2016年ACCA知识点:Bonds

2016年ACCA F9《财务管理》重要知识点讲解(3)

2016年ACCA F9《财务管理》重要知识点讲解(3)et Present ValueWhen using the NPV method the present value table is required in order to find out the present value factors of the pound at different rates over different time periods. Your examination question paper has often in the past provided the table for candidates? use with the examination questions. There is no indication that this will not continue. However the figures in the table can be calculated if a table is unavailable.Deluxe modelUnder the NPV method super has a positive NPV of £51,840 whilst deluxe has a negative NPV of £41,040. Any project with a negative NPV should not be undertaken at all. On the basis of this super model will be recommended but not deluxe model.Internal Rate of Return (IRR)Under NPV we have used 12% discount rate and arrived at both a positive and negative NPV respectively for the two machines. We need to use a higher rate for the Super model to arrive at a negative NPV and a lower rate for Deluxe model to arrive at a positive NPV. Remember that the higher the IRR the better. Let us now use 20% for Super model and 4% for Deluxe model.Super ModelNow that we have a negative NPV for Super model we can now use the IRR formula we had earlier to establish IRR for this model.Now let us turn our attention to the second machine, but first we need to find a positive NPV for this machine. We have stated earlier that we will use 4%, let us use that straight away.Deluxe ModelThe Deluxe module has an IRR of 10.51%. As this is lower than the super model?s 16.52%, once again super model will be recommended.ConclusionIt can be seen that all four methods of investment appraisal have consistently recommended the Super model. This has happened because the example was designedto do so. A real life exercise on investment appraisal will probably not be as easy and straightforward as this. Life is never straightforward. The author has not introduced any complications into the example. Areas that could bring in complications such as projects with unequal lives, effects of taxation and inflation have been deliberately left out of the example in this article. A future article by the author will bring in some of these complications so that readers can appreciate that life in this area is not always as straightforward as depicted in this article.by Samuel O Idowu01 Sep 2000In Capital Investment Appraisal 1, a second article, was promised which would look at projects with unequal lives, taxation and the impact of inflation. Students at this stage of their studies should be aware that questions in this area would not always be straightforward.This second article intends to focus on some of these complications which may be introduced into capital investment appraisal questions. It is hoped that by working through the author?s approach in the following example, students will learn the techniques required in tackling questions of this sort and be able to apply them in an examination environment.Before looking at the example, let us say a word or two about them.Unequal life projectsWhen considering possible investment projects, it is often the case that competing projects are not of the same life span. For example, an organisation may have to choose between two projects in which project A might have a useful life of, say, five years whilst another competing project, B may have a useful life of seven years. To simply compare the net present values of the two projects without looking at the unequal life span will not be comparing like with like. Under normal circumstances project B will have a higher net present value, as it has the opportunity of generating cash for two additional years. To recommend undertaking project B solely, on the basis of the higher net present value may not be based on a sound reason. This is because there is a possibility that the net cash inflow generated from project A at the end of its five-year life could be reinvested elsewhere for the two equivalent additional years generating additional NPV which may total more than project B?s NPV. This fact is often ignored as only the net present values of projects at the end of their respective lives are compared.What needs to be done is to express the two projects in equal terms. If two or more unequal life projects being considered had the same level of risk, then it will be appropriate to use the Equivalent Annual Cost Approach also known as Annual Equivalent Annuity Method to compare net present values of costs on an annualised basis. If the projects had different levels of risk then the appropriate approach will be to assume Infinite Re-investment for each project and calculate their net present values to infinity.These two approaches will now be examined in detail.The equivalent annual cost (EAC) approachThis approach computes the present value of costs for each project over a cycle and then expresses the present value in an annual equivalent cost using the appropriate annuity factors for each cycle. The annual equivalent of NPVs of the two or more projects can then be compared. Having calculated the EAC for each cycle and each project, then compare the EACs. The project that has the lowest EAC over the cycles is the better one if lowest outlay is the objective or the higher EAC would be preferred if the highest revenue were the objective.Infinite re-investment approachThis approach is appropriate when projects of unequal lives and unequal risks are being considered. The first step to take will be to establish the net present value of the projects in the normal way and then calculate the net present value of projects to infinity using the formula:NPV 關= NPV of project/PV of annuity for the life of project at discount rate Discount rate for the projectThe project, which has the highest NPV to infinity, is the one to recommendProject appraisal under inflationInflation is a state of affairs under which prices are constantly rising. When this happens the purchasing power of money depreciates. The currency will buy fewer goods and services than previously and consequently the real returns on investments will fall. Investors understandably, will expect to be compensated for the fall in the value of money during inflation. When appraising investment opportunities the appraiser requires an understanding of three discount rates. These are Money Rates,Real Rates and Inflation Rates. Money rate (also known as Nominal rate) is a combination of the real rate and inflation rate and should be used to discount money cash flows. If on the other hand you were given real cash flows these must be discounted using the real discount rates. In order to be able to use either of these two rates, you need to know how to calculate both of them. They can be calculated from the following formula, devised by Fisher1 + m = (1 + r) x (1 + i)Where:m = money rater = real ratei = inflation rateFrom the above formula it is possible to calculate m, r and i if you were given information about two of the three variables. For example if you were told that the money rate was 20% and real rate was 12% the inflation rate will be calculated as follows:i =1 + m ? 11 + ri =1 + 0.20? 11 + 0.12i =1.0714?= 7.14%Equally m and r could be calculated as follows.m =(1.12 x 1.0714) ? 1(1.19999) ? 120%r =1.20? 11.071412%When the appropriate discount rate has been established the present value factors of this rate at different time periods can be obtained from the present value table or the present value factors calculated using the following formula:11111(1+r)(1+r)2(1+r)3(1+r)4(1+r)5?etcWhere r = discount rate.Present value tables are only available for whole numbers, so if your r is not a whole number you will have to use the formula to calculate the required present value factors. Let us calculate for example the present value factors of 7.14% for years 1 to 5.11111(1.0714)(1.0714) 2(1.0714) 3(1.0714) 4(1.0714)5?etc0.9330.8710.8130.7590.708Having either obtained or calculated the present value factors for the relevant discount rates, these are then used to discount the future cash flows to give the net present values of the projects. It is important to understand when to use which rate. If the question gives you money cash flows, then use the money rate; if the question gives real cash flow it follows then that the real rate must be used. To confuse one with the other would give the wrong answer.。

常见ACCA会计术语汇总

常见ACCA会计术语汇总Account 有很多意思,常见的主要是“说明、解释;计算、帐单;银行帐户”。

例如:1、He gave me a full account of his plan。

他把计划给我做了完整的说明。

2、Charge it to my account。

把它记在我的帐上。

3、Cashier:Good afternoon。

Can I help you ?银行出纳:下午好,能为您做什么?Man :I'd like to open a bank account .男人:我想开一个银行存款帐户。

还有account title(帐户名称、会计科目)、income account(收益帐户)、account book(帐簿)等。

在account 后面加上词缀ing 就成为accounting ,其意义也相应变为会计、会计学。

例如:1、Accounting is a process of recording, classifying,summarizing and interpreting of those business activities that can be expressed in monetary terms.会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程。

2、It has been said that Accounting is the language of business.据说会计是“商业语言”3、Accounting is one of the fastest growing profession in the modern business world.会计是当今经济社会中发展最快的职业之一。

4、Financial Accounting and Managerial Accounting are two major specialized fields in Accounting.财务会计和管理会计是会计的两个主要的专门领域。

ACCAsbl知识点总结

ACCAsbl知识点总结ACCA留学考试是英国特许公认会计师协会资格考试。

ACCA资格被国际性企事业单位、很多跨国公司和工商企业以及国际会计和金融服务行业所承认和接受,是全球金融和会计领域的最优秀的证书之一,所以选修ACCA资格是广大学生的首选。

那么,接下来我将围绕ACCA的知识点来对ACCA进行一番总结。

一、会计基础1.1 会计基础知识首先,ACCA会计基础知识部分主要包括会计基础、商业环境和财务管理三部分内容。

会计基础是ACCA考试的重要考核内容之一。

ACCA会计基础知识部分包括了财务报表的基本原则、资产负债表和利润表的基本结构、会计方程式等。

商业环境是ACCA考试的重要考核内容之一,是ACCA考试的核心内容之一。

商业环境是ACCA考试的核心内容之一。

商业环境是ACCA考试的核心内容之一。

商业环境是ACCA 考试的核心内容之一。

财务管理是ACCA考试的核心内容之一,主要包括了财务管理基本概念、财务管理工具和技术以及财务管理的决策分析。

1.2 财务会计财务会计是ACCA考试的重要考核内容之一。

ACCA财务会计主要包括了财务报表的编制和解释、资产负债表和净资产变动表、现金流量表、财务报告分析和预算。

1.3 管理会计管理会计是ACCA考试的重要考核内容之一。

ACCA管理会计主要包括了管理会计的基本概念、成本类型与行为、成本估算和成本计算方法、作业成本法、作业成本法、预算控制等。

1.4 审计及验视审计及验视是ACCA考试的重要考核内容之一。

ACCA审计及验视主要包括了审计的基本概念、审计程序、审计证据收集、审计报告以及内部控制。

二、财务管理2.1 财务管理基本知识财务管理基本知识是ACCA考试的重要考核内容之一。

ACCA财务管理基本知识部分主要包括了财务管理的概念、财务管理的目标、财务管理的环境分析与内外部环境等。

2.2 资本预算资本预算是ACCA考试的重要考核内容之一。

ACCA资本预算主要包括了资本成本的概念与分析、资本预算的基本概念、资本收益分析、风险分析、资本预算的决策与评价。

acca考试知识点总结

acca考试知识点总结ACCA全称为Association of Chartered Certified Accountants,是全球最有影响力的专业会计师协会之一。

