Probabilistic versus Possibilistic Fuzzy Clustering An Unifying Model

英文速读资料金融时报

经济预测,欲望永不眠辞旧迎新的时候,人们为何总期望经济学家做预测呢?预测成绩怎样?这是FT"卧底经济学家"蒂姆·哈福德有趣的解答。

An insatiable desire to peer into the futureThe wonderful thing about forecasts is that they all sound very profound--------------------------It’s that time of year again. Time for you to make your predictions for 2013.You’re kidding, right? You’re asking an economist for predictions?Just my little joke. But surely you’re not a propereconomist if you can’t make a few predictions. Isn’t that the whole point of the economic profession – to make dozens of mutually contradictory forecasts with impunity?Well, the impunity is a topic worth discussing. But the economics profession could do with a few more disagreements, I think. In 1995, FT columnist John Kay examined the record of British economic forecasters from 1987 to 1994. He discovered that they tended to all say much the same thing. The only dissenter was reality: economic growth often fell outside the range of all 34 forecasts.So economists are terrible forecasters. What else is new?It isn’t just economists who are terrible forecasters. Take the quantitative analysts responsible for Goldman Sachs’s notorious “25 standard deviation” episode – presumably physicists or mathematicians.25 standard deviation?At the beginning of the financial crisis, the chief financial officer of Goldman Sachs explained that the firm was seeing “25 standard deviation moves, several days in a row” – a statement that, translated into English, means “according to our models, what we’re seeing is very unlucky”.How unlucky?Oh, the sort of bad luck you see once every 28, 900, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000,000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000, 000 years, given certain assumptions about what Goldman might have meant. For reference the universe is about 14,000,000,000 years old. The alternative to the “very unlucky” hypothesis, of course, is that the quantitative models didn’t produce very good forecasts.Well, that’s a forecast so bad that I can’t believe an economist wasn’t involved somewhere.You may be right. But I can give you another example: the 300-odd experts recruited by Philip Tetlock, the psychologist, for his epic study of forecasting in political science. Prof Tetlo ck’s conclusions are wide-ranging and painstaking, but if I can be forgiven an excessively brief summary, he finds that all sorts of people with plausible claims to expertise –diplomats, political advisers, journalists and academics –produce lame forecasts of political and economic events.Nate Silver seems to be able to forecast just fine.Well, yes, notwithstanding the politically motivated “Nate Silver can’t add up” school of criticism, Mr Silver, and other statisticians such as Drew Linzer and Sam Wang, successfully forecast the outcome of the US elections in some detail. Contrasted against a background of bloviation, it was impressive. But if psephology is Exhibit A in the Museum of Successful Social Science Forecasts, let’s reflect on how modest our ambitions must have become: US elections are frequently repeated, with behaviour that shows considerable historical persistence, and an astonishing amount of detailed quantitative data are available. The elections take place at a fixed date, according to well-understood rules, and with a narrowly defined space of possible outcomes. It’s easy to see that forecasting a win for Barack Obama, while better than forecasting a win for Mitt Romney, is not quite as hard as successfully predicting if and when Greece will leave the eurozone.You’re pretty quick with the excuses.No excuses. We just can’t see into the future. I don’t thinkthat’s any surprise, nor an embarrassment. The question is why there’s such a hunger for social science predictions, when the practice is so transparently pointless.It’s a test of expertise.If so, then monkeys are as expert as professors of political economy. I wouldn’t want to be quite so cynical. I think forecasting in a complex world is a poor test of expertise because luck is the overwhelming success factor.So why do we love predictions?No idea. Here’s one guess: saying “the UK economy will recover strongly in 2012” or “President Assad will be out of office by June” compresses a vast amount of expertise and analysis into a few words.But the words are probably meaningless.Yes. But it’s Christmas. Actually studying the situation in detail is far too much like hard work真是费神的事. Thewonderful thing about a forecast is that both the forecaster and his audience feel that something profound has been expressed. And nobody will remember the forecast anyway.It’s time of …….time for; but surely you…..if you …….; Isn’t that the whole point of …….Well, but……..I think.So…… what else is new?It isn’t just , presumably……;But if I can be forgivenWell yes,notwithstandingAs hard asIf and whenIf so….共和党旗手埃里克·坎托年轻的国会共和党领袖坎托是个野心勃勃和勤奋异常的人,FT华盛顿分社社长马利德(Richard McGregor)认为他是共和党的新旗手。

Fuzzy Logic - PCU Teaching Staffs模糊逻辑与教学人员

e.g. On a scale of one to 10, how good was

the dive?

10

9

9

9.5

Fuzzy Probability

Example #1

Billy has ten toes. The probability Billy has nine toes is zero. The fuzzy membership of Billy in the set of people with about nine toes, however, is nonzero.

Looking at Fuzzy Logic

4. Degree of Membership (Fuzzy Linguistic Variables)

Fuzzy and “Crisp” Control

Examples include close, heavy, light, big, small, smart, fast, slow, hot, cold, tall and short.

Gödel showed all such theories are either incomplete or inconsistent.

Gödel & Einstein (Princeton: August 1950)

Gödel’s Proof

Inconsistent: Show that 1+1=2 and 1+12. Incomplete: We cannot show that 1+1=2 .

Is such logic more compatible with Asian philosophy?

1Cor 13:12 “For now we see through a glass, darkly; but then face to face: now I know in part; but then shall I know even as also I am known.”

超实用备战高考英语考试易错题——阅读理解:主旨大意题(大陷阱) (解析版)

易错点17 阅读理解主旨大意题目录01 易错陷阱(3大陷阱)02 举一反三【易错点提醒一】标题类易混易错点【易错点提醒二】段落大意类易混易错点【易错点提醒三】文章大意类易混易错点03 易错题通关养成良好的答题习惯,是决定高考英语成败的决定性因素之一。

做题前,要认真阅读题目要求、题干和选项,并对答案内容作出合理预测;答题时,切忌跟着感觉走,最好按照题目序号来做,不会的或存在疑问的,要做好标记,要善于发现,找到题目的题眼所在,规范答题,书写工整;答题完毕时,要认真检查,查漏补缺,纠正错误。

易错陷阱1:标题类易混易错点。

【分析】标题类是对中心思想的加工和提炼,可以是单词、短语、也可以是句子。

她的特点是短小精悍,多为短语;涵盖性、精确性强;不能随意改变语言表达的程度和色彩。

如果是短语类选项,考生容易混淆重点,此时应当先划出选项的关键词。

此类题和文章的中心主题句有很大关系。

中心主题句一般出现在第一段,有时第一段也可能引出话题,此时应当重点关注第二段和最后一段,看看是否会出现首尾呼应。

易错陷阱2:段落大意类易混易错点。

【分析】每个段落都有一个中心思想,通常会在段落的第一句或最后一句体现,这就是段落主题句。

如果没有明显的主题句时,应当根据段落内容概括处段落大意。

有时考生还会找错文章对应位置,盲目选词文中相同的词句,而出现文不对题的现象。

易错陷阱3:文章大意类易混易错点。

【分析】确定文章主旨的方法是:先看首尾段或各段开头再看全文找主题句,若无明显主题句,就通过关键词句来概括。

如,议论文中寻找表达作者观点态度的词语,记叙文中寻找概括情节和中心的动词或反映人物特点的形容词。

文中出现不同观点时,要牢记作者的观点彩色体现全文中心的。

此时,要注意转折词,如:but, however, yet, in spite of, on the contrary等。

【易错点提醒一】标题类易混易错点【例1】(浙江省义乌五校2023-2024学年高三联考试题)The scientist’s job is to figure out how the world works, to “torture (拷问)” Nature to reveal her secrets, as the 17th century philosopher Francis Bacon described it. But who are these people in the lab coats (or sports jackets, or T-shirts and jeans) and how do they work? It turns out that there is a good deal of mystery surrounding the mystery-solvers.“One of the greatest mysteries is the question of what it is about human beings — brains, education, culture etc. that makes them capable of doing science at all,” said Colin Allen, a cognitive scientist at Indiana University.Two vital ingredients seem to be necessary to make a scientist: the curiosity to seek out mysteries and the creativity to solve them. “Scientists exhibit a heightened level of curiosity,” reads a 2007 report on scientific creativity. “They go further and deeper into basic questions showing a passion for knowledge for its own sake.” Max Planck, one of the fathers of quantum physics, once said, the scientist “must have a vivid and intuitive imagination, for new ideas are not generated by deduction (推论), but by an artistically creative imagination.”......ong as our best technology for seeing inside the brain requires subjects to lie nearly motionless while surrounded by a giant magnet, we’re only going to make limited pro gress on these questions,” Allen said.What is a suitable title for the text?A.Who Are The Mystery-solversB.Scientists Are Not Born But MadeC.Great Mystery: What Makes A ScientistD.Solving Mysteries: Inside A Scientist's Mind【答案】C【解析】文章标题。

虚无悖论

上节提及,资产的升值代表着财富累积的增加,因此,所有资产皆可以看为财富累积的仓库。问题是,在费雪的传统中,资产有生产力,带来租值或收入,而这些收入以利率折现是资产的价值,称财富。本身毫无生产力的资产也是资产,但我们无从以其产出的收入折现。这类资产的主要用场是累积财富,当年费雪没有分析过。以「仓库」来描述这类资产是恰当的,虽然其他有生产力的资产也是财富累积的仓库。-

这里顺便一提。在同类的收藏品中,那些所谓「精品」的,在市价一般上升时其升幅的百分率通常比较高,而市价一般下降时其跌幅百分率比较小。不是永远如是,是或然率如是。有两个原因。其一是精品通常不多,其存在市场通常知道。比较平庸的不仅远为量大,其总量究竟有多少市场通常不知道。其二,称得上是精品的,假冒远为困难,出现赝品的机会比较少。-

从上述的四个需要的条件看,一个健全的收藏品仓库的形成可真不易,而正因为得之不易,失之也难。一个健全的收藏仓库可以长存不破。-

印象画派对乾隆皇帝-

要举出收藏仓库的成功例子,西方应该首推法国十九世纪的印象派画作。中国呢?今天看我选十八世纪的乾隆皇帝。乾隆不仅是神州历来最大的收藏家,也可能是人类历史的收藏一哥。此帝也,有点发神经,收藏兴趣广泛,工程之巨属天方夜谭。我个人认为乾隆自己指导炮制的物品有点俗气,但风格明确。(他的书画收藏有他的题跋、玺印风格。)不乱来,乾隆凡事苛求:瓷器华丽,玉雕精绝。魄力雄强,这个皇帝写过逾万首诗;手痒,到处题字,遗留下来的墨宝无数。好印章,据说为他刻的逾八千件。别的我没有研究,但有点研究的印章钮雕,我认为乾隆御用的来来去去是同一组人,不仅风格相同,刀法也差不多。这样的皇帝日理万机,六下江南,竟然活到八十然在第二章我细说了复息利率的杀伤力,持久地收藏不容易斗得过利息代价的蹂躏。然而,收藏品的市值上升不是平稳的,可以有大幅的波动,机缘巧合,市值的上升可以有一段长时期高于利息的代价。上世纪八十年代,因为日本的经济不济,法国印象派的画作下跌得急,但十年后回升。今天回顾,六十年前收藏印象派的画,选择得对,其升值高于以复息算的利息。-

贝叶斯学派的英文

贝叶斯学派的英文The Bayesian school of thought offers a probabilistic approach to statistical inference, emphasizing the updatingof beliefs based on new evidence. It's a way of learning from the world, where each piece of information refines our understanding.This method stands in contrast to the frequentist interpretation, which relies on fixed parameters and long-term frequencies. Bayesians, however, treat probabilities as degrees of belief, which can be subjective and personal.The beauty of Bayesian analysis lies in its ability to incorporate prior knowledge, making it incredibly flexibleand powerful in uncertain situations. It's not just about the data we have, but also about the wisdom we bring to the table.In fields ranging from medicine to machine learning, Bayesian techniques are revolutionizing the way we make decisions. By continuously updating our models with new data, we can navigate through the fog of uncertainty with greater confidence.Yet, the Bayesian approach also comes with challenges. It requires careful consideration of prior assumptions, whichcan significantly influence the conclusions drawn. It's a reminder that even in the realm of mathematics, oursubjective perspectives play a crucial role.As we delve deeper into the Bayesian paradigm, we find a philosophy that resonates with the human condition: our quest for knowledge is an ongoing journey, never a destination.It's a testament to the power of embracing change and learning from the world around us.。

