Accounting English (part5)

会计专业英语 (5)

Accounting English

Lesson five— accounting cycle

On 1 June 20X8, Jock Heiss commenced trading as an ice cream salesman, using a van which he drove around the streets of his town. (a) He rented the van at a cost of $1,000 for three month. Running expenses for the van averaged $300 per month. (b) He hired a par time helper at a cost of $100 per month. (c) He borrowed $2,000from his bank, and the interest cost of the loan was $25 per month. (d) His main business was to sell ice cream to customers in the street, but he also did some special catering for business customers, supplying ice creams for office parties. Sales to these customers were usually on credit. (e) for the three months to 31 August 20X8, his total sales were as follows: (i) cash sales $8,900 (ii) credit sales $1,100

会计英语第五单元课件

2 Account balance errors (1) Balance incorrectly computed (2) Balance entered in wrong column of account

3 Posting errors (1 ) Wrong amount posted to an account (2) Debit posted as credit, or vice versa (3) Debit or credit posting omitted

Pay Attention: 1 procedures for correcting errors

Errors 1 journal entry is incorrect but not posted 2 journal entry is correct but posted incorrectly 3 journal entry is incorrect and posted Corrections Procedures Draw a line through the error and insert correct title or amount. Draw a line through the error and post correctly. Journalize and post a correcting entry.

Unit Five Accounting cycle

(二) Trial Balance

Learning Objectives:

