2015年ACCA考试《F9财务管理》辅导资料(17)

《ACCA考试之财务管理 FINANCIAL MANAGEMENT》课件PPT 4 Working Capital

Cash operating cycle= stock holding period + debtors’ collections period – creditors’ payment period.

Capital assets

Long-term debt and equity

11

1.1 Working capital characteristic of different business

Holding inventory Taking time to pay suppliers and other account payable Allowing customers time to pay

> current liabilities

Current liabilities

Capital assets

Long-term debt and equity

9

NWC: An operational focus

Current assets = current liabilities

Current assets

15

3 Role of working capital management

Fast forward

A business needs to have clear policies for management of each component of working capital.

《ACCA考试之财务管理 FINANCIAL MANAGEMENT》课件PPT 8 Investment appraisal using DCF methods

1 Discounted cash flows

Two important points about DCF are as follows:

DCF analysis is based on future cash flows, not accounting profits or losses. The timing of cash flows is taken into account by discounting them to a ‘present value’.

6

ቤተ መጻሕፍቲ ባይዱ

1.1 Compounding

Key terms

A sum money invested or borrowed is known as principal. When money is invested it earns interest, similarly when money is borrowed, interest is payable. Interest on an investment can be calculated as either simple interest or compound interest.

FVn P0 (1 i n)

Present value The current value of a future amount of money, or a series of payments, evaluated at a given interest rate.

3

Exam guide

Applying the various investment appraisal techniques Discussing theirs relative merits

2015年ACCA考试《F7财务报告》重要讲义(10)

2015年ACCA考试《F7财务报告》重要讲义(10)本文由高顿ACCA整理发布,转载请注明出处History Question AnalysisQuestion 1 (Q3/December 2003)IAS 37’ Provisions,Contingent Liabilities and Contingent Assets’ was issued in 1998. The Standard sets out the rinciples of accounting for these items and clarifies when provisions should and should not be made. Prior to its issue,the inappropriate use of provisions had been an area where companies had been accused of manipulating the financial statements and of creative accounting.Required:(a) Describe the nature of provisions and the accounting requirements for them contained in IAS 37.(6 marks)(b) Explain why there is a need for an accounting standard in this area. Illustrate your answer with three practical examples of how the standard addresses controversial issues.(6 marks)(a) IAS 37 ‘Provisions,Contingent Liabilities and Contingent Assets’ only deals with those provisions that are regarded as liabilities. The term provision is also generally used to describe those amounts set aside to write down the value of assets such as depreciation charges and provisions for diminution in value (e.g. provision to write down the value of damaged or slow moving inventory). The definition of a provision in the Standard is quite simple; provisions are liabilities of uncertain timing or amount. If there is reasonable certainty over these two aspects the liability is a creditor. There is clearly an overlap between provisions and contingencies. Because of the ‘uncertainty’ aspects of th e definition,it can be argued that to some extent all provisions have an element of contingency. The IASB distinguishes between the tow by stating that a contingency is not recognized as a liability if it is either only possible and therefore yet to be confirmed as a liability,or where there is a liability but it cannot be measured with sufficient reliability. The IASB notes the latter should be rare.The IASB intends that only those liabilities that meet the characteristics of a liability in its Framework for the Preparation and Presentation of Financial Statements should be reported in the balance sheet.IAS 37 summarises the above by requiring provisions to satisfy all of the following three recognition criteria:- there is a present obligation (legal or constructive) as a result of a past event;- it is probable that a transfer of economic benefits will be required to settle the obligation;A provision is triggered by an obligating event. This must have already occurred,future events cannot create current liabilities. The first of the criteria refers to legal or constructive obligations. A legal obligation is straightforward and uncontroversial,but constructive obligations are a relatively new concept. These arise where a company creates an expectation that it will meet certain obligations that is not legally bound to meet. These may arise due to a published statement or even by a pattern of past practice. In reality constrictive obligations are usually accepted because the alternative action is unattractive or may damage the reputation of the company. The most commonly quoted example of such is a commitment to pay for environmental damage caused by the company,even where there is no legal obligation to do so.To summarise:a company must provide for a liability where the three defining criteria of a provision are met,but conversely a company cannot provide for a liability where they are not met. The latter part of the above may seem obvious,but it is an area where there has been some past abuse of provisioning as is referred to in (b).(b) the main need for an accounting standard in this area is to clarify and regulate when provisions should and should not be made. Many controversial areas including the possible abuse of provision are based on contravening aspects of the above definitions. One of the most controversial examples of provisioning is in relation to future restructuring or recognization costs (often as part of an acquisition). This is sometimes extended to providing for future operating losses. The attraction of providing for this type of expense/loss is that once the provision has been made,the future costs are then charged to the provision such that they bypass the income statement (of the period when they occur). Such provisions can be glossed over by management as ‘exceptional items’,which analysts are expected to disregard when assessing the company’s future prospects. If thistype of provision were to be incorporated as a liability as part of a subsidiary’s net assets at the date of costs and operating losses (unless they are for an onerous contract) do not constitute past events.Another important change initiated by IAS 37 is the way in which environmental provisions must be treated. Practice in this area has differed considerably. Some companies did provide for such costs and those that did often accrued for them on an annual basis. If say a company expected environmental site restoration cost of $10 million in 10 years time,it might argue that this is not a liability until the restoration is needed or it may accrue $1 million per annum for 10 years (ignoring discounting). Somewhat controversially this practice is no longer possible. IAS 37 requires that if the environmental costs are a liability (legal or constructive),then the whole of the costs must be provided for immediately. That has led to large liabilities appearing in some companies’ balance sheets.A third example of bad practice is the use of‘big bath’ provisions and over provisioning. In its simplest form this occurs where a company makes a large provision,often for non-specific future expenses,or as part of an overall restructuring package. If the provision is deliberately overprovided,then its later release will improve future profits. Alternatively the company could charge to the provision a different cost than the one is was originally created for IAS 37 addresses this practice in two ways:by not allowing provisions to be created if they do not meet the definition of an obligation;and specifically preventing a provision made for one expense to be used for a different expense. Under IAS 37 the original provision would have to be reversed and a new one would be created with appropriate disclosures. Whilst this treatment does not affect overall profits,it does enhance transparency.Note:other examples would be acceptable.(c) Bodyline sells sports goods and clothing through a chain of retail outlets. It offers customers a full refund facility for any goods returned with in 28days of their purchase provided they are unused and in their original packaging. In addition,all goods carry a warranty against manufacturing defects for 12 months from their date of purchase. For most goods the manufacturer underwrites this warranty such that Bodyline is credited with the cost of the goods that are retumed as faulty. Goods purchased from one manufacturer,Header,are sold to Bodyline at a negotiated discount which is designed to compensate Bodyline for manufacturing defects. No refunds are given by Header,thus Bodyline has to bear the cost of any manufacturing faults of these goods.Bodyline makes a uniform mark up on cost of 25% on all goods it sells,except for those supplied from Header on which it makes a mark up on cost of 40%. Sales of goods manufactured by Header consistently account for 20% of all Bodyline’s sales.Sales in the last 28 days of the trading year to 30September 2003 were $1,750,000. Past trends reliably indicate that 10% of all goods are returned under the 28(e) Profits on disposal of assets.l effect.更多ACCA资讯请关注高顿ACCA官网:。