抗帕金森病药

Origin of Parkinson disease

James Parkinson (Britain): 1817 年在Essay on the shaking Palsy 一书中第一次提出“震颤麻痹” 。 Parkinson去世40年后,神经病学家Charcot JM对震 颤麻痹补充了肌强直这一重要体征,完善了震颤麻痹 的诊断. 为纪念James Parkinson遂以其名字命名为

依据:⑴阻断DA-R的抗精神病药、耗竭DA 抑制纹状体摄取储存DA的利血平 ⑵MPTP→选择性破坏黑质-纹状体 DA能神经元 ⑶帕金森病患者中脑纹状体DA↓

⑷病理学改变:大体/组织学

帕金森病/帕 金森氏征

Sketch map of PD

On physiology state

Ach(+)

DA(-)

中枢胆碱能受体阻断药,减弱纹状体中Ach作用

Clinical uses

早期轻症PD患者

不能耐受L-dopa或L-dopa禁忌症患者

抗精神病药物引起的帕金森氏综合征

与复方多巴合用—协同

L-dopa 口服

90%被外周代谢

药物相互作用

脑内

10%进入血液、 外周组织

L-dopa

卡比多巴

多巴脱羧酶 多潘立酮

Relationship with other drugs

1. 禁止同时服用 Vit-B6

因Vit-B6 是L-dopa脱羧酶辅酶,加速L-dopa在外周 脱羧,进入脑循环L-dopa ↓, ↓疗效、↑不良反应

2.不宜合用吩噻嗪类,利血平

因吩噻嗪类、利血平等通过阻断中枢DA受体和耗竭 DA储存而引起药源性帕金森氏综合征,它们可拮抗 L-dopa的作用

第22章模糊理论

❖本章的學習主題 ❖ 1.認識模糊理論 2.模糊合成 3.模糊綜合評判 4.模糊運算 5.模糊推論 6.模糊控制 7.模擬理論之應用範例

企業研究方法 第 22 章 1

22.1 前言

一般可將資訊分為「可量化的資訊」與「不可量 化的資訊」,其中不可量化的資訊又稱為質化的 資訊,如:「這家公司總經理能力很強」、「這項 產品的品牌形象很好」等口語化的描述。 模糊理論(Fuzzy Theory)乃是積極承認主觀性問 題的存在,進而以模糊集合理論來處理不易量化 的問題,以便能適當而可靠的處理人們主觀評估 問題的方法。 模糊理論是為解決真實世界中普遍存在的模糊現 象而發展的一門學問,1965年美國自動控制學家 Lotfi. A. Zadeh首先提出的一種定量表達工具。

企業研究方法 第 22 章 3

22.2 模糊理論發展歷史

3.人類知識可說是用語言來表達的,而語言中存 在的模糊性,特別是因人而異所產生的主觀 性,也各不相同,這些模糊現象無法使用傳統 的數學工具例如機率等解決,故必須尋找另外 的替代途徑。

企業研究方法 第 22 章 4

22.3 模糊理論的基本概念

表 22-1 傳統集合與 Fuzzy 集合基本精神的比較

傳統集合 使用特徵函數 強調非此即彼的關係 只接受精確不模糊的資訊 硬性二分類法

Fuzzy 集合 (fuzzy set) 使用隸屬函數 接受亦此亦彼的關係 可接受精確不模糊的資訊 軟性的分類法

企業研究方法 第 22 章 5

22.3 模糊理論的基本概念

企業研究方法 第 22 章 6

在模糊集合的定義中,對某一元素X而言,是以μ(x) 來表示X屬於某集合的程度,即將X對應到[0,1]的 函數中,等級愈接近1,則表示該集合包合X元素的 程度愈大,此值稱為(degree of membership),所 以μ(x)稱為隸屬函數(membership function)。 隸屬函數的值只有0與1兩種時,該集合就是傳統的 明確集合(crisp set)。以圖22 - 1為例,來說明模糊 集合與明確集合間的不同。μ(x)表示「中年」的模 糊集合,而C (X)則表示傳統的明確集合。

概率逻辑、不确定逻辑和模糊逻辑之比较

Computer Engineering and Applications 计算机工程与应用2017,53(12)1引言最早人们基于视任何命题不是真就是假,建立了经典数理逻辑及其推理理论[1]。

1920年,Lukasiewicz 考虑到一些命题真假的不确定性,通过模仿经典数理逻辑的演算方法提出了Lukasiewicz n 值逻辑理论。

后来人们又提出了Godel 逻辑,乘积逻辑等[2-3]。

1933年,Kolmogorov 为了处理事件发生的不确定性(称为随机性,如,掷一枚硬币出现正面还是出现反面是随机性问题),基于统计频率的性质建立了概率论。

注意,概率论建立在经典逻辑之上:一个事件要么发生要么不发生,并且要求对于可数个两两不相交事件的并的测度具有可数可加性。

当缺乏历史的和客观的数据时,一些学者也把概率论的思想方法(称为主观概率)用到处理不确定性上去。

1965年,Zadeh 针对概念的不确定性(称为模糊性),通过取值于[0,1]区间的函数,提出了模糊集理论。

自然的,人们通过概率论提出了一种新的非经典逻辑-概率逻辑[4],通过模糊集理论又提出了各种非经典逻辑(称为模糊逻辑),如Hajek 的三角模逻辑(也称BL 逻辑,后来发展到MTL 逻辑)[5-9]。

在2007年,刘宝碇发现概率论和模糊集理论有时不适应主观处理某些问题,又基于正规性公理、对偶性公理、次可加性公理和乘积公理提出了一种主观处理不确定性的新的数学理论,称为不确定理论[10-12]。

它已广泛应用到各种实际问题中[13-14]。

特别是,李和刘基于不确定理论初步提出了不确定命题逻辑[15],陈孝伟提出了带有独立性不确定命题的公式的真值(本项目称真度)计算的一般方法[16]。

张兴芳改进了刘的不确定逻辑推理方法[17-18]。

三种理论处理同一种不确定性问题,自然使得某些概率逻辑、不确定逻辑和模糊逻辑之比较师肖静,张兴芳SHI Xiaojing,ZHANG Xingfang聊城大学数学科学学院,山东聊城252059School of Mathematical Science,Liaocheng University,Liaocheng,Shandong 252059,ChinaSHI Xiaojing,ZHANG paring of probabilistic logic,uncertain logic and fuzzy puter Engi-neering and Applications,2017,53(12):50-52.Abstract :The thinking method of probabilistic logic,subjective probabilistic logic,uncertain logic and fuzzy logic are compared by an example.Own opinions is presented as follows :probabilistic logic based on date statistics is better than other logics.Uncertain logic is better than subjective probabilistic logic.When atom propositions with uncertainty are independent,uncertain logic and fuzzy logic is consistent.However,uncertain logic is better than fuzzy logic in dealing with relevant propositions with uncertainty.But,fuzzy logic is better than their logics in logic reasoning.Key words :probabilistic logic;subjective probabilistic logic;uncertain logic;fuzzy logic摘要:通过一个实例分析比较了概率逻辑、主观概率逻辑、不确定逻辑和模糊逻辑的思想方法。

