inventory(600 x $80)$ 48,000

Purchases:

1,000 x $ 95$95,000

800 x $10080,000175,000

Cost of goods available(2,400 units)$223,000

First-in, first-out (FIFO)

Cost of goods available for sale(2,400 units)$223,000

Less: Ending inventory(below)(80,000)

Cost of goods sold$143,000

Cost of ending inventory:

6,000(from 8/8 purchase)5.5033,000

Aug. 254,000(from 8/8 purchase)5.5022,000

3,000(from 8/18 purchase)5.0015,000

Total15,000$82,200

Ending inventory= 3,000 units x $5.00 =$15,000

Cost of ending inventory:

Date of

purchaseUnitsUnit costTotal cost

August 183,000$5.00$15,000

Last-in, first-out (LIFO)

Cost of goods available for sale(18,000 units)$97,200

6,000 @ $5.00

财务会计英语版课后答案

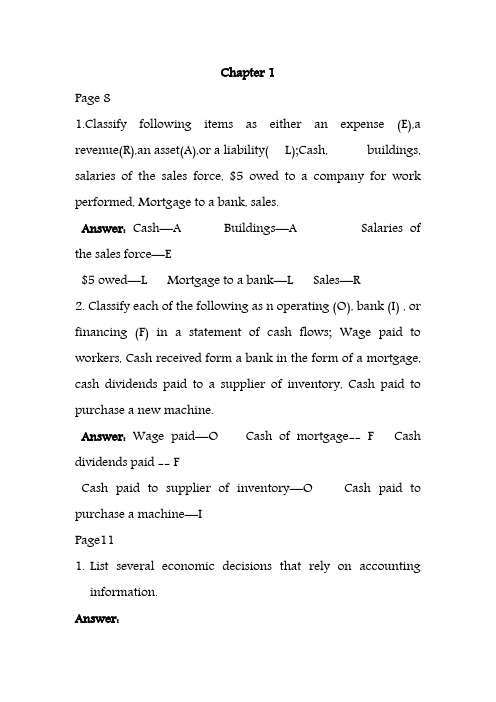

Chapter 1Page 81.Classify following items as either an expense (E),a revenue(R),an asset(A),or a liability( L);Cash, buildings, salaries of the sales force, $5 owed to a company for work performed, Mortgage to a bank, sales.Answer:Cash—A Buildings—A Salaries of the sales force—E$5 owed—L Mortgage to a bank—L Sales—R2. Classify each of the following as n operating (O), bank (I) , or financing (F) in a statement of cash flows; Wage paid to workers, Cash received form a bank in the form of a mortgage, cash dividends paid to a supplier of inventory, Cash paid to purchase a new machine.Answer:Wage paid—O Cash of mortgage-- F Cash dividends paid -- FCash paid to supplier of inventory—O Cash paid to purchase a machine—IPage111.List several economic decisions that rely on accounting information.Answer:·Whether to grant a loan·How much to pay for a share of common stock.·Whether to grant a rate increase to an electric utility·How much in damages the loser of a lawsuit must pay ·How much of a bonus to pay a plant manager·Whether to enter a new market2. Why do financial statements have footnotes, and what kinds of information might you find in them?Answer:Financial statements have footnotes because financial disclosure is a complex business. The notes tell us some of the specifics about the company environment , what accounting methods the company has used, what the accounting numbers might be if alternative methods had been used, and some of the major contingencies that are not formally included in the statement proper.Page 201.Describe the process of setting accounting standards. What are the roles of all the parties you mention?Answer:The FASB, a private, not-for-profit organization ,sets GAAP in the U.S. It publicly declares an agenda, promulgates "ExposureDrafts" of proposed standards, holds open meetings, and invites input from interested parties. The FASB has been delegated this authority by the SEC, a government agency with legal authority to determine GAAP.2.Think of an example, like the executive compensation example in the chapter, where incentives might exist to bias accounting numbers one way or another.Answer:There are other examples, but here is one that is different. A taxpayer has incentives to bias reported income downward in order to minimize income tax payments. However, it is important to understand that tax accounting rules are different from GAAP, and this book is about GAAP. Chapter 14 covers GAAP for taxes in more detail.Other examples include:·An entrepreneur seeking a loan from a bank or funding from a venture capitalist might have incentives to bias accounting numbers to look favorable.·A firm that is subject to scrutiny for earning excess profits(e.g.,an oil company)might have incentives to bias accounting numbers to look less favorable.·A utility subject to rate regulation might have an incentive tobias accounting numbers to look less favorable in order to gain more generous increases in its rates. (At this writing, there is a rather severe controversy about whether electric utilities in California are genuinely in financial difficulty and should be allowed to continue to impose large rate increase.)Chapter 2Page 381 Define assets, liabilities, and equities.Gave an example ofeach. How are assets valued? How are liabilities valued? Answer:An asset is a probable future economic benefit obtained or controlled by an entity as a result of a past transaction. Cash marketable securities, accounts receivable, inventories, prepaid expenses, patents, copyrights, trademarks, and property, plant and equipment are all examples of assets. A liability isa probable future sacrifice of economic benefits arisingfrom present obligations of an entity to transfer assets or provide services as a result of a past transaction or event.Accounts payable, accrued liabilities, unearned revenues, warranties, and bonds payable are all examples of liabilities.Accounting valuation of assets uses severaldifferent methods, including market value, expected realizable value, lower of cost or market, present value of future cash flows, and historical cost. Accounting valuation of liabilities is the expected amount that will be paid, perhaps adjusted for the time value of money.2. Explain what is meant by the entity concept. Answer:The entity is the person or organization about which accounting's financial history is being written.3 .A company signs a ten-year employee contract with a vicepresident. The salary is $ per year, guaranteed. Is this contract an asset? Would it appear on the balance sheet?Explain.Answer:The rights conveyed by the contrat may be an asset from an economic point of view, but they are not an asset under GAAP. The contract would not appear on the balance sheet as an asset, because GAAP does not record executory contracts, which are contracts that require future performance form both parties. That is ,GAAP views the contract as determining what services will be provided, no asset is recognized under GAAP.(Neither is a liability for payment recognized until services have beenperformed.)4 .A company purchased a parcel of land 10 years ago at a cost of $.The land has recently been appraised at $. At what value is the land carried in the balance sheet? How does the appraisal affect the carrying value in the balance sheet? Answer:The land is on the balance sheet at its historical cost of $.The carrying value of the land is unaffected by the appraisal. Page 421、Define debit and credit .What kind of balance ,debit or credit ,would you expect to find in the inventory T-account?In the Common Stock T-account?Answer:A debit is an entry on the left side of a T-account. A credit is an entry on the right side of a T-account. We would except to find a debit balance in Inventory, and credit balances in Bonds Payable and Common Stock. The reason is the convention that increases in assets are debits and increases in liabilities and equities are credits.2、If the trial balances, it means that you have analyzed all the effects of transactions correctly. True or false?Explain.Answer:False. A balanced means that the trial balance is consistent, not necessarily correct. For example. If an arbitrary entry is made that debits Cash and credits Common Stock for an equal amount, the trial balance will balance but it will be wrong. An accounting can receipt of cash and the issuance of common stock, but it alone can not make cash or additional common shares.3﹑Suppose Web sell leases a portion of its space to another company. Web sell’s accounts are debited and credited to record this transaction?Answer:Web sell would debit Cash and a liability, Rent Received in Advance, for the prepayment.Chapter 3Page 571. Define revenue and expense. How does one decide to list an item as revenue in an income statement? What is matching? Answer:Revenues are increases in net assets resulting from operations over a period of time .Expense are decreases in net assets resulting from operations over a period of time .Revenue isrecognized the earnings process is substantially complete , a transaction2. Give an example not found in the text , of an expense that is paid for in cash in a prior accounting period .In a subsequent accounting period.Answer:There are many allowable responses . An example is a patent that is purchased and paid for in one year and used in next .3. Give an example, not found in the text , of a revenue that is received in cash in a prior accounting period . In a subsequent accounting period .Answer:An example is a house painting contractor that receives payment for one-third of the contract price before beginning the painting .4. Explain why it is right to think of an asset as a cost and an expense as an expired cost .Answer:An asset is a future benefit . And there is an opportunity cost associated with not selling it for cash or exchanging it to settleChapter 6Page 120:1.The following table lists the adjustments and has an X in thecolumn indicating the approach:2. We first take adjustment for prepaid insurance and insurance expense. It would be easy to think of this adjustment as focusing on how much of the insurance coverage remained, as opposed to how much was used. In fact, the same type of logic could be used---computing a monthly rate for the coverage and applying that to the months reminding, instead of the months used.Now take adjustment for depreciation expense and accumulated depreciation. Estimating the value of the equipment at year end might be easy, for example, if there is a market for used equipment, or very difficult, for example, if the equipment was specially designed for Websell. Once a value estimate for the equipment at year end is obtained, depreciation expense would be the change in value over the year.Page 1231.$5000×(1+0.06)^10=$5000×1.79085=$8954.242.$5000×(1+0.06/2)^(10×2)=$5000×(1+0.03)^20=$5000×1.80611=$9030.563. $1000×(1.05)^3+$1000×(1.05)^2+$1000×(1.05)^1=$3310.134. ($1000×0.05/5)^13+$1000×(1+0.05/5)^10+$1000×(1+0.05/5)^5=($1000×(1.01)^15)+($1000×(1.01)^10)+($1000×(1.01)^5) =$1160.97+$1104.62+$1051.01=$3316.6Page 1241.x×.