3I - Controlliing Project Financial Performance项目财务控制

财务管理英文第十三版

Corporate Capital Gains / Losses

Currently, capital gains are taxed at ordinary income tax rates for corporations, or a maximum 35%.

The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate after-tax incremental operating cash flows for the investment projects.

c) - (+) Taxes (tax savings) due to asset sale or disposal of “new” assets

d) + (-) Decreased (increased) level of “net” working capital

e) = Terminal year incremental net cash flow

Depreciation and the MACRS Method

Everything else equal, the greater the depreciation charges, the lower the taxes paid by the firm.

风险投资案例分析3i普瑞投资牵手小肥羊

投资作用

资金退出

5

案例背景

行 业 分 析

• 内蒙古小肥羊餐饮连锁有限公司是一家以自然人做发起人的股份制 企业,公司于1999年8月诞生在草原鹿城——包头市,以小肥羊特 色火锅连锁为主业。于2008年6月12日在香港上市,是中国首家在 香港上市的品牌餐饮企业,被誉为中华火锅第一股。

• “小肥羊火锅”将延续了千百年的蘸着小料涮羊肉食法,改革为” 不蘸小料涮羊肉” 的新食法。就是这样一个小店,如今拥有一个 投资作用 调味品基地,两个肉业基地,一个物流配送中心,一个外销机构, 国内、外多个餐饮管理区域;360家火锅连锁店遍布了全国各省、 市、区以及美国、日本、加拿大、印尼、阿联酋等海外市场,成为 一个国际性的大型餐饮连锁公司。 资金退出

27

2. 案例背景

提供先进服务,引进优质人才

在投资过程中,3i请来国际知名战略咨询公司罗兰贝格,为小 肥羊做全方位诊断,包括财务状况、企业历史、公司结构和资产状 可 行 况等。做这样的尽职审查,并不是不信任合作伙伴,而是为了更好 性 地规避风险,有效帮助合作伙伴诊断出隐藏问题从而可以对症下药 分 地加以解决,同时,这样的审查也可坚定3i投资小肥羊的决心。 析 投行作用 在管理层面,3i为小肥羊带来更多实际的“头脑”资源,先是 汉堡王国际公司前总裁Nish Kankiwala尼什-坎基瓦拉,之后又引进 现任肯德基香港运营公司总裁的杨耀强(Yuka Yeung)。签约后, Nish Kankiwala 以及杨耀强成为小肥羊的独立董事,王岱宗和另一 资金退出 位同事则代表3i进入董事会。

投资作用

供应商议价能力: 1、垂直整合(对国际市场是否 有效,还有待验证) 买家议价能力: 1、细分客户(依据不同需求, 提供不同标准) 2、保证质量,不要为低成本而 低成本

IASB主要项目、研究项目、已完成项目简介

本文汇总国际会计准则委员会(IASB)正在进行的主要项目、研究项目以及IASB 成立以来已完成的项目并作简介,以方便读者检索。

一、IASB 主要项目1.conceptual framework — comprehensive IASB project (概念框架——IASB 综合性项目)。

该项目仅由IASB 主持的以财务报表要素、计量、报告主体、列报与披露为重点的综合性项目。

2013年7月,IASB 发布综合性讨论稿“财务报告概念框架的复核”,征求意见截止日期为2014年1月14日。

对反馈意见的审议预计在2014年第一季度展开。

2. financial instruments — comprehensive project (金融工具——综合性项目)。

该项目为重写对金融工具会计处理要求的多方参与的IASB 与FASB 联合项目,包含大量子项目。

3. financial instruments — general hedge accounting (金融工具——一般套期会计)。

该项目对套期会计的会计处理要求进行重新评估,以便企业在财务报表中更充分地反映其风险管理活动。

对一般套期会计阶段的复核草稿于2012年9月发布,然后将完成终稿。

4. financial instruments — impairment (金融工具——减值)。

该项目以金融工具减值计量和确认为重点的IASB 与FASB 的联合项目。

2013年3月7日,IASB 发布“金融工具:预期信贷损失”征求意见稿,征求意见截止日期为2013年7月5日,然后将审议反馈意见。

5. financial instruments — limited reconsideration of IFRS 9(金融工具——对IFRS 9的有限复议)。

该项目对IFRS 9提出具有针对性的有限改进。

2012年11月28日发布“分类与计量:对IFRS 9的有限改进(对IFRS 9准则修订建议(2010))”,征求意见截止日期为2013年3月28日。

绿色信贷与企业债务融资成本研究综述

绿色信贷与企业债务融资成本研究综述摘要:绿色信贷源于绿色金融,常被称为可持续融资或环境融资。

它主要通过对企业债务融资利率设限以期达到限制重污染企业或增加绿色企业的贷款投资。

本文通过阐述国内外绿色信贷与企业债务融资成本的研究现状,并对二者之间的关系进行简要梳理和总结,以便后期能够更深入的研究相关问题。

关键词:绿色信贷;债务融资成本一、引言改革开放政策推行以来,我国的经济迅猛增长,国际地位也不断提高。

然而,与经济发展速度相对应的是我国的环境污染和资源浪费问题层出不穷。

企业作为环境问题的制造主体,其对环境造成的污染问题一直备受关注。

2012年2月,原中国银监会发布了《绿色信贷指引》,该文件对国家支持的绿色行业提供更充足的信贷资源与优惠利率,对国家不鼓励甚至限制的重污染行业减少贷款额度并提高他们的借款利率,引导资本由“两高”产业向绿色产业转型。

本文旨在对绿色信贷的产生与企业债务融资成本影响因素二者之间的国内外发展状况做一个简要梳理,以便于今后更深入的研究相关问题。

二、绿色信贷绿色信贷的概念源于绿色金融,绿色信贷在国外属于可持续融资或环境融资的研究范围,是一种将生态环境保护嵌入到金融业中、推动实现经济与环境协调发展的创新金融工具。