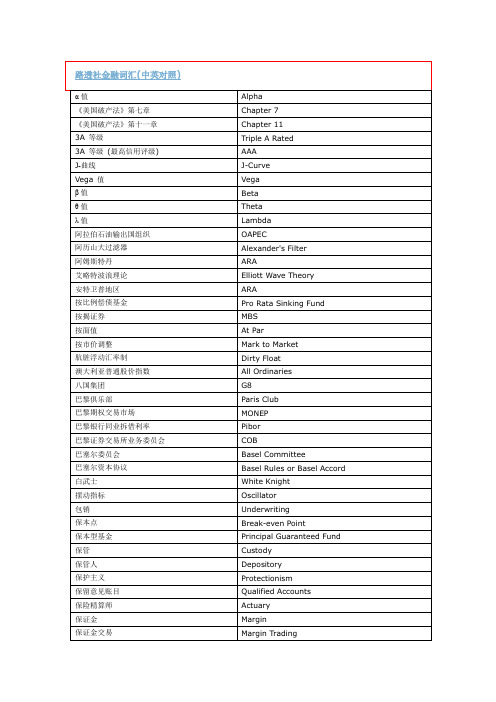

路透社金融词汇中英

路透社金融词汇(中英对照)α值Alpha《美国破产法》第七章Chapter 7《美国破产法》第十一章Chapter 113A 等级Triple A Rated3A 等级(最高信用评级) AAAJ-曲线J-CurveVega 值Vegaβ值Betaθ值Thetaλ值Lambda阿拉伯石油输出国组织OAPEC阿历山大过滤器Alexander's Filter阿姆斯特丹ARA艾略特波浪理论Elliott Wave Theory安特卫普地区ARA按比例偿债基金Pro Rata Sinking Fund按揭证券MBS按面值At Par按市价调整Mark to Market肮脏浮动汇率制Dirty Float澳大利亚普通股价指数All Ordinaries八国集团G8巴黎俱乐部Paris Club巴黎期权交易市场MONEP巴黎银行同业拆借利率Pibor巴黎证券交易所业务委员会COB巴塞尔委员会Basel Committee巴塞尔资本协议Basel Rules or Basel Accord 白武士White Knight摆动指标Oscillator包销Underwriting保本点Break-even Point保本型基金Principal Guaranteed Fund 保管Custody保管人Depository保护主义Protectionism保留意见账目Qualified Accounts保险精算师Actuary保证金Margin保证金交易Margin Trading保证金账户Margin Account报价Quotation报价驱动Quote Driven北美自由贸易协定NAFTA备兑认股权证Covered Warrant备用信贷Back-up Facility背对背贷款Back-to-back Loans倍数Multiples被动式管理Passive Management 被冻结的资产Frozen Assets本地生产总值GDP本国收益率Native Yield本金Principal本票Promissory Note逼仓Squeeze比率分析Ratio Analysis必要收益率Required Return避风港货币Safe Haven Currency 避险Hedging边际成本Marginal Cost变动保证金Variation Margin变动率ROC变动速度ROC变化率Rate of Change标的Underlying标价货币Quoted Currency标普/国际金融公司指数S&P/IFCI标普公司S&P标准差Standard Deviation标准普尔500 股指S&P500标准普尔评级公司Standard & Poor's表达认购意愿Indications of Interest 表决权信托Voting Trust表决权信托凭证VTC表外项目Off Balance Sheet表现费Performance Fees别人的钱OPM并购M&A并股Reverse Stock Split波动率Volatility波动性Volatility波动性分析Volatility Analysis波动性指数Volatility Index波动远期Range Forward波林格区间Bollinger Bands不偿还债务Default不带任何权利Ex-All不带应计利息Flat不抵押保证Negative Pledge不兑现纸币Fiat Money不记名股票Bearer Shares不加权或加权的指数Unweighted/Weighted Indices 不可抗力Force Majeure不可商议的Non-negotiable不可转让的Non-negotiable不良贷款Non-performing Loan不相配Mismatch不需进一步确认的指令Firm Order不做多头亦不做空头Flat布莱克—斯科尔斯模型Black & Scholes Model布雷迪债券Brady Bonds布雷顿森林协定Bretton Woods Agreement部分还本Paydown部分缴款Partly Paid财阀Chaebol财务长CFO财务总监CFO财政年度Financial Year财政收支Fiscal Balance财政政策Fiscal Policy采购经理人指数PMI参与权益Participation参与证书Participation Certificate仓位T aking a Position差价合约Contract for Difference掺水股Watered Stock产能利用率Capacity Utilization产业分析师Sectoral Analysts产业或区域型基金Sector Fund尝试在底部买进Bottom Fishing常规收益率曲线Normal Yield Curve常规债券Vanilla Bond偿付能力Solvency Margin偿付能力比率Solvency Ratio偿还Redemption偿债比率Debt Service Ratio偿债次序Ranking偿债基金Sinking Fund偿债净额Paydown场外交易市场Kerb Market场外交易市场报价表Pink Sheets场外市场OTC超额配股权Greenshoe Option超额认购Oversubscribed超国家金融机构Supranational超级蒙太奇交易显示系统SuperMontage超买Overbought超卖Oversold超前交易Front Running超值股票股息Enhanced Scrip Dividend撤销前有效的指令Good Till Cancelled沉没成本Sunk Costs成本加保费CIF成本加运费价格 C and F成交Done成交额Turnover成交了Mine成交量Trading Volume成交量加权平均价VWAP成交量净额法On Balance Volume承兑行Acceptance House承诺费Commitment Fee承销Underwriting承销商Underwriter承约费Commitment Fee程式交易Program Trading持仓费Carrying Charge持仓头寸Open Position持平Flat持续经营Going Concern持续联系结算(CLS)银行CLS Bank赤字Deficit赤字财政Deficit Financing冲销Write Off筹备七国集团峰会的政府高官Sherpas出口促进计划Export Enhancement Programme出口配额Export Quota出售后回租Sale and Leaseback 初步公开招股说明书Red Herring初步估计Early Estimates初步预测Early Estimates初级产品Commodity初级金属Primary Metals初级市场Primary Markets初级市场交易商Primary Dealer初始保证金Initial Margin除净Ex-All除权/无权获得认股权证Ex-Rights除权/无权获得认股权证Ex-Rights除息Ex-Dividend除息价格Clean Price储备Reserves储备货币Reserve Currency 储蓄率Savings Rate处理能力Throughput触发价格Trigger Price触及市价单MIT触价指令MIT触碰生效期权Trigger Option触碰失效的期权Knockout Option传闻中的预估Whisper Estimates 船舶抵押贷款Bottomry船上交货价格FOB船只总载重量DWT创业基金Venture Capital垂直价差Vertical Spread次级金属Secondary Metals 次级债务Subordinated Debt 次日T/N促销品Kicker存款Deposits存款单CD存款证CD存托凭证Depository Receipts 错配Mismatch错配式票据Mismatch Note大额交易Block Trading大量抛售Bear Raid大数Big Figure大型跨国银行Money Centre Bank大宗商品Commodity呆账Bad Debt代理人账户Nominee Account代理银行Agent Bank贷款安排费Facility Fee贷款损失准备金Loan Loss Provisions贷款息差Lending Margin丹麦的股份有限公司A/S担保Hypothecation担保品Collateral单位信托Unit Trust单一报价Choice Price单一股票期货Simple Stock Future当冲客Day Traders当地交货价Loco当期收益率Current Yield当期证券Current Issue当前票面利率Current Coupon当日交易者Day Traders当日之内Intraday当事人Principal倒挂的收益率曲线Inverted Yield Curve倒挂收益率曲线Inverse Yield Curve倒价Backwardation到岸价格CIF到期价值Maturity value到期前所剩时间Current Maturity到期日Expiry Date到期收益率YTM道德劝说Moral Suasion道琼斯工业指数DJIA道琼斯欧洲STOXX50 指数Euro STOXX道氏理论Dow Theory得尔塔套期保值Delta Hedging得尔塔值Delta德国DAX 30 种股价指数DAX 30德国Hermes 信用保险公司Hermes德国巴登符腾堡州银行Landesbank Baden-Wüttemberg (LBBW) 德国德意志联邦银行Bundesbank德国抵押债券Pfandbriefe德国长期公债Bunds德国证券集中保管银行Kassenverein德国政府债券Schatz德国中期公债Bundesobligationen (BOBL) 登记日Record Date等级Grades低价股票Penny Stocks低收费经纪商Discount Brokerage迪拜原油Dubai Crude敌意收购Hostile Bid抵押Hypothecation抵押贷款担保证券CMO抵押品Collateral递升卖出Scaleup第一通知日First Notice Day点Point点数图Point and Figure Chart点子Pip电子交易Screen Trading电子商务E-commerce电子通讯网络ECN店头市场OTC店头市场基金OTC Fund掉期Swap跌价抛售Selloff跌深反弹Dead Cat Bounce跌停板Limit Down蝶式买卖Butterfly Spread蝶状价差Butterfly Spread盯市Mark to Market订单积压Backlog定点期权Binary Option定量分析Quantitative Analysis定盘Fix定期存款Fixed-term Deposit定期存款单Term CD定期回购Term Repo定值过低Undervalued东京工业品交易所TOCOM东京国际金融期货交易所TIFFE东京证券交易所TSE东盟ASEAN东南亚国家联盟Association of South East Asian Nations 动产中介公司SIM动量指标Momentum Indicator动用贷款Drawdown动用资本Capital Employed毒丸行动Poison Pill独立发行的认股权证Naked Warrant短期的远期外汇或存款Short Dated Forwards短期借贷额度Swing Line短期借款Short-term Borrowing短期票据Short Bill对冲Hedging对冲或投机石油交易Paper Barrel对冲基金Hedge Fund对手风险Counterparty Risk对应账簿Matched Book兑现货Against Actuals多边投资担保机构MIGA多哈回合Doha Round多数法则Majority Rule多数股权Majority Interest多头Bull多头对冲Long Hedge多头市场Bull Market多元化投资Diversification多种选择融资安排MOFs俄罗斯国库券GKO额外的卖点Bells and Whistles恶性通货膨胀Hyperinflation二度衰退Double Dip二级金属Secondary Metals二级市场Secondary Market二级销售Secondary Offering二级资本Tier Two二十四国集团G24二项式期权定价模型Binomial Model二择一委托OCO发行股票筹资Equity Financing发行红股Free Issue发行红利股Bonus Issue发行价Issue Price发行前交易W/I发行前交易市场Grey Market (Gray Market)发行日Issue Date发行章程Prospectus发起人Sponsor法比荷交易所联盟Euronext法定贬值Devaluation法定存款准备金率Reserve Requirements法国CAC-40 股价指数CAC-40法国补偿动产行业公司SICOVAM法国财政部的可替代债券OAT法国国际期货及期权交易所MATIF法国国家统计暨经济研究所INSEE法国国库券BTF法国两或五年期公债BTAN法郎区Franc Zone反弹Rally反垄断法Anti-trust Laws反收购Greenmail反收购毒药Poison Pill反托拉斯法Anti-trust Laws反向操作投资人Contrarian反向股票分割Reverse Stock Split反向买现卖期交易Reverse Cash and Carry Trade 反向收购Reverse T akeover反转Reversal反转日Reversal Day泛美开发银行IADB泛欧交易所Euronext防火墙Chinese Wall防御性股票Defensive Stock房利美FNMA房屋抵押贷款协会Building Society非标准交易日期Broken Date非法交易链Daisy Chain非法经纪公司Bucket Shop非经常性项目Extraordinary Item非竞争投标拍卖Non-competitive Bid Auction 非上市股票Unlisted Stock非指标债券Off-the-Run Issue非中介化Disintermediation非洲发展新伙伴计划NEPAD非洲开发银行AFDB非注册股票Letter Stock非足额即撤销指令FOK非足额即撤销指令FOK费波纳奇数字序列Fibonacci Numbers费城证券交易所PHLX分拆Spin Off分割式资本投资信托公司Split Capital Investment分轨股票Tracking Share分离式认股权证Detachable Warrant分期偿还Amortization分期付款购买Hire Purchase分散风险Diversification分析人士Analyst分析师Analyst粉饰账目的日子Window Dressing Dates份额Tranche丰厚的离职金Golden Handshake丰厚的签约金Golden Hello风险Exposure风险承受程度Exposure风险逆转Risk Reversal风险溢价Risk Premium风险与收益的关系Risk-Return Relationship风险资本Venture Capital封闭式基金Closed-end Fund峰顶/高点Peaks浮动汇率制Floating Exchange Rates浮动利率票据FRN浮动利率债券Floating Rate Bond浮动利率债务Floating Debt浮息票据FRN付息日Pay Date负利差Negative Carry负商誉Negative Goodwill负债Liabilities负债权益比率Debt附带条件的托管Escrow附各项权利Cum All附认股权的债券Warrant Bonds附属保险公司Captive Insurance Company 附息Interest Bearing附有股息Cum Dividend复合期权Compound Option复利Compound Interest复利式年增长率CAGR复利增长Compounding富时100 指数FTSE 100富时Eurotop 300 股价指数FTSE Eurotop 300伽玛值Gamma概念性债券Notional Bonds甘恩Gann干预Intervention干预区间Intervention Band杠杆比率Gearing杠杆式收购LBO高点/峰顶Peaks高点低点开盘收盘四价格High Low Open Close (HLOC) 高点反转Top Reversal高科技股High Tech Stock高速缓冲存储器Cache高现金收益的产品或业务Cash Cow隔拆资金O/N Funds隔日交易Bed and Breakfast Deal隔夜O/N隔夜持仓额度O/N Limit隔夜钱O/N Funds工业生产Industrial Production公共部门净借款PSNB公积金Reserves公开发行价格POP公开发售Offer for Sale公开发售价POP公开喊价Open Outcry公开交易的基金Publicly Traded Fund公开配售Public Placement公开认购Offer for Subscription公开市场操作Open Market Operations公募Public Placement公认会计原则GAAP公司Cia公司财务Corporate Finance公司交易商Corporate Dealer公司结算方式Corporate Settlement公司融资Corporate