财务管理教程

第二章 财务管理的价值观念

货币的时间价值和投资的风险价值是财务管 理的基础观念。

第一节 货币的时间价值 第二节 风险和报酬 第三节 利息率

财务管理

第一节 货币的时间价值

货币的时间价值或资金的时间价值是指货币经历一定 时间的投资和再投资所增加的价值,是没有风险和没有 通货膨胀条件下的社会平均资金利润率。

财务管理

四、财务管理的基本理论

1.有效市场假说(EMM,The Efficient-Market Hypothesis) 股票市价反映了现时与股票相关的各方面信息,股价总处 于均衡状态,任何证券的出售者或购买者均无法持续获得超 常利润。

2.现值分析理论(Present Value Analysis Theory) 基于货币的时间价值原理,对企业未来的投资活动、筹资活 动产生的现金流量进行贴现分析,以便正确地衡量投资收益、 计算筹资成本、评价企业价值。

财务管理

三、企业财务关系

1.所有者:国家、法人、个人、外商 委托代理问题、内部人控制 2.债权人:金融中介机构(银行、基金、信托投资公司)、债券

持有人、商业信用提供者(供应商) 3.被投资单位:短期投资(证券市场的股票和债券投资)、直接

投资(企业集团的财务关系) 4.债务人:企业购买其他公司的债券、提供借款、提供商业信用 5.政府有关部门:税务、工商、财政 6.职工:激励与控制、报酬计划 7.企业内部各单位:内部经济核算

A 5000 5000 1319 (PVA10%,5 ) 3.791

贷款等额摊还计算表 单位:万元

年末 等额摊还额 支付利息 偿还本金 年末贷款余额

1

1319

500.00 819.00 4181.00

2

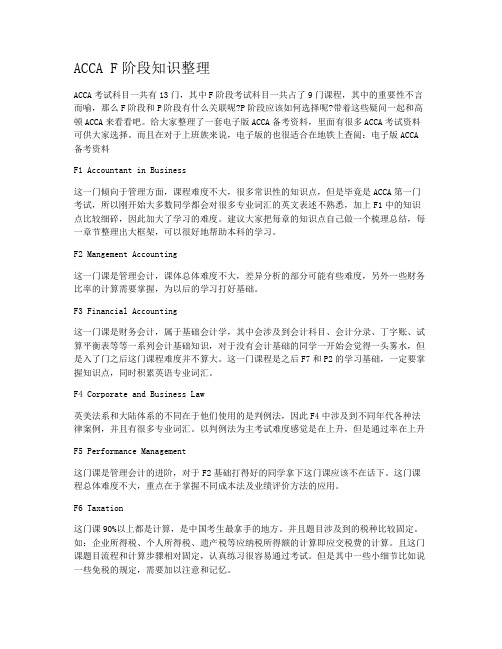

ACCA考试F阶段、P阶段大纲全解析

本文由高顿ACCA整理发布,转载请注明出处

课程类别

课程序号

课程名称(中)

课程名称(英)

知识课程

F1

会计师与企业

Accountant in Business (AB/FAB)

F2

管理会计

Management Accounting (MA/FMA)

F3

财务会计

Financial Accounting (FA/FFA)

本文由高顿ACCA整理发布,转载请注明出处,更多ACCA资讯请关注高顿ACCA官网:

选修课程

(4选2)

P4

高级财务管理

Advanced Financial Management (AFM)

P5

高级业绩管理

Advanced Performance Management (APM)

P6

高级税务

Advanced Taxation (ATX)

P7

高级审计与认证业务

Advanced Audit and Assurance (AAA)

技能课程

F4

公司法与商法

Corporate and Business Law (CL)

F5

业绩管理

Performance Management (PM)

F6

税务

Taxation (TX)

F7

财务报告

Financial Reporting (FR)

F8

审计与认证业务

Audit and Assurance (AA)

F9

财务管理

Financial Management (FM)

课程类别

课程序号

课程名称(中)

一文看懂ACCA各科目内容、特点、题型、分值、通过率、难度、彼此关系·····

ACCA考试共有15个考试科目,其中AB(F1)、MA(F2)、FA(F3)、LW(F4)、PM(F5)、TX(F6)、FR(F7)、AA(F8)、FM(F9)为F阶段课程,共9个科目,SBL、SBR、AFM(P4)、APM(P5)、ATX(P6)、AAA(P7)为P阶段课程,共6个科目。