(1.07)^3=$3000 x=$3000/(1.07)^3=$2448.892. Calculate the present value at 10% of $1300 received two years from now. If that is greater than $1000, you are better offwith the $1300 to be received in two years. If its present value is less that $1000, you better off with $1000 now. $1300/(1.10)^2=$1074.38Therefore, you are better off receiving $1300 two years from now.Another way to do this problem is to take the future value at 10% of $1000. At the end of two years, the $1000 would compound up to:$1000×(1.10)^2=$1210,Which is less than you would have at that point if you took the $1300.3.The most I would be willing to pay is the present value at 8% of the stream of $1000 payment:$1000/(1.08)^1+$1000/(1,08)^2+$1000/(1,08)^3=$925.926+857.339+793.832=$ 2577.1(rounded)Chapter 8Page 1681.Aging takes the balance in accounts receivable at the end of the year, and sorts it by how long ago the transaction occurred that gave rise to that receivable. Experience has shown that “older” accounts have less likelihood of ever being collected.Percentages of likely uncollectibles for each category are applied to the totals in that category , and the results added to obtain an estimate of the allowance for uncollectibles required to value properly the estimated amount that will be collected from the accounts receivable. The bad debts expense then falls out as a “plug” in the allowance for uncollectibles.The percentage-of-sales method just estimates bad debt expense as a percent of sales, and plug the balance in the allowance account.2. Cash (118)Accounts receivable (118)12/31/2003(to recognize collection of cash from companies owing service co. from 2002 sales)Allow ance for doubtful accounts (7)Accounts receivable (7)12/31/2003(to write off accounts we know will not be collected) Ac counts receivable (125)Sales reven ue (125)12/31/2003(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2003, we would record.06×$=$7500 in baddebts expense.B ad debts expense………………………………………7.5 Allowan ce for doubtful accounts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accounts(10.5 is the “plug”,i.e., the number that drops out)Now we move to 2004, where events now proceed as expected . Collections are $117.5 thousand. Cash………………………………………………..117.5 Accounts receivable…………………………………117.512/31/2004(to recognize collection of cash form companies owing service co. from 2003 sales)Allowance for doubtful ac counts………………………7.5 Accounts receivable………………………………….7.512/31/2004(to write off accounts we know will not be collected)Accounts receivable (125)Sales revenue (125)12/31/2004(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2004, we would record.06×$=$7500 in bad debts expense.Bad debts expense……………………………………7.5 Allowance for doubtful acco unts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)The allowance for doubtful accounts using the peentage-of-sales method looks like this:Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accountsOnly the entries recording bad debt expense are different using the aging method. Instead of the above entries recording bad debt expense, we would have the following analysis: Each year, we would adjust the balance in the allowance for doubtful accounts so that the net receivable ends up at $. That is, we would solve $-X=$,and find that the ending balance in the allowance for doubtful accounts must be $7500.Analyzing the account, we would determine that at 12/31/2003 we must add $4500 to the allowance for doubtful accounts: Bad debts expense………………………………..4.5 Allowanc e for doubtful accounts…………………….4.512/31/2004(to record bad debt expense in anticipation of not collecting 100% of receivables)At 12/31/2004, we must add $7500 to the allowance for doubtful accounts:Bad debts expense………………………………..7.5 Allowan ce for doubtful accounts…………………….7.512/31/2004(to record bad debt expense in anticipation of not collecting 100% of receivables)Using aging, the allowance for doubtful accounts T-account looks like this:Method two: focus on the ending balance in the allowance for doubtful accounts.Allowance for doubtful accountsChapter 9Page 1831.LIFO is last-in first-out. It means that in computing ending inventoryand cost of goods sold, the cost of items sold is assigned in reverse chronological order of their purchase, beginning from the most regent items purchased in a period. FIFO is first-in, first-out .It means that in computing ending inventory and cost of goods sold, the cost of items sold is assigned in chronological order of their purchase, beginning from the goods on hand at the beginning of the period. Average cost means that in computing ending inventory and cost of goods sold, the average unit cost of the beginning inventory and items purchased in a period is used to determine the cost of goods sold and remaininginventory.2.Yes, it is still a positive net present value project. In fact, its netpresent value is higher than when the purchase was made at$1.05 per unit, since the cash outflow is reduced but the cash inflow remains the same. The cash outflow on 12/31/01 when purchases are at $0.95 per unit is $114.This means the net cash flow at 12/31/01 is ($4) instead of ($16),and the NPV for Widget Company is:NPV=-100-$4/1.1+$10/ (1.1^2) +$144/ (1.1^3) =$12.82First, we redo the case of FIFO. The inventory T-account is:Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Net incomes are:Widget Incomes using FIFONow we redo the case of FIFO. First, the inventory T-account is: Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Net incomes are:Page 186To calculate the market-to-book ratios and accounting returns on equity: Market-to-book Ratios under Average CostAccounting Rates of Return under Average CostCollecting the results for FIFO from the chapter and these results for average cost, we have:Market-to-book Ratios under Various Cost Flow AssumptionAccounting Rates of Return under Various Cost Flow AssumptionAs is apparent, the market-to-book ratios and accounting rates of return for average cost are between for LIFO and FIFO.2. Because it has more recent costs on the balance sheet in the inventory account, FIFO has market-to-book ratios closer to 1regardless of whether prices rise or fall.Chapter 10Page 1961. The total profit on the transaction is the sales price of $880.00 less the original cost of $734.03:Sales price of securities $880.00Less : original cost ($735.03)Profit on transaction $144.97The cash flows were: $735.03 out on January1, 2001, and $880.00 in on January 3, 2003.There were profit in 2001, 2002, and 2003.In 2001, therewas a profit of $81.17.In 2003,there was a profit of $5.00.2. The unadjusted book value of the security on December 31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing its carrying value by $3.83 is required to write it down to its market value: Unrealized loss on market value securities-trading ……3.83 Marketable securities –trading ………… 3.83 If the security were sold for $810.00 on January 3, 2003, the entry would be:Cash ………………………………810.00Marketable securities –trading ………………790.00Gain on marketable securities-trading …………20.001/03/2003(To record the sale of the Marketable securities—trading )Page 1981. When a securities is classified as trading security, profits or losses show up on the income statement in every period from when the security is purchased until when it is sold. when a security is classified as available-for-sale ,profits or losses only show up on the income statement in the period in which the security is sold.2. the unadjusted book value of the security on December31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing it’s carrying value by $3.83 is required to write it down to it’s market value. however unlike the trading security case ,the unrealized loss is an equity account ,not a temporary account:Unrealized loss on marketable securities-available-for-sale 3.38 Marketable securities –trading ………………3.83To record the sale of the security for $810.00 on January 3,2003: Cash ………810.00Unrealized gain on marketable securities-available-for-sale(58.80-3.83) ………54.97Marketable securities-trading …………790.00Realized gain on marketable securities-available-for-sale ……………74.9712/31/2002(To mark-to-market the Marketable securities—available-for-sale)Chapter 111.a. Under straight-line depreciation, the depreciation expense each year is$600-$100/5 years=$100 per year.b. Under double-declining balance depreciation, the depreciation expense each year is given in the following table:c. Under sum-of-year’-digits depreciation, the depreciation expense each year is given in the following table:Sum-of years’-digits depreciation2. Intangible assets are most often shown in one line that is cost net of amortization. Tangible assets are sometimes shown in three lines: cost , accumulated depreciation, and net .3. Economic depreciation is the change in the economic value of the asset. Economic depreciation can be appreciation when the asset increases in value. We seen this already with marketable debt securities, which sometimes increase in valuebecause of unpaid interest4.It is easy and fulfills the requirement of GAAP to provide depreciation using a systematic and rational method. No GAAP depreciation method likely correctly reflects economic depreciation anyway ,so a simple expedient may be good enough.1.Sraight-line depreciation is $100 per year ($300/3 years).Double-declining balance depreciation is given in the following table:2.For straight-line depreciation,the entry is the same each year:Depreciation expense (100)Accumulateddepreciation (100)For double-declining balance depreciation,the entries are: Year1Depr eciation expense (200)Accu mulated depreciation (200)Year2Depreciation expense………………………………66.67 Acc umulated depreciation………………………66.67 Year3.declining balance because depreciation expense under straight-line is only $100,while under double-declining balance depreciation expense is $200.4.If the company buys one asset every year and each asset lasts three years,then in year 4 it will have three assets.Under straight-line depreciation,each of those assets generates a depreciation expense of $100;therefore total depreciation expense would be 3*$100,or $300.Under double-declining balance depreciation,total depreciation expense depends on the age of each asset.The company would have one asset in its first year of life,one in its second year of life,and one in its third year.Therefore,totaldepreciation expense would be:$200+$66.67+$33.33=$300,the same as under straight-line.Both depreciation methods give the same total depreciation because:1.Both methods fully depreciate the assets over their lives.2.The cost of the assets has remained constant.3.The company is in a steady state in which the number ofnew assets purchased in a period equals the number ofold assets being retired in that period.。