Cowan(1998)认为环境融资是可持续发展的重要部分,需要充分利用信贷、互换等以市场为基础的工具,为金融创新与环境保护二者之间搭建桥梁。

Jeucken(2001)指出,目前金融机构的投资资金面临的问题主要是环境风险,发展绿色金融已成为其保持自身可持续发展的现时客观要求。

Lee& Zhong(2015)认为,商业银行可以利用新型衍生金融工具开展绿色信贷,通过发行混合债券等规避可再生能源产业存在的融资风险和信用风险。

国外学者在定义绿色信贷时,主要研究绿色信贷在金融市场中对环境保护或经济的可持续发展方面的宏观研究,而国内有关绿色信贷的研究起步相对较晚,在2007年原中国银监会颁布《节能减排授信工作指导意见》后,绿色信贷政策才逐渐得到了国内学者的普遍关注。

1、appendix 6 - credit risk management

4

Process Categorisation: Used for: Categorisation:

Used for:

Monitoring Techniques

Loan application and Loan administration drawdown

Bad debt management

Portfolio risk management

quality Risk based

reporting Capital

allocation

Risk management

objectives

Selection based on transaction quality

Risk price Return on

capital

Limit setting on quality

Risk based assessment

Automation utilisation

Risk/exception based pricing

Automation utilisation on credit approval

Target portfolio on quality

Active management

Portfolio management

Loan balance: bad debt by geography bad debt by customer type bad debt by product

Revision of lending criteria

This table shows the monitoring techniques in credit risk management. It involves the categorization of 5 main processes and the purpose of the categorization. More than one categorization may be needed for each process to serve different monitoring purposes.

英语作文-金融资产管理公司创新投资策略,提高市场竞争力

英语作文-金融资产管理公司创新投资策略,提高市场竞争力Innovative Investment Strategies for Financial Asset Management Companies to Enhance Market Competitiveness。

The landscape of financial asset management is evolving rapidly, driven by dynamic market conditions, technological advancements, and shifting investor preferences. In this context, the adoption of innovative investment strategies becomes crucial for financial asset management companies aiming to bolster their market competitiveness.Effective utilization of data analytics stands at the forefront of modern investment strategies. By leveraging big data and machine learning algorithms, asset managers can extract actionable insights from vast datasets. These insights are pivotal in identifying emerging market trends, predicting asset price movements, and optimizing portfolio allocations in real-time. Moreover, the integration of artificial intelligence enhances decision-making processes, enabling quicker adjustments to market volatility and improving overall investment performance.Diversification remains a cornerstone of resilient investment strategies. Beyond traditional asset classes, such as equities and bonds, diversified portfolios now encompass alternative investments like private equity, venture capital, and real estate. These assets offer unique risk-return profiles and can provide essential diversification benefits, reducing portfolio volatility and enhancing long-term returns. Furthermore, strategic partnerships with niche investment firms or specialized asset managers facilitate access to exclusive investment opportunities, further enriching portfolio diversification.Risk management strategies have also evolved significantly, becoming more sophisticated and proactive. Modern asset management firms employ advanced risk assessment models that incorporate scenario analysis, stress testing, and Monte Carlo simulations. These methodologies allow firms to quantify and mitigate various riskseffectively, including market risk, credit risk, liquidity risk, and operational risk. By implementing robust risk management frameworks, companies can safeguard investor capital while maintaining competitive performance metrics.In response to growing environmental, social, and governance (ESG) considerations, sustainable investing has gained prominence across asset management sectors. Integrating ESG factors into investment strategies not only aligns with ethical principles but also mitigates risks associated with regulatory changes and reputational damage. Sustainable investments encompass a broad spectrum, ranging from renewable energy projects to socially responsible corporate bonds, thereby attracting a diverse investor base and enhancing overall portfolio resilience.Technological innovation continues to redefine client engagement and service delivery within asset management. The proliferation of digital platforms and fintech solutions enables firms to offer personalized investment advice, real-time portfolio monitoring, and seamless transaction capabilities. Additionally, leveraging blockchain technology enhances transparency, security, and efficiency in managing investment operations and fund distributions.Amidst the evolving landscape, agility emerges as a critical determinant of competitive advantage. Financial asset management companies must embrace a culture of innovation and adaptability, continually refining investment strategies to capitalize on emerging opportunities and navigate evolving market dynamics. Proactive monitoring of global macroeconomic trends, geopolitical developments, and regulatory changes is essential to anticipate market shifts and optimize investment outcomes.In conclusion, the pursuit of innovative investment strategies is imperative for financial asset management companies seeking to enhance market competitiveness. By harnessing data analytics, diversifying portfolios, strengthening risk management frameworks, embracing sustainable investing practices, leveraging technological advancements, and fostering organizational agility, firms can position themselves at the forefront of the industry. Ultimately, a commitment to innovation not only drives superiorinvestment performance but also cultivates long-term client trust and satisfaction in an increasingly competitive marketplace.。

资产负债管理系统简介

资产负债管理系统简介一、导读提醒本章简介旳资产负债管理系统是企业2023年12月V2.0设计产品(V1.0为2023年设计产品), 体现了企业反思2023年西方金融风暴起因、防备金融风险旳最新理论研究成果。

重新设计旳资产负债管理系统最突出特点是: 以巴塞尔新资本协议第一、第二、第三支柱规定、银监会《商业银行资本充足率审查评估要素及措施》等监管规定为根据, 从银行发展战略及高管角度, 构建起可操作旳银行全面风险管理框架。

二、系统简述资产负债管理是在世界金融自由化浪潮旳冲击下, 尤其是90年代中后期迅速发展并占据主流地位旳现代商业银行经营管理措施。

敏感性测试、市值分析、情景模拟、组合管理等先进旳管理思想和技术不停发展, 使得资产负债管理体系深入完善, 并逐渐成为现代商业银行经营管理框架旳关键内容。

概括地说, 目前西方银行业较为通行旳资产负债管理措施和技术有如下四种:一是基础旳风险度量措施――缺口及敏感性分析;二是动态旳、前瞻旳度量措施情景分析和压力测试;三是风险旳管理技术表内调整和表外对冲;四是组合管理技术资金转移计价和风险调整资本收益率等。

这些措施和技术由简朴到复杂, 由单一到组合, 充足展现了西方商业银行风险管理旳思想轨迹和技术演变过程。

现代商业银行旳资产负债管理体系是一种复杂旳系统:第一, 它规定建立由银行高级管理人员和重要业务部门负责人构成资产负债管理委员会, 负责制定资产负债管理政策、确定内部资金定价原则、审查市场风险状况、并对风险偏好、风险敞口调整、业务方略选择等有关事项做出决策。