ACCA课程中,F阶段科目全部为必修课,P阶段科目中SBL、SBR为必修课,其他为选修课(4选2参加考试),ACCA考试一共考过13科即可变成ACCA准会员。

考试之前一定要对ACCA有全面的了解,知己知彼方能百战不殆。

AB (F1)1英文名:Accountant in Business2中文名:会计师与企业3课程内容:主要是帮助无任何商业背景知识的学员初步建立人力资源、企业组织、商业环境及相互之间影响关系的相关知识内容。

内容涵盖:企业组织,公司管理,会计和报告体系,内部财务控制,人力资源管理,会计职业道徳。

4科目联系:AB(F1)是SBL课程中《公司治理,风险管理与职业道德》和《商务分析》的基础。

5考试时间:2小时(机考)6考试分值:A部分一一30道单选题(每题2分,共计60分)一一16道单选题(每题1分,共计16分)B部分一一情景为基础的6道多任务题(由单选、多选、判断题构成,每题4分,共计24分)7课程难度:☆☆8时间花费:☆☆☆2019年全球平均通过率:82.50%MA (F2)1英文名:Management Accounting2中文名:管理会计3课程内容:主要向学员介绍了管理会计体系的主要元素以及管理会计如何发挥支持企业决策, 制定企业决策的作用。

内容涵盖:管理会计,管理信息,成本会计,预算和标准成本,业绩衡量,短期决策方法。

4科目联系:MA(F2)《管理会计》是PM(F5)《业绩管理》和APM(P5)《高级业绩管理》的基础。

5考试时间:2小时(机考)6考试分值:A部分一一35道单选题(每题2分,共计70分)B部分一一3道多任务题(由计算、简单、论述题构成,每题10分,共计30分)7课程难度:☆☆8时间花费:☆☆☆2019年全球平均通过率:65.00%FA (F3)1英文名:Financial Accounting2中文名:财务会计3课程内容:主要向学员介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

ACCA笔记 F9 FM 文字题总结

PART A[1]As agents of the company’s shareholders,the directors may not always act inways which increase the wealth of shareholders,a phenomenon called theagency problem.[2]They can be encouraged to increase or maximize shareholders wealth bymanagerial reward schemes such as performance-related pay and shareoption schemes.Through these methods,the goals of shareholders anddirectors may increase in congruence.解决代理问题的⽅法有managerialreward schemes。

Managerial reward schemes⼜包括share option schemes和performance-related pay这两种⽅法。

[3]Performance-related pay links part of remuneration of directors to someaspect of cooperate performance.One problem here is that is difficult tochoose an aspect of cooperate performance which is not influenced by theactions of directors,leading to the possibility of managers influencingcooperate affairs for their own benefit rather than the benefit of shareholders.[4]Share option schemes bring the goals of shareholders and directors closertogether to the extent that directors become shareholders themselves.Unfortunately,a general increase in share prices can lead to directors beingreward for poor performance,while a decrease in share prices can lead todirectors not being reward for good performance.[5]However,share option schemes can lead to a culture of performanceimprovement and so can bring continuing benefit to shareholders.股票期权计划可以带来绩效改善的⽂化,因此可以为股东带来持续的利益。

2015年12月ACCA考试F4讲义(二)

2015年12月ACCA考试F4讲义(二) 12月ACCA考试就要到了,为了方便大家更好地复习12月ACCA F4考试,小编在百度文库定期传一些考试资料,如有需要请关注财萃财经的百度文库。

Session 3 Types of cost and cost behaviorMain contents:1. Classifying costs2. Cost objects, cost and cost centers3. Analysis of costs into fixed and variable elements3.1 Classifying costsCosts can be classified in a number of different ways:·Element –costs are classified as materials, labor or expenses (overheads)·Nature –costs are classified as being direct or indirect.a. Direct cost is expenditure that can be directly identified with a specific cost unit or cost center.(1). Direct material is all material becoming part of the product unless used in negligible amount and/or having negligible cost. (component parts, part finished work and primary packing material)(2). Direct wages –are wages paid for labor either as basic hours or as overtime expensed on the product line.(3). Direct expense are any expense which are incurred on a specified product other than direct material and direct labor.b. Indirect costs/ overheads; are expenditure that can not be directly identified with a specific unit or cost center and must be ‘shared out’on an equitable basis.·Behavior –costs are classified as being fixed, variable, semi-variable or stepped fixed.a. Fixed costs: are costs that are not affected in total by the level of activity, but remain the same.b. Variable costs: are the costs that change in total in direct proportion to the level of activity.c. Semi-variable/semi-fixed/mixed costs: are costs which contain both fixed and variable components and so it partly affected by changes in the level of activity.d. Step costs: are fixed in nature but only within certain level of activity.·Function: costs are classified as being production or non-production costs.e. Production costs: are costs included in a stock valuation. The product cost is the cost of making or buying.f. Period costs (general cost): are costs that are not attributed to product costs, but instead are treated as a cost of the time period when they arise.·Other cost classification:Avoidable cost: cost which can be eliminated by changing operationsUnavoidable cost: cost which will not be changed by decision making.Controllable cost: those cost controllable by a particular manager in a given period.Uncontrollable cost: any cost that can not be affected by management within a given period.COST MODEL: $Direct material: 2Direct labor 3Direct expense 1Direct cost 6Production overhead (Note) 1Total production cost 7Administration Overhead 1Selling and distribution Overhead 1Total cost 9Note: Production overhead includes indirect material, indirect labor and indirect expense.3.2 Analyzing costs:Cost objects: a cost object is any activity for which a separate measurement of cost is undertaken.Cost units: a cost unit is a unit of product or service in relation to which costs are ascertainedResponsibility centers: a department whose performance is the direct responsibility of a specific manager.The main responsibility centers are:·Cost center –the performance of a cost center manager is judged on the extent to which cost targets have been achieved.·Revenue center –Within an organization, this is a centre or activity that earns sales revenue. And whose manager is responsible for the revenue earned but not for the costs incurred.·Profit center – a part of the business whose manager is responsible and accountable for both costs and revenue. The performance of a profit center manager is measured in terms of the profit made by the centre.·Investment centre– a profit centre with additional responsibility for investment and possibly also for financing, and whose performance is measured by its return on capital employed.(ROCE).Cost equations:Equation of a straight lineThe equation of a straight line is a linear function and is represented by the following equation:Y = a + bxTotal cost = Total FC + Total VCY= a + bx·Y = total cost· a = the fixed cost for the given period · b = the variable cost per unit·x = the number of units of activity Cost graphsCost and revenue $。

ACCA 全球考F9真题

3

[P.T.O.