Finance公司施放信号Signalling公用事业Utilities公债National Debt公众有限公司Plc共同行动Acting in Concert共同基金Mutual Fund共同农业政策CAP供给学派经济学Supply-side Economics供给与需求Supply/Demand购股勒索Greenmail购买基金Purchase Fund购买力平价PPP沽出备兑期权Covered Call Writing谷物Cereals股本Equity股本融资Equity Financing股本收益率Return on Equity股东Shareholder股东价值Shareholder value股东名册Share Register股东权益Shareholders’Equity股东权益收益率ROE股东特别大会EGM股东资金Shareholders’Funds股份公司AB股份公司或有限责任公司AS股份两合公司KGaA股份有限公司Kft股价的相对强弱Relative Strength股利Dividend股票Equity股票代号Ticker Symbol股票分割Stock Split股票风险溢价Equity Risk Premium股票股息Stock Dividend股票国际销售International Share Offering 股票合并Negative Stock Split股票红利Stock Dividend股票回购Share Repurchase股票价格平均数Stock Average股票交易显示带Ticker T ape股票借贷Stock Lending股票经纪人Stock Broker股票期权Equity Options股票认购权发行Rights Issue股票升水Share Premium股票贴水Share Discount股票邀标定价法Book Building股票指数Stock Index股票指数基金Stock Index Fund股票指数期货Stock Index Future股票指数期权Stock Index Option股票自由流通量Free Float股权Equity股权互换Equity Swap股权信托Voting Trust股息Dividend股息保障倍数Dividend Cover股息截止过户前买进、除息后卖出Dividend Stripping股息派发比率Payout Ratio股息收益率Dividend Yield股息贴现模型DDM股息宣布日Declaration Date股灾Crash固定/浮动利率混合型债券Fixed固定成本Fixed Costs固定汇率Peg固定汇率制Fixed Exchange Rate固定价格邀投Fixed Price Offer固定利率支付方Payer of Fixed固定收入债务工具Fixed Income固定资本Fixed Capital固定资产Fixed Assets寡头垄断Oligopoly挂钩汇率Peg挂牌Flotation关联公司Affiliate关贸总协定GATT关税与贸易总协定General Agreement on T ariffs and Trade 官方允许的汇率波动区间Trading Band管理层收购MBO广场协议Plaza Agreement广泛性风险Systemic Risk规格说明Specifications规模经济Economies of Scale规模效益Economies of Scale贵金属Precious Metals国际财团Consortium国际复兴开发银行IBRD国际互换和衍生产品协会ISDA国际会计准则理事会IASB国际货币基金组织IMF国际货币基金组织的贷款条件Conditionality国际货币市场IMM国际结算系统Clearstream国际金融公司IFC国际金融机构Supranational国际咖啡组织ICO国际开发协会IDA国际可可组织ICCO国际劳工组织ILO国际能源机构IEA国际清算银行BIS国际商会ICC国际商品协定Commodity Agreement国际石油交易所IPE国际收支Balance of Payments国际糖组织International Sugar Organization 国际投资争端解决中心ICSID国际外汇交易商协会ACI国际小麦理事会International Wheat Council国际证券市场协会ISMA国际证券委员会组织IOSCO国家风险Country Risk国家计划State Planning国库券Bill国民生产总值GNP国民账户National Accounts国内生产总值GDP国内生产总值价格平减指数GDP Deflator国内最终销售Domestic Final Sales国有化Nationalization国债National Debt过度频密的买卖Churning过渡性贷款Bridging含息Cum Dividend含息价Dirty Price韩国综合企业财团Chaebol行号代名Street Name行使价Strike Price行使价格Exercise Price行使价可重设的期权Moving Strike Option行使权利Exercise行业股指Sector Index行政总裁CEO合并Merger合并套利Merger Arbitrage合并资产负债表Consolidated Balance Sheet 合成金融工具Synthetic合格交割Good Delivery合格票据Eligible Bills合理价值Fair value合约等级Contract Grades合约月份Contract Month合作公司Ste Cve河底摸鱼Bottom Fishing荷兰式拍卖Dutch Auction核定资本Authorized Capital核心资本Core Capital褐皮书Beige Book黑市经济Black Market Economy恒生指数Hang Seng Index横向波动Flat红利Dividend红皮书Red Book宏观经济学Macro-economics哄抬股价的炒作行为Pump and Dump后进先出法LIFO后勤部门Back Office后台业务部Back Office互换Swap互换价差Swap Spread互换期权Swaption互联网服务供应商Internet Service Provider, ISP 互联网域名与网址管理机构ICANN华尔街Wall Street华尔街炼油商Wall Street Refiner华尔街石油交易商Wall Street Refiner坏账Bad Debt坏账准备Provision for Bad Debts环比年率Annualized Rate环球银行金融电信协会SWIFT环球银行金融电信协会电码SWIFT Codes缓冲库存Buffer Stock换取现货Against Actuals黄金降落伞Golden Parachute黄牛Scalpers黄色报价带Yellow Strip回本期Payback Period回购Buy Back回购利率Repo Rate回购市场Repo Market回购协议Repo回顾式期权Lookback Option汇率定盘Currency Fixings汇率风险Currency Risk汇票Bill of Exchange会计年度Financial Year会议委员会Conference Board混合经济Mixed Economy混合式期权Combined Option混合型互换Cocktail Swap活期存款Sight Money活期远汇Forward Option伙同方Concert Party或有负债Contingent Liability或有期权Contingent Option货币Money货币贬值Depreciation货币掉期Currency Swap货币供应量Money Supply货币互换Currency Swap货币回笼额Corto货币交易限额Currency Limit货币局制度Currency Board货币市场Money Market货币市场基础Money Market Basis货币学派Monetarism货币政策Monetary Policy货币政策委员会Monetary Policy Committee货币主义Monetarism获利回吐Profit-taking机构经纪Prime Broker机构投资者Institutional Investors机会成本Opportunity Cost鸡尾酒式互换Cocktail Swap积极型基金管理Active Fund Management 基本金属Base Metals基本面分析Fundamental Analysis基差Basis基差风险Basis Risk基差交易Basis Trading基点Basis Point基金Fund基金经理Fund Manager基金收费Load基年Base Year基准Benchmark基准货币Base Currency基准日Base Date级差Basis即期/次日S/N即期汇票Sight Draft集资Equity Financing集资章程Prospectus几何平均数Geometric average挤油交易Churning计划经济Planned Economy计量经济学Econometrics计算机病毒Virus计息Interest Bearing记录持有人Holder of Record记名证券Registered Form记账证券Book-entry securities技术分析Technical Analysis季节性调整Seasonal Adjustment绩优股Blue Chip Stock加按Equity Withdrawal加曼柯尔哈根模型Garman Kohlhagen Model 加密Encryption加权Weighting加权或不加权的指数Weighted加权平均票面利率Weighted Average Coupon 加权平均期限Weighted Average Maturity 加权平均资本成本WACC加权值Weighting夹层融资Mezzanine Finance价差Basis价差赌注Spread Betting价差交易Spread Trading价差巨大Wide Opening价格触发点In strike价格高低分析Rich Cheap Analysis价格过高Overvalued价格偏低Undervalued价格趋势分离Broadening价格通道Price Channel价格折返率Retracement价格指标Price Indicators价量指数PVI价值被低估Undervalued减记Write Down减少投资Disinvestment减少资本支出Disinvestment减值Write Down简单移动平均数Simple Moving Average简明扼要的商务方案Elevator Pitch建立头寸T aking a Position建设—经营—移交方式(BOT 方式) BOT将公司资产拆卖Asset Stripping将军债券Shogun Bond降低信用评级Downgrade降价Markdown交叉汇率Cross Rate交叉盘交易Cross交割价格Delivery Price交割日Prompt Date交换现货Exchange for Cash交货价Delivery Price交投清淡Thin Market交易部门Front Office交易成本Transaction Costs交易大厅Floor交易费用Transaction Fees交易岗Trading Post交易回合Round Turn交易结算室Back Office交易量Trading Volume交易区间Trading Range交易圈Pit交易日后一天结算T+1交易商Dealer交易商持仓报告Commitments of Traders 交易商之间的经纪人IDB交易实物Exchange for Physical交易所交割结算价EDSP交易所交易基金ETF交易头寸限额Position Limit交易席位Seat交易限额Deal Limit较现货价贴水Around Par接管人Receiver接受获分配的证券T akedown接受收购要约Tender结构性赤字Structural Deficit结构性调整Structural Adjustment结清头寸Closing a Position结算Settlement结算风险Settlement Risk结算价格Settlement Price结算日Settlement Date结算所Clearing House结算系统Clearing System结算银行Clearing Bank介绍上市Introduction界限期权Barrier Option借记卡Debit Card借款新安排NAB借款需要额Borrowing Requirement 借款总安排GAB借款总协定GAB金本位制Gold Standard金边证券Gilt-edged金股Golden Share金融市场协会FMA金融稳定论坛FSF金融衍生产品Derivatives金融衍生工具Derivatives金融中介化Financial Intermediation金融中介活动Financial Intermediation金融中心Financial Centre金手铐Golden Handcuffs金银条Bullion金字塔骗局Pyramid Scheme紧缩银根Squeeze尽职调查Due Diligence Process禁运Embargo经常项目Current Account经常性获利Current Earnings经常账户Current Account经合组织OECD经纪公司Brokerage经纪行Trading House经纪人Broker经纪人佣金Brokerage经纪商Broker经济ECONOMY经济合作暨发展组织Organization for Economic Co-operation andDevelopment经济衰退Recession经济增加值EVA经济指标Economic Indicators经济周期Business Cycle经济周期活动指标Activity Indicators经济作物Cash Crop经团联Keidanren经营风险Business Risk经营现金流Operating Cash Flow精算师Actuary景气判断指数IFO景气循环Business Cycle景气循环股Cyclical Stocks净额Net净额法Netting净交易Net Transaction净利Bottom Line净利润Net Profit净头寸Net Position净现金流量Net Cash Flow净现值NPV净资产Net Assets净资产收益率RONA竞价投标Book Building竞争性标售Competitive Bid Auction就业人口Payrolls菊花链交易Daisy Chain矩形价格形态Rectangle巨无霸汉堡包指数Big Mac Index决定不派股息Pass a Dividend卡特尔Cartel开放式基金Open-end Fund凯恩斯经济学Keynesian Economics凯利指标Kairi看跌Bearish看多Bullish看空Bearish看涨Bullish看涨期权Call可变成本Variable Costs可变动资本额股份有限公司SA de CV可变利率Variable Rate可变资本投资公司SICAV可分配的利润Attributable Profit可互换的Fungible可交割等级Tenderable Grades可交换的债券Exchangeable Bonds可卖回的Puttable可商议的Negotiable可提前赎回的Callable可替代的Fungible可展期的债券Extendible Bond可转换优先股Convertible Preference Share 可转换债券Convertible Bond可转换债券套利Convertible Arbitrage可转让的Negotiable可转让证券集合投资事业UCITS空壳公司Shell Company空头Bear空头回补Short covering空头卖出Short-selling空头平仓Short covering空头市场Bear Market空头套期保值Short Hedge空头头寸Short Position空头陷阱Bear Trap控股公司Holding Company扣押权Lien库存Inventory跨国公司Multinational跨国货币结算风险Cross Currency Settlement Risk 跨国石油公司Majors跨境Cross Border跨期买卖Horizontal Spread跨市场上市Cross Listing跨式期权组合Straddle快取记忆体Cache宽限期Grace Period款货分付Free Delivery扩大贷款额度Enlarged Access垃圾债券Junk Bonds拉弗曲线Laffer Curve拉高出货Pump and Dump蓝筹股Blue Chip Stock蓝天法Blue Sky Laws劳埃德Lloyd's劳动股份有限公司SAL劳动力市场Labour Market劳合社Lloyd's勒式组合Strangle类股Market Sector类股指数Sector Index累积投票法Cumulative Method累积优先股Cumulative Preferred Stock累计投标Book Building离岸基金Offshore Fund离岸价格FOB黎明突袭Dawn Raid历史波动性Historical Volatility历史成本Historical Cost利差Cost of Carry利克斯银行Riksbank利率Interest Rate利率风险Interest Rate Risk利率互换Interest Rate