第二, 它规定建立专门旳资产负债管理团体来承担详细旳政策实行、风险计量和管理运作。

第三, 它规定建立一种包括识别风险种类、确定风险限额、评估风险收益、调整风险敞口、选择业务方略、配置经济资本、考核风险绩效等一系列环节在内旳顺畅旳管理流程。

第四, 它必须以科学旳分析措施、先进旳管理工具和有效旳管理手段为支柱。

第五, 它充足体现了银行全面风险管理框架旳总体思绪及实行手段旳最终效果, 从某种意义上说, 金融风险管理失控, 就是金融企业资产负债管理失控。

大股东掏空行为研究综述

大股东掏空行为研究综述摘要:近年来,随着对股权集中以及控股股东利用其控制权进行掏空认识的逐渐深入,大股东对中小股东利益的侵占即第二类代理问题就成为了公司治理研究的新热点,因此从控制权私人收益角度研究大股东对中小股东的侵害问题成为公司治理研究的迫切需要。

本文在查阅了大量股东掏空行为研究的科研成果之后,决定通过以下几个方面对其做系统综述:(1)控制权私人收益的界定(2)其与企业绩效的复杂关系(3)大股东掏空行为的度量(4)大股东掏空行为的动因。

最后结合我国公司治理实践指出现有研究的不足以及未来的研究方向。

以期通过此综述为今后研究做铺垫,从而为上市公司治理方面相关问题提供理论依据,为政府相关职能部门提供决策支持。

关键词:控制权私人收益;掏空;企业绩效;掏空行为度量;掏空动机;伦理决策一、引言传统公司治理理论中,Berle和Means(1932)认为公司所有权结构极度分散,管理层拥有实际控制权。

但随着公司股东多元化,现代公司的所有权结构逐步集中。

LLSV(1998)研究表明除英美等少数国家外,大部分发达国家的公司股权都集中在控股股东手中,而在一些法律不健全的国家,大股东控制现象尤为明显。

1980年Grossman和Hart首次提出控制权私人收益( Private Benefit of Control)概念,瞬时控制权私人收益就成为了公司治理研究领域的核心。

他们认为控制权私人收益又称控制权收益,是指控股股东(controlling shareholder)利用其控制权而谋取的不可转移利益。

之后,国内外学者也从不同视角对控制权私人收益进行了深入探讨,对控制权私人收益的概念进行了不同的界定。

针对其与企业绩效的关系,主流研究多认为控制权私人收益是对公司整体利益的侵害,但也有一些学者提出控制权私人收益对企业绩效存在积极的影响。

因此现有研究中控制权私人收益与企业绩效关系仍有着不明确性。

从大股东掏空行为的度量方面来看,这是解决该领域研究的关键点,具有极其重要的理论意义和现实意义。

香港MJ国际融资公司商业计划书

香港M J国际融资公司商业计划书模板Business Plan 商业计划书Table of contents 目录Executive Summary 执行总汇Introduction 介绍Company background 公司背景Concept and Market Niche 理念及市场环境Mission 任务Milestones 里程碑Financial summary 财务汇总Management 管理Board of Directors 董事会Senior Management 高级管理Staff 员工Business Model and Product 商务模式及产品Industry review 产业回顾Operation and Production 经营与生产Marketing 市场Competitors Analysis 结构分析Sales and Distribution Strategy 销售及分配策略Funds raised 融资Funds requirements 融资方式及额度Use of funds 资金计划使用情况Exit plan for funder 资金返还计划Finance 财务状况Last three year audited 前三年经审计过的财务报表Forecast for the coming two years 未来两年预测的财务报表香港投资公司和新家坡投资公司的要求较为相近,而且习惯于中英文两种文字.请企业注意两种文本应具有同等法律效力.3-4 欧洲风险投资协会商业计划书模板商业计划书中文模版结构第一章:摘要………………………………………………………………一、宗旨任务…………………………………………………………二、公司简介……………………………………………………………三、公司战略……………………………………………………………1、产品及服务A:…………………………………………………………2、产品及服务B,等等:…………………………………………………3、客户合同的开发、培训及咨询等业务:………………………………四、技术……………………………………………………………………1、专利技术:………………………………………………………………2、相关技术的使用情况技术间的关系:……………………………五、价值评估………………………………………………………………六、公司管理………………………………………………………………1、管理队伍状况…………………………………………………………2、外部支持:………………………………………………………………3、董事会:…………………………………………………………………七、组织、协作及对外关系:……………………………………………九、场地与设施……………………………………………………………十、风险……………………………………………………………………第三章:市场分析…………………………………………………………一、市场介绍………………………………………………………………二、目标市场………………………………………………………………三、顾客的购买准则………………………………………………………四、销售策略………………………………………………………………五、市场渗透和销售量……………………………………………………第四章:竞争性分析………………………………………………………一、竞争者…………………………………………………………………二、竞争策略或消除壁垒…………………………………………………1、竞争者A、B等………………………………………………………第五章:产品与服务………………………………………………………一、产品品种规划…………………………………………………………二、研究与开发……………………………………………………………三、未来产品和服务规划…………………………………………………四、生产与储运……………………………………………………………五、包装……………………………………………………………………六、实施阶段………………………………………………………………七、服务与支持……………………………………………………………第六章:市场与销售………………………………………………………一、市场计划………………………………………………………………二、销售策略………………………………………………………………1、实时销售方法…………………………………………………………2、产品定位………………………………………………………………三、销售渠道与伙伴………………………………………………………四、销售周期………………………………………………………………五、定价策略………………………………………………………………1、产品、服务:……………………………………………………………2、产品/服务B……………………………………………………………六、市场联络:……………………………………………………………2、广告宣传………………………………………………………………3、新闻发布会……………………………………………………………4、年度会议/学术讨论会…………………………………………………5、国际互联网促销………………………………………………………6、其它促销因素…………………………………………………………7、贸易刊物、文章报导……………………………………………………8、直接邮寄………………………………………………………………七、社会认证………………………………………………………………第七章:财务计划…………………………………………………………一、财务汇总………………………………………………………………二、财务年度报表…………………………………………………………三、资金需求………………………………………………………………四、预计收入报表…………………………………………………………五、资产负债预计表………………………………………………………六、现金流量表……………………………………………………………一、你公司或项目的背景与机构设置:………………………………二、市场背景:……………………………………………………………三、管理层人员简历………………………………………………………四、行业关系………………………………………………………………五、竞争对手的文件资料…………………………………………………六、公司现状………………………………………………………………七、顾客名单………………………………………………………………八、新闻剪报与发行物……………………………………………………九、市场营销………………………………………………………………十、专门术语………………………………………………………………第九章:图表………………………………………………………………。

baker et al(2003)投融资研究模型

Baker et al(2003)在其研究中提出了一种全新的投融资研究模型,该模型涉及多个方面,包括投资决策的过程、投资风险的评估、融资来源的选择以及资本结构的优化等内容。