10 Which of the following statements concerning working capital management are correct? 1 2 3 A B C D Working capital should increase as sales increase An increase in the cash operating cycle will decrease profitability Overtrading is also known as under-capitalisation 1 and 2 only 1 and 3 only 2 and 3 only 1, 2 and 3

6

Which of the following statements is correct? A B C D Tax allowable depreciation is a relevant cash flow when evaluating borrowing to buy compared to leasing as a financing choice Asset replacement decisions require relevant cash flows to be discounted by the after-tax cost of debt If capital is rationed, divisible investment projects can be ranked by the profitability index when determining the optimum investment schedule Government restrictions on bank lending are associated with soft capital rationing

ACCA F阶段知识整理

ACCA F阶段知识整理ACCA考试科目一共有13门,其中F阶段考试科目一共占了9门课程,其中的重要性不言而喻,那么F阶段和P阶段有什么关联呢?P阶段应该如何选择呢?带着这些疑问一起和高顿ACCA来看看吧。

给大家整理了一套电子版ACCA备考资料,里面有很多ACCA考试资料可供大家选择。

而且在对于上班族来说,电子版的也很适合在地铁上查阅:电子版ACCA 备考资料F1 Accountant in Business这一门倾向于管理方面,课程难度不大,很多常识性的知识点,但是毕竟是ACCA第一门考试,所以刚开始大多数同学都会对很多专业词汇的英文表述不熟悉,加上F1中的知识点比较细碎,因此加大了学习的难度。

建议大家把每章的知识点自己做一个梳理总结,每一章节整理出大框架,可以很好地帮助本科的学习。

F2 Mangement Accounting这一门课是管理会计,课体总体难度不大,差异分析的部分可能有些难度,另外一些财务比率的计算需要掌握,为以后的学习打好基础。

F3 Financial Accounting这一门课是财务会计,属于基础会计学,其中会涉及到会计科目、会计分录、丁字账、试算平衡表等等一系列会计基础知识,对于没有会计基础的同学一开始会觉得一头雾水,但是入了门之后这门课程难度并不算大。

这一门课程是之后F7和P2的学习基础,一定要掌握知识点,同时积累英语专业词汇。

F4 Corporate and Business Law英美法系和大陆体系的不同在于他们使用的是判例法,因此F4中涉及到不同年代各种法律案例,并且有很多专业词汇。

以判例法为主考试难度感觉是在上升,但是通过率在上升F5 Performance Management这门课是管理会计的进阶,对于F2基础打得好的同学拿下这门课应该不在话下。

这门课程总体难度不大,重点在于掌握不同成本法及业绩评价方法的应用。

F6 Taxation这门课90%以上都是计算,是中国考生最拿手的地方。

ACCA F4-F9模拟题及解析(6)