(精品中级财务会计英文版.课后答案(chap2)

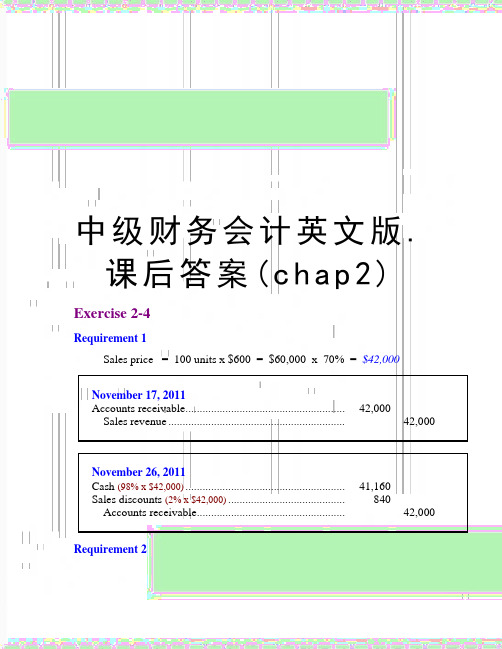

中级财务会计英文版.课后答案(c h a p2) Exercise 2-4Requirement 1Sales price = 100 units x $600 = $60,000 x 70% = $42,000November 17, 2011Accounts receivable ........................................................ 42,000Sales revenue .............................................................. 42,000 November 26, 2011Cash (98% x $42,000)........................................................ 41,160Sales discounts (2% x $42,000) (840)Accounts receivable .................................................... 42,000 Requirement 2Exercise 7-4 (concluded)Requirement 3Requirement 1, using the net method:Requirement 2, using the net method:Exercise 2-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000Less: Actual returns (450,000)Remaining estimated returns $10,000Note: another series of journal entries that produce the same end result would be:Exercise 2-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 2-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2011 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 2-9Requirement 1To record the write-off of receivables.To reinstate an account previously written off and to record the collection.Allowance for uncollectible accounts:Balance, beginning of year $32,000Deduct: Receivables written off (21,000)Add: Collection of receivable previously written off 1,200Balance, before adjusting entry for 2011 bad debts 12,200Required allowance: 10% x $625,000 (62,500)Bad debt expense $50,300To record bad debt expense for the year.Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 2-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2011 $20,030 Exercise 2-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388Exercise 2-12Requirement 1Requirement 22011 income before income taxes would be understated by $900 2012 income before income taxes would be overstated by $900.Exercise2-13Requirement 1Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 2-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year $ 2,200= 10% rate Divided by value of note $ 22,000Requirement 2To record sale of stock in exchange for note receivable.To accrue interest on note receivable for twelve months.Exercise 2-15Exercise 2-16Exercise 2-17Exercise 2-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet of Mountain High, and they must record a liability.Exercise 2-19Step 1: Accrue interest earned.Step 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21Requirement 1Step 1: To accrue interest earned for two months on note receivableStep 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 2-21 (concluded)Requirement 2To accrue interest earned on note receivable.。