本文将对Baker et al(2003)的投融资研究模型进行详细分析和解读,以期为相关研究和实践提供借鉴和参考。

1. 投资决策的过程Baker et al(2003)的投融资研究模型首先着眼于投资决策的过程。

在该模型中,投资决策被视为一个包含多个阶段的过程,包括项目筛选、投资评估、风险分析、资金调配等环节。

研究者指出,投资决策的过程中需要考虑到不同的因素,如经济环境、产业前景、竞争格局等,以便全面评估投资项目的可行性和风险。

2. 投资风险的评估在投融资研究模型中,Baker et al(2003)还对投资风险的评估进行了深入研究。

他们认为,投资风险包括市场风险、信用风险、流动性风险等多个方面,需要通过量化和定性的方法进行评估。

研究者还指出,投资风险的评估需要考虑不同的投资工具和投资组合,以便寻找最佳的风险收益平衡点。

3. 融资来源的选择在投融资决策中,融资来源的选择至关重要。

Baker et al(2003)的研究模型中强调了融资来源多样化的重要性,以及不同融资方式对企业成长和风险承担的影响。

研究者指出,融资来源的选择需要综合考虑企业的资本需求、融资成本、融资期限等因素,以便实现最佳的资本结构和财务效益。

4. 资本结构的优化Baker et al(2003)的投融资研究模型还涉及到资本结构的优化问题。

研究者认为,企业的资本结构应当是动态调整的,需要根据经营环境和市场条件进行不断优化。

他们建议,企业在考虑资本结构时应当综合考虑债务和股权的结构、融资成本、税收影响等多个因素,并通过财务管理手段实现最优化的资本结构。

总结起来,Baker et al(2003)的投融资研究模型在理论层面提供了全面而系统的分析框架,为投资决策和融资决策提供了一系列有益的启示。

单一资产管理计划 英语

单一资产管理计划英语English Response:Single-Asset Management Plan.A single-asset management plan is a plan that is created for the management of a single asset. This plan can be used to manage any type of asset, including real estate, equipment, or investments. The plan should outline the goals for the asset, the strategies that will be used to achieve those goals, and the metrics that will be used to measure the plan's success.There are many benefits to creating a single-asset management plan. First, it can help to improve the asset's performance. By outlining the goals for the asset and the strategies that will be used to achieve those goals, the plan can help to ensure that the asset is managed in a way that is consistent with those goals. Second, a single-asset management plan can help to reduce the risk of loss. Byidentifying the risks that are associated with the asset and developing strategies to mitigate those risks, the plan can help to protect the asset from loss. Third, a single-asset management plan can help to improve the efficiency of the asset's management. By outlining the processes and procedures that will be used to manage the asset, the plan can help to ensure that the asset is managed in a way that is efficient and effective.There are a few key elements that should be included in a single-asset management plan. First, the plan should include a statement of the goals for the asset. These goals should be specific, measurable, achievable, relevant, and time-bound (SMART). Second, the plan should include a description of the strategies that will be used to achieve the goals. These strategies should be specific, measurable, achievable, relevant, and time-bound (SMART). Third, the plan should include a description of the metrics that will be used to measure the success of the plan. These metrics should be specific, measurable, achievable, relevant, and time-bound (SMART).Single-asset management plans can be a valuable toolfor managing assets. By outlining the goals for the asset, the strategies that will be used to achieve those goals,and the metrics that will be used to measure the plan's success, a single-asset management plan can help to improve the performance of the asset, reduce the risk of loss, and improve the efficiency of the asset's management.中文回答:单一资产管理计划。