Swap利率上下限期权Collar利率上限期权Cap利率下限期权Floor利率项圈期权Collar利润Profit利润率Profit Margin利润再投资Ploughed Back利息偿付倍数Interest Cover利息再投资债券Multiplier Bond例行结算Regular Way Settlement连带违约条款Cross Default Clauses联邦银行Buba联贷Syndicated Loan联合国开发计划署UNDP联合国拉丁美洲及加勒比海经济委员会ECLAC联合国粮农组织FAO联合国粮食和农业组织Food and Agriculture Organization联合国贸易和发展会议United Nations Conference on Trade andDevelopment联合国欧洲经济委员会UNECE联合融资Co-financing联系汇率Peg联营公司Associated Company廉价股Penny Stocks廉价债券Distressed Debt两合公司KG裂解价差Crack Spread零成本期权策略Zero Cost Option零售价格指数Retail Price Index零碎交易Odd Lot Trade零息利率互换Zero Coupon Swap零息债券Zero Coupon Bond零息债券收益率曲线Zero Coupon Yield Curve领头羊Bellwether领先指标Leading Indicators另类投资市场AIM留存收益Retained Earnings留置权Lien流动比率CURRENT RATIO流动负债Current Liabilities流动性Liquidity流动性风险Liquidity Risk流动性余裕Liquidity Margin流动资产Current Assets流动资金Liquidity流量Throughput龙头Bellwether龙债券Dragon Bonds垄断Monopoly伦敦城City伦敦国际金融期货期权交易所LIFFE伦敦结算所London Clearing House 伦敦金融区City伦敦金属交易所LME伦敦金银市场协会LBMA伦敦俱乐部London Club伦敦银行同业拆借利率Libor伦敦银行同业借入利率Libid伦敦银行同业中间利率Limean伦敦证券交易所LSE伦敦证券交易所电子交易系统SETS伦敦证券与衍生工具交易所OMLX罗素3000 指数Russell 3000裸头寸Naked Position履约Exercise履约价Strike Price履约价格Exercise Price绿地投资Greenfield Investment 绿函Greenmail绿色汇率Green Rates绿靴条款Greenshoe Option马城条约Maastricht Treaty马城条约标准Maastricht Criteria马来西亚国家银行Bank Negara Malaysia 马斯特里赫特条约Maastricht Treaty买断Outright Purchases买方出价Bid买方过剩市场Bid Market买方有权不接受延后还本的债券Exit bond买卖方报价Bid-Ask Quote买卖权平价Put-Call Parity买入对冲Long Hedge买现卖期交易Cash and Carry Trade麦考利存续期Macauley duration卖出持有标的看涨期权Covered Call Writing卖方Sell-side卖方报价Ask卖方过剩市场Offer Market卖空Short-selling卖空者Bear卖权Put毛利Gross Profit贸易壁垒Trade Barrier贸易差额Balance of Trade贸易收支差额Balance of Trade贸易数据Trade Figures每股盈余Earnings Per Share每股账面净值BVPS每日价格涨跌限幅Daily Price Limit每日桶数Barrels per Day每日限价Daily Price Limit每一用户平均收入ARPU每张认股权证可认购股票数的比率Shares Per Warrant Ratio美国财务会计准则委员会FASB美国参议院财政委员会Senate Finance Committee美国存管信托公司Depository Trust Corporation美国供应管理协会ISM美国国库券US Treasury Bill美国国库券与欧洲美元期货之价差TED Spread美国国税局IRS美国经济咨商会Conference Board美国联邦储备体系Federal Reserve System美国联邦储备委员会Federal Reserve Board美国联邦存款保险公司FDIC美国联邦公开市场委员会FOMC美国联邦国民抵押贷款协会FNMA美国联邦能源监管委员会FERC美国联邦住房抵押贷款公司Federal Home Loan Mortgage Corporation美国农产品出口补贴方案Export Enhancement Programme美国农业部USDA美国全国采购管理协会NAPM美国全国证券交易商协会NASD美国全国证券交易商协会自动报价系统National Association of Securities Dealers'Automated Quotations美国商品期货交易委员会Commodities Futures Trading Commission 美国商品期货交易委员会(CFTC) CFTC美国审计局General Accounting Office美国石油学会API美国石油学会重力指标API Gravity美国通膨保值公债TIPS美国预托证券ADR美国债市的标准计息方法US Street Method美国证交会SEC美国证券集中保管结算公司DTCC美国证券交易委员会SEC美国政府国民抵押贷款协会Ginnie Mae美国政府长期债券US Treasury Bond美国政府中期债券US Treasury Note美联储Fed美式期权American Option美元化Dollarization猛犬债券Bulldog Bond猛涨Run Up免费发行Free Issue免费认股权Nil Paid Rights免税红利Franked dividends免佣金No-load面值Face value民营化/私有化Privatization民营化/私有化Privatization名义本金Notional Principal名义利率Nominal Interest Rates名义上的Nominal名义性债券Notional Bonds明日T/N摩擦性失业Frictional Unemployment摩根士丹利资本国际指数MSCI Indices末行数字Bottom Line母公司Holding Company穆迪信贷评级Moody's纳斯达克NASDAQ纳斯达克综合股价指数NASDAQ Composite南方共同市场MERCOSUR内部回报率Internal Rate of Return内插法Interpolation内幕交易Insider Dealing内推法Interpolation内在价值Intrinsic value能量分析On Balance Volume逆回购协议Reverse Repurchase Agreement逆经济周期而动的股票Counter-cyclical Stock逆时针价量图Counter Clockwise年报Annual Report年度报告Annual Report年度股东大会AGM年金Annuity年率Annual Rate年增长率Annualized Rate年终股息Final Dividend牛市Bull Market牛市的Bullish纽约咖啡、糖及可可交易所Coffee, Sugar and Cocoa Exchange 纽约期货交易所NYBOT纽约商品交易所COMEX纽约商业期货交易所New York Mercantile Exchange纽约证交所Big Board纽约证券交易所NYSE挪威合伙公司的简称ANS挪威上市公司的简称ASA欧盟EU欧盟经济财政部长会议ECOFIN欧盟统计局Eurostat欧米加Omega欧佩克OPEC欧式期权European Option欧央行ECB欧元区Euroland欧元银行同业拆息Euribor欧元银行同业隔夜拆息Eonia欧洲存款Eurodeposits欧洲贷款Eurocredits欧洲复兴开发银行EBRD欧洲汇率机制ERM欧洲货币Eurocurrency欧洲货币机构EMI欧洲货币体系EMS欧洲结算系统Euroclear欧洲经济货币联盟EMU欧洲美元Eurodollar欧洲期货期权交易所EUREX欧洲市场Euromarkets欧洲投资银行EIB欧洲信贷Eurocredits欧洲债券Eurobond欧洲中期债券EMTN欧洲自由贸易联盟EFTA爬行钉住汇率制Crawling Peg拍卖Auction派发指标Accumulation派息率Payout Ratio盘购Acquisition盘后交易After-hours Dealing 盘前交易Pre-market Trading 盘整Backing and Filling 盘整期Consolidation Phase 庞氏骗局Ponzi Scheme泡沫Bubble配售Placing批发Wholesale票据Bill票据承兑商行Acceptance House 票据发行便利NIF票面利率Coupon撇账Write Off平仓Closing a Position平仓成本Cost to Close平等待遇Pari Passu平行贷款Parallel Loans平衡预算Balanced Budget平滑异同移动平均线MACD平价At Par平价债券Par Bond平均价格期权Average Price平均值Mean屏幕交易Screen Trading破产Bankruptcy破产保护Chapter 11破产保护企业融资DIP Financing蒲式耳Bushel普氏Platts普通股Common Stock普通股本Ordinary Share Capital 普通合股公司SC普通合伙公司SNC普通提款权ODR七国集团G7七十七国集团G77期货的最近月合约Nearbys期货合约Futures期货交易所公开喊价区Futures Pit期货经纪商Commission Merchant 期货升水Contango期货转换现货交易Exchange for Physical 期末股息Final Dividend期末价值Terminal value期末整还式贷款Balloon Loan期票Promissory Note期权Option期权策略Option Strategies期权持有者Option Holder期权费Option Premium期权价内(实值)状态In the Money期权价外状态Out of the Money期权价值随时间过去而下跌Time Decay期权卖方Option Writer期权平值状态At the Money期权系列Option Series期权组合Combined Option旗形态/三角旗形态Flags企业对企业电子商务B2B企业分拆Demerger企业分割Demerger企业集团Conglomerate企业价值EV企业区Enterprise Zone企业融资Corporate Finance启用贷款Drawdown起息日Dated Date契约Covenant牵头经理费Praecipuum前台业务部Front Office前线部门Front Office前置定价法Backpricing欠发达国家LDC抢帽子式交易商Scalpers抢先交易Front Running清算所Clearing House清算系统Clearing System清算银行Clearing Bank趋势反转Trend Reversal趋势轨道Channel Lines趋势连续性Continuation趋势线Trendline趋同Convergence曲线Curve圈售Circling权利股发行Scrip Issue权利金Option Premium权重Weighting全价Dirty Price全面摊薄每股盈余Fully Diluted EPS全球预托凭证GDR全权管理账户Discretionary Account 全数包销Bought Deal全数完成或作废单FOK劝导Moral Suasion券款对付DVP缺乏流动性Illiquid缺口Gap缺口操作Gapping确定的委托Firm Order燃料油Fuel Oil让产易股Spin Off热门股票Hot Stock人均国内生产总值GDP per Head认购不足Undersubscribed认购期权Call认股权发行Rights Issue认股权证Warrant日/桶Barrels per Day日本大阪证券交易所OSE日本国际合作银行JBIC日本进出口银行EX-IM Bank of Japan 日本经济团体联合会Keidanren日本央行短观调查报告T ankan日本邮政省简易保险局Kampo日本债券回购市场Gensaki Market日本政府公债JGB日本综合商社Sogo Shosha日交易限制Intraday Limit日经225 指数Nikkei 225日历价差Calendar Spread日历套利Calendar Spread融券Stock Lending融券保证金账户Short Margin Account 软贷款Soft Loan软性商品Softs瑞士期权和金融期货交易所SOFFEX瑞士市场指数SMI萨尔巴尼斯—奥斯利法Sarbanes-Oxley Act 三格转向Three Box Reversal 三国集团G3三角旗形态Pennants三角形Triangles三十国国际财经事务顾问团G30三巫日Triple Witching三巫同时显灵(日) Triple Witching三约同时到期(日) Triple Witching三重顶/三重底Triple Top/Bottom散布图Scatter Chart散点图Scatter Chart丧失转换价值的可转换证券Busted Convertible商人银行Merchant Bank商业汇票Trade Bill商业票据CP商业银行Commercial Banks商誉Goodwill上升趋势/下跌趋势Uptrend/Downtrend 上市Flotation上市公告Listing Particulars上市公司OYJ上市股票Listed Stock上市交易基金ETF上市前推介Pre-marketing上市要求Listing Requirements 上游产业Upstream上涨生效期权Up and In上涨失效期权Up and Out烧钱Burn烧钱率Cash Burn少数股东权益Minority Interest申报交易商Reporting Dealer申请了破产保护的公司DIP审计Audit审计师Auditors审计员Auditors升级Upgrade升水Around Par升值Revaluation生产者物价指数PPI,Producer Price Index 失败的振荡Failure Swing失业Unemployment十国集团G10十亿Yard石油下游产业Downstream时间价值Time value时间序列Time Series实际的Real实际汇率Effective Exchange Rate实际控制Working Control实际利率Real Interest Rates实际收益率Real Yield实缴股本Paid-up Capital实时数据Real-time Data实收资本Paid-up Capital实物交割之通知Tender实物商品市场Terminal Market实物石油Wet Barrels实质利率Real Interest Rates实质收益率Real Yield世界贸易组织WTO世界银行World Bank市场板块Market Sector市场风险Market Risk市场风险Market Risk市场经济Market Economy市场平均预估Consensus Estimates市场趋势Market Trend市场正常交易规模Normal Market Size市价单Market Order市价指令Market Order市盈率P/E Ratio市盈增长比率Price Earnings Growth Ratio 市盈增长比率(PEG 值) PEG Ratio市帐率Price To Book Ratio市政债券Municipal Bond市值Capitalization市值加权指数Capitalization-weighted Index 市值帐面值比率Price To Book Ratio收购Acquisition收购出价T akeover Bid收购要约Tender Offer收集Accumulation收入Income收入政策Incomes Policy收益股Income Stock收益率Rate of Return收益率差额Yield Gap收益率曲线Yield Curve收益率缺口Yield Gap首次付息First Coupon首次公开招股IPO首期短期息票Short First Coupon首席财务官CFO首席执行官CEO受托人Depository授权Mandate授权买卖账户Discretionary Account授权书Proxy赎回Redemption赎回认股权证Redemption Warrant赎回收益率Redemption Yield赎回值可变动的债券Variable Redemption Bond数量招标Fixed Price Offer双底衰退Double Dip双价制Dual Pricing双巫日Double Witching双巫同时显灵(日) Double Witching双向市场Two-way Market双约同时到期(日) Double Witching。