ACCA会员遍布全球180个国家,是世界上最大的国际专业会计师组织。

ACCA证书不仅在英国和欧洲有很高的认可度,而且在亚洲、非洲和中东等地区也备受青睐。

ACCA证书是一个标志,是对专业能力、行业经验和国际视野的认可。

ACCA考试是全球专业会计师考试,它涵盖了财务管理和会计领域的所有知识点,需要考生具备相当的知识储备和能力。

下面我们来总结一下ACCA考试的知识点。

第一部分:核心基础知识1.管理会计管理会计是一门研究如何为组织做决策和分配资源的学科,主要包括成本管理、预算管理、绩效评价和风险管理等知识点。

2.财务报告财务报告是组织向外部利益相关者提供的关于其财务状况和经营业绩的信息,主要包括财务报表分析、财务信息披露和国际财务报告准则等知识点。

3.税收税收是政府为了筹集财政收入而向纳税人征收的一种收费,主要包括个人所得税、公司所得税、增值税和财产税等知识点。

4.审计与保险审计是一种独立的评价活动,用来评估组织内部控制的有效性和财务报告的可靠性,主要包括内部审计、外部审计和信息系统审计等知识点。

第二部分:商业专业化知识1.企业法企业法是一门研究组织和企业在商业活动中的法律关系的学科,主要包括合同法、公司法、竞争法和知识产权法等知识点。

2.财务管理财务管理是一种为组织提供资金和资本的管理活动,主要包括投资决策、资金成本、风险管理和财务市场等知识点。

3.商业伦理商业伦理是一种研究商业活动中道德规范和价值观的学科,主要包括道德决策、企业社会责任和道德风险管理等知识点。

4.财务分析财务分析是一种评估组织财务状况和经营业绩的方法,主要包括财务比率分析、现金流量分析和经济附加值分析等知识点。

以上就是ACCA考试的知识点总结,希望对考生有所帮助。

在备考过程中,考生需要充分理解和掌握这些知识点,并且进行大量的练习和模拟考试,才能在考试中取得好成绩。

ACCA会计科目

会计科目中英对照2015-07-09中国ACCA考试网分类:ACCA基础学习阅读(236)中国ACCA学习网将为广大中国ACCA学习者带来更多最新的学习考试资讯和学习经验等内容,今天给大家带来的是会计科目中英对照一级科目二级科目三级科目四级科目代码名称代码名称代码名称代码名称英译1 资产assets11~ 12 流动资产current assets111 现金及约当现金cash and cash equivalents1111 库存现金cash on hand1112 零用金/周转金petty cash/revolving funds1113 银行存款cash in banks1116 在途现金cash in transit1117 约当现金cash equivalents1118 其它现金及约当现金other cash and cash equivalents112 短期投资short-term investments1121 短期投资-股票short-term investments - stock1122 短期投资-短期票券 short-term investments - short-term notes and bills1123 短期投资-政府债券 short-term investments - government bonds1124 短期投资-受益凭证 short-term investments - beneficiary certificates1125 短期投资-公司债 short-term investments - corporate bonds1128 短期投资-其它short-term investments - other1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现 discounted notes receivable1137 应收票据-关系人 notes receivable - related parties1138 其它应收票据 other notes receivable1139 备抵呆帐-应收票据 allowance for uncollec- tible accounts- notes receivable 114 应收帐款accounts receivable1141 应收帐款 accounts receivable1142 应收分期帐款 installment accounts receivable1147 应收帐款-关系人 accounts receivable - related parties1149 备抵呆帐-应收帐款 allowance for uncollec- tible accounts - accounts receivable 118 其它应收款other receivables1181 应收出售远汇款 forward exchange contract receivable1182 应收远汇款-外币 forward exchange contract receivable - foreign currencies 1183 买卖远汇折价 discount on forward ex-change contract1184 应收收益 earned revenue receivable1185 应收退税款 income tax refund receivable1187 其它应收款- 关系人 other receivables - related parties1188 其它应收款- 其它 other receivables - other1189 备抵呆帐- 其它应收款 allowance for uncollec- tible accounts - other receivables 121~122 存货inventories1211 商品存货 merchandise inventory1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失 allowance for reduction of inventory to market 1221 制成品 finished goods1222 寄销制成品 consigned finished goods1223 副产品 by-products1224 在制品 work in process1225 委外加工 work in process - outsourced1226 原料 raw materials1227 物料 supplies1228 在途原物料 materials and supplies in transit1229 备抵存货跌价损失 allowance for reduction of inventory to market 125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费 prepaid insurance1254 用品盘存 office supplies1255 预付所得税prepaid income tax1258 其它预付费用other prepaid expenses126 预付款项prepayments1261 预付货款prepayment for purchases1268 其它预付款项 other prepayments128~129 其它流动资产other current assets1281 进项税额 VAT paid ( or input tax)1282 留抵税额 excess VAT paid (or overpaid VAT)1283 暂付款 temporary payments1284 代付款 payment on behalf of others1285 员工借支advances to employees1286 存出保证金 refundable deposits1287 受限制存款certificate of deposit-restricted1291 递延所得税资产 deferred income tax assets1292 递延兑换损失 deferred foreign exchange losses1293 业主(股东)往来 owners'(stockholders') current account 1294 同业往来current account with others1298 其它流动资产-其它 other current assets - other13 基金及长期投资funds and long-term investments131 基金funds1311 偿债基金 redemption fund (or sinking fund)1312 改良及扩充基金fund for improvement and expansion 1313 意外损失准备基金 contingency fund1314 退休基金 pension fund1318 其它基金 other funds132 长期投资long-term investments1321 长期股权投资long-term equity investments1322 长期债券投资 long-term bond investments1323 长期不动产投资 long-term real estate in-vestments1324 人寿保险现金解约价值 cash surrender value of life insurance1328 其它长期投资 other long-term investments1329 备抵长期投资跌价损失 allowance for excess of cost over market value of long-term investments14~ 15 固定资产property , plant, and equipment141 土地land1411 土地 land1418 土地-重估增值land - revaluation increments142 土地改良物land improvements1421 土地改良物 land improvements1428 土地改良物-重估增值 land improvements - revaluation increments1429 累积折旧-土地改良物 accumulated depreciation - land improvements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值 buildings -revaluation increments1439 累积折旧-房屋及建物 accumulated depreciation - buildings144~146 机(器)具及设备machinery and equipment1441 机(器)具 machinery1448 机(器)具-重估增值 machinery - revaluation increments1449 累积折旧-机(器)具 accumulated depreciation - machinery151 租赁资产leased assets1511 租赁资产 leased assets1519 累积折旧-租赁资产 accumulated depreciation - leased assets152 租赁权益改良leasehold improvements1521 租赁权益改良 leasehold improvements1529 累积折旧- 租赁权益改良 accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment1561 未完工程 construction in progress1562 预付购置设备款prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值 miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, and equipment16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resources -revaluation increments1619 累积折耗-天然资源 accumulated depletion - natural resources17 无形资产intangible assets171 商标权trademarks1711 商标权 trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权 franchise174 著作权copyright1741 著作权 copyright175 计算机软件computer software1751 计算机软件 computer software cost176 商誉goodwill1761 商誉 goodwill177 开办费organization costs1771 开办费 organization costs178 其它无形资产other intangibles1781 递延退休金成本 deferred pension costs1782 租赁权益改良 leasehold improvements1788 其它无形资产-其它 other intangible assets - other 18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond issuance costs1812 长期预付租金long-term prepaid rent1813 长期预付保险费long-term prepaid insurance 1814 递延所得税资产deferred income tax assets1815 预付退休金 prepaid pension cost1818 其它递延资产other deferred assets182 闲置资产idle assets1821 闲置资产 idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables 1841 长期应收票据 long-term notes receivable1842 长期应收帐款long-term accounts receivable1843 催收帐款 overdue receivables1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款 allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others1851 出租资产 assets leased to others1858 出租资产-重估增值 assets leased to others - incremental value from revaluation 1859 累积折旧-出租资产 accumulated depreciation - assets leased to others186 存出保证金refundable deposit1861 存出保证金 refundable deposits188 杂项资产miscellaneous assets1881 受限制存款 certificate of deposit - restricted1888 杂项资产-其它 miscellaneous assets - other2 负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款bank loan2114 短期借款-业主 short-term borrowings - owners2115 短期借款-员工 short-term borrowings - employees2117 短期借款-关系人 short-term borrowings- related parties2118 短期借款-其它 short-term borrowings - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券 other short-term notes and bills payable2129 应付短期票券折价 discount on short-term notes and bills payable 213 应付票据notes payable2131 应付票据 notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据 other notes payable214 应付帐款accounts pay able2141 应付帐款 accounts payable2147 应付帐款-关系人accounts payable - related parties216 应付所得税income taxes payable2161 应付所得税 income tax payable217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐-其它accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款other payables2181 应付购入远汇款forward exchange contract payable2182 应付远汇款-外币 forward exchange contract payable - foreign currencies 2183 买卖远汇溢价 premium on forward exchange contract2184 应付土地房屋款 payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款-关系人other payables - related parties2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳compensation payable to directors and supervisors2198 其它应付款-其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款 long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项 long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人 long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债 other long-term lia- bilities - current portion228~229 其它流动负债other current liabilities2281 销项税额 VAT received(or output tax)2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债 estimated warranty liabilities2291 递延所得税负债deferred income tax liabilities2292 递延兑换利益 deferred foreign exchange gain2293 业主(股东)往来 owners' current account2294 同业往来 current account with others2298 其它流动负债-其它other current liabilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价 premium(discount) on corporate bonds payable232 长期借款long-term loans payable2321 长期银行借款 long-term loans payable - bank2324 长期借款-业主long-term loans payable - owners2325 长期借款-员工long-term loans payable - employees2327 长期借款-关系人long-term loans payable - related parties2328 长期借款-其它long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes payable2332 长期应付帐款long-term accounts pay-able2333 长期应付租赁负债 long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税 estimated accrued land value incremental tax pay-able235 应计退休金负债accrued pension liabilities2351 应计退休金负债 accrued pension liabilities238 其它长期负债other long-term liabilities2388 其它长期负债-其它other long-term liabilities - other28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入 deferred revenue2814 递延所得税负债 deferred income tax liabilities2818 其它递延负债other deferred liabilities286 存入保证金deposits received2861 存入保证金 guarantee deposit received288 杂项负债miscellaneous liabilities2888 杂项负债-其它 miscellaneous liabilities - other3 业主权益owners' equity31 资本capital311 资本(或股本) capital3111 普通股股本capital - common stock3112 特别股股本capital - preferred stock3113 预收股本 capital collected in advance3114 待分配股票股利 stock dividends to be distributed3115 资本capital32 资本公积additional paid-in capital321 股票溢价 paid-in capital in excess of par3211 普通股股票溢价 paid-in capital in excess of par- common stock 3212 特别股股票溢价 paid-in capital in excess of par- preferred stock 323 资产重估增值准备 capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积 capital surplus from gain on disposal of assets 3241 处分资产溢价公积 capital surplus from gain on disposal of assets 325 合并公积 capital surplus from business combination3251 合并公积capital surplus from business combination326 受赠公积 donated surplus3261 受赠公积donated surplus328 其它资本公积 other additional paid-in capital3281 权益法长期股权投资资本公积 additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易 additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积 legal reserve3311 法定盈余公积 legal reserve332 特别盈余公积 special reserve3321 意外损失准备 contingency reserve3322 改良扩充准备improvement and expansion reserve3323 偿债准备 special reserve for redemption of liabilities3328 其它特别盈余公积 other special reserve335 未分配盈余(或累积亏损) retained earnings-unappropriated (or accumulated deficit) 3351 累积盈亏accumulated profit or loss3352 前期损益调整 prior period adjustments3353 本期损益 net income or loss for current period34 权益调整equity adjustments341 长期股权投资未实现跌价损失 unrealized loss on market value decline of long-term equity investments3411 长期股权投资未实现跌价损失 unrealized loss on market value decline of long-term equity investments342 累积换算调整数 cumulative translation adjustment3421 累积换算调整数 cumulative translation adjustments343 未认列为退休金成本之净损失 net loss not recognized as pension cost 3431 未认列为退休金成本之净损失net loss not recognized as pension costs 35 库藏股treasury stock351 库藏股 treasury stock3511 库藏股 treasury stock36 少数股权minority interest361 少数股权 minority interest3611 少数股权 minority interest4 营业收入operating revenue41 销货收入sales revenue411 销货收入 sales revenue4111 销货收入sales revenue4112 分期付款销货收入installment sales revenue417 销货退回 sales return4171 销货退回 sales return419 销货折让 sales allowances4191 销货折让 sales discounts and allowances46 劳务收入service revenue461 劳务收入 service revenue4611 劳务收入 service revenue47 业务收入agency revenue471 业务收入 agency revenue4711 业务收入 agency revenue48 其它营业收入other operating revenue488 其它营业收入-其它 other operating revenue4888 其它营业收入-其它other operating revenue - other 5 营业成本operating costs51 销货成本cost of goods sold511 销货成本 cost of goods sold5111 销货成本 cost of goods sold5112 分期付款销货成本installment cost of goods sold 512 进货 purchases5121 进货 purchases5122 进货费用 purchase expenses5123 进货退出 purchase returns5124 进货折让charges on purchased merchandise513 进料 materials purchased5131 进料 material purchased5132 进料费用charges on purchased material5133 进料退出material purchase returns5134 进料折让 material purchase allowances514 直接人工 direct labor5141 直接人工 direct labor515~518 制造费用 manufacturing overhead5151 间接人工indirect labor5152 租金支出 rent expense, rent5153 文具用品 office supplies (expense)5154 旅费travelling expense, travel5155 运费 shipping expenses, freight5156 邮电费 postage (expenses)5157 修缮费 repair(s) and maintenance (expense ) 5158 包装费 packing expenses5161 水电瓦斯费 utilities (expense)5162 保险费 insurance (expense)5163 加工费 manufacturing overhead - outsourced 5166 税捐taxes5168 折旧 depreciation expense5169 各项耗竭及摊提 various amortization5172 伙食费meal (expenses)5173 职工福利 employee benefits/welfare5176 训练费 training (expense)5177 间接材料 indirect materials5188 其它制造费用 other manufacturing expenses 56 劳务成本制ervice costs561 劳务成本 service costs5611 劳务成本service costs57 业务成本gency costs571 业务成本 agency costs5711 业务成本 agency costs58 其它营业成本other operating costs588 其它营业成本-其它 other operating costs-other 5888 其它营业成本-其它other operating costs - other 6 营业费用operating expenses61 推销费用selling expenses615~618 推销费用 selling expenses6151 薪资支出 payroll expense6152 租金支出 rent expense, rent6153 文具用品 office supplies (expense)6154 旅费travelling expense, travel6155 运费 shipping expenses, freight6156 邮电费 postage (expenses)6157 修缮费 repair(s) and maintenance (expense) 6159 广告费 advertisement expense, advertisement 6161 水电瓦斯费 utilities (expense)6162 保险费 insurance (expense)6164 交际费 entertainment (expense)6165 捐赠 donation (expense)6166 税捐taxes6167 呆帐损失loss on uncollectible accounts6168 折旧 depreciation expense6169 各项耗竭及摊提 various amortization6172 伙食费 meal (expenses)6173 职工福利 employee benefits/welfare6175 佣金支出 commission (expense)6176 训练费 training (expense)6188 其它推销费用 other selling expenses62 管理及总务费用general & administrative expenses625~628 管理及总务费用 general & administrative expenses 6251 薪资支出 payroll expense6252 租金支出 rent expense, rent6253 文具用品 office supplies6254 旅费 travelling expense, travel6255 运费 shipping expenses,freight6256 邮电费 postage (expenses)6257 修缮费repair(s) and maintenance (expense)6259 广告费 advertisement expense, advertisement6261 水电瓦斯费 utilities (expense)6262 保险费 insurance (expense)6264 交际费 entertainment (expense)6265 捐赠 donation (expense)6266 税捐 taxes6267 呆帐损失loss on uncollectible accounts6268 折旧 depreciation expense6269 各项耗竭及摊提 various amortization6271 外销损失 loss on export sales6272 伙食费 meal (expenses)6273 职工福利 employee benefits/welfare6274 研究发展费用 research and development expense6275 佣金支出 commission (expense)6276 训练费 training (expense)6278 劳务费professional service fees6288 其它管理及总务费用 other general and administrative expenses 63 研究发展费用research and development expenses635~638 研究发展费用 research and development expenses6351 薪资支出 payroll expense6352 租金支出 rent expense, rent6353 文具用品office supplies6354 旅费travelling expense, travel6355 运费 shipping expenses, freight6356 邮电费 postage (expenses)6357 修缮费repair(s) and maintenance (expense)6361 水电瓦斯费 utilities (expense)6362 保险费insurance (expense)6364 交际费 entertainment (expense)6366 税捐 taxes6368 折旧depreciation expense6369 各项耗竭及摊提various amortization6372 伙食费 meal (expenses)6373 职工福利employee benefits/welfare6376 训练费training (expense)6378 其它研究发展费用 other research and development expenses7 营业外收入及费用non-operating revenue and expenses, other income(expense) 71~74 营业外收入non-operating revenue711 利息收入 interest revenue7111 利息收入 interest revenue/income712 投资收益 investment income7121 权益法认列之投资收益 investment income recognized under equity method 7122 股利收入 dividends income7123 短期投资市价回升利益 gain on market price recovery of short-term investment 713 兑换利益 foreign exchange gain7131 兑换利益foreign exchange gain714 处分投资收益 gain on disposal of investments7141 处分投资收益 gain on disposal of investments715 处分资产溢价收入 gain on disposal of assets7151 处分资产溢价收入 gain on disposal of assets748 其它营业外收入 other non-operating revenue7481 捐赠收入 donation income7482 租金收入 rent revenue/income7483 佣金收入 commission revenue/income7484 出售下脚及废料收入 revenue from sale of scraps7485 存货盘盈 gain on physical inventory7486 存货跌价回升利益 gain from price recovery of inventory7487 坏帐转回利益 gain on reversal of bad debts7488 其它营业外收入-其它 other non-operating revenue- other items75~ 78 营业外费用non-operating expenses751 利息费用 interest expense7511 利息费用interest expense752 投资损失 investment loss7521 权益法认列之投资损失 investment loss recog- nized under equity method7523 短期投资未实现跌价损失 unrealized loss on reduction of short-term investments to market753 兑换损失 foreign exchange loss7531 兑换损失foreign exchange loss754 处分投资损失 loss on disposal of investments7541 处分投资损失 loss on disposal of investments755 处分资产损失 loss on disposal of assets7551 处分资产损失 loss on disposal of assets788 其它营业外费用 other non-operating expenses7881 停工损失 loss on work stoppages7882 灾害损失 casualty loss7885 存货盘损loss on physical inventory7886 存货跌价及呆滞损失loss for market price decline and obsolete and slow-moving inventories7888 其它营业外费用-其它other non-operating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit)811 所得税费用(或利益) income tax expense (or benefit)8111 所得税费用(或利益)income tax expense ( or benefit)9 非经常营业损益nonrecurring gain or loss91 停业部门损益gain(loss) from discontinued operations911 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segments9111 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segment912 停业部门损益-处分损益 gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益 gain(loss) from disposal of discontinued segment92 非常损益extraordinary gain or loss921 非常损益 extraordinary gain or loss9211 非常损益extraordinary gain or loss93 会计原则变动累积影响数cumulative effect of changes in accounting principles 931 会计原则变动累积影响数 cumulative effect of changes in accounting principles 9311 会计原则变动累积影响数 cumulative effect of changes in accounting principles 94 少数股权净利minority interest income941 少数股权净利 minority interest income9411 少数股权净利minority interest income2016年最新会计科目表2016-03-19 ACCA收藏,稍后阅读点击上方"ACCA"免费订阅一、资产类顺序号编号会计科目名称会计科目适用范围1 1001 库存现金2 1002 银行存款3 1003 存放中央银行款项银行专用4 1011 存放同业银行专用5 1015 其它货币基金6 1021 结算备付金证券专用7 1031 存出保证金金融共用8 1051 拆出资金金融共用9 1101 交易性金融资产10 1111 买入返售金融资产金融共用11 1121 应收票据12 1122 应收帐款13 1123 预付帐款14 1131 应收股利15 1132 应收利息16 1211 应收保护储金保险专用17 1221 应收代位追偿款保险专用18 1222 应收分保帐款保险专用19 1223 应收分保未到期责任准备金保险专用20 1224 应收分保保险责任准备金保险专用21 1231 其它应收款22 1241 坏帐准备23 1251 贴现资产银行专用24 1301 贷款银行和保险共用25 1302 贷款损失准备银行和保险共用26 1311 代理兑付证券银行和保险共用27 1321 代理业务资产28 1401 材料采购29 1402 在途物资30 1403 原材料31 1404 材料成本差异32 1406 库存商品33 1407 发出商品34 1410 商品进销差价35 1411 委托加工物资36 1412 包装物及低值易耗品37 1421 消耗性物物资产农业专用38 1431 周转材料建造承包商专用39 1441 贵金属银行专用40 1442 抵债资产金融共用41 1451 损余物资保险专用42 1461 存货跌价准备43 1501 待摊费用44 1511 独立帐户资产保险专用45 1521 持有至到期投资46 1522 持有至到期投资减值准备47 1523 可供出售金融资产48 1524 长期股权投资49 1525 长期股权投资减值准备50 1526 投资性房地产51 1531 长期应收款52 1541 未实现融资收益53 1551 存出资本保证金保险专用54 1601 固定资产55 1602 累计折旧56 1603 固定资产减值准备57 1604 在建工程58 1605 工程物资59 1606 固定资产清理60 1611 融资租赁资产租赁专用61 1612 未担保余值租赁专用62 1621 生产性生物资产农业专用63 1622 生产性生物资产累计折旧农业专用64 1623 公益性生物资产农业专用65 1631 油气资产石油天然气开采专用66 1632 累计折耗石油天然气开采专用67 1701 无形资产68 1702 累计摊销69 1703 无形资产减值准备70 1711 商誉71 1801 长期待摊费用72 1811 递延所得资产73 1901 待处理财产损益二、负债类顺序号编号会计科目名称会计科目适用范围74 2001 短期借款75 2002 存入保证金金融共用76 2003 拆入资金金融共用77 2004 向中央银行借款银行专用78 2011 同业存放银行专用79 2012 吸收存款银行专用80 2021 贴现负债银行专用81 2101 交易性金融负债82 2111 专出回购金融资产款金融共用83 2201 应付票据84 2202 应付帐款85 2205 预收帐款86 2211 应付职工薪酬87 2221 应交税费88 2231 应付股利89 2232 应付利息90 2241 其他应付款91 2251 应付保户红利保险专用92 2261 应付分保帐款保险专用93 2311 代理买卖证券款证券专用94 2312 代理承销证券款证券和银行共用95 2313 代理兑付证券款证券和银行共用96 2314 代理业务负债97 2401 预提费用98 2411 预计负债99 2501 递延收益100 2601 长期借款101 2602 长期债券102 2701 未到期责任准备金保险专用103 2702 保险责任准备金保险专用104 2711 保户储金保险专用105 2721 独立帐户负债保险专用106 2801 长期应付款107 2802 未确认融资费用108 2811 专项应付款109 2901 递延所得税负债三、共同类顺序号编号会计科目名称会计科目适用范围110 3001 清算资金往来银行专用111 3002 外汇买卖金融共用112 3101 衍生工具113 3201 套期工具114 3202 被套期项目四、所有者权益类顺序号编号会计科目名称会计科目适用范围115 4001 实收资本116 4002 资本公积117 4101 盈余公积118 4102 一般风险准备金融共用119 4103 本年利润119120 4104 利润分配120121 4201 库存股121五、成本类顺序号编号会计科目名称会计科目适用范围122 5001 生产成本123 5101 制造费用124 5201 劳务成本125 5301 研发支出126 5401 工程施工建造承包商专用127 5402 工程结算建造承包商专用128 5403 机械作业建造承包商专用六、损益类顺序号编号会计科目名称会计科目适用范围129 6001 主营业务收入130 6011 利息收入金融共用131 6021 手续费收入金融共用132 6031 保费收入保险专用133 6032 分保费收入保险专用135 6041 租赁收入租赁专用135 6051 其他业务收入136 6061 汇兑损益金融专用137 6101 公允价值变动损益138 6111 投资收益139 6201 摊回保险责任准备金保险专用140 6202 摊回赔付支出保险专用141 6203 摊回分保费用保险专用142 6301 营业外收入143 6401 主营业务成本144 6402 其它业务成本145 6405 营业税金及附加146 6411 利息支出金融共用147 6421 手续费支出金融共用148 6501 提取未到期责任准备金保险专用149 6502 撮保险责任准备金保险专用150 6511 赔付支出保险专用151 6521 保户红利支出保险专用152 6531 退保金保险专用153 6541 分出保费保险专用154 6542 分保费用保险专用155 6601 销售费用156 6602 管理费用157 6603 财务费用158 6604 勘探费用159 6701 资产减值损失160 6711 营业外支出161 6801 所得税162 6901 以前年度损益调整。