ACCA F4-F9模拟题及解析(6)1 BQK Co, a house-building company, plans to build 100 houses on a development site over the next four years. The purchase cost of the development site is $4,000,000, payable at the start of the first year of construction. Two types of house will be built, with annual sales of each house expected to be as follows:Year 1 2 3 4Number of small houses sold: 15 20 15 5Number of large houses sold: 7 8 15 15Houses are built in the year of sale. Each customer finances the purchase of a home by taking out a long-term personal loan from their bank. Financial information relating to each type of house is as follows:Small house Large houseSelling price: $200,000 $350,000Variable cost of construction: $100,000 $200,000Selling prices and variable cost of construction are in current price terms, before allowing for selling price inflation of 3% per year and variable cost of construction inflation of 4·5% per year.Fixed infrastructure costs of $1,500,000 per year in current price terms would be incurred. These would not relate to any specific house, but would be for the provision of new roads, gardens, drainage and utilities. Infrastructure cost inflation is expected to be 2% per year.BQK Co pays profit tax one year in arrears at an annual rate of 30%. The company can claim capital allowances on the purchase cost of the development site on a straight-line basis over the four years of construction.BQK Co has a real after-tax cost of capital of 9% per year and a nominal after-tax cost of capital of 12% per year.New investments are required by the company to have a before-tax return on capital employed (accounting rate of return) on an average investment basis of 20% per year.Required:(a) Calculate the net present value of the proposed investment and comment on its financial acceptability. Workto the nearest $1,000. (13 marks)(b) Calculate the before-tax return on capital employed (accounting rate of return) of the proposed investmenton an average investment basis and discuss briefly its financial acceptability. (5 marks) (c) Discuss the effect of a substantial rise in interest rates on the financing cost of BQK Co and its customers,and on the capital investment appraisal decision-making process of BQK Co. (7 marks)(25 marks)2.KXP Co is an e-business which trades solely over the internet. In the last year the company had sales of $15 million.All sales were on 30 days’ credit to commercial customers.Extracts from the company’s most recent statement of financial position relating to working capital are as follows:$000Trade receivables 2,466Trade payables 2,220Overdraft 3,000In order to encourage customers to pay on time, KXP Co proposes introducing an early settlement discount of 1% for payment within 30 days, while increasing its normal credit period to 45 days. It is expected that, on average, 50% of customers will take the discount and pay within 30 days, 30% of customers will pay after 45 days, and 20% of customers will not change their current paying behaviour.KXP Co currently orders 15,000 units per month of Product Z, demand for which is constant. There is only one supplier of Product Z and the cost of Product Z purchases over the last year was $540,000. The supplier has offered a 2% discount for orders of Product Z of 30,000 units or more. Each order costs KXP Co $150 to place and the holding cost is 24 cents per unit per year.KXP Co has an overdraft facility charging interest of 6% per year.Required:(a) Calculate the net benefit or cost of the proposed changes in trade receivables policy and comment on your findings. (6 marks)(b) Calculate whether the bulk purchase discount offered by the supplier is financially acceptable and comment on the assumptions made by your calculation. (6 marks)(c) Identify and discuss the factors to be considered in determining the optimum level of cash to be held by a company. (5 marks)(d) Discuss the factors to be considered in formulating a trade receivables management policy.(8 marks) (25 marks)试题答案:1. (1,530) (1,561) (1,592) (1,624)–––––– –––––– –––––– ––––––Before-tax cash flow 1,053 1,722 2,288 1,236Tax liability (316) (517) (686) (371)CA tax benefits 300 300 300 300–––––– –––––– –––––– –––––– ––––––After-tax cash flow 1,053 1,706 2,071 850 (71)Discount at 12% 0·893 0·797 0·712 0·636 0·567–––––– –––––– –––––– –––––– ––––––Present values 940 1,360 1,475 541 (40)–––––– –––––– –––––– –––––– ––––––$000PV of future cash flows 4,276Initial investment (4,000)––––––276–––––– CommentSince the proposed investment has a positive net present value of $276,000, it is financially acceptable.WorkingsSales revenueYear 1 2 3 4Sales of small houses (houses/yr) 15 20 15 5Sales of large houses (houses/yr) 7 8 15 15Small house selling price ($000/house) 200 200 200 200Large house selling price ($000/house) 350 350 350 350Sales revenue (small houses) ($000/yr) 3,000 4,000 3,000 1,000Sales revenue (large houses) ($000/yr) 2,450 2,800 5,250 5,250–––––– –––––– –––––– ––––––Total sales revenue ($/yr) 5,450 6,800 8,250 6,250–––––– –––––– –––––– –––––– Inflated sales revenue ($/yr) 5,614 7,214 9,015 7,034Variable costs of constructionYear 1 2 3 4Sales of small houses (houses/yr) 15 20 15 5Sales of large houses (houses/yr) 7 8 15 15Small house variable cost ($000/house) 100 100 100 100Large house variable cost ($000/house) 200 200 200 200Variable cost (small houses) ($000/yr) 1,500 2,000 1,500 500Variable cost (large houses) ($000/yr) 1,400 1,600 3,000 3,000–––––– –––––– –––––– ––––––Total variable cost ($/yr) 2,900 3,600 4,500 3,500–––––– –––––– –––––– –––––– Inflated total variable cost ($/yr) 3,031 3,931 5,135 4,174Fixed infrastructure costsYear 1 2 3 4Fixed costs ($000/yr) 1,500 1,500 1,500 1,500Inflated fixed costs ($000/yr) 1,530 1,561 1,592 1,624Alternative NPV calculationYear 1 2 3 4 5$000 $000 $000 $000 $000Before-tax cash flow 1,053 1,722 2,288 1,236Capital allowances (1,000) (1,000) (1,000) (1,000)–––––– –––––– –––––– ––––––Taxable profit 53 722 1,288 236Taxation (16) (217) (386) (71)–––––– –––––– –––––– –––––– –––––– Profit after tax 53 706 1,071 (150) (71)Add back allowances 1,000 1,000 1,000 1,000–––––– –––––– –––––– ––––––After-tax cash flow 1,053 1,706 2,071 850 (71)Discount at 12% 0·893 0·797 0·712 0·636 0·567–––––– –––––– –––––– –––––– ––––––Present values 940 1,360 1,475 541 (40)–––––– –––––– –––––– –––––– –––––– $000PV of future cash flows 4,276Initial investment (4,000)––––––276–––––– (b)Calculation of return on capital employed (ROCE)Total before-tax cash flow $6,299,000Total depreciation $4,000,000–––––––––––Total accounting profit $2,299,000Average annual profit ($000/year) = 2,299,000/4 = $574,750Average investment ($000) = 4,000,000/2 = $2,000,000ROCE (ARR) = 100 x 574,750/2,000,000 = 28·7%DiscussionThe ROCE is greater than the 20% target ROCE of the investing company and so the proposed investment is financially acceptable. However, the investment decision should be made on the basis of information provided by a discounted cash flow (DCF) method, such as net present value or internal rate of return.