中级财务会计英文版.课后答案(chap06)

Exercise 6-11. Straight-line:$33,000 - 3,000= $6,000 per year5 years2. Sum-of-the-years’ digits:Exercise 6-1 (concluded)3. Double-declining balance:Straight-line rate of 20% (1 ÷ 5 years) x 2 = 40% DDB rate.4. Units-of-production:$33,000 - 3,000= $.30 per mile depreciation rate 100,000 milesExercise 6-21. Straight-line:$115,000 - 5,000= $11,000 per year10 years2. Sum-of-the-years’ digits:Sum-of-the-digits is ([10 (10 + 1)] ÷2) = 552011 $110,000 x 10/55 = $20,0002012 $110,000 x 9/55 = $18,0003. Double-declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 2 = 20% DDB rate2011 $115,000 x 20% = $23,0002012 ($115,000 - 23,000) x 20% = $18,4004. One hundred fifty percent declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 1.5 = 15% rate2011 $115,000 x 15% = $17,2502012 ($115,000 - 17,250) x 15% = $14,6635. Units-of-production:$115,000 - 5,000= $.50 per unit depreciation rate220,000 units2011 30,000 units x $.50 = $15,0002012 25,000 units x $.50 = $12,500Exercise 6-31. Straight-line:$115,000 - 5,000= $11,000 per year10 years2011 $11,000 x 3/12 = $ 2,7502012 $11,000 x 12/12 = $11,0002. Sum-of-the-years’ digits:Sum-of-the-digits is {[10 (10 + 1)]/2} = 552011 $110,000 x 10/55 x 3/12 = $ 5,0002012 $110,000 x 10/55 x 9/12 = $15,000+ $110,000 x 9/55 x 3/12 = 4,500$19,5003. Double-declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 2 = 20% DDB rate2011 $115,000 x 20% x 3/12 = $5,7502012 $115,000 x 20% x 9/12 = $17,250+ ($115,000 - 23,000) x 20% x 3/12 = 4,600$21,850 or,2012 ($115,000 - 5,750) x 20% = $21,8504. One hundred fifty percent declining balance: Straight-line rate is 10% (1 ÷ 10 years) x 1.5 = 15% rate 2011 $115,000 x 15% x 3/12 =$ 4,313 2012 $115,000 x 15% x 9/12 = $12,937 + ($115,000 - 17,250) x 15% x 3/12 = 3,666$16,603Or,2012 ($115,000 - 4,313) x 15% = $16,603Exercise 6-3 (concluded)5. Units-of-production:$115,000 - 5,000= $.50 per unit depreciation rate220,000 units2011 10,000 units x $.50 =$ 5,0002012 25,000 units x $.50 =$12,500Exercise 6-4Building depreciation:$5,000,000 - 200,000= $160,000 per year30 yearsBuilding addition depreciation:Remaining useful life from June 30, 2011 is 27.5 years.$1,650,000= $60,000 per year27.5 years2011 $60,000 x 6/12 = $30,0002012 $60,000 x 12/12 =$60,000Exercise 6-6Requirement 11. Straight-line:$260,000 - 20,000= $40,000 per year6 years2011 $40,000 x 8/12 = $26,667 2012 $40,000 x 12/12 = $40,0002. Sum-of-the-years’ digits:Sum-of-the-yea rs’ digits is ([6 (6 + 1)] ÷2) = 212011 $240,000 x 6/21 x 8/12 = $45,7142012 $240,000 x 6/21 x 4/12 = $22,857+ $240,000 x 5/21 x 8/12 =38,095$60,9523. Double-declining balance:1/6 (the straight-line rate) x 2 = 1/3 DDB rate2011 $260,000 x 1/3 x 8/12 = $57,7782012 $260,000 x 1/3 x 4/12 = $28,889+ ($260,000 – 86,667) x 1/3 x 8/12 = 38,518$67,407 or,2012 ($260,000 – 57,778) x 1/3 = $67,407Exercise 6-9Requirement 1$5,675Group depreciation rate = = 17.2% (rounded)$33,000Group life = $28,500= 5.02 years (rounded)$5,675Requirement 2To record the purchase of new refrigerators.To record the sale of old refrigerators.Exercise 6-10Requirement 1Cost of the equipment:Purchase price $154,000Freight charges 2,000Installation charges 4,000$160,000Straight-line rate of 12.5% (1 ÷ 8 years) x 2 = 25% DDB rate.Requirement 2For plant and equipment used in the manufacture of a product, depreciation is a product cost and is included in the cost of inventory. Eventually, when the product is sold, depreciation will be included in cost of goods sold.Exercise 6-15To record the purchase of a patent.To record amortization of a patent for the year 2011.To record amortization of the patent for the year 2012.To record costs of successfully defending a patent infringement suit.Exercise 6-15 (concluded)To record amortization of patent for the year 2013.Calculation of revised annual amortization:($ in thousands)$500 Cost$62.5 Previous annual amortization ($500 ÷ 8 years) x 2 years 125 Amortization to date (2011-2012)375 Unamortized cost (balance in the patent account)45Add420 New unamortized cost÷ 6 Estimated remaining life(8 years – 2 years)$ 70 New annual amortizationExercise 6-21Requirement 1Analysis:Correct Incorrect(Should Have Been Recorded) (As Recorded)2008 Machine 350,000 Expense 350,000Cash 350,000 Cash 350,0002008 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,0002009 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,0002010 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,000During the three-year period, depreciation expense wasunderstated by $210,000, but other expenses were overstated by$350,000, so net income during the period was understated by$140,000, which means retained earnings is currently understatedby that amount.During the three-year period, accumulated depreciation wasunderstated, and continues to be understated by $210,000.To correct incorrect accountsMachine ............................................................ 350,000Accumulated depreciation ($70,000 x 3 years) .. 210,000 Retained earnings ($350,000 – 210,000) ............ 140,000 Requirement 2Correcting entry:Assuming that the machine had been disposed of, no correctingentry would be required because, after five years, the accountswould show appropriate balances.。