2016年ACCA考试知识点:公司法与商...

2016年ACCA考试知识点:公司法与商法(3)Chapter 3 Legal reasoning1 Doctrine of judicial precedent1.1 Common law and equity are a body of judge洠愀搀攀 laws contained in decisions of the courts called judgements.1.2 Judge – made law or case law is whereby judges follow the decisions of other judges. The doctrine of precedent is sometimes referred to as 'stare decisis': let the decision stand.1.3 For case law to be workable as a source of law it needs to achieve consistency. Various 'rules' have therefore developed to achieve this aim.1.4 ‘Rules’:1.4.1 Only statements of law made by judges can form precedent. In turn these statements must be divided up into ratio decidendi (the reason for the decision) and obiter dicta (other comments).Only the ratio decidendi forms the basis of precedent as it is this reasoning which is vital to his decision. Obiter dicta are statements of general law (or hypothetical situations) which are not necessary for the decision in the case and hence are not binding.1.4.2 As the ratio decidendi of a case stems from specific facts if a precedent is to be followed in a subsequent case the facts of that case must be sufficiently similar.1.4.3 The precedent must have been set by a court capable of creating precedent and not have been overruled.1.5 Hierarchy of the courts:(a) House of Lords – binds all lower courts but not itself (exceptional cases)(b) Court of Appeal – binds all lower courts and itself(c) High CourtJudge sitting alone – binds all lower courts not divisional courtsJudges sitting together – binds all lower courts and divisional courts(d) CrownMagistrates – bind no-one at allCounty1.6 A precedent ceases to be binding if:(i) It has been overruled by statute or EU law or by a higher court.(ii) It can be distinguished on the facts i.e. if the material facts are not the same.1.7 Advant。