1 What is trial balance?

2 How to prepare trial balance?

会计英语 Accounting English

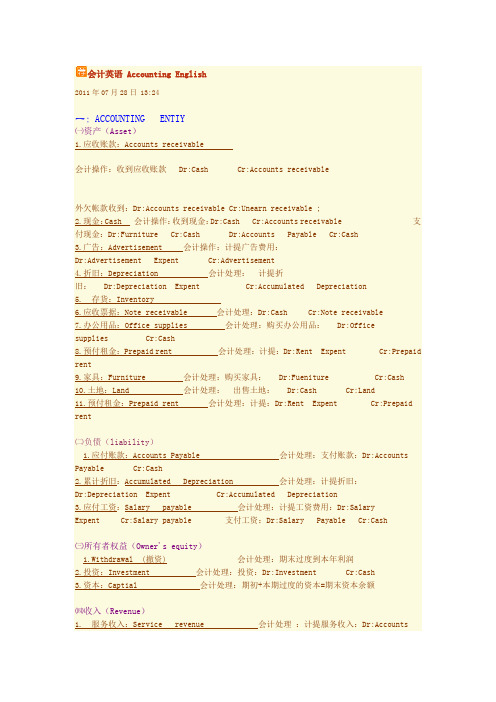

会计英语 Accounting English2011年07月28日 13:24一:ACCOUNTING ENTIY㈠资产(Asset)1.应收账款:Accounts receivable会计操作:收到应收账款 Dr:Cash Cr:Accounts receivable外欠帐款收到:Dr:Accounts receivable Cr:Unearn receivable ;2.现金:Cash 会计操作:收到现金:Dr:Cash Cr:Accounts receivable 支付现金:Dr:Furniture Cr:Cash Dr:Accounts Payable Cr:Cash3.广告:Advertisement 会计操作:计提广告费用:Dr:Advertisement Expent Cr:Advertisement4.折旧:Depreciation 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation5. 存货:Inventory6.应收票据:Note receivable 会计处理:Dr:Cash Cr:Note receivable7.办公用品:Office supplies 会计处理:购买办公用品: Dr:Officesupplies Cr:Cash8.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent9.家具:Furniture 会计处理:购买家具: Dr:Fueniture Cr:Cash10.土地:Land 会计处理:出售土地: Dr:Cash Cr:Land11.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent㈡负债(liability)1.应付账款:Accounts Payable 会计处理:支付账款:Dr:AccountsPayable Cr:Cash2.累计折旧:Accumulated Depreciation 会计处理:计提折旧:Dr:Depreciation Expent Cr:Accumulated Depreciation3.应付工资:Salary payable 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable 支付工资:Dr:Salary Payable Cr:Cash㈢所有者权益(Owner's equity)1.Withdrawal (撤资) 会计处理:期末过度到本年利润2.投资:Investment 会计处理:投资:Dr:Investment Cr:Cash3.资本:Captial 会计处理:期初+本期过度的资本=期末资本余额㈣收入(Revenue)1. 服务收入:Service revenue 会计处理:计提服务收入:Dr:Accountsreceivable Cr:Service renenue收到:Dr:Cash Cr:Accounts receivable Dr:Unearned Servicerenenue Cr:Service renenue2.保险收入:Commission revenue 会计处理:计提:Dr:Unearned commission revenue Cr:Commission revenue3.销售收入:Sales revenue 会计处理:现金收到:Dr:Cash Cr:Sales revenue销售收入赊账处理:Dr:Accounts receivable Cr:Sales revenue㈤费用(Expent)1.公用事业费用:Utilities Expent2.租金费用:Rent Expent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent3.工资费用:Salary Expent 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable4.办公费用:Supplies Expend 会计处理:计提:Dr:Supplies Expent Cr:Supplies5.折旧费用:Depreciation Expent 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation㈥过户:Dr:Income Summary Cr:费用类科目Dr:收入类科目 Cr:Income SummaryDr:Withdrawal Cr:Income SummaryDr:Income Summary Cr:Captial二:THE ACCOUNTING CYCLEA→→→→→→→→→↓↓Transaction source document→Joural→Ledger→Worksheet→Finacial statementsB→→→Closing→→→→↓↓Analyzing→Recording→Posting→Adjusting→Preparing三:存货(Inventory)---会计处理1.购买存货:Dr:Purchase Cr:Cash OR Accounts Payable2.购货折扣与退回折让:Dr:Accounts Payable Cr:CashPurchase DiscountsPurchase returns and allowances3.Purchase(Dr) ---Purchase Discounts(Cr)---Purchase returnsand allowances(Cr) =Net purchase(Dr)4.运输成本:Dr:Freight In Cr :Cash5.销售折扣与销售折让、退回:Dr:Sales DiscountSales Returnsand allowancesCr:Accounts receivable6.Sales revenue (Cr) ---Sales Discount (Dr)--- Sales Returnsand allowances(Dr)=Net Sales (Cr)7.Beginning inventory(Dr)+Net purchase(Dr)+Freight In =Cost of inventory ---Ending inventory=Cost of goods sold。

财务会计英文版原书第5版ch02bwzg

Steps in the Recording

Process

Journal Ledger

The Recording Process Illustrated

Summary illustration of journalizing and posting

The Trial Balance

Limitations of a trial balance Locating errors Use of dollar signs

Expense

Debit / Dr.

Credit / Cr.

Normal Balance

Chapter 3-25

Revenue

Debit / Dr.

Credit / Cr.

Chapter 2-8

Normal Balance

Chapter 3-27

Normal Balance

Chapter 3-26

SO 2

See notes page for discussion

Chapter 2-11

SO 2 Define debits and credits and explain their use in recording business transactions.

Assets and Liabilities

Common Stock

Debit / Dr.

Credit / Cr.

Retained Earnings

Debit / Dr.

Credit / Cr.

Dividends

Debit / Dr.

Credit / Cr.

Chapter 3-25

Chapter 2-13

财务会计(英文版·原书第5版)ch03

a. Events that change a company’s financial statements are recorded in the periods in which the events occur.

b. Revenue is recognized in the period in which it is earned.

In a service enterprise, revenue is considered to be earned at the time the service is performed.

Chapter 3-9

LO 2 Explain the accrual basis of accounting.

Recognizing revenues and expenses

The Basics of Adjusting Entries

Types of adjusting entries Adjusting entries for deferrals Adjusting entries for accruals Summary of journalizing and posting

d. all of the above.

Chapter 3-15

LO 3 Explain the reasons for adjusting entries.

Types of Adjusting Entries

Deferrals

1. Prepaid Expenses. Expenses paid in cash and recorded as assets before they are used or consumed.

英文版财务会计第五章精品PPT课件

Objectives

9. Estimate the cost of inventory, using the retail method and the gross profit method.

✓ Inventory is central to the main activity of merchandising and manufacturing companies.

✓ Mistakes in determining inventory cost can cause critical errors in financial statements.

Chapter 9

Inventories

Accounting, 21st Edition

Warren Reeve Fess

PowerPoint Presentation by Douglas Cloud

Professor Emeritus of Accounting Pepperdine University

✓ Inventory must be protected from external risks ( such as fire and theft) and internal fraud by employees.

Receiving report

AGREE

Purchase order

Invoice

Objectives

5. Compute the cost of inventory under the periodic inventory system, using the following costing methods: first-in, first-out; last-in, first-out; average cost.