ProjectedCostsofGeneratingElectricity

Executive SummaryExecutive SummaryThe overall objective of the study is to provide reliable information on key factors affecting the economics of electricity generation using a range of technologies. The report can serve as a resource for policy makers and industry professionals seeking to better understand generation costs of these technologies.The study was carried out by an ad hoc group of officially appointed national experts. Cost data provided by the experts were compiled and used by the joint IEA/NEA Secretariat to calculate generation costs.Cost data were provided for more than 130power plants. This comprises 27coal-fired power plants, 23gas-fired power plants, 13nuclear power plants, 19wind power plants, 6solar power plants, 24combined heat and power (CHP) plants using various fuels and 10plants based on other fuels or technologies. The data provided for the study highlight the increasing interest of participating countries in renewable energy sources for electricity generation, in particular wind power, and in combined heat and power plants.The technologies and plant types covered by the present study include units under construction or planned that could be commissioned in the respondent countries between 2010 and 2015, and for which they have developed cost estimates generally through paper studies or bids.The calculations are based on the reference methodology adopted in previous studies, i.e., the levelised lifetime cost approach. The calculations use generic assumptions for the main technical and economic parameters as agreed upon in the ad hoc group of experts, e.g., economic lifetime (40years), average load factor for base-load plants (85%) and discount rates (5% and 10%).Electricity generation costs calculated are busbar costs, at the station, and do not include transmission and distribution costs. The costs associated with residual emissions– including greenhouse gases– are not included in the costs provided and, therefore, are not reflected in the generation costs calculated in the study.The cost estimates do not substitute for detailed economic evaluations required by investors and utilities at the stage of project decision and implementation that should be based on project specific assumptions, using a framework adapted to the local conditions and a methodology adapted to the particular context of the investors and other stakeholders.Moreover, the reform of electricity markets has changed the decision making in the power sector and led investors to take into account the financial risks associated with alternative options as well as their economic performance. In view of the risks they are facing in competitive markets, investors tend to favour less capital intensive and more flexible technologies. The used methodology for calculating generation costs in this study does not take business risks in competitive markets adequately into account.The introduction of liberalisation in energy markets is removing the regulatory risk shield where integrated monopolies can transfer costs and risks from investors to consumers and taxpayers. Investors now have additional risks to consider and manage. For example, generators are no longer guaranteed the ability to recover all costs from power consumers. Nor is the future power price level known. Investors now have to internalise these risks into their investment decision making. This adds to the required rates of return and shortens the time frame that investors require to recover the capital. Private investors’required real rates of return may be higher than the 5% and 10% discount rates used in this study and the time required to recover the invested capital may be shorter than the 30 to 40years generally used in this study.Main resultsCoal-fired generating technologiesMost coal-fired power plants have specific overnight construction costs ranging between 1000 and 1500USD/kWe. Construction times are around four years for most plants. The fuel prices (coal, brown coal or lignite) assumed by respondents during the economic lifetime of the plants vary widely from country to country. Expressed in the same currency using official exchange rates, the coal prices in 2010 vary by a factor of twenty. Roughly half of the responses indicate price escalation during the economic lifetime of the plant while the other half indicates price stability.At 5% discount rate, levelised generation costs range between 25 and 50USD/MWh for most coal-fired power plants. Generally, investment costs represent slightly more than a third of the total, while O&M costs account for some 20% and fuel for some 45%.At 10% discount rate, the levelised generation costs of nearly all coal-fired power plants range between 35 and 60USD/MWh. Investment costs represent around 50% in most cases. O&M cost account for some 15% or the total and fuel costs for some 35%.Gas-fired generating technologiesFor the gas-fired power plants the specific overnight construction costs in most cases range between 400 and 800USD/kWe. In all countries, the construction costs of gas-fired plants are lower than those of coal-fired and nuclear power plants. Gas-fired power plants are built rapidly and in most cases expendi-tures are spread over two to three years. The O&M costs of gas-fired power plants are significantly lower than those of coal-fired or nuclear power plants. Most gas prices assumed in 2010 are ranging between 3.5 and 4.5USD/GJ. A majority of respondents are expecting gas price escalation.At a 5% discount rate, the levelised costs of generating electricity from gas-fired power plants vary between 37 and 60USD/MWh but in most cases it is lower than 55USD/MWh. The investment cost represents less than 15% of total levelised costs; while O&M cost accounts for less than 10% in most cases. Fuel cost represents on average nearly 80% of the total levelised cost and up to nearly 90% in some cases. Consequently, the assumptions made by respondents on gas prices at the date of commissioning and their escalation rates are driving factors in the estimated levelised costs of gas generated electricity. The current gas prices are on a relatively high level. The gas price projections in 2010 of some of the respondents in the study are higher than the current level and a few are lower than the current level. The IEA gas price assumptions given in World Energy Outlook 2004(IEA, 2004) are markedly different.At a 10% discount rate, levelised costs of gas-fired plants range between 40 and 63USD/MWh. They are barely higher than at the 5% discount rate owing to their low overnight investment costs and very short construction periods. Fuel cost remains the major contributor representing 73% of total levelised generation cost, while investment and O&M shares are around 20% and 7% respectively.Nuclear generating technologiesFor the nuclear power plants the specific overnight investment costs, not including refurbishment or decommissioning, vary between 1000 and 2000USD/kWe for most plants. The total levelised investment costs calculated in the study include refurbishment and decommissioning costs and interest during construction. The total expense period ranges from five years in three countries to ten years in one country. In nearly all countries 90% or more of the expenses are incurred within five years or less.At a 5% discount rate, the levelised costs of nuclear electricity generation ranges between 21 and 31USD/MWh except in two cases. Investment costs represent the largest share of total levelised costs, around 50% on average, while O&M costs represent around 30% and fuel cycle costs around 20%.At a 10% discount rate, the levelised costs of nuclear electricity generation are in the range between 30 and 50USD/MWh except in two cases. The share of investment in total levelised generation cost is around 70% while the other cost elements, O&M and fuel cycle, represent in average 20% and 10% respectively.Wind generating technologiesFor wind power plants the specific overnight construction costs range between 1000 and 2000USD/kWe except for one offshore plant. The expense schedules reported indicate a construction period of between one to two years in most cases.The costs calculated and presented in this report for wind power plants are based on the levelised lifetime methodology used throughout the study for consistency sake. This approach does not reflect specific costs associated with wind or other intermittent renewable energy source for power generation and in particular it ignores the need for backup power to compensate for the low average availability factor as compared to base-load plants.For intermittent renewable sources such as wind, the availability/capacity of the plant is a driving factor for levelised cost of generating electricity. The reported availability/capacity factors of wind power plants range between 17 and 38% for onshore plants, and between 40 and 45% for offshore plants except in one case.At a 5% discount rate, levelised costs for wind power plants considered in the study range between 35 and 95USD/MWh, but for a large number of plants the costs are below 60USD/MWh. The share of O&M in total costs ranges between 13% and nearly 40% in one case.At a 10% discount rate, the levelised costs of wind generated electricity range between 45 and more than 140USD/MWh.Micro-hydro generating technologiesThe hydro power plants considered in the study are small or very small units. At a 5% discount rate, hydroelectricity generation costs range between some 40 and 80USD/MWh for all plants except one. At a10% discount rate, hydroelectricity generation costs range between some 65 and 100USD/MWh for most plants. The predominant share of investment in total levelised generation costs explains the large difference between costs at 5 and 10% discount rate.Solar generating technologiesFor solar plants the availability/capacity factors reported vary from 9% to 24%. At the higher capacity/availability factor the levelised costs of solar-generated electricity are reaching around150USD/MWh at a 5% discount rate and more than 200USD/MWh at a 10% discount rate. With the lower availability/capacity factors the levelised costs of solar-generated electricity are approaching or well above 300USD/MWh.Combined heat and power generating technologiesFor combined heat and power the total levelised costs of generating electricity are highly dependent on the use and value of the co-product, the heat, and are thereby very site specific. The expert group agreed on a pragmatic approach of calculating the levelised costs of generating electricity for this study. At a 5%discount rate, the levelised costs range between 25 and 65USD/MWh for most CHP plants. At a10%discount rate, the costs range between 30 and 70USD/MWh for most plants.Other generating technologiesLevelised costs were also computed for the remaining technologies. Considering the low number of responses for these technologies the results cannot be used outside the context of each specific case. ConclusionsThe lowest levelised costs of generating electricity from the traditional main generation technologies are within the range of 25-45USD/MWh in most countries. The levelised costs and the ranking of technologies in each country are sensitive to the discount rate and the projected prices of natural gas and coal.The nature of risks affecting investment decisions has changed significantly with the liberalisation of electricity markets, and this has implications for determining the required rate of return on generating investments. Financial risks are perceived and assessed differently. The markets for natural gas are under-going substantial changes on many levels. Also the coal markets are under influence from new factors. Environmental policy is also playing a more and more important role that is likely to significantly influence fossil fuel prices in the future. Security of energy supply remains a concern for most OECD countries and may be reflected in government policies affecting generating investment in the future. This study provides insights on the relative costs of generating technologies in the participating countries and reflects the limitations of the methodology and generic assumptions employed. The limita-tions inherent in this approach are stressed in the report. In particular, the cost estimates presented are not meant to represent the precise costs that would be calculated by potential investors for any specific project. This is the main reason explaining the difference between the study’s findings and the current global preference in reformed electricity markets for gas-fired technologies.Within this framework and limitations, the study suggests that none of the traditional electricity generating technologies can be expected to be the cheapest in all situations. The preferred generating technology will depend on the specific circumstances of each project. The study indeed supports that on a global scale there is room and opportunity for all efficient generating technologies.。