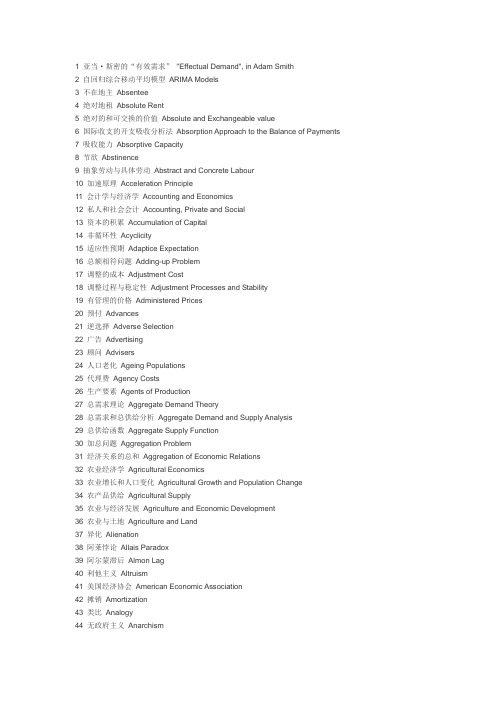

新帕尔格雷夫经济学大辞典 中英对照

1 亚当·斯密的“有效需求”"Effectual Demand", in Adam Smith2 自回归综合移动平均模型ARIMA Models3 不在地主Absentee4 绝对地租Absolute Rent5 绝对的和可交换的价值Absolute and Exchangeable value6 国际收支的开支吸收分析法Absorption Approach to the Balance of Payments7 吸收能力Absorptive Capacity8 节欲Abstinence9 抽象劳动与具体劳动Abstract and Concrete Labour10 加速原理Acceleration Principle11 会计学与经济学Accounting and Economics12 私人和社会会计Accounting, Private and Social13 资本的积累Accumulation of Capital14 非循环性Acyclicity15 适应性预期Adaptice Expectation16 总额相符问题Adding-up Problem17 调整的成本Adjustment Cost18 调整过程与稳定性Adjustment Processes and Stability19 有管理的价格Administered Prices20 预付Advances21 逆选择Adverse Selection22 广告Advertising23 顾问Advisers24 人口老化Ageing Populations25 代理费Agency Costs26 生产要素Agents of Production27 总需求理论Aggregate Demand Theory28 总需求和总供给分析Aggregate Demand and Supply Analysis29 总供给函数Aggregate Supply Function30 加总问题Aggregation Problem31 经济关系的总和Aggregation of Economic Relations32 农业经济学Agricultural Economics33 农业增长和人口变化Agricultural Growth and Population Change34 农产品供给Agricultural Supply35 农业与经济发展Agriculture and Economic Development36 农业与土地Agriculture and Land37 异化Alienation38 阿莱悖论Allais Paradox39 阿尔蒙滞后Almon Lag40 利他主义Altruism41 美国经济协会American Economic Association42 摊销Amortization43 类比Analogy44 无政府主义Anarchism45 反托拉斯政策Antitrust Policy46 适用技术Appropriate Technology47 套利Arbitrage48 套利定价理论Arbitrage Pricing Theory49 仲裁Arbitration50 军备竞赛Arms Races51 阿罗定理Arrow''s Theorem52 阿罗-德布勒一般均衡模型Arrow-Debren Model of General Equilibrium53 资产定价Asset Pricing54 资产与负债Assets and Liabilities55 指派问题Assignment Problems56 非对称信息Asymmetric Information57 原子状竞争Atomistic Competition58 拍卖者Auctioneer59 拍卖Auctions60 奥地利经济学派Austrian School of Economics61 自给自足Autarky62 自发支出Autonomous Expenditures63 自回归和移动平均时间序列过程Autoregressive and Moving-average Time-series Processes64 平均成本定价Average Cost Pricing65 阿弗奇一约翰逊效应Averch-Johnson effect66 公理化理论Axiomatic Theories67 交割延期费Backwardation68 落后性Backwardness69 贸易差额理论史Balance of Trade, History of The Theory70 平衡预算乘数Balanced Budget Maltiptier71 平衡增长Balanced Growth72 中央银行利率Bank Rate73 银行学派,通货学派,自由银行学派Banking School, Currency School, Free Banking School74 讨价还价(议价) Bargaining75 物物交换Barter76 物物交换和交易Barter and Exchange77 基本品和非基本品Basics and Non-Basics78 基点计价制Basing Point System79 杂牌凯恩斯主义Bastard Keynesianism80 贝叶斯推断Bayesian Inference81 以邻为整Beggar-the-neighbor82 行为经济学Behavioral Economics83 有偏和无偏的技术进步Biased and Unbiased technological Change84 出价Bidding85 双边垄断Bilateral Monopoly86 复本位制Bimetallism87 生物经济学Bioeconomics88 经济学在生物学中的应用Biological Applications of Economics89 伯明翰学派Birmingham School90 生死过程Birth-and-death Processes91 债券Bonds92 有限理性论Bounded Rationality93 资产阶级Bourgeoisie94 贿赂Bribery95 泡沫状态Bubbles96 预算政策Budgetary Policy97 缓冲存货Buffer Stocks98 内在稳定器Built-in Stabilizers99 金银本位主义的争论Bullionist Controversy100 束状图Bunch Maps101 公债负担Burden of The Debt102 官僚制度Bureaucracy103 经济周期Business Cycles104 不变替代弹性生产函数CES Production Function105 变分法Calculus of Variations106 官房经济学派Cameralism107 资本资产定价模型Capital Asset Pricing Model108 资本预算的编制Capital Budgeting109 资本外逃Capital Flight110 资本的收益与损失Capital Gains and Losses111 资本品Capital Goods112 资本的反常现象Capital Perversity113 资本理论Capital Theory114 资本的理论:争论Capital Theory: Debates115 资本理论:悖论Capital Theory: Paradoxes116 固定资本利用程度Capital Utilization117 作为一种生产要素的资本Capital as A Factor of Production118 作为一种社会关系的资本Capital as a Social Relation119 资本、信贷和货币市场Capital, Credit and Money Markets120 资本主义Capitalism121 资本主义的与非资本主义的生产Capitalistic and Acapitalistic Production 122 卡特尔Cartel123 交易学Catallactics124 突变论Catastrophe Theory125 赶超Catching-up126 因果推理Causal Inference127 经济模型中的因果关系Causality in Economic Models128 删截数据模型Censored Data Models129 中央银行业务Central Banking130 中心地区理论Central Place Theory131 中央计划Central Planning132 波动重心Centre of Gravitation133 确定性等价Certainty Equivalent134 如果其他条件不变Ceteris Paribus135 偏好的改变Changes in Tastes136 宪章运动:宪章的条款Chantism: the point of the Charter 137 物品特性Characteristics138 宪章运动Chartism139 低息借款Cheap Money140 芝加哥学派Chicago School141 技术选择与利润率Choice of Technique and the Rate of Profit 142 牟利学(理财) Chrematistics143 基督教社会主义Christian Socialism144 循环流动Circular Flow145 流通资本Circulating Capital146 阶级Class147 古典经济学Classical Economics148 古典增长模型Classical Growth Models149 古典货币理论Classical Theory of Money150 历史计量学Cliometrics151 社团Clubs152 合作社Co-operatives153 科斯定理Coase Theorem154 柯布-道格拉斯函数Cobb-Douglas Function155 蛛网定理Cobweb Theorem156 共同决定和利润分享Codetermination and Profit-sharing157 同族学科Cognate Displines158 柯尔培尔主义Colbertism159 集体行动Collective Action160 集体农业Collective Agriculture161 劳资集体谈判Collective bargaining162 合谋Collusion163 殖民主义Colonialism164 殖民地Colonies165 联合Combination166 组合论Combinatorics167 命令经济Command Economy168 商品拜物教Commodity Fetishism169 商品货币Commodity Money170 商品储备货币Commodity Reserve Currency171 公共土地Common Land172 习惯法Common Law173 公共财产权Common Property Rights174 通讯Communications175 共产主义Communism176 社会(公共)无差异曲线Community Indifference Curves177 比较利益Comparative Advantage178 比较静态学Comparative Statics179 补偿需求Compensated Demand180 补偿Compensation181 补偿原理Compensation Principle182 竞争Competition183 竞争政策Competition Policy184 竞争与效率Competition and Efficiency185 竞争与选择Competition and Selection186 国际贸易竞争Competition in International Trade187 奥地利学派的竞争理论Competition: Austrian Conceptions188 古典竞争理论Competition: Classical Conceptions189 马克思学派的竞争理论Competition: Marxian Conceptions190 竞争性市场过程Competitive Market Processes191 一般均衡的计算Computation of General Equlibria192 集中比率Concentration Ratios193 冲突与解决Conflict and Settlement194 冲突与战争Conflict and War195 拥挤Congestion196 综合性大企业Conglomerates197 推测均衡Conjectural Equilibria198 炫耀性消费Conspicuous Consumption199 不变资本和可变资本Constant and Variable Capital200 制度经济学Constitutional Economics201 耐用消费品Consumer Durables202 消费者剩余Consumer Surplus203 消费者支出Consumers, Expenditure204 消费函数Consumption Function205 消费集Consumption Sets206 消费税Consumption Taxation207 消费与生产Consumption and Production208 可竞争市场Contestable Markets209 或有商品Contingent Commodities210 经济历史的连续性Continuity in Economic History211 连续和离散时间模型Continuous and Discrete Time Models212 连续-时间随机模型Continuous-time Stochastic Model213 连续时间随机过程Continuous-time Stochastic Processes214 矛盾Contradiction215 资本主义的矛盾Contradictions of Capitalism216 经济活动的控制与协调Control and Coordination of Economic Activity 217 趋向性假说Convergence Hypothesis218 凸规划Convex Programming219 凸性Convexity220 合作均衡Cooperative Equilibrium221 合作对策Cooperative Games222 核心Cores223 谷物法Corn Laws224 谷物模型Corn Model225 公司经济Corporate Economy226 公司Corporations227 社团主义Corporatism228 对应原理Correspondence Principle229 对应Correspondences230 成本函数Cost Functions231 成本最小化和效用最大化Cost Minimization and Utility Maximization 232 成本和供给曲线Cost and Supply Curves233 生产成本Cost of Production234 成本-效益分析Cost-benefit Analysis235 成本推动型通货膨胀Cost-push Inflation236 反向贸易Counter Trade237 反设事实Counterfactuals238 抗衡力量Countervailing Power239 蠕动钉住汇率Crawling Peg240 创造性破坏Creative Destruction241 信贷Credit242 信贷周期Credit Cycle243 信贷配给Credit Rationing244 犯罪与处罚Crime and Punishment245 危机Crises246 关键路径分析Critical Path Analysis247 挤出效应Crowding Out248 累积的因果关系Cumulative Causation249 累积过程Cumulative Processes250 通货Currencies251 通货委员会Currency Boards252 关税同盟Customs Unions253 周期Cycles254 社会主义经济的周期Cycles in Socialist Economies255 技能退化De-skilling256 高息借款Dear Money257 销路理论Debouches, Theorie des258 分权Decentralization259 决策理论Decision Theory260 衰落产业Declining Industries261 人口下降Declining Population262 国防经济学Defence Economics263 赤字财政Deficit Financing264 赤字支出Deficit Spending265 垄断程度Degree of Monopoly266 效用程度Degree of utility267 需求管理Demand Management268 需求价格Demand Price269 需求理论Demand Theory270 货币需求:经验研究Demand for Money: Empirical Studies271 货币需求:理论研究Demand for Money: Theoretical Studies272 需求拉动型通货膨胀Demand-pull Inflation273 人口转变Demographic Transition274 人口统计学Demography275 依附Dependency276 折耗Depletion277 折旧Depreciation278 萧条Depressions279 派生需求Derived Demand280 决定论Determinism281 发展Development282 发展经济学Development Economics283 发展计划Development Planning284 辩证唯物主义Dialectical Materialism285 辩证推理Dialectical Reasoning286 微分对策Differential Games287 获得的困难Difficulty of Attainment288 生产的难易程度Difficulty or Facility of Production289 技术扩散Diffusion of Technology290 经济量的维数Dimension of Economic Quantities291 直接税Direct Taxes292 直接非生产性寻利活动Directly Unproductive Profit-seeking (DUP) Activities 293 离散的选择模型Discrete Choice Models294 歧视性垄断Discriminating Monopoly295 歧视Discrimination296 非均衡分析Disequilibrium Analysis297 隐蔽性失业Disguised Unemployment298 反中介行动Disintermediation299 扭曲Distortions300 分配Distribution301 占典分配理论Distribution Theories: Classical302 凯恩斯主义的分配理论Distribution Theories: Keynesian303 马克思主义的分配理论Distribution Theories: Marxian304 新古典分配理论Distribution Theories: Neoclassical305 分配伦理Distribution, Ethics of306 分配规律Distribution, Law of307 分配公平Distributive Justice308 多样化经营Diversification of activities309 分段的总体和随机模型Divided Populations and Stochastic Models310 股息政策Dividend Policy311 迪维西亚指数Divisia Index312 劳动分工Division of Labour313 经济学说Doctrines314 土地调查清册Domesday Book315 家务劳动Domestic Labour316 复式簿记Double-entry Bookkeeping317 二元经济Dual Economies318 二元性Duality319 虚拟变量Dummy Variables320 倾销Dumping321 双头垄断Duopoly322 动态规划和马尔可夫决策过程Dynamic Programming and Markov Decision Process 323 经济增长和发展的动力学Dynamics, Growth and Development324 东西方经济关系East-west Economic Relations325 伊斯特林假说Easterlin Hypothesis326 经济计量学Econometrics327 经济人类学Economic Anthropology328 社会主义经济的经济计算Economic Calculation in Socialist Economies329 经济自由Economic Freedom330 经济增长Economic Growth331 经济和谐Economic Harmony332 经济史Economic History333 经济一体化Economic Integration334 历史的经济学解释Economic Interpretation of History335 经济法则Economic Laws336 经济人Economic Man337 经济组织Economic Organization338 经济组织与交易成本Economic Organization and Transaction Costs339 经济科学与经济学Economic Science and Economics340 经济剩余与等边际原理Economic Surplus and the Equimarginal Principle341 经济理论与理性假说Economic Theory and The Hypothesis of Rationality342 国家的经济理论Economic Theory of the State343 经济战Economic War344 经济和社会人类学Economic and Social Anthropology345 经济和社会史Economic and Social History346 经济学图书馆与文献的使用Economics Libraries and Documentation347 规模经济与规模不经济Economies and Diseconomies ofScale348 经济计量学Economitrics349 有效需求Effective Demand350 实际保护Effective Protection351 有效配置Efficient Allocation352 有效率市场假说Efficient Market Hypothesis353 国际收支的弹性分析方法Elasticities Approach to the Balance of Payments354 弹性Elasticity355 替代弹性Elasticity of Substitution356 就业理论Employment, Theories of357 空匣Empty Boxes358 内生性与外生性Endogencity and Exoyeneity359 内生货币与外生货币Endogenous and Exogenous Money360 能源经济学Energy Economics361 强制执行Enforcement362 恩格尔曲线Engel Curve363 恩格尔定律Engel''s Law364 英国历史学派English Historical School365 权利Entitlements366 企业家Entrepreneur367 熵Entropy368 进入与市场结构Entry and Market structure369 包络定理Envelope Theorem370 环境经济学Environmental Economics371 妒忌Envy372 国民历代大事记或民族精神编年史Ephemerides du Citoyen ou Chronique de I''esprit National 373 经济学中的认识论问题Epistemological Issues in Economics374 均等利润率Equal Rates of Profit375 平等Equality376 交易方程Equation of Exchange377 均衡:概念的发展Equilibrium: Development of The Concept378 均衡:一个预期性的概念Equilibrium: an Expectational Concept379 公平Equity380 遍历理论Ergodic Theory381 变量误差Errors in Variables382 估计Estimation383 欧拉定理Euler''s Theorem384 欧洲美元市场Eurodollar Market385 事前与事后Ex Ante and Ex Post386 过度需求与供给Excess Demand and Supply387 交换Exchange388 外汇管制Exchange Control389 汇率Exchange Rate390 可能竭资源Exhaustible Resources391 一般均衡的存在性Existence of General Equilibrium392 退出和进言Exit and Voice393 预期Expectations394 预期效用假说Expected Utility Hypothesis395 预期效用及数学期望Expected Utility and Methematical Expectation396 消费支出税Expenditure Tax397 经济学中的实验方法(i) Experimental Methods in Economics(i)398 经济学中的实验方法(ii) Experimental Methods in Economics(ii)399 剥削Exploitation400 展延家庭Extended Family401 扩展型对策Extensive Form Games402 粗放与集约地租Extensive and Intensive Rent403 外债External Debt404 外在经济External Economies405 外在性Externalities406 费边经济学Fabian Economics407 因子分析Factor Analysis408 要素价格边界Factor Price Frontier409 公平分配Fair Division410 公平性Fairness411 下降的利润率Falling Rate of Profit412 家庭Family413 计划生育Family Planning414 饥荒Famine415 法西斯主义Fascism416 生育力Fecundity417 人口出生率Fertibity418 封建主义Feudalism419 法定不兑现纸币Fiat Money420 虚拟资本Fictitious Capital421 信用发行Fiduciary Issue422 最终效用程度Final Degree of Utility423 最终效用Final Utility424 金融Finance425 金融资本Finance Capital426 融资和储蓄Finance and Saving427 金融危机Financial Crisis428 金融中介Financial Intermediaries429 金融新闻业Financial Journalism430 金融市场Financial Markets431 微调Fine Tuning432 厂商理论Firm, Theory of The433 财政联邦主义Fiscal Federalism434 财政态势Fiscal Stance435 发展中国家的财政和货币政策Fiscal and Monetary Policies in Developing Countries 436 渔业Fisheries437 固定资本Fixed Capital438 固定汇率Fixed Exchange Rates439 不变生产要素Fixed