(c) A substantial increase in interest rates will increase the financing costs of BQK Co and its customers. These will affect the discount rate used in the investment appraisal decision-making process and the value of project variables.Customer financing costs Each customer finances their house purchase through a long-term personal loan from their bank. A substantial rise in interest rates will increase the borrowing costs of existing and potential customers of BQK Co, and will therefore increase the amount of cash they pay to buy one of the houses.Company financing costsThe cost of debt of BQK Co will change with interest rates in the economy. A substantial rise in interest rates will therefore lead to a substantial increase in the cost of debt of the company. This will lead to an increase in the weighted average cost of capital (WACC) of BQK Co, the actual increase depending on the relative proportion of debt compared to equity in the company’s capital structure.The cost of equity will also increase as interest rates rise, contributing to the increase in the WACC. Since most companies have a greater proportion of equity finance as compared to debt finance, the increase in the cost of equity is likely to have a more significant effect on theWACC than the increase in the cost of debt.Effect on the capital investment appraisal processSince the business of the company is building houses, the WACC of the company is likely to be the discount rate it uses in evaluating investment decisions such as the one under consideration. An increase in WACC will therefore lead to a decrease in the NPV of investment projects and some projects may no longer be attractive.In order to make the investment project more attractive, the prices of the houses offered for sale might have to increase. This could make the houses more difficult to sell and lead to increased costs due to slower sales.Houses could also be more difficult to sell as customers would be more reluctant to commit themselves to long-term personal loans when interest rates are historically high.Construction and infrastructure costs might increase as suppliers seek to pass on their higher borrowing costs.Overall, income per year could decrease and the time period for the investment might need to be extended to accommodate the slower sales process.2 (a)Calculation of net cost/benefitCurrent receivables = $2,466,000Receivables paying within 30 days = 15m x 0·5 x 30/365 = $616,438Receivables paying within 45 days = 15m x 0·3 x 45/365 = $554,795Receivables paying within 60 days = 15m x 0·2 x 60/365 = $493,151Revised receivables = 616,438 + 554,795 + 493,151 = $1,664,384Reduction in receivables = 2,466,000 – 1,664,384 = $801,616Reduction in financing cost = 801,616 x 0·06 = $48,097Cost of discount = 15m x 0·5 x 0·01 = $75,000Net cost of proposed changes in receivables policy = 75,000 – 48,097 = $26,903Alternative approach to calculation of net cost/benefitCurrent receivables days = (2,466/15,000) x 365 = 60 daysRevised receivables days = (30 x 0·5) + (45 x 0·3) + (60 x 0·2) = 40·5 daysDecrease in receivables days = 60 – 40·5 = 19·5 daysDecrease in receivables = 15m x 19·5/365 = $801,370(The slight difference compared to the earlier answer is due to rounding)Decrease in financing cost = 801,370 x 0·06 = $48,082Net cost of proposed changes in receivables policy = 75,000 – 48,082 = $26,918CommentThe proposed changes in trade receivables policy are not financially acceptable. However, if the trade terms offered are comparable with those of its competitors, KXP Co needs to investigate the reasons for the (on average) late payment of current customers. This analysis also assumes constant sales and no bad debts, which is unlikely to be the case in reality.(b) Cost of current inventory policyCost of materials = $540,000 per yearAnnual ordering cost = 12 x 150 = $1,800 per yearAnnual holding cost = 0·24 x (15,000/2) = $1,800 per yearTotal cost of current inventory policy = 540,000 + 1,800 + 1,800 = $543,600 per yearCost of inventory policy after bulk purchase discountCost of materials after bulk purchase discount = 540,000 x 0·98 = $529,200 per yearAnnual demand = 12 x 15,000 = 180,000 units per yearKXP Co will need to increase its order size to 30,000 units to gain the bulk discountRevised number of orders = 180,000/30,000 = 6 orders per yearRevised ordering cost = 6 x 150 = $900 per yearRevised holding cost = 0·24 x (30,000/2) = $3,600 per yearRevised total cost of inventory policy = 529,200 + 900 + 3,600 = $533,700 per yearEvaluation of offer of bulk purchase discountNet benefit of taking bulk purchase discount = 543,600 – 533,700 = $9,900 per yearThe bulk purchase discount looks to be financially acceptable. However, this evaluation is based on a number of unrealistic assumptions. For example, the ordering cost and the holding cost are assumed to be constant, which is unlikely to be true in reality. Annual demand is assumed to be constant, whereas in practice seasonal and other changes in demand are likely.(c)The following factors should be considered in determining the optimum level of cash to be held by a company, for example,at the start of a month or other accounting control period.The transactions need for cashThe amount of cash needed for the next period can be forecast using a cash budget, which will net off expected receipts against expected payments. This will determine the transactions need for cash, which is one of the three reasons for holding cash.The precautionary need for cashAlthough a cash budget will provide an estimate of the transactions need for cash, it will be based on assumptions about the future and will therefore be subject to uncertainty. The actual need for cash may be greater than the forecast need for cash.In order to provide for any unexpected need for cash, a company can include some spare cash (a cash buffer) in its cash balance. This is the precautionary need for cash. In determining the optimal level of cash to be held, a company will estimatethe size of this cash buffer, for example from past experience, because it will be keen to minimise the opportunity cost of maintaining funds in cash form.The speculative need for cash There is always the possibility of an unexpected opportunity occurring in the business world and a company may wish to be prepared to take advantage of such a business opportunity if it arises. It may therefore wish to have some cash available for this purpose. This is the speculative need for cash. Building ‘a war chest’ for possible company acquisitions reflects this reason for holding cash.The availability of finance A company may choose to hold higher levels of cash if it has difficulty gaining access to cash when it needs it. For example,if a company’s bank makes it difficult to access overdraft finance, or if a company is refused an overdraft facility, its precautionary need for cash will increase and its optimum cash level will therefore also increase.(d)The factors to be considered in formulating a trade receivables policy relate to credit analysis, credit control and receivables collection.Credit analysisIn offering credit, a company must consider that it will be exposed to the risk of late payment and the risk of bad debts. To reduce these risks, the company will assess the creditworthiness of its potential customers. In order to do this, the company needs information, which can come from a variety of sources, such as trade references, bank references, credit reference agencies, published accounts and so on. As a result of assessing the creditworthiness of customers, a company can decide on the amount of credit to offer, the credit terms to offer, or whether to offer credit at all.Credit controlHaving extended credit to customers, a company needs to consider ways to ensure that the terms under which credit was granted are followed. It is important that customers settle outstanding accounts on time and keep to agreed credit limits.Factors to consider here are, therefore, the number of overdue accounts and the amount of outstanding cash. This information can be provided by an aged receivables analysis.Another factor to consider is that customers need to be made aware of the amounts outstanding on their accounts and reminded when payment is due. This can be done by providing regular statements of account and by sending reminder letters when payment is due.Receivables collectionCash received needs to be banked quickly if payment is not made electronically by credit transfer. Overdue accounts must be followed up in order to assess the likelihood of payment and to determine what further action is needed. In the worst cases,legal steps may need to be taken in order to recover outstanding amounts.A key factor to consider here is that the benefit gained from chasing overdue amounts must not exceed the costs incurred.参与ACCA考试的考生可按照复习计划有效进行,另外高顿网校官网ACCA考试辅导高清课程已经开通,还可索取ACCA考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升复习备考效果。