财务会计英语练习及答案ch

财务会计英语练习及答案ch个人收集整理勿做商业用途CHAPTER 16 STATEMENT OF CASH FLOWS个人收集整理勿做商业用途Chapter 16—Statement of Cash FlowsTRUE/FALSE1. The statement of cash flows is not one of the basic financial statements.ANS: F DIF: 1 OBJ: 012. Cash, as the term is used for the statement of cash flows, could indicate either cash or cashequivalents.ANS: T DIF: 1 OBJ: 013. The statement of cash flows is an optional financial statement.ANS: F DIF: 1 OBJ: 014. The statement of cash flows shows the effects on cash ofa company's operating, investing,and financing activities.ANS: T DIF: 1 OBJ: 015. The statement of cash flows reports a firm's major sources of cash receipts and major uses ofcash payments for a period.ANS: T DIF: 1 OBJ: 016. Cash flows from operating activities, as part of the statement of cash flows, include cashtransactions that enter into the determination of net income.ANS: T DIF: 1 OBJ: 017. To arrive at cash flows from operations, it is necessary toconvert the income statement froman accrual basis to the cash basis of accounting.ANS: T DIF: 2 OBJ: 018. Cash flows from investing activities, as part of the statement of cash flows, include receiptsfrom the sale of land.ANS: T DIF: 2 OBJ: 019. Cash flows from financing activities, as part of the statement of cash flows, include paymentsfor dividends.ANS: T DIF: 2 OBJ: 0110. Cash flows from investing activities, as part of the statement of cash flows, include paymentsfor the purchase of treasury stock.ANS: F DIF: 2 OBJ: 0111. Cash flows from investing activities, as part of the statement of cash flows, include receiptsfrom the issuance of bonds payable.ANS: F DIF: 2 OBJ: 0112. There are two alternatives to reporting cash flows from operating activities in the statement ofcash flows: (1) the direct method and (2) the indirect method.ANS: T DIF: 1 OBJ: 0113. The direct method of preparing the operating activities section of the statement of cash flowsreports major classes of gross cash receipts and gross cash payments.ANS: T DIF: 1 OBJ: 0114. Under the direct method of reporting cash flows from operations, the major source of cash iscash received from customers.ANS: T DIF: 1 OBJ: 0115. The main disadvantage of the direct method of reporting cash flows from operating activitiesis that the necessary data are often costly to accumulate.ANS: T DIF: 2 OBJ: 0116. A major disadvantage of the indirect method of reporting cash flows from operating activitiesis that the difference between the net amount of cash flows from operating activities and net income is not emphasized.ANS: F DIF: 2 OBJ: 01个人收集整理勿做商业用途17. Cash outflows from financing activities include the payment of cash dividends, theacquisition of treasury stock, and the repayment of amounts borrowed.ANS: T DIF: 2 OBJ: 0118. Cash flows from investing activities, as part of the statement of cash flows, include paymentsfor the acquisition of fixed assets.ANS: T DIF: 2 OBJ: 0119. The acquisition of land in exchange for common stock is an example of noncash investing andfinancing activity.ANS: T DIF: 2 OBJ: 0120. If a business issued bonds payable in exchange for land, the transaction would be reported in aseparate schedule on the statement of cash flows.ANS: T DIF: 2 OBJ: 0121. A cash flow per share amount should be reported on thestatement of cash flows.ANS: F DIF: 1 OBJ: 0122. Although there is no order in which the noncash balance sheet accounts must be analyzed indetermining data for preparing the statement of cash flows by the indirect method, time can be saved and greater accuracy can be achieved by selecting the accounts in the reverse order in which they appear on the balance sheet.ANS: T DIF: 1 OBJ: 0223. The 2002 edition of Accounting Trends and Techniques reported that 90% of the companiessurveyed used the indirect method to report changes in cash flows from operations.ANS: F DIF: 2 OBJ: 0224. Rarely would the cash flows from operating activities, as reported on the statement of cashflows, be the same as the net income reported on the income statement.ANS: T DIF: 2 OBJ: 0225. If land costing $75,000 was sold for $135,000, the amount reported in the investing activitiessection of the statement of cash flows would be $75,000.ANS: F DIF: 2 OBJ: 0226. If land costing $150,000 was sold for $205,000, the $55,000 gain on the sale would be addedto net income in converting the net income reported on the income statement to cash flows from operating activities for the statement of cash flows prepared by the indirect method.ANS: F DIF: 2 OBJ: 0227. In preparing the cash flows from operating activitiessection of the statement of cash flows bythe indirect method, the net decrease in inventories from the beginning to the end of the period is added to net income for the period.ANS: T DIF: 2 OBJ: 0228. In determining the cash flows from operating activities for the statement of cash flows by theindirect method, the depreciation expense for the period is added to the net income for the period.ANS: T DIF: 2 OBJ: 0229. In preparing the cash flows from operating activities section of the statement of cash flows bythe indirect method, the amortization of bond discount for the period is deducted from the net income for the period.ANS: F DIF: 2 OBJ: 02个人收集整理勿做商业用途30. If cash dividends of $145,000 were declared during the year and the decrease in dividendspayable from the beginning to the end of the year was $7,000, the statement of cash flows would report $152,000 in the financing activities section.ANS: T DIF: 2 OBJ: 0231. The declaration and issuance of a stock dividend would be reported on the statement of cashflows.ANS: F DIF: 2 OBJ: 0232. If 900 shares of $40 par common stock are sold for $48,000, the $48,000 would be reported inthe cash flows from financing activities section of the statement of cash flows.ANS: T DIF: 2 OBJ: 0233. If $500,000 of bonds payable are sold at 101, $500,000 would be reported in the cash flowsfrom financing activities section of the statement of cash flows.ANS: F DIF: 2 OBJ: 0234. Net income was $ 52,000 for the year. The accumulated depreciation balance increased by$17,000 over the year. There were no sales of fixed assets or changes in noncash current assets or liabilities. The cash flow from operations is $35,000ANS: F DIF: 2 OBJ: 0235. Net income for the year was $29,000. Accounts receivable increased $2,500, and accountspayable increased $5,100. The cash flow from operations is $31,600.ANS: T DIF: 2 OBJ: 0236. A building with a cost of $153,000 and accumulated depreciation of $42,000 was sold for an$11,000 gain. The cash generated from this investing activity was $121,000.ANS: F DIF: 2 OBJ: 0237. The indirect method reports cash received from customers in the cash flows from operatingactivities section of the statement of cash flows.ANS: F DIF: 2 OBJ: 0238. Cash paid to acquire treasury stock should be shown on the statement of cash flows frominvesting activities.ANS: F DIF: 2 OBJ: 0239. Repayments of bonds would be shown as a cash outflow in the investing section of thestatement of cash flows.ANS: F DIF: 2 OBJ: 0240. Acquiring equipment by issuing a six-month note should be shown on the statement of cashflows under the investing activities section.ANS: F DIF: 2 OBJ: 0241. In reporting cash flows from investing activities on the statement of cash flows, the cashinflows are usually reported first, followed by the cash outflows.ANS: T DIF: 1 OBJ: 0242.Cash inflows and outflows are not netted in any activity section of the statement of cash flows but are separately disclosed to give the reader full information.ANS: T DIF: 1 OBJ: 0243. The manner of reporting cash flows from investing and financing activities will be differentunder the direct method as compared to the indirect method.ANS: F DIF: 1 OBJ: 0344. Sales reported on the income statement were $375,000. The accounts receivable balancedeclined $6,500 over the year. The amount of cash received from customers was $368,500.