Factors440 不动点定理Fixed Point Theorems441 固定价格模型Fixprice Models442 浮动汇率Flexible Exchange Rates443 强制储蓄Forced Saving444 预测Forecasting445 对外援助Foreign Aid446 国外投资Foreign Investment447 对外贸易Foreign Trade448 对外贸易乘数Foreign Trade Multiplier449 森林经济Forests450 欺骗Fraud451 自由银行制度Free Banking452 自由处置Free Disposal453 免费物品Free Goods454 免费午餐Free Lunch455 自由贸易和保护主义Free Trade and Protection456 充分就业Full Employment457 充分就业预算盈余Full Employment Budget Surplus458 完全及有限信息方法Full and Limited Information Methods459 泛函分析Functional Analysis460 功能财政Functional Finance461 根本性失衡Fundamental Disequilibrium462 可替代性Fungibility463 期贷市场、套头交易与投机Futures Markets, Hedging and Speculation 464 期货交易Futures Trading465 模糊集合Fuzzy Sets466 贸易收益Gains from Trade467 对策论(博奕论) Game Theory468 不完全信息对策Games With Incomplete Information469 赌博合同Gaming Contracts470 度规函数Gauge Functions471 资本搭配Gearing472 性别Gender473 一般均衡General Equilibrium474 一般系统理论General System Theory475 德国历史学派German Historical School476 吉布拉定律Gibrat''s Law477 吉芬悖论Giffen''s Paradox478 赠品Gifts479 吉尼比率Gini Ratio480 经济理论中的整体分析Global Analysis in Economic Theory481 金本位Gold Standard482 黄金时代Golden Age483 黄金律Golden Rule484 货物与商品Goods and Commodities485 政府预算约束Government Budget Restraint486 图论Graph Theory487 重力模型Gravity Models488 格莱辛定律Gresham''s Law489 总替代品Gross Substitutes490 群(李群)论Group(Lie Group)Theory491 增长的核算Growth Accounting492 增长与周期Growth and Cycles493 经济增长与国际贸易Growth and International Trade494 哈恩问题Hahn Problem495 汉密尔顿体系Hamiltonians496 哈里斯-托达罗模型Harris-Todaro Model497 哈罗德-多马增长模型Harrod-Domar Growth Model498 霍金斯一西蒙条件Hawkins-Simon Condition499 卫生经济学Health Economics500 赫克歇尔-俄林贸易理论Heckscher-Ohlin Trade Theory501 套头交易Hedging502 享乐函数和享乐指数Hedonic Functions and Hedonic Indexes503 享乐主义Hedonism504 黑格尔主义Hegelianism505 赫芬达尔指数Herfindahl index506 异方差性Heteroskedasticity507 隐蔽活动,道德风险与合同理论Hidden Action, Moral Hazard and Contract Theory 508 等级制度Hierarchy509 讨价还价Higgling510 健全货币与货币基础High-powered Money and The Monetary Base511 历史成本会计Historical Cost accounting512 历史人口统计学Historical Demography513 经济思想及学说史History of Thought and Doctrine514 齐次函数和位似函数Homogeneous and Homothetic Functions515 国际游资Hot Money516 家庭预算Household Budgets517 家庭生产Household Production518 家务劳动Housework519 住房市场Housing Markets520 人力资本Human Capital521 人类资源Human Resources522 虚构的生产函数Humbug Production Function523 持猎和采集经济Hunting and Gathering Economies524 恶性通货膨胀Hyperinflation525 假设检验Hypothesis Testing526 IS-LM分析IS-LM Analysis527 理想指数Ideal Indexes528 理想产出Ideal Output529 理想类型Ideal Type530 识别Identification531 意识形态Ideology532 贫困化增长Immiserizing Grow533 尽早消费偏好Impatience534 不完全竞争Imperfect Competition535 不完全模型Imperfectionist Models536 帝国主义Imperialism537 默认契约Implicit Contracts538 进口替代和出口导向型增长Import Substitution and Export-Led Growth 539 派算Imputation540 剌激的协调性Incentive Compatibility541 刺激性合同Incentive Contracts542 收入Income543 收入-支出分析Income-Expenditure Analysis544 收入政策Incomes Policies545 不完全合同Incomplete Contracts546 不完全市场Incomplete Markets547 规模报酬递增Increasing Return to Scale548 指数Index Numbers549 指数化证券Indexed Securities550 指导性计划Indicative Planning551 指标Indicators552 无差异定律Indifference, Law of553 间接税Indirect Taxes554 间接效用函数Indirect Utility Function555 个人主义Individualism556 不可分性Indivisibilities557 归纳Induction558 产业组织Industrial Organization559 劳资关系Industrial Relations560 产业革命Industrial Revolution561 工业化Industrialization562 不等式Inequalities563 不平等Inequality564 国家之间的不平等Inequality between Nations565 人与人的不平等Inequality between Persons566 性别的不平等Inequality between The Sexes567 工资的不平等Inequality of Pay568 新生工业Infant Industry569 婴儿死亡率Infant Mortality570 通货膨胀Inflation571 通货膨胀会计Inflation Accounting572 通货膨胀与增长Inflation and Growth573 通货膨胀预期Inflationary Expections574 通货膨胀缺口Inflationary Gap575 非正规经济Informal Economy576 信息论Information Theory577 继承Inheritance578 继承税Inheritance Taxes579 创新Innovation580 投入-产出分析Input-output Analysis581 制度经济学Institutional Economics582 工具变量Instrumental Variables583 保险Insurance584 整数规划Integer Programming585 需求的可积性Integrability of Demand586 智力Intelligence587 相依偏好Interdependent Preferences588 利率Interest Rate589 利息和利润Interest and Profit590 多种利益Interests591 代际模型Intergenerational Models592 内部经济Internal Economies593 国内移民Internal Migration594 内部收益率Internal Rate of Return595 国际资本流动International Capital Flows596 国际金融International Finance597 国际收入比较International Income Comparisons598 国际债务International Indebtedness599 国际清偿能力International Liquidity600 国际移民International Migration601 国际货币经济学International Monetary Economics602 国际货币体制International Monetary Institutions603 国际货币政策International Monetary Policy604 国际贸易International Trade605 人际效用对比Interpersonal Utility Comparison606 时际均衡与效率Intertemporal Equilibrium and Efficiency607 时际资产组合理论和资产定价Intertemporal Portfolio Theory and Asset Pricing 608 价值的不可变标准Invariable Standard of value609 存货Inventories610 存货周期Inventory Cycles611 确定性条件下的存货政策Inventory policy under certainty612 投资Investment613 投资决策标准Investment Decision Criteria614 投资计划Investment Planning615 投资与积累Investment and Accumulation616 看不见的手Invisible Hand617 非自愿失业Involuntary Unemployment618 工资铁律Iron Law of Wages619 作为经济理论家的杰文斯Jevons As An Economic Theorist 620 联合生产Joint Production621 线性模型中的联合生产Joint Production in Linear Models 622 法理学Jurisprudence623 公平价格Just Price624 公平Justice625 公平、不平等及岐视Justices, Inequality and Discrimination 626 凯恩斯的《通论》Keynes''s General Theory627 凯恩斯主义经济学Keynesian Economics628 凯恩斯革命Keynesian Revolution629 凯恩斯主义Keynesianism630 弯折的需求曲线Kinked Demand Curve631 圣殿骑士团Knights Templar632 康德拉季耶夫周期Kondratieff Cycle633 库兹涅茨波动Kuznets Swings634 劳动经济学Labour Economics635 劳动交换Labour Exchange636 劳动市场歧视Labour Market Discrimination637 劳动市场Labour Markets638 劳动力Labour Power639 劳动过程Labour Process640 妇女劳动供给Labour Supply of Women641 劳动剩余经济Labour Surplus Economies642 劳动价值论Labour Theory of value643 劳动与就业Labour and Employment644 劳动者管理经济Labour-Managed Economies645 拉格朗日乘子Lagrange Multipliers646 自由放任主义Laissez-Faire647 土地改革Land Reform648 地租Land Rent649 土地税Land Tax650 兰格一勒纳机制Lange一Lerner Mechanism651 巨大经济Large Economies652 潜在变量Latent Variables653 大庄园制Latifundia654 法律与经济学Law and Economics655 解雇Layoffs656 沙特利耶原理Le Chatelier Principle657 起前与滞后Leads and Lags658 边干边学Learning-by-doing659 最小二乘法Least Squares660 闲暇Leisure661 有闲阶级Leisure Class662 里昂惕夫悖论Leontief Paradox663 字典式序Lexicographic Orderings664 自由主义Liberalism665 自由Liberty666 生命周期假说Life Cycle Hypothesis667 人寿保险Life Insurance668 寿命表Life Tables669 似然Likelihood670 极限定价Limit Pricing671 有限应变量Limited Dependent Variables672 增长的极限Limits to Growth673 林达尔均衡Lindahl Equilibrium674 林达尔论财政Lindahl on Public Finance675 线性模型Linear Models676 线性规划Linear Programing677 联系Linkages678 流动性Liquidity679 流动性偏好Liquidity Preference680 可贷资金Loanable Funds681 地方财政Local Public Finance682 经济活动的区位Location of Economic Activity683 对数正态分布Lognormal Distribution684 长周期Long Cycles685 经济增长中的长波Long Swing in Economic Growth686 长期和短期Long-run and Short-run687 洛伦茨曲线Lorenz Curve688 低工资Low Pay689 一次总付税Lump Sum Taxes690 李雅普诺夫函数Lyapunov Functions691 李雅普诺夫定理Lyapunov''s Theorem692 机器问题Machinery Question693 宏观经济计量模型Macroeconometric Models694 宏观经济政策Macroeconomic Policy695 宏观经济学理论Macroeconomic Theory696 宏观经济学:与微观经济学的关系Macroeconomics Relations with Microeconomics 697 保持资本完整无缺Maintaining Capital Intact698 马尔萨斯的人口理论Malthus Theory of Population699 马尔萨斯与古典经济学Malthus and Classical Economics700 经理资本主义Managerial Capitalism701 曼彻斯特学派Manchester School702 制造业活动与非工业化Manufacturing and De-industrialization703 资本边际效率Marginal Efficiency of Capital704 边际生产力理论Marginal Productivity Theory705 货币的边际效用Marginal Utility of Money706 边际和平均成本定价Marginal and Average Cost Pricing707 边际主义经济学Marginalist Economics708 市场失灵Market Failure709 营销期Market Period710 集贸市场Market Places711 市场价格Market Price712 市场份额Market Share713 市场社会主义Market Socialism714 市场结构Market Structure715 市场结构与创新Market Structure and Innovation716 市场价值与市场价格Market value and Market Price717 购销管理局Marketing Boards718 马歇尔-勒纳条件Marshall-Lerner Condition719 鞍Martingales720 马克思主义经济学Marxian Economics721 马克思主义价值分析Marxian value Analysis722 马克思主义Marxism723 马克思主义经济学Marxist Economics724 物资平衡Material Balances725 数理经济学Mathematical Economics726 政治经济学的数学方法Mathematical Method in Political Economy727 矩阵乘子Matrix Multiplier728 极大似然Maximum Likelihood729 最大满足Maximum Satisfaction730 平均值Mean value731 均值-方差分析Mean-variance Analysis732 确义性与不变性Meaningfulness and Invariance733 测度论Measure Theory734 经济增长的测算Measurement of Economic Growth735 测算理论Measurement, Theory of736 重商主义Mercantilism737 兼并Mergers738 有益品Merit Goods739 方法论之争Methodentreit740 方法论Methodology741 微观经济学Microeconomics742 军费开支Military Expenditure743 最低工资Minimum Wages744 生产方式Mode of Production745 模型与理论Models and Theory746 增长模型Models of growth747 货币主义Monetarism748 国际收支的货币分析法Monetary Approach to the Balance of Payments749 货币基础Monetary Base750 货币幻想Monetary Cranks751 货币非均衡和市场出清Monetary Disequilibdum and Market Clearing752 货币均衡Monetary Equilibrium753 货币体制Monetary Institution754 货币政策Monetary Policy755 货币理论Monetary Theory756 货币幻觉Money Illusion757 货币供应Money Supply758 货币和一般均衡理论Money and General Equilibrium Theory759 货币与宏观经济学Money and Macroeconomics760 经济活动中的货币Money in Economic Activity761 货币贷款者Moneylenders762 城市经济学中的单中心模型Monocentric Models in Urban Economics 763 垄断性竞争Monopolistic Competition764 垄断性竞争与一般均衡Monopolistic Competition and General Equilibrium 765 垄断Monopoly766 垄断资本主义Monopoly Capitalism767 垄断与寡头垄断Monopoly and Oligopoly768 单调映射Monotone Mappings769 蒙特卡罗方法Monte Carlo Methods770 道德风险Moral Hazard771 道德哲学Moral Philosophy772 死亡率Mortality773 多重共线性Multicollinearity774 多国公司Multinational Corporations775 乘数分析Multiplier Analysis776 乘数-加速器相互作用Multiplier-accelerator Interaction777 多部门增长模型Multisector Growth Models778 多元时间序列模型Multivariate Time Series Models779 近视决策规则Myopic Decision Rules780 纳什均衡Nash Equilibrium781 国债National Debt782 国民收入National Income783 国民体系National System784 民族主义Nationalism785 国有化Nationalization786 自然法Natural Law787 自然垄断Natural Monopoly788 自然价格Natural Price789 自然利率和市场利率Natural Rate and Market Rate790 自然失业率Natural Rate of Unemployment791 自然资源Natural Resources792 自然资源和环境Natural Resources and Enviroment793 自然选择与进化Natural Selection and Evolution794 自然工资Natural Wage795 自然和人类资源Natural and Human Resources796 自然的及正常的条件Natural and Normal Conditions797 自然的和有保证的增长率Natural and Warranted Rates of Growth 798 必需品Necessaries799 负所得税Negative Income Tax800 负量Negative Quantities801 新李嘉图主义Neo-Ricardianism802 新古典的Neoclassical803 新古典增长理论Neoclassical Growth Theory804 新古典综合Neoclassical Synthesis805 净产品Net Product806 中性税收Neutral Taxation807 货币中性Neutrality of Money808 新古典宏观经济学New Classical Macroeconomics809 非合作对策Non-Cooperative Game810 非线性规划Non-Linear Programming811 非参数统计方法Non-Parametric Statistical Methods812 非竞争集团Non-competing Groups813 非凸性Non-convexity814 经济计量学中的非线性方法Non-linear Methods in Econometrics 815 非嵌套假设Non-nested Hypotheses816 非价格竞争Non-price Competition817 非盈利机构Non-profit Organizations818 非标准分析Non-standard Analysis819 无替代定理Non-substitution Theorems820 南北经济关系North-south Economic Relations821 价值标准Numeraire822 效用定律的数值确定Numerical Determination of the Laws of utility 823 营养Nutrition824 奥卡姆剃刀Occam''s (Ockham''s) Razor825 职业分离Occupational Segregation826 提供Offer827 提供曲线或相互需求曲线Offer Curve or Reciprocal Demand Curve 828 (卖方)寡头垄断Oligopoly829 寡头垄断与对策论Oligopoly and Game Theory830 敞地制Open Field System831 公开市场业务Open-market Operations832 运筹学Operations Research833 满足度Ophelimity834 机会成本Opportunity Cost835 最优控制与动态经济学Optimal Control and Economic Dynamics 836 最适度储蓄Optimal Savings837 最优关税Optimal Tariffs838 最优税收Optimal Taxation839 最优性与效率Optimality and Efficiency840 乐观主义与悲观主义Optimism and Pessimism841 最优货币区Optimum Currency Areas842 最适度人口量Optimum Population843 最适度货币数量Optimum Quantity of Money844 期权定价理论Option Pricing Theory845 期权Options846 序Orderings847 资本有机构成Organic Composition of Capital848 组织理论Organization Theory849 离群值Outliers850 产出与就业Output and Employment851 过度储蓄Over saving852 过度投资Over-investment853 间接成本Overhead Costs854 一般均衡的交叠世代模型Overlapping Generations Model of General Equilibrium 855 生产过剩Overproduction856 峰突Overshooting857 自生利率Own Rates of Interest858 帕尔格雷夫政治经济学辞典Palgrave''s Dictionary of Political Economy859 范式Paradigm860 悖论与异常Paradoxes and Anomalies861 帕累托分布Pareto Distribution862 帕累托效率Pareto Efficiency863 作为经济学家的帕累托Pareto as an Economist864 专利Patents865 路径分析Path Analysis866 回收期Pay-off Period867 工资税Payroll Taxes868 旺季定价Peak-load Pricing869 小农经济Peasant Economy870 小农Peasants871 货币经济与非货币经济Pecuniary and Non-Pecuniary Economies872 完全竞争Perfect Competition873 完全预见Perfect Foresight874 完全信息Perfect Information875 完全竞争市场和不完全竞争市场Perfectly and Imperfectly Competitive Markets 876 表演艺术Performing Arts877 生产周期Period of Production878 外围Periphery879 佩龙一弗罗宾尼斯定理Perron-Frobenius Theorem880 菲利普斯曲线Phillips Curve。