《ACCA考试之财务管理 FINANCIAL MANAGEMENT》课件PPT 3 Financial Markets and Institutions

11

Major Categories of Financial Assets

5

1.1 Financial intermediation

Key term

A financial intermediary is a party bring together providers and users of finance, either as broker or as principal. A financial intermediary is an institution which links lender with borrowers, by obtaining deposits from lenders and re-lending them to borrowers.

7

Financial Intermediation

Example of intermediaries

Clearing banks Investment banks Savings banks Building societies Finance companies Pension funds Insurance companies Investment/unit trusts

6

1.1 Financial intermediation

Surplus unit

Person

savings funds

财务管理(第三版)复习资料整理

第1章总论一、企业财务活动1、企业筹资引起2、企业投资引起3、企业经营引起4、企业分配引起二、企业财务关系1、企业与其所有者之间2、企业与债权人3、企业与被投资单位4、企业与债务人5、企业内部各单位之间6、企业与职工7、企业与税务机关三、企业财务管理特点1、是一项综合性管理工作2、财务管理与企业各方面具广泛联系3、财务管理能迅速反映企业生产经营状况四、财务管理目标(一)基本特点1、相对稳定性2、多元性3、层次性(二)财务管理的整体目标1、以产值最大化为目标2、以利润最大化为目标3、以股东财富最大化为目标4、以企业价值最大化(三)分部目标1、筹资管理目标——在满足生产经营需要情况下,不断降低成本和财务风险2、投资管理目标——认真进行投资项目可行性研究,力求提高投资报酬,降低投资风险。

3、营运资金管理——合理使用资金,加速资金周转,不断提高资金使用效率。

4、收益分配的目标——采取各措施,努力提高收益水平,合理分配企业收益。

五、财务管理的原则(一)系统原则1、目的性2、整体性3、层次性4、环境适应性(二)平衡原则(数量和时间上收支平衡)目前现金余额+预计现金收入-预计现金支出=预计现金余额(三)弹性原则(四)比例原则(五)优化原则六、财务管理的方法(一)预测方法1、定性预测法2、定量预测法(二)财务决策方法1、优选对比法2、数学微分法3、线性规划法4、概率决策法5、损益决策法(三)计划方法1、平衡法2、因素法3、比例法4、定额法(四)控制方法1、防护控制法2、前馈性控制法3、反馈性控制法(五)分析方法1、对比分析法2、比率分析法3、综合分析法第二章 财务管理的基础理念一、时间价值1、时间价值:是扣除风险报酬和通货膨胀贴水后的真实报酬率。

只有在风险和没有通货膨胀的情况下,时间价值才与上述各报酬率相等。

2、复利终值和现值 (F 、P 、i 、n )复利终值:n i P F )1(+==P*FVIF i,n 或:(F/P ,i ,n ) 复利现值:n i F P )1(+=或:=F*PVIF i,n或:F (P/F ,i ,n ) 3、年金终值和现值 (A 、F 、P 、i 、n)(1)普通年金(后付年金):普通年金是指在每期期末收到或支付相等金额的年金形式。

财务管理系课程介绍(中英对照)

财务管理系课程介绍(中英对照)序号:1课程编码:11001030、11001020课程名称:管理会计Management Accounting学分:3周学时: 3开课系部:财务管理系预修课程:会计学基础、财务会计修读对象:本科生课程简介:本课程是财务管理专业的专业方向课,主要介绍管理会计的基本理论,及如何运用会计及其它经营信息,对企业经济活动进行规划、控制、评价和考核;其主要内容包括:本量利分析、预测分析、投资决策、全面预算、成本控制与标准成本系统、责任会计等。

拟用教材:《管理会计》,毛付根主编,高等教育出版社2000年版参考教材:《管理会计》,余绪缨主编,中国人民大学出版社 1999年版;《管理会计学》(英文版),Ronald W. Hiltion主编,机械工业出版社 2000年版;《管理会计应用与发展的典型案例研究》,潘飞主编,中国财政经济出版社 2002年版Course Code: 11001030、11001020Course Title: Management AccountingDepartment: Financial Management Dept.Credit: 3Periods per week: 3Preparatory Course: Fundamental Accounting, Financial AccountingStudents: UndergraduatesContents:This is a core course for the students whose major is Financial Management. This course introduces the basic theories of management accounting system and itsapplication in the operational activities such as planning, control, evaluation,performance assessing of a business enterprise. The topics covered includecost-volume-profit analysis, business forecasting and its analysis, long-terminvestment decisions making (capital budgeting), master budgeting, cost controland standard costing system, responsibility accounting, etcCourse Book: Mao fugen. Ed. 2000. Managerial Accounting, Higher Education Press Reference Book:Yu Xuying. Ed. 1999. Managerial Accounting, China RenMin University Press;Ronald W. Hiltion. Ed. 2000. Managerial Accounting (English version), ChinaMachine Press; Pan Fei. Ed. 2000. Managerial Accounting Application andDevelopment and Typical Cases Analysis, The Chinese Finance and EconomicsPublishing House.序号: 2课程编码:11002040课程名称:财务管理Financial Management学分: 4周学时:4开课系部:财务管理系预修课程:会计学基础、财务会计修读对象:本科生课程简介:本课程是财务管理专业的专业方向课,主要介绍现代财务管理的基本理论和方法及其具体应用。