ACCA资产类中英文词汇表

ACCA资产类中英文词汇表流动资产Current assets货币资金Cash and cash equivalents库存现金Cash on hand银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier's cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits交易性金融资产Financial assets held for trading短期投资Short-term investments股票Short-term investments-stock债券Short-term investments-corporate bonds基金Short-term investments-corporate funds其他Short-term investments-other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance、应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves资产减值损失Asset impairment loss预付账款Advance payment应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods在途物资Materials in transport库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process-outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis 存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves 股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor's rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves 机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks,Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income长期待摊费用Long-term deferred and prepaid expenses待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income待处理固定资产损溢Wait deal fixed assets loss or income。

商英名词解释

1.sole proprietorship: (个人企业)A business that is established, owned, operated and often financed by oneperson.2.partnership: (合伙企业)An association of two or more individuals who agree to operate a business together for profit.3.corporation: (公司)A legal entity with an existence and life separate from its owner, whotherefore are not personally liable for the entity’s debts. A corporation is chartered by the state in which it is formed and can own property, enter into contracts, sue and be sued, and engage in business operations under the terms of its charter.4.franchising: (特许企业)A form of business organization based on a business arrangement between afranchisor, which supplies the product concept, and the franchisee, who sells the goods or services of the franchisor in a certain geographic area .5.trade credit: (商业信用)The extension for credit by the seller to the buyer between the time the buyer receives the goods or services and when it pays for them.6.factoring: (贴现)A form of short-term financing in which a firm sells its accounts receivableoutright at a discount to a factor .7.bond: (债券)Long-term debt obligations (liabilities) issued by corporations and government.8.preferred stock: (优先股)An equity security for which the dividend amount is set at the time the stock is issued.9.demand deposit: (活期存款)Money kept in checking accounts that can be withdrawn by depositors on demand.10.time deposit: (定期存款)Deposit at a bank or other financial institution that pay interest but cannot be withdrawn on demand.11.central bank: (中央银行)Government institutions with authority over the size and growth of the national monetary stock . Central banks frequently regulate commercial banks and usually act as the government’s fiscal agent.12.discount rate: (贴现率)The interest rate that central bank charges its member banks.13.reserve requirement: (准备金要求)It requires banks that are members of the central bank to hold some of their deposits in cash in their vaults of in an account at a district bank.14.balance sheet: (资产负债表)Financial statement that shows assets, liabilities, and owner’s equity on a given date; also known as a statement of financial position .15.income statement: (损益表)Financial statement showing how a business’s revenues compare with expenses for a given period of time .16.assets: (资产)Physical objects and intangible rights that have economic value to the owner .17.liabilities: (负债)Debts or obligations that are owned to individuals or organizations .18.owners’ equity: (所有者权益)Portion of a company’s assets that belongs to the owners after obligations to all creditors have been met.19.working capital: (营运资本)Current assets minus current liabilities.20.current ratio: (流动比率)Measure of a company’s short-term liquidity, calculated by dividing current assets by current liabilities.Current Ratio = Current Assets/Current Liabilities21.quick ratio: (速动比率)Measure of a company’s short-term liquidity, calculated by adding cash, marketable securities, and receivables, and then dividing that sum by currentliabilities; also known as the acid-test ratio.Quick Ratio = Cash + Marketable Securities + Receivables/Current Liabilities22.return on investment: (投资收益率)Profit from an investment as a percentage of the amount invested.23.earnings per share: (每股收益)Measure of a company’s profitability for each share of outstanding stock, calculated by dividing net income after taxes by shares of common stock outstanding.Earnings per Share = Net Income after Taxes/Number of Average Shares Outstanding 24.price-earnings (P/E) ratio: (市盈率)The current market price of a stock divided by its annual earnings per share.P/E Ratio = Market Price per Share of Common Stock/Earning per Share of Common Stock25.dividend yield: (收益率)A measure of the return on an investment calculated by dividing dividendsper year by current share price.Dividend Yield = Dividends per Share of Common Stock/Market Price per Share of Common Stock 26.primary market: (一级市场)First buying opportunity for new security; the first opportunity that investors have to buy a newly issued security. After the first purchases, subsequent trading is in the secondary market.27.secondary market: (二级市场)The market where investors buy securities from other investors rather than from an issuing company. All stock exchanges are part of the secondary market.28.over-the-counter market: (场外交易市场)A sophisticated telecommunications network that links dealers throughoutthe United States and enables them to trade securities.29.money market: (货币市场)A financial market involving institutions that deal with securities with a lifeof less than one year.30.capital market: (资本市场)A financial market involving institutions that deal with securities with a lifeof more than one year.31.mercantilism: (重商主义)An economic philosophy based on the belief that (1) a nation’s wealth depends on accumulated treasure, usually gold, and (2) to increase wealth, government policies should promote exports and discourage imports.32.absolute advantage: (绝对优势)Nation’s ability to produce a particular product with fewer resources ( per unit of output ) than any other nation.parative advantage: (相对优势)Nation’s ability to produce an item more efficiently than other nations because of its natural and human resources.34.opportunity cost: (机会成本)Value of using a resource; measured in terms of the value of the next best alternative for using that resource.。

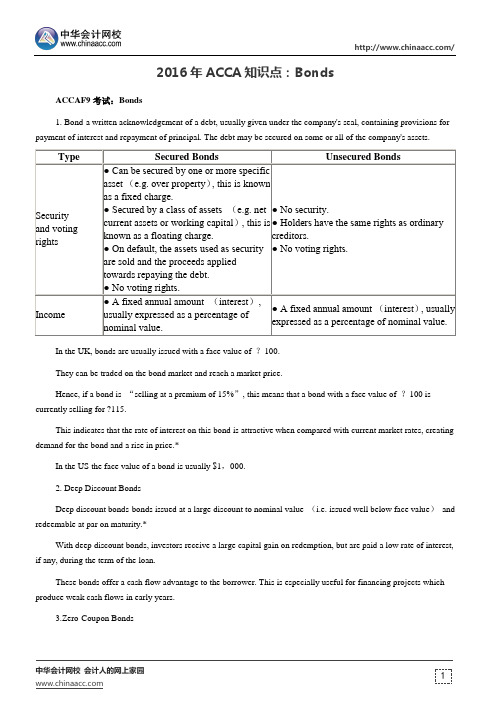

2016年ACCA知识点:Bonds

2016年ACCA知识点:BondsACCAF9考试:Bonds1. Bond-a written acknowledgement of a debt, usually given under the company's seal, containing provisions for payment of interest and repayment of principal. The debt may be secured on some or all of the company's assets.In the UK, bonds are usually issued with a face value of ?100.They can be traded on the bond market and reach a market price.Hence, if a bond is “selling at a premium of 15%”, this means that a bond with a face value of ?100 is currently selling for ?115.This indicates that the rate of interest on this bond is attractive when compared with current market rates, creating demand for the bond and a rise in price.*In the US the face value of a bond is usually $1,000.2. Deep Discount BondsDeep discount bonds-bonds issued at a large discount to nominal value (i.e. issued well below face value)and redeemable at par on maturity.*With deep discount bonds, investors receive a large capital gain on redemption, but are paid a low rate of interest, if any, during the term of the loan.These bonds offer a cash flow advantage to the borrower. This is especially useful for financing projects which produce weak cash flows in early years.3.Zero-Coupon BondsZero-coupon bonds-bonds issued at a discount to face value and which pay zero annual interest. Zero-coupon bonds have the following advantages:The issuing company pays no interest and the only cash payout is at the bonds' maturity.Investors gain from the difference between issue and redemption price.。

2016年ACCA F9《财务管理》重要知识点讲解(4)