个人收集整理勿做商业用途ANS: F DIF: 2 OBJ: 0345. To determine cash payments for merchandise for the cash flow statement using the directmethod, a decrease in accounts payable is added to the cost of merchandise sold.ANS: T DIF: 2 OBJ: 0346. To determine cash payments for operating expenses for the cash flow statement using thedirect method, a decrease in prepaid expenses is added to operating expenses other thandepreciation.ANS: F DIF: 2 OBJ: 0347. To determine cash payments for operating expenses for the cash flow statement using thedirect method, a decrease in accrued expenses is added to operating expenses other thandepreciation.ANS: T DIF: 2 OBJ: 0348. To determine cash payments for income tax for the cash flow statement using the directmethod, an increase in income taxes payable is added to the income tax expense.ANS: F DIF: 2 OBJ: 0349. Free cash flow is cash flow from operations, less cash used to purchase fixed assets tomaintain productive capacity and cash used for dividends.ANS: T DIF: 1 OBJ: 0450. Free cash flow is the measure of operating cash flow available for corporate purposes afterproviding sufficient fixed asset additions to maintain current productive capacity anddividends.ANS: T DIF: 1 OBJ: 04MULTIPLE CHOICE1. Which of the following is not one of the four basic financial statements?a. balance sheetb. statement of cash flowsc. statement of changes in financial positiond. income statementANS: C DIF: 1 OBJ: 012. Which of the following concepts of cash is not appropriate to use in preparing the statementof cash flows?a. cashb. cash and money market fundsc. cash and cash equivalentsd. cash and U.S. treasury bondsANS: D DIF: 2 OBJ: 013. The statement of cash flows reportsa. cash flows from operating activitiesb. total assetsc. total changes in stockholders' equityd. changes in retained earningsANS: A DIF: 1 OBJ: 014. On the statement of cash flows, the cash flows from operating activities section would includea. receipts from the issuance of capital stockb. receipts from the sale of investmentsc. payments for the acquisition of investments个人收集整理勿做商业用途d. cash receipts from sales activitiesANS: D DIF: 2 OBJ: 015. Preferred stock issued in exchange for land would be reported in the statement of cash flowsina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: C DIF: 2 OBJ: 016. Cash paid to purchase long-term investments would be reported in the statement of cash flowsina. the cash flows from operating activities sectionb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. a separate scheduleANS: C DIF: 2 OBJ: 017. A statement of cash flows would not disclose the effects of which of the followingtransactions?a. stock dividends declaredb. bonds payable exchanged for capital stockc. purchase of treasury stockd. capital stock issued to acquire fixed assetsANS: A DIF: 2 OBJ: 018. Which of the following does not represent an outflow of cash and therefore would not bereported on the statement of cash flows as a use of cash?a. purchase of noncurrent assetsb. purchase of treasury stockc. discarding an asset that had been fully depreciatedd. payment of cash dividendsANS: C DIF: 2 OBJ: 019. Which of the following represents an inflow of cash and therefore would be reported on thestatement of cash flows?a. appropriation of retained earningsb. acquisition of treasury stockc. declaration of stock dividendsd. issuance of long-term debtANS: D DIF: 2 OBJ: 0110. A ten-year bond was issued at par for $150,000 cash. This transaction should be shown on astatement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activitiesd. operating activitiesANS: B DIF: 1 OBJ: 0111. Cash paid for preferred stock dividends should be shown on the statement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activities个人收集整理勿做商业用途d. operating activitiesANS: B DIF: 2 OBJ: 0112. The last item on the statement of cash flows prior to the schedule of noncash investing andfinancing activities reportsa. the increase or decrease in cashb. cash at the end of the yearc. net cash flow from investing activitiesd. net cash flow from financing activitiesANS: B DIF: 2 OBJ: 0113. Which of the following is a noncash investing and financing activity?a. payment of a cash dividendb. payment of a six-month note payablec. purchase of merchandise inventory on accountd. issuance of common stock to acquire landANS: D DIF: 2 OBJ: 0114. Which of the following should be shown on a statement of cash flows under the financingactivity section?a. the purchase of a long-term investment in the common stock of another companyb. the payment of cash to retire a long-term notec. the proceeds from the sale of a buildingd. the issuance of a long-term note to acquire landANS: B DIF: 2 OBJ: 0115. A company purchases equipment for $29,000 cash. This transaction should be shown on thestatement of cash flows undera. investing activitiesb. financing activitiesc. noncash investing and financing activitiesd. operating activitiesANS: A DIF: 2 OBJ: 0116. Cash flow per share isa. required to be reported on the balance sheetb. required to be reported on the income statementc. required to be reported on the statement of cash flowsd. not required to be reported on any statementANS: D DIF: 1 OBJ: 0117. On the statement of cash flows prepared by the indirect method, the cash flows from operatingactivities section would includea. receipts from the sale of investmentsb. amortization of premium on bonds payablec. payments for cash dividendsd. receipts from the issuance of capital stockANS: B DIF: 2 OBJ: 0118. The statement of cash flows may be used by management toa. assess the liquidity of the businessb. assess the major policy decisions involving investments and financingc. determine dividend policyd. do all of the aboveANS: D DIF: 1 OBJ: 01个人收集整理勿做商业用途19. Depreciation on factory equipment would be reported in the statement of cash flows preparedby the indirect method ina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: D DIF: 2 OBJ: 0220. Which of the following should be added to net income incalculating net cash flow fromoperating activities using the indirect method?a. an increase in inventoryb. a decrease in accounts payablec. preferred dividends declared and paidd. a decrease in accounts receivableANS: D DIF: 2 OBJ: 0221. Which of the following should be deducted from net income in calculating net cash flow fromoperating activities using the indirect method?a. depreciation expenseb. amortization of premium on bonds payablec. a loss on the sale of equipmentd. dividends declared and paidANS: B DIF: 2 OBJ: 0222. Which of the following below increases cash?a. depreciation expenseb. acquisition of treasury stockc. borrowing money by issuing a six-month noted. the declaration of a cash dividendANS: C DIF: 2 OBJ: 0223. Which one of the following below would not be classified as an operating activity?a. interest expenseb. income taxesc. payment of dividendsd. selling expensesANS: C DIF: 2 OBJ: 0224. Which one of the following below should be added to net income in calculating net cash flowfrom operating activities using the indirect method?a. a gain on the sale of landb. a decrease in accounts payablec. an increase in accrued liabilitiesd. dividends paid on common stockANS: C DIF: 2 OBJ: 0225. On the statement of cash flows prepared by the indirect method, a $50,000 gain on the sale ofinvestments would bea. deducted from net income in converting the net income reported on the incomestatement to cash flows from operating activitiesb. added to net income in converting the net income reported on the income statementto cash flows from operating activitiesc. added to dividends declared in converting the dividends declared to the cash flowsfrom financing activities related to dividends个人收集整理勿做商业用途d. deducted from dividends declared in converting the dividends declared to the cashflows from financing activities related to dividendsANS: A DIF: 2 OBJ: 0226. Accounts receivable arising from trade transactions amounted to $45,000 and $52,000 at thebeginning and end of the year, respectively. Net income reported on the income statement for the year was $105,000. Exclusive of the effect of other adjustments, the cash flows from operating activities to be reported on the statement of cash flows prepared by the indirect method isb. $112,000c. $98,000d. $140,000ANS: C DIF: 2 OBJ: 0227. The net income reported on the income statement for the current year was $275,000.Depreciation recorded on fixed assets and amortization of patents for the year were $40,000 and $9,000, respectively. Balances of current asset and current liability accounts at the end and at the beginning of the year are as follows:End Beginning Cash $ 50,000 $ 60,000 Accounts receivable 112,000 108,000 Inventories 105,000 93,000 Prepaid expenses 4,500 6,500 Accounts payable (merchandise creditors) 75,000 89,000 What is the amount of cash flows from operating activities reported on the statement of cash flows prepared by the indirect method?a. $198,000b. $324,000c. $352,000d. $296,000ANS: D DIF: 3 OBJ: 0228. The following information is available from the current period financial statements:Net income .................................... $140,000Depreciation expense ..................... 