盈透证券决策模型

盈透证券决策模型

盈透证券(Interactive Brokers)是一家提供在线交易平台的券商,其决策模型主要包括以下几个方面:

1. 基本面分析:盈透证券提供了丰富的公司财务数据和市场研究分析,帮助投资者分析企业的基本面情况,例如财务报表、业绩增长、市场竞争等因素。

2. 技术分析:盈透证券提供了多项技术分析工具,包括各种形态图、均线、指标等,帮助投资者分析股票的价格趋势及波动情况,以及预测未来的价格变动方向。

3. 市场情绪分析:盈透证券提供了社交媒体情绪分析工具,帮助投资者了解市场情绪变化、投资者情绪、市场热点等信息,从而更好地进行投资决策。

4. 风险控制:盈透证券提供了多种风险控制工具,例如止损单、融资融券等,帮助投资者在投资过程中更好地保护风险,降低投资亏损的风险。

综上所述,盈透证券的决策模型主要以基本面分析、技术分析、市场情绪分析和风险控制为主要内容,为投资者提供全面的决策支持。

英汉对照QFII

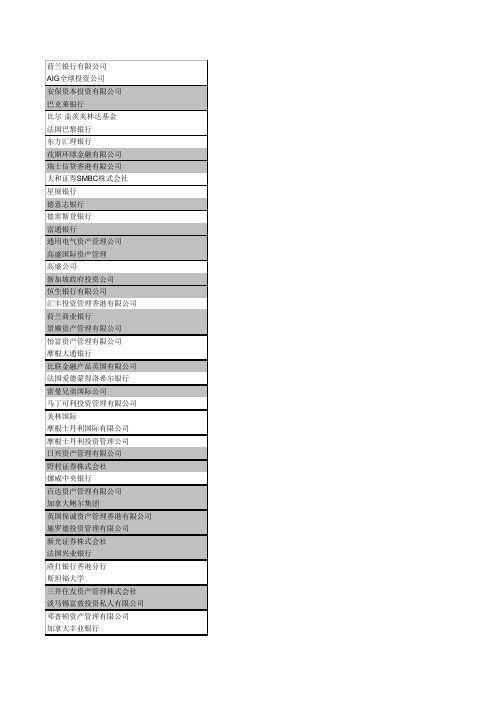

荷兰银行有限公司 AIG全球投资公司 安保资本投资有限公司 巴克莱银行 比尔· 盖茨美林达基金 法国巴黎银行 东方汇理银行 花期环球金融有限公司 瑞士信贷香港有限公司 大和证券SMBC株式会社 星展银行 德意志银行 德雷斯登银行 富通银行 通用电气资产管理公司 高盛国际资产管理 高盛公司 新加坡政府投资公司 恒生银行有限公司 汇丰投资管理香港有限公司 荷兰商业银行 景顺资产管理有限公司 怡富资产管理有限公司 摩根大通银行 比联金融产品英国有限公司 法国爱德蒙得洛希尔银行 雷曼兄弟国际公司 马丁可利投资管理有限公司 美林国际 摩根士丹利国际有限公司 摩根士丹利投资管理公司 日兴资产管理有限公司 野村证券株式会社 挪威中央银行 百达资产管理有限公司 加拿大鲍尔集团 英国保诚资产管理香港有限公司 施罗德投资管理有限公司 新光证券株式会社 法国兴业银行 渣打银行香港分行 斯坦福大学 三井住友资产管理株式会社 淡马锡富敦投资私人有限公司 邓普顿资产管理有限公司 加拿大丰业银行

第一生命保险相互会社 香港上海汇丰银行有限公司 瑞士银行 瑞银环球资产管理新加坡有限RO Bank N.V. AIG Global Investment Corp AMP Capital Investors Limited Barclays bank PLC Bill & Melinda Gates Foundation BNP Paribas CALYONS.A. Citigroup Global Markets Limited Credit Suisse Hong Kong Limited Daiwa Securities SMBC CO. Ltd. DBS Bank Ltd. Deutsche Bank Aktiengesellschaft Dresdner Bank Aktiengesellschaft Fortis Bank SA/NV GE Asset Management Incorporated Goldman Sachs Asset Management International. Goldman, Sachs &Co Government of Singapore Investment Corporation Pte Ltd Hang seng Bank HSBC Investments Hong Kong Limited ING Bank N. V. INVESCO Asset Management Limited JF Asset Management Limited JPMORGAN CHASE BANK KBC Financial Products UK Ltd La Compagnie Financierr Edmond de Rothschild Banque Lehman Brothers InternationalEurope Martin Currie Investment Management Ltd Merrill Lynch International Morgan Stanley & Co. International Limited Morgan Stanley Investment Management Inc. Nikko Asset Management Co. Ltd. Nomura Securities co, Ltd. Norges Bank Pictet Asset Management Limited Power Corporation of Canada Prudential Asset ManagementHong KongLimited Schroder investment Management Limited Shinko Securities Co. Ltd Société Générale Standard Chartered BankHong Konglimited Stanford University Sumitomo Mitsui Asset Management Company, Limited Temasek Fullerton Alpha Investments Pte Ltd Templeton Asset Management Ltd The Bank of Nova Scotia