2016年ACCA F9《财务管理》重要知识点讲解(4)Effects of taxation on project appraisalInvestment in capital assets has taxation implications, which should be included in the analysis. To ignore the effect of taxation could affect the quality of the decision, which is consequently made about an investment opportunity. If the resulting project from the appraisal is profitable then taxation becomes payable on these profits thus reducing the net cash inflows by the amounts of tax payable. Capital allowances are given by the Inland Revenue at about 25% on a reducing balance basis over the life of the project. Capital allowances reduce the amount of tax which becomes payable. If the project has a terminal value at the end of its useful life, it will be necessary to establish whether this gives rise to a balancing allowance or a balancing charge. Net cash inflows are used in pay back, net present value and Internal rate of return methods. If the entity will not be in a tax-paying position during the entire life of the project then it is known as tax exhausted and tax can be ignored but this situation is most unlikely to occur.Now that we have looked at these possible areas of complication let us look at a fictitious company we shall call Samco Plc.CaseSamco Plc is a manufacturer of electric drills. The company has just developed two new models of electric drills. Model 1 is called Automatic and model 2 is called Super. Senior managers have resolved that if production were to commence in making the automatic model, 200,000 drills per annum will be produced and sold over the next five years at a price of £200 per drill, whereas if production were to commence with the super model, 150,000 drills per annum will be sold over the next seven years at a price of £140 per drill. Budgeted operating costs of each of the two models at today?s prices are as stated below:Automatic model£Direct material70Direct Labour20Variable overheadFixed production overheadSelling, Distribution etc20Net Cash inflow per unit = (£200 ? £140) = £60Super model£Direct material20Direct labour12Variable overhead15Fixed production overheadSelling, distribution, etc.Net Cash inflow per unit = (£140 ? 70) = £70Net present value to infinityAutomatic modelNPV μ= NPV of the project/PV of annuity of appropriate years and rateDiscount Rate= £17,130,000/3.7360.155= £29,581,405Super model= £18,920,000/3.6050.20= £26,241,332Having calculated the net present values of the two projects to infinity clearly one can see that the automatic model has a net present value of about £29.5m whereas super has a lower net present value of about £26.2m. This means that the automatic model will give a higher return to the shareholders of Samco plc. This is the model the Board should manufacture and sell to their customers, because shareholders? wealth will be maximised by taking this course of action.ConclusionThe main objective of this second article in the area of project appraisal was to demonstrate to readers that cases might not necessarily be straightforward. Aspects such as inflation, taxation and unequal life spans must be understood in order that candidates can competently answer questions requiring an understanding of these further aspects. The scenario in Samco plc should be carefully followed ensuring that you understand how the author has used the available information to answer the question.by John Richard Edwards01 Oct 2000The merits of cash based financial reporting ? for example, it is based principally on facts rather than problematic accounting measurements ? have been known for many years. However, it was not until 1990 (revised 1996) that the Accounting Standards Board made the publication of Cash Flow Statements (FRS 1) a standard requirement for UK companies. FRS 1 tells us that the ?cash flow statement in conjunction with a profit and loss account and balance sheet provides information on financial position and performance as well as liquidity, solvency and financial adaptability?. Wise words, but what do they mean?The usefulness of financial statements is enhanced by an examination of the relationship between them; also by comparisons with previous time periods, other entities and expected performance. Value can be further added through the calculation and interpretation of accounting ratios. An examination of accounting textbooks and the pages of accounting periodicals reveals an enthusiasm for rehearsing the potential of ?accounting ratios? demonstrated through calculations of the net profit margin, return on capital employed, current ratio and a host of other ?traditional? measures based on the contents of the profit and loss and balance sheet. But what about the cash flow statement? We have seen that its publication was required by the ASB in order to improve the informative value of published financial information. Indeed, some say it is the most important financial statement. One based on ?hard facts? which has helped prevent financial machinations such as those that are believed to have occurred at companies such as Polly Peck in the 1980s.The lack of attention to cash flow-based ratios in accounting textbooks is particularly surprising given their acknowledged role in credit rating assessments and in the prediction of corporate failure. In these and other contexts, the traditional ratios suffer from the same defect as the financial statements (the profit and loss account and balance sheet) on which they are based. Such ratios are the result of comparing figures which have been computed using accounting conventions and ?guestimations?.Given the difficulty of deciding the length of the period over which a fixed asset should be written off, whether the tests which justify the capitalisation of development expenditure have been satisfied, the amount of the provision to be made for claims under a manufacturer?s twelve month guarantee (to give just a few examples), ratios based on such figures are also bound to have limited economic significance. This is not to suggest that the traditional ratios are irrelevant. Clearly this is not so, as they reveal important relationships and trends that are not apparent from the examination of individual figures appearing in the accounts. However, given the fact that cash flow ratios contain at least one element that is factual (the numerator, the denominator or both), their lack of prominence in the existing literature is puzzling.Some recognition of cash flow ratiosThe importance of cash flow ratios was dramatically demonstrated, early on, by W. H. Beaver whose 1966 study showed that the most effective predictor of corporate failure was the ratio of cash flow to total debt. Indeed, one of his most surprising findings was that the current ratio proved to be one of the least useful ratios in predicting impending collapse. The importance of cash as an indicator of continuing financial health should not be surprising in view of its crucial role within the business. Colourfully described as a company?s ?life-blood?, a strong cash flow will enable a business to recover from temporary financial problems whereas future negative cash flow will cause even an apparently sound enterprise to move towards liquidation. Expressing the importance of cash differently: a company which descends into aloss-making position often succeeds in making a comeback; one which runs out of cash is unlikely to have a second chance.Ratios which link the cash flow statement with the two other principal financial statementsCash flow from operations to current liabilitiesCash flow from operations to current liabilities= Net cash flow from operating activities x 100Average current liabilitiesWhere:Net cash flow from operating activities is taken directly from the cash flow statement published to comply with FRS 1. Average current liabilities are computed from the opening and closing balance sheet.This ratio examines the liquidity of the company by providing a measure of the extent to which current liabilities are covered by cash flowing into the business from normal operating activities. The ratio is thought to possess some advantage over balance sheet-based ratios such as the liquidity ratio as a measure of short-term solvency. This is because balance sheet ratios are based on a static positional statement(the ?instantaneous financial photograph?) and are therefore subject to manipulation by, for example, running down stock immediately prior to the year end and not replacing it until the next accounting period. Balance sheet based ratios may alternatively be affected by unusual events which cause particular items to be abnormally large or small. In either case, the resulting ratios will not reflect normal conditions.Cash recovery rateCash recovery rate (CRR) =Cash flow from operations x 100Average gross assetsWhere:Cash flow from operations is made up of ?net cash flow from operating activities? together with any proceeds from the disposal of long-term assets. Gross assets is the average gross value of the entity?s assets.Assets are required to generate a return which is ultimately, if not immediately, in the form of cash. The CRR is, therefore, a measure of the rate at which the company recovers its investment in fixed assets. The quicker the recovery period, the lower the risk. You may have noticed that the CRR is thus the reciprocal of the pay back period used for capital project appraisal purposes assuming projects have equal (or roughly equal) annual cash flows.Cash flow per shareCash flow per share =Cash flowWeighted average no. of sharesRatios which link the cash flow statement with the two other principal financial statementsCash flow from operations to current liabilitiesCash flow from operations to current liabilities= Net cash flow from operating activities x 100Average current liabilitiesWhere:Net cash flow from operating activities is taken directly from the cash flow statement published to comply with FRS 1. Average current liabilities are computed from the opening and closing balance sheet.This ratio examines the liquidity of the company by providing a measure of the extent to which current liabilities are covered by cash flowing into the business from normal operating activities. The ratio is thought to possess some advantage over balance sheet-based ratios such as the liquidity ratio as a measure of short-term solvency. This is because balance sheet ratios are based on a static positional statement(the ?instantaneous financial photograph?) and are therefore subject to manipulation by, for example, running down stock immediately prior to the year end and not replacing it until the next accounting period. Balance sheet based ratios may alternatively be affected by unusual events which cause particular items to be abnormally large or small. In either case, the resulting ratios will not reflect normal conditions.Cash recovery rateCash recovery rate (CRR) =Cash flow from operations x 100Average gross assetsWhere:Cash flow from operations is made up of ?net cash flow from operating activities? together with any proceeds from the disposal of long-term assets. Gross assets is the average gross value of the entity?s assets.Assets are required to generate a return which is ultimately, if not immediately, in the form of cash. The CRR is, therefore, a measure of the rate at which the company recovers its investment in fixed assets. The quicker the recovery period, the lower the risk. You may have noticed that the CRR is thus the reciprocal of the pay back period used for capital project appraisal purposes assuming projects have equal (or roughly equal) annual cash flows.。

2016年ACCA F9《财务管理》重要知识点讲解(1)