高中英语哲学思想单选题50题

高中英语哲学思想单选题50题1. Which of the following statements best represents the idea of Plato's Theory of Forms?A. The physical world is the ultimate reality.B. Ideas are more real than the physical objects.C. Sensory experiences are the only source of knowledge.D. Everything is constantly changing and unpredictable.答案:B。

柏拉图的理念论认为理念(形式)比具体的物质世界更真实,A 选项说物质世界是终极现实,与柏拉图的观点相悖;C 选项感官经验是唯一知识来源并非柏拉图的观点;D 选项一切都在不断变化且不可预测不符合柏拉图的理念论。

2. In Aristotelian philosophy, the concept of "entelechy" refers to:A. The potentiality of a thing to become something else.B. The final cause that guides the development of a thing.C. The randomness in the evolution of all beings.D. The complete absence of purpose in nature.答案:B。

亚里士多德哲学中的“隐德来希”指的是引导事物发展的最终原因,A 选项指的是事物成为其他东西的可能性;C 选项说的是所有生物进化的随机性不符合;D 选项自然界完全没有目的也不正确。

3. According to Stoicism, which of the following is most important for a person to achieve inner peace?A. Pursuing pleasure and material wealth.B. Controlling one's emotions and accepting fate.C. Always striving to change the external world.D. Focusing on personal achievements and recognition.答案:B。

Fuzzy Logic

小王子主题ppt模板

Theme Reporter

xxx xxx

单击此处添加正文,文字是您思想的提炼,为了演示发布的良好效果, 请言简意赅地阐述您的观点。

2018/05/06

POWER YOUR POINT

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa. Fusce posuere, magna sed pulvinar ultricies, purus lectus malesuada libero, sit amet commodo magna eros quis urna. Nunc viverra imperdiet enim.

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa. Fusce posuere

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa. Fusce posuere, magna sed pulvinar ultricies, purus lectus malesuada libero, sit amet commodo magna eros quis urna. Nunc viverra imperdiet enim.

SUPPORTER S SAY

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa

完整性与功利主义伦理学

完整性与功利主义伦理学关于《完整性与功利主义伦理学》,是我们特意为大家整理的,希望对大家有所帮助。

摘要:伯纳德威廉斯强调哲学必须直面人类生活的复杂性和困难性,他批判以往哲学回避现实,特别是功利主义和康德主义,以恶劣的方式将生活简单化,忽视了个人情感、规划和运气对伦理生活的影响。

他通过对功利主义后果论结构的分析,指出其中所包含的消极责任特征,批判功利主义忽视了个人分离性的重要性以及对个人完整性的破坏。

威廉斯强调个人是情感需要、功利偏好和理性能力的综合体,主张应该从人的主体自身出发去思考道德问题,认为重要问题是人如何过有意义的生活,而不是我应该遵守什么样的规则。

威廉斯的批判是强有力的,对功利主义的发展具有重要启发。

下载论文网关键词:伯纳德威廉斯;个人完整性;后果论;消极责任;不偏不倚;功利主义中图分类号:B561.6 文献标识码:A 文章编号:1672-3104(2014)03?A50?A8一、关于后果论的理论架构及其缺陷经过古典功利主义与现代功利主义的发展演进,功利主义的理论形态发生了很大的变化,但是在核心原则上仍然保持一致。

阿玛蒂亚森将功利主义的核心要素归结为三个:“后果主义”“福利主义”“总量排序”,并指出所谓“后果主义”“指的是以下主张:一切选择(无论是对于行动、规则、机构等等所做的)都必须根据其后果(即它们所产生的结果)来评值”[1]。

根据后果论,行为的道德属性取决于其后果的价值,其根本目的在于提高事态的内在价值,而对达到这一目的的手段置之不理。

伯纳德威廉斯指出:“我认为,后果论的中心思想是,只有那种具有内在价值的事物是事态(state of affairs);任何其他事物具有价值,这是因为它导致了某些具有内在价值的事态。

”[2](8081)也就是说,具有内在价值的事物是事态而非产生价值的行为,行为与行为者只是达成事态的手段。

“功利主义者所感兴趣的,只是幸福的总量。

他们完全不在意幸福是如何产生的,也不在乎是谁的幸福岌岌可危”[3],这种后果论的理论架构使得功利主义饱受批评。

旅行的意义简约模板PPT

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa. Fusce posuere, magna sed pulvinar ultricies, purus lectus malesuada libero, sit amet commodo magna eros quis urna.

这里填写标题

添加文本信息

Maecenas porttitor congue massa. sit amet commodo magna eros

quis urna.

添加文本信息

Maecenas porttitor congue massa. sit amet commodo magna eros

quis urna.

添加标题文本信息

Lorem ipsum dolor sit amet, consectetuer adipiscing elit. Maecenas porttitor congue massa. Fusce posuere, magna sed pulvinar ultricies, purus lectus malesuada libero

这里填写标题

添加文本信息

Fusce posuere, magna sed pulvinar ultricies, commodo magna eros quis urna.

添加文本信息 添加文本信息

这里填写标题

添加文本信息

Lorem ipsum dolor

consectetuer adipiscing elit.

添加文本信息

概率产品