28,000Increase in accounts receivable ....... 16,000Decrease in accounts payable ......... 21,000The net cash flow from operating activities using the indirect method isb. $163,000c. $107,000d. $205,000ANS: A DIF: 3 OBJ: 0229. On the statement of cash flows, the cash flows from investing activities section would includea. receipts from the issuance of capital stockb. payments for dividendsc. payments for retirement of bonds payabled. receipts from the sale of investmentsANS: D DIF: 2 OBJ: 02个人收集整理勿做商业用途30. A building with a book value of $ 45,000 is sold for $50,000 cash. Using the indirect method,this transaction should be shown on the statement of cash flows as follows:a. an increase of $45,000 from investing activitiesb. an increase of $50,000 from investing activities and a deduction from net income of$5,000c. an increase of $50,000 from investing activitiesd. an increase of $45,000 from investing activities and an addition to net income of$5,000ANS: B DIF: 2 OBJ: 0231. Cash paid for equipment would be reported in the statement of cash flows ina. the cash flows from operating activities sectionb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. a separate scheduleANS: C DIF: 2 OBJ: 0232. If a gain of $9,000 is incurred in selling (for cash) office equipment having a book value of$55,000, the total amount reported in the cash flows from investing activities section of the statement of cash flows isa. $46,000b. $9,000c. $55,000d. $64,000ANS: D DIF: 2 OBJ: 0233. Which of the following types of transactions would be reported as a cash flow from investingactivity on the statement of cash flows?a. issuance of bonds payableb. issuance of capital stockc. purchase of treasury stockd. purchase of noncurrent assetsANS: D DIF: 2 OBJ: 0234. Land costing $47,000 was sold for $78,000 cash. The gain on the sale was reported on theincome statement as other income. On the statement of cash flows, what amount should be reported as an investing activity from the sale of land?a. $78,000b. $47,000c. $109,000d. $31,000ANS: A DIF: 2 OBJ: 0235. Equipment with an original cost of $50,000 and accumulated depreciation of $20,000 wassold at a loss of $7,000. As a result of this transaction, cash woulda. increase by $23,000b. decrease by $7,000c. increase by $43,000d. decrease by $30,000ANS: A DIF: 2 OBJ: 0236. On the statement of cash flows, the cash flows from financing activities section would includea. receipts from the sale of investmentsb. payments for the acquisition of investmentsc. receipts from a note receivabled. receipts from the issuance of capital stockANS: D DIF: 2 OBJ: 0237. On the statement of cash flows, the cash flows from financing activities section would includeall of the following excepta. receipts from the sale of bonds payableb. payments for dividendsc. payments for purchase of treasury stockd. payments of interest on bonds payableANS: D DIF: 2 OBJ: 0238. Cash dividends paid on capital stock would be reported in the statement of cash flows ina. the cash flows from financing activities sectionb. the cash flows from investing activities sectionc. a separate scheduled. the cash flows from operating activities sectionANS: A DIF: 2 OBJ: 0239. Cash dividends of $80,000 were declared during the year. Cash dividends payable were$10,000 and $15,000 at the beginning and end of the year, respectively. The amount of cash for the payment of dividends during the year isa. $85,000b. $80,000c. $95,000d. $75,000ANS: D DIF: 2 OBJ: 0240. On the statement of cash flows, a $20,000 gain on the sale of fixed assets would bea. added to net income in converting the net income reported on the income statementto cash flows from operating activitiesb. deducted from net income in converting the net income reported on the incomestatement to cash flows from operating activitiesc. added to dividends declared in converting the dividends declared to the cash flowsfrom financing activities related to dividendsd. deducted from dividends declared in converting the dividends declared to the cashflows from financing activities related to dividendsANS: B DIF: 2 OBJ: 0241. A business issues 20-year bonds payable in exchange for preferred stock. This transactionwould be reported on the statement of cash flows ina. a separate scheduleb. the cash flows from financing activities sectionc. the cash flows from investing activities sectiond. the cash flows from operating activities sectionANS: A DIF: 2 OBJ: 0242. Land costing $68,000 was sold for $50,000 cash. The loss on the sale was reported on theincome statement as other expense. On the statement of cash flows, what amount should be reported as an investing activity from the sale of land?a. $50,000b. $78,000c. $118,000d. $68,000ANS: A DIF: 2 OBJ: 0243. The current period statement of cash flows includes the flowing:Cash balance at the beginning of the period................... $410,000Cash provided by operating activities ............................ 185,000 Cash used in investing activities .................................... 43,000Cash used in financing activities .................................... 97,000 The cash balance at the end of the period isa. $45,000b. $735,000c. $455,000d. $85,000ANS: C DIF: 2 OBJ: 0244. On the statement of cash flows, the cash flows from operating activities section would includea. receipts from the issuance of capital stockb. payment for interest on short-term notes payablec. payments for the acquisition of investmentsd. payments for cash dividendsANS: B DIF: 2 OBJ: 0345. The cost of merchandise sold during the year was $50,000. Merchandise inventories were$12,500 and $10,500 at the beginning and end of the year, respectively. Accounts payable were $6,000 and $5,000 at the beginning and end of the year, respectively. Using the direct method of reporting cash flows from operating activities, cash payments for merchandise totala. $49,000b. $47,000c. $51,000d. $53,000ANS: A DIF: 2 OBJ: 0346. Sales for the year were $600,000. Accounts receivable were $100,000 and $80,000 at thebeginning and end of the year. Cash received from customers to be reported on the cash flow statement using the direct method isa. $700,000b. $600,000c. $580,000d. $620,000ANS: D DIF: 2 OBJ: 0347. Operating expenses other than depreciation for the year were $400,000. Prepaid expensesincreased by $17,000 and accrued expenses decreased by $30,000 during the year. Cash payments for operating expensesto be reported on the cash flow statement using the direct method would bea. $353,000b. $413,000c. $447,000d. $383,000ANS: C DIF: 2 OBJ: 0348. The following selected account balances appeared on the financial statements of the FranklinCompany:Accounts Receivable, Jan. 1 ........... $13,000Accounts Receivable, Dec. 31 ........ 9,000Accounts Payable, Jan 1 ................ 4,000Accounts payable Dec. 31 .............. 7,000Merchandise Inventory, Jan 1 ......... 10,000Merchandise Inventory, Dec 31 ...... 15,000Sales ............................................. 56,000Cost of Goods Sold ........................ 31,000The Franklin Company uses the direct method to calculate net cash flow from operatingactivities. Cash collections from customers area. $56,000b. $52,000c. $60,000d. $45,000ANS: C DIF: 3 OBJ: 0349. The following selected account balances appeared on the financial statements of the FranklinCompany:Accounts Receivable, Jan. 1 ......... $13,000Accounts Receivable, Dec. 31 ...... 9,000Accounts Payable, Jan 1 .............. 4,000Accounts payable Dec. 31 ............ 7,000Merchandise Inventory, Jan 1 ....... 10,000Merchandise Inventory, Dec 31 .... 15,000Sales ........................................... 56,000Cost of Goods Sold ....................... 31,000The Franklin Company uses the direct method to calculate net cash flow from operatingactivities. Cash paid to suppliers isa. $39,000b. $33,000c. $29,000d. $23,000ANS: B DIF: 3 OBJ: 0350. Income tax was $400,000 for the year. Income tax payable was $30,000 and $40,000 at thebeginning and end of the year. Cash payments for income tax reported on the cash flow statement using the direct method isa. $400,000b. $390,000c. $430,000d. $440,000ANS: B DIF: 2 OBJ: 0351. Free cash flow isa. all cash in the bankb. cash from operationsc. cash from financing, less cash used to purchase fixed assets to maintain productive。