ACCA考试复习资料推荐

ACCA考试复习资料推荐ACCA(Association of Chartered Certified Accountants)考试是国际上享有盛誉的会计资质认证考试。

通过ACCA考试,可以获得全球范围内认可的专业会计资格。

为了帮助考生高效备考ACCA考试,本文将推荐一些值得使用的复习资料。

一、教材类资料1. Kaplan学习资料:Kaplan是ACCA考试备考领域的知名机构,其提供的教材以内容全面、讲解详细而著称。

Kaplan的教材包含了每一门考试科目的重点知识点和考点,还有大量练习题和模拟考试题,非常适合考生进行系统性的学习和巩固。

2. BPP教材:BPP也是ACCA备考教材领域的翘楚,其教材内容准确、深入浅出,被广大考生所推崇。

BPP的教材结构清晰,理论和实践相结合,适用于各个考试科目的学习。

二、题库类资料1. ACCA 官方题库:ACCA官方题库包含了大量的过往考试真题和模拟考试题,具有很高的可信度和代表性。

通过做官方题库,考生可以对考试的难度和考点有更加准确的把握,同时也可以熟悉考试的时间要求。

2. ACCA 培训机构提供的题库:许多ACCA培训机构会提供自制的题库,这些题库经过精心整理和筛选,具有一定的难度和质量保证。

通过做这些题库,考生可以更好地了解各个知识点的考察形式和难度,进行针对性的复习。

三、讲义类资料1. ACCA 培训机构提供的讲义:ACCA培训机构一般会提供自编的讲义,这些讲义通常会根据各个考试科目的内容进行整理和编写,内容简明扼要,并配有重点知识点和案例分析。

这些讲义可以作为复习和备考的参考资料,帮助考生更好地理解和掌握考试内容。

2. ACCA 官方教材补充讲义:ACCA官方教材中有时会包含一些附加的讲义,用于解释和扩展主教材的知识点。

这些讲义内容丰富,且与教材内容相互补充,有助于加深对知识点的理解和记忆。

四、在线学习资源1. ACCA官方网站:ACCA官方网站上提供了大量的考试信息和学习资源,包括考试介绍、报考指南、考试教材等。

财务管理专业英语_PDF图书下载_刘媛媛编_在线阅读_PDF免费电子书下载_第一图书网(5篇模版)

财务管理专业英语_PDF图书下载_刘媛媛编_在线阅读_PDF免费电子书下载_第一图书网(5篇模版)第一篇:财务管理专业英语_PDF图书下载_刘媛媛编_在线阅读_PDF 免费电子书下载_第一图书网财务管理专业英语_PDF图书下载_刘媛媛编_在线阅读_PDF免费电子书下载_第一图书网前言A journey of a thousand miles begins with a single step.——Chinese proverb The future is not what it used to be.——Paul Valery 21世纪是一个竞争激烈、国际化的高科技时代,21世纪的高级专门人才要具备扎实的专业知识、较高的信息素养和能在专业领域用外语进行交流沟通的能力。

作为一名财务管理专业教师,近几年来,我一直采用国外原版教材从事财务管理专业和非财务管理专业的财务管理课程的双语教学。

我深切体会到,虽然学生已经系统学习了大学基础英语,但由于缺乏专业英语基础,财务管理双语课程的教学效果并不尽如人意。

因此,很有必要在财务管理专业教学中设置财务管理专业英语课程。

财务管理专业英语教学,作为从基础英语教学向专业课双语教学过渡的桥梁,是财务管理专业学生从基础英语学习向专业领域英语应用过渡的不可或缺的中间环节。

要对学生进行财务管理专业英语素养的培养,一本合适的财务管理专业英语教材就成为至关重要的因素。

本书从财务管理专业培养目标出发,力求成为一本实用的财务管理专业英语教材,并采用有助于提高学生专业知识和实际运用能力的编写形式,以期能使学生成为满足日益激烈的国际竞争和频繁的国际交流需求的高素质财务管理人才。

本书按财务管理专业主干课程的架构分为12个专题,分别介绍财务管理各个方面的专业英语基础知识。

每一专题均先以“名人名言”和“微型案例”开始,以激发学生的兴趣去主动获取知识、开阔视野。

正文尽量体现财务管理专业的基本理念与核心内容,每一专题还设有“知识扩展”、“相关网址”等,进一步丰富了教学内容。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2015年ACCA考试《F9财务管理》辅导资料(17)

本文由高顿ACCA整理发布,转载请注明出处

by Anthony Head

28 Oct 2003

y examiner's report on Paper 2.4 at the June 2003 session noted the need for students to improve their understanding of market efficiency. This article addresses this issue and also discusses other market matters contained in Section 2 of the Paper 2.4 syllabus,'the financial management environment'

Capital markets,efficiency and fair prices

Investors in capital markets want to be sure that the prices they pay for securities,such as ordinary shares and bonds,are fair prices. In order for security prices to be fair,the capital markets must be able to process relevant information quickly and accurately. Relevant information is anything that could affect security prices e.g. previous movements in security prices,newly-released company financial statements,changes in interest rates or details of sales of their own company’s shares by company directors. We say that a capital market is efficient when we are confident that security prices are fair. A capital market can be efficient when share prices in general are falling (a bear market) or rising (a bull market).

Types of efficiency

It is usual to identify four types of capital market efficiency1:

1. Operational efficiency requires that transaction costs are low and do not hinder investors in the sale or purchase of securities.

2. Informational efficiency means that relevant information is widely available to all investors at low cost.

3. Pricing efficiency refers to the ability of capital markets to process information quickly and accurately,and arises as a consequence of operational efficiency and informational efficiency.

4. Allocational efficiency means that capital markets are able to allocate available funds to their most productive use and arises as a result of pricing efficiency.

Most of the research into market efficiency has been into pricing efficiency.

更多ACCA资讯请关注高顿ACCA官网:。