会计英语unit5CompletionoftheAccountingCycle精课件

Depreciation is the process of allocating the cost of an asset to expense over its useful life.

The amount of interest accumulation is determined by three factors:

Interest = Face Value of Note x Annual Interest Rate x Time in Terms of One Year

21

Interest cost for a month : $10,000 x 12% x 1/12=$100

At the end of month

Dr. Interest Expense Cr. Interest Payable

100 100

22

Example(2) Accrued Salaries

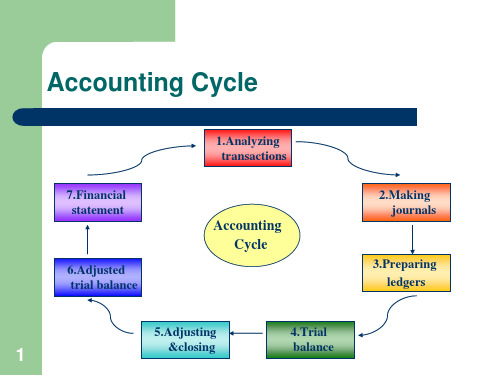

Accounting Cycle

7.Financial statement

6.Adjusted trial balance

1.Analyzing transactions

Accounting Cycle

2.Making journals

3.Preparing ledgers

5.Adjusting

4.Trial

At the end of month

Dr. Unearned Revenue 1,000 Cr. Service Revenue 1,000

会计英语5

XXX Company

Payment voucher

Credit account:

ption

debit account

amount

PR

General Ledger account

Subsidiary account

Approved by:

Signature:

3. Income accounts are generally listed first in the general ledger.

T

T

F

Accounts that normally have debit balances are: assets, expenses, and revenues. assets, expenses, and owner’s capital. assets, liabilities, and owner’s drawings. assets, owner’s drawings, and expenses.

Posting: normally occurs before journalizing. transfers ledger transaction data to the journal. is an optional step in the recording process. transfers journal entries to ledger accounts.

2.5 Practices in China

XXX Company

Transfer Voucher

date

No.

Description

General Ledger account

Subsidiary account

CHAPTER5 《会计英语》

Unit 2 Depreciation of Plant Assets

Exhibit 5-2-2

2. trade in

以旧换新,这是企业取得固定资产的一种方式,不全部以现金支付新

增固定资产的价款,而是以一项旧的固定资产作为一部分抵价,差额部分以现金

支付。

Special Terms

3. betterments 也称improvement,改造投资,指更换固定资产的重要组成部

分,从而延长该固定资产的使用年限,提高生产能力或降低操作成本。在会计处理

equipment.

Unit 1 Balance Sheet

➢MAJOR CATEGORIES OF PLANT AND EQUIPMENT. Plant and

equipment items are often classified into the following groups:

➢Depreciable assets. Depreciable assets are plant assets with physical

substance, which are expected to be used during more than one

accounting period and have limited useful life. This charge is called

depreciation. Examples include buildings, machinery and equipment.

book value.

Special Terms

1. plant and equipment 固定资产,字面意思是厂房和设备,在国际会计准则

会计英语第五章

Dishonored Notes Receivable:

fist question:

What is the dishonored notes

receivable?

Accounting treatment:

for example:

°TOM sold merchandise to BOB and accepted a $ 1000,10% , six-month note dated November 30,2002, that is due on May 30,2003,BOB defaults on the six-month note and TOM charges the amount to Accounts receivable .On June 30,TOM collects the accounts receivable with interest .

recording receipt and collection of note

to record revenue earnd, the general format for the entry to record the receipt of a note is:

Notes receivable-x co

10197.26

interest earned

62.47

interest receivable

134.79

notes receivable

10000.00

$10000×12%×19/365

note that this cash receipt includes interest for the entire period of the onte. part of this amount is the interest that was earned in the previous period and accrued as a receivable,the remainder is the interest earned in the current period.

金融英语5-accounting

• Current liabilities are expected to be paid within a year of the date of the balance sheet. • 流动负债是需要在资产负债表日之前的一年内 需要偿还的债务。

• Creditors: suppliers of goods or services to the business who are not paid at the time of purchase; • 债权人:商品或服务的供货商

• Recent news reports of China„s plan to impose(征收) a fuel tax have sparked (引发) widespread speculation over the cost of fuel after the reforms are implemented. • Sun Gang is a tax policy researcher. He believes oil prices will drop after fuel tax reform begins in China.