股票阿莱德简介

股票阿莱德简介

股票阿莱德(AllyInvest)是美国知名的在线投资平台,旨在提供全方位的投资服务。

该平台由阿莱德金融公司(Ally Financial)运营,公司总部位于密歇根州的底特律市。

阿莱德金融公司成立于1919年,最初是一家汽车贷款公司,随着时间的推移,公司逐渐扩大了业务范围,涉及到了银行、理财、证券等领域。

2016年,阿莱德金融公司收购了在线券商TradeKing,并将其改名为股票阿莱德。

股票阿莱德提供了多种投资产品,包括股票、期权、债券、基金等。

用户可以通过网页端或移动端进行交易,同时,该平台还提供了丰富的研究和分析工具,帮助用户更好地了解市场动态和投资机会。

股票阿莱德的交易费用相对较低,股票交易费用为$4.95,期权交易费用为$4.95加上每张合约$0.65的费用,债券交易费用为$1每张债券,基金交易费用为免费。

此外,该平台还提供了免佣金交易的ETF交易。

股票阿莱德的客户服务也备受好评,用户可以通过电话、邮件、在线聊天等多种方式联系客服,平台还提供了专业的投资顾问服务,帮助用户制定个性化的投资计划。

总体来说,股票阿莱德是一家值得信赖的在线投资平台,其低廉的交易费用、丰富的投资产品和优质的客户服务,使其成为了广大投资者的首选之一。

- 1 -。

如何选择资金盘,tec,lti,nel东亿国际案例分析

1、什么是电子股?为什么电子股只涨不跌?电子股就是网上理财,理财模式是借鉴的基金股票,推广模式是借鉴的直销,为广大会员提供一个虚拟循环投资理财的游戏平台,平台的操作完全由会员二十四小时自由操作,随时可将投资的资金转入自己的银行卡内,不存在用欺骗手段甚至强制进行交易的敛财行为,只有当会员获利要收回资金时,收取适当的手续费,这应该是天经地义的事吧!游戏理财是个新的商业机会,就像当初股票、房地产一样。

至于为什么只涨不跌,我不是说了么理财模式是借鉴的基金股票,但是还有推广啊,股票是没有推广制度存在的,正因为推广制度存在,所以做的人越来越多,累计的资金就越来越多,而电子股不增发,那么其价值就会增加,所以电子股只涨不跌,单边上涨。

不过要是认为没风险就错了,电子股风险和股票风险不一样,股票风险在于股票下跌,而电子股风险在于崩盘,崩盘原因一般是因为公司操盘不好造成的,比如动态奖励太高,抽资严重,负面效应严重等。

2、电子股如何选择简单说盘子分两类,长期和短期,做投资并想发展人脉的做长期盘子,做投机想四两拨千斤的做短期盘子,一般比较专业的都选择做一个长期稳定的盘子做动态,再选择几个短期盘子做静态,一旦短期盘子涨不动了就抛售,再换其他的短期盘子。

3、对于新手来说选盘子比较难,很难看出盘子是长期还是短期的,以下是几个判断依据:选择稳健长久的资金盘:1、涨势合理(按市场供需情况来)2、原始发行数量不要太多(一百多万股较合适),不要经常拆分(拆分次数多,卖盘压力大,泡沫就多)3、服务器在国外(国内政策风险大)4、提现、卖股自由,没有限制5、百度资金盘网站价值,如百度:“网站价值”,服务器所在地、租用年限都一目了然,租用时间就跟我们租店铺付店租一样,租的时间越长,证明老板心态越好,公司也越有实力。

4、如何区分长期和短期盘子网络理财项目动态推广奖励主要是直推和对碰奖励,其他奖励也有,但是都比较少,长期盘子一般对碰奖励设置得比较高,直推奖励很少甚至没有,而短期盘子直推奖比较高,对碰奖相对要低些。

顺安资本投过的项目

顺安资本投过的项目顺安资本是一家专注于投资初创企业的风险投资公司,其投资项目覆盖了多个领域,涵盖了科技、金融、医疗、教育等多个行业。

以下是顺安资本曾经投资过的几个项目。

一、智能科技领域顺安资本投资了一家名为“智能科技”的初创公司。

该公司致力于开发智能化的解决方案,通过人工智能和大数据分析,为企业提供智能化的业务流程管理工具。

这一项目得到了市场的广泛认可,并取得了良好的成绩。

该公司的产品已经成功应用于多个行业,提升了企业的效率和竞争力。

二、金融科技领域顺安资本还投资了一家金融科技初创企业。

该企业致力于利用新技术和创新模式改变传统金融行业的格局。

通过引入区块链技术和人工智能算法,该企业为用户提供了更安全、高效的金融服务。

该项目在金融科技领域取得了重要突破,被认为是行业的领军者之一。

三、医疗健康领域顺安资本还投资了一家医疗健康初创企业。

该企业致力于开发基于人工智能的医疗诊断和治疗方案。

通过深度学习算法和医学数据库的结合,该企业研发出了一套准确、高效的医疗解决方案。

该项目在医疗健康领域具有重要的应用价值,为患者提供了更加精准和个性化的医疗服务。

四、教育科技领域顺安资本还投资了一家教育科技初创企业。

该企业致力于利用新技术和创新模式改变传统教育行业的发展方式。

通过引入虚拟现实技术和在线教育平台,该企业为学生提供了更加丰富、互动的学习体验。

该项目在教育科技领域取得了显著的突破,为学生提供了更加优质的教育资源。

五、文化娱乐领域顺安资本还投资了一家文化娱乐初创企业。

该企业致力于推广中国传统文化和优秀的文化艺术作品。

通过线上线下结合的方式,该企业为用户提供了更加便捷、多样化的文化娱乐体验。

该项目在文化娱乐领域取得了良好的市场反响,为用户带来了丰富多彩的文化生活。

以上是顺安资本投资过的几个项目,这些项目在各自领域都取得了不错的成绩。

顺安资本将继续致力于发现和培育有潜力的创新企业,为他们提供资金和资源支持,帮助它们实现快速成长并取得成功。

经理人薪酬管制政策的中美比较

经理人薪酬管制政策的中美比较

王新;毛慧贞

【期刊名称】《财会月刊(理论版)》

【年(卷),期】2012(000)008

【摘要】无论是高度发达市场经济的美国,还是正处于转轨期的我国,经理人过高薪酬的问题已成为社会关注的热点。

政府如何对经理人薪酬实施干预既关系到社会的公平与稳定,也关系到能否有效调砘经理人积极性。

本文系统对比和研究了中关企业经理人薪酬管制政策的历史背景、管制目标、管制措施、管制立法手段、经理人对薪酬管制态度等方面的差异,以期对我国企业的经理人薪酬管制政策的制定提供参考和政策建议。