2016年ACCA F9《财务管理》重要知识点讲解(1)Capital investment appraisal - part 1by Samuel O Idowu01 Aug 2000Organisations operate in a dynamic environment. They must therefore continually make changes in different areas of their operations in order to meet the challenges that the dynamic nature of the environment brings and also in order to survive and prosper. It is believed that continuous change could improve the way things are done, thereby putting the organisation at an advantage over their competitors. Most changes involve capital expenditure, which can invariably involve large sums of money. The expenditure might involve replacing existing fixed assets with something more efficient and up to date or to acquire an entire business.The decision to go ahead with any capital expenditure of a significant amount could necessitate spending a large sum of money. Managers must give careful thought to every step that they need to take before a final decision is made on whether or not to invest money on such a project. Most investments will have one form of return or another. The question to address is whether or not the future returns will be sufficient to justify the sacrifices the investing entity would have to make.The intention of this article is to demonstrate how organisations justify capital investments using different appraisal techniques. It is hoped that the reader will supplement the knowledge gained from it with that gained elsewhere.The article will be of interest to students taking paper 8, Managerial Finance, at the certificate level and also to those taking Paper 9, Information for Control and Decision-Making at the professional level.Basic informationTo appraise an investment project, the appraiser must have information about the following relevant areas:1 Cost of investment project.2 Estimated life ofproject3 Estimated net cash inflows from project.4 Estimated residual value of project at the end of its life if applicable.5 Costofcapital.6 Taxation implications of project.7 Inflation rates and effect on project.Anyone who has had to plan for a future activity/event should understand that the future is never certain. Bearing this in mind, one must try to predict the future by drawing from past experience and using available information either from published statistics or from other sources. Some of the data required about the project would have to be estimated taking into consideration all available information. The accuracy of these estimated data would have a consequential effect on the final result of the decision, as such care must be taken in making these estimates.Methods of investment appraisalWhen the decision-maker has at his/her disposal basic information about the project as stated above, he/she is then ready to use one or more of the four main methods used in appraising investment projects.Payback methodThe payback method is used to determine how long it will take for future cash inflows from the project to equal the initial cost of the project. The method as the name implies establishes the payback period of each project. As the method stands, the shorter the payback period the better. It is often argued that industries where products get outdated quickly such as fashion and computers will prefer to use the payback method. The reason being that it is critical that the initial cost of the project is recovered quickly. In any case, most organisations have a set of standard payback periods for each investment project. They will in most cases compare the payback period from each investment project with the pre-determined payback period. Any project that falls short of the standard payback period will be rejected.Evidence has shown that apart from this fact, managers will prefer to use the method as an initial screening process because it is easy to use and understand by them. One important disadvantage of the method is that it ignores the time value of money. It also ignores profitability of the project but stresses the importance of liquidity. Whether this is an advantage or not will depend on the area of interest to the individual concerned.Accounting Rate of Return (ARR)This method ARR is also referred to by some other names such as Return on Investment (ROI), Return on Capital Employed (ROCE). The most important thing to remember about this method is that it establishes rates of return on projects. There are different ways of determining a rate of return. For the purposes of this article, we will use Average Accounting Profits divided by Average Capital Employed multiplied by 100. That is:Average accounting profitsAPR =Average capital employedWhere:Profits over the life of the projectAverage accounting profits =Life of the projectandInitial cost of project + Scrap valueAverage capital employed =2When there are two or more investment projects, rates of return are compared. A project, which has a higher rate, will be recommended, as this is an indication that it will give a higher return to the investing entity compared with the one with a lower rate.ACCA考试F9财务:报告现金流量折现法Discounted Cash Flow (DCF) methodsThe Net Present Value (NPV) and Internal Rate of Return (IRR) are the two investment appraisal methods under DCF. Let us now describe and comment upon the two methods.Net Present Value (NPV) MethodOf all the investment appraisal methods, NPV is often argued to be the most superior. This is because it takes into account the time value of money. The method assumesthat a pound today is worth more than a pound this time next year. It works under the assumption that if one is owed a pound and the borrower offers a choice of either giving the pound now or in a years time, the more rational option for the lender is to take the pound now. Provided the lender does not keep the pound under his mattress at home, it will be worth more than a pound in a year's time. The reverse is true if the borrower has the option to pay either now or in a year's time, the borrower would choose to pay in the future as the pound he/she pays in the future will be worth less than what he/she would have paid now. It stresses that future cash flows should be expressed in terms of what they are worth now when cash is expended on the project. The present values of these future cash flows can then be compared with what we are spending now on the project. In other words, the NPV is saying that one should compare like with like, which of course is a fair statement. By setting the future cash inflows from the project without discounting them against the initial capital cost, one is not being realistic and fair.When present values of cash outflows and inflows are compared, if the result gives a positive NPV, then the project should be recommended. In a mutually exclusive situation, that is, when you can only undertake one project and not two projects at the same time, if two projects were to give positive NPVs, then the project with the higher NPV is the one to recommend.。

有关ACCA中Bonds债券的概念及基础辅导

有关ACCA中Bonds债券的概念及基础辅导本文由高顿ACCA整理发布,转载请注明出处政府债券政府或政府机构发行的债券,目的是为公共项目募集资金。

DiscountThe market value of a bond which is below its face value.BondAn interest-bearing government or corporate security that obligates the issuer to make specified payments on a specific schedule to the bondholder.债券政府或公司发行的计息证券,要求发行人按照一定的日期向债券持有人支付一定金额。

Face ValueThe principal amount of a bond which is stated on its face and which the issuer is obligated to pay at the date of maturity.票面价值债券的票面价值是票面所列价值,代表发行人在到期日必须支付的金额。

Maturity, Date ofThe date the issuer of a bond is obligated to pay its face value.到期日债券发行人必须支付票面价值的日期。

Bond, MunicipalBond issued by a government or government agency to raise money for public works projects.折价债券的市场价低于票面价值。

PremiumThe market value of a bond which is above its face value.溢价债券的市场价超过票面价值。

Total ReturnReturn on a bond investment including appreciation and dividends.总收益债券投资的收益,包括增值和红利。

2016年ACCA考试词汇总结(一)

2016年ACCA考试词汇总结(一)12月ACCA考试就要到了,为了方便大家更好地复习12月ACCA考试,小编在百度文库定期传一些考试资料,如有需要请关注财萃财经的百度文库。

1、Accelerated Depreciation 加快折旧:任何基于会计或税务原因促使一项资产在较早期以较大金额折旧的折旧原则2、Accident and Health Benefits 意外与健康福利:为员工提供有关疾病、意外受伤或意外死亡的福利。

这些福利包括支付医院及医疗开支以及有关时期的收入。

3、Accounts Receivable (AR)应收账款:客户应付的金额。

拥有应收账款指公司已经出售产品或服务但仍未收取款项4、Accretive Acquisition 具增值作用的收购项目:能提高进行收购公司每股盈利的收购项目5、Acid Test 酸性测试比率:一项严谨的测试,用以衡量一家公司是否拥有足够的短期资产,在无需出售库存的情况下解决其短期负债。

计算方法:(现金+ 应收账款+短期投资)/ 流动负债6、Act of God Bond 天灾债券:保险公司发行的债券,旨在将债券的本金及利息与天然灾害造成的公司损失联系起来7、Active Bond Crowd 活跃债券投资者:在纽约股票交易所内买卖活跃的定息证券8、Active Income 活动收入:来自提供服务所得的收入,包括工资、薪酬、奖金、佣金,以及来自实际参与业务的收入9、Active Investing 积极投资:包含持续买卖行为的投资策略。

主动投资者买入投资,并密切注意其走势,以期把握盈利机会10、Active Management 积极管理:寻求投资回报高于既定基准的投资策略。

acca 知识点总结

acca 知识点总结As a globally recognized accountancy qualification, the Association of Chartered Certified Accountants (ACCA) offers an in-depth understanding of accounting, finance, and management. With its comprehensive syllabus and professional development opportunities, ACCA equips graduates with the knowledge, skills, and values required to build successful careers in the accounting industry. In this knowledge summary, we will explore the key topics covered in the ACCA qualification.Financial AccountingFinancial accounting is a fundamental aspect of the ACCA syllabus. It involves the preparation of financial statements, including the income statement, balance sheet, and cash flow statement. Candidates learn about the principles of double-entry accounting, accruals, and prepayments, as well as the accounting treatment of non-current assets, inventory, and financial instruments. They also gain an understanding of accounting regulations and standards, such as International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP).Management AccountingManagement accounting focuses on providing information to support decision-making within organizations. Candidates learn about cost classification, cost behavior, and cost-volume-profit analysis. They also study budgeting, variance analysis, and performance measurement techniques. In addition, they explore the role of management accounting in strategic planning, including the use of relevant costing and capital investment appraisal methods.Corporate and Business LawThis area of study covers the legal framework within which businesses operate. Candidates learn about contract law, company law, and employment law, as well as the regulations governing corporate governance and ethics. They also gain an understanding of the legal responsibilities of directors, shareholders, and creditors, and the implications of insolvency and liquidation.TaxationTaxation is a core component of the ACCA qualification, covering both personal and corporate taxes. Candidates learn about income tax, capital gains tax, and inheritance tax, as well as value-added tax and corporation tax. They also study the principles of tax planning, compliance, and ethical considerations in tax practice.Audit and AssuranceAuditing is a vital aspect of the accounting profession, ensuring the accuracy and reliability of financial information. Candidates learn about the principles of auditing, including theplanning, execution, and reporting phases. They also gain an understanding of internal control systems, risk assessment, and the ethical responsibilities of auditors.Financial ManagementFinancial management involves the strategic allocation of resources to maximize the wealth of shareholders. Candidates learn about the principles of investment appraisal, working capital management, and the cost of capital. They also study the theories of capital structure, dividend policy, and risk management, as well as the use of financial derivatives and hedging strategies.Performance ManagementPerformance management focuses on the measurement and evaluation of organizational performance. Candidates learn about key performance indicators (KPIs), balanced scorecards, and performance measurement frameworks. They also study the principles ofbehavioral aspects of performance management, including motivation, leadership, and team dynamics.Strategic Business ReportingStrategic business reporting involves the communication of financial and non-financial information to stakeholders. Candidates learn about the preparation and interpretation of financial statements, as well as the reporting requirements for sustainability and integrated reporting. They also gain an understanding of the ethical considerations in financial reporting and the implications of international developments in corporate reporting. Strategic Business LeadershipStrategic business leadership encompasses the skills required to lead and manage organizations effectively. Candidates learn about strategic management, including the development of corporate mission, vision, and values. They also study the principles of corporate governance, risk management, and business ethics, as well as the strategies for organizational change and transformation.Professional EthicsProfessional ethics is a fundamental aspect of the ACCA qualification, emphasizing integrity, objectivity, and ethical behavior in the accounting profession. Candidates learn about the fundamental principles of ethical behavior, as well as the application of ethical reasoning to real-world scenarios. They also gain an understanding of the ethical standards set by professional accounting bodies and the implications of ethical violations.In conclusion, the ACCA qualification provides a comprehensive understanding of accounting, finance, and management, preparing graduates for successful careers in the accounting industry. With its focus on technical knowledge, professional skills, and ethicalvalues, ACCA equips candidates with the expertise required to excel in the global business environment. Whether pursuing careers in public practice, industry, or the public sector, ACCA graduates are well-prepared to contribute to the success and sustainability of organizations worldwide.。