• But I think, as a result of the combination of the two factors, current oil prices will drop after the reform, to a level that ordinary people are able to accept." • Sun says China's proposed fuel tax is different from that in western countries. • He says the fuel tax would replace(取代) current road tolls and other fees imposed on drivers.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Special journals

Special journal code Sales journal S Cash Receipts CR Journal Purchase journal P (Invoice Register) Cash Disbursements Journal CD Specific transactions to be recorded Sales on credit terms Receipts of cash (including cash sales) Purchase of merchandise and other items (supplies, fixed assets, etc,) on credit terms Payments of cash (including cash purchases)

PR

11 31

Credit

16

10

2000

General Journal

Date Account Title PR

21 Accounts payable To record the purchase of Office equipment on credit 20 Cash service revenue To record service revenue 30 Salaries Expenses cash To record the payment of wages to an employee

General journals/special journals

A journal may be a general journal or it may be a group of special journals特种 日记账. The basic form of a journal is the general journal 普通日记账(coded as G) in which any type of business transaction can be recorded.

The purpose and form of the Journal

The journal is known as the book of original or first entry. All business transactions are first recorded in the journal. The journal has three basic advantages over the ledger: 1. It shows the complete business transaction in one place. Regardless of the number of debits or credits to a particular business transaction, all parts of the transaction are shown together.

Steps in recording a business transaction in a journal

For each transaction, the debit account and its amount are entered first; the credit account and its amount are written below the debit portion (d) An adequate explanation 备注 should be given for each transaction.

General journals

(4) Debit and credit money column are designed to record the amounts of the transactions. (5) page number is preprinted and will be used to cross reference the amount to the general journal page.

Example

General Journal

Date 2002 June 22 Account and explanation PR Debit Credit

Furniture and Fixtures Office Supplies Cash

Sent check No. 345 to Green Office Equipment and Supply Co.

General Journal

Date

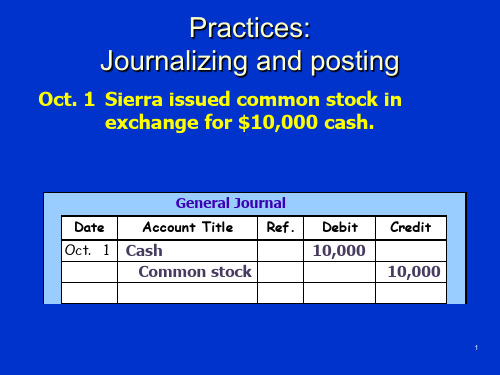

20xx Jan 1.

P.1

Debit

3000 3000

Account Title

Cash S. Wise, Capital To record the investment in the business by the Owner Office equipment

Accounting English (5)

College of Foreign Studies Jinan University Ms Peng

Journals

Main contents 1. Nature of journals 2. General journal 普通日记账 3. Special journals 特种日记账 4. Recording business transactions in a journal

Example

Recording the following compound 两个 journal entry 分录 using the proper accounting form: On June 22, 2002, the business acquired office furniture at a cost of $1,200 and related office supplies costing $75. The entire amount was paid by issuing check No.345 to the Green Office Equipment and Supply Co. of Andover, Mass.

General journals

General Journal P.1

Date Accounts Title PR Debit Credit

General journals

(1) date column is designed to record the date of journalizing (2) Account title column is used to record the accounts to be debited or credited and identify the source document. (3) PR column stands for posting reference.

General journals

When special journals are used, only those transactions that do not occur often enough to warrant entry in a special journal are recorded in the general journal. The following diagram shows the major features of the general journal

Steps in recording a business transaction in a journal

1. Analyze transactions from source documents(原始凭证). Source documents are the business papers that support the existence of business transactions. Source documents take the form of checks, invoices, bills, receipts and flight/train/ship tickets etc. They are used as the basis of recording transactions. All information used in accounting must be

The Journal

A deficiency inherent in merely using the ledger account is that the entire transaction is not recorded together. Also, the ledger account lacks a chronological order of transactions. To correct the inadequacies of the ledger account system, a record known a journal, or a businessperson’s diary is used.

General journals/special journals

A special journal is designed to record a specific type of frequently occurring business transaction. Most companies use, in addition to a generowing special journals:

The purpose and form of the Journal

2. All business transactions are recorded in the journal in chronological order. 3. The journal provides for an adequate explanation of what has taken place.