会计学财务会计分册英文版27答案

会计学财务会计分册英文版27答案1、The traffic jams often happen in _______ hours. [单选题] *A. lunchB. workC. leisureD. rush(正确答案)2、19.Students will have computers on their desks ________ . [单选题] * A.in the future(正确答案)B.on the futureC.at the momentD.in the past3、The classmates can' t()Alice from her twin sister. [单选题] *A. speakB. tell(正确答案)C. talkD. say4、He spoke too fast, and we cannot follow him. [单选题] *A. 追赶B. 听懂(正确答案)C. 抓住D. 模仿5、These oranges look nice, but _______ very sour. [单选题] *A. feelB. taste(正确答案)C. soundD. look6、He does ______ in math.()[单选题] *A. goodB. betterC. well(正确答案)D. best7、It was()of you to get up early to catch the first bus so that you could avoid the traffic jam. [单选题] *A. senselessB. sensible(正确答案)C. sentimentalD. sensitive8、Don’t _______ to close the door when you leave the classroom. [单选题] *A. missB. loseC. forget(正确答案)D. remember9、_______ your help, I can’t finish my job. [单选题] *A. withB. without(正确答案)C. inD. into10、I hope Tom will arrive _______ to attend the meeting. [单选题] *A. in timesB. on time(正确答案)C. at timesD. from time to time11、Ordinary books, _________ correctly, can give you much knowledge. [单选题] *A. used(正确答案)B. to useC. usingD. use12、6.Hi, boys and girls. How are you ________ your posters for the coming English Festival at school? [单选题] *A.getting onB.getting offC.getting with (正确答案)D.getting13、25.A watch is important in our life. It is used for ______ the time. [单选题] *A.telling (正确答案)B.sayingC.speakingD.holding14、—Can you play tennis? —______, but I’m good at football.()[单选题] *A. Yes, I can(正确答案)B. Yes, I doC. No, I can’tD. No, I don’t15、The beautiful radio _______ me 30 dollars. [单选题] *A. spentB. paidC. cost(正确答案)D. took16、Though my best friend Jack doesn’t get()education, he is knowledgeable. [单选题] *A. ManyB. littleC. fewD. much(正确答案)17、—Does your grandpa live ______ in the country?—Yes. So I often go to visit him so that he won’t feel ______. ()[单选题] *A. alone; aloneB. lonely; lonelyC. lonely; aloneD. alone; lonely(正确答案)18、99.—Would you please show me the way _________ the bank?—Yes, go straight ahead. It’s opposite a school. [单选题] *A.inB.forC.withD.to(正确答案)19、Some students are able to find jobs after graduation while _____will return to school for an advanced degree. [单选题] *A. otherB. anotherC. others(正确答案)D. the other20、—Whose book is it? Is it yours?—No, ask John. Maybe it’s ______.()[单选题] *A. hersB. his(正确答案)C. he’sD. her21、—______ do you pay for it? —Over the Internet. ()[单选题] *A. WhatB. How muchC. How(正确答案)D. When22、Can you _______ this form? [单选题] *A. fillB. fill in(正确答案)C. fill toD. fill with23、The train is coming. Be ______! [单选题] *A. careful(正确答案)B. carefullyC. carelessD. care24、Finally he had to break his promise. [单选题] *A. 计划B. 花瓶C. 习惯D. 诺言(正确答案)25、pencil - box is beautiful. But ____ is more beautiful than ____. [单选题] *A. Tom's; my; heB. Tom's; mine; his(正确答案)C. Tom's; mine; himD. Tom's; my; his26、It’s usually windy in spring, ______ you can see lots of people flying kites.()[单选题] *A. so(正确答案)B. orC. butD. for27、He doesn’t smoke and hates women _______. [单选题] *A. smokesB. smokeC. smokedD. smoking(正确答案)28、_________ along the old Silk Road is an interesting and rewarding experience. [单选题]*A. TravelB. Traveling(正确答案)C. Having traveledD. Traveled29、How I wish I()to repair the watch! I only made it worse. [单选题] *A. had triedB. hadn't tried(正确答案)C. have triedD.didn't try30、He always did well at school _____ having to do part-time jobs every now and then. [单选题] *A despite ofB. in spite of(正确答案)C. regardless ofD in case of。

财务会计英文版课后习题答案Ch12