acca会计英文词汇

acca会计英文词汇Here are some common accounting terms in English:1. Account: A record of financial transactions for a specific category or entity.2. Ledger: A book or computerized system used to record and summarize financial transactions.3. Balance sheet: A financial statement that provides a snapshot ofa company's assets, liabilities, and shareholders' equity at a specific point in time.4. Income statement: A financial statement that shows a company's revenues, expenses, and net income over a specific period of time.5. Cash flow statement: A financial statement that provides information about the cash inflows and outflows of a company during a specific period.6. Assets: Resources that are owned or controlled by a company, such as cash, accounts receivable, and property.7. Liabilities: Obligations or debts owed by a company, such as accounts payable, loans, and bonds.8. Equity: The residual interest in the assets of a company after deducting liabilities.9. Revenue: The income generated by a company through its primary operations, such as sales of goods or services.10. Expenses: The costs incurred by a company in order to generate revenue, such as salaries, rent, and utilities.11. Depreciation: The systematic allocation of the cost of an asset over its useful life.12. Audit: An examination and verification of financial records and statements by an independent third party to ensure accuracy and compliance with relevant laws and regulations.13. Taxation: The process of calculating and paying taxes owed to the government.14. Financial ratios: Numerical relationships between different financial data points that are used to analyze and assess a company's financial performance.15. Internal controls: Policies and procedures implemented by a company to ensure the accuracy, reliability, and integrity of its financial reporting.16. Cost of goods sold: The direct costs incurred by a company in producing or acquiring the goods or services it sells.17. Accruals: Revenues or expenses that have been earned or incurred but have not yet been recorded in the accounts.18. Profit margin: The percentage of each sales dollar that is retained as profit after deducting all costs and expenses.19. Cash discount: A reduction in the invoice amount offered by a seller to a buyer who pays within a specified time frame.20. Amortization: The gradual reduction of an intangible asset's value over time.。

金融学基础ACCA必备知识点解析

金融学基础ACCA必备知识点解析金融学是ACCA(特许公认会计师协会)考试中的重要科目之一,对于考生来说,掌握金融学的基础知识点是非常关键的。

本文将从理论、工具和实践三个方面解析金融学基础的ACCA必备知识点。

一、理论知识点解析1. 时间价值货币概念时间价值货币概念是金融学中的一个基础概念,指的是金钱在不同时间点的价值不同。

它涉及到贴现与复利的计算,通过现值和未来值的比较,帮助人们做出金融决策。

2. 资本预算技术资本预算技术是一种评估和选择投资项目的方法,它包括净现值、内部收益率和投资回收期等指标。

这些技术可以帮助企业决定是否投资某个项目,并进行风险评估和资金分配。

3. 多元资本结构理论多元资本结构理论是研究公司如何选择不同资本来源的理论,它涉及到资本结构的权益与债务的组合比例。

考生需要了解不同资本结构对公司价值、成本和风险的影响。

二、工具知识点解析1. 利率计算利率计算是金融学中的一项基本技能,包括简单利率和复合利率的计算方法。

考生需要熟练掌握计算利率的公式和使用计算器或电子表格进行计算的技巧。

2. 资本成本计算资本成本计算是评估资本投资项目的关键工具,它涉及到权益成本和债务成本的计算。

考生需要了解权益成本的计算方法、债务成本的计算方法以及加权平均资本成本的计算方法。

3. 理论价格计算理论价格计算是金融学中的一项重要技能,用于估计金融资产的价值。

考生需要了解期权定价、债券定价和股票定价等不同类型金融资产的计算方法。

三、实践知识点解析1. 财务管理财务管理是企业金融学的核心内容,考生需要了解财务分析、资金预测、资本预算和风险管理等相关知识。

财务管理的目的是最大化股东财富,优化企业的财务决策。

2. 投资组合投资组合是指将不同的金融资产按照一定比例组合在一起,以达到风险分散和收益最大化的目标。

考生需要了解不同类型资产的风险和收益特征,以及如何构建有效的投资组合。

3. 市场分析市场分析是金融学中的一项基本技能,用于预测金融市场的发展趋势。

2016年ACCA考试知识点:公司法与商... (1)

2016年ACCA考试知识点:公司法与商法(2) Sources of English law1 Sources of law(a) Common law(b) Equity(c) Statute (legislation) including delegated legislation(d) European Union Law2 Common law and equity2.1 This is a system of law based upon decided cases. Legal rules (initially created by judges when hearing cases) are followed by judges in subsequent like cases.It developed after the Norman Conquest.2.2 Initially only common law rules were derived from cases. The aim of common law was certainty. However various problems within the common law system resulted in the development of another kind of case law called equity. Equity sought to address some of the problems contained in the common law system. Its aim is fairness.2.3 Amongst the common law problems were inadequate remedies, a failure to recognise trusts and a reluctance to allow new causes of action to develop.2.4 At first common law and equity operated as two distinct systems of law with their own independent court and judges. Given that equity is based on fairness however it was eventually decided that in the event of conflict between the two systems equity should prevail.2.5 The two systems have now been merged together. In practice therefore, if you seek a remedy in the courts today, the court will look first to the common law. If the common law can deal with your problem adequately there will be no recourse to equity. If the common law is unable to deal adequately with the problem the court will look to equity.2.6 Equity is therefore referred to as to a supplement to the common law.2.7 The operation of equity is entirely discretionary whereas common law applies automatically.2.8 Maxims:'He who comes to equity must come with clean hands.' 'Equity does not suffer a wrong to be without a remedy.' 3 Statute (primary law)3.1 Acts of Parliament:Created by parliament. All ne。

ACCA中文知识点

ACCA中文知识点ACCA(特许公认会计师协会)是全球领先的会计师组织之一,其认证被广泛认可并被许多国家和地区的会计师所追求。

为了获得ACCA资格,学生需要通过一系列考试,其中包括一些重要的知识点。

本文将介绍一些ACCA中文知识点,帮助读者更好地理解和掌握这些内容。

一、财务报表财务报表是企业向外界展示其财务状况和经营情况的主要工具。

ACCA中文知识点中涉及到的财务报表包括资产负债表、利润表和现金流量表。

资产负债表展示了企业在特定日期的资产、负债和所有者权益;利润表展示了企业在一定期间内的收入、成本和利润;现金流量表展示了企业在一定期间内的现金流量情况。

二、管理会计管理会计是指为企业管理层提供决策支持和信息的会计领域。

ACCA中文知识点中涉及到的管理会计内容包括成本核算、预算管理和绩效评估等。

成本核算是指对企业成本的计算和分析,帮助企业了解和控制成本情况;预算管理是指制定和执行预算计划,帮助企业控制和管理财务资源;绩效评估是指对企业绩效进行评估和分析,帮助企业改进经营和决策。

三、审计与认证审计是指对企业财务报表和财务信息的审查和评估,以确定其是否真实、准确和合规。

ACCA中文知识点中包括了审计的基本概念、流程和方法。

此外,ACCA还涉及到认证领域,如企业估值、财务风险评估和内部控制等。

四、税务与法规税务与法规是ACCA中文知识点中不可或缺的内容。

税务知识包括个人所得税、企业所得税和增值税等,帮助企业合规缴税;法规知识包括公司法、劳动法和证券法等,帮助企业理解和遵守相关法律法规。

五、商业伦理商业伦理是ACCA中文知识点中的一个重要内容,强调了会计师职业道德和行为准则。

ACCA要求会员在从事会计工作时具备诚信、保密和专业行为等素养,以确保公众利益和企业利益的最大化。

总结起来,ACCA中文知识点涉及了财务报表、管理会计、审计与认证、税务与法规以及商业伦理等内容。

掌握这些知识点对于想要在会计领域取得成功的人来说是非常重要的。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2016年ACCA知识点:Bonds ACCAF9考试:Bonds

1. Bond-a written acknowledgement of a debt, usually given under the company's seal, con ta ining provisions for payment of interest and repayment of principal. The debt may be secured on some or all of the company's assets.

In the UK, bonds are usually issued with a face value of ?100.

They can be traded on the bond market and reach a market price.

Hence, if a bond is “selling at a premium of 15%”, this means that a bond with a face value of ?100 is currently selling for ?115.

This indicates that the rate of interest on this bond is attractive when compared with current market rates, creating demand for the bond and a rise in price.*

In the US the face value of a bond is usually $1,000.

2. Deep Discount Bonds

Deep discount bonds-bonds issued at a large discount to nominal value (i.e. issued well below face value)and redeemable at par on maturity.*

With deep discount bonds, investors receive a large capital gain on redemption, but are paid a low rate of interest, if any, during the term of the loan.

These bonds offer a cash flow advantage to the borrower. This is espe cia lly useful for financing projects which produce weak cash flows in early years.

3.Zero-Coupon Bonds

Zero-coupon bonds-bonds issued at a discount to face value and which pay zero annual interest. Zero-coupon bonds have the following advantages:

The issuing company pays no interest and the only cash payout is at the bonds' maturity. Investors gain from the difference between issue and redemption price.。