【总页数】3页(P75-77)

【作者】王新;毛慧贞

【作者单位】西南财经大学国际商学院,成都610074/西南财经大学会计学院,成都610074;西南财经大学国际商学院,成都610074/西南财经大学会计学院,成都610074

【正文语种】中文

【中图分类】F272.91

【相关文献】

1.薪酬管制降低了经理人的激励效率吗?——基于迎合效应的薪酬结构模型分析[J], 陈菊花;隋姗姗;王建将

2.经理人自定薪酬与薪酬考核委员会的本原性质分析 [J], 杨慧辉;张晓岚;张若远

3.薪酬管制与经理人超额薪酬的研究综述 [J], 竹丽婧

4.经理人股票期权会计处理的中美比较与思考 [J], 姚宝燕

5.审计委员会与薪酬委员会委员交叠任职、盈余管理与经理人薪酬 [J], 邓晓岚;陈运森;陈栋

因版权原因,仅展示原文概要,查看原文内容请购买。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

9

Slides\projplan\finperf.ppt

CLIENT SATISFACTION

• LS:

– Meeting the Contract Requirements

– Avoid Providing Extras Due to the Lure of Future Work

– Client Personnel May Not Understand Contract. Help Them

• T&E: Do What It Takes. Relationship Maintenance Is Critical

10

Slides\projplan\finperf.ppt

OVERHEARD COMMENTS

• If You Hear These Types of Comments on LS Projects, Watch Out!

20

Slides\projplan\finperf.ppt

Common Design Overruns

• Failure to obtain Owner’s timely decision

• Staff starting too soon, leaving late

• Understand every discipline can’t finish at same time • Failure to ask for enough compensation for charges

PM Workshop

Controlling Project Financial Performance

TOPICS

• LS Versus T&E Mentality

• Controlling IDC Labor to Budget

• Forecast Preparation

• Design to Estimate

– “It Would Be Nice to Show Some Added Details.”

11

Slides\projplan\finperf.ppt

SUMMARY

• LS

– Meet Contract Requirements and Profit Goals

– Staff LS Mentality, a Good Plan and PM Negotiating Skills Are Keys to Success

Controlling IDC Labor To Budget

EXPECTATIONS

• Each Discipline Will Complete Their Scope of Work and Finish Within +/- 5% of Their Current Budget • PM Will Control the Project to Meet All Requirements and Finish at or Below the Current Budget

5

Slides\projplan\finperf.ppt

BUDGET

LS • Management to Budget Critical • Each Discipline, Expense, Contract and Overall Project Managed on Not to Exceed Basis • Contingency Covers Variations From Plan • Use Internal DCNs • Encourage Labor Avoidance Ideas T&E • Expenditures Will Be Fully Justifiable • Client Will Recognize That Value Received and Cost Are in Balance

Slides\projplan\finperf.ppt

SCOPE OF WORK

LS • Well Defined • Bounded Tasks • Specific Deliverables • Specific Level of Detail • Staff Must Understand Scope • Frequent Scope Negotiations With Client T&E • Only a Very General Understanding at Start • Evolution of Tasks, Deliverables, Level of Detail As Project Progresses • Scope Evolution Must be well Documented

6

Slides\projplan\finperf.ppt

SCHEDULE

LS

• Not on Schedule = Schedule May = Contract Penalties

• Client Decisions/input Must Be Expedited

• Follow Standard IDC Techniques to Control and Coordinate the Project

• Stay On Schedule!

19

Slides\projplan\finperf.ppt

WHEN PROBLEMS ARISE

• Hold In-depth Discussion With Lead(s) Having Budget Problems. Lead Will Develop Written Plan to Regain Control - Short Term • Plan Doesn’t Work - Request DM Assistance Until the Problem or the Lead Is Fixed • Still Got Problems? Analyze How You Are Running the Project

T&E

• Maintain an Acceptable Level of Client Satisfaction

7

Slides\projplan\finperf.ppt

CHANGES - LS

• Avoid Causing Changes

– Disrupts Plan

– Hard to Negotiate (Perception) – Client Chose LS Because They Knew What They Wanted – No “Scope Creep”

• Client Adds Over and Above Contract - Get a Signed Change Order Before Proceeding

8

Slides\projplan\finperf.ppt

CHANGES - T&E

• Changes Are Expected by Client and Add to A&E Revenue • Document All Changes to Fully Justify Cost

• T&E

– Maintain Client Satisfaction and Relationship

– Staff T&E Mentality and Keeping the Client Informed Are Keys to Success

12

Slides\projplan\finperf.ppt

– Discuss Problems/Constraints

• Internal DCNs - LS Projects:

– Shift Budget Between Disciplines

– Allocate Contingency – Capture Forecasted Discipline Underruns for Contingency

14

Slides\projplan\finperf.ppt

TECHNIQUES

• Proposal: Use workplan with forecasted margin (multiplier). • At Project Start PM and Each Lead Update:

– Scope/deliverables – Schedule – Workplan (Both Sign)

– “This Drawing Would Be a Lot Easier to Understand If We Made It Two Drawings.”

– “No E3s Are Available. I’ll Use an E5.”

– “If We Rework the Design, We Can Save the Client a Lot During Construction.”

• Update Forecasts at Least Every Two Weeks

15

Slides\projplan\finperf.ppt

TECHNIQUES

• Provide a Report to Leads and Discuss Weekly:

– Last Weeks Labor Actuals Versus Forecast – Expected Labor This Week

17

Slides\projplan\finperf.ppt

TECHNIQUES

• External DCNs - T&E Projects:

– Handle Similar to